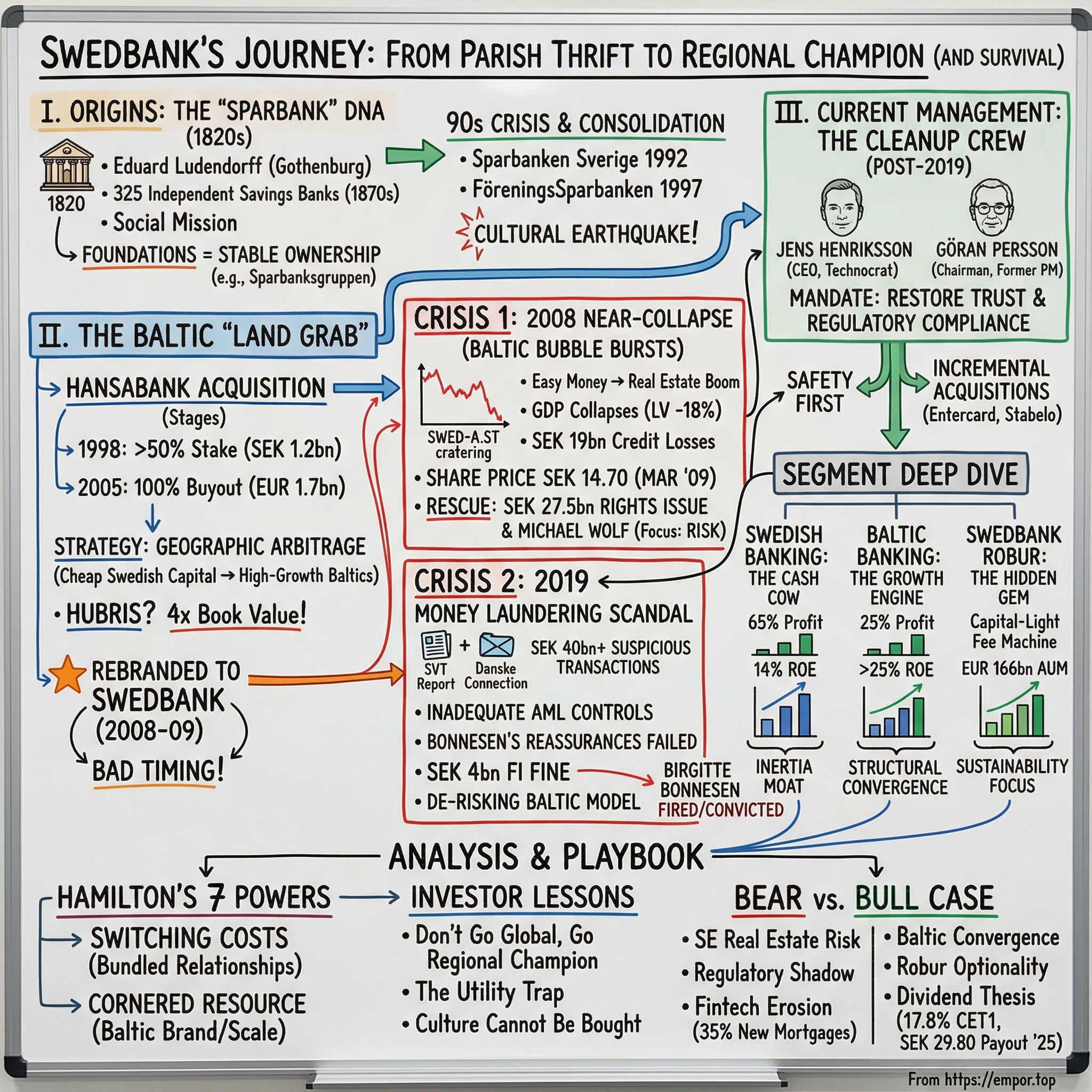

Swedbank: The Savings Bank That Conquered the Baltics (and Survived Itself)

I. Introduction: The "Everyman's" Bank

In the winter of 2009, Swedbank's share price touched SEK 14.70. Ninety percent of the bank's market value had evaporated in eighteen months. The culprit was a massive, leveraged bet on three tiny countries most Western investors couldn't find on a map: Estonia, Latvia, and Lithuania. The Baltic Tigers, as the markets had christened them, were imploding. Swedbank, which had spent a decade positioning itself as the dominant retail bank across all three nations, was staring into the abyss.

Fast forward to 2018. Swedbank was a profit machine. Return on equity was hovering around fifteen percent. Dividends were flowing. The Baltics, far from being the albatross, had become the crown jewel, generating returns that dwarfed the mature Swedish domestic business. Analysts loved the story: a boring Nordic utility bank with a hidden growth engine in Eastern Europe. And then, on a cold February evening in 2019, Sweden's public broadcaster SVT aired an investigative report that connected Swedbank to one of the largest money laundering networks in European history. The CEO was fired within weeks. Billions in fines followed. The stock cratered again.

This is a company that has been to the edge twice in a decade and come back both times. That pattern, the oscillation between mundane reliability and existential crisis, is not a bug. It is a feature of Swedbank's fundamental architecture.

At its core, Swedbank is a study in geographic arbitrage and the fragility of trust. The Swedish domestic business is a utility, a deeply entrenched, high-switching-cost franchise built on mortgages and salary accounts. The Baltic business is something else entirely: a dominant market leader operating in economies that are still catching up to Western European living standards, generating returns on equity north of twenty-five percent. Robur, the asset management arm, is a capital-light fee machine hidden inside a capital-heavy balance sheet. Together, these three businesses produce a blended return profile that ranks among the best in European banking.

But the flip side of geographic arbitrage is geographic risk concentration. When the Baltics boomed, Swedbank soared. When they crashed, Swedbank nearly died. And when the compliance infrastructure failed to keep pace with the commercial ambition, the entire franchise was called into question. The question for investors has always been the same: is Swedbank a world-class franchise temporarily derailed by manageable risks, or is the risk itself structural and recurring?

To answer that, one has to go back to the beginning, to the peculiar DNA of Sweden's savings banks and the century-long journey from parish thrift societies to a twenty-billion-dollar banking group.

II. Origins: The "Sparbank" DNA

In 1820, a German-born merchant named Eduard Ludendorff opened a small savings institution in Gothenburg. There was no government mandate, no royal charter, no shareholders expecting a return. The idea was simple and, for its time, radical: ordinary Swedes, workers and tradespeople and servants, should have a safe place to put their money. The concept had been percolating across Northern Europe, inspired by similar institutions in Hamburg and Edinburgh, but Ludendorff's Gothenburg savings bank was the first of its kind in Sweden.

The movement caught fire. By the 1870s, there were 325 savings banks scattered across the country, each one locally governed, each one embedded in its community. They were not banks in the modern sense. They had no shareholders. They existed to serve a social mission: encourage thrift, build financial resilience among the working class, and channel local savings into local lending. Control was vested in foundation-like structures, boards of local notables who saw themselves as stewards rather than profit-maximizers.

This model persisted, remarkably unchanged, for over 150 years. The first Savings Bank Act was not passed until 1892, meaning these institutions operated for seventy-two years on nothing more than social convention and local trust. That is an extraordinary fact. It tells you something about the depth of the relationship between the savings banks and Swedish society. These were not financial intermediaries in the Wall Street sense. They were civic institutions.

The stability of this model was shattered in the early 1990s by the Swedish banking crisis, one of the most severe financial disruptions in modern Nordic history. Between 1991 and 1993, Sweden's banking system lost approximately SEK 20 billion. Real estate values collapsed. Credit losses mounted. The savings banks, with their conservative lending traditions, were not the worst hit, but the crisis exposed a fundamental vulnerability: hundreds of tiny, independent institutions lacked the scale to absorb systemic shocks, invest in technology, or compete with the increasingly consolidated commercial banks.

The response was consolidation at a pace that would have been unthinkable a decade earlier. In 1992, eleven of Sweden's largest savings banks merged to form Sparbanken Sverige, simultaneously converting from the old foundation structure to a limited liability company. It was a cultural earthquake. Institutions that had operated for a century and a half as community cooperatives were suddenly a single, publicly traded corporation. Sparbanken Sverige listed on the Stockholm Stock Exchange in 1995.

But the consolidation was not finished. In 1997, Sparbanken Sverige merged with Föreningsbanken, the cooperative banking arm that served Sweden's agricultural sector. The resulting entity was christened FöreningsSparbanken, a name that sounded like it had been designed by a committee, which it had. The combined bank served nearly five million customers and had one of the densest branch networks in Northern Europe.

Here is what makes this history more than just corporate archaeology: the savings bank foundations that originally governed those 325 local institutions did not disappear. They converted their ownership stakes into shares of the new public company and held on. Today, the Sparbanksgruppen collective remains Swedbank's single largest shareholder at roughly twelve and a half percent, with additional savings bank foundations holding another four percent. This is not a normal ownership structure for a major European bank. The foundations' principal mission remains what it was in 1820: advance the savings bank concept and promote saving. They are not activist investors. They are not hedge funds. They are the institutional memory of a two-hundred-year-old social mission, and their presence on the shareholder register gives Swedbank a governance profile that is genuinely different from its commercial bank peers.

That DNA, the tension between social mission and commercial imperative, between local roots and global ambitions, would define every major strategic decision the bank made in the decades that followed. And the biggest of those decisions was about to take the bank far from the parishes of rural Sweden, eastward across the Baltic Sea, into countries that were barely a decade removed from Soviet rule.

III. The Baltic "Land Grab": The Hansabank Acquisition

To understand why Swedbank looked East in the late 1990s, you have to understand what the Baltic states looked like to a Swedish banker in 1998. Estonia, Latvia, and Lithuania had declared independence from the Soviet Union only seven years earlier. Their banking systems were embryonic. Per capita GDP was a fraction of the Swedish level. But the trajectory was unmistakable: these were small, well-educated, culturally European nations that were sprinting toward EU membership, NATO accession, and integration with the Western economic order. The growth rates were staggering, the kind of numbers you associate with emerging Asia, not Northern Europe.

Most Western European banks looked at the Baltics and saw risk: political instability, weak legal frameworks, opaque corporate cultures. Swedbank, or rather FöreningsSparbanken as it was still known, saw something else. It saw three countries with combined populations smaller than metropolitan Stockholm, where a single well-capitalized player could build dominant market share in the space of a few years. It was, in essence, a geographic arbitrage play: take the cheap funding and regulatory credibility of a Swedish banking license, deploy it in high-growth economies where competition was fragmented and unsophisticated, and harvest the spread.

The vehicle for this strategy was Hansabank, the crown jewel of Baltic banking. Founded in Estonia in 1992, just one year after independence, Hansabank had expanded rapidly into Latvia and Lithuania. By the late 1990s, it was the most valuable publicly traded company in the entire Baltic region, a full-service retail and corporate bank with a brand that carried enormous local trust.

FöreningsSparbanken moved in stages. In 1998, it acquired a majority stake of over fifty percent in Hansabank for approximately SEK 1.2 billion. The deal was not hostile; Hansabank's founders and management recognized that access to Swedish capital markets and the credibility of a Nordic parent would be transformative. The initial price, for a majority stake in the region's leading bank, looks almost quaint in retrospect.

The second stage came in 2005, by which time FöreningsSparbanken had rebranded as Swedbank. The bank made a buyout offer for the remaining forty percent of Hansabank shares, paying approximately EUR 1.7 billion and valuing the entire institution at roughly EUR 4.3 billion. This was a significant number. It implied a valuation of approximately four times book value, double the roughly two times book that Nordic banks were trading at during the same period. By any conventional metric, Swedbank was paying a premium that assumed the Baltic growth story would continue uninterrupted.

Was it an overpay? In the short term, catastrophically so. Within three years, the Baltic economies would collapse, Hansabank's loan book would implode, and Swedbank would be forced to raise nearly SEK 28 billion in emergency capital to survive. The four-times-book-value acquisition would look like the kind of top-of-cycle hubris that fills business school case studies.

But here is where the story gets more interesting. In the long run, the Hansabank acquisition was arguably the single best strategic decision Swedbank ever made. Once the crisis passed and the Baltic economies recovered, the franchise that Swedbank had bought proved to be exactly what the optimists had predicted: a dominant, deeply entrenched retail banking platform in fast-growing economies with limited competition. The Baltic business would go on to generate returns on equity consistently above twenty-five percent, far exceeding what any Nordic domestic market could produce. The branch network, the customer relationships, the brand equity, all of it was real. Swedbank had not bought a bubble. It had bought a franchise through a bubble.

The lesson is nuanced. Swedbank absolutely overpaid in 2005, and the timing nearly killed the company. But the underlying asset was sound. The problem was not the strategy; it was the execution, specifically, the failure to manage the credit risk that came with explosive lending growth in overheating economies. That failure would define the next chapter of Swedbank's history and fundamentally reshape the institution.

Hansabank was formally rebranded to Swedbank between 2008 and 2009, right in the teeth of the crisis. The timing was almost comically bad, like christening a ship as it takes on water. But it also represented a commitment: Swedbank was not going to cut and run from the Baltics. It was going to absorb the losses, rebuild the franchise, and come out the other side as the undisputed market leader. Whether that was courage or stubbornness depended entirely on how the next two years played out.

IV. The Inflection Point 1: The 2008 Near-Collapse

The Baltic boom of the mid-2000s was, in hindsight, a textbook credit bubble. Easy money from Nordic parent banks, including Swedbank, flooded into economies that were growing at seven to ten percent annually. Real estate prices doubled and tripled. Consumer lending exploded. Latvians who had never owned property were suddenly taking out Euro-denominated mortgages at loan-to-value ratios that would have made an American subprime lender blush.

Swedbank was not a passive participant in this frenzy. It was the market leader. Approximately sixteen percent of the bank's total lending was concentrated in the three Baltic states, a staggering exposure for a bank of its size. And the lending standards had deteriorated in lockstep with the euphoria. When the global financial crisis hit in 2008, the Baltic economies did not just slow down. They fell off a cliff. Estonia's GDP contracted by fourteen percent in 2009. Latvia's fell by eighteen percent, one of the sharpest peacetime economic collapses in modern history.

The loan losses were devastating. In the first three quarters of 2009 alone, Swedbank booked SEK 19 billion in credit losses, with roughly sixty percent originating from the Baltic portfolio. The bank's share price, which had peaked above SEK 200 before the crisis, collapsed to SEK 14.70 on March 6, 2009. Ninety percent of the market capitalization had been destroyed. For a few weeks in early 2009, there were genuine questions about whether Swedbank would survive.

The rescue came in two stages. First, a SEK 12.4 billion rights issue in 2008, followed by a second, even larger SEK 15.1 billion raise in 2009. In total, approximately SEK 27.5 billion in fresh equity was injected into the bank, diluting existing shareholders massively but averting the existential threat. Swedbank also participated in the Swedish government's guarantee program, a backstop that provided implicit state support without an explicit bailout.

The leadership change was decisive. CEO Jan Lidén, who had presided over the expansion phase, was replaced in March 2009 by Michael Wolf. Wolf was a very different kind of banker. Where Lidén had been expansionist, Wolf was a consolidator. He slashed the Baltic loan book, tightened credit standards dramatically, rebuilt the capital buffers, and reoriented the entire organization around risk management rather than growth. It was unglamorous work, the kind of restructuring that generates no headlines and wins no awards, but it was exactly what Swedbank needed.

The recovery that followed was remarkable. Under Wolf's leadership, Swedbank's share price rose roughly tenfold from its crisis nadir. The Baltic franchise, once written off by the market, came roaring back as the economies recovered. By the mid-2010s, Swedbank was generating returns on equity in the Baltics that ranked among the highest in global banking. The near-death experience of 2008-2009 had, paradoxically, strengthened the franchise by forcing the bank to optimize the cost structure, clean up the loan book, and build a capital position that was genuinely fortress-like.

This period defined what analysts now call "Modern Swedbank." The bank that emerged from the crisis was fundamentally different from the one that had entered it. The growth-at-all-costs mentality was replaced by an almost obsessive focus on capital adequacy. The risk management function, which had been inadequate during the boom years, was rebuilt from the ground up. And the board developed a keen appreciation for the difference between geographic diversification, which reduces risk, and geographic concentration, which amplifies it. Swedbank had learned the hard way that being the dominant bank in a small economy is wonderful on the way up and terrifying on the way down.

Wolf himself was removed by the board in February 2016 in what was described as a "shock move," a sudden and unexplained departure that raised eyebrows across the Nordic financial community. His successor, Birgitte Bonnesen, would inherit a bank that was in excellent financial shape but, as the world would soon discover, harbored a compliance failure of staggering proportions. The crisis that had forged Modern Swedbank was not the last one the institution would face. The next one would come not from the loan book but from the plumbing.

V. The Inflection Point 2: The 2019 Money Laundering Scandal

The story broke on February 20, 2019, when SVT's investigative program Uppdrag Granskning aired a report that sent shockwaves through Nordic financial markets. The journalists had been digging for months, following a trail that led from Swedbank's Baltic branches to a web of shell companies, offshore accounts, and suspicious transactions totaling tens of billions of kronor. The connection was to the Danske Bank scandal, which had already been dominating European headlines for months, but the Swedbank revelations suggested the problem was far larger and more systemic than anyone had realized.

The numbers were staggering. At least SEK 40 billion in suspicious and high-risk transactions had been channeled between Swedbank and Danske Bank accounts in the Baltics between 2007 and 2015. Among the entities involved were companies linked to the Sergei Magnitsky case, the Russian tax fraud scandal that had become a symbol of Kremlin-connected financial crime. One subsidiary alone, Diron Trade LLP, had facilitated USD 5.8 billion in transfers between Swedbank's and Danske Bank's Baltic operations in 2010 and 2011.

The fundamental issue was that Swedbank's anti-money-laundering controls in the Baltics had been woefully inadequate during the very years when the franchise was generating its most impressive returns. The non-resident banking business, serving customers from outside the Baltic states, particularly from Russia and other former Soviet republics, was enormously profitable. It was also, as it turned out, a conduit for vast amounts of illicit money. The compliance infrastructure simply had not kept pace with the commercial ambition.

CEO Birgitte Bonnesen became the face of the scandal. In October 2018, before the SVT report aired but after the Danske Bank revelations had already raised questions about Nordic banks' Baltic operations, Bonnesen had publicly reassured investors and regulators that Swedbank's AML controls were robust and that the bank had no significant exposure to the Danske Bank laundering networks. Those assurances, as the SVT investigation would demonstrate, were not accurate.

Bonnesen was fired in March 2019. Her severance pay was cancelled. But the legal reckoning would take years. She went on trial in October 2022 for gross fraud, charged with making deliberately misleading public statements about the bank's AML controls. The Stockholm District Court acquitted her in 2023, but the Svea Court of Appeal reversed that decision in September 2024, finding her guilty and sentencing her to fifteen months in prison. The court concluded that her public reassurances were deliberately misleading and could have materially affected investors' perceptions. The case, which Bonnesen has indicated she will appeal to Sweden's Supreme Court, represents a landmark moment in Nordic corporate governance: a sitting bank CEO convicted of fraud for misleading the market about compliance failures.

The financial penalty for Swedbank itself came in the form of a SEK 4 billion fine levied by Sweden's Finansinspektionen, the largest fine in the regulator's history. The grounds were twofold: serious deficiencies in anti-money-laundering controls, and withholding information from the authorities. American regulators also scrutinized the bank's activities, though the primary enforcement action remained in Sweden.

The structural consequences went beyond the fine. The scandal forced Swedbank to fundamentally de-risk its Baltic business model. The high-margin non-resident banking operations that had been a significant profit contributor were effectively shut down. Going forward, the Baltic franchise would be built exclusively on domestic retail and corporate banking, serving the residents and businesses of Estonia, Latvia, and Lithuania rather than acting as a gateway for cross-border capital flows. This was a trade-off: lower margins in exchange for dramatically reduced compliance risk.

The scandal also triggered a complete overhaul of the bank's governance. The board was reconstituted. The compliance function was rebuilt and elevated in the organizational hierarchy. And the bank brought in new leadership specifically chosen for their ability to restore trust with regulators, investors, and the public. The cleanup would take years, but the scandal had one clarifying effect: it forced Swedbank to decide, once and for all, what kind of bank it wanted to be. The answer was a boring, transparent, compliance-first retail franchise. The days of chasing high-margin, high-risk business in the Baltics were over.

VI. Current Management: The Cleanup Crew

When Swedbank's board needed a new CEO in 2019, they did not reach for a swashbuckling dealmaker or a charismatic visionary. They reached for Jens Henriksson, a technocrat's technocrat, a man whose entire career had been spent navigating the intersection of finance and regulation.

Henriksson was born in 1967 and holds degrees in both electrical engineering and economics, a combination that suggests a mind oriented toward systems and quantitative rigor rather than narrative and inspiration. His career path reads like a deliberate preparation for the job he now holds. He served as State Secretary at the Swedish Ministry of Finance, where he was deeply involved in the regulatory architecture of the Swedish financial system. He spent time on the supervisory board of the International Monetary Fund in Washington, gaining a global perspective on banking regulation. He ran the Stockholm Stock Exchange during its transition to Nasdaq OMX. And he served as CEO of Folksam, Sweden's largest insurance group, a role that required managing a complex financial institution with a social mission not unlike Swedbank's own.

This is not the résumé of a growth CEO. This is the résumé of someone you hire when your institution needs to rebuild credibility with regulators, demonstrate governance competence to institutional investors, and execute a multi-year compliance remediation program without blowing up the commercial franchise in the process. Henriksson's compensation structure reflects this mandate: the bank's Long-term Incentive Program ties executive pay heavily to return on equity and capital buffer targets rather than to pure share price appreciation. The incentives are aligned with the "Safety First" mandate that the board has embedded into the post-scandal operating philosophy.

The chairman's seat tells a complementary story. Göran Persson, born in 1949, served as Prime Minister of Sweden from 1996 to 2006, leading the Social Democratic government through a period of fiscal consolidation and EU integration. Before that, he was Minister of Finance from 1994 to 1996, the period when Sweden was cleaning up the wreckage of the early-1990s banking crisis. Persson understands, at a visceral level, what a banking crisis does to a country and to the politicians who fail to prevent one. His appointment to Swedbank's board in 2019, and his re-election at the March 2026 annual general meeting in Stockholm, brought a specific kind of credibility: the gravitas of a former head of state who had navigated financial turmoil before and understood the stakes.

Together, Henriksson and Persson represent a management philosophy that is the mirror image of the expansionist era. Where the CEOs of the 2000s were focused on growth, M&A, and geographic expansion, the current leadership is focused on digital efficiency, regulatory compliance, and ESG integration. The acquisitions they have made, Stabelo, a digital mortgage firm purchased for approximately SEK 350 million and consolidated in November 2025, and Entercard, the former Barclays joint venture in credit cards acquired for roughly SEK 2.75 billion and consolidated in December 2025, are not transformative bets on new geographies. They are incremental additions to the existing Nordic franchise, designed to defend market share in mortgages and expand the card business. Entercard, which serves 1.5 million customers across Sweden, Denmark, Finland, and Norway, positions Swedbank as what it calls "the largest card business in the Nordics and Baltics." But this is optimization, not revolution.

The management style is deliberately low-key. Henriksson does not give visionary speeches about the future of banking. He talks about cost-to-income ratios, capital adequacy, and compliance milestones. In a post-scandal institution, this is exactly the right tone. The market does not need to be excited by Swedbank. It needs to trust Swedbank. And trust, once lost, is rebuilt not through bold pronouncements but through years of consistent, boring, predictable execution.

For investors, the key question about current management is whether the pendulum has swung too far toward conservatism. The cleanup was necessary and overdue. But at some point, a bank that is focused exclusively on defense risks losing ground to more aggressive competitors. The fintech threat is real and growing. Smaller banks now account for thirty-five percent of new mortgage originations in Sweden, far above their ten percent share of outstanding mortgages. If Swedbank's leadership is too cautious for too long, the franchise could erode not through a dramatic crisis but through a slow, steady loss of market share. This is the tension at the heart of Modern Swedbank: how to be safe enough to survive the next crisis while remaining competitive enough to thrive in the absence of one.

VII. Hidden Businesses and Segment Deep Dive

To understand how Swedbank actually makes money, you need to look past the consolidated numbers and into the three distinct businesses that sit underneath the corporate umbrella. Each one has a different competitive dynamic, a different growth profile, and a different risk/return signature. Together, they create a blended return that looks deceptively simple from the outside but is actually the product of very different economic engines.

Swedish Banking: The Cash Cow

The Swedish domestic business is the foundation. It generates approximately sixty-five percent of operating profit and produces a return on equity of around fourteen percent. By Nordic standards, this is solid if unspectacular. The business is built on the Swedish mortgage market, where Swedbank holds a substantial share of outstanding loans, and the salary account relationship, which brings with it current account deposits, card transactions, and cross-selling opportunities for insurance, savings products, and advisory services.

The moat here is switching costs. Moving a mortgage in Sweden is a multi-step process involving appraisals, documentation, and administrative friction that most customers simply cannot be bothered to endure. When your mortgage, salary account, pension, and everyday banking are all with the same institution, the gravitational pull is enormous. This is not a sexy competitive advantage. It is not a technology moat or a brand moat. It is an inertia moat, and in retail banking, inertia is one of the most durable competitive advantages that exists.

The risk, however, is that this moat is being eroded at the margins. Fintech challengers like Avanza have captured a significant share of the savings and investment wallet. Klarna is moving aggressively into broader banking services. And smaller banks and digital-first mortgage lenders are winning a disproportionate share of new mortgage originations. The Stabelo acquisition was a direct response to this dynamic: buying a digital mortgage platform to ensure Swedbank does not cede the fastest-growing distribution channel to insurgents. But the trend is clear. The Big Four Swedish banks collectively hold around sixty-three percent of the credit market, but that share has declined by nearly five percentage points since 2014.

Baltic Banking: The Growth Engine

The Baltic business is where the economics get genuinely interesting. It contributes approximately twenty-five percent of operating profit but generates returns on equity that consistently exceed twenty-five percent, nearly double the Swedish domestic business. This is the premium that comes with market dominance in fast-growing, under-banked economies.

The numbers on market share are striking. Swedbank commands approximately twenty-seven percent of banking assets in Estonia, thirty-five percent in Latvia, where it is the largest bank, and around thirty-one percent in Lithuania. It serves roughly 3.5 million private customers and 300,000 corporate clients across the three countries. In populations this small (Estonia has 1.3 million people, Latvia 1.9 million, Lithuania 2.8 million), these market shares translate into a level of brand ubiquity that has few parallels in Western European banking.

The competitive dynamics are favorable. Unlike Sweden, where four well-capitalized banks compete intensely for a relatively static market, the Baltic banking market is less crowded, and the barriers to entry for a new full-service retail bank are substantial. The regulatory requirements, the technology investment, the branch infrastructure, and the local expertise required to compete effectively all create significant obstacles for potential entrants. Swedbank's two-decade head start, inherited from the Hansabank acquisition, is a cornered resource in the Helmer's 7 Powers sense.

The growth is also structural rather than cyclical. The Baltic economies are still converging toward Western European income levels. As GDP per capita rises, demand for financial services, mortgages, consumer loans, investment products, and insurance, rises with it. Swedbank's corporate market share has been expanding: from nineteen to twenty percent in Latvia and from twenty-two to twenty-eight percent in Lithuania, with a target of twenty-five to thirty percent by 2030. Total lending in the Baltics grew nine percent in 2024, driven by green mortgage products. This is organic growth in a franchise that Swedbank already owns outright, meaning the incremental returns on capital deployed are exceptionally high.

Swedbank Robur: The Hidden Gem

And then there is Robur. If Swedish Banking is the cash cow and Baltic Banking is the growth engine, Robur is the business that most investors undervalue because it sits inside a bank.

Swedbank Robur is one of the largest asset managers in Northern Europe, with approximately EUR 166 billion, or roughly SEK 1.9 trillion, in assets under management. It accounts for six of the ten largest funds in Sweden. In the Baltic fund markets, its market shares hover around thirty-seven to thirty-nine percent across all three countries. It serves over four million retail, institutional, and corporate customers.

The economic significance of Robur lies in its capital-light, fee-based business model. A bank's lending business requires capital, lots of it, to support the loan book and meet regulatory requirements. Every krona of mortgage lending sits on the balance sheet and consumes a portion of the bank's equity. Robur's asset management business, by contrast, generates fee income from assets that belong to the customers, not the bank. The capital requirements are minimal. The margins on fund management fees, while under pressure industry-wide from passive investing and fee compression, remain attractive relative to the capital employed.

As Swedish households gradually shift their savings from bank deposits to investment funds, Robur captures that flow. This is a secular trend, not a cyclical one, driven by low interest rates on deposits, growing financial literacy, and the government's pension system, which channels a portion of every worker's retirement savings into the fund market. Robur's sustainability focus, with a dedicated team of ESG analysts and a stated vision to be "the world leader in sustainable value creation," has also resonated with the growing segment of investors who want their money managed with environmental and social considerations in mind.

For investors in Swedbank, Robur represents embedded optionality. If the asset management business were independently listed, it would likely trade at a significant premium to the parent bank's valuation multiple. Inside Swedbank's consolidated financials, Robur's contribution is visible but not fully appreciated by a market that tends to value the entire entity as a bank rather than as a bank plus a high-quality asset manager. This is the kind of sum-of-the-parts story that long-term investors find compelling.

VIII. Analysis: Hamilton's 7 Powers and Porter's 5 Forces

The 7 Powers Framework

Of Hamilton Helmer's seven strategic powers, three apply directly to Swedbank, and their interaction explains why the bank has been able to sustain returns that are above average for European banking despite multiple existential crises.

The primary power is switching costs. Swedbank's "full service" relationship, encompassing mortgage, salary account, pension, insurance, and savings, creates a bundle of services that is individually easy to replicate but collectively very expensive to move. The friction is not technological; it is administrative and psychological. A customer who has their entire financial life with Swedbank faces a multi-week, multi-step process to replicate that setup at a competitor. For the vast majority of retail customers, the hassle cost simply exceeds the potential benefit. This is why mortgage market share, once established, tends to be remarkably sticky, and why the Big Four Swedish banks have maintained their collective dominance for decades despite waves of fintech innovation.

The second power is scale economies. The cost of building and maintaining a modern, fully compliant banking technology stack is enormous and rising. Regulatory requirements around capital adequacy, anti-money-laundering, data privacy, and cybersecurity create a fixed-cost base that must be spread across a large customer base to be economically viable. Fintechs have successfully attacked specific niches: Avanza in self-directed investing, Klarna in payments, Stabelo (before its acquisition) in digital mortgages. But none of them has yet built the full-service, fully regulated, fully compliant platform that a major bank operates. The regulatory moat, paradoxically, is one of the strongest competitive advantages that traditional banks possess.

The third power is cornered resource, specifically in the Baltics. The Sparbank brand, the branch network, the customer relationships, and the institutional knowledge that Swedbank accumulated through the Hansabank acquisition and two decades of market leadership represent a resource that cannot be easily replicated. A new entrant to the Estonian or Latvian banking market would need to build not just the technology and the capital base but the trust, and in a market where Swedbank has been the dominant brand since the early 2000s, trust is a resource that accrues through time, not through investment.

Porter's 5 Forces

Viewed through Porter's lens, Swedish banking is a stable oligopoly with manageable but growing threats at the margins.

Rivalry among the Big Four, Swedbank, SEB, Handelsbanken, and Nordea, is intense in the sense that they compete actively on price and service, but it operates within the bounds of a mature, disciplined oligopoly. None of the four has an incentive to start a price war that would destroy industry profitability. The competitive dynamic resembles the U.S. wireless market more than it resembles, say, European low-cost airlines. Performance among the four has diverged recently: Nordea's profits fell six percent in the first nine months of 2025, SEB declined sixteen percent, and Handelsbanken dropped fourteen percent, while Swedbank's decline was more moderate, suggesting relative competitive strength within the oligopoly.

Threat of new entrants is low for full-service banking but meaningful in specific verticals. The regulatory barriers to launching a full-service bank in Sweden are formidable. But niche entrants can and do attack profitable segments: digital mortgages, investment platforms, payment solutions. The aggregate impact is significant. Smaller banks now constitute thirty-five percent of new mortgage originations, suggesting that the Big Four's origination dominance is eroding even as their stock of outstanding mortgages remains large.

Threat of substitutes is the most interesting force. Neo-banks and fintechs are genuine substitutes for specific banking products, but they have not yet cracked the bundled relationship. A customer might use Avanza for investing and Klarna for payments, but they still need a traditional bank for their mortgage, salary account, and pension. The "mortgage moat" remains intact, and as long as it does, the core franchise is defensible. The risk is that over time, unbundling becomes complete enough that the mortgage alone does not justify the switching-cost premium.

Bargaining power of customers is low for individual retail customers (high switching costs) but increasing for large corporate clients, who have the sophistication and the scale to negotiate aggressively and shift business between banks.

Bargaining power of suppliers is largely irrelevant in banking, where the primary "inputs" are deposits and wholesale funding, both of which are available from liquid, competitive markets.

The net assessment is that Swedbank operates in a structurally attractive industry with durable competitive advantages, particularly in the Baltics, but faces a secular erosion of its Swedish domestic franchise that requires ongoing investment in digital capabilities and customer experience to counteract. The 2008 crisis was a stress test of the balance sheet. The 2019 scandal was a stress test of the governance. The next test may well be a competitive one: whether Swedbank can defend its position against a thousand small cuts from fintech challengers and smaller banks that are winning a disproportionate share of new business.

IX. Playbook: Lessons for Investors and Founders

Lesson One: Don't Go Global. Go Regional Champion.

Swedbank's history offers a crisp illustration of the difference between international diversification and regional dominance. The bank's most successful strategic moves have been about deepening its position in a defined set of markets: Sweden and the three Baltic states. Its least successful moments came when it considered expanding further, into Russia, Ukraine, and other post-Soviet markets where it lacked the institutional knowledge and the risk management infrastructure to operate safely.

The Hansabank acquisition worked, despite the near-death experience of 2008, because Swedbank was buying into countries where it could achieve genuine market dominance. Thirty-five percent market share in Latvia is not diversification; it is control. And control in a small market is enormously valuable because it confers pricing power, brand ubiquity, and the ability to set the competitive terms. The lesson is not "don't expand." It is "expand into markets where you can win decisively, and avoid markets where you will be a marginal player competing against well-entrenched locals."

Lesson Two: The Utility Trap

A bank is a utility in good times: predictable revenues, steady dividends, modest but reliable returns. In bad times, it is a liability: levered to the credit cycle, exposed to confidence shocks, subject to regulatory intervention that can fundamentally reshape the business model. The 2008 and 2019 crises both illustrate this dynamic. In 2008, the utility became a liability because of credit risk concentration. In 2019, it became a liability because of compliance failure. In both cases, the resolution required massive capital raises, leadership changes, and years of remediation.

The practical implication for investors is that the capital buffer is the single most important variable in assessing a bank's durability. Swedbank's current CET1 ratio of 17.8 percent represents a buffer that would have been considered excessive a decade ago but is now viewed as appropriate, even conservative, in the post-crisis, post-scandal environment. The bank paid an ordinary dividend of SEK 20.45 per share for 2025, plus a special dividend of SEK 9.35, reflecting the excess capital that the fortress balance sheet has generated. The total payout of SEK 29.80 per share is a tangible expression of the "utility" value proposition: stable, predictable returns funded by a business that generates more capital than it needs to grow.

Lesson Three: You Can Buy a Market, But You Cannot Buy a Risk Culture

The Hansabank acquisition gave Swedbank the market share, the brand, and the customer relationships. What it did not give Swedbank was a compliance culture that could withstand the temptations of high-margin non-resident banking. The money laundering scandal was not a failure of the Baltic franchise per se; it was a failure of the parent company to impose its own risk standards on a subsidiary that was operating in a very different environment with very different incentive structures.

This is a universal lesson for any company expanding into new geographies through acquisition. The commercial integration, aligning products, pricing, and brand, is the easy part. The cultural integration, aligning values, risk appetite, and compliance standards, is far harder and far more important. Swedbank learned this lesson at a cost of SEK 4 billion in fines, incalculable reputational damage, and a CEO conviction. It is a lesson worth studying for any business contemplating international M&A.

X. Closing: Bear vs. Bull

The Bear Case

The most immediate risk is the Swedish real estate market. Swedish household debt is among the highest in Europe relative to disposable income, and a significant portion of Swedbank's loan book is concentrated in residential mortgages. A sustained decline in Swedish property values, whether triggered by rising interest rates, a recession, or a shift in housing policy, would directly impact Swedbank's asset quality and potentially require additional provisioning. This is the same kind of geographic concentration risk that nearly destroyed the bank in the Baltics in 2008, now manifest in the home market.

Regulatory risk has not disappeared. The money laundering fines have been paid, but the Bonnesen case is still potentially before the Supreme Court, and the bank's Baltic operations remain under heightened regulatory scrutiny. Further enforcement actions, whether from Swedish, Baltic, or American regulators, are not impossible. The compliance remediation has been extensive, but the history of the last decade suggests that regulatory surprises can emerge from directions that no one anticipated.

And then there is the fintech erosion. The thirty-five percent share of new mortgage originations captured by smaller banks and digital lenders is not a one-year anomaly. It is a trend. Swedbank's response, acquiring Stabelo and investing in digital channels, is appropriate but may not be sufficient to reverse the direction of travel. If the Big Four's mortgage origination share continues to decline, the switching-cost moat that underpins the Swedish domestic business will gradually narrow.

The Bull Case

The Baltics remain the strongest argument for long-term optimism. The convergence story is far from complete. GDP per capita in Estonia, Latvia, and Lithuania remains well below the Western European average, and the trend toward convergence is supported by EU membership, structural funds, and the ongoing integration of these economies into European supply chains and technology ecosystems. As incomes rise, demand for financial services rises with them, and Swedbank, as the dominant provider, captures a disproportionate share of that growth.

Robur represents significant embedded value. If the secular shift from deposits to investment funds continues, and if Robur can maintain its market-leading position in Swedish and Baltic fund markets, the asset management business could become an increasingly important earnings contributor with minimal additional capital requirements. In a world where investors are paying premium multiples for capital-light, fee-based financial businesses, Robur's value inside Swedbank's consolidated balance sheet is likely being underappreciated.

The dividend thesis is compelling. With a CET1 ratio of 17.8 percent and a cost-to-income ratio of just 0.36, Swedbank generates more capital than it needs to support organic growth. The combined 2025 dividend of SEK 29.80 per share, including the special dividend, signals a willingness and an ability to return excess capital to shareholders. If the bank can maintain its current profitability trajectory and avoid a third existential crisis, it has the financial profile of a "dividend king": a company that can fund consistent, growing distributions from operating cash flow without impairing the balance sheet.

The KPIs That Matter

For investors tracking Swedbank's performance over time, three metrics deserve primary attention.

First, Baltic ROE. This is the single best indicator of the health and competitive positioning of the crown jewel franchise. If Baltic returns on equity remain above twenty percent, the geographic arbitrage thesis is intact. If they decline materially, it signals either increased competition, regulatory pressure, or economic deceleration in the region.

Second, Swedish mortgage market share, specifically the share of new originations rather than the stock of outstanding loans. The stock is a lagging indicator; the flow tells you where the franchise is heading. A sustained loss of new mortgage origination share to fintechs and smaller banks would be an early warning of moat erosion.

These two numbers, Baltic ROE and Swedish mortgage flow share, capture the essential tension at the heart of Swedbank: the growth engine and the cash cow, the future and the present, the opportunity and the risk. They are the metrics that will determine whether Swedbank's next decade looks like the recovery from 2009, a steady compounding machine generating elite returns from dominant franchises, or something more challenged.

Swedbank has been to the brink twice and come back stronger both times. The savings bank DNA, the Baltic franchise, the Robur hidden gem, and the fortress balance sheet are genuine strategic assets. But the history teaches caution: in banking, the next crisis is always the one you did not see coming. The question is not whether Swedbank is a good bank. It is whether it has finally built the institutional resilience to match the quality of its underlying franchises.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube