Verve Group SE: The AdTech Alchemist

I. The "Big Idea" and The Pivot

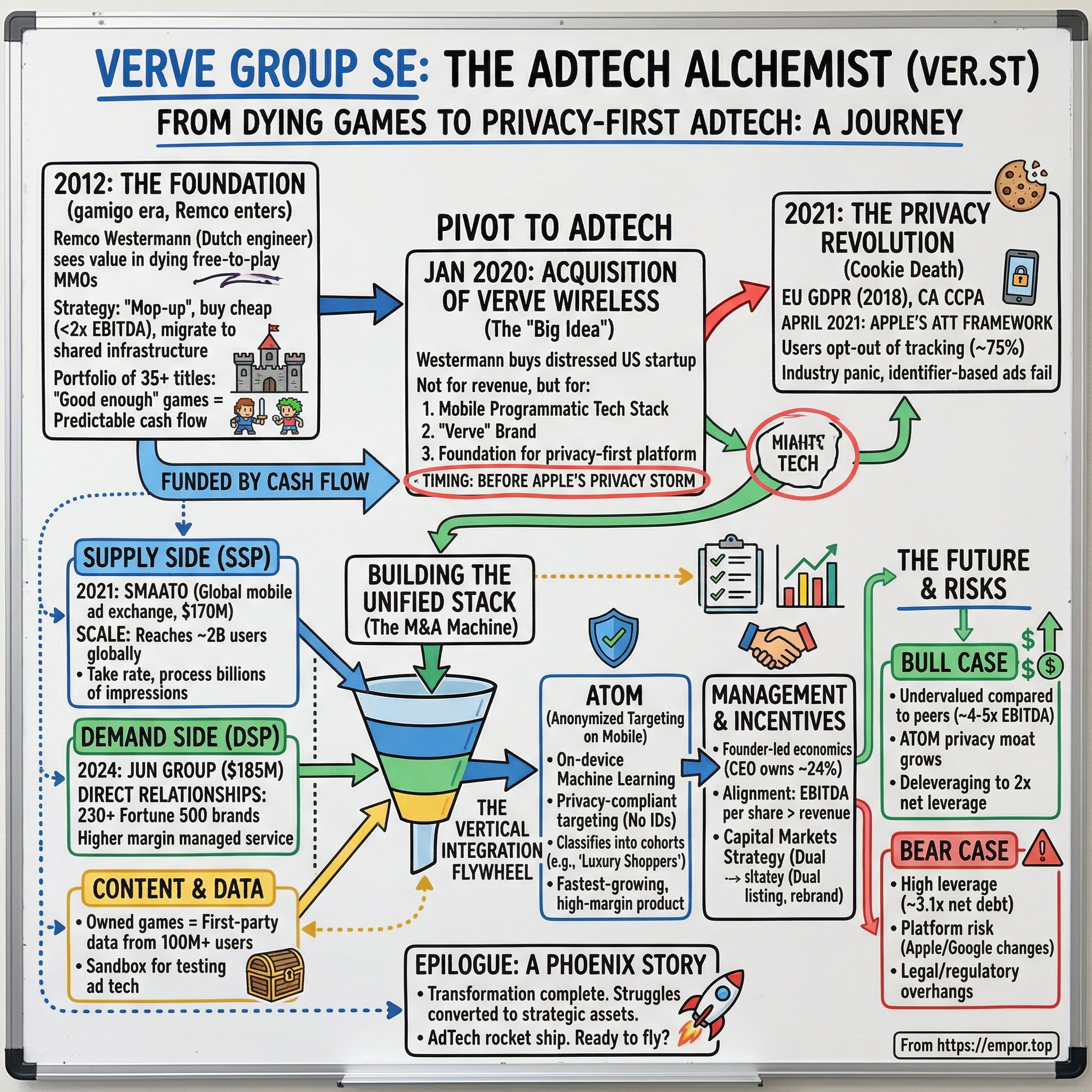

Picture a dreary conference room in Düsseldorf, sometime in late 2019. Remco Westermann, a Dutch-born engineer-turned-entrepreneur who had spent the better part of a decade buying up dying online games, sat across the table from the distressed-asset brokers representing Verve Wireless, a once-promising mobile advertising startup based in New York. The company had pioneered location-based mobile advertising back in 2005 but had burned through its venture capital and was struggling to stay relevant in an industry rapidly consolidating around Google and Facebook. Westermann saw something nobody else wanted to see: not a failing ad company, but the missing piece of a puzzle he had been assembling for seven years.

That acquisition, which closed in January 2020 for an undisclosed sum widely estimated in the low tens of millions of dollars, would become one of the most asymmetric bets in European tech history. Within four years, the technology and brand Westermann bought out of near-distress would lend its name to an entirely new company — Verve Group SE — valued at hundreds of millions of euros and processing billions of ad impressions daily.

The transformation was so complete that the original business — a German free-to-play games publisher called gamigo — became a mere footnote in its own corporate story. If you had told anyone in the European gaming industry in 2019 that a dying MMO publisher would become a globally competitive advertising technology platform within half a decade, they would have questioned your sobriety.

But to understand how a German PC games publisher became a top-tier global advertising technology platform, you have to understand the single most important trend reshaping the internet economy: the death of the cookie and the collapse of identifier-based advertising.

For two decades, the digital advertising industry operated on a simple bargain. Users got free content — news articles, social media feeds, mobile games, weather apps. In exchange, advertisers tracked them across the web using small text files called cookies (on desktop browsers) and mobile device identifiers like Apple's IDFA (on smartphones).

These tracking mechanisms allowed advertisers to build extraordinarily detailed profiles of individual users: what they browsed, what they bought, where they went, what apps they used. The entire programmatic advertising ecosystem — worth roughly four hundred billion dollars globally — was built on this infrastructure. It was the plumbing of the "free internet," and almost nobody questioned whether the plumbing would last forever.

Then the walls started closing in. The European Union's General Data Protection Regulation arrived in 2018, imposing strict consent requirements on data collection. California followed with the CCPA. Apple's App Tracking Transparency framework launched in April 2021, requiring every iPhone app to explicitly ask users for permission to track them — and roughly seventy-five percent of users said no.

Google announced (and repeatedly delayed, and then partially reversed, and then recommitted to) the deprecation of third-party cookies in Chrome. The old rules were breaking, and most of the industry was panicking. Companies that had built their entire business models on the assumption that user-level tracking would exist forever were suddenly staring at an existential threat.

Verve Group was not panicking. Verve Group was building.

The significance of the 2024 name change from Media and Games Invest — the clunky corporate moniker the company had traded under since its Frankfurt listing — to Verve Group SE was more than cosmetic. It was announced on May 14, 2024, approved at the annual general meeting on June 13, and took effect on the Stockholm exchange from June 18 of that year. The ticker changed from MGI to VER in Stockholm and to VRV in Frankfurt.

This was a declaration of identity. The company that once derived the majority of its revenue from free-to-play online games now generated roughly eighty percent of its top line from programmatic advertising software. The gaming assets remained valuable, but their primary purpose had shifted: they were no longer the business. They were the data source that powered the business.

The name "Verve" itself carried meaning. It came from the distressed American startup Westermann had acquired four years earlier — a company that had failed to scale on its own but whose technology and brand would end up defining a billion-euro enterprise. There is a certain poetic justice in that: in an industry obsessed with scale and network effects, the most important asset in Verve Group's arsenal was not the biggest acquisition, but the smallest one.

This is the story of how a company used the ashes of dying video games to fuel a privacy-first advertising rocket ship. It is a story about acquisition discipline, vertical integration, and the rare strategic foresight to build a business that thrives precisely because the old internet is breaking apart. And it begins, improbably, in a small German city with a magazine about PC games.

II. Origins: The gamigo Era and Remco's Entry

The story begins in the spring of 2000, in the small German city of Rheine, where media giant Axel Springer AG and investment firm bmp AG formed a joint venture called gamigo. The timing was conspicuous — this was the peak of the dot-com bubble, when every media company in Europe felt compelled to plant a flag in the digital world, however dubious the business model. The original concept for gamigo was modest: an online magazine covering PC and console games, essentially a digital-native version of the gaming press that was thriving in print.

Within a year, the team pivoted from writing about games to publishing them, launching a fantasy MMO called "Die 4. Offenbarung" in 2001. It was a small title, barely a blip on the radar of an industry dominated by the likes of EverQuest and, later, World of Warcraft.

But it established a template that would define gamigo for the next decade: free-to-play massively multiplayer online games with modest production values, targeting the European market. Think "Fiesta Online," "Last Chaos," "Aura Kingdom" — titles that attracted loyal but small communities of players who preferred not to pay fifteen dollars a month for a World of Warcraft subscription.

The free-to-play model was straightforward. The game itself was free to download and play. Revenue came from microtransactions — small in-game purchases for cosmetic items, experience boosts, or premium content. In Asia, particularly South Korea and China, this model had produced enormous companies like Nexon and Tencent.

In Europe and North America, it was harder. The audience was smaller, the willingness to pay for virtual goods was lower, and the competition for attention from big-budget titles was relentless. gamigo survived, but it never thrived. The games generated enough revenue to keep the lights on, but not enough to justify the ambitions of a media conglomerate like Axel Springer.

By the late 2000s, Springer had taken full ownership of gamigo — consolidating its stake in 2009 — and was in the midst of a strategic overhaul that would transform it from a traditional publishing house into a digital media powerhouse. The priority was premium digital assets: classified advertising (through acquisitions like StepStone and Immowelt), news (Bild, Die Welt), and eventually business media (the 2015 acquisition of Business Insider).

A small online games publisher with thin margins, aging titles, and no clear path to scale did not fit the vision. In the lexicon of corporate strategy, gamigo was a "non-core asset" — the polite term for a business unit that the parent company has decided to stop caring about.

In October 2012, Springer divested its entire stake to Samarion S.E., a Düsseldorf-based investment vehicle. The sale price was never publicly disclosed.

In deal-making parlance, an undisclosed price for a division being shed by a major corporation usually means it was embarrassingly low — likely a nominal sum in exchange for taking the liabilities and employees off Springer's hands. gamigo was, for all practical purposes, a castoff. It was the kind of deal that generates a one-line mention in the acquirer's annual report and a collective shrug from the financial press.

This is where Remco Westermann enters the picture, and the story takes its decisive turn.

Westermann, who holds a master's degree in business economics, was not a gamer. He had never designed a game, never run a gaming studio, and by his own account had no particular passion for the gaming industry as such.

What he was, definitively, was a serial operator in the mobile and digital entertainment space. He had founded Bob Mobile AG, a publicly listed mobile entertainment company in Germany. Before that, he had served as CEO of the German subsidiary of Sonera Zed, a mobile media company owned by the Finnish telecom group.

His career had been spent at the intersection of technology, media, and financial engineering — building, buying, and restructuring digital businesses. He was not the kind of person who stayed up late debating whether a mage or a warrior was the better class choice. He was the kind of person who stayed up late modeling the cash flows of the company that published the game where those debates happened.

Westermann looked at gamigo and saw what a game designer would never see: a cash-flow machine hiding inside a collection of low-value assets.

The games were "dying" in the sense that they were past their growth phase and losing players to newer titles. But dying games have an underappreciated financial characteristic. Their development costs have already been sunk. Their server infrastructure is paid for. Their remaining player base, while declining, is intensely loyal — these are players who have invested hundreds or thousands of hours in their characters and communities.

They continue to make in-game purchases at a remarkably stable rate, even as the total player population slowly shrinks. The result is a stream of predictable, high-margin cash flow that can persist for years. It is the digital equivalent of a toll bridge that still collects tolls long after the construction bonds have been paid off.

Westermann became CEO following the Samarion takeover and immediately set about executing what might be called the "mop-up strategy." The free-to-play gaming market in the mid-2010s was littered with studios in the same position gamigo had been in: past-their-peak games with dedicated player bases, owned by companies that had lost patience waiting for a growth reacceleration that was never coming. Venture-backed studios were running out of runway. Corporate parents were divesting non-core assets. Independent publishers were looking for exits. Westermann was the buyer of last resort — and he was perfectly content with that role.

The acquisition discipline was rigorous. He targeted properties trading at just one to two times EBITDA, sometimes even less. He would buy the game, migrate it to gamigo's shared server infrastructure (eliminating redundant hosting and IT costs), cut the development team (no new content investment — just maintain the servers and the microtransaction shop), and optimize the monetization.

The result was a portfolio of dozens of game titles across multiple genres. None were hits. None needed to be. The strategy was not about finding the next World of Warcraft. It was about buying a portfolio of "good enough" games that collectively generated predictable, recurring revenue. Each title was a small stream; combined, they formed a river.

Think of it as the gaming equivalent of a real estate investor buying B-class apartment buildings in secondary markets. The properties will never appreciate dramatically. The tenants are not glamorous. But the rent checks clear every month, maintenance costs are predictable, and over time the portfolio compounds quietly while everyone else is chasing trophy assets. By 2018, Westermann had accumulated enough scale — and enough predictable cash flow — to take the company public on the Frankfurt Stock Exchange's Scale segment under the name Media and Games Invest.

The Frankfurt listing was a means to an end. The Scale segment — designed for smaller growth companies with lighter regulatory requirements than the main market — gave Westermann access to public market capital while maintaining the operational flexibility of a private company.

The IPO raised modest capital and gave the gaming portfolio a public market valuation, but the real significance was what it funded. The gaming cash flows had accumulated enough "dry powder" for the pivot Westermann had been planning all along. And that pivot, when it came, would make the gaming chapter look like nothing more than prologue.

The inflection point came in January 2020 with the acquisition of Verve Wireless. On paper, this was a modest deal — perhaps the least dramatic acquisition in the company's history.

Verve Wireless was a mobile programmatic advertising company founded in 2005, with offices in New York and San Diego. It had been a pioneer in location-based ad targeting, using GPS and other location signals to serve relevant ads to mobile users. The idea was compelling: if you know someone is standing near a coffee shop, you can serve them a coffee ad. But Verve Wireless had failed to achieve the scale needed to compete with the giants of programmatic advertising, and by 2019, the company was available at a distressed price.

The expected financial contribution was modest: low double-digit million euros in additional revenue and low single-digit million euros in EBITDA in its first year. This was not a deal that made headlines.

But Westermann was not buying revenue. He was buying three things. First, a technology stack for programmatic mobile advertising that was production-tested and operational. Second, a brand name — "Verve" — that would eventually replace his own company's identity. And third, the foundation for a privacy-first advertising platform at a moment when the entire industry was about to be forced to find alternatives to identifier-based tracking.

The timing was extraordinary. Within months of the Verve Wireless deal closing, Apple announced App Tracking Transparency, the privacy framework that would reshape the mobile advertising industry.

Whether Westermann anticipated this specific move or simply understood the broader direction of travel is debatable. What is not debatable is that by the time the industry woke up to the privacy revolution, Westermann already had the building blocks in place. In business, timing is often dismissed as luck. But consistently being in the right place at the right time starts to look less like luck and more like judgment.

By May 2020, Westermann had consolidated Verve Wireless with PubNative — a mobile supply-side platform acquired through the 2019 AppLift deal — and AppLift itself under a single umbrella: the Verve Group.

The adtech play was no longer a side bet. It was the main event. And the gaming portfolio that had seemed like the whole company just two years earlier was being repositioned as a strategic data asset — a hundred-million-user sandbox for testing advertising technology. The caterpillar had begun its metamorphosis, and the butterfly would look nothing like what came before.

III. The M&A Machine: Building the Stack

To understand Verve Group's acquisition strategy, you first need to understand the plumbing of the digital advertising industry. The technology is complex, but the concept is surprisingly simple if you think of it as a marketplace — like a stock exchange, but instead of trading shares, buyers and sellers are trading the right to show you an ad.

On one side, you have publishers — websites, mobile apps, games — who have "inventory." Every time you open a news article or launch a mobile game, there are empty ad slots on the screen waiting to be filled. The publisher wants to fill those slots with ads that pay the highest price. On the other side, you have advertisers — brands like Nike, agencies like WPP — who want to reach specific audiences. Nike wants to show its new running shoe ad to twenty-five-year-old fitness enthusiasts, not to seventy-year-old gardeners. The advertiser wants to find those audiences and bid on the right to show them ads.

Connecting these two sides is a complex chain of technology that operates in real time. When you open an app and an ad slot needs to be filled, the publisher's technology sends out a "bid request" to dozens or hundreds of potential buyers simultaneously. Those buyers evaluate the opportunity — who is the user? what app are they in? what time of day is it? — and submit bids within milliseconds.

The highest bidder wins, their ad appears on the user's screen, and the whole process takes less time than it took to read this sentence. This is "programmatic advertising," and it accounts for the vast majority of digital ad spending today. The sheer scale is staggering: trillions of these auctions happen every day, invisibly, behind every app and website you visit.

Within this ecosystem, there are specialized roles. Supply-Side Platforms, or SSPs, help publishers manage their inventory and run the auctions. Think of the SSP as the publisher's agent — it maximizes the revenue from each ad slot by connecting to many potential buyers and running efficient auctions. Demand-Side Platforms, or DSPs, sit on the other side, helping advertisers find the right audiences and bid on inventory across thousands of publishers simultaneously. Think of the DSP as the advertiser's agent. And ad exchanges sit in the middle, facilitating the actual transactions.

Most adtech companies specialize in one piece of this chain. Magnite and PubMatic are primarily SSPs — they represent publishers. The Trade Desk is the dominant independent DSP — it represents advertisers. AppLovin has built a vertically integrated platform focused on mobile gaming, but even it started primarily on the demand side. Specialization is the norm because each piece of the chain requires deep domain expertise and massive technical investment.

What made Westermann's vision distinctive — and what made many observers initially skeptical — was the ambition to own the whole stack: the content (games), the supply side (SSP), and the demand side (DSP). In his framing, owning all three creates a flywheel where each piece makes the others more valuable.

The games generate users, the SSP monetizes those users' ad inventory, and the DSP gives advertisers a direct channel to buy that inventory — with Verve capturing margin at every step and learning from every transaction.

It is the programmatic advertising equivalent of vertical integration in manufacturing — except the raw materials are attention, the factory is code, and the finished product is a precisely targeted ad impression. Whether this vertically integrated model would work in practice, or whether it would produce the same kind of organizational complexity that has hobbled other "do everything" technology companies, would depend entirely on execution. And execution, for Westermann, meant acquisitions.

The Verve Wireless deal in 2020 established the supply-side foundation. But building a globally competitive SSP required scale that the combined Verve Wireless and PubNative assets could not deliver on their own. The programmatic advertising business is ruthlessly scale-dependent: publishers want to connect to SSPs that bring the most demand (because more bidders means higher prices), and advertisers want to connect to SSPs that have the most inventory (because more supply means more opportunities to find the right audience at the right price). This creates a classic network effect where the big get bigger and the small get squeezed out.

The answer was Smaato, and the deal that closed in July 2021 transformed Verve from a promising upstart into a legitimate global player.

Smaato was a heavyweight — a top-ten global mobile ad exchange processing billions of ad requests daily, with a footprint spanning thousands of publisher apps worldwide. Founded in Hamburg, Germany, in 2005, Smaato had built a strong technology platform and a global publisher network over sixteen years.

The company had been acquired in 2016 by Spearhead Integrated Marketing Communication Group, a Shanghai-based marketing firm, but the cross-cultural and cross-geographic ownership had failed to produce the synergies either side expected. By 2021, Smaato was available — and Westermann pounced.

The price was approximately one hundred and seventy million dollars — a significant step up from the distressed gaming assets Westermann had been buying at one to two times EBITDA. At roughly three and a half times Smaato's revenue, the multiple raised eyebrows among investors accustomed to Verve's penny-pinching deal discipline.

But context matters enormously here. The adtech M&A market in 2021 was white-hot. Magnite had acquired SpotX for approximately 1.17 billion dollars earlier that year — a deal valued at roughly five times revenue. AppLovin would later acquire MoPub from Twitter for over one billion dollars. IronSource merged with Unity in a multi-billion-dollar combination.

Against this backdrop, Verve's Smaato deal looked like a relative bargain, buying comparable technology at a meaningful discount to what larger players were paying.

The deal loaded Verve's balance sheet with meaningful debt — a trade-off that would define the company's financial story for years to come. But the strategic logic was sound.

Overnight, Verve went from processing modest volumes to operating a top-ten global mobile ad exchange. The combined supply-side platform — Verve Wireless plus PubNative plus Smaato — reached approximately two billion users globally. The "scale problem" was, if not fully solved, dramatically improved.

The integration playbook was where Verve's approach diverged most sharply from typical adtech M&A. In many acquisitions across the industry, the acquiring company lets the purchased business continue to operate semi-independently, keeping its own technology stack, its own brand, and much of its own overhead.

Verve did the opposite. Every acquisition went through the same rigorous integration process: migrate the acquired platform's technology onto Verve's centralized infrastructure, consolidate sales teams and eliminate redundant corporate overhead, and unify the customer base onto a single platform. The target was to strip out thirty to forty percent of the acquired company's overhead within twelve to eighteen months.

This is what Verve calls "synergy math," and it is the financial engine that makes the M&A machine work.

Instead of running Smaato as a standalone business with its own servers, engineering team, sales force, and corporate overhead, Westermann's team absorbed it into the Verve platform. The headcount could be reduced because Verve already had engineers maintaining a similar tech stack. The server costs could be reduced because Verve already had infrastructure running at scale. The sales costs could be reduced because the same sales team could now offer publishers a larger combined platform.

The result was not just revenue addition but margin expansion — the acquired business becomes more profitable as part of Verve than it was on its own. It is a simple formula, but executing it consistently across dozens of deals requires operational discipline that most companies never develop.

The third major deal completed the strategic puzzle. On July 31, 2024, Verve acquired Jun Group from Advantage Solutions for one hundred and eighty-five million dollars.

Jun Group was the demand-side play — the piece Verve had been missing. While the Verve Wireless and Smaato deals built the supply side (helping publishers sell their ad inventory), Jun Group brought direct relationships with over two hundred and thirty Fortune 500 advertisers and agencies in the United States. These are the buy-side relationships — the brands actually spending money on advertising — that fuel the revenue flowing through the supply-side pipes.

If the SSP was the highway, Jun Group was the fleet of trucks. You need both to move cargo.

The deal structure revealed Verve's increasing financial sophistication. The total consideration of approximately one hundred and seventy million euros on a cash-and-debt-free basis was structured with roughly one hundred and twenty million euros in cash at closing, plus two deferred installments of approximately twenty-five million euros each at twelve and eighteen months post-close.

This staggered payment structure served multiple purposes: it reduced the upfront cash burden, it created an implicit escrow mechanism (if the business underperformed, Verve would be making deferred payments on a diminished asset), and it aligned the seller's incentives with a smooth transition.

The financial impact was immediate and telling. On a pro forma basis for 2024, the combined entity generated approximately four hundred and forty-seven million euros in revenue and one hundred and fifty-one million euros in adjusted EBITDA. Jun Group alone added roughly twenty-three percent to revenue and an outsized forty-three percent to adjusted EBITDA.

That disproportionate EBITDA contribution is the key number: it means Jun Group operated at substantially higher margins than Verve's legacy business, suggesting the demand-side economics (where platforms charge advertisers fees for access and optimization) are inherently more profitable than the supply-side exchange business. This is why management's long-term target of a fifty-fifty revenue split between SSP and DSP is so important — it implies a structural margin improvement as the mix shifts.

The pace did not stop there. In September 2025, Verve acquired Captify, a search intelligence and contextual advertising specialist, for approximately twenty-six million euros. In October 2025, it added acardo, a German coupon and retail media platform, for roughly twenty-five million euros. These were smaller, bolt-on deals, but they followed the same logic: fill capability gaps, bolt them onto the platform, strip out cost, and cross-sell to the existing customer base.

Across more than thirty-five acquisitions spanning gaming and adtech, Verve has developed a pattern that resembles what Constellation Software practices in vertical market software or what Danaher perfected in industrial instrumentation: serial acquisition of niche businesses, integration onto a common platform, margin expansion through shared infrastructure, and reinvestment of cash flows into the next deal.

The critical question — and one the market has not yet fully answered — is whether Verve can sustain this discipline as deal sizes grow and integration complexity compounds. Thirty-five small acquisitions are one thing. Integrating hundred-million-dollar-plus platforms with thousands of publisher and advertiser relationships is a different challenge entirely.

The most recent acquisitions suggest the appetite remains strong. In September 2025, Verve acquired Captify, a search intelligence company, for approximately 25.6 million euros, and in October 2025, it added acardo, a digital promotions platform, for roughly 24.5 million euros. Both were smaller, tuck-in deals that expand the company's data capabilities without adding to the integration burden of the Jun Group assimilation. The M&A machine, it seems, has not stopped — it has merely downshifted to a lower gear while the larger deals are digested.

IV. Management and Incentives

Remco Westermann is not the kind of CEO who gives rousing keynote speeches at CES or tweets about the future of the metaverse. He is an engineer and a dealmaker, more comfortable in a spreadsheet than on a stage. In an industry where CEOs routinely promote themselves as "visionaries" and "thought leaders," Westermann maintains a conspicuously low public profile. He does not have a significant presence on social media. His rare public interviews — notably a well-known conversation with the Swedish research firm Redeye around the time of the 2024 rebranding — are characterized by precise financial language and a reluctance to engage in the kind of speculative optimism that adtech executives often traffic in.

Colleagues and analysts describe a methodical operator who approaches every acquisition with the same analytical framework: What is the asset worth on a standalone basis? What are the integration costs and timeline? What is the marginal contribution to platform scale? What does the deal do to adjusted EBITDA per share?

This analytical culture permeates the organization and stands in sharp contrast to the "growth at all costs" mentality that defined much of the adtech industry during the 2020-2021 boom. Where other CEOs chased headlines with billion-dollar deals, Westermann consistently bought the assets nobody else wanted and turned them into something nobody expected.

The alignment of incentives tells a powerful story. Westermann personally holds ninety percent of Sarasvati GmbH, which in turn holds one hundred percent of Bodhivas GmbH, the entity that owned approximately 24.38 percent of Verve Group's shares as of March 2025.

Let that ownership structure sink in for a moment. Nearly a quarter of the entire company is economically controlled by the CEO. For a company that Westermann did not technically found — he acquired a struggling gamigo through the Samarion vehicle in 2012 — this level of ownership concentration is extraordinary.

It creates what investors call "founder-led economics" in a non-founder company. Westermann may not have written the first line of code or registered the original corporate entity, but he has built the vast majority of the value that exists today — and he has done so with a proportion of his own capital on the line that would make most professional CEOs uncomfortable.

The practical implication is straightforward: when Verve's stock price rises by ten percent, Westermann's net worth increases by roughly the same proportion of a substantial personal fortune. When it drops, he feels it.

There are no golden parachutes, no stock options with exercise prices set conveniently below water, no financial engineering that cushions the CEO from the same pain felt by outside shareholders. This kind of alignment is rare in European corporate governance, where professional managers frequently own token equity positions and rely on guaranteed salary and bonus packages for their compensation. Westermann is not playing with house money. He is playing with his own.

Beyond the ownership stake, Westermann has been a consistent buyer of shares on the open market, with multiple insider purchase transactions documented in regulatory filings over the past several years. This is the kind of behavior institutional investors pay particular attention to. There is a well-documented asymmetry in insider trading signals: insider selling is often meaningless (executives sell for all sorts of personal financial reasons — taxes, diversification, buying a house), but insider buying is almost always meaningful. A CEO who buys shares with his own money, after taxes, when he already owns a quarter of the company, is making an unambiguous statement about his view of intrinsic value versus market price.

The broader management incentive structure reinforces this ownership alignment. The Long Term Incentive Plan approved at the June 2024 annual general meeting covers approximately fifty key employees, including top management, with a maximum allocation of 4.75 million Class A shares delivered through directed warrants (series 2024/2036). The performance metric underlying the LTIP is the critical detail: management is compensated based on adjusted EBITDA per share rather than simple top-line revenue growth.

This distinction is more important than it might initially appear. A management team compensated on revenue growth has every incentive to do dilutive acquisitions — issuing millions of new shares to buy companies that boost the top line but add little per-share value.

A team compensated on EBITDA per share has to care about three things simultaneously: growing profitability, managing capital allocation efficiently, and avoiding unnecessary dilution. Every acquisition, every share issuance, every debt raise gets filtered through a single question: does this grow earnings per share? The LTIP structure creates a natural brake on the empire-building tendency that plagues many serial acquirers.

The appointment of Christian Duus as Chief Financial Officer, effective January 2025, added another layer of credibility to the management bench. Duus came from Adform, one of the most respected independent adtech platforms in Europe, and before that spent years at Bain & Company. His combination of strategic consulting pedigree and hands-on adtech operating experience suggests a company that is professionalizing its finance function in anticipation of the next stage of growth — and perhaps in preparation for the deleveraging story to become the dominant narrative.

Verve's approach to capital markets has been equally deliberate and is worth understanding as a piece of the management story. In October 2020, the company added a dual listing on Nasdaq First North Premier Growth Market in Stockholm, raising capital through a placement of twenty-five million new shares at twelve Swedish kronor per share. Why Stockholm? Because Frankfurt's Scale segment attracted primarily German institutional investors and retail traders oriented toward traditional "old economy" businesses — manufacturing, automotive, chemicals, real estate. Explaining why a gaming-company-turned-adtech-platform deserves a SaaS-like multiple to an investor base that thinks in terms of price-to-book and dividend yield is an uphill battle.

The Stockholm exchange, by contrast, had developed a deep bench of investors fluent in platform economics, SaaS metrics, and recurring revenue business models. Sweden's tech ecosystem — home to companies like Spotify, Klarna, and a vibrant universe of mid-cap tech companies listed on Nasdaq Nordic — had produced an investor base that understood what "net revenue retention," "take rate," and "programmatic yield" meant.

By seeking out capital that understood the model, Westermann could attract a more patient shareholder base willing to look past the company's complex corporate history and leveraged balance sheet to evaluate the underlying business quality.

The strategy continued with the May 2025 uplisting from the Scale segment to the Regulated Market of the Frankfurt Stock Exchange, effective from May 12 of that year. This move broadened the potential investor base by making Verve eligible for inclusion in indices and accessible to institutional investors with mandates restricted to regulated market securities.

Each capital markets move — the Frankfurt IPO in 2018, the Stockholm dual listing in 2020, the rebrand in 2024, the Frankfurt uplisting in 2025 — reflects a consistent philosophy: match the investor base to the business model, and ensure the people running the company eat their own cooking.

V. The "Hidden" Engines and Segment Deep Dive

If you visit Verve Group's investor relations page today, the financial reports break the business into two segments: Supply Side Platform and Demand Side Platform. This clean taxonomy masks a more complex and interesting reality — one that requires peeling back the layers to understand where the real value creation is happening and where the growth potential lies.

The supply side — built on the foundation of Verve Wireless, PubNative, and Smaato — is the company's revenue backbone. This is the ad exchange infrastructure that processes billions of ad impressions daily across thousands of publisher apps. In simple terms, think of the SSP as a wholesale market. Publishers bring their ad inventory — every ad slot in every mobile game, news app, and utility app that uses Verve's technology. Verve's platform runs real-time auctions, measured in milliseconds, where dozens of potential advertisers compete to show their ad. The highest bidder wins. The publisher gets paid. Verve takes a percentage of the transaction as its fee — the "take rate" that is the fundamental economic unit of any ad exchange.

The economics of an SSP are driven by volume and efficiency. Every billion additional impressions processed through the platform spreads Verve's fixed costs (servers, engineering salaries, data center leases) across a larger transaction base. The marginal cost of processing the ten-billionth impression is nearly zero if the infrastructure is already in place for the first nine billion. This creates a natural scale advantage: larger SSPs can afford to charge publishers lower take rates while still generating more absolute profit, making it harder for smaller competitors to match both the price and the service level.

The demand side, built primarily on the 2024 Jun Group acquisition and the smaller Match2One platform, represents the more strategic and potentially more valuable half of the business. This is where advertisers come to buy.

Jun Group's direct relationships with over two hundred and thirty Fortune 500 brands give Verve something most independent adtech companies lack: demand that it controls, rather than demand it must compete for through open auctions. When a Fortune 500 brand wants to run a mobile advertising campaign, it can go to Jun Group's team directly, which then uses Verve's technology to find the right audiences across Verve's supply-side inventory.

The margin capture on this kind of "managed service" is significantly higher than on open-exchange transactions. Think of the difference between a commodity broker facilitating anonymous trades and a private wealth manager offering bespoke service — the same underlying product, but dramatically different economics.

The revenue split between the two segments tells its own story. The SSP currently generates roughly seventy-five percent of total revenue, with the DSP contributing the remaining twenty-five percent. Management has publicly stated a long-term target of reaching a fifty-fifty balance between the two sides. If they achieve that rebalancing while maintaining or growing total revenue, the margin implications are significant — the demand side operates at higher margins than the supply side, so every percentage point of mix shift toward the DSP lifts the blended margin of the entire business.

The real power of owning both sides becomes clear when you follow the money. In a typical programmatic advertising transaction, an advertiser's dollar might pass through four or five intermediaries before reaching the publisher — a DSP, an ad exchange, an SSP, and various data providers each taking their cut. Industry studies have shown that publishers often receive less than fifty cents of each dollar an advertiser spends, with the rest consumed by the "adtech tax."

When an advertiser using Verve's DSP buys inventory on Verve's SSP, the company captures margin on both sides of the transaction and eliminates the intermediaries in between. More of each ad dollar reaches the publisher (making Verve's SSP more attractive to publishers) and more of each dollar is spent on actual ad delivery rather than intermediary fees (making Verve's DSP more attractive to advertisers). This is the flywheel in action — and it spins faster with every new publisher and advertiser that joins the platform.

But the real technological differentiator — the product that turns heads among privacy-conscious publishers and performance-oriented advertisers alike — is ATOM. The acronym stands for Anonymized Targeting on Mobile, and understanding what it does requires a brief detour into the mechanics of ad targeting and why the traditional approach is breaking down.

For years, mobile advertising relied on a unique identifier assigned to every smartphone. On iPhones, this was Apple's IDFA — Identifier for Advertisers. On Android devices, it was Google's GAID — Google Advertising ID. These identifiers functioned like social security numbers for your phone: they allowed advertisers, data brokers, and ad platforms to build detailed profiles of individual users across apps and websites. If you opened a fitness app in the morning, browsed a sneaker website at lunch, and played a mobile game in the evening, all three of those data points could be linked back to your IDFA and used to build an advertising profile. Advertisers would then bid more aggressively to show ads to users whose profiles matched their target audience.

The system worked extraordinarily well for advertisers and terribly for privacy. When Apple introduced App Tracking Transparency in April 2021, requiring every iOS app to display a pop-up asking users for explicit permission to track them across apps and websites, the results were devastating for the existing model.

The opt-in rate plummeted to roughly twenty to twenty-five percent. Overnight, seventy-five percent of iPhone users became effectively invisible to the traditional targeting infrastructure. For context, iPhone users tend to be higher-income and more valuable to advertisers than the average mobile user, so losing visibility into this demographic was particularly painful. The highest-value customers disappeared from the screen — literally.

The industry response was a mixture of despair and desperate improvisation. Meta — the company formerly known as Facebook — famously warned investors that Apple's privacy changes would cost it ten billion dollars in annual revenue in 2022 alone, and the actual impact may have been even larger.

Smaller adtech companies saw their targeting accuracy collapse and their revenue per impression fall off a cliff. Some pivoted to "contextual advertising" — targeting based on the content of the page rather than the identity of the user (showing car ads on automotive websites, for example). Others tried to build probabilistic identity graphs that could infer user identity from fragments of data without relying on a single identifier.

Many simply went out of business. The privacy revolution was not a rising tide that lifted all boats — it was a tsunami that sank most of them.

Verve took a fundamentally different approach, and it was this approach that would prove to be the company's most important strategic asset.

Instead of trying to identify individual users through workarounds or replacements for the deprecated identifiers, ATOM processes signals entirely on the user's device. Here is how it works in practice: when a user has an app with Verve's SDK installed, the ATOM technology uses on-device machine learning — small AI models running directly on the smartphone — to analyze behavioral patterns without ever transmitting personal data off the device.

What kinds of patterns? Think about the signals your phone generates throughout the day that have nothing to do with your identity: which categories of apps you use most frequently, how long your typical session lasts, what time of day you are most active, whether you tend to use apps in short bursts or long sessions, your screen brightness settings, your gesture patterns (how you scroll, how quickly you navigate).

Individually, none of these signals reveal who you are. But collectively, processed through machine learning models, they can classify users into broad audience cohorts — "Tech Enthusiasts," "Active Gamers," "Health and Fitness Advocates," "Parents," "Luxury Shoppers" — with remarkable accuracy. The analogy is imperfect but instructive: a skilled bartender does not need to know your name or see your ID to know whether you are a craft beer person or a cocktail person. They read the signals — how you carry yourself, what you order first, whether you check your phone or talk to the person next to you — and make an informed judgment.

Crucially, no personal data ever leaves the device. There is no user identifier, no cross-app tracking, no personally identifiable information transmitted to Verve's servers or to advertisers. The classification happens on-device, and only the cohort label — "this user is likely a Tech Enthusiast" — is transmitted to the ad auction.

This means ATOM is compliant with GDPR, Apple's ATT framework, and virtually every privacy regulation in existence, because it never collects the kind of data those regulations restrict. It is a genuinely elegant solution to what most of the industry treated as an unsolvable problem.

ATOM launched in its first iteration in 2021, and the latest version — ATOM 3.0 — is integrated into Verve's standard SDK across more than ten thousand apps. The technology has become Verve's fastest-growing high-margin product, because it solves a problem that hundreds of billions of advertising dollars are chasing: how do you deliver relevant, targeted ads to users who have opted out of tracking?

The gaming portfolio plays a subtle but critical role in this ecosystem. Verve's owned-and-operated game properties — the legacy of those gamigo-era mop-up acquisitions — generate first-party data from over one hundred million users. These are not third-party data points acquired from brokers or inferred from fragments. This is data from users actively engaging with content that Verve owns and controls.

The games serve as a controlled laboratory where Verve can test new ad formats, train and optimize ATOM's machine learning models, validate targeting performance against known outcomes, and refine the technology before offering it to third-party publishers. It is a sandbox that competitors simply cannot replicate without building or acquiring their own content properties — and that is precisely the strategic connection between the "old" gaming business and the "new" adtech platform.

When Verve divested its remaining PC and console gaming assets in April 2023, it retained the mobile gaming properties specifically because of this data advantage. The divestiture was itself revealing: it showed that management understood exactly which pieces of the legacy gaming portfolio were strategically essential and which were simply legacy deadweight.

The financial evidence suggests the strategy is working. In the fourth quarter of 2025, Verve reported a gross margin of 44.6 percent, up sharply from 40.6 percent in the same quarter of the prior year and up dramatically from 36.6 percent in the third quarter of 2025.

This expansion reflects the growing share of high-margin, technology-driven revenue — particularly from ATOM-powered campaigns and managed-service demand-side offerings — relative to lower-margin commodity ad exchange volume. The trajectory is unmistakable: the business is shifting from commodity exchange to technology platform, and the margins are following.

The company's platform unification, which consolidated all acquired technologies onto a single tech stack and was completed in late 2025, removed redundant infrastructure and enabled more efficient cross-selling across the supply and demand sides. As the full customer base migrates to the unified platform, these margin dynamics should continue to improve.

VI. Framework Analysis: 7 Powers and 5 Forces

Understanding where Verve Group sits in the competitive landscape requires stepping back from the financial details and looking at the business through two complementary analytical lenses: Hamilton Helmer's 7 Powers framework, which identifies the structural sources of durable competitive advantage, and Michael Porter's 5 Forces, which maps the industry dynamics that determine profitability.

Starting with Helmer's framework, three of the seven powers are most relevant to Verve's position.

The first is what Helmer calls a Cornered Resource — an asset that competitors cannot easily replicate or acquire, and that confers an ongoing benefit to the business. For Verve, this is the first-party data generated by its gaming portfolio. Over one hundred million users actively playing games that Verve owns and operates produce behavioral signals that feed ATOM's machine learning models and inform targeting algorithms. This is not scraped data or purchased data — it is proprietary, first-party data generated on platforms Verve controls. A pure-play SSP like Magnite or PubMatic can aggregate third-party publisher data, but they cannot replicate the controlled, first-party data environment that comes from owning the content itself. The Trade Desk can buy data from thousands of sources, but it does not own the content that generates the data. This is the moat that the "dying games" built, and it is perhaps the most ironic twist in the entire Verve story: the assets that seemed least valuable turned out to be the most strategically important.

The second relevant power is Scale Economies. Programmatic advertising is a volume business where the economics improve dramatically with scale, and the improvement is non-linear. Every additional billion impressions processed through Verve's platform spreads the fixed costs of infrastructure, engineering talent, R&D investment, and regulatory compliance across a larger transaction base. The marginal cost of processing additional volume approaches zero once the infrastructure is built. This creates the dynamic that industry practitioners call the "AdTech Tax" — the percentage of each ad dollar consumed by the technology platform. As Verve scales, its per-unit cost drops, allowing it to offer publishers a larger share of ad revenue (attracting more supply) or offer advertisers better performance at lower cost (attracting more demand), creating a virtuous cycle that is very difficult for smaller competitors to break into.

The third power is Switching Costs, which in Verve's case operate at a technical level that makes them particularly sticky. When a publisher integrates Verve's SDK — its software development kit — into a mobile app, the integration is not trivial. It involves engineering work to embed the code, testing to ensure compatibility with the app's existing functionality, certification by app stores (both Apple and Google review SDK integrations as part of their app review processes), and weeks or months of yield optimization to maximize revenue.

Once this work is done and the SDK is generating revenue, switching to a competitor's SDK means repeating the entire process — at a cost in engineering time, testing risk, temporary revenue disruption, and opportunity cost.

The deeper the integration — particularly with ATOM's on-device machine learning models, which improve over time as they learn from the specific app's user behavior — the higher the switching costs become. Publishers who have been running Verve's SDK for years have effectively trained the system to optimize for their specific audience, and walking away from that accumulated learning would mean starting from scratch. It is like switching from a doctor who has treated you for a decade to one who has never seen your file — technically possible, but costly in ways that go beyond the obvious.

Now turn to Porter's 5 Forces, which paint a more nuanced and in some cases more cautionary picture.

The bargaining power of buyers — in this context, the advertisers who spend money on programmatic ads — is a study in contradictions. On one hand, the digital advertising market is dominated by two walled gardens: Google and Meta together control a combined share exceeding fifty percent of global digital ad spend. Advertisers have enormous choice and can always shift budgets back to the duopoly if independent platforms fail to deliver. On the other hand, the very dominance of Google and Meta has created intense demand among brands and agencies for independent alternatives. Concentration risk is a real concern for chief marketing officers, and the regulatory scrutiny facing both Google and Meta creates additional incentive to diversify. Brands that want to reduce their dependence on the duopoly are actively seeking platforms like The Trade Desk, Magnite, and Verve. This structural demand for alternatives provides independent adtech players with meaningful pricing power, particularly those — like Verve — that can offer differentiated capabilities like privacy-compliant targeting.

The bargaining power of suppliers — publishers providing ad inventory — is moderate and varies by publisher size. Large publishers with premium, brand-safe inventory — think major news organizations, top-tier gaming companies, and popular utility apps — have significant leverage and can negotiate favorable revenue shares or even exclusive arrangements. Smaller publishers, particularly long-tail mobile app developers who generate modest traffic, have less bargaining power and rely heavily on platforms like Verve to monetize their impressions. Verve's position as both an SSP serving thousands of publishers and a content owner operating its own games gives it unusual insight into publisher economics — it knows exactly what margins are reasonable because it experiences both sides of the equation.

The threat of new entrants is low in the current environment, and arguably declining. Building a programmatic advertising platform from scratch requires massive upfront investment in infrastructure (servers, data centers, real-time bidding systems capable of processing millions of auctions per second), relationships with thousands of publishers and advertisers (which take years to develop), regulatory compliance across multiple jurisdictions (GDPR, CCPA, ATT, and an ever-expanding alphabet of privacy frameworks), and years of accumulated data to train optimization algorithms. The industry has already consolidated significantly from the hundreds of adtech startups that existed a decade ago to a handful of scaled players. The remaining independents benefit from barriers to entry that grow with each passing year.

The threat of substitutes is the most concerning of the five forces for Verve — and for the independent adtech ecosystem broadly. The rise of closed-ecosystem advertising on platforms like TikTok, Amazon, and Apple's own growing ad business represents a meaningful and potentially existential alternative to open-web programmatic advertising. When an advertiser spends a dollar on TikTok's in-app advertising platform, that dollar never enters the open programmatic ecosystem where Verve operates. It goes directly to TikTok, which owns the content, the audience data, the ad serving technology, and the measurement — the complete vertical stack, but in a walled garden. Amazon's advertising business, which has grown to over forty billion dollars in annual revenue, operates the same way. Apple, which has been steadily expanding its own ad platform while restricting competitor access to iOS user data, represents perhaps the most direct threat to companies like Verve. Every privacy restriction Apple imposes on third-party advertising makes Apple's own first-party ad platform more relatively valuable.

However, Verve's focus on mobile gaming — a specific content vertical where in-game advertising requires specialized technology (rewarded video ads, playable ads, interstitial formats that do not disrupt gameplay) — provides some insulation from this threat. TikTok and Amazon are powerful in their respective domains but have limited presence in mobile gaming ad formats.

Competitive rivalry is intense and requires honest assessment. The independent adtech space includes well-capitalized public companies operating at dramatically different scales. The Trade Desk commands a market capitalization exceeding forty billion dollars. AppLovin, riding the success of its Axon 2.0 AI-driven optimization engine, has surged past one hundred billion dollars in market value — a breathtaking number for an adtech company. Magnite sits at roughly 1.7 billion dollars in market cap. PubMatic at roughly one billion. And then there is Verve, at approximately three hundred million dollars — the smallest among its publicly traded peers by a wide margin.

The question investors must grapple with is what this size gap means. Is Verve's smaller scale a genuine competitive disadvantage that will eventually lead to marginalization as larger players benefit from superior scale economies and deeper pockets?

Or is it a market mispricing driven by the company's European listing, complex corporate history, leveraged balance sheet, and the name-change confusion that caused many investors to simply lose track of the company? The answer probably contains elements of both — the leverage is a real constraint, and the European listing is a real handicap — but the magnitude of the valuation gap suggests that at least some of it is mispricing.

The answer probably contains elements of both — the leverage is a real constraint, and the European listing is a real handicap in attracting the US-centric growth investors who set multiples in adtech — but the magnitude of the valuation gap suggests that at least some of it is mispricing.

For investors tracking Verve's competitive position over time, two KPIs matter more than any others. The first is organic revenue growth — not total revenue growth, which is inflated by acquisitions, but the underlying growth of the existing platform excluding recently acquired businesses. In 2025, this metric told a complicated story: organic growth decelerated to 5.3 percent for the full year, depressed by the disruptive effects of the platform migration that unified all acquired technologies onto a single stack. But the fourth-quarter exit rate was more encouraging — 9.9 percent organic growth — suggesting the unified platform was beginning to deliver on its promise. The trajectory of this number over the next several quarters will determine whether Verve is a genuine organic growth business or primarily an M&A-driven roll-up that needs continuous acquisitions to maintain its growth narrative.

The second critical KPI is adjusted EBITDA margin, which captures the efficiency of the platform and the success of acquisition integration. Verve has consistently delivered margins in the twenty-four to twenty-five percent range, which is respectable but not exceptional by adtech standards. However, the gross margin expansion visible in late 2025 — from 36.6 percent in Q3 to 44.6 percent in Q4 — driven by ATOM adoption and platform unification, hints at meaningful operating leverage that has yet to flow through to the EBITDA line. If adjusted EBITDA margins can expand toward thirty percent and beyond as the unified platform scales and high-margin ATOM revenue grows as a share of the mix, the business begins to look much more like a high-quality software platform and less like a middleman clipping tickets on commodity ad transactions.

VII. The Playbook: Business Lessons

There is a school of business strategy that says the most durable competitive advantages are built not by doing one extraordinary thing, but by combining ordinary things in ways that are extraordinarily difficult to replicate.

Verve Group is a case study in this principle. Each individual element of the strategy — buying distressed assets, integrating acquisitions, building privacy technology, listing on multiple exchanges — is something other companies have done. But the combination, executed over a decade by a management team with skin in the game, has produced something genuinely distinctive.

Three lessons from the Verve playbook stand out as particularly instructive — not just for adtech, but for anyone building a technology business in a rapidly shifting landscape.

The Platformization of Content. The first lesson from Verve's playbook is about the relationship between content and distribution — a relationship that has defined the economics of the media industry for a century. In nearly every era, the companies that own the distribution infrastructure capture more value than the companies that create the content flowing through it. Cable companies made more money than most cable networks. Telecom companies made more money than most of the services running on their networks. App stores capture more margin than most app developers. Spotify captures more of the music industry's economics than any individual record label.

Westermann understood this dynamic intuitively, even if he expressed it in the language of spreadsheets rather than media theory. The gaming companies he was acquiring in the 2010s were content producers trapped in a commodity market, competing for players' attention with ever-increasing marketing costs and ever-decreasing player lifetime values. The games themselves were modestly profitable, but there was no path to exceptional returns because the market for free-to-play MMOs was structurally competitive and the cost of acquiring new players was rising every year.

By building an advertising technology platform alongside the gaming portfolio, Westermann transformed the content from a standalone business into a strategic asset that fed the platform.

The games generate users. The users generate data and ad impressions. The data powers ATOM's targeting algorithms. The ad impressions flow through Verve's SSP. The targeting accuracy drives premium pricing. Every layer amplifies the value of the layers below it. The whole becomes worth far more than the sum of its parts — which is the very definition of a platform business.

The analog is not Netflix — which also owns both content and distribution but primarily uses content to attract subscribers — but rather Amazon. Amazon used its retail business to build the logistics infrastructure (warehouses, delivery network, IT systems) that eventually became a platform serving third-party sellers through Fulfillment by Amazon. The retail business was the seedbed; the platform was the crop. In the same way, Verve used its gaming business to build the adtech infrastructure that now serves thousands of third-party publishers. The games were never the destination. They were the on-ramp.

M&A as R&D. The second lesson concerns the buy-versus-build decision in fast-moving technology markets, and it challenges the Silicon Valley orthodoxy that organic innovation is always superior to acquisition.

The conventional wisdom says that great technology companies build their own products. Apple designs its own chips. Google builds its own search algorithms. The best companies innovate from within. This narrative is powerful, and it is not wrong — but it is incomplete.

In theory, building proprietary technology from scratch yields higher margins, deeper competitive moats, and stronger culture. In practice, the adtech landscape moves so quickly — with new ad formats, new privacy regulations, new platform policies from Apple and Google, new measurement standards, and new competitive dynamics emerging every quarter — that the time required to build a competitive product from zero can exceed the useful life of the technology itself. By the time you finish building version one, the market has moved on to version three.

Verve's thirty-five-plus acquisitions represent not just a growth strategy but a deliberate R&D substitution. Each deal brought not only customers and revenue but also engineers who had spent years building and refining specific technologies, patents and intellectual property that would have taken years to develop, and production-tested systems that had already survived the Darwinian process of market selection. The Smaato acquisition brought a global ad exchange that had been processing billions of bid requests daily for sixteen years. Jun Group brought a demand-side platform with two hundred and thirty Fortune 500 relationships that had been built over more than a decade. Building those capabilities organically would not merely have been expensive; it would have been competitively suicidal, because the window of opportunity would have closed long before the technology was ready.

The risk, of course, is what all serial acquirers eventually face: integration fatigue, cultural dilution, technical debt accumulated from stitching together incompatible systems, and the gradual erosion of operational focus as management attention is consumed by deal-making rather than execution.

Verve's completion of its platform unification in late 2025 — consolidating all acquired technologies onto a single stack after years of integration work — was the critical proof point that this approach can work at scale. The fourth-quarter gross margin expansion provides early financial evidence that the unified platform is delivering on its promise.

But the jury remains out on whether the next wave of integration — as the Jun Group demand-side platform, the Captify contextual intelligence technology, and the acardo retail media capabilities are fully absorbed — will proceed as smoothly. The integration muscle has been built, but it has never been tested at this level of simultaneous complexity.

Arbitraging Public Markets. The third lesson is about capital markets strategy as competitive advantage — a dimension that most technology companies neglect entirely.

The typical tech company treats its stock listing as a one-time administrative decision: pick an exchange, satisfy the listing requirements, ring the bell, move on. The choice of exchange is usually driven by prestige (New York or Nasdaq for US companies, London for European ones) or convenience (listing where the headquarters is located). Most CEOs never think about it again.

Westermann treated Verve's listing strategy as an ongoing competitive weapon. The 2018 Frankfurt listing on the Scale segment gave access to public capital and provided a currency for acquisitions. The 2020 dual listing in Stockholm gave access to a community of tech-savvy investors who could evaluate the business on the right metrics. The 2024 rebrand made the company legible to adtech-focused investors who had simply never encountered "Media and Games Invest" in their screening. The 2025 uplisting to Frankfurt's Regulated Market expanded the institutional investor universe and made Verve eligible for index inclusion.

Each move was designed to solve a specific problem: finding capital that would value the company on the right metrics rather than dismissing it as an overly complex European small-cap that defied easy categorization.

This matters because valuation is itself a competitive weapon. A company trading at higher multiples can use its stock as acquisition currency more efficiently (issuing fewer shares to acquire the same target), attract better talent with equity compensation (the same number of options is worth more at a higher share price), and access cheaper debt (lenders price leverage against enterprise value, so a higher-valued company can borrow at lower rates for the same EBITDA).

The fact that Verve currently trades at roughly four to five times EBITDA — a fraction of the fifteen to twenty-five times commanded by US-listed peers — represents either a market inefficiency waiting to be corrected or a legitimate discount reflecting real risks. Which interpretation proves correct will determine whether Verve's capital markets strategy ultimately succeeds or remains an exercise in financial engineering that never quite bridges the valuation gap.

There is a deeper lesson here about the European tech ecosystem itself. Companies like Verve, Shelly Group, and numerous Scandinavian mid-caps operate in a peculiar no-man's-land: too small and too European for the US growth investors who set multiples in technology, but too tech-forward for the European value investors who dominate their home exchanges. The result is a persistent valuation discount that some call a market failure and others call appropriate compensation for real structural risks — illiquidity, currency exposure, regulatory complexity, and the simple fact that most of the world's technology capital is denominated in dollars and deployed in California.

VIII. The Bull vs. Bear Case and Epilogue

The bull case for Verve Group rests on a straightforward proposition: the company has built, through a decade of disciplined acquisitions and organic development, a full-stack programmatic advertising platform with a unique privacy-first technology moat — and the market has not yet priced this correctly.

Start with valuation.

At roughly four to five times EBITDA, Verve trades at a steep discount to every meaningful public comparable. Magnite, PubMatic, and The Trade Desk all command double-digit EBITDA multiples. AppLovin trades at multiples that would have been unthinkable for an adtech company just three years ago. Even after adjusting for Verve's higher leverage — net debt stood at approximately 446 million euros at the end of 2025, representing about 3.1 times adjusted EBITDA — the equity appears substantially undervalued if you believe the business deserves to trade anywhere close to its peer group.

The financial trajectory supports the optimistic narrative. The company's 2026 guidance calls for revenue of 680 to 730 million euros and adjusted EBITDA of 145 to 175 million euros, implying continued strong growth and stable-to-expanding margins.

Management has earmarked an additional ten million euros for non-capex sales force investments in 2026, signaling confidence that organic growth can accelerate from the platform-migration-depressed levels of 2025. This is a company that is leaning into growth, not hunkering down — a bullish signal from a management team that has demonstrated discipline in distinguishing productive investment from wasteful spending.

The April 2025 bond refinancing was a watershed moment for the bull thesis. The new 500-million-euro senior unsecured floating rate facility, priced at EURIBOR plus four percent and maturing April 2029, replaced higher-cost legacy bonds and reduced annualized interest costs by an estimated 34.7 million euros. In a business generating 134 million euros of adjusted EBITDA, savings of nearly 35 million euros is not incremental — it is transformative. That capital flows directly to free cash flow and debt reduction, accelerating the deleveraging path toward management's stated target of two times net leverage at the midterm. If Verve can reach two-times leverage while growing EBITDA, the financial risk premium embedded in the equity valuation should compress substantially.

The technological bull case centers on ATOM and the privacy megatrend. Every regulatory signal — from ongoing GDPR enforcement in Europe, to state-level privacy legislation in the United States, to Apple's continued tightening of iOS data access — points in one direction: less tracking, more privacy, more restrictions on identifier-based advertising. Each incremental privacy restriction increases the relative value of Verve's identifier-free targeting technology. ATOM's integration across ten thousand-plus apps creates a network effect: more apps generating on-device signals means better cohort classification, which means better ad performance, which attracts more advertisers, which drives higher revenue per impression for publishers, which attracts more publishers to integrate the SDK.

Now for the other side of the ledger.

The bear case is equally straightforward and cannot be dismissed.

The most immediate risk is the balance sheet. At 3.1 times net leverage, Verve is operating with significantly less financial flexibility than its US-listed peers, most of which carry minimal debt.

Digital advertising is a cyclical industry — ad budgets are among the first line items cut during economic downturns. In an ad-spend recession, Verve's debt service obligations become a progressively larger share of shrinking cash flows, potentially forcing asset sales at distressed prices, dilutive equity raises at depressed valuations, or covenant renegotiations that restrict management's operational flexibility.

The April 2025 refinancing improved the maturity profile and reduced interest costs, but it did not reduce the absolute debt load. The delevering story is credible but unproven. And in capital markets, "credible but unproven" earns a discount, not a premium.

The second bear risk is technological platform risk. The privacy landscape that has been so favorable to Verve is defined by Apple and Google — two companies that can unilaterally change the rules of the game with a single software update. Apple's ATT framework disrupted the entire mobile advertising ecosystem in 2021, and further restrictions are always possible.

If Apple were to restrict the on-device signals that ATOM relies upon — app usage patterns, session data, behavioral indicators — the technology's effectiveness could be materially impaired. Verve has built its house on the assumption that Apple will continue to allow on-device processing as long as no personal data leaves the device, but Apple has demonstrated a willingness to restrict third-party functionality in ways that surprise the market. Building your core product on another company's platform is never entirely safe, no matter how rational the current rules may seem.

The third risk is geographic and customer concentration. Roughly seventy percent of Verve's revenue comes from North America, and the Jun Group acquisition only increased this exposure.

A US-specific advertising downturn, a shift in brand spending toward walled-garden platforms, or increased competitive intensity in the US mobile advertising market would disproportionately impact Verve's results. For a company headquartered in Europe and listed on European exchanges, this transatlantic dependency adds currency risk and regulatory complexity that pure-play US competitors do not face.

There is also a material legal overhang worth noting. A class action lawsuit in the United States alleges that Verve's PubNative SDK allowed unauthorized "backdoor access" to consumers' devices, covering California residents who used apps with the PubNative SDK without proper disclosure of Verve's data practices. While the outcome and financial impact remain uncertain, privacy-related litigation against adtech companies is a structural risk in an industry where the legal boundaries of acceptable data practices are being actively redrawn. The case bears watching.

On the accounting and disclosure front, a note of caution that applies to Verve and to serial acquirers generally: the company's reporting relies heavily on "adjusted" EBITDA, which excludes stock-based compensation, acquisition-related costs, restructuring charges, and various one-time items. Adjusted EBITDA is a useful metric for understanding the underlying operating performance of the business, but the excluded items are real costs — stock-based compensation dilutes shareholders, acquisition costs consume cash, and restructuring charges represent real operational disruption. Investors should track the conversion of adjusted EBITDA into operating cash flow and, ultimately, into actual debt reduction — because in a leveraged business, the only metric that truly matters is the cash available after debt service.

The revenue miss for fiscal year 2025 — 550.9 million euros against a guidance range of 560 to 580 million — also warrants attention. Management attributed the shortfall to the disruptive effects of the platform migration, and the fourth-quarter acceleration to 9.9 percent organic growth supports this explanation.

But a miss is a miss, and investors should watch whether 2026 guidance proves more achievable now that the migration headwinds have passed. In the serial-acquirer playbook, credibility is a currency that takes years to build and one bad quarter to destroy.

The Verve Group story, stripped to its essence, is one of the most improbable corporate transformations in European tech.

A struggling German games publisher, acquired for a pittance in 2012, systematically accumulated distressed gaming assets, used those assets to generate the cash flows and data advantages needed to pivot into advertising technology, executed over thirty-five acquisitions to build a full-stack programmatic platform, developed proprietary privacy-first targeting technology at precisely the moment the industry needed it most, and rebranded itself for a new era.

The company has roughly a thousand employees, generates over half a billion euros in annual revenue, and competes — not always on equal terms, but genuinely competes — with platforms backed by billions of dollars in market capitalization.

Whether the market ultimately rewards this transformation with a valuation that reflects the underlying business quality — or whether the European listing, leveraged balance sheet, and small-cap status continue to suppress the multiple — is the central question.

Verve Group is not a simple story. It carries real financial risk, real competitive challenges, and the inherent uncertainty of operating in an industry where two companies — Apple and Google — can rewrite the rules at any time.

But it is, without question, one of the most fascinating "phoenix" stories in adtech: a company that literally used its own ashes to fuel a rocket ship. The next chapter — whether it ends in triumph, consolidation, or something in between — will be determined by whether the privacy-first thesis proves durable, whether the balance sheet can be tamed, and whether a Dutch engineer in Düsseldorf can continue to outmaneuver competitors with ten times his resources.

The ashes, at least, have already been transformed. What remains to be seen is how high the rocket flies.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube