Unilever: Soap, Margarine, and the Battle for the Consumer Soul

I. Introduction & Episode Roadmap

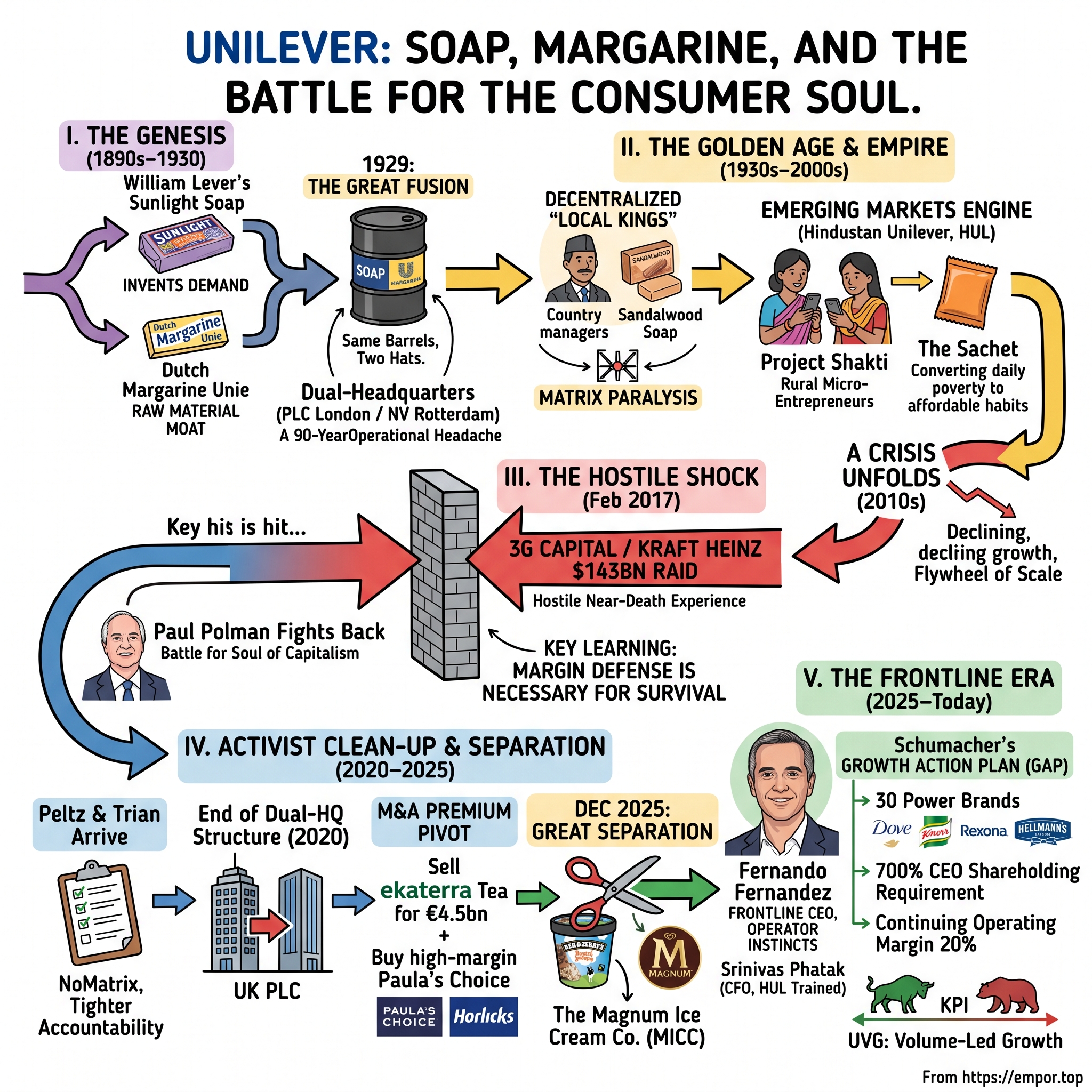

Walk into almost any home on Earth and you will find a piece of Unilever sitting on a shelf. A bar of Dove in the shower in São Paulo. A jar of Hellmann's in a fridge in Chicago. A sachet of Sunsilk hanging in a one-room shop in rural Uttar Pradesh. A tub of Comfort fabric softener in a Jakarta laundry. By the company's own reckoning, its products are used by around 3.4 billion people on any given day.1 That is not a market. That is close to half of humanity brushing up against a single company's brands before breakfast.

And yet the thing itself is almost impossible to picture. There is no single Unilever factory, no signature product, no founder-genius in a black turtleneck. What there is — and this is the paradox that animates the whole story — is a 19th-century business built on the least glamorous raw materials imaginable: animal fat, palm oil, tallow, and the alkaline chemistry of soap. In 1929, a British soap empire and a Dutch margarine cartel looked at each other, realized they were fighting over the exact same barrels of vegetable oil, and merged into one of the largest industrial combinations Europe had ever seen.2 Ninety-six years later, that fat-and-soap conglomerate is trying to reinvent itself as something lighter and faster: a "powerhouse of premium brands" throwing off cash at a 20% operating margin.3

Can it actually do that? Can a company this old, this sprawling, this exposed to commodity costs and supermarket own-label really compound like a modern consumer-tech business? That is the question a long-term investor has to answer, and it is the spine of everything that follows.

Here is the road we will travel:

- The Genesis — William Lever's Sunlight soap, the Dutch margarine union, and why fat and soap were always the same business wearing two hats.

- The Empire — post-war global expansion, the "country manager as local king" model, and the legendary emerging-markets distribution machine, best expressed in Hindustan Unilever.

- The Hostile Shock — the $143 billion near-death experience of February 2017, when Kraft Heinz and 3G Capital came for Unilever and lost, but changed it forever.

- The Activist Clean-Up — Nelson Peltz's Trian, the end of the 90-year dual-headquarters structure, and the leadership churn that carried Unilever from Alan Jope to Hein Schumacher to "frontline CEO" Fernando Fernandez.

- The Great Separation — the December 2025 demerger of the entire ice-cream business into a separately listed company, the sharpest act of self-surgery in Unilever's history.

- The Playbook & Investment Case — Helmer's 7 Powers, Porter's 5 Forces, and an honest bull-versus-bear reckoning with the "Growth Action Plan."

Before we start, one myth worth puncturing, because it colors how people misread this company. Unilever spent the 2010s branding itself as a sustainability pioneer — the "purpose-led" corporation that would save the planet while it sold you soap. Admirers treated it as an ESG poster child; critics dismissed it as a marketing-department morality play. Both miss the point. Strip away the mission statements and Unilever is, at its core, neither a virtue machine nor a food-and-cosmetics company. It is a distribution and brand-building machine — an organization whose real, durable asset is the ability to get a branded product from a factory onto nine million shelves and into three billion routines, and to keep a name alive in the customer's head against relentless cheaper competition. Everything else — the purpose, the portfolio, the CEO of the moment — is downstream of that machine. Judge the machine, and you judge the company.

Throughout, one discipline: separating what Unilever has proven from what management merely asserts. This is a company that has promised transformation many times. Let's see which promises the evidence actually supports.

II. The Origins: Sunlight Soap, Margarine Cartels, and the Raw Material Moat (1890s–1930)

In the early 1880s, soap was a commodity in the most literal sense. A grocer kept a long, greasy bar of it behind the counter, hacked off a chunk with a wire when a customer asked, weighed it, and wrapped it in whatever paper was handy. Nobody knew, or cared, who made it. It was fat and lye, sold by the pound.

William Hesketh Lever looked at that anonymous slab and saw an opportunity nobody else had. In 1884, Lever and his brother James entered the soap trade, and Lever did something almost heretical: he pre-cut the bars into neat, uniform tablets, wrapped each one in distinctive imperial-purple paper, stamped a name on it — Sunlight — and advertised it not as a chemical but as a promise.4 Cleanliness. Domestic virtue. A better life. He was, in effect, inventing the packaged consumer brand a full generation before it became the default. The soap inside was ordinary. The idea around it was not, and the idea is what people paid a premium for.

Understand the man and you understand the method. William Hesketh Lever was a grocer's son from Bolton, a Lancashire mill town, who left school at fifteen to keep the books in his father's shop. He was not a chemist and not, by temperament, an inventor of products; he was an inventor of demand. He grasped, earlier and more ruthlessly than almost anyone of his generation, that the money in soap was not in the manufacturing — anyone could boil fat and caustic soda — but in the mind of the customer. Own the name in her head, and you own the shelf. His advertising spend was, for the era, almost scandalous; he plastered "Sunlight" across Britain and pumped out promotional booklets, competitions, and coupons at a scale that made rivals dizzy. He was building, in the 1880s and 1890s, the operating manual that Unilever would still be running a century later: brand first, product second, distribution everywhere.

To industrialize that idea, Lever built something extraordinary on the marshy banks of the Mersey: Port Sunlight, a model factory village where his workers lived in tidy cottages with gardens, schools, an art gallery, and a hospital. It is easy to romanticize this as pure Victorian benevolence, and easy to be cynical and call it control — Lever set the rules of the town as tightly as he set the wages, and expected sobriety, thrift, and gratitude in return. Both readings are true. What matters for the business is that Port Sunlight functioned simultaneously as a labor moat (a contented, loyal workforce in an era of brutal industrial strife and bitter unionization battles) and as a marketing set piece: the cleanest workers in the cleanest town, making soap for a nation Lever was teaching to wash. Lever also pushed his empire outward early — into West Africa for palm oil, into the United States, into a global scramble for the fatty raw materials his factories devoured — so that by the time he died in 1925, Lever Brothers was already a multinational with an appetite for oil that would soon collide with someone else's.

Meanwhile, across the North Sea in the Dutch town of Oss, two rival families — the Jurgens and the Van den Berghs — were waging their own war, not over soap but over its culinary cousin: margarine. Margarine is butter's understudy, an emulsion of vegetable and animal fats first patented in France to feed armies and the working poor when dairy was dear. The Jurgens and Van den Berghs had been butter and margarine merchants in the same small town for generations, and their rivalry curdled into something close to a blood feud — two dynasties expanding factories, undercutting each other's prices, and racing to lock up supplies of the same imported oils. It was a mutually assured destruction of the margins both craved. Eventually they did what exhausted rivals so often do: they stopped fighting and started colluding. First came non-aggression pacts and profit-pooling arrangements; then, in 1927, the full fusion into the Margarine Unie, a cartel built to control pricing across Europe and, crucially, to control the flow of imported palm and coconut oil. What both families had learned in Oss — that scale in raw-material buying is the whole game — was precisely the lesson that would soon make a marriage with a British soap-maker irresistible.

And there is the hinge of the whole story. Soap and margarine, it turns out, are the same business. Both are manufactured by processing vast quantities of the same raw materials — palm oil, coconut oil, and animal tallow. A soap giant and a margarine giant were, without quite intending it, the two largest buyers in the world for identical barrels of fat, bidding against each other in the global oilseed markets and driving up their own costs.

On 2 September 1929, they signed the agreement that ended the absurdity, and on 1 January 1930 Unilever was formally born — a combination The Economist called one of the biggest industrial amalgamations in European history.2 The industrial logic was pure vertical arithmetic: merge the two biggest fat-buyers on the planet, and you become the undisputed king of the oilseed trade, able to command scale and squeeze suppliers that neither could touch alone.

But the merger carried a strange birth defect that would shape Unilever for the next ninety years. Neither the British nor the Dutch would surrender national control. So the founders built a two-headed creature: Unilever PLC in London and Unilever NV in Rotterdam, two legally separate parent companies, two share listings, two boardrooms, stitched together by equalization agreements so that they moved as one economic entity. It was a diplomatic masterpiece and an operational headache — a structural compromise that solved a 1929 problem and would quietly tax the company for the rest of the century. Remember that split-brain. Nearly every reformer who follows will eventually collide with it.

III. The Golden Age of Conglomeration & The Emerging Markets Pioneer (1930s–2000s)

If the great American consumer-goods champion, Procter & Gamble, was built like a fortress — centralized, uniform, everything decided in Cincinnati — Unilever grew up as something closer to a federation of city-states. And that was a deliberate response to the world it inherited.

The mid-20th century was an age of trade barriers, currency controls, and rising economic nationalism. Newly independent nations wanted local factories, local jobs, and local ownership, not imports. Unilever's answer was to go native everywhere. Instead of one global product line pushed out from headquarters, it planted semi-autonomous operating companies inside dozens of countries, each with its own factories, its own supply chain, and — the load-bearing element — its own country manager, a near-sovereign local boss who could tailor products, pricing, and marketing to the tastes and politics of his market. In India the soap smelled of sandalwood; in Europe the margarine tracked local butter culture. This was Unilever's original strategic personality: decentralized, adaptive, close to the ground.

There was a hidden cost to this model, and it is worth naming because it becomes the villain of the later chapters. A federation of local kings is superb at responsiveness and terrible at coherence. Every country reinvented the wheel; a good idea in Indonesia might take a decade to reach Brazil; procurement, IT, and manufacturing splintered into hundreds of sub-scale operations; and a thicket of committees grew up to coordinate the chaos. For most of the 20th century the trade-off was worth it — local dominance beat global efficiency in a world of tariffs and nationalism. But as trade liberalized and the internet flattened the globe in the 1990s and 2000s, the same decentralization that had been Unilever's moat curdled into what critics would later call "matrix paralysis." The company's greatest strength and its most persistent weakness were, characteristically, the same trait viewed in different weather.

That personality became a genuine competitive weapon in exactly the places global rivals found hardest to reach — none more so than India, through Hindustan Unilever Limited (HUL), the separately listed and to this day partly public Indian arm.5 HUL is not merely a subsidiary; it is one of India's most admired companies in its own right, a talent factory whose alumni run businesses across the subcontinent, and a laboratory where the hardest problems in mass-market distribution get solved first and then exported to the rest of Unilever.

The problem HUL solved is one that defeats most multinationals: how do you sell a branded product to a customer who earns a few dollars a day, lives in a village with no paved road, and shops at a stall with no shelf and no electricity? Unilever's answers became case studies taught around the world.

The first was the sachet — selling shampoo or detergent in single-use packets for a rupee or two, converting the "too poor to buy a bottle" objection into a daily-affordable habit. The second, and more ingenious, was Project Shakti, launched in 2001. Rather than fight the absence of roads and distributors, HUL recruited rural women — the Shakti ammas — trained them, and turned them into micro-entrepreneurs who sold Unilever products directly within their own villages. Over 200,000 women have since been enrolled across the country, and independent surveys commissioned by the company found their household incomes rising 30–40% in the first year.6 For Unilever, Shakti was a distribution moat disguised as a social program: it put branded goods into hamlets a truck could never economically reach, and it did so through sellers who were themselves trusted neighbors.

Then Unilever digitized the last mile. The Shikhar app shifted hundreds of thousands of small "kirana" shopkeepers onto a digital ordering system — a shopkeeper taps a phone at midnight to reorder, and the algorithm nudges what else to stock.6 Collectively, HUL's machine reaches something on the order of nine million retail outlets across India, a physical footprint a new entrant would need decades and a fortune to replicate.5 This is the closest thing in consumer goods to a genuine process power: an advantage that lives not in a patent but in an operating capability built up over generations.

While the distribution engine hummed, the portfolio kept widening. Unilever assembled a pantry and a bathroom cabinet: tea (Lipton, Brooke Bond, PG Tips), dressings and condiments (Hellmann's), soups and stocks (Knorr), and a personal-care stable that would become the crown jewels — deodorants (Rexona, and the teenage-boy juggernaut sold as Axe or Lynx) and, above all, Dove, launched in 1957 as a "beauty bar" built around a quarter-moisturizing-cream formulation, later grown into one of the most valuable personal-care brands on the planet.

Dove deserves a moment on its own, because it became the template for how Unilever wanted to think about brands in the modern era. It started as a functional pitch — a "beauty bar" that was gentler than soap because a quarter of it was moisturizing cream — but its second act, the "Real Beauty" campaign launched in the mid-2000s, turned a bar of cleanser into a cultural statement about self-image and marketed it to women who were tired of being sold impossible ideals. That is the holy grail of consumer branding: a product that competes not on price or even on performance but on meaning, which is the one axis where private label struggles to follow. Dove showed Unilever what its best brands could be, and set the standard the rest of the portfolio has spent two decades trying to reach.

All of this was fought out in what insiders half-jokingly called the "aisles of doom" — the finite shelf space of the world's supermarkets, where Unilever's armies of sales reps and its multi-billion-euro advertising budget could dictate which products a shopper even saw. For decades, scale in advertising plus scale in distribution equaled a self-reinforcing flywheel: big brands bought attention, attention drove volume, volume funded bigger brands. The economics were beautiful precisely because they were self-financing — every euro of scale bought a slightly cheaper euro of reach. But by the 2010s the flywheel was slowing. E-commerce was hollowing out the retailer's gatekeeping power; social media let tiny brands reach millions for the price of a phone; discounters like Aldi and Lidl were turning private label from an embarrassment into a badge of smart shopping; and Unilever's own organic growth had drifted down toward the low single digits. The conglomerate was bloated, its margins trailed the best-run American peers, and its share price had gone quiet. To a certain kind of investor, that combination — great brands, lazy structure, mediocre margins — does not read as a problem. It reads as an opportunity. Which is precisely the vulnerability that, in early 2017, a pair of ruthless cost-cutters decided to exploit.

IV. The Hostile Wake-Up Call: Kraft Heinz & The 3G Capital Threat (2017)

Friday, 17 February 2017. Paul Polman, Unilever's chief executive, was blindsided. On his desk sat an approach that would have created the second-largest consumer-goods company in history: Kraft Heinz, backed by the Brazilian private-equity house 3G Capital and by Warren Buffett's Berkshire Hathaway, was proposing to buy Unilever for roughly $143 billion, around $50 per share.7

To understand why this landed like a thunderclap, you have to understand what 3G was. This was the most feared operating model in consumer goods — a machine built on zero-based budgeting (every expense re-justified from zero each year, not rolled forward), aggressive leverage, and relentless headcount reduction. 3G bought sleepy, over-fed food giants, stripped them to the bone, and expanded margins toward 20%-plus, well above where Unilever's sprawling structure sat, in the mid-teens. The playbook manufactured earnings not from growth but from subtraction.

To understand Unilever's reaction you have to understand Paul Polman, because for a decade he was Unilever's public conscience. The son of a Dutch family of modest means, once destined for the priesthood, Polman spent nearly three decades at Procter & Gamble learning the trade, then a stint at Nestlé, before becoming the first outsider ever appointed to run Unilever in 2009. He arrived preaching a gospel that made him a hero to some and an irritant to others: that a corporation exists to serve society, that quarterly earnings guidance is a trap, and that sustainability is a growth strategy, not charity. On practically his first day he scrapped quarterly profit guidance altogether — an almost heretical act — and told short-term hedge funds they were not welcome as shareholders. His Sustainable Living Plan aimed to double revenue while halving environmental footprint. Critics grumbled that it was self-righteous and that the growth never quite matched the rhetoric. But it meant that when 3G came knocking, Unilever's chief executive was the single least likely person on the planet to sell his company to zero-based budgeters for a quick premium.

Polman — who had, pointedly, learned the consumer-goods trade at the very rivals now backing the raid — regarded 3G's approach as everything he opposed. He viewed cutting a company to hit a margin number, at the expense of brands, research, and employees, as value destruction dressed up as discipline. He worked the phones relentlessly that weekend, lobbying politicians in London and The Hague, framing the fight not as a boardroom disagreement but as a battle for the soul of capitalism itself — a framing so vivid that Harvard Business School would later build a case study around exactly that phrase. He rejected the bid outright. Unilever's board declared the offer "fundamentally undervalues" the company and saw "no merit, either financial or strategic."7

There is a delicious irony buried in the raider's roster. Warren Buffett, 3G's financing partner and the co-architect of the Kraft Heinz combination, was and is celebrated as the patron saint of patient, long-term, buy-and-hold investing — the very philosophy Polman claimed to embody. Yet here Buffett's capital was fueling a machine whose method was the opposite: leverage up, cut deep, extract fast. That contradiction was not lost on anyone, and it made the fight resonate far beyond one boardroom. It was, quite literally, two rival theories of what a great company is for, colliding over the largest household-goods business in Europe.

What happened next was startling in its brevity. The bid collapsed almost as fast as it appeared; by 19 February, just days after it surfaced, Kraft Heinz publicly withdrew.8 For a hostile approach to a company that size to evaporate over a weekend was extraordinary, and it owed much to political friction — a Trump-era American raider swallowing a European champion was awkward for all sides — and to the reality that a genuinely hostile takeover of Unilever, whose dual British-Dutch structure was a lawyer's nightmare, would have been a financial and regulatory epic. Buffett, characteristically, later shrugged that Kraft Heinz had misjudged how unwelcome the approach would be; 3G walked away rather than mount a protracted siege. Vindication, in the moment, for Polman. But he understood better than his cheering section that the reprieve was conditional.

But here is the part that matters for investors: winning the battle terrified Unilever more than losing it would have. The approach exposed, in public, exactly how vulnerable a slow-growing, high-overhead staple had become in a market that would happily hand it to whoever promised more cash. Polman's answer was to try to out-3G 3G without becoming it. Unilever launched Connected 4 Growth (C4G), importing zero-based budgeting into its own house, simplifying product formulations, and — the headline commitment — pledging to lift the underlying operating margin toward 20% by 2020.

The subtler cost was cultural. The gentlemanly, patient, federated Unilever of the country-kings died a little that February. Management had internalized a permanent lesson: in the public markets, even a century-old household name must defend its margin or be devoured. Whether it could defend that margin and keep growing — rather than simply cutting its way to a number, the very thing Polman condemned — became the open question. And the way Unilever spent its money over the following decade would reveal just how hard that balance is to strike.

V. M&A Capital Deployment: Flops, Divestments, and the Premiumization Pivot (2010s–2024)

Every consumer-goods giant eventually faces the same anxiety: the world is shifting from mass to niche, from the supermarket aisle to the phone screen, and the big incumbent brand suddenly looks slow. Unilever's response was a decade of buying, selling, and occasionally stumbling — a capital-allocation record that is genuinely mixed and worth reading honestly rather than through the company's own gloss.

Start with the stumble, because it is the most instructive. In 2016, Unilever paid a reported $1 billion for Dollar Shave Club, the razor-subscription upstart whose viral video had humiliated Gillette. The logic was seductive: buy a native direct-to-consumer (DTC) brand, learn its digital subscription economics, and mount a flanking attack on P&G in shaving. It did not work. DTC economics are brutal — customer-acquisition costs balloon as you scale past the early adopters, and a subscriber who signs up for a dollar is expensive to keep. P&G defended Gillette's pricing hard. Unilever never cracked the model at scale. In 2023, it offloaded Dollar Shave Club to Nexus Capital Management, retaining only a 35% minority stake, on undisclosed terms widely understood to be a fraction of what it paid.9 The lesson is uncomfortable but important: owning a disruptor is not the same as understanding one, and a legacy giant's instincts can smother the very economics it bought.

The divestment story was cleaner, if painful. Management concluded that slow-growth, capital-hungry legacy categories were dragging down both growth and valuation, and began pruning. The signature cut was tea — Lipton, PG Tips, Brooke Bond and the rest, bundled into a unit called ekaterra and sold to CVC Capital Partners for €4.5 billion, announced in late 2021 and completed in 2022.10 Tea was a business Unilever had owned for the better part of a century; letting it go was an admission that heritage is not the same as strategic fit, and that a category growing slower than the group average is a liability no matter how storied.

Then came the acquisitions that reveal where Unilever actually wants to go. In India, HUL absorbed GSK's consumer-healthcare nutrition business — the Horlicks and Boost malt-drink empire — in a roughly €3.3 billion all-equity merger completed in April 2020, cementing HUL's grip on India's enormous and profitable "health food drinks" category.11 And in the West, Unilever went hunting for structurally superior economics through a cluster of premium buyouts: Liquid I.V. (hydration) in 2020, Paula's Choice (science-led skincare) in 2021, the professional-haircare brand K18 in 2024, plus Olly and Dermalogica along the way.

The thread connecting these is margin architecture. A masstige skincare or wellness brand can run gross margins north of 70% — far above a bar of soap or a tub of margarine — and grow faster besides. This is the "premiumization pivot" in one sentence: rotate capital out of commodity categories exposed to private label and into science-backed, higher-priced brands where the consumer is buying efficacy and identity, not just cleaning power.

Step back and grade the capital allocation as a discipline, because this is where a management team's true character shows. The pattern is coherent on paper — sell slow, buy fast; sell commodity, buy premium; sell scale-for-scale's-sake, buy margin. That is the textbook prescription. But a skeptical investor should hold two facts in tension. First, the aborted £50 billion lunge at GSK's consumer-health business in early 2022 revealed a management team still tempted by transformational, empire-building M&A of exactly the kind that destroys value — investors were so alarmed they publicly revolted, and the episode arguably invited the activist through the door. Second, the Dollar Shave Club write-down is a standing reminder that Unilever pays full prices for trophy assets and does not always earn them back. The generous reading is a company learning, in real time, to be a more disciplined allocator. The wary reading is a serial acquirer whose instinct for the big, splashy deal has to be actively restrained by activists and angry shareholders. Both readings have evidence. What the next few years must show is whether the bolt-on-and-prune discipline holds when the next transformational temptation appears — because it always does. Strategically the direction is right; the self-control is the thing still on trial. And by the early 2020s, an activist had arrived to make sure management felt the pressure.

VI. Nelson Peltz, the Corporate Divorce, and the Growth Action Plan (2020–2024)

The first big structural reckoning actually predated the activist. For ninety years, the dual London-Rotterdam parentage had been treated as immovable — a founding treaty nobody dared reopen. But the Kraft Heinz scare had shown how the split structure complicated defense and confused investors, and after one aborted attempt to consolidate in the Netherlands (killed by a British shareholder revolt), Unilever finally went the other way. On 29 November 2020, the cross-border merger of Unilever NV into Unilever PLC completed, and the company became a single, UK-incorporated entity trading on one share, with one pool of liquidity, listed in London, Amsterdam and New York.12 Ninety years of dual-nationality complexity — gone. It made Unilever simpler to value, simpler to acquire, and simpler to hold to account. Which was convenient timing, because accountability was about to walk in the door.

Enter Nelson Peltz, and it is worth pausing on the man, because activists come in flavors and knowing the flavor tells you what to expect. Peltz, then in his late seventies, was octogenarian Wall Street royalty — a former frozen-foods entrepreneur turned billionaire investor who had spent decades buying into consumer giants and demanding they run tighter. His firm Trian had famously waged a bruising, narrowly lost proxy fight at Procter & Gamble in 2017, secured a board seat anyway, and — by most accounts — helped nudge P&G toward the very brand-focus-and-simplification program that turned its performance around. That P&G history is the key to reading his Unilever play. Peltz is not a corporate raider who wants to break the furniture and flip the pieces; he is an operational activist who wants a seat, a scorecard, and a management team that stops hiding behind the org chart.

He began building a Unilever position in January 2022, ultimately amassing interests equal to roughly 1.5% of the company.13 By May 2022 he had negotiated a board seat, effective that July.13 His diagnosis was almost identical to the one he had brought to Cincinnati: too many brands, too much matrix, too little accountability, and volume growth that had gone soft. At Unilever his target was the very thing that had once been a strength — the sprawling, consensus-choked lattice of country managers and category heads, which critics blamed for slow decisions and anemic volume growth under then-CEO Alan Jope. The presence of a Peltz on the board changes the physics of a management team: every strategic promise now had a famously impatient, deeply experienced skeptic sitting across the table, checking the homework.

Jope's tenure had already been bruised — most visibly by a botched, £50 billion attempt to buy GSK's consumer-health arm in early 2022 that investors savaged as value-destructive empire-building, and which helped invite Peltz in the first place. Jope announced his departure, and in July 2023 Hein Schumacher — a Dutch executive who had run the dairy group FrieslandCampina and sat on Unilever's own board — took over as chief executive.

Schumacher moved fast. In October 2023 he unveiled the Growth Action Plan (GAP), the strategic frame that still governs the company today.14 Its logic was concentration, and it had three moving parts. First, structure: dismantle the geographic matrix in favor of five accountable, end-to-end Business Groups — Beauty & Wellbeing, Personal Care, Home Care, Nutrition, and Ice Cream — each with its own P&L and its own boss to blame or reward. Second, focus: pour resources into roughly 30 "Power Brands" — Dove, Knorr, Rexona, Hellmann's, and their peers — that together drive around three-quarters of turnover, and stop spreading investment thinly across a long tail of also-rans.14 Third, cost: an €800 million productivity program underwritten by cutting about 7,500 mostly office-based roles, aimed at a leaner, less bureaucratic organization.15

Read against the file, GAP is less a revolution than a disciplined admission that the previous decade's complexity had become a tax on growth. The strategy is coherent and, importantly, measurable — which is exactly how a skeptical investor should want it, because it creates falsifiable promises. Did volume growth actually reaccelerate? Did the €800 million show up? Schumacher set the targets. Whether he would be the one to hit them was, it turned out, already in doubt — and the boldest structural move of all was still to come.

VII. The Demerger Climax: Spinning Off Ice Cream into TMICC (December 2025)

Of the five Business Groups that GAP created, one never quite belonged, and everyone inside knew it. Ice cream — Magnum, Ben & Jerry's, Cornetto, Wall's — is a wonderful set of brands attached to a fundamentally alien business model, and in early 2024 Unilever's board decided to cut it loose.

Why? Because ice cream breaks every rule that makes the rest of Unilever attractive. Consider the plumbing. A bottle of shampoo or a jar of mayonnaise is ambient — it rides on a normal truck, sits on a normal shelf, and keeps for a year. Ice cream demands an unbroken cold chain: a capital-intensive lattice of freezer warehouses, refrigerated trucks, and — most expensively — hundreds of thousands of branded freezer cabinets that Unilever places and powers in shops around the world. None of that infrastructure shares a single synergy with laundry detergent. It is a different logistics company wearing a Unilever badge.

Then there is the rhythm of the business. Ice cream is violently seasonal and weather-dependent — a cold, wet European summer can wreck a quarter — which injects exactly the kind of volatility that a company selling itself as a steady compounder does not want on its income statement. And there is the drag on the headline number: ice cream ran an operating margin around the low-teens, materially below the roughly 20% that Beauty & Wellbeing and Personal Care were throwing off.1 Bolted to the group, ice cream depressed the blended margin and muddied the growth story every single quarter.

There was also a governance headache with a name: Ben & Jerry's. When Unilever bought the Vermont ice-cream maker in 2000, it agreed to an unusual arrangement preserving an independent social-mission board — and over the years that board became a recurring public thorn, clashing with the parent over political statements, over sales in contested territories, and over who really controlled the brand's famously activist voice. Litigation and open feuding between a subsidiary's board and its corporate owner is not a good look for a company trying to project disciplined focus. The demerger did not so much resolve that tension as re-home it — sending it off with the rest of the cold-chain business to become someone else's problem to manage. For a management team obsessed with simplification, offloading a source of recurring, unpredictable headline risk was a feature, not a footnote.

So Unilever performed the largest act of self-surgery in its modern history. The ice-cream business was carved into a standalone company — The Magnum Ice Cream Company — and spun off to shareholders. The demerger completed in early December 2025, and the new company's shares began trading on 8 December 2025 under the ticker MICC, listed across Euronext Amsterdam, the London Stock Exchange, and the New York Stock Exchange — a rare triple listing mirroring its former parent.3 Existing Unilever holders received one MICC share for every five Unilever shares, and Unilever retained a roughly 19.9% stake it said it intends to sell down over time.316 (The timetable had been briefly disrupted in October 2025 by, of all things, a US government shutdown that gummed up SEC processing — a reminder that even flawless corporate engineering runs on functioning bureaucracy.)16

What remained after the knife came out is the whole point. Continuing Unilever emerged as a simpler, higher-margin, structurally faster-growing business concentrated in ambient, high-frequency categories — beauty, personal care, home care, and foods — with 2025 continuing turnover of around €50.5 billion and an underlying operating margin that reached 20.0%, alongside €5.9 billion of free cash flow, a fresh €1.5 billion buyback, and a 3% dividend increase.3 For 2026, management guided to underlying sales growth of 4–6% with at least 2% from volume.3 Those are the numbers of a business that has genuinely slimmed down.

But note the honest caveat a demerger always carries: separating a business does not create value out of thin air. It can reveal value — by letting each company be run and valued on its own terms, by focusing two management teams instead of dividing one — and it can destroy value through duplicated overhead, lost purchasing scale, and one-off transaction costs. Unilever kept a roughly 19.9% stake in the spun-off ice-cream company partly to fund exactly those costs and to keep some optionality on the upside. Whether shareholders ultimately win depends on a question the spin-off itself cannot answer: is the sum of the two focused companies worth more than the muddled whole was? Management's thesis is yes. The market will spend years marking that thesis to reality — and it will judge the person now holding the knife.

VIII. The Frontline Era: Fernando Fernandez & The New Unilever (2025–Today)

The most consequential twist in this whole saga is that the CEO who designed the demerger did not survive to execute it. On 25 February 2025, Unilever stunned the market: Hein Schumacher would step down as chief executive on 1 March 2025, barely eighteen months into the job, "by mutual agreement."17

The board's language was polite; the subtext was not. Schumacher had been the architect — he drew the blueprints, reorganized the Business Groups, launched GAP. But the board evidently concluded that the next phase required a different animal: not a strategist who redesigns the org chart, but an operator who can drive the plan through the field with speed and grip. As the chairman framed it, the market wanted execution, and it wanted it faster.

The man they reached for was Fernando Fernandez, and his résumé is the entire message. Fernandez is an Argentine-born Unilever lifer of roughly four decades who had served as CFO only since January 2024, and before that ran Beauty & Wellbeing — but the biographical detail that matters is where he was forged.17 He built his career in the hardest schools of consumer-goods execution: President of Latin America, CEO of Unilever Brazil, CEO of the Philippines — hyperinflationary, chaotic, fiercely competitive markets where you win by out-hustling on the ground, day by day, price point by price point. There is no better training for operating under pressure than running a business in an economy where the currency can lose a third of its value in a year and a competitor will steal your shelf space the moment your delivery truck is late. This is the "frontline CEO" the board wanted: someone whose instincts were shaped not in a strategy department but in a São Paulo distribution war.

His early public appearances as CEO reinforced the character. On results calls through 2025 and into 2026, Fernandez's language ran noticeably more operational and blunt than his predecessor's — talk of "unmissable brand superiority," of fixing specific underperforming markets (the United States and Indonesia were repeatedly singled out as problem children), of "10 brand-country combinations" that mattered most, and of a willingness to spend on marketing even at the expense of a softer near-term margin. Analysts who cover the stock noted the shift in register: fewer strategy abstractions, more granular accountability for named businesses. Whether that translates into sustained volume is unproven, but the communication style is itself a signal — a management that talks in specifics is easier to hold to account than one that talks in frameworks. Srinivas Phatak, the deputy CFO and group controller — himself a former CFO of Hindustan Unilever — stepped up as CFO, a promotion that once again drew Unilever's leadership gravity back toward the India-trained operating school.17

The signal was reinforced by how Unilever proposed to pay Fernandez, and here the company invited a genuine investor fight. Under a revised remuneration policy, the CEO's required personal shareholding was lifted to a striking 700% of base salary, up from 500% — a demand that the boss eat an enormous amount of his own cooking, with long-term awards tied to volume-led growth, operating margin, and cash conversion.18 In principle this is textbook alignment. In practice, the broader pay package drew a sharp shareholder backlash at the 2025 AGM, with a significant protest vote against the remuneration report, as investors worried that "aligning with global peers" was code for ratcheting American-style pay onto a European staple.19 It is a live tension, not a settled virtue: strong alignment on paper, contested legitimacy in the room.

Strategically, Fernandez has leaned into one reversal above all — the pledge to stop starving the brands. Years of margin defense, going back to the post-2017 austerity, had quietly squeezed Brand & Marketing Investment (BMI), the advertising and product spending that keeps a brand "unmissably superior" to private label. The new mandate is to route gross-margin gains back into BMI rather than banking them as profit. That is the right theory. It is also, conveniently, unfalsifiable in the short run — and it is exactly the sort of promise a disciplined investor should track quarter by quarter rather than take on faith, because it directly trades reported margin today for brand health tomorrow.

IX. The Four Core Business Segments: Economics and Moats

Strip out ice cream and modern Unilever stands on four legs, and the striking thing is how different those legs are in quality. Two are genuine premium engines; one is a fat, slow cash cow under fire; one is a commodity grind. A serious investor should never think of "Unilever margins" as a single number — the blend hides a bimodal reality. Using the 2024–2025 reporting as the baseline, here is the anatomy.120

Personal Care (roughly €13–14 billion turnover, ~20% operating margin). The engines here are Dove, Rexona, and the hygiene workhorse Lifebuoy. Personal care is a beautiful business for one structural reason: frequency. People use deodorant and soap every single day, which means constant repurchase, constant habit, and constant brand reinforcement. The strategy is to premiumize within the category — nudging a shopper from a cheap aerosol to a clinically-positioned deodorant stick at two or three times the price — and in 2024 it was deodorant innovation that led the segment's growth.1 Emotional branding plus proprietary formulation gives this segment real, if not impregnable, pricing power.

Foods / Nutrition (roughly €13 billion turnover, low-20s% margin). Knorr, Hellmann's, and Maille anchor a highly profitable but structurally slow business. The margin is excellent; the growth is pedestrian; and the strategic threat is acute and named: supermarket private label. When inflation squeezes households, a shopper who reaches for Aldi's or Walmart's own-brand stock cube instead of Knorr is voting with a very rational wallet, and in dry, undifferentiated foods the branded premium is hardest to defend. This is the segment most exposed to the bear case, and management knows it.

Beauty & Wellbeing (roughly €13 billion turnover, ~21% margin). This is the jewel and the designated growth engine. It pairs big, scaled classics (Sunsilk, Clear, Vaseline) with the acquired premium and "wellbeing" brands — Paula's Choice, Dermalogica, Liquid I.V., K18, Olly — that carry structurally superior gross margins and faster growth. In 2024, Beauty & Wellbeing grew underlying sales 6.5% with volume up 5.1%, the strongest of the group.1 The playbook is to take science-backed premium products and pour them through Unilever's incomparable global distribution — a genuinely defensible combination if the company can keep the premium brands growing after acquisition, which, per the Dollar Shave Club cautionary tale, is not automatic.

Home Care (roughly €12 billion turnover, ~14–15% margin). Omo, Persil, Sunlight, Comfort — the direct heirs of William Lever's original soap. This is the toughest segment: structurally lower-margin, acutely sensitive to commodity inputs (surfactants, soda ash, and the petrochemical building blocks of detergent), and, like foods, permanently stalked by private label. In 2024, home care's growth was volume-led as commodity deflation actually pulled prices down.1 The escape route management is betting on is innovation-led premiumization — concentrated liquids, capsule formats, "clean future" chemistry — that can command a premium and better shelf placement. It is a real lever, but home care will likely remain the margin anchor dragging on the blended average.

There is a second-order point hiding in this barbell that matters for how the whole company gets valued. A conglomerate is typically valued at a discount to the sum of its parts, because the market cannot cleanly price a business that blends a 21%-margin skincare jewel with a 14%-margin detergent grind — the good gets dragged down by association with the mediocre, and vice versa. The entire logic of GAP, and of the ice-cream demerger, is to fight that conglomerate discount: separate the businesses into legible Business Groups, spin off the ones that don't fit, concentrate on the Power Brands, and let the market see — and pay for — the quality that was previously buried in the blend. Whether investors ultimately award Unilever a re-rating toward its premium peers, or keep discounting it as a fundamentally mixed bag, is one of the most important open questions in the stock. It will be settled not by strategy but by segment-level growth: if Beauty & Wellbeing keeps compounding at mid-single digits while Home Care merely holds, the mix shifts, the blended quality rises, and the argument for a higher multiple builds itself.

The investable summary: Unilever is not one business but a barbell. Roughly half the portfolio (Beauty & Wellbeing, Personal Care) has premium economics and a credible growth story; the other half (Foods, Home Care) is defensive, commodity-exposed, and locked in permanent trench warfare with store brands. The bull case lives or dies on whether the premium half can grow fast enough to outrun the gravity of the commodity half. Which is exactly the terrain the strategic frameworks are built to war-game.

X. Strategic Playbook: Porter's 5 Forces & Hamilton Helmer's 7 Powers

Step back from the brands and ask the harder question a long-term owner must ask: what, precisely, protects Unilever's returns from being competed away? Two frameworks — Hamilton Helmer's 7 Powers and Michael Porter's 5 Forces — are useful precisely because they force you to be specific about advantages rather than romantic about heritage.

Helmer's 7 Powers. The honest read is that Unilever holds two strong powers, one medium, and largely blanks on the rest.

-

Scale Economies (High). With a marketing and advertising budget running into the many billions of euros annually, Unilever buys media, R&D, and manufacturing at a unit cost a regional competitor cannot match. Launching a new variant of an existing global brand is comparatively cheap for Unilever and ruinously expensive for a challenger who must build awareness from zero. This is real and durable.

-

Process Power (High, but concentrated in emerging markets). The single hardest advantage to replicate is the emerging-markets distribution machine — the HUL system of sachets, Shakti sellers, Shikhar digitization, and reach into millions of tiny outlets, refined over decades. You cannot buy this; you cannot copy it in a strategy offsite. It is embedded organizational capability, and it is Unilever's most genuinely defensible asset.

-

Brand (Medium to High). The Power Brands — Dove, Hellmann's — command mindshare that lets Unilever pass through price during inflation. But note the asymmetry: the Power brands have this power, and the long tail of non-power brands does not. Brand power at Unilever is real but unevenly distributed, which is precisely why GAP concentrates spending on thirty names.

-

Counter-Positioning (Low, and a historic weakness). Unilever has repeatedly been wrong-footed by DTC-native disruptors it could not counter with its own business model — Dollar Shave Club being the exhibit. Its defensive answer is now to acquire or partner early rather than to out-innovate, which is a real strategy but also an admission that this is a vulnerability, not a strength.

-

Cornered Resource / Switching Costs / Network Effects (Negligible). A shopper faces essentially zero cost to switch from Dove to a rival tomorrow. There is no lock-in. This is the uncomfortable truth beneath all consumer staples: every purchase is a fresh election, and loyalty must be re-won daily with marketing money.

Porter's 5 Forces sharpens the same picture from the outside:

-

Threat of New Entrants (Low, at scale). A digitally-native brand can be born on Instagram cheaply, but getting onto physical grocery shelves globally requires logistics, working capital, and retailer relationships that function as a formidable barrier. The threat is real at the niche level and modest at the mass level.

-

Bargaining Power of Buyers (High). The true counterparty power sits with the giant retailers — Walmart, Carrefour, Tesco, Target — who control the shelf and squeeze suppliers relentlessly. Unilever's only durable defense is what it calls "unmissable brand superiority": making its brands so wanted by shoppers that a retailer cannot afford to delist them. That is a treadmill, not a moat, and it must be funded forever.

-

Threat of Substitutes (Very High). Private label is the substitute that never sleeps, and it strengthens exactly when consumers are weakest — during recessions and inflation — and precisely in Unilever's soft underbelly, Home Care and dry Foods.

The synthesis for an investor is bracing but clarifying: Unilever's advantages are real but bounded. Scale and emerging-market distribution are genuine and hard to attack. But there are no switching costs, buyers are powerful, and substitutes are relentless. This is a company that must run to stand still — and that reality is the hinge of the bull-versus-bear debate.

XI. The Investment-Story Spine: Bull vs. Bear Case & Risk Radar

So, does Unilever win from here — and what would prove the case wrong? Strip away the corporate language and the debate comes down to a single tension: a genuinely improved, simplified portfolio versus a large slice of business permanently exposed to commodity gravity and private label.

The three KPIs that actually matter. An investor tracking this company should watch, above almost everything else:

-

Underlying Volume Growth (UVG). The most revealing number Unilever reports. Growth that comes from volume (more units sold) is healthy and durable; growth that comes only from price (UPG) is borrowed from the future, because you can raise prices past the consumer's tolerance for only so long before they defect to private label. In FY2024 the group grew underlying sales 4.2% and, encouragingly, the mix tilted toward volume; in FY2025, continuing underlying sales growth was 3.5% with volume up 1.5% — solid, but a step down that bears watching.13 The question every quarter: is the growth real (volume) or rented (price)?

-

Brand & Marketing Investment (BMI) as a percentage of turnover. The single best early-warning gauge of whether management is building brand equity or quietly harvesting it to flatter short-term profit. If margin expands while BMI as a share of sales falls, be suspicious — the profit may be borrowed from tomorrow's brand health.

-

The premium/wellbeing contribution. The share of turnover and growth coming from Beauty & Wellbeing and the high-margin prestige brands. This is the structural engine of the entire premiumization thesis; if it stalls, the thesis stalls.

The bull case. Post-demerger, Unilever is objectively a cleaner animal: higher-margin, faster-growing on paper, no longer dragging a cold-chain business through its quarterly numbers, and hitting a 20% underlying operating margin in 2025.3 It is led, for the first time in years, by a pure operator whose entire career is field execution rather than strategy decks. And it retains a compounding structural asset that few rivals can touch: outsized exposure to emerging markets — a large share of sales comes from India, Latin America, and Southeast Asia — where a rising middle class trades up into branded personal care and beauty year after year. If premiumization plus emerging-market volume compounds as management hopes, the math is attractive.

The bear case. Begin with private-label gravity: a large chunk of Home Care and dry Foods sits in commodity-like categories under permanent siege, and every recession hands share to store brands. Add the valuation and mix problem: peers like P&G have historically traded at a premium partly because their US-weighted, higher-margin portfolios are seen as safer, while Unilever's emerging-market tilt — its great growth asset — is also a source of currency volatility and geopolitical risk that can shred a reported result via FX alone. Layer on execution and restructuring fatigue: firing 7,500 white-collar employees, dismantling a decades-old matrix, integrating premium acquisitions, changing CEOs mid-transformation, and spinning off an entire division — all at once — is a staggering amount of operational and cultural disruption, any strand of which could fray. And finally, the activist stress test: a skeptical long/short investor would prod exactly where the company is softest — is the pay package (700% shareholding demands and all) truly aligned or simply richer; is BMI reinvestment real or a slogan; is 3.5% underlying growth genuinely "competitive," or is it merely respectable in a low-growth staples world dressed up as victory?

The risk radar deserves specifics rather than a generic list, because for this company only a few risks actually move the needle. Currency and emerging-market exposure is the largest: with a majority of sales outside the developed West, a strengthening euro or a wave of devaluations across India, Brazil, Indonesia, and Turkey can turn healthy local-currency growth into a shrinking reported top line — precisely what happened in 2025, when currency movements and disposals pushed continuing turnover down 3.8% even as underlying sales grew.3 That is the double edge of the emerging-market moat: the same markets that supply the growth also supply the volatility, and there is no hedging your way out of a structural euro-reporting mismatch. Input-cost inflation is the second — surfactants, palm oil, and packaging can whipsaw the commodity-heavy half of the portfolio faster than pricing can respond, compressing Home Care and Foods margins in exactly the quarters when consumers are least willing to accept price rises. Execution risk in the transformation is the third and most self-inflicted: layered restructuring, a spin-off, a management change, and an incentive overhaul all running at once is a lot of moving machinery, and disruption of that scale reliably produces at least one bad quarter of distracted execution. Notably absent from the top of the list is the technology-disruption fear that dominates other sectors — nobody is going to invent an AI that replaces deodorant — though e-commerce and the shift of discovery to social platforms do steadily erode the retail-shelf gatekeeping that once protected incumbents. The risks here are old-economy risks: weather, currency, commodities, and the store brand. That is either reassuring or dull, depending on your temperament.

A word on management credibility, judged the only way that counts — behavior over time rather than promises in a deck. The record here is genuinely mixed, and an investor should hold the whole of it. On the negative side: a decade of margin targets that were hit partly by underinvesting in brands; the GSK misadventure; a revolving door of chief executives (Polman to Jope to Schumacher to Fernandez in the space of a few years) that suggests a board still hunting for the right formula; and a pay policy that provoked an open shareholder rebellion at the very moment it was asking investors to trust the new regime. On the positive side: the company has, unusually, been willing to reverse itself publicly — admitting the portfolio was too complex, cutting loose tea and ice cream and Dollar Shave Club rather than defending sunk costs, and setting the kind of specific, measurable GAP targets that make failure visible. That willingness to name misses and act on them is worth something. The fair conclusion is that this is a management team under real external discipline — from Peltz, from a restive shareholder base, from the ghost of 2017 — rather than one that reformed itself from conviction. Which is fine, so long as the discipline holds; it is the removal of that discipline (Peltz's eventual departure, a quiet AGM, a run of easy quarters) that a careful investor should watch for as the moment complacency can creep back.

The peer comparison sharpens the stakes. Procter & Gamble is the benchmark bear-case investors reach for, and the contrast is instructive: P&G runs a more concentrated, more premium, more US-weighted portfolio at structurally higher margins, and the market rewards that consistency with a richer valuation. Nestlé, the other giant in the frame, shares Unilever's breadth and its emerging-market exposure and has struggled with many of the same growth and pricing debates. Unilever sits between them — broader and more emerging-market-tilted than P&G, more focused than the old Nestlé — and its entire strategic program can be read as an attempt to close the quality gap with Cincinnati without surrendering the emerging-market growth optionality that Cincinnati largely lacks. That is a genuinely interesting position. It is also a demanding one, because it asks the company to be excellent at two different games — premium innovation in the West and mass distribution in the developing world — at the same time.

The intellectually honest verdict is that Unilever is a better business than it was five years ago and still not a great one. The demerger and GAP have removed real drag and imposed real discipline; the frameworks confirm that scale and emerging-market distribution are durable. But the absence of switching costs, the power of retail buyers, and the eternal private-label threat mean this will never be a compounding machine that runs itself. It is a company that has to earn its growth every quarter, in every aisle, against a store brand that costs 30% less. The investment case rests entirely on execution — which is why the board bet the company on an operator, and why the next several years of volume and BMI numbers, not the press releases, will settle the argument.

XII. Epilogue & Outro

Return, at the end, to that anonymous slab of soap behind a Victorian grocer's counter. The entire arc of Unilever runs from there: William Lever's insight that a name and a wrapper could turn a commodity into a promise; a Dutch margarine cartel discovering it was fighting the same fat war from the other side; a 1929 merger that made two rivals the kings of the oilseed trade and saddled them with a split brain for ninety years. From that unlikely seed grew a company that touches nearly half the planet every day.

What makes the modern chapters compelling is that Unilever has spent the last decade doing the hardest thing an old, successful company can do: attacking its own comfortable structure before the market forced it to. The 2017 Kraft Heinz raid was the alarm bell — a warning that heritage and scale are no defense against a buyer promising more cash. The response was a slow, contested, still-unfinished reinvention: end the dual nationality, let an activist into the boardroom, concentrate on thirty brands, cut the bureaucracy, promote a frontline operator, and — the boldest stroke of all — amputate the historic ice-cream business precisely because its cold-chain roots no longer fit the future management wanted to build.

That last move is the through-line worth remembering. A hundred-year-old staple, prodded by an activist and haunted by a hostile bid it barely survived, ultimately chose to shed part of its own history to protect its ability to compound.

There is a deeper lesson here for anyone who studies great companies over long horizons. The businesses that endure are rarely the ones that never change; they are the ones that manage to change their structure faster than their soul decays. Unilever has now done this twice in living memory — reinventing itself for the post-colonial, post-tariff world of country-kings in the mid-20th century, and reinventing itself again for the post-conglomerate, activist-policed, private-label world of the 21st. Each reinvention was forced as much as chosen, provoked by an external shock rather than sprung from internal genius, and each left the company leaner and more focused than the comfortable version that preceded it. That is not the romance of the visionary founder. It is something less glamorous and, for a long-term investor, arguably more valuable: an institution with a demonstrated capacity to be dragged, reluctantly and repeatedly, into doing the right thing.

Whether that capacity delivers this time — whether the purified, premium, emerging-markets Unilever actually outgrows the private-label gravity pulling on half its portfolio — is the question the next several years will answer, and the scorecard is refreshingly concrete. Watch the split between volume and price in the underlying growth number. Watch whether brand-and-marketing investment actually rises as a share of sales, or quietly gets harvested for margin the moment a quarter looks soft. Watch whether Beauty & Wellbeing keeps compounding fast enough to shift the whole company's center of gravity toward quality. And watch what happens to the discipline when the external pressure eases. The strategy is coherent, the incentives are sharpened, and the operator is in the chair. What remains unproven is the only thing that ever mattered in this business: execution, in every aisle, one purchase at a time.

References

-

Improved performance – volume growth, gross margin expansion (FY2024 results) — Unilever, 2025-02-13 ↩↩↩↩↩↩↩

-

2025 Full Year Results — Unilever / Investegate RNS, 2026-02-12 ↩↩↩↩↩↩↩↩

-

Hindustan Unilever Limited Investor Relations — HUL India ↩↩

-

How AI and digital tools are empowering women micro-entrepreneurs (Project Shakti / Shikhar) — Unilever, 2025 ↩↩

-

Unilever Has Rejected a $143 Billion Merger Bid From Kraft Heinz — Fortune, 2017-02-17 ↩↩

-

Kraft Heinz Withdraws Its $143 Billion Bid For Unilever — Forbes, 2017-02-19 ↩

-

Unilever announces the sale of Dollar Shave Club — Unilever, 2023 ↩

-

Unilever to sell its Tea business, ekaterra, to CVC Capital Partners for €4.5bn — CVC, 2021-11-18 ↩

-

GSK completes divestment of Horlicks and other Consumer Healthcare nutrition products in India — GSK, 2020-04-01 ↩

-

Completion of Unilever's Unification — Unilever, 2020-11-29 ↩

-

Unilever names activist investor Nelson Peltz to board — CNBC, 2022-05-31 ↩↩

-

Solid Q3 results and action plan to drive growth and unlock potential (Growth Action Plan) — Unilever, 2023-10 ↩↩

-

Unilever completes Magnum ice cream spin-off as shares begin trading — FoodIngredientsFirst, 2025-12 ↩↩

-

Unilever hit by investor backlash over CEO pay — Grocery Gazette, 2025-04-10 ↩

-

A look at Unilever's full-year results by business group — Unilever, 2025 ↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube