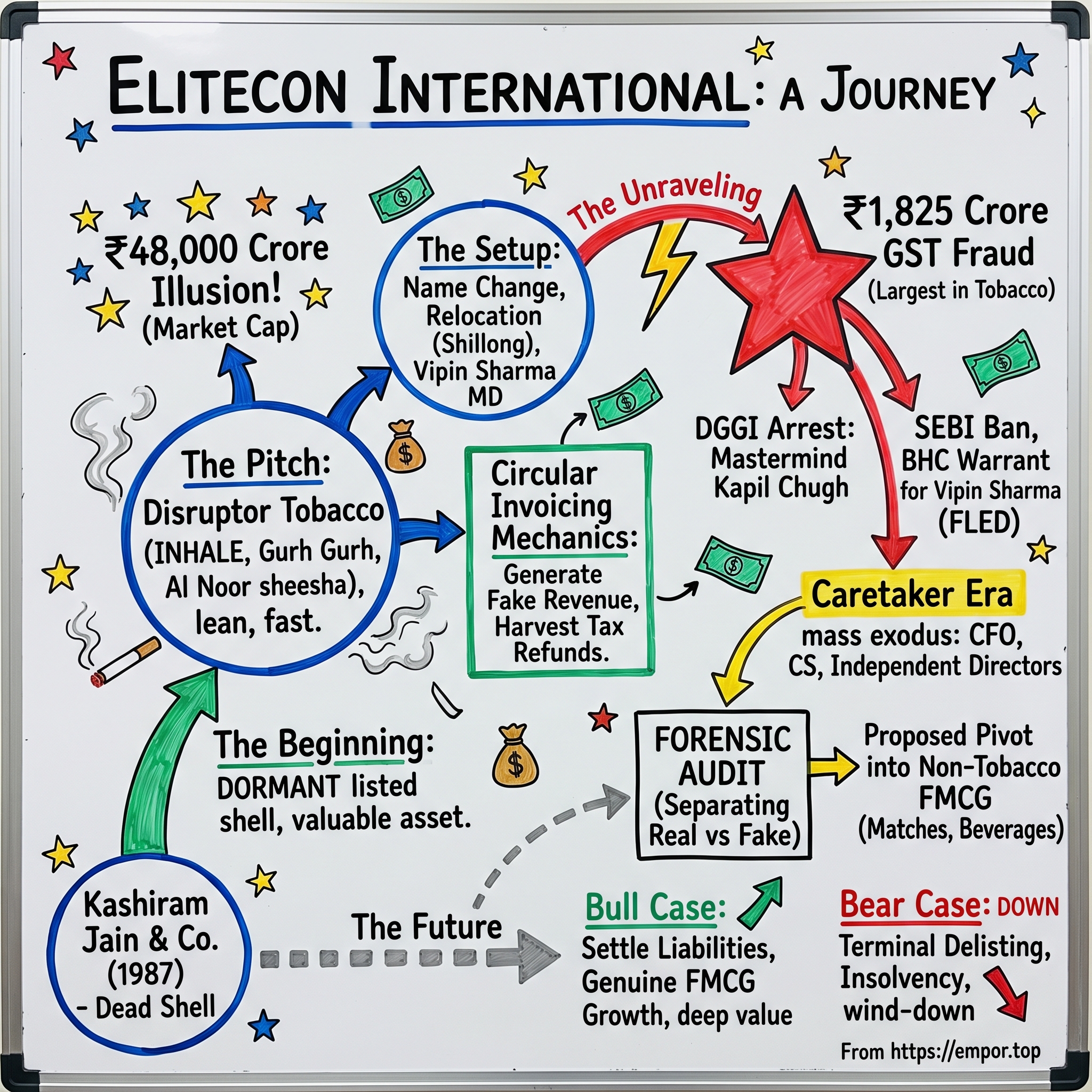

Elitecon International: The Anatomy of a ₹48,000 Crore Illusion

I. Introduction & Episode Setup

It is a sweltering morning in the back half of 2024, and somewhere in a cramped Mumbai apartment a retail investor is doing the thing every retail investor does first thing: refreshing a brokerage app before the kettle has even boiled. On the screen is a ticker that had, until recently, been the financial equivalent of a houseplant left to die in a dark corner — a penny stock bought eighteen months earlier for ₹1.10, almost as a joke, the kind of "lottery ticket" position you take when the entry cost is roughly the price of a vada pav. Except the houseplant has not died. The number reads ₹259.65.1

Do the arithmetic and your stomach drops. That is a 23,504% return — not over a decade, not over a career, but in roughly a year and a half. A stake that cost a few thousand rupees is now worth a small flat. And the company behind it, a sleepy entity called Elitecon International Limited, has been catapulted from total obscurity to a market capitalization of ₹48,035 Crore, or about $5.7 billion on paper.1[^2] On paper is doing an enormous amount of work in that sentence, but in the moment, nobody refreshing their screen cares about the qualifier. They are looking at a vertical green line that defies gravity, and they are wondering, as humans always do, whether it is too late to get in.

This is the story of how that line got drawn, and what was hiding underneath it.

The Pitch. Elitecon was sold to the market as something genuinely exciting: India's newest tobacco powerhouse. Not a stodgy legacy giant weighed down by century-old factories and unionized labor, but a lean, fast-moving disruptor. The narrative went like this — Elitecon manufactured and exported premium cigarettes, traditional smoking mixtures, and sheesha molasses across four continents, capturing fat export margins in the Gulf and Europe while the domestic incumbents fought trench warfare over India's saturated cigarette aisles. It was, in the language of the Telegram tip groups, "the next ITC," except capital-light, debt-free, and growing at a rate that no hundred-year-old company could ever match. To a market hungry for the next multibagger, it was catnip.

The Reality Check. Beneath the audited growth rates and the suspiciously pristine, debt-free balance sheet lay something far darker. In March and April 2026 — only weeks before this episode — the entire structure came apart in public, in real time. Elitecon was unmasked not as an operational miracle but as the visible, exchange-listed centerpiece of a ₹1,825 Crore GST refund fraud and a coordinated pump-and-dump scheme.3[^5] The exports that justified the valuation had, to a significant degree, never physically left the country. The revenues were, in substantial part, paper — circular invoices passed between dummy firms to manufacture the appearance of a thriving business and to harvest fraudulent tax refunds from the government.[^5] The market cap was an illusion, and the illusion had a price tag attached to it that taxpayers and retail shareholders would ultimately pay.

The Roadmap. Over the next two-plus hours, we are going to take this thing apart piece by piece, the way you would dismantle a magic trick once you know it was a trick:

- How a 32-year comatose listed shell — a company that began life in 1987 as Kashiram Jain and Company Limited — became a "global tobacco exporter" without ever really becoming one.

- The mechanics of circular invoicing: what fake billing actually is, in plain language, and why it is such a powerful tool for manufacturing both revenue and tax refunds out of thin air.

- The microstructure of the pump — upper circuits, a tiny free float, the conspicuous absence of futures and options, and an army of finfluencers — that allowed a stock to go vertical on almost no real volume.

- The regulatory bust: SEBI's ex-parte freeze in March 2026, the DGGI's dramatic airport arrest of the alleged mastermind in April, and the Bombay High Court's non-bailable warrants.23[^8]

- The caretaker era now unfolding — a retired IAS officer, a forensic auditor, and a proposed pivot into legitimate consumer goods — and whether there is anything real left to salvage.

- And finally, the playbook: the durable lessons for any long-term investor about information asymmetry in emerging markets, the seductive lie of "skin in the game," and why the oldest piece of fundamental-investing advice — go look at the shelf — has never stopped being the best.

There is a particular kind of business story that Acquired loves, which is the story of a company that built something extraordinary. This is the inverse: the story of a company that built the appearance of something extraordinary, and very nearly got away with it. Both, it turns out, teach you the same things about how value actually works — one by example, one by counterexample. Let's start at the beginning, in a quiet office in Northeast India, with a company that did nothing at all for three decades.

II. Shell Mechanics & The Lost Decades (1987–2019)

Picture the least cinematic company you can imagine. There is no garage, no whiteboard sketch, no founder pulling all-nighters. There is, instead, a registered office in Shillong — the cool, hill-station capital of Meghalaya in India's far Northeast — and a sheaf of statutory filings in a registrar's cabinet. On December 15, 1987, a company called Kashiram Jain and Company Limited was incorporated, with an authorized and paid-up capital of roughly ₹11 lakhs.5 Eleven lakhs. That is about the price of a modest hatchback today. It is the corporate equivalent of a seed that was planted and then, almost immediately, forgotten.

And forgotten it largely stayed. For more than three decades, Kashiram Jain was what market participants politely call a "dormant" company and what everyone else would simply call dead. There was no meaningful business activity to speak of. AGM filings trickled in sporadically, the bare minimum required to keep the listing alive. The stock — and it was, technically, a listed stock — sat below ₹2 for years on end, with effectively zero liquidity. On most days, not a single share changed hands. It was a ticker that existed the way a switched-off neon sign exists: present, inert, waiting.

Here is the question that matters, and it is the question that unlocks this entire genre of fraud: why do companies like this persist at all? Why does a commercial ghost sit on a stock exchange for thirty-two years instead of simply being wound up?

The answer is that a clean, dormant, listed shell is not worthless. It is, in fact, quietly valuable — and the value is structural. In India, taking a company public the legitimate way is a slow, expensive, intensely scrutinized ordeal. An IPO means merchant bankers, a draft red herring prospectus, SEBI review, due diligence, roadshows, underwriting, and a regulatory microscope trained on every claim you make about your business. It can take years and it can fail. A listed shell is a way to skip the entire queue. If you can quietly acquire control of a company that is already listed, you inherit the one thing the IPO process exists to grant — a public listing, a ticker, the ability to issue and trade shares to the general investing public — without submitting to the gauntlet that normally precedes it.

And a clean shell is the premium product. Think of it like buying a building. A used factory comes with someone else's problems — legacy debt, pension liabilities, unionized labor contracts, environmental cleanup, lawsuits, angry creditors. A pristine empty lot with a valid address and clear title comes with none of that. Kashiram Jain, having done essentially nothing for three decades, was a blank canvas. No operational baggage, no entangled liabilities, no skeletons — just a clean listing waiting for someone with a story to tell and the means to reverse-merge that story in through the back door. In the hands of an honest operator, a shell is a legitimate, if aggressive, route to public markets. In the hands of someone else, it is the perfect stage, pre-built and unencumbered, for a performance.

The first sign that the lights were about to come on arrived in November 2019. Quietly — and "quietly" is the operative word throughout this story — the company changed its name from Kashiram Jain and Company Limited to Elitecon International Limited, relocated its registered office, and became the object of patient, low-profile share accumulation.5 The buyers were a man named Vipin Sharma and a co-promoter vehicle called the DUC Education Foundation. None of this made headlines. A name change and an office move are about as boring as corporate filings get, which is precisely why they make such effective camouflage. To a casual observer, nothing was happening. To anyone who understood what a clean shell is for, everything was happening at once: a new name to anchor a new narrative, a fresh address to break continuity with the dead past, and a slow, deliberate hoovering-up of cheap shares before anyone was watching.

The canvas had been bought. The next step was to put a face on it — a managing director with a story, a sector, and an aura of expertise. That face arrived in 2021.

III. The Vipin Sharma Takeover & Capital Shuffling (2021–2023)

Every pump needs a protagonist, and Elitecon got Vipin Sharma. When he was appointed Managing Director in 2021, Sharma arrived wrapped in exactly the kind of biography that retail investors find reassuring: a tobacco veteran, a man of "domain expertise," someone who supposedly understood the unglamorous crafts that separate a real tobacco business from a pretender — sourcing leaf from the right regions, blending for taste and burn, curing to lock in aroma and shelf life. This is the language of a real industry, and deploying it fluently is half the battle in convincing the market that there is real industry underneath. Under Sharma's stewardship, the corporate focus shifted, on paper, from "dormant shell" to "active tobacco manufacturer." The story now had an author.

What happened next is the part that should have stopped every sophisticated observer cold, and it is worth slowing down on because it is the cleanest tell in the entire saga.

In 2024, Sharma executed an off-market block transaction to consolidate his grip on the company. He acquired an additional 7.23% stake — 87,500 shares — from the co-promoter DUC Education Foundation, the vehicle represented by Dina Nath Chugh. The price he paid was ₹0.92 million in total, which works out to roughly ₹10.5 per share.5

Now sit with that number for a moment, because the context is everything. At the time of this transaction, Elitecon shares were trading on the BSE at prices north of ₹200.1 So a major co-promoter block changed hands at a discount of more than 95% to the price that public investors were paying in the open market on the very same days. Let that asymmetry land. The general public was bidding the stock up past ₹200 in a frenzy. The insiders were transferring large blocks among themselves for the price of a cup of coffee.

In a well-functioning market, this almost never happens, and there are good reasons why. When a substantial block of shares is sold or a promoter stake is acquired, the price is normally pegged close to the recent volume-weighted average price (VWAP) — typically the two-week VWAP. That convention exists to protect minority shareholders and to ensure that insiders cannot quietly enrich themselves by moving assets around at fictional prices. A block deal struck at a 95% discount to the public price is not an arm's-length transaction between a willing buyer and a willing seller who disagree about value. It is something else entirely.

What it actually was, the regulators would later allege, was a transfer between people on the same side of the table. In market-structure terms, Sharma, the DUC Education Foundation, and their associates functioned as Persons Acting in Concert — PACs, in the regulatory jargon: parties who appear independent on the share register but are in fact coordinating their actions toward a common objective.2[^8] The point of moving 87,500 shares at ₹10.5 was not to change the economic reality of who controlled Elitecon — that group already controlled it. The point was to consolidate cheap shares in the right hands ahead of the next act: dumping those shares onto retail investors at ₹200-plus during the manufactured frenzy. You buy at ten and a half rupees on the inside. You sell at two hundred and sixty on the outside. The 95% discount was not an anomaly to be explained away; it was the entire business model, expressed in a single line of a related-party filing.

While the capital was being shuffled into position behind the curtain, the front-of-house operation was building a product story — because even a pump needs something to point at. Elitecon launched a portfolio designed to span the full price ladder of the smoking world:

- INHALE — cigarettes, positioned to undercut premium international brands. The aspirational, modern-trade play.

- Gurh Gurh — traditional smoking mixtures aimed at lower-income domestic consumers. The volume, mass-market play, rooted in India's deep and very old habits around jaggery-and-tobacco preparations.

- النور Al Noor — premium sheesha molasses, the flavored, sticky tobacco that fuels hookah lounges, pitched as "value-luxury" to capture lounges across the Middle East and Europe.

Three brands, three price points, three continents of ambition. On a pitch deck it looked like a thoughtfully segmented consumer-goods company in the making. The most important of the three — the one the entire investment thesis would come to rest on — was النور Al Noor, the sheesha line, because sheesha was where the margins lived and where the "export miracle" story would be set. To understand why that mattered, and why it was such fertile ground for fiction, we need to look at the real industry Elitecon claimed to be conquering, and at the genuine titans it claimed to be outrunning.

IV. Core Business: Structure, Economics, & Real Competitors

Walk into a hookah lounge in دبي Dubai on a warm evening and you are looking at the economic engine that Elitecon's whole story was bolted to. The water pipe gurgles, the coals glow, and the apple-and-mint smoke hangs sweet in the air. What you are actually consuming is sheesha molasses — sometimes called shisha or hookah tobacco — a thick, sticky blend of tobacco, glycerin, molasses or honey, and flavoring, packed into the bowl and heated indirectly with charcoal. It is a fundamentally different product from a cigarette, and crucially for our story, a far more profitable one.

This is where Elitecon told investors the magic was. Hookah and sheesha tobacco — the النور Al Noor line — was pitched as the highest-margin slice of the business, carrying gross margins above 40%.6 That is a fat number in tobacco, and the logic was at least superficially plausible: sheesha is a premium, flavored, experiential product sold into affluent leisure settings, not a commodity stick sold by the pack. Better still, the story went, Elitecon was exporting it — to the Gulf, where hookah is woven into the culture, and to European lounges chasing the same vibe. Exports meant hard-currency revenue and, under India's tax code, a category of "zero-rated" supplies that, as we will see, turned out to be the load-bearing wall of the entire fraud. We dwell on sheesha because the bulls dwelt on sheesha: exports of النور Al Noor to دبي Dubai and Europe were the investment thesis.

Now let's introduce the giants this upstart claimed to be disrupting — because the scale gap between Elitecon's story and the real industry is the single most damning piece of context in this whole episode.

ITC Limited is the colossus, and "colossus" undersells it. ITC controls roughly 75% of India's cigarette market, a dominance built over more than a century. Its distribution network reaches over 6 million retail outlets — paan shops, kirana stores, supermarkets, every roadside kiosk from Kashmir to Kanyakumari — and its combined FMCG and tobacco revenues run well past ₹70,000 Crore a year.5 Six million points of sale. Sit with that. Building physical distribution at that density is the work of generations; it is, quite literally, ITC's moat, and we will return to it when we war-game the competitive landscape.

Below ITC sit the regional powers. Godfrey Phillips India (GPIL) dominates the North, with more than 800,000 points of sale and revenues north of ₹4,000 Crore.5 VST Industries holds key pockets of the South, turning over ₹1,500 Crore-plus.5 And in the sheesha world specifically, the undisputed global benchmark is الفاخر Al Fakher — the Emirati-origin brand that is to hookah what Coca-Cola is to cola, alongside established Lebanese and Egyptian exporters who have spent decades building the trade routes, the lounge relationships, and the flavor reputations that Elitecon claimed to be displacing.

Hold those numbers next to Elitecon's. ITC: ₹70,000 Crore, 6 million outlets, 75% share, 100-plus years. Elitecon: a renamed 1987 shell that did nothing until 2019, reporting in a single recent quarter the kind of revenue surge that suggested it was somehow capturing meaningful export share against الفاخر Al Fakher and selling at a velocity that the regional Indian players had needed decades to approach. When a company that materialized three years ago reports growth that dwarfs incumbents who have spent a century building physical distribution, the right response is not excitement. It is suspicion. Extraordinary claims require extraordinary distribution, and distribution is the one thing you cannot fake on a shelf — only on a spreadsheet.

So how did Elitecon claim to have pulled it off? The pitch was a familiar one, and on its surface it was even sensible. Rather than fight ITC head-on for shelf space in the brutal domestic cigarette trade — a war no newcomer can win — Elitecon claimed to bypass the incumbents entirely. It would go direct-to-retailer in modern trade channels, skipping the layers of distributors that eat into margin. It would offer distributors better economics than the giants did, buying loyalty with generosity. And offshore, it would push customizable sheesha into lounges with crowd-pleasing local flavor profiles — Double Apple, Mint, the hits that move product in a دبي Dubai lounge on a Friday night. It is a coherent strategy. Plenty of real challenger brands have used exactly this playbook. The problem, as the tax authorities would eventually establish, was not that the strategy was implausible. It was that, to a substantial degree, the products were not actually moving through these channels at all — the channels existed mostly as line items.[^5] Which brings us to the place where the fiction was actually authored: the financial statements.

V. The Financial Explosion: Masterclass in Fake Billing

If you want to understand how Elitecon hypnotized the market, you have to read its financials the way the bulls read them in 2024 — not yet knowing the ending, just seeing the numbers land one after another, each more intoxicating than the last. So let's do that. Let's read them straight, the way a retail investor refreshing Screener.in would have read them, and then let's take them apart.

The headline that lit the fuse: in a recent fiscal year, quarterly revenues exploded from near-zero to roughly ₹549 Crore.5 From a dead shell to half a thousand crore in quarterly sales — that is not growth, that is a resurrection. And the profitability that came with it was even more seductive. Net profit surged 94% to about ₹69.6 Crore, implying a net margin of roughly 12.7%.5 Stop on that margin. In a hyper-taxed industry — and tobacco in India is among the most heavily taxed product categories on earth, layered with excise, GST, and a compensation cess that can dwarf the base price — a clean 12.7% net margin is not impressive. It is implausible. The real incumbents grind through that tax wall with the help of enormous scale and decades of pricing power. A three-year-old operation clearing 12.7% to the bottom line was reporting economics that the industry's own giants would envy, which should have been the tell. Margins that good, that fast, in a category that punishing, do not signal genius. They signal that something in the income statement is not real.

And the balance sheet was the closer. Elitecon reported itself as virtually debt-free, with strongly positive operating cash flow.5 This is the detail that disarms skeptics, because the classic accounting fraud is supposed to leave fingerprints — you fake profits, but the cash never shows up, and the gap between reported earnings and real cash widens until it screams. Elitecon appeared to have no such gap. It looked like a company that was not just profitable on paper but generating cash and carrying no debt — the holy trinity of a quality compounder. How do you fake cash flow?

Here is the answer, and it is the most elegant and most damning trick in the whole structure: the working-capital "hack."

Elitecon reported a negative working-capital cycle — meaning, in plain terms, that it collected money from customers before it had to pay its own suppliers. The story it told to explain this was beautifully specific. International clients, it claimed, paid 30–50% advances in foreign currency before goods shipped, because that is how nervous overseas buyers de-risk a new supplier. Meanwhile, domestic tobacco farmers were kept on 60-day credit — paid two months after delivery, as is common in agricultural supply chains. Put those two together and you get a money machine: cash flows in from customers up front, flows out to suppliers months later, and in between the company is effectively financing its own explosive growth with other people's money. No debt needed. No equity dilution needed. A self-funding, high-velocity cash engine.

It is a genuinely brilliant narrative, and that is exactly why it worked. A negative working-capital cycle is the signature of some of the best businesses in the world — it is how Amazon funded its early growth, how a great retailer turns inventory faster than it pays for it. By dressing the fraud in the clothing of a legitimately admirable financial structure, Elitecon made its fake cash flows look not just plausible but enviable. The "advances from foreign customers" line, in particular, did double duty: it explained the cash, and it reinforced the export story. Of course there was cash on the balance sheet — look, the Gulf buyers were prepaying. Except, as the investigation would reveal, a large share of those foreign buyers and those advances lived in the same circular paper network as the revenue itself.

The final flourish was the no-dividend moat. Elitecon paid out nothing to shareholders, and it framed this not as a red flag but as a virtue. Every rupee of profit, management said, was being plowed back into modular manufacturing facilities in Maharashtra — capacity that would let the business scale almost linearly, adding production lines like Lego bricks without taking on debt or diluting shareholders.6 This is the kind of capital-allocation story that growth investors swoon over: a company reinvesting at high returns, compounding internally, refusing to "leak" cash out as dividends when it can redeploy at 40% margins. The market rewarded the reinvestment narrative the way it always does — with multiple expansion. At the peak, Elitecon traded at a price-to-earnings multiple reported around 300x.[^2]

Three hundred times earnings. For context, the established, genuinely profitable, century-old leaders in this very industry trade at a small fraction of that. A 300x multiple is not a valuation; it is a mood. It only makes sense if you believe the growth is real, the margins are durable, and the runway is enormous — and Elitecon had engineered every one of those beliefs. But a no-dividend policy has a quiet second function that the bulls never examined: a company that never returns cash never has to prove the cash exists in a way a shareholder can touch. A dividend is real. A reinvested rupee, plowed into "modular facilities" you have never visited, is whatever the income statement says it is. The no-dividend moat was not just a growth story. It was a way of keeping the cash permanently theoretical.

So you had fake revenue, fake margins, fake-but-beautiful cash flow, and a valuation multiple to match. But a great fraud needs more than great fiction in the filings. It needs the stock itself to behave in a way that makes the fiction feel true. And the way Elitecon's stock behaved was its own separate work of art.

VI. The Stock Market Mania & Microstructure Tricks

There is a reason the chart went vertical rather than merely up, and it has almost nothing to do with how many people wanted to buy Elitecon and almost everything to do with how the Indian micro-cap market is plumbed. To understand the mania, you have to understand the pipes — and the pipes were rigged in the operators' favor from the start.

Begin with the float, which is the single most important variable in any small-cap pump. The "float" is simply the supply of shares actually available to trade in the open market — the shares not locked away in the hands of insiders. With Vipin Sharma and the DUC Education Foundation together holding close to 60% of the company, and friendly, long-term-aligned entities holding perhaps another 20%, the genuinely tradable public float was under 20% of the shares outstanding.2 In a company this size, that is a vanishingly thin sliver of stock. And the most basic law in markets is the law of supply and demand: when you choke supply down to almost nothing, even a trickle of demand can move the price violently. The operators had not just written a great story — they had pre-arranged a market where almost no shares were available to anyone who got excited about it.

Now layer on the upper-circuit mechanism, which is where the Indian micro-cap structure becomes almost custom-built for this exact abuse. To curb volatility, Indian exchanges impose daily price bands — a stock can only move so far up or down in a single session before trading in it halts. For many small-caps, that band is 20%. Elitecon began hitting its upper circuit — the 20% ceiling — day after day after day. Here is why that is so insidious. When a stock is "locked" at upper circuit, it means there are buyers stacked up wanting in at the ceiling price, but no sellers willing to part with shares. The order book shows a wall of buy orders and an empty offer side. The price ratchets up the maximum 20% the next day, and the next, and the next — and critically, it does this on almost no actual volume. You do not need real money flowing in to push a circuit-locked stock higher; you just need an absence of sellers, which the tiny float and the aligned holders guaranteed. The vertical chart was not evidence of a flood of buyers overwhelming the market. It was evidence of a market with the sell side deliberately emptied out. Scarcity, manufactured.

Then there is the dog that did not bark: the absence of futures and options. Elitecon was never admitted to the derivatives segment — there were no F&O contracts on the stock. In a normal, liquid large-cap, a parabolic move like this would summon the short-sellers: traders who borrow shares, sell them, and profit when the inflated price collapses back to reality. Short-sellers are the immune system of a market; they are the people whose entire job is to lean against bubbles and bet on frauds unwinding. But you cannot easily short a stock that has no derivatives, almost no borrowable float, and a price locked at upper circuit where you cannot even get a sell order filled. The structure had, in effect, disabled the market's own immune system. The skeptics who might have called the top had no tool with which to act on their skepticism. The parabola ran unopposed.

And finally, the human accelerant: the finfluencer echo chamber. While the microstructure did the mechanical work of levitating the price, an informal media machine did the work of recruiting marks. Telegram tip groups, YouTube stock-tipsters, and breathless forum threads seized on Elitecon and amplified it relentlessly. The framing was always the same gravitational pull toward a familiar reference point: this was the "next ITC," a "global tobacco disruptor," the multibagger you were a fool to miss. The chart itself became the argument — look how much it's up, it must be real — in a perfect circular reinforcement: the price rose because the float was choked, the rising price drew the influencers, the influencers drew retail money, and retail money pressed harder against an order book with nothing on the sell side. By the peak, retail investors held over 35% of the free float, which sounds like broad participation but actually means something darker.[^2] It means the public had been steadily handed the shares the insiders wanted to offload — the float was migrating from the people who knew into the hands of the people who believed. That is the entire mechanical purpose of a pump: to convert a vertical chart into an exit. The insiders did not want to own Elitecon at ₹260. They wanted you to.

The trouble with a machine that manufactures fake revenue and fake exports is that it leaves a trail in one place the operators could not control: the tax system. And in late 2024, the tax system started asking questions.

VII. The Great Unraveling: The ₹1,825 Crore GST Fraud

Frauds rarely die where they were born. Elitecon's death certificate was not written by an outraged shareholder or a short-selling research firm — India's market structure had seen to it that those forces were largely neutralized. It was written by the plumbing of the tax code, by officers in the Directorate General of GST Intelligence (DGGI) who were not looking at a stock chart at all. They were looking at refund claims.

The first tremor came in late 2024, when the DGGI issued GST demand notices against Elitecon. The figures were staggering relative to the company's reported scale: demands of ₹387.43 Crore and ₹22.23 Crore, together representing close to 90% of the company's reported revenue, with the department alleging large-scale irregularities in input tax credit (ITC).[^5] To grasp why that ratio is so devastating, you have to understand what input tax credit is, because ITC is the beating heart of this entire fraud — and of a great many Indian tax frauds.

Here is ITC in plain language. Under a value-added tax system like GST, a business pays tax when it buys its inputs and collects tax when it sells its outputs. To avoid taxing the same value over and over at every link in the chain, the system lets a business claim credit for the tax it already paid on its inputs, and only remit the difference. So if you paid ₹100 of GST on raw tobacco and collected ₹150 of GST on the cigarettes you sold, you only hand the government ₹50, because you get credit for the ₹100 you already paid. ITC is the mechanism that makes a value-added tax actually tax only the value added at each step. It is essential, and it is sound — as long as the underlying transactions are real.

Now add the second ingredient: "zero-rated" supplies. Exports, under GST, are zero-rated. The logic is that a country should not export its own taxes — you want your goods to be competitive abroad, so you don't load them with domestic tax. So when you export, you charge no GST on the sale, but you still get to claim the input tax credit on everything you bought to make the exported goods. And because you collected no output tax to net it against, the government refunds that credit to you in cash.

Put those two mechanics together and you can see the trap door the operators walked through. If you can manufacture the appearance of exports — generate invoices showing that you bought heavily taxed inputs (tobacco is taxed at punishing rates) and then "exported" the finished product — you can claim a fat cash refund from the government for input tax credits on goods that, in reality, never moved. You are not selling tobacco abroad. You are selling the paperwork of selling tobacco abroad, and the buyer of that paperwork is the Indian treasury, paying in real rupees.

That is precisely what the investigation alleged Elitecon's network was doing, and the full scale, revealed in April 2026, was breathtaking. The DGGI's Ahmedabad Zonal Unit announced it had uncovered what it described as India's largest tobacco export fraud, totaling ₹1,825 Crore.3[^5] And the unraveling had a face and a name. The primary alleged mastermind, Kapil Chugh, was arrested at Delhi's IGI Airport in April 2026, intercepted as he returned from دبي Dubai.3 There is something almost too on-the-nose about it — the man at the center of a fake-export empire built on imaginary Gulf shipments, taken into custody at the arrivals gate, walking off a flight from the very city the whole fiction had been pointed at.

The modus operandi, as laid out by investigators, was a textbook of circular fraud executed at industrial scale. Chugh and Vipin Sharma allegedly operated a sprawling network of dummy firms — shell companies that existed only as names on invoices, often registered using borrowed or stolen KYC documents, the identity papers of real people who frequently had no idea their credentials were being used to anchor a paper company.[^5] Through this web of phantom entities, the network generated fake invoices that passed bogus input tax credits up and down the chain on high-value tobacco products. The same goods — or rather, the idea of the same goods — could be billed in a circle, A to B to C and back toward A, each hop generating fresh paper, fresh ITC, and the documentary appearance of a thriving, high-velocity trade. And at the end of the loop, the network claimed enormous cash refunds on "zero-rated" supplies — the export refunds — without any actual exports taking place.[^5]

Step back and the full picture resolves into something genuinely chilling in its coherence. Every layer we have examined was a facet of the same machine. The ₹549 Crore of quarterly revenue was, to a substantial degree, this circular billing — the loops were the sales.5 The beautiful negative working-capital cycle and the "foreign advances" were the export refunds and inter-firm transfers dressed as customer prepayments. The 40%-plus sheesha margins and the 12.7% net margin were arithmetic performed on imaginary trade. And the entire purpose of generating these gorgeous, fictitious financials was not, in the end, to build a tobacco company. It was to justify a stock price — to give the finfluencers their "next ITC," to keep the upper circuits locked, and to let the insiders dump pumped shares onto the retail investors who had been so carefully recruited into the float.2[^8] The operating business and the market scheme were not two frauds. They were one fraud, viewed from two angles.

The regulators arrived at the same conclusion from the securities side. On March 30, 2026, SEBI issued an ex-parte interim order — "ex-parte" meaning the regulator acted immediately, without first hearing the accused, because it judged the harm ongoing and urgent. SEBI barred Elitecon, Vipin Sharma, and five officials from the securities market, and ordered the impounding of ₹51.2 Crore in unlawful gains.2[^8] The language of the order cut to the bone: the regulator found that Elitecon's stock price had been artificially pumped through "delayed, manufactured, and highly misleading disclosures" — that the corporate communications feeding the market's frenzy were themselves part of the apparatus.2 The exports were fictitious. The growth was fictitious. The "operational miracle" was a billing scheme with a stock ticker attached.

And the protagonist? When the warrants came, Vipin Sharma was gone. The Bombay High Court issued a lookout circular and a non-bailable warrant against him after he fled the jurisdiction and refused to cooperate with the proceedings.34 The managing director who had been marketed to retail India as a tobacco veteran with deep domain expertise exited the same way the cash had — across a border, into the air, untraceable. What he left behind was a listed shell once again, except this time it was not empty and quiet. It was radioactive, frozen by the regulator, and full of shareholders holding a stock that had been revealed as a stage set. Someone had to walk in and turn the lights back on. In late April 2026, someone did.

VIII. Current Caretaker Management & The Clean-Up Battle

The most thankless job in Indian capital markets in the spring of 2026 was, arguably, "incoming director of Elitecon International." Imagine the role: you are handed the wheel of a company whose former leadership is under non-bailable warrant, whose financials are presumed fictitious until a forensic auditor proves otherwise, whose stock is frozen and whose name is now shorthand for fraud, and whose tens of thousands of retail shareholders are looking to you to tell them whether anything they own is real. That is the company that changed hands in the final days of April 2026.

The old guard left all at once, which is its own kind of tell. On April 29, 2026, Vipin Sharma resigned as Managing Director.4 He did not go alone. In what amounted to a mass board exodus, the CFO Sachin Sabale, the Company Secretary Rajlaxmi Saini, and multiple independent directors resigned in the same window.4 When the entire senior apparatus of a company evacuates simultaneously, it is rarely a coincidence of personal timing; it is people stepping away from a structure they expect to be examined, and examined hard. The independent directors, in particular — the people whose statutory job is to be the conscience of the board and the guardians of the minority shareholder — left rather than stay to answer for what had happened on their watch. Their departure was, in its way, a verdict.

Into the vacuum stepped a deliberately different kind of leadership, assembled to send a single message to a market that had lost all trust: the adults are here now. Kumar Anubhav Upadhyay was appointed Executive Additional Director to take operational control — to run the day-to-day of whatever real business remained.4 But the appointments that mattered most for credibility were the non-executive ones, because they spoke to oversight rather than operations.

The marquee name was Dr. Venkata Ramesh Penumaka — widely known as Dr. P.V. Ramesh — a highly decorated retired IAS officer, brought in as a Non-Executive Independent Director.4 For readers outside India, the significance of "retired IAS officer" is hard to overstate. The Indian Administrative Service is the elite, permanent, career civil service that runs the machinery of the Indian state — its officers spend decades inside the apparatus of governance, regulation, and public finance. Parachuting a senior, decorated IAS veteran onto the board of a fraud-tainted company is a very specific signal: it says the new Elitecon intends to speak the language of regulators fluently, to cooperate rather than evade, and to be seen doing so. Alongside him, Edward Michael Bourgoin was appointed as a Non-Executive Independent Director, rounding out an oversight bench designed to project administrative and regulatory seriousness.4 Crucially, all of this unfolds against a hard constraint: the promoter shares are effectively frozen under SEBI's order, so the old controlling bloc can neither trade nor easily reassert itself.2 The caretakers are operating in a company where the people who built the fraud have been ring-fenced out of the share register's active power.

So what does the caretaker board actually do with a company like this? The strategy that has emerged has three legs.

The first and most fundamental is the forensic audit, formally appointed on May 20, 2026.[^9] This is the foundational act, because nothing else can be trusted until it is done. A forensic auditor's job here is brutally specific: to go line by line through the accounting ledger and separate the real from the fake — to identify whatever genuine operational cash, inventory, plant, and customer relationships actually exist, and to strip away the circular invoicing, the phantom receivables, and the imaginary exports. Until that report lands, every number Elitecon ever published is presumed suspect, including the cash. The forensic audit is, in effect, the company trying to find out what it actually is.

The second leg is the forward-looking pivot — an attempt to give the listed vehicle a reason to exist that has nothing to do with its poisoned past. The new board has proposed a ₹700 Crore vertical expansion into non-tobacco FMCG — consumer products like mouth fresheners, matches, and beverages — with a stated ambition of reaching ₹20,000 Crore in legitimate revenue by FY30.4 One has to hold this proposal at arm's length. A ₹700 Crore expansion plan and a ₹20,000 Crore revenue target, announced by a company whose actual cash reserves are precisely the thing under forensic investigation, sits somewhere between genuine turnaround strategy and aspirational placeholder. It is the kind of clean, legitimate, addressable-market story that a caretaker board needs to tell to keep a listing alive and to give shareholders a non-zero reason to stay. Whether the capital to fund it actually exists is, quite literally, the open question the forensic audit will answer.

The third leg is incentive realignment — a quieter but telling move. The plan is to shift Elitecon away from the founder-concentrated, "black-box" control that defined the Sharma era and toward professionalized structures, including ESOP plans designed to retain middle management.4 The logic is sound in principle: the old model concentrated all information and all economic upside in a tiny coordinating clique, which is exactly the condition that lets a pump-and-dump operate. Spreading equity to professional managers and building institutional processes is the textbook antidote — it dilutes the black box. Of course, ESOPs on a stock that may be worth a fraction of its peak, in a company that may be insolvent, are a thin currency. But the direction of travel is the point.

Whether any of this amounts to a genuine rescue or merely a dignified wind-down depends entirely on what is real underneath — which is, finally, the question that lets us step back from the narrative and analyze Elitecon as a business, or rather as the absence of one. To do that properly, we turn to the frameworks.

IX. Playbook: Porter's 5 Forces & Hamilton's 7 Powers

Here is the most useful thing about analyzing a fraud with the standard tools of competitive strategy: a fraud is a business with all the real sources of advantage surgically removed, leaving only the appearance of them. So when you run Elitecon through Porter's Five Forces and Hamilton Helmer's Seven Powers, you are not just diagnosing this one company. You are getting a vivid, X-ray view of what a genuine moat actually is — by looking at a company that had to fake every single one. Let's war-game it.

Porter's Five Forces describes the structural attractiveness of an industry — the forces that determine whether anyone in it can earn durable profits. The Indian tobacco industry, it turns out, is genuinely attractive for incumbents, which is exactly why it was such a tempting costume.

-

Threat of New Entrants — the high/low paradox. On paper, tobacco has towering barriers to entry. Regulation is ferocious, advertising is banned, taxation is punitive, and licensing is restrictive. A legitimate new tobacco company is nearly impossible to build from scratch — which is wonderful news if you are ITC, and a wall if you are an honest newcomer. Elitecon's entire existence was an exploitation of this paradox: rather than scale the wall, it tunneled under it by reverse-merging into a listed shell, acquiring the apparatus of a public tobacco company without ever building the substance. The high barrier did not protect the industry from Elitecon; it became the very thing that made Elitecon's story credible, because investors assumed anyone inside the wall must have legitimately climbed it.

-

Bargaining Power of Suppliers — low, with one exception. Tobacco farmers are numerous, fragmented, and price-takers; they have little leverage over a buyer. But the truly powerful "supplier" in this industry is not the farmer at all — it is the government, supplying the right to operate via excise duties, GST rates, and the compensation cess. The state holds existential power over every tobacco company's economics, and can reshape the entire industry's profitability with a single budget line. Elitecon's fatal irony is that it tried to monetize this relationship — to extract cash from the government via fake export refunds — and in doing so it picked a fight with the one supplier that holds true power. The DGGI was always going to win.

-

Bargaining Power of Buyers — low. Tobacco's products are addictive and brand-loyal; consumer price elasticity is low, which is the foundation of the real incumbents' pricing power. But note the trap Elitecon fell into: low buyer power is only an asset if you have buyers. Elitecon's "buyers," to a large degree, were entries in a circular billing ledger, who have no power because they have no existence.

-

Threat of Substitutes — moderate and rising. The genuine long-term risk to the whole category is the migration toward herbal and synthetic nicotine, vapes, and wellness-oriented alternatives. This is a real force that even ITC must reckon with, and it is the one Porter force that is moving against the incumbents over time.

-

Rivalry Among Existing Competitors — high. This is the force that should have buried Elitecon's pitch on contact. The real industry is a knife-fight among capital-rich titans — and a company like ITC, with six million outlets and a war chest, can engage in predatory pricing to suffocate any genuine upstart long before it reaches scale. Elitecon's claim to be winning meaningful share against this field, this fast, was not a competitive achievement. It was a confession that the share gains were not happening in the real economy at all.

If Porter tells us the industry was attractive and the incumbents formidable, Hamilton Helmer's Seven Powers tells us why Elitecon had no defensible position within it. Helmer's framework asks a sharper question than Porter's: not "is this industry good?" but "does this specific company have a power — a persistent differential that lets it earn outsized returns and prevents competitors from arbitraging them away?" Run Elitecon through all seven and the result is almost eerie: it is a perfect zero. Every power is absent, and in the few places Elitecon simulated one, the simulation was the fraud itself.

-

Scale Economies — absent. Real scale power belongs to ITC, whose six-million-outlet distribution network spreads fixed costs across a volume no newcomer can touch. Elitecon had no real scale. So it simulated scale through fraudulent billing — the circular invoices made the company look like it was operating at volume, which is the counterfeit version of the one power that most defines its giant competitor.

-

Network Effects — absent and inapplicable. Tobacco consumption simply does not have network dynamics; your cigarette is not more valuable because others smoke the same brand. There was nothing here to fake and nothing real to build.

-

Counter-Positioning — absent. This is the subtle one, and worth a beat. Counter-positioning is when a newcomer adopts a business model that incumbents cannot copy without damaging their existing business — the classic disruptor's weapon. Elitecon gestured at counter-positioning with its "affordable premium" export model, the direct-to-retailer pitch that supposedly let it undercut the giants. But counter-positioning only counts if the alternative model actually works and the incumbent actually can't follow. Elitecon's model "worked" only because the underlying exports were nonexistent. You cannot counter-position with a business that isn't there.

-

Switching Costs — very low. A smoker can change cigarette or sheesha brands between one purchase and the next; nothing locks them in except brand equity. The real incumbents have spent a century building that equity. Elitecon had none, which means even if its products had been real, customers could have abandoned them instantly.

-

Brand / Cornered Resource — absent. النور Al Noor had zero defensive brand power against established Gulf names like الفاخر Al Fakher, which owns the cornered resource of being the trusted sheesha name. Brand is the slow accretion of repeated, satisfied experience; you cannot manufacture decades of it in three years, and Elitecon did not try — it simply asserted a brand into existence on a pitch deck.

-

Process Power — fake. Process power is a proprietary operational capability that competitors cannot replicate even if they know about it — Toyota's production system is the canonical example. Elitecon did have one genuinely distinctive "process," and that is the darkly comic punchline of this whole analysis: its proprietary capability was the industrialized, automated generation of fake invoices through a network of dummy firms. It was a real process. It was just a process for committing fraud, not for making anything.

-

System / Operating-Process Moats — none. Helmer's deepest moats are the compounding, hard-to-see systems that make a company more efficient the longer it operates. Elitecon's "system" had the opposite property: it became more fragile the longer it ran, because every additional cycle of fake billing was additional evidence sitting in a tax database. The moment a genuine regulatory audit occurred, the entire structure collapsed — which is the precise inverse of a system moat. A real moat gets stronger under pressure. Elitecon's got weaker with every passing quarter, until the DGGI applied the pressure that ended it.

The frameworks converge on a single, clarifying verdict: Elitecon possessed not one genuine source of competitive advantage. Everything that looked like a power was either absent or a counterfeit of a power its real competitors actually held. Which leaves the practical question every investor in the listed shell now faces — is there anything of value left to own, or only the wreckage? That is the bull-versus-bear debate, and unusually for this kind of story, it is a live one.

X. Bear vs. Bull Case & Lessons for Investors

Most fraud post-mortems have no bull case left to argue — the company is a smoking crater and the only question is the size of the loss. Elitecon is more interesting, because the caretaker board has, deliberately, manufactured genuine uncertainty about the endgame. The stock having crashed somewhere in the range of 60–80% from its manic peak means the market has already priced in catastrophe — and that, paradoxically, is what makes both cases worth stating plainly.[^2] Let us steel-man each.

The Bull Case — the professional-caretaker bet. The optimistic thesis does not require believing anything Vipin Sharma ever said. It requires believing in the people who replaced him. In this scenario, the retired-IAS-led board does exactly what it was assembled to do: it cooperates fully with the DGGI, uses the forensic audit to cleanly separate the real underlying business from the fraudulent overlay, negotiates and settles the GST liabilities at a survivable number, and emerges with a smaller but legitimate operating core. On top of that cleansed foundation, the ₹700 Crore FMCG expansion gives the listed vehicle a real reason to exist — a genuine, growing consumer-goods business in matches, mouth fresheners, and beverages, sectors where there is no fraud required to make a rupee. If even a fraction of that materializes, today's distressed price could prove to have been a deep-value option on competent professional management cleaning up someone else's mess. There is a real, if narrow, path here: frauds occasionally leave behind salvageable assets, and a credentialed board with regulatory goodwill is exactly the vehicle that can monetize them.

The Bear Case — terminal delisting. The pessimistic thesis is brutally simple and requires only that the investigation's worst implications be true. In this scenario, the forensic audit reveals that essentially 100% of the reported operational growth was fabricated — that there is no meaningful real business, no genuine cash reserves, no plant of value, nothing but the husk of a billing scheme. Then the tax liabilities finish the job: a DGGI penalty of around ₹442.29 Crore — the adjudicated demand the company faces — lands on a company with no real assets to pay it, triggering insolvency, bankruptcy, and eventual delisting from the BSE.[^5] In this version, the caretaker board is not a turnaround team but a hospice — there to manage a dignified death and protect themselves from liability while the listed shell is wound down to zero. The crashed stock price, in this telling, has not overshot. It is on its way to its true value, which is nothing.

The honest answer is that no outsider can yet adjudicate between these two cases, because the facts that decide it have not been published. And that points directly to the discipline this episode demands: rather than guess, track the three pieces of information that will actually resolve the uncertainty. These are the only KPIs that matter for Elitecon right now, and notice that not one of them is a sales figure or a margin — the ordinary metrics of a normal company are meaningless until the question of reality itself is settled:

- The release of the delayed audited financials for FY 2025-26. Their very delay is the loudest signal in the story — a company that cannot close its books is a company that does not yet know what it owns.[^9] When (and whether) these land, and what they say, is the first real data point.

- The publication of the forensic audit report. This is the master KPI. It is the document that will state, in numbers, how much of Elitecon was ever real. Every other question is downstream of this one.[^9]

- The formal adjudication of the ~₹442 Crore DGGI show-cause notice. The final tax liability — settled, reduced, or upheld in full — determines whether a cleansed business could survive its obligations or is mathematically insolvent the moment the gavel falls.[^5]

Watch those three. Ignore the price chart, the forum chatter, and any new "turnaround" narrative until the forensic report tells you what the company actually is. Which brings us to the one decision in this whole saga that the entire retail crowd got exactly backwards — and the lesson hiding inside it.

XI. Epilogue & Final Reflections

Return, one last time, to that block of 87,500 shares — the ones Vipin Sharma bought from the DUC Education Foundation at ₹10.5 per share while the open market priced the same stock north of ₹200. When that transaction surfaced, the retail forums did not recoil. They cheered. And the reason they cheered is the reason this story is worth telling at all.

For decades, the gospel of value investing has held that there is no more bullish signal than a promoter buying his own company's shares. The logic is airtight and usually correct: insiders know more than anyone about the true state of the business, and when they put their own money in, they are betting on themselves. It is the celebrated principle of "skin in the game" — alignment between the people running the company and the people who own it. When retail investors saw the managing director scooping up 7.23% of Elitecon, they read it through this lens. He's buying. He believes. Get in.

But look at what the signal actually was once you knew the price. Sharma was not buying conviction at the market price, risking real capital on the company's future the way the gospel imagines. He was acquiring shares at a 95% discount in a coordinated transfer among Persons Acting in Concert — locking up cheap stock on the inside specifically so it could be sold dear on the outside.25[^8] The "skin in the game" was not alignment with minority shareholders. It was the opposite of alignment: it was the pre-positioning of inventory for a pump-and-dump, dressed in the most trusted bullish signal in all of investing. The promoter was not betting with the retail crowd. He was loading the gun he would point at them. The most dangerous deceptions are not the ones that look like lies. They are the ones that look exactly like the things we have been trained to trust.

And that is the lesson that outlives Elitecon. The financial statements told a beautiful story — explosive revenue, enviable margins, a self-funding working-capital machine, a debt-free balance sheet, a visionary reinvestment runway. Every number reconciled. Every ratio impressed. And every bit of it was, to a substantial degree, paper — circular invoices and phantom exports rendered into the grammar of a great compounder.2[^5] A diligent analyst reading only the filings would have found almost nothing wrong, because the filings were the fraud's finished product, not its evidence.

The thing the filings could not fake was the physical world. The shelf in the modern-trade store. The product in the دبي Dubai lounge. The container actually leaving the actual port. The 6-million-outlet distribution that a real tobacco company takes a century to build and that no spreadsheet can conjure. The oldest technique in fundamental investing — scuttlebutt, Philip Fisher's word for it — is simply this: go look. Talk to the distributors. Walk the channel. Check whether the exports that justify the valuation are physically leaving the country. In an emerging market, where information asymmetry is wider and verification is harder, scuttlebutt is not a quaint supplement to financial analysis. It is the analysis. When a company in a capital-heavy, savagely regulated industry reports hypergrowth that dwarfs the multi-decade giants who built that industry, the correct response is not to admire the income statement. It is to get up, go to the port, and count the containers. Elitecon's investors read the statements. They never went to the port. The containers were never there.

References

-

Elitecon International Ltd — Stock Price & Share Data (Script Code 539533) — BSE India ↩↩↩

-

Interim Order in the matter of Elitecon International Limited — Securities and Exchange Board of India (SEBI), 2026-03-30 ↩↩↩↩↩↩↩↩↩

-

DGGI Arrests Key Mastermind in ₹1,825 Crore Tobacco GST Fraud — Press Information Bureau (PIB), 2026-04 ↩↩↩↩↩

-

Elitecon International MD Vipin Sharma Resigns; Board Appoints Former IAS Officer — Business Standard, 2026-04-29 ↩↩↩↩↩↩↩↩

-

Elitecon International Limited — Corporate Profile & Peer Analysis — Screener.in ↩↩↩↩↩↩↩↩↩↩↩

-

Elitecon International Limited — Annual Reports and Statutory Filings ↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube