Aadhar Housing Finance: India's Affordable Housing Revolution

I. Introduction & Episode Teaser

Picture a man in Surat who lays bricks for a living. He earns in cash, paid at the end of each week, the notes folded into a plastic sleeve he keeps tucked behind a calendar at home. He wants to buy a one-room concrete house on the edge of town — the kind with a proper roof, where the monsoon does not come through the ceiling. He walks into a bank branch with that plastic folder of irregular deposits, and a polite officer asks him for a salary slip, a Form 16, a CIBIL score. He has none of these. He is told, gently, to come back when he has documentation he will never have. This happens to him five times, at five banks. To the formal financial system, he is invisible — not poor, exactly, but unreadable. There is no document that proves he is good for the money, even though he is.

Now multiply that man by tens of millions. That is the market that traditional Indian banking spent decades stepping over. And it is the market on which a quiet, unglamorous lender named Aadhar Housing Finance built a business that commanded a market capitalization of roughly ₹21,819 Crore by mid-2026 — and became one of the most prized assets in Blackstone's entire Asian private equity portfolio.1

Here is the paradox that makes this story worth two hours of your attention. Conventional wisdom says you cannot lend profitably to people who cannot document their income. The losses, the theory goes, will eat you alive. Yet Aadhar runs a loan book of self-employed brick-layers, vegetable vendors, tailors, and tea-stall owners while keeping its Gross Non-Performing Assets — the share of loans gone genuinely bad — at roughly 1.1%.2 For comparison, plenty of banks lending to salaried, fully documented borrowers have done worse. How does a lender get lower default rates from "un-lendable" customers than the establishment gets from prime ones? The answer is the whole episode.

The scale today is striking. As of fiscal year 2026, Aadhar managed about ₹30,571 Crore in Assets Under Management — the total pool of loans it has out in the market — making it the largest pure-play affordable housing finance company in India.1 It generated net profit of roughly ₹1,095 Crore on operating revenue of about ₹3,243 Crore.1 This is not a charity dressed up as a business. It is a genuinely high-return lending machine that happens to do enormous social good as a byproduct.

So how did we get here? The roadmap runs through some unlikely terrain: a sleepy 1990-era bank subsidiary in Bengaluru that nobody remembers; a parallel financial-inclusion experiment bankrolled by the World Bank's private-sector arm; a 2017 merger that fused old branches with new brains; Blackstone's coldly brilliant 2019 raid during India's worst credit panic in a generation; the strange detective-work of underwriting people who keep no records; a 2024 IPO; and a 2026 corporate reshuffle that told the market Blackstone had no intention of leaving. By the end, we will run the whole thing through Hamilton Helmer's 7 Powers and Michael Porter's Five Forces to ask the only question that matters for a long-term owner: what, exactly, keeps the competition out? Let's start where it started — with a bank you have never heard of.

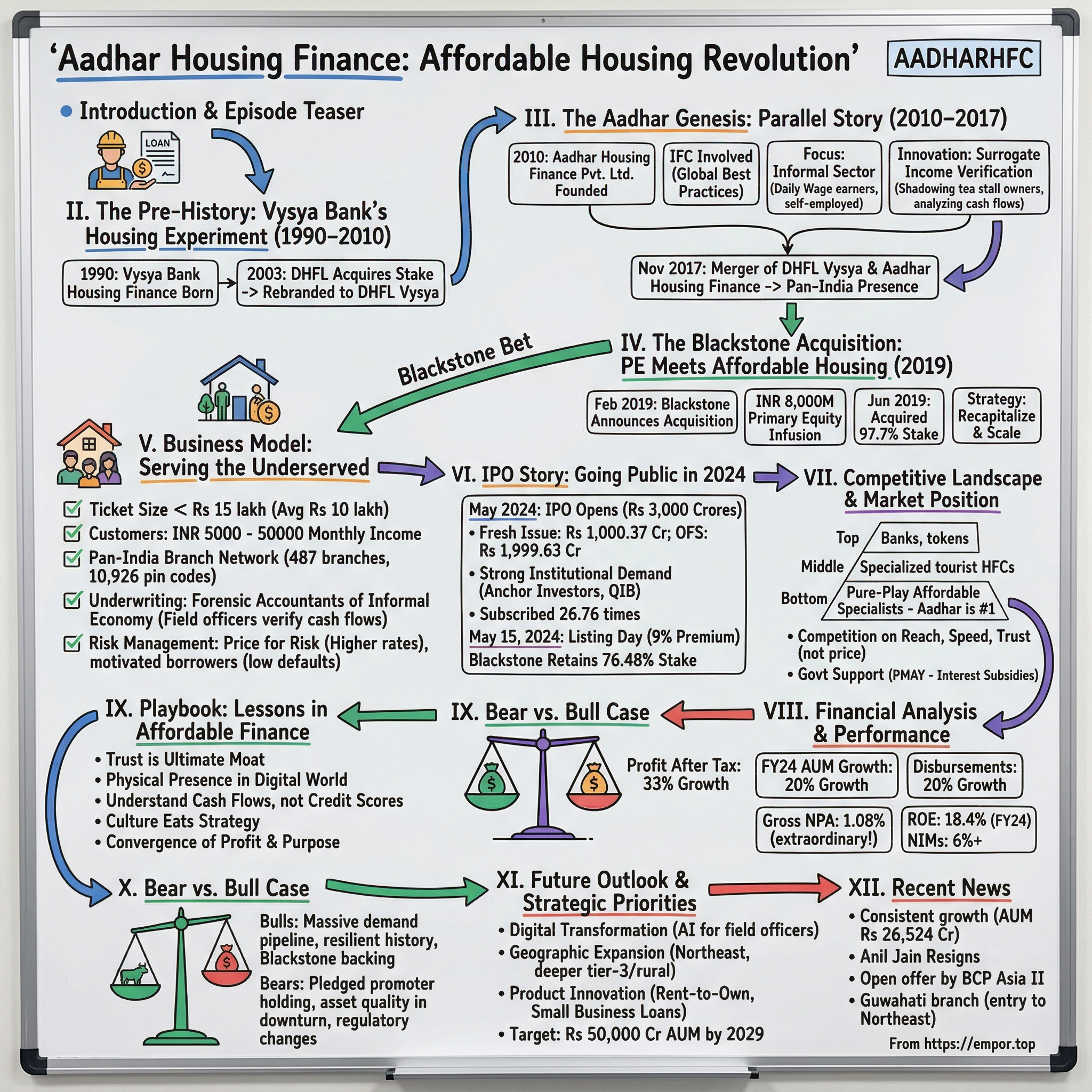

II. Pre-History: The Sleepy Regional Subsidiary (1990–2010)

Bengaluru, late 1990. Long before the city became India's Silicon Valley, it was a genteel town of bungalows, dosa joints, and conservative South Indian banking. On November 26, 1990, a modest entity was incorporated there: Vysya Bank Housing Finance, a subsidiary of the old Vysya Bank.[^3] If you had walked into its office in those years, you would have found a handful of clerks processing a trickle of home loans for the kind of customers everyone wanted — government clerks, schoolteachers, employees of established companies, all with stamped pay slips and pensions to come. It was, for more than a decade, almost aggressively unremarkable.

To understand why, you have to understand the trap that Indian housing finance was caught in. In the 1990s and early 2000s, the entire industry played what we might call the prime-only game. The giants — HDFC and LIC Housing Finance — competed for the same narrow band of low-risk, well-documented, salaried borrowers. The logic was airtight and self-reinforcing: lend only to people you can verify, keep losses near zero, and grow steadily. But it meant everyone fished in the same small pond. And for a small player like Vysya Bank Housing Finance, the pond was brutal.

The reason was funding, and it is worth pausing on because it explains the company's entire early existence. A bank makes money on the spread between what it pays for money and what it charges for money. Big banks have current and savings accounts — cheap, sticky deposits that cost almost nothing. A standalone housing finance company has no such thing. It must borrow wholesale, at higher rates, and then lend at rates the prime market keeps razor-thin through competition. Squeezed on both ends, the subsidiary struggled to push its Return on Equity — the profit it earned on each rupee of shareholder capital — much above 10%. In a business where the best operators were compounding at twice that, single-digit returns are not a business; they are a holding pattern.

The first jolt came in July 2003, when Dewan Housing Finance Corporation — DHFL, then one of India's most aggressive mortgage lenders — acquired Vysya Bank's majority stake and rebranded the entity DHFL Vysya Housing Finance Limited.[^3] DHFL's DNA was different. Where Vysya had been cautious to the point of inertia, DHFL had built its reputation lending a notch down-market from the HDFC elite. Under its early influence, something quietly interesting began happening in the branches.

In tier-2 and tier-3 towns across Karnataka — places like Shimoga and Hubli — branch managers started experimenting. A carpenter would walk in, or a trader, or the owner of a small grinding mill, none of them with salary slips, all of them clearly running real businesses with real cash flows. The managers began writing small, documentation-light loans against this informal income. It was the germ of a genuinely radical idea: that the absence of a pay slip is not the same as the absence of income.

But the germ could not grow. Two forces held it back. The National Housing Bank — then the sector's regulator — imposed traditional documentation norms designed for the salaried world. And the company's own internal risk systems, inherited from its conservative Vysya roots, treated undocumented borrowers as inherently dangerous. So the experiment stayed small, the self-employed book stayed under ₹1,000 Crore, and DHFL Vysya remained what it had always been: a regional footnote with a good instinct it could not act on. The instinct was right. It just needed a different company, built from scratch, to prove it. That company was already being born a thousand kilometers away in Mumbai.

III. The Parallel Story: The Aadhar Genesis & The IFC Blueprint (2010–2017)

On May 3, 2010, in Mumbai, a separate and far more deliberate experiment was incorporated under the name Aadhar Housing Finance Private Limited.[^3] This was not a bank subsidiary stumbling into a niche. It was a financial-inclusion thesis given corporate form, and crucially, it carried the imprimatur of the International Finance Corporation — the World Bank's private-sector arm — whose backing signaled that serious, patient, development-minded capital believed there was a real business hiding inside India's informal economy.

The founding insight was almost philosophical, and it is the intellectual heart of this entire company. India's informal sector — the hundreds of millions who work for cash, who run micro-enterprises, who have no employer and no payroll — is not unreliable. It is simply undocumented. Those are completely different problems. An unreliable borrower will not pay you back. An undocumented one will pay you back perfectly well; you just have to figure out, without the usual paperwork, who they are. The microfinance movement had already proven this with tiny working-capital loans. Aadhar's bet was that the same philosophy could be ported to housing — to loans ten and twenty times larger, secured against the home itself.

So the company set about building what became its signature capability, a playbook insiders came to describe as 360-degree forensic underwriting. Strip away the jargon and it is exactly what it sounds like: detective work. If a borrower cannot hand you a salary slip, you go and reconstruct his income yourself. Aadhar's field officers became, in effect, credit investigators. The legendary example, repeated inside the company like scripture, is the vegetable vendor: a field officer would arrive at the wholesale market at five in the morning and simply count — how many crates the vendor bought, how fast he sold them, what margin he took, how many customers came through. From a morning of observation you can build a startlingly accurate picture of a cash business that appears, on paper, not to exist.

The officers interviewed the vendor's suppliers to verify his purchase volumes. They sat in the household and mapped the family's cash flows — what came in, what went out, what was left. And they leaned heavily on what the industry calls surrogate income proxies: indirect footprints that a person leaves even when they keep no books. A consistent record of paying the electricity bill on time tells you something about discipline and surplus. Regular mobile recharges, school-fee receipts for the children, the rent on a shop — each is a fragment, and assembled together they form a credit profile more honest, in some ways, than a salary slip a salaried borrower can lose his job the day after producing.

The target customer was defined with real precision: the Economically Weaker Sections and Low-Income Groups, households earning roughly ₹5,000 to ₹50,000 a month, taking loans that averaged around ₹10 Lakh.[^4] These are small tickets — a fraction of a metropolitan home loan — which matters enormously, because it makes the book granular. No single borrower can hurt you. A lender's nightmare is concentration: a handful of large loans that all go bad together. Aadhar's book was the opposite, thousands upon thousands of tiny exposures spread across the country, so that risk was diversified almost to the point of being statistical. For investors, that granularity is not a detail; it is the foundation of the low, stable default rate that makes the whole model bankable. Two companies now existed with two halves of a complete business — old branches in the South, new brains in the North and West. The obvious move was to put them together.

IV. The 2017 Merger: Unifying Legacy with Innovation

For a few years, the two stories ran on parallel tracks under the same broad corporate family — DHFL Vysya plodding along with its Southern branches and its untapped instinct, the newer Aadhar entity refining its forensic underwriting across Northern and Western India. The merger that united them, completed on November 20, 2017, is the moment a footnote became a force.[^3] On paper it was an amalgamation of two mid-sized housing finance companies. In reality it was one of those rare corporate marriages where each partner supplied precisely what the other lacked.

Think about what each side brought to the altar. DHFL Vysya contributed something that is slow, expensive, and nearly impossible to build quickly: a legacy physical footprint. Decades of branches across South India, the brick-and-mortar infrastructure, the local staff, the muscle memory of actually collecting money in small towns. That kind of distribution is not a line item you can conjure with capital; it accretes over years. What it lacked was the brains to lend down-market safely — the very capability that had been bottled up since the Shimoga days.

The newer Aadhar entity brought exactly that missing piece: the data-driven, high-touch credit underwriting DNA, the forensic playbook, the surrogate-income methodology, and a strong presence in the North and West where DHFL Vysya was thin. Put the two together and the geographic overlap nearly vanished — one was strong where the other was weak, almost as if drawn that way. The combined entity emerged as a systemically relevant, genuinely pan-India affordable housing lender operating 292 branches from day one.[^3]

Why does a merger like this matter so much more than the sum of its parts? Three reasons that any student of capital allocation should internalize. First, it killed regional concentration risk. A lender confined to South India lives and dies with one region's monsoon, one region's crop cycle, one region's local economy; a pan-India book is insulated from any single shock. Second, it stripped out redundant overhead — two head offices, two sets of systems, two compliance functions collapsed into one. Third, and most consequentially, scale unlocked cheaper money.

That last point deserves a beat, because it is the engine of everything that follows. Once the combined loan book pushed past ₹10,000 Crore, the company crossed an invisible threshold in the eyes of wholesale lenders. Institutions that fund housing finance companies — banks, mutual funds, bond buyers — prefer scale; bigger borrowers are seen as safer, more liquid, more permanent. A larger, more diversified, pan-India lender simply commands better terms than a regional minnow. And in a lending business, your cost of borrowing is not one cost among many — it is the raw material. Shave it, and every loan you write becomes more profitable. The merger, in other words, did not just make Aadhar bigger; it made it structurally more competitive for funding. Which was a very good thing, because within a year the entire Indian credit system was about to seize up — and the company's owners were about to be forced into a sale.

V. The 2019 Blackstone Buyout: Distressed PE Capital Allocation

In September 2018, India's financial system had a heart attack. The trigger was IL&FS — Infrastructure Leasing & Financial Services, a sprawling infrastructure financier widely assumed to be too important to fail. It failed. It defaulted on its obligations, and the shock rippled outward with terrifying speed. Mutual funds, suddenly terrified of any non-bank lender, stopped rolling over the short-term commercial paper that the entire shadow-banking sector relied on to fund itself. Banks froze. Overnight, India's NBFCs — non-bank finance companies — faced a liquidity drought: the money they needed to refinance their own borrowings simply stopped flowing.

For Aadhar, the danger came not from its own book, which was healthy, but from its parents. Its ultimate owners — Wadhawan Global Capital and the now-infamous DHFL — were among the most exposed names in the entire crisis. DHFL would go on to become one of the largest financial collapses in Indian corporate history. Cornered, drowning in their own liabilities, the Wadhawans were forced to do what distressed sellers always do: sell the best thing they own. And the best thing they owned was Aadhar — a clean, profitable, growing affordable-housing lender sitting inside a burning building.

Enter Blackstone. In a transaction agreed in early 2019 and completed in June, Blackstone's vehicle BCP Topco VII Pte. Ltd. acquired a controlling stake — about 97.7% — in Aadhar for roughly $300 million, around ₹2,200 Crore.[^5]3 The headline price tells you very little. The valuation tells you everything, and it is one of the cleaner illustrations of distressed-asset arbitrage you will find.

Blackstone bought Aadhar at roughly 2.0 times book value — that is, twice the accounting net worth of the company.3 For most businesses that would sound full. For a high-quality, fast-growing affordable housing lender, it was a steal, and the comparables prove it. At that very moment, Aadhar's closest listed peers — pure-play affordable housing financiers like Aavas Financiers and Home First Finance — traded at 3.5 to 4.5 times book value.4 The market was happily paying nearly double the multiple for the same kind of business. Blackstone, in other words, acquired the largest player in the category at a 40-50% discount to where the public market valued its smaller rivals. The discount did not exist because Aadhar was worse. It existed because its sellers were desperate and the whole sector was radioactive. Buying a structurally sound platform from a forced seller during a system-wide panic — that is as close to the holy grail as private equity gets.

But the genius of the deal was only half in the buying. The other half was the turnaround playbook Blackstone ran afterward, and it is a small clinic in financial engineering. The first move was a primary equity infusion of ₹800 Crore — fresh capital injected straight into the company rather than paid out to the old sellers.[^5] This roughly doubled Aadhar's net worth at a stroke and cut its debt-to-equity ratio in half. For a lender clawing through a liquidity crisis, that is not just a balance sheet repair; it is oxygen.

The second move was subtler and more lucrative: the rating arbitrage. A stronger balance sheet plus a blue-chip global sponsor standing behind you changes how credit-rating agencies see you. Aadhar's ratings climbed — eventually into the AA+ / AAA tier — and here is why that mattered in hard rupees. A higher credit rating directly lowers your cost of borrowing. In the year after the deal, Aadhar's funding costs fell by roughly 150 basis points — 1.5 percentage points.5 In a lending business, where you make money on the gap between borrowing and lending rates, cutting your input cost by 1.5 points while holding your lending rate steady widens your net interest margin almost instantly. Blackstone did not just rescue Aadhar. It re-engineered the company's profitability with a few balance-sheet moves and the borrowed credibility of its own name. Now we should look at what that re-engineered machine actually does for a living.

VI. Business Model Deep Dive: Underwriting the Informal Sector

To understand where Aadhar actually makes its money, picture the loan book as two engines bolted to the same airframe. The first and far larger engine is core housing loans, which make up roughly 73% of AUM.6 This is the bedrock. These are highly granular retail mortgages with an average ticket size around ₹10.7 Lakh and — critically — conservative loan-to-value ratios of about 58%.6 That LTV figure is worth dwelling on, because it is the company's safety net. It means Aadhar typically lends only about 58 paise against every rupee of the home's value, so the borrower has real equity in the property from day one and the lender has a thick cushion if it ever has to repossess and sell. In a down-market book, that cushion is everything; it is the reason losses stay contained even when individual borrowers stumble.

The second, smaller, faster-spinning engine is non-housing loans, primarily Loan Against Property — LAP — and commercial-property lending, making up the remaining 27% of AUM.6 LAP is exactly what it sounds like: a borrower pledges property they already own and takes a loan against it, often to fund a business. The appeal to Aadhar is yield. LAP loans earn roughly 300 basis points — three full percentage points — of higher risk-adjusted return than plain housing loans.6 Management's stated strategy is to grow LAP toward 30% of AUM over roughly the next three years, nudging the blended yield of the whole book upward while keeping the risk tightly leashed.6 The logic is sound, but it carries an honest caveat worth flagging: LAP is, by nature, a slightly riskier product than a primary home loan, because the borrower's emotional attachment to a business-collateral property is weaker than to the roof over their family's head. Scaling it is a yield decision that must be matched by underwriting discipline, and it is one of the things a careful owner should watch.

That brings us to distribution, where Aadhar has made a deliberate and somewhat contrarian bet. The network has expanded to 620-plus branches across 20 states, reaching into more than 10,900 pin codes.6 The company calls its approach "phygital" — physical plus digital — and the ordering of those words is the whole philosophy. In an era when fintech evangelists insist that all lending is migrating to the smartphone, Aadhar has consciously refused to go purely digital, and for a very good reason rooted in its customers' reality.

Think back to our brick-layer in Surat. He deals in cash. He has no credit history a machine can scrape. If he misses a payment, no automated dunning email is going to fix it — someone has to physically visit, understand what went wrong, and work out a solution. In a cash-dominant informal economy, the physical branch is not a legacy cost to be optimized away; it is the mechanism of collection, the source of local trust, and the front line of fraud detection. The forensic underwriting we described earlier requires feet on the ground. So Aadhar uses technology as the enabler, not the closer: field officers carry tablets running cloud-native underwriting apps that speed up and standardize the paperwork. But the human being who counted the vegetable crates at dawn — that person is irreplaceable. The technology makes the human faster; it does not make the human optional. Hold that distinction, because it is the foundation of the competitive moat we will analyze later. First, though, the company had to show this machine to the public markets.

VII. The IPO and the 2025/2026 Blackstone Restructuring

Blackstone first tried to take Aadhar public in 2022. It pulled the offering. Global markets that year were a mess — rising rates, war in Europe, risk appetite evaporating — and a forced listing into a hostile tape would have left value on the table. So Blackstone did what disciplined sponsors do: it waited. The patience paid off. In May 2024, Aadhar finally went public via a ₹3,000 Crore book-built issue, split between ₹1,000 Crore of fresh capital and a ₹2,000 Crore offer for sale by the existing owners.7

The reception validated the wait. The IPO, which ran from May 8 to May 10, 2024, was priced at ₹315 per share and was oversubscribed an impressive 26.76 times overall — with the institutional, or QIB, portion bid up more than 72 times, a strong signal of professional conviction.78 The stock listed on May 15, 2024, and despite an at-par open, traded up meaningfully on its debut.8 For Blackstone, the listing was both a partial monetization and, more importantly, the establishment of a public currency and a transparent market price for an asset it had bought in the dark days of 2019. The five-year compounding between the 2019 entry and the 2024 listing was already enormous; the public market simply put a visible number on it.

Most private equity stories would end there — list, sell down, exit, return the fund. What Blackstone did next is the genuinely interesting part, and it sends a signal that long-term owners should read carefully. Rather than heading for the door, Blackstone engineered an internal reorganization that effectively re-upped its own bet. In July 2025, a different Blackstone vehicle, BCP Asia II Holdco VII Pte. Ltd., signed a Share Purchase Agreement to buy a 64.14% controlling stake from the original 2019 vehicle, BCP Topco VII, at up to ₹425.00 per share.[^12]9

Under Indian takeover rules, when a new controlling acquirer crosses certain thresholds, it must make a mandatory open offer to public shareholders — a chance for ordinary investors to sell on the same broad terms. That open offer was pitched to acquire up to 25.82% of public shares at ₹469.97 per share, valuing the offer at roughly ₹5,335 Crore.[^12]9 Sit with that price for a moment: ₹469.97 is roughly a 71% premium to the ₹315 IPO price of just two years earlier.89 The transaction received Competition Commission of India clearance in November 2025 and moved through its regulatory steps into completion in early 2026.10

Here is the strategic translation. This was not an exit; it was a transfer from one Blackstone fund to another — selling the asset from a maturing vehicle into a fresh one so the firm could keep holding it for another multi-year cycle. You do not pay a 71% premium to buy something from yourself unless you are deeply convinced it has years of compounding left. The 2025-26 reshuffle was Blackstone's way of saying, in the only language private equity truly speaks — capital — that it believes Aadhar's best years are still ahead. And running that machine day to day is a chief executive worth understanding.

VIII. Current Management: Rishi Anand & The Incentive Engine

Every lending business is, in the end, a culture of risk discipline, and culture flows from the person at the top. Since January 2023, that person has been Rishi Anand, Aadhar's Managing Director and Chief Executive Officer.[^15] He inherited the company at a pivotal moment — after Blackstone's turnaround had taken hold but before the public listing — and it fell to him to steer Aadhar through its IPO and the expansion that followed. A leadership transition timed right before going public is no small thing; it means the executive who tells the public-market story is also the one accountable for delivering on it.

What is most instructive about Anand is not his biography but his compensation structure, because how you pay a lending CEO tells you what behavior the board is trying to buy. For FY25, Anand's total compensation was ₹7.03 Crore — but the composition is the point.[^16] Only ₹2.03 Crore was fixed base salary. The other ₹5 Crore was performance-linked variable pay.[^16] In other words, roughly 70% of the chief executive's pay was at risk, contingent on results rather than guaranteed. That ratio is a deliberate design choice: it ties the person making the biggest risk decisions to the outcomes of those decisions.

By Indian disclosure norms, Anand's pay worked out to about 65.89 times the median Aadhar employee's salary.[^16] One should read a ratio like that with both eyes open. On one hand, it reflects an intensely performance-weighted structure rather than a fat guaranteed package. On the other, a 66-times multiple is a real number, and governance-minded owners are right to keep an eye on whether executive rewards stay tethered to genuine, durable performance rather than to a rising market that lifts all boats.

The deeper alignment lives in equity, not salary. Anand directly owns only about 0.02% of the company's shares — a small slice in percentage terms.[^16] But he also holds 578,267 stock options, vested and unvested, granted under the 2020 and 2021 schemes at strike prices ranging from roughly ₹90.8 to ₹147.5.[^16] Recall that the stock listed at ₹315 and the 2026 open offer was priced near ₹470. Options struck around ₹90 to ₹150 against a market price several times higher represent serious personal wealth — wealth that exists only because, and only to the extent that, the public share price has climbed. That is alignment doing its job: the CEO gets rich in lockstep with outside shareholders, not ahead of them.

Looking forward, the company has put in place an ESOP 2025 framework that hard-codes this philosophy for the broader senior team. Vesting is structured 65% on time and 35% on performance, with the performance portion tied to the two metrics that matter most for a down-market lender: AUM growth and Gross NPA staying within defined boundaries.[^16] That last clause is the elegant part. By bolting a chunk of leadership wealth to keeping bad loans below a ceiling, the incentive system directly punishes the one temptation that destroys lenders — chasing growth by loosening underwriting. The pay plan, in effect, encodes the company's risk culture. Whether that culture truly holds, of course, is best judged against the field of rivals trying to take Aadhar's market.

IX. Competitive Landscape: Scale Advantages & Hamilton's 7 Powers

Line up the affordable housing finance sector by size in FY26 and Aadhar's lead is not subtle. Aadhar carried about ₹30,571 Crore in AUM, a market cap near ₹21,819 Crore, and profit around ₹1,095 Crore.1 Its nearest pure-play rivals trailed well behind: Aavas Financiers at roughly ₹23,451 Crore of AUM and an ~₹11,673 Crore market cap; Home First Finance at about ₹15,878 Crore AUM and ~₹12,000 Crore market cap; Aptus Value Housing at roughly ₹13,107 Crore AUM; and India Shelter Finance at about ₹11,044 Crore AUM.4 Aadhar, in short, is nearly the size of the next two combined. But scale alone is not a moat — plenty of large companies get disrupted. The right question is structural: what powers actually protect this business? Hamilton Helmer's 7 Powers framework gives us a clean way to test it, and four of the seven apply with real force.

Counter-Positioning — the primary power. This is the one that matters most, and it is the most beautiful, because it is a moat the incumbents cannot cross without harming themselves. India's giant retail banks — SBI, ICICI, HDFC — have funding so cheap it is almost unfair; their current and savings deposits cost a fraction of what Aadhar pays. On paper they should be able to crush a niche lender. But they cannot, and the reason is that their entire business model is built for low-touch, high-volume, document-driven lending. To serve a cash-only daily-wage earner, you need the expensive, manual, feet-on-the-ground forensic underwriting we described — branch visits, dawn market counts, household cash-flow mapping. If a big bank tried to replicate that, the labor cost would shatter its prized low cost-to-income ratio. The very efficiency that makes the banks great in the prime market makes them structurally incapable of competing down-market. They are not unwilling to copy Aadhar; they are unable to, because copying it would break the model that makes them what they are. That is counter-positioning in its purest form.

Scale Economies. As the largest pure-play in the category, Aadhar borrows more cheaply than its smaller rivals because of its premium credit rating and Blackstone's sponsorship — the rating arbitrage we saw earlier, now compounding. Lower funding cost spread across a bigger book lets Aadhar absorb the high operating expense of a high-touch model while still posting an industry-leading cost-to-income ratio around 35% and a net interest margin comfortably above 6%.62 Smaller competitors face the same high-touch cost base but pay more for their money, so they cannot match both margins at once. Scale buys Aadhar the right to be expensive where it counts.

Cornered Resource. Aadhar's true crown jewel is human, not financial: a proprietary network of more than 10,000 localized, bilingual credit and field officers embedded in underbanked micro-markets, holding relationships and local knowledge that took years to build.6 You cannot hire ten thousand such people overnight, and you cannot teach the tacit feel for a local market from a manual.

Process Power. Layered on top is more than fifteen years of refining surrogate-income assessment and, just as valuably, a proprietary database of micro-market default history — which neighborhoods, which trades, which patterns predict trouble. A new entrant cannot buy this; it can only earn it the hard way, by lending into early loan cohorts and absorbing the credit losses that come from not yet knowing what Aadhar already knows. That accumulated learning is a tax on every newcomer.

Run the same landscape through Porter's Five Forces and the picture holds. The threat of new entrants is muted by exactly the process power and cornered resource above. Buyer power — the borrowers — is low; these customers have few alternatives and value access over price. Supplier power, here meaning the providers of funding, is real but softened by Aadhar's scale and rating. Substitutes — informal moneylenders — are vastly more expensive and serve only to make Aadhar's product look attractive. The sharpest force is internal rivalry among the affordable-housing specialists, which is intensifying. That rivalry, and the numbers behind it, is where we turn next.

X. Financial Analysis & Core KPIs

Strip the story down to its financial skeleton and what you find is a lender that converts revenue into profit with unusual efficiency. In FY26, operating revenue ran about ₹3,243 Crore and net profit about ₹1,095 Crore — a third of every revenue rupee dropping to the bottom line, which for a lender is excellent.1 The market valued the business at roughly 3.4 times book value, broadly in line with peers such as Aavas near 3.2 times and Home First near 3.6 times — neither a screaming bargain nor an obvious excess relative to the category.4 But for an owner trying to monitor this business over time, the valuation multiple is the wrong thing to watch. Three operating metrics tell you whether the machine is still working, and they are the only three worth obsessing over.

The first is Gross NPA — the risk anchor. In FY26 it sat at roughly 1.08% to 1.1%.2 This single number is the heartbeat of the entire thesis, because the whole bet is that forensic underwriting lets Aadhar lend safely to the undocumented. As long as Gross NPA stays near 1%, the model is validated; the credit detectives are doing their job. Any sustained spike would be the canary in the coal mine — a sign that the surrogate-income models are misfiring, or that growth is outrunning discipline. This is the number to watch above all others.

The second is Net Interest Margin — the gap between what Aadhar earns on loans and pays on borrowings — running at roughly 6.0% to 6.5%.2 To see why this is so wide, look at the two ends. Aadhar lends at yields of roughly 13-16%, because its customers have few alternatives and value access over a few points of interest. It borrows at roughly 7.5-8%, thanks to the scale and rating advantages we have traced.2 That spread is pricing power made visible, and it is what funds both the high-touch cost base and the fat profit margin.

The third is the Cost-to-Income ratio, leading the industry at around 35%.6 Here is the apparent paradox worth savoring: how does the most labor-intensive, feet-on-the-ground lender in the sector also run the lowest cost ratio? The answer is operating leverage from the hub-and-spoke branch model. Once a branch matures, its fixed costs are spread across a growing book, and each incremental loan is far cheaper to service than the first. A falling or stable cost-to-income ratio as the company grows is proof the expansion is paying for itself rather than bloating overhead.

One last feature puzzles newcomers: despite minting profit, Aadhar pays almost nothing in dividends. This is not stinginess; it is arithmetic. The company earns a Return on Equity around 18.4%.6 When management can reinvest retained earnings inside the business at 18% returns, paying that cash out as dividends — which shareholders would then have to redeploy at lower returns elsewhere — actively destroys value. Every rupee kept and recompounded at 18% is worth more than a rupee handed back. For a high-return compounder with a vast runway, hoarding capital is the shareholder-friendly choice. The question, then, is how long that runway really runs — and what could shorten it.

XI. Bear vs. Bull Case

Every great compounder is a tug-of-war between an enormous opportunity and a set of real, unglamorous risks. Let us war-game both sides honestly.

The bull case starts with a number that is almost hard to comprehend: India faces a structural shortage of more than 25 million affordable homes, and urbanization is expected to push roughly 40% of the population into cities by 2030.6 This is not a market Aadhar has to steal from competitors; it is a market being created faster than anyone can serve it. On top of that demographic tide sits government policy, which is squarely on Aadhar's side. The Pradhan Mantri Awas Yojana — the national affordable housing mission — has carried massive budget allocations, on the order of ₹80,000 Crore, including interest-subsidy support that directly lowers the effective cost of a home loan for exactly Aadhar's customers.6 When the government is paying part of your customers' interest bill, demand for your product gets a structural tailwind. Layer on the yield optionality from growing LAP toward 30% of the book, and the long-term stability of a Blackstone sponsor that just re-upped its commitment, and the bull case is genuinely powerful: a dominant player with the widest moat, riding a demographic and policy wave, run by management paid to compound it.

The bear case deserves equal seriousness, and a thoughtful owner should sit with each point rather than wave it away.

First, the share-pledge overhang. Roughly 67.6% of the promoter's holding is pledged or encumbered under technical fund vehicles.[^17] In most Indian companies, heavy promoter pledging is a genuine red flag — a sign of a cash-strapped founder borrowing against his own shares. Here the context is more benign, because the "promoter" is Blackstone and the encumbrances relate to its fund structures rather than personal distress. But "more benign" is not "irrelevant." It is an optical overhang that can weigh on sentiment and creates structural complexity, and it belongs on the watch list.

Second, and most fundamentally, macro vulnerability. Aadhar's borrowers are low-income, self-employed people without formal financial safety nets — no salaried fallback, no large savings buffer, no unemployment insurance. The granularity of the book protects against idiosyncratic defaults, but it offers less protection against a correlated shock. A severe, broad economic downturn that hits the informal economy all at once — a deep recession, a demonetization-style policy jolt — could push many of these households into trouble simultaneously. The model has been tested in good times and through COVID; a genuine prolonged downturn would be its sternest exam.

Third, rate squeeze. Aadhar's fat margin depends on borrowing cheaply and lending dear. In a world of sustained high interest rates, its own funding costs could rise faster than it can pass them on, because its customers are intensely price-sensitive and the regulator watches lending rates to vulnerable borrowers. Margins are wide today, but they are not guaranteed.

Fourth, down-market competition. The counter-positioning moat holds as long as big banks find the segment structurally unattractive. But several large lenders have begun forming specialized affordable-housing wings aimed precisely at the ₹10-15 Lakh ticket. If a deep-pocketed bank decides to subsidize a high-touch unit with its cheap deposits and treat early losses as a customer-acquisition cost, the competitive calculus shifts. The moat is strong, not infinite. Weighing both sides, what endures are the lessons the whole story teaches.

XII. Epilogue & Playbook Lessons

Step back from the numbers and Aadhar's arc offers a handful of durable lessons for anyone who allocates capital.

The first is that social impact and outsized profit are not opposites — they can be the same thing. The reflexive assumption is that lending to the poor must be either charity or predation. Aadhar's roughly 18% return on equity, earned while putting a roof over hundreds of thousands of informal-economy families, demolishes that binary. True financial inclusion, structured with the right risk mitigation and the right granularity, is not a cost center with a halo; it is a high-margin, scalable business. The doing-good and the doing-well come from the same engine.

The second lesson is that in a cash-dominant, informal economy, physical presence is the moat, not a liability to be optimized away. A decade of fintech orthodoxy insisted that the branch was dead and the app was destiny. Aadhar's results argue the opposite for this particular market: when your customers deal in cash and leave no digital trail, the feet on the ground that collect, verify, and build trust are precisely what keeps your default rate near 1%. Technology accelerates the human; it does not replace them.

The third lesson belongs to Blackstone, and it is the oldest truth in private equity wearing fresh clothes: the highest returns come from buying structurally sound platforms from forced sellers during liquidity panics. The 2019 acquisition worked not because Blackstone was clever about housing finance — though it was — but because it had the capital and the nerve to act when the IL&FS crisis had made everyone else too frightened to bid. The asset was always good. The discount came entirely from the timing.

From a sleepy Bengaluru bank office that could not break a 10% return, to a parallel Mumbai experiment in counting vegetable crates at dawn, to a merger that fused old branches with new brains, to a crisis-era buyout and a public listing and a sponsor confident enough to sell the company to itself at a 71% premium — Aadhar's journey is finally a story about doing unglamorous things exceptionally well at scale. Patient capital, localized underwriting, and the relentless execution of basics. That, more than any single number, is what built a ₹21,800 Crore powerhouse out of borrowers the rest of the system could not even read.

References

-

Aadhar Housing hits record high after strong results, open offer by promoter Blackstone — Moneycontrol via TradingView News, 2026 ↩↩↩↩↩

-

Aadhar Housing Finance Limited — Credit Rating Report, CARE Ratings, 2025-06-15 ↩↩↩↩↩

-

Blackstone to Acquire India's Aadhar Housing Finance — Reuters, 2019-02-02 ↩↩

-

Aadhar Housing Finance Ltd IPO 2024 — Price, Date, Review and Key Insights (peer comparables), Business Standard, 2024 ↩↩↩

-

Blackstone Buys Aadhar Housing Finance From DHFL, Wadhawan Group — NDTV Profit, 2019-06-11 ↩

-

Aadhar Housing Finance — Public Disclosures and SEBI LODR Filings (business and operating metrics) ↩↩↩↩↩↩↩↩↩↩↩↩

-

Aadhar Housing Finance sets IPO price band at Rs 300-315 per share — Business Standard, 2024-05-02 ↩↩

-

Aadhar Housing Finance IPO Date, Price, GMP, Details (subscription and listing) — Chittorgarh, 2024 ↩↩↩

-

Blackstone Entities Announce Open Offer for 25.82% Stake in Aadhar Housing Finance at ₹469.97 Per Share — ScanX, 2025 ↩↩↩

-

CCI Approves Acquisition of Aadhar Housing Finance by BCP Asia II — Press Information Bureau, Government of India, 2025-11-20 ↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube