3B BlackBio Dx: The Bhopal-to-Brussels Biotech Pivot

I. Introduction & The "Incredible Pivot"

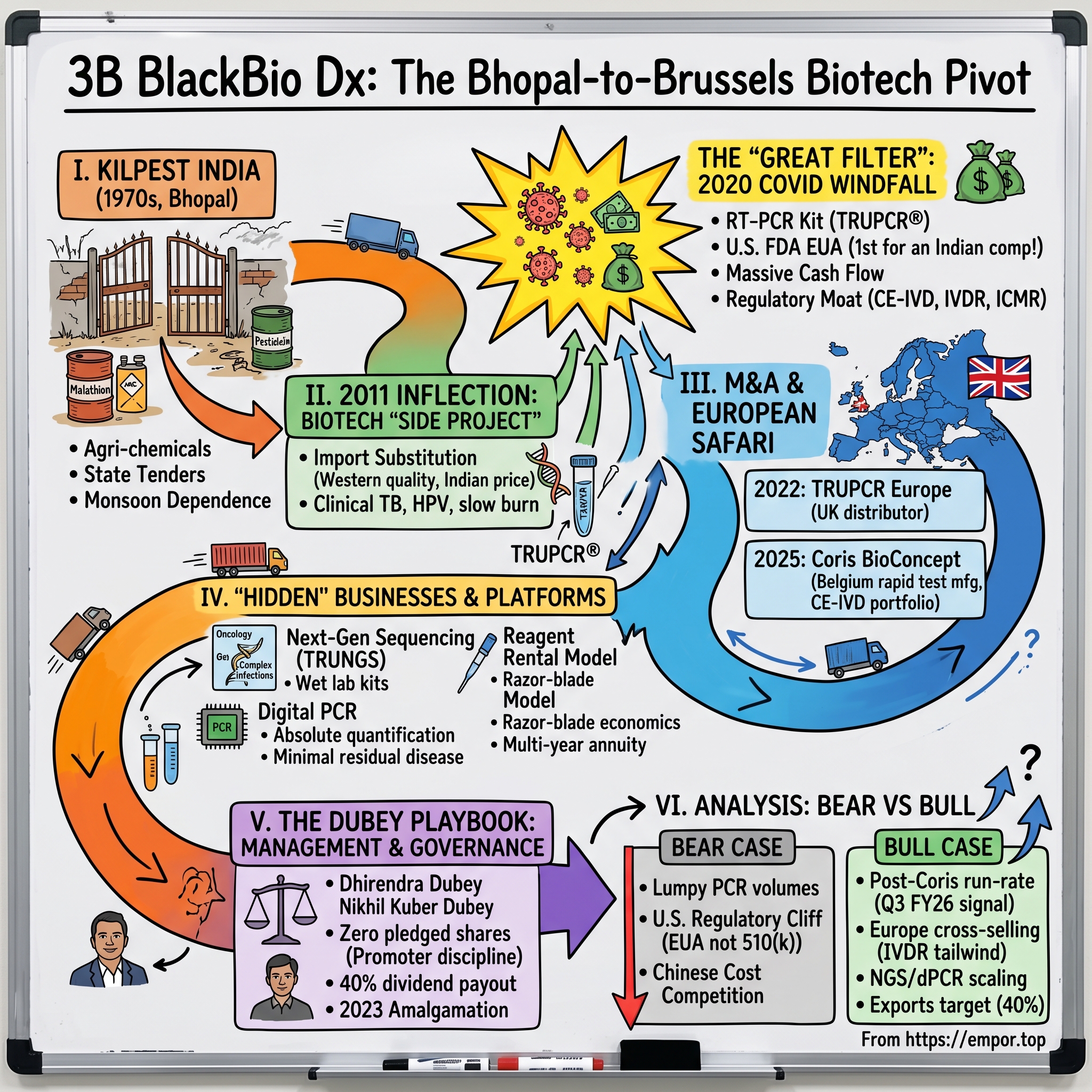

Picture the scene. It is the late 1970s in भोपाल Bhopal — a sleepy, lake-fringed administrative capital in the geographic heart of India, decades before the city would become globally infamous for the 1984 Union Carbide disaster. Down a dusty service lane in the Govindpura Industrial Area, behind a metal gate that has long since rusted into the colour of the surrounding earth, a small chemicals plant is pumping out drums of malathion and chlorpyrifos. The signage on the gate is in painted block lettering: किलपेस्ट इंडिया Kilpest India Limited. Inside, the founder, R.K. Dubey, is doing what every agri-input entrepreneur in Madhya Pradesh did in that era — fighting for tenders from state cooperatives, hedging against an erratic monsoon, and praying that the Centre does not change its fertilizer subsidy policy again.

Now fast-forward almost half a century. It is a wet Brussels morning in August 2025. In a glass-fronted office park in Gembloux, on the edge of the Walloon countryside, a small team of Belgian molecular biologists is signing share-transfer paperwork. The buyer on the other side of the table is a delegation from that very same Bhopal company.1 The product is a portfolio of CE-IVD rapid lateral-flow kits aimed at respiratory, gastro-enteric and antibiotic-resistance markers. The cheque is denominated in pounds sterling. And the corporate name on the buyer's signature block is no longer Kilpest India — it is 3B BlackBio Dx Limited, ३बी ब्लैकबायो डीएक्स लिमिटेड, the same company, but reborn.2

This is the question we want to sit with for the next two hours: how does a 50-year-old pesticide formulator from the middle of India, with no obvious technological pedigree and no Silicon Valley venture money in the cap table, become the buyer of a Belgian rapid-test specialist in 2025? How does the small-cap arithmetic actually work — a company carrying a market capitalisation of roughly ₹1,400 crore on the Bombay Stock Exchange, generating around 45% EBITDA margins, paying a 40% dividend, and yet still operating out of the same Bhopal address?3

The answer is one of the more remarkable corporate metamorphoses on the BSE. It is a story about a windfall — a once-in-a-century pandemic that dropped a forklift-load of cash on the company's doorstep. It is also, more interestingly, a story about what management did next. Plenty of Indian diagnostic and pharma names rode the COVID wave and then crashed back to earth as test volumes evaporated. A small subset did something different. They took the cash, looked at the global molecular diagnostics map, and decided to play offence — quietly, in pound-sterling-denominated deals, on the other side of the world.

The roadmap for today's episode follows the arc of that decision. We will start in 1972 with crop protection chemicals, walk through the 2011 founding of a biotech "side project," sit inside the 2020 inflection point when the U.S. Food and Drug Administration awarded the first-ever Emergency Use Authorisation to an Indian-made COVID-19 RT-PCR kit, and then trace the European expansion through the 2022 acquisition of a Manchester distributor and the 2025 buyout of the Belgian Coris BioConcept business. Along the way we will dig into hidden businesses (Next-Gen Sequencing, digital PCR), unpack the "reagent rental" razor-blade economics, examine the Dubey family's governance posture, and stress-test the bull and bear cases.

Settle in. The Bhopal-to-Brussels pivot is not a metaphor — it is a literal corporate-development thesis.

II. Legacy Origins: The Kilpest Years

The story of Kilpest India does not start with a venture pitch deck. It starts with a problem of bugs.

In 1972, Madhya Pradesh was an agricultural state still in the middle of India's Green Revolution. Hybrid wheat and rice were ramping, fertilizer consumption was exploding, and with the new yields came the new pests. The state's farmers — soybean growers in Sehore, paddy farmers in Balaghat, wheat farmers around Gwalior — needed crop-protection chemistry, and they needed it formulated locally so it did not have to ride a thousand kilometres up the Bombay–Agra trunk road. Into this vacuum walked R.K. Dubey, who founded Kilpest as the only pesticide-formulating company in the entire region of Madhya Pradesh at the time.4 The plant was set up at Govindpura, the state's flagship industrial estate, and for the next three decades the company's bread and butter consisted of insecticides, fungicides, herbicides, and the slow accretion of a public health business selling to mosquito- and vector-control programmes.

If you have ever studied Indian SMEs of the License Raj generation, the playbook will be familiar. You apply for capacity. You wait for the licence. You source technicals from a Gujarat or Maharashtra supplier, you formulate locally, you sell into a captive geography that the freight cost makes hard to attack. Margins are thin because the molecules are commoditised. Working capital is brutal because government cooperatives pay late. And the entire business is geared to a single binary variable that no spreadsheet can model: whether the monsoon hits the long-period average that year, or doesn't.

For thirty years that was Kilpest. A solid, profitable, family-owned crop-protection player, with no obvious reason to be anything else. But by the early 2000s the next-generation Dubey — Dhirendra Dubey, धीरेंद्र दुबे — was running the show, and the constraints of the legacy business were getting harder to ignore.5 The molecules Kilpest formulated were going off-patent generics, with prices crashing as more North Indian formulators entered. Public-health budgets for mosquito-control sprays were lumpy and tender-driven, with bid-rigging an open secret in some states. And the addressable market for agrochemicals in central India was, in the most polite phrasing, asymptotic: you can only sell so many bags of cypermethrin into a soybean belt that has not really grown its acreage in a decade.

There is a question that haunts every second-generation promoter of a profitable but stagnant SME in India: do you milk the legacy business and pay yourself a comfortable dividend until the cash flow runs out, or do you reinvest into something risky and probably fail? Most pick the dividend. The Dubeys — and this is the part that quietly matters — picked the risky reinvestment, but with a peculiar Indian-promoter twist: they did not bet the farm. They kept Kilpest's legacy crop-protection cash flow churning, and they incubated the second act inside a separate subsidiary so that if it failed, the parent would survive.

That is the strategic chess piece that gets repositioned in 2011, and it is what makes the rest of this story possible.

For long-term investors, the takeaway from the Kilpest years is not nostalgic. It is structural. The agrochemical business gave the family two things that no biotech start-up in India had: a working manufacturing culture and patient capital that was not on the clock for an exit. When the time came to bet on PCR, that combination — Govindpura discipline plus no investor pressure for a quick flip — turned out to be unusually well-matched to a regulated, capital-cycle business like molecular diagnostics.

III. The 2011 Inflection Point: The Biotech "Side Project"

In 2011, the average Indian diagnostic lab that needed a real-time PCR kit had essentially three vendors to choose from, and all three were sitting in either Basel, Foster City, or Hilden. Roche dominated infectious-disease PCR globally. Applied Biosystems — by then part of Thermo Fisher — owned the instrumentation. Qiagen owned the sample prep. The kits arrived in cold chain from Europe at prices that, when converted to rupees and grossed up for customs and a distributor margin, made high-end molecular testing a service that only the largest tertiary hospitals and elite metro labs in India could routinely afford.

Sitting in Bhopal, the Dubeys looked at this market and saw something specific. The molecular biology of a PCR kit — primers, probes, enzymes, buffers, controls — is not, by the standards of modern pharma, on the bleeding edge. The chemistries were well published, the instruments were standardising, and the bottleneck was not science but trust: trust that a kit's sensitivity and specificity would clear regulatory benchmarks, trust that the lot-to-lot variability would not embarrass a hospital lab, trust that the manufacturer would still be in business in five years to honour kit revisions. If you could build that trust, in India, at Indian cost, the spread between local manufacturing economics and import-parity pricing was enormous — and structurally widening as PCR moved from a research tool to a routine clinical test.

That thesis became 3B BlackBio Biotech India Limited, incubated as a subsidiary of Kilpest in 2011.6 The branded product line — TRUPCR — was positioned not as a discount alternative but as a "Western-quality, India-priced" play, which is a meaningfully different commercial pitch. The first kits targeted high-volume clinical applications: tuberculosis (where India carries roughly a quarter of the global disease burden and where the public-health imperative was crystal-clear), HPV (where cervical cancer screening was beginning to scale through state programmes), and a basket of sexually transmitted and bloodstream infections that the larger private lab chains were starting to roll out.

The early years were, in a word, slow. Validation by the Indian Council of Medical Research is not a process that can be rushed; the ICMR's enrolment pipelines for new diagnostic kits typically run six to eighteen months, longer if the kit targets a notifiable disease. Lab adoption is slower still: a microbiology head at a tertiary hospital who has been running Roche kits for five years has near-zero professional incentive to switch to an unproven domestic vendor, regardless of the price differential, because the downside of a false negative on a hospital infection is career-ending in a way that the upside of saving the lab a few rupees per test is not. So the first half of the 2010s was a grind. Build the kit. Validate the kit. Get one academic medical centre to publish a head-to-head comparison. Get a second site. Apply for ICMR's NIB approval. Tender. Lose. Tender again. Place an instrument in a regional lab. Wait.

The financials of the parent company through that period reflect the grind. Revenue growth was modest, biotech was a fraction of total sales, and the agrochemical business continued to subsidise the R&D and validation costs that no Indian bank was going to underwrite as a clean credit. From the outside, 3B BlackBio looked like one more well-intentioned import-substitution play that would forever remain a sub-scale subsidiary on the consolidated statements.

This is the part of the story that the bull narrative typically glosses over, but it matters: by 2019, after eight years of grinding, 3B BlackBio was a real but small molecular diagnostics business. It had built a kit portfolio, an ICMR validation track record, a customer base of mid-tier private labs, and — crucially — a manufacturing process and quality system that was already running under ISO 13485 discipline. That last detail is what made everything that happened next possible. When a wholly unexpected demand shock hit in early 2020, 3B BlackBio was not a biotech start-up scrambling to design a kit from scratch. It was a working factory that could re-tool a new assay into validated production in weeks rather than quarters.

That is the difference between participating in a windfall and being annihilated by one.

IV. The "Great Filter": The 2020 COVID-19 Windfall

The first reports out of 武汉 Wuhan began circulating in late December 2019. By the middle of January 2020 the virus's genome was on GenBank, the World Health Organization had a draft case definition, and laboratories around the world were racing to design RT-PCR primers against the SARS-CoV-2 N, E, and RdRp genes. Almost every molecular diagnostics company on the planet — from Roche in Basel to a hundred small ISO-certified shops in tier-2 cities across Asia — was sprinting to put a kit on the market.

Inside the Govindpura facility, the team had two advantages most competitors didn't have. The first was that they had spent the prior eight years building exactly this capability: a multi-gene RT-PCR assay running on standard real-time thermal cyclers, with established ICMR relationships and a quality system already audited to international standards. The second was scale-up speed — when your factory has been making TB and HPV PCR kits for years, retargeting the line to a new respiratory virus is a question of months, not a question of years.

By May and June 2020, the regulatory dominoes fell in sequence. ICMR approval came first. Then, on 19 June 2020, the U.S. FDA granted Emergency Use Authorisation to the TRUPCR® SARS-CoV-2 RT qPCR Kit – 2 Tube Assay — making 3B BlackBio the first Indian molecular diagnostics company to receive a U.S. FDA EUA for a COVID-19 RT-PCR test.7 On 23 December 2020, the FDA amended the EUA to include OraSure Technologies' OMNIgene·ORAL collection device, which broadened the sample-type compatibility of the kit and opened up new collection workflows in U.S. labs.8

To understand why that single regulatory line item mattered so much, you have to think about how the global diagnostic procurement system actually works during a pandemic. In a normal year, an Indian PCR kit can sell on price and quality into the Indian market and a handful of cost-conscious export geographies in Africa, Southeast Asia, and the Middle East. In a pandemic year, the demand curve looks completely different: every health ministry on earth is buying tests at any price, but with one binding constraint — a recognised regulatory stamp from a tier-1 jurisdiction. A U.S. FDA EUA is the gold standard. It functions as a passport: once you have it, the same kit can be sold into developed-market labs at developed-market prices, and into emerging-market tenders with a credibility premium that an ICMR-only competitor cannot match.

The financial consequences for 3B BlackBio were instantaneous. The diagnostics segment — which had been a sub-scale, ICMR-grinding business through the 2010s — went from a fraction of the consolidated top line to the overwhelming majority of it. Margins on COVID PCR kits, especially in the first nine months when global capacity was bottlenecked, were extraordinary by historical biotech standards. Cash conversion was fast because diagnostics buyers in a pandemic do not negotiate payment terms the way agri-cooperatives do. By the time FY21 had closed, the consolidated balance sheet looked like a different company.

Here is where the story diverges from every other Indian "COVID wonder." Plenty of small caps caught the wave — domestic kit manufacturers, PPE makers, hand-sanitiser converters — and most of them, when the wave receded, did one of three things with the cash. They diworsified into unrelated verticals (a hand sanitiser maker buying a hotel chain remains a permanent cautionary tale). They paid out the cash as one-time special dividends and reverted to the prior business. Or they sat on the cash, watching it earn 6% in fixed deposits while the operating business shrank back to its pre-pandemic baseline.

3B BlackBio did none of those things. Management did something that, with the benefit of hindsight, looks unusually disciplined for an Indian small cap: they took the windfall cash, did not spread it across vanity projects, and instead used it to fund three structural moves. First, a re-architecture of the parent — folding the operating subsidiary back into the listed entity in 2023, so that the molecular diagnostics business was no longer hidden inside a Kilpest holdco wrapper.9 Second, an aggressive R&D pipeline build-out across higher-margin adjacencies (next-generation sequencing assays, digital PCR, rapid antigen tests, oncology panels). Third, the European M&A strategy, which is what makes the post-COVID chapter genuinely interesting.

That third move is where the next section lives.

V. M&A and Capital Deployment: The European Safari

The reasoning behind the European push is worth slowing down on, because it is the kind of strategic call that separates a company that survives a windfall from a company that compounds one.

Sitting in 2021, the 3B BlackBio leadership had a problem most Indian small caps would kill for: too much cash and a domestic market that was already pivoting back to pre-pandemic test volumes. They could see the runway for COVID kits collapsing — the global vaccination programmes were ramping, the wholesale demand was about to crater, and the kit price per test was going to compress as Chinese low-cost manufacturers re-flooded the market. They could also see, from their TRUPCR sales abroad, that Europe was a structurally different opportunity. The continent had just adopted the EU's In Vitro Diagnostic Regulation (IVDR), a tightening of standards that was going to wash out small, non-compliant manufacturers and consolidate buying around vendors with serious regulatory infrastructure. The labs were sticky, the per-test pricing was healthier, and the existing player set was not, generally, hyper-aggressive on cost.

So the M&A strategy began with a deliberately small first move. In March 2022 the company acquired a 70% equity stake in HS Biolabs Ltd, a Manchester-based distributor that had previously been TRUPCR's exclusive European partner since October 2020. The entity was promptly rebranded as TRUPCR Europe Ltd.10 To outside observers this looked like a routine downstream-integration move — a manufacturer buying its distributor. The deeper logic was different. By owning the channel, 3B BlackBio could now sit in front of European labs as a manufacturer-of-record, not as a brand riding on someone else's customer relationships. That changes the conversation when you walk into a procurement meeting in Manchester or Munich. You are no longer a vendor's vendor; you are the principal.

The HS Biolabs move was scaffolding. The real strategic chess piece came three years later, on 29 August 2025, when 3B BlackBio Dx — through its UK subsidiary — completed the acquisition of Coris BioConcept SRL from the AIM-listed Avacta Group. The headline financial terms were an upfront cash consideration of £2.15 million, plus an earn-out of up to £0.615 million tied to future business performance, for a maximum total of approximately £2.765 million.1112

Read that sentence twice. A Bhopal-headquartered, ₹1,400-crore-market-cap small cap bought a 30-year-old Belgian molecular diagnostics manufacturer — one with a CE-IVD-marked lateral-flow portfolio across respiratory, gastro-enteric, blood-borne, and antibiotic-resistance markers — for under three million pounds, cash, no financing required.1

The valuation is where this transaction becomes a clinic in counter-cyclical buying. Coris had been bought by Avacta from BBI Group back in 2021 for a meaningfully higher number, and the rapid-test segment of the diagnostics industry had been mauled in the post-COVID hangover as commodity antigen tests collapsed in price and volume. Avacta had taken multiple impairments on the asset and was openly pivoting to a "pure-play therapeutics" identity, which made Coris non-core to its strategy and a forced seller. 3B BlackBio walked into that situation with cash, a clean balance sheet, and zero pressure to overpay.

Benchmark the deal: the implied price-to-sales multiple on the upfront consideration sat at roughly the same order as one times trailing revenue, which is the kind of multiple you simply do not see in global diagnostics M&A. Strategic acquisitions in the molecular diagnostics space have historically transacted in the three-to-six-times sales range, sometimes meaningfully higher for proprietary platform technologies. The Roche-Foundation Medicine, Thermo Fisher-Qiagen-attempt, Hologic-Mobidiag style deals were all priced as platform plays, not as distressed carve-outs.

What did 3B BlackBio do with the asset post-close? Take a hard look at the Q3 FY26 numbers (the quarter ending December 2025), which give us the first proper post-acquisition window. In Q3 FY26, the consolidated revenue from operations was ₹50.34 crore — up 98.30% year-on-year — and consolidated net profit was ₹22.44 crore, up 66.30% year-on-year.13 The acquired Coris business contributed roughly ₹24.01 crore of revenue and ₹7.00 crore of profit for that single quarter.14 For a nine-month FY26 view, the consolidated top line was ₹106.48 crore with a net profit of ₹50.13 crore, of which Coris's contribution (since closing) was about ₹27.66 crore in sales, with a positive EBITDA of roughly ₹7.12 crore.14

The signal in those numbers is what matters. Avacta had been running Coris as a structurally loss-making, non-core unit. 3B BlackBio put it on the consolidated balance sheet and within a single quarter the unit was contributing positive operating profit at the parent level. That is not magic; it is the predictable result of bolting a sub-scale European manufacturer onto a manufacturer that already has IVDR-aware distribution rails, a complementary PCR portfolio to cross-sell against, and the kind of low-cost back-end procurement that comes with an Indian parent. The piece they bought was a portfolio of CE-IVD assays and a European manufacturing footprint, both of which are far more valuable in 3B BlackBio's hands than in Avacta's.

If you are wondering what the bridging sentence to the next section is, it is this: most of the operating leverage you are looking at on the consolidated P&L does not come from the legacy crop-protection business. It comes from a stack of hidden, high-margin businesses inside the diagnostics segment that the company has been quietly building. We need to talk about those.

VI. Hidden Businesses & The Segment Deep Dive

If you read the 3B BlackBio Dx annual report cover-to-cover, you will encounter a corporate description that sounds modest enough — molecular diagnostic kits, PCR reagents, agrochemical products — and you might walk away thinking this is essentially a one-trick PCR shop with a residual pesticide business attached. That framing badly understates what is actually inside the segment mix.

Let us start with the broad split. By the time the company had completed the Coris acquisition and run a full quarter on the new structure, the consolidated revenue mix had tilted decisively toward the diagnostics franchise — comfortably over 85% of total revenue — with the legacy agrochemical operation reduced to a stable, low-growth cash cow contributing the residual.14 The agrochemical business has not been killed off; it still generates predictable, working-capital-light cash that funds dividends and corporate overhead. But it is no longer a strategic priority and it is not where the marginal capital is going.

Inside the 85% diagnostics bucket, the interesting story is the platform diversification. The first hidden business is Next-Generation Sequencing, marketed under the TRUNGS brand. To translate for the layperson: a PCR test answers a binary question — "is pathogen X present in this sample, yes or no?" An NGS panel answers a categorically different question — "what is the full set of mutations or pathogens present in this sample?" If PCR is a metal detector, NGS is the X-ray. The clinical applications are largely in oncology (tumour profiling for targeted therapy decisions) and in complex infections (where the differential diagnosis includes a dozen possible organisms and a PCR-by-PCR fishing expedition is too slow). Each NGS assay is materially more expensive per run than a PCR kit, the reagent consumption is heavier, and the gross margin profile is structurally higher. The Indian private-lab oncology market — Apollo, Tata 1mg, Metropolis, SRL, the Apollo-owned Apollo Diagnostics, the newer Tata-Trust-backed labs — has been ramping NGS demand for several years. 3B BlackBio's positioning here is not to compete with Illumina at the instrument layer, where the U.S. incumbent has a near-monopoly. It is to compete at the wet-lab kit and assay layer, where you can sell into the existing installed base of Illumina and Thermo sequencers as the validated reagent supplier.

The second hidden business is digital PCR. Without going into the chemistry: standard real-time PCR gives you a relative quantification of nucleic acid in a sample. Digital PCR partitions the sample into thousands of micro-reactions and gives you an absolute quantification — molecules per microlitre — at extraordinary sensitivity. Why this matters clinically: in oncology, you can detect minimal residual disease (the few thousand cancer cells circulating in a patient's blood after a "successful" surgery) at dilutions that conventional PCR will miss entirely. In transplant medicine, you can quantify donor-derived cell-free DNA at levels that predict rejection before symptoms appear. The MNCs — Bio-Rad, Thermo, Qiagen — have priced this segment as a premium, low-volume, specialist tool. 3B BlackBio's play is to bring digital-PCR-compatible chemistries to Indian and emerging-market labs at price points that make the diagnostic affordable enough to be ordered routinely, not exceptionally.

The third hidden lever, and arguably the most strategically important, is the commercial model. 3B BlackBio runs a "reagent rental" go-to-market in a significant share of its lab placements. The structure is straightforward: the lab does not pay capex for the thermal cycler or the sample-prep instrument; the manufacturer places the box for free (or for a nominal fee), in exchange for a multi-year commitment to consume reagents and kits from that manufacturer at agreed prices. To the lab, the proposition is unbeatable — no capital outlay, predictable per-test cost, guaranteed instrument service. To the manufacturer, it is a razor-and-blades business in the literal Gillette sense. Each installed box is a five-to-seven-year annuity. The switching cost, once a lab's technicians have been trained on a specific kit's protocols and the lab's standard operating procedures have been written around a specific instrument's quirks, is high enough that mid-cycle defection is rare.

Underwriting the entire diagnostics flywheel is the regulatory moat. CE-IVD compliance under the EU's tightened IVDR regime, ICMR validation in India, and the precedent of a U.S. FDA EUA acceptance — each of these is a fixed cost that is amortised across an expanding kit portfolio. A new entrant cannot replicate the regulatory footprint cheaply, and an MNC incumbent cannot price down to 3B BlackBio's level without cannibalising their developed-market book.

The thing to internalise as an investor is that the company is no longer a "COVID kit maker that lucked out." It is, structurally, a diversified molecular diagnostics manufacturer with three platforms (PCR, NGS, digital PCR), a rapid-test extension via Coris, a reagent-rental annuity model, and a multi-geography regulatory wrapper. That is a different conversation entirely from the one you have about a typical Indian small-cap pesticide formulator.

VII. The Dubey Playbook: Management & Governance

Spend an hour reading 3B BlackBio's annual reports, earnings transcripts, and BSE filings and a particular kind of corporate personality emerges. It is not flashy. There are no celebrity hires from McKinsey or BCG, no big-name independent directors freshly imported from Mumbai banking circles, no ESG glossies featuring drone shots of the factory. The communication tone is sober, the operating updates are detailed, and the management itself is, by Indian SME standards, unusually understated.

At the top of the chart sits Dhirendra Dubey, धीरेंद्र दुबे, the Chairman and Managing Director. He is the family member who made the original strategic call in 2011 to incubate a molecular diagnostics subsidiary inside a pesticide company, which in retrospect was the single most important capital allocation decision in the company's history. Sitting alongside him as Chief Financial Officer is Nikhil Kuber Dubey, निखिल कुबेर दुबे, who handles the financial operations and increasingly the investor-facing function. The earnings calls — and the company has, to its credit, started doing them on a regular cadence — typically feature Nikhil walking analysts through the quarter and Dhirendra coming in for the strategic framing.

The skin-in-the-game arithmetic is the part that long-term investors will care about most. Promoter holding sits at around 41% of the equity, and the more important data point is the share-pledge column: zero shares are pledged.15 In Indian small caps, that single line item is the single most reliable proxy for promoter financial discipline. A pledged promoter is a promoter with a leveraged personal balance sheet, which means they have an interest in driving short-term reported numbers (or in some cases, share price levels) that may diverge from long-run business interests. A zero-pledged promoter is one whose financial fate is tied to the company doing well over multi-year horizons, not over the next quarter's stock chart.

The dividend policy is also worth dwelling on. For FY25, the board recommended a final dividend of ₹4 per equity share — a 40% payout on the ₹10 face value.16 On a consolidated FY25 net profit of ₹47.65 crore (versus ₹32.73 crore the prior year, a 45.59% jump), this represents a meaningful but not aggressive payout: enough to signal management confidence in cash generation, but not so high that it constrains the reinvestment runway that the European M&A pipeline requires.17 For comparison, many of the post-COVID Indian diagnostic and pharma small caps either went to zero dividend (because the windfall had been spent) or to abnormally high one-time payouts (because management was capitulating on the second-act thesis). A consistent 40%-style payout is the middle path: rewarding shareholders while keeping powder dry for opportunistic M&A.

The amalgamation in 2023 is the corporate-structure detail that ties this all together. For years, the listed entity had been Kilpest India — a name redolent of crop chemistry — with the 3B BlackBio Biotech business sitting as a subsidiary inside it. In 2023, the company executed a Scheme of Amalgamation under Sections 230 to 232 of the Companies Act, 2013, merging the subsidiary upward and renaming the parent to 3B BlackBio Dx Limited.18 The share swap was set at 8.33 shares of Kilpest for every 1 share of 3B BlackBio Biotech, with shares issued only to the existing minority shareholders of the subsidiary (Kilpest itself had held 87.44% of the subsidiary's equity, so the parent's holding was simply extinguished in the merger).9

To outside observers the amalgamation looked like a tidying-up exercise. In substance it was something more strategic: by consolidating the diagnostics IP and operating business into a single listed entity, the company eliminated the minority-interest leakage that had been masking a portion of its true earnings power on the consolidated statements, simplified the cap table for any future global investor, and re-positioned the listed ticker — both literally (the rename) and in market perception — as a diagnostics business rather than an agrochemical one with a biotech option attached.

The transition that is genuinely difficult, and that is still in motion, is the move from a family-run Bhopal SME with a single domestic factory to a professionally managed global entity with Belgian manufacturing assets, a UK distribution subsidiary, a CE-IVD regulatory presence in Europe, and an investor base that increasingly includes institutional names rather than just retail and HNIs. Holding the family ethos — long-term thinking, conservative balance sheet, low-pledge promoter discipline — while installing the global infrastructure — multi-jurisdictional GMP audits, European management hires, IVDR compliance teams, English-Hindi-French-Dutch operating cadence — is a real cultural challenge that the next two to three years will test in earnest.

That cultural transition is also where the competitive analysis gets interesting.

VIII. Playbook: Porter's 5 Forces & Hamilton's 7 Powers

It is one thing to describe a corporate metamorphosis. It is another to ask, structurally, whether the resulting business has any durable competitive advantage — or whether the post-COVID 3B BlackBio is just a small-cap participating in a temporarily attractive industry that will eventually be commoditised by Chinese low-cost manufacturers and Indian regional copycats. The frameworks worth running through are Hamilton Helmer's 7 Powers and Porter's Five Forces.

Start with Helmer. The strongest of the 7 Powers in 3B BlackBio's case is Counter-Positioning. The classic counter-positioning play is one where the new entrant's business model would actively harm the incumbent's existing P&L if the incumbent tried to copy it. 3B BlackBio's "Western-quality, India-priced" molecular diagnostics value proposition is exactly that. Roche cannot — without cannibalising its global premium pricing — drop the per-test price of its PCR kits to compete with TRUPCR in India or in cost-conscious export markets. Abbott has the same constraint; so does Qiagen, which is now a Thermo Fisher subsidiary by the time of this episode. Any MNC that tried to match the Indian price book on the same product portfolio would be signalling to its developed-market customers that the historical pricing was extractive, which would trigger a global renegotiation cycle that no MNC product head wants to start.

The second power in the stack is Switching Costs. The reagent-rental model is a textbook switching-cost generator. Once a lab has accepted a free thermal cycler from 3B BlackBio, retrained its technicians on the TRUPCR protocols, and rewritten its standard operating procedures around the supplier's kit lots and quality controls, the cost of switching to a competitor — even if that competitor offers a lower per-test price — is non-trivial. Lab manager risk-aversion is the hidden variable here: nobody wants to be the technician who switched suppliers and then had a false-negative on a TB patient.

A third, weaker power is Process Power: the manufacturing know-how to run a molecular diagnostics line at Indian cost with European-equivalent quality is not trivially replicable, and 3B BlackBio has been running that process for over a decade. But this is the most attackable of the moats — a well-funded competitor with patient capital could, over five to seven years, build a parallel process. The moat is real but not impenetrable.

There is no meaningful Network Economy, no Scale Economy at the scale this company currently runs, no Cornered Resource in any obvious IP sense, and no Branding power in the consumer sense — TRUPCR is a B2B kit brand, not a consumer name. So the operative powers are counter-positioning, switching costs, and a process-power foundation.

Now the Porter view. Threat of New Entrants: medium-high in domestic India (the regulatory cost is non-trivial but achievable for any well-capitalised pharma company), but medium-low in IVDR-compliant Europe (where the regulatory build-out is now a multi-year, multi-million-euro investment that washes out small players). Threat of Substitutes: structurally low in the near term. The substitute for a PCR test is either a worse-performing test (antigen/lateral flow, where Coris now gives 3B BlackBio an internal hedge) or a more advanced test (NGS, dPCR, where 3B BlackBio is already a participant). Bargaining Power of Buyers: split. Large lab chains (Dr. Lal PathLabs, Metropolis, Thyrocare, SRL) have meaningful negotiating leverage, but the placement model and switching costs partially neutralise that leverage once a lab is on the platform. Smaller hospital labs have very little bargaining power. Bargaining Power of Suppliers: medium. Specialty enzymes (Taq polymerase variants, reverse transcriptases) are still sourced from a small number of global suppliers, but the kit chemistry is sufficiently modular that no single supplier holds a chokehold. Rivalry: this is where the picture is most nuanced. Inside India, the competitive set is real and aggressive — Mylab Discovery Solutions, Molbio Diagnostics (with the well-known Truenat platform), Trivitron Healthcare, Krishgen Biosystems, and a handful of others all compete for similar lab placements. In CE-IVD Europe, the competitive set is structurally different: the IVDR regime has thinned the field, the incumbents are MNCs not local rivals, and 3B BlackBio's cost positioning is most differentiated there.

The myth vs reality test is worth running here. The consensus narrative on 3B BlackBio is that it is a "COVID winner that pivoted to Europe." The fact-check on that is mixed. The COVID windfall was real, but the diagnostics business existed for nine years before COVID and was already an ISO-13485-running, ICMR-validated kit manufacturer. Europe is genuinely a strategic axis, not a press-release talking point — the HS Biolabs and Coris transactions are not symbolic, they are functional. But the bear-case framing that says "this is just another distressed-asset arbitrage" understates the operating intent: Coris was bought to be integrated into a CE-IVD product portfolio, not to be flipped.

A short second-layer diligence aside before we move on. The 2023 amalgamation introduced some non-cash one-time items into the comparable P&L, which means investors need to compare like-for-like consolidated numbers from FY24 onward, not raw historical Kilpest-only sequences. The auditor's report has been clean to our knowledge, and there is no going-concern or material related-party item we are aware of in the public filings; that said, the rapid expansion across multiple geographies will put a real burden on internal financial controls, and the next two reporting cycles are where that infrastructure will be tested in practice.

IX. Analysis & Bear vs. Bull Case

Every interesting investment debate eventually collapses into two competing stories about the same set of facts, and 3B BlackBio is no exception. Let us walk both of them honestly.

The bull case starts with the post-Coris run-rate. The Q3 FY26 quarter, with consolidated revenue of ₹50.34 crore and net profit of ₹22.44 crore, gives us a first clean window into the combined entity's earnings power. If you simply annualise that quarter — and acknowledge the obvious risks of doing so — you get a roughly ₹200 crore revenue run-rate and an ₹85-90 crore profit run-rate, against an FY25 base of ₹96.47 crore in revenue and ₹47.65 crore in profit.1317 On top of that base, the bull case layers three structural tailwinds. First, the European business — Coris plus TRUPCR Europe — is still in the early innings of cross-selling its product portfolios, and the IVDR-driven consolidation in European labs is a multi-year supply-side tailwind for compliant manufacturers. Second, the company has guided toward 40% of revenue from exports as a stated objective, which (if executed) materially de-risks the India-only concentration that plagues most domestic small caps. Third, the NGS and digital PCR adjacencies are higher-margin platforms that are still ramping; even modest market-share gains in the Indian oncology NGS space would be incrementally accretive at the consolidated margin level.

Layer onto that a clean governance posture (zero pledged shares, 41% promoter holding, consistent 40% dividend payout), a debt-free balance sheet, and the optionality of further European bolt-on acquisitions at distressed valuations — Coris cost under £3 million all-in — and the bull case is essentially: this is one of the few Indian small-cap diagnostics businesses with a credible path to becoming a globally relevant mid-cap, and the market has not yet repriced it as such.

The bear case is honest about three categories of risk that the bull case tends to gloss.

The first is the lumpiness of the underlying diagnostics business. PCR test volumes are episodic — they spike with infectious-disease outbreaks (influenza seasons, dengue outbreaks, the various coronaviruses that lurk in epidemiological literature) and they slump in quiet years. A bad influenza season in 2026 could flatter the FY27 numbers; a quiet flu year in 2027 could embarrass them. The 9M FY26 strength is meaningfully boosted by both the Coris consolidation and a strong respiratory-pathogen season in Europe, and disentangling underlying organic growth from those tailwinds is not trivial from the public disclosures.

The second is the regulatory cliff in the United States. The 2020 FDA EUA was an emergency authorisation. It does not convert automatically into a full 510(k) clearance, and any path to a sustained U.S. market presence would require a multi-year, multi-million-dollar regulatory submission, with no guarantee of success. The U.S. market is the largest single diagnostics market in the world, and 3B BlackBio's commercial presence there is — as of today — meaningfully smaller than the EUA-era headline would suggest.

The third is Chinese cost competition. Mainland Chinese molecular diagnostics manufacturers — particularly the larger ones with established ISO 13485 footprints — have been aggressive on price into emerging-market tenders since 2022. In the African and Southeast Asian government-tender business, where price is the dominant procurement criterion and IVDR or FDA branding is not strictly required, Chinese kits have repeatedly undercut Indian kits by margins that no operational efficiency can close. 3B BlackBio's response — pivoting to higher-regulation Europe where Chinese suppliers face IVDR friction — is the right strategic move, but it concedes a part of the addressable market that earlier bullish narratives had counted on.

If you are wondering which one or two KPIs to actually track quarter-to-quarter to decide which of these scenarios is playing out, the honest answer is to watch two things. First, export revenue as a share of total revenue, and within exports, the European share specifically — that is the cleanest leading indicator of whether the strategic pivot is converting into durable revenue. Second, gross margin trajectory in the molecular diagnostics segment, ex-Coris consolidation effects, because gross margin is the variable that will tell you whether the kit ASPs are holding up against Chinese competition or quietly eroding. Everything else — PAT, ROCE, dividend, even segment revenue mix — is downstream of those two variables.

The frameworks-meets-fundamentals reading is that 3B BlackBio sits in an unusually attractive structural position (counter-positioning moat, switching-cost annuities, IVDR-friendly geography) inside an inherently cyclical industry. Investors who weight the structural moat will lean bullish; investors who weight the diagnostic-cycle volatility will lean cautious. Both are reading the same balance sheet — they are just weighting different cells.

X. Conclusion & Outro

There is a particular kind of corporate transformation that the Indian small-cap market produces more often than any other equity market in the world. It usually goes like this. A multi-generational family business in a tier-2 city sits on a profitable but stagnant legacy operation. The second-generation promoter inherits both the cash flow and the constraint. A macro shock arrives — a regulatory change, a global commodity cycle, a pandemic — and dumps cash on the doorstep. What happens next is what separates the franchises from the footnotes.

3B BlackBio Dx is, to date, in the franchise column. The pesticide-to-PCR pivot was incubated patiently across the better part of a decade before COVID accelerated it. The windfall cash was redeployed into capability, regulatory infrastructure, and counter-cyclical M&A rather than into dividends, vanity acquisitions, or fixed deposits. The corporate structure was simplified through a clean amalgamation that re-positioned the listed entity for a global audience. The governance posture — zero pledged shares, 41% promoter holding, a steady 40% dividend payout, a debt-free balance sheet, consistent quarterly disclosures — is the version of Indian SME stewardship that institutional investors reward over decade-long horizons.

The remaining questions are the ones that will be answered by execution rather than by analysis. Will Coris's CE-IVD portfolio cross-sell meaningfully into TRUPCR Europe's existing customer base, or will the integration cost more management bandwidth than the synergies are worth? Will the NGS and digital PCR platforms scale to a level that materially shifts the consolidated margin mix, or will they remain interesting line items that don't move the needle? Will the next external shock — and there is always a next external shock — find 3B BlackBio better-positioned than its peers, the way COVID did, or will it find the company over-extended across too many geographies and product lines? Will the next generation of European management retain the cost discipline that the Bhopal centre has carried forward for fifty years?

The Acquired-style takeaway is simple. Old companies can learn new tricks. But only the ones with the unusual combination of patient family capital, manufacturing humility, and the strategic discipline to recognise a windfall as an opportunity to build durable IP rather than to extract cash. The Bhopal-to-Brussels arc is, at its core, a story about that combination. From an industrial-area gate in Govindpura to a Walloon office park in Gembloux, by way of a Manchester distribution office and a U.S. FDA Emergency Use Authorisation — the geography of the journey is improbable, but the strategic logic of every step is, in retrospect, internally consistent.

The next chapter of Indian biotech on the global stage will not be written by the venture-backed bio-IPOs that dominate the press cycle. It will be written, more likely, by a handful of patiently compounded, family-run, regulatory-compliant manufacturers from cities that most international investors have never visited. 3B BlackBio's pivot is one entry in that ledger. There are probably others quietly underway. The job of the long-term investor is to find them before the consensus narrative does.

References

References

-

Avacta Announces Agreement to Sell Coris Bioconcept SRL — Avacta Therapeutics, 2025-07-28 ↩↩

-

Kilpest India Limited to merge subsidiary with itself, change name as 3B BlackBio Dx Ltd — EquityBulls ↩

-

3B Blackbio DX Ltd share price | About 3B Blackbio | Key Insights — Screener.in ↩

-

FDA Grants EUAs for Coronavirus Tests from 3B Blackbio, Ohio State, and Others — 360Dx/GenomeWeb, 2020-06-19 ↩

-

OraSure's OMNIgene·ORAL Device Included in EUA Amendment Granted to 3B BlackBio Biotech India for SARS-CoV-2 Test — GlobeNewswire, 2020-12-23 ↩

-

Kilpest India to merge subsidiary with itself; stock down 2% — India Infoline ↩↩

-

Kilpest India's 3B BlackBio acquires 70% stake in HS Biolabs — India Infoline, 2022-03-29 ↩

-

Avacta sells Coris for £2.2m in therapeutics shift — BusinessCloud, 2025-07-28 ↩

-

Avacta completes transition to therapeutics with Coris Bioconcept sale — Investing.com, 2025-08-29 ↩

-

3B BlackBio Q3 FY26 Revenue ₹99Cr; Guides 10-15% Growth Amid M&A — Whalesbook ↩↩

-

3B Blackbio DX Ltd Share Price & Shareholding — Screener.in ↩

-

3B BlackBio Dx Reports 18% Revenue Growth in Q1 FY26, Acquires Belgium-Based Coris Bioconcept — Scanx Trade ↩↩

-

3B BlackBio Dx Limited — Annual Report and Corporate Filings, 2023 ↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube