Vodafone Group Plc: The Rise, Over-expansion, and Retrenchment of a Global Telecom Titan

I. Introduction & Episode Roadmap

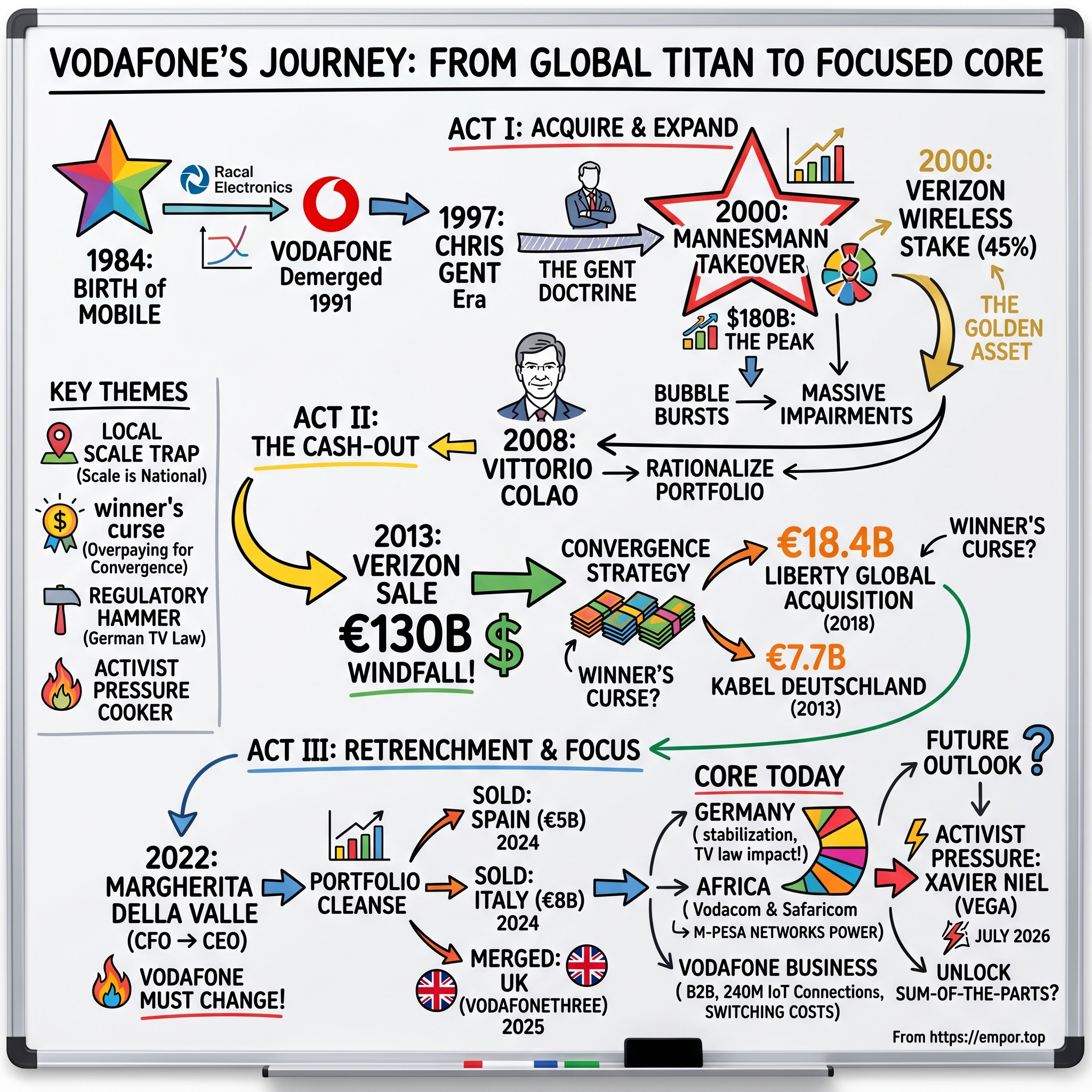

On the morning of February 4, 2000, in a cluster of law offices spanning London and Düsseldorf, a British mobile-phone company barely a decade into its independent life closed the largest corporate takeover the world had ever seen. Vodafone AirTouch had spent four months waging open warfare on Mannesmann AG, a 110-year-old German industrial icon that made everything from seamless steel tubes to the fastest-growing mobile network in continental Europe. When Mannesmann's board finally capitulated, the price tag was roughly $180 billion — a sum larger than the entire GDP of most countries on earth at the time.2 It was the absolute crest of the dot-com wave, and it was a declaration of intent. Vodafone would not merely participate in the mobile revolution; it would own it, borderless and unbounded, from the English Channel to the Pacific.

Now fast-forward to the summer of 2026. The company that once believed geography was a solved problem is dismantling itself, one national flag at a time. Its market capitalization sits near £26.9 billion — a figure smaller than what it paid for Mannesmann alone a quarter-century earlier.1 Spain has been sold. Italy has been sold. The UK has been folded into a joint venture. And on July 10, 2026, the Abu Dhabi sovereign-linked telecoms group that had been Vodafone's largest and most patient shareholder walked out the door entirely, handing its stake to a French billionaire famous for setting fire to telecom margins.[^18]

Here is the paradox this story turns on. Vodafone did almost everything the 1999 playbook said a winner should do. It got big first. It got global first. It spent tens of billions building a footprint no rival could match. And it still lost — not to a smarter empire-builder, but to the stubborn, unglamorous truth that in telecoms, scale is local, not global. A cell tower in Frankfurt does nothing to lower the cost of a cell tower in Milan. Spectrum bought in one country cannot be redeployed in another. The synergies that justify a $180 billion merger in a slide deck evaporate the moment you cross a border.

This is a masterclass in the limits of corporate size, and the story traces it across four decades and four distinct acts. First, the improbable birth: how a mobile network spun out of a British military-radio contractor became, for one dizzying moment, the most valuable company in Europe. Second, the peak and the cash-out: the golden American asset Vodafone owned but never controlled. Third, the convergence trap: the debt-fueled decision to become a cable company. And fourth, the retrenchment: the activist-driven, country-by-country dismantling now being carried out by CEO Margherita Della Valle — and the arrival of an activist who may decide her plan does not go nearly far enough.

There is a useful way to hold the whole arc in your head. Vodafone spent its first act proving it could acquire anything, its second act discovering that acquiring was not the same as earning, and its third act — the one still unfolding — trying to give back everything the first two acts had bought. The tragedy, if that is the word for a company that still turns over tens of billions of euros a year, is that almost none of the value created by the mobile revolution itself accrued durably to Vodafone's owners. The technology changed the world. The shareholders mostly paid for the privilege of watching it happen.

Four themes will recur. The local scale trap — why a global footprint delivered almost no economic advantage. The winner's curse — how overpaying for cable and fixed-line assets destroyed shareholder capital. The regulatory hammer — how a single change to German rental law gutted the company's most profitable business. And the activist pressure cooker — the boardroom transformation now underway as a supportive sovereign partner exits and a ruthless disruptor takes its place. To understand how far Vodafone has fallen, you first have to understand how impossibly high it once climbed.

II. Racal, Chris Gent, and the Birth of a Mobile Empire (1984–2000)

The origin of the world's most aggressive telecom consolidator was, fittingly, an afterthought. In the early 1980s, the British government decided to license a second cellular network to compete with the state-owned incumbent, and the winning bidder was not a media conglomerate or a telephone company. It was Racal Electronics, a maker of military radios and defense electronics run by a demanding, self-made engineer named Ernest Harrison. Racal's small "Vodafone" division — a compression of voice, data, and phone — switched on its first call on January 1, 1985, from a car in Newbury. The technology was clunky, the handsets were the size of bricks, and the addressable market looked, to most sober observers, like traveling salesmen and property developers.

Harrison and his young lieutenants saw something else. Mobile telephony was not a niche business tool; it was a mass-market utility waiting for the price of a handset to fall. But a fast-growing network trapped inside a defense contractor was a valuation prisoner — investors priced Racal as a sleepy engineering firm, not a growth story. So in 1991, in one of the cleaner pieces of corporate financial engineering of the era, Vodafone was demerged and floated as an independent company on the London Stock Exchange, with a parallel listing in New York. Freed from its parent, it became a pure-play bet on the mobile revolution, and the market repriced it accordingly.[^1]

The man who would turn that bet into an empire was Christopher Gent. A cricket-loving former Barclays banker with an outwardly genial manner and an inner core of pure competitive steel, Gent took the chief executive's chair in 1997. He was, in the truest sense, an empire-builder — a leader convinced that in a scale business, the operator with the most subscribers, the most spectrum, and the most countries would compound its advantages until rivals simply could not keep up. In an industry racing toward mass adoption, Gent decided that Vodafone's job was to consolidate faster than anyone else could.

Before the German war, though, came the American beachhead — and it is worth pausing on, because it explains the "AirTouch" that sat in Vodafone's name for a few years and seeded the asset that would later save the company. In 1999, Vodafone won a transatlantic bidding contest for AirTouch Communications, a California-based cellular operator spun out of Pacific Telesis, in a cash-and-stock transaction that briefly rebranded the group "Vodafone AirTouch."2 The prize was not just AirTouch's own networks but its web of US wireless partnerships. Gent had a habit of turning every acquisition into the fuel for the next one, and AirTouch was the clearest example: within months of closing it, Vodafone folded its new American assets into a joint venture with Bell Atlantic that would soon be christened Verizon Wireless. Gent bought an operating company and, almost as a byproduct, manufactured a minority stake that would one day be worth more than the whole of Vodafone. Momentum, in his hands, was a machine.

His defining battle came in Germany. Mannesmann, the old-line industrial conglomerate, had reinvented itself as a telecom pioneer through its D2 mobile network — and then, in late 1999, it acquired Orange in the United Kingdom, planting a flag squarely in Vodafone's home market. To Gent, this was not a competitive nuisance; it was a declaration of war in his own backyard. His response was audacious to the point of recklessness: a hostile, all-share bid for the entire Mannesmann enterprise, financed not with cash the company did not have but with Vodafone's own richly valued stock.

What followed was one of the great corporate sieges of the era. For four months, the two companies waged a transnational public-relations war across the front pages of Germany and Britain. Mannesmann's chief executive, Klaus Esser, mounted a fierce defense, appealing to German pride and the country's tradition of stakeholder capitalism against the idea of a foreign raider seizing a national champion. Gent, backed by an army of bankers, kept sweetening the exchange ratio until Esser's own shareholders could no longer refuse. In February 2000, Mannesmann's board relented, and Vodafone AirTouch became the largest mobile operator on earth, with more than 42 million customers spread across Britain, the United States, Germany, Italy, and France.2

The human drama of those months became legend. Gent conducted parts of the final negotiation by mobile phone while attending a cricket match in South Africa — a detail that critics seized on as emblematic of the era's casual audacity, and that admirers cited as proof of his unflappable nerve. On the other side, Esser's defense had rallied German public opinion around the idea of Standort Deutschland — the nation's economic model — under siege. When he finally settled, the exchange terms handed Mannesmann shareholders a large minority of the combined company, and Esser himself later became the center of a criminal trial in Germany over the multimillion-euro payments approved for departing executives, a case that turned into a landmark examination of boardroom conduct. The takeover did not just redraw the corporate map; it forced a reckoning with what a hostile, foreign-led acquisition meant for a country that had believed itself immune to one.

The triumph carried a poison pill written in accounting ink. Because Vodafone paid in stock at the very peak of the dot-com bubble, the deal loaded the combined balance sheet with an astronomical mountain of goodwill — the premium over the tangible value of what it bought. When the bubble burst and telecom valuations collapsed, that goodwill had to be written down. By the year to March 2006, Vodafone booked one of the largest impairment charges in British corporate history, tens of billions of pounds, and reported a full-year statutory loss that stunned even hardened observers.[^1] The lesson was hiding in plain sight from the moment the champagne was poured: Vodafone had proven it could win any takeover it wanted. It had not yet proven those takeovers would create value. That question would define the next twenty years.

III. The Peak and the Cash-Out: The Golden Verizon Wireless Asset (2000–2013)

The most valuable thing Vodafone ever owned, it never actually controlled. In 1999, as part of its American expansion, Vodafone merged its US wireless operations with those of Bell Atlantic to create a new entity called Verizon Wireless, taking a 45% stake and handing operational control to its American partner. On paper it looked like a compromise. In practice it turned out to be a golden ticket — and a lesson in the difference between owning a great business and running one.

While Vodafone spent the 2000s slugging it out in Europe's brutally fragmented markets, where four, five, or six operators fought over the same subscribers and average revenue per user ground steadily lower, Verizon Wireless was quietly becoming one of the best businesses in the world. The United States mobile market consolidated into a cozy handful of national carriers, each earning high revenue per customer with rational pricing and enormous scale. Verizon Wireless printed cash. Its margins dwarfed anything achievable in Europe. There was just one catch: Vodafone, as the minority partner, could not direct its strategy, could not always compel it to pay dividends, and could not consolidate it as a wholly owned crown jewel. It was a passenger in the fastest car on the track.

The awkwardness was compounded by an emerging-markets adventure that ran in parallel. In the mid-2000s, still chasing the empire logic, Vodafone had pushed into high-growth developing economies on the theory that the next billion mobile subscribers would come from Asia and Africa, not saturated Europe. The centerpiece was India: in 2007 Vodafone paid billions of dollars to acquire a controlling interest in Hutchison Essar, one of India's largest mobile operators, betting on a market adding millions of subscribers a month. The bet on volume was correct; the bet on economics was not. India descended into a spectrum-fueled price war among more than a dozen operators that drove per-minute tariffs to among the lowest on earth, and the acquisition dragged Vodafone into a multi-year, multi-billion-dollar tax dispute with the Indian authorities over the deal's structure. Alongside India sat a scattering of other positions — in Egypt, Turkey, and across Eastern Europe — that added subscribers and complexity in roughly equal measure while generating uneven returns. Vodafone was learning, market by expensive market, that being present everywhere was not the same as being profitable anywhere.

Into this awkward arrangement stepped Vittorio Colao, who became chief executive in 2008. An elegant, cerebral Italian — a former McKinsey consultant with an MBA from Harvard and a reputation for cool analytical rigor — Colao inherited an empire that Gent's acquisitive instincts had assembled but never rationalized. Vodafone held a bewildering patchwork of stakes across the globe: controlling interests in some markets, awkward minority holdings in others, sprawling positions in India, Egypt, Turkey, and Eastern Europe that generated headlines about scale but stubbornly failed to generate unified economic returns. Colao's temperament was the opposite of Gent's. Where Gent asked how big Vodafone could become, Colao asked which pieces were actually worth owning.

The answer to that question produced one of the largest transactions in corporate history. Under mounting pressure from shareholders to convert the paper value of the Verizon Wireless stake into something tangible, Colao struck a deal in September 2013 to sell Vodafone's 45% holding back to Verizon Communications for $130 billion.3 The structure told its own story about how enormous the asset had become: roughly $58.9 billion in cash, about $60.2 billion in Verizon stock, and some $11 billion in other considerations.4 It was the third-largest acquisition ever announced at the time, and it crystallized a windfall so large it briefly made Vodafone one of the most cash-rich companies on the planet.

The strategic logic of the sale was impeccable, and it captured Colao's temperament perfectly. A minority stake you cannot control, in a market where you have no operating role, is not a strategic asset — it is a financial holding dressed as one, and financial holdings should be sold when the price is right. Verizon's own hunger to own its wireless business outright meant the price was more than right. But a sale of that magnitude poses a question that has ruined more companies than any acquisition ever did: what do you do with the money? A windfall is a test of institutional character. It reveals whether a management team is disciplined enough to hand cash back when it lacks high-return uses for it, or whether it will manufacture reasons to spend.

Here the story reaches its hinge — the decision that, more than any other, set the stage for Vodafone's modern struggles. A disciplined operator might have returned the vast majority of that $130 billion to shareholders and shrunk into a leaner, more focused business. Vodafone did return a substantial slug of capital. But it also chose to redeploy billions into a sweeping new strategic bet: buying up fixed-line and broadband assets across Europe to build "converged" telecom champions. The Verizon cash-out was not an ending. It was the funding round for the next great gamble — and this time, the winner's curse would come not from an American cash machine but from European cable networks strung through the streets of Germany.

IV. The Convergence Trap: Overpaying for Cable & European Consolidation (2013–2018)

Every disastrous acquisition spree begins with a strategy memo that sounds completely reasonable. Vodafone's was called "convergence," and its logic ran like this: mobile connectivity is becoming a commodity. Data is data; a gigabyte from one carrier is indistinguishable from a gigabyte from the next, and price wars will grind mobile-only margins into dust. The way to defend the customer relationship, the theory went, was to sell people everything at once — mobile, home broadband, a landline, and pay-TV, bundled into a single "quad-play" package. Bundle enough services together and customers become sticky; churn falls, lifetime value rises, and the operator escapes the commodity trap. It was a coherent thesis. It was also expensive, and the price of admission turned out to be far higher than the theory allowed.

The buying began even before the Verizon cash landed. In June 2013, Vodafone launched a €7.7 billion takeover of Kabel Deutschland, the country's largest cable operator, cleared by European regulators that September.[^6] It was Vodafone's entry into German fixed broadband, and it was struck at an enterprise-value-to-EBITDA multiple north of twelve times — a steep premium at a time when many European telecom peers traded at single-digit multiples. Vodafone was paying a growth price for an infrastructure asset.

Then came the truly colossal move. In May 2018, Vodafone agreed to acquire the bulk of Liberty Global's European cable operations — its networks in Germany (including the second-largest German cable operator, Unitymedia), Romania, Hungary, and the Czech Republic — for an enterprise value of €18.4 billion.5 The deal comprised roughly €10.8 billion of cash paid to Liberty Global plus around €7.6 billion of assumed debt.6 With it, Vodafone became the dominant cable player in Germany and a converged operator across Central Europe. On the strategy slides, it looked like the endgame: mobile plus cable, wall to wall, in Vodafone's most important market.

The structural mismatch beneath the strategy took years to fully surface. The first problem was the capex treadmill. A high-margin mobile operator is a relatively capital-light business once the network is built. A cable operator is not. Vodafone had bought sprawling networks of aging coaxial cable that needed to be upgraded to fiber to stay competitive — a multi-billion-euro, multi-year construction obligation with no natural end point. Convergence had quietly transformed Vodafone from a nimble spectrum-and-software company into a heavy infrastructure company, precisely the kind of capital-intensive utility that struggles to earn its cost of capital.

There was a deeper strategic misread buried in the convergence thesis, and it is the kind that only becomes obvious in hindsight. The theory assumed that bundling would raise switching costs enough to protect pricing — that a customer with mobile, broadband, landline, and TV all on one bill would be too much trouble to leave. But the German market did not cooperate. Deutsche Telekom could bundle too, and it did so from a superior fiber network. Discount players could pick off the mobile line alone. And the TV component of the bundle — supposedly the sticky glue — turned out to rest on a legal privilege the government was already preparing to abolish. Vodafone had bought its way into a bundling war it did not have the network quality to win, in a country where its most defensible bundle ingredient was living on borrowed time.

The second problem was integration, and it was worse. Merging the mobile IT stack with the fragmented, legacy billing and provisioning systems of multiple acquired cable operators — each with its own technology, its own customer databases, its own quirks — proved to be an execution nightmare, most visibly in Germany. The years following the Unitymedia integration brought system outages, billing errors, collapsing customer-service quality, and, inevitably, subscriber churn. The very metric convergence was supposed to fix got worse. Here is the uncomfortable analytical conclusion the numbers force: Vodafone paid double-digit multiples to acquire assets whose defensive "bundling" benefit was more than offset by the capital required to keep them competitive and the operational chaos of stitching them together. The convergence premium was real. The convergence payoff was not — and the epicenter of the damage was the very market Vodafone considered its crown jewel.

V. The German Trap & The TV Law Bomb

To understand Vodafone today, you have to understand a peculiar feature of German rental law that most Vodafone shareholders had never heard of until it detonated under them. But first, the setup: Germany is not just a large market for Vodafone. It is the market. For years it generated somewhere between 30% and 40% of the group's adjusted EBITDAaL — the earnings measure Vodafone uses after leasing costs — making it the engine that funded the dividend and serviced the debt.[^1] When Germany catches a cold, the whole group runs a fever.

And Germany is a hard place to win. The competitive landscape is defined by three distinct threats. The incumbent, Deutsche Telekom, is a national champion with towering brand equity and the country's most extensive fiber-to-the-home rollout — a structurally superior fixed network that Vodafone's upgraded cable struggles to match on the highest-end connections. The aggressive challenger, Telefónica Deutschland's O2 brand, competes hard on price and keeps mobile ARPU under permanent pressure. And the disruptor, 1&1, has been building out a fourth mobile network from scratch, adding structural rivalry to a market that was already crowded. Game out that three-front war and Vodafone's position looks structurally uncomfortable. Against Deutsche Telekom it is fighting a network-quality battle it is not obviously equipped to win, because fiber-to-the-home is generally superior to upgraded cable at the very top end where the most valuable customers live, and Deutsche Telekom has both the deeper fiber footprint and the incumbent's brand halo. Against O2 it is fighting a price battle that compresses everyone's mobile margins. And against 1&1 it faces the one thing a crowded market least needs — a determined new network operator willing to spend to take share. In each direction the pressure runs against pricing power. Vodafone Germany is not a fortress; it is a large, valuable business defending a broad perimeter against three different attackers at once.

In that arena, Vodafone's most profitable business was never its hard-fought mobile subscribers or its churning broadband base. It was television — and television is where the bomb was buried.

For decades, German landlords enjoyed the right to bundle basic cable-TV fees directly into their tenants' monthly rent under a provision known as the Nebenkostenprivileg, the "ancillary rental cost privilege." A landlord signed one bulk contract with a cable operator to wire an entire apartment block, and every tenant paid for TV automatically through their rent, whether they watched a single minute of it or not. Vodafone, through its Kabel Deutschland and Unitymedia inheritance, held a near-monopoly on these multi-dwelling units. The result was roughly 8.5 million households paying for television on autopilot — stable, recurring, near-100%-margin revenue that landed with almost no marketing cost and almost no churn. It was, quietly, one of the best revenue streams in European telecoms.

Then the German government took it away. After a long legislative transition, the Nebenkostenprivileg was abolished, and from July 1, 2024, tenants were free to choose their own TV provider rather than paying automatically through their rent.[^9] Overnight, a captive base of 8.5 million households became a marketing problem. Vodafone now had to persuade each of those tenants, one by one, to sign an individual contract for a product many of them had never actively chosen and did not realize they were paying for. Predictably, millions declined. The near-100%-margin autopilot revenue began draining out of the German business, and because that revenue was so profitable, its loss hit EBITDAaL far harder than the headline subscriber numbers alone would suggest.

It is worth dwelling on why this hurt so much more than a normal subscriber loss, because the accounting is the whole story. A typical telecom customer comes with real costs attached — a handset subsidy, a service center, a share of the network. Losing one hurts, but you also stop spending on serving them. The bulk-TV tenant was different. Vodafone spent almost nothing to acquire or serve that customer; the landlord did the selling, the rent did the collecting, and the cable was already in the wall. That meant nearly every euro of bulk-TV revenue fell straight through to profit. When it disappeared, there were no offsetting costs to shed. The revenue was gone and the margin went with it, one-for-one — which is why a change that looked like a line item in a consumer-protection bill landed on Vodafone's earnings like a demolition charge.

The fallout rippled through every subsequent set of results. Across FY25 and into FY26, Germany's service revenue and profitability sagged under the weight of the TV exodus, dragging down the entire group's financial profile at the worst possible moment. By the FY26 preliminary results reported on May 12, 2026, German service revenue was essentially flat — down 0.2% — with the final leg of the multi-dwelling-unit transition still weighing on the numbers even as management pointed to a return toward growth.[^14] The episode is a near-perfect case study in a risk that never appears on a network map: the regulatory moat. Vodafone's most defensible profits in its most important country turned out to rest not on superior technology or customer loyalty, but on a quirk of legislation that a parliamentary majority could erase with a single vote. It did. And it fell to a new chief executive to manage the wreckage.

VI. The Della Valle Reshaping: Carving Up the European Map (2022–2026)

By late 2022, the patience of Vodafone's shareholders had run out. Nick Read — a long-serving finance chief who had been elevated to chief executive in 2018 — had spent four years watching the share price slide while resisting the kind of radical surgery that activists and analysts increasingly demanded. His argument that Vodafone needed time and consolidation, not amputation, no longer commanded a majority. In December 2022, Read stepped down, and the board turned to an insider to steady the ship: Margherita Della Valle, the group's chief financial officer, who took over on an interim basis and was confirmed as permanent CEO in April 2023.

Read's exit deserves a moment, because it marked the end of an entire management philosophy. A career telecom-finance executive, he had spent his tenure trying to fix Vodafone from within the existing structure — negotiating incremental deals, pursuing tower-company carve-outs, and arguing that European in-market consolidation would eventually deliver the scale the group lacked. The trouble was that the stock kept falling and the strategy kept looking incremental against problems that were structural. Activist investors circled, openly questioning whether Vodafone's sprawling portfolio should exist in its current form at all. When the board finally lost confidence, it did not reach outside for a turnaround specialist; it reached for the insider who had been signing off on the same numbers, on the theory that the disease was well enough understood and what was missing was the will to cut. That theory is itself a bet, and it remains only partly settled.

Della Valle was, in one sense, the ultimate continuity candidate — an Italian-born executive who had spent nearly three decades inside Vodafone, rising through its Italian operation and its finance function to become group CFO. But she brought a message that broke sharply with the empire-building past. "Vodafone must change," she declared on taking the job, and her strategy fit on a single line: Customers, Simplicity, and Growth. The subtext was blunt. Vodafone had become a sprawling, underperforming conglomerate of sub-scale national businesses, and the fix was not to buy more — it was to sell, ruthlessly, any market where Vodafone could not earn its cost of capital.

The portfolio cleansing came fast, and each disposal is worth reading as a verdict on the empire Gent and Colao had built. Spain went first. In late 2023 Della Valle agreed to sell the underperforming Spanish unit to Zegona Communications, and the deal completed in the first half of 2024 for headline proceeds of around €5 billion.[^10] The multiple — roughly five times EBITDAaL — told the story: Spain's market had degenerated into a hyper-fragmented price war where premium operators bled share to low-cost rivals. Having poured well over €10 billion into acquiring and upgrading Spanish assets over the years, Vodafone crystallized an enormous economic loss to be rid of them. The disposal was not a triumph; it was a confession.

Italy followed. Vodafone agreed to sell Vodafone Italia to Swisscom for roughly €8 billion, a deal completed at the end of 2024, with the Italian business subsequently merged into Swisscom's Fastweb to form a combined operator from the start of 2026.78 At around 7.6 times EBITDAaL, the Italian exit fetched a meaningfully better price than Spain — a reflection of Vodafone Italia's stronger mobile infrastructure — but it was still a total retreat from one of Vodafone's founding continental markets, another admission that scale without local dominance does not pay.

The United Kingdom got a different treatment: not a sale, but a merger of equals-in-spirit. Della Valle negotiated the combination of Vodafone UK with CK Hutchison's Three UK to create "VodafoneThree," with Vodafone holding 51% and Hutchison 49%. The strategic logic was the local-scale thesis in its purest form: the UK had four sub-scale mobile operators, none of which could earn its cost of capital, and merging two of them into a single champion was the only way to make the economics work. The UK Competition and Markets Authority cleared the deal in December 2024 subject to binding commitments, and it completed in May 2025.9 The price of approval was steep — a committed £11 billion, ten-year investment programme to build out an advanced 5G network, plus a three-year cap on certain consumer tariffs and guaranteed wholesale terms for virtual operators.9 Vodafone got its scale, but the regulator kept it on a leash.

Read the three moves together and a coherent doctrine emerges, one that quietly repudiates the previous quarter-century. Sell where you are sub-scale and cannot become dominant (Spain, Italy). Combine where scale is achievable but requires a partner (the UK). Keep only what you can either dominate or grow (Germany, Africa, B2B). It is the local-scale thesis converted into an operating manual, and it has the intellectual honesty of a management team that has stopped pretending a global footprint was ever worth anything on its own. The uncomfortable corollary, which Della Valle rarely says aloud but her actions concede, is that most of the empire her predecessors assembled was value-destructive to build and is worth more dismantled than intact. That is a remarkable admission for an insider of nearly thirty years to make with the balance sheet.

Underpinning all of this was a hard reset of capital allocation. Della Valle did the thing her predecessors had spent two decades avoiding: she cut the dividend, halving it from 9.0 eurocents to 4.5 eurocents starting in FY25 to match a smaller cash-generating perimeter.[^1] In its place she promised discipline — a €4.0 billion capital-return programme, funded largely by the Spanish and Italian exit cash and delivered through share buybacks rather than an unsustainable payout. The message to the market was that Vodafone would finally be run for returns rather than reach. Whether the leaner company left standing could actually grow was now the only question that mattered.

VII. The Core Today: Financial Segments, B2B Optionality, and the African Growth Engine

Strip away the disposals, the write-downs, and the forty years of accumulated ambition, and what is the business that remains? By the summer of 2026, Vodafone is a materially smaller and simpler machine than the one that bought Mannesmann — and the shape of the surviving perimeter tells you exactly where management believes the value now lives.

Germany remains the legacy cash cow, still generating on the order of €11.5 billion in service revenue and anchoring the group's economics.[^1] But it is a cash cow in convalescence. The TV base is still being nursed through the post-Nebenkostenprivileg transition, mobile ARPU is under competitive pressure, and management spent the FY26 results calls insisting that Germany had turned the corner back toward growth even as the reported numbers hovered around flat.[^14] For investors, Germany is less a growth story than a stabilization story: the single most important operational task in the entire company is simply to stop the bleeding and prove the core utility can hold its ground against Deutsche Telekom's superior fiber.

The United Kingdom is now a different animal. Through the VodafoneThree joint venture, Vodafone has gone from a sub-scale also-ran to the largest mobile operator in the market by connections. The healthier market structure should, in theory, support more rational pricing and better returns over time. But the CMA's conditions mean the venture carries an aggressive, decade-long capital-expenditure commitment, so the near-term reality is heavy investment against a promise of eventual scale economics — a bet that will take years to validate.

A word on the currency problem, because it is easy to wave past and it matters enormously to how this asset is valued. Vodacom and Safaricom earn in rand, shillings, and — through Vodacom's Egyptian operations — Egyptian pounds. Vodafone reports in euros. When those African currencies weaken against the euro, which they have done persistently for years, a business growing at double digits in local terms can translate into flat or shrinking euros on Vodafone's consolidated statements. Local management can be executing brilliantly and the number that reaches a London investor still looks mediocre. This is not an accounting quirk to be dismissed; it is a real economic headwind, because the cash ultimately has to cross a border to fund a euro dividend or a euro debt repayment. But it is also exactly the kind of distortion that a standalone Johannesburg-listed Africa business, valued by investors who think natively in rand and in growth, would not suffer in the same way — which is precisely why activists eye a separation.

Then there is Africa, which is where the growth actually is. Vodafone owns roughly 60% of Vodacom Group, listed in Johannesburg, which in turn holds a major stake in Kenya's Safaricom.11 The crown jewel of this constellation is M-Pesa, the mobile-money platform that turned a Kenyan text-message service into the beating heart of East African commerce, processing billions of dollars in transactions and, for millions of people, functioning as their primary bank.12 M-Pesa is genuinely one of the strongest assets anywhere in the Vodafone empire — a real network effect, a point the frameworks section returns to. But there is a structural catch that keeps it from lighting up the group's headline numbers: Safaricom is equity-accounted rather than consolidated, and the African currencies that dominate the region — the South African rand, the Egyptian pound, the Kenyan shilling — suffer persistent devaluation against the euro. The result is that a high-growth, high-margin fintech asset delivers strong local performance that is repeatedly translated away on the road to Vodafone's consolidated income statement. The value is real; it is just partially hidden.

It is worth understanding why M-Pesa became a genuine moat when almost nothing else in the portfolio did, because the mechanism is instructive. When Safaricom launched it in Kenya in 2007, the product solved a problem banks had ignored for a century: most Kenyans had no bank account, but many had a mobile phone, and they needed a safe way to send money home. M-Pesa let anyone convert cash to digital value at a corner kiosk, text it across the country, and cash out at another kiosk. Every new agent made the network more convenient; every new user made it more attractive to become an agent. Over time it absorbed bill payments, merchant checkout, savings, and lending, until it became less a feature and more the financial operating system of East Africa. That is a self-reinforcing loop of the kind Vodafone's European consumer business has never possessed — and it explains why the sum-of-the-parts argument for spinning out Africa has such intuitive force. A fintech platform with a real network effect does not belong, valued as an afterthought, inside a low-growth European telco.

The quietest source of resilience is Vodafone Business, the B2B division, which generates upward of €8 billion in service revenue and behaves nothing like the churn-prone consumer business.[^1] Its most striking asset is scale in the Internet of Things: Vodafone is the global leader in IoT connectivity, managing well over 240 million connections — the SIM cards embedded in cars, shipping containers, industrial sensors, and utility meters that quietly transmit data across its network.[^1] The revenue per connection is tiny, but that misses the point. Think of what these connections actually are: the SIM that lets a carmaker's vehicles phone home for software updates and emergency calls, the module that tells a logistics firm where its containers are, the sensor that lets a utility read a meter without sending a technician. Once a manufacturer designs Vodafone's connectivity into a product line that will ship for years, ripping it out means re-engineering the hardware — a switching cost measured not in months of notice but in product cycles. These are sticky, low-churn enterprise relationships wired directly into customers' operations and workflows, and they serve as a wedge to sell higher-value cloud, connectivity, and cybersecurity services on top. In a portfolio where the consumer moats keep eroding, this is one of the few places where Vodafone actually holds a customer captive for the right reasons — because it is useful, not because a landlord signed a form. It is where switching costs genuinely bite, a point worth holding onto when the bull and bear cases are weighed. First, though, it is worth extracting the hard lessons from four decades of capital allocation.

VIII. Playbook: M&A Benchmarking, Corporate Governance, and Capital Allocation Failures

If you wanted to design a corporate case study on the difference between size and value, you could hardly do better than Vodafone's forty-year record. Three lessons run through the entire story, and each one is written in shareholder capital.

The first is that scale is local, not global. This is the master theme, and every disposal of the past three years is a fresh proof point. A mobile network's economics are set inside national borders: spectrum is licensed country by country, towers are built and amortized locally, and market share within a single country determines whether an operator earns high margins or fights a price war. Having 200 million-plus customers spread across fifteen countries delivered almost no procurement leverage and almost no network synergy — you cannot share a German cell site with an Italian subscriber — while adding enormous corporate overhead, governance complexity, and management distraction. The global footprint was a cost center dressed up as a competitive advantage. Della Valle's entire strategy is, in effect, the belated admission of this truth: she is selling geography to buy local density.

The second lesson is the fallacy of the convergence premium. Buying legacy cable assets at double-digit EBITDA multiples to defend against mobile commoditization was a value-destructive trade in disguise. The defensive logic ignored the cost of keeping those assets competitive — the endless capital required to upgrade copper and coax to fiber — which consumed any theoretical bundling margin and then some. The clean way to see it: the disposal multiples on Spain and Italy came in well below the multiples Vodafone had historically paid to build those positions, and the German cable integration destroyed value operationally on top of the price overpayment. Vodafone bought high, ran into execution walls, and sold low. That is the winner's curse rendered in fiber and coaxial cable.

The third lesson is about incentives, and it is the most damning because it explains the first two. For most of its history, Vodafone's executive incentive structure rewarded absolute scale — revenue, subscribers, footprint — far more than return on capital employed. When you pay managers to get bigger, they get bigger, whether or not bigger creates value. This is the empire-building disease in its clinical form, and it is precisely why Della Valle's own pay package is worth reading as a corrective. Her arrangement ties a large majority of potential compensation — a long-term incentive that can reach up to 500% of a base salary of around £1.29 million, plus an annual bonus capped at 200% — to metrics like free cash flow, relative total shareholder return, and return on capital employed, rather than to sheer size.[^1] It is a belated attempt to bolt capital discipline onto a culture that spent decades optimizing for the opposite.

There is a fourth theme that a skeptical long/short investor would press hard on: disclosure and complexity as a value-destruction mechanism in their own right. For years, Vodafone's accounts were a thicket of joint ventures, associates, minority stakes, and equity-accounted holdings that made it genuinely difficult for outsiders to know what they owned. Verizon Wireless sat off the top line. Safaricom still does. Vantage Towers was partly floated and then taken into a consortium. Each arrangement had its own logic, but the cumulative effect was a business whose true economics were obscured by structure — and obscured businesses trade at a discount, because investors will not pay full price for value they cannot clearly see. Part of the sum-of-the-parts gap that activists now target is not operational at all; it is the market's rational refusal to underwrite complexity it cannot penetrate. Simplification, on this view, is not just about cost. It is about letting the market finally price what is there.

So how should a skeptical investor grade the current management team? The honest answer is: incomplete, with genuine credits and real unresolved risks. On the credit side, Della Valle has moved with impressive speed and clarity, exiting low-return markets that her predecessors had clung to for years and finally aligning pay with returns. There is also a consistency test worth applying, and here the record is more encouraging than the empire-building years. Across successive results — the FY26 preliminary presentation and the H1 update before it — management's framing of the German problem has stayed broadly stable: acknowledge the multi-dwelling-unit transition as the drag, quantify its diminishing impact, and point to an eventual return to growth rather than pretending the hit was smaller than it was.[^14] That willingness to name a miss and attach a mechanism to it is the opposite of the vague, size-obsessed narrative of the past, and it is the kind of behavior a careful investor rewards with the benefit of the doubt. The benefit is provisional, though. Narrative discipline earns credibility only when the promised inflection actually arrives in the numbers.

On the debit side, her credibility now rests on two things she has not yet delivered: engineering a genuine recovery in the German TV and broadband base, and completing the €4.0 billion capital return without letting the debt load spiral. Net debt stood at roughly €25.4 billion after the FY26 year-end, having actually risen as the VodafoneThree consolidation and buybacks landed on the balance sheet.[^14]10 A leaner Vodafone is not yet a deleveraged Vodafone. And into that unfinished turnaround, an uninvited new voice has just arrived in the boardroom.

IX. Activist Stress Test: Xavier Niel's Vega Coup & Governance Under Fire

The phone call that changed Vodafone's ownership structure came without warning on July 10, 2026. For years, the anchor at the top of Vodafone's shareholder register had been إي آند e& — the Abu Dhabi-based telecoms group formerly known as Etisalat — which had built up a substantial holding and secured a board seat as a patient, sovereign-backed strategic partner. That relationship ended in a single transaction. e& sold its entire holding — 3,944,743,685 shares, representing about 16.21% of the share capital and 17.13% of the voting rights — for roughly £4.4 billion, or €5.1 billion, at £1.104792 per share.13 The buyer was Vega, an acquisition vehicle wholly owned by the family of French billionaire Xavier Niel. And e&'s chief executive, Hatem Dowidar, resigned from Vodafone's board with immediate effect.15

To grasp why this sent a jolt through the register, you have to know who Xavier Niel is. He is not a passive sovereign investor content to collect dividends. Niel is the founder of Iliad, the French operator whose Free Mobile brand detonated the French market in 2012 by launching plans so cheap they forced every incumbent to slash prices, permanently compressing industry margins. He then exported the same scorched-earth playbook to Italy through Iliad's entry there. Niel is, quite literally, the disruptor who spent a decade destroying the pricing power of exactly the kind of legacy incumbent Vodafone is. Having previously held around a 2.5% stake through his Atlas Investissement vehicle, he now controls the single largest voting block in the company.14

The Free Mobile story is worth telling in full, because it is the template for everything Vodafone's board now has to fear. When Niel's Iliad launched Free Mobile in France in January 2012, it offered an unlimited plan at a price that undercut incumbents by a margin the industry had assumed was impossible, and a stripped-down entry plan for close to nothing. Distribution was almost entirely online, with no army of retail stores and no salespeople on commission — a radically lower cost base that let Niel price where legacy operators could not follow without gutting their own economics. Millions of French subscribers switched within a year. Incumbent margins collapsed, and the entire market repriced permanently downward. Niel had not built a better network; he had built a cheaper business model and used it as a weapon, a textbook example of counter-positioning where the incumbent's own cost structure becomes the trap. He then ran the same play in Italy, entering as a fourth operator and dragging prices down again. This is the man who now sits atop Vodafone's share register.

For the moment, the disruption is being conducted with velvet gloves. Vega has stated the investment is intended as a long-term strategic minority holding, and under Rule 2.8 of the UK Takeover Code it formally confirmed it does not intend to bid for the whole of Vodafone — while carefully reserving the right to change its mind should the board invite it, a rival bid emerge, or circumstances materially shift.13 Settlement of the shares is expected by the end of 2026, pending regulatory approvals. But no one who has watched Niel operate believes his ambition ends at collecting a coupon.

What does he want? The activist playbook writes itself, and it points in a single direction: unlock the sum-of-the-parts discount that has trapped Vodafone's shares. Niel has long been publicly scornful of Vodafone's corporate bloat and strategic incoherence. The most likely pressure points are cost and structure. On cost, expect him to push Della Valle to go far deeper than her existing plan to cut some 11,000 jobs, attacking the corporate center that the local-scale thesis has already exposed as economically hard to justify.[^1] On structure, expect demands for further monetization of Vodafone's infrastructure — its stake in the Vantage Towers mast business — and, most provocatively, for a full separation or spin-off of the African Vodacom operations, whose faster growth and fintech optionality might command a richer standalone multiple than they receive buried inside a European telco.

The tower question is the cleanest illustration of the value-unlock logic, and it is worth understanding why. Mobile masts are boring, capital-intensive, and utterly essential — which is exactly what makes them valuable to a certain kind of investor. Stripped out of a telecom operator and run as a standalone infrastructure business that leases space to multiple carriers, towers throw off predictable, inflation-linked, contracted cash flows that pension funds and infrastructure funds will pay a rich multiple to own — often a far richer multiple than the market assigns to the volatile telecom parent. Vodafone already recognized this when it floated Vantage Towers and later took it private within a consortium. An activist will simply ask the obvious follow-up: if a mast is worth more outside Vodafone than inside it, why does Vodafone still own the parts it does, and what else on the balance sheet is trapped at the wrong multiple? The same question, asked of the African business, of the B2B division, of every self-contained asset, is the engine of the entire sum-of-the-parts campaign.

The governance implication is the real story here, and it is a genuine regime change. For years, Vodafone's largest shareholder was a supportive sovereign partner whose interests were strategic and long-horizon. That anchor is gone, replaced by the most transaction-hungry disruptor in European telecoms. The boardroom has shifted from a environment that tolerated a patient, multi-year turnaround to one that will demand to know, quarter by quarter, why the parts are worth more than the whole and what management intends to do about it. Della Valle's restructuring was already aggressive. She may now discover it was merely the opening bid.

X. Strategic Frameworks: Hamilton Helmer's 7 Powers & Porter's 5 Forces

Step back from the drama of the boardroom and ask the coldest possible question: does Vodafone possess any durable competitive advantage at all? Two analytical frameworks — Hamilton Helmer's 7 Powers and Michael Porter's Five Forces — offer a disciplined way to test the answer, and the results are sobering for anyone hoping the core business is quietly a compounder in disguise.

Start with Helmer's powers, the sources of persistent excess returns. Scale economies, in Vodafone's case, are weak at the group level and only moderate locally. The relevant scale in mobile is national — enough local share to amortize towers and spectrum across a big subscriber base — and for years Vodafone conspicuously lacked it in the UK and Italy, which is precisely why it merged or sold those businesses. Network effects are largely absent in consumer voice and data; one more Vodafone subscriber does not make the service more valuable to existing subscribers. The glaring exception is M-Pesa, where mobile money exhibits a textbook network effect: every additional merchant who accepts it makes the wallet more useful to every user, and every additional user makes acceptance more valuable to every merchant, creating a self-reinforcing ecosystem that is genuinely hard to dislodge in its home markets. That single asset has more moat than most of the European business combined.

The remaining powers are thin. Switching costs in consumer mobile are low to moderate — mobile number portability has made changing providers nearly frictionless, which is exactly why price wars are so vicious. They are meaningfully higher in B2B, where IoT connections and secure enterprise communications are woven into customers' operational workflows and cannot be swapped out with a phone call. Counter-positioning is not a power Vodafone holds; it is a power used against it. Vodafone is the legacy incumbent that low-cost digital sub-brands and disruptors like Iliad counter-position against, offering a cheaper business model the incumbent cannot match without cannibalizing itself. And a cornered resource is absent — spectrum, the obvious candidate, is auctioned by governments to all comers and cannot be monopolized. The honest verdict: outside M-Pesa and pockets of B2B, Vodafone's competitive advantages are structurally weak.

Before turning to Porter, it is worth naming the uncomfortable implication of the Helmer scorecard. If the only genuinely powered assets Vodafone holds are M-Pesa and slices of B2B, then the market's persistent discount is not a mistake to be corrected by better investor relations. It is a rational assessment that the bulk of the company operates in a business without durable advantage, and that the powered pieces are precisely the ones an activist would argue should be liberated from it. The frameworks and the activist thesis converge on the same conclusion from opposite directions.

Porter's Five Forces, applied to European consumer telecoms, reinforce the diagnosis. Rivalry is extreme — a commoditized service, chronic price wars, and heavy marketing spend, with disruptors always threatening to reset pricing to the floor. Buyer power is high — short contracts, easy switching, and regulators who actively intervene on the consumer's behalf, as the abolition of German TV bulk-billing demonstrated in the most painful way possible. The one force that favors incumbents is the threat of new entrants, which is low: the capital required for spectrum and physical network infrastructure is a formidable barrier, which is why disruption tends to come from a handful of well-funded players rather than a swarm. Supplier power is high — the network-equipment market is concentrated among a few vendors like Nokia and Ericsson, giving Vodafone limited leverage over a critical cost base. And the threat of substitutes is moderate and rising: fixed-wireless access is beginning to substitute for traditional broadband, and satellite networks like Starlink are capturing remote and niche demand. Put the two frameworks together and the picture is clear — this is a structurally difficult industry in which durable advantage is the exception, and Vodafone holds only a few pockets of it. That is the terrain on which the investment case must be argued.

XI. Bull vs. Bear: The Investment Case and 1-3 KPIs

So where does that leave a long-term investor weighing whether the retrenched Vodafone is a value trap or a genuine turnaround? The case cuts both ways, and the honest version refuses to resolve the tension prematurely.

The bull case rests on the idea of the retrenched winner. On this reading, Vodafone emerges from three years of surgery as a focused operator: a stabilizing cash engine in Germany, a newly scaled market leader in the UK through VodafoneThree, and a fast-growing African business with a fintech crown jewel in M-Pesa that the market barely credits inside the consolidated numbers. Capital discipline reinforces the story — the €4.0 billion buyback shrinks the share count against a halved but now-covered dividend, and a leaner perimeter should convert more reliably into free cash flow. And then there is the wildcard: Xavier Niel's arrival could act as a catalyst, forcing the corporate center to strip out legacy bloat and pursue the kind of sum-of-the-parts value unlock — spinning out towers or Africa — that management might never have attempted on its own. In this world, the sub-scale conglomerate finally gives way to the profitable core that was always trapped inside it.

The bear case is equally coherent and arguably better supported by the recent numbers. It begins in Germany, where the TV losses from the Nebenkostenprivileg shift may prove structural and irreversible, while the broadband base keeps leaking to Deutsche Telekom's superior fiber. If the crown jewel is a melting ice cube, the entire capital-return thesis is built on sand. Layer on the debt overhang — roughly €25.4 billion of net debt that has been rising, not falling, and must be refinanced in a higher-rate environment than the one in which it was raised — and the financial margin for error looks thin. Add the UK integration and regulatory risk, where the CMA's binding commitments cap tariffs and lock Vodafone into an £11 billion, decade-long capex schedule that limits the synergies the merger was supposed to deliver. The bear does not need Vodafone to collapse; it only needs the core to keep grinding lower faster than the buybacks can flatter per-share metrics.

What tips the balance between these two stories is, ultimately, a judgment about time and control — and here the arrival of an activist genuinely changes the calculus. Left to its own devices, a management team running a slow structural decline can keep a stock aloft for years through buybacks and reassuring guidance, shrinking the share count while the underlying business erodes beneath it. That is the classic value trap, and it is a fate Vodafone has flirted with for a decade. An impatient, transaction-focused largest shareholder makes that equilibrium harder to sustain. He will demand that the sum-of-the-parts discount be closed through action rather than narrowed through patience — and whether that pressure produces a genuine value unlock or a value-destroying fire sale depends on execution neither side fully controls. The bull and bear cases, in other words, are no longer just about the business. They are about who now sets the clock.

Cut through the noise, and three key performance indicators will tell investors which case is winning, without any need to model the whole company. First, German broadband and TV net additions — the single clearest read on whether the most important business has stabilized or is still bleeding; every quarter of continued losses validates the bear. Second, group adjusted free cash flow after leases — the master metric that determines whether the dividend, the buyback, and debt reduction are all genuinely affordable or whether one of them eventually gives. Third, Vodafone Business organic service-revenue growth, and specifically its digital-services and IoT contribution — the proof point for whether B2B is a real long-term growth engine or merely a stable-but-flat annuity. Watch those three, and the abstract debate between bull and bear resolves into something you can actually track.

XII. Epilogue

The story of Vodafone is, in the end, the story of the modern telecom sector compressed into a single company. It is a cautionary tale about how the genuine excitement of a technological revolution — the arrival of the mobile phone as a universal human tool — curdled into an empire-building incentive structure that mistook size for strength and footprint for moat. Chris Gent won the largest takeover in history and was celebrated as a visionary. A quarter-century later, the value created by that borderless ambition has been substantially unwound, sold back to the market one country at a time at prices that confessed the original strategy's flaw.

Margherita Della Valle's task, stripped to its essence, is to undo the legacy of Chris Gent — to prove that inside the bloated, underperforming conglomerate of the past there was always a lean, profitable, cash-generative core waiting to be set free. She has moved faster and more decisively than her predecessors dared, and the perimeter she is left with is genuinely simpler and more defensible than the one she inherited. Whether it is also good enough — good enough to grow, good enough to cover its capital returns, good enough to escape the structural forces that make European consumer telecoms such a hard place to earn a return — remains unproven.

And now the question has a new author. With Xavier Niel's Vega installed as the largest shareholder and the patient sovereign partner gone, the pace and shape of Vodafone's transformation are no longer entirely management's to set. Whether Niel's aggressive, transaction-focused presence accelerates the turnaround into a genuine value unlock or fractures a fragile recovery before it can take hold is the defining question for Vodafone's next decade. The empire is gone. What remains to be seen is whether what replaces it is a disciplined survivor — or simply a smaller version of the same trap.

References

-

Vodafone Group Plc LSE Company Page — London Stock Exchange ↩

-

Vodafone Acquires Mannesmann in the Largest Acquisition in History — Goldman Sachs, 2000 ↩↩↩

-

Vodafone sells Verizon stake for $130bn — Al Jazeera, 2013-09-03 ↩

-

Verizon Communications Inc. Form 8-K (Exhibit 99.1) — U.S. Securities and Exchange Commission, 2013 ↩

-

Vodafone to acquire Liberty Global's operations in Germany, the Czech Republic, Hungary and Romania — Vodafone Group Plc, 2018-05-09 ↩

-

Vodafone strikes €18.4bn deal for Liberty Global's European operations — Financier Worldwide, 2018-05 ↩

-

Swisscom Acquires Vodafone Italia for €8 Billion to Merge with Fastweb — Swisscom AG, 2024-03-15 ↩

-

Fastweb and Vodafone Italia Merge Under Single Corporate Entity — Fastweb SpA, 2026-01-01 ↩

-

CMA clears Vodafone / Three merger, subject to legally binding commitments — UK Competition and Markets Authority, 2024-12-05 ↩↩

-

Vodafone Group announces FY26 Preliminary Results — Vodafone Group Plc, 2026-05-12 ↩

-

Vodacom Group Limited Integrated Report 2025 — Vodacom Group, 2025-06-30 ↩

-

Safaricom PLC Annual Report FY24 — Safaricom PLC, 2024-05-31 ↩

-

Investment in Vodafone (RNS) — Vega / GlobeNewswire, 2026-07-10 ↩↩

-

Xavier Niel's Disruptive Telecom Strategy Explained — Financial Times, 2026-07-11 ↩

-

e& sells entire Vodafone stake to Xavier Niel — Telecoms.com, 2026-07-10 ↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube