Wise: The Architecture of Money Without Borders

I. Introduction: The "Magic" of the Spreadsheet

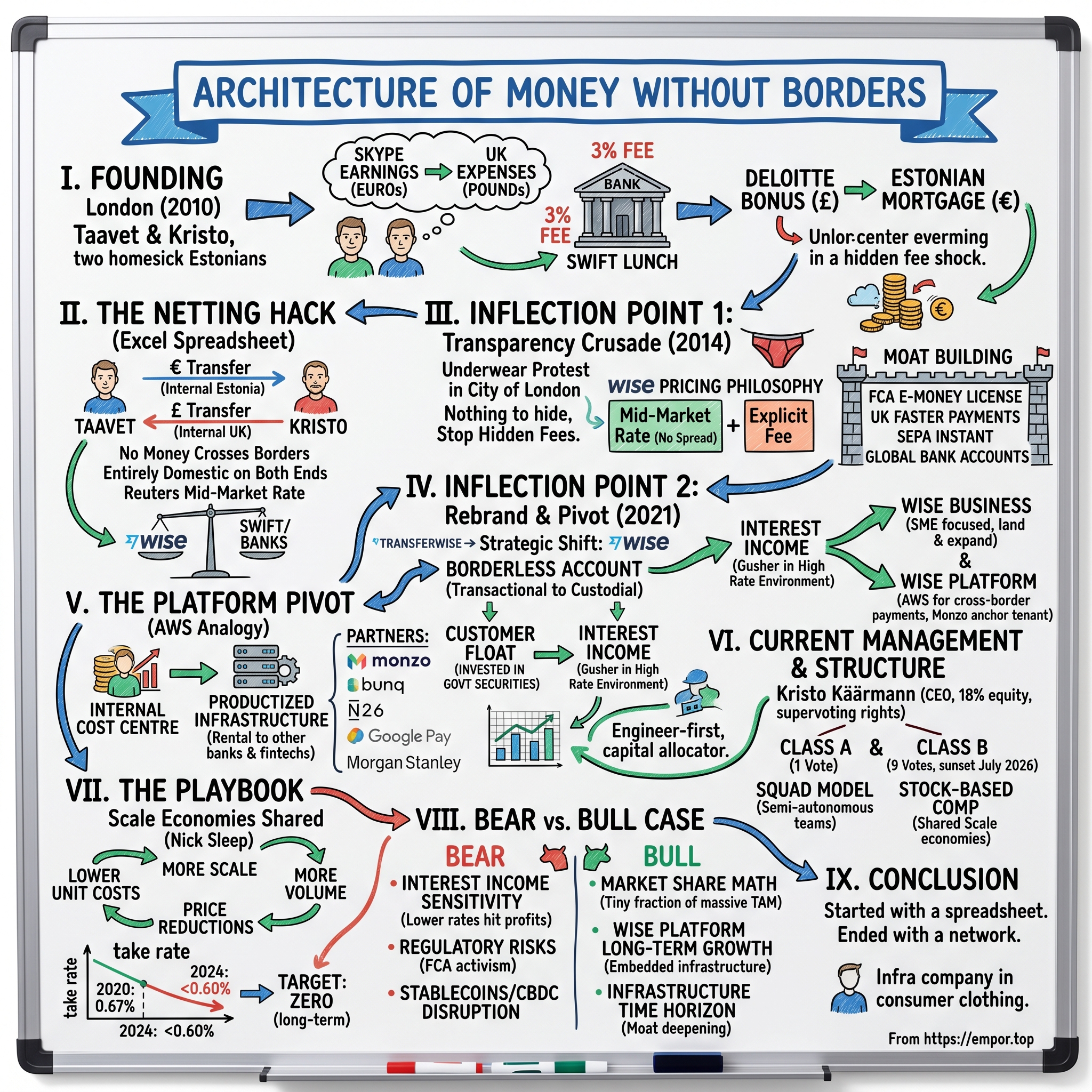

Picture London in the autumn of 2010. A twenty-something Estonian named Taavet Hinrikus walks into a branch of one of the high street banks, staring at the exchange rate flashing on the screen behind the teller. He is still being paid in euros by Skype, the company he was the very first employee of, but his rent, his groceries, his Oyster card top-ups—all of it has to come out in pounds. Every time he moves money across the Channel, the bank quietly skims two, sometimes three percent off the top. On the other side of town, a friend of his, Kristo Käärmann, is facing the mirror-image problem. He is a management consultant at Deloitte, paid in pounds, with a mortgage back home in Estonia denominated in euros. Every transfer home is an act of slow, ritualised wealth destruction.

Then one evening, over coffee, the two of them—both trained as engineers, both programmed to seek arbitrage—realise the absurdity of their situation. Taavet needs pounds. Kristo needs euros. Taavet has euros. Kristo has pounds. They did not need a bank. They did not need SWIFT. They needed an Excel spreadsheet and a little trust. Taavet would look up the mid-market rate on Reuters, Kristo would transfer pounds to Taavet's British account, Taavet would transfer euros to Kristo's Estonian one. No money crossed a border. No correspondent bank took a bite. The "international" transfer was, in fact, entirely domestic on both ends. They were, without quite realising it yet, running their own tiny clearing house.

That, in a single image, is the entire thesis of this episode. A business now valued at over £9 billion, processing more than £140 billion of customer money a year, doing what investors like to call "eating SWIFT's lunch"—all of it was, at its core, a spreadsheet hack between two homesick Estonians. The question the market has been asking for fifteen years is whether that hack scales into something like the "AWS of cross-border payments," a set of pipes the rest of the financial system quietly leases, or whether it settles into being a very good, very cheap remittance app that the giants eventually clone.

The roadmap for this episode takes us from the "Estonian Mafia" that Skype spawned, through the guerrilla underwear protests in the City of London, past the 2021 rebrand and direct listing, and into the far more interesting and less understood parts of the business today: Wise Business, Wise Platform, and the enormous pile of customer float now earning interest inside their balance sheet. Along the way we ask how a company that insists on lowering its own take rate every year has managed to compound revenue so fast, how its CEO survived a very public tax scandal, and whether the arrival of stablecoins rewrites or reinforces the rails Wise has spent a decade laying down.

It is a story, ultimately, about a strange kind of ambition. Most fintech founders wanted to build the next bank. Taavet and Kristo wanted to build the thing that made the border itself disappear. The difference turns out to matter enormously.

II. The Founding & The "Netting" Hack

Tallinn in the early 2000s was an unlikely place to birth a generation of global software companies. Still shaking off the Soviet hangover, the country had made a deliberate, almost civic-religious bet on digitisation—every citizen got a digital ID, filing taxes took under five minutes, school children learned to code, and by 2005 you could vote online from your couch. Out of this petri dish came Skype, a peer-to-peer voice app that did to international phone calls what Wise would later do to international money. Taavet Hinrikus, a lanky, soft-spoken engineer, walked into Skype's Tallinn office as employee number one, later running business development and watching from the inside as the company was sold to eBay for $2.6 billion in 2005 and to Microsoft for $8.5 billion in 2011. The payout was life-changing. The lesson was larger: a tiny team from a tiny country, armed with nothing but internet protocols and a disdain for incumbents, could punch a hole through a telecom cartel that had lasted a hundred years.

Kristo Käärmann's path was less romantic, more plodding, and in a way more decisive. He had trained as a mathematical engineer, moved to London to work at Deloitte and later PwC, and spent his days inside the engine rooms of big banks—doing integration work, stress testing, and, crucially, watching in horror how much of the financial system still ran on FTP file dumps, overnight batches, and nested foreign exchange markups. When Kristo bought a home in Estonia and tried to remit his Christmas bonus of £10,000, he discovered HSBC had quietly charged him about £500 through a shaved exchange rate. The shock was not the fee. The shock was that no one at HSBC had ever lied to him—the fee was simply invisible, wrapped inside the rate itself. For an engineer, invisibility is a deeper sin than theft.

The netting hack the two of them worked out over coffee sounds almost too obvious once you say it aloud. If at any given moment there is roughly as much money wanting to flow from London to Tallinn as from Tallinn to London, you do not need to actually move anything across borders. You just pair the flows off, credit local accounts on each side, and pocket a tiny fee for doing the matching. The insight was not that this was technologically impossible before—banks had been netting interbank positions for decades—but that no one had turned the trick around and offered it directly to consumers. Banks made too much money on the old way to disrupt themselves.

TransferWise, as it was originally called, launched in January 2011. The early product was almost embarrassingly simple—a website, a handful of corridors, and a founder pair personally answering customer emails from a shared flat. Their first real oxygen came in 2012, when the company won the TechCrunch Disrupt London competition and, more importantly, caught the attention of Index Ventures and Peter Thiel's Valar Ventures, who led a Series A of roughly $6 million. Thiel, who rarely invests outside the Bay Area, reportedly liked the fact that the founders had chosen London rather than Silicon Valley. His reasoning was almost counter-intuitive: regulation in financial services is a moat, and you want to be moated where the regulators take you seriously.

The choice of London over Tallinn or San Francisco turned out to be one of the most consequential decisions of the company's life. London gave them the Financial Conduct Authority, one of the few regulators on earth that was willing to grant e-money licences to scrappy startups; it gave them access to SEPA and UK Faster Payments; and it gave them a talent pool of disillusioned ex-bankers who knew exactly how much fat was in the system. It also, crucially, gave them a time zone that overlapped with both Asia and the Americas—a detail that mattered when you were trying to build a product that literally never stopped moving.

The net effect, by the end of the company's first two years, was a tiny team, a tiny product, and a mathematically enormous idea: eighty percent of cross-border flows, they gradually realised, could be netted rather than truly transferred. The rest of the story is essentially what happens when you let that insight run for fifteen years.

III. Inflection Point 1: The Transparency Crusade

In April 2014, a group of bewildered City of London commuters looked up from their morning coffees to see a crowd of about fifty people, mostly men, marching down Cheapside in their underwear. They were carrying signs that read "Nothing to hide" and "Stop hidden fees." At the front of the parade, shivering slightly under the grey London sky, were Taavet and Kristo themselves. It remains one of the most perfectly on-brand marketing stunts in European fintech history—a British-by-way-of-Estonia cocktail of earnestness and absurdity that somehow captured the entire worldview of the company in a single image. The message was not subtle. Banks, the underwear protest was saying, are hiding things. We are not.

That was the surface of it. The substance was a pricing philosophy that, at the time, was genuinely radical. Wise decided it would always show customers the mid-market rate—the same rate two banks use with each other on the interbank market, the one you see on Reuters or Bloomberg—and then charge a separate, explicit fee on top. A transfer of £1,000 to euros might cost you £4 and change. You saw the £4. You saw the rate. Nothing was hidden inside the spread. This sounds obvious. It was not obvious. Every other player in the market, from Western Union to the big banks to the "zero commission" upstarts, made their real money in the exchange rate itself, which meant a customer sending $1,000 might lose $40 and never see a line item for it.

The audacity of the strategy was that it often made Wise look more expensive in side-by-side comparisons. If a competitor advertised "zero fees" and quietly took three percent in the rate, and Wise charged a visible 0.5% fee on a tight rate, the unsophisticated buyer saw "free" and picked the competitor. Wise bet, correctly, that the sophisticated buyer would do the maths once and become a customer for life. Retention curves in their early cohorts were the kind of numbers you usually see in software, not financial services—eighty-plus percent of revenue in a given year came from customers who had been there the year before.

The underwear protest was only the most visible expression of a broader cultural posture. Wise's marketing team spent years running campaigns that essentially mocked its competitors—posters on the London Underground showing how much HSBC or Barclays would charge for the same transfer, animated explainers deconstructing correspondent banking, a "Stop Hidden Fees" petition filed with the European Commission. For a while, the company behaved less like a startup and more like a political movement with a revenue line. That was intentional. Kristo in particular believed that trust was the scarce resource in financial services, and that the only way to earn it at scale was to make transparency a weapon rather than a virtue.

Behind the campaigns, the operational lift was brutal. To actually deliver on the netting model, Wise needed to hold real bank accounts, in real local currencies, in real countries. That meant walking into a bank in Budapest or Kuala Lumpur or São Paulo and convincing a compliance officer that you were not laundering money for cartels. It meant obtaining e-money licences in the UK, the US (state by state, a Sisyphean exercise), Singapore, Australia, Canada, Japan, and eventually over fifty jurisdictions. By the mid-2010s, Wise had built something its competitors would spend the next decade trying to replicate: a sprawling, unglamorous network of local banking relationships and direct access to domestic payment systems like the UK's Faster Payments, the Eurozone's SEPA Instant, and eventually the US Federal Reserve's FedNow. Each integration took years, cost millions, and was essentially invisible to the customer. But each one removed another layer of correspondent banks—the intermediaries that had historically eaten margin every time money crossed a border.

The lesson embedded in the transparency crusade, and the reason it matters for anyone thinking about the business as an investment, is that Wise discovered early that its real moat was not software. Anyone can build a website that quotes an exchange rate. The moat was the regulatory surface area and the plumbing. And the transparency marketing was, in a sense, just the brand layer on top of that plumbing—a way of pre-announcing to customers that if they came to Wise, they would be coming into a different system entirely. It made the switching costs psychological as well as functional, which turned out to matter a great deal when the product went from being a one-shot transfer tool to something much closer to a bank account.

IV. Inflection Point 2: The Rebrand & The Platform Pivot

On the morning of February 22, 2021, customers who logged into their TransferWise app were greeted by an unfamiliar green logo and a new name that had lost a syllable. "Wise." Just that. The rebrand was announced in a short, almost curt blog post by Kristo, who had by then taken over as sole CEO after Taavet stepped back from day-to-day operations. To outsiders, it looked like a cosmetic exercise—the kind of thing marketing agencies bill six figures for. Inside the company, it was a very explicit declaration that the business had outgrown its founding product. "Transfer," the verb, was a description of what they did on day one. It was no longer what they did.

The setup for the rebrand had actually begun four years earlier, in 2017, when Wise launched what it called the "Borderless Account," later renamed the Multi-Currency Account. On the surface, it was a deposit-like account that could hold balances in dozens of currencies simultaneously—you could leave money sitting in euros, convert a chunk to yen when the rate was favourable, and spend directly from a Mastercard-branded debit card linked to any of the balances. Underneath, it was a profound strategic shift. For the first six years of the company's existence, Wise had been a transactional business: you showed up, sent money, went away. The Multi-Currency Account turned Wise into a custodial business: you showed up and stayed. Money sat on Wise's balance sheet. The customer relationship became continuous rather than episodic.

That single product change did three things that turned out to matter enormously. First, it transformed the unit economics—customers who held balances transacted far more often and referred more aggressively, which pushed customer acquisition cost down and lifetime value up. Second, it gave Wise a cost of funds problem that quickly revealed itself to be a cost of funds opportunity: customer deposits, though legally segregated and held in partner banks rather than on Wise's own balance sheet, could be invested in short-duration government securities. When interest rates were at zero, this was a nuisance. When rates rose in 2022 and 2023, it became a gusher. Third—and this is the subtlest effect—the Multi-Currency Account repositioned Wise from a remittance company to something more like a consumer bank, which in turn changed the kind of customer who found the product attractive. Expats, digital nomads, freelancers on Upwork, cross-border e-commerce sellers, even small hedge funds—anyone whose life or business straddled more than one currency—started treating Wise as their primary operational account.

Dropping "Transfer" from the name was thus the acknowledgement of a reality that had existed for years. But it was also a flag planted for the next chapter. By 2021, something quietly important was happening in the back office: other financial institutions had started asking whether they could plug into Wise's rails. Monzo, the UK challenger bank, was the first high-profile partner, using Wise to power its international transfers. Then came Bunq in the Netherlands, N26 in Germany, and eventually unexpected names like Shinhan Bank in South Korea and Morgan Stanley's client operations in the US. The rebrand carved out space for this B2B business—Wise Platform—to exist without confusing the consumer brand. You cannot easily sell API access to a bank if your brand name includes the word "Transfer," which to a CFO sounds like a consumer product rather than infrastructure.

The other thing that is worth pausing on is what Wise did not do during the 2021 fintech bubble. While PayPal spent $2.7 billion buying the Japanese buy-now-pay-later company Paidy, while Robinhood went public at an $32 billion valuation, while Revolut raised a round valuing it at $33 billion, Wise's M&A record in the period was almost conspicuously restrained. The company made a handful of tiny acqui-hires—engineering teams in Hyderabad and Singapore, a credit-card tokenisation startup, a small compliance tools outfit—and stayed away from the big, splashy, customer-acquisition-driven deals that were the fashion of the moment. Kristo said in multiple interviews that he looked at the peer acquisitions and could not make the maths work at those prices. In retrospect, given the subsequent re-rating of the fintech sector, this restraint looked less like timidity and more like a very specific kind of capital discipline—the kind usually associated with much older companies than Wise.

Then, on July 7, 2021, Wise chose to list on the London Stock Exchange via a direct listing rather than a conventional IPO. The opening reference price implied a market capitalisation of about £8 billion. No investment bank priced it, no institutional allocation happened, no lock-ups beyond the normal post-listing restrictions were imposed. Employees and early investors could sell from day one. The direct listing was a deliberate statement: Wise did not need the syndication machinery of Goldman Sachs or Morgan Stanley to find buyers, because it already had a waiting list of retail customers and institutional funds that had been trying to buy secondary shares for years. It was also, in classic Wise style, a transparency statement—no underwriting spread, no "IPO pop" going to favoured clients, just a public market finding a price on its own.

The decision to list in London rather than New York, incidentally, remains controversial. Detractors argue Wise would trade at a richer multiple in the US; defenders point out that the company's European regulatory centre of gravity is in London and that getting a hometown listing locks in political goodwill with the FCA. The listing also gave the company the dual-class share structure that now dominates the rest of this story.

V. Current Management & Ownership Structure

To understand Wise as an investment, you eventually have to reckon with the fact that it is, in a very practical sense, Kristo Käärmann's company. Co-founders who stay on after a listing are common. Co-founders who still own roughly eighteen percent of the equity and wield enhanced voting rights are uncommon. Co-founders who do both while being the sitting CEO are rare enough that the structure itself becomes a key variable in the investment thesis.

Kristo's style has been, by his own description, "engineer-first." He is known inside the company for sending detailed written memos rather than holding meetings, for insisting that every price cut be accompanied by a clear accounting of where the savings came from, and for publishing an annual mission roadmap that reads less like a marketing document and more like a software release note. He is also famously unpolished in his public appearances—Estonian-accented, prone to long pauses, occasionally visibly impatient with journalists who ask questions he considers obvious. There is a mildly famous clip of him at a 2022 conference, responding to a question about whether Wise would get into crypto, by simply saying "No," and then refusing to elaborate. Investors who like their CEOs to be masters of spin do not like Kristo. Investors who prefer their CEOs to act like capital allocators tend to like him very much.

The dual-class share structure, introduced at the 2021 direct listing, is a Class A/Class B design common in American tech but unusual in the UK. Class B shares carry nine times the voting rights of Class A shares, but only for a fixed period—five years from listing, meaning the supervoting structure sunsets in July 2026 unless shareholders vote to renew it. The Class B shares are held by the "Owners Group," a set of employees and early backers who took a public pledge to stay aligned with the long-term mission of the company. Kristo is the largest member. Taavet retains a substantial but diminished stake. Index Ventures, Valar, and Baillie Gifford remain significant institutional holders.

The sunset is worth dwelling on. In mid-2026, Wise's governance will either revert to one-share-one-vote or the company will have to persuade its minority shareholders to extend the dual-class structure. This matters because at that point the company's biggest strategic decision—whether to re-domicile or dual-list in the United States—will likely be on the table. The FT and others have been reporting for over a year that Wise has been looking seriously at a US secondary listing, partly for valuation reasons and partly because the company's fastest-growing segment, Wise Platform, has more potential banking customers in the US than anywhere else. Whether that move happens, and whether it is done with or without a change in governance, will say a great deal about Kristo's priorities.

The most difficult chapter in the CEO's recent history was his 2021 tax problem. In September of that year—just two months after the direct listing—the FCA disclosed that Kristo had been fined £365,651 by HMRC for failing to pay his 2017/18 UK tax bill on time. The amount owed was over £720,000, eventually paid in full, but the late filing put him on HMRC's list of deliberate defaulters. The FCA opened its own investigation into whether he was a "fit and proper person" to run a regulated firm. In 2024, that investigation concluded with a further fine of £350,000 directly from the FCA and a finding that while Kristo had failed to notify his primary regulator of the tax issue as he was required to do, he remained fit and proper. The market's reaction was essentially a shrug; the share price had largely digested the overhang during the three-year investigation, and by the time the resolution came, the business had compounded so substantially that the episode looked like a footnote rather than a chapter. It is nevertheless a permanent part of the record, and it illustrates a recurring theme in Wise's governance: the company is willing to tolerate significant personal risk at the top in exchange for founder-led clarity.

Below Kristo, the senior team is heavily Estonian and heavily alumni-of-the-founding-cohort. Harsh Sinha, the CTO, has been in the company for over a decade and is the closest thing Wise has to an engineering cultural totem. Matt Briers, the long-standing CFO, took a medical leave of absence in 2024 and was replaced on an interim and then permanent basis; his departure was handled with unusual grace and the finance function continued to operate cleanly through the transition. The CEO of Wise Platform, Steve Naudé, has become an increasingly visible figure, which itself is a signal about where the company believes its future growth lives.

The deeper cultural artefact inside Wise is what employees—who internally call themselves "Wisers" rather than any more saccharine variant—refer to as the "squad model." Borrowed loosely from Spotify's engineering playbook, it organises the company into small, semi-autonomous teams with end-to-end ownership of a product area. Squads set their own roadmaps, hire against their own budgets, and are held accountable by a small set of company-wide metrics—speed of transfer, price, customer growth—rather than top-down feature lists. This is a far cry from the traditional banking hierarchy, where decisions move up and down org charts like batch files. The result is an organisation that ships product updates several times a day and deprecates underperforming experiments without needing executive cover. It also means that the CEO's job is less about managing operations and more about setting constraints—on price, on risk, on mission alignment—and then getting out of the way.

The stock-based compensation regime reinforces this autonomy. A meaningful portion of Wisers' total comp is paid in equity that vests over four years, and the company has historically been aggressive about extending grants deep into the organisation. The phrase you hear often in internal documents is "scale economies shared"—a direct nod to the Nick Sleep letters that circulate as spiritual literature inside the senior team—which captures the idea that as Wise grows, the benefits flow first to customers through lower prices, second to employees through equity, and only third to shareholders. In practice, this has meant that operating margins expand more slowly than revenue, which has at times frustrated investors who wanted faster profit growth. It has also meant that Wise has not had to bleed talent to Silicon Valley competitors the way many London fintechs have.

Whether the "shared" half of "scale economies shared" eventually shifts more toward shareholders—especially as the Multi-Currency float becomes a genuinely massive interest-income business—is one of the live debates on the stock.

VI. The "Hidden" Businesses: The Next Growth Engine

Here is a useful mental model. Imagine Wise is an iceberg. The part everyone sees—the TikTok ads, the branded debit cards, the app that expats use to send rent to their landlords in Lisbon—is the consumer business, which still makes up the majority of revenue. Now imagine the three-quarters of the iceberg under the waterline. That is Wise Business, Wise Platform, and the interest income on the customer float. The consumer business is what got Wise to roughly £1.3 billion in annual revenue by FY2024. The submerged three-quarters is what the bull case argues gets them to £5 billion or £10 billion over the next decade.

Start with Wise Business, the SME-focused arm of the company. SMEs—small and medium-sized enterprises—are, from a bank's perspective, a commercial problem disguised as a commercial opportunity. They are small enough that a traditional corporate banker cannot profitably serve them (the relationship manager costs more than the account generates), but complex enough that consumer banking products do not fit them (payroll in five currencies, supplier invoices from eight countries, tax obligations in three jurisdictions). The result is that millions of small exporters, e-commerce merchants, freelance agencies, and cross-border consultants have historically been stuck with bad tools and worse fees.

Wise Business attacks this segment with essentially the same Multi-Currency Account that consumers use, dressed up with batch payments, API access, accounting software integrations (Xero, QuickBooks), team permissions, and a set of receiving account details that let an SME in Manchester get paid in US dollars as if they had a US bank account. The commercial logic is that SMEs transact more per account, hold larger balances, and churn less than consumers. Wise Business revenue has been growing at a meaningful premium to the consumer segment for the last several years, and internal commentary suggests the cohort-level lifetime value is several multiples of the retail cohort. Crucially, the gross take rate for the business product is typically lower than retail—SMEs do larger transfers, which Wise prices at lower basis points—but the net contribution margin is higher because the same customer transacts many more times per year. This is the "land and expand" pattern familiar to anyone who has watched SaaS businesses: acquire the account for the cheap first product, let volume compound, and monetise through depth rather than price.

The second, and in many ways more strategically interesting, segment is Wise Platform. This is the company's B2B API business—the one that lets other banks, fintechs, and even non-financial companies plug into Wise's rails and offer international transfers under their own brand. Monzo was the anchor tenant; customers who sent money internationally from the Monzo app were, without necessarily knowing it, being routed through Wise's infrastructure while seeing Monzo's user interface. From there the partner list has metastasised. Mexico's Nubank. Japan's GMO Aozora. Singapore's Standard Chartered. Google Pay in the United States for remittances to India, the Philippines, and Singapore. Morgan Stanley for client operational cash. By late 2025, Wise had disclosed over ninety platform partners globally, with several of the largest contributing materially to overall volumes.

The AWS analogy is overused in tech commentary, but it is genuinely applicable here. In the early 2000s, Amazon spent years building internal infrastructure for its retail operation—storage, compute, databases—and then realised the same infrastructure could be rented to third parties who did not want to build their own. AWS emerged not as a greenfield bet but as a productisation of an existing cost centre. Wise's cross-border infrastructure—local bank accounts in every major corridor, direct connections to Faster Payments, SEPA Instant, ACH, PIX in Brazil, and so on, plus the compliance and KYC machinery to move money across all of it—was built for the consumer business. Wise Platform turns it into something other financial institutions can rent.

Why would a bank choose to rent rather than build? The simple answer is that building your own cross-border network from scratch is a ten-year project with an unclear ROI. A mid-sized regional bank in Asia looking to offer remittance services to its customer base can spend five years and fifty million dollars trying to replicate a subset of what Wise has, or it can integrate Wise's API in three months and split the margin. For most banks, the make-versus-buy calculation is not close. Wise Platform also benefits from a curious competitive dynamic: the more banks it onboards, the more it validates the model to the next bank, while simultaneously denying competitors the reference customers they would need to build a credible alternative. It is, in Hamilton Helmer's language, a network economy wrapped around a cornered resource.

The third, and in the near term most financially consequential, hidden business is the interest income generated on customer float. When a Wise Multi-Currency Account holder leaves £10,000 sitting in their GBP balance overnight, that money is not held on Wise's own balance sheet—it is legally safeguarded in segregated accounts at partner banks and, where regulation permits, in short-duration government securities. Historically, in the zero-interest-rate era of 2011–2021, this was a cost, not a revenue line. But when the Bank of England and the Federal Reserve began aggressively raising rates in 2022, the same deposits suddenly started earning four, five, even five-and-a-half percent yields.

Wise, to its credit and controversially, started passing some of that interest back to customers through a feature called "Assets" (in some markets rebranded as "Interest" or "Stocks"), which let users opt in to receive a portion of the yield on their balances. But the economics are such that even after sharing, the net interest income to Wise ballooned. By FY2024, interest income from customer balances accounted for close to a third of total revenue—a number which, when rates start falling, will compress, but which also represents a structurally new profit stream that did not exist five years ago. The key investor question is how much of this is "normalised" and how much is a one-off gift from the Fed. The bull argument is that customer balances keep growing even as rates normalise, so the absolute dollar contribution holds up. The bear argument is that a world of 2% policy rates halves the contribution overnight.

The common thread running through all three of these hidden businesses is that they emerge organically from the consumer product—they are not new businesses so much as byproducts of the core infrastructure being large enough to have useful exhaust. That is the mark of a genuine platform: the same underlying capability generates more than one P&L line without meaningful additional capex. It is also the reason that Wise's long-term operating leverage story is more interesting than a casual reading of its income statement suggests.

VII. The Playbook: Seven Powers & Strategic Analysis

Strip away the brand, the protests, the Estonian accents, and the story of Wise is ultimately a story about a specific kind of feedback loop. It is the kind of loop that Nick Sleep, the legendary Nomad Investment Partnership manager, obsessed over in his letters on Costco, Amazon, and Berkshire Hathaway. He called it "scale economies shared." The idea is disarmingly simple. Most businesses, as they get bigger, find that their unit costs fall—cheaper procurement, better labour productivity, spread of fixed costs. Most businesses then pocket this scale benefit as margin expansion. A small minority of businesses do the opposite. They take the cost savings and hand them back to customers in the form of lower prices, which drives more volume, which drives more scale, which drives more cost savings, which funds more price cuts. The loop, once started, is almost impossible for competitors to break, because any rival who does not share must either accept inferior unit economics at the same price, or match the price and burn cash forever.

Wise's public pricing history is almost a laboratory demonstration of this loop. In 2020, the average "take rate"—the fee Wise charged as a percentage of the amount transferred—was 0.67%. By 2024, it was below 0.60%. The stated goal, embedded in the Wise mission roadmap, is to push it toward "zero" over the very long term, not because the company wants to be a charity, but because it believes the equilibrium take rate for commoditised cross-border transfers is close to the cost of operating the rails, and it would rather be the operator at equilibrium than the victim of someone else reaching it first. Management openly tells shareholders that any time unit costs fall, they will prefer to pass most of it through as price reductions. For an investor used to SaaS businesses, where price leverage is the whole point, this can be disorienting. For an investor used to Costco, it is the model working as designed.

Stacking this against Hamilton Helmer's Seven Powers framework gives a useful audit of where the competitive moat actually lives. Cornered Resource is the most obvious one—Wise's direct integrations into local payment systems are, individually, unremarkable, but collectively they represent a regulatory and operational footprint that would take a competitor five to seven years of dedicated effort to replicate, and that is if the regulators in question were feeling generous. In several key markets—the UK being the most notable—Wise was among the first non-bank institutions granted direct participation in the domestic payment system, a privilege that required not just an e-money licence but a sustained track record of operational stability.

Switching Costs, the second Power, are more subtle and arguably more important. A customer who uses Wise only for a one-off transfer has zero switching cost and will go wherever is cheapest next time. A customer who has adopted the Multi-Currency Account as their de facto financial operating system—direct deposit of their salary, recurring payments to landlords in two countries, an invoicing workflow integrated with Xero, a debit card they use in local currency when they travel—is in a completely different category. Moving that setup to a competitor involves changing direct deposit instructions across multiple employers, updating counterparties, and re-integrating accounting software. The psychological friction is often bigger than the financial friction. This is exactly analogous to the stickiness of a primary banking relationship, which is why banks have historically traded at such rich multiples on deposit bases.

Scale Economies, the third Power, feed the shared-scale loop described above. Network Economies show up most clearly in Wise Platform, where each new bank partner increases the gravitational pull of the network on the next prospective partner. Process Power—the accumulated operational knowledge of running a regulated business across fifty jurisdictions without a major compliance incident—is the least glamorous Power but arguably the hardest to replicate in short order. Branding is real but limited; Wise is a household name among expats and freelancers but not yet at the Visa-or-Mastercard level of consumer recognition. Counter-Positioning, the seventh Power, is where the story is most vivid: the incumbent banks cannot match Wise's pricing without cannibalising their own far-more-profitable FX desks, which generates a structural asymmetry that favours the entrant. Every time Wise cuts prices, HSBC and Citi are faced with a choice: match and kill their own margin, or ignore and slowly cede share.

Porter's Five Forces gives another cut. Threat of New Entrants is moderated by the regulatory surface area; any new fintech hoping to offer global cross-border transfers must traverse the same licensing gauntlet Wise did, and the gauntlet has only gotten harder. Bargaining Power of Buyers is high in theory—customers can switch—but mitigated by the switching costs described above. Bargaining Power of Suppliers is an interesting one: Wise's key "suppliers" are the local payment systems and the partner banks that safeguard deposits, and in several markets the relationships are close to monopsonistic, which is a vulnerability. The Threat of Substitutes is the most live part of the analysis, and it centres on two candidates: stablecoins and central bank digital currencies.

Stablecoins, in their purest form, threaten to route around the entire edifice of local payment rails by letting value move across borders on a public blockchain at settlement finality of seconds. In practice, they are currently more complementary than competitive; Wise has begun experimenting with stablecoin settlement in certain corridors, treating it as just another rail rather than an existential threat. The economic logic for customers is that they care about the end-to-end experience—sending pounds from Barclays and receiving pesos into a Mexican account—not about which pipes the money traverses in between. If stablecoins turn out to be faster and cheaper for the middle leg, Wise will adopt them; if not, it will not. Where the threat would become real is if a stablecoin-native wallet captured end-user demand directly, which has happened in small pockets (Argentina, Turkey) but not in any of the Wise core corridors at scale.

CBDCs are a longer-term concern, mostly because they would involve central banks building government-operated rails for cross-border payments that could in principle commoditise the underlying network. The current timelines for CBDCs in the major economies are measured in decades rather than years, but this is the kind of risk that accrues slowly and then all at once.

Competitive Rivalry, the fifth force, is where the immediate competitive pressure lives. Revolut, the UK-based neobank, is the most frequently cited competitor—it offers multi-currency accounts, international transfers, and a consumer-banking feature set that overlaps substantially with Wise. The difference is mostly in the business model: Revolut monetises through a broader product surface (crypto, stocks, subscription tiers, premium features) and accepts the remittance business as one of many, while Wise is maniacally focused on the cross-border vertical. PayPal, through Xoom, remains the highest-volume remittance competitor globally, but Xoom's per-transaction economics and user experience have visibly lagged for years. Remitly, the Seattle-based specialist focused on remittances from developed markets to emerging ones, has a legitimately different positioning—cash pickup networks, mobile wallet integrations in countries where bank accounts are rare—and competes with Wise primarily on the margins where the receiver is unbanked. WesternUnion and MoneyGram remain gigantic but declining businesses, ceding share every year on the digital fringes while still dominating the physical agent-based corridors in places like Latin America and Africa.

Within this landscape, Wise's particular insistence on owning the infrastructure rather than renting it, and on building the global network rather than focusing on one geography, is its defining strategic bet. It is slower and more capital-intensive than the alternatives. It is also the hardest to copy.

VIII. Bear vs. Bull Case

Every thesis worth its salt has a mirror-image anti-thesis, and Wise is no exception. Start with the bear case, because that is where the most thoughtful long-term investors tend to go first.

The most concrete bear case lives on the income statement. Somewhere between twenty-eight and thirty-three percent of Wise's FY2024 revenue came from interest income on customer balances—the same line item that barely existed in 2020. That revenue is directly sensitive to base rates in the Bank of England, the ECB, and the Federal Reserve. If, over the next two years, policy rates drop from their current levels back toward two percent, the absolute contribution of interest income could nearly halve. Wise can offset some of this by growing the underlying float—more customers, larger balances—but the arithmetic is unforgiving. A bear would argue that a meaningful portion of the stock's post-2022 re-rating reflected a permanence assumption on interest income that is not actually permanent, and that the next rate-cutting cycle will compress reported profits even as the underlying cross-border business continues to grow.

The second bear concern is regulatory. Kristo's tax episode was resolved, but the broader regulatory surface area continues to widen. The FCA has become significantly more activist in recent years, EU regulators are rewriting the rulebook under PSD3 and the Instant Payments Regulation, and US state-level money transmission regimes remain fragmented and expensive to navigate. A single major compliance failure—an AML finding in a key market, a consumer protection issue around the Multi-Currency Account, a data incident—could be materially disruptive both to operations and to the "trust" brand that Wise has carefully cultivated. This risk is not hypothetical; several Wise competitors have faced FinCEN settlements, MAS fines, or restrictions on operations in the last five years. The bear argument is that as Wise gets larger, its regulatory target grows faster than its ability to defend against it.

A third, more esoteric concern is CBDC and stablecoin disruption. The optimistic framing here is that these are complementary technologies. The pessimistic framing is that if a major central bank—say, the Fed or the ECB—rolls out a retail CBDC with built-in cross-border interoperability, and if private stablecoins like USDC become the de facto settlement layer for cross-border B2B flows, then the "rails" that Wise has spent fifteen years building could suddenly look like the analogue telegraph network in an age of digital fibre. This is the kind of risk that is almost certainly overstated in the short term and probably underestimated in the long term. The direction of travel in global payments infrastructure is unambiguously toward faster, cheaper, more transparent rails. Whether Wise or a stablecoin-native competitor ends up as the dominant interface to those rails remains genuinely open.

A fourth, more mundane bear argument is about take-rate compression and its limits. If management is philosophically committed to reducing prices in line with cost reductions, then the revenue line grows only as fast as volume grows multiplied by a shrinking take rate. Analysts who model this out aggressively conclude that revenue growth will inevitably decelerate to the mid-teens and then lower. The bull's answer is that volume growth is compounding off a very small base—Wise still has less than five percent of the global consumer cross-border market—but the bear replies that market share in a commoditising industry is worth less than share in a pricing-power industry.

Now the bull case, which rests on three pillars.

The first is market-share math. The global cross-border payments market, across consumer and SME segments, is measured in the tens of trillions of dollars annually. Wise handles, at current run rates, somewhere around £140 billion a year. That is, rounding generously, a mid-single-digit share of just the addressable consumer slice, and a rounding error of the SME slice. The TAM argument is that even if take rates continue to fall, volume has two or three orders of magnitude of room to grow before saturating. This is the kind of runway that fundamentally changes how an investor should think about current valuation multiples.

The second pillar is Wise Platform. If you believe the story that banks around the world will increasingly outsource their cross-border infrastructure—just as they outsourced their core banking systems to FIS and Fiserv, their card networks to Visa and Mastercard, their fraud detection to specialist vendors—then Wise Platform has the potential to become a genuinely embedded infrastructure business with enterprise-software economics. The take rate on platform revenue is lower than on direct consumer, but the customer lifetime is measured in decades, and the churn, once a bank has integrated, is close to zero. There is a version of this story where, in ten years, most of Wise's revenue comes from partners rather than end users, and the company's multiple expands to reflect the more durable revenue mix.

The third pillar is what one might call "infrastructure time horizon." Building genuine financial infrastructure is slow, capital-intensive, regulatory-dependent, and almost impossible to accelerate with venture funding. This is bad news for new entrants and good news for incumbents. Every year Wise survives and grows without a major compliance failure, the moat deepens, because the cost for a competitor to replicate it rises. At some point—and reasonable people disagree on whether this is five years or fifteen years away—the moat around the global money-moving business looks as intimidating as the moat around the Visa/Mastercard duopoly does today. The bull case, essentially, is that Wise is a decade into building that moat, and the market is still pricing it as if it were a consumer fintech.

Sitting in the middle of these arguments, the useful thing is to identify the KPIs that matter most. Three stand out. First, underlying volume growth—the total customer money processed, excluding any interest-income effects. That is the cleanest measure of whether the core network is still gathering gravity. Second, cross-border take rate, which tracks the pace of price cuts and tells you whether the scale-economies-shared loop is still being honoured. Third, Wise Platform volume as a percentage of total volume, because that is the best leading indicator for the B2B pivot that underpins most of the long-term bull case. Anything else—statutory profit, headline revenue, marketing efficiency—is noise relative to these three.

There are a handful of second-order items worth watching that are not KPIs in themselves but can move the story. The FCA's ongoing supervisory posture, particularly around safeguarding rules for customer funds, matters because regulatory changes can reshape the economics of the float overnight. The sunset of the dual-class share structure in mid-2026 will be a governance inflection point and will likely coincide with any serious discussion of a secondary US listing. Thirteen-F ownership data for the UK-listed shares—especially moves by Baillie Gifford, Capital Group, and the other concentrated long-term holders—has historically been a reasonable tell for sentiment shifts. Kristo's own share sales, which have been infrequent and disclosed, are another signal worth tracking, as is the composition of the senior team following recent CFO transitions.

IX. Conclusion

In 2011, two Estonians in a London flat decided that the most radical thing they could do to disrupt global banking was to not actually move any money. Fifteen years later, the company that grew out of that Excel spreadsheet moves more than £140 billion a year, serves more than thirteen million customers, powers the international transfer engines of some of the largest banks in the world, and still, according to its own mission roadmap, considers itself to be in the early innings of its project.

Is Wise the first "true" twenty-first-century bank? The question is almost a trick, because Wise itself resists the label. It does not lend. It does not take proprietary credit risk. It does not do investment banking or wealth management. It is, in the strictest sense, not a bank at all. What it is, instead, is something newer and odder—an infrastructure company in consumer clothing, a piece of global financial plumbing that happens to have a really good mobile app. The most useful analogy is probably not to HSBC or Citibank but to Visa in the 1970s, building a network that would, decades later, become so embedded in global commerce that it was effectively impossible to compete with.

The broader legacy, beyond the business itself, is what the "Estonian Mafia" did to the London fintech scene. Before Wise, London's financial technology sector was a collection of rate-comparison websites and retail brokerage tools. After Wise, and alongside companies like Revolut, Monzo, and Starling, London suddenly had an identity as a genuine fintech capital—one that produced infrastructure, not just interfaces. The cultural lineage runs directly back to Skype and the quiet Estonian conviction that software could eat any industry if you were stubborn enough. Taavet and Kristo did not invent that conviction, but they exported it to London and embedded it in an entire generation of entrepreneurs.

The final, and perhaps most underrated, observation is that Wise's most successful strategic decisions were often the smallest ones. Choosing London over Tallinn. Charging a visible fee instead of hiding it in the spread. Dropping "Transfer" from the name. Refusing to do splashy M&A at the peak of the 2021 bubble. Directing most price cuts back to customers rather than letting them flow to the bottom line. Each of these, in isolation, looks modest. Taken together, they describe a company with a very specific and unusually consistent strategic personality—one that has remained remarkably recognisable from the underwear protest on Cheapside to the direct listing on the London Stock Exchange to the Wise Platform deal with Shinhan Bank. Consistency of philosophy, applied across fifteen years of operating cycles, compounds into something that starts to look less like a startup and more like an institution.

Whether Wise becomes the dominant cross-border payments infrastructure of the 2030s, or whether it ends up as one option among several in a world of stablecoins and CBDCs, is a question for future episodes. What is already settled is that the problem Taavet and Kristo identified on a rainy evening in London—that the global financial system was systematically overcharging ordinary people to do something that should cost almost nothing—has been, for millions of customers and thousands of businesses, fundamentally solved. They started with a spreadsheet. They ended with a network. That is a very particular kind of ambition, and it turns out to have been worth listening to from the beginning.

X. Essential Reading & Links

- Kristo Käärmann's founder letters, 2011–2024, which trace the "Amazon-style" evolution of thought from a single-corridor remittance tool to a global infrastructure thesis.

- The Wise Mission Roadmap, the company's public-facing product plan, which is unusual in the fintech industry for the specificity with which it commits to pricing reductions and corridor additions.

- Comparative analyses of capital allocation in fintech, particularly Wise versus Adyen, which represent two very different philosophies—infrastructure-for-consumers versus infrastructure-for-merchants—and offer a useful lens on how disciplined growth looks in the sector.

- Histories of the "Estonian Mafia," the network of founders and early employees that spilled out of Skype and went on to build Bolt, Pipedrive, Veriff, and Wise, reshaping the landscape of European technology far out of proportion to Estonia's size.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube