Yü Group: The Digital Insurgent of British Energy

I. Introduction: The Survival of the Fittest

Picture this: it is the autumn of 2021, and the British energy market is in freefall. Natural gas prices have surged to levels not seen in a generation. The wholesale cost of electricity has tripled. One by one, the dominoes begin to fall. Avro Energy, with its 580,000 customers, goes first. Then Green. Then PFP Energy. Then Symbio. By the time the dust settles in early 2022, twenty-nine energy suppliers have collapsed in barely twelve months, leaving more than four million customers stranded and forcing Ofgem, the industry regulator, into an unprecedented scramble to redistribute accounts through its Supplier of Last Resort process.

This was not a downturn. This was an extinction-level event.

And yet, in a modest office park in Nottingham, a company with fewer than 300 employees was not just surviving—it was feasting. Yü Group PLC, an independent business energy supplier that most City analysts had written off three years earlier, watched its revenues climb past 279 million pounds in 2022 and then rocket to 460 million the following year. Profits surged. The share price, which had been trading in the low hundreds of pence, began a relentless march toward all-time highs. In an industry graveyard, Yü Group was building a cathedral.

How did a company that nearly died from a spreadsheet error in 2018 become the most resilient independent energy supplier in Britain? The answer is a story about founder tenacity, disciplined risk management, and the transformative power of technology in what might be the least glamorous industry on earth. It is also a story about what happens when a founder with 50 percent ownership of a public company decides that survival is not optional.

The thesis is straightforward: Yü Group transformed itself from a traditional commodity reseller—buying wholesale gas and electricity and marking it up for small businesses—into what management calls a "Digital Utility," a technology-first platform that uses proprietary software and disciplined hedging to undercut the legacy giants on price, speed, and service. The company's journey from nursing homes to the London Stock Exchange, through the accounting crisis that nearly destroyed it, and into the current era of rapid profitable growth is one of the most underappreciated turnaround stories in British small-cap history.

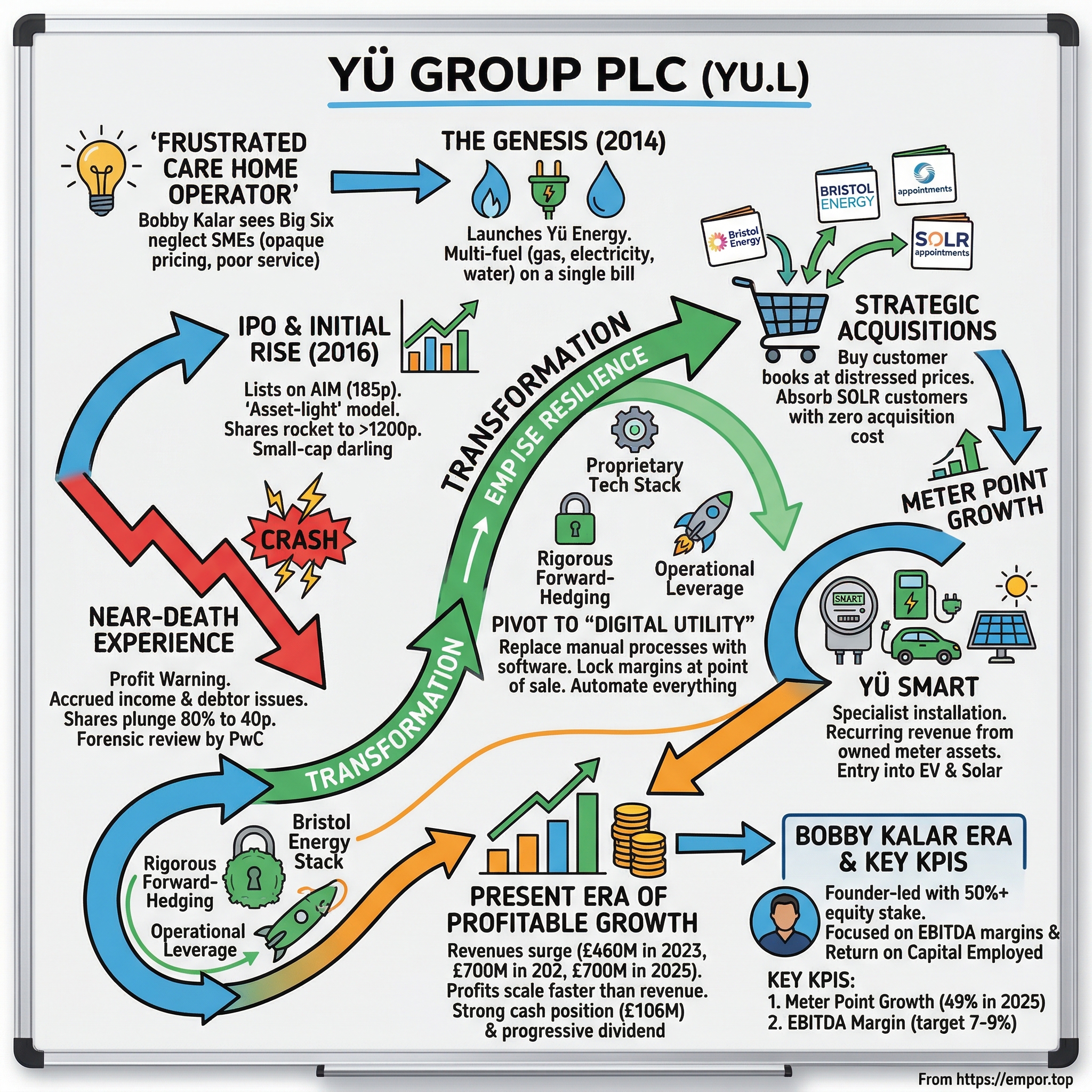

To understand where Yü Group is going, we need to start where it began: with a frustrated care home operator in the East Midlands who decided that the Big Six energy companies were ripe for disruption.

II. The Genesis: Frustration as a Business Plan

Baljit "Bobby" Kalar never planned to become an energy entrepreneur. Born and raised in the Midlands, he studied Electrical and Electronics Engineering at the University of Derby and launched his career at Marconi PLC, the venerable British electronics firm. He was good at it—technically sharp, commercially minded, restless. He moved to London to work for COLT Telecommunications, where he led a team of engineers building the infrastructure behind the London congestion charge scheme for Transport for London. It was serious, complex work, and it gave him a taste for running large projects with real-world consequences.

But Kalar was not the type to spend decades climbing a corporate ladder. In 2002, with a loan from his parents, he did something audacious: he bought a care home. At 26, he became the youngest care home owner in Britain. Over the next decade, he built a portfolio of four homes generating more than four million pounds in annual revenue. It was a grinding, operationally intense business—staffing, regulation, compliance, the emotional weight of caring for elderly residents. But it taught him how to run a real company, manage cash, and deal with the thousand small fires that define small business ownership.

It also taught him something else: how badly the Big Six energy companies treated their SME customers.

The British energy market in the early 2010s was dominated by six vertically integrated giants—British Gas (Centrica), EDF Energy, E.ON, SSE, Scottish Power, and npower. These companies owned the power stations, the gas fields, the distribution networks, and the retail arms that sold energy to homes and businesses. For large corporate customers, they offered bespoke deals with dedicated account managers. For residential consumers, there was at least some price transparency and switching competition. But for the vast middle ground—small and medium enterprises like Kalar's care homes—the experience was somewhere between neglect and hostility. Opaque pricing, poor service, long contract terms, and a general attitude that SMEs should be grateful for whatever they got.

Kalar experienced this firsthand. He found the electricity sector "antiquated and inefficient," as he later told MoneyWeek. The billing was often wrong. The customer service was nonexistent. And the prices bore little relationship to the actual cost of wholesale energy. He saw a gap: millions of British businesses were being overcharged and underserved, and nobody was building a modern, technology-driven supplier specifically for them.

In 2013, he sold his care home portfolio and began planning what would become Yü Energy. The timing was deliberate. Deregulation had opened the energy supply market to independent entrants, and the technology to manage complex energy portfolios—smart metering, automated billing, online account management—was finally becoming affordable. Kalar's insight was that the consumer energy market was a "race to the bottom" where razor-thin margins and price comparison websites made profitability nearly impossible. The B2B market, by contrast, offered higher margins, stickier customers, and less price sensitivity—businesses cared more about reliability and service quality than saving a few pounds on their monthly bill.

Yü Energy launched in 2014 with a tiny team in Nottingham and a simple proposition: gas, electricity, and water on a single bill, with transparent pricing, digital account management, and actual human beings who answered the phone. The "multi-fuel" approach was the key differentiator. Instead of dealing with three separate suppliers, three separate bills, and three separate customer service nightmares, a pub owner or dental practice or care home could consolidate everything with Yü. It sounds obvious in retrospect, but in an industry built on siloed legacy systems, it was genuinely novel.

What Kalar built, in essence, was not an energy company. It was a technology company that happened to sell energy. And the market was about to reward him for it—before very nearly destroying him.

III. The IPO and the First Inflection Point

On March 17, 2016—barely two years after founding—Yü Group listed on the AIM market of the London Stock Exchange. The IPO was priced at 185 pence per share, valuing the company at 26 million pounds. The offering was significantly oversubscribed. Bobby Kalar sold approximately 40 percent of his personal holding in the placing but retained a controlling 52 percent stake, raising 7.5 million pounds in gross proceeds to fuel growth. Shore Capital acted as nominated adviser and broker.

The narrative that Kalar sold to investors was compelling in its simplicity. Yü Group was an "asset-light" energy supplier. It owned no power stations, no gas fields, no pipelines. It was a pure sales and technology engine that bought wholesale energy, marked it up, and delivered it to business customers through a modern digital platform. The capital requirements were minimal. The addressable market—millions of British SMEs collectively spending billions on energy—was enormous. And the incumbents were slow, complacent, and burdened with legacy infrastructure.

Investors loved it. The stock became a small-cap darling. Revenue was doubling year over year as Kalar's sales team signed up thousands of businesses across England and Wales. The share price climbed from the 185 pence IPO to 300, then 500, then past 800 pence. Analysts wrote breathless notes about the "asset-light growth story" and the potential for Yü to take meaningful market share from the Big Six.

By early 2018, shares were trading above 1,200 pence—a sixfold increase from the IPO price in less than two years. Bobby Kalar, still holding more than half the equity, was sitting on a paper fortune. The company seemed unstoppable.

But beneath the surface, something was very wrong.

The problem was one that plagues every fast-growing energy supplier: the gap between when you buy energy and when you get paid for it. Energy companies purchase wholesale gas and electricity months or even years in advance, supply it to customers over the contract period, and then bill for it—often in arrears, often based on estimated rather than actual meter readings. This creates a large and growing balance of "accrued income"—revenue that the company has recorded on its books but has not yet invoiced or collected.

For a company growing as fast as Yü, the accrued income balance was expanding rapidly. And the systems to track it—to reconcile what had been bought, what had been consumed, and what had been billed—were struggling to keep up. The company was, in effect, flying a jet while building it. The sales engine was working beautifully. The back office was held together with manual processes, spreadsheets, and hope.

In the summer of 2018, the cracks began to show. And in October, the whole edifice came crashing down.

IV. The Near-Death Experience: The 2018 Crash

The profit warning landed on a Wednesday in October 2018, and it was devastating.

An internal review had identified what the company euphemistically called "significant non-cash adjustments" in three areas: aged accrued income totalling 4.2 million pounds for the year ended December 2017 and 4.3 million in the first half of 2018; higher-than-expected trade debtor impairments, meaning customers who simply were not going to pay; and gross margin compression, indicating that the actual margins achieved on energy sold were meaningfully below what had been projected.

The combined impact: a 10 million pound reduction in profitability versus market expectations. What analysts had been modelling as a profitable, rapidly growing company was, in fact, loss-making.

The stock market's reaction was swift and brutal. Shares opened at 580 pence the day before the announcement. By mid-morning on the day of the warning, they were trading at 117 pence—an 80 percent collapse in a single session, making Yü Group the largest faller on the entire London Stock Exchange that day. In the weeks that followed, the selling continued. By December 21, 2018, the stock hit an all-time low of 40 pence per share. A company that had been valued at over 170 million pounds at its peak was now worth less than 6 million.

The fallout was comprehensive. PricewaterhouseCoopers was brought in for a forensic review of the accounts. The board scrambled to strengthen financial controls. Paul Rawson, a qualified chartered accountant who had spent years at KPMG before moving into the energy industry, was appointed CFO in September 2018—essentially parachuted in to stop the bleeding. The company's credibility with the City was in tatters.

For many small-cap companies, this would have been the end. The playbook is well established: profit warning, board crisis, loss of banking facilities, administration, liquidation. The investors lose their money, the employees lose their jobs, and the story ends with a cautionary tale about the dangers of fast growth without adequate controls.

But Yü Group had something that most small caps do not: a founder-CEO with a controlling stake who refused to give up.

Bobby Kalar still held roughly half the equity. At the post-crash share price, his stake was worth less than three million pounds—a fraction of the paper fortune he had held months earlier. He could have sold. He could have walked away, blamed the CFO, blamed the systems, blamed the market. Instead, he doubled down.

This is the moment that defines companies. Most die here. The ones that survive do so because the people in charge make a conscious decision to use the crisis as a catalyst for transformation rather than an excuse for surrender. Kalar chose transformation.

The decision was not purely emotional. Kalar understood something that the market, in its panic, had overlooked: the underlying business was real. Yü Group had genuine customers buying real energy. The multi-fuel proposition worked. The B2B market opportunity was as large as ever. What had failed was not the strategy—it was the execution. Specifically, the systems and processes for tracking accrued income, managing credit risk, and reconciling billing had not kept pace with the company's growth.

The fix was clear, even if it was painful: rebuild the entire operational backbone of the company from scratch. Automate everything that could be automated. Replace manual processes with software. Build a proprietary technology stack that could handle the complexity of energy portfolio management at scale. And above all, institute a hedging discipline so rigorous that the company would never again be exposed to the kind of margin surprises that had nearly killed it.

The crisis of 2018 was not the end of Yü Group. It was the beginning of the company that exists today.

V. The Pivot: Becoming a "Digital Utility"

The transformation that followed the 2018 crash was not a cosmetic rebrand. It was a fundamental re-engineering of how the company operated.

Before the crisis, Yü Group's back office looked like most small energy suppliers: a patchwork of spreadsheets, manual data entry, and legacy billing systems stitched together with custom workarounds. Customer onboarding required phone calls, paper contracts, and days of back-and-forth. Meter reading reconciliation was a quarterly exercise conducted largely by hand. The accrued income balance—the gap between what had been supplied and what had been billed—was tracked in spreadsheets that grew more unwieldy with every new customer.

Think of it like running an e-commerce business where you ship products immediately but only figure out what to charge customers three months later, using estimates based on what similar customers ordered last year. The potential for error is enormous, and it compounds with scale.

Management set about replacing this entire infrastructure with a proprietary, automated technology stack. The goal was what they called "Digital by Default": a platform where businesses could onboard entirely online, receive automated quotes in seconds rather than days, manage their accounts through a self-service portal, and have their billing reconciled continuously rather than quarterly. Live chat advisers replaced call centre queues. Automated data flows replaced manual meter reading reconciliation.

The results were transformative. Cost-to-serve dropped as automation replaced headcount. Billing accuracy improved dramatically, shrinking the accrued income balance that had caused the 2018 crisis. Customer onboarding accelerated, meaning the sales team could sign up more businesses without a proportional increase in back-office staff. The company was building what tech investors call "operational leverage"—the ability to grow revenue without growing costs at the same rate.

But the technology transformation was only half the story. The other half was hedging.

To understand why hedging matters so much in the energy supply business, consider the basic economics. An energy supplier signs a contract with a business customer to supply electricity at, say, 20 pence per kilowatt-hour for two years. The supplier then needs to purchase that electricity on the wholesale market. If wholesale prices are 15 pence when the contract is signed, the supplier locks in a 5 pence margin. But if wholesale prices spike to 25 pence before the supplier has purchased the energy, the supplier is now losing 5 pence on every unit delivered. Multiply that by millions of kilowatt-hours across thousands of customers, and you can see how quickly an unhedged energy supplier can go bankrupt.

This is exactly what happened to the 29 suppliers that collapsed in 2021. Many of them, particularly the smaller consumer-facing companies, had adopted a strategy of buying energy on the spot market—essentially gambling that wholesale prices would remain stable or fall. When gas prices tripled, their business models imploded overnight.

Yü Group took the opposite approach. Under the discipline imposed after the 2018 crisis, the company adopted a rigorous forward-hedging strategy. When a customer signed a contract, Yü immediately purchased the corresponding wholesale energy for the full contract term. The margin was locked in at the point of sale. No speculation. No spot market exposure. No hope-and-pray.

The initial hedging arrangement was with SmartestEnergy, a subsidiary of Japanese trading house Marubeni. This worked well during the calmer market conditions of 2019 and 2020. But when wholesale prices went haywire in 2021 and 2022, the cash collateral requirements under the SmartestEnergy arrangement ballooned. At one point, Yü had posted nearly 50 million pounds in collateral—cash that was locked up and unavailable for growth.

The solution came in the form of what management described as a "transformational" new hedging facility with Shell Energy Europe. The arrangement, structured as an initial five-year term, gave Yü direct access to Shell's gas and power trading infrastructure without the punishing cash collateral requirements. When the transition completed, 52.25 million pounds of previously lodged collateral was released back to the company—a massive boost to working capital that funded the next phase of growth.

Think of the Shell arrangement like a small retailer getting a credit line from a major wholesaler. Instead of paying cash up front for every shipment, Yü could now hedge its customer book through Shell's balance sheet, freeing up capital to invest in growth while maintaining the same disciplined approach to risk management.

The third pillar of the transformation was acquisitive growth—but with a distinctive twist. Rather than buying whole companies, with their messy balance sheets, legacy systems, and cultural baggage, Yü focused on buying customer books.

The template was set in August 2020 with the acquisition of Bristol Energy's B2B customer portfolio. Bristol Energy was a wholly-owned subsidiary of Bristol City Council that had been struggling financially. Through a competitive tender, Yü acquired approximately 4,000 meter points—increasing its own meter base by roughly 40 percent—for just 1.24 million pounds in cash plus assumed receivables and deferred payments. The total consideration was barely two million pounds for a customer book generating meaningful recurring revenue. Bristol Energy's B2B staff were retained as part of the deal, providing institutional knowledge and customer relationships.

A few months later, Yü picked up the business customer book of an undisclosed Midlands-based energy group for a mere 200,000 pounds, adding 400 meter points and roughly three million pounds in annual revenue.

Then came the bonanza of the 2021 crisis. When suppliers collapsed, Ofgem appointed Suppliers of Last Resort to absorb their customers. In November 2021, Yü was appointed SOLR for Ampoweruk, inheriting 8,158 predominantly business electricity meter points—a 38 percent increase in its portfolio overnight, with an immediate revenue uplift of more than 7.5 million pounds per month. In February 2022, further SOLR appointments for Whoop Energy and Xcel Power added another 675 meter points.

The economics of this strategy were extraordinary. Through a combination of book acquisitions at distressed prices and SOLR appointments that essentially came with zero acquisition cost, Yü was scaling its customer base at a fraction of the cost that organic marketing would have required. While competitors were spending hundreds of pounds per customer acquisition through brokers and advertising, Yü was picking up thousands of customers for pennies on the pound—or, in the case of the SOLR appointments, for free.

This was capital allocation at its finest: deploying cash opportunistically during a market panic, acquiring productive assets at distressed valuations, and integrating them onto a modern technology platform that could handle the additional volume without a proportional increase in costs. It was, in essence, the Warren Buffett playbook applied to British energy supply.

VI. Current Management and the "Bobby Kalar" Era

To understand Yü Group today, you have to understand its centre of gravity, and that centre is Bobby Kalar.

In an era of professional CEOs parachuted in by private equity firms, hired guns who optimize for two-year bonus cycles and then move on, Kalar is a throwback. He founded the company. He nearly lost it. He rebuilt it. And he still owns just over 50 percent of the equity—8.7 million shares out of 17.2 million in issue. At the current share price of approximately 1,790 pence, that stake is worth roughly 156 million pounds. This is not a CEO who is going to make a short-term decision to juice the stock price. His incentive structure is perfectly aligned with long-term shareholders because he is, by a wide margin, the largest long-term shareholder.

Kalar's management philosophy has evolved significantly since the early days. The pre-2018 Kalar was a sales-driven entrepreneur who built a fast-growing business by sheer force of will and commercial instinct. The post-2018 Kalar is a more disciplined operator focused on EBITDA margins, return on capital employed, and the kind of boring-but-essential metrics that separate sustainable businesses from flash-in-the-pan growth stories. He has spoken publicly about the 2018 crisis as a formative experience—not something to be ashamed of, but something that forged the systems and discipline that allowed the company to thrive when competitors were going bust.

The leadership team around Kalar has been strengthened significantly. Andy Simpson joined as Group Finance Director in February 2025 and was appointed to the board as CFO effective September 2025, succeeding Paul Rawson. Simpson brings serious credibility: he is a qualified CIMA accountant with a degree in Business Management, seven years as Finance Director at BT Group, and prior CFO roles at Origin and ITS Technology. His background in high-growth utility businesses makes him a natural fit for a company that is scaling rapidly while trying to maintain financial discipline.

Rawson, who was brought in during the 2018 crisis as the firefighter CFO, transitioned to a non-executive director role—a smooth succession that preserved institutional knowledge while bringing in fresh operational capability. Andrew Hughes serves as Group COO, overseeing the day-to-day operational machine.

The cultural transformation has been equally significant. Pre-2018, Yü was a sales-led organization where the heroes were the people signing up the most customers. Post-2018, the company pivoted to what might be called a "tech-and-risk-led" culture, where the heroes are the people building systems that prevent billing errors, improve hedging accuracy, and reduce cost-to-serve. The opening of a UAE office for technology development and AI automation signals the direction of travel: this is a company that views technology investment not as a cost centre but as its primary competitive weapon.

The concept of "operational leverage" pervades everything. Management's explicit goal is to grow revenue without proportionally growing headcount. In a commodity business where the product itself is undifferentiated—a kilowatt-hour of electricity is a kilowatt-hour of electricity, regardless of who sells it—the only sustainable advantage comes from delivering that commodity more efficiently, more accurately, and at lower cost than the competition. That requires technology. And technology scales in a way that human beings do not.

The board is in a transitional phase. Both John Glasgow and Tony Perkins, longstanding non-executive directors, announced their intentions to retire during 2026, with successor searches underway. This is worth monitoring: the quality of independent oversight on the board matters, particularly for a company where the founder-CEO holds a controlling stake. Strong non-executives provide the checks and balances that prevent an owner-operator from making unchallenged decisions—a dynamic that becomes more important as the company grows larger and more complex.

VII. The "Hidden" Business: Yü Smart

Tucked inside Yü Group's financial statements, easy to overlook amid the headline revenue and profit numbers, sits a business that may ultimately prove more valuable than the commodity supply operation that generates most of the top line.

Yü Smart began when the company integrated Magnum Utilities, a specialist smart meter installation business, bringing over a team of 28 technicians and engineers who began trading under the Yü Smart brand as a wholly-owned subsidiary. Today, the operation has grown to approximately 85 employees and generates estimated revenue of around 15.6 million pounds.

The services span the full spectrum of energy infrastructure: installation and maintenance of SMETS2 smart electricity and gas meters, EV charging point installation, revenue protection (identifying and addressing energy theft or meter tampering), emergency call-outs, and data flow management. It is, in essence, the "last mile" of the energy system—the physical hardware that sits between the grid and the customer.

Why does this matter so much? Consider the information asymmetry that has plagued the energy supply business for decades. Traditional "dumb" meters are read manually, often quarterly, by a person with a clipboard. Between readings, the supplier estimates consumption based on historical patterns and bills accordingly. This creates the accrued income problem that nearly destroyed Yü in 2018: the gap between estimated and actual consumption can be enormous, and it compounds over thousands of customers and multiple billing periods.

Smart meters eliminate this problem. They transmit consumption data in real time—every half hour—directly to the supplier. No estimates. No reconciliation surprises. No accrued income black holes. For an energy supplier, smart meter coverage is not just a regulatory box to tick; it is the foundation of accurate billing, reliable cash flow forecasting, and customer trust.

By installing its own smart meters through Yü Smart rather than relying on third-party contractors, Yü Group captures multiple layers of value. First, the installation itself is a revenue-generating service. Second, the company gets proprietary access to granular consumption data that improves billing accuracy and reduces bad debt. Third, the ongoing maintenance and data management create a recurring revenue stream that is far stickier than the underlying energy supply contract—even if a customer switches suppliers, the meter hardware remains.

In 2025, Yü Smart installed 16,400 smart meter units. Management acknowledged this was disappointing, down from 22,900 in 2024, likely reflecting supply chain constraints and scheduling challenges rather than any fundamental shift in demand. More importantly, the index-linked annualised recurring revenue from owned meter assets reached 2.2 million pounds, up from 1.3 million the prior year—a 69 percent increase in high-quality, inflation-protected revenue.

The future optionality embedded in Yü Smart is significant. EV charging infrastructure is an obvious growth vector: as British businesses electrify their vehicle fleets, they need charging points installed, maintained, and managed. Solar panel maintenance for commercial rooftops is another. These are high-margin, recurring-revenue services that leverage the same field engineering workforce and customer relationships that Yü Smart has already built.

The strategic parallel is worth noting. In the same way that Amazon built AWS as an internal infrastructure capability that eventually became a standalone profit engine, Yü Smart started as an in-house service supporting the core energy supply business. Its evolution into a potentially standalone business—one that could serve third-party energy suppliers and commercial property managers, not just Yü's own customers—represents a valuable call option on future growth that the market may not be fully pricing today.

The company reports through three segments: Retail (the core energy supply business), Smart (the installation and services business), and Metering Assets (the ownership and rental of smart metering hardware). The three-segment structure provides unusual transparency into the economics of each activity and allows investors to track the growing contribution of the higher-margin infrastructure businesses relative to the commodity supply operation.

VIII. Framework Analysis: 7 Powers and 5 Forces

To assess whether Yü Group's competitive position is durable or merely cyclical, it is worth running the business through two rigorous analytical frameworks.

Hamilton Helmer's "7 Powers" framework identifies the structural advantages that allow a company to sustain above-normal returns over time. Not every company possesses all seven, and most possess none. Yü Group's case is instructive because its advantages are subtle—they do not announce themselves the way a patent portfolio or a network effect might—but they are real.

The most evident power is Process Power: the proprietary digital onboarding and billing system that Yü has built over the years since the 2018 crisis. When a business customer requests a quote from Yü, the system can generate one in seconds. When the same customer approaches one of the Big Six incumbents, the process typically takes days, involves multiple handoffs between departments, and frequently results in errors. This is not because the Big Six are staffed by incompetent people; it is because their systems were designed in the 1990s for a regulated monopoly environment and have been patched, extended, and band-aided for three decades. The accumulated technical debt in their billing and CRM platforms is staggering. Yü, having rebuilt from scratch, operates on a modern stack that is faster, cheaper, and more accurate. This advantage compounds over time: every process improvement Yü makes to its own system widens the gap with incumbents who are still trying to maintain legacy mainframes.

The second power is Counter-Positioning: Yü has adopted a business model that incumbents cannot replicate without dismantling their existing operations. The Big Six are vertically integrated behemoths that own generation assets, distribution networks, and retail operations. Their organisational structures, incentive systems, and regulatory obligations are designed around this integrated model. Pivoting to an asset-light, digital-first approach would require them to strand billions of pounds in physical infrastructure and retrain or replace thousands of employees. They know Yü's model is better for serving SME customers. They simply cannot adopt it without destroying value elsewhere in their portfolios. This is the essence of counter-positioning: the incumbent's rational response to the entrant's strategy is to do nothing, because the cost of imitation exceeds the cost of concession.

The third, more debatable power is Cornered Resource: Bobby Kalar himself. A founder with deep SME empathy—he has been the target customer—combined with hard-nosed energy trading discipline and a controlling equity stake is genuinely difficult to replicate. Founder-led businesses in regulated industries carry specific advantages: the willingness to invest through downturns, the institutional memory that comes from having nearly failed, and the alignment of incentives that comes from having most of your net worth tied up in the company. Whether this constitutes a true "cornered resource" in Helmer's framework or merely a temporary advantage tied to a single individual is a matter of debate. It is certainly a factor that differentiates Yü from the professionally managed competitors on either side.

Porter's Five Forces paint a more nuanced picture of the competitive landscape.

Rivalry is intense. The UK B2B energy supply market includes Drax Group (through its Haven Power and Opus Energy brands, supplying energy to some 250,000 businesses), EDF Energy, British Gas Business, E.ON Next Business, TotalEnergies, and a roster of independents including CNG, Pozitive Energy, D-ENERGi, and Crown Gas and Power. Yü's 3.5 percent market share, up from 2.7 percent the prior year, is growing but still modest. The competitive dynamic is one of a nimble digital insurgent picking off the slower, less responsive incumbents at the margins—winning customers not on price alone but on the combination of price, speed, and service quality.

Bargaining Power of Suppliers is high. Wholesale gas and electricity markets are global commodity markets where no single buyer has pricing power. Yü is a price-taker. However, the Shell Energy hedging facility partially mitigates this exposure by providing structured access to wholesale markets without the punishing collateral requirements that constrain smaller competitors. The facility is a genuine competitive advantage: many independent suppliers lack the creditworthiness or scale to negotiate comparable arrangements.

Bargaining Power of Buyers is moderate. SME customers are price-sensitive but also value convenience, reliability, and the multi-utility proposition. The switching costs are not trivial—changing energy supplier involves paperwork, potential billing disruptions, and the hassle of establishing new relationships. Yü's strategy of bundling gas, electricity, and water on a single bill increases switching costs by making the proposition more integrated and harder to unbundle. A customer might switch electricity suppliers on price, but switching all three utilities simultaneously is a much bigger decision.

Threat of New Entrants is real but diminishing. The 2021 crisis raised the bar for entry dramatically. Ofgem has tightened licensing requirements, increased financial resilience standards, and made it harder for undercapitalised newcomers to enter the market. The survivors—those who navigated the crisis without collapsing—now benefit from a regulatory environment that favours scale, financial strength, and proven operational capability. Yü's growing scale and its Shell hedging facility create barriers that a startup would struggle to replicate.

Threat of Substitutes is the most intriguing force. In the near term, there are no substitutes for grid-supplied gas and electricity. But the medium-term trajectory of the energy market—on-site solar generation, battery storage, demand response programs, peer-to-peer energy trading—could eventually erode the traditional supply model. Yü Smart's positioning in EV charging and solar maintenance is, in part, a hedge against this substitution risk: if businesses increasingly generate their own energy, Yü wants to be the company installing and maintaining the hardware that enables it.

IX. The Playbook: Lessons for Founders and Investors

The Yü Group story offers three lessons that transcend the specifics of British energy supply and speak to broader principles of business building and investing.

Lesson One: Technology as a Moat in Boring Industries. There is a persistent bias in venture capital and public market investing toward "exciting" technology sectors—artificial intelligence, autonomous vehicles, quantum computing. The reality is that some of the most durable competitive advantages are built by applying modern technology to industries that nobody thinks about. Energy supply is not glamorous. Billing reconciliation is not going to feature in a TED talk. But when you are a 10x better technology company operating in an industry where the incumbents are running on 1990s mainframes, the advantage is enormous and widening. Yü's digital onboarding, automated billing, and real-time data management are not breakthrough innovations in an absolute sense—a fintech or SaaS company would consider them table stakes. But in the context of British energy supply, they are genuinely transformative, and they create the kind of structural cost advantage that compounds over time.

Lesson Two: The Value of the Near-Death Experience. The 2018 crash was, in retrospect, the best thing that ever happened to Yü Group. Not because the accounting problems were trivial—they were genuinely serious, and the stock's 80 percent collapse was a rational response to a real loss of credibility. But because the crisis forced management to build the systems, processes, and risk management discipline that allowed the company to thrive during the 2021 market meltdown. If Yü had continued growing at breakneck speed without the 2018 wake-up call, it almost certainly would have been among the 29 suppliers that collapsed when wholesale prices spiked. The crisis imposed the discipline that survival required. This is a pattern that recurs across business history: the companies that survive existential threats often emerge stronger than those that never face them, because the threat forces the kind of root-and-branch transformation that comfortable companies never undertake.

Lesson Three: Capital Allocation During Market Panic. Yü Group's acquisitive strategy—buying customer books at distressed prices during the 2020-2022 period and absorbing SOLR-appointed customers at zero cost—was a masterclass in opportunistic capital deployment. The Bristol Energy book acquisition, at roughly 1.24 million pounds for 4,000 meter points, worked out to approximately 310 pounds per customer. Compare this to the cost of organic customer acquisition through brokers and marketing, which industry estimates place at several hundred to over a thousand pounds per customer, and the value creation is obvious. The SOLR appointments were even better: thousands of customers for effectively zero acquisition cost, with the additional revenue uplift flowing straight to the bottom line. This is the energy supply equivalent of buying foreclosed properties during a housing bust—ugly at the time, enormously profitable in retrospect.

The financial trajectory tells the story. From a revenue base of 279 million pounds in 2022, the company grew to 460 million in 2023 (up 65 percent), 646 million in 2024 (up 40 percent), and approximately 700 million in 2025 (up 8 percent, reflecting a normalisation of growth from the extraordinary post-crisis surge). More importantly, profitability scaled faster than revenue: adjusted EBITDA went from 7.9 million pounds in 2022 to 42.6 million in 2023, 48.8 million in 2024, and 51 million in 2025. Pre-tax profit followed a similar trajectory, reaching 49 million in 2025.

The cash position tells an equally compelling story. Yü ended 2025 with 106 million pounds in cash, up 21 million from the prior year. Net assets reached 98 million pounds. The total contracted book of business stood at 1.4 billion pounds, up 40 percent from 1.0 billion, with one-year forward contracted revenue of 668 million pounds providing strong visibility on near-term earnings. Management has guided for 2026 revenue of 850 to 875 million pounds, with adjusted EBITDA broadly in line with 2025 as incremental investment in growth moderates near-term profitability.

The company's meter point base—the fundamental unit of scale in the energy supply business—grew 49 percent to 131,000, representing a 3.5 percent share of the addressable market. Energy supplied reached 2.5 terawatt-hours, up 14 percent. A progressive dividend policy has been introduced, with the payout rising from 60 pence per share in 2024 to 67 pence in 2025, representing a yield of approximately 3.7 percent at the current share price.

For investors tracking this business, two KPIs stand above all others as the key indicators of ongoing performance. The first is meter point growth, which is the fundamental driver of revenue scale and market share. The 49 percent increase in 2025 was exceptional, and the trajectory of this metric will signal whether Yü is continuing to gain share or plateauing. The second is EBITDA margin, which captures the interplay between revenue growth, hedging effectiveness, and operational leverage. The margin expanded from 2.8 percent in 2022 to over 9 percent in 2023 before moderating to around 7 percent as the extraordinary crisis-era conditions normalised. Sustained margins in the 7 to 9 percent range on a growing revenue base would confirm the thesis that Yü's technology platform delivers genuine structural cost advantages over competitors.

X. Conclusion: The Bull versus Bear Case

Every investment thesis ultimately reduces to a bet on which story proves true.

The Bear Case is not trivial. Regulatory risk from Ofgem is omnipresent: changes to licensing requirements, market structure, or pricing rules could disrupt Yü's business model. A severe, prolonged dislocation in wholesale energy markets—beyond anything seen in 2021—could potentially overwhelm even a disciplined hedging strategy, particularly if the Shell facility's terms prove less protective than management believes in a true tail-risk scenario. The reliance on Bobby Kalar as founder-CEO creates key-person risk; while his 50 percent ownership provides alignment, it also means that a single individual's health, judgment, and motivation are load-bearing for the entire enterprise. The transition of two non-executive directors during 2026 adds near-term governance uncertainty. And there is the perennial risk of commoditised competition: if the technology advantage narrows, Yü becomes just another energy supplier competing on price in a low-margin industry.

The accounting history, while firmly in the past, also warrants a brief mention as a diligence overlay. The 2018 restatement was forensically reviewed by PwC, the controls have been rebuilt, and there is no suggestion of recurring issues. But for investors who track auditor signals and accounting judgments, it is worth noting that accrued income remains an inherent feature of energy supply accounting. The difference today is that smart metering and automated billing dramatically reduce the estimation error that caused the original problem. The appointment of Andy Simpson as CFO—with his BT Group and utility sector credentials—is a further reassurance on financial controls.

The Bull Case is that Yü Group is building the dominant digital platform for business utilities in the UK, with a roadmap that extends well beyond traditional gas and electricity supply. The multi-utility proposition—gas, electricity, and water through a single platform—already differentiates Yü from competitors, and the company describes itself as the only supplier offering this comprehensive combination. Expansion into adjacent services through Yü Smart—EV charging, solar maintenance, smart metering as a service—creates a recurring-revenue business embedded in the physical infrastructure of its customers' premises. The forward contracted book of 1.4 billion pounds provides multi-year earnings visibility. The Shell hedging facility eliminates the capital constraint that historically limited growth. And the combination of founder ownership, digital efficiency, and acquisitive discipline gives Yü the ability to compound growth in a market where competitors are either too large and slow to adapt or too small and undercapitalised to compete.

At a market capitalisation of roughly 303 million pounds, trading at approximately 8 times trailing earnings and 5 times enterprise value to EBITDA (adjusting for the 106 million pounds in cash), with a 3.7 percent dividend yield and management guiding for 850 to 875 million in 2026 revenue, the valuation does not appear to reflect a company with this growth trajectory, this market share momentum, or this quality of earnings. Whether that discount reflects legitimate scepticism about sustainability or simply the chronic undervaluation of AIM-listed companies by institutional investors is a question each investor must answer for themselves.

The story of Yü Group is, at its core, a story about resilience. A founder who refused to let a spreadsheet error define his legacy. A company that used a near-death experience as the catalyst for a genuine transformation. And a market opportunity—the digitisation of business energy supply in the UK—that is still in its early innings, with Yü Group holding 3.5 percent of a market where the incumbents are lumbering, the regulations favour the well-capitalised, and the technology gap is widening with every passing quarter.

Bobby Kalar once told an interviewer that if he had listened to the logical side of his brain, he would never have started the company. The logical side of the brain would have said that a care home operator from Nottingham had no business taking on the Big Six energy giants. The logical side would have said that the 2018 crash was a death sentence. The logical side would have said that an AIM-listed micro-cap could not survive an energy market Armageddon.

The logical side, as it turns out, would have been wrong about all of it.

XI. Links and Further Reading

Yü Group PLC Annual Reports, available through the company's investor relations page at yugroupplc.com. The comparison between the 2018 and 2023 accounts is a masterclass in corporate turnaround, documenting the transformation from manual processes and accounting write-downs to automated systems and record profitability.

Ofgem's "State of the Market" reports covering the 2021 energy supplier crisis, documenting the collapse of 29 suppliers and the regulatory response including tightened financial resilience requirements for licensed suppliers.

MoneyWeek profile of Bobby Kalar (June 2016), providing early biographical detail on the founder's journey from care homes to energy supply, including his reflections on entrepreneurship and the challenges of building a business from scratch.

Yü Group FY 2025 Final Results announcement (Investegate), detailing the company's record revenue of approximately 700 million pounds, adjusted EBITDA of 51 million, cash position of 106 million, and 2026 guidance for revenue of 850 to 875 million.

Shore Capital research coverage of Yü Group, providing independent analyst perspective on the company's competitive positioning, growth trajectory, and valuation relative to peers in the UK B2B energy supply market.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube