Harshdeep Hortico: Scaling the Economics of the Green Revolution

I. Introduction & Episode Roadmap

Walk into the marble-and-glass arrivals hall of Mumbai's international airport, or the newly minted terminal at Mangaluru, and you will pass a row of tall, sculptural planters holding manicured greenery. Most travellers never look twice. They assume the pots are imported, or that they materialised from some anonymous corner of the supply chain. Almost nobody realises they are looking at the product of a company that started in a small Thane workshop in 1999 with roughly ₹50,000 of capital and a pile of borrowed equipment.1 Those airport planters were a real, invoiced order — ₹64.9 lakh for Mumbai and ₹21.7 lakh for Mangaluru, both operated by the Adani Group — booked in September 2024 by a firm most public-market investors have never heard of.2

That firm is Harshdeep Hortico Limited, ticker 544105 on the BSE-SME platform. It is a micro-cap by any definition — a market value that has hovered in the region of ₹130–170 crore since its listing.3 And yet it has quietly done something unusual: it has begun to institutionalise one of the most fragmented, unglamorous, and stubbornly unorganised industries in India — the business of pots, planters, and garden accessories. This is an industry where your typical competitor is a family running a kiln in a semi-rural lot, or an importer bringing in a container of cheap unbranded plastic from China. It is not where you expect to find a listed company earning gross margins near 46% and a full-year EBITDA margin approaching 29%.4

The central puzzle of this story is exactly that tension. How does a business built on plastic flowerpots — a product most people would classify as a low-value commodity — generate the kind of profitability that would make a branded consumer company proud? In the second half of the fiscal year ending March 2026, management reported an EBITDA margin of roughly 31%.5 For a company that melts petroleum-derived polymer and moulds it into garden décor, that number demands scrutiny rather than applause.

This episode traces four intertwined themes. The first is a materials story: the slow migration of the Indian nursery market from fragile clay and heavy cement toward engineered polymers. The second is a distribution story: how a business-to-business dealer network became the closest thing this company has to a moat. The third is a commodity story: the uncomfortable truth that a "premium" brand melting polypropylene remains hostage to crude oil cycles. And the fourth is a capital-markets story: how a family proprietorship used a modest SME listing not as an exit but as a deleveraging and working-capital engine, and what that did to its margins.

Throughout, the posture here is neutral. Harshdeep tells a good story about itself, and much of it checks out. But a good narrative is not the same as a durable competitive advantage, and a two-year run of expanding margins is not the same as a proven cycle-tested franchise. Let us start where the story starts — in the workshop.

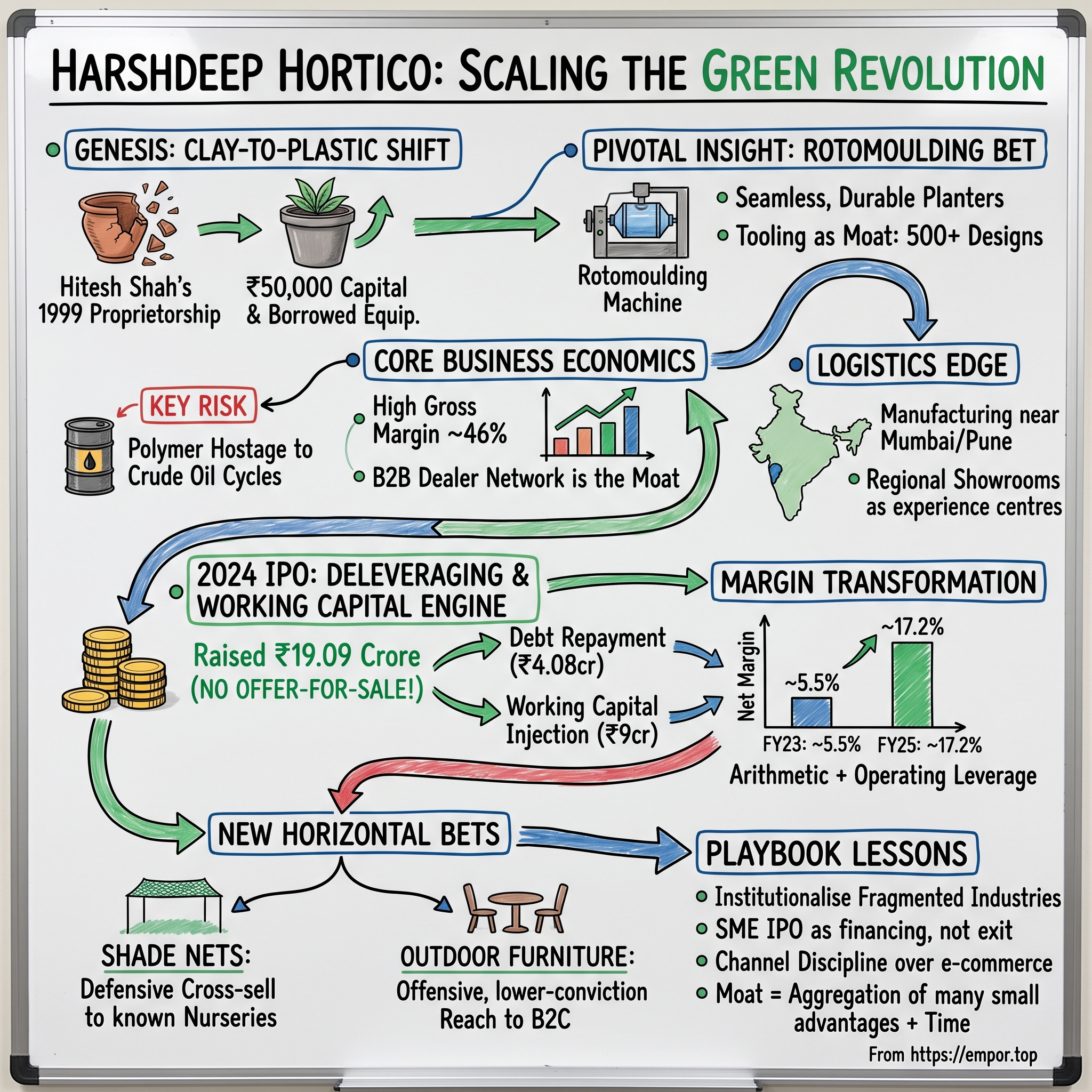

II. The Genesis: Hitesh Shah's Proprietorship & the Clay-to-Plastic Shift

Picture the Indian nursery trade at the close of the 1990s. It was, in the truest sense, a cottage economy. A gardener or landscaper wanting pots bought them from whoever fired clay locally, or from a cement caster down the road. The product was terracotta or concrete — beautiful, traditional, and deeply impractical the moment you tried to move it. Clay shattered in transit. Cement was back-breakingly heavy. Neither offered much in the way of design, and both were priced by the kilogram of raw earth rather than by any notion of a brand.

Into this world stepped Hitesh Chunilal Shah. He came from modest circumstances — the son of a grain merchant — and in 1999 he launched a sole proprietorship called Harshdeep Agro Products out of a small workshop in Thane, on the northern edge of Mumbai.1 The starting capital was roughly ₹50,000, supplemented by borrowed machinery, and the early output was exactly what you would expect: basic garden pots, hand-supplied to nurseries around Pune and the western suburbs.1 There was nothing inevitable about what came next. The early years were, by the founder's own account, a grind of inconsistent demand, thin cash flow, and debt.

The pivotal insight was not a product; it was a frustration. Shah kept running into the same operational complaints from the nursery owners and landscapers he sold to. Clay pots broke on the truck, so a shipment of a hundred might arrive as ninety intact and ten shards — a breakage tax baked into every delivery. Cement was so heavy that freight ate the margin and workers hated hauling it. And neither material let a buyer choose a shape, a colour, or a finish. The answer, Shah reasoned, was to abandon earth entirely and mould pots from plastic — polymers that were light, effectively unbreakable in transit, and infinitely variable in form and colour.

The bet required capital he did not really have. The turning point came when he saved enough to buy a rotational moulding machine for around ₹10 lakh — a purchase he later described as an enormous risk at the time.1 Rotational moulding, or "rotomoulding," is worth pausing on, because it is central to how this business works. Imagine a hollow metal mould shaped like a planter. You pour in a measured charge of polymer powder, close it, and then slowly rotate it in two axes inside an oven. The powder melts and coats the inside walls evenly by gravity and tumbling — no injection pressure required. The result is a seamless, hollow, thick-walled object that is remarkably durable and can be made very large. It is the same process used for water tanks and kayaks. For a garden planter that has to survive years of sun, monsoon, and rough handling, it is close to ideal.

That single machine converted a pot-reseller into a manufacturer, and it seeded what would become the company's real asset base: moulds. Each new design requires its own tooling, and tooling is expensive. But once you own the mould, the marginal cost of the hundredth or thousandth pot is just polymer, power, and labour. Over two decades, Shah accumulated a catalogue of designs and the moulds to make them — a slow-compounding library that a new entrant cannot replicate with a single machine and a good idea.

The other quiet asset built in these years was relationships. Selling to nurseries, landscapers, and eventually municipal bodies is a trust business: buyers reorder from suppliers who deliver consistent quality and stand behind it. Shah spent years becoming that supplier. The "Harshdeep" name, attached to a product category that was otherwise entirely unbranded, began to mean something — not to consumers, who rarely knew it, but to the trade, which did. That B2B credibility, accumulated pot by pot, is the foundation everything later was built on. And it set up the question the next chapter has to answer: what exactly do you own when your product is, at bottom, moulded plastic that anyone can also mould?

III. The Core Business: Planter Economics & Industry Structure

Here is the uncomfortable place to begin an analysis of Harshdeep: the barriers to entry in plastic pots are, at the unit level, almost non-existent. Anyone with a moulding machine and a polymer supplier can make a bucket-shaped pot. Walk any wholesale market and you will find the two archetypal competitors. On one side sit the unorganised local players — small potteries and moulders, often unbranded, competing purely on price. On the other sit importers bringing in cheap, low-durability plastic planters, historically much of it from China, that undercut on shelf price and disappoint on lifespan. This is not a market with a natural monopoly waiting to be claimed.

So the interesting question is not "why is this hard to enter?" but "what does Harshdeep do that turns a commodity into something with pricing power?" The company's answer has three parts, and each deserves testing rather than acceptance.

The first is catalogue scale. Harshdeep operates a portfolio of more than 2,200 stock-keeping units built on 500-plus distinct designs, spanning indoor planters, outdoor planters, decorative ranges, illuminated (LED) planters, rotomoulded pieces, fibre-reinforced plastic (FRP) planters, and an "Eco Series" using rice husk and natural-fibre materials.67 This matters because of how the buyers actually buy. A landscape architect specifying pots for a residential tower or a corporate campus does not want to source a dozen shapes from a dozen vendors; they want one supplier who can deliver a coordinated range, in stock, in the sizes and finishes the design calls for. Breadth is a service. It is also a barrier — not because any single SKU is hard to copy, but because the whole library, plus the moulds behind it, plus the inventory to serve it on demand, is expensive to assemble.

The second is the manufacturing footprint. Harshdeep runs two principal units in Maharashtra — a larger facility at Bhiwandi of roughly 93,700 square feet and a Pune plant that stood near 40,000 square feet before expansion — together comprising well over 130,000 square feet of capacity.8 In-house design and mould-making sit at the centre of this. The ability to conceive a design, cut the mould, and run it on both injection and rotational lines is precisely the capital-intensive step that a small imitator cannot afford. This is Harshdeep's cleanest genuine advantage: not the pots, but the tooling and design capability that produce them at scale.

The third — and arguably the most underrated — is logistics. A planter is a paradox of freight: voluminous but light. You are, in effect, paying to ship air inside a plastic shell. That makes transport cost enormous relative to product value, and it is why cheap imports and distant manufacturers struggle to serve the premium end economically. Harshdeep's response is geographic: manufacture close to India's commercial heartland around Mumbai and Pune, then push product outward through regional showrooms and warehousing in Ahmedabad, Delhi, Hyderabad, Bengaluru, and Rajahmundry.7 By shortening the average haul from factory to buyer, the company protects a cost position that an importer physically cannot match on bulky, low-value goods. This is a real, structural edge — though it is a regional one, and it would erode if a well-capitalised competitor built comparable capacity near the same demand centres.

Now the economics. The company earns gross margins in the region of 46%, which for a plastic-moulding business is high and signals genuine brand premiumisation and pricing power at the design-led premium end.6 But that gross margin sits atop a cost structure with two exposed nerves. The first is raw material. Harshdeep's inputs are petroleum-derived polymers — polypropylene, HDPE, LDPE, and Nylon 66 — whose prices track crude oil. When crude spikes, polymer follows, and a B2B business cannot instantly reprice a distributor catalogue; there is a lag during which margin gets squeezed. The second is power and fuel. Rotational and injection moulding are energy-hungry — you are heating and cooling metal moulds continuously — so electricity tariffs and factory utilisation are not footnotes but core operating levers. A half-empty plant spreads fixed energy and overhead across too few units.

The takeaway for an investor is balanced. Harshdeep has manufactured a real margin structure out of design, breadth, and freight geography. But the moat is a composite of modest, replicable advantages rather than one unassailable one, and the input side leaves the whole edifice exposed to a commodity it does not control. That exposure is exactly why the events of 2022–2024 — corporatisation and a public listing — mattered so much.

IV. The Corporate Transition & The 2024 IPO Catalyst

For twenty-three years, Harshdeep was a proprietorship — a single individual's business, with a single individual's balance sheet and a single individual's appetite for debt. The machinery that changed the trajectory was not a new product. It was a legal reorganisation and a stock listing.

The first move came quietly in December 2022, when the proprietorship was reconstituted as Harshdeep Hortico Limited, a public limited company. This was the necessary plumbing for everything that followed: you cannot list what is legally one person. Just as important, this period coincided with the arrival of the next generation. Harshit Hitesh Shah — the founder's son, a mechanical engineer with an MBA from NMIMS — had joined the business around 2020 and set about converting a family workshop into a corporate entity, professionalising processes and, by his own account, growing the team from roughly 75 people toward 300-plus and revenue from around ₹30 crore toward ₹60 crore.1 The father-son division of labour — Hitesh as the founding operator, Harshit as the corporatising modernizer — is the human engine of the transition.

Then came the event itself. In late January 2024, Harshdeep opened its SME IPO on the BSE-SME platform: a pure fresh issue of 42.42 lakh shares priced at ₹45 (within a ₹42–45 band), raising ₹19.09 crore.9 Bidding ran from January 29 to 31, 2024, allotment was finalised on February 1, and the shares listed on February 5 at ₹70 — a listing-day pop of roughly 56%.910 The lead manager was Hem Securities. One detail matters enormously for reading management's intent: there was no offer-for-sale component. Not a single promoter share was sold. Every rupee raised went into the company, not into the founders' pockets. In a market where SME IPOs are too often disguised exits, that is a meaningful signal of alignment.

What did the company do with the money? The use of proceeds was deliberately unglamorous: repay roughly ₹4.08 crore of high-cost debt and inject about ₹9 crore into working capital, with the balance for general corporate purposes.9 This is the fulcrum of the entire investment story, so it is worth explaining why it mattered rather than just noting it.

Consider the arithmetic of deleveraging. High-cost debt in the Indian SME world can carry double-digit interest rates. Retiring ₹4 crore of it removes a fixed charge that was previously eating into pre-tax profit every year. Simultaneously, injecting working capital solved the business's structural constraint: a company holding 2,200 SKUs in inventory and extending credit to builders and distributors is perpetually starved of cash, and cash starvation caps growth. Give it working capital and it can hold more stock, serve more orders on demand, and take on larger institutional contracts without choking.

The result was a margin transformation that is genuinely striking, though it needs the right caveat. In FY23, the business earned a net profit of roughly ₹2.23 crore on revenue of about ₹40.77 crore — a net margin near 5.5%.[^11] By FY25, revenue had grown to ₹56.27 crore and net profit to ₹9.70 crore, a margin of about 17.2%.[^11] And in the year ended March 2026, revenue reached ₹68.74 crore with profit after tax of ₹12.52 crore — up 29% year on year — for a net margin around 18%.4 Profit before tax rose 41% to ₹16.04 crore, EBITDA rose 32% to ₹19.78 crore, and net worth climbed 44% to ₹59.94 crore, producing a return on equity of 23.3%.4

Here is the analytical point that management's press releases will not volunteer: a large share of that net-margin leap from 5.5% to 18% is arithmetic, not operating magic. Removing interest expense and taxing a cleaner pre-tax number mechanically lifts net margin even if the underlying gross margin barely moves. The deleveraging was real and value-creating — but an investor should credit it as balance-sheet repair plus operating leverage on rising volumes, not as evidence that the core pot business suddenly became twice as good. The genuinely encouraging signals are the 22% revenue growth and the EBITDA expansion, which speak to demand and operating leverage. Sustaining a ~23% ROE from here, with the debt already retired, will have to come from the business, not the balance sheet. And the business, as the next chapter shows, runs on a distribution engine that is easy to describe and hard to build.

V. Core Distribution: The B2B Engine vs. B2C Showroom Play

There is a temptation, when a garden-products company opens glossy showrooms in metros, to assume it is chasing the consumer. Harshdeep's structure says the opposite. Roughly three-quarters of its revenue comes from B2B — institutional and wholesale channels — and only about a quarter from retail and B2C.6 Understanding why the company guards that ratio, rather than trying to flip it, is the key to the whole strategy.

Start with the B2B engine, because it is where the durability lives. Harshdeep sells through a pan-India network — a modest number of exclusive distributors (the company has described roughly ten to a low-teens count) sitting atop a much broader base of dealers, reaching buyers across 27 states and union territories.117 The customers at the end of that pipe are the ones that make the model interesting: large real-estate developers and their landscapers, infrastructure projects, and institutional buyers. The company has publicly booked orders from Adani-operated airports at Mumbai and Mangaluru, and management points to relationships across major builders and large infrastructure sites as the backbone of demand.2 Claims of specific marquee developer relationships such as Lodha or DLF come largely from company framing rather than independent disclosure, and should be read as management's characterisation of its client base rather than audited fact.

Why is this a moat and not just a customer list? Because institutional buyers, once they have specified and approved a supplier, are sticky. A developer whose landscape architect has already selected Harshdeep pots for one tower, verified the quality, and integrated them into a design specification faces real friction switching to an unknown vendor to save a few percent on a low-value line item. The switching cost is not enormous, but it is real, and it recurs project after project. Combined with the freight-geography advantage and the on-demand breadth of the catalogue, it produces reorder behaviour that unorganised competitors cannot easily poach.

Now the showrooms — and here is the strategic subtlety. Harshdeep's physical showrooms in metros are not really retail outlets in the mass-market sense; they function as experience centres aimed at architects, interior designers, and specifiers.7 The logic is elegant. The person who decides which planters go into a ₹500-crore residential project is not a walk-in shopper; it is a design professional who wants to see, touch, and imagine the product at scale. A showroom converts that professional into a channel: they specify Harshdeep, and the order then flows through the B2B network. The showroom is marketing for the wholesale business dressed up as retail.

Which brings us to the most deliberate choice of all: Harshdeep has kept direct online B2C sales intentionally minimal, even as it lists on marketplaces like Amazon and Flipkart.12 To an outside observer trained on direct-to-consumer playbooks, this looks like leaving money on the table. It is actually channel-conflict management. If Harshdeep aggressively sold to end consumers online at competitive prices, it would undercut the very distributors and dealers who carry its inventory, service its institutional accounts, and give it reach into 27 states. Cannibalising your own distribution to chase thin-margin e-commerce volume is a classic way to blow up a wholesale business. By restraining B2C, Harshdeep protects the loyalty of the network that is its actual competitive asset. Whether that discipline holds as the brand grows — and as the temptation of high-margin direct sales increases — is a genuine open question.

Exports round out the picture, and honesty requires calling them what they are: nascent. International sales contributed roughly 2% of total revenue, sold into select markets in Europe, Africa, and Asia, supported by an international sales presence including a sales office in Amsterdam.71 The strategic logic — targeting higher-margin overseas garden-centre chains — is sound, and the freight math is less punishing for premium products, but at 2% of revenue this is optionality, not yet a business line. The same "promising but small" description applies to the new categories the company is betting on next.

VI. New Horizonal Bets: Shade Nets & Outdoor Furniture

Every specialist eventually confronts the same question: do you go deeper in your niche, or do you use your distribution to sell adjacent products to the same customers? In August 2024, Harshdeep answered by announcing an expansion into two new lines, and the tell is in whom they are aimed at.

The first bet is AgriShield shade nets. The company expanded its Pune plant by 12,000 square feet — taking that facility past 50,000 square feet — to establish an annual capacity of 210,000 kilograms of nursery shade netting.7 Shade nets are the fabric-like mesh that growers stretch over nurseries and farms to regulate sunlight, temperature, and moisture — an everyday necessity for the exact commercial nurseries and large growers who already buy Harshdeep's planters. That customer overlap is the entire rationale. A distributor already carrying Harshdeep pots to a nursery can now put shade nets on the same invoice, and the sales relationship that took years to build gets amortised across a second product. In FY26, shade nets contributed roughly 3% of total revenue — small, but it is a first-year contribution from a standing start, and the cross-sell logic is coherent rather than a random diversification.6

The word "coherent" matters, because the graveyard of small companies is full of adjacencies that made a slide look good and a P&L look worse. Shade nets pass the test that a lot of "diworsification" fails: they are sold to the same buyer, through the same channel, using broadly similar polymer-processing know-how. That is genuine adjacency, not empire-building.

The second bet is more speculative: rotomoulded outdoor furniture, plus a range of decorative garden fountains. On April 19, 2026, the company launched what it described as India's first rotomoulded indoor and outdoor fountain range.5 Here the strategic fit is looser. Outdoor furniture uses the same rotational-moulding technology and the same weather-resistant durability story, so on the factory floor it is a natural extension. But the customer is different. Furniture and fountains reach toward the premium residential B2C market — a buyer Harshdeep has, by design, deliberately underserved. So this line asks the company to develop a muscle (consumer-facing premium retail) it has consciously not built, which is precisely why it should be treated as real optionality rather than a core plan. It is sized smaller than the planter business but carries the promise of higher absolute margins per piece if it works.

The honest framing is this: shade nets are a defensive, high-conviction cross-sell to a known customer; furniture and fountains are an offensive, lower-conviction reach toward a new one. Both are early enough that neither should be underwritten as a certainty, and management's own language — "we hope to add significantly to our revenues in the coming years" — is aspirational rather than committed.7 For an investor, the right posture is to watch the revenue contribution of these non-planter lines as a live experiment in whether Harshdeep's distribution can carry more than pots. That experiment, in turn, is only as good as the people running it and the discipline with which they allocate capital.

VII. Management Assessment & Capital Allocation Strategy

The leadership of Harshdeep is, by design, a two-person story. Hitesh Chunilal Shah serves as Chairman and Managing Director — the founder-operator whose two-decade slog built the moulds, the catalogue, and the trade relationships. Harshit Hitesh Shah serves as Whole-time Director and, in the group's framing, the finance and modernisation lead — the second-generation professionaliser who steered the corporatisation and listing.1 It is a classic Indian promoter-family structure, with the attendant strengths and weaknesses: deep operational knowledge and long-term commitment on one hand, concentration and key-person risk on the other.

On alignment, the numbers are unambiguous. The promoter group held about 72.96% of the company after the IPO, down from Hitesh Shah's roughly 97.4% pre-issue — a reduction that reflects the fresh-issue dilution, not any promoter selling.[^11]13 A curiosity worth naming: Harshit Shah is reported to hold effectively no shares individually, with the family's economic interest concentrated in the promoter group and the father's holding.13 For an outside minority investor, the practical implication is straightforward — this remains a founder-controlled company where the family's incentives are overwhelmingly tied to the equity, but where minority holders have essentially no ability to influence outcomes. Skin in the game is enormous; independent oversight is correspondingly thin, as is typical for a micro-cap SME.

The capital-allocation record, over the short window since listing, has been coherent and conservative — and that consistency is itself the most useful evidence about management. There has been no dilutive or empire-building M&A; capital has gone into factory capacity, additional moulds, working capital, and debt reduction.7 The absence of an offer-for-sale in the IPO, the immediate use of proceeds to retire high-cost debt, and the organic-only growth all tell the same story: management has, so far, done what it said it would do with cash. In a segment of the market notorious for the opposite, that is worth crediting — while remembering that the track record as a public company is barely two years long, which is far too short to declare capital discipline a settled trait.

The genuine operational drag — and the item a skeptic should press hardest on — is the working-capital cycle. The B2B model is structurally cash-hungry from both ends. On one side, serving 2,200-plus SKUs on demand requires carrying a large inventory, because a distributor who wants a specific planter in a specific size expects it in stock, not in six weeks. On the other, selling to large builders and distributors means extending credit — receivables that stretch out for months. The gap between paying for polymer and collecting from a developer is the cash the business must fund, and it is exactly what the ₹9 crore working-capital injection from the IPO was meant to relieve. It is not a one-time problem; it grows with revenue. If receivables lengthen or a large institutional buyer defaults, the pain would show up first here.

Finally, governance signalling. In FY26 the company declared its maiden dividend — a modest ₹0.25 per share.4 On its own, the amount is immaterial. As a signal, it is the kind of thing a maturing, post-IPO company does to tell the market it intends to behave like a real listed entity rather than a private fiefdom that happens to be quoted. It is a small down-payment on governance credibility, and it should be read as such — a gesture, not yet a policy. What all of this adds up to, in playbook terms, is the subject of the next chapter.

VIII. Playbook: Business & Investing Lessons

Step back from the specifics and Harshdeep offers a set of transferable lessons — some for operators, some for investors — about how value gets built in unglamorous corners of an economy.

The first lesson is that you can institutionalise a fragmented industry without inventing anything. Harshdeep did not discover a new polymer or a proprietary technology. Its edge was assembled from mundane parts: a wide SKU catalogue, an accumulating library of moulds, a regional manufacturing-and-distribution network positioned to beat freight economics, and years of trade relationships. Individually, each is copyable. Collectively, and compounded over two decades, they form a position a new entrant cannot cheaply assemble. The lesson is that in low-barrier industries, the moat is often the aggregation of many small advantages plus time — not a single defensible secret. The corollary, which an investor must hold onto, is that such moats are shallower and more contestable than a patent or a network effect, and they demand continuous reinvestment to stay ahead.

The second lesson is about the SME platform itself. Harshdeep used its listing the way capital markets are supposed to be used — as a financing event, not a liquidity event. Zero offer-for-sale, proceeds directed to deleveraging and working capital, and a resulting step-change in net margin driven substantially by lower interest cost. This is a template for how a profitable small business can use a modest public raise to unlock growth it could not self-fund. It is also a caution: the margin lift from deleveraging is a one-time reset, not a repeatable trick. You get to retire your expensive debt once.

The third lesson is the counterintuitive value of not chasing every channel. Harshdeep's deliberate restraint on direct e-commerce, to avoid cannibalising its distributor base, is a live demonstration that channel discipline can be worth more than incremental revenue. Many companies destroy their most valuable asset — a loyal distribution network — in pursuit of the shiny direct-to-consumer growth story. Protecting the people who carry your inventory and service your institutional accounts is sometimes the highest-return decision available.

The fourth lesson is the darker one, and it is the thread that runs through the whole business: the commodity-input trap. No matter how premium the brand, how clever the design, or how loyal the dealer, Harshdeep melts petroleum-derived polymer to make its products. Its cost base is chained to crude oil and to the pricing power of upstream polymer giants. Brand equity can buy pricing power and a repricing lag; it cannot sever the link to the input cost cycle. A premium consumer brand with a commodity cost structure is only as safe as the next crude spike is gentle. The company has not yet been tested by a violent input-cost cycle as a listed entity, and until it is, the durability of those gross margins remains a hypothesis rather than a proven fact. That hypothesis is what the formal competitive analysis has to stress-test.

IX. Analysis: Porter's 5 Forces, Helmer's 7 Powers, & The Stress Test

To move from narrative to discipline, it helps to run Harshdeep through two standard frameworks and then war-game the bull and bear cases. The point is not to reach a verdict but to locate precisely where the advantage is real and where it is fragile.

Porter's Five Forces. Begin with competitive rivalry, which is high in aggregate but uneven by segment. In the unorganised mass market, rivalry is brutal and price-driven. In the organised, design-led premium B2B segment where Harshdeep actually competes, rivalry is lower — there are simply fewer players who can offer a national branded catalogue with in-house moulding. Buyer power splits along the same seam: large real-estate and infrastructure buyers wield significant leverage on price and payment terms because their orders are big and they know it, whereas nursery distributors and fragmented B2C buyers have little. Supplier power is moderate: polymers are commoditised and available from large producers such as Reliance, so no single supplier holds Harshdeep hostage — but the entire supplier base reprices with crude, so the category exerts pressure even if no individual firm does. The substitution threat is moderate and permanent: traditional clay and concrete pots remain cheaper and will always appeal to the price-first buyer, but they cannot match plastic on weight, breakage, or design. And the barrier to new entry is genuinely high at the premium end — the capital for industrial injection and rotational moulds, plus the pan-India distribution logistics, is exactly what a garage competitor lacks — even as it stays low at the commodity end.

Hamilton Helmer's 7 Powers. Of Helmer's seven, three plausibly apply, and it is worth being strict about which. Scale economies are real but regional rather than national: 130,000-plus square feet of capacity and a large mould count lower unit cost meaningfully, though Harshdeep is not so large that scale alone crushes all comers. A cornered resource case can be made for the accumulated relationships with landscape architects, specifiers, and the largest nursery networks — access that took two decades to build — though "cornered" overstates it; these relationships are strong, not exclusive. Brand is the most interesting: "Harshdeep" is arguably the only listed, branded standard in an ocean of unbranded plastic, which confers recognition in the trade. But brand power in Helmer's strict sense requires customers to pay more for objectively identical goods purely on trust, and it is not yet clear Harshdeep's brand commands that at the consumer level, as opposed to simply signalling reliability to professional buyers. The other four powers — network economies, switching costs strong enough to be a standalone power, counter-positioning, and process power — are weak or absent. This is an honest three-out-of-seven, and the three are moderate rather than overwhelming.

The Investment Case Spine. The bull case is straightforward and not unreasonable. India's real-estate and infrastructure build-out continues to generate demand for institutional landscaping; urban premiumisation lifts the average selling price of décor; the balance sheet is now clean, removing the interest drag that once capped profit; and the adjacent bets, especially shade nets, offer credible cross-sell growth into an existing customer base. Stack those and you get a small company with a long runway and improving returns on capital.

The bear case is equally coherent, and it attacks the same points from the other side. A sharp, sustained crude-oil spike would drive polymer costs up faster than a B2B catalogue can be repriced, compressing the very gross margins the bull case relies on. The working-capital model is a slow-motion risk: heavy inventory plus extended receivables to large builders means a single bad debt or a general lengthening of payment terms could lock up cash and stall growth. And the low barrier at the commodity end means low-cost competition — domestic or imported — can perpetually pressure distributor margins, forcing Harshdeep to spend to defend its shelf. To these an activist skeptic would add three governance-and-quality flags proportionate to an SME: a promoter group holding nearly 73% leaves minority investors with no real voice; disclosure is thin relative to a mainboard company, so operating metrics must often be inferred; and the dazzling net-margin expansion is partly a one-time deleveraging effect that will not repeat. None of these is disqualifying, but each is real.

KPIs to Track. Cutting through all of it, three metrics carry most of the signal for this specific business. The first is the polymer raw-material price trend — polypropylene, HDPE, and LDPE — because it is the single largest swing factor on gross margin and the one thing management least controls. The second is the revenue contribution from non-planter segments, chiefly shade nets and furniture, because that is the live test of whether the distribution network can carry more than pots and justify the diversification. The third is working-capital days — receivables plus inventory — because that is where growth either funds itself or quietly chokes, and where the first sign of trouble with a large institutional buyer would appear. Watch those three and you are watching the parts of the story that can actually break.

X. Epilogue

Return, finally, to those airport planters. They are a fitting emblem for what Harshdeep Hortico has become and for the question it now faces. A product almost everyone ignores, made by a company almost no one has heard of, sold into a marquee infrastructure project through a distribution network built one relationship at a time — and, remarkably, at a margin that would flatter a branded consumer goods company.

The path forward forks. In one direction, Harshdeep remains what it is today: a highly profitable micro-cap gem, disciplined and cash-generative, dominating a niche too small and too unglamorous to attract a larger predator, compounding quietly. In the other, it uses its distribution muscle, its clean balance sheet, and its adjacent bets to scale into something bigger — a genuine mid-cap consumer-and-institutional garden brand, with shade nets, furniture, and exports carrying meaningful weight alongside the core planter business. Which path it takes will be decided less by the pots than by execution: by whether the working-capital cycle stays disciplined as revenue grows, whether the new categories earn their place, and whether the margins survive their first real encounter with a hostile input-cost cycle as a public company.

The genuine surprise of this story is not that a plastic-pot maker exists; it is the scale of profitability that turned out to be possible in a mundane utility product, once someone applied corporate discipline, capital-markets access, and two decades of patient network-building to it. That is the lesson worth carrying away — that unglamorous industries, run with discipline, can hide unexpected economics. Whether those economics prove durable through a full cycle is the test still to come, and it is the one an investor should keep watching.

References

-

Started With Just ₹50,000, This Mumbai-based Sustainable Garden & Horticulture Brand Is Now Worth ₹170 Crore — Startuppedia ↩↩↩↩↩↩↩

-

Harshdeep Hortico bags orders worth INR 86.6 lakhs from Mumbai and Mangaluru International Airports — PR Newswire, 2024-09-16 ↩↩

-

Harshdeep Hortico Reports Strong H2 FY26 — ANI News, 2026-05-05 ↩↩↩↩

-

Harshdeep Hortico Reports Strong H2 FY26 — The Tribune, 2026-05-05 ↩↩

-

Low PE Stock Reports 29% PAT Growth in FY26; Declares Dividend and Expands Into New Product Categories — DSIJ, 2026 ↩↩↩↩

-

Harshdeep Hortico Limited announces expansion plans — PR Newswire, 2024-08-28 ↩↩↩↩↩↩↩↩

-

Harshdeep Hortico Limited — Manufacturer of Flower Pot & Planter from Bhiwandi — IndiaMART ↩

-

Harshdeep Hortico IPO Date, Price, GMP, Review, Details — Chittorgarh ↩↩↩

-

Harshdeep Hortico Ltd IPO Review, Valuation & Details — Finowings ↩

-

Harshdeep Hortico Ltd. Latest Shareholding Pattern — Trendlyne ↩↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube