Thule Group: Owning the Active Life

I. Introduction: The "Roof Rack" of the World

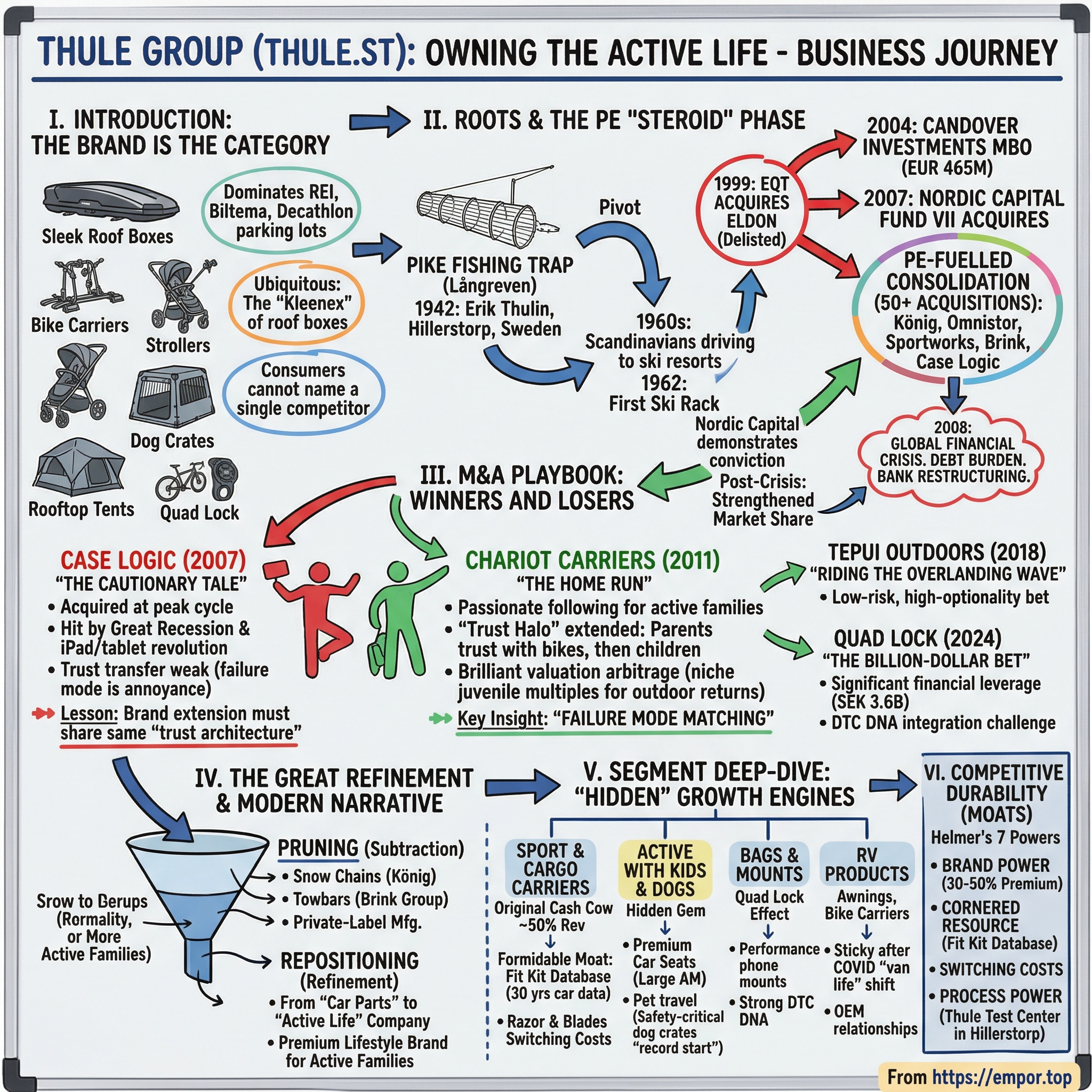

Picture this scene: a Saturday morning at any REI parking lot in America, any Biltema in Sweden, any Decathlon in Germany. Families loading up SUVs for a weekend escape. Look at the roofs. One brand dominates—those sleek, aerodynamic boxes and bike carriers with the unmistakable logo. Thule.

It is so ubiquitous that many consumers cannot name a single competitor. Ask someone what brand makes their roof box, and they will say "Thule" the way someone says "Kleenex" for tissues or "Google" for search.

The brand has become the category.

Walk into any outdoor specialty retailer, and the Thule wall is impossible to miss. It occupies prime real estate—usually right near the entrance, with gleaming displays showing the full ecosystem: base racks, cargo boxes in jet black, bike carriers with aerospace-grade clamping mechanisms, kayak mounts, and increasingly, strollers that look more like something from a Formula 1 design studio than a baby store. The staff can recite fit guides from memory. The customer who walks in knowing they want "a Thule" is the retailer's dream: high average ticket, low return rate, and a lifetime of accessory purchases ahead.

But here is the thing most investors miss.

Thule Group AB is no longer just "the box on top of the car." As of early 2026, this Malmö-headquartered company commands a market capitalization north of SEK 24 billion. It sells in 136 countries through 4,700 points of sale. Its products range from $1,200 strollers and crash-tested dog crates to rugged luggage, rooftop tents, and—following its landmark 2024 acquisition of Quad Lock—performance phone mounts for cyclists and motorcyclists worldwide. The revenue base has climbed back above SEK 10 billion, and management has publicly targeted 7% annual organic growth with 20% EBIT margins. The employee base is lean—roughly 2,800 full-time staff generating over SEK 3.5 million in revenue per employee, a figure that would make most consumer goods companies envious.

The thesis of this deep dive is deceptively simple.

How does a company take a "utility" product—steel bars bolted to a car roof—and transform it into a Veblen-esque lifestyle brand that commands premium pricing, earns fat margins, and extends trust across entirely new categories? The answer involves a PE-fueled consolidation phase that rolled up an entire fragmented industry, a disciplined post-IPO "refinement" that pruned away everything that did not fit the premium narrative, and a series of bold category expansions built on a single insight—that parents who trust Thule with their $8,000 carbon-fiber road bike will trust the same brand with their firstborn child.

Along the way, there are cautionary tales of overpaying at cycle peaks, a financial crisis that nearly broke the company, and a CEO succession that shifted strategic emphasis from engineering-first to retail-first.

And then there are the "hidden" growth engines—juvenile products, pet travel, overlanding—that could double the addressable market over the next decade. Whether Thule ultimately becomes the "LVMH of the Outdoors" or succumbs to the secular decline of car ownership in dense cities is the central debate for long-term investors. Let us unpack it.

II. Roots and the Private Equity "Steroid" Phase

In 1942, in the tiny village of Hillerstorp in Sweden's Småland province—the same hardscrabble region that produced IKEA's Ingvar Kamprad—a man named Erik Thulin had a simple idea. He designed a pike fishing trap, a "långreven," and began selling it to Scandinavian fishermen under a brand name derived from the mythical Nordic land of Thule, the northernmost edge of the known world. It was modest, handmade, deeply local. Nobody could have predicted what it would become.

For two decades, Thule remained exactly what it was: a small-town Swedish workshop making outdoor gear.

The pivot came in the 1960s. Thulin noticed that Scandinavians were increasingly driving to ski resorts and lakeside cabins for weekend getaways, but they had no good way to carry their equipment. In 1962, Thule introduced its first ski rack.

It was an elegant, practical solution—and it changed everything. By 1977, the company had launched the TB-11, its first enclosed ski box, and recruited alpine legend Ingemar Stenmark as a brand ambassador. The association with elite athletes was no accident—it planted the seeds of the premium, performance-oriented brand identity that would define Thule for decades to come.

There is something characteristically Swedish about this origin story. Småland, the province where Thule was born, is known for its frugal, entrepreneurial culture. The soil is rocky, the winters long, and the people resourceful. Ingvar Kamprad grew up in Småland and built IKEA on the same instincts: observe a practical problem in everyday life, design an elegant solution, and manufacture it efficiently enough to reach millions. Thulin was cut from the same cloth. He was not trying to build a luxury brand or a tech company; he was solving a problem for neighbors who wanted to go skiing with their families. The brand identity that would later command premium pricing around the world was, at its origin, rooted in Scandinavian practicality.

By the early 1980s, Thule had expanded into the United States—entering with surfboard carriers in 1983, with champion surfer Robby Naish as brand ambassador—and Japan, establishing itself as the default name in roof-mounted transport systems. The fishing trap company had become a car accessories company. Each new product followed the same pattern: identify an activity that required transporting gear by car, engineer a safe and elegant mounting solution, and sell it through outdoor specialty channels where the customer valued quality over price.

The Thulin family sold Thule to the Eldon Group in 1979, ending the founding family's era.

For the next two decades the business grew steadily but unspectacularly as part of a publicly listed Swedish conglomerate. It was a comfortable existence—reliable revenue, modest growth, no drama. But it was also a period of missed opportunity. The global outdoor recreation market was growing rapidly, driven by rising affluence, increasing leisure time, and the emergence of activities like mountain biking, kayaking, and snowboarding that required transporting large equipment. Thule had the brand and the engineering to dominate this expanding market, but as a division within a diversified conglomerate, it lacked the focus and investment to capitalize on its potential.

The real inflection point came in 1999, when the private equity firm EQT acquired Eldon and delisted it.

EQT recognized something the public markets had undervalued: Thule was not a "car parts" company. It was an "active life" company with enormous brand equity and a fragmented competitive landscape ripe for consolidation.

EQT sold Thule to UK-based Candover Investments in 2004 for EUR 465 million in a management buyout.

And this is where the story gets interesting. Candover looked at the global market for roof racks, bike carriers, cargo boxes, and related accessories, and saw dozens of small, regional players—each strong in their home market but lacking the scale to invest in global distribution, safety testing, or brand marketing. The strategy was textbook private equity: buy the platform, then bolt on acquisitions to create a category killer.

Under Candover's ownership from 2004 to 2007, Thule went on a debt-fueled acquisition binge that transformed the company.

König, a European snow chains manufacturer, was added in 2004. Omnistor, an RV products maker specializing in awnings and bike carriers for caravans, came in 2005 and was later rebranded under the Thule name. Sportworks, a US-based car rack company, broadened the North American footprint. Brink, a towbar manufacturer, was also absorbed during this period, adding a complementary product line. Case Logic, the electronic accessories company, rounded out the Candover-era deals.

By the time Candover sold to Nordic Capital's Fund VII in May 2007, Thule's turnover had more than tripled. Candover exited with a reported 2.5x return and an internal rate of return above 40 percent—a spectacular outcome that validated the roll-up thesis.

Nordic Capital, the next PE owner, continued the playbook but with a different emphasis.

Two transformative acquisitions landed in this era: Chariot Carriers in 2011 (which deserves its own deep analysis, which follows) and the Dutch child bike seat maker Yepp in 2016. But Nordic Capital also had to navigate something Candover never faced: the 2008 global financial crisis. The timing was brutal.

Thule carried significant acquisition debt from the roll-up binge. Consumer spending on discretionary outdoor gear collapsed almost overnight. Retailers slashed orders. By December 2008, the lending bank consortium had to take an equity stake in the company as part of a restructuring.

It was the closest Thule ever came to the abyss.

Nordic Capital demonstrated conviction in the darkest moment. By December 2010, with markets recovering, Nordic Capital acquired the remaining equity from the banks, taking full control again.

The restructuring had actually strengthened the business—weaker competitors had exited or shrunk during the crisis, and Thule emerged with even greater market share. The financial crisis, paradoxically, was one of the best things that ever happened to Thule's competitive position. Smaller rack and carrier companies that lacked the financial backing to survive the downturn either went bankrupt or sold out at distressed valuations, further consolidating the market around the Thule platform.

There is a broader lesson here for students of PE-driven roll-ups, and it is worth pausing to absorb it. The Candover-to-Nordic Capital transition illustrates how PE firms can play complementary roles in a company's evolution. Candover was the "builder"—fast, aggressive, focused on market share and revenue growth. Nordic Capital was the "optimizer"—more patient, focused on operational efficiency, debt management, and positioning the company for an eventual public listing. Each firm's skill set matched the phase of growth the company needed. Not every roll-up gets this sequencing right, and many fail precisely because the same aggressive acquisition pace that builds the platform becomes a liability when the economy turns. Thule survived because Nordic Capital knew when to shift from offense to defense.

The cumulative legacy of the PE era—spanning roughly 1999 to 2014—was transformative. Three successive buyout firms had each played a distinct role in building what Thule became. Through more than fifty acquisitions, Thule consolidated what had been a cottage industry of regional rack-and-carrier makers into a single global platform. But more importantly, the PE owners funded the infrastructure that would become Thule's long-term moat: the Thule Test Center in Hillerstorp, the "fit kit" database covering every major car model manufactured in the prior three decades, and a global distribution network that no new entrant could replicate without billions in investment and years of effort. The manufacturing footprint spanned Sweden, Belgium, Poland, and the United States—a geographic diversification that would later prove invaluable for managing currency risk and supply chain resilience. The PE "steroid" phase was over, but the muscles it built would last.

III. The M&A Playbook: Winners and Losers

Every acquisition-driven company has a portfolio of deals that range from brilliant to regrettable. Thule's M&A track record is instructive precisely because it contains both.

Three deals, in particular, tell the story of how Thule's strategy evolved—and where it stumbled. A fourth, more recent deal raises the stakes to a level the company has never faced as a public entity.

Case Logic: The Cautionary Tale

In May 2007, riding the momentum of the PE roll-up era, Thule acquired Case Logic, a Boulder, Colorado-based maker of bags and cases for consumer electronics. The company had roughly $140 million in annual sales, about 250 employees, and a strong brand in what was then a booming category: laptop bags, CD cases, and accessories for the newly mainstream portable electronics market.

The timing could not have been worse.

Thule paid for a business at the peak of the laptop bag cycle, just before two seismic shifts hit simultaneously. First, the Great Recession of 2008-2009 crushed consumer discretionary spending. Second, the iPad launched in 2010, and the subsequent tablet revolution eroded the traditional laptop bag market that was Case Logic's bread and butter. CD cases—once a meaningful revenue line—became irrelevant almost overnight as streaming music took hold.

It took nearly a decade to reposition Case Logic from "that company that makes CD wallets" to a modern tech accessories and travel bag brand. The product line had to be completely reimagined: sleek laptop sleeves, camera bags for the mirrorless photography boom, and travel backpacks that competed with the likes of Targus, Osprey, and Fjällräven. Case Logic survived, and it remains Thule's second brand today, but the acquisition was a lesson in the danger of buying into a consumer electronics cycle at the top. The multiples Thule likely paid for a $140 million revenue luggage-adjacent business in 2007 were rich by any standard—exit multiples for consumer bags and luggage were elevated across the board in that pre-crisis vintage.

The deeper lesson was strategic.

Case Logic taught Thule that brand extension works best when the new category shares the same "trust architecture" as the core. People trust Thule to keep their $5,000 bike safe at 130 kilometers per hour on the autobahn. That trust transfers naturally to child carriers and dog crates—other high-stakes, safety-critical categories. It transfers less naturally to laptop sleeves, where the purchasing decision is driven more by fashion and price than by engineering credibility. Case Logic works as a portfolio brand, but it was never going to be the growth engine that justified its acquisition price.

Chariot Carriers: The Home Run

If Case Logic was the cautionary tale, Chariot Carriers was the deal that changed Thule's destiny. It deserves a close examination because it established the template for everything that followed. In June 2011, Thule acquired Chariot Carriers, a Calgary, Canada-based company that was the world leader in multi-functional child carriers and bike trailers. Founded by brothers Dan and Chris Britton, Chariot had built a passionate following among active families who wanted a single product that could function as a jogging stroller, a bike trailer, a cross-country skiing pulk, and a hiking carrier—swapping attachments depending on the activity.

Chariot's annual turnover was roughly CAD 25 million, or about SEK 160 million at the time—a modest sum. The price was not publicly disclosed, but by all indications it was a reasonable multiple for a niche juvenile products company. What made the deal transformative was not the revenue Thule acquired; it was the insight it unlocked.

The Chariot acquisition proved a hypothesis that would define Thule's next decade.

If parents trust you with their most expensive sporting equipment, they will trust you with their most precious cargo—their children. The "trust halo" from roof racks and bike carriers extended seamlessly into the juvenile category. Active parents already knew the Thule brand, already associated it with safety and quality, and were willing to pay premium prices for a child carrier that met the same engineering standards as their bike mount. Thule rebranded the product line to "Thule Chariot" in 2013, and sales grew rapidly as the combined distribution network placed these premium strollers and trailers in outdoor retailers across North America and Europe.

From an investor's perspective, the brilliance of the Chariot deal was the valuation arbitrage. Traditional juvenile products companies—think Bugaboo, Cybex, or Stokke—were valued on toy/baby industry multiples, which tended to be moderate because the sector is perceived as cyclical and fashion-driven. But Thule was buying into a different slice of the juvenile market: the premium active-family segment, where purchasing decisions are driven by safety engineering and outdoor credibility rather than nursery aesthetics. This segment proved to be less cyclical, higher-margin, and more brand-loyal than the broader baby products market. Chariot, acquired at juvenile multiples, generated returns more consistent with premium outdoor-brand economics.

The Chariot playbook became the template for everything that followed in Thule's category expansion—including the eventual move into dog products and car seats. It also revealed something profound about how brand trust works in consumer markets: trust is not infinitely elastic, but it stretches much further than most brand managers assume—provided the new category shares the same "failure mode." When the consequence of product failure is physical harm (a bike falling off a rack, a child carrier collapsing), the same engineering credibility that justifies premium pricing in one category justifies it in the other. When the consequence of failure is merely inconvenience (a laptop sleeve that tears), the trust transfer is weaker. This insight—failure mode matching—became the implicit filter for every subsequent category expansion decision at Thule.

Tepui Outdoors: Riding the Overlanding Wave

In October 2018, Thule announced the acquisition of Tepui Outdoors, a California-based pioneer in the North American rooftop tent market, for $9.5 million. In dollar terms, this was a tiny deal. In strategic terms, it was a bet on a trend that was about to explode.

Rooftop tents—fabric and foam shelters that mount on top of a vehicle's roof rack and fold out into a sleeping platform—had been popular in Africa and Australia for decades but were just beginning to gain traction in North America and Europe. The "overlanding" movement, fueled by Instagram and YouTube, was transforming car camping from a budget activity into an aspirational lifestyle. Tepui was the category leader in North America, but it was a small, scrappy startup that lacked the manufacturing scale, safety testing infrastructure, and global distribution to capitalize on the trend.

Thule brought exactly what Tepui lacked.

Within two years of the acquisition, Thule had integrated Tepui's products into its global distribution network—4,700 retail points across 136 countries—run them through the Hillerstorp Test Center for quality and durability certification, and launched next-generation designs under the Thule brand. A standalone startup could never have scaled rooftop tents this fast. Thule's distribution muscle turned a niche product into a meaningful revenue contributor, and the COVID-19 pandemic of 2020-2021, which drove an unprecedented surge in outdoor recreation and "van life" culture, accelerated adoption beyond anyone's projections.

The COVID-19 pandemic of 2020-2021 supercharged the rooftop tent category in ways nobody anticipated. Campground reservations surged, "van life" content exploded across social media, and consumers who had never considered sleeping on top of their car suddenly found themselves browsing Thule Tepui models at REI. Revenue from rooftop tents spiked. Even after the pandemic normalization, the category has shown surprising stickiness as overlanding has transitioned from a niche pursuit to a mainstream outdoor activity with dedicated festivals, media outlets, and a rapidly growing accessories ecosystem.

What is notable about the Tepui deal is how it refined Thule's acquisition criteria. Unlike Case Logic, Tepui fit perfectly within the "trust architecture"—a rooftop tent is literally mounted on the same rack system as a Thule cargo box, and the safety stakes (sleeping two meters off the ground at a campsite) are intuitively high. Unlike Chariot, which was a proven product in a mature niche, Tepui was a bet on an emerging trend—but at $9.5 million, the downside was negligible while the upside was enormous. It was low-risk, high-optionality M&A at its finest.

And then, in late 2024, came the biggest deal of all. A deal that would test the limits of the acquisition playbook that Thule had spent fifteen years refining.

Quad Lock: The Billion-Dollar Bet

In December 2024, Thule completed the acquisition of Quad Lock, the Australian global market leader in performance phone mounts, for AUD 500 million—approximately SEK 3.6 billion. This was, by a wide margin, the largest acquisition in Thule's history, financed through a combination of cash, credit facilities (79 percent), and a modest new share issuance of 2.1 million shares at roughly SEK 351 per share (21 percent).

The numbers were compelling. Quad Lock brought approximately SEK 1.4 billion in annual revenue with EBITDA margins around 25 percent, implying a purchase price of roughly 10x trailing EBITDA. The business designs and sells premium phone mounting systems for bicycles, motorcycles, cars, and active use—products that sit squarely within Thule's "active life" positioning. In its first full quarter under Thule ownership (Q1 2025), Quad Lock delivered sales growth exceeding 20 percent while maintaining strong margins. It effectively doubled the size of Thule's "Bags & Mounts" segment from roughly 9 percent to roughly 18 percent of group sales.

The strategic logic follows the same playbook Thule has refined over two decades: acquire a brand-leading niche product with safety-critical attributes (a phone flying off a motorcycle mount at highway speed is a genuine hazard), integrate it into Thule's global distribution and testing infrastructure, and cross-sell to the existing customer base of active outdoor enthusiasts.

But the Quad Lock deal also introduced a new element to Thule's M&A strategy.

Significant financial leverage. The SEK 3.6 billion price tag was roughly equivalent to two years of the company's EBITDA—a level of acquisition debt that Thule had not carried since the PE era. The financing structure, with 79 percent funded through cash and credit facilities and 21 percent through new equity, reflected management's confidence in Quad Lock's cash flow generation. But it also meant that Thule's balance sheet, previously a fortress of conservative Swedish financial management, now carried meaningful acquisition debt that would need to be serviced through the integration period.

Whether Quad Lock ultimately proves to be a Chariot-level home run or a Case Logic-level overpay will depend on execution and whether the phone mount category remains durable as smartphones evolve. The early returns are encouraging, but the financial stakes are higher than anything Thule has bet on as a public company.

IV. The "Great Refinement" and the Modern Narrative

On November 26, 2014, Thule Group AB debuted on the Nasdaq Stockholm exchange at SEK 70 per share. After fifteen years of private equity ownership—three successive buyout firms, a financial crisis, a bank restructuring, and more than fifty acquisitions—the company was finally a public entity. Nordic Capital retained a significant stake initially but gradually sold down over subsequent years, eventually completing a full exit after a nine-year holding period. The IPO was not just a liquidity event for PE; it marked the beginning of a fundamentally different strategic era.

The PE years had been about accumulation—buying everything that moved in the roof rack, cargo carrier, and adjacent markets to build scale.

The public company years would be about subtraction. Management, led by CEO Magnus Welander, recognized that the post-IPO Thule needed a different story. Public investors do not reward conglomerates of loosely related businesses; they reward focused brand compounders with clear growth narratives and expanding margins. The task was to transform Thule from a PE-owned "roll-up" into a premium "brand compounder."

The tool management used was ruthless portfolio pruning, guided by an 80/20 logic that would have made Vilfredo Pareto proud. Welander and his team analyzed every product line and business unit, asking a simple question: does this strengthen the Thule brand, or does it dilute it? The answers were often uncomfortable. Snow chains, sold under the König brand acquired during the Candover era, were a perfectly fine business—but they had nothing to do with the "active life" positioning and competed in a commodity market where Thule's brand premium was irrelevant. Towbars were similar: functional, low-margin, undifferentiated. Private-label manufacturing—producing roof racks and accessories for other companies to sell under their own names—was the most insidious diluter of all, because it actively undermined Thule's pricing power by putting identical products on the market at lower price points.

One by one, these businesses were divested or wound down. The timeline tells the story of systematic discipline. The towbar business became Brink Group B.V. in 2014, returning to its historical name. The trailer business spun off as Brenderup Group the same year. König, the snow chains operation, was sold to Austrian company Schneketten AG in 2015. UWS, a work-gear brand, was sold in 2017. Private-label contracts were allowed to expire rather than renewed. Each divestiture was individually small, but the cumulative effect was dramatic. The portfolio that remained was leaner, more focused, and overwhelmingly branded under the Thule name—with Case Logic as the sole secondary brand, positioned in a complementary rather than competing segment.

The narrative shift that accompanied this pruning was equally deliberate. In fact, the narrative was arguably the more important transformation. Under PE ownership, Thule's story had been "the world's largest maker of car racks and accessories"—a positioning that anchored the brand in the parking lot, tied to the automotive cycle, and inherently limited by the number of cars on the road. Welander reframed the company as a premium lifestyle brand for active families and outdoor enthusiasts. The products were no longer "car accessories"; they were "solutions for bringing what you care about most on your next adventure." The Thule website, product photography, and marketing shifted from showing products mounted on cars in parking lots to showing families at trailheads, on beaches, and at mountain summits—with the products visible but secondary to the lifestyle.

This was not mere marketing spin.

The portfolio pruning and category expansion into juvenile products, luggage, backpacks, and camping gear gave the narrative real substance. By 2020, a meaningful share of Thule's revenue came from products that had nothing to do with cars—strollers, child bike seats, travel bags, and backpacks. The brand was literally walking away from the parking lot and into the front door of the consumer's home.

The financial results validated the strategy in terms that even skeptics could appreciate. From the 2014 IPO through the pre-COVID peak in 2021, Thule's EBIT margin expanded from the mid-teens to above 22 percent—a remarkable achievement for a company in the consumer durables space. Revenue grew steadily as the higher-margin branded products replaced the lower-margin private-label and commodity businesses that had been pruned. The stock became a compounder darling among Scandinavian and European quality-growth investors.

The 2022-2023 period brought a normalization that tested the faith of even committed shareholders. The pandemic-era surge in outdoor equipment spending had pulled forward demand, and the subsequent correction—combined with rising interest rates, inflation in raw materials, and destocking across retail channels—pushed EBIT margins back into the high-16 to 17 percent range. Revenue dipped from its 2021 peak of SEK 10.4 billion to SEK 9.1 billion in 2023. This was painful but not structural; the core brand strength, distribution moat, and category positions remained intact. It was a cyclical correction, not a strategic failure.

Consider what the pruning achieved in quantitative terms. At the time of the IPO, Thule operated multiple brands across loosely related categories, with a meaningful chunk of revenue coming from private-label manufacturing and commodity products where the Thule name added no value. By 2020, after six years of systematic divestiture and focus, virtually all revenue came from Thule-branded products (with Case Logic as the deliberate exception), the gross margin had expanded by several percentage points, and the return on invested capital had improved materially. The company was generating more profit on less revenue—the hallmark of successful strategic pruning.

The direct-to-consumer channel deserves mention as a developing subplot that may become a main plot in the years ahead. Historically, Thule sold almost exclusively through third-party retailers. But the rise of e-commerce—accelerated by the pandemic—opened a direct channel that Thule has been building steadily. The company's own website now features a full e-commerce experience in key markets, allowing consumers to configure rack systems, check fit compatibility, and order directly. This channel offers higher margins (no wholesale discount), richer customer data, and tighter brand control. It is still a small percentage of total revenue, but it is growing, and it aligns perfectly with the retail-first orientation of the new CEO.

The refinement era established the template that Thule operates under today.

It is a focused portfolio of premium branded products, organized around the "active life" theme, sold globally through specialty outdoor retailers, sporting goods chains, and an expanding direct-to-consumer channel. The company that went public in 2014 as a PE roll-up looks nothing like the company that exists in 2026—and that transformation is arguably the most important chapter in the Thule story.

V. Current Management: The Ankarberg Era

In the summer of 2023, after seventeen years at the helm, Magnus Welander stepped down as CEO. On August 9, 2023, Mattias Ankarberg officially assumed the role. It was a succession that mattered—not because Welander had failed (he had been the architect of virtually everything that made modern Thule valuable), but because the next phase of the company's evolution required a different skill set.

Welander was an engineer's CEO.

Trained in the Swedish industrial tradition, with prior experience at Tetra Pak and Envirotainer, he had joined Thule in 2006 during the Candover era and shepherded the company through the Nordic Capital years, the financial crisis restructuring, the IPO, the Great Refinement, and the initial category expansions into juvenile and camping products. His instinct was to lead with product—to invest in the Test Center, to obsess over crash-test ratings and aerodynamic drag coefficients, to let the engineering speak for itself. It worked brilliantly for the phase of building credibility in new categories. Thirty-five quarterly reports as a public company CEO, delivered with the steady hand of someone who understood manufacturing, safety testing, and the outdoor consumer deeply.

Ankarberg, born in 1976, represents a deliberate pivot toward the next challenge: scaling the brand as a retail and consumer operation. His background tells the story. After earning a Master of Science in Business from the Stockholm School of Economics and further studies at the Ivey Business School in Canada, Ankarberg spent eight years at McKinsey from 2001 to 2009, consulting on strategy in both Sweden and the United States. He then moved to H&M, the Swedish fast-fashion giant, where he held a series of increasingly senior roles over seven years—Global Head of Sales and Marketing, Global Head of Online, and Global Head of Store Development. These were operational, consumer-facing roles at one of the world's most scaled retail organizations.

After H&M, Ankarberg served as CEO of Byggmax Group, a Swedish home improvement retailer listed on Nasdaq Stockholm, from late 2016 through mid-2023. Byggmax operates in the value segment of DIY retail—a seemingly odd predecessor for a premium outdoor brand—but the experience gave Ankarberg deep expertise in retail operations, supply chain management, pricing strategy, and direct-to-consumer channel development. He had also served on Thule's board of directors since 2018, giving him five years of board-level visibility into the company's strategy and financials before stepping into the CEO chair.

The Ankarberg appointment signals where Thule's board believes the next wave of value creation lies.

It is not in inventing new product categories (though that continues) but in optimizing how existing products reach consumers. Direct-to-consumer sales, digital marketing, retail partnerships, pricing architecture, and global channel management—these are Ankarberg's domain. In a world where Thule's products are already best-in-class from an engineering standpoint, the marginal dollar of value creation increasingly comes from selling those products more effectively, not from making them incrementally better.

Think of it this way: Welander built the product engine.

Ankarberg's job is to build the go-to-market engine. The product development team in Hillerstorp continues to do what it has always done—obsess over crash tests, aerodynamics, and material science. But the commercial organization—pricing, channel strategy, digital marketing, retail partnerships, and the direct-to-consumer buildout—is where Ankarberg's McKinsey training, H&M operating experience, and Byggmax retail leadership converge. The Quad Lock acquisition, with its strong direct-to-consumer DNA, is particularly well-suited to Ankarberg's skill set. Integrating a primarily DTC brand into a primarily wholesale distribution model—while preserving the best of both—is exactly the kind of complex commercial challenge that his background prepared him for.

In terms of alignment, Ankarberg holds approximately 15,000 shares in Thule Group directly, plus significant warrant packages: 110,000 warrants in the 2023/2026 series, roughly 100,000 in the 2024/2027 series, and 110,000 in the 2025/2028 series. These rolling warrant programs ensure that the CEO's economic interests are tied to multi-year share price appreciation—the kind of incentive structure that "compounder" investors look for. The warrants vest over three-year horizons, discouraging short-term earnings management and encouraging investments that build long-term brand equity and competitive position.

The cultural backdrop is important too.

Thule's headquarters are in Malmö, Sweden's third-largest city—a pleasant but decidedly unglamorous choice compared to Stockholm, London, or New York. The product development and testing center remains in Hillerstorp, the village where Erik Thulin first made fishing traps. There is a Swedish concept called "lagom"—roughly translated as "just the right amount"—that permeates the corporate culture. No corner offices, no flashy perks, no Manhattan lease. Management meetings happen in functional Swedish offices, and the company's annual report photography features real products in real outdoor settings rather than corporate lifestyle imagery. This is a company that spends its money on crash-test rigs and wind tunnels, not on employer branding.

At the 2025 Capital Markets Day, Ankarberg and his team updated Thule's long-term financial targets, sending a clear signal about the company's ambitions. The organic revenue growth target was raised to 7 percent or higher annually—up from the roughly 5 percent average achieved since the 2014 IPO—reflecting confidence in the newer categories and the Quad Lock addition. The EBIT margin target remains 20 percent, and the dividend payout ratio target sits at or above 75 percent of net income. For a company that paid SEK 8.30 per share in its most recent dividend, these targets imply a trajectory of steady, compounding returns to shareholders—exactly the profile that attracts the long-duration institutional capital that dominates Thule's shareholder register.

Speaking of that register: Thule's ownership structure is notable for what it lacks. There is no overhang from a PE sponsor preparing to sell. There is no activist waiting to pounce. There is no controlling family, no PE anchor, no strategic investor with a blocking stake. The free float is approximately 99.8 percent, and the four largest shareholders—AMF Tjänstepension, Handelsbanken Fonder, Swedbank Robur Fonder, and Alecta—are all Swedish pension and mutual fund managers. This is an investor base that thinks in decades, not quarters, and it gives management the latitude to invest through cyclical downturns without activist pressure to cut costs for short-term earnings.

VI. Segment Deep-Dive: The "Hidden" Growth Engines

To understand where Thule's value creation comes from—and where it is heading—requires a granular look at the company's product segments. The numbers tell a story of deliberate transformation. The narrative has evolved from a single-product company to a multi-category platform, and the relative importance of each segment is shifting rapidly.

Sport and Cargo Carriers: The Cash Cow

This is the original Thule. Roof racks, cargo boxes, bike carriers, ski racks, water sport carriers, and the associated "fit kits" that customize each mounting system for a specific car model. Historically representing about 60 percent of sales, this segment's share has been gradually declining—not because it is shrinking, but because the newer categories are growing faster. Following the Quad Lock acquisition and the expansion of "Bags & Mounts," Sport and Cargo now represents closer to 50 percent of group revenue.

The competitive moat in this segment is formidable, and it is worth understanding in detail because it is the foundation upon which everything else rests. The "fit kit" database deserves particular attention because it is one of those assets that sounds mundane but is nearly impossible to replicate. Every car model has a different roof profile—different dimensions, different weight tolerances, different attachment points. Thule has spent decades measuring and cataloging the exact specifications for virtually every passenger vehicle manufactured in the last thirty years. When a consumer walks into an outdoor retailer and says "I need a roof rack for my 2024 Volvo XC60," the retailer pulls up the Thule fit guide and selects the exact components. A competitor starting from scratch would need decades and millions of dollars in engineering work to build a comparable library—and during that time, new car models would keep launching, requiring continuous investment to stay current.

The switching costs compound the advantage.

Once a consumer has invested in a Thule rack system—a base rack plus foot pack can easily cost $400 to $600—they are economically and psychologically locked into the Thule ecosystem for accessories. The bike carrier, ski rack, cargo box, and kayak carrier all attach to the same base system. Switching to Yakima or another competitor means replacing the entire setup, not just adding an accessory. This is a classic "razor and blades" dynamic, except that the "razor" (the base rack) is itself a high-margin product.

The electric vehicle transition adds an interesting wrinkle to the Sport and Cargo story, and it is one that deserves honest assessment. On one hand, EVs create a potential headwind: many EV owners are sensitive to aerodynamic drag (which reduces range), and some newer EV designs lack traditional roof rails. On the other hand, EVs create an opportunity: Thule has been developing low-drag, EV-optimized cargo solutions that minimize range impact, and the company's fit kit engineering capability allows it to design mounting solutions for even the most unconventional roof geometries. Tesla owners, Rivian owners, and Volvo EX90 owners are precisely the demographic that buys premium outdoor accessories—affluent, active, environmentally conscious. The EV transition is not the existential threat to Thule's core business that some bears assume; it is a product redesign challenge that Thule's R&D capabilities are well-positioned to address.

The segment faces a legitimate long-term question about car ownership trends more broadly. This is the elephant in the room for any Thule investor. If urbanization and ride-sharing reduce the number of privately owned vehicles, the addressable market for car-mounted accessories shrinks. This is the central bear case for Thule, and it deserves serious analysis (which follows in the bear/bull section). But for now, the segment continues to generate strong cash flows, and the barriers to entry remain as high as ever.

Active with Kids and Dogs: The Hidden Gem

This is where the Thule story gets truly exciting for growth investors. The numbers are still modest, but the trajectory is steep. What began with the 2011 Chariot Carriers acquisition has evolved into a full-fledged juvenile and pet products platform—renamed "Active with Kids & Dogs" in 2024 to signal the breadth of ambition.

The juvenile product line now spans multi-sport child carriers (the descendant of Chariot's original product), child bike seats (bolstered by the 2016 acquisition of Dutch brand Yepp), jogging strollers, and—in the most significant category expansion—car seats. Yes, Thule is now competing in the global premium car seat market, one of the largest addressable markets in the entire juvenile products industry. The company has invested heavily in R&D and crash-testing infrastructure to enter this category, and if it captures even a low-single-digit market share of the global premium car seat segment, the revenue impact would be material.

The pet products initiative, launched in January 2024, is the newest frontier—and perhaps the most counterintuitive extension of the brand. The flagship product is the Thule Allax dog crate—a crash-tested, safety-engineered transport crate for dogs, available in ten sizes, designed with a crumple zone and an emergency escape hatch. Later in 2024, the Thule Bexey dog bike trailer followed, allowing cyclists to bring their dogs along for the ride. The company has described the dog transport category as having a "record-breaking start."

The strategic logic is the same "trust halo" that worked with juvenile products, extended one step further. And the math is compelling. If active families trust Thule with their children, they will trust Thule with their dogs. The pet travel market is large, growing, and—critically—underserved at the premium end. Most pet transport products are cheaply made, untested for crash safety, and sold through commodity channels. Thule is applying automotive-grade crash testing to dog crates, the same way it applies it to child carriers. The result is a product that justifies a significant price premium because it offers something no competitor does: verified safety performance.

To understand the scale of the opportunity, consider the car seat market specifically. This is where the numbers become genuinely exciting. The global child car seat market is a multi-billion-dollar industry dominated by established players like Britax-Römer, Cybex (owned by Goodbaby International), Maxi-Cosi (owned by Dorel), and Nuna. These are formidable competitors with decades of experience and deep relationships with baby specialty retailers. Thule is not going to displace them overnight. But Thule does not need to. The company is targeting a specific slice of the market: the premium, safety-obsessed, active-family segment that is already buying Thule strollers and child carriers. If Thule captures even 3 to 5 percent of the global premium car seat market, the incremental revenue—potentially hundreds of millions of SEK—would be material relative to the company's current scale. And because the R&D infrastructure (crash testing, safety certification) already exists in Hillerstorp, the incremental investment required to enter the category is far lower than what a new entrant would face.

What makes this segment a "hidden gem" from an investor perspective is the margin profile, which is structurally superior to the core Sport & Cargo business. Juvenile and pet products command higher gross margins than roof racks because the competitive set includes fashion-driven brands like Bugaboo and Stokke that have conditioned consumers to pay $800 to $1,500 for a stroller. Thule competes at similar price points but with a fundamentally different value proposition—engineering credibility and multi-sport versatility rather than nursery aesthetics. The customer acquisition cost is also lower because Thule already has a relationship with the active-family demographic through its core outdoor products. Cross-selling a stroller to someone who already owns a Thule bike carrier is far cheaper than acquiring that customer from scratch.

Bags and Mounts: The Quad Lock Effect

This segment was historically a modest contributor—almost an afterthought in the Thule story—built primarily around the Case Logic brand's laptop bags, camera cases, and travel accessories. The December 2024 acquisition of Quad Lock transformed it overnight. With Quad Lock's SEK 1.4 billion in revenue and 25 percent EBITDA margins, Bags & Mounts roughly doubled in size to approximately 18 percent of group sales.

Quad Lock's product is conceptually simple—a proprietary mounting system that securely attaches a smartphone to a bicycle handlebar, motorcycle mount, car dashboard, or armband.

But the execution is technically demanding. The mount must hold a $1,000+ smartphone stable and secure during vibration, rain, extreme temperatures, and the forces of a crash. This is another "trust architecture" product: the consequences of failure (a shattered phone, a distracted cyclist, a motorcycle accident) are severe enough to justify premium pricing and brand loyalty.

The early integration results have been encouraging.

Quad Lock posted 20-plus percent sales growth in its first full quarter under Thule ownership. The cross-selling opportunity is immediately apparent.

Every cyclist who owns a Thule bike carrier is a natural customer for a Quad Lock phone mount, and vice versa. The distribution leverage—taking a product that was primarily sold direct-to-consumer in Australia and plugging it into 4,700 global retail points—is a repeat of the Tepui playbook at much larger scale.

RV Products: Sticky After COVID

Thule's RV segment—awnings, bike carriers, and accessories for caravans and motorhomes—represents about 18 percent of group revenue.

It was a COVID-era winner that has shown surprising durability. The "van life" movement, initially dismissed as a pandemic fad, has proved to be a genuine demographic shift. What started as Instagram-driven aspiration has matured into a permanent leisure category. Younger consumers are choosing experiential travel over traditional vacations, and the European caravan market, while cyclically soft in 2023-2024, has a long structural tailwind from aging populations with disposable income and time.

Thule's RV products benefit from OEM relationships with major caravan and motorhome manufacturers.

These manufacturers specify Thule awnings and carriers as factory-installed equipment. Once embedded in the OEM supply chain, switching costs are high—manufacturers must recertify alternative products for safety and fit, which is costly and time-consuming. New product launches in 2024 and 2025, including the Thule Subsola, VeloTrack, VeloSwing, Outset, and Sidehill, have kept the pipeline fresh even in a weak overall market.

The RV segment also illustrates one of Thule's less-discussed advantages.

It is the ability to ride demographic waves without over-committing to any single trend. When "van life" was at peak hype in 2020-2021, Thule had the products to capture the demand. When the trend normalized, Thule's diversified portfolio ensured that the RV segment's softness was offset by strength elsewhere. This optionality—being positioned to benefit from trends without being dependent on them—is a structural advantage of the multi-category platform that Thule has built.

It is also a key difference between the Thule of 2026 and the Thule of 2006, when the business was overwhelmingly dependent on a single product category tied to a single vehicle trend.

VII. Competitive Moats: 7 Powers and Porter's 5 Forces

To assess Thule's durability as an investment, it helps to apply two rigorous competitive analysis frameworks.

Hamilton Helmer's 7 Powers asks what structural advantages allow persistent excess returns. Michael Porter's 5 Forces maps the competitive dynamics of the industry. Together, they paint a comprehensive picture of Thule's strategic position.

Hamilton Helmer's 7 Powers

The 7 Powers framework asks: what structural advantage allows a company to persistently earn returns above its cost of capital?

In Thule's case, three of the seven powers are clearly present, with a fourth emerging.

Brand Power is Thule's primary moat.

In the roof rack and cargo carrier market, Thule is not just a brand—it is the category. The logo on a roof box functions as a status symbol among the "outdoor elite," signaling that the owner is serious about their outdoor pursuits and willing to invest in quality. This brand power translates directly into pricing power: Thule's products typically command a 30 to 50 percent premium over comparable products from Yakima, Kuat, or unbranded alternatives. Consumers pay the premium not because the products are marginally better in some measurable dimension, but because the brand carries a guarantee of safety, durability, and aesthetic coherence that cheaper alternatives cannot match. This is the hallmark of true brand power—pricing above commodity levels that persists over time because the brand itself is the product.

Cornered Resource is the fit kit database—an asset that sounds mundane but is strategically invaluable. As discussed earlier, Thule possesses the exact measurements, weight tolerances, and mounting specifications for virtually every passenger vehicle produced in the last three decades. This is not intellectual property in the traditional patent sense—it is an accumulated, proprietary dataset built through decades of painstaking measurement and testing. A competitor could theoretically replicate it, but the cost in time and engineering hours would be prohibitive, and the database requires continuous maintenance as new car models launch every year. It is a "cornered resource" in Helmer's framework because it took decades to build, it is essential for competing in the rack market, and there is no shortcut to acquiring it.

Switching Costs operate at both the consumer and retail levels, creating a dual lock-in effect. Consumers who have invested in a Thule base rack system face significant switching costs to move to a competitor—they would need to replace not just the base rack but all associated accessories. At the retail level, outdoor specialty stores have invested in Thule display systems, trained staff on Thule fit guides, and built their car-rack business around Thule's product architecture. Switching to a competitor's system would require re-training, new displays, and a period of customer confusion.

Process Power is the emerging fourth advantage, and it may be the most durable of all. The Thule Test Center in Hillerstorp, expanded with a SEK 100 million investment completed in 2021, represents an institutionalized process for safety testing, quality certification, and product development that competitors cannot easily replicate. Thule crash-tests its child carriers, dog crates, and bike mounts to standards that exceed regulatory requirements—and then markets the results. This process turns R&D spending (approximately 7 percent of sales in 2024, roughly double the industry average for "utility" competitors) into a durable competitive advantage. The test center is not just a cost center; it is a moat-building machine.

Porter's 5 Forces

Threat of New Entrants: Low.

The barriers to entering Thule's core markets are formidable. Consider what a credible new entrant would require.

They would need to build a fit kit database (decades of work), establish OEM relationships with automakers (years of negotiation and certification), invest in safety testing infrastructure (tens of millions of dollars), build a global distribution network (4,700+ retail points), and overcome the brand premium that Thule commands. The total investment required to credibly compete across Thule's product range would likely exceed a billion dollars—and even then, the new entrant would face a dominant incumbent with thirty-plus years of consumer trust. In adjacent categories like juvenile products, regulatory barriers add another layer: car seats and child carriers must meet stringent safety certifications in each geography, and the testing and certification process itself requires specialized infrastructure.

Bargaining Power of Suppliers: Moderate.

Thule's products are manufactured from steel, aluminum, plastics, and fabrics—commodity inputs that are available from multiple sources. The company is large enough to negotiate favorable terms but not so dominant that it can dictate pricing to raw material suppliers. Currency exposure (Thule manufactures in Sweden, Belgium, Poland, and the US but sells globally) introduces a secondary supply-cost variable that management hedges actively.

Bargaining Power of Buyers: Low.

This is one of Thule's most underappreciated advantages. Because consumers demand the Thule brand by name, retailers like REI, Backcountry, Biltema, and Decathlon have limited ability to push back on Thule's wholesale pricing. A retailer that dropped Thule would lose a significant share of its car-rack and outdoor-transport business, because customers would simply go to a competitor that carries the brand. This consumer "pull" dynamic gives Thule pricing power throughout the channel, which is a rarity in consumer durables.

Threat of Substitutes: Mixed.

For technical, safety-critical products—roof racks, bike carriers, child carriers, car seats—the threat of substitutes is low. A cheap, untested roof rack that fails at highway speed is not merely an inconvenience; it is a safety hazard. Consumers understand this, and the premium for tested, certified products is well-established. However, in the luggage and bags segment (Case Logic), substitutes are abundant and the competitive landscape is far more fragmented, with lower barriers to entry and more price sensitivity. The Quad Lock phone mount category falls somewhere in between—there are cheap alternatives, but the consequences of failure are severe enough to support premium pricing.

Competitive Rivalry: Moderate.

In the core rack and carrier market, Thule's primary competitor is Yakima (strong in North America, growing in Europe), with secondary competition from regional players like Kuat (US bike racks), Atera and Uebler (German bike racks), Kamei and Hapro (European roof boxes), and Rhino Racks (Australia/New Zealand, focused on tradesmen). In Japan, Inno competes as part of a larger industrial group. The rivalry is real but manageable because Thule's scale advantages—distribution, R&D, brand, fit kits—create a wide gap between the number one and number two positions. In juvenile products, the competitive set is different (Bugaboo, Cybex, Britax-Römer, Croozer, Burley) and more fragmented, but Thule's unique positioning at the intersection of outdoor credibility and juvenile safety gives it a differentiated lane. In luggage and bags, competitors include Targus, Samsonite/TUMI, Osprey, Deuter, and Fjällräven—a crowded space where Case Logic competes on design and price rather than engineering differentiation. In RV products, Fiamma is the primary competitor, with Dometic (another Swedish listed company) playing a more limited role.

One final observation on competitive dynamics deserves emphasis.

Thule benefits from what might be called "competitive fragmentation by segment." No single competitor challenges Thule across all of its categories. Yakima is a threat in racks but does not make strollers. Bugaboo is a threat in strollers but does not make bike carriers. Fiamma competes in RV but not in cargo boxes. This means Thule can leverage its platform—shared distribution, shared brand, shared testing infrastructure—against opponents who are fighting category by category. It is the advantage of being a diversified platform competing against specialists, provided (and this is the critical proviso) that the platform's categories are genuinely connected by a shared brand promise rather than merely collected under a corporate umbrella.

VIII. The Bear vs. Bull Case

The Bear Case: Peak Car and Diworsification

The strongest bear argument against Thule is structural, not cyclical.

What happens to a company built on car-mounted accessories if the world starts owning fewer cars? Urbanization is accelerating globally. Ride-sharing services are expanding. Autonomous vehicles could reduce private car ownership in dense cities. Electric vehicles, with their flat roofs and aerodynamic sensitivities, may discourage roof-mounted accessories. If Thule's core "attachment" business—the segment that still represents about half of revenue—faces a secular decline in its addressable market, the entire investment thesis is at risk.

The counterargument is worth taking seriously. Thule's target customer is not the urban apartment dweller who uses Uber; it is the suburban or exurban family with two vehicles, a garage, and a weekend outdoor habit. This demographic is large, growing (especially in the US, Scandinavia, and parts of Asia-Pacific), and arguably the last to give up private car ownership. But the bear would note that "the last to give up" is still "giving up eventually," and a ten-to-twenty-year investment horizon must account for structural shifts in mobility.

The second bear argument is diworsification—a term coined by Peter Lynch to describe companies that diversify into unrelated businesses, destroying value in the process. Thule started as a razor-focused roof rack company.

Now it makes strollers, dog crates, phone mounts, luggage, rooftop tents, and RV awnings. Is this disciplined brand extension, or is it a classic case of a management team chasing growth by wandering into adjacent markets where the core competitive advantages do not apply? The Case Logic acquisition is exhibit A for the prosecution: a deal that looked smart on paper but landed in a category where Thule's engineering credibility provided little differentiation.

The Quad Lock acquisition, at SEK 3.6 billion, raises the stakes on this question dramatically. Phone mounts are certainly "active life" products, but the competitive moat is narrower than in roof racks or child carriers. This is a legitimate concern.

The barriers to entry are lower. There is no fit kit database, no car-specific engineering, no regulatory safety certifications. And the market is more susceptible to disruption from smartphone manufacturers who could integrate mounting solutions directly into their devices. If Quad Lock turns out to be a Case Logic-scale misstep at five times the price, it would significantly impair Thule's returns on invested capital.

A side note on balance sheet risk: goodwill and intangible assets on Thule's balance sheet now stand at SEK 7.8 billion—representing 57 percent of total assets. This is overwhelmingly driven by the cumulative acquisition history. While the underlying businesses are performing, investors should note that any significant impairment of goodwill would directly reduce reported equity. The net debt to EBITDA ratio of approximately 2.5 times, elevated by the Quad Lock financing, adds a layer of financial risk that the company has not carried as a public entity. Deleveraging over the next two to three years will be closely watched.

Finally, the bears point to the margin trajectory. Thule's EBIT margin peaked above 22 percent in 2021, during the pandemic outdoor spending boom, and has since compressed to the 16-17 percent range. Management targets 20 percent, but the gap between current performance and target is meaningful. Integration costs from Quad Lock, continued investment in new categories (dog products, car seats), and a mixed macroeconomic environment for consumer discretionary spending all create headwinds.

The Bull Case: The LVMH of the Outdoors

The bull case starts with a simple observation.

Thule is one of the very few consumer brands in the world that has successfully ported trust from one high-stakes category to another, repeatedly, over decades. Roof racks to bike carriers to child carriers to dog crates to car seats—each extension felt risky at the time and proved accretive in hindsight. The "trust halo" is not just a marketing concept; it is a demonstrated capability that has generated real revenue and real margins across multiple categories.

The "LVMH of the Outdoors" analogy is instructive, and worth unpacking. LVMH took luxury brands with narrow original niches (Louis Vuitton in trunks, Dior in couture, Hennessy in cognac) and built a platform that extended each brand's equity into adjacent luxury categories—handbags, perfume, watches, wine. Thule is doing something similar in the "premium active lifestyle" space: taking brand equity built in car-mounted transport and extending it into every product category that active families need. The total addressable market for "things that help active families transport what they care about" is vastly larger than the total addressable market for "roof racks."

The juvenile market alone represents a massive expansion opportunity, and the numbers are striking. The global premium stroller market, the premium car seat market, and the premium child carrier market collectively represent tens of billions of dollars in annual spending. Thule currently has a small but rapidly growing share of this market, and its differentiated positioning—engineering-led safety for active families—gives it a lane that does not directly compete with the incumbent juvenile brands on their home turf. Thule is not trying to out-design Bugaboo in nursery aesthetics; it is offering something Bugaboo cannot—a stroller that converts to a bike trailer that converts to a jogging stroller, all crash-tested to automotive standards.

The pet market adds another dimension entirely. The premium pet travel segment is growing rapidly as pet ownership and "pet humanization" trends accelerate globally. The global pet industry now exceeds $300 billion annually, and the intersection of pet travel and active lifestyles—exactly where Thule's new dog crates and bike trailers sit—is one of the fastest-growing subsegments. Thule's description of its dog transport launch as having a "record-breaking start" suggests the early market reception validates the thesis.

The 2024 recognition as Red Dot Design Team of the Year, alongside twelve iF Design Awards including a Gold for the Thule Urban Glide 3 stroller, underscores the point. These are not vanity awards. They are signals to distributors, retail partners, and consumers that Thule's products meet the highest standards of both engineering and aesthetics—a combination that justifies premium pricing.

The bulls also point to the R&D moat. At approximately 7 percent of sales, Thule's R&D spend is roughly double that of its nearest "utility" competitors and comparable to premium consumer brands in other categories. This spending funds the Thule Test Center, the fit kit database, and the continuous product innovation that justifies premium pricing. The SEK 100 million expansion of the Test Center, completed in 2021, was not a one-time event; it was an investment in a permanent, institutionalized advantage that compounds over time as the facility develops testing capabilities for new categories.

The bulls also highlight the geographic expansion opportunity, which is perhaps the least discussed but most significant optionality in the Thule story. Thule's revenue is heavily weighted toward Europe and North America—its traditional strongholds. Asia-Pacific, despite being the world's largest and fastest-growing market for outdoor recreation, premium consumer goods, and increasingly, suburban car ownership, represents a relatively small share of Thule's sales. China, South Korea, Japan, and Australia all have large, affluent, outdoors-oriented consumer populations that are under-penetrated by the Thule brand. The Quad Lock acquisition, with its strong Australian base and growing Asian distribution, provides a beachhead for accelerated expansion in the region. If Thule can replicate even a fraction of its European and North American success in Asia-Pacific over the next decade, the revenue upside is significant.

Finally, the ownership structure supports the bull case in ways that are easy to overlook. With nearly 100 percent free float and a shareholder register dominated by long-duration Swedish institutional investors, Thule's management has the luxury of investing for the long term without short-term activist pressure. The updated financial targets—7 percent organic revenue growth with 20 percent EBIT margins and a 75 percent-plus dividend payout—describe a capital allocation framework that balances growth investment with shareholder returns. If executed, this framework would compound shareholder value at attractive rates for the foreseeable future.

There is also a valuation argument worth noting, though it requires careful qualification. As of early April 2026, Thule's share price has pulled back from its 52-week high of roughly SEK 299 to around SEK 227—a correction of about 24 percent that reflects the broader consumer discretionary selloff and concerns about the Quad Lock integration timeline. For long-term investors, this creates a potential entry point into a business with demonstrable competitive advantages, a proven brand-extension playbook, and multiple category growth drivers. The margin recovery from 17 percent to the 20 percent target, if achieved, would alone generate significant earnings expansion even on flat revenue—and revenue is unlikely to be flat given the new categories ramping up.

IX. Playbook: Business and Investing Lessons

Three strategic lessons emerge from the Thule story that have broad applicability for investors evaluating other companies. Each is deceptively simple to state but extraordinarily difficult to execute.

The "Trust Halo" as a Growth Strategy

Thule's most replicable insight is that trust earned in one high-stakes category can be ported to adjacent high-stakes categories—if the brand's core promise is genuinely relevant in the new domain.

The core promise, in Thule's case, is safety, durability, and engineering excellence. The key word is "high-stakes." Trust transfers when failure has serious consequences: a bike falling off a car rack at highway speed, a child carrier collapsing during a jog, a dog crate failing in a crash. Trust does not transfer as effectively into low-stakes categories where the consequences of failure are merely inconvenient (a laptop sleeve that wears out, a luggage zipper that sticks). This explains why Chariot was a home run and Case Logic was not, and it provides a framework for evaluating future category extensions. Investors should ask: would a product failure in the new category cause genuine harm, or merely annoyance? If harm, the trust halo applies. If annoyance, competitive differentiation must come from somewhere else.

R&D as a Moat, Not a Cost

Most consumer durables companies treat R&D as a cost to be minimized. Thule treats it as a moat to be maximized.

The difference is philosophical but has enormous economic consequences. At 7 percent of sales—SEK 671 million in FY2024—Thule's R&D spending is roughly double the industry norm—an expense that depresses short-term margins but creates the safety certifications, fit kit data, and product innovations that justify premium pricing and customer loyalty over the long term. The Thule Test Center is not a laboratory that produces patents (Thule has relatively few patents in the traditional sense); it produces trust. The crash-test videos, the safety certifications, the "Thule Test Program" stamp on every product—these are the outputs of R&D spending, and they are worth far more than patents because they speak directly to the consumer's purchasing decision in a way that patent filings never could. For investors, the lesson is to look past the income statement impact of R&D spending and ask: what is this spending producing in terms of competitive position, pricing power, and customer loyalty?

The "Swedish Premium" Aesthetic

Thule's success in commanding premium pricing is inseparable from its Swedish identity. This is not merely a marketing overlay; it is a structural competitive advantage rooted in genuine national culture. Sweden has a global reputation for design excellence (IKEA, Volvo, Spotify, H&M, Acne Studios), engineering quality (Saab, Ericsson, Atlas Copco), and a particular aesthetic sensibility that balances form with function. Thule leverages this national brand equity relentlessly. Its products are clean-lined, minimalist, and functional—design choices that signal quality without ostentation. The color palette is muted (blacks, grays, dark blues), the materials are premium, and the packaging is understated. This is the opposite of the American approach to outdoor gear (loud colors, aggressive branding, feature overload) and the opposite of the Chinese approach to manufacturing (low cost, high volume, minimal design). The "Swedish Premium" occupies a unique position in the consumer's mind: serious, trustworthy, quietly excellent. For companies in other categories seeking to escape the commodity trap, Thule's playbook suggests that a strong national design identity, consistently applied, can justify pricing power that pure engineering specs cannot.

The KPIs That Matter

For investors tracking Thule's ongoing performance, two metrics cut through the noise. These are the KPIs that matter above all others.

First, organic revenue growth by segment—particularly in the "Active with Kids & Dogs" and "Bags & Mounts" categories. These are the businesses that determine Thule's future trajectory. These are the growth engines that will determine whether Thule successfully decouples from the automotive cycle. If juvenile, pet, and phone mount revenue grows at double-digit rates while Sport & Cargo grows at low-to-mid-single-digits, the bull thesis is playing out. If the growth categories stall, the "diworsification" bear argument gains weight.

Second, EBIT margin trajectory. This is the financial signal that tells the full story of operational execution.

Management has publicly and repeatedly committed to 20 percent EBIT margins, which would represent a recovery from the current high-16 to 17 percent range and approach the 22-plus percent peak achieved in 2021. The path to 20 percent depends on several factors: operating leverage as revenue grows, margin accretion from higher-margin juvenile and pet products, successful Quad Lock integration, and disciplined cost management.

Each of these factors is within management's control, which is itself a positive signal. Quarterly progress toward this target—or lack thereof—is the single best indicator of whether Thule's strategic vision is translating into financial reality.

X. Epilogue: The Most Ambitious Product Cycle in Company History

In the spring of 2026, Thule Group stands at a remarkable inflection point. Eighty-four years after Erik Thulin crafted a pike fishing trap in a Småland workshop, his company is entering the most ambitious product cycle in its history. The 2024-2026 product launch cycle is the most ambitious in the company's eighty-four-year history. The company described 2024 as the year it "launched more new products than ever before," and 2025 built on that momentum.

Crash-tested dog crates and dog bike trailers have opened an entirely new market. Car seats are expanding the juvenile platform into one of the largest addressable categories in consumer durables. Quad Lock has added a high-growth, high-margin digital-active category that doubles the Bags & Mounts segment. New RV products continue to refresh the most durable legacy of the COVID outdoor boom. And the core roof rack and cargo carrier business—the franchise that started with Erik Thulin's fishing trap in a Småland workshop—continues to generate cash flows protected by three decades of accumulated fit-kit data and a brand that has become synonymous with its category.

The FY2025 results tell a company in transition. Revenue reached SEK 10.4 billion, with gross margins expanding to 46 percent—a meaningful improvement from the 41 percent recorded just two years earlier. Organic growth was modestly negative at minus 1.3 percent, reflecting continued softness in some legacy categories, but acquisition-driven growth of 15.4 percent from Quad Lock more than compensated. The company proposed a dividend of SEK 8.30 per share, implying a yield of roughly 3.7 percent at current prices—a meaningful cash return while the growth investments mature.

Step back and consider the arc of this story. In 1942, a man in a tiny Swedish village made a fishing trap. In 1962, his company made its first ski rack. In 2004, private equity turned it into a global platform. In 2014, the public markets got access to it. In 2024, it acquired a phone mount company for half a billion Australian dollars. Each chapter would have seemed improbable from the vantage point of the previous one. A fishing trap maker becoming a roof rack company. A roof rack company becoming a child carrier brand. A child carrier brand acquiring a phone mount company for half a billion dollars. And yet each chapter followed logically from the same core insight: people who live active lives need reliable, well-designed products to bring what they care about with them. The specific products change—from fishing traps to ski racks to bike carriers to strollers to dog crates to phone mounts—but the underlying human need is permanent.

Whether Thule achieves its stated ambition of 7 percent organic growth and 20 percent EBIT margins depends on execution in the next three to five years. The strategy is clear. The talent is in place. The question is whether the world cooperates. The strategic vision is clear, the management incentives are aligned, the shareholder base is patient, and the competitive moats are deep. But the risks are equally real: the macro environment for consumer discretionary spending remains uncertain, the Quad Lock integration must deliver on its promise, and the secular trends in car ownership will eventually test the resilience of the core business. The company's balance sheet, loaded with acquisition debt for the first time since the PE era, adds a layer of financial risk that did not exist two years ago.

What is not in doubt is Thule's status as one of the most compelling "hidden in plain sight" stories in European public markets. It is a company that most consumers interact with without thinking about—the brand on the roof box they see in every parking lot, at every trailhead, on every highway. And yet that ubiquity is precisely the source of its power. Thule has spent eighty-four years earning the trust of active families around the world, one roof rack at a time.

The question for the next chapter is whether that trust can carry the brand far beyond the roof of the car—into strollers, dog crates, phone mounts, and categories not yet imagined.

The early evidence suggests it can. But the definitive answer lies in the execution of the next three to five years, as Ankarberg's retail-first vision meets the reality of a competitive global consumer market. The products are in the pipeline. The test center is expanding. The shareholder base is patient. And somewhere, on a highway in Sweden or a trail in Colorado or a campsite in New South Wales, another family is loading up their car, reaching for the product with the familiar logo, and trusting it with what matters most.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube