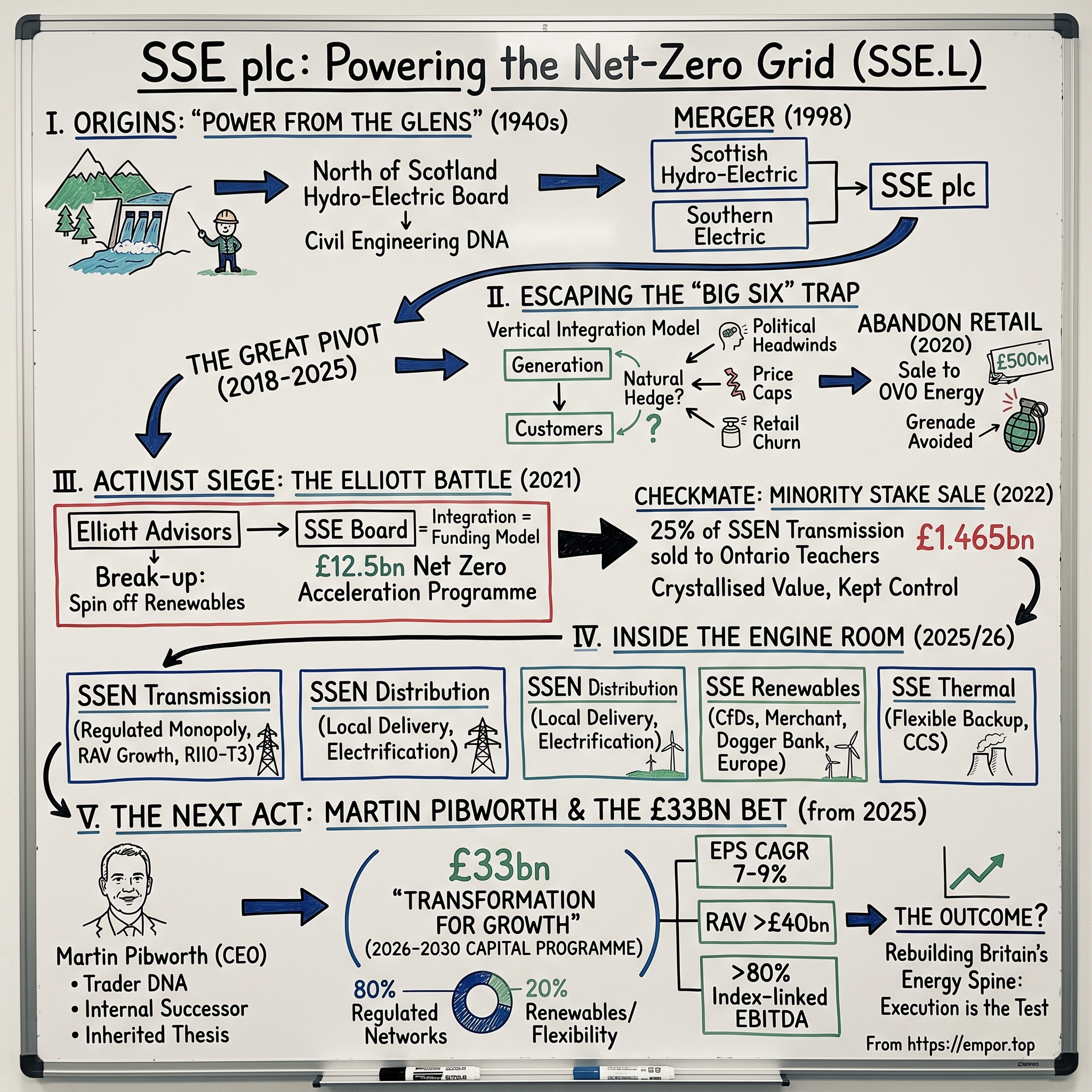

SSE plc: Powering the Net-Zero Grid

I. Introduction & Episode Roadmap

Picture the boardroom mood at SSE in the autumn of 2021. The company had just spent three years dismantling the business model that generations of managers had been taught to protect. It had sold its household energy supply arm. It had cut its dividend. And now, into that carefully rearranged house, walked Elliott Advisors — the New York activist fund that had bloodied Whitbread, AT&T, and half the FTSE — demanding that SSE tear the whole thing in two.9

The hook of the SSE story is this paradigm shift. For twenty years, the received wisdom in British energy was vertical integration: own the power stations, own the customers, and let the two hedge each other. SSE was a charter member of the "Big Six" suppliers that dominated UK households. And then management concluded that the retail customer — the very relationship the industry had fought to own — was a low-margin, politically radioactive distraction compared with the patient, compounding growth of regulated electricity networks and offshore wind.

The dramatic climax came when chief executive Alistair Phillips-Davies refused Elliott's demand to spin off SSE's renewables business. Instead of breaking the company apart to satisfy the activist's sum-of-the-parts arithmetic, he did something more surgical: he sold a 25% minority stake in the crown-jewel transmission network to Canada's Ontario Teachers' Pension Plan for £1.465 billion in cash, validating the network's value in public without surrendering control — and, in doing so, took the wind out of Elliott's sails.6

It is a genuinely interesting question whether that was the right call. The independent lens matters here: SSE's management won the argument, but winning an argument with an activist is not the same as being proven correct by the fundamentals. That verdict is still being written, and the £33 billion the company is now spending is the ultimate test of the thesis.

Here is the roadmap for the episode:

- The Origins — post-war nationalisation and "Power from the Glens."

- The "Big Six" Trap — the vertical-integration model and the pain of retail price caps.

- The Great Pivot — shedding consumer assets and restructuring the core.

- The Activist Siege — the battle with Elliott Advisors over structural separation.

- Inside the Engine Room — a segment-by-segment tour of SSEN Networks, SSE Renewables, and SSE Thermal.

- The Next Act — Martin Pibworth's ascent and the £33 billion "Transformation for Growth."

- The Playbook — Helmer's 7 Powers and Porter's 5 Forces applied to the moat.

- The Investment Spine — bull versus bear, the risk radar, and the KPIs that matter.

Let's begin where the water begins — in the Highlands.

II. The Origins: "Power from the Glens" & State Monopolies

In 1943, with the Second World War still raging and much of the northern Scottish Highlands unconnected to any electricity supply at all, a Labour politician named Tom Johnston pushed a remarkable piece of legislation through Parliament. Johnston, the Secretary of State for Scotland, believed electricity could do for the depopulating glens what nothing else had managed: keep people on the land. The Hydro-Electric Development (Scotland) Act 1943 received Royal Assent on 5 August that year, and out of it was born the North of Scotland Hydro-Electric Board.14

The Board's mandate was almost romantic in its ambition — to harness the rain and the mountains of the Highlands for the benefit of the people who lived there. Johnston chaired it from 1945 to 1959, and under a slogan that became folklore — "Power from the Glens" — the Board embarked on one of the great civil-engineering campaigns of post-war Britain.14 Engineers bored tunnels through granite mountains, threw dams across remote glens, and strung cable to crofts that had never seen a lightbulb. Dozens of hydro schemes rose across a landscape where the logistics alone — hauling turbines up single-track roads in a Highland winter — would have defeated a less determined enterprise.

Why does this matter to an investor looking at SSE in 2026? Because institutional DNA is real. The muscle that a company builds early tends to persist, and SSE's founding muscle was large-scale, capital-heavy civil engineering in hostile conditions. The ability to project-manage enormous, multi-year construction programmes through weather, terrain, and cost pressure was baked in from the beginning — and it is precisely the capability the company is now betting the house on with offshore wind and subsea cables. The hydro assets themselves, fully depreciated and still generating, remain quietly on the balance sheet decades later.

Then came Margaret Thatcher. The privatisation wave of the late 1980s and early 1990s swept through Britain's nationalised utilities, and Scottish electricity was no exception. The Board was reorganised — North of Scotland Electricity plc was formed in 1989 to take over its assets, promptly renamed Scottish Hydro-Electric plc — and floated on the London Stock Exchange in June 1991.14 For the first time, the glens' power belonged to shareholders.

The defining corporate marriage came in December 1998. Scottish Hydro-Electric merged with Southern Electric — a Regional Electricity Company serving the wealthy, densely populated south of England — to create Scottish and Southern Energy plc, later simply SSE.14 The industrial logic was elegant. The northern business was generation-heavy, rural, and growth-oriented; the southern business was a stable, cash-generative distribution network feeding millions of affluent homes. Bolting a high-growth generator onto a low-risk cash machine gave the combined group a balanced footprint and a network-plus-generation duality that, remarkably, still defines the company nearly three decades later.

There is a further legacy of the glens that rarely makes the headlines but sits quietly in SSE's back pocket: those Highland reservoirs and dams are natural sites for pumped-hydro storage — the technique of pumping water uphill when power is cheap and abundant and releasing it through turbines when it is scarce and expensive. In a grid increasingly reliant on intermittent wind, long-duration storage is one of the most valuable and hardest-to-replicate assets there is, and the geography SSE inherited from Tom Johnston's engineers gives it an option on that future that few rivals can match. It is a reminder that the deepest moats are sometimes eight decades old.

That duality — regulated networks on one side, power generation on the other — is the through-line of everything that follows. It is also, as we will see, exactly the structure an activist would one day try to smash apart. But first, SSE had to survive its most seductive strategic mistake: falling in love with the retail customer.

III. The Big Six Era: Vertically Integrated Conglomerates & Political Headwinds

By the 2000s, the entire British energy industry had converged on a single article of faith: to survive, you had to own both ends of the value chain. You generated the electricity upstream, you sold it to households downstream, and the theory went that when wholesale prices spiked, your generation profits would offset the squeeze on your retail margins — and vice versa. It was a natural hedge, elegant on a whiteboard, and every serious player adopted it.

SSE became one of the "Big Six" suppliers who came to dominate the UK household market, sharing the field with Centrica's British Gas, E.ON, ScottishPower (owned by Spain's Iberdrola), RWE's npower, and EDF. Together the six controlled the overwhelming majority of Britain's gas and electricity accounts. For a while it worked beautifully. SSE grew its supply base into the millions, cross-sold services, and enjoyed the reliable churn of a captive customer relationship.

Then the politics arrived. And in Britain, energy politics is a blood sport.

As household bills climbed through the early 2010s, the Big Six became a national villain. "Rip-off Britain" headlines multiplied. Politicians of every stripe discovered that few things won applause faster than accusing energy companies of profiteering off pensioners. The suspicion hardened into policy: the regulator, Ofgem, moved toward a cap on the standard variable tariff that most households paid — a price ceiling that fundamentally changed the economics of supply, converting a business that was supposed to be a hedge into a politically administered, low-margin utility with all the downside of consumer exposure and little of the upside.

The competitive ground was shifting underneath the incumbents at the same time. A wave of venture-backed challenger brands — Bulb, Octopus Energy, and dozens of smaller upstarts — stormed the market. They were asset-light software companies wearing energy-supplier costumes. They carried none of the legacy cost base, none of the ageing power stations, and none of the balance-sheet weight of the incumbents; they simply undercut on price and hoovered up switchers. The incumbents, saddled with heavy assets and public scorn, watched their most loyal customers get poached by brands promising a cheaper deal and a nicer app.

Into this deteriorating picture stepped Alistair Phillips-Davies, who became SSE's chief executive in 2013. A Cambridge-educated accountant by training who had joined the company in 1997 and worked his way up through its energy businesses, "APD," as he was universally known, inherited a sprawling machine. He had a generation fleet, a pair of regulated networks, a growing renewables ambition — and, bolted to the side, a capital-hungry, reputationally toxic, margin-compressed retail supply operation that was consuming management attention and dragging on the group's valuation.

The uncomfortable analytical truth was that the natural hedge no longer hedged. Price caps had severed the link between wholesale costs and retail prices; when wholesale prices rose, the cap prevented suppliers from passing the cost through fast enough, and the retail book bled. The industry's foundational logic had quietly inverted. The question was who would be first to admit it — and act.

This is where the story turns on a genuine strategic dilemma, the kind that separates competent managers from bold ones. Exiting retail was heresy. The entire industry, decades of orthodoxy, and most of SSE's own institutional memory said that owning the customer was the point — that generation without a captive demand base left you dangerously exposed to merchant power prices, and that scale in supply was a defensive necessity. To walk away from millions of customer relationships was to admit that a core competency the company had spent a generation building was, in fact, a liability. Incumbents almost never make that admission voluntarily; they defend the model that made them until the model kills them. The interesting analytical question for an investor is not whether SSE was clever in hindsight, but whether its leadership possessed the rare institutional willingness to declare a cherished business obsolete before the market forced its hand. On the evidence of what came next, it did — and that willingness to cannibalise its own history would become the single most important trait in the SSE story.

IV. The Great Pivot: Dumping Retail & Redefining the Core

The moment of truth arrived, as these things often do, through a deal that fell apart.

In 2017, SSE agreed to merge its household energy-supply business with the UK retail arm of Germany's Innogy, which owned npower. The plan was to hive off the combined retail operation as a separately listed company — a tidy way for SSE to reduce its consumer exposure without simply eating a loss. But the energy market moved against them. As wholesale conditions and the looming price cap eroded the commercial terms, the deal became less and less attractive, and in December 2018 the parties abandoned it.

For most executives, a collapsed transaction is a setback to be quietly managed. Phillips-Davies drew the opposite conclusion. If the market would not let him spin retail off, he would get out of it altogether. It was a genuinely counter-consensus call — the rest of the Big Six were still clinging to vertical integration — and it set the direction for everything that followed.

In January 2020, SSE completed the sale of SSE Energy Services, the household supply business carrying roughly 3.5 million customer accounts, to the challenger brand OVO Energy. The headline price was £500 million — £400 million in cash and £100 million in loan notes — and the deal moved around 8,000 employees off SSE's books and onto OVO's.8

Now, judged purely as a financial transaction, this was not a triumphant multiple. Half a billion pounds for 3.5 million accounts is a modest price, and a shareholder looking only at the sticker would grumble that SSE sold cheap. But the strategic value has to be measured against what happened next, and the timing turned out to be extraordinary. Within eighteen months of the sale, Europe plunged into the 2021–2022 energy crisis. Wholesale gas prices exploded, the price cap trapped suppliers on the wrong side of their hedges, and the UK retail energy sector simply detonated. Dozens of suppliers went bankrupt — Bulb, the poster child of the challenger era, collapsed into a government-funded special administration. Retail supply proved to be exactly the balance-sheet grenade Phillips-Davies had suspected it was.

By selling when he did, SSE side-stepped the bad-debt write-downs, the hedging losses, and the regulatory chaos that engulfed the businesses that stayed. This is where the independent analyst should be fair to management: the price was unimpressive, but the decision was vindicated by events in a way few strategic calls ever are. Getting the direction right and the timing lucky is still worth a great deal.

There is a subtler prize hidden in the retail exit, and it is one that fundamental investors should weigh carefully: the strategic re-rating opportunity. A conglomerate that mixes a politically toxic, low-margin consumer business with high-quality regulated assets and green generation tends to trade at the multiple of its ugliest part. Investors apply a discount for complexity, for headline risk, and for the sheer difficulty of valuing a business that is three unrelated things at once. By amputating the consumer arm, SSE did not merely dodge the coming crisis — it cleaned up the equity story. It could now present itself to the market as a focused infrastructure and green-generation compounder, the kind of business that attracts patient capital, ESG mandates, and infrastructure funds willing to pay up for predictable, inflation-linked cash flows. Whether the market has fully awarded that re-rating is debatable — utilities remain unloved in a higher-rate world — but the option on a cleaner multiple was created by the exit, and it cost shareholders only a modest sale price to buy. In capital-allocation terms, that is a favourable trade even before the crisis-avoidance bonus is counted.

With the consumer albatross gone, SSE rebuilt its identity around two pillars, both aligned to the same secular tailwind — the decarbonisation of the energy system. The first was regulated electricity networks: the wires and pylons that Ofgem allows the company to earn a set return on. The second was low-carbon generation: wind, hydro, and the flexible gas plants that back them up. Capital, management attention, and the corporate story were all re-routed toward those two engines.

It was a cleaner, more focused SSE. But focus attracts attention — and the most dangerous kind of attention was about to arrive from across the Atlantic.

V. The Activist Siege: Defeating Elliott Advisors

In the autumn of 2021, word began to circulate through the City that a new name had appeared on SSE's share register — and not a passive one. Elliott Advisors, the European arm of Paul Singer's Elliott Management, had built a stake reported to make it one of SSE's top-five investors, and it had a thesis it wanted the world to hear.10

Elliott's argument was seductive in its simplicity, and it was the same sum-of-the-parts logic that had made the fund billions elsewhere. Look at SSE, Elliott said, and you see two utterly different businesses stapled together. On one side, a fast-growing renewables developer — the sort of green-energy pure-play that public markets, at the peak of the ESG boom, were valuing at dizzying multiples, the way they valued Denmark's Ørsted or Spain's EDP Renováveis. On the other, a stodgy regulated network business trading at a utility multiple. Bolted together inside one conglomerate, Elliott argued, the whole was worth less than the parts — a classic conglomerate discount. Split SSE Renewables off into its own listed company, the fund contended, and you would unlock billions in trapped value; Elliott put the number at around £5 billion.9

SSE's board pushed back, hard and publicly. Phillips-Davies and chairman Sir John Manzoni made an argument rooted in the physics of capital, not the arithmetic of multiples. The stable, regulated, inflation-linked cash flows of the transmission and distribution networks, they argued, were not dead weight — they were the ballast. Those predictable cash flows underpinned SSE's investment-grade credit rating and its low cost of capital, and it was precisely that cheap, dependable balance sheet that allowed the group to fund the high-risk, multi-billion-pound equity commitments that deep-water offshore wind demanded. Rip the two apart, and the renewables business would lose its financial anchor while the networks lost their growth engine. Integration, in this telling, was not laziness. It was the funding model.

There is a real debate to be had about which side was right, and a skeptic would note that "we need the networks to fund the wind" is also a convenient argument for a management team that would rather run a bigger empire than a smaller one. But SSE did more than argue. In November 2021 it pre-empted Elliott by unveiling a £12.5 billion Net Zero Acceleration Programme — a concrete, capital-backed alternative to a break-up, designed to show shareholders that the integrated group could deliver growth without dismemberment.9 It later expanded the ambition further as the plan evolved.

Then came the checkmate. Rather than spin off the crown jewel, SSE reached for a scalpel. In November 2022 it agreed to sell a 25% minority stake in SSEN Transmission — the high-voltage network in the north of Scotland — to the Ontario Teachers' Pension Plan Board for £1.465 billion in cash, with completion confirmed at the end of that month.67 The deal was a masterclass in having it several ways at once. It priced the transmission business at a gross enterprise value of roughly £5.86 billion — a healthy premium to its regulated asset value — thereby validating in a real, cash transaction exactly the hidden network worth that Elliott claimed was trapped.6 It raised a large slug of capital to fund the investment programme without diluting ordinary shareholders. And crucially, SSE kept majority control and full operational command, with Ontario Teachers taking only proportionate board representation.7

The elegance was that it answered Elliott's valuation point without conceding Elliott's structural demand. If the market doubted the networks were worth more than the accounts implied, here was a sophisticated Canadian pension fund paying a premium to prove otherwise. The pressure dissipated, and Elliott faded from the story without ever forcing the demerger it had sought.

It is worth understanding why this worked, because the mechanics reveal a deeper truth about activist campaigns. Elliott's leverage came entirely from the perception of hidden value — the claim that the market was mispricing SSE's parts. Perception, however, is fragile: it evaporates the moment a real transaction sets a real price. By selling a minority stake at a premium to regulated asset value, SSE did not just raise cash; it converted Elliott's strongest rhetorical weapon into a settled fact and then pocketed it. An activist arguing "the networks are worth more than you think" has nowhere to go once a buyer has already paid more than the book. The genius, such as it was, lay in monetising the argument rather than the asset — selling a quarter of the value to validate the whole, while giving up none of the control that a full demerger would have surrendered. Whether SSE's integrated structure is genuinely superior on the fundamentals remains a fair question; what is not in doubt is that management out-manoeuvred one of the most feared funds in the world on the terrain of financial engineering, which is precisely Elliott's home turf. That, in the annals of European corporate defence, is a rare scalp.

For investors, the episode revealed something durable about how SSE's leadership operates: a preference for partial disposals and minority partnerships that raise capital and crystallise value while retaining control — a playbook the company would return to again and again. It kept the house intact. The question was whether the house was worth keeping. To answer that, you have to go inside it.

VI. Inside the Engine Room: Segment Economics & Profit Engines

Strip away the corporate narrative and SSE is, at heart, a portfolio of very different money-making machines running on very different rules. Some earn regulated returns set by a government body. Some earn subsidised returns guaranteed by long-term contracts. And some earn nothing but the raw, volatile spread of the wholesale power market. Understanding how each one makes money — and how much — is the whole game. Let's open the hood.

SSEN Transmission — The Grid Backbone

Start with the crown jewel, the business Ontario Teachers paid a premium to co-own. SSEN Transmission owns, operates, and maintains the high-voltage transmission system across the northern third of Scotland — the pylons and, increasingly, the subsea cables that carry bulk power from where it is generated to where it is consumed.

The economics are the closest thing to a licence to print money that exists in legitimate business — with an asterisk. It is a regulated natural monopoly. Nobody is going to build a competing set of pylons across the Highlands. Ofgem, the regulator, sets the rules through multi-year price controls — the current framework is RIIO-T2, transitioning to the tougher RIIO-T3 period.20 Here is the mechanism in plain terms: every pound of approved capital that SSEN Transmission invests gets added to its Regulated Asset Value, or RAV, and the company is then permitted to earn a set return on that asset base plus recover its costs. Invest more, grow the RAV, grow the allowed earnings. It is a compounding machine, provided the regulator keeps approving the spend — and provided the company can physically build it.

The engine is roaring. Transmission's adjusted operating profit surged around 74% to £562.6 million in the year to March 2025, driven by the sheer volume of investment going into connecting Scottish wind to the grid.5 By the year ended 31 March 2026, the networks businesses — with transmission leading — had grown to represent roughly 40% of group profit.4 The asterisk, always, is the regulator: allowed returns are a political and technical negotiation, and a stingier settlement would slow the compounding.

And in 2025, that asterisk turned into a genuine confrontation — one worth dwelling on, because it shows exactly how the regulated model can bite. On 1 July 2025, Ofgem published its draft determination for RIIO-T3, the price control that governs transmission from April 2026 to March 2031.19 SSEN Transmission's response was unusually pointed for a regulated monopoly that normally treads carefully around its own regulator: the draft, it said, "does not go far enough to deliver the investible, financeable and ambitious framework required."19 Translated from the diplomatic, that meant the proposed allowed return was too thin to justify the enormous equity SSE was being asked to sink into the grid. The regulator and the company then spent five months negotiating in public. When Ofgem published its final determination on 4 December 2025, it landed the allowed return on equity for electricity transmission at 5.70% on a CPIH-real, post-tax basis — an improvement on the draft but still below what the networks had lobbied for — while approving £28.1 billion of upfront funding across the sector for the period.21 SSEN's response softened to a careful welcome of the improved cost allowances, paired with the caveat that it still needed to assess the "overall investability" of the package.24 For an investor, this episode is the whole regulated-returns bargain in miniature: the monopoly is protected from competition, but its profitability is set by an official with a spreadsheet and a political mandate to keep bills down — and roughly every dozen basis points of allowed return, multiplied across a £30 billion asset base, is real money that flows to shareholders or to consumers depending on who wins the argument.

SSEN Distribution — The Local Delivery System

If transmission is the motorway, distribution is the network of local roads. SSEN Distribution runs the lower-voltage wires that deliver electricity to homes and businesses across northern Scotland and central southern England — the geographic echo of that 1998 merger. It, too, is a regulated monopoly, governed by a separate price control, RIIO-ED2.

Distribution is a useful lesson in how regulated earnings actually behave, because they are not a smooth line. The segment earned an unusually high £736 million in the year to March 2024, a figure inflated by non-recurring inflation adjustments baked into the regulatory formula. The following year it dropped to £335.3 million.5 A casual reader sees a business falling apart; the reality is a business whose allowed revenue is recalculated in steps, with true-ups and timing effects that make any single year a poor guide to the trend. The signal for investors is that regulated earnings are predictable over a price-control period but lumpy within it — you have to look through the annual noise to the RAV growth underneath.

Distribution also carries an under-appreciated growth story of its own. If transmission is about moving bulk wind power from north to south, distribution is about absorbing the coming surge in local electricity demand as Britain electrifies. Every heat pump that replaces a gas boiler, every electric vehicle plugged into a driveway, and every data centre wired into a business park lands on the distribution network — and much of it requires the network to be reinforced, upgraded, and extended. That, too, feeds the regulated asset base. So while transmission is the headline compounder, distribution is a quieter second engine geared to the demand side of the same transition. The risk cuts both ways: if electrification of heat and transport proceeds more slowly than the official net-zero pathway assumes — and consumer take-up of heat pumps in particular has consistently lagged government hopes — then some of the distribution investment case softens. The RAV grows on approved spending, but approved spending ultimately has to be justified by demand that actually shows up.

SSE Renewables — The Generation Engine

Now for the business Elliott wanted to set free. SSE Renewables is the leading owner-operator of renewable generation across the UK and Ireland — a fleet spanning onshore and offshore wind and the old, faithful hydro assets that trace all the way back to Tom Johnston's glens.

The portfolio contains genuine trophies. Seagreen, off the Angus coast, is Scotland's largest offshore wind farm and the world's deepest fixed-bottom project, with SSE holding a 49% stake in its roughly 1.1 GW of capacity.16 Viking, a wholly owned 443 MW onshore wind farm on the wind-battered islands of Shetland, is one of the most productive onshore sites in Europe. And the headline act is Dogger Bank — a colossal 3.6 GW development being built in three 1.2 GW phases far out in the North Sea, structured as a joint venture in which SSE holds 40% alongside Norway's Equinor (40%) and Vårgrønn (20%), and destined to be the world's largest offshore wind farm.16

SSE also went shopping for European growth. In 2022 it acquired Siemens Gamesa's Southern European onshore development platform for €580 million — a pipeline of roughly 3.9 GW of onshore wind projects concentrated in Spain with more across France, Italy, and Greece, plus co-located solar potential.15 The timing was interesting: buying development optionality on the Continent just as offshore turbine and vessel supply chains were tightening was a way of diversifying beyond a UK-and-Ireland concentration, though it is optionality that still has to be converted into built, earning assets to justify the price.

How does renewables actually earn? Two ways. Much of the output is locked into long-term, government-backed Contracts for Difference, or CfDs — a clever subsidy design that works like a two-way price floor and ceiling: if market power prices fall below the contracted "strike price," the government tops the generator up; if they rise above it, the generator pays the difference back. It converts famously volatile power revenues into something bond-like and bankable.

But the CfD machine is only as reliable as the auctions that feed it — and here the recent history is a cautionary tale about the limits of the model. In September 2023, the UK's fifth CfD auction round (AR5) produced a genuine shock: not a single megawatt of new offshore wind secured a contract. Developers simply refused to bid, because the government's administrative maximum price of around £44/MWh had been set before the supply-chain and financing costs of turbines, steel, and vessels exploded, and no serious player would lock in a fixed price below the cost of building.17 It was an object lesson that a subsidy floor set too low is no floor at all. The government absorbed the humiliation and reset. The following year's AR6, in 2024, raised the ceiling and revived the market, with new offshore projects clearing at around £58.87/MWh.22 And in the seventh round announced in January 2026, SSE itself secured a contract for roughly 1.4 GW of its Berwick Bank project at a strike price of £89.49/MWh — a striking illustration of how far the "bankable" price of new offshore wind had climbed in three years as the industry repriced its costs.23 The lesson for investors is that CfDs de-risk revenue only after a project wins one at an economic price; the auction itself is a gauntlet, and the strike prices needed to make new offshore wind viable have been marching upward, not down.

The rest of the output is sold merchant into the market, hedged by SSE's trading desk. The division generated £1,076.4 million of adjusted operating profit in the year to March 2025, and profits rose around 4% in the year to March 2026 despite weaker wind conditions — a reminder that this business's single biggest uncontrollable input is literally the weather.54

SSE Thermal — The System Stabilizer

Here is the paradox at the heart of the green transition, and SSE Thermal is where it lives. When the wind does not blow and the sun does not shine — the Germans have a wonderfully bleak word for it, Dunkelflaute, the "dark doldrums" — somebody has to keep the grid from going dark. That somebody, for now, is flexible gas-fired generation.

SSE Thermal runs modern, efficient gas plants whose economic value is not steady output but availability: they earn their keep by firing up precisely when renewable output collapses and power prices spike. That makes them highly cash-generative in periods of volatility and quiet in periods of calm. The segment contributed £195.4 million in the year to March 2025.5 In the year to March 2026, the broader "Flexibility" grouping — thermal and related businesses — saw profits fall around 15% as market conditions normalised from the extreme volatility of the crisis years.4 Thermal is also SSE's laboratory for what comes next: it is developing carbon capture and hydrogen-ready projects such as Keadby 3 and Peterhead 2, betting that the backup fleet of the future will need to be low-carbon too.

Gas Storage — The Small, Volatile Hedge

Finally, the odd corner of the empire: fast-cycling gas storage in underground salt caverns at Atwick and Aldbrough. It is a small business and, when price spreads are thin, a loss-making one — it posted a £37.1 million adjusted operating loss in the year to March 2025.5 It survives in the portfolio less for its earnings than as a commercial hedging tool, a reminder that not every asset in a conglomerate needs to be a star to be useful.

Add it all together and the picture is of a company deliberately rebalancing away from the volatile, weather- and market-dependent generation businesses toward the steady compounding of regulated wires. Which is exactly the bet the new chief executive was about to supersize.

VII. The Next Act: Martin Pibworth and the £33 Billion Bet

On 17 July 2025, at SSE's annual general meeting, Alistair Phillips-Davies handed over the keys. After twelve years as chief executive — years in which he had dumped retail, survived an activist, and rewired the company's entire strategy — APD stepped down from the board, remaining with the group only until later that autumn.12 It was, by the standards of British corporate life, an orderly and long-signalled succession; his retirement had been announced back in November 2024.11

His successor was not a parachuted-in outsider but the ultimate insider. Martin Pibworth joined SSE in 1998 — the very year the Scottish and Southern merger created the modern company — and he joined it as an energy trader.11 That detail matters. Over nearly three decades he rose through the commercial heart of the business, joining the executive committee in 2012 and the board in 2017, and latterly serving as chief commercial officer with oversight of renewables, thermal, energy markets, and customer solutions.11

Pibworth's profile is that of a market operator rather than an engineer or an accountant. He came up understanding how power is traded, hedged, and physically dispatched — how the machine actually earns money hour by hour in a volatile market. For a company whose future rests on both building enormous assets and monetising their output through CfDs and merchant hedging, a chief executive who cut his teeth on the trading floor is a logical, arguably reassuring, choice. His base salary was set at £970,000, rising to £1,050,000 from April 2026 — with the analytical caveat that continuity appointments, however sensible, rarely bring the fresh challenge to strategy that an outsider might.12 He inherits, and now owns, the thesis rather than questioning it. Barry O'Regan, appointed chief financial officer in December 2023, completes the top team.

The results Pibworth inherited set the scene for the ambition to come. In the year to 31 March 2026 — his first as chief executive — SSE reported adjusted operating profit of around £2,237 million, roughly 8% lower than the prior year, with statutory operating profit down about 4% to £1.8 billion.18 On the surface, a company announcing its largest-ever investment plan while profits dipped looks incongruous. Underneath, the numbers told the transition story precisely: networks profit rose as the grid build accelerated, renewables edged up around 4% despite a poor wind year, and the "Flexibility" businesses fell about 15% as the extreme power-price volatility of the crisis years faded.4 Capital investment jumped 23%, with regulated networks absorbing roughly 72% of the total spend — a foretaste of the mix the new plan would enshrine.4 Adjusted net debt and hybrid capital stood at around £10.1 billion.4 This is what a company mid-metamorphosis looks like: current earnings treading water while capital pours into assets that will not fully earn for years. Whether that is disciplined investment or value destruction depends entirely on execution — which is the crux of everything that follows.

Then, in his first major act as chief executive, Pibworth went big.

"Transformation for Growth"

On 12 November 2025, alongside the interim results, SSE unveiled a strategic plan it branded "Transformation for Growth" — and at its centre sat a number designed to command attention: a fully-funded £33 billion capital investment programme over the five years to 2029/30.1 That is roughly three times the £11 billion the group had spent in the prior five-year window; it is one of the largest private-sector infrastructure commitments in the UK.1

The most revealing feature of the plan is not its size but its shape. Around 80% of the money — some £27 billion — is directed at regulated UK electricity networks, with the balance of roughly 20%, about £6 billion, going selectively into renewables and system flexibility.1 Broken down further, SSEN Transmission alone is slated for around £22 billion, distribution around £5 billion, renewables around £4 billion, and thermal around £2 billion.2 Pause on that. This is a company that fought an activist to protect its renewables business — and is now pouring four times as much capital into wires as into wind. The energy transition, as SSE now reads it, will be won less at the turbine than at the pylon: the binding constraint is getting Scottish wind power down to English demand centres, and that means grid.

The logic behind this tilt is worth unpacking, because it is not merely a bet on where demand is greatest — it is a bet on where the returns are safest. Networks earn a regulated return regardless of the weather, the power price, or the vagaries of a CfD auction; renewables earn only if the wind blows, the auction clears at an economic price, and the project gets built on budget. Having spent 2023 to 2025 watching offshore wind absorb blow after blow — the failed AR5 auction, turbine cost inflation, blade failures, and construction delays — SSE's capital allocators reached a conclusion that would have been heretical to the ESG bulls of 2021: the lower-risk, lower-glamour wires business is the better place to compound shareholder capital. It is a quiet vote of no-confidence in the idea that offshore wind is a reliable growth engine on its own, and a bet that the safest way to profit from the energy transition is to own the toll road rather than the traffic. Sceptics will note the irony that this is close to the position Elliott implicitly rejected — that networks, not renewables, are the crown jewel. Management would counter that it is deploying capital where the risk-adjusted returns are best, which is exactly what capital allocators are supposed to do. Both can be true.

The targets attached to the plan are specific enough to be testable, which is what an independent analyst wants. Management is guiding to an adjusted earnings-per-share compound annual growth rate of 7–9%, reaching 225–250 pence by 2029/30 — a step-up of roughly 50% over the plan.3 Underpinning it, gross RAV in the networks businesses is projected to more than treble to around £40 billion by the end of the decade, with transmission's RAV alone heading toward £30 billion — an implied compound growth rate of roughly 30% a year.3 By the plan's end, management expects around 80% of group EBITDA to be index-linked, meaning inflation-protected regulated earnings.3 That is the whole strategic bet in one statistic: SSE is deliberately converting itself from a weather-exposed generator into an inflation-linked, regulated-asset compounder.

Paying For It

A £33 billion programme has to be funded, and here management leaned on the credibility of its balance sheet. The plan is underpinned by roughly £21 billion of operational cash flow, about £14 billion of new debt and hybrid capital, around £2 billion of asset sales, and — the piece the market watched most nervously — a £2 billion equity raise.1 SSE launched an equity placing of new shares alongside the November announcement to help fund the step-up.13 For a company that had spent years telling shareholders it could grow without dilution, tapping them for £2 billion of fresh equity was a notable concession — a signal that the ambition had outrun what cash flow and debt alone could support, and a reasonable thing for a skeptic to press management on.

Discipline and the Dividend

Two things anchor management's credibility here. The first is compensation alignment: executive directors are required to hold shares worth at least 300% of base salary, tying their personal wealth to the outcomes of these enormous capital-allocation decisions. The second, and more revealing, is the dividend history. Back in 2021, as part of the pivot, the board took the painful decision to rebase the dividend down from its high-yielding legacy levels — a move that stung income investors who had owned SSE precisely for its yield. But management then did what credible teams do: it set a clear post-rebase policy and delivered against it. SSE is targeting annual dividend growth of 5–10% from a 64.2 pence baseline for 2024/25, and in the year to March 2026 it paid a full-year dividend of 68.7 pence, up 7% — comfortably inside its own guidance.34

That pattern — take the pain, reset expectations, then hit the reset targets — is the strongest evidence in the file that management does roughly what it says. The £33 billion plan asks investors to extend that trust across a much longer and riskier runway. Whether the trust is warranted depends on whether SSE actually has a moat worth pouring £33 billion into. So let's war-game it.

VIII. The Playbook: Hamilton Helmer's 7 Powers & Porter's 5 Forces

Every capital-allocation story eventually reduces to one question: can the company earn returns above its cost of capital, and can it keep doing so when competitors, regulators, and customers all try to compete those returns away? Two frameworks help stress-test SSE's answer.

Hamilton Helmer's 7 Powers

Scale Economies (Networks). The most durable power SSE holds is the plainest. SSEN Transmission is a legal and physical monopoly across the north of Scotland. The capital required to duplicate a high-voltage transmission network, combined with the regulatory consents needed to build one, makes entry not merely uneconomic but effectively impossible. No rational competitor would string a parallel set of pylons across the Highlands to compete for the same load. This is as close to an impregnable barrier as exists in any industry — the catch being that the monopoly's returns are capped by the very regulator that protects it. The moat is deep, but Ofgem controls the drawbridge.

Cornered Resource (Seabed Rights & the Grid Queue). SSE's second power is control over genuinely scarce inputs. Prime seabed — locations with high, consistent wind yields and manageable water depths — is finite, and SSE has secured premier rights through the ScotWind leasing round and earlier auctions. Arguably more valuable, and less appreciated, is priority position in the grid-connection queue. In a system where hundreds of projects are waiting years for a connection date, an early, secured slot is a cornered resource in its own right. A rival can raise capital and buy turbines; it cannot manufacture a shallow, windy patch of the North Sea that is already spoken for, nor jump the connection queue.

Counter-Positioning. This is the subtlest of SSE's powers, and it flows directly from the retail exit. By cleanly leaving household supply before the 2021–2022 crisis, SSE positioned itself as a clean, pure-play green-infrastructure investment at exactly the moment rivals such as Centrica were consumed by retail chaos. A competitor still wedded to a large consumer supply book could not credibly pitch the same story without first inflicting on itself the very pain SSE had already absorbed. That is counter-positioning: an incumbent's existing business model makes it reluctant to copy the disruptor's move.

The remaining Helmer powers — network economies, switching costs, branding, and process power — are largely absent or weak for SSE, and it is more honest to say so than to force the framework. Electricity is an undifferentiated commodity; there is no brand premium on an electron and no customer lock-in in a wholesale market. SSE's moat is real but narrow: it rests on regulated monopoly, scarce physical rights, and a well-timed strategic repositioning — not on any hold over end customers.

Porter's 5 Forces

Threat of New Entrants — Very Low. The combination of monopoly network structures and multi-billion-pound capital requirements restricts the field to a handful of global utility and infrastructure titans. This is not an industry a start-up disrupts.

Bargaining Power of Suppliers — High. Here is the genuine vulnerability. The market for offshore wind turbines and the specialised vessels that install them is a tight oligopoly — Vestas, Siemens Gamesa, GE, and a short list of marine contractors. When supply chains tighten, as they did through 2023–2025, developers like SSE are price-takers on their single largest cost, and project economics and timelines are hostage to suppliers they cannot replace. This is the force most likely to damage returns.

Bargaining Power of Buyers — Low. Regulated network revenue is collected through national tariffs; there is no "customer" who can negotiate it down. And generation output is largely insulated by long-term, government-backed CfDs. SSE has engineered away most buyer power by design.

Threat of Substitutes — Very Low. Low-carbon electricity is the non-negotiable energy carrier for a decarbonising economy — the fuel for electrified heat, transport, and industry. There is no substitute waiting in the wings; if anything, demand for the product is structurally set to rise.

Rivalry Among Competitors — Moderate and Bifurcated. In the geographic network businesses, rivalry is essentially nil — monopoly is monopoly. But in the contested arenas — seabed auctions, CfD allocation rounds, the scramble for scarce turbines and vessels — competition among the global developers is fierce and can compete away project returns before a single turbine spins.

The net read is a business with an exceptionally strong position on four of the five forces and a single, serious exposure — supplier power over the offshore-wind supply chain. Which is precisely why the £33 billion plan tilts so heavily toward regulated networks, where the moat is deepest, and away from the offshore wind where SSE is most exposed. The strategy, viewed through Porter, is management steering capital toward its strongest forces.

The Competitive Landscape

It helps to place SSE against the field, because the same forces that shape SSE shape its peers very differently — and the contrasts are instructive. National Grid, SSE's closest listed analogue in the UK, is the purer network play: after selling down its gas businesses, it is now overwhelmingly a regulated wires-and-pylons compounder, and it faced the identical RIIO-T3 negotiation with Ofgem. SSE's networks look much like National Grid's, but SSE bolts on a generation business National Grid lacks — more upside if renewables deliver, more volatility if they do not. At the opposite pole sits Denmark's Ørsted, the pure-play offshore-wind champion that Elliott held up as the valuation SSE should aspire to; Ørsted's subsequent, brutal write-downs on un-hedged US offshore projects became the cautionary tale that retrospectively vindicated SSE's decision to keep its networks ballast. Iberdrola's ScottishPower and Germany's RWE and E.ON offer variations on the integrated theme, each balancing networks and generation on different ratios. And then there is Centrica — the mirror image of SSE, the company that stayed wedded to household supply and was duly savaged by the retail crisis before staging its own recovery. Set side by side, SSE occupies a deliberate middle ground: more diversified and lower-risk than Ørsted, more growth-exposed than National Grid, and structurally cleaner than the retail-heavy Centrica. Whether that middle ground is the best of both worlds or a diluted version of each is exactly the debate an investor has to resolve. It is also the final question we have to answer.

IX. The Investment-Story Spine: Bull vs. Bear & Risk Radar

Every long-term investment case can be reduced to a single confrontation: why this company wins from here, and what could break it. Let's put both sides on the table and stress-test each.

The Bull Case — "Why We Win"

One: regulated cash flows funding option value. The heart of the bull case is the machine described earlier — inflation-linked, regulated network cash flows, validated in hard cash by the Ontario Teachers transaction, that grow predictably, support an investment-grade credit rating, and fund the equity portions of higher-return generation projects. If SSE hits its target of around 80% index-linked EBITDA by decade's end, it becomes something rare: a growth stock with a bond-like earnings floor. That combination is genuinely hard for the market to replicate.

Two: structural position at the physical bottleneck. SSE's Scottish transmission network sits at the exact chokepoint of Britain's energy transition — the wind blows hardest in the north, the demand sits in the south, and the electrons have to travel down SSE's wires to get there. As long as the UK's legally binding net-zero targets stand, double-digit RAV growth is close to underwritten by government policy rather than by SSE's own commercial guesswork. The demand for what SSE builds does not depend on winning customers; it depends on the law of the land.

Three: a proven ability to build. The bull points to Seagreen, Viking, and the early phases of Dogger Bank as evidence that SSE can actually execute the enormous, complex programmes that sink smaller developers. In an industry where the graveyard is full of announced projects that never got built, demonstrated delivery capability — that founding Highland engineering muscle — is a real edge.

The Bear Case — "Why We May Not"

One: the supply chain can break the build. The bear's first and best argument is that offshore wind construction is brutally hard and getting harder. Dogger Bank has suffered well-publicised delays through 2024 and 2025 — adverse North Sea weather, scarce installation vessels, and, across the industry, high-profile turbine blade failures. Every month of delay pushes back cash generation and inflates cost. The very supplier power identified in the Porter analysis is not theoretical; it has already bitten the flagship project.

Two: capital intensity meets the cost of capital. Spending £33 billion is only attractive if you can finance it cheaply. In a higher-for-longer interest-rate world, the arithmetic of a heavily leveraged, capital-hungry infrastructure plan gets uncomfortable: every rise in the cost of debt compresses the spread between allowed returns and financing costs, and the £2 billion equity raise is a reminder that the plan already stretches the balance sheet. Refinancing £14 billion of new debt and hybrid capital over five years is a live risk, not a footnote.

Three: the regulator and the taxman hold the pen. SSE's greatest strength — regulated returns — is also its greatest dependency, and the point is no longer hypothetical. Ofgem's RIIO-T3 final determination in December 2025 set the allowed return on equity for transmission at 5.70% (CPIH-real), better than the draft but below what SSEN had argued was needed to make the framework "investible."2124 Every fraction of a percent of allowed return, compounded across an asset base heading toward £30 billion, is a large sum — and the company does not control the pen that sets it. Add the political temptation to extend windfall levies on generators — the UK's Electricity Generator Levy was exactly this kind of intervention — and a meaningful slice of the economics sits at the mercy of decisions made in Whitehall and at the regulator, not in SSE's boardroom. The bull says a monopoly with government-underwritten growth is the safest place to be; the bear says a business whose returns are legislated is a business whose returns can be legislated away.

The Activist Stress Test

A skeptical long/short investor would press three points. First, the strategy shifted dramatically — from defending an integrated renewables-and-networks group against Elliott to pouring 80% of capital into networks and demoting renewables to a £4 billion afterthought. Is that vindication of the integrated model, or a quiet admission that the offshore-wind growth story was never as valuable as claimed? Second, the £2 billion equity raise, after years of "we can grow without dilution," is precisely the kind of promise-then-pivot that activists pounce on. Third, the whole edifice depends on a regulator's goodwill and a government's policy consistency — a lot of trust to place in Westminster. None of these is fatal, but all three deserve to sit in the file alongside the bull case.

Risk Radar

Beyond the headline debates, two specific mechanisms bear watching. Input-cost inflation: escalating steel and copper prices feed directly into the cost of subsea cables, transformers, and pylons, and can erode the returns on capital that has already been committed at lower assumed costs. The grid connection queue: the same bottleneck that is a cornered resource for SSE's own projects can also delay them — physical constraints on connecting new assets to the wider network can push back the cash flows the whole plan depends on.

The Three KPIs That Matter Most

Cutting through the complexity, three metrics tell an investor almost everything about whether the thesis is on track:

- RAV growth rate. Is SSEN Transmission adding regulated assets on the schedule needed to reach roughly £40 billion of gross networks RAV by 2030? This is the compounding engine; if it stalls, the EPS target falls with it.

- Renewable capacity build rate (GW installed). Is SSE bringing wind capacity — especially the Dogger Bank phases — online on time, or is the supply chain causing slippage? Delivered gigawatts are the truth serum for the execution story.

- Return on Regulated Equity (RoRE). Is SSEN beating Ofgem's baseline allowed return through operational efficiency and incentive performance? Outperformance here is the difference between a monopoly that merely earns its cost of capital and one that compounds above it.

Watch those three and the annual noise — a weak wind year, a lumpy distribution true-up — mostly falls away.

X. Epilogue & Surprises

Step back far enough and the SSE story delivers a strategic lesson that reaches well beyond one Scottish utility. Here was a legacy conglomerate, weighed down by a politically toxic consumer business and dismissed as a sleepy income stock, that managed to do the thing legacy incumbents almost never do: it reinvented itself before it was forced to, and it timed the reinvention with something close to luck. While Centrica was mauled by the retail crisis and Denmark's Ørsted took brutal write-downs on unhedged, pure-play offshore exposure, SSE's balanced networks-plus-renewables model proved more resilient than either the activists or the bulls of 2021 fully appreciated.

Which brings us to the great irony — the biggest surprise of the whole saga. In 2021, Elliott Advisors looked at SSE and saw the regulated networks as dead weight dragging down a shiny renewables business that deserved to fly free. Four years later, the verdict of SSE's own capital allocation is almost the mirror image: it is the networks — the "boring" wires that were supposedly holding the company back — that have become the core growth engine, now commanding 80% of a £33 billion investment programme, while renewables has been rationed to a selective, capital-disciplined 20%. The asset the activist wanted to liberate turned out to be the passenger; the asset the activist dismissed turned out to be the driver.

Before the final reflection, it is worth puncturing two myths that cling to the SSE story. The first is the myth of the "safe utility." SSE still carries the folk-memory of a sleepy dividend stock, but the company an investor buys today is a heavy-construction and regulatory-negotiation business running a £33 billion capital programme with a fresh £2 billion of equity dilution and a live dependence on Ofgem's next ruling — closer in risk profile to an infrastructure developer than to the bond-proxy of old. The second is the myth, popularised during the Elliott campaign, that renewables were the whole growth story and the networks were dead weight. The company's own capital plan has now inverted that narrative so completely that it is the networks doing the heavy lifting, while renewables have been rationed. Consensus narratives about SSE have had a habit of being not just wrong but backwards — a useful reminder to interrogate the current consensus too.

There is a caution worth holding onto here, and the independent posture demands it. SSE has told a persuasive story and, on the evidence of its dividend discipline and the Ontario Teachers valuation, has backed a good deal of it with action. But the £33 billion bet is still mostly ahead of the company, not behind it. The RAV has not yet trebled. The EPS has not yet reached 250 pence. Dogger Bank is not yet finished. The regulator has not yet set the returns that will make or break the plan. A thesis this dependent on execution, financing, and policy — on building on time, refinancing at acceptable rates, and a regulator's continued goodwill — is a thesis that has to be re-underwritten every year against those three KPIs, not accepted on faith.

Rebuilding the physical spine of a nation's energy system is the ultimate long-duration compounding game — and also the ultimate test of whether a management team can execute over a decade what it promises in a press release. Under Martin Pibworth, SSE has staked its identity on being not a traditional utility but the literal, physical infrastructure of Britain's decarbonised future. The blueprint is drawn and the capital is committed. Whether the glens' old power company can pour that much concrete and string that much cable, on time and at a return that rewards its owners, is the story that the next five years will tell.

References

-

SSE unveils £33bn investment plan to unlock clean, secure, affordable energy and support economic growth — SSE plc, 2025-11-12 ↩↩↩↩

-

Transformation for growth — Interim results for the six months to 30 September 2025 — SSE plc, 2025-11-12 ↩

-

SSE HY26 Results Presentation — Transformation for Growth — SSE plc, 2025-11-12 ↩↩↩↩

-

SSE generates nearly £10bn for UK economy as it invests to strengthen the electricity system (FY2026 preliminary results) — SSE plc, 2026-05 ↩↩↩↩↩↩↩

-

Preliminary Results for the year ended 31 March 2025 — SSE plc, 2025-05 ↩↩↩↩↩

-

SSE agrees sale of 25% stake in Transmission business for £1.465bn to unlock further growth — SSEN Transmission, 2022-11-25 ↩↩↩

-

Ontario Teachers' agrees to acquire a 25% stake in SSEN Transmission — Ontario Teachers' Pension Plan, 2022 ↩↩

-

OVO Energy completes acquisition of SSE Energy Services — Reuters, 2020-01-15 ↩

-

SSE pledges £12.5 bln to stave off activist Elliott break-up calls — Reuters, 2021-11-17 ↩↩↩

-

Elliott Advisors public letter to the SSE plc board — Business Wire, 2021-12-07 ↩

-

SSE plc announces Martin Pibworth as Chief Executive — SSE plc, 2025-03 ↩↩↩

-

SSE names Martin Pibworth as successor to CEO Alistair Phillips-Davies — Scottish Financial News, 2025-07-17 ↩↩

-

Proposed placing of new ordinary shares — SSE plc RNS via Investegate, 2025-11-12 ↩

-

Our Story: The 1940s — North of Scotland Hydro-Electric Board — SSE Heritage ↩↩↩↩

-

SSE Renewables acquires European onshore wind platform from Siemens Gamesa Renewable Energy — SSE Renewables, 2022-04 ↩

-

A Joint Venture: SSE, Equinor & Vårgrønn — Dogger Bank Wind Farm ↩↩

-

Contracts for Difference (CfD) Allocation Round 5: results — GOV.UK, 2023-09 ↩

-

SSE reports 4% drop in annual profit for March 2026 — Power Technology, 2026-05 ↩

-

SSEN Transmission response to Ofgem's RIIO-T3 Price Control Draft Determination — SSE plc, 2025-07-01 ↩↩

-

RIIO-3 Final Determinations for the Electricity Transmission, Gas Distribution and Gas Transmission sectors — Ofgem, 2025-12-04 ↩↩

-

Boost for offshore wind as government raises maximum prices in renewable energy auction (AR6) — GOV.UK, 2024 ↩

-

Contracts for Difference Allocation Round 7 results and breakdown — NeuWave Technologies, 2026-01-14 ↩

-

SSEN Transmission responds to Ofgem's RIIO-T3 Final Determination — SSE plc, 2025-12 ↩↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube