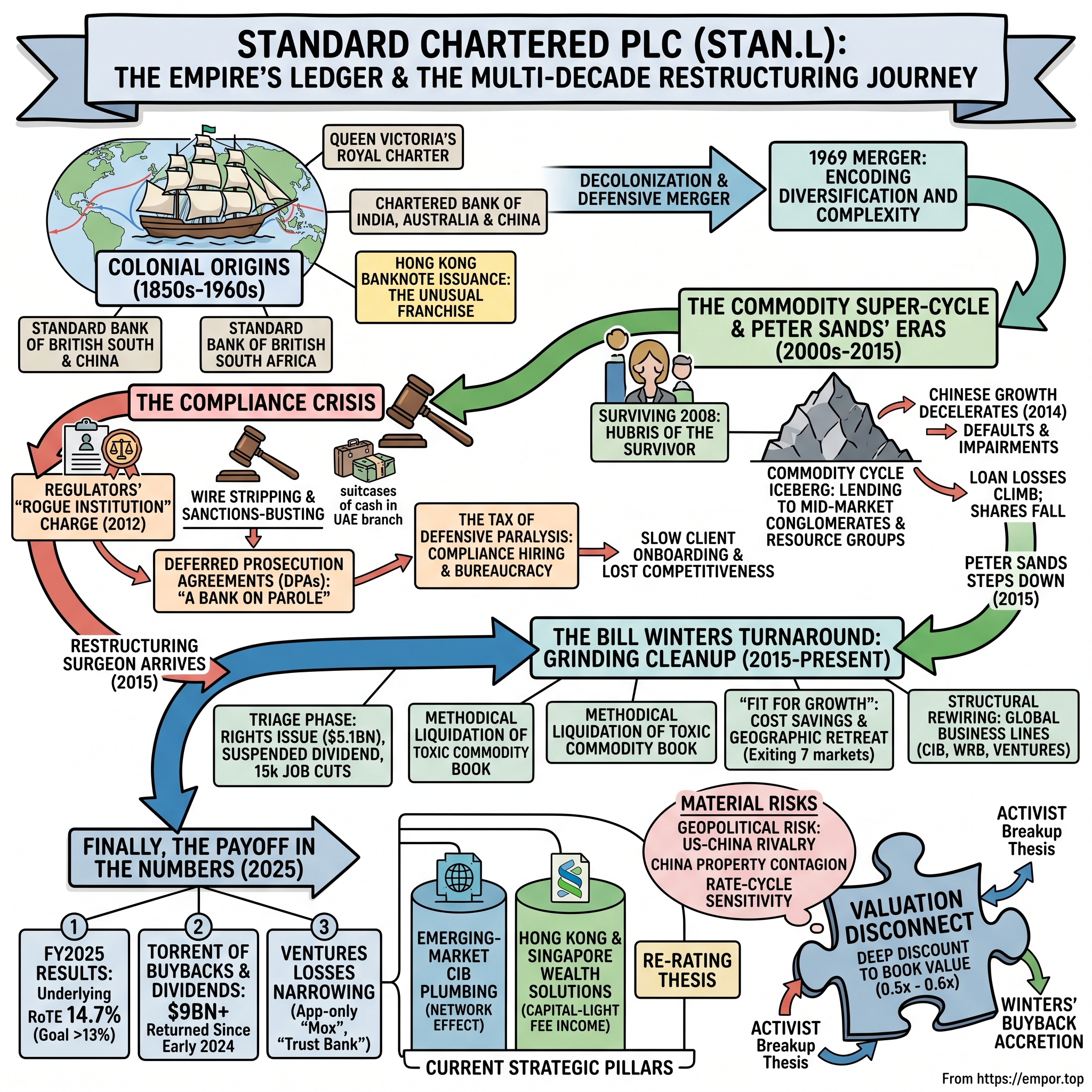

Standard Chartered: The Empire's Ledger and the Multi-Decade Restructuring

I. Introduction & Episode Roadmap

Walk into the lobby of any global bank and you can usually guess where its money comes from. JPMorgan is America. BNP Paribas is France. But stand in the marble atrium of Standard Chartered's headquarters in the City of London, at 1 Basinghall Avenue, and the map on the wall tells a stranger story. The bank is British by passport, listed on the London Stock Exchange under the ticker STAN.L, a constituent of the FTSE 100. And yet it has essentially no domestic retail bank. You cannot walk into a Standard Chartered branch in Manchester and open a current account. The register in London collects the dividends, but the profits are earned nine time zones away — in Hong Kong, Singapore, Dubai, Lagos, and Mumbai.1

That is the first paradox of Standard Chartered: a company that files its accounts in pounds, pays its board in London, and answers to British regulators, while generating almost the entirety of its earnings across Asia, Africa, and the Middle East. It is, in the most literal sense, a colonial relic — two Victorian trade banks stapled together — that has been dragged, sometimes kicking, into the role of a modern emerging-markets trade and wealth machine.

The second paradox is the one that keeps sophisticated investors up at night. Here is a bank plugged directly into the fastest-growing trade corridors on the planet — the arteries carrying goods between China, India, the Gulf, and Africa — and yet for most of the last decade it has traded at a deep discount to its own book value, frequently around 0.5x to 0.6x price-to-book. In plain English: the stock market has repeatedly said the bank is worth less than the accounting value of the assets on its balance sheet. Something in that equation does not add up, and the whole point of this story is to figure out which side of it is wrong — the market, or the balance sheet.

That persistent discount is also why the bank has spent years as a magnet for activists and a recurring name on the takeover rumor mill. The most dramatic episode came in early 2023, when First Abu Dhabi Bank — the largest lender in the United Arab Emirates — was reported to have studied a bid, briefly lighting up the shares before publicly backing away.2 The question of whether Standard Chartered is a coiled spring or a value trap has become the central debate of the stock.

Here is the roadmap for how we get to an answer. We start in the 1850s with the twin chartered banks and the imperial trade they were built to finance. We move through the golden era of Peter Sands, when the bank sailed through the 2008 crisis only to sail straight into a commodity-cycle iceberg. We sit inside the compliance crisis — the sanctions-busting, the suitcases of cash, the billions in fines that turned the bank into a defensive, paralyzed bureaucracy. Then we spend real time on the Bill Winters turnaround: a decade of cleanup, geographic retreat, organizational surgery, a pay overhaul, and the metamorphosis into a share-buyback machine. Finally, we take apart the segment economics, run the business through Hamilton Helmer's 7 Powers and Porter's Five Forces, stress-test the takeover thesis, and lay out the honest bull-versus-bear case. Let's begin where the ledger does.

II. The Twin Pillars of Empire: Colonial Origins

In 1853, a Scottish businessman and journalist named James Wilson — the same man who a decade earlier had founded The Economist — persuaded Queen Victoria to grant him a Royal Charter. The document authorized the creation of the Chartered Bank of India, Australia and China. The name reads today like a shipping manifest, and that is precisely the point: this was a bank built to move money along the trade routes of the British Empire.3

Its first branches opened in Bombay, Calcutta, and Shanghai in 1858, followed by Hong Kong and Singapore in 1859. The cargo it financed was the raw material of nineteenth-century globalization — tea, cotton, silk, indigo, and, in the unsentimental commerce of the era, opium. The Chartered Bank existed to solve one problem: a merchant in London wanted to buy tea in Fujian, and someone had to bridge the months-long gap between payment and delivery across oceans patrolled by the Royal Navy. That bridge — trade finance — is a business Standard Chartered still runs today, though the tea is now semiconductors and the ships carry containers.

Nine years later and a hemisphere away, a second bank was born from a different boom. In 1862, in the Cape Colony of southern Africa, John Paterson founded the Standard Bank of British South Africa. Its timing was extraordinary. Within a few years, prospectors struck diamonds at Kimberley and then gold on the Witwatersrand, and the Standard Bank found itself financing the largest mineral rush in human history. Where the Chartered Bank was built on the trade of the East, the Standard Bank was built on the minerals of the South.3

What made both institutions powerful was not clever banking. It was the charter itself — and here we meet the first of the moats we will examine throughout this story. A Royal Charter was not a license to compete; it was a license to be an extension of the state. These banks enjoyed government-backed privileges, clearing dominance in colonial ports, and, most valuably, the right to issue currency. To this day, Standard Chartered is one of only three commercial banks authorized to print and issue physical banknotes in Hong Kong, alongside 滙豐 HSBC and the 中國銀行 Bank of China.4 It is worth pausing on how unusual that is. When a Hong Kong resident pulls a HK$500 note from their wallet, there is a meaningful chance it was printed by a British-listed private bank. The privilege to create money that the public holds is about as close to a government-granted franchise as commercial banking gets — a source of brand equity and low-cost funding that no fintech can replicate by writing code.

By the late 1960s, however, the empire that granted those charters was dissolving. Decolonization swept across Africa and Asia, and a bank whose entire value proposition was imperial protection suddenly faced a world of newly independent governments, many with a taste for nationalizing foreign-owned assets. The strategic logic that produced the merger of 1969 was defensive and geographic: if a newly sovereign nation in Africa seized the Standard Bank's local operations, earnings from Asia could cushion the blow, and vice versa. The two banks combined, incorporated in London, and became Standard Chartered.3

That merger encoded the company's central trait — and its central weakness — into its DNA. Diversification across dozens of volatile emerging markets is a genuine risk buffer. It is also, as the next century would prove, a recipe for sprawling complexity, thin oversight of far-flung branches, and a management team perpetually fighting fires in jurisdictions few in London could find on a map. The empire's ledger had been consolidated. The question was whether anyone could actually control it.

III. The Commodity Super-Cycle & Peter Sands' Hyper-Growth Era

For a brief, intoxicating stretch in the late 2000s, Peter Sands looked like the smartest banker in the world. A former McKinsey consultant with a cerebral, understated manner, Sands became group chief executive in 2006, and within two years he had steered Standard Chartered through the event that maimed nearly every one of its Western peers: the 2008 global financial crisis.

While Citigroup and Royal Bank of Scotland were being nationalized or rescued, Standard Chartered barely flinched. It had almost no exposure to the toxic American subprime mortgages and structured products that detonated the balance sheets of London and New York. Its funding was conservative, its balance sheet liquid, its loan book anchored in the real economy of Asian trade rather than the financial engineering of the Atlantic. Where others were begging for government capital, Standard Chartered raised money from shareholders on its own terms and kept lending. The narrative practically wrote itself: the boring bank in the emerging markets had out-thought the geniuses of Wall Street.

The problem with surviving a crisis intact is that it can teach the wrong lesson. The correct lesson was "we avoided a catastrophe we had no exposure to." The lesson management appears to have absorbed was "our risk underwriting is peerless." That is the hubris of the survivor, and it is one of the durable morals of this entire story. Convinced that its credit judgment was superior, the bank leaned into an aggressive lending push across the emerging markets just as those markets were being inflated by the greatest commodity boom in a generation.

The engine of that boom was China. In the decade after 2003, Chinese industrialization sucked in staggering volumes of copper, coal, iron ore, and palm oil, and the prices of those commodities soared. Standard Chartered positioned itself as the financier of choice for the ecosystem feeding that appetite — mid-market conglomerates, commodity traders, and highly leveraged mining and resources groups across India, Indonesia, and Singapore. These were not blue-chip multinationals with pristine credit. They were aggressive, fast-growing, thinly capitalized borrowers whose entire business model assumed commodity prices would keep climbing. For a while, they did, and the loans looked brilliant.

Then, around 2014, the music stopped. Chinese growth decelerated, the commodity super-cycle rolled over, and prices for copper and coal cratered. The mid-market borrowers who had loaded up on Standard Chartered's credit found their revenues collapsing while their debts stayed fixed. Defaults arrived not one at a time but in waves. The bank was forced to recognize a mountain of impairments, and the profits that had made Sands a banking darling evaporated. Loan losses climbed, the share price fell hard, and rating agencies began to circle. The capital buffer that had looked so robust in 2009 was now visibly thinning.5

The board's verdict was blunt. In February 2015, Standard Chartered announced that Peter Sands would step down, and that a very different kind of banker would replace him.5 The man brought in was not a growth apostle. He was a restructuring surgeon. But before he could operate on the credit book, he would discover that the balance sheet was only half the emergency. The other half was sitting in a courtroom in New York.

IV. The Compliance Crisis: Suitcases of Cash & Regulators

The commodity losses were the storm everyone could see coming. The compliance crisis was the storm that broke over the bank's head from a clear sky, and in reputational terms it did far more lasting damage.

The first strike landed in August 2012. Benjamin Lawsky, the newly installed superintendent of New York's Department of Financial Services, published an order that used a phrase which would follow the bank for years: he accused Standard Chartered of operating as a "rogue institution." The allegation was extraordinary in scale. Regulators charged that, over roughly a decade, the bank had systematically stripped identifying information out of wire-transfer messages — a practice known as "wire stripping" — to disguise the origin of transactions on behalf of sanctioned Iranian clients, routing them through its dollar-clearing branch in New York. Lawsky's order alleged the scheme touched some 60,000 transactions worth around $250 billion.6 Standard Chartered disputed the characterization but settled with the New York regulator for $340 million.6

Later that same year, the federal machinery caught up. In December 2012, the bank agreed to forfeit $227 million to the U.S. Department of Justice and entered a Deferred Prosecution Agreement over illegal transactions with Iran, Sudan, Libya, and Burma.7 A Deferred Prosecution Agreement — a DPA — is a crucial concept for understanding everything that followed. It is a form of corporate probation: prosecutors agree to suspend criminal charges provided the company behaves, submits to independent monitoring, and cleans up its controls. Break the terms, and the original prosecution comes roaring back. Standard Chartered was now, in effect, a bank on parole, with U.S. authorities watching its every move.

And then, astonishingly, it happened again. While still under the DPA, the bank's controls failed a second time, and in April 2019 it agreed to a combined settlement of roughly $1.1 billion with U.S. and U.K. authorities.[^8] As part of that resolution, the DOJ extracted an additional $240 million forfeiture and extended the deferred prosecution agreement.[^9] The details that emerged from the U.K. side were what made the episode unforgettable. The Financial Conduct Authority fined the bank £102.2 million — one of the largest anti-money-laundering penalties in British history at the time — and its account of the failures read like farce. In one instance regulators cited, a Standard Chartered branch in the United Arab Emirates had accepted the equivalent of millions of dollars in cash, delivered physically in suitcases, without adequately verifying where the money came from.8

Sit with that image, because it captures the core failure. A globally systemic bank, already on probation for sanctions violations, was taking suitcases of cash across the counter. The nominal fines — a billion here, a hundred million there — were painful but survivable for an institution of this size. The real cost was something the accounts never captured directly: the tax of defensive paralysis.

To satisfy the DPAs and the regulators, the bank installed external monitors and hired thousands of compliance officers. Every process was rebuilt around the assumption that any client might be a liability and any transaction might be a trap. The consequences for the business were corrosive. Onboarding a new corporate client, which nimble rivals could do in days, could stretch into months of documentation and internal sign-off at Standard Chartered. In the fast-moving trade hubs of Asia, that latency was a competitive gift to everyone else. Singapore's 星展銀行 DBS Bank and other aggressive regional lenders won business precisely because they could say yes while Standard Chartered was still checking boxes. A bank designed to move at the speed of trade had been re-engineered to move at the speed of an audit. Fixing that — restoring the ability to actually do business without inviting the next scandal — would define the entire era that followed.

V. The Bill Winters Turnaround: Restructuring, "Fit for Growth," and Incentives

Bill Winters did not need the job. By 2015, the American-born banker had already lived one full, celebrated career as co-head of JPMorgan's investment bank, where he had earned a reputation as one of the sharpest risk minds of his generation — famously helping steer the firm away from the worst of the subprime disaster — before an internal power struggle pushed him out. He had gone on to found his own asset-management firm. When Standard Chartered's board came calling, they were not hiring a growth visionary. They were hiring a man who understood, in his bones, how a bank breaks and how to put one back together.5

Winters took over as group chief executive in June 2015, and his first phase was pure triage. The patient was bleeding capital, and he stopped the bleeding with a series of hard, unpopular decisions. He raised $5.1 billion in fresh equity through a rights issue — asking existing shareholders to write another large check to shore up the balance sheet. He suspended the dividend, a move that infuriates income investors but preserves capital when it is scarce. He announced roughly 15,000 job cuts. And he attacked the source of the rot directly, methodically liquidating the toxic mid-market commodity book that Sands-era lending had built and grinding through the backlog of non-performing loans.5 This was not glamorous work. It was the banking equivalent of debridement — cutting away the dead tissue so the healthy business could recover.

The triage phase lasted, in effect, from 2015 to 2020, and it was slow, grinding, and frequently disappointing to shareholders who wanted a faster payoff. But it set up the second act, which was about structure rather than survival. In 2023, management launched a program branded "Fit for Growth," a multi-year effort targeting roughly $1.5 billion in structural cost savings. The substance behind the marketing was an attack on complexity itself: simplifying a tangle of legacy technology systems accumulated over decades, standardizing platforms across dozens of countries, and stripping out layers of corporate and regional management that a sprawling colonial footprint had accreted.

That footprint was the next thing to go. For 150 years, Standard Chartered's presence in a country had been treated almost as a matter of heritage — you did not simply abandon a market your predecessors had banked since the days of empire. Winters was willing to. In 2022, the bank announced it would exit or partially exit seven markets across Africa and the Middle East — including Angola, Cameroon, Sierra Leone, Zimbabwe, Jordan, and Lebanon — to redeploy that capital toward denser, more profitable financial hubs.9 The strategic message was unsentimental: sub-scale operations in small, hard-to-supervise markets generated more compliance risk and management distraction than profit. Better to concentrate on the corridors that actually mattered — Hong Kong, Singapore, and Dubai — than to keep flying the flag everywhere.

The most consequential change, though, was invisible to customers and easy for outsiders to miss. In April 2024, the bank rewired how it reports itself to the world. It abolished the old regional structure — the "Asia," "Africa & Middle East," and "Europe & Americas" buckets that had organized its accounts for generations — and replaced it with three global business lines: Corporate & Investment Banking (CIB), Wealth & Retail Banking (WRB), and Ventures. This was not cosmetic. Reorganizing around global product lines rather than colonial geography signaled that management now thought of the bank as a set of businesses that happen to operate across borders, rather than a federation of country fiefdoms. It also, conveniently, made the high-return wealth franchise far more visible to investors.

Then came the money question — specifically, how management pays itself. When British regulators scrapped the EU-era cap on banker bonuses, Winters moved quickly to rebuild executive pay around variable, performance-linked incentives rather than large fixed salaries. His own package rose 46% year-on-year to £10.7 million (about $13.6 million) for 2024, a figure that drew predictable headlines.10 The independent read here cuts both ways. On one hand, tying compensation tightly to Return on Tangible Equity and shareholder payouts is exactly the alignment activists demand — pay for delivered returns, not for showing up. On the other, a 46% raise for a CEO is precisely the kind of item a skeptical investor flags, and the alignment only looks good so long as the returns keep coming.

And for now, they have. This is the phase where the decade of grinding cleanup finally showed up in the numbers, and management turned the bank into something it had never been: a capital-return machine. The commitment was to return at least $8 billion to shareholders between 2024 and 2026 through dividends and buybacks. The full-year 2025 results, reported in February 2026, showed that target being blown through early. Underlying return on tangible equity reached 14.7%, clearing the bank's own ">13%" goal a full year ahead of schedule.11 The full-year dividend was lifted 65% to 61 cents per share; underlying pre-tax profit rose 18% to $7.9 billion on income of $20.9 billion; and the bank announced a fresh $1.5 billion buyback, bringing cumulative distributions since early 2024 to more than $9 billion — already past the three-year commitment.1112 What it means is straightforward, and we will test it hard later: after a decade of promising discipline, management is now demonstrating it, converting a cleaned-up balance sheet into real cash returned to owners. Whether that is durable or merely well-timed to a favorable interest-rate cycle is the question the rest of this story has to answer.

VI. Deep Dive: CIB Powerhouse, WRB Wealth Machine, and Digital Ventures

To understand where the money actually comes from, forget the map and look at the two engines under the hood — because they could hardly be more different in character.

The first and by far the larger is Corporate & Investment Banking. This is the modern incarnation of James Wilson's original tea-financing business, and it is the statutory profit core of the group, generating the lion's share of earnings — on the order of $4 billion in annual pre-tax profit.1 But calling it "investment banking" undersells what makes it special. Standard Chartered is not trying to out-muscle Goldman Sachs on Wall Street M&A. Its edge is plumbing — the unglamorous, deeply defensible business of moving money and trade across emerging-market borders. When a multinational needs to pay a supplier in Bangladesh, clear dollars in Lagos, hedge a Kenyan-shilling exposure, or finance a shipment of goods from Vietnam to the Gulf, Standard Chartered's physical network across more than 50 markets is the rail the transaction rides on. In FY2025, CIB's pre-tax profit rose 9%, powered by a record performance in Global Markets and strong double-digit growth in Global Banking, partly offset by softer transaction-services income as interest rates eased.11 The takeaway for investors is that CIB's advantage is structural, not cyclical: it is very hard for a competitor to replicate a five-continent clearing network, but the income it throws off does breathe with rates and trade volumes.

The second engine is Wealth & Retail Banking, and it contains the crown jewel of the entire modern strategy. Plain retail banking — current accounts, mortgages, credit cards — is a localized, low-margin grind, and in most of Standard Chartered's markets it competes at a scale disadvantage against domestic giants. But threaded inside WRB is the Wealth Solutions business, which serves affluent and high-net-worth clients in the great private-banking hubs of Hong Kong and Singapore, and it is a genuinely excellent business. It sells investment products, structured notes, insurance, and advice, and it earns recurring fee income while consuming very little of the bank's capital — the holy grail of banking economics, because returns on equity soar when you can earn fees without tying up a balance sheet. Wealth Solutions grew at a record pace of around 29% in 2024, and its momentum carried WRB's pre-tax profit up 14% in FY2025 on the back of another record wealth performance.1113 Why does this matter so much? Because a dollar of stable, capital-light wealth fee income is worth far more to a bank's valuation than a dollar of volatile, capital-hungry lending income — and management's whole re-rating thesis rests on convincing the market that Standard Chartered is becoming more of the former.

The third piece is the smallest and the most speculative: Ventures, the bank's digital laboratory. It houses Mox in Hong Kong and Trust Bank in Singapore, two app-only "neobanks" built from scratch to defend against the fintech disruptors nibbling at the edges of traditional banking. Ventures has consistently lost money — the drag was around $390 million in 2024 — but the losses have been narrowing sharply as the digital banks mature and their credit quality improves, and from 2025 the bank folded Ventures reporting inside WRB rather than treating it as a standalone segment.1113 The honest analytical read is that Ventures is a rational, appropriately small hedge: if fintech does erode the deposit base, the bank owns its own attacker; if it does not, the losses are a manageable insurance premium. What it is not, at least yet, is a profit engine — and investors should size it accordingly.

Finally, no honest tour of the balance sheet skips the China property scar. Standard Chartered holds a 16.26% stake in 渤海银行 China Bohai Bank, and when the Chinese real-estate crisis tore through the mainland financial system, the bank was forced to take an $850 million impairment on that associate stake in 2023 — a hit large enough to miss profit expectations for the quarter and a vivid reminder that the bank's emerging-market exposure cuts both ways.1415 Since then, management has aggressively provisioned and shrunk its Mainland China commercial real-estate portfolio, pushing the coverage ratio on impaired loans in that book high enough to argue the contagion is ring-fenced.11 "Ring-fenced" is management's word; the market's skepticism about Chinese property is why the stock still carries a discount, and that tension — between a cleaned-up disclosed exposure and an unknowable systemic risk — is exactly where the bull and bear cases collide.

VII. The Competitive Moat: Hamilton Helmer's 7 Powers & Porter's 5 Forces

Strip away the narrative and ask the cold question an analyst has to answer: what actually stops a competitor from taking this business away? Hamilton Helmer's 7 Powers framework — a taxonomy of the durable advantages that let a company sustain returns above its cost of capital — is a useful scalpel here, and Standard Chartered turns out to possess three of the seven in real measure.

The first is scale economies, and it lives in the transaction-banking network we just described. Building a physical clearing and settlement presence across 50-plus emerging markets, each with its own currency, central bank, and regulatory regime, is not a matter of money alone — it is decades of accumulated licenses, correspondent relationships, and local knowledge. The marginal cost to Standard Chartered of processing one more cross-border payment through infrastructure it already owns is tiny; the cost to a new entrant of building that infrastructure from zero is effectively prohibitive. That asymmetry is what lets the bank attract enormous volumes of low-cost corporate operating deposits, because multinationals want their money to sit where the plumbing already reaches.

The second is switching costs, and it is embodied in a piece of software most people have never heard of: Straight2Bank, the bank's proprietary corporate platform for cash management, payments, trade, and payroll. Once a multinational treasurer has wired their company's global operations through Straight2Bank — integrating it with their internal systems, training their staff, building their reconciliation processes around it — ripping it out to switch banks is a project fraught with operational risk, the kind that can miss a payroll run in a dozen countries at once. The stickiness is not about loyalty; it is about the terror of breaking something that works. That is the strongest form of a switching-cost moat.

The third is the cornered resource, and here we return to where the story began: the Hong Kong banknote-issuing license and the web of institutional banking charters the bank holds across its markets. These are not advantages you can compete your way into. They are privileges granted by sovereign states, protected by regulation, and unavailable at any price to a would-be rival. It is the nineteenth-century Royal Charter, living on in twenty-first-century form.

Now run the same business through Porter's Five Forces, which asks not "what does the company have" but "how brutal is the industry." The threat of new entrants is extremely low — the capital, clearing access, and compliance apparatus required to build a globally systemic bank are a moat measured in decades and billions, and the fintechs nibbling at retail edges are nowhere near systemic scale. The bargaining power of customers is genuinely split: a Fortune 500 treasury can play banks against each other and squeeze pricing hard, but an affluent wealth client or a mid-market corporate that depends on Standard Chartered's specific market access has far less leverage. The bargaining power of suppliers — in a bank, that means depositors — is low, which is the quiet secret of the funding advantage: those sticky operational deposits sit in the bank because of what it does, not because it pays the highest rate, so the bank funds itself cheaply.

The forces that bite are the last two. The threat of substitutes is real and rising over the long term: digital payment networks, blockchain-based B2B settlement, and increasingly capable domestic banks all threaten to disintermediate the legacy trade-finance corridors that are Standard Chartered's heartland. And competitive rivalry is intense. The bank fights its far larger sibling 滙豐 HSBC — which occupies the same "British bank of Asia" niche but with roughly triple the balance sheet — plus American giants like Citigroup in transaction banking, and ferociously well-run local champions like DBS on their home turf. The verdict from both frameworks is consistent and worth stating plainly: Standard Chartered has a genuine, defensible moat in its plumbing and its franchises, but it operates in a bruising industry where the long-term substitution threat is the thing to watch, not the entrant threat. A moat is not the same as growth, and investors should not confuse the two.

VIII. The Takeover Stress Test, Activist Battles, and Valuation Disconnect

For years, a certain kind of investor has looked at Standard Chartered and seen not a bank but a sum-of-the-parts arbitrage waiting to be unlocked. The breakup thesis goes like this: the crown-jewel wealth and retail businesses in Hong Kong and Singapore are premium, high-return, capital-light franchises that would command a rich valuation if they stood alone — but they are trapped inside a conglomerate, weighed down and obscured by the capital-intensive, lower-return corporate network stretched across Africa and the Middle East. Separate the jewel from the setting, the argument runs, and the whole is worth far more broken up than it is today. It is the classic activist case against any sprawling financial holding company: complexity destroys value, so simplify or split.

The most concrete real-world test of what the bank might be worth came in early 2023. Reports emerged that First Abu Dhabi Bank, the UAE's largest lender and a vehicle backed by Gulf sovereign wealth, had been evaluating a bid for Standard Chartered. On 5 January 2023, FAB issued a statement saying it was no longer evaluating an offer.2 A month later, after the speculation and a share-price spike refused to die, FAB went further and formally ruled out a bid.16 The episode was brief, but it was clarifying, because it exposed exactly why Standard Chartered is so easy to fantasize about acquiring and so nearly impossible to actually buy.

Start with the regulatory wall. Standard Chartered is not just a big bank; it is a globally systemically important bank with a dollar-clearing operation in New York. Any acquirer — especially a Middle Eastern, sovereign-linked one — would need the blessing of the U.S. Federal Reserve, which guards access to the dollar-clearing system jealously and would look very hard at who ultimately controls a bank plugged into it. Layer on top the Bank of England's Prudential Regulation Authority, the Hong Kong Monetary Authority, and a dozen other national regulators, each with a veto over the change of control in its jurisdiction. A hostile or even friendly takeover would require threading approvals through roughly 50 distinct regulatory regimes simultaneously — a coordination problem that borders on the impossible.

Then add the complexity penalty. Even setting regulators aside, integrating and ring-fencing banking operations across dozens of jurisdictions, each with its own capital requirements, currency, and legal system, is an operational nightmare that could consume years and destroy value in the process. The FAB episode showed that the market will periodically get excited about a bid; the collapse of that episode showed why the excitement rarely survives contact with reality.

Which brings us to the most important strategic point, and Winters' actual answer to the activists. Rather than break up the bank or wait for a bidder who cannot clear the regulatory bar, management has been quietly running its own value-unlock program through the buyback. Here is the arithmetic, and it is genuinely powerful. When a company's stock trades at, say, 0.6x book value, every share the company buys back and cancels is bought for 60 cents on the dollar of the assets behind it. That instantly increases the book value and earnings attributable to each remaining share — buying back stock below book value is mathematically accretive to return on tangible equity and to per-share value. In effect, Winters has been capturing the very discount the activists complain about, on behalf of the shareholders who stay. It is a legitimate response, and it partly explains why activist pressure has cooled even as the discount persists. The open question — the one a short-seller would press — is whether buying back stock is a substitute for closing the valuation gap or merely a way of managing it indefinitely. If the market never re-rates, the buyback is a permanent tax the bank pays on its own cheapness.

IX. Playbook, Balanced Bull vs. Bear Spine, and Material Risks

Every long story eventually has to answer the only question that matters to an investor: from here, why does this company win, and what would break the case? Let us make the spine explicit and then test it, because the honest answer is that both sides have real evidence.

The bull case is that Standard Chartered has finally become the disciplined machine it always should have been. After a decade of surgery, it is a leaner corporate structure aimed at two genuinely attractive prizes: the cash-cow cross-border trade corridors that only a handful of banks can serve, and the high-margin, capital-light Asian wealth franchise that is compounding at double-digit rates. The 14.7% return on tangible equity delivered in FY2025 is not a rhetorical target but a reported result, achieved a year ahead of schedule, and the bank is converting that profitability into a torrent of buybacks and dividends.11 And the persistent discount to book value, on this reading, is not a warning but an opportunity — a wide margin of safety and a coiled spring for re-rating if the market ever decides to believe the numbers.

The bear case is that none of the cleanup changes the fundamental nature of the beast. Standard Chartered remains structurally chained to the most volatile credit cycles on earth and sits directly in the path of every emerging-market shock and geopolitical crossfire. The recent earnings surge owes a great deal to the global spike in interest rates, which handed every bank a windfall on the cheap deposits it holds. As rates fall, that windfall reverses: net interest margins compress, and the question is whether the growth in wealth fees can offset the fade in interest income fast enough. A permanent cooling of the Chinese economy, layered on top of a lower-rate world, could squeeze both engines at once. On this reading, the discount is not a mispricing at all — it is the market's rational assessment of a genuinely riskier, more cyclical business than its clean FY2025 headline suggests.

The independent verdict is that this is a real debate, not a settled one, and the risk radar sharpens why. Geopolitical risk is not abstract for this bank: its single largest profit engine sits in Hong Kong, deep inside the U.S.-China rivalry, while the bank must strictly obey U.S. Treasury sanctions — a needle it has already, expensively, failed to thread twice before. Chinese property contagion remains a live tail risk; the Bohai impairment showed that mainland real-estate weakness can reach the income statement through associate stakes, and no coverage ratio fully neutralizes an unknowable systemic event. And rate-cycle sensitivity is the mechanical risk hiding inside the good results — a large share of recent profitability is the easy income earned on excess deposits during a high-rate era that is now ending.

So what should a serious investor actually watch? Not the dozens of metrics in the annual report, but three signals that cut to the heart of the thesis. First, underlying Return on Tangible Equity — the single cleanest test of whether the 14.7% is a durable feature of a re-engineered bank or a rate-cycle peak, and whether it stays comfortably above the bank's cost of capital. Second, Wealth Solutions income growth — the momentum of the capital-light, high-margin fee engine that the entire re-rating case depends on; if that decelerates, the bull story loses its spine. Third, the CET1 ratio alongside payout volume — the Common Equity Tier 1 ratio measures the capital cushion protecting the bank, and management has guided to keeping it in a 13-14% range; watching it against the buyback and dividend outflow tells you whether the capital return is genuinely funded by surplus or is being pushed too far.11

The durable lessons of this story reach well beyond one bank. The first is the hubris of crisis survival: Standard Chartered emerged from 2008 convinced its underwriting was superior, and that very conviction led it to lend aggressively into the commodity cycle that nearly broke it. Surviving a macro shock you had no exposure to tells you nothing about whether you can survive a structural cycle you are standing right inside. The second is the long tail of compliance debt: the cash value of the sanctions fines was almost trivial next to the years of defensive paralysis they imposed — remediation of a broken compliance culture takes a decade, costs multiples of the headline penalty in lost business, and cannot be paid off in a single check. And the third is the listing disconnect that opened this story: a company can be listed in a Western market and operate entirely in emerging ones, and the gap between where its shares trade and where its business lives can persist for a very long time. Whether Bill Winters' successor finally closes that gap, or whether it proves to be a permanent feature of the empire's ledger, is the story's next chapter — and it has not yet been written.

References

-

First Abu Dhabi Bank says not evaluating offer for Standard Chartered — Reuters, 2023-01-05 ↩↩

-

Standard Chartered Hong Kong — banknote issuance — Wikipedia ↩

-

Standard Chartered replaces CEO Peter Sands with Bill Winters — Reuters, 2015-02-26 ↩↩↩↩

-

Standard Chartered in $340M Settlement on Iran Charges — Fox Business, 2012-08-14 ↩↩

-

Standard Chartered Bank Agrees to Forfeit $227 Million for Illegal Transactions with Iran, Sudan, Libya, and Burma — U.S. Department of Justice, 2012-12-10 ↩

-

FCA fines Standard Chartered Bank £102.2 million for poor AML controls — UK Financial Conduct Authority, 2019-04-09 ↩

-

Standard Chartered exits seven countries in Africa, Middle East — Reuters, 2022-04-14 ↩

-

Standard Chartered overhauls pay to tilt executive packages toward performance — Financial Times, 2024-03-05 ↩

-

Full Year 2025 Results — Standard Chartered, 2026-02-24 ↩↩↩↩↩↩↩↩

-

Standard Chartered reports 14.7% RoTE and announces $1.5 billion share buyback — The Asian Banker, 2026-02-24 ↩

-

Standard Chartered PLC Full Year 2024 Results Press Release — Standard Chartered, 2025-02-21 ↩↩

-

Standard Chartered hit by $850m China Bohai impairment — Financial Times, 2023-10-26 ↩

-

Standard Chartered profit misses on China Bohai Bank hit — Bloomberg, 2023-10-26 ↩

-

First Abu Dhabi Bank rules out fresh Standard Chartered bid after share spike — Financial Times, 2023-02-10 ↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube