VEON: From Post-Soviet Pioneer to Frontier Markets Digital Operator

I. Introduction: The Audacious Pivot

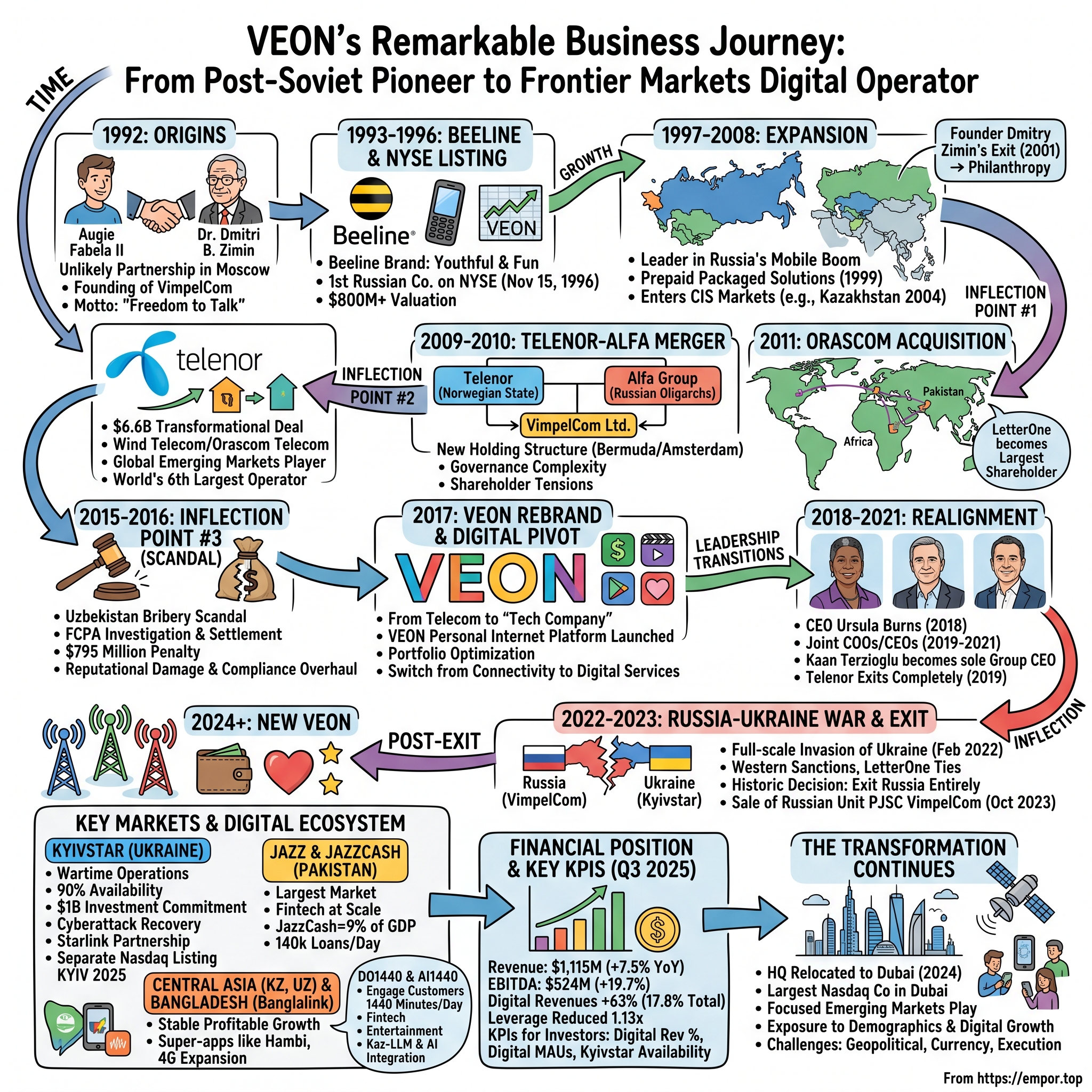

Imagine telling an investor in 1996 that the first Russian company ever listed on the New York Stock Exchange—a Moscow-based mobile carrier founded by a 25-year-old American who couldn't speak Russian and a 59-year-old Soviet rocket scientist who couldn't speak English—would, three decades later, be a Dubai-headquartered digital operator serving 160 million customers across six frontier markets, having completely exited Russia, survived an $800 million bribery settlement, weathered war in its most valuable market, and become the largest foreign investor in a country actively under military assault.

You would have been right to be skeptical. Yet here we are.

VEON is a Nasdaq-listed digital operator that provides connectivity and digital services to nearly 160 million customers. Operating across six countries that are home to more than 7% of the world's population, VEON is transforming lives through technology-driven services that empower individuals and drive economic growth.

The company operates through subsidiaries that read like a geography lesson in emerging market complexity: Kyivstar in Ukraine, Beeline in Kazakhstan and Uzbekistan, Jazz in Pakistan, and Banglalink in Bangladesh. These aren't marginal markets—they represent population centers where mobile phones are often the primary and sometimes only gateway to the digital economy.

VEON reported Q3 2025 revenue of USD 1,115 million (+7.5% YoY USD) and EBITDA of USD 524 million (+19.7% YoY USD). Digital revenues grew 63% YoY and accounted for 17.8% of total revenue, while the EBITDA margin expanded to 47.0%.

But the numbers only tell part of the story. VEON's journey encompasses virtually every challenge facing emerging market multinationals: post-Soviet chaos, oligarch politics, FCPA enforcement, geopolitical crises, and now, the crucible of operating in a war zone while trying to execute one of the telecom industry's most ambitious digital transformations.

The themes that emerge—post-Soviet capitalism, telecom as infrastructure for emerging markets, the pivot from connectivity to digital services, and navigating geopolitical complexity—offer lessons far beyond the telecommunications sector. This is a story about building businesses in places where institutions are weak, capital is scarce, and the rules can change overnight.

II. Origins: The Birth of Russian Mobile Telecom (1992–1996)

The Founders' Unlikely Partnership

In October 1991, a young American entrepreneur named Augie K. Fabela II stepped off a plane in Moscow. At 25, he traveled to the Soviet Union to explore sales opportunities for selling Plexsys mobile network systems. He did not sell a single system, but instead he identified a significant opportunity for establishing a mobile communications company.

The Soviet Union was in its final weeks. The command economy was collapsing. The ruble was worthless. Infrastructure was crumbling. And yet Fabela saw something others missed: a massive market with zero mobile phone penetration and a population desperate for communication technology that worked.

He met his future partner after he met Dr. Dmitri B. Zimin, a senior scientist at MAK Vimpel—a Soviet defense contractor. Despite numerous challenges, including that they didn't speak each other's language, they shared a vision of establishing a start-up mobile communications company in Russia.

Dr. Zimin was no ordinary scientist. Dmitry Borisovich Zimin was born in 1933 in Moscow. In 1957 Dr Zimin graduated from the Radio-Electronics Department of the Moscow Aviation Institute. Dr Zimin's first career was in the Soviet defense industry, working as an engineer on long-range missile attack detecting radars. At 59, he was contemplating a radical career change at an age when most would be planning retirement.

Inspired to do what everyone said couldn't be done; Mr. Fabela and Dr. Zimin set out to accomplish their vision of bringing basic wireless communications to Russia. A young American entrepreneur who was only 25 years old and spoke no Russian and a 63-year-old Russian scientist who spoke no English, were determined to build an independent company with an entrepreneurial and pioneering spirit—which led to the founding of VimpelCom in 1992.

The cultural chasm between them was immense. Fabela came from the entrepreneurial tradition of Silicon Valley—he had founded multiple businesses by age 25. Zimin came from the Soviet defense establishment, where scientific brilliance coexisted with bureaucratic conformity. Yet they found common ground in technical excellence and commercial ambition.

In 1992, they founded VimpelCom, now known as VEON, starting with just thirteen employees and under the motto "Freedom to Talk". Augie and Dr. Zimin, 58, combined their strengths to build a greenfield independent company characterized by an entrepreneurial and "pioneering spirit".

The Beeline Brand and Early Operations

The commercial service was launched under the Beeline brand, a brand created by Mr. Fabela in late 1993 to differentiate the company as a youthful and fun company, rather than a technical company. Very soon, the Beeline brand became the choice for admirers of state-of-the-art technology and mobile fans.

The name "Beeline" itself reflected Fabela's marketing instincts—it referenced the English idiom meaning the most direct path between two points, suggesting efficient communication while also evoking the distinctive black and yellow stripes that would become the brand's visual identity.

One year later, VimpelCom launched its first commercial network, a five base station system in Moscow, limiting sales to only 1,000 mobile phones in order to ensure quality of service.

This disciplined approach—limiting initial sales to ensure service quality—demonstrated an operating philosophy that would prove crucial. In emerging markets where infrastructure failures could destroy credibility overnight, quality mattered more than volume.

The Historic NYSE Listing

In November 1995, Augie and Dr. Zimin decided to take VEON public. The initial public offering (IPO) on the New York Stock Exchange took place on November 15, 1996, making VEON the first mobile communications firm to ever list on the NYSE. At 30, Augie became the youngest Chairman (still to date) of any NYSE-listed company.

The path to listing was not smooth. Zimin was cautious but was eventually persuaded by the enthusiastic American. Thirteen different banks initially rejected them, stating "He's too old, you're too young," but by November 1996 they had found a backer, rang the opening bell, and made history: VimpelCom became the first company from Russia to list on the New York Stock Exchange, with the IPO valuing the business at over $800 million.

What this meant for Russian capitalism cannot be overstated. VimpelCom proved that Russian companies could meet Western governance standards, attract international capital, and compete on global markets. In an era of lawless privatization and oligarch-dominated deals, VimpelCom represented an alternative path—one built on transparency, institutional investment, and operational excellence.

For investors, this origin story matters because it established the DNA that would help VEON survive challenges that would destroy less resilient companies. The combination of American entrepreneurial aggression and Russian technical sophistication, the insistence on quality, the willingness to seek international capital and governance standards—these would prove decisive in the decades ahead.

III. The Russian Growth Years & CIS Expansion (1997–2008)

Building the Russian Franchise

With NYSE capital in hand, VimpelCom moved aggressively to build out its network and capture Russia's emerging mobile market. The late 1990s and early 2000s were a gold rush in Russian telecommunications—mobile penetration was growing exponentially as prices fell and networks expanded.

In the 1990s, the Company introduced two digital cellular communications standards to Russia and built a dual band GSM-900 / 1800 cellular network.

In 1999, VimpelCom led the emergence of the mass consumer market for wireless communications in Russia by introducing a prepaid packaged product solution. Then, in 2000, the Company continued to innovate with new technologies such as WAP (wireless application protocol) and BeeOnline – a multi-access Internet portal offering its customers a wide variety of wireless information and entertainment services.

VimpelCom's expansion in Russia accelerated in 2003. In April 2003, VimpelCom launched operations in St. Petersburg and by the end of that year had 55 regional networks in commercial operation and a total customer base in Russia exceeding 10 million.

The company also pursued strategic acquisitions to build a more integrated offering, acquiring internet service providers and fixed-line assets to complement its mobile business. By the mid-2000s, VimpelCom was a full-service telecommunications provider with a strong brand and extensive infrastructure across Russia.

Expansion into CIS Markets

The strategic logic of CIS expansion was compelling: these were markets with shared history, similar regulatory frameworks, Russian-speaking populations, and low mobile penetration. For a company that had already navigated the Russian market's complexities, Central Asia and the Caucasus represented natural expansion opportunities.

In September 2004, VimpelCom began to implement its strategic plan to expand its operations into the CIS by acquiring over 50% of KaR-Tel, a mobile telecommunications services provider with a national GSM license in Kazakhstan.

In 2004, PJSC VimpelCom, in its first move outside Russia's territory, acquired Kazakhstani cellular operator KaR-Tel (brand names K-Mobile and Excess).

This expansion continued across the region, establishing the geographic footprint that would later prove crucial to the company's survival.

The Founder's Exit

In 2001, at the age of 68, Dmitry Zimin sold his controlling stake in VimpelCom and left the position of general director of the company. He was honored with the title of the Founder and Honorary President of the company.

Zimin's departure marked the end of the founding era. After his retirement and selling controlling stake in VimpelCom in 2001 Dr Zimin devoted himself to philanthropy. He transferred 90% of his wealth to an endowment. Since 2002 and for more than ten years his philanthropic activities have been focused mainly on Russia and have been facilitated through the Dynasty Foundation.

Zimin died in Switzerland on 22 December 2021, at the age of 88. His legacy endures in the company's pioneering spirit and technical excellence.

The competitive landscape in Russia was intense. VimpelCom found itself in a three-way battle with MTS and MegaFon for dominance in the world's largest country by territory. Each company represented different ownership structures and strategic priorities, creating a dynamic market that drove innovation but also margin pressure.

IV. INFLECTION POINT #1: The Telenor-Alfa Merger & VimpelCom Ltd. Formation (2009–2010)

The Complex Shareholder Dance

If VimpelCom's founding story is a tale of East-meets-West entrepreneurship, the 2009-2010 period is a story of corporate complexity that would challenge even the most sophisticated institutional investor.

The creation of VimpelCom Ltd. brought together assets from multiple companies under a new holding structure. The new entity was incorporated in Bermuda and headquartered in Amsterdam—a structure designed to optimize tax efficiency while providing a neutral governance framework acceptable to all parties.

In the years that followed, Mr. Fabela led the teams that consummated multiple ground-breaking capital markets and M&A transactions, including the US$200 million equity investments into VimpelCom by Telenor in 1998 and US$200 million equity investment by Alfa Group in 2000.

The shareholder composition reflected the deal's complexity. Telenor, the Norwegian state-controlled telecommunications company, brought international credibility and operational expertise. Alfa Group, controlled by Russian oligarch Mikhail Fridman, brought capital and political relationships essential for operating in Russia and the CIS.

The Telenor-Alfa Tensions

The marriage between a Norwegian state-owned enterprise and a Russian oligarch-controlled entity was always going to be complicated. Different corporate cultures, different strategic priorities, and different governance expectations created friction that would persist for years.

Telenor's representatives pushed for transparent governance, international accounting standards, and strategic coherence. Alfa's representatives prioritized Russian market dominance and opportunistic expansion. These tensions manifested in board disputes, litigation, and strategic paralysis at key moments.

The 2010 establishment of headquarters in Amsterdam represented a compromise—creating physical distance from both Oslo and Moscow while placing the company under Dutch corporate governance standards. The choice was pragmatic but also symbolic: VimpelCom was trying to become a genuinely international company, not merely a Russian one with foreign shareholders.

For investors trying to understand VEON today, this history matters. The shareholder conflicts that characterized the 2009-2012 period established patterns of governance complexity that would resurface repeatedly. The company learned to operate with strategic shareholders who had divergent interests—a capability that would prove valuable when navigating even more challenging circumstances later.

V. INFLECTION POINT #2: The Transformational Wind Telecom/Orascom Acquisition (2011)

The Mega-Deal That Changed Everything

In October 2010, VimpelCom announced what would become one of the most transformational—and controversial—deals in emerging market telecom history: a $6.6 billion acquisition of Wind Telecom and control of Orascom Telecom Holding from Egyptian billionaire Naguib Sawiris.

The deal closed on April 15, 2011, fundamentally reshaping the company's geographic footprint and strategic positioning. Overnight, VimpelCom transformed from a Russia-CIS focused operator into a global emerging markets player with operations spanning from Italy to Pakistan to Algeria.

Scale and Consequences

The subscriber numbers were staggering. VimpelCom's customer base effectively doubled, with operations now spanning multiple continents. The company became the world's sixth-largest mobile operator by subscribers, a remarkable achievement for what had been a Moscow startup less than two decades earlier.

Under his leadership, VEON achieved multiple groundbreaking capital markets transactions, including the acquisition of Orascom in 2012, which doubled VEON's revenue to $24 billion and increased its market capitalization to $42 billion, with 60,000 employees worldwide across 22 countries.

But scale came at a price. The acquisition was financed with substantial debt, creating leverage that would constrain strategic flexibility for years. Moreover, the newly acquired assets came with their own complexities—regulatory challenges, minority shareholder disputes, and, as would later emerge, compliance problems that would cost the company dearly.

The Italian operations (Wind) faced intense competition in a mature European market. The African assets operated in politically volatile environments. Pakistan and Bangladesh offered growth potential but required substantial investment in network infrastructure.

The emergence of LetterOne as the largest shareholder following the transaction further complicated the governance picture. This investment vehicle associated with Fridman and his partners held approximately 47.9% of shares by 2017, making it the dominant shareholder without technical control—a structure that would create ongoing governance ambiguity.

VI. INFLECTION POINT #3: The Uzbekistan Bribery Scandal & FCPA Settlement (2015–2016)

The Corruption Exposed

The Orascom acquisition brought more than just new markets—it brought an FCPA time bomb. The U.S. Justice Department's investigation into VimpelCom's operations in Uzbekistan revealed a textbook case of emerging market corruption.

In summer 2015, the United States Justice Department claimed VimpelCom had used a network of shell companies and phony consulting contracts to funnel bribes in exchange for market access in Uzbekistan. VimpelCom's affiliate Telenor severed consulting ties with Telenor's former CEO Jon Fredrik Baksaas due to the police investigation.

In November 2015, VimpelCom CEO Jo Lunder was arrested on corruption charges in Oslo, Norway. The case alleged that in exchange for an operating license, VimpelCom funneled $57.5 million to Takilant, a company linked to Gulnara Karimova, the daughter of Uzbek President Islam Karimov.

Gulnara Karimova represented a particularly egregious case of kleptocratic corruption. The daughter of Uzbekistan's authoritarian president had allegedly extracted massive payments from multiple telecom companies seeking to operate in the country. VimpelCom was neither the first nor the last to pay, but it would face the most severe consequences.

The Costly Resolution

The case was settled in February 2016, with the Securities and Exchange Commission, the U.S. Department of Justice, and Dutch regulators requiring VimpelCom to pay $795 million to resolve violations of the Foreign Corrupt Practices Act (FCPA).

The settlement was among the largest FCPA penalties in history at the time. Beyond the direct financial cost, the company suffered reputational damage that would take years to repair. Management turnover, board changes, and enhanced compliance programs followed.

For investors, the Uzbekistan scandal offered sobering lessons about emerging market risk. The same factors that create growth opportunities—weak institutions, opaque governance, concentrated political power—also create compliance minefields. The question isn't whether a company operating in frontier markets will face corruption risks, but rather how it manages those risks and responds when problems emerge.

VimpelCom's response—acknowledging wrongdoing, cooperating with authorities, paying substantial penalties, and implementing enhanced compliance programs—represented the playbook for corporate crisis management. The company survived, but the episode permanently altered its risk appetite and operational culture.

VII. INFLECTION POINT #4: The VEON Rebrand & Digital Pivot (2017)

From Telecom to Tech Company

In March 2017, VimpelCom Ltd. became VEON Ltd. The rebrand was more than cosmetic—it signaled a fundamental strategic reorientation from a traditional telecommunications company to a digital services provider.

The company explained that the rebranding was part of a shift towards marketing itself as a technology company instead of just a telecommunications firm. The VEON name itself derived from a messaging platform the company had developed, symbolizing the digital ambitions at the heart of the new strategy.

In July 2017, VEON launched its personal internet platform in Ukraine, Bangladesh, Pakistan, Italy, and Georgia—a coordinated rollout designed to demonstrate the company's capability to deliver digital services across its diverse geographic footprint.

Portfolio Optimization

The rebrand coincided with aggressive portfolio management. VEON divested marginal markets and non-core assets, concentrating resources on markets where it had leadership positions and growth potential.

The Italy operation became part of a joint venture with CK Hutchison, creating Wind Tre and allowing VEON to reduce its exposure to the challenging European market while maintaining optionality through its stake in the combined entity.

By summer 2017, VEON had around 200 million combined subscribers across 12 markets—still substantial, but more focused than the sprawling empire created by the Orascom acquisition. The company was betting that concentration would drive better returns than diversification.

The digital pivot reflected broader industry trends. Traditional voice and SMS revenues were declining globally as WhatsApp and other over-the-top applications commoditized basic communication services. Telecom operators worldwide faced existential questions about their role in a world where they risked becoming "dumb pipes" for others' content and services.

VEON's answer was to become a digital platform company—offering not just connectivity but financial services, entertainment, healthcare, and other applications that would maintain customer engagement and create new revenue streams. The strategy was ambitious, perhaps even audacious, given the execution challenges of building digital ecosystems across markets with vastly different characteristics.

VIII. Leadership Transitions & Strategic Realignment (2018–2021)

The Ursula Burns Era

Leadership instability following the FCPA settlement created uncertainty about VEON's strategic direction. In March 2018, CEO Jean-Yves Charlier resigned, and CEO duties were temporarily assumed by VEON's chair, Ursula Burns.

Burns brought impressive credentials to the role. As former CEO of Xerox, she had experience managing complex global operations and leading corporate transformations. Her appointment also brought American corporate governance discipline to a company that had struggled with governance complexity.

Burns was appointed CEO in December 2018 while remaining chair—a dual role that consolidated authority but also raised governance questions about board independence.

New Leadership & Structure

The search for permanent leadership culminated in October 2019, when VEON hired Sergi Herrero and former Turkcell CEO Kaan Terzioğlu as joint COOs. They both succeeded Burns as co-CEOs in February 2020.

In June 2020, Gennady Gazin succeeded Burns as chairman, completing the leadership transition.

Commenting on the results, VEON Group CEO Kaan Terzioglu said: "Our third-quarter performance once again demonstrates the resilience and strength of VEON's Digital Operator model."

In July 2021, Terzioğlu became sole Group CEO, ending the co-CEO structure. His background at Turkcell—another emerging market telecom operator that had navigated shareholder conflicts and market challenges—proved highly relevant for VEON's circumstances.

Telenor Exit

The Norwegian state-controlled telecom's exit from VEON marked the end of an era. In 2019, Telenor initiated its departure, selling portions of its stake in open market transactions. By March 2019, it had reduced to 8.9%, and by November 2019, it had divested completely.

Telenor's exit had multiple causes. Governance frustrations with Alfa-controlled shareholders had persisted for years. The FCPA settlement had damaged the partnership. And Telenor's strategic focus was shifting toward Southeast Asia, where it saw better growth prospects.

For VEON, the Telenor exit eliminated a source of governance conflict but also removed a shareholder with strong institutional credibility. The company's free float increased to approximately 44%, making it more of a public company but also potentially more vulnerable to hostile moves.

IX. INFLECTION POINT #5: Russia's Ukraine Invasion & The Russian Exit (2022–2023)

War and Its Consequences

Russia's full-scale invasion of Ukraine in February 2022 created an impossible situation for VEON. The company's two most valuable assets were PJSC VimpelCom in Russia (its founding business) and Kyivstar in Ukraine (its crown jewel for growth). These assets were now at war with each other.

Western sanctions on Russian entities and individuals with ties to Russia threatened VEON's access to international capital markets and banking relationships. The company's largest shareholder, LetterOne, was associated with sanctioned individuals.

Reputational damage has been done to telecommunications holding VEON in connection with the fact that its main shareholder, investment company LetterOne, which holds a 47.85% stake, is affiliated with Mikhail Fridman and Petr Aven, VEON said in an annual report. "As a result of the association of Designated Persons with our largest shareholder, we have suffered reputational harm," VEON said. Fridman and Aven, who have 37.86% and 12.13% respective stakes in LetterOne, have been placed on the sanctions lists of the European Union and the United Kingdom.

Following the imposition of sanctions on Mikhail Fridman and Petr Aven on 28 February 2022 by the Council of Europe, Mr. Fridman has resigned from his position as a member of the Board of VEON. Mr. Fridman and Mr. Aven have also resigned from their positions as members of the Boards of Directors of LetterOne Investment Holdings S.A., LetterOne Holdings S.A. and LetterOne Core Investments S.a.r.l.

Portfolio Restructuring

VEON moved quickly to clarify its position and streamline its portfolio. The company sold its Georgia unit for $45 million in June 2022, stating it was streamlining operations. In August 2022, VEON completed the sale of Djezzy to the government of Algeria for USD$682 million.

The Historic Russian Exit

The most consequential decision was exiting Russia entirely—divesting the founding business that had made VimpelCom a pioneering success story.

On November 24, 2022, VEON announced that it had entered into an agreement to sell its Russian subsidiary PJSC VimpelCom to the subsidiary's local management team. PJSC VimpelCom was valued at approximately $6.1 billion under the agreement.

The sale completed on October 9, 2023, completely severing VEON's Russian ties. The company that had started as the first Russian NYSE listing no longer had any Russian operations.

The decision was financially costly—Russia represented the single largest market in the pre-invasion portfolio. But strategically, it was arguably necessary. Maintaining Russian operations would have continued sanctions-related complications, made it nearly impossible to attract Western investment, and created ongoing reputational challenges.

With the Russian exit complete, VEON emerged as a genuinely frontier-markets-focused company: Pakistan, Ukraine, Bangladesh, Kazakhstan, Uzbekistan, and Kyrgyzstan. The geographic concentration was more coherent, even if individual markets remained challenging.

X. Kyivstar: Operating Through War & Becoming the Crown Jewel (2022–Present)

Wartime Operations

Kyivstar's performance during Ukraine's defense against Russian aggression has been remarkable by any standard. As Ukraine's market-leading operator, the company has maintained network availability of above 90% on average since February 2022, supporting the connectivity of not only its own customers but also the broader Ukrainian population.

Maintaining telecommunications in a war zone requires extraordinary operational capability. Power grid attacks, physical damage to infrastructure, and the constant threat of cyberattacks created challenges that peacetime operators never face.

In Ukraine, staying connected means staying safe. To ensure this, we have equipped our network with batteries and generators, providing up to 10 hours of continuous coverage when the grid power is not available due to extended blackouts.

The Cyberattack and Recovery

On December 12, 2023, Kyivstar experienced a massive cyberattack that disrupted its mobile and internet services nationwide. The attack also affected critical services, including air raid warning systems in Kyiv and Sumy regions.

On December 12, 2023, Kyivstar's network suffered one of the largest cyber-attacks in the history of the global telecom market, which prevented the operator's subscribers from using communication services.

Ukrainian authorities attributed the attack to Sandworm, a hacker group linked to Russia's military intelligence agency, the GRU.

The company's recovery was swift. The company's services were restored in phases, with fixed communication services partially restored at 20:00 on the 12th of December 2023, and home fixed line internet and voice communications resumed on the 13th. Two days later, mobile communications were restored in some areas, and became available across the country on the 15th of December. With the restoration of international roaming service on the 20th, the company announced that all domestic and international services were fully restored. It had been a week since the hack was discovered.

The revenue impact of these offers is currently estimated to be approximately 3.6 billion UAH (approximately 95 million USD).

Investment Commitment

VEON, Kyivstar's parent company, has invested more than USD 10 billion in Ukraine since 2013 and has committed USD 1 billion to the country's recovery and reconstruction from 2023 through 2027. VEON, through Kyivstar, was named the top international investor in Ukraine for 2022 and 2023 by Forbes Ukraine and NV Ukraine.

The Starlink Partnership

VEON Ltd. announces today that Kyivstar Group Ltd., VEON's digital operator in Ukraine, has launched Starlink's Direct to Cell satellite technology for its customers in Ukraine. Powered by Starlink's Direct to Cell constellation, the service will enable all Ukrainians to stay connected on regular 4G smartphones in remote areas where the terrestrial network is not available. Kyivstar is the first mobile operator in Europe to launch Direct to Cell satellite connectivity.

Kyivstar has signed an agreement with Starlink, a division of SpaceX, to introduce groundbreaking direct-to-cell satellite connectivity in Ukraine. Upon its launch, the service will make Ukraine one of the first countries to have the game-changing Starlink direct-to-cell service, enhancing the resilience of the country's connectivity landscape.

The Historic Nasdaq Listing

In a remarkable milestone for both Kyivstar and Ukraine, the company achieved a separate Nasdaq listing in August 2025.

Kyivstar today starts trading on Nasdaq Stock Market ("Nasdaq") under the ticker symbol "KYIV". With the commencement of today's trading, Kyivstar Group (Nasdaq: KYIV) becomes the first and only pure-play Ukrainian investment opportunity listed on U.S. stock markets.

The company said Kyivstar has already secured at least $52 million in commitments, with hopes to raise $200 million through the Nasdaq listing. The market-leading operator previously received a pro forma valuation of $2.21 billion.

Shares in Ukraine's top telecom and digital service provider Kyivstar rose by 20% since the company was listed on Nasdaq, Kyivstar President Oleksandr Komarov said in a CNBC interview.

In 2024, Kyivstar Group's revenue was $919.00 million, an increase of 0.44% compared to the previous year's $915.00 million. Earnings were $283.00 million, an increase of 0.71%.

For investors, Kyivstar represents both VEON's greatest opportunity and greatest risk. The commitment to Ukraine during wartime has built extraordinary goodwill and positioned the company for reconstruction opportunities. But ongoing conflict means continued operational challenges and unpredictable outcomes.

XI. Jazz & JazzCash: The Pakistan Digital Ecosystem Story

Market Leadership

Pakistan represents VEON's largest single market by revenue, accounting for approximately 37% of group revenue. Jazz, as the operating subsidiary is known, has built a dominant position in one of the world's largest telecom markets.

With a population exceeding 230 million and relatively low smartphone penetration, Pakistan offers substantial runway for mobile services growth. Jazz has capitalized on this opportunity through aggressive network investment and digital services expansion.

JazzCash: Fintech at Scale

The JazzCash mobile financial services platform represents perhaps the clearest success story in VEON's digital transformation strategy. In 2024, JazzCash processed transactions equivalent to 9% of Pakistan's GDP.

The value of total transactions in a year on the JazzCash platform is the equivalent to 9% of Pakistan's Gross Domestic Product (GDP), said Ali. JazzCash had 48 million registered users and 19.7 million monthly active users, as of the end of December 2024. It has 122,000 active agents across the country and a retail network of 350,000 active merchants who use JazzCash.

JazzCash processes more than 140,000 loans per day, which is "probably bigger than the entire financial services financial industry put together in Pakistan".

The number of digital wallet transactions surged 134% year-on-year to 269 million for the 12 months ended 30 June 2024, accounting for 87% of all online e-commerce payments.

The social impact extends beyond commercial metrics. Since JazzCash started offering loans, it has produced credit histories for 10 million people who otherwise would not have financial records and would remain excluded from other banking services.

Investment and Infrastructure

With a record PKR 53.9 billion investment in 2024—a 46.2% year-on-year (YoY) increase—Jazz is redefining how Pakistanis connect, transact, and engage in an increasingly digital economy.

Digital services accounted for 25% of Jazz's total revenue in Q4 2024. Underpinning digital service usage is a 4G subscriber base of more than 50 million, which is 70% of Jazz's total customers.

By 2024, we had become the largest digital loan issuer, with 80 million loans issued for productive purposes, disbursing approximately 120,000 loans daily, around 20% of which were issued to women.

The Jazz/JazzCash ecosystem demonstrates VEON's ability to execute on its digital operator strategy. By combining connectivity infrastructure with financial services, the company has created switching costs and engagement that pure connectivity players cannot match.

XII. Central Asia & Bangladesh: The Diversified Growth Portfolio

Beeline Kazakhstan and Uzbekistan

VEON's Central Asian operations under the Beeline brand represent stable, profitable businesses in markets undergoing digital transformation.

Beeline Uzbekistan is a digital operator that serves 8.2 million customers with mobile connectivity and 7.6 million total monthly active users across its digital services and applications. Its digital portfolio includes financial services application BeePul, digital-first brand OQ, the recently launched streaming application Kinom and super-app Hambi.

Beeline Kazakhstan serves 11 million customers with mobile connectivity and two million with fixed internet services. Since 2018, the company has been executing its digital operator strategy. Over the past five years, leveraging its expertise in digital solution development, Beeline has created an ecosystem of 60 internal and external products, and serves a total monthly active user base of 11.6 million with its digital products as of June 2024.

With nearly two decades of investment and innovation in Uzbekistan, VEON remains deeply committed to the country's digital future. Since entering the market in 2006, VEON has invested in the country's telecommunications and digital infrastructure, and has continued to expand beyond traditional connectivity, delivering impactful digital financial and AI-powered technologies under VEON's DO1440 and AI1440 initiatives.

The deployment in Ukraine follows VEON's group framework agreement with Starlink, facilitating potential future collaborations on bringing Direct to Cell satellite connectivity to VEON markets, that are collectively home to 528 million people. Beeline Kazakhstan, another VEON Group company, also announced the signing of a commercial agreement to launch Starlink Direct to Cell services in Kazakhstan.

Banglalink in Bangladesh

Bangladesh offers another compelling growth market, with Banglalink serves 41.3 million mobile subscribers and 20.8 million digital subscribers every month transforming lives through technology.

Banglalink's 4G subscriber base have grown from 8.0 million at the end of 2020 to 21.5 million at the end of the first quarter of 2024, while its population coverage in 4G increased from 60% to 88% in the same period. The operator is recognized for the provision of fastest 4G service in the country, winning the Ookla® Speedtest Award™ for four consecutive years.

This deal with Total Sports Management (TSM) marks the country's biggest digital content partnership in cricket segment, encompassing six ICC events in 2024 and 2025, including the ICC Men's and Women's T20 World Cup 2024 and the ICC Men's Champions Trophy 2025.

VEON and Banglalink said their capabilities in nationwide customer and merchant onboarding, risk management, interoperability, financial literacy and inclusion, cybersecurity and fraud prevention could be adapted to Bangladesh to support a shift toward a digitally driven, cash-lite economy. The companies indicated they would pursue a localisation strategy and work within Bangladesh's regulatory framework.

XIII. The Digital Operator Model: DO1440 and AI1440

Strategic Framework

VEON's DO1440 strategy—referencing the 1,440 minutes in each day—articulates the company's ambition to move beyond connectivity to become an integral part of customers' daily digital lives. The framework encompasses financial services, entertainment, healthcare, education, and enterprise solutions.

As JazzCash improves financial inclusion in Pakistan, it is also propelling Jazz's transition to a digital service provider as part of a transformation program launched by parent VEON Group four years ago, called DO1440, along with a newer AI strategy, named AI1440. The 1,440 figure is the number of minutes in a day, as the operator's aim is to be a digital operator that engages customers every minute of the day.

The financial results validate this approach. Total revenue growth of 8.3% YoY to USD 4,004 million (+14.6% YoY in underlying local currency terms) EBITDA growth of 4.9% YoY to USD 1,691 million (+12.0% YoY in underlying local currency terms) Direct digital revenue growth of 63.0% YoY.

Demonstrating the role of digital services in the Group's financial growth, direct revenues from digital accounted for 11.5% of Group's total revenues, growing at a rate of 63% year-on-year in reported currency.

As of the end of 2024, VEON served 122 million total monthly active users across its digital services portfolio. These services empowered our customers by providing access to financial services, digital information and entertainment as well as digital healthcare and learning opportunities.

AI Integration

In 2024, we also successfully deployed VEON's AI-based solutions and capabilities, including of the launching of Kaz-LLM, a large language model in Kazakhstan. Driven by our AI1440 ambition – creating solutions that augment human capabilities across our markets – VEON's digital operators also introduced other AI-powered consumer and enterprise offers that support financial and digital inclusion and data-driven business decisions.

XIV. Financial Position & Operational Metrics

Current Performance

VEON Ltd. announces selected unaudited financial and operating results for the third quarter ended September 30, 2025. VEON reported Q3 2025 revenue of USD 1,115 mn (+7.5% YoY USD) and EBITDA of USD 524 mn (+19.7% YoY USD). Digital revenues grew 63% YoY and accounted for 17.8% of total revenue, while the EBITDA margin expanded to 47.0%. The Group reduced leverage to 1.13x, maintained USD 1.7 bn in liquidity, and raised its EBITDA outlook for 2025.

Direct digital revenue growth of 63.1% YoY to USD 198 mn, representing 17.8% of Group revenue. Financial services revenues grew 32.6% to $107.5 mn.

VEON has mitigated the material uncertainty previously raised about its ability to continue as a going concern. Management now concludes that substantial doubt no longer exists.

Guidance and Outlook

For FY25, VEON is guiding for underlying local currency growth for total revenue of 12% - 14% YoY, and underlying EBITDA growth of 13% - 15% YoY. VEON's outlook for the Group's capex intensity is in the range of 17%-19% for 2025.

Capital Allocation

VEON's Board of Directors has authorized buyback programs for up to USD 100 mn of the Company's ADSs and/or outstanding bonds.

XV. Competitive Analysis & Strategic Framework

Porter's Five Forces Assessment

Threat of New Entrants: Low to Moderate Telecommunications requires substantial capital investment, spectrum licenses (often limited by government allocation), and regulatory approvals. In VEON's markets, established players have significant advantages. However, technology shifts (like satellite connectivity) could potentially enable new forms of competition.

Bargaining Power of Suppliers: Moderate Network equipment is supplied by a handful of global vendors (Ericsson, Nokia, Huawei). While operators have some negotiating leverage due to scale, the concentrated supplier base limits alternatives. Sanctions have further complicated equipment sourcing in some markets.

Bargaining Power of Buyers: Moderate to High Mobile services are increasingly commoditized, with customers willing to switch providers for better pricing. VEON's digital services strategy aims to increase switching costs through ecosystem lock-in.

Threat of Substitutes: Moderate Over-the-top services (WhatsApp, etc.) have substituted for traditional voice and SMS revenues. However, these services still require underlying connectivity, which operators provide. The key strategic question is whether operators can capture value from digital services or remain utility providers.

Industry Rivalry: High Each of VEON's markets features intense competition. In Pakistan, Jazz competes with Telenor and Zong. In Ukraine, Kyivstar faces Vodafone Ukraine and Lifecell. In Bangladesh, Banglalink competes with Grameenphone and Robi. Competitive pressure constrains pricing power but also drives innovation.

Hamilton Helmer's Seven Powers Analysis

Scale Economies: VEON benefits from scale in infrastructure investment, customer acquisition, and digital platform development. Larger subscriber bases reduce per-unit costs for network operations and enable more efficient digital service delivery.

Network Effects: JazzCash demonstrates network effects—the platform becomes more valuable as more merchants and consumers participate. Each additional user increases utility for existing users.

Switching Costs: VEON is building switching costs through digital ecosystem integration. Customers using JazzCash for financial services, Tamasha for entertainment, and Jazz for connectivity face increasing inconvenience from switching providers.

Counter-Positioning: VEON's digital operator strategy represents counter-positioning against traditional telecoms that remain focused purely on connectivity. Incumbents in digital services (banks, entertainment providers) face challenges replicating VEON's mobile-first, frontier market approach.

Cornered Resource: Spectrum licenses represent cornered resources in each market. These government-allocated frequencies cannot be replicated by competitors without regulatory approval.

Process Power: Operating in challenging frontier markets has developed distinctive organizational capabilities—managing through war in Ukraine, navigating regulatory complexity across diverse jurisdictions, and executing digital transformation in low-infrastructure environments.

Branding: The Beeline, Jazz, and Kyivstar brands carry significant equity in their respective markets, built over decades of operation.

XVI. The Bull and Bear Cases

The Bull Case

Digital Transformation Acceleration: The 63% year-over-year growth in digital revenues demonstrates that VEON's strategy is working. As smartphone penetration increases and digital services expand, this revenue stream should continue growing rapidly. Digital services typically carry higher margins than connectivity, implying EBITDA margin expansion potential.

Frontier Market Demographics: VEON's markets contain young, growing populations increasingly adopting digital services. Pakistan alone has 230 million people with relatively low but rapidly growing smartphone penetration. The total addressable market across VEON's footprint exceeds 500 million people.

Kyivstar Reconstruction Optionality: If/when the Ukraine conflict concludes, Kyivstar is positioned to benefit from massive reconstruction investment. The company's $1 billion commitment to Ukrainian infrastructure and its status as the largest foreign investor create significant goodwill and first-mover advantages.

Deleveraging Progress: The reduction in leverage to 1.13x provides financial flexibility that was absent during the 2022-2023 crisis period. Reduced debt burden enables investment in growth opportunities and potentially shareholder returns.

Starlink Partnership: The direct-to-cell partnership with SpaceX positions VEON at the frontier of telecommunications technology. Satellite integration could dramatically expand addressable markets and network resilience.

Valuation: Following the Russian exit and associated value destruction, VEON trades at levels that potentially undervalue its remaining assets, particularly given the digital services growth trajectory and Kyivstar's Nasdaq listing.

The Bear Case

Geopolitical Risk: Ukraine remains at war with Russia, with uncertain duration and outcome. A prolonged conflict could damage infrastructure, disrupt operations, and deter investment. Adverse geopolitical scenarios (Russian territorial gains, protracted stalemate) create ongoing risk to Kyivstar, VEON's most valuable asset.

Shareholder Complexity: LetterOne remains VEON's largest shareholder at approximately 48%. While sanctioned individuals have stepped down from governance roles, the association creates ongoing reputational and operational complexity. Any sanctions-related complications could disrupt banking relationships, capital market access, or business partnerships.

Currency Exposure: VEON operates in markets with volatile currencies (Pakistan rupee, Ukrainian hryvnia, Uzbek som, etc.). Currency depreciation can significantly impact reported results and dollar-denominated returns.

Regulatory Risk: Telecommunications is heavily regulated in all markets. Spectrum allocations, pricing regulations, and licensing requirements could change adversely. Pakistan has historically had unpredictable regulatory interventions.

Competition: Intense competition in all markets constrains pricing power. New entrants, particularly in digital services, could erode market share. Global technology companies increasingly compete for digital services revenue.

Execution Risk: The digital transformation strategy requires sustained execution across diverse markets with different characteristics. Building fintech, entertainment, healthcare, and enterprise platforms simultaneously is challenging.

XVII. Key Performance Indicators for Investors

Based on VEON's strategic positioning and business model, investors should focus on three primary KPIs:

1. Digital Revenue as Percentage of Total Revenue This metric captures the progress of VEON's transformation from connectivity provider to digital operator. Currently at approximately 17-18% of total revenue and growing at 63% year-over-year, the trajectory of this metric will determine whether VEON achieves the margin expansion and growth potential implicit in its strategy.

2. Monthly Active Users (MAUs) on Digital Platforms The company reported 122 million total monthly active users across its digital services portfolio at year-end 2024. Growth in MAUs indicates increasing engagement with digital services beyond basic connectivity, creating the ecosystem stickiness that differentiates digital operators from traditional telecoms.

3. Kyivstar Network Availability Given Kyivstar's importance to VEON's portfolio and the operational challenges of wartime operations, network availability serves as a proxy for operational resilience. The company has maintained above 90% average availability since February 2022—maintaining or improving this metric demonstrates continued operational capability despite external challenges.

XVIII. Risk Factors & Regulatory Considerations

Material Legal/Regulatory Overhangs

Shareholder Sanctions Complexity: While VEON itself is not sanctioned, the association with LetterOne and its indirect ties to sanctioned individuals creates ongoing complexity. Any changes to sanctions regimes or their interpretation could impact the company.

Ukraine Regulatory Environment: Ukrainian authorities had previously imposed partial corporate rights seizure on VEON shares related to Kyivstar, though these have been lifted. Ongoing regulatory scrutiny in the war environment remains a risk factor.

Pakistan Regulatory Uncertainty: Pakistan's regulatory environment for telecommunications and digital financial services has been subject to change. JazzCash operations depend on regulatory approval and banking licenses that could face future challenges.

Accounting Considerations

Currency Translation: VEON reports in USD but generates revenue in local currencies across its markets. Investors should monitor both reported currency and local currency growth figures to understand underlying business performance.

Consolidation of Kyivstar: Following the Kyivstar Nasdaq listing, VEON retains approximately 89.6% ownership. The accounting treatment of minority interests and any future ownership changes will impact consolidated results.

Going Concern Resolution: Management has concluded that substantial doubt about going concern no longer exists following the resolution of debt maturities and leverage reduction. However, the previous going concern discussion highlights the financial risks inherent in the business model.

XIX. Leadership & Governance

Current Leadership

Augie K Fabela II is the Chairman of the Board and VEON Founder. He also serves as Chair of the Remuneration and Governance Committee and a Member of the Audit and Risk Committee. He has been an independent director and a lead director of VEON Ltd. since June 2022 and he previously served as Chairman of the Board of VEON Ltd. from June 2011 to December 2012 and in 1994 to 2002.

The return of founder Augie Fabela to the chairmanship represents a full-circle moment for the company. Augie Fabela, VEON's co-founder, was appointed chair of the VEON board in May 2024.

Several other new directors were also named to the board, including Mike Pompeo, Brandon Lewis, and Duncan Perry.

The board composition reflects VEON's strategic positioning: international credibility through high-profile directors, while maintaining operational expertise through management representation.

Headquarters Relocation

We also relocated our headquarters to the Dubai International Financial Center, bringing us closer to the Group's operating markets.

These steps make VEON the largest Nasdaq-listed company headquartered in Dubai, offering a unique opportunity for global investors interested in frontier market growth opportunities.

XX. Conclusion: The Transformation Continues

VEON's journey from post-Soviet Moscow startup to frontier markets digital operator represents one of the most dramatic corporate transformations in telecommunications history. The company has navigated challenges that would have destroyed less resilient organizations: oligarch politics, FCPA enforcement, sanctions complexity, and active warfare.

The strategic repositioning—exiting Russia, doubling down on Ukraine, building digital ecosystems across Pakistan, Bangladesh, and Central Asia—creates a focused emerging markets play unlike any publicly traded alternative. Whether this positioning generates shareholder returns will depend on execution, geopolitics, and market development.

For long-term investors, VEON offers exposure to some of the world's most compelling demographic growth stories, with digital services optionality that could dramatically expand the business model's economics. For risk-averse investors, the concentrated geopolitical exposures—particularly Ukraine—represent significant uncertainty that may not be adequately compensated.

What's undeniable is that the company has survived. "From today onwards, the ticker KYIV will symbolize the opportunity to invest in Ukraine and to be part of the country's economic recovery," said Augie Fabela, Chairman and Founder of VEON.

The pioneering spirit that Dr. Zimin and Augie Fabela brought to Moscow in 1992—dreaming the impossible and building something from nothing—continues to animate the company three decades later. Whether that spirit translates into shareholder value remains the open question for the next chapter of this remarkable story.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube