The Internet's Invisible Giant: The Story of Team Internet Group

I. Introduction: The Most Important Company You've Never Heard Of

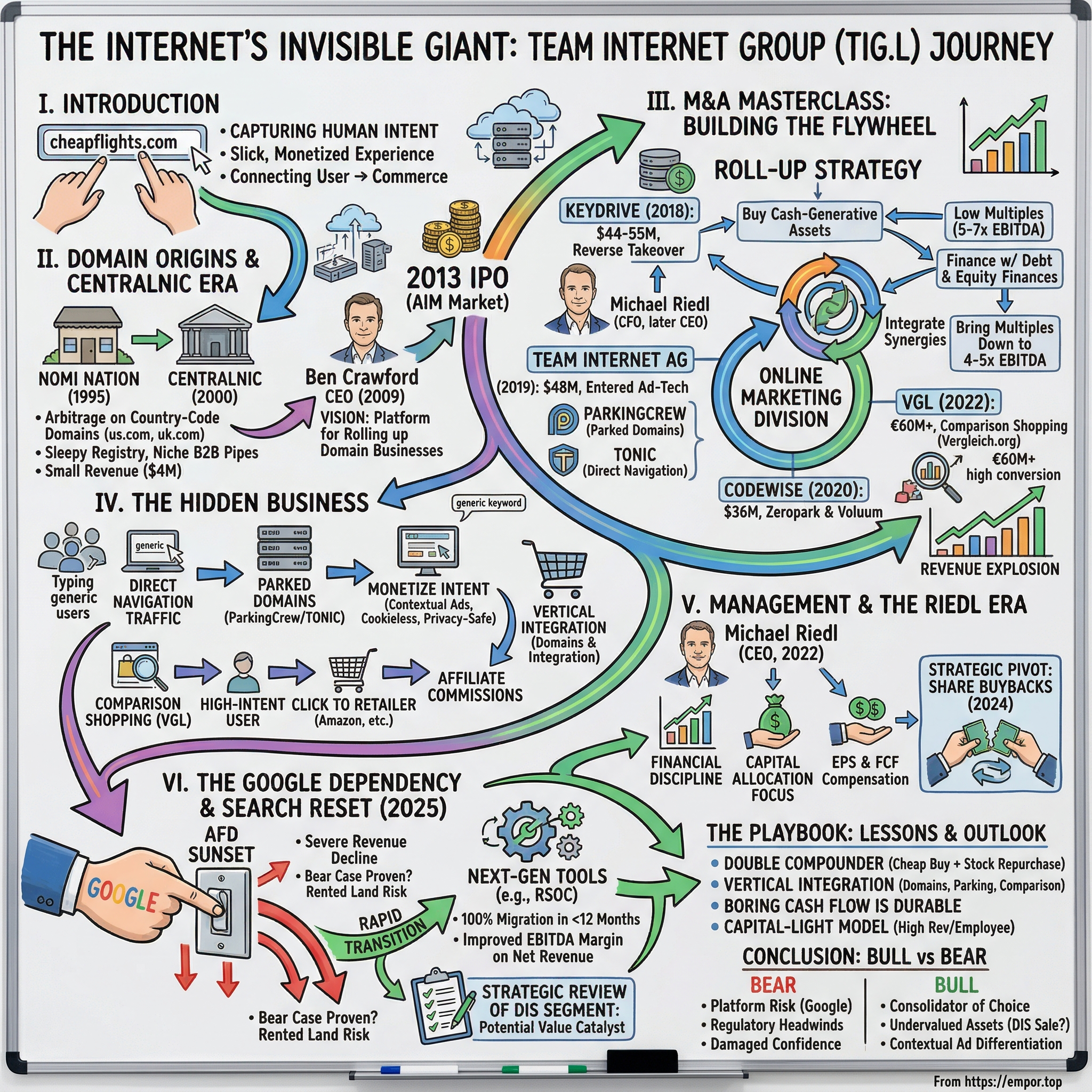

Picture this: you type "cheapflights.com" into your browser. Not because you remembered a specific website, but because it felt like the right domain to try. You land on a page — not a dead end, not a 404 error, but a slick, monetized experience serving you flight comparison ads, affiliate links, and product recommendations. You click. An advertiser pays. Somewhere in London, a company you have never heard of just made money.

That company is Team Internet Group.

Most people think of the internet as the apps on their phone and the websites they visit — Google, Amazon, Netflix. But beneath that visible layer lies an enormous, high-margin plumbing system that connects human intent to commerce. Every day, hundreds of millions of people type words into browser address bars, click on parked domains, browse comparison shopping sites, and follow links that route them toward purchasing decisions. The infrastructure that captures, routes, and monetizes that intent is worth billions. And Team Internet Group, a company listed on London's AIM market under the ticker TIG.L, sits right at the center of it.

Here is the thesis: Team Internet Group, formerly known as CentralNic, is one of the most remarkable roll-up stories in European public markets over the past decade. It transformed from a sleepy UK domain registry turning over four million dollars a year into a global performance marketing powerhouse with gross revenues exceeding eight hundred million dollars. It did this not through venture capital hype or speculative bets on unproven technology, but through disciplined acquisition of cash-generative internet assets at attractive multiples — compounding value quietly while the market looked elsewhere.

Think of it as the "mini-Google" of the alternative internet. Google captures intent through search. Team Internet captures intent through everything else: parked domains, direct navigation traffic, comparison shopping sites, and content monetization platforms. In a world where advertisers are desperate for alternatives to the Google-Meta duopoly, Team Internet built a privacy-safe, cookieless advertising engine that was never dependent on third-party tracking — long before the rest of the industry started panicking about cookie deprecation.

The story stretches from the dot-com leftovers of the 1990s to a billion-dollar-plus gross merchandise advertising engine. It involves a visionary domain entrepreneur, a finance-first CEO who understood capital allocation better than most Silicon Valley operators, and a series of acquisitions that look, in retrospect, like a masterclass in buying internet assets at the bottom of their valuation cycle. Along the way, the company changed its name, its business model, and its destiny.

This is how they did it — and what it means for investors trying to understand the hidden economics of the internet.

II. The Domain Origins and The CentralNic Era

In 1995, the commercial internet was barely a toddler. Netscape had just gone public. Amazon was operating out of a garage. And two British entrepreneurs named Steve Dyer and Robert Pooke had an idea that was either brilliant or absurd: what if you could sell domain names that looked like country-code domains but were not actually sanctioned by the official registries?

The company they founded was called NomiNation, and the concept reportedly originated from a suggestion by Jon Postel — one of the founding fathers of the internet's domain name system. The idea was to offer domains like "us.com" and "uk.com" and "eu.com" — extensions that felt official but operated outside the traditional country-code registry system. It was a clever arbitrage on human psychology: people trusted domains that looked like they belonged to a country, and NomiNation could sell them without needing permission from any government.

In 2000, the company rebranded to CentralNic, a name that better reflected its positioning as a central hub for alternative domain extensions. For the next decade, it operated as a small but profitable registry service provider — the kind of business that sold the "pipes" of the internet but did not own the "water" flowing through them. CentralNic managed about twenty-five domain extensions, including the country-code top-level domain for Laos (.la) and a portfolio of subdomain services. It was a niche business, deeply technical, and almost entirely invisible to anyone outside the domain industry.

The inflection point came around 2009, when Ben Crawford took over as CEO. Crawford inherited a company with roughly twelve employees and a few million dollars in revenue. But he saw something that most people missed: the domain name industry was quietly consolidating, and CentralNic's registry infrastructure could serve as a platform for rolling up fragmented domain businesses around the world.

Crawford's vision was not glamorous. He was not building a social network or a consumer app. He was building a wholesale distribution platform for domain names — a business-to-business operation where CentralNic would provide the back-end technology and services that enabled thousands of smaller registrars to sell domains to end customers. Think of it as the Sysco of the domain industry: not the restaurant you eat at, but the company that supplies the restaurant with everything it needs to operate.

The 2013 IPO on London's AIM market was the moment CentralNic stepped onto the public stage. The company raised ten million dollars at a time when it was generating approximately four million in annual revenue. By the standards of the domain industry's giants — GoDaddy with its Super Bowl ads and fifty million registered domains, Verisign with its monopoly on .com and .net — CentralNic was microscopic. It was listed on AIM, the junior exchange that most institutional investors ignored. Its market capitalization was trivial.

But the IPO gave Crawford something invaluable: a public currency for acquisitions. In the domain industry, there were hundreds of small, profitable registrars and registry operators scattered across the globe — family-owned businesses in Australia, niche players in Romania, corporate services firms in France. Most of them generated steady cash flows with renewal rates above ninety percent. They were attractive acquisition targets, but too small for private equity and too boring for venture capital. CentralNic could buy them, integrate them onto its platform, and extract synergies that the previous owners could never achieve alone.

The first few acquisitions were modest: DomiNIC GmbH in 2014, Internet.BS for seven and a half million dollars, Instra Corp in 2015. Each one added customers, domains under management, and geographic reach. But Crawford and his team quickly recognized a fundamental limitation of the registry and registrar business: it was stable, it was profitable, and it was maddeningly slow-growing. Domain registrations were a mature market. To win — to truly compound value for shareholders — CentralNic needed to move up the stack. It needed to find a way to monetize the traffic that flowed through its domains, not just collect registration fees.

That realization would transform the company. But first, it needed to make the biggest bet of its life.

III. The M&A Masterclass: Building the Flywheel

In 2018, CentralNic's board approved an acquisition that would fundamentally reshape the company. The target was KeyDrive Group, a Luxembourg-based domain services company with operations spanning wholesale distribution, retail domain sales, and corporate domain management across Europe and beyond. The price tag was approximately forty-four to fifty-five million dollars, including an earn-out — a number that was larger than CentralNic's own market capitalization at the time.

This was, in every meaningful sense, a "bet the company" move. The deal was structured as a reverse takeover, meaning KeyDrive was so large relative to CentralNic that it required shareholder approval and effectively merged the two organizations into a new entity. The transaction closed in October 2018, and overnight, CentralNic doubled in size.

But the KeyDrive deal brought something even more valuable than revenue: it brought Michael Riedl. Riedl had served as KeyDrive's CFO and Executive Vice President since 2011, overseeing the financial architecture of a complex, multi-jurisdictional domain business. He held a bachelor's in computer science from James Madison University, an MBA from EBS Universitat, a law degree from Frankfurt School of Finance and Management, and had completed the Harvard Advanced Management Programme. He was a chartered management accountant with deep experience in private equity and ICT management. When he walked through the door as CentralNic's new Group CFO, he brought a financial discipline and M&A sophistication that would prove decisive in the years ahead.

The KeyDrive integration was still underway when CentralNic made its next transformational move. In November 2019, the company announced the acquisition of Team Internet AG for approximately forty-eight million dollars — forty-five million in cash plus three million deferred. The seller was Matomy Media, an Israeli ad-tech firm that had fallen into financial difficulty and was liquidating assets.

This is where the narrative fundamentally shifts. Team Internet AG was not a domain registrar. It was an advertising technology company that operated two platforms: ParkingCrew and TONIC. ParkingCrew monetized parked domains — the millions of registered domain names that do not host active websites but instead display advertising when someone types them into a browser. TONIC handled direct navigation traffic, routing users who typed generic keywords into their address bars toward relevant advertising. Together, these platforms represented something genuinely unusual: an ad-tech engine that generated revenue from human intent without relying on search engines, social media, or third-party cookies.

The strategic logic was elegant. CentralNic already managed millions of domains through its registry and registrar operations. Many of those domains were parked — registered but not actively used by their owners. By acquiring Team Internet AG, CentralNic could now monetize those parked domains directly, creating a vertical integration play that no competitor could easily replicate. It was like a real estate company that had been collecting rent on empty lots suddenly discovering it could build profitable billboards on every single one of them.

The financial logic was equally compelling. While SaaS companies in Silicon Valley were trading at ten to fifteen times revenue, CentralNic was buying cash-generative internet assets at five to seven times EBITDA. The Matomy distressed sale meant Team Internet AG was available at a price that reflected the seller's desperation, not the asset's intrinsic value. And CentralNic's post-acquisition playbook consistently delivered: by integrating acquired businesses onto its platform, eliminating duplicate costs, and cross-selling services, the company routinely brought effective acquisition multiples down to the four to five times EBITDA range.

The funding mechanism deserves attention. CentralNic financed the Team Internet AG acquisition through a forty-million-euro bond arranged by Macquarie — using relatively low-cost debt to acquire high-yield internet assets. This was the arbitrage at the heart of the strategy: borrow cheaply in London's capital markets, buy profitable internet businesses at depressed valuations, integrate them quickly, and use the resulting cash flows to pay down debt and fund the next acquisition. It was a flywheel, and once it started spinning, the compounding became remarkable.

The acquisition pace accelerated. In 2019 alone, CentralNic also acquired TPP Wholesale in Australia for twenty-four million Australian dollars, Hexonet Group for up to ten million euros, and Ideegeo Group in New Zealand. Each deal added geographic reach and customer density. Then in September 2020, the company made another game-changing move: acquiring Codewise, a Polish ad-tech company that operated Zeropark (an ad exchange) and Voluum (a SaaS analytics platform for performance marketers), for thirty-six million dollars.

The Codewise numbers are worth pausing on. The company was generating sixty million dollars in annual revenue and seven and a half million in adjusted EBITDA. CentralNic paid thirty-six million — roughly 0.6 times revenue and 4.9 times EBITDA. In an era when the median SaaS company traded at twelve times revenue, this was the kind of deal that value investors dream about. CentralNic funded it by placing forty million new shares at a price that raised thirty-nine million dollars, diluting existing shareholders modestly but acquiring a business that would immediately contribute to earnings.

By 2021, the flywheel was spinning at full speed. Revenue had grown from fifty-six million in 2018 (the year of KeyDrive) to four hundred and eleven million — a compound annual growth rate that put CentralNic in the company of the fastest-growing public companies in the UK. Organic growth alone was running at thirty-nine percent. The company had completed twenty-one acquisitions under Ben Crawford's leadership, each one adding a new capability, a new geography, or a new revenue stream to the platform.

The M&A playbook that CentralNic perfected during this period offers a genuine lesson in capital allocation. Every acquisition had to meet three criteria: it had to be cash-generative immediately, it had to integrate cleanly onto the existing platform, and it had to be available at a price that reflected the seller's circumstances rather than the asset's long-term value. The company was not buying growth at any price. It was buying profitable businesses at attractive prices and using its scale advantages to make them even more profitable after integration. In a market obsessed with revenue multiples and "growth at all costs," this approach was almost quaint. It was also extraordinarily effective.

IV. The Hidden Business: Performance Marketing and VGL

To understand what Team Internet Group actually does — and why it matters — you need to understand a corner of the internet that most people never think about.

Every day, millions of people type words directly into their browser's address bar. Not a Google search. Not a URL they bookmarked. Just a word or phrase — "cheapinsurance," "bestlaptops," "hoteldeals" — hoping that something useful appears. In many cases, the domain they land on is parked: it is registered by someone who recognized the keyword's commercial value but never built a website on it. Instead, the domain displays advertising — search ads, product listings, affiliate links — that are contextually relevant to the keyword the user typed.

This is "direct navigation" traffic, and it represents one of the purest forms of commercial intent on the internet. The user has effectively told you exactly what they want by typing it into their browser. No search engine mediation. No social media algorithm. No cookie tracking. Just a human being expressing a need and a domain name capturing that expression.

Team Internet Group monetizes more than twenty million of these parked domains through its ParkingCrew and TONIC platforms. ParkingCrew handles the domain parking monetization — serving ads on parked domains and splitting the revenue with the domain owners. TONIC manages direct navigation routing, directing users toward the most relevant and highest-paying advertising outcomes. Together, they form what the company calls its "Search" segment (recently carved out as a distinct business unit).

But the even more interesting business — and the one most frequently misunderstood by investors — is what Team Internet calls its "Comparison" segment. This is where the VGL acquisition comes in.

In March 2022, CentralNic completed its largest acquisition ever: VGL Verlagsgesellschaft, a Berlin-based company that operated Vergleich.org and a network of comparison and review websites across the German-speaking DACH region (Germany, Austria, Switzerland). The enterprise value was approximately sixty million euros, with a total consideration including earn-outs that could reach over a hundred million. The deal was funded through a combination of a forty-two-million-pound share placing at 120 pence per share, a twenty-one-million-euro bond, and a three-million-pound open offer.

VGL is a leader in what the industry calls "comparison shopping" or "commerce media." Its websites publish detailed product reviews and comparisons — think "best vacuum cleaners 2025" or "top health insurance plans" — that attract users with genuine purchase intent. These users read the reviews, click through to retailers like Amazon or eBay, and make purchases. VGL earns revenue through affiliate commissions and advertising fees. The conversion rates are extraordinary because the traffic is "high-intent": these are not casual browsers scrolling through social media. These are people actively researching a purchase decision.

The secret sauce — the thing that ties the entire Team Internet platform together — is how these different pieces interact. Consider the full vertical stack: Team Internet manages millions of domains through its registry and registrar operations (the "Domains, Identity and Software" segment). Many of those domains generate direct navigation traffic. That traffic is monetized through ParkingCrew and TONIC. Meanwhile, VGL's comparison sites capture purchase-intent traffic through organic search and content marketing. The advertising feeds that monetize all of this traffic flow through Team Internet's ad-tech infrastructure.

What you have, in effect, is a company that captures users before they even reach a search engine and routes them toward commerce. This is privacy-safe, cookieless advertising by design — not by retrofit. Team Internet's monetization model was never dependent on third-party cookies because it relies on contextual signals: the keyword in the domain name, the user's geographic location, the device they are using. In a post-GDPR world where regulators are cracking down on tracking and Google has been deprecating third-party cookies in Chrome, Team Internet's model represents something approaching the holy grail for privacy-conscious advertisers.

The segment data tells the story of transformation. By 2023, the Online Marketing division (which included both Search and Comparison) was generating six hundred and fifty-seven million dollars in gross revenue — nearly eighty percent of the company's total. The domain business, while still highly profitable with its ninety-percent-plus renewal rates and recurring revenue characteristics, had become the smaller sibling. When Team Internet restructured its reporting in 2024 to break out three segments — Domains, Identity and Software; Comparison; and Search — the shift became even clearer. The DIS and Comparison segments together contributed over fifty-one percent of net revenue, up from forty-four percent the prior year, reflecting a deliberate strategy to reduce dependence on the more volatile Search segment.

For investors, the VGL acquisition represented a bet on the durability of comparison shopping as an advertising channel. The logic was sound: as long as consumers research purchases online, comparison sites will capture high-intent traffic. Unlike social media advertising, which interrupts users who are not necessarily in a buying mindset, comparison shopping captures users who have already decided to buy and are merely deciding what. The economics of that distinction are profound — conversion rates are multiples higher, and advertisers are willing to pay substantially more per click.

The risk, of course, is concentration. Team Internet's Search segment was historically dependent on Google's AdSense for Domains program, which served ads on parked domains. That dependency would come back to haunt the company — but more on that later.

V. Management: The Riedl Era

In December 2022, Ben Crawford stepped down as CEO of what was then still called CentralNic Group. His tenure had been extraordinary by any measure: he took a company with twelve employees and a few million in revenue and built it into a global platform generating over seven hundred million dollars annually. Twenty-one acquisitions. Organic growth exceeding sixty percent in some years. A share price that had risen from the IPO level to become one of the better-performing stocks on AIM. Crawford later moved on to become CEO of Com Laude, a corporate domain management firm, continuing his career in the domain industry he knew so well.

His successor was the man who had been quietly architecting the financial strategy behind CentralNic's acquisition spree for four years: Michael Riedl.

Riedl's appointment as CEO was a signal that the company's next chapter would be defined by financial discipline rather than deal volume. His background was unusual for a tech CEO — not an engineer, not a product visionary, but a chartered management accountant with degrees in computer science, business administration, and law, plus the Harvard Advanced Management Programme on his resume. He had spent years in private equity and ICT management before joining KeyDrive in 2011, where he built the financial infrastructure that enabled the kind of complex, cross-border transactions CentralNic would later execute at scale.

The "finance-first CEO" archetype is more common in the roll-up world than people realize, and for good reason. When your strategy depends on buying businesses at the right price, integrating them efficiently, and allocating capital between debt repayment, acquisitions, and shareholder returns, the CEO's most important skill is not product intuition — it is financial judgment. Riedl understood the spread between the cost of capital and the return on acquired assets better than almost anyone in the UK small-cap universe. He could evaluate a potential acquisition not just on its standalone merits but on how it would interact with the existing portfolio, what synergies were realistic, and how the combined entity's cost of capital would change after the deal closed.

His management style reflected this orientation. Where Silicon Valley CEOs communicate through product launches and keynote speeches, Riedl communicated through Medium articles and investor presentations that laid out the company's strategy with unusual transparency. He was direct about the company's evolution, writing publicly about the journey from four million to eight hundred million in revenue and explaining why the CentralNic name no longer fit a business that derived most of its value from advertising technology.

The incentive structure under Riedl reinforced the capital allocation focus. Management compensation was heavily weighted toward adjusted earnings per share growth and free cash flow generation — the two metrics that matter most for a roll-up strategy. This was not a company where executives got rich from revenue growth alone. They had to grow earnings, which meant every acquisition had to be accretive and every integration had to deliver promised synergies. The alignment between management incentives and shareholder interests was tight.

The board composition added another layer of governance strength. Max Royde of Kestrel Partners held roughly twenty-three percent of outstanding shares — the largest single position — giving the company a committed, long-term anchor shareholder with significant influence over strategic decisions. Horst Siffrin, a former German diplomat who had chaired KeyDrive's supervisory board, held nearly twelve percent. Samuel Dayani, who had purchased the company back in 2003 and managed the restructuring that led to the 2013 IPO, retained a seven percent stake. These were not passive shareholders. They had deep institutional knowledge and strong opinions about capital allocation.

One of the most telling strategic decisions of the Riedl era was the pivot toward share buybacks. In September 2024, with the stock trading well below what management believed was intrinsic value, the board authorized a buyback program of up to thirteen million shares or nineteen and a half million pounds, whichever was reached first. The company executed purchases through late 2024 and into early 2025 at prices between seventy-nine and eighty-five pence per share.

The buyback signaled something important: management believed the most attractive acquisition target was no longer an external business — it was their own stock. When a roll-up company shifts from buying other companies to buying its own shares, it tells you one of two things: either there are no more attractive acquisition targets available, or the stock is so undervalued that no external acquisition can compete with the returns from repurchasing. Given that Team Internet's shares were trading at a fraction of what similar assets would cost in the private market, the latter explanation seems more persuasive.

The communication style with London's investor community also evolved under Riedl. CentralNic had always been a somewhat awkward fit for the London market — a UK-listed company whose operations were overwhelmingly Continental European and whose business model had more in common with American ad-tech firms than with the British industrial companies that dominated AIM. Riedl worked to bridge this gap, but the challenge remained: London analysts who covered the stock often struggled to benchmark it against familiar comparables, and the company's dual identity as both a domain business and an advertising business made it difficult to categorize cleanly.

This communication challenge would become more acute as the company navigated the most difficult period in its history — a forced transition in its largest revenue segment that would test whether the management team's financial discipline could survive a genuine crisis.

VI. The Google Dependency and The Search Reset

No analysis of Team Internet Group is complete without confronting the elephant in the room: Google.

For years, Team Internet's Search segment depended heavily on Google's AdSense for Domains program, known in the industry as AFD. The mechanics were straightforward: when a user landed on a parked domain, AFD served Google search ads on the page. The user clicked an ad, the advertiser paid Google, and Google shared a portion of that revenue with Team Internet, which in turn shared a portion with the domain owner. It was a three-way split on high-intent traffic, and it worked beautifully — until Google decided to change the rules.

In early 2025, Google completed the sunset of its AFD program ahead of schedule and introduced new policies — Restricted Access Features and Referrer Ad Creative requirements — that dramatically altered the economics of domain parking monetization. The impact on Team Internet was immediate and severe. The Search segment, which had been the company's largest revenue contributor, saw gross revenue decline sharply. For the first half of 2025, total group revenue fell thirty-six percent compared to the prior year period, driven almost entirely by the Search reset.

This was the moment that validated or invalidated the entire bull case for Team Internet. The bears had always warned that the company's advertising business was built on rented land — Google's platform, Google's rules, Google's ability to change terms unilaterally. And here was the proof: a single policy change by a single supplier had wiped out a significant portion of the company's revenue almost overnight.

But the story of how management responded reveals a great deal about the quality of the organization. Team Internet had been preparing for this transition for years, developing alternative monetization technologies under the umbrella of "next-generation" tools. The most important was Related Search on Content, or RSOC — a format that delivers search advertising within content pages rather than on bare parked domains. RSOC generates higher revenue per click than AFD because the user engagement is deeper, but it requires a fundamentally different technical approach and a different relationship with advertising partners.

The transition numbers tell the story of a company managing through genuine adversity. At the start of 2025, next-generation monetization tools including RSOC accounted for just four percent of gross revenue. By mid-year, that figure had risen to twenty-four percent. By late 2025, the company reported that "nearly one hundred percent of revenue" came from next-generation tools — a complete migration accomplished in under twelve months.

The financial cost was real. Management guided for full-year 2025 adjusted EBITDA of forty to forty-five million dollars, less than half the ninety-two million achieved in 2024. But the adjusted EBITDA margin on net revenue actually improved, reaching fifty percent for the nine months through September 2025, because the revenue that remained was higher-quality and higher-margin. The company was smaller in gross revenue terms but arguably healthier in economic terms.

The Shinez impairment added to the pain. In the 2024 annual results, Team Internet recognized a thirty-six-million-dollar impairment charge on Shinez I.O., an Israeli social media marketing subsidiary acquired as part of the broader online marketing portfolio. The impairment drove a reported loss after tax of nearly eighteen million dollars for the year. While impairments are non-cash charges that do not affect the company's operating performance, they do reflect management's acknowledgment that a previous acquisition had failed to deliver expected returns — a rare blemish on an otherwise strong M&A track record.

The strategic review announced in 2025 was perhaps the most interesting response to the crisis. Team Internet disclosed that it had received "a number of inbound approaches" and appointed a top-tier financial adviser to evaluate options for the Domains, Identity and Software segment specifically. The board stated publicly that the DIS segment alone could be valued above the company's entire market capitalization — an extraordinary claim that, if validated, would mean the market was assigning zero or negative value to the Comparison and Search businesses.

This is the kind of situation that attracts activist investors and strategic acquirers. A company trading at a significant discount to the sum of its parts, with a board that has acknowledged the discount and is actively exploring ways to close it. The potential outcomes include a sale of the DIS segment (with proceeds used for debt repayment and capital returns), a sale of the entire company, or a restructuring that separates the businesses to allow each one to be valued on its own merits.

For investors watching this story unfold, the Google dependency episode offers a crucial lesson about platform risk in internet businesses. Team Internet's parked domain monetization was always one policy change away from disruption — and when that change came, it came hard. The fact that management had been building alternative revenue streams and was able to migrate relatively quickly speaks to operational competence, but it does not erase the fundamental vulnerability. Any investment thesis for Team Internet must grapple with the reality that a meaningful portion of the company's advertising revenue flows through channels controlled by third parties.

VII. Strategic Framework: The Seven Powers and Five Forces

To assess Team Internet Group's competitive position rigorously, it helps to apply the frameworks that serious investors use to distinguish durable advantages from temporary ones.

Hamilton Helmer's Seven Powers framework identifies the specific sources of persistent competitive advantage that allow a business to earn returns above its cost of capital over long periods. Team Internet possesses several of these powers, though the strength of each varies.

The most compelling is what Helmer calls a "Cornered Resource" — proprietary access to an asset that competitors cannot replicate. Team Internet's cornered resource is its access to direct navigation traffic through more than twenty million parked domains. When a user types a generic keyword into a browser address bar and lands on a monetized domain, that traffic flows through Team Internet's infrastructure. Google cannot intercept it. Meta cannot redirect it. No social media algorithm determines whether the user sees it. The traffic exists because humans have an ingrained habit of typing words into browsers, and Team Internet controls the monetization layer between that habit and the advertising market. As long as browsers support direct navigation — and there is no indication that this behavior is declining — this represents a genuine cornered resource.

Switching costs provide another source of power. Team Internet manages domains and digital identity services for approximately thirty-five thousand customers, many of whom have large portfolios. A corporation with ten thousand domains managed through Team Internet's platform faces an enormous switching cost: every domain requires DNS configuration, renewal management, security certificates, and often brand protection monitoring. Migrating that portfolio to a competitor is not just expensive — it is operationally risky. The fear of a botched migration causing downtime on business-critical domains keeps customers locked in, producing renewal rates above ninety percent.

Counter-positioning is arguably Team Internet's most interesting strategic power. The company provides an alternative to the Google-Meta advertising duopoly for brands and performance marketers seeking lower customer acquisition costs. Its advertising is privacy-safe, contextual, and based on direct intent signals rather than behavioral tracking. For advertisers watching the regulatory environment tighten around data privacy — GDPR in Europe, state-level privacy laws in the United States, Apple's tracking restrictions — Team Internet offers a way to reach high-intent consumers without the compliance headaches. Google and Meta could theoretically build competing products, but doing so would cannibalize their own tracking-based advertising businesses. That reluctance to self-cannibalize is the essence of counter-positioning.

Applying Porter's Five Forces provides a complementary view. The bargaining power of suppliers is low: there are millions of domain owners worldwide, and no single domain owner has leverage over Team Internet's monetization platform. The bargaining power of buyers (advertisers) is moderate: while large advertisers have alternatives, the specificity and intent quality of direct navigation traffic commands premium pricing. The threat of new entrants is low in the domain infrastructure business due to the capital requirements and regulatory complexity of operating registries and registrars, though higher in the advertising segment where technology barriers are lower. The threat of substitutes is the most significant force: social media advertising, influencer marketing, and other channels compete for the same advertising budgets, though none offer the same combination of intent quality and privacy safety.

The competitive rivalry within Team Internet's specific niche is relatively low. In domain services, the company competes with GoDaddy, Verisign, and a fragmented landscape of smaller registrars — but Team Internet's wholesale and B2B positioning means it is often a supplier to these competitors rather than competing with them directly. In comparison shopping, competition is more intense, with players like Check24 in Germany and various vertical-specific comparison sites vying for the same high-intent traffic. In domain parking monetization, Team Internet is the dominant player globally, with ParkingCrew holding a patented position in HTTPS traffic monetization that is difficult to replicate.

The framework analysis suggests that Team Internet's competitive position is stronger than its market valuation implies, but not impregnable. The cornered resource in direct navigation traffic is real but subject to the risk that browser behavior changes over time — if Chrome, which runs on Chromium, were to alter how it handles direct navigation (routing typed keywords to Google Search instead of resolving them as domains), the entire parked domain monetization model would be at risk. This is not a theoretical concern: Google controls Chrome, and Google's incentive is to capture as much search traffic as possible. The fact that Microsoft's Edge, Apple's Safari, and Firefox all handle direct navigation similarly provides some diversification, but Chrome's market share dominance makes this a material risk factor.

For investors tracking Team Internet's ongoing performance, three key performance indicators stand out above all others. First is net revenue growth (as opposed to gross revenue), because net revenue strips out the traffic acquisition costs that are passed through to domain owners and advertising partners, revealing the true economic value the company captures. Second is adjusted EBITDA margin on net revenue, which measures the company's ability to convert its economic value into cash profits — the fifty-percent level achieved in late 2025 represents a strong benchmark. Third, and this one matters for understanding the sustainability of the business model, is the mix of revenue between the three segments: DIS, Comparison, and Search. A healthy Team Internet is one where the high-recurring DIS segment and the high-growth Comparison segment are increasing their share of total revenue relative to the more volatile and Google-dependent Search segment.

VIII. The Playbook: Lessons for Investors and Founders

Team Internet Group's decade-long transformation offers several lessons that extend well beyond the domain industry.

The first is the power of what might be called the "double compounder" model. Most roll-up strategies create value in one dimension: they buy businesses and integrate them. Team Internet compounded in two dimensions simultaneously. It bought businesses at low multiples — consistently in the four-to-seven-times EBITDA range — and then used the cash flow from those businesses to either pay down debt (reducing the cost of capital) or buy back undervalued shares (increasing per-share value). The mathematics of this approach are powerful: if you can buy businesses generating twenty-percent cash-on-cash returns and simultaneously repurchase stock trading at a thirty-to-forty percent discount to intrinsic value, the per-share value compounds at a rate that far exceeds the underlying business growth.

The second lesson is the strategic value of vertical integration in internet businesses. Team Internet does not just sell domains. It does not just monetize parked domains. It does not just operate comparison shopping sites. It does all three, and the interaction between these businesses creates value that would not exist if each operated independently. A domain registered through the DIS segment can be monetized through the Search segment's parking infrastructure, driving traffic that converts through the Comparison segment's review content. Each layer of the stack reinforces the others, creating a flywheel that is difficult for competitors to replicate because no single competitor operates across all three layers.

The third lesson is the enduring importance of "boring" cash flow in building long-term shareholder value. In a decade dominated by narratives about growth at all costs, zero-interest-rate speculation, and venture-backed companies burning cash in pursuit of market share, Team Internet proved that disciplined acquisition of profitable businesses could generate extraordinary returns. From its 2013 IPO through its peak share price in August 2024, the stock delivered returns that rivaled many of the most celebrated growth stories. It did this not by disrupting industries or changing consumer behavior, but by patiently accumulating cash-generative internet assets at attractive prices and managing them with financial rigor.

Revenue per employee of approximately 1.6 million dollars underscores just how capital-light this business model is. Team Internet does not need factories, warehouses, or large sales forces. Its infrastructure is digital, its products are virtual, and its marginal costs are close to zero. This operating leverage means that incremental revenue flows almost directly to the bottom line — a characteristic that makes the business highly attractive in inflationary environments where labor and material costs are rising.

The vertical integration playbook also created an underappreciated optionality. By owning assets across the domain value chain — from the registry to the registrar to the advertising feed — Team Internet has the ability to launch new products and services that leverage its existing infrastructure without significant incremental investment. The expansion of VGL's comparison shopping model from the DACH region into new international markets is one example. The development of AI-generated consumer journeys is another. These are not speculative bets on unproven technology; they are extensions of proven business models into adjacent markets, funded by existing cash flows.

IX. Conclusion: The Bull and Bear Case

The bear case for Team Internet Group centers on three interlocking risks.

First, the Google dependency that was exposed in 2025 may not be a one-time event. The Search segment's transition to RSOC and other next-generation monetization tools reduces direct AFD exposure, but the advertising ecosystem remains fundamentally influenced by Google's policies and platform decisions. If Google were to change how Chromium handles direct navigation — routing typed keywords to Google Search results rather than resolving them as domain addresses — the entire parked domain monetization model could face existential pressure. Google controls approximately sixty-five percent of the global browser market through Chrome, and its incentive to capture more search traffic is permanent.

Second, the ad-tech regulatory environment is tightening globally. While Team Internet's privacy-safe, cookieless model is better positioned than most for a world of stricter data protection rules, the broader regulatory trend toward transparency in digital advertising could introduce compliance costs or restrict certain monetization practices. The EU's Digital Markets Act, the UK's Digital Markets, Competition and Consumers Act, and evolving privacy regulations in the United States all represent potential headwinds.

Third, the 2024 Shinez impairment and the 2025 revenue decline have damaged investor confidence. The share price declined from a peak of approximately two hundred and eight pence in August 2024 to around forty-eight pence by early 2026 — a decline of roughly seventy-seven percent. Rebuilding credibility with the market after that kind of drawdown takes time, and the stock may remain in "show me" territory for an extended period regardless of underlying business improvement.

The bull case is equally compelling, and perhaps more so.

Team Internet is the "Consolidator of Choice" in a fragmented market. The domain services industry remains highly fragmented globally, with hundreds of small registrars and registries that could be acquired at attractive multiples. The company's proven integration playbook and its global platform give it structural advantages in executing and integrating these transactions. If management resumes acquisitive growth once the Search transition stabilizes, the flywheel could begin spinning again.

The strategic review of the DIS segment represents a potential catalyst. If the board's assertion that the DIS segment alone is worth more than the company's current market capitalization is validated through a sale or partial divestiture, the resulting capital return could be transformative for shareholders. Even a partial crystallization of DIS value could fund a special dividend or tender offer that rewards patient investors.

The market re-rating potential is significant. Team Internet is currently valued by the market as a troubled ad-tech roll-up in decline. But if the Comparison and Search segments stabilize and return to growth — management has guided for double-digit earnings growth in 2026 — the stock could be re-rated toward the multiples enjoyed by SaaS-adjacent platform businesses. The gap between the current valuation (low single-digit EBITDA multiples) and the multiples that comparable platforms trade at (mid-to-high single digits or higher) represents substantial upside if the re-rating materializes.

The privacy-safe advertising positioning becomes more valuable with each passing year. As regulators crack down on behavioral tracking and consumers become more privacy-conscious, Team Internet's contextual, intent-based advertising model becomes increasingly differentiated. The company does not need to adapt to a cookieless future because it was built for one. For advertisers seeking alternatives to the Google-Meta duopoly — and regulators are actively encouraging such alternatives through competition policy — Team Internet offers a proven, scaled platform.

Team Internet Group is, in the end, the ultimate story of reinvention through capital allocation. A company that started life as a tiny British domain registry, changed its name, changed its business model, and transformed itself into a global internet platform managing the invisible infrastructure between human intent and digital commerce. The next chapter — whether it involves a strategic sale, a return to acquisitive growth, or a market re-rating as the business stabilizes — will be written by the same forces that created the company: disciplined financial management, a deep understanding of internet economics, and the willingness to act decisively when the market presents an opportunity.

The question for investors is not whether Team Internet built something real. It did. The question is whether the market will ever recognize it.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube