360 ONE: India's Wealth Management Disruptor

I. Introduction & Episode Roadmap

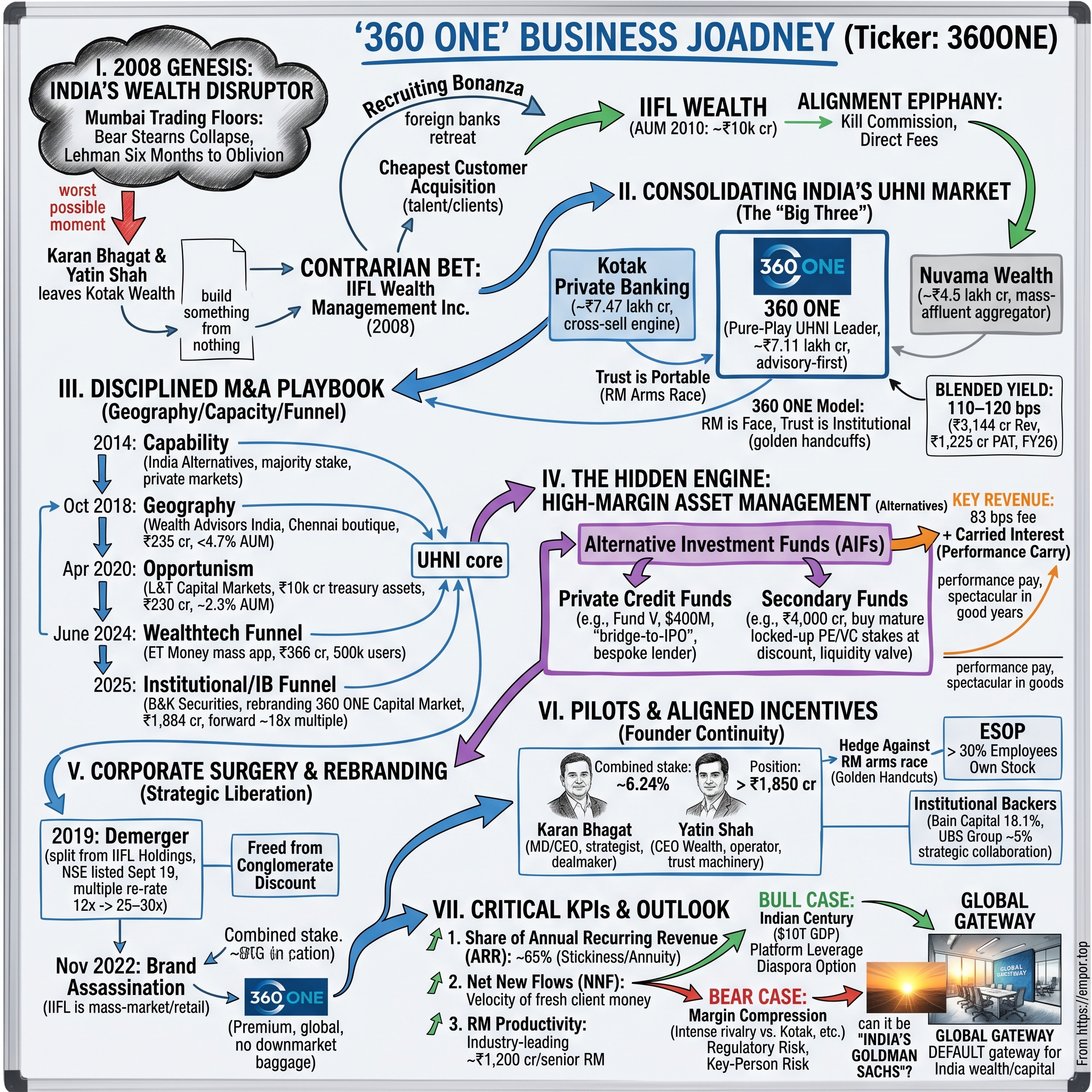

Picture the trading floors of Mumbai in March 2008. The Bombay Stock Exchange ticker is a wall of red. Bear Stearns, an 85-year-old Wall Street institution, has just been swallowed by JPMorgan in a weekend fire sale for two dollars a share. Lehman Brothers is six months from oblivion, though almost nobody yet knows it. On one particularly brutal session, the Sensex shed roughly 1,400 points, one of the steepest single-day falls the index had ever recorded. Across the financial district, the conversation among bankers is about survival: which desks get cut, which bonuses evaporate, who gets the dreaded tap on the shoulder.

And it is precisely at this moment — the worst possible moment, by any rational reading of a spreadsheet — that a 28-year-old named Karan Bhagat walks away from a secure, prestigious job running Kotak's wealth practice in Mumbai to build something from nothing.3 He pulls his friend Yatin Shah along with him. To the outside world, it looks like a young man setting fire to his own career on the eve of a depression.

It was, instead, one of the great contrarian bets in modern Indian finance.

Here is the question this episode circles around. How did a firm conceived in the teeth of the worst financial crisis in three generations grow from a blank sheet of paper into a platform managing ₹7.11 lakh crore — roughly US$79 billion — in client assets, serving more than 7,500 of India's wealthiest families, and commanding a market capitalization north of ₹42,000 crore?110 That firm is 360 ONE, listed on the NSE under the ticker 360ONE, and known for the first fourteen years of its life as IIFL Wealth.

There is a deeper puzzle underneath the growth story, and it is the one that should interest a long-term investor most. Wealth management is, historically, a terrible business to try to scale. It is a regional, relationship-driven trade where the asset — trust — walks out the door every evening in the mind of a single relationship manager. It does not compound like software. It does not enjoy the winner-take-all dynamics of a marketplace. For a century, the private bank was a cottage industry wearing a tailored suit. The interesting thing 360 ONE did was to take this stubbornly artisanal business and force it to behave like an institutional, technology-enabled platform — one where assets, products, and even client relationships could be industrialized without snapping the thread of trust that holds the whole thing together.

Why does this matter beyond the curiosity of one company's success? Because the answer reveals something general about which businesses compound and which merely grow. A firm that depends on a handful of irreplaceable rainmakers is a collection of lottery tickets; a firm that institutionalizes the thing its rainmakers do is an asset that keeps paying long after any individual leaves. The whole of 360 ONE's history can be read as a slow, deliberate campaign to move from the first category to the second — to convert personal relationships into platform relationships, one-off commissions into recurring fees, and founder credibility into an institution that no longer needs its founders. Whether that campaign has succeeded is the real question under the stock price, and it is the thread we will follow through every section.

So here is the roadmap. First, we map the modern battlefield — the "Big Three" who now dominate Indian wealth and the structural tailwind blowing at all of their backs. Second, the contrarian origin story and how a 2008 launch turned a catastrophe into a recruiting bonanza. Third, the single product insight — killing the commission — that gave them product-market fit. Fourth, a tour through one of the most disciplined M&A playbooks in Indian financial services, where we will keep asking the only question that matters: did they overpay? Fifth, the quiet, high-margin engine hiding inside the asset management arm. Sixth, the corporate surgery — the demerger and the brand assassination — that liberated the equity. Seventh, the people flying the plane and how they are paid. And finally, the moats, the bull and bear cases, and the handful of numbers that actually tell you whether the thesis is intact.

Let's start with the shape of the war.

II. The Big Three: The Battle for Indian Wealth

To understand 360 ONE, you first have to understand a tectonic shift happening underneath the entire Indian economy — one so slow and so vast that most people living through it barely notice. Analysts call it the "financialization of savings," which is a clumsy phrase for a beautiful idea. For generations, the Indian household stored its wealth in two things it could touch: gold locked in a cupboard and land it could walk across. These were not investments so much as talismans against catastrophe. But over the past decade, a structural migration has been underway — capital is leaving the cupboard and the field and moving into capital markets: equities, mutual funds, bonds, and private market structures. The pool of financial assets has been compounding at roughly 15–17% a year, and the steepest part of that curve sits at the very top of the wealth pyramid, where the entrepreneurs who built India's tech, pharma, and manufacturing fortunes are looking for somewhere sophisticated to put their money.

To grasp the scale of this, hold two numbers in your head. India's household savings have historically been parked overwhelmingly in physical form — by various estimates, well over half of household wealth sat in gold and real estate, assets that generate no fee income for anyone and no productive capital for the economy. As that ratio shifts, even a few percentage points migrating into financial instruments unleashes a torrent of new money into mutual funds, equities, bonds, and private structures. And the migration compounds: each newly liquid entrepreneur who sells a business creates not just a one-time pool of capital but a multi-decade advisory relationship, and often a new generation of inheritors who will need the same services. This is why the addressable market for a firm like 360 ONE is not growing arithmetically; it is growing geometrically, and from a low base.

This is the river 360 ONE fishes in. And here is a piece of consensus wisdom worth fact-checking. The popular image of wealth management is of a hopelessly fragmented cottage industry — thousands of small advisors, no scale economics, no winners. That was true a decade ago. It is no longer true at the top. The reality is that the ultra-high-net-worth tier has consolidated hard into three distinct archetypes, and the gap between the Big Three and everyone else has widened, not narrowed, as scale, technology, and product breadth have started to matter. Think of these three less as companies and more as three competing theories about how to win.

The first theory is The Bank-Led Giant, and its champion is Kotak Private Banking, the wealth arm of Kotak Mahindra Bank, which oversaw customer assets of roughly ₹7.47 lakh crore (about US$83 billion).11 Kotak plays the establishment card with the full weight of an institution behind it. It has a fortress balance sheet, a banking license, decades of trust, and — crucially — a giant retail and corporate banking customer base it can mine. When a Kotak business banking client sells his company, the bank already holds the account. The wealth team simply walks down the hall. This is the cross-sell engine, and it is formidable. The weakness is the flip side of the strength: a bank is a department store, and the ultra-wealthy increasingly want a specialist boutique.

The second theory is The Pure-Play UHNI Leader, and that is 360 ONE itself, with assets of ₹7.11 lakh crore (about US$79 billion) — neck and neck with Kotak at the top of the league table despite having none of Kotak's deposit base.1 Their entire strategy is to ignore the broad market and camp out at the absolute summit of the pyramid: families with ₹25 crore-plus in net worth, the ultra-high-net-worth, or UHNI, segment. It is an advisory-first, pure-play model, deliberately concentrated, that behaves less like an Indian bank and more like the private wealth division of Goldman Sachs. The bet is that the very richest clients value independence and specialization over the comfort of a banking brand. The risk, of course, is concentration: when your business is built on a few thousand families, the loss of a few hundred relationships matters.

The third theory is The Mass-Affluent Aggregator, embodied by Nuvama Wealth, controlled by the private equity firm PAG, with client assets around ₹4.5 lakh crore (roughly US$50 billion).4 Nuvama runs an integrated three-pillar model — wealth management, capital markets, and asset management — and aims a notch below the summit, at the rapidly swelling ₹5 crore to ₹25 crore HNI band. This is the fastest-growing slice of the pyramid by sheer number of new entrants, and Nuvama's bet is that scale and breadth in the middle beats exclusivity at the peak.

Why do these three dominate, and why is it so hard for a fourth to muscle in? The answer is the most uncomfortable truth in wealth management: trust is portable, and it does not belong to the firm. It belongs to the relationship manager. A top RM in Mumbai is a free agent who can resign on a Friday and have a meaningful share of his book follow him to a competitor by the following quarter. This creates a brutal arms race for talent — annual packages for star RMs in Mumbai now run past ₹5 crore — and it is the single greatest source of fragility in the entire industry. The genius of 360 ONE's operating model is the attempt to make trust institutional rather than personal: wrapping the client in so many firm-level products, structures, and reporting systems that the RM becomes the face of the relationship rather than the sole owner of it. Their top 20 relationship managers control something like 40% of assets, and keeping those people — through ownership, process, and platform lock-in rather than ever-escalating cash — is arguably the central management problem of the whole enterprise. We will return to how they do it.

Before leaving the competitive map, it is worth naming the single most dangerous dynamic in this industry, because it explains nearly everything about how the Big Three behave. Trust, as we said, is portable — but the people who carry it are not infinitely loyal. A star relationship manager is, functionally, a small business that happens to sit inside a larger one, and he can pack up that business and move it across the street. This is the RM arms race, and it is why packages for the best bankers in Mumbai have spiraled past ₹5 crore a year. It is a war of attrition that, fought on cash alone, erodes everyone's margins simultaneously — a prisoner's dilemma in pinstripes. The firms that win are the ones that find a way to make their best people stay for reasons other than the next pay cheque, which is a problem 360 ONE has tried to solve structurally rather than chequebook by chequebook. Hold that thought; it returns when we look at how the firm pays its people.

The economics that fall out of this are what make the business worth studying. 360 ONE earns a blended revenue yield of roughly 110–120 basis points on the assets it manages — that is, a little over one rupee of revenue for every hundred rupees of client money. That sounds thin until you remember the assets are measured in lakhs of crores. It translated into total revenue of around ₹3,144 crore and profit after tax of ₹1,225 crore in the financial year ended March 2026.1 The strategic question hanging over that yield — and over every bull and bear argument we will make later — is whether a pure-play boutique can defend a premium price while a bank like Kotak, with a near-zero cost of capital, is perfectly happy to cut fees to win the relationship and make its money elsewhere.

To see how 360 ONE earned the right to be in this conversation at all, we have to go back to the empty office in 2008.

III. The Genesis: Surviving the 2008 Financial Storm

We can skip the ancient history, because 360 ONE doesn't really have any. Its entire story begins in a single year, and that year happens to be the worst one imaginable to start a financial firm.

In December 2007, Karan Bhagat was 28 years old and running Kotak's wealth management practice for Mumbai — a genuinely good job, the kind a young banker spends a decade earning.3 But Bhagat had spotted something his employers, and most of the industry, were structurally incapable of acting on. India was minting a new species of rich person: not the old industrial dynasties, but first-generation founders in technology, pharmaceuticals, and manufacturing who had built companies and, increasingly, sold them. These people were self-made, skeptical, and allergic to being condescended to. And what the banking industry offered them was to be "sold" — handed cookie-cutter, high-commission products designed to maximize the bank's take, not the client's outcome. Bhagat's insight was that this new generation would pay handsomely to be advised rather than sold to, if only someone would build a firm honest enough to do it.

So he went to see Nirmal Jain, the founder and chairman of IIFL Holdings (then known as India Infoline), and pitched him on backing a wealth practice built from scratch. Jain said yes. Bhagat resigned from Kotak, pulled in his friends Yatin Shah and Amit Shah, and on January 17, 2008, IIFL Wealth Management was incorporated as a unit of the IIFL group.3 They opened the doors for business in April 2008 — just as the global financial system began to seize.

Now, here is where the story turns from reckless to brilliant. To everyone watching, launching a wealth firm into the 2008 collapse looked like jumping out of a plane to test a parachute you hadn't finished sewing. But Bhagat and Shah understood a piece of counter-cyclical logic that the panicked herd missed. When global banks are in a crisis, they don't just stop hiring — they retreat. Merrill Lynch, UBS, and the other Wall Street and Swiss houses that had planted flags in India began pulling capital and attention back to their bleeding home markets. Whole teams of talented Indian private bankers, with deep client relationships, were suddenly surplus to requirements at firms fighting for their own survival on another continent.

IIFL Wealth went on the offensive into that vacuum. While the foreign banks were in defensive crouch, the startup hired the star teams those banks were laying off, and inherited the client relationships that London and New York no longer cared to service. A crisis that destroyed competitors became, for a firm with no legacy book to defend and a hungry balance sheet behind it, the cheapest customer-acquisition event of a generation. You cannot buy that kind of talent and those kinds of relationships in a bull market at any price; in early 2009, they were practically being handed out.

But the recruiting coup was only the delivery mechanism for the real idea — the one that would define the firm's identity for the next two decades. Bhagat and Shah looked hard at how traditional wealth managers actually made money, and they didn't like what they saw. The industry ran on commissions. A bank would sell a client a mutual fund or a structured note and pocket an upfront commission of 4–5% from the product manufacturer. The client often had no idea this was happening. The result was a grotesque conflict of interest baked into the foundation of the relationship: the advisor's incentive was not to recommend the best product, but to recommend the one that paid the fattest commission, and then to "churn" the client into a new one as often as decency allowed.

The founders' "alignment" epiphany was to blow this model up. Instead of taking hidden commissions from product manufacturers, they would charge the client a direct, transparent annual advisory fee — on the order of 50 to 100 basis points of assets — and sit, as the firm liked to put it, "on the same side of the table" as the client. If the client's portfolio grew, the firm's fee grew. If it shrank, so did the fee. Suddenly the advisor's incentive and the client's interest pointed in the same direction. For a generation of self-made entrepreneurs who had spent their careers smelling out misaligned incentives, this was an irresistible pitch. It also happened to anticipate, by the better part of a decade, the direction Indian regulators would eventually push the entire industry.

It is worth dwelling for a moment on the human chemistry that made this work, because the firm's culture flows directly from its two founders, and they are temperamentally complementary in a way that good partnerships usually are. Bhagat is the strategist and the public figure — restless, deal-minded, comfortable on a stage and in a boardroom, the man who would later bet ₹50 crore on a brand change and pour his own variable pay into stock. He thinks in terms of platforms and decades. Yatin Shah is the relationship operator, closer to the day-to-day machinery of client trust, the one who understood that a wealth firm lives or dies on whether the phone gets answered at 2 a.m. when a family is in crisis. Neither came from old money or an established franchise; they were, in a sense, the same species as their clients — first-generation builders making something from nothing. That shared identity with the self-made entrepreneur is not a marketing line. It is why the pitch landed. A founder who has just sold his company can smell a salesman, and these two did not feel like salesmen. They felt like peers.

The clientele this attracted were precisely the people Bhagat had identified from the start: first-generation founders sitting on a once-in-a-lifetime pool of liquidity, terrified of squandering it and obsessed with passing it intact to their children. These are sticky, multi-decade, multi-generational relationships — exactly the kind that compound, the kind a competitor cannot easily pry loose. By 2010, barely two years in and through the worst of the storm, the startup was managing around ₹10,000 crore. The contrarian bet had paid off in a way that few of the firm's panicked rivals could have imagined when the screens were bleeding red. But survival and growth are not the same as durability, and the harder question — how to turn a fast-growing boutique built on two founders' personal credibility into a durable institution that outlives them — was only just beginning.

IV. Capital Deployment & The M&A Playbook: Did They Overpay?

Every acquisitive company tells you its deals are "strategic" and "accretive." The job of an investor is to ignore the adjectives and check the arithmetic. 360 ONE has used M&A as a core instrument of growth, but what makes the record worth studying is that it wasn't deal-making for its own sake. Each acquisition bought a specific, identifiable thing the firm could not easily build — a capability, a geography, a distribution funnel — and, with remarkable consistency, it bought them at prices that look disciplined in hindsight. Let's walk the timeline and audit the math.

The first move, in 2014, was a capability play. The firm took a majority stake in India Alternatives, an established private equity and venture capital advisory outfit.13 The logic was classic build-versus-buy. 360 ONE's UHNI clients were increasingly asking for access to private markets — pre-IPO deals, growth equity, venture — and building a credible private markets team from scratch is a multi-year slog requiring scarce talent and a track record you cannot fake. Rather than spend years assembling it, they bought a running start. This was small in rupee terms but large in strategic terms: it planted the seed of what would become the firm's highest-margin engine, the alternatives business we will dig into shortly.

The second move, in October 2018, was a geography play, and it is a small masterpiece of cultural arbitrage. Southern India — Chennai, Bangalore — is famously its own world when it comes to money: conservative, relationship-driven, and deeply skeptical of slick Mumbai firms parachuting in. You do not win a Chennai textile dynasty's trust with a glossy deck. So instead of trying to crack the South cold, 360 ONE acquired Chennai's premier wealth boutique, Wealth Advisors India, for ₹235 crore (about US$27 million), inheriting around ₹5,000 crore of assets and, more importantly, the local trust those assets represented.9 Run the numbers and the discipline shows: paying ₹235 crore for ₹5,000 crore of AUM is a price of under 4.7% of assets, squarely in line with global benchmarks for buying a wealth book. They didn't pay up for the privilege of entering the South; they paid a fair market clip and got instant credibility thrown in.

The third move, in April 2020, was opportunism of the purest kind — executed virtually, in the eerie silence of the first COVID-19 lockdown, while most of corporate India sat frozen at home. 360 ONE acquired L&T Capital Markets, the wealth arm of L&T Finance Holdings, for ₹230 crore, bringing roughly ₹10,000 crore of assets onto the platform.9 And not just any assets — these were highly sticky corporate treasury and institutional relationships, the kind of money that doesn't chase the latest fad and doesn't leave in a panic. The price works out to about 2.3% of AUM, half what they paid for the Chennai book two years earlier. Buying high-quality, sticky assets at a distressed-market price while everyone else was paralyzed is the corporate equivalent of the 2008 hiring spree: the same counter-cyclical muscle memory, applied at scale. It was, by any reasonable benchmark, a steal.

The fourth move, in June 2024, was the most debated, because on its face it looked like the disciplined acquirer finally overpaying for a shiny object. 360 ONE bought ET Money, a mass-market investment app with around 500,000 users, from Times Internet for about ₹366 crore (US$44 million), settling part in cash and part by issuing roughly 3.5 million new shares.614 This was a wealthtech play, a leap down-market from the firm's UHNI heartland into the world of robo-advisory and retail SIPs. Did they overpay? On a standalone basis, the optics were ugly: somewhere around 11.9 times sales for a loss-making app, a multiple that would make a value investor wince.

But look at how it was paid for, because that is where the cleverness hides. 360 ONE's own stock was trading at a rich valuation — roughly 40 times earnings. By funding most of the deal in its own highly-valued equity, the firm was effectively swapping expensive paper for a strategic asset, and the dilution to existing shareholders came in at only about 1%. The strategic logic underneath was a funnel. The ultra-wealthy of 2040 are the mass-affluent professionals of 2026, and a wealthtech app is a low-cost machine for capturing them young — onboarding a 30-year-old saver with ₹5 lakh today and graduating her into the core wealth business as she compounds into a ₹5 crore client over twenty years. You don't judge that deal on this year's P&L; you judge it on whether the funnel works.

The fifth move, in 2025, was the biggest in the firm's history and the most quietly consequential. 360 ONE agreed to acquire Batlivala & Karani Securities — B&K, a storied institutional brokerage — in a stock-and-cash deal valued at roughly ₹1,884 crore, and rebranded it 360 ONE Capital Market.2 B&K brought something the firm conspicuously lacked: a top-tier institutional equities desk servicing nearly every major domestic and foreign financial institution, plus a corporate advisory and mid-market investment banking team, all run by 300-plus professionals. Did they overpay? On a trailing basis the multiple looked frightening — around 47 times earnings. But B&K's profits were surging, hitting roughly ₹105 crore in FY25, which pulls the forward multiple down to something closer to 18 times. Set that against 360 ONE's own ~40x multiple and the trade becomes obvious: they used their own expensive currency to buy a fast-growing, highly accretive corporate-and-institutional funnel at roughly half their own valuation. The strategic prize is bigger than the brokerage itself — an investment banking relationship with a founder is the on-ramp to managing that founder's personal fortune the day his company lists.

A second-layer diligence point is worth flagging here, because acquisitive financial firms are exactly where accounting and integration risks hide. Serial acquirers can flatter their growth by stacking deals on top of each other, masking weak organic performance behind a wall of inorganic AUM. The reassuring counter-evidence at 360 ONE is twofold: the deals have generally been paid for in equity at high multiples or cash at distressed multiples rather than debt — so the balance sheet has not been levered up to fund the spree — and the firm has repeatedly retained the key people from the acquired businesses rather than gutting them, which is the difference between buying a franchise and buying a fleeing list of clients. Saahil Murarka, who led B&K, joined the 360 ONE group to run the broking and capital markets business rather than cashing out, a detail that tells you the acquirer understood it was buying people, not just a license.2 The risk that remains, and that a careful owner should keep watching, is integration: bolting an institutional brokerage and a retail wealthtech app onto a UHNI advisory firm creates cultural and systems complexity, and complexity is where margins quietly leak.

Step back from the individual deals and a pattern emerges that tells you more about the company than any single transaction. The acquisitions of capability (private markets), geography (the South), sticky assets (corporate treasury), a down-market funnel (wealthtech), and an up-market funnel (institutional and IB) are not a random shopping spree. They are the methodical assembly of a vertically integrated wealth platform that touches a client at every stage of the wealth journey, from first SIP to IPO to dynastic trust. And almost every time, they paid in either cheap distressed-market cash or expensive overvalued stock — never the other way around. That is the signature of an operator who treats their own equity as real money. Which raises an interesting question: where, inside this sprawling platform, does the real money actually get made? The answer is not where most people look.

V. The Hidden Engine: High-Margin Alternatives & Secondaries

Walk into 360 ONE and ask what the company does, and the obvious answer is wealth management — advising rich families, the business that generates roughly 70% of revenue and gives the firm its public identity. But the most interesting story isn't in the obvious place. It's in the other 30%: the asset management arm, 360 ONE Asset, which has quietly become the firm's real growth-and-margin booster. To understand why, you have to understand a fork in the road that 360 ONE chose early and most of its rivals didn't.

There are two ways to run an asset manager in India. The first is the traditional mutual fund business — selling diversified equity and debt funds to the masses. It is a fine business, but it is fundamentally a commodity: fees are regulated down toward the floor, scale is everything, and a handful of giants compete on basis points. The second way is to walk away from the commodity entirely and build in Alternative Investment Funds, or AIFs — the Indian regulatory wrapper for private, sophisticated, high-yield strategies sold only to wealthy and institutional investors. 360 ONE Asset went almost entirely down the second road, scaling its alternates and related mandates to well over US$8.5 billion.8 This is the part of the business that doesn't compete with the index-fund price war, because the product is scarce, bespoke, and impossible to commoditize.

Two pillars hold up this hidden engine, and both are worth explaining in plain terms.

The first is private credit. In simple language, this is lending — but not the boring kind a bank does. When a company founder needs financing that a conventional bank won't or can't provide quickly — say, borrowing against his own shareholding to fund an expansion, or a "bridge-to-IPO" loan to tide the company over until it lists — he turns to a private credit fund that can move fast and structure creatively, in exchange for a meaningfully higher interest rate. 360 ONE has become one of India's largest private credit managers, and the demand is structural: in March 2026 the firm closed its fifth private credit fund with roughly US$400 million in commitments, having previously raised over ₹2,000 crore in a single earlier vintage.15 Think of it as a specialist lender funded by the very same wealthy families the firm advises — money flowing in a neat circle inside the platform.

The second pillar is secondaries, and this one requires a beat of explanation because it is genuinely clever. When you invest in a private equity or venture fund, your money is locked up for many years — you cannot simply sell on a Tuesday. But life happens: an early investor in a startup or a PE fund — a limited partner, or LP — sometimes needs cash before the lockup ends. A secondaries fund is the buyer who shows up in that moment, purchasing those mature, locked-up private stakes from sellers who need liquidity, and almost always at a discount to their underlying value, because the seller is paying for the convenience of getting out early. 360 ONE launched one of India's first dedicated secondaries funds, targeting roughly ₹4,000 crore (about US$480 million), buying seasoned private assets at attractive discounts and providing a liquidity valve to a market that badly lacks one.16 It is a wonderful position to occupy: you make money precisely because you are the patient buyer in an impatient market.

Now, the economics — and this is the part that should make an investor lean forward. On the face of it, these alternative funds yield around 83 basis points in annual management fees, which is healthy but not extraordinary. The real magic is the second income stream that traditional wealth managers structurally cannot replicate: carry, or carried interest. In a private fund, once the manager clears a minimum return for investors — a "hurdle rate" — it keeps a share, often as much as 20%, of all the profit above that line. This is performance pay, and it is spectacularly lucrative in good years and almost free to produce, because the cost of running the fund barely changes whether returns are mediocre or magnificent. It is lumpy and non-linear — you cannot forecast it quarter to quarter the way you can a management fee — but over a cycle it is the difference between a good asset manager and a great one. A plain wealth advisor earns a flat fee for advice; a manager of private capital earns a slice of the upside it creates. That is the structural reason this 30% of revenue punches so far above its weight on the bottom line, and the reason the alternates business is, quietly, the most valuable thing inside 360 ONE.

There is a structural reason both pillars are well-positioned in India specifically, and it is worth understanding because it underpins the durability of the margin. India's banking system, dominated by public-sector lenders with rigid rulebooks, is chronically bad at financing anything that doesn't fit a standard template — and a founder borrowing against his own shares, or a company needing a fast bridge loan before an IPO, is the definition of non-standard. That gap is the private credit opportunity, and it is not closing quickly; it is a feature of how Indian banking is built. Likewise, India's private equity and venture markets boomed for a decade, which means a vast stock of locked-up, ageing LP positions now exists with almost no organized place to sell them. 360 ONE is building the marketplace for that liquidity before most competitors have noticed the need. In both cases the firm is not riding a cyclical fad; it is filling a permanent hole in the country's financial plumbing, which is exactly the kind of position that defends a fee.

A clear-eyed investor should, however, hold the lumpiness of carry in proper perspective rather than capitalizing it as if it were an annuity. Performance fees are real and lucrative, but they are realized only when funds mature and clear their hurdles, which means they arrive in irregular bursts tied to vintage years and market conditions, not in smooth quarterly increments. A bad couple of years for Indian private markets could see carry income dry up almost entirely even as management fees keep ticking along. The right way to read it is as a powerful but cyclical kicker on top of a stable management-fee base — a reason the great years will look spectacular, not a reason to expect every year to. That nuance matters most precisely when the market is euphoric and tempted to extrapolate a banner carry year into perpetuity.

But a high-margin engine trapped inside a sprawling, low-multiple conglomerate is worth less than the same engine running free. Which brings us to the most important piece of corporate surgery in the company's history.

VI. The Demerger & Rebranding: Strategic Liberation

By 2018, IIFL Wealth had a problem that most companies would kill to have, and it was driving its founders quietly mad. The business was a jewel — fast-growing, high-margin, asset-light, riding a structural tailwind. And the public market was valuing it as if it were ordinary.

The reason was an old and stubborn feature of equity markets called the conglomerate discount — the tendency of the market to value a bundle of different businesses at less than the sum of their separable parts, on the theory that a confusing bundle is harder to analyze, harder to manage, and prone to cross-subsidizing the weak with the strong. IIFL Wealth was a unit inside IIFL Holdings, a sprawling group that also housed a lending business and a retail broking operation. When the market looked at the parent, it saw a financial conglomerate, slapped a conglomerate multiple on the whole thing — roughly 12 times earnings — and called it a day. The crown jewel and the costume jewelry were being valued at the same price. A high-quality, capital-light wealth franchise was being dragged down to the multiple of a balance-sheet-heavy lender, simply because they shared a corporate roof. For the founders, who could see exactly what their business would be worth if investors could only see it cleanly, this was intolerable.

So in 2019 they performed the surgery. Nirmal Jain and the founding team executed a clean demerger, splitting the wealth business out of the conglomerate as a standalone entity, and IIFL Wealth listed on the NSE and BSE as an independent stock on September 19, 2019.4 The result was almost immediate and almost theatrical. Freed from the conglomerate, investors could finally price the business for what it was, and the multiple re-rated from the low-teens toward the 25–30 times range that a specialized, high-return wealth franchise deserves. Nothing about the underlying business had changed on September 19 — same clients, same RMs, same revenue. What changed was that the market could now see it. It is one of the cleanest real-world demonstrations you will find of a simple truth: specialization beats diversification in the eyes of the market, and structure can unlock value that operations alone cannot.

If the demerger was a calculated financial move, the next act was a genuine gamble. In November 2022, the firm did something that makes most marketing executives break out in a cold sweat: it killed its own brand.5 After fourteen years of building "IIFL" into a name the wealthy recognized, Karan Bhagat spent ₹50 crore-plus to retire it entirely and rebrand the whole enterprise as 360 ONE — 360 ONE Wealth, 360 ONE Asset, the lot. Throwing away a hard-won brand is the kind of decision that gets a CEO fired if it goes wrong.

The risk was not theoretical. A brand is an accumulated stock of recognition and trust, and in wealth management trust is the entire product. Throwing away fourteen years of it overnight, in a business where a hesitant client might read the change as instability, was the kind of move that could have triggered exactly the outflows a wealth firm fears most. That 360 ONE did it deliberately, and absorbed the ₹50 crore cost without flinching, tells you how strongly the leadership believed the old name had become a ceiling rather than an asset.

But the logic was sound, and it cut to the heart of who the firm wanted to serve. "IIFL" carried baggage. The name traced back to India Infoline, a mass-market franchise associated in the public mind with retail broking, gold loans, and lending to the masses — perfectly respectable businesses, but exactly the wrong associations for a firm trying to convince a billionaire family or an international sovereign allocator that it belonged in the same conversation as the great global private banks. A UHNI client in Dubai does not want his family office managed by a brand he associates with microfinance. "360 ONE" was deliberately engineered to be premium, neutral, and global — a name with no downmarket history, equally at home on a brass plate in Mumbai, Singapore, or the DIFC in Dubai, and built to attract the international family-office and sovereign capital that the firm increasingly courts. The rebrand wasn't vanity; it was a repositioning of the entire franchise toward the top of the global market. The brand was renamed; the people stayed the same. And it is the people — and crucially, how they are paid — that determine whether any of this holds together.

VII. The Pilots: Current Management & Aligned Incentives

There is a useful test for any people-driven business: would you trust the founders to run it with your money the way they run it with their own? In a wealth manager, where the founders' job is literally to be trusted with other people's money, the question is doubly pointed — alignment is not a nice-to-have, it is the product being sold. At 360 ONE, the answer is written into the cap table and the compensation structure, and it is unusually revealing.

The story remains, to a striking degree, the story of the two men who walked out of Kotak in 2008. Karan Bhagat is Managing Director and CEO, the public face and the architect of the firm's strategy — the dealmaker who drove the M&A playbook and bet ₹50 crore on torching the brand. Yatin Shah runs the wealth business as CEO of 360 ONE Wealth, the operator closest to the relationships that are the firm's lifeblood. Eighteen years on, they are still flying the plane, and that continuity is itself a feature: in a business where clients buy trust, founder permanence is part of the product.

Look at what they own and the alignment becomes concrete. The broader promoter group holds a combined stake of around 6.24%. Bhagat directly holds about 0.33% of the company, while Yatin Shah holds roughly 2.39% — a position worth more than ₹1,850 crore at recent valuations.79 These are not founders who cashed out and stuck around for the title. A very large fraction of their personal net worth rides on the same share price their outside investors care about, which is precisely the configuration a long-term shareholder wants to see.

But the cap table is only half the alignment story. The compensation structure is the other half, and at first glance it looks shocking. Karan Bhagat's total annual compensation has run to an eye-watering ₹146.69 crore — roughly US$1.76 million in cash terms but far larger in headline rupee value once incentives are counted.7 That is a number that invites outrage until you read the fine print. Only about 20% of it is fixed salary. The other roughly 80% is variable — performance bonuses and stock options that pay out only if the business performs and the share price rises. In other words, the headline figure is not a salary; it is the realized value of a bet on the company that happened to pay off. Yatin Shah's compensation, around ₹75.93 crore, is structured on the same heavily performance-weighted logic.7 You can argue these numbers are large — they are — but you cannot argue they are unaligned. The executives get paid like owners because, structurally, that is what they are.

And the alignment runs far deeper than the corner office, which may be the single most important cultural fact about the firm. More than 30% of 360 ONE's employees participate in the employee stock ownership program. This is the firm's real answer to the RM arms race we described earlier — the brutal reality that trust is portable and star bankers walk. You cannot out-bid every rival on cash forever; it is a losing game that erodes margins. But you can make your best people owners, so that leaving means walking away from a stake that compounds with the firm. Junior employees who joined a decade ago and accepted stock are now, in many cases, multi-millionaires on paper. That is what converts a roster of free-agent relationship managers into something closer to a partnership — and it is why 360 ONE can credibly claim to hold its top talent through institutional ownership rather than endless salary escalation.

Then there are the backers, who bring more than money. Bain Capital, which entered through an affiliate, holds around 18.1% of the company — a large, sophisticated, patient owner whose presence signals institutional confidence and disciplines capital allocation.5 And in April 2025, in a move with strategic weight far beyond its size, UBS Group took a nearly 5% stake, paying roughly US$220 million, as part of a broader collaboration in which 360 ONE also acquired UBS's onshore Indian wealth portfolio.512 UBS is one of the largest wealth managers on earth, and the logic of the tie-up is a neat division of labor: 360 ONE brings unrivaled on-the-ground knowledge of Indian clients and Indian markets, while UBS brings a global product shelf, offshore booking capabilities, and relationships with international allocators that a Mumbai-born firm could spend a decade trying to replicate. For UBS, which had struggled to make its own onshore Indian wealth operation work, handing that business to a local champion and taking equity in it instead is a pragmatic reset. For 360 ONE, the value is the credibility a Swiss imprimatur confers when it sits across the table from a sovereign wealth fund or an international family office weighing where to route its India allocation — credibility that money alone cannot buy. The pilots own the plane; the backers extended the runway. Now we have to ask how defensible the whole aircraft really is.

VIII. Strategic Moats: 5 Forces & Hamilton's 7 Powers

Growth is not the same as durability. Plenty of fast-growing companies have no moat at all, and a long-term investor's real job is to figure out what, if anything, stops a competitor from simply copying the playbook. Let's run 360 ONE through two of the standard frameworks — Hamilton Helmer's 7 Powers and Porter's Five Forces — not as an academic exercise, but to locate exactly where the defenses are real and where they are thinner than the bulls admit.

Start with switching costs, which in wealth management at the top end are less a financial barrier than a near-insurmountable emotional and operational one. When 360 ONE manages a family's affairs, it is rarely just managing a portfolio. It is administering generational trusts, orchestrating succession planning across squabbling heirs, structuring the family's tax affairs, and — through 360 ONE Prime, the lending arm — holding the family's own securities as collateral against a customized loan. To switch providers, the family would have to unwind a decade of interlocking legal, tax, and credit structures, re-paper every trust, and re-explain its entire intergenerational psychodrama to strangers. People do not do this lightly, or often. The portfolio is portable; the estate is not. This is the deepest moat 360 ONE has, and it gets deeper the longer and more complex a relationship runs.

Next, network effects, which appear here in two distinct flavors. The indirect version comes from sheer scale: when you control assets in the lakhs of crores, you become the buyer that private deal-makers call first. 360 ONE can secure allocations to scarce private equity and private credit deals, and institutional-grade pricing on those deals, that a small wealth manager simply cannot access — and the better the deal flow, the more assets it attracts, which in turn improves the deal flow. The direct version is more human and arguably more powerful: through its wealth forums and "NextGen" programs, the firm has built an exclusive club where wealthy families meet each other, co-invest together, and quietly come to view membership as a marker of status. Leaving the platform means leaving the club, and the social cost of that is something no fee schedule captures.

Then the cornered resource, which is the talent itself. We have already met the firm's answer to the RM arms race — 30% employee ownership and a proprietary internal training pipeline that the company has built up to manufacture and retain advisors rather than perpetually rent them. The result is a pool of relationship managers who are both unusually productive and unusually sticky, held by golden handcuffs they helped forge. It is not a perfect moat — people can always leave — but it materially raises the cost and lowers the probability of the talent raids that periodically gut weaker competitors.

It is worth war-gaming the rivalry directly, because the three archetypes attack from different directions and a moat that stops one does little against another. Kotak comes from above and to the side — it cannot be out-spent or out-trusted on the balance sheet, and when a Kotak business-banking client sells his company, the wealth team is already in the building. 360 ONE's defense against the bank is specialization and independence: the pitch that a dedicated, conflict-light boutique will simply do a better, more bespoke job than a department-store bank with a thousand other priorities. Nuvama comes from below — winning the mass-affluent client at ₹5 crore who may one day be a ₹50 crore client, the same logical territory 360 ONE bought ET Money to defend. And the fintechs come from underneath everyone, with scale and slick technology but no answer to the human, high-touch demands of real wealth. The honest assessment is that 360 ONE's moats are deepest at the very top of the pyramid and thinnest as you move down toward the mass-affluent, which is exactly why the down-market funnel and the technology investments matter: they are not where the firm is strong, they are where it is exposed.

Now turn it around and apply Porter's lens, which is less flattering and therefore more useful. The bargaining power of buyers is genuinely high: UHNI clients are sophisticated, fee-conscious, and perfectly capable of playing one firm against another. 360 ONE's counter is to migrate them away from negotiable, transactional pricing and into recurring advisory arrangements and proprietary alternative products, where the value is bundled and the price is far harder to shop around. The threat of new entrants is more nuanced than the headlines suggest. Retail fintechs like Zerodha and Groww have enormous scale and technical sophistication, and the lazy assumption is that they will one day eat the wealth business from below. But they sell convenience and low cost to the mass market, and that is almost the opposite of what a billionaire wants. You cannot automate the 2 a.m. phone call about a family dispute or the bespoke structuring of a cross-border trust. Human trust at the top of the pyramid is the one thing a slick app cannot manufacture — at least not yet. And finally, the intensity of rivalry is simply fierce and will stay that way. The war against Kotak's bank-led machine and Nuvama's mass-affluent aggregator is fought every day on technology budgets, brand prestige, and the perennial poaching of star RMs. None of the moats above make 360 ONE immune to that fight; they just make it the kind of fight 360 ONE can keep winning. Whether it keeps winning is, in the end, an empirical question — which is what the investment debate comes down to.

IX. The Investment Thesis: Bull vs. Bear and the Critical KPIs

Every investment case eventually has to leave the realm of narrative and confront the question of what you would actually watch to know if it was working. For 360 ONE, the temptation is to drown in metrics — there are dozens — but three numbers carry most of the signal, and a disciplined owner of this business would track these and largely ignore the noise.

The first is the share of annual recurring revenue, or ARR, which currently sits at roughly 65% of the total. This is the cleanest single gauge of business quality. Recurring revenue is the sticky, predictable, asset-based fee income that arrives whether markets are euphoric or grim; the rest is transactional and commission-based, which spikes in good times and collapses in bad ones. The whole thesis of 360 ONE — the alignment revolution of 2008 brought to its logical conclusion — is the steady conversion of volatile transaction income into durable recurring income. If that 65% keeps climbing, the business is becoming more annuity-like and more valuable. If it stalls or slips, the quality of earnings is quietly deteriorating, no matter what the headline growth looks like.

The second is net new flows — the velocity of fresh client money entering the platform each quarter, stripped of the effect of market movements. This matters because total AUM is a flattering and misleading number: in a roaring bull market, assets swell even if not a single new rupee walks in the door, and in a crash they shrink even if the firm is winning every client it pitches. Net new flows cut through the market noise and tell you whether 360 ONE is actually gaining ground — whether the sales engine and the brand are pulling in capital on their own merits. It is the truest real-time read on competitive health.

The third is RM productivity and retention — most usefully captured as assets managed per senior relationship manager, where the firm runs at an industry-leading level of roughly ₹1,200 crore per senior RM. This single number folds together two of the most important things about the business at once: whether the firm is keeping its best people (retention) and whether those people are getting more productive on a stable platform (efficiency). Rising productivity per RM is the quantitative proof that the institutional model is working — that the firm is scaling assets faster than it is scaling headcount, which is the entire promise of turning artisanal wealth management into a platform.

A useful way to weight these three is to notice that they map onto the three things that can break a wealth manager: earnings quality (ARR share), competitive position (net new flows), and the talent base (RM productivity). A bull who only watches AUM and profit is watching the scoreboard; an owner who watches these three is watching the game itself. None of them requires the reader to compute anything — the firm reports them, and the trajectory over several quarters is what counts, not any single print.

With those gauges in hand, the bull case writes itself, and it is genuinely powerful. India is on a path that, if it holds, takes the economy toward a $10 trillion GDP and expands the UHNI population dramatically — toward something like half a million ultra-wealthy families. Even holding 360 ONE's market share constant, that tide alone could multiply its assets several times over; this is the "Indian Century" thesis, and 360 ONE is one of the purest listed ways to own it. Layered on top is platform leverage: the marginal cost of serving an additional rupee of assets, once the technology and the team are built, is close to zero, which means operating margins should expand structurally as scale grows — from the high-30s toward the mid-40s in percentage terms as AUM climbs toward ₹10 lakh crore. And then there is the optionality of the global Indian diaspora — a roughly $1 trillion pool of non-resident wealth that the firm's Dubai and Singapore offices, now turbocharged by the UBS partnership, are built to capture. Three independent growth vectors, all pointing the same way — and crucially, they are largely uncorrelated. The domestic financialization story does not depend on the diaspora story, and neither depends on margin expansion from platform leverage; any one of the three failing to deliver does not necessarily sink the others. For a long-term owner, that diversification of upside is itself a form of risk reduction, the mirror image of the diversified-downside worry in the bear case.

But a thoughtful owner gives the bear case equal time, because each of these strengths has a shadow. The first and most serious is margin compression. Indian advisory fees of 100-plus basis points are luxuriously high by global standards; in mature developed markets, the same services fetch 50 to 70 basis points. As the Indian market deepens and competition intensifies — particularly with a price-insensitive bank like Kotak willing to use wealth as a loss-leader — it is entirely plausible that the premium yield erodes toward developed-market levels. If yields compress faster than assets grow, revenue stalls even as AUM rises. The second is the regulatory hammer. The firm's most lucrative products — PMS and AIF structures, and the high-margin alternates engine — sit squarely in SEBI's field of vision. A tightening of fee caps, a clampdown on carry economics, or an outright ban on remaining trail commissions could compress the very pools where pricing power is strongest. The alignment-first model was partly built to stay ahead of the regulator, but no one stays ahead forever. The third is the most human: key-person risk. For all the talk of institutionalizing trust, a meaningful share of the firm's credibility, its deal flow, and its relationships still runs through Karan Bhagat's personal network. The 30% ESOP culture is the explicit hedge against this, but it is a hedge, not an elimination. A fourth, slower-burning risk deserves a mention precisely because it is easy to wave away: the fintechs may not stay confined to the mass market forever. Today the assumption that an app cannot serve a billionaire is correct, but the children of today's UHNI clients are digital natives who may not share their parents' need for the 2 a.m. phone call, and the technology for sophisticated, low-cost advice keeps improving. The moat at the top of the pyramid is real, but moats are defended, not inherited, and a generation from now the definition of "high-touch" may look very different. That 360 ONE is investing in its own technology and bought a wealthtech funnel suggests its leadership takes this seriously rather than dismissing it.

The bull and bear cases are not really in conflict; they are a bet on which force — the rising Indian tide or the maturing-market squeeze — proves stronger over the next decade.

X. Epilogue

Return, for a moment, to that office in early 2008 — the screens bleeding red, the foreign banks in retreat, two young men with a contrarian idea and no clients, opening for business into the worst financial storm in living memory. From that improbable beginning to an independent, pure-play powerhouse valued north of ₹42,000 crore is an arc that almost didn't happen, and that says something about the difference between timing the market and understanding it. Bhagat and Shah didn't survive 2008 in spite of the crisis; they used it — to hire the talent nobody else wanted, to win the clients nobody else was serving, and to build, from the start, a model honest enough to last.

The comparison to Goldman Sachs is flattering and partly apt — the pure-play focus, the advisory-first DNA, the alternates engine, the ambition to be the firm that serious capital calls first. But it is worth being honest about the ways it is also a stretch, because the gap is where the work remains. Goldman's franchise survives the departure of any individual; 360 ONE's still leans, more than its leadership would like, on a founder's personal Rolodex. Goldman operates across dozens of markets and decades of crises; 360 ONE has been independent only since 2019 and has yet to be truly tested by a prolonged bear market as a standalone public company. The aspiration is the right one — it points the firm toward institutional durability rather than personal heroics — but aspiration is not arrival, and the distance between them is precisely what the next decade will measure.

The question that hangs over the next decade is the one the firm itself keeps asking: can 360 ONE truly become India's Goldman Sachs — the default gateway through which both Indian wealth matures and global capital enters the country? The pieces are in place. The alternates engine throws off the kind of capital-light, performance-linked cash flow that the great franchises are built on. The platform has the scale to command deal flow. The brand has been deliberately polished for the global stage, and the UBS partnership hands it a passport. The answer ultimately rests on two transitions running in parallel. The first is internal to India — whether the great migration of household wealth from gold and land into financial assets, the so-called Amrit Kaal or golden era, unfolds as the bulls expect, and whether 360 ONE remains the firm the newly liquid entrepreneur calls first. The second is external — whether its overseas offices can become the primary on-ramp for the trillion-dollar diaspora and the international allocators eyeing India. Get both right, and the firm born in the 2008 storm becomes a permanent fixture of the Indian financial landscape. Either way, it remains one of the most instructive case studies in how a stubbornly un-scalable business was, against the odds, made to scale.

References

-

360 ONE WAM FY26 Profit Rises 20.7% To ₹1,225 Crore; Q4 Revenue Grows 18.5% To ₹780 Crore — Free Press Journal, 2026-04-21 ↩↩↩

-

Bain Capital backed 360 One WAM to acquire B&K Securities for $205 million — Business Standard, 2025-01-27 ↩↩

-

Hottest Young Executive 2015: IIFL Wealth's Karan Bhagat — Business Today, 2015-03-06 ↩↩↩

-

IIFL Wealth & Asset Management is now 360 ONE — Cafemutual, 2022-11-15 ↩↩

-

Board of 360 ONE WAM approves collaboration with UBS AG — Business Standard, 2025-04-22 ↩↩↩

-

Wealth management firm 360 ONE acquires ET Money for Rs 366 crore — Business Standard, 2024-06-12 ↩

-

For Karan Bhagat of 360 ONE WAM it's all about industry dominance — Business Today, 2026-04-03 ↩↩↩

-

IIFL Wealth Finance buys L&T Capital Markets for Rs 230 cr — Business Standard, 2020-04-24 ↩↩↩

-

360 ONE WAM Q4 FY26 Results: AUM ₹7.11 Lakh Crore, Dividend ₹6/Share — Univest, 2026-04-21 ↩

-

360 ONE WAM × UBS Strategic Collaboration — 360 ONE Newsroom, 2025-04-22 ↩

-

360 ONE Asset — Asset Management Services (PMS, Mutual Fund & Alternatives) — 360 ONE ↩

-

360 One acquires Times Internet's ET Money for Rs 366 crore — Storyboard18, 2024-06-12 ↩

-

360 ONE Asset closes fifth private credit fund with $400m commitments — Alternative Credit Investor, 2026-03-09 ↩

-

360 ONE Asset Launches ₹4,000 Cr Secondary Fund to Provide Liquidity Solutions — 360 ONE Newsroom ↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube