YIT Oyj: Building Northern Europe's Future

I. Introduction: The Finnish Giant

There is a photograph from 1985 that tells you everything you need to know about YIT's ambitions. It shows an entire city rising from the frozen Karelian wilderness — apartment blocks, a school for eight hundred students, a hospital, mining facilities, municipal roads — all built by a single Finnish construction company in the middle of Soviet Russia. The Kostamuksha project, valued at roughly one and a half billion dollars, was not just a construction contract. It was a diplomatic instrument, a piece of Cold War economic statecraft, and a demonstration that a mid-sized Nordic builder could operate at a scale that most Western companies would never attempt.

Four decades later, that same company — YIT Oyj, Finland's largest construction group — finds itself in a very different position.

The Russian adventure that defined its identity for generations ended in a fire sale. A "merger of equals" with its oldest rival produced years of indigestion. The Finnish housing market, its core profit engine, collapsed under the weight of the most aggressive monetary tightening cycle in European Central Bank history. And the dividend that Finnish pension funds had relied on for decades was suspended — not once, but twice.

Yet the company still stands. It still operates. And under a new CEO who arrived from McKinsey with a mandate to transform rather than merely manage, YIT is attempting something that sounds simple but is extraordinarily difficult in practice: to become a genuinely efficient construction company.

That distinction matters more than it might appear.

Construction is an industry famously resistant to efficiency gains. Productivity in global construction has been essentially flat for decades — one of the only major industries where this is true. Buildings still go up largely the way they did thirty years ago: armies of subcontractors, fragmented supply chains, project-by-project bidding, and a culture of "site autonomy" where individual project managers operate as quasi-independent fiefdoms. YIT's new leadership is betting that centralised procurement, data-driven bidding, and ruthless capital discipline can break this pattern — at least within their own operations.

The thesis on YIT is not complicated, but it is demanding.

At its core, YIT is a capital allocation and land-banking play. The company sits on a land bank worth approximately EUR 720 million at book value, supporting the construction of roughly thirty thousand homes across Finland and Central Eastern Europe. That land bank — concentrated in urban growth centres like Helsinki, Tampere, Prague, and Warsaw — represents a cornered resource that competitors cannot replicate without decades of patient accumulation. The question is whether the company's balance sheet can survive long enough for the housing cycle to turn, and whether new management can squeeze enough margin out of the contracting businesses to justify the capital tied up in the platform.

The roadmap of this story runs through three inflection points. First, the Lemminkäinen merger of 2018 — the deal that was supposed to create an unassailable Nordic champion and instead produced a decade of integration headaches. Second, the 2022 Russian exit — the geopolitical shock that amputated a limb of the business and forced a wholesale strategic rethink. And third, the efficiency era under Vuorenmaa — the ongoing transformation that will determine whether YIT emerges as a leaner, more profitable platform or succumbs to the gravitational pull of an industry that has resisted optimisation for as long as anyone can remember.

This is the story of a 114-year-old company that built modern Finland, bet big on Russia, merged with its archrival, lost hundreds of millions of euros in the process, and now faces a deceptively simple question: can a construction company learn to be efficient before its balance sheet runs out of patience?

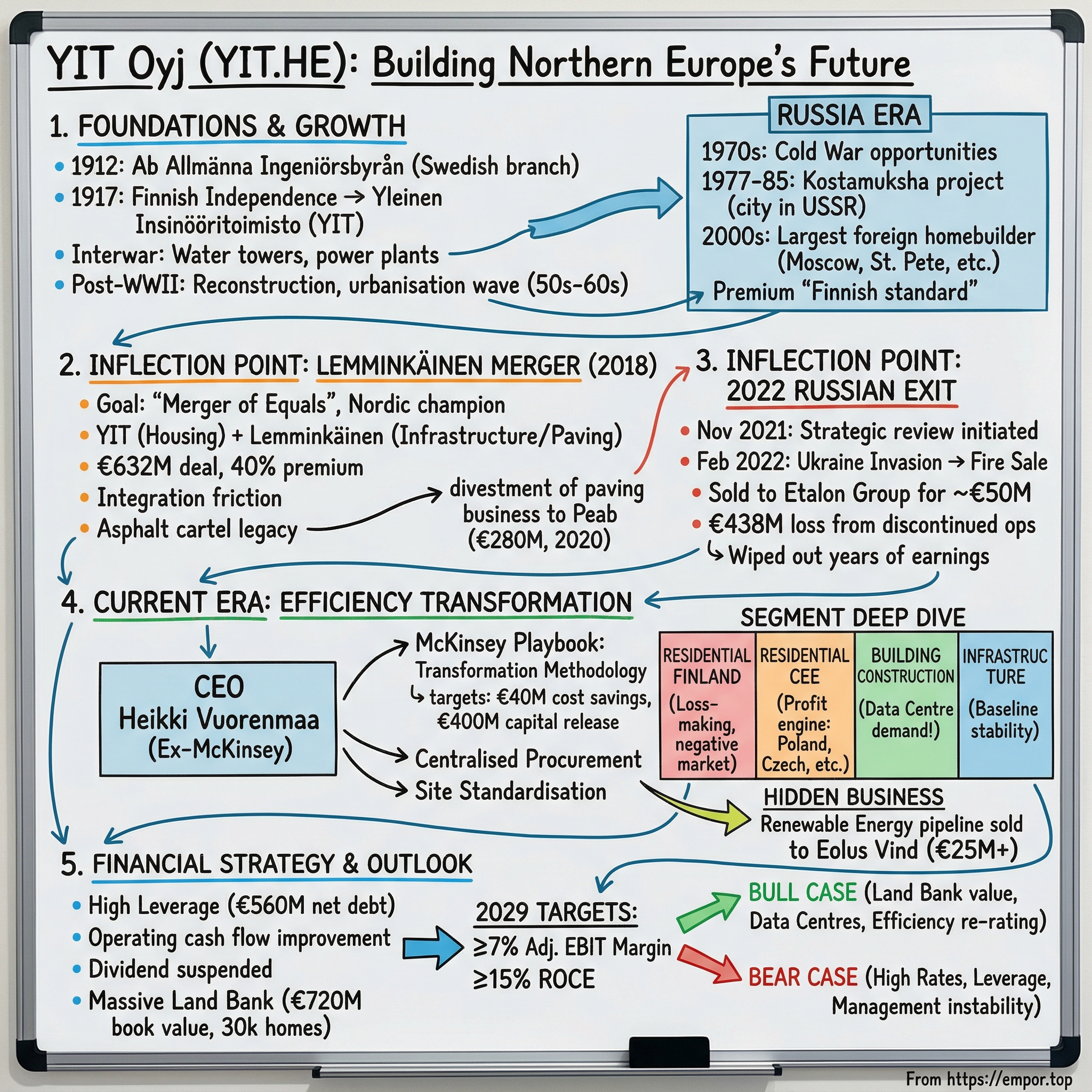

II. The Foundations: A Succinct History

The company that would become YIT was born in 1912 as Ab Allmänna Ingeniörsbyrån — the General Engineering Bureau — a Swedish engineering firm that opened a branch office in Helsinki when Finland was still a Grand Duchy of the Russian Empire.

The timing was consequential. Five years later, Finland declared independence on December 6, 1917, and the Swedish parent, suddenly operating in a foreign country rather than a provincial outpost, withdrew. Finnish businessmen reconstituted the Helsinki office as Yleinen Insinööritoimisto — YIT — and the company's fate became permanently intertwined with the fate of the young Finnish state. From its first day as a Finnish company, YIT existed to build a nation that was simultaneously inventing itself.

The interwar decades were foundational in the most literal sense. YIT built water towers, power plants, and industrial installations across a country that was still overwhelmingly rural and desperately short of modern infrastructure.

When Finland emerged from World War Two — having fought the Soviet Union to a negotiated peace in the Winter War and Continuation War, one of the remarkable military achievements of the twentieth century — the reconstruction effort required builders on a massive scale. The nation had lost territory, absorbed hundreds of thousands of displaced Karelian refugees, and owed punishing war reparations to Moscow. Every one of those challenges created demand for construction: new homes for the displaced, new factories for the reparations, new infrastructure for a country rebuilding from scratch.

What followed was the great urbanisation wave of the 1950s and 1960s. Rural Finns migrated to cities by the hundreds of thousands, and someone had to build the dense apartment blocks that define Nordic urbanism to this day. YIT built tens of thousands of apartments during this period, establishing the residential development capability that remains its core business over six decades later. The company was not just participating in Finland's modernisation — it was physically constructing it, one concrete pour at a time.

The Russia era began in earnest during the 1970s, when Finland's unique geopolitical position — neutral but Soviet-adjacent, a member of neither NATO nor the Warsaw Pact — created commercial opportunities that no other Western construction firm could access. Finland maintained a careful diplomatic balance during the Cold War, trading with the Soviet Union while preserving its democratic institutions and market economy. That balancing act created a commercial corridor that YIT exploited more successfully than perhaps any other Finnish company.

The Kostamuksha project, running from 1977 to 1985, was the crown jewel: a complete mining city built from scratch in Soviet Karelia. Construction exports to the USSR constituted ten to fifteen percent of all Finnish exports during this period, and YIT was the primary contractor.

The project demonstrated a capability that would serve the company for decades: the ability to operate in extremely challenging environments, managing vast labour forces across cultural and linguistic barriers, in climates where temperatures regularly dropped below minus thirty degrees Celsius. Finnish construction crews learned to pour concrete at temperatures that would cause it to crack in most other countries, developing cold-weather building techniques that became a genuine competitive advantage.

When the Soviet Union collapsed in 1991, most Western companies saw chaos. YIT saw opportunity.

The company had spent decades building relationships with Soviet officials, learning to navigate the bureaucratic labyrinth, and establishing a reputation for quality that no Russian competitor could match. Those relationships did not disappear with the USSR — they transformed into commercial channels. By the early 2000s, YIT had expanded into Russian residential construction, becoming the largest foreign homebuilder in the country.

Operations spanned Moscow, St. Petersburg, Yekaterinburg, Kazan, and Tyumen. The Finski residential area in the Moscow region alone comprised more than 3,300 apartments with schools and daycare facilities. At peak, Russian revenues exceeded EUR 200 million annually — a remarkable figure for a company whose home market had a population of just 5.5 million.

For a generation of YIT executives, Russia was the growth story. It was where the margins were fat, where demand seemed inexhaustible, and where YIT's Nordic construction quality commanded a genuine premium over domestic competitors.

Finnish apartments in Russian cities were marketed as prestige products — better insulated, better finished, built to standards that Russian developers could not match. In a market where domestic construction quality was notoriously uneven — where buyers routinely hired independent inspectors to check for defects before taking possession — the "Finnish standard" carried real commercial value. YIT apartments sold at a premium because they were, demonstrably, better built.

But the Russia era also planted the seeds of a strategic vulnerability that would not become fully visible for two decades.

The company's identity became entangled with its Russian operations in ways that made retreat psychologically difficult even when the commercial logic started to deteriorate. When the ruble collapsed in 2014 following the Crimea annexation, YIT took significant currency translation losses. When Western sanctions tightened after the first round of Ukrainian conflict, the operating environment grew more complex. Counterparties became harder to work with. Financing channels narrowed.

But the company stayed, because Russia was not just a market — it was part of who YIT believed itself to be. Walking away from Russia meant walking away from a piece of corporate identity that had been built over four decades, from Kostamuksha onward.

Finland's severe early-1990s banking crisis — GDP contracted fourteen percent, unemployment hit twenty percent — nearly destroyed the company along with much of the Finnish economy. The crisis was triggered by the simultaneous collapse of the Soviet trade relationship, a domestic banking bubble, and a currency devaluation that exposed the fragility of Finnish corporate balance sheets.

YIT survived, listed on the Helsinki Stock Exchange in 1995, and emerged into the post-crisis boom as a leaner, more disciplined operator. But the crisis left a scar tissue of conservatism that would shape the company's risk appetite for decades — making the eventual Russian disaster all the more painful, because it was precisely the kind of catastrophic, unhedgeable geopolitical risk that the 1990s generation of Finnish managers should have understood better than anyone. They had lived through one existential crisis. They should have been better prepared for the next one.

The old model — build everywhere, from Helsinki to St. Petersburg to Yekaterinburg — had reached its breaking point.

The revenue base that looked so impressive on paper was in reality a collection of geographically dispersed operations with inconsistent margins, currency exposure, and political risk that no amount of project management expertise could fully mitigate. Finland remained the profitable core, but the periphery was increasingly fragile.

What came next would be the most consequential period in YIT's century-long history: a merger that promised transformation, a geopolitical crisis that forced amputation, and a new leader who believed that the path forward led not through geographic expansion but through operational excellence.

III. Inflection Point 1: The Lemminkäinen Merger

Picture a boardroom in Helsinki in the spring of 2017. Two of Finland's oldest construction companies — rivals for over a century — are sitting down to discuss a combination that would reshape their industry. The executives across the table know each other. They have competed against each other on tenders. Their project managers have cursed each other's names on job sites. And now they are going to become one company.

In June 2017, YIT announced what both companies' boards described as a "merger of equals" — a statutory absorption of Lemminkäinen Corporation, Finland's second-largest construction company. The deal was structured as an all-share transaction: Lemminkäinen shareholders received 3.6146 new YIT shares for each Lemminkäinen share, implying a total deal value of approximately EUR 632 million and a premium of roughly forty percent over Lemminkäinen's pre-announcement share price.

The premium demands scrutiny.

Forty percent is not a modest premium in any industry, and in construction — where assets are largely tangible, margins are thin, and growth rates are pedestrian — it is particularly aggressive. For context, the median acquisition premium in European industrial M&A at the time hovered around twenty to twenty-five percent. YIT was paying nearly double the norm.

The justification rested on synergies: EUR 40 million in annual cost savings, to be fully realised by the end of 2020, generated through administrative consolidation, procurement optimisation, and process harmonisation. At a deal value of EUR 632 million, that implied a payback period on synergies alone of roughly sixteen years — not exactly a screaming bargain, even before accounting for integration costs and execution risk.

To understand why the merger happened, you need to understand what Lemminkäinen was. Founded in 1910 — two years before YIT — and named after a hero of the Kalevala, Finland's national epic, Lemminkäinen had evolved into a company defined by infrastructure rather than housing. Its crown jewels were its paving operations: roughly two hundred quarries across the Nordic region, sixty-three asphalt production plants, and a heavy equipment fleet that gave it dominant positions in road construction from Helsinki to Tromsø. Where YIT built apartments, Lemminkäinen built the roads that connected them.

The strategic logic was seductive. Combine YIT's residential development expertise with Lemminkäinen's infrastructure capabilities, and you create a full-spectrum construction platform that can bid on everything from single-family homes to highway megaprojects.

The combined entity would have pro forma revenues exceeding EUR 3 billion and roughly ten thousand employees, creating scale advantages in Finnish procurement that no domestic competitor could match. In a country of 5.5 million people with a limited construction market, being the largest player by a wide margin confers real advantages: better supplier terms, first look at the best tenders, and the financial capacity to carry large multi-year projects that smaller rivals cannot underwrite.

The merger completed on February 1, 2018, creating the largest construction company in the Nordics by Finnish market share — but "merger of equals" is a phrase that should always trigger scepticism. In practice, one company's culture always dominates, and in this case, YIT's residential-focused DNA won out over Lemminkäinen's infrastructure heritage.

The reality of integration was messier than the PowerPoint suggested. Project managers who had competed for decades — sometimes bitterly, on the same tenders — were suddenly expected to collaborate. Regional offices that had been rivals were merged, with all the human friction that implies. YIT's residential development culture, focused on consumer marketing and apartment sales, collided with Lemminkäinen's infrastructure ethos, where the customer was typically a government agency and the relationship was defined by technical specifications rather than showroom aesthetics.

There was also baggage — the kind that surfaces during due diligence but gets rationalised away in the excitement of a transformative deal.

Lemminkäinen had participated in an asphalt price-fixing cartel from 1994 to 2002, receiving a EUR 68 million fine as part of a total cartel penalty of EUR 82.55 million. Civil damages claims from the Finnish state and municipalities dragged on for years and were not fully settled until 2018 — the same year the merger closed. The cartel history did not derail the merger, but it coloured the cultural integration in ways that are difficult to quantify. YIT was absorbing not just a company but a legacy, and not all of that legacy was attractive.

Integration costs ultimately reached EUR 73 million — at the upper end of the EUR 50 to 70 million budget.

The promised synergies of EUR 40 million were achieved, eventually upgraded to EUR 43 million, but the timeline slipped. More importantly, the benefits were subsequently overwhelmed by forces that no amount of procurement optimisation could offset: COVID-19, the Russian exit, and the most severe Finnish housing downturn in a generation. The synergies were real, but they were dwarfed by the macro headwinds. Achieving EUR 43 million in annual savings matters very little when you are simultaneously absorbing hundreds of millions in impairments and watching your core market shrink by forty percent.

Perhaps the most revealing post-merger decision was the sale of the paving and mineral aggregates business — the very assets that had made Lemminkäinen distinctive — to Swedish peer Peab for EUR 280 million. The transaction, announced in July 2019 and closed in April 2020, divested approximately two hundred quarries, sixty-three asphalt plants, and seventeen hundred employees. The divested business had generated EUR 566 million in revenue and EUR 23 million in adjusted EBITDA in 2018.

Think about what that sequence means for a moment.

YIT paid a forty percent premium to acquire Lemminkäinen, then sold one of Lemminkäinen's most distinctive business lines to a competitor within eighteen months. The paving business was profitable, but it was capital-intensive, low-margin, and — crucially — it did not fit the strategic direction that YIT's board had settled on: a focus on residential development and higher-value construction. The sale was the right decision in isolation, but it raised a legitimate question about whether the merger premium reflected the value of the company YIT actually wanted to keep, or the value of the company it was about to sell off piecemeal.

Benchmarked against Nordic peers, the merger's legacy is mixed. Skanska, with a market capitalisation of roughly EUR 9.5 billion, generates revenue of approximately EUR 17 billion across Sweden, the Nordics, the US, and the UK. Peab, at EUR 2.8 billion, operates primarily in Sweden and Norway. NCC, at EUR 1.9 billion, covers Sweden and Denmark. YIT, at EUR 630 million, is by far the smallest of the major Nordic contractors — a fraction of the scale that the Lemminkäinen merger was supposed to create.

The net assessment of the Lemminkäinen merger, viewed from 2026 with the benefit of hindsight, is that it was strategically sound but financially costly. The assets acquired were real and valuable. The price paid was too high. And the timing — just before COVID, the Russian crisis, and the housing freeze — was catastrophically unlucky.

The merger did achieve one thing that its architects intended: it created a domestic champion. In Finland specifically, YIT's market position is dominant in ways that smaller competitors simply cannot challenge. The combined procurement volumes, the breadth of the land bank, the ability to absorb the enormous fixed costs of construction machinery — these are genuine scale advantages in a geography-constrained market. Whether those advantages justify the decade of disruption that followed is a question the company's financial trajectory continues to answer.

IV. Inflection Point 2: The 2022 Russian Exit

The irony is almost too neat.

YIT initiated a strategic review of its Russian businesses in November 2021 — three months before Russia invaded Ukraine. The review was driven by commercial logic, not geopolitical foresight: margins in the Russian housing segment had been deteriorating, the ruble's chronic weakness created persistent translation losses, and the regulatory environment had grown increasingly unpredictable. The board concluded that the capital tied up in Russian operations could be deployed more productively elsewhere.

Then, on February 24, 2022, everything changed. Russian tanks rolled across the Ukrainian border, and the geopolitical architecture of Europe was shattered overnight.

Russia's full-scale invasion of Ukraine transformed a measured strategic exit into a desperate fire sale.

What had been a calm evaluation of capital allocation priorities became a scramble to divest before the window closed entirely. Western sanctions were tightening by the week. Financial channels between Russia and Europe were being severed. The SWIFT banking network was partially cut off. Insurance coverage for Russian operations became impossible to obtain at any price. The reputational risk of continued Russian operations became untenable for a publicly listed Finnish company whose pension fund shareholders included entities with explicit ESG mandates.

For Finland specifically, the invasion carried an existential weight that no other EU country except perhaps the Baltic states could fully understand. Finland shares a 1,340-kilometre border with Russia — the longest of any EU member state. The same country where YIT had been building apartments was now waging a war of aggression against a sovereign European neighbour. The psychological rupture was profound, and it made continued commercial engagement in Russia unthinkable in a way that purely financial analysis could not capture.

On April 1, 2022 — in one of those dates that seems deliberately chosen for its ironic resonance — YIT signed a sale agreement with Etalon Group PLC, a Russian residential developer, for a price of approximately EUR 50 million.

That figure bore no relationship to the book value of the assets being sold. Etalon acquired nineteen projects at various stages of planning and construction, with net sellable area exceeding six hundred thousand square metres — entire residential districts, in some cases, changing hands for pennies on the ruble. The sale was completed on May 30, 2022, barely two months after signing.

The financial trauma was staggering.

YIT booked EUR 152 million in impairment charges upon classifying the Russian business as held-for-sale. But the impairment was only the beginning. The full-year result from discontinued operations was negative EUR 438 million — a figure that included not just the impairment but also the release of accumulated ruble-to-euro translation differences that had been sitting in equity for years, suddenly crystallised into realised losses. These translation reserves are an accounting technicality that most investors ignore until they cannot be ignored anymore: as long as you hold a foreign subsidiary, currency gains and losses accumulate in equity rather than flowing through the income statement. The moment you sell, they are released — and decades of ruble weakness hit the profit and loss statement all at once.

The bottom-line net loss for FY2022 was EUR 375 million, wiping out years of accumulated earnings in a single stroke.

To put the EUR 50 million sale price in context: YIT's Russian operations had been generating annual revenue of approximately EUR 200 million.

The company was selling a business with hundreds of millions in annual revenue and thousands of apartments in various stages of construction for a price that would barely cover two quarters of the divested revenue stream. It was the commercial equivalent of selling a house during a natural disaster — the buyer knows you have no choice, and the price reflects their leverage, not the asset's value.

The buyer, Etalon Group, knew that YIT had no alternatives. Every Western company was trying to exit Russia simultaneously: Ikea, Renault, Shell, BP, dozens of others, all scrambling for the exits at the same time. The bargaining power was entirely on the Russian side. In a buyer's market this extreme, the sale price bore no relationship to intrinsic value.

The human dimension deserves attention, because it is too easily lost in the financial analysis.

Thousands of Russian employees who had built their careers at YIT — many of whom had been trained in Finnish construction methods and took genuine pride in the quality differential that YIT apartments represented in the Russian market — found their employer and their professional identity severed overnight. Project managers who had spent years learning Nordic building standards were suddenly working for a Russian company with different practices. Engineers who had been part of an international organisation found themselves isolated from the global construction community.

The geopolitical crisis did not distinguish between the decisions of governments and the lives of individual construction workers in Yekaterinburg or Kazan. For YIT's Finnish employees, the exit was a relief. For the Russian employees who stayed behind, it was a loss that carried personal as well as professional consequences.

What emerged from the wreckage was a fundamentally different company.

YIT was now a Northern Europe-focused construction group — Finland, the Baltics, the Czech Republic, Slovakia, Poland, and Sweden — with a significant hole in its earnings power. Russian operations had been contributing meaningful profit, and that profit was now gone. Revenue, which had peaked at EUR 2.86 billion in FY2021 with Russia still contributing, would decline to EUR 2.16 billion by FY2023 and further to EUR 1.76 billion by FY2025 — a thirty-eight percent contraction in four years.

The company needed a new strategy, a new narrative, and arguably new leadership capable of reimagining the business without its most familiar growth engine. The old board and management team had been defined by the Russia era — they had championed the expansion, believed in the opportunity, and built their careers on its success. A fresh perspective was needed, someone who could see the company without the emotional attachment to what had been lost.

The Russian exit also crystallised a lesson about unhedgeable risk that applies far beyond YIT. No amount of financial modelling, scenario planning, or risk management can protect against the sudden transformation of an entire country into a commercially inaccessible territory. The companies that suffered least were those with the least exposure — a tautology that offers cold comfort but genuine strategic wisdom. Geographic diversification is a source of resilience only when the geographies in question remain accessible. When they become inaccessible overnight, diversification becomes a trap.

YIT was not the only Finnish company burned by Russia — Nokia, Fortum, and others suffered comparable or worse losses — but YIT's exposure was uniquely painful because the Russian business was not a peripheral activity. It was central to the company's identity, its growth story, and its strategic positioning. Losing Russia did not just reduce YIT's revenue. It forced a fundamental re-examination of what the company was and what it wanted to become — an existential reckoning that the board answered by reaching for a very different kind of leader.

V. Current Management: The Efficiency Era

The board's choice of successor was revealing — and deliberate.

When YIT announced in October 2022 that Heikki Vuorenmaa would become President and CEO effective November 28, the selection signalled a decisive break with the past. The board did not promote from within the existing construction management ranks. It did not recruit a seasoned CEO from a Nordic peer. It chose someone who had left the construction industry entirely, gone to McKinsey, and returned with a transformation agenda.

Vuorenmaa was not a "traditional" construction lifer. Born in 1981 — making him forty-one at appointment, young for a CEO of Finland's largest construction group — he brought a resume that read more like a management consultant's career trajectory than a builder's.

His path to the corner office was anything but linear, and it is worth tracing in detail because it explains both his strategic instincts and his credibility with the organisation.

Vuorenmaa spent seven years at Nokia from 2008 to 2015, working in operations and procurement during the mobile phone giant's traumatic transition from hardware dominance to near-irrelevance. Anyone who spent those years at Nokia witnessed firsthand what happens when a market leader fails to adapt: not a gradual decline but a sudden, vertiginous collapse. That experience inoculated him against the comfortable assumption that market leadership is permanent — a lesson directly applicable to a construction company watching its core housing market evaporate.

He then joined Lemminkäinen as Senior Vice President of Procurement in 2015, two years before the YIT merger was announced. When the merger closed in 2018, he transitioned to YIT as Executive Vice President of the paving division. When that division was sold to Peab in 2020, he briefly joined Peab to manage the integration — seeing the other side of the transaction he had facilitated, learning how a Swedish acquirer absorbed Finnish assets.

Then came the most unconventional move — the one that made Vuorenmaa an unusual candidate for a construction CEO and, paradoxically, exactly what the board was looking for.

Rather than seeking another operational role in construction, Vuorenmaa joined McKinsey & Company as an Associate Partner specialising in industrial transformations. For roughly eighteen months, he helped other companies do what he would soon be asked to do at YIT: strip out complexity, centralise procurement, impose financial discipline on operationally fragmented organisations. When the YIT board came calling in late 2022, they were hiring not just a CEO but a methodology — the McKinsey transformation playbook, wielded by someone who knew YIT's specific dysfunctions from the inside.

The transformation program launched in February 2023 with two headline targets: EUR 40 million in annualised cost savings by end-2024, and approximately EUR 400 million in capital release through inventory reduction and balance sheet optimisation.

The first number was about efficiency. The second was about survival. A company with EUR 560 million in net debt carrying EUR 1.6 billion in inventory needed to convert assets into cash before the interest burden consumed whatever operating profit remained.

The organisational restructuring was immediate and blunt. YIT moved from five segments to four, then refined the structure further effective January 1, 2025, into the current configuration: Residential Finland, Residential CEE, Building Construction, and Infrastructure. Roughly one hundred and fifty positions were eliminated in Finland. Matrix management structures were dismantled. Centralised procurement replaced the site-by-site purchasing that had allowed individual project managers to negotiate their own supply contracts — often at prices well above what the group's combined volumes could command.

The cultural shift was arguably more significant than the cost cuts. Construction companies, more than almost any other type of industrial enterprise, operate through a culture of project-site autonomy. Each construction site is a self-contained universe: its own budget, its own timeline, its own subcontractor relationships, its own local adaptations. This autonomy is partly functional — no two construction sites are identical, and local knowledge genuinely matters — but it is also a source of enormous inefficiency, because it prevents the kind of standardisation and bulk purchasing that drives margins in other industries.

Vuorenmaa's agenda was to preserve the functional autonomy while eliminating the wasteful variety. Standardise the materials. Centralise the procurement. Impose uniform bidding methodologies. Let the site managers manage their sites, but take away their ability to reinvent the purchasing wheel on every project. Think of it as the difference between a franchise model and a collection of independent restaurants: the kitchen stays local, but the supply chain runs through headquarters.

The cost savings came through: EUR 43 million, exceeding the target.

But the program costs also reached EUR 73 million — the upper end of the budget, reflecting the reality that transformation in construction is expensive because so much of the cost structure is embedded in contracts, relationships, and physical assets that cannot be restructured with a slide deck. Severance payments for one hundred and fifty people. Contract renegotiation costs. Systems integration. Office consolidation. The savings are recurring; the costs are one-time. But the front-loaded nature of the spending created a period where YIT was simultaneously investing in transformation and absorbing the losses of a depressed housing market.

The capital release target proved far more elusive.

By mid-2024, approximately EUR 140 million had been freed — well short of the EUR 400 million aspiration. The gap was not a failure of execution so much as a failure of market conditions. You cannot liquidate apartments when nobody is buying apartments. You cannot sell land plots at book value when developers across Finland are sitting on their own unsold inventory. The Finnish housing market simply would not cooperate with YIT's balance sheet optimisation timeline, and no amount of management determination could force a market that had stopped transacting.

Vuorenmaa has also made his commitment visible through an unusual dual role. Since January 2025, he has served as interim Executive Vice President of the Residential Finland segment — the company's most troubled division — in addition to his CEO responsibilities. The move signals that he considers the Finnish housing turnaround important enough to oversee personally. Mari Puoskari has been appointed as the permanent EVP of Residential Finland, but she will not start until July 2026 at the latest, leaving Vuorenmaa in the dual role for at least eighteen months.

The management team has been in flux, and this is worth flagging as a risk factor that goes beyond the usual corporate reshuffling.

CFO Tuomas Mäkipeska resigned in late 2025 to join Kemira — a move that raised eyebrows because CFOs typically do not leave during the middle of a balance sheet restructuring unless they see limited upside in staying, or the transformation is progressing well enough that they feel comfortable departing. Markus Pietikäinen, previously SVP of Treasury and M&A, stepped in as interim CFO from November 2025 — a capable internal appointment, but an interim one nonetheless. Aleksi Laine was appointed Deputy to the President and CEO the same month.

The combination of a departing CFO, an interim replacement, and a CEO running double duty in the most challenged segment creates a leadership structure that is functional but visibly stretched. In construction, where project execution depends on management attention to detail, stretched leadership is not an abstract concern — it is an operational risk.

The incentive architecture tells its own story. The Strategic Long-Term Incentive Plan established in April 2025 covers a single performance period from FY2025 to FY2029, with rewards paid in YIT shares. The performance criteria — 2029 net sales, adjusted EBIT, ROCE, and strategic milestones — are explicitly designed to align top management with the five-year strategy. It is a bet-the-career structure: either the transformation succeeds by 2029 and the management team is rewarded generously, or it does not and the shares are worth little. The CEO's maximum annual bonus of ninety percent of base salary, combined with the share-based LTI, means that Vuorenmaa's personal financial outcome is materially tied to YIT's share price performance over the remainder of the decade. Skin in the game is real — and it cuts both ways.

VI. Segment Deep Dive and Hidden Businesses

The November 2024 Capital Markets Day — the most important investor event in YIT's recent history — introduced financial targets for 2025-2029 that, if achieved, would represent a near-complete transformation of YIT's economic profile.

Adjusted operating profit margin of at least seven percent — roughly double the FY2025 actual of 3.1 percent. Return on capital employed of at least fifteen percent — nearly four times the FY2025 actual of 3.9 percent. Revenue growth of at least five percent compound annual growth.

These are not incremental improvement targets. They are aspirational, and the gap between current reality and stated ambition is the central question facing any investor evaluating the stock. To put the margin target in perspective: achieving seven percent adjusted operating margin would place YIT roughly in line with Skanska and above NCC — companies that have spent decades optimising their operations. YIT is targeting in three years what its Nordic peers built over a generation.

Start with Residential Finland, because it is both the largest opportunity and the most painful current reality.

The segment posted a negative EUR 8 million in adjusted operating profit in FY2025, an improvement from the EUR 20 million loss in FY2024 but still deeply in the red. The direction is right; the destination is still far away. Consumer apartment sales fell to 490 units, down from 589 the prior year — a number that in any normal year would be considered catastrophically low.

Consumer apartment starts — the leading indicator of future revenue — were just 477, a tripling from the 160 units started in 2024 but still far below any reasonable definition of normalised activity. To put it in perspective, YIT was starting thousands of apartments per year in Finland during the mid-2010s boom. Four hundred and seventy-seven is not a slow market. It is a market that has effectively stopped.

The Finnish housing market has been in a deep freeze since the ECB began its historic tightening cycle. The central bank raised its deposit rate from negative 0.50 percent to positive 4.00 percent in fourteen months — the most aggressive monetary tightening in European history.

The impact on Finnish housing was devastating. Finland has an unusually high proportion of variable-rate mortgages compared to other European countries — roughly ninety percent of Finnish home loans are tied to Euribor, versus a much smaller share in markets like France or Germany where fixed-rate mortgages dominate. This means that ECB rate hikes transmit into household budgets almost immediately, with no lag and no cushion. When rates went from negative to four percent, Finnish mortgage payments roughly doubled for many households overnight.

Apartment transactions fell approximately forty percent during the downturn. Building permits dropped 15.9 percent year-over-year in 2025 to just 15,942 units. Sales of newly built homes fell 17.9 percent to 1,685 units.

There are early signs of thaw. The twelve-month Euribor has dropped from above four percent in 2024 to approximately 2.4 percent by mid-2025, providing meaningful mortgage payment relief. The Finnish government changed mortgage regulations in 2025: maximum loan terms extended from thirty to thirty-five years, the loan-to-value ceiling was raised to ninety-five percent, and first-time buyers now need only five percent down. Housing transactions increased 10.7 percent year-over-year to 58,282 in 2025. Property prices are forecast to rise modestly in 2026, with Helsinki and Espoo leading at two to four percent annually.

YIT has responded creatively to the frozen market, offering buyers a two percent interest rate cap for five years — essentially an embedded insurance product that reduces the perceived risk of variable-rate mortgages. It is the kind of commercial innovation that a smaller developer could not afford to offer, because the hedging cost must be absorbed across a large enough portfolio to make the economics work. Scale advantage manifesting in a consumer-facing product rather than a back-office procurement saving.

Residential CEE is the profit engine, and it is the segment that most clearly demonstrates what YIT can achieve when the market cooperates.

The segment sold 2,169 apartments in FY2025, up sharply from 1,644 the prior year, with consumer starts surging to 1,555 from 783. Adjusted operating profit was EUR 30 million, down from EUR 37 million due to mix effects, but the volume trajectory is strongly positive.

Operations span Poland, the Czech Republic, Slovakia, and the Baltic states — markets where urbanisation is still accelerating, mortgage penetration is still growing, and housing quality expectations are rising toward Western European standards. A young professional in Prague or Warsaw increasingly expects the same apartment quality as their counterpart in Helsinki — energy-efficient windows, modern ventilation systems, high-quality finishes — and is willing to pay a premium for it.

CEE is where YIT's Nordic construction quality commands a genuine premium, much as it once did in Russia — but in geographies where EU membership provides regulatory stability and NATO membership provides security guarantees that Russia never offered.

Building Construction — the segment formerly known as Business Premises — delivered the most dramatic turnaround in FY2025. Adjusted operating profit jumped from EUR 3 million in FY2024 to EUR 16 million, driven by a surge in data centre and industrial construction demand. Finland has emerged as a preferred location for hyperscale data centres, thanks to its cold climate (reducing cooling costs by twenty to thirty percent versus temperate locations), abundant clean energy from hydroelectric and nuclear sources, and stable political environment. In February 2026, YIT doubled its growth targets for both Building Construction and Infrastructure, revising to at least four percent and ten percent annual growth respectively through 2029, explicitly citing data centre demand as the catalyst.

The data centre opportunity deserves elaboration because it represents a structural shift in demand that could persist for years, perhaps decades.

Global cloud computing investment is growing at double-digit rates. Artificial intelligence workloads require exponentially more compute capacity. And unlike most commercial construction, data centres have highly specific requirements — precisely controlled temperature and humidity, redundant power systems, massive electrical capacity, seismically stable foundations — that reward specialised construction expertise. A builder who has completed one data centre understands the engineering requirements in ways that a generalist contractor does not, creating a learning curve advantage that compounds with each completed project.

The Nordics are attracting a disproportionate share of this investment because they offer the cheapest possible cooling — cold ambient air that costs nothing — combined with among the cheapest electricity in Europe from hydroelectric and nuclear sources. For YIT, this translates into a pipeline of high-value construction contracts with creditworthy counterparties — technology companies and institutional investors — that is largely independent of the housing cycle. It is, in essence, a natural hedge against residential weakness, and one that did not exist five years ago.

Infrastructure grew revenue over thirty percent year-over-year in FY2025 and posted EUR 22 million in adjusted operating profit, up from EUR 17 million.

This segment is the "utility-like" revenue stream — road construction, bridge building, municipal infrastructure, and energy-related construction — that provides baseline earnings stability regardless of where the housing cycle stands. Infrastructure projects are typically government-funded, multi-year in duration, and awarded through competitive tenders where YIT's scale and track record provide meaningful advantages. The Finnish government's infrastructure investment pipeline, combined with energy transition projects and the incremental defence-related construction that Finland's 2023 NATO accession has begun to generate, provides multi-year visibility that the residential segments cannot offer.

The renewable energy business deserves a note, even though YIT ultimately sold it — because the sale itself tells a story about strategic discipline under financial pressure.

By 2023, YIT had assembled a development pipeline of approximately 2.3 gigawatts — 900 megawatts of onshore wind, 200 megawatts of solar, and 1.2 gigawatts of earlier-stage projects. For context, 2.3 gigawatts is enough capacity to power roughly one million homes — a substantial pipeline by any measure. The company had built foundations for more than one hundred wind turbines and developed marquee projects like the Lestijärvi wind farm, a seventy-two-turbine, four-hundred-megawatt development sold to OX2.

The logic of a construction company entering renewable energy development was compelling. Wind and solar projects require exactly the skills that construction companies possess: land acquisition, permitting, environmental impact assessment, foundation construction, grid connection infrastructure, and project management. YIT's model was asset-light: develop the projects through the capital-intensive early stages, then sell the completed or near-completed projects to energy companies or infrastructure funds. Keep the development margin; avoid the operational complexity of running power plants.

But in a strategic review initiated in June 2023, YIT concluded that the renewable energy business, while promising, required capital and management attention that would be better directed toward the core construction operations. The business — YIT Energy Oy, including sixteen employees and the entire project pipeline — was sold to Swedish firm Eolus Vind for a fixed price of EUR 25 million plus variable consideration of up to EUR 75 million based on project completions, generating a gain of approximately EUR 46 million.

The decision to sell the renewable energy pipeline was strategically rational but optically unfortunate. At the moment when "green developer" narratives were attracting premium valuations in European equity markets, YIT was divesting its most obvious claim to that narrative. The decision reflected a pragmatic assessment of capital constraints rather than a judgment about the attractiveness of renewable energy. A company carrying the balance sheet burden that YIT carries does not have the luxury of funding a multi-year development pipeline in an adjacent industry, however attractive the long-term economics might appear from the outside.

VII. The Playbook: Seven Powers and Five Forces

Every construction company claims competitive advantages. The question that separates genuine moats from marketing rhetoric is whether those advantages persist through cyclical downturns — when volumes fall, competitors become desperate, and the temptation to compete on price alone becomes overwhelming.

Hamilton Helmer's Seven Powers framework provides a useful structure for evaluating which of YIT's competitive advantages are durable and which are merely circumstantial — a distinction that matters enormously for any company navigating a cyclical downturn.

The most compelling power is the cornered resource — YIT's land bank. The company holds plot reserves with a book value of approximately EUR 720 million, supporting the future construction of roughly thirty thousand homes: fifteen to sixteen thousand in Finland and approximately fifteen thousand in Central Eastern Europe. In Helsinki specifically, these plots are concentrated in urban growth centres where new land simply does not become available on a meaningful scale. Helsinki sits on a peninsula with restrictive zoning, surrounded by water on three sides. Every buildable plot in the metropolitan area was assembled through decades of patient negotiation with municipal authorities, land use planning processes, and competitive bidding against other developers.

A competitor entering the Finnish residential market today cannot replicate YIT's land bank in any reasonable timeframe. They can acquire individual plots, but the cost of assembling a comparable portfolio from scratch — in a market where every transaction is public, every zoning change takes years, and every incumbent landowner understands the scarcity value of their position — would be prohibitive.

Think of it like a game of Monopoly where one player already owns Boardwalk, Park Place, and most of the properties on the board. A new player can enter the game, but the best locations are already taken, and buying them from the incumbent requires paying a premium that makes the economics difficult.

This is a genuine cornered resource: a competitively valuable asset that YIT controls and that rivals cannot obtain at a price that makes economic sense. The land will still be there when interest rates normalise. The question is what it will be worth when that happens — and whether YIT's balance sheet can carry the costs of holding it until the answer becomes clear.

The second relevant power is scale economies, and it operates at multiple levels simultaneously.

At the procurement level, YIT's dominance in Finnish purchasing volumes — the combined orders for concrete, steel, timber, insulation, mechanical systems, and electrical components — creates unit cost advantages that smaller competitors cannot match. When you are building thousands of apartments simultaneously across a country, you can negotiate framework agreements with suppliers that lock in prices and guarantee delivery timelines. When you are building dozens, you are a price-taker who absorbs whatever the market dictates.

At the organisational level, the fixed costs of central functions — engineering, legal, finance, human resources, IT systems — are spread across a much larger revenue base than any domestic competitor can achieve. A compliance department that costs EUR 5 million per year is a rounding error for a EUR 1.8 billion revenue company. It is a crushing overhead for a EUR 200 million competitor.

The Lemminkäinen merger, for all its integration costs and cultural friction, did deliver this procurement scale advantage, and it is likely permanent as long as YIT maintains its volume position.

The third power, more tentatively, is switching costs — though they operate differently in construction than in technology businesses. YIT's long-standing relationships with Finnish municipalities, its institutional knowledge of local building codes and zoning processes, and its track record of project completion create a form of institutional inertia. When a city is planning a major urban development project and needs a partner who understands the local permitting maze, has the financial capacity to carry multi-year developments, and has a local workforce already in place, the tendency is to work with the incumbent. Not because alternatives are unavailable, but because the cost of educating a new partner on local conditions — regulatory, geological, political — is meaningful and adds risk.

These three powers — cornered resource, scale economies, and switching costs — are meaningful but not individually decisive. The moat is the combination: prime land feeding a scaled procurement machine embedded in deep municipal relationships. Remove any one element and the competitive position weakens, but the combination is genuinely difficult to replicate.

Porter's Five Forces analysis reveals a mixed competitive landscape with some genuinely attractive structural features and some forces that are far less benign.

Bargaining power of buyers varies dramatically by segment and by cycle. In residential construction during a housing shortage, buyer power is low — people need homes, and when mortgage conditions are favourable, they buy what is available at the price offered. But during a housing glut — which is effectively the current Finnish situation, with roughly five thousand unsold new apartments sitting in inventory across the market — buyer power spikes. Buyers can negotiate, delay, walk away, and wait for the next interest rate cut. In government infrastructure tenders, buyer power is structurally high because the customer is a sophisticated institutional buyer running competitive procurement processes designed to minimise the price paid.

Threat of new entrants is genuinely low, and this is one of YIT's most underappreciated structural advantages. Entering the Nordic construction market requires deep regulatory expertise (building codes are complex and vary by municipality), substantial financial capacity (projects require hundreds of millions in working capital), a local workforce (construction labour is unionised and skilled workers are perennially scarce), and a track record that institutional clients demand before awarding contracts. The capital intensity alone is formidable — YIT carries over EUR 1.3 billion in inventory at any given time. A new entrant would need to fund comparable working capital from day one, an almost insurmountable barrier.

Threat of substitutes is moderate and evolving. Modular construction — factory-built apartment modules assembled on site like oversized Lego blocks — represents a genuine long-term substitute threat to traditional on-site building methods, though adoption in the Nordics has been slower than advocates predicted. Cross-laminated timber construction is gaining share in the low-rise residential market, and Finnish timber companies are investing heavily in this technology. Neither substitute threatens YIT's position in the near term, but both represent credible long-term competitive pressures.

Bargaining power of suppliers has been elevated in recent years due to construction materials inflation — cement, steel, and timber prices all spiked during the post-COVID supply chain disruption. YIT's scale gives it some protection through framework agreements and volume discounts, but no construction company is fully insulated from materials cost inflation. The centralised procurement that Vuorenmaa has implemented is partly a response to this force.

Competitive rivalry within Finland is surprisingly concentrated — and this concentration works in YIT's favour more than most investors appreciate. YIT's domestic competitors include SRV Yhtiöt (roughly EUR 90 million market cap), Kreate Group (EUR 140 million, focused on infrastructure), and Consti Oyj (EUR 94 million, focused on renovation). None operates at anything close to YIT's scale. The more relevant competitive comparison is with the broader Nordic peer group — Skanska, Peab, NCC, Veidekke — which operates across multiple countries with substantially larger balance sheets and market capitalisations. YIT's strategic challenge is that it is too large to compete on agility with Finnish specialists and too small to compete on scale with Nordic giants — an uncomfortable middle ground that the efficiency program is designed to resolve through margin improvement rather than revenue growth.

VIII. Capital Allocation and Financial Strategy

The balance sheet is the single most important factor in any near-term assessment of YIT, and it demands honest analysis rather than optimistic framing.

Net interest-bearing debt stood at EUR 560 million at the end of FY2025, with gearing of seventy-one percent — sitting right at the upper boundary of the company's own target range of thirty to seventy percent through the cycle. When a company is at the ceiling of its own stated comfort zone, it is by definition operating with limited room for manoeuvre. The equity ratio was thirty-eight percent, improved from thirty-four percent in 2024 but still reflecting a company where creditors own a larger share of the capital structure than shareholders would ideally prefer.

The debt structure reveals both the challenge and the sophistication of YIT's treasury operations. The company maintains a layered capital structure that includes EUR 120 million in green senior secured notes issued in March 2025 at a floating rate of three-month Euribor plus 4.75 percent, maturing March 2028. There is a EUR 100 million senior secured green note maturing in June 2027. A EUR 36 million convertible note issued in March 2024 carries an eight percent coupon with a conversion price of EUR 2.25 per share, maturing March 2029. Two tranches of EUR 100 million green capital securities — hybrid bonds that are perpetual instruments with periodic reset dates — provide quasi-equity capital. A term loan matures in January 2027, and a revolving credit facility of EUR 200 million provides liquidity backstop, with EUR 160 million unused at year-end 2025.

For non-financial readers, a quick explanation of why the pricing matters. When a company borrows money by issuing bonds, the interest rate it pays reflects how risky lenders believe the company to be. The "spread" above a benchmark rate like Euribor is the premium that compensates lenders for the risk of default. A blue-chip company might pay Euribor plus 100 basis points. A company in financial difficulty might pay Euribor plus 800.

The Euribor-plus-475-basis-points pricing on the secured notes tells you what the credit market thinks of YIT's risk profile. That is not investment-grade pricing. It is the cost of capital for a company that lenders view as meaningfully leveraged with earnings that have not yet demonstrated the stability required for lower-cost financing. Every basis point of spread above investment-grade pricing represents a direct tax on profitability — money flowing to creditors rather than to shareholders or reinvestment. In a business where operating margins are already single-digit, the financing cost differential between investment-grade and sub-investment-grade debt is not a rounding error. It is a structural headwind that compounds year after year.

Operating cash flow after investments was EUR 111 million in FY2025 — a genuine bright spot and a dramatic improvement from the cash-burning years that preceded it.

This is the number that keeps YIT's bankers comfortable. Cash generation of this magnitude — if sustained — would allow the company to reduce debt by roughly EUR 100 million per year while maintaining its operations, a deleveraging pace that would bring gearing back toward the middle of the target range within two to three years. But the run rate needs to be sustained and ideally improved for the deleveraging trajectory to work. One strong cash flow year is an encouraging data point. Two consecutive years would be a trend. YIT needs the trend.

The directed share issue of 20,960,000 new shares in 2024 — placed with institutional investors including pension funds Varma and Ilmarinen along with Conficap — was a necessary but dilutive measure to shore up the equity base. The share count expanded by roughly nine percent, diluting existing shareholders but providing capital needed to maintain covenant compliance and fund the transformation program. The Ehrnrooth family, through Tercero Invest AB, remains the anchor shareholder at 18.53 percent, with the broader family vehicle Virala Oy Ab bringing the aggregate family stake to approximately twenty percent.

The Tripla Mall refinancing announced in December 2025 enabled EUR 51 million in capital returns and profit distributions from Tripla Mall Ky to YIT — a reminder that the company's balance sheet contains real estate assets beyond the construction operations that can be monetised or refinanced when conditions permit.

Dividend policy is the most visible — and for many Finnish retail investors, the most emotionally painful — expression of YIT's financial constraints.

The dividend was suspended starting with FY2023 results, and no dividend was proposed for FY2024 or FY2025. The last payment was EUR 0.09 per share in October 2023. For a company that had been paying regular dividends for decades — EUR 0.25 per share at the post-merger peak — the suspension is painful for the Finnish institutional and retail shareholders who held YIT as an income stock. The 2025-2029 strategy targets a payout ratio of at least fifty percent of net income once financial conditions allow, but resumption requires sustained profitability that has not yet materialised. There is no realistic path to dividend resumption until the Residential Finland segment returns to profitability and the leverage ratio declines to more comfortable levels.

The inventory management challenge is where YIT's capital allocation decisions become most consequential and most visible.

Total inventories stood at EUR 1,308 million at end-2025, down from EUR 1,609 million in 2023, reflecting active efforts to reduce tied-up capital. The EUR 300 million reduction over two years is genuine progress, but EUR 1.3 billion in inventory is still an enormous number for a company with a EUR 630 million market capitalisation. Let that ratio sink in: the inventory is literally worth more than double what the stock market says the entire company is worth. Either the market is dramatically undervaluing the company, or the inventory is less liquid and less valuable than the balance sheet suggests. The truth, as usual, is somewhere in between. This inventory includes plots under development, apartments under construction, completed but unsold apartments, and the land bank itself. Each category has a different liquidity profile and a different risk exposure. Completed unsold apartments lose value if they sit too long, while land reserves appreciate or depreciate based on zoning decisions, infrastructure development, and demographic trends largely outside YIT's control.

A note on the board composition: the current board, chaired by Jyri Luomakoski — who also serves as CEO of Fiskars Corporation — includes Casimir Lindholm, CEO of Meyer Turku shipyard, and Anders Dahlblom, COO of Virala Oy Ab, the Ehrnrooth family's investment vehicle. The Ehrnrooth connection through Dahlblom gives the family direct board representation, ensuring that the largest shareholder's interests are embedded in governance rather than expressed solely through shareholder votes. It is a governance structure common in Finnish family-influenced companies, providing stability but also raising the usual questions about minority shareholder protection.

The 2026 guidance for adjusted operating profit of EUR 70 to 100 million implies meaningful improvement over the EUR 54 million delivered in FY2025. If the midpoint is achieved, it would bring leverage ratios toward more sustainable levels. But the wide range — reflecting genuine uncertainty about the pace of Finnish housing recovery — underscores how much of YIT's near-term financial trajectory depends on macroeconomic variables that management cannot control, no matter how effective the efficiency program proves to be.

IX. The Bear versus Bull Case

The bear case for YIT is straightforward, which is exactly why the stock trades where it does. Every bear argument is visible in the financial statements; there are no hidden skeletons needed to make the bearish case. The risks are on the surface, quantifiable, and real.

Start with interest rates, because in a construction company with ninety percent variable-rate mortgage exposure in its home market, rates are everything.

The ECB has begun easing, but the pace and terminal rate remain uncertain. If rates remain elevated — or if inflation resurges, forcing the ECB to pause or reverse — the Finnish housing recovery stalls. YIT's Residential Finland segment, currently loss-making, would remain in the red for another year or potentially longer. Consumer apartment starts, already at historically depressed levels, would stay depressed. The land bank, rather than being a cornered resource, becomes a millstone — generating carrying costs without producing revenue. Every quarter that the housing market stays frozen, the balance sheet deteriorates further as interest accrues on debt that is not being reduced by asset sales.

The leverage amplifies every downside risk, and this is the point where the bear case shifts from concerning to potentially existential.

Net debt of EUR 560 million against adjusted operating profit of EUR 54 million is a ratio that leaves no margin for error. A single bad quarter — a major project overrun, a client default, an unexpected impairment on the land bank — could trigger covenant pressure or force another dilutive equity raise. Construction companies with stretched balance sheets do not fail gradually. They fail suddenly, when creditor confidence evaporates and bonding capacity is withdrawn. YIT is not at that point today, but the distance between current conditions and genuine financial stress is narrower than it should be for a company of this size and heritage.

The 2029 targets — seven percent margins and fifteen percent ROCE — require roughly a tripling of profitability from current levels. The gap is enormous, and the path to closing it depends on assumptions about housing recovery, interest rates, and execution that are individually plausible but collectively ambitious. If any one of the three assumptions fails — housing stays weak, rates stay elevated, or the efficiency program stalls against the structural resistance of the construction industry — the 2029 targets become unachievable.

There is a fourth concern that sophisticated investors watch closely: management continuity.

The bear notes the management instability: a departing CFO, an interim replacement, a CEO pulling double duty as segment head, and several recent executive departures. Transformation programs require sustained leadership focus, and leadership transitions during transformation are inherently distracting, consuming management bandwidth that should be directed at operational improvement.

The bull case is equally compelling, which is why the stock has not fallen further and retains meaningful institutional ownership. The bull case requires looking through the current cyclical trough to the normalised earnings power of the underlying assets — a leap of faith that some investors are willing to make and others are not.

Begin with the land bank — the single most important asset on YIT's balance sheet and the one that the bear case most dramatically undervalues.

Approximately EUR 720 million at book value, supporting thirty thousand future homes across Finland and CEE. In a normalised housing market, this land bank would generate hundreds of millions in revenue per year as plots are developed and apartments sold. The current depressed valuation — YIT's entire enterprise value of roughly EUR 1.75 billion includes the land bank, the operating businesses, the order backlog of EUR 2.9 billion, the brand, and the institutional knowledge — arguably undervalues the land alone. If you could buy thirty thousand buildable residential plots in Helsinki, Tampere, Prague, and Warsaw for EUR 720 million, you would do it without hesitation. The land is real. The demand, when rates normalise, will be real. The only question is timing — and timing, for a leveraged company, is not a trivial caveat.

The second pillar of the bull case is the data centre opportunity, which transforms YIT's growth narrative from a pure housing recovery story to a structural demand story that has nothing to do with mortgage rates or consumer sentiment. Finland's emergence as a preferred destination for hyperscale data centres creates a pipeline of high-value, creditworthy construction contracts that are independent of the residential cycle. If data centre investment continues growing at current rates — and every major technology company's capital expenditure plans suggest it will — the Building Construction and Infrastructure segments could more than compensate for continued housing weakness.

The third pillar of the bull case is the efficiency program itself.

If it delivers on the remaining capital release and margin improvement targets, it could unlock a dramatically different financial profile. Construction companies that achieve genuine operational efficiency — standardised procurement, data-driven bidding, disciplined capital allocation — trade at significantly higher multiples than those perceived as project-driven businesses with volatile margins. If YIT can demonstrate sustained improvement in ROCE toward the fifteen percent target, the multiple re-rating alone would generate substantial shareholder value, because the starting point is so depressed.

The fourth element of the bull case is the valuation itself, which provides a margin of safety for patient investors.

At EUR 2.73 per share and a market capitalisation of EUR 630 million, YIT trades at a price-to-book ratio of approximately 1.1 times and a price-to-sales ratio of just 0.41 times. The stock has traded as low as EUR 2.20 over the past year and as high as EUR 3.38 — a fifty-three percent range that reflects the market's genuine uncertainty about the direction of the business. Among Nordic construction peers, these are among the lowest multiples in the sector. Skanska, Peab, and NCC all command materially higher valuations relative to both book equity and revenue. The discount reflects YIT's leverage and depressed earnings, but if earnings normalise, the gap could close rapidly — and the upside from multiple expansion on a recovering earnings base compounds powerfully.

Finally, the ownership structure itself provides a form of downside protection that is easy to overlook.

The Ehrnrooth family's continued anchor shareholding at approximately twenty percent provides a degree of strategic patience that a dispersed shareholder base might not. The family's investment horizon is generational, not quarterly, and their willingness to support the transformation — including the dilutive 2024 share issue — suggests confidence that is backed by meaningful capital at risk.

So which view is correct?

The honest answer is that both the bear and bull cases are well-supported by evidence, and the outcome depends almost entirely on variables — ECB policy, Finnish housing demand, data centre investment trends — that are outside management's control. What management can control is efficiency, and there the early signs are encouraging but not yet conclusive.

For investors tracking this story, two KPIs matter above all others.

The first is Return on Capital Employed (ROCE), currently at 3.9 percent against a 2029 target of at least fifteen percent. ROCE captures everything that matters about YIT in a single number: revenue growth, margin improvement, and capital efficiency. It measures how effectively the company converts its enormous invested capital base — the land bank, the work in progress, the machinery, the operating infrastructure — into profits. A sustained trajectory toward double-digit ROCE would validate the entire transformation thesis. Stagnation in the low single digits would signal that the capital intensity of construction is simply too great for any efficiency program to overcome.

The second is the unsold completed apartment count in Finland. This metric, reported quarterly, measures the inventory of finished apartments that have not yet been sold to consumers. It is the most sensitive real-time indicator of housing market conditions and YIT's ability to convert completed construction into cash. A declining unsold count — driven by rising consumer demand, improved mortgage conditions, or creative sales programs like the interest rate cap — would signal that the housing cycle has turned and that Residential Finland is approaching profitability. A rising count would signal continued distress and further cash consumption in a segment that is already bleeding money.

Together, these two metrics tell you everything you need to know about whether YIT's transformation is working.

ROCE tells you whether the company is becoming more efficient — whether the massive capital base tied up in land, buildings, and equipment is generating returns that justify the investment. The unsold apartment count tells you whether the market is cooperating — whether Finnish consumers are returning to the housing market with enough confidence and purchasing power to absorb the apartments that YIT builds.

Both need to move in the right direction for the investment thesis to play out. If ROCE improves but apartments remain unsold, the efficiency gains are being consumed by working capital costs. If apartments sell but ROCE stagnates, the company is growing without improving profitability — a treadmill that benefits customers more than shareholders.

X. Epilogue: The Bellwether

Stand on the rooftop of Tripla — the massive mixed-use complex in Helsinki's Pasila district that YIT developed, combining a shopping centre, hotel, residential towers, and a rail station into a single integrated urban project — and you can see the entire arc of the company's ambition laid out across the Helsinki skyline.

Tripla itself is a monument to what YIT can achieve at its best: a 180,000 square metre development that transformed a derelict rail yard into one of Finland's most important urban nodes, connecting three forms of public transport with commercial, residential, and hospitality uses. It is also a reminder of the capital intensity of the business — projects of this scale tie up hundreds of millions of euros for years before generating returns. To the south, the traditional city centre, built with the construction methods and materials that YIT mastered over a century. To the north, the suburban sprawl that absorbed a generation of apartment construction. And in between, data centres under construction, infrastructure projects reshaping the urban landscape, and residential developments that are either filling with buyers or sitting empty, depending on where you look and when you look.

To the south, the traditional city centre, built with the construction methods and materials that YIT mastered over a century. To the north, the suburban sprawl that absorbed a generation of apartment construction. And in between, data centres rising alongside infrastructure projects, residential developments waiting for buyers, and the physical evidence of a company caught between its glorious past and its uncertain future.

YIT is, in many ways, a bellwether for the entire Finnish economy — a barometer of national confidence expressed in concrete and steel. When Finland builds, YIT builds. When Finland's housing market freezes, YIT freezes with it. When Finnish infrastructure investment accelerates — driven by energy transition, data centre construction, or the NATO-era defence spending that Finland's 2023 accession to the alliance has begun to catalyse — YIT is positioned to capture a disproportionate share. The company's fortunes are inseparable from the country's, which is both a source of stability and a ceiling on ambition.

The lesson that YIT's 114-year history teaches is deceptively simple but fiendishly difficult to execute in practice: you cannot build your way out of a bad capital structure, but you can, with sufficient discipline and patience, efficient your way into a new competitive position. The building is the easy part. The efficiency is the hard part. And the patience — well, patience is what separates the investors who profit from cyclical lows from those who give up too early or arrive too late. The Lemminkäinen merger added scale but also complexity and debt. The Russian exit removed risk but also earnings. The transformation program is removing costs but requires time — and time, for a company with YIT's leverage profile, is the most expensive resource of all.

Heikki Vuorenmaa's bet is that there is enough time. That the ECB will continue easing. That the Finnish housing market will recover before the balance sheet is stretched to breaking point. That data centres will keep coming. That the efficiency gains are structural and not merely cyclical windfalls that will fade when the next construction boom encourages the return of old habits. That the land bank will prove to be worth multiples of its current book value when the cycle turns. That the 2029 targets represent a genuine destination rather than a mirage that recedes with every step forward.

But there is a counter-argument, and it deserves equal weight.

The counter-argument is that construction is construction. That the industry's resistance to productivity improvement is not a failure of management but an intrinsic feature of the work itself — each project unique, each site different, each set of conditions demanding local adaptation that defies the standardisation playbook. That YIT's margins are thin not because the company is poorly run but because the industry punishes capital deployment in ways that no amount of McKinsey methodology can structurally overcome.

Both views contain truth. The construction industry's historical resistance to efficiency improvement is not a myth — it is documented across decades of academic research and industry data. But it is also true that some construction companies, in specific markets, with specific management teams, have achieved meaningfully better returns than the industry average. The question is whether YIT can be one of them, and the answer will not be known for several more years.

The investment case for YIT ultimately rests on which truth proves more powerful: the structural challenge of construction economics, or the specific opportunity created by a dominant market position, a cornered land resource, and a leadership team with both the mandate and the personal incentive to transform. At EUR 2.73 per share, the market is offering its assessment — but the market's assessment and the correct assessment are not always the same thing, and the gap between them is where patient investors either build wealth or learn expensive lessons about the difference between value and a value trap.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube