The Invisible Grid: The Rajesh Power Services Story

I. Introduction: The "Nerve Center" of the Energy Transition

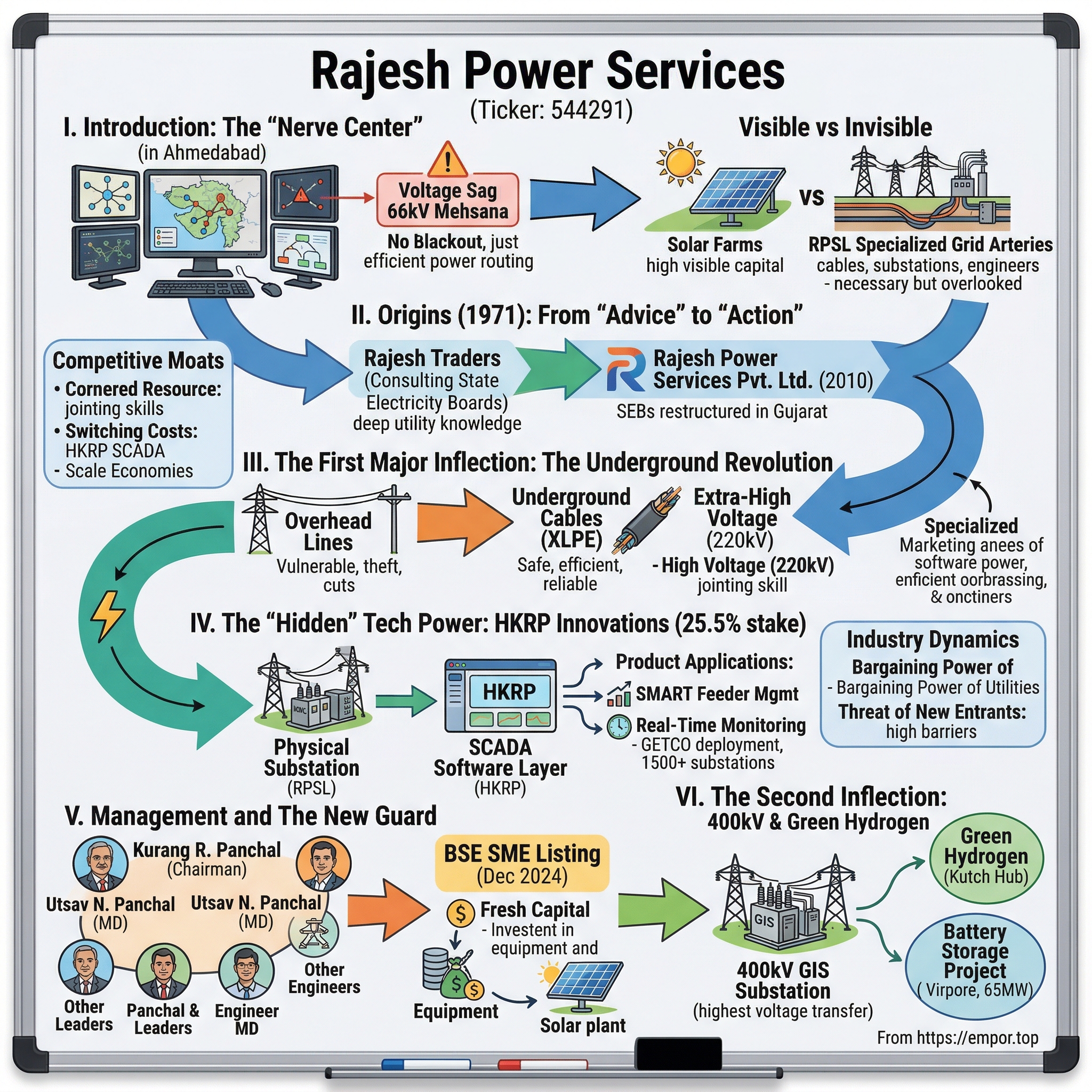

Picture a control room in Ahmedabad at two in the morning. Banks of screens glow with real-time telemetry from over thirty thousand nodes scattered across Gujarat. A voltage sag triggers an alert on a 66kV feeder outside Mehsana. Within seconds, the system isolates the fault, reroutes power through an alternate underground circuit, and logs the event for the morning crew. No blackout. No scramble. No headlines. The lights in a million homes stay on, and nobody notices a thing.

That invisibility is the point. And it is the entire business model of Rajesh Power Services Limited.

The global conversation about India's energy transition fixates on the glamorous end of the spectrum: solar farms carpeting the Thar Desert, offshore wind turbines rising in the Gulf of Khambhat, green hydrogen electrolysers that promise to decarbonize heavy industry. These are the technologies that attract billions of dollars in capital and dominate the front pages. But here is the question almost nobody asks: once you generate all that clean power, how does it actually reach the factory floor, the apartment block, the hospital ward? The answer involves tens of thousands of kilometers of cable, thousands of substations, and an army of specialized engineers who can joint a 220kV cable at precise tolerances without blowing up a city block. That answer, in Gujarat at least, increasingly runs through Rajesh Power Services.

RPSL occupies a peculiar and powerful position in the Indian power sector. It is not a power generator. It is not a distribution company that sends you a monthly bill. It is the specialized "surgical team" that sits between generation and consumption, building and upgrading the arteries and nerve centers of the grid itself. Think of it this way: if India's energy transition is open-heart surgery, the solar panels and wind turbines are the new heart. Rajesh Power is the vascular surgeon reconnecting every artery to make sure the patient actually survives the operation.

The company's operating geography tells its own story. Gujarat is not just any Indian state. It has been the laboratory for India's most aggressive infrastructure modernization for over two decades, beginning with the electricity reforms of the early 2000s that separated generation, transmission, and distribution into distinct entities. When other states were still struggling with endemic power theft and crumbling infrastructure, Gujarat was already laying underground cables and installing supervisory control systems. RPSL grew up inside that ecosystem, learning the specific pain points of every state utility from the inside out.

The numbers frame the opportunity. As of September 2025, RPSL sat on an order book of approximately three thousand five hundred crore rupees. In October 2025, the company signed a memorandum of understanding with the Government of Gujarat worth four thousand seven hundred and fifty-four crore rupees at the Vibrant Gujarat Regional Conference. For a company that listed on the BSE SME platform in December 2024 at a market capitalization of roughly twelve hundred crore rupees, that pipeline represents a transformational runway. But order books are promises, not profits. The real story of Rajesh Power is how a fifty-five-year-old family business built the technical credibility, the institutional relationships, and the quiet technological edge to position itself at the center of one of the world's largest infrastructure build-outs.

To understand that story, you have to go back to 1971, to a trading firm in Ahmedabad, and to a family that understood something fundamental: in the power business, the people who know where the problems are will always find work.

II. The Origins: From "Advice" to "Action"

Ahmedabad in 1971 was a city in transition. Gujarat had been a separate state for barely a decade, carved out of the old Bombay State in 1960, and its industrial base was still dominated by textiles. The electricity infrastructure was rudimentary. State Electricity Boards, or SEBs, were the monolithic entities responsible for everything from generating power to delivering it to homes and factories. These were massive, bureaucratic organizations, chronically short of technical expertise and perpetually struggling with the gap between India's explosive demand growth and its creaking grid infrastructure.

Into this gap stepped the founders of what was then called Rajesh Traders, a partnership firm established on May 5, 1971. The initial business was modest: trading in electrical goods and providing consultancy services to the state utilities. It was not glamorous work. It meant understanding transformer specifications, cable ratings, switchgear compatibility, and the thousand small technical decisions that determine whether a substation works reliably or becomes a recurring headache for the utility engineers.

But this is where the information advantage was born. A consultant who spends years embedded in the operations of a State Electricity Board learns things that no outside contractor ever could. They learn which equipment fails most often and why. They learn the specific soil conditions and climate factors that affect cable performance in different regions of Gujarat. They learn the procurement cycles, the budget constraints, the political pressures, and the institutional preferences of each utility. Most importantly, they build relationships with the engineers and managers who will, years later, be the ones awarding contracts worth hundreds of crore rupees.

The insight from Rajesh Traders' early decades was that India's power problem was evolving. In the 1970s and 1980s, the primary challenge was simple: there was not enough generation capacity. Power cuts were a daily reality. Air conditioning was a luxury. Factories ran their own diesel generators as backup. But by the 1990s, a subtler and more complex problem was emerging. Even as generation capacity expanded, the grid itself could not handle the load. Transmission losses were staggering, sometimes exceeding twenty-five percent in some states. Power theft through illegal tapping of overhead lines was endemic. And the distribution infrastructure in rapidly urbanizing cities was dangerously obsolete.

This was the shift from "power shortages" to "grid stability," and it demanded a fundamentally different set of capabilities. You did not need more power plants. You needed smarter substations, more resilient cables, better monitoring systems, and contractors who could execute complex upgrades without shutting down service to millions of people.

The partnership firm saw this transition coming. The pivot from advisory work to execution, from telling utilities how to build substations to actually building them, did not happen overnight. It was a gradual process that accelerated through the late 1990s and 2000s as Gujarat's reform-minded government began restructuring its power sector. In February 2010, Rajesh Traders formally converted from a partnership firm into a private limited company, Rajesh Power Services Pvt. Ltd. The timing was not accidental. Gujarat had by then split its monolithic SEB into separate entities for generation (GSECL), transmission (GETCO), and distribution (the four regional Vij companies: UGVCL, DGVCL, PGVCL, and MGVCL). Each of these new entities needed contractors who understood the whole system but could deliver specialized, high-quality execution.

The Siddhi Group, the family business conglomerate that housed RPSL, had by this point built relationships with every major utility in the state. They were not the biggest contractor. They were not the cheapest. But they were the ones the utilities called when the job was technically difficult and failure was not an option. That reputation, built over three decades of consultancy and gradually expanding execution work, became the foundation for everything that followed.

For investors, the takeaway from this origin story is the depth of the moat that was being dug long before anyone was thinking about moats. In infrastructure, relationships and track record are not soft advantages. They are the primary qualification criteria. When a state utility issues a tender for a 220kV underground cable project, the bidder must demonstrate that they have successfully completed similar projects of similar scale. You cannot fake that history. You cannot acquire it overnight. RPSL spent forty years building it, one project at a time.

III. The First Major Inflection: The Underground Revolution

Walk through any older neighborhood in an Indian city and look up. You will see a chaotic lattice of overhead power lines, some sagging dangerously low, others illegally spliced with improvised connections. During monsoon season, these lines become lethal. Falling branches cause outages. Flooding shorts out transformers mounted on wooden poles. And the sheer visual clutter of overhead infrastructure makes urban planning nearly impossible. In rural areas, the problems are different but equally severe: overhead lines are easy targets for power theft, and the vast distances involved mean that even small inefficiencies in transmission compound into enormous losses.

The solution, increasingly adopted by progressive state utilities beginning in the early 2000s, was to move those lines underground. Underground cabling eliminates theft because you cannot tap a cable buried in a concrete duct. It eliminates weather-related outages because cables encased in protective conduits are immune to wind, rain, and falling trees. It dramatically reduces transmission losses because modern XLPE (cross-linked polyethylene) cables are far more efficient than aging overhead conductors. And it frees up urban space for development, which is why real estate developers and municipal planners love it.

Gujarat was at the forefront of this shift, and this is where the "Gujarat Model" becomes central to the RPSL story. Under a succession of infrastructure-focused state governments, Gujarat invested heavily in converting its urban distribution networks from overhead to underground systems. This was not just an engineering decision. It was a political and economic strategy. A state with reliable, modern power infrastructure attracts industrial investment, which creates jobs, which generates tax revenue, which funds more infrastructure. It is a virtuous cycle, and Gujarat pursued it more aggressively than almost any other Indian state.

RPSL was perfectly positioned to ride this wave. Their decades of consultancy work had given them an intimate understanding of the technical requirements. Their relationships with all four Gujarat distribution companies meant they were already trusted partners. And their decision to invest heavily in the specialized equipment and workforce needed for underground cable laying, including cable jointing kits, fault location equipment, and trained technicians, gave them a capability that few competitors could match.

But the truly transformative decision came in the last fifteen years, when RPSL made a deliberate strategic choice to move upmarket into extra-high voltage underground cabling, specifically cables rated at 66kV, 132kV, and eventually 220kV. This is where the analogy to surgery becomes most apt. Laying an 11kV distribution cable underground is skilled work, but it is relatively standardized. Hundreds of contractors across India can do it. Laying a 220kV transmission cable underground is an entirely different discipline. The cables themselves are massive, sometimes weighing several tons per meter. The jointing process, where two cable sections are connected, must be executed in a climate-controlled environment with surgical precision. A single contamination particle in a 220kV joint can cause a catastrophic failure that takes weeks to repair and costs the utility millions in lost revenue and emergency response.

The number of firms in India with proven capability in extra-high voltage underground cable jointing can be counted on two hands. RPSL made a calculated bet that by investing in this specialized capability, they could move out of the commodity construction space, where competition is fierce and margins are thin, into a rarified tier where technical qualification matters more than price and barriers to entry are formidable.

This strategy also allowed RPSL to avoid the debt trap that destroyed many Indian infrastructure companies during the 2012-2014 period. That era saw a wave of bankruptcies among companies that had taken on massive debt to build and own power generation assets, only to find that fuel costs were rising, power purchase agreements were being renegotiated, and their balance sheets were collapsing under the weight of leveraged capital expenditure. RPSL never played that game. They remained asset-light, focused on consultancy and high-skill EPC rather than owning the power plants themselves. They provided the specialized labor and project management; the utilities owned the assets. This meant lower revenue than the empire-builders, but it also meant that when the tide went out, RPSL was still standing with a clean balance sheet and an intact reputation.

The proof of this strategy showed up in the financial results. In FY24, the company reported revenue of approximately two hundred and eighty-five crore rupees. By FY25, consolidated revenue had exploded to over eleven hundred crore rupees, a growth rate of nearly two hundred and ninety percent. Profit after tax rose from twenty-six crore to over ninety-three crore. That kind of growth does not come from a company that suddenly got lucky. It comes from a company that spent years building capability in a space where demand was about to explode.

IV. The "Hidden" Tech Power: HKRP Innovations

Here is a question that separates the casual observer from the serious analyst: what is the most valuable asset on RPSL's balance sheet? It is not the cable-laying equipment. It is not the order book. It is a twenty-five-point-five percent stake in a company most investors have never heard of: HKRP Innovations.

To understand why this matters, you need to understand what happens after a substation is built. The physical infrastructure, the transformers, switchgear, cables, and protective relays, is only half the story. The other half is the software layer that monitors, controls, and optimizes the performance of that infrastructure in real time. This is the domain of SCADA, which stands for Supervisory Control and Data Acquisition.

Think of SCADA as the operating system of the power grid. Just as your smartphone's operating system manages the hardware beneath it, a SCADA platform collects data from sensors across the grid, displays it on operator consoles, sends control commands to switches and breakers, and logs everything for analysis. Without SCADA, a modern power grid is flying blind. Operators would have to physically visit each substation to check equipment status, respond to faults, and manage load balancing. With SCADA, all of this happens from a centralized control room, in real time, across thousands of locations simultaneously.

HKRP Innovations, which became a public limited company in July 2024, builds cloud-based SCADA and industrial IoT solutions specifically for the Indian energy sector. Their product portfolio reads like a checklist of the critical software layers that modern utilities need: SFMS (Smart Feeder Management System) for managing distribution feeders, VFS (Virtual Feeder Segregation) for separating agricultural and domestic power loads, RTMS (Real-Time Monitoring System) for oil well operations, and SEDM (Solar Energy Data Management) for tracking distributed solar generation.

The scale of HKRP's deployments is remarkable for a company that operates far below the radar of most investors. In FY25, HKRP implemented what it described as one of the largest SCADA initiatives in India, centralizing over fifteen hundred distribution substations onto a single platform for GETCO, Gujarat's transmission utility. The platform currently monitors more than thirty thousand nodes and over ten thousand megawatts of load across Gujarat.

Now here is the strategic insight that makes RPSL's stake in HKRP so significant. When RPSL builds a physical substation for a utility, HKRP can install the SCADA system that monitors it. The hardware and software are delivered together, by entities under the same ownership umbrella, with deep integration between the physical and digital layers. For the utility, this means a single point of accountability: if the substation has an issue, they call one group, not two separate vendors who point fingers at each other.

But the real power of this arrangement is the switching costs it creates. Once a utility has its entire grid monitored through HKRP's SCADA platform, with years of historical data, customized dashboards, trained operators, and integration with their internal systems, the cost of switching to a different SCADA provider is enormous. It is not just the financial cost of buying new software. It is the operational risk of migrating a live monitoring system without losing visibility into the grid, the retraining cost for hundreds of operators, and the institutional knowledge embedded in years of historical data that would be lost or degraded in a transition.

Consider the specific applications. HKRP's platform monitors twelve hundred solar agricultural pumps and tracks performance data from forty thousand smart oil wells. These are not generic, off-the-shelf deployments. They are deeply customized implementations that reflect the specific operational requirements of Gujarat's utilities and industrial users. Every customization adds another layer of stickiness.

The "Trojan Horse" analogy is apt. RPSL gets the initial contract to build the physical infrastructure. HKRP gets embedded as the intelligence layer on top. Once both are in place, the utility is effectively locked into the ecosystem for the lifetime of the asset, which for a substation is typically thirty to forty years.

For investors evaluating RPSL, the HKRP stake represents an optionality that is difficult to value using conventional metrics. If HKRP remains a niche Gujarat-focused SCADA provider, it is a nice complementary business. But if India's grid modernization drives a national rollout of smart grid infrastructure, and HKRP can replicate its Gujarat playbook in other states, the value of that twenty-five percent stake could dwarf the EPC business that most analysts focus on.

V. Management and The New Guard

Every family business in India faces the same existential question: can the next generation institutionalize what the founders built on intuition and relationships? The history of Indian conglomerates is littered with examples of brilliant first-generation businesses that crumbled when the founders stepped back and the heirs could not manage the transition from entrepreneurial hustle to professional governance. RPSL's answer to this question is still being written, but the early evidence is encouraging.

The company is led by four promoters who collectively represent both continuity and evolution. Kurang Ramchandra Panchal, the Managing Director and Chairman, brings over four decades of experience in the transmission and distribution sector. He is the institutional memory of the organization, the person who built the relationships with Gujarat's utilities over decades of patient, relationship-driven business development. In a sector where trust is the primary currency, Panchal's standing with the state's utility executives is an asset that cannot be replicated by hiring a team of MBAs.

Rajendra Baldevbhai Patel plays a critical role in managing the broader operations of the Siddhi Group and driving turnkey project execution. His focus on operational discipline, on ensuring that projects are delivered on time and within budget, addresses the single biggest risk in the EPC business: execution failure.

But it is the younger generation that signals the company's ambitions. Utsav Nehal Panchal holds an MBA from IIM Kashipur and a Six Sigma Green Belt certification from the Indian Statistical Institute in Pune. Kaxil Prafulbhai Patel combines a BE and M.Tech in Electrical Engineering with an executive program in Financial Reporting and Corporate Governance from IIM Ahmedabad. These are not sons who wandered into the family business by default. They are technically trained, institutionally credentialed professionals who bring the analytical rigor and governance frameworks that public market investors demand.

The IPO itself was a statement of intent. When RPSL listed on December 2, 2024, it was not just raising capital. It was submitting itself to the discipline of public market scrutiny: quarterly reporting, independent audits, institutional investor expectations, and the relentless demand for transparency that comes with being a publicly traded company. The fresh issue of approximately ninety-three and a half crore rupees was specifically earmarked for investments that signal a shift from dependent contractor to self-sufficient capability builder.

The allocation of IPO proceeds tells its own story. A portion went toward purchasing fault-location equipment, the specialized instruments used to pinpoint the exact location of a failure in an underground cable. Previously, RPSL had been renting this equipment from third parties, which created both a cost drag and a dependency. Owning the equipment means faster response times, lower operating costs, and the ability to offer fault-location as a standalone service to other contractors.

Another allocation funded the construction of a thirteen-hundred-kilowatt solar power plant. This is not a revenue play. It is a demonstration facility. By building and operating their own solar plant, RPSL gains first-hand experience with the engineering challenges of solar EPC, which they can then offer as a service to utility and commercial clients. It is the same consultancy-to-execution playbook that the founders ran in the 1970s, updated for the renewable energy era.

The market's response was emphatic. The IPO was oversubscribed fifty-nine times. Non-institutional investors bid at nearly one hundred and thirty-eight times the available allocation. On listing day, the stock opened at approximately ninety percent above the issue price and immediately hit the upper circuit. By April 2026, shares traded around eight hundred and fifty-eight rupees, roughly one hundred and fifty-six percent above the IPO price of three hundred and thirty-five rupees.

Post-IPO promoter holding settled at approximately sixty-two percent, a level that signals strong alignment between management and public shareholders. The promoters retained a controlling stake while creating enough public float to attract institutional interest and provide liquidity. The independent board includes professionals with backgrounds from IIT Delhi, the Institute of Company Secretaries, and the Institute of Chartered Accountants, providing the governance infrastructure that institutional investors look for.

The management philosophy that emerges from these decisions is clear: RPSL is transitioning from a family business that happened to do power infrastructure to an institutional EPC powerhouse that happens to be family-led. The distinction matters enormously for long-term investors, because it determines whether the company can scale beyond the personal networks of its founders into a repeatable, process-driven organization capable of executing a multi-thousand-crore order book.

VI. The Second Inflection: 400kV and Green Hydrogen

In September 2025, RPSL announced a set of orders totaling two hundred and seventy-eight crore rupees. For a company with a three-thousand-five-hundred-crore order book, this was not the largest win. But it might have been the most important. Buried in the announcement was a detail that industry observers immediately recognized as a watershed moment: RPSL had won its first contract for a 400kV Gas Insulated Switchgear substation.

To appreciate why this matters, think of voltage levels as altitude bands for an airplane. Most of RPSL's historical work has been in the 11kV to 66kV range, the equivalent of flying at cruising altitude for regional flights. Their move into 220kV projects over the past fifteen years was like qualifying for transcontinental routes. But 400kV is the stratosphere. It is the backbone of India's national transmission grid, the highest voltage level used for bulk power transfer across long distances. The companies that operate at this level, globally, are names like ABB, Siemens, and GE. In India, the 400kV space has been dominated by a handful of large engineering conglomerates.

Gas Insulated Switchgear adds another layer of complexity. In a conventional Air Insulated Substation, the various components, circuit breakers, isolators, bus bars, are separated by open air, which provides the electrical insulation between them. This works fine in rural areas where land is cheap and plentiful. But in dense urban environments, AIS substations are impractical because they require enormous amounts of space. GIS substations use sulfur hexafluoride gas as the insulating medium, which allows the entire assembly to be enclosed in sealed metal housings that occupy a fraction of the footprint. They are more expensive, more complex, and vastly more demanding to install and commission. They are also the future of urban power infrastructure in land-scarce Indian cities.

The 400kV GIS contract was awarded by a private entity in Gujarat. It included supply, installation, testing, and commissioning of both 400kV/33kV and 66kV/33kV gas insulated substations. The stock jumped seven percent on the announcement, reflecting the market's understanding that this was not just an order. It was a credential. Once you have successfully delivered a 400kV GIS project, you can bid on similar projects anywhere in India and eventually internationally. The track record becomes self-reinforcing.

The second frontier is green hydrogen, and here the story is more speculative but potentially more consequential. RPSL allocated three crore rupees from IPO proceeds for developing in-house technical expertise in green hydrogen production and purchasing electrolyser equipment. Three crore is a modest sum, essentially seed money for a research and development initiative. But the context makes it significant.

Gujarat is positioning itself as India's primary green hydrogen hub. The Kutch region in western Gujarat and the northern districts have been identified as ideal locations for large-scale green hydrogen production, thanks to abundant solar and wind resources and proximity to industrial consumers. The Gujarat government has been actively promoting green hydrogen through policy incentives and land allocation. If even a fraction of the planned green hydrogen capacity materializes, it will require massive grid infrastructure to connect electrolyser facilities to renewable energy sources and to distribute hydrogen and its derivatives to end users.

RPSL is positioning itself to be the EPC partner for this build-out. The logic is consistent with the company's historical playbook: identify the next wave of grid infrastructure demand, build the technical capability before the demand fully materializes, and be ready to execute when the tenders start flowing.

Meanwhile, the company has made a more immediate move into battery energy storage. In January 2026, RPSL received approval from GUVNL for a sixty-five-megawatt, one-hundred-and-thirty-megawatt-hour standalone battery energy storage project at Virpore in Gujarat. The company signed a twelve-year Battery Energy Storage Purchase Agreement at a tariff of one lakh eighty-nine thousand rupees per megawatt per month. In February 2026, RPSL incorporated a wholly owned subsidiary specifically for battery energy storage projects. This represents a meaningful expansion beyond traditional EPC into asset ownership, though on a scale that remains manageable relative to the company's balance sheet.

The risk, of course, is that green hydrogen remains in the "five years away" zone for longer than optimists expect. Electrolyser costs need to fall significantly. Green hydrogen production needs reliable, low-cost renewable electricity. The distribution infrastructure does not yet exist. RPSL's modest investment means the downside is limited, but the company could find itself with expertise that no one is ready to pay for if the timeline slips.

For investors, the 400kV credential is the near-term catalyst. It opens a new addressable market and validates RPSL's upward trajectory along the voltage curve. Green hydrogen and battery storage are longer-dated options that add strategic depth to the story without materially changing the near-term risk profile.

VII. The Playbook: Competitive Moats and Industry Dynamics

Now it is time to step back from the narrative and examine RPSL through the cold lens of competitive strategy. What are the structural advantages that protect this business, and how durable are they likely to be?

Start with Hamilton Helmer's Seven Powers framework. The most obvious power RPSL possesses is a Cornered Resource: specialized technical labor. There is a critical and well-documented shortage of certified technicians capable of performing extra-high-voltage cable jointing in India. The skills required, steady hands, deep electrical engineering knowledge, years of supervised practice, and the temperament to work with equipment where a mistake can be fatal, cannot be mass-produced through training academies. RPSL has spent decades recruiting, training, and retaining these specialists. Competitors cannot simply hire them away because the supply does not exist in the open market, and building an internal training pipeline takes years.

The second power is Switching Costs, primarily driven through the HKRP SCADA integration discussed earlier. Once a utility has deployed HKRP's monitoring platform across hundreds or thousands of substations, the operational and financial cost of switching to an alternative provider creates a powerful lock-in effect. This is the classic "razor and blade" dynamic, except that both the razor (RPSL's physical infrastructure) and the blade (HKRP's software) are sticky in their own right.

The third power is emerging Scale Economies. As RPSL's order book has grown past three thousand five hundred crore, its procurement leverage for cables, transformers, switchgear, and other major components has improved significantly. The company can negotiate better pricing from suppliers, secure priority allocation during supply shortages, and amortize its overhead costs across a larger revenue base. This advantage compounds over time: larger order books attract better suppliers, better suppliers enable better project execution, better execution wins larger orders.

Now apply Porter's Five Forces.

Bargaining Power of Buyers is the most obvious risk. RPSL's primary customers are government-owned utilities, which are large, sophisticated, and price-sensitive. Historically, Indian government procurement has been dominated by the L1 system, where the lowest bidder wins. This is brutal for contractors because it commoditizes their capabilities and drives margins toward zero. However, the industry has been gradually shifting toward what is called Q1 procurement, where technical qualification is weighted alongside price. For specialized work like 400kV GIS installation, technical qualification is not just a factor but the primary determinant, because the consequences of awarding such a contract to an unqualified bidder are catastrophic. This shift benefits RPSL enormously.

Threat of New Entrants is low and getting lower. The barriers to entering the extra-high-voltage underground cabling and GIS installation space are formidable. You need decades of documented project history to qualify for tenders. You need specialized equipment that costs crore of rupees and takes months to procure. You need a trained workforce that takes years to develop. And you need relationships with utilities that are built over multiple successful project deliveries. A new entrant with deep pockets and ambition would need five to ten years of sustained investment before they could compete for the contracts that RPSL wins today.

Threat of Substitutes is minimal in the near term. Underground cabling is not a technology that can be disrupted by some clever software innovation. It is physical infrastructure that must be engineered, manufactured, transported, installed, and maintained in the real world. Wireless power transmission and distributed microgrids represent long-term theoretical substitutes, but for the foreseeable future, copper and aluminum cables buried in concrete ducts remain the only proven technology for urban power distribution.

Supplier Power is moderate. RPSL does not manufacture cables or transformers. It procures them from established manufacturers and provides the engineering, installation, and commissioning services. This means it is dependent on a supply chain that can experience shortages and price fluctuations. However, RPSL's growing scale mitigates this risk, and the EPC model means that material cost increases can often be passed through to clients under cost-escalation clauses in long-term contracts.

Competitive Rivalry within RPSL's specific niche is manageable. The company's direct peers, firms like Advait Energy, Viviana Power Tech, Kay Cee Energy and Infra, and Kaycee Industries, are generally smaller, with market capitalizations below RPSL's roughly sixteen-hundred-crore level. The larger industry players like L&T, KEC International, and Kalpataru Projects International operate at a different scale and focus more heavily on overhead transmission, leaving the specialized underground and GIS niche as a space where RPSL can compete without facing the full weight of these conglomerates.

The risks that keep this thesis in check are concentration and execution. RPSL derives the overwhelming majority of its revenue from Gujarat. If the state's infrastructure spending decelerates, whether due to political changes, fiscal constraints, or shifting priorities, RPSL's growth could stall. The company has begun expanding into Rajasthan, where its order book grew from ten to twelve crore in 2021 to two hundred to two hundred fifty crore, and has taken on projects in Uttarakhand, Madhya Pradesh, Jharkhand, and Odisha. A joint venture with VITS Total Power Solutions for a 132kV railway transmission line project under East Central Railway's Danapur division represents another diversification effort. But Gujarat remains the heartland, and geographic concentration remains the single biggest risk factor.

Execution risk compounds with scale. Managing a three-thousand-five-hundred-crore order book requires fundamentally different organizational capabilities than managing a three-hundred-crore one. The company needs to hire and train hundreds of additional technicians, manage multiple large projects simultaneously, coordinate complex supply chains, and maintain quality standards across a much larger operational footprint. The transition from "founder-driven execution" to "institutional project management" is the bridge that many infrastructure companies fail to cross.

VIII. Bear vs. Bull and The "Gujarat" Premium

The bull case for RPSL begins with the sheer scale of the addressable market. India's planned transmission and distribution capital expenditure exceeds nine lakh twelve thousand crore rupees through 2032. India's peak power demand recently hit a record of two hundred and fifty gigawatts and continues to climb as the economy grows, urbanization accelerates, and new demand sources like electric vehicles and data centers come online. Every gigawatt of new generation capacity requires corresponding investment in the grid infrastructure to transmit and distribute it. RPSL sits squarely in the path of this spending.

The MoU with the Gujarat government provides a specific, quantifiable roadmap. At four thousand seven hundred fifty-four crore rupees, it represents a pipeline that, if executed even partially, would transform the company's revenue trajectory over the next several years. The MoU was signed at the Vibrant Gujarat Regional Conference in Mehsana and covers power transmission and distribution projects, primarily focused on converting overhead high tension lines to underground cable networks across Gujarat. It is expected to create over thirty-three thousand jobs in the state. An MoU is not a binding contract, and the actual order flow will depend on government budgets, regulatory approvals, and competitive bidding. But it signals a clear intent and provides RPSL with visibility that few companies its size enjoy.

The HKRP stake adds a technology premium to what would otherwise be a pure infrastructure play. If India's grid modernization follows the trajectory of other developing markets, the demand for smart grid software, IoT monitoring, and SCADA systems will grow faster than the demand for physical infrastructure. RPSL's ownership stake in HKRP means it participates in both curves, capturing the margin from hardware installation and the recurring value from software-enabled monitoring.

The financial trajectory supports the bull case. Revenue growth of nearly two hundred ninety percent in FY25, profit growth of two hundred fifty-eight percent, and an improving PAT margin that expanded from three percent to over eight percent demonstrate that the company is not just growing but growing profitably. In the first half of FY26, revenue grew a further one hundred four percent year over year, EBITDA margins expanded to over thirteen percent, and net worth nearly tripled.

The bear case centers on concentration risk and execution uncertainty. Geographic concentration in Gujarat means RPSL is essentially a single-state play. The state's infrastructure spending is currently at a cyclical high, driven by favorable political alignment between state and central governments, strong industrial investment, and an aggressive renewable energy push. If any of these tailwinds weaken, RPSL's growth could decelerate sharply.

The government utility customer base introduces its own risks. Payment cycles for state utilities can be extended, sometimes stretching to six months or longer. Working capital management becomes critical at scale. Receivables from government entities are generally considered low-risk for default but can create significant cash flow strain for a growing contractor. RPSL's expansion into asset ownership through the BESS project, while modest in scale, represents a philosophical shift from asset-light EPC toward capital-intensive operations that carry balance sheet risk.

The green hydrogen investment, while limited to three crore rupees, represents a strategic bet on a technology that remains commercially unproven at scale. If the green hydrogen timeline extends beyond current projections, as many energy analysts expect, RPSL could find itself maintaining capabilities with no near-term revenue opportunity.

Valuation is always relative in the SME space, where comparisons are imperfect and liquidity premiums distort multiples. RPSL's market capitalization of approximately sixteen hundred crore against trailing earnings of ninety-three crore in FY25 implies a price-to-earnings ratio that reflects significant growth expectations. Whether those expectations are justified depends entirely on execution.

The HKRP stake is difficult to value independently. The question for investors is whether RPSL "overpaid" for this position or acquired it at a strategic discount. Given that HKRP became a public limited company only in July 2024, its financials and growth trajectory are still emerging. If HKRP can replicate its Gujarat SCADA deployments in other states, the stake could prove to be extraordinarily valuable. If HKRP remains a niche regional player, it is a complement to the core business but not a needle-mover.

For investors tracking this company, three KPIs deserve ongoing attention above all others. First, order book-to-revenue ratio, which measures how many years of revenue visibility the current pipeline provides; a sustained ratio above three signals strong demand and commercial momentum. Second, EBITDA margin trajectory, which reveals whether the company is successfully moving up the value chain into higher-margin specialized work or being dragged back into commodity contracting. At thirteen percent in H1 FY26, the trend is favorable, but this metric will tell the story of whether RPSL can sustain its pricing power as it scales.

The final reflection on Rajesh Power is that it represents a "pick and shovel" play on the Indian energy transition. The company does not need solar to beat wind, or green hydrogen to beat natural gas, or any particular technology to "win." It just needs India to keep building and upgrading its grid, which is as close to a certainty as infrastructure investing offers. The question is not whether the demand exists. The demand is overwhelming. The question is whether RPSL can scale its organization fast enough to capture its share, execute its projects flawlessly enough to protect its reputation, and expand beyond Gujarat before the growth premium in its valuation demands it.

IX. Closing Thoughts

The arc from Rajesh Traders to Rajesh Power Services traces one of those quiet transformations that the Indian infrastructure story produces in abundance but rarely celebrates. A 1971 consultancy that understood the power grid's pain points from the inside. A multi-decade build of technical credibility in the most demanding specialization within power transmission. A technology investment through HKRP that adds a software layer on top of the physical infrastructure. And an IPO that submitted the entire operation to the discipline and opportunity of public markets.

The story of RPSL is, at its core, about the infrastructure behind the infrastructure. It is a reminder that the most consequential companies in the energy transition are not always the ones building the solar panels or manufacturing the batteries. Sometimes they are the ones running the cables underground, commissioning the substations, and writing the software that makes sure the lights stay on when thirty thousand nodes are humming at full capacity across an entire state.

If you want to understand the future of the Indian grid, do not look at the power plants. Look at the substations. Look at who builds them, who monitors them, and who the utilities call at two in the morning when something goes wrong. Increasingly, in Gujarat at least, the answer is Rajesh Power.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube