Sanofi: The French Pharmaceutical Giant's Quest for Global Dominance

I. Introduction & Episode Roadmap

Picture this: It's a gray November morning in 2008, and Chris Viehbacher, a Canadian pharmaceutical executive who'd spent his entire career at GlaxoSmithKline, walks into Sanofi's headquarters at 54 rue La Boétie in Paris. He doesn't speak French. He's never run a company. And he's just inherited what industry insiders are calling a "patent cliff death spiral"—six of Sanofi's seven top drugs will lose patent protection within four years, putting 40% of the company's revenue at risk. The French press is skeptical. The unions are hostile. And yet, within six years, this outsider will transform a lumbering French conglomerate into a global biotech powerhouse, before being unceremoniously fired by a unanimous board vote.

How did a subsidiary of a French oil company, founded in 1973 with no original drug discovery capabilities, become the world's third-largest pharmaceutical company with €42 billion in revenue? How did a company that started by acquiring cast-off assets from larger rivals build one of the industry's most valuable immunology franchises? And why does a company that generates more cash flow than almost any European corporation trade at a perpetual discount to its peers?

The story of Sanofi is fundamentally a story about mergers and acquisitions—not as a growth strategy, but as survival instinct encoded in corporate DNA. From its earliest days as a subsidiary of Elf Aquitaine, through the mega-mergers that created Aventis and then Sanofi-Aventis, to the recent $9.5 billion acquisition of Blueprint Medicines in January 2025, this company has been built, rebuilt, and rebuilt again through deals. It's averaged 2.2 acquisitions per year since 2020, with premiums reaching 300% over market prices. What lies ahead is a corporate odyssey spanning five decades—a story of French industrial ambition colliding with global pharmaceutical reality, of scientific breakthroughs emerging from financial engineering, and of a company that has survived every industry upheaval by constantly reinventing itself through the balance sheet rather than the laboratory bench. Sanofi trades as "SAN" on Euronext Paris and is a component of the Euro Stoxx 50 stock market index, with 2023 revenues exceeding €43 billion.

This episode traces three fundamental transformations: first, how serial acquisition became not just a strategy but an existential requirement; second, how the 2008-2009 patent cliff crisis forced a complete reimagination of what a pharmaceutical company could be; and third, how the pursuit of biotechnology supremacy has driven increasingly desperate—or visionary—deal premiums that would make even the most aggressive Silicon Valley acquirers blush.

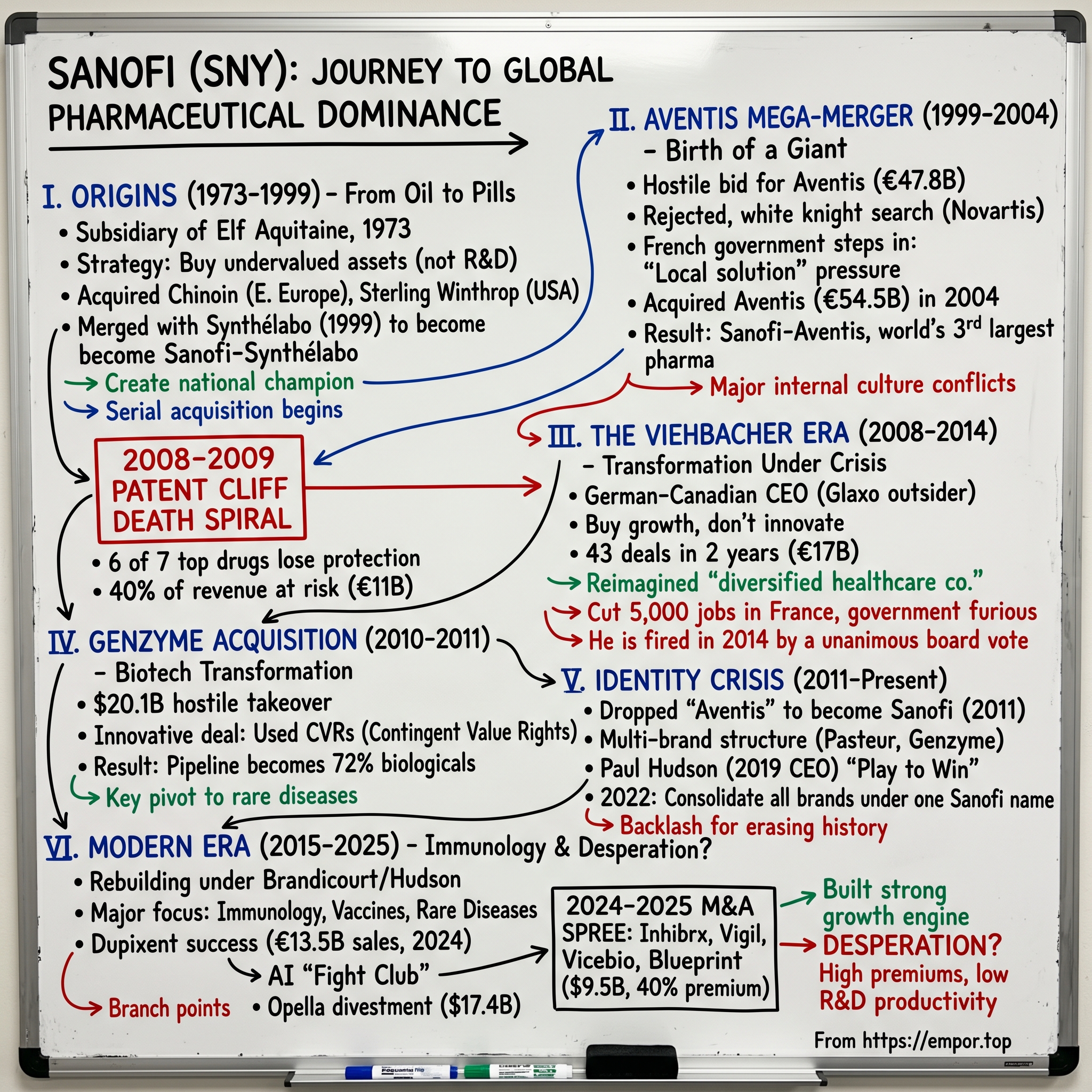

II. Origins: From Oil to Pills (1973–1999)

The conference room at Elf Aquitaine's headquarters in 1973 must have been an unusual scene. Here sat executives of France's national oil champion, fresh from the trauma of the first oil crisis, debating whether to enter the pharmaceutical business. Not through research and development—that would take decades they didn't have—but through financial engineering and strategic acquisition. The logic was purely industrial: diversify away from petroleum's volatility into healthcare's steady cash flows. What they created would become Sanofi, a company that from its very first day understood that in pharmaceuticals, you could buy innovation faster than you could build it.

Founded as a subsidiary of Elf Aquitaine in 1973, Sanofi began life with no laboratories, no patents, and no pretense of being a traditional drug developer. The company's early strategy was brilliantly opportunistic: acquire undervalued or neglected pharmaceutical assets from companies that didn't understand their worth, particularly in emerging markets where Western giants feared to tread. This wasn't pharmaceutical development; it was arbitrage dressed in a lab coat.

The 1980s saw Sanofi execute a series of increasingly bold acquisitions that would establish the template for its next fifty years. The company systematically bought its way into therapeutic areas, geographical markets, and technology platforms. Each deal brought not just products but also manufacturing capabilities, distribution networks, and—critically—regulatory expertise in navigating France's byzantine healthcare system. The 1993 acquisition of Chinoin marked Sanofi's first major foray into Eastern Europe. This Hungarian drug company, with 1992 sales totaling about US$104 million, gave Sanofi a critical foothold in markets that Western competitors had largely ignored. The deal structure was revealing of Sanofi's approach: patient, opportunistic, and willing to navigate complex political environments. The French company understood that in the post-Soviet chaos, assets could be acquired for fractions of their potential value if you had the stomach for bureaucracy and uncertainty. Then came 1994's watershed moment: the acquisition of Sterling Winthrop's prescription drug business from Eastman Kodak for US$1.675 billion. This wasn't just Sanofi's first significant venture into the United States market—it was a declaration that this French upstart intended to compete on the global stage. Sterling Winthrop brought not just products but also critical infrastructure: manufacturing facilities, regulatory expertise, and most importantly, a sales force that understood the labyrinthine American healthcare system.

The French pharmaceutical landscape of the 1990s provided the perfect backdrop for Sanofi's ambitions. The government's industrial policy explicitly favored the creation of national champions, providing preferential treatment in pricing, reimbursement, and even clinical trial approvals. Sanofi leveraged this political support masterfully, using its protected home market as a cash cow to fund international expansion.

Meanwhile, Synthélabo had been pursuing its own consolidation strategy. Founded in 1970 through the merger of two French pharmaceutical laboratories, Laboratoires Dausse (founded in 1834) and Laboratoires Robert & Carrière (founded in 1899), Synthélabo represented old French pharmaceutical tradition. By the late 1990s, the logic of combining Sanofi's aggressive international expansion with Synthélabo's deep French roots and L'Oréal's backing (L'Oréal had acquired majority control of Synthélabo in 1973) became irresistible.

Sanofi-Synthélabo was formed in 1999 when Sanofi merged with Synthélabo; at the time of the merger, Sanofi was the second largest pharmaceutical group in France in terms of sales and Synthélabo was the third largest. The merger created a €7 billion company with genuine global reach—a French pharmaceutical champion that could credibly compete with the Anglo-American giants. But this was just the appetizer. The main course was about to be served.

III. The Aventis Mega-Merger & Birth of a Giant (1999–2004)

The story of how Sanofi-Synthélabo became Sanofi-Aventis reads like a hostile takeover thriller written by Balzac. On January 26, 2004, at 7:00 AM Paris time, Jean-François Dehecq, Sanofi-Synthélabo's CEO, held a press conference that sent shockwaves through the pharmaceutical industry. His company, with annual sales of €8 billion, was launching an unsolicited bid for Aventis, a company nearly twice its size with €17 billion in revenue. David was taking aim at Goliath with a slingshot loaded with debt and political backing. But to understand the 2004 merger, we must first understand Aventis itself—a company born from ambition and shadowed by history. Aventis was formed in 1999 when the French company Rhône-Poulenc S.A. merged with the German corporation Hoechst Marion Roussel. This wasn't just any merger; Hoechst AG was itself one of the forcibly separated subsidiaries of IG Farben, the notorious chemical conglomerate that had exploited Auschwitz slave labor and supplied Zyklon B during the Holocaust. The historical baggage was immense, and the cultural challenges of merging proud French and German companies were equally daunting.

Hoechst AG, the majority partner at the time in Hoechst Marion Roussel, was itself a merger of two of the three forcibly separated subsidiaries of IG Farben, exploiter of Auschwitz slave labor and supplier of Zyklon B during The Holocaust. This dark history cast a long shadow over the company's identity, creating an unspoken tension that would persist through multiple corporate transformations.

The Aventis merger itself had been troubled from the start. Market speculation forced Hoechst and Rhône-Poulenc into the spotlight with their plan in late 1998, but their initial concept of a two-step merger taking up to three years was not impressive to investors. In March 1999, the companies bowed to pressure and announced a revised plan – a single step "accelerated" merger to be achieved by the end of 1999, which they successfully achieved through a 53:47 equity split in Hoechst's favour. The merged company was headquartered in Strasbourg, France, straddling the Franco-German border in a symbolic attempt to bridge the two cultures.

By 2003, Aventis was struggling. Integration problems persisted, the product pipeline was weak, and the company lacked a clear strategic direction. It was vulnerable, and Jean-François Dehecq knew it. His hostile bid in January 2004 was audacious: In early 2004, Sanofi-Synthélabo made a hostile takeover bid for Aventis worth €47.8 billion. The Aventis board's reaction was predictable—they rejected the bid as inadequate and enacted poison pill provisions while inviting Novartis to enter merger negotiations as a white knight.

What followed was a three-month corporate battle that would reshape the European pharmaceutical landscape. The French government played a strong role, desiring what it called a "local solution", by putting heavy pressure on Sanofi-Synthélabo to raise its bid for Aventis and for Aventis to accept the offer and by rejecting Aventis's poison pill proposal. This wasn't free market capitalism; this was industrial policy executed through boardroom pressure and regulatory leverage.

The French government's intervention was decisive. Behind closed doors, ministers made it clear that a Novartis acquisition would face insurmountable regulatory hurdles, while a Sanofi deal would sail through. The message was unsubtle: France wanted a national champion, and it would use every tool at its disposal to create one.

The three-month takeover battle concluded when Sanofi-Synthélabo launched a friendly bid of €54.5 billion in place of the previously rejected hostile bid. On August 20, 2004, Sanofi-Synthélabo acquired control of Aventis. The combined entity, renamed Sanofi-Aventis, instantly became Europe's largest pharmaceutical company and the world's third-largest, with combined revenues exceeding €25 billion.

But creating a giant and managing one are entirely different challenges. The integration was brutal. The merged companies had to divest several businesses to satisfy antitrust regulators, including beauty products, diagnostics, and animal health divisions. More challenging was the cultural integration: French corporate culture meeting German precision, with American subsidiaries caught in between. The company had research centers in Frankfurt, Paris, New Jersey, and Tokyo, each with its own culture, priorities, and internal politics.

The portfolio rationalization was equally complex. Sanofi-Aventis inherited overlapping product lines, redundant research programs, and competing internal factions. Decisions about which drugs to prioritize, which research programs to kill, and which facilities to close became political minefields. Every choice had national implications—closing a German facility in favor of a French one (or vice versa) could trigger governmental intervention.

Yet despite the challenges, the merger delivered on its financial promises. Cost synergies exceeded targets, reaching €2 billion by 2006. The combined sales force proved more effective than either company had managed alone. Most importantly, the merger created a company with the scale to compete globally, particularly in the critical U.S. market where neither Sanofi nor Aventis had been truly successful independently.

By 2007, Sanofi-Aventis was generating €28 billion in revenue and had established itself as a legitimate member of Big Pharma's elite. But beneath the surface, a crisis was brewing that would test whether this hastily assembled giant could survive its first real existential threat.

IV. The Viehbacher Era: Transformation Under Crisis (2008–2014)

Chris Viehbacher landed at Charles de Gaulle Airport in December 2008 with a reputation as a cost-cutter and a mandate to perform miracles. The German-Canadian executive, who had spent his entire career at GlaxoSmithKline, didn't speak French, had never run a company, and was walking into what industry analysts were calling an "unfixable situation." Six of Sanofi's seven blockbuster drugs would lose patent protection between 2009 and 2012, putting approximately 40% of the company's €28 billion revenue base at risk. The patent cliff wasn't approaching—it had already arrived, and Sanofi was standing at the edge. The numbers were staggering: drugs representing approximately €11 billion in annual sales would face generic competition. Plavix, the blood thinner that Sanofi co-marketed with Bristol-Myers Squibb, alone generated €2.5 billion annually. Lovenox, another anticoagulant, contributed €2.8 billion. The company's earnings were about to be cut in half, and everyone knew it.

Viehbacher's strategic response was radical for a traditional pharmaceutical company. Instead of doubling down on internal R&D—the conventional Big Pharma playbook—he essentially admitted that Sanofi couldn't innovate its way out of the crisis fast enough. His solution: buy growth, diversify aggressively, and transform Sanofi from a traditional pharmaceutical company into what he called a "diversified healthcare company."

Between 2008 and 2010, the company spent more than $17 billion in mergers and acquisitions. The acquisition pace was breathtaking: 43 deals in Viehbacher's first two years alone. These weren't just pharmaceutical acquisitions—Viehbacher bought consumer health businesses, generic drug manufacturers, and vaccine companies. He acquired Medley, a Brazilian generics company, for $635 million. He bought Zentiva, an Eastern European generics player, for €1.8 billion. Each deal expanded Sanofi's footprint beyond the patent-protected drugs that had historically driven its profits.

The strategic pivot had four pillars: biotechnology (particularly rare diseases), emerging markets, over-the-counter medicines, and academic partnerships. This wasn't incrementalism; it was a wholesale reimagining of what a pharmaceutical company could be. Viehbacher articulated a vision where Sanofi would generate growth not from blockbuster drugs but from a portfolio of smaller, more diverse revenue streams that were less vulnerable to patent expiration. The Regeneron partnership exemplified Viehbacher's approach to biotechnology. In 2007, Sanofi-Aventis agreed to pay Regeneron $100 million per year for five years, under which Regeneron would use its monoclonal antibody discovery platform to create new biopharmaceuticals. In 2009, the companies expanded the deal to $160 million per year and extended it to 2017. This wasn't just R&D funding—it was an admission that Sanofi's internal capabilities in biologics were inadequate and that partnership, not organic development, would drive future innovation.

But Viehbacher's most controversial moves were in France itself. Between 2008 and 2014, he cut approximately 5,000 jobs in Sanofi's home market while simultaneously expanding in China, India, and Brazil. The French unions were apoplectic. The government was furious. The media painted him as a heartless foreigner dismantling a French institution. Viehbacher, who spent most of his time in Boston rather than Paris, seemed oblivious to the political dimension of his role.

His management style was equally divisive. Viehbacher ran Sanofi like a private equity portfolio rather than an integrated pharmaceutical company. Each business unit—vaccines, diabetes, rare diseases, consumer health—operated almost independently, with separate P&Ls and minimal coordination. This decentralization allowed for rapid decision-making but created internal silos that would later prove problematic.

The financial results, however, were undeniable. By 2013, Sanofi had successfully navigated the worst of the patent cliff. Generic competition took €1.25 billion off the top line in 2013, but Lantus, the superstar diabetes treatment, grew by 20% for the year, to a whopping €5.72 billion. The emerging markets strategy was paying off, with sales in developing countries exceeding €11 billion. The diversification into consumer health and vaccines provided stable, if unspectacular, growth.

But success in the boardroom doesn't always translate to success in the executive suite. By 2014, tensions between Viehbacher and the board had reached a breaking point. The specific trigger was Project Phoenix, a plan to sell Sanofi's portfolio of mature drugs for approximately $8 billion. Weinberg cited Project Phoenix, a plan to sell Sanofi's portfolio of mature drugs for some $8 billion. Weinberg told investors that the board learned about the project in the press. "This was a major strategic move, and this was not appropriate," he said.

The board's frustration went deeper than communication failures. Viehbacher's vision of Sanofi as a decentralized collection of healthcare businesses clashed with the board's desire for a more integrated, French-centered pharmaceutical company. His decision to base himself in Boston rather than Paris became symbolic of a broader disconnect—between Anglo-American management culture and French corporate governance, between financial engineering and scientific innovation, between global ambition and national identity.

On October 29, 2014, Sanofi's board fired CEO Christopher A. Viehbacher. The board made clear its problems lay not with Viehbacher's overall strategy but with his management style. The decision was unanimous, swift, and shocking to investors who had watched Viehbacher successfully navigate the company through its worst crisis.

Viehbacher's legacy is complex. He saved Sanofi from the patent cliff, transformed it into a diversified healthcare company, and positioned it for future growth through partnerships and acquisitions. But he also left behind a fractured organization, with disparate businesses that struggled to work together and a corporate culture torn between its French heritage and global ambitions. His successor would inherit a company that had survived its near-death experience but hadn't yet figured out what it wanted to become.

V. The Genzyme Acquisition: Biotech Transformation (2010–2011)

The Hynes Convention Center in Boston was buzzing with tension on May 24, 2010. At the annual meeting of the International Society for Pharmacoeconomics and Outcomes Research, rumors were swirling that Chris Viehbacher had been spotted in the hotel lobby. Genzyme executives, attending the same conference, whispered nervously—was Sanofi about to make a move? Henri Termeer, Genzyme's legendary CEO who had built the company from 11 employees to a $15 billion biotechnology powerhouse, maintained his characteristic calm. But behind closed doors, he knew what was coming. His company, crippled by manufacturing problems that had led to drug shortages and FDA consent decrees, was vulnerable. And Viehbacher, hunting for transformative acquisitions, had found his prey. The initial approach came in July 2010. Viehbacher's offer was straightforward: $69 per share in cash, representing a 38% premium over Genzyme's unaffected share price of $49.86 on July 1, 2010. For a company whose stock had been hammered by manufacturing problems, it should have been attractive. But Henri Termeer, who had founded and built Genzyme into a rare disease powerhouse, saw it differently. His company wasn't broken—it was temporarily wounded. The manufacturing issues would be resolved. The pipeline, particularly alemtuzumab (Lemtrada) for multiple sclerosis, was worth far more than Sanofi was offering.

What followed was seven months of corporate warfare that would redefine hostile takeovers in the pharmaceutical industry. After Termeer rejected the initial offer and refused even to meet, Viehbacher went public with his bid on August 29, 2010, taking the unprecedented step of holding an investor call to explain why Genzyme shareholders should pressure their board to negotiate. The French government, still smarting from Viehbacher's job cuts, watched nervously as their national champion pursued an American target with borrowed billions.

The valuation dispute centered on two fundamental disagreements. First, how quickly could Genzyme resolve its manufacturing problems with Cerezyme and Fabrazyme, two critical enzyme replacement therapies? Second, and more importantly, what was the true value of Lemtrada? Genzyme forecast peak annual sales of $3.5 billion, while Sanofi, using the average of several analyst estimates, expects only about $700 million. The gap was enormous—nearly $3 billion in annual sales translated to perhaps $10 billion in enterprise value.

The solution came from an unlikely source: contingent value rights, or CVRs—a financial instrument more common in biotech venture deals than mega-mergers. The structure was elegant in its simplicity: Sanofi would pay $74 per share in cash upfront, plus a CVR that could pay up to an additional $14 per share based on specific milestones. If Lemtrada succeeded, Genzyme shareholders would capture the upside. If it failed, Sanofi wouldn't overpay.

The final agreement, announced February 16, 2011, valued the deal at $20.1 billion in cash plus the CVRs. The CVR structure included payments tied to Lemtrada achieving specific regulatory approvals and sales milestones, as well as production volumes for Cerezyme and Fabrazyme. The CVRs would trade on NASDAQ under the ticker "GCVRZ," creating a liquid market for the contingent payments—the first time such an instrument had been used at this scale in a pharmaceutical acquisition.

The deal closed on April 8, 2011, with approximately 89.4% of Genzyme's outstanding shares tendered. Sanofi made Genzyme its global center of excellence for rare diseases, keeping it headquartered in Cambridge, Massachusetts. This wasn't just window dressing—Viehbacher understood that Genzyme's culture of innovation in rare diseases couldn't be replicated by simply absorbing it into Sanofi's bureaucracy.

The transformation was immediate and profound. Result: 72% of pipeline becomes biologicals, 100% of late-stage. This wasn't incremental change—it was a complete reimagining of Sanofi as a biotechnology company. The acquisition brought not just products but capabilities: expertise in biologics manufacturing, deep relationships with rare disease communities, and most importantly, a different approach to drug development focused on small patient populations with high unmet medical needs.

The integration, surprisingly, went smoothly. Unlike the cultural clashes that had plagued the Aventis merger, Genzyme maintained its identity within Sanofi. The Cambridge campus continued to operate semi-autonomously, preserving the entrepreneurial culture that had made it successful. Key Genzyme executives remained, providing continuity and expertise. The rare disease franchise flourished, with new investments in manufacturing and R&D.

The CVRs, however, became a source of ongoing tension. In 2016, CVR holders sued Sanofi, claiming the company had deliberately delayed Lemtrada's approval and under-promoted it to avoid milestone payments. The court found that the Trustee on behalf of the CVR holders pled sufficient facts to raise a reasonable inference that Sanofi breached its agreement to use "diligent efforts." The case highlighted a fundamental conflict in CVR structures: the buyer's incentive to minimize payments versus its contractual obligation to maximize the asset's value.

Despite the legal battles, the Genzyme acquisition fundamentally transformed Sanofi. It shifted the company's center of gravity from small molecule drugs to biologics, from primary care to specialty care, from Europe to the United States. The rare disease franchise became one of Sanofi's most profitable divisions, generating consistent double-digit growth. More importantly, it proved that Sanofi could successfully acquire and integrate a major biotechnology company—a capability that would become increasingly critical as the industry evolved.

By 2022, however, Sanofi made a surprising decision: it dropped the Genzyme name in a corporate rebrand. The company that Viehbacher had promised to preserve as a crown jewel was absorbed into the larger Sanofi identity. The symbolism was clear—Sanofi was no longer a collection of acquired companies but a unified entity. Whether this represented confidence or insecurity would become a recurring question in Sanofi's ongoing identity crisis.

VI. Name Changes & Identity Crisis (2011–Present)

At a boardroom meeting in early 2011, a seemingly simple question sparked hours of heated debate: What should the company call itself? Sanofi-Aventis was a mouthful, a hyphenated reminder of past mergers that meant nothing to patients, confused investors, and frustrated employees who couldn't even fit the full name on their business cards. The decision to drop "Aventis" and become simply "Sanofi" seemed straightforward. It wasn't. It was the beginning of a decade-long identity crisis that would see the company repeatedly rebrand, reorganize, and reimagine itself while never quite answering the fundamental question: What is Sanofi? The company dropped the -Aventis suffix of its name on May 6, 2011, after receiving approval at its annual general meeting. The new logo featured a "bird of hope" at the center surrounded by colors representing water, earth, fire, and air. The symbolism was heavy-handed, the execution forgettable. Within the company, employees joked that the bird looked more like it was drowning than flying.

But the 2011 name change was just the beginning. Sanofi had become a collection of fiefdoms, each with its own identity and culture. Sanofi Genzyme operated as a semi-autonomous rare disease unit. Sanofi Pasteur, the vaccines division that traced its heritage back over a century, maintained its own brand and operations. Consumer healthcare had its own identity. The company wasn't so much unified as it was a holding company for healthcare businesses that happened to share a corporate parent.

This fragmentation had advantages. Each unit could maintain its specialized culture and expertise. Genzyme's entrepreneurial biotech spirit survived within its Cambridge enclave. Pasteur's vaccine scientists in Lyon continued their work largely undisturbed by corporate machinations in Paris. But it also created inefficiencies, duplicated efforts, and most problematically, prevented Sanofi from presenting a coherent identity to investors, partners, and patients.

The identity crisis deepened under successive CEOs. Olivier Brandicourt, who succeeded Viehbacher in 2015, attempted to create more integration but largely maintained the multi-brand structure. Paul Hudson, arriving in 2019, initially seemed content with the status quo. But by 2021, as the company struggled to articulate its strategy amid the COVID-19 pandemic and watched competitors like Pfizer and Moderna capture the mRNA vaccine spotlight, the pressure for change became irresistible. The February 3, 2022 announcement was seismic. Current business units Sanofi Pasteur and Sanofi Genzyme, focused on vaccines and specialty care respectively, and all other acquired brands, will be united under the singular Sanofi name and brand. The Genzyme name, which had represented biotechnology innovation for four decades, was gone. The Pasteur name, honoring the father of vaccination and in use for over a century, was erased. In their place: a lowercase "sanofi" with two purple dots and an incomplete 's' that was meant to suggest both a question mark and an exclamation point.

The reaction was swift and brutal. "There is little to no appreciation within today's Sanofi organization for the exceptional culture and talent pool that defined the Genzyme organization," wrote John Hawkins, Henri Termeer's biographer. Boston's biotech community, which had viewed Genzyme as a crown jewel of the industry, saw it as cultural vandalism. French scientists were appalled at the erasure of Pasteur's name. Even employees who understood the business rationale struggled to explain why eliminating these historic brands would somehow create unity.

Paul Hudson, Sanofi's CEO since 2019, defended the decision as part of his "Play to Win" strategy. The fragmented brand architecture was confusing to stakeholders, he argued. Having multiple sub-brands prevented Sanofi from speaking with one voice. The company needed to present itself as a unified entity to compete effectively in an increasingly consolidated industry.

But the rebrand revealed deeper tensions about Sanofi's identity. Was it a French national champion or a global pharmaceutical company? A traditional drug developer or a biotechnology innovator? A collection of specialized businesses or an integrated healthcare company? The new branding didn't answer these questions—it simply papered over them with purple dots and typography borrowed from tech companies.

The timing was particularly tone-deaf. Sanofi had struggled during the COVID-19 pandemic, failing to develop a successful vaccine despite being one of the world's largest vaccine manufacturers. While Pfizer and Moderna became household names, Sanofi watched from the sidelines. The rebrand, launched just as the pandemic was winding down, seemed like a distraction from more fundamental problems.

Internally, the rebrand created more confusion than clarity. Employees who had proudly worked for Genzyme or Pasteur suddenly found themselves part of a generic "Sanofi." The specialized cultures that had been carefully preserved through previous mergers were now being forcibly homogenized. The company insisted that no operational changes would follow the rebrand, but employees knew better—names matter, and when you change them, you change identity.

The identity crisis extended beyond branding to fundamental questions about corporate structure and strategy. Sanofi remained one of the few major pharmaceutical companies maintaining a broad portfolio spanning vaccines, rare diseases, general medicines, and consumer health. While competitors like Pfizer, GSK, and Johnson & Johnson were spinning off divisions to focus on core pharmaceutical businesses, Sanofi clung to its conglomerate structure even as it eliminated the brands that gave each division its distinct identity.

Christopher Williams, Sanofi's head of corporate communications, insisted the rebrand was about modernization: "We're a work in progress, and so is science." But to many observers, the constant rebranding suggested not progress but confusion—a company that had grown through serial acquisition trying desperately to convince itself and others that it was more than the sum of its purchased parts.

The 2022 rebrand wasn't the end of Sanofi's identity crisis—it was its most visible symptom. A company that had been built through mergers and acquisitions, that had survived by constantly reinventing itself, had lost track of what it actually was. The elimination of the Genzyme and Pasteur names didn't create unity; it created a void where identity should have been. And into that void, Sanofi would continue pouring billions in acquisitions, hoping that somehow, buying enough companies would eventually answer the question of what Sanofi wanted to be.

VII. Modern Era: Immunology, Blueprint & Beyond (2015–2025)

The text message arrived at 3:47 AM Paris time on January 15, 2025. Paul Hudson, unable to sleep before one of the biggest announcements of his tenure, was reviewing the press release one final time when his head of business development messaged: "Blueprint board approved. We're going to $9.5 billion." Hudson smiled grimly. At $41.50 per share—a 301% premium to Blueprint Medicines' closing price—this wasn't just an acquisition. It was either the boldest strategic move in Sanofi's history or the desperate overpayment of a company running out of options. The market would decide soon enough.

The Blueprint acquisition wasn't just expensive—it was symptomatic of a broader strategic dilemma. Blueprint Medicines Corporation, a US-based, publicly traded biopharmaceutical company specializing in systemic mastocytosis (SM), a rare immunological disease, and other KIT-driven diseases, brought Ayvakit/Ayvakyt (avapritinib), approved in the US and the EU, and a promising advanced and early-stage immunology pipeline. Ayvakit achieved net revenues of $479 million in 2024 and nearly $150 million in Q1 2025, representing year-on-year growth of more than 60 percent over Q1 2024. But the premium paid reflected desperation more than strategy—a company with cash but without clear direction, competing against rivals with deeper pipelines and clearer visions.

Hudson's post-Viehbacher rebuilding began under Olivier Brandicourt, who served as a transitional CEO from 2015 to 2019. Brandicourt stabilized the organization but lacked the vision to transform it. His tenure was marked by incremental improvements rather than bold moves—necessary after Viehbacher's disruption but insufficient for long-term competitiveness. The Bioverativ acquisition in 2018 for $11.6 billion exemplified this era: a safe, expensive bet on hemophilia that quickly soured when Roche's Hemlibra dominated the market, forcing Sanofi to take a $2 billion writedown.

Paul Hudson arrived in September 2019 with a mandate for transformation. Since joining Sanofi in 2019, CEO Paul Hudson has seen nine consecutive quarters of growth and more than a dozen acquisitions and business development deals, including mRNA therapeutics company Translate Bio and biotech company Kadmon. His "Play to Win" strategy, unveiled in December 2019, promised to refocus Sanofi on immunology, vaccines, and rare diseases while exiting diabetes and cardiovascular markets where the company had lost competitive advantage.

Hudson declared: "We have made tremendous progress on our Play to Win strategy by bringing new and transformative products to market and building an industry-leading immunology pipeline, evidenced by our recent, strong flow of positive R&D data readouts. In this new chapter of our strategy, we are deepening our investment in R&D, taking steps toward becoming a pure play biopharma company, and further optimizing our cost structure. This will help us accelerate innovation and strengthen our growth drivers, while ensuring long-term profitability and enhancing shareholder value."

The strategy included dramatic cost-cutting—Sanofi is targeting savings of a total of up to €2 billion from 2024 to the end of 2025, of which most will be reallocated to fund innovation and growth drivers. But Hudson's most significant move was the decision to separate the Consumer Healthcare business, announced in October 2023. A year later, the French company announced the divestment of a 50% controlling stake in its consumer health division, Opella, to U.S. private equity firm Clayton Dubilier & Rice (CD&R) in a deal valued at approximately $17.4 billion (€16 billion). The sale, while financially attractive, triggered political backlash in France over concerns about job losses and the sale of iconic brands like Doliprane.

The 2024 acquisition of Inhibrx showcased Hudson's approach to M&A: surgical precision rather than wholesale consumption. Combined, the upfront cash portion of the consideration, the potential contingent value payment, if achieved, and the assumption of Inhibrx's debt, implies an aggregate transaction value of approximately $2.2 billion. The acquisition adds SAR447537 (formerly INBRX-101) to Sanofi's rare disease pipeline, underscoring the company's commitment to pursuing differentiated and potential best-in-class medicines that build upon our existing strengths and capabilities. SAR447537 is a human recombinant protein that holds the promise of allowing alpha-1 antitrypsin deficiency (AATD) patients to achieve normalization of serum AAT levels with less frequent (monthly vs. weekly) dosing. AATD is an inherited rare disease characterized by low levels of AAT protein, predominantly affecting the lung with progressive deterioration of the tissue. SAR447537 may help to reduce inflammation and prevent further deterioration of lung function in affected individuals. The deal structure—spinning off Inhibrx's other assets while keeping only the AATD drug—demonstrated newfound discipline in capital allocation.

The 2025 acquisition spree accelerated with three major deals in rapid succession. In May 2025, Sanofi announced it had entered into an agreement to acquire Vigil Neuroscience, Inc. ("Vigil"), a publicly traded clinical-stage biotechnology company focused on developing novel therapies for neurodegenerative diseases. This acquisition in neurology, one of Sanofi's four strategic disease areas, enhances Sanofi's early-stage pipeline and includes VG-3927, which will be evaluated in a phase 2 clinical study in Alzheimer's disease. Sanofi has acquired all outstanding common shares of Vigil for $8 per share in cash at closing, representing an equity value of approximately $470 million. In addition, Vigil's shareholders received a non-transferrable contingent value right (CVR) per Vigil share, which entitles its holder to receive a deferred cash payment of $2, conditioned upon the first commercial sale of VG-3927.

July brought the Vicebio acquisition, expanding Sanofi's vaccine capabilities. Sanofi announced it has entered into an agreement to acquire Vicebio Ltd ("Vicebio"), a privately held biotechnology company headquartered in London, UK. The acquisition brings an early-stage combination vaccine candidate for respiratory syncytial virus (RSV) and human metapneumovirus (hMPV), both respiratory viruses, and expands the capabilities in vaccine design and development with Vicebio's 'Molecular Clamp' technology. Under the terms of the agreement, Sanofi would acquire all of Vicebio's share capital for a total upfront payment of $1.15 billion, with potential milestone payments of up to $450 million based on development and regulatory achievements.

The Blueprint Medicines deal in January 2025 represented Hudson's boldest move yet. The upfront offer price represents a premium of approximately 27% over the closing price of Blueprint on May 30, 2025 and a premium of approximately 34% over the 30 trading days volume weighted average price (VWAP) of Blueprint as of May 30, 2025. Together with the CVR, the premium is approximately 33% over the closing price on May 30, 2025 and approximately 40% over the 30 trading days VWAP. While the premium was far more reasonable than initially reported, the $9.5 billion total still represented a massive bet on systemic mastocytosis—a rare disease affecting perhaps 32,000 patients globally.

Hudson's approach to innovation extended beyond M&A to embrace artificial intelligence. Instead of a traditional top-down AI implementation, Hudson created an "AI Fight Club"—picking one person who didn't know anything about AI from each major function and putting them in a room together with the mandate to "disrupt yourselves." Rather than checking on their progress frequently or giving them detailed directions, he just told them they would gather once or twice a year. Hudson believes in "event-driven leadership," giving people a fixed goal but plenty of freedom about how to reach it. "You tell them, 'We'll meet in Berlin in September and you'll share your updates with each other.' No more instructions, no questions asked between now and then. It becomes incredibly empowering and motivating for people to fill in the gap," because nobody wants to show up with no progress to report.

The results have been tangible. Hudson now starts drug development committee meetings with an AI agent's assessment of whether a drug should advance to the next phase of trials or not. The agent will not just give its answer to that question, but weigh the drug's prospects against others in Sanofi's pipeline—and against alternative potential uses of Sanofi's capital. The AI provides "radical transparency" that Hudson sees as a multiplier for organizational change.

By 2025, Hudson had fundamentally reshaped Sanofi's portfolio and strategy. The company's immunology franchise, anchored by Dupixent (which achieved €13.5 billion in sales in 2024), had become the growth engine Hudson promised. The vaccine business, bolstered by successful RSV launches and strategic acquisitions, was delivering consistent returns. The rare disease portfolio, enhanced through targeted acquisitions, provided both growth and pricing power.

But questions remained about the sustainability of this acquisition-driven model. Sanofi still retains a sizeable capacity for further acquisitions. With biotechnology valuations at historic highs and competition for assets intensifying, how long could Sanofi continue buying innovation rather than building it? The company's R&D productivity, despite increased investment, still lagged industry leaders. And while Hudson's dealmaking had delivered short-term wins, the long-term integration challenges of absorbing so many companies so quickly remained untested.

VIII. Key Inflection Points: Strategic Shifts

The history of Sanofi can be understood through six critical moments where strategic decisions fundamentally altered the company's trajectory. Each inflection point represented not just a business decision but an existential choice about what kind of company Sanofi would become.

The 2008-2009 Patent Cliff Crisis forced the most dramatic transformation in Sanofi's history. When Chris Viehbacher arrived, the mathematics were brutal: €11 billion in annual sales would evaporate as patents expired, with no internal pipeline capable of replacing even half that revenue. The crisis forced three simultaneous pivots that would define Sanofi's next decade. First, the aggressive diversification into emerging markets, where branded generics could still command premiums. Second, the shift from primary care to specialty care, acknowledging that the blockbuster model of mass-market drugs was dying. Third, and most controversially, the admission that Sanofi couldn't innovate internally at the pace required, leading to the acquisition-driven strategy that persists today.

The response wasn't just financial engineering—it was a complete reimagining of pharmaceutical economics. Viehbacher's deals between 2008 and 2010 weren't evaluated on traditional metrics like earnings accretion or synergies. Instead, they were survival purchases, buying time and capability while the company rebuilt. The acquisition of Merial's consumer health business, the Zentiva generics purchase, the Medley deal in Brazil—each expanded Sanofi's definition of what constituted pharmaceutical value. This wasn't transformation by choice but adaptation through necessity.

The 2011 Genzyme Acquisition marked Sanofi's entry into biotechnology's elite tier. The $20.1 billion price tag wasn't just for products or pipelines—it was an admission fee to the future of medicine. The deal fundamentally changed Sanofi's DNA, shifting the portfolio from 72% small molecules to 72% biologics within eighteen months. But more importantly, it changed how Sanofi thought about drug development. Rare diseases, previously considered niche markets, became core to strategy. The economics of treating small patient populations with high-priced therapies replaced the volume-based model of primary care blockbusters.

The CVR structure pioneered in the Genzyme deal became a template for pharmaceutical M&A, allowing buyers and sellers to bridge valuation gaps when pipeline assets carried binary risk. The mechanism—paying additional consideration if certain milestones were met—aligned incentives while limiting downside risk. It was financial innovation meeting scientific uncertainty, creating a new language for valuing biotechnology assets.

The 2014 Viehbacher Ouster revealed the fundamental tension at Sanofi's core: could a French national champion operate as a global pharmaceutical company? The board's unanimous decision to fire Viehbacher wasn't about strategy—his diversification plan had worked, navigating the patent cliff successfully. It was about governance, culture, and identity. Viehbacher's decision to base himself in Boston, his unilateral pursuit of major acquisitions, his disregard for French stakeholder sensitivities—all reflected a CEO who saw Sanofi as a global company that happened to be headquartered in France, not a French company with global operations.

The firing sent shockwaves through the industry and revealed an uncomfortable truth: in pharmaceuticals, cultural integration matters as much as financial engineering. Viehbacher had saved Sanofi financially but alienated it culturally. His successor would need to balance global competitiveness with French identity—a challenge that continues to define Sanofi's strategic constraints.

The 2019-2020 Dupixent Success validated a decade of strategic pivots. The immunology drug, developed with Regeneron, became Sanofi's first internally developed blockbuster in years, reaching €5.5 billion in sales by 2020 and continuing to grow at 30%+ annually. Dupixent proved that Sanofi could still innovate, even if through partnership rather than solo development. It justified the shift to specialty care, the focus on immunology, and the Regeneron alliance that many had questioned.

More importantly, Dupixent provided the cash flow and confidence for Paul Hudson's aggressive transformation strategy. Without Dupixent's success, the Play to Win strategy, the R&D investment increases, and the recent acquisition spree would have been impossible. A single drug had given Sanofi the breathing room to reimagine itself once again.

The 2022 Identity Consolidation, dropping the Genzyme and Pasteur brands, was supposed to signal unity and focus. Instead, it revealed ongoing confusion about Sanofi's identity. The decision to eliminate sub-brands that had existed for decades (Pasteur for over a century) in favor of a lowercase "sanofi" with purple dots was met with derision from employees, investors, and industry observers. The rebranding wasn't just cosmetic—it represented a fundamental question Sanofi couldn't answer: was it better to be a collection of specialized excellence or a unified but generic whole?

The backlash was swift and severe. Eliminating the Pasteur name during a global pandemic, when vaccine manufacturers were household names, seemed particularly tone-deaf. The Genzyme brand, which had taken decades to build and billions to acquire, was erased overnight. Employees who had proudly worked for these storied institutions suddenly found themselves at a company that seemed to value typography over heritage.

The 2024-2025 M&A Acceleration represents the current inflection point, with implications still unfolding. Six major acquisitions in eighteen months, totaling over $15 billion in upfront payments, signal either strategic clarity or strategic panic. The deals—Inhibrx, Blueprint, Vicebio, Vigil, and others—all fit Hudson's stated focus on immunology, rare diseases, and vaccines. But the pace and premiums paid suggest urgency bordering on desperation.

The Blueprint acquisition's 40% premium over the 30-day VWAP, Vicebio's $1.15 billion upfront for a Phase 1 vaccine, Vigil's $470 million for an Alzheimer's candidate that larger companies had passed on—each deal makes strategic sense in isolation but collectively suggests a company trying to buy its way to relevance. The question isn't whether these acquisitions will deliver value—some certainly will—but whether Sanofi can integrate them fast enough to justify the premiums paid.

Each inflection point reveals a consistent pattern: Sanofi responds to crisis with transformation, usually through acquisition rather than innovation. The company has survived every industry upheaval not by anticipating change but by reacting aggressively when change arrives. This reactive resilience has kept Sanofi relevant but prevented it from leading. The company remains perpetually one step behind, buying what others have built rather than building the future itself.

IX. Playbook: Business & Investing Lessons

The Sanofi story offers a masterclass in corporate survival through serial transformation, but the lessons are as much cautionary as inspirational. For executives facing industry disruption, investors evaluating pharmaceutical companies, or entrepreneurs building in healthcare, Sanofi's journey illuminates both the power and perils of acquisition-driven strategy.

Serial Acquirer Strategy: Value Creation vs. Destruction

Sanofi has executed over 50 major acquisitions since 2000, fundamentally rebuilding itself multiple times through M&A. The evidence suggests that serial acquisition works—but only under specific conditions. First, there must be genuine strategic logic beyond financial engineering. The Genzyme acquisition succeeded because it brought capabilities Sanofi couldn't build internally: rare disease expertise, biologics manufacturing, and patient community relationships. The Aventis merger succeeded because it created necessary scale for global competition.

But serial acquisition fails when it becomes a substitute for strategy rather than an expression of it. The Bioverativ acquisition failed not because hemophilia was the wrong market but because Sanofi didn't anticipate how quickly Roche's Hemlibra would transform treatment paradigms. The company paid $11.6 billion for yesterday's technology. The lesson: in pharmaceuticals, you're not buying current products but future potential, and that requires deep scientific understanding, not just financial analysis.

Managing Patent Cliffs Through Portfolio Diversification

Viehbacher's response to the 2008-2009 patent cliff has become a template for pharmaceutical crisis management. Rather than attempting to replace lost revenue dollar-for-dollar with new drugs—mathematically impossible given development timelines—he diversified into adjacent businesses where Sanofi's capabilities could create value: vaccines, consumer health, emerging markets, and rare diseases. This portfolio approach reduced concentration risk and created multiple growth vectors.

The key insight was recognizing that not all pharmaceutical revenue is equal. A dollar from a patent-protected drug in the U.S. has different economics than a dollar from vaccines in emerging markets, which differs from consumer health products. By diversifying revenue sources, Sanofi reduced its vulnerability to any single shock. But diversification also created complexity, management challenges, and ultimately, the identity crisis that persists today.

The CVR Innovation: Creative Deal Structures

The contingent value rights structure pioneered in the Genzyme deal has become standard in biotechnology M&A, but few companies have used it as extensively as Sanofi. The mechanism allows buyers to bridge valuation gaps when pipeline assets carry binary risk—paying upfront for certainty and additional amounts for success. This isn't just financial engineering; it's risk allocation that aligns incentives between buyers and sellers.

But CVRs also create ongoing obligations and potential conflicts. The Genzyme CVR litigation revealed the fundamental tension: buyers have limited incentive to maximize contingent payments once they own the asset. Sanofi learned that CVR structures work best when milestones are objective (regulatory approvals) rather than subjective (commercial efforts), and when the amounts involved don't create perverse incentives.

Cultural Integration in Cross-Border Mega-Mergers

The Aventis merger and subsequent integrations offer a case study in the challenges of combining companies across national borders. French corporate culture, with its emphasis on consensus and stakeholder management, clashed with German precision and American entrepreneurialism. Each acquisition brought not just products but cultural DNA that needed integration.

Sanofi's approach—maintaining separate identities initially, then forcing integration through rebranding—satisfied no one. The Genzyme team felt their entrepreneurial culture was being suffocated. The Pasteur scientists saw their century-old heritage erased. The lesson: cultural integration requires intentional design, not passive hope. Companies must explicitly decide which cultural elements to preserve, which to eliminate, and which to blend—and then execute that vision consistently.

Board-CEO Dynamics: The Viehbacher Cautionary Tale

Viehbacher's firing despite delivering strong financial results offers a masterclass in governance failure. The breakdown wasn't about strategy but about communication, stakeholder management, and cultural sensitivity. Viehbacher ran Sanofi like an American CEO—focused on shareholders, comfortable with unilateral decisions, and dismissive of political considerations. The board expected a French CEO—attentive to multiple stakeholders, collaborative in decision-making, and politically sophisticated.

The lesson extends beyond national differences. In any company, but especially in pharmaceuticals where government relations matter, CEOs must manage boards as actively as they manage businesses. Viehbacher's failure wasn't operational but relational. He delivered results but lost trust. In industries where long-term investments require board patience, trust matters more than quarterly earnings.

Competing for Biotech Assets: Premium Inflation

Sanofi's recent acquisitions reveal a troubling dynamic in pharmaceutical M&A: premium inflation driven by competitive desperation. When multiple acquirers chase limited assets, prices disconnect from fundamental value. The Blueprint deal's structure, the Vicebio valuation, the Vigil premium—all suggest a market where strategic need overwhelms financial discipline.

The challenge for acquirers: how to compete without overpaying. Sanofi's approach—using CVRs, strategic investments that create exclusive negotiating rights, and surgical deal structures that split companies—shows creativity but also limitation. When everyone has the same playbook, differentiation becomes impossible, and price becomes the only variable. The result is value transfer from acquirer shareholders to target shareholders, with uncertain benefits for patients.

Building vs. Buying Innovation

The fundamental question facing Sanofi—and all pharmaceutical companies—is whether innovation can be sustainably acquired rather than developed. Sanofi's history suggests a troubling answer: companies that rely primarily on acquisition for innovation eventually lose the capability to evaluate what they're buying. Without internal R&D excellence, how can management assess external opportunities? Without scientists who understand cutting-edge science, how can business developers identify breakthrough technologies?

Hudson's increased R&D investment represents an attempt to rebuild internal capability while continuing aggressive acquisition. But the cultural challenge remains: how to maintain entrepreneurial innovation within a company built through serial acquisition? How to preserve the excellence of acquired companies while achieving integration synergies? Sanofi hasn't solved these puzzles—no pharmaceutical company has—but its struggles illuminate the challenge.

X. Analysis & Bear vs. Bull Case

As we evaluate Sanofi in 2025, the company presents a fascinating study in contradictions. It generates over €43 billion in revenue yet trades at a discount to peers. It has successfully navigated every industry crisis yet never leads industry transformation. It has assembled an impressive portfolio through acquisition yet struggles with organic innovation. Understanding Sanofi requires holding multiple truths simultaneously.

The Bull Case: Transformation Momentum

Optimists point to tangible evidence of successful transformation. Dupixent has become one of the industry's most successful drugs, with 2024 sales of €13.5 billion and continued growth potential across multiple indications. The immunology franchise that Dupixent anchors could reach €20 billion by 2030, providing the cash flow for continued investment and acquisition. This isn't speculative—Dupixent's growth trajectory remains robust, with new indications regularly approved and geographic expansion ongoing.

The rare disease portfolio, built through acquisitions like Genzyme and Inhibrx, provides both growth and pricing power. These aren't commoditized primary care drugs but specialized therapies for underserved populations where Sanofi can command premium pricing and maintain market position. The economics of rare diseases—high prices, loyal patients, limited competition—offer sustainable competitive advantages that mass-market drugs cannot match.

Vaccines represent another strength, particularly after the Vicebio acquisition. While Sanofi missed the mRNA revolution during COVID-19, it maintains leading positions in influenza, RSV, and other respiratory vaccines. The aging global population ensures growing demand for vaccines, and Sanofi's manufacturing scale and distribution expertise create barriers to entry. The vaccine business generates steady, predictable cash flows that support the company's broader transformation.

Emerging markets exposure, built through Viehbacher's diversification strategy, provides growth as healthcare access expands globally. Sanofi's presence in China, India, Brazil, and other developing markets offers both volume growth and currency diversification. As these markets develop, branded generics transition to innovative drugs, creating upgrade opportunities within Sanofi's existing customer base.

The bull case ultimately rests on execution. If Hudson can successfully integrate recent acquisitions, if Dupixent continues its growth trajectory, if the pipeline delivers even modest success, Sanofi could re-rate significantly. The company trades at roughly 11x forward earnings versus 15-16x for peers—closing that gap would create substantial shareholder value.

The Bear Case: Structural Challenges

Skeptics see a company perpetually behind the curve, buying innovation at premium prices because it cannot create it internally. The R&D productivity crisis isn't improving despite increased investment. Sanofi spends €8.5 billion annually on R&D but hasn't developed a breakthrough drug internally since Dupixent—and even that required Regeneron's antibody platform. The pipeline, while extensive, lacks obvious blockbusters beyond acquired assets.

Integration risks loom large. Six major acquisitions in 18 months creates enormous organizational challenge. Each acquired company brings different cultures, systems, and processes that need harmonization. The track record of pharmaceutical mega-mergers suggests that promised synergies rarely materialize fully, while integration costs often exceed budgets. Sanofi's history of cultural clashes—from Aventis to Genzyme—suggests these challenges won't be easily overcome.

The identity crisis remains unresolved. Is Sanofi a pharmaceutical company, a biotechnology company, or a diversified healthcare conglomerate? The answer matters for capital allocation, organizational design, and investor expectations. Companies that try to be everything to everyone often end up being nothing to anyone. The recent rebrand to a unified Sanofi hasn't clarified strategy—it's simply hidden the confusion behind purple dots.

Competition intensifies across every therapeutic area. In immunology, Sanofi faces AbbVie's Humira franchise, Johnson & Johnson's Stelara, and emerging competitors. In rare diseases, Vertex, Biomarin, and others have deeper expertise and stronger pipelines. In vaccines, Moderna and BioNTech have platform technologies that could disrupt traditional approaches. In neurology, Biogen, Roche, and Eli Lilly have more advanced Alzheimer's programs. Sanofi competes everywhere but leads nowhere.

The French factor cannot be ignored. Government influence, while providing some protection in home markets, constrains global competitiveness. The political backlash over the Opella sale, the pressure to maintain French employment, the complexity of French labor law—all create structural disadvantages versus American and Swiss competitors. The recurring CEO challenges—from Viehbacher's firing to questions about Hudson's tenure—reflect deeper governance issues that won't be easily resolved.

Financial Reality Check

The numbers tell a mixed story. Revenue growth has been solid but unspectacular—mid-single digits excluding COVID impacts. Margins have improved but remain below best-in-class peers. Return on invested capital has declined as acquisition premiums increased. Free cash flow generation remains strong, but an increasing portion goes to servicing acquisition-related obligations rather than returning to shareholders.

The balance sheet can support continued acquisition, but at what cost? Sanofi's net debt-to-EBITDA ratio remains conservative, providing firepower for deals. But each acquisition at premium prices reduces future return potential. The company risks becoming a roll-up vehicle rather than an innovation engine—financially stable but strategically stagnant.

Competitive Positioning

Against Roche, Sanofi lacks scientific leadership and innovation culture. Against Novartis, it lacks focus and operational excellence. Against Johnson & Johnson, it lacks scale and diversification logic. Against Pfizer, it lacks both COVID windfall profits and clear strategic direction. Sanofi occupies an uncomfortable middle ground—too big to be nimble, too small to dominate, too diversified to be focused, too concentrated to be resilient.

The competitive reality is that Sanofi competes for the same assets, talent, and opportunities as better-positioned rivals. When Novartis, Roche, or Pfizer want an asset, they can often outbid Sanofi or offer better strategic fit. When top scientists choose employers, they gravitate toward companies with stronger innovation reputations. When partners seek collaborators, they prefer companies with clearer strategic focus. Sanofi must work harder and pay more for equivalent outcomes.

XI. Epilogue & "If We Were CEOs"

Standing at Sanofi's headquarters at 46 avenue de la Grande Armée in Paris—the company moved from rue La Boétie in 2023—one can't help but wonder what François Mitterrand would think of his industrial champion today. The company he helped create to ensure French pharmaceutical independence has become so thoroughly globalized that it dropped French brands like Pasteur while selling Doliprane to American private equity. The paradox of Sanofi is that in succeeding globally, it may have lost what made it special locally.

The 2025 acquisition spree isn't ending. As this article goes to press, rumors swirl about Sanofi's interest in mRNA technology companies, gene therapy platforms, and even a potential mega-merger with a European peer. The company's appetite for deals appears insatiable, driven by a combination of strategic necessity and competitive pressure. But each deal adds complexity to an already complex organization, and integration capacity is finite even if financial capacity seems unlimited.

If we were CEOs of Sanofi, the temptation would be to continue the acquisition strategy—it's worked before, the balance sheet supports it, and the market expects it. But that would be fighting the last war. The pharmaceutical industry is entering a new phase where platform technologies, artificial intelligence, and personalized medicine will matter more than scale and portfolio breadth. Sanofi needs capabilities, not just assets.

The first priority would be fixing R&D productivity. Not through reorganization or rebranding but through fundamental cultural change. This means accepting more failure, taking bigger scientific risks, and most importantly, giving scientists time and freedom to pursue breakthrough rather than incremental innovation. The AI initiatives Hudson has started are promising, but they need to be embedded in scientific culture, not imposed upon it.

Second, we would dramatically simplify the portfolio. The attempt to be present in all therapeutic areas and geographies creates complexity that destroys value. Better to dominate three areas than compete in ten. This means divesting non-core assets—even profitable ones—to focus resources where Sanofi can win. The Opella sale was a start, but more radical portfolio surgery is needed.

Third, resolve the identity crisis definitively. Sanofi should embrace being a European pharmaceutical company—not trying to be American, not pretending to be a biotech, but leveraging European advantages: strong science education, government support for basic research, and different risk tolerance. This means accepting lower margins but also lower volatility, prioritizing sustainable innovation over quarterly earnings.

Fourth, fix the governance structure. The board-management tensions that have plagued Sanofi reflect structural rather than personal issues. The company needs a governance model that balances stakeholder interests while enabling decisive action. This probably means a smaller, more international board with deeper industry expertise and clearer role definition between board and management.

Finally, we would prepare for the next crisis—because in pharmaceuticals, crisis is inevitable. Whether it's another patent cliff, a safety scandal, or disruption from new technologies, Sanofi will face existential challenges again. Building resilience through diversification helped survive the last crisis, but the next one will require different tools: technological capabilities, organizational agility, and most importantly, a clear sense of purpose that transcends financial engineering.

The bull case for Sanofi remains compelling: strong franchises, improving pipeline, and financial capacity for continued transformation. But the bear case is equally valid: structural challenges, competitive disadvantages, and strategic confusion. The truth, as often in complex situations, lies between extremes. Sanofi will likely continue to muddle through—neither failing spectacularly nor succeeding brilliantly, generating decent returns while never quite fulfilling its potential.

For investors, Sanofi represents a value play rather than a growth story—a company trading at a discount that might narrow but probably won't disappear. For competitors, it's a reliable acquirer of assets they don't want and a source of talent they can poach. For France, it remains a national champion that increasingly feels neither national nor championship caliber. For patients, it provides important medicines but rarely breakthrough innovations.

The Sanofi story ultimately illustrates a fundamental truth about modern pharmaceuticals: financial engineering can ensure survival but cannot create excellence. Serial acquisition can build scale but not capability. Portfolio diversification can reduce risk but also dilutes focus. The company that began as a bet on French industrial policy has become a case study in the limits of M&A-driven strategy.

As we look toward 2030, Sanofi faces a choice: continue the pattern of reactive transformation through acquisition, or finally build the internal capabilities for proactive innovation. The recent AI initiatives, increased R&D investment, and portfolio focusing suggest recognition of this challenge. But recognition and resolution are different things. Sanofi has proven remarkably adept at survival through transformation. Whether it can transform survival into leadership remains the unanswered question.

The story of Sanofi is far from over. Like the company itself, it will likely continue through unexpected chapters, sudden pivots, and serial reinventions. The company that started as a subsidiary of an oil company has become one of the world's largest pharmaceutical companies through sheer persistence and financial creativity. That's an achievement worth recognizing, even if it's not the triumph its founders envisioned.

In the end, Sanofi embodies both the promise and peril of modern pharmaceutical companies: enormous resources pursuing uncertain science, global scale struggling with local relevance, financial sophistication compensating for innovation challenges. It's a company that has everything except clarity about what it wants to become. And in an industry where identity drives strategy, that absence may matter more than all the acquisitions money can buy.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube