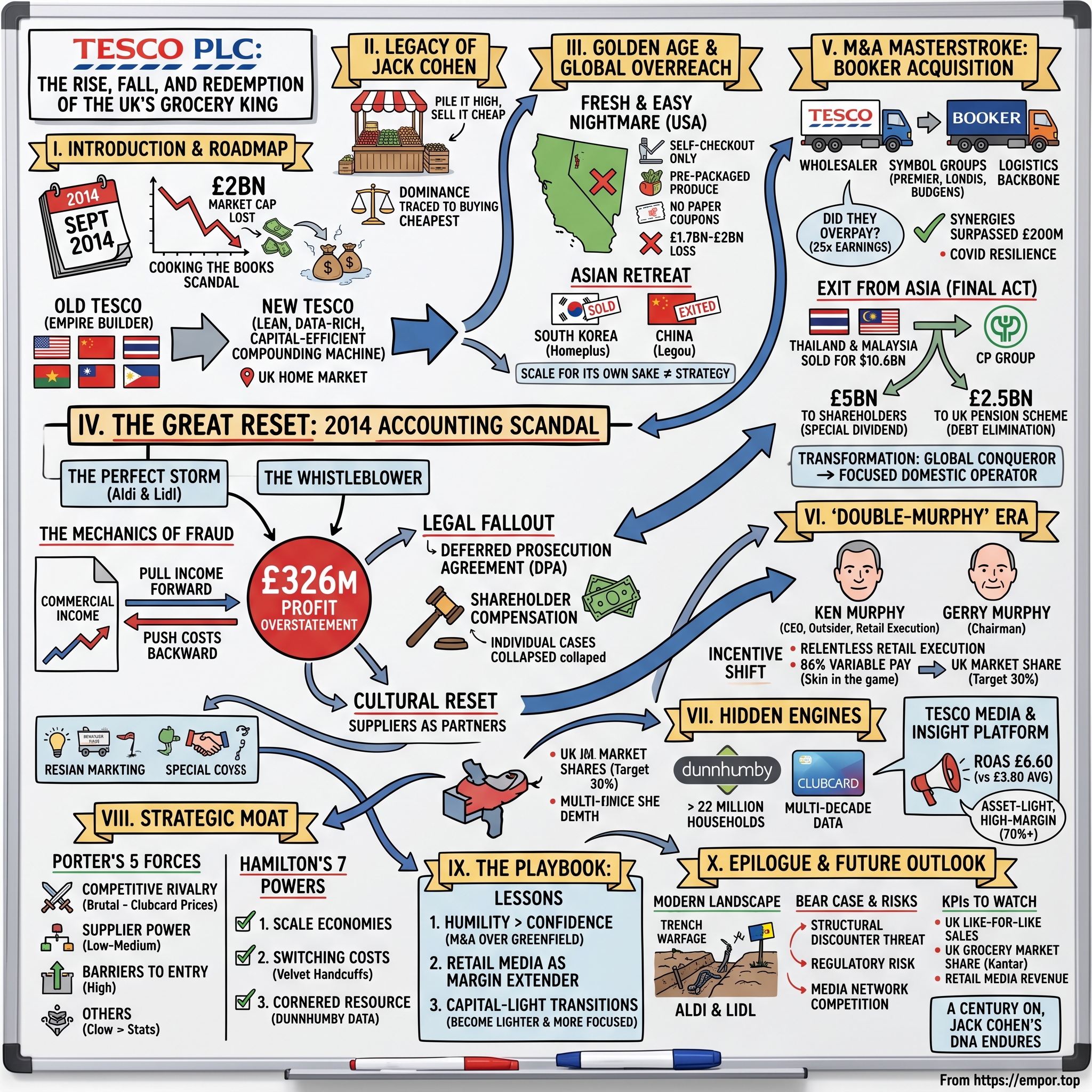

Tesco PLC: The Rise, Fall, and Redemption of the UK's Grocery King

I. Introduction & Episode Roadmap

Picture a single trading day in September 2014. The opening bell rings on the London Stock Exchange, and within minutes, one of the most trusted blue-chip names in Britain — a company that fed roughly one in every three baskets of groceries bought in the United Kingdom — begins to hemorrhage value. By the close, two billion pounds of market capitalization had simply evaporated.1 Not because of a recession, not because of a natural disaster, but because of a number. A made-up number. Tesco, the company that had taught Britain how to shop, had been caught cooking its own books.

How does a retail powerhouse — the unchallenged king of the British high street, the third-largest retailer on the planet at its peak — nearly collapse under the weight of a £326 million accounting scandal, only to reinvent itself a decade later as a lean, data-rich, capital-efficient compounding machine?6 That is the story we are going to tell. And it is one of the great corporate redemption arcs of modern business history.

This is Tesco PLC, trading on the London Stock Exchange under the ticker TSCO.L, with its corporate home at tescoplc.com. But the Tesco of 2026 is a fundamentally different animal from the Tesco of 2008. The earlier Tesco was an empire-builder, planting flags across the United States, China, Thailand, South Korea, and Central Europe in a quixotic bid to become the Walmart of the world. The Tesco of today has retreated home, sold off its overseas adventures, shed its banking balance sheet, and refocused with almost monastic discipline on a single market it utterly dominates.

What makes this transformation so fascinating is that it represents a complete inversion of corporate strategy. The 2000s Tesco was about more — more countries, more formats, more financial services, more ambition. The 2020s Tesco is about better — better margins, better data, better capital returns, better execution within a tightly defined arena. It is the difference between a conquistador and a craftsman.

Over the next several hours, we will unpack the full arc. We will dig into the Fresh & Easy disaster in America — perhaps the most expensive cultural misunderstanding in retail history. We will meet the whistleblower whose conscience cracked open the accounting fraud. We will analyze the Booker acquisition, an M&A move that the market initially hated and that turned out to be a masterstroke. We will explore the hidden genius of dunnhumby and the Clubcard — the best acquisition you have probably never heard of. And we will examine the "Double-Murphy" era of current management, two unrelated Irishmen named Murphy who together steer the modern ship.

Let's begin, as all great corporate sagas do, with a man and a market stall.

II. The Legacy of Jack Cohen: "Pile It High and Sell It Cheap"

The year was 1919, and the place was the chaotic, shouting, elbow-to-elbow sprawl of an East End London street market. A 21-year-old demobbed RAF veteran named Jack Cohen, the son of Jewish immigrants from Poland, stood behind a tiny market stall with his army gratuity of about £30 burning a hole in his pocket. He had bought up a job lot of surplus groceries — tins of food, including, as legend has it, a batch of salmon — and he was selling them faster than the established merchants around him by doing one simple, radical thing: charging less.

That first day, the story goes, Cohen turned a profit of a few pounds on sales of a few more. It was not glamorous. It was not sophisticated. But it contained, in embryonic form, the entire DNA of what would become Tesco. Cohen understood something visceral about the working-class shopper: price was king. You did not need to dazzle people with presentation or selection. You needed to give them what they wanted at a price their neighbor could not beat, and you needed to do it at enormous volume.

The brand name itself was born of this scrappy resourcefulness. In 1924, Cohen bought a shipment of tea from a supplier named T.E. Stockwell. He combined those initials with the first two letters of his own surname — COhen — and "TESCO" was christened. The first actual Tesco store opened its doors in 1931 in Burnt Oak, north London. But the spirit predated the bricks.

Cohen's defining philosophy was distilled into a phrase that became both a company motto and, eventually, a cautionary tale: "Pile it high and sell it cheap." It was the doctrine of the discount merchant taken to its logical extreme. Stack the goods to the ceiling, accept wafer-thin margins on each item, and make your fortune on turnover. Cohen was a ruthless, charismatic, occasionally chaotic operator — a man who reportedly kept the company's deals in his head and on the backs of envelopes, who haggled suppliers into submission, and whose buying power grew with every new store.

And here is why a 1919 market stall matters to an investor in 2026. The core competitive weapon Cohen forged — the ability to buy goods cheaper than anyone else by virtue of sheer scale, and to pass just enough of that saving on to the customer to win the sale — is precisely the weapon Tesco wields today. The company commanded roughly 27.8% of the UK grocery market in 2026, more than its next two supermarket rivals combined.[^2] That dominance traces a direct genetic line back to Cohen's instinct that whoever buys cheapest wins.

But here is the twist, and the setup for everything that follows. Somewhere in the boom years of the 2000s, Tesco's leadership began to forget Cohen's lesson. Flush with success, intoxicated by global ambition and premium "Finest" ranges, the company drifted upmarket and outward, away from the cheap-discount discipline that built it. It stopped being the leanest operator and started being the most ambitious one. That drift created an opening — an opening that two German discounters would drive a truck through. And it set the stage for the crises that nearly destroyed the company.

To understand the fall, we first have to understand the hubris. Let's travel to the golden age.

III. The Golden Age & Global Overreach

By the dawn of the new millennium, Tesco was on top of the world, and it knew it. Under chief executive Terry Leahy — knighted, lionized, the most celebrated retailer in Britain — Tesco had pulled decisively ahead of arch-rival Sainsbury's to become the UK's number one grocer. The Clubcard loyalty scheme was minting proprietary data. Profits marched relentlessly upward. At its zenith, the boast in the City was that £1 in every £8 spent in British retail went through a Tesco till.

Success on this scale breeds a particular kind of corporate intoxication: the belief that the formula which conquered home can conquer anywhere. Leahy's Tesco set out to build a global empire that could one day rival the great American behemoth, Walmart. The company pushed into Eastern Europe, into Asia, and — most fatefully — set its sights on the largest consumer market on Earth, the United States.

The Fresh & Easy Nightmare

In 2007, Tesco did something almost no foreign retailer had ever succeeded at: it attempted a greenfield entry into the American grocery market. Rather than buying an existing US chain and learning the ropes, Tesco would build its own brand from scratch — a chain of small-format neighborhood stores called Fresh & Easy Neighborhood Market, concentrated in California, Arizona, and Nevada. The company reportedly spent months sending executives to live undercover near American households, studying how they shopped and what was in their fridges. The confidence was total.

The confidence was also catastrophically misplaced. Fresh & Easy became a near-textbook case study in cultural tone-deafness. Tesco built the stores around self-checkout only — no traditional staffed tills — at a time when American shoppers, unlike the British, found the experience cold and alienating. The fresh produce was largely pre-packaged in plastic wrap, which Tesco saw as efficient and hygienic but which American consumers read as a signal of staleness; they wanted to squeeze the avocados and pick their own apples. And in a masterstroke of misreading the market, Tesco initially resisted the great American institution of the paper coupon — the very lifeblood of US grocery promotion.

The stores were clean, the concept was rational, and almost nobody came. Fresh & Easy bled cash year after year. The 2008 financial crisis, which hammered precisely the cash-strapped Sunbelt suburbs where Tesco had planted its flags, turned a difficult launch into a death spiral.

By April 2013, Tesco had seen enough. The company announced its exit from the United States, taking a writedown of approximately £1.2 billion (around $1.8 billion at the time) on the failed venture.2 But the true cost ran higher. To extract itself from the leases and obligations, Tesco effectively paid the investment firm Yucaipa Companies, controlled by billionaire Ron Burkle, to take most of the business off its hands. When all the exit costs were tallied, the total "misadventure" — as the press dubbed it — landed somewhere between £1.7 billion and £2 billion.2 Six years, billions of pounds, and a humbling lesson: you cannot export a culture. You have to understand the one you are entering.

The Asian Retreat

America was the most spectacular failure, but it was not the only retreat. Tesco's Asian empire, built with similar ambition, would also be dismantled — though here the story is more nuanced, a mix of genuine success, hard slog, and ultimately a strategic decision that the capital was better deployed at home.

In South Korea, Tesco had built one of its most successful international operations through the 홈플러스 Homeplus hypermarket chain, a business many considered the jewel of its overseas portfolio. But by 2015, a debt-laden Tesco — reeling from the accounting scandal we are about to discuss — needed cash badly. It sold Homeplus to the private equity firm MBK Partners for roughly £4.2 billion, the largest private equity deal in Asia at the time, using the proceeds to pay down a mountain of domestic debt.

In China, the story was tougher from the start. Tesco entered under the brand 乐购 Legou — a clever piece of localization, since the characters roughly evoke "happy shopping." But it struggled to gain real traction against entrenched local hypermarket operators who understood Chinese consumers and supply chains far better. Rather than keep burning capital, Tesco folded its China operations into a joint venture with 华润创业 China Resources Enterprise, specifically the state-backed 华润万家 CR Vanguard retail network, taking a minority stake. By 2020, Tesco had exited China entirely, selling its remaining 20% interest. The grand Asian adventure was over — though, as we will see, its final chapter in Thailand would prove enormously lucrative.

The common thread across America and Asia is a single strategic truth that would come to define the modern Tesco: scale for its own sake is not a strategy. Empire-building consumed capital, management attention, and balance-sheet capacity that the company would soon desperately need at home. Because while Tesco's executives were studying American refrigerators and negotiating Chinese joint ventures, a rot was setting in at the very center of the business — in the finance department, in the numbers themselves.

IV. The Great Reset: The 2014 Accounting Scandal

Every great fraud begins not with villainy but with pressure. And by the early 2010s, the pressure on Tesco's core UK business was becoming unbearable.

The Perfect Storm

Two German names had arrived on British shores and were quietly dismantling Tesco's value proposition: Aldi and Lidl, the hard-discounters. These were ruthless, limited-range, no-frills operators who had taken Jack Cohen's "pile it high, sell it cheap" gospel and out-Tesco'd Tesco at its own founding game. As they expanded store by store across Britain, they peeled away exactly the price-conscious shoppers Tesco had drifted away from during its upmarket, globe-trotting boom years.

Tesco's UK sales and margins came under withering attack. And here is where corporate culture turns toxic. The legacy leadership, accustomed to decades of unbroken profit growth, had set internal margin and profit targets that the deteriorating reality of the business simply could not support. Rather than accept the painful truth and reset expectations, the commercial team began running the business "too hot" — straining to conjure profits that the underlying operations were no longer generating. When the real numbers will not meet the target, something has to give. Either the target, or the integrity of the numbers.

The Whistleblower

The crack appeared from inside the finance team. A senior accountant named Amit Soni — newly arrived and looking at the books with fresh eyes — grew alarmed at what he saw in the way Tesco was recognizing what is called "commercial income." He flagged what he and colleagues came to call the "Legacy Paper" to the company's legal team in the summer of 2014. It was an act of professional conscience that would detonate the entire edifice. The legal team escalated. New chief executive Dave Lewis — who had been in the job for barely three weeks — was informed. And Tesco was forced to confront the fact that its profits were, in significant part, a fiction.

The Mechanics of the Fraud

So what exactly was the "commercial income" trick? Let's break it down in plain terms, because it is the crux of the whole affair, and it is more mundane and more insidious than outright embezzlement.

In the grocery business, supermarkets do not simply buy products from suppliers and sell them. They also collect enormous sums from suppliers in the form of rebates, discounts, and payments — money paid by a brand like a soup maker or a soft-drinks company in exchange for prominent shelf positioning, promotional support, and hitting volume targets. This is "commercial income," and for a giant like Tesco it ran into billions of pounds annually. Crucially, the timing of when you recognize this income involves judgment. And judgment is where fraud lives.

Tesco's manipulation worked on both ends of the ledger simultaneously. On one side, it pulled forward — booking commercial income into the current quarter before it had actually been earned, recognizing rebates and supplier payments prematurely to flatter the present-period profit. On the other side, it pushed back — delaying the recognition of costs, particularly the costs of running promotions, into future periods. Pull income forward, push costs backward, and presto: the current quarter looks far healthier than the business actually is. It is the accounting equivalent of borrowing from next month's paycheck to make this month look prosperous — and then doing it again, and again, each period digging the hole deeper.

The September 2014 Bombshell

On September 22, 2014, Tesco dropped the bomb. It announced that it had overstated its profits — initially estimated at around £250 million for the half-year guidance.1 The market's reaction was instant and brutal. Tesco shares cratered, wiping roughly £2 billion off the company's market capitalization in a single day.1 An independent investigation by Deloitte and the law firm Freshfields followed, and as accountants pored over multiple years of accounts, the figure swelled. The final tally of the profit overstatement reached £326 million, spread across the relevant periods.6

For a company whose entire brand rested on being the trustworthy, everyday choice of Middle Britain, the reputational damage was incalculable. This was not a complex derivatives blow-up at an investment bank. This was the supermarket where your gran bought her tea, caught fiddling the figures.

The Legal Fallout

The legal reckoning stretched on for years. In 2017, Tesco reached a landmark settlement with the UK's Serious Fraud Office: a Deferred Prosecution Agreement (DPA), one of the first major uses of this tool in British corporate law.3 Under the DPA, Tesco agreed to pay a financial penalty of £129 million.3 Separately, to compensate investors who had bought shares at fraudulently inflated prices, Tesco agreed through a settlement overseen by the Financial Conduct Authority to pay around £85 million in shareholder compensation for market abuse.3

But here is the twist that says so much about how corporate accountability actually works. The criminal cases brought against the individual executives — the three senior managers dubbed by the press the "Tesco Three" — collapsed entirely. The charges were ultimately dismissed or resulted in acquittals, with judges finding the evidence insufficient to put to a jury. The corporate entity paid the fines and wore the scar, while the individuals walked free. It is a recurring pattern in white-collar enforcement: the institution is punishable, the people inside it frequently are not.

The Squeeze and the Cultural Reset

The deepest consequence of the scandal was not financial but cultural — and ultimately, paradoxically, restorative. The fraud had grown directly out of an abusive relationship with suppliers, in which Tesco's commercial teams squeezed brands for ever-larger payments and then played accounting games with the timing. In the aftermath, under Dave Lewis, Tesco was forced into a radical reset of how it dealt with the thousands of suppliers it depended on. Aggressive squeezing gave way to transparency, simpler terms, and a rebuilt relationship of trust.

That reset, painful as it was, laid the groundwork for the operational recovery that followed. A company that treats its suppliers as adversaries to be gamed cannot build a resilient supply chain. A company that treats them as partners can. The scandal, in other words, forced Tesco to relearn a discipline it had lost. And from that chastened, transparent, back-to-basics foundation, the new leadership could finally go back on the offensive — not through reckless overseas empire-building, but through a single, bold, controversial acquisition at home.

V. M&A Masterstroke: The Booker Acquisition

By early 2017, Dave Lewis had steadied the ship. The accounting wound was healing, the UK turnaround was taking hold, and Tesco was ready to do something no one expected from a company so recently on its knees: go on the attack. And the target raised eyebrows across the City.

The Pivot

On January 27, 2017, Tesco announced it would acquire Booker Group, the United Kingdom's largest food wholesaler, in a cash-and-shares deal valued at approximately £3.7 billion.4 This was not a defensive crouch. This was Tesco using M&A to extend its dominance into an entirely adjacent part of the food chain — the business of supplying other businesses.

Booker was a fascinating creature. At its core, it was a cash-and-carry wholesaler — the company that supplied independent corner shops, restaurants, pubs, caterers, and small businesses with everything from baked beans to cooking oil. But it was much more than a warehouse operation. Booker owned and franchised a portfolio of "symbol group" convenience brands — names like Premier, Londis, and Budgens — under which thousands of independently owned corner shops traded. And it ran the logistics backbone supplying a vast slice of Britain's "out-of-home" eating market — the restaurants, takeaways, and caterers that make up the roughly £85 billion catering sector.

The man behind Booker was Charles Wilson, a widely respected retail operator who, in a neat twist, would join Tesco's board through the deal and bring exactly the kind of operational rigor the company needed. The strategic logic Lewis laid out was that Tesco and Booker together would create the UK's leading "food business" — spanning both the retail customer who shops for the home and the business customer who buys to feed others.

Did They Overpay?

Here is where it got contentious, and where the investor lens gets interesting. On the raw financials, Tesco was paying a rich price. The deal valued Booker at roughly 25 times forward earnings and an enterprise value of around 20 times EBITDA — multiples you would expect for a fast-growing technology company, not a low-margin grocery wholesaler.

For comparison, standard wholesale and distribution peers typically traded at something like 12 to 15 times earnings. By that yardstick, Tesco appeared to be paying nearly double the going rate for a business operating on margins of just a few percent. The reaction from a chunk of Tesco's own shareholder base was open revolt. Major institutional investors — including Schroders and Artisan Partners, two of Tesco's largest shareholders — publicly attacked the deal, arguing that Tesco was wildly overpaying for a low-margin business and should instead be returning cash to long-suffering shareholders or fixing its core operations.

It was a genuine governance confrontation, the kind that occasionally erupts when management's ambition collides with investors' skepticism. The bears had a real point: pay 25 times earnings for a thin-margin wholesaler, and you had better be very sure about the synergies.

The Counter-Argument

Management's defense rested on the idea that the headline multiple obscured the strategic value. Booker was not just a box-shifter. First, it gave Tesco a commanding position in the out-of-home food market — the structurally growing slice of consumer spending as Britons increasingly ate at restaurants, ordered takeaways, and grabbed food on the go, rather than cooking every meal at home. Tesco's core supermarket business was almost entirely exposed to the in-home meal; Booker was a hedge into the out-of-home one.

Second, the combined buying power was formidable. Merge the procurement of the UK's largest grocer with the UK's largest food wholesaler, and you create purchasing scale that no domestic competitor could match — Jack Cohen's original weapon, sharpened to a razor's edge. Third, Booker's B2B operations carried structurally different and in places higher margins than commodity grocery retail, and its customer base of independent shops and caterers diversified Tesco's revenue away from pure supermarket footfall.

The deal cleared the UK's Competition and Markets Authority in December 2017 — notably without forced store disposals, as the regulator concluded the two businesses largely served different customers — and completed in March 2018.5

The Verdict

So who was right — the ambitious management or the revolting shareholders? With the benefit of hindsight, this one goes decisively to management. Tesco had set a target of £200 million in annual cost synergies from the merger, and it comfortably surpassed that target by the third year, wringing out procurement savings, distribution efficiencies, and shared infrastructure faster than promised.

But the real vindication came from an event no one in the room in 2017 could have predicted: COVID-19. When the pandemic struck in 2020 and Britain went into lockdown, the value of owning both halves of the food chain became vivid. As supermarket demand surged and the catering market temporarily collapsed, then violently reversed as restaurants reopened, Tesco's combined retail-and-wholesale machine proved far more resilient and adaptable than a pure-play supermarket would have been. Booker's diversification was exactly the kind of hedge that only looks obvious in retrospect. The "overpriced" deal had become a cornerstone of the modern Tesco.

The Exit from Asia

Even as Tesco was integrating Booker at home, it was executing the final, lucrative act of its overseas retreat. In March 2020, Tesco agreed to sell its operations in Thailand and Malaysia — anchored by the highly successful เทสโก้ โลตัส Tesco Lotus hypermarket chain — to a Thai consortium for an enterprise value of $10.6 billion (around £8.2 billion).7

The buyer was the conglomerate เครือเจริญโภคภัณฑ์ CP Group, controlled by Thailand's richest man, ธนินท์ เจียรวนนท์ Dhanin Chearavanont, acting through its listed arms including the convenience-store giant ซีพี ออลล์ CP All and CP Foods.7 There was a poetic symmetry to the buyer: CP Group had been Tesco's original local partner when it first entered Thailand two decades earlier. The student was buying back the empire from the teacher.

What Tesco did with the proceeds tells you everything about the company's new philosophy. Rather than redeploy the windfall into fresh expansion, Tesco split it between shareholders and the balance sheet. It returned roughly £5 billion to shareholders as a special dividend — one of the largest cash returns in London market history — and used about £2.5 billion to eliminate the historic deficit in its UK pension scheme, a long-running liability that had hung over the company for years.7

That capital allocation decision was the symbolic moment Tesco completed its transformation: from a sprawling global conqueror into a laser-focused domestic operator with a clean balance sheet and a discipline of returning capital. And to run this newly streamlined machine, a new and rather unusual leadership pairing took the helm.

VI. The "Double-Murphy" Era: Current Management & Governance

Here is a detail that delights anyone who loves a corporate coincidence. The modern Tesco is led by two Irishmen, both named Murphy, who are entirely unrelated to one another — yet whose shared cultural background and strategic alignment have given the company an unusually coherent voice at the top. The City calls it, inevitably, the "Double-Murphy" era.

The first is Ken Murphy, who became chief executive in September 2020, succeeding the turnaround hero Dave Lewis. The second is Gerry Murphy, who became chairman in June 2023. No relation, as every profile dutifully notes — but a fantastic talking point, and a genuinely effective partnership.

Ken Murphy's Operational Philosophy

Ken Murphy was, in the truest sense, an outsider. He arrived not from the rough-and-tumble world of UK grocery but from Walgreens Boots Alliance, the transatlantic pharmacy and health-and-beauty giant, where he had held senior commercial and international roles. He was a retail operator and a brand man, steeped in the disciplines of merchandising, sourcing, and execution rather than dealmaking.

That background shaped his entire approach. Where the Leahy-era Tesco had been defined by bold strategic gambles and global ambition, Murphy's Tesco has been defined by what he calls relentless retail execution — the unglamorous, ceaseless grind of being a little bit better than the competition on price, availability, quality, and convenience, every single day. He is not a man chasing the next transformative acquisition. He is a man obsessed with the fundamentals: getting the right product on the right shelf at the right price, and defending market share inch by inch against Aldi and Lidl. In an industry where flashy strategy has repeatedly destroyed value — see Fresh & Easy — there is real wisdom in a leader who prizes operational consistency over the grand gesture.

Incentives, Remuneration, and Shareholding

For long-term investors, how a chief executive is paid and how much skin he has in the game matters enormously, because it reveals what the board is actually rewarding. Let's look under the hood.

Ken Murphy's direct shareholding in Tesco is modest in percentage terms — roughly 0.017% of the company — but in absolute terms that stake was worth approximately £6.7 million (around $8.5 million), enough to ensure his personal wealth rises and falls with the share price.[^9] His total pay, meanwhile, has drawn the predictable headlines that any large UK CEO package attracts. For the 2025/26 financial year, Murphy's total compensation reached approximately £10.8 million, built on a base salary of around £1.51 million, with that base rising to roughly £1.54 million for 2026/27.[^9]

The headline number invites outrage, but the structure is what an investor should focus on, and here the structure is genuinely well-designed. A striking 86% of Murphy's total compensation is variable — that is, it is not guaranteed salary but is tied to performance, much of it deferred into shares that vest over multiple years.[^9] In other words, the overwhelming majority of his pay only materializes if Tesco actually performs and the share price actually delivers for shareholders. That is exactly the alignment long-term owners want: a leader who eats his own cooking.

The Incentive Shift

The most strategically revealing detail is what metrics trigger the bonuses, because incentive design tells you what the board truly wants management to chase. In a notable recent change, Tesco added UK market share as a direct trigger in the executive bonus framework. This is a fascinating signal. It tells you the board has decided that holding and growing its share of the home market — fending off the discounters — is the single most important strategic priority, more important than chasing growth abroad or in adjacent categories. It is the boardroom equivalent of planting a flag in the ground and saying: this is the hill we defend.

Crucially, it comes with a self-imposed ceiling. Tesco management has spoken of targeting market share around the 30% mark but treating that as something of a soft cap — because pushing materially beyond it would invite exactly the kind of competition-regulator scrutiny no dominant grocer wants. It is a delicate dance: grow, but not so much that you trigger a referral to the Competition and Markets Authority.

The Food Waste Governance Controversy

Not every governance decision has been universally applauded, and an investor should note the awkward ones too. Tesco had for years included an ambitious 50% food waste reduction target within its executive Performance Share Plan — an ESG-linked metric meant to tie pay to sustainability progress. But after the company missed the relevant milestone, the board made the controversial decision to remove the food waste target from the long-term incentive plan, replacing it with cleaner commercial and free-cash-flow performance metrics.

To critics, this looked like moving the goalposts — quietly dropping an environmental commitment from executive pay precisely because it had become inconvenient to hit. To management, it was a rationalization toward metrics that more directly drive shareholder value. Reasonable people disagree, but it is a useful reminder that ESG-linked pay can be quietly unwound when it stops flattering the numbers, and that investors should watch what gets removed from incentive plans as closely as what gets added.

With the leadership and incentives mapped, we can now turn to the part of the Tesco story that genuinely separates it from a run-of-the-mill supermarket — the hidden engines of data and media that throw off margins a traditional grocer can only dream of.

VII. Hidden Engines: dunnhumby, Tesco Media, & Segment Data

In the late 1990s, a husband-and-wife team of mathematicians, Edwina Dunn and Clive Humby, walked into a Tesco boardroom to present the early results of an analysis they had run on the company's fledgling loyalty card data. The story, now legend in retail circles, is that after listening to them explain what their models could see about Tesco's customers, then-chairman Lord MacLaurin uttered the line that defined the relationship: "What scares me about this is that you know more about my customers after three months than I know after 30 years."

That company was dunnhumby, and acquiring it was, dollar for dollar, perhaps the most quietly brilliant capital allocation decision in Tesco's history.

The Best Acquisition You've Never Heard Of

Tesco took a majority stake in dunnhumby in stages through the early 2000s — building its ownership across roughly 2001 to 2004 — for a total outlay of less than £100 million. Set that number against everything else in this story: a £1.7 billion American failure, a £3.7 billion Booker deal, a £326 million fraud. Less than £100 million for the analytical engine that would become the crown jewel of the entire enterprise. It is the kind of asymmetric bet that defines great businesses.

The Power of Clubcard

What dunnhumby did was transform Tesco's Clubcard from a simple loyalty gimmick — collect points, get money off — into something far more valuable: the most comprehensive proprietary database of British shopping behavior ever assembled. Every time a shopper scanned their Clubcard, Tesco learned not just what was bought but who bought it, when, how often, in what combination, and in response to which promotion. Multiply that across more than 22 million households and tens of millions of baskets, and you have something no competitor can replicate: a multi-decade, closed-loop record of how the nation actually shops.

The genius is the closed loop. Tesco does not just see an ad impression; it sees the ad, the click, the store visit, and the purchase, all tied to the same identified customer. It knows whether the marketing actually worked, all the way through to the till. That is the holy grail of advertising — and Tesco has been quietly compiling it for over two decades.

Tesco Media & Insight Platform

Which brings us to the business that has the City genuinely excited: the Tesco Media & Insight Platform, powered by dunnhumby, now Europe's largest retail media network.

Here is the concept in plain terms. A retail media network turns a retailer's own digital and physical real estate — its app, its website, its in-store screens, its email list — into advertising space, and sells that space to the very brands whose products sit on its shelves. When Unilever or Coca-Cola wants to reach exactly the shoppers who buy a competitor's soap or soft drink, Tesco can target those specific Clubcard households with personalized offers and ads, then prove, using its closed-loop data, that the campaign drove real sales. It is Google and Facebook-style targeted advertising, except powered by real-world grocery purchases rather than browsing history.

The financials of this business are what make it so special. In FY2024/25, the Tesco Media & Insight Platform ran more than 9,000 custom advertising campaigns for suppliers, and it delivered an average return on ad spend (ROAS) of £6.60 for every pound brands spent — well above the roughly £3.80 industry average for comparable advertising.[^11] In other words, advertising with Tesco worked nearly twice as hard as the typical alternative, because the targeting was sharper and the measurement was real.

And here is the part that should make any investor sit up. Retail media is an asset-light, very high-margin business — margins north of 70% — bolted onto a traditional grocery operation whose own margins are measured in low single digits. Every pound of high-margin media revenue flows almost straight to the bottom line, effectively subsidizing the thin economics of selling actual groceries. It is, in essence, a software-like profit stream hiding inside a supermarket. This is one of the most important structural stories in modern Tesco, and it deserves to be understood as the genuine differentiator it is.

Segment-Level Performance

Let's now step back and look at how the whole machine performed across its segments, drawing on Tesco's FY2023/24 disclosures, because the segment picture reveals where the profit really lives.8

The heart of the business is UK & Republic of Ireland Retail, which generated around £57.2 billion in sales and produced approximately £2.67 billion in retail operating profit — a meaningful jump of roughly 15.7% year on year — at an operating margin in the region of 4.6%.8 That margin number is worth dwelling on: in grocery, a 4–5% operating margin is strong. This is a business of pennies on enormous volumes, which is precisely why the high-margin overlays like retail media matter so much.

The Booker (wholesale) segment contributed roughly £9.0 billion in revenue and around £290 million in operating profit — vindication, in hard numbers, of that controversial 2017 deal.8

The picture in Central Europe was the troubling one. The region delivered around £4.3 billion in sales, but operating profit halved — falling roughly 50% to about £90 million — battered by heavy government intervention.8 In Hungary in particular, the state imposed price caps on staple goods and levied special retail taxes targeted at large foreign-owned chains. This is a textbook illustration of political and regulatory risk eating directly into returns, and a reminder of why the modern Tesco is so happy to be concentrated in the relatively stable UK market.

The Capital-Light Tesco Bank Pivot

The final piece of the segment puzzle reflects the company's defining modern theme: shedding capital-intensive baggage. For years Tesco had run Tesco Bank, a full retail bank offering current accounts, savings, loans, mortgages, and credit cards. The problem is that banking is a brutally capital-intensive, heavily regulated business — every loan requires capital to be held against it, dragging down returns and tying up the balance sheet.

So in February 2024, Tesco agreed to sell the core retail banking operations — the deposits, loans, and credit cards — to Barclays in a deal worth around £600 million, structured with a long-term partnership under which Barclays would run Tesco-branded banking products.9 Critically, Tesco kept the genuinely attractive, capital-light pieces: the insurance and travel money operations, which require little capital and throw off steady profit — contributing on the order of £69 million in profit in the relevant period.9 Offload the heavy, capital-hungry balance sheet; keep the light, fee-generating annuity. It is the capital-light playbook in a single transaction, and it rhymes perfectly with the pension-clearing, cash-returning instincts of the post-2020 company.

So we have mapped the engines. Now the essential investor question: how durable is all this? What actually stops a competitor from copying it? For that, we need the strategy frameworks.

VIII. Strategic Moat: Porter's Five Forces & Hamilton's 7 Powers

Every business looks impressive when it is winning. The harder question — the one that separates a durable compounder from a temporary champion — is whether its advantages can survive contact with determined competitors. Let's war-game Tesco's position using two classic frameworks.

Porter's Five Forces

Start with competitive rivalry, which in UK grocery is nothing short of brutal. This is a low-growth, low-margin industry where Aldi and Lidl have spent a decade waging relentless price war, building store after store and forcing the entire sector to compete on price. Tesco's most elegant counter-move was the Clubcard Prices initiative — and it is worth understanding precisely why it was so clever. Rather than cutting prices for everyone (which simply destroys margin across the board), Tesco restricted its sharpest promotional prices exclusively to Clubcard members. A shopper sees two prices on the shelf: a higher standard price and a lower Clubcard price. To get the deal, you have to be a member and scan your card — which means Tesco competes hard on headline price perception while simultaneously harvesting ever more of the proprietary data that powers its media business. It is a price war fought with a data-gathering weapon.

Next, supplier power, which sits in the low-to-medium range. On one hand, Tesco's sheer scale — amplified by the Booker merger — gives it formidable leverage over the brands and farmers who supply it. On the other hand, that power is deliberately constrained by the Groceries Code Adjudicator (GCA), the UK regulator created specifically to stop large supermarkets from bullying suppliers — a watchdog born, in part, from the era of behavior that contributed to Tesco's own accounting scandal. So Tesco wields enormous buying power, but inside guardrails that prevent the worst abuses of the past.

The remaining forces round out the picture: the threat of new entrants into full-scale UK grocery is low (the capital and scale required are immense), buyer power is diffuse (millions of individual shoppers, no single one with leverage), and the threat of substitutes is real but bounded (discounters, online players like Ocado and Amazon, and meal-delivery services all nibble at the edges).

Hamilton's 7 Powers

Now the sharper lens — Hamilton Helmer's framework, which asks not just whether a company is winning but which specific, durable power lets it keep winning. Three of Helmer's seven powers map cleanly onto Tesco.

The primary power is Scale Economies. This is Jack Cohen's original weapon, now operating at national scale. Because Tesco buys more groceries than any other UK retailer, it secures a lower cost per unit than any domestic competitor. That cost advantage is not a temporary promotion; it is a structural feature of being the biggest. It allows Tesco to absorb inflationary cost shocks — passing less of them on to shoppers than smaller rivals must — and to fund its price competitiveness from a position of strength. In a commodity business measured in pennies, the lowest-cost operator holds a permanent, compounding edge.

The second power is Switching Costs, expressed through Clubcard Prices in a particularly subtle form. The "cost" of switching here is not a contract or a fee — it is the price penalty a customer pays for not participating. A shopper who does not engage with Clubcard effectively pays a premium of roughly 15–20% on promoted items versus the member price. That creates both a financial and a psychological lock-in: once you are habituated to scanning your card for the better price, defecting to a competitor means giving up real, visible savings. It is a velvet handcuff, and millions of households wear it.

The third, and perhaps most defensible, power is the Cornered Resource embodied in dunnhumby's closed-loop data. A competitor with infinite money cannot simply buy twenty-plus years of UK shopping-transaction history tied to identified households. That dataset can only be accumulated over time, by actually operating at scale, year after year. It is non-replicable by definition. And it is what makes Tesco's retail media network not merely strong but, in the language of strategy, incontestable — a rival can build the technology, but it cannot build the past.

Taken together, these three powers — structural cost advantage, customer lock-in, and a non-replicable data asset — are what justify viewing Tesco not as a commodity grocer trading on thin margins, but as a business with genuine, layered moats. The risk, of course, is that moats can be overestimated, and we will weigh the bear case shortly. But first, let's extract the transferable lessons, because the Tesco saga is a masterclass that applies far beyond groceries.

IX. The Playbook: Key Business & Investing Lessons

Strip away the British specifics, and the Tesco story yields a handful of lessons that travel to almost any industry and any era. Let's distill them.

Lesson One: Greenfield versus M&A in international scaling. The single starkest contrast in this entire saga is Fresh & Easy versus Booker. In the United States, Tesco tried to build from scratch — to impose a British retail formula, refined over decades at home, onto American consumers it fundamentally did not understand. It controlled everything and learned nothing fast enough, and it lost the better part of £2 billion. With Booker, by contrast, Tesco bought a local market leader — complete with its existing logistics, its established customer relationships, and its management team that already understood the terrain. The lesson is not that greenfield always fails or that acquisition always wins. It is that when you are entering an arena whose culture you do not deeply understand, buying embedded local knowledge beats trying to manufacture it from a foreign playbook. Humility, in the form of an acquisition, is often cheaper than confidence, in the form of a greenfield build.

Lesson Two: Retail media is the ultimate margin extender. Tesco's media business is the template for one of the most powerful ideas in modern business — that a company sitting on proprietary customer data and physical foot traffic can monetize that asset as advertising real estate, layering a software-margin profit stream on top of a low-margin physical operation. The thin economics of selling groceries become tolerable, even attractive, when each customer interaction also throws off high-margin media revenue. Any business with a loyal, identified customer base and a closed loop from impression to purchase should be asking whether it is sitting on an undermonetized media network. Amazon proved it online; Tesco proved it on the high street.

Lesson Three: The danger of "running too hot." The accounting scandal was not, at root, a story about a few dishonest individuals. It was a story about incentive structures under pressure. When a company sets profit and margin targets that the underlying business genuinely cannot meet — and then attaches careers, bonuses, and reputations to hitting those targets — it manufactures the conditions for fraud. The numbers do not lie about reality; they get forced to lie. The investor's takeaway is to be deeply suspicious of any business posting results that seem too smooth, too consistent, or too good relative to a deteriorating competitive environment. Structural rot often hides behind impossibly clean numbers. Ask not just "are the results good?" but "are the results plausible given what the competition is doing?"

Lesson Four: Capital-light transitions as a compounding playbook. The defining strategic motif of the modern Tesco is the deliberate shedding of capital-intensive assets and the return of the freed-up capital to shareholders. Selling the heavy banking balance sheet to Barclays while keeping the light insurance fees; exiting capital-hungry overseas hypermarkets and returning £5 billion as a special dividend; clearing the pension deficit to remove a balance-sheet overhang — each move follows the same logic. A mature business in a low-growth industry often creates more value by becoming lighter and more focused than by chasing growth for its own sake. Free the capital, return it to owners, and let the high-return core compound. It is the antithesis of the empire-building that nearly sank the company a decade earlier — and a reminder that for mature businesses, discipline frequently beats ambition.

These lessons set up the final question every investor ultimately cares about: where does Tesco go from here, and what should you actually watch?

X. Epilogue & Future Outlook

Stand back and consider the arc. A company that in September 2014 looked like it might be facing an existential crisis — its profits exposed as partly fictional, its market value collapsing, its reputation in tatters, its overseas empire bleeding cash — has, by 2026, remade itself into something genuinely impressive: a focused, disciplined, data-rich domestic champion, throwing off cash, returning capital, and defending a commanding share of its home market. Few corporate turnarounds of this scale and completeness exist in the modern record. The patient, unglamorous work of two chief executives — Lewis the fixer, Murphy the operator — rebuilt a great business from a position of near-disgrace.

The Modern Landscape

But the war is not won, because in grocery the war is never won. The competitive landscape remains relentless. Aldi and Lidl have not gone away; they continue to open new stores across Britain, methodically expanding their physical footprint and forcing the entire sector to keep prices keen. As the inflation spike of the early 2020s normalizes, the battleground shifts back to the eternal grind of value perception, availability, and convenience. Tesco's scale advantage and Clubcard lock-in give it powerful tools, but the discounters have proven they can grow share even against a strong incumbent. This is trench warfare, and it does not end.

The Bear Case and the Risks

A complete picture demands the bear case. Three risks stand out. First, the discounter threat is structural, not cyclical — if Aldi and Lidl continue compounding their store counts, they can keep chipping at Tesco's share regardless of how well Tesco executes. Second, the regulatory and political risk is real and was vividly illustrated in Central Europe, where Hungarian price caps and special retail taxes halved segment profit; a dominant grocer is always a tempting target for politicians, and that vulnerability exists at home as well as abroad. Third, the retail media growth story, exciting as it is, is still small relative to the core grocery business and faces the risk that as every major retailer builds a media network, the scarcity value — and the premium ROAS — erodes over time. Moats can be overestimated, and a prudent investor weighs the possibility that today's incontestable advantage becomes tomorrow's commoditized table stakes.

What to Watch

The single most important strategic tension to monitor is the market share ceiling. Ken Murphy has openly oriented the company around UK market share, even building it into executive pay — but with share already near 28% and an internal target around 30%, the question becomes: at what point does success itself become the problem? If Tesco's share inches toward and past 30%, will the Competition and Markets Authority intervene, scrutinizing future moves or even constraining growth? It is the paradox of dominance — the more completely Tesco wins, the more attention it draws from the regulators who guard against winning too completely. Watching how Tesco manages that ceiling, growing share without tripping the regulatory wire, will define the next chapter.

The KPIs That Matter Most

For an investor tracking this company's ongoing health, three metrics cut through the noise. The first is UK like-for-like sales growth — the cleanest measure of whether the core business is actually winning customers and volume against the discounters, stripped of the distortion of new store openings. The second is UK grocery market share (the Kantar figures), the literal scoreboard of the war with Aldi and Lidl and the metric management itself has chosen to be judged on. The third is retail media revenue and its margin contribution — the clearest indicator of whether the high-margin, asset-light profit engine is scaling fast enough to meaningfully lift group economics above the thin baseline of selling groceries. Track those three, and you will understand the Tesco investment case better than any single headline earnings number could tell you.

Final Reflections

There is a pleasing symmetry to ending where we began — with Jack Cohen and his market stall. The Tesco that nearly destroyed itself in 2014 was a company that had forgotten Cohen's lesson, seduced by global ambition and upmarket aspiration into abandoning the ruthless, low-cost discipline that built it. The Tesco that recovered did so, in essence, by remembering — by returning to scale-driven cost advantage, operational rigor, and an obsessive focus on giving the British shopper a fair price. It dressed that old wisdom in modern clothes: closed-loop data, retail media, capital-light returns. But at the core, the company that rose from the ashes of the accounting scandal is recognizably Jack Cohen's creation — pile it high, sell it cheap, and never let anyone buy cheaper than you. A hundred years on, the DNA endures.

References

-

Tesco shares plunge after profit overstatement disclosed — Reuters, 2014-09-22 ↩↩↩

-

Tesco takes 1.2 billion pound writedown on failed U.S. Fresh & Easy chain — Reuters, 2013-04-17 ↩↩

-

Tesco agrees landmark 129 million pound Deferred Prosecution Agreement with Serious Fraud Office — Reuters, 2017-03-28 ↩↩↩

-

Tesco buys wholesale giant Booker for 3.7 billion pounds — Reuters, 2017-01-27 ↩

-

Tesco and Booker £3.7bn Merger Clearances Statement — UK Competition and Markets Authority, 2017-12-20 ↩

-

Tesco PLC Reports, Results and Presentations Hub — Tesco Investor Relations ↩↩

-

Tesco agrees to sell Thailand and Malaysia businesses for $10.6 billion — Reuters, 2020-03-09 ↩↩↩

-

Tesco PLC Remuneration and Governance Policies — London Stock Exchange RNS, 2024-05-14 ↩↩↩↩

-

Tesco, Barclays strike 600 million pound retail banking deal — Reuters, 2024-02-09 ↩↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube