Shelly Group: The Open-Source Trojan Horse of the IoT

I. The Hidden European Tech Giant

Open the settings app on your phone. Somewhere in the background, a trillion-dollar company is watching: which lights you turned on, when you left the house, what temperature you keep the bedroom at night. Amazon, Google, and Apple have spent a decade building smart home ecosystems that are, beneath the polished marketing, elaborate surveillance apparatuses disguised as convenience. Every voice command to Alexa, every "Hey Google" request, every HomeKit trigger feeds a data pipeline that ultimately serves advertising and services businesses.

Now imagine a device that connects to your Wi-Fi, responds to your commands, and then does something radical: it lets you control everything from your own local network, without sending a single byte to the cloud. No account required. No app mandatory. No data harvested.

And if you want to write your own software to control it, the company publishes every API endpoint and actively encourages you to hack the firmware. You can flash third-party firmware onto the device without voiding the warranty. You can integrate it with any automation platform you choose. You can run it entirely offline, in a bunker, on a boat, in a cabin without internet, and it will work perfectly.

This is the Shelly value proposition. And it is the foundation of one of the most improbable corporate journeys in European technology.

It has turned a small Bulgarian company, founded as an SMS services business in Sofia, into one of the most remarkable growth stories in European technology. Shelly Group SE, trading on the XETRA exchange under the ticker SLYG, crossed the one-billion-euro market capitalization threshold in June 2025. As of April 2026, it trades at approximately fifty-six euros per share. Revenue grew forty percent in fiscal 2025 to nearly one hundred and fifty million euros. The company has shipped twenty-nine million devices into one hundred and thirty countries. Five and a half million households use Shelly products.

The gross margin sits at roughly fifty-eight percent, a figure that would be respectable for a pure software company and is extraordinary for a business that ships physical hardware. For context, Logitech operates at gross margins in the low forties. Even Apple runs at roughly forty-six percent on its products division.

On April 10, 2026, the Deutsche Börse announced that Shelly Group would join the SDAX index, the small-cap benchmark that sits beneath the MDAX and DAX in Germany's equity index hierarchy. For a company founded in Sofia, Bulgaria, and listed on the Bulgarian Stock Exchange just ten years ago, the inclusion represents an extraordinary corporate arc.

And yet, outside the world of smart home enthusiasts, professional electricians, and a growing community of European institutional investors, almost nobody has heard of them. There is no iconic origin story involving a Stanford dorm room or a Palo Alto garage. The global technology press, fixated on Silicon Valley and Shenzhen, has largely ignored a company compounding revenue at forty-plus percent annually while generating genuine operating profits.

This is not venture-capital-subsidized growth. This is profitable growth, funded from internal cash flow, in a market where most competitors are either burning through investor capital or surviving on razor-thin margins.

The thesis is straightforward but powerful. Shelly is the "Linux of the Home": a capital-light, high-margin hardware platform that succeeded by doing the exact opposite of what every competitor was doing. Where Amazon, Google, and Apple built walled gardens, Shelly built an open field. Where Chinese manufacturers built cloud-dependent devices that stopped working when the server went down, Shelly built devices that work perfectly with no internet connection at all. Where venture-backed hardware startups burned through hundreds of millions chasing growth, Shelly funded its expansion from cash flow and a modest Bulgarian stock exchange listing.

From SMS billing to custom silicon, from the Bulgarian Stock Exchange to the SDAX, from hobbyist relays to professional building infrastructure, this is the story of how a company that started selling ringtones became the most trusted name in open smart home technology.

II. The Pivot: From VAS to IoT

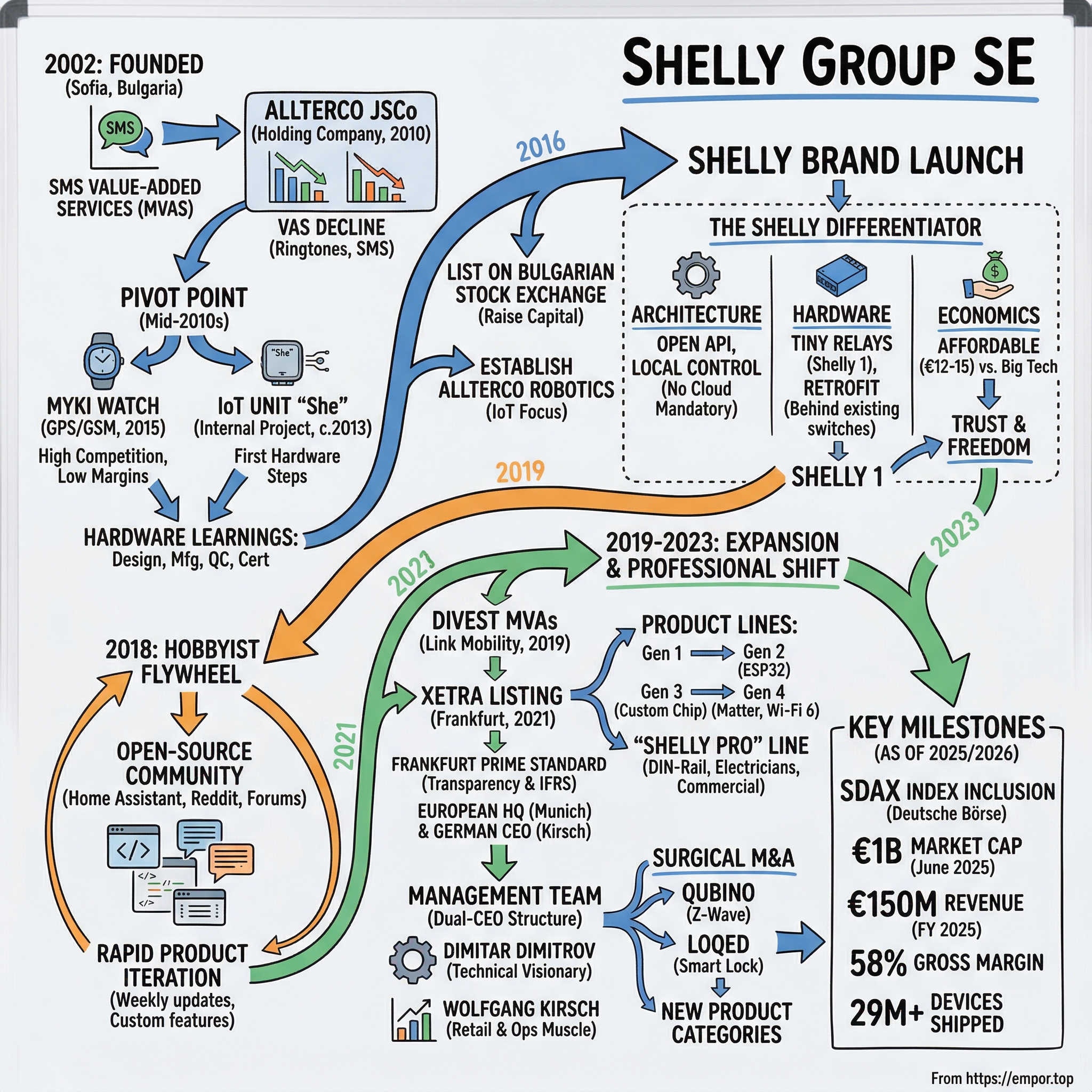

Before there was Shelly, there was Allterco. And before Allterco, there were ringtones.

Dimitar Dimitrov began his business career in 2002, building relationships with mobile operators in Bulgaria. The early 2000s were a golden age for mobile value-added services, the industry that provided everything from premium SMS notifications to downloadable ringtones to mobile billing solutions. If you lived in Eastern Europe in 2004 and texted a shortcode to vote in a TV talent show or download a polyphonic ringtone of a pop song, there is a reasonable chance the infrastructure behind that transaction was built by Dimitrov and his partners.

In 2003, Dimitrov and Svetlin Todorov co-founded Teracomm, a Sofia-based telecommunications company. The partnership between the two men would prove remarkably durable: more than two decades later, they still run the company together, still hold the majority of the equity, and still drive the strategic direction. Teracomm grew into a network of entities operating across Romania, Macedonia, Singapore, the United States, and half a dozen other countries. Todorov handled international expansion and ran the US-based division.

The business was profitable, cash-generative, and growing.

It was also, as both founders recognized with increasing clarity, a melting ice cube. Smartphone app stores eliminated the need for premium SMS as a distribution channel. Why would you text a shortcode to download a ringtone when you could open the App Store? Mobile operators began cutting the revenue shares. Social media platforms destroyed the economics of paid messaging.

By the mid-2010s, the VAS business model was in terminal decline. The revenue was still flowing, but the trend line was unmistakable.

In 2010, the founders restructured their various entities into a holding company called Allterco JSCo.

The restructuring was not just administrative. It was existential. Dimitrov and Todorov needed a new business to build before the old one disappeared entirely.

Their first forays into hardware were tentative and instructive. Around 2013, an internal IoT unit began developing a home automation system called "She," a precursor to the Shelly brand. The project was modest in scope but important in ambition: it marked the first time the company's engineers shifted from pure software and telecom services to building physical products.

In 2015, the company launched MyKi, a GPS and GSM smartwatch designed for children. The concept was elegant: a wearable that allowed parents to track their child's location and make calls, powered by a SIM card and the same mobile network infrastructure that Dimitrov's team had been building on for years. MyKi was a learning experience rather than a breakthrough. The children's wearable market was crowded, price-sensitive, and dominated by Chinese manufacturers who could undercut any European competitor on cost. Margins were thin. Distribution was difficult.

But the MyKi experience taught the Allterco team something invaluable: how to design, manufacture, and distribute physical consumer electronics. They learned about component sourcing, firmware development, quality control, certification, and the brutal economics of consumer hardware where a single defective batch can wipe out a quarter's margin. These were expensive lessons, but they would prove essential when the company found the product that would change everything.

What gave Allterco an advantage that most hardware startups lacked was the absence of venture capital.

This sounds counterintuitive. But the VAS cash flows, while declining, provided a financial runway that eliminated the need for outside investors and the pressure to pursue growth at all costs. The constraints of the Bulgarian market reinforced this discipline. Sofia in 2015 was not a city with venture capital firms eager to fund hardware moonshots. The founders had to build a profitable business from the start, because the only alternative was running out of money.

In 2015, an affiliate company called Allterco Robotics was established specifically to house the IoT and hardware initiatives.

This was not merely an organizational reshuffle. It was a signal of strategic intent: the IoT business would have its own identity, its own team, and its own mandate to grow, rather than being buried inside a telecommunications conglomerate focused on managing decline.

In 2016, the company made two pivotal decisions. First, it divested the entire European telecommunications business and committed fully to IoT and consumer devices. Second, Allterco listed on the Bulgarian Stock Exchange in December 2016, raising capital to fund the hardware business. The decision to go public rather than seeking venture capital was characteristic of the founders' approach: a stock exchange listing provided capital without the governance constraints, aggressive growth expectations, and forced-exit timelines that come with institutional venture funding.

In 2019, the remaining MVAS operations were sold to Link Mobility, a Norwegian communications platform company, for 7.9 million euros. The sale severed the last tie to the company's original identity and committed every euro of resources to the IoT future.

Now came the product that changed everything. The smart home market in 2016 and 2017 was dominated by smart bulbs, smart plugs, and smart speakers. Philips Hue had established the premium end with a Zigbee-based system requiring a dedicated bridge, a proprietary app, and fifty-dollar smart bulbs. Chinese manufacturers were flooding Amazon with cheap Wi-Fi plugs that stopped functioning when a cloud server went down.

Both approaches shared a fundamental limitation: they required the homeowner to replace existing hardware. If you wanted to make your living room lights smart, you either bought new bulbs, new switches, or new plugs. The existing infrastructure, the wiring, the switches, the fixtures that an electrician had installed, was treated as dead infrastructure to be bypassed rather than upgraded. This replacement model had a second problem: cost. A typical European home might have thirty to forty light circuits, plus shutters, plus heating controls. Making everything smart by replacing components could easily cost two thousand euros, and the result was a fragile ecosystem of devices from different manufacturers with different apps, different cloud dependencies, and different update schedules.

The Shelly 1 took a completely different approach. It was a tiny Wi-Fi-enabled relay, about the size of a matchbox, that fit inside a standard electrical junction box behind an existing light switch. You did not replace anything. You added intelligence to what was already there. The existing switch continued to work exactly as before. But now, the light could also be controlled remotely, automated through schedules, and integrated into any smart home platform.

The retail price was roughly twelve to fifteen euros.

For context, a single Philips Hue smart bulb cost fifty euros and required an additional sixty-euro bridge. For the price of one Hue bulb, a homeowner could make four or five conventional circuits smart. Unlike a smart bulb that needed replacing when the LED failed, the Shelly relay was a solid-state device with no moving parts. Its expected operational lifetime was measured in decades.

But the price was only half the story. The other half was architecture. The Shelly 1 was based on the ESP8266, a cheap but capable Wi-Fi microcontroller made by Espressif Systems, a Shanghai-based semiconductor company. This chip had become the darling of the open-source hardware community because it was inexpensive, well-documented, and supported by a thriving ecosystem of open-source firmware projects, most notably Tasmota and ESPHome.

Every Shelly device exposed a local REST API, a technical interface that allowed users to send commands directly to the device over the local network without ever touching the internet. Think of it like this: most smart home devices are like a restaurant where you can only order through the restaurant's own app. Shelly is like a restaurant that publishes its recipe book and lets you cook in the kitchen. The device included an embedded web server for configuration, accessible from any browser. And native MQTT support, a lightweight messaging protocol widely used in industrial automation, meant that technically sophisticated users could integrate Shelly devices into virtually any automation system.

MQTT deserves a brief explanation for non-technical readers. It is a protocol designed for machines to talk to each other efficiently. Originally developed for oil pipeline monitoring in the desert, where bandwidth was scarce and reliability critical, it has become the lingua franca of the industrial and home automation world. Shelly's native MQTT support meant its devices spoke the same language as industrial automation equipment, a capability that would prove strategically important when the company expanded into professional building management.

But the real genius was subtler than pricing or protocols. The Shelly 1 solved the "spouse test." Smart home enthusiasts had been fighting a losing battle to get non-technical family members to use smart home technology. Smart bulbs failed because flipping the physical switch disconnected them from the network, breaking all automations. Smart plugs failed because they added ugly dongles between wall outlets and appliances.

The Shelly 1, installed behind the wall, was invisible. The physical switch continued to work exactly as before. No one in the household needed to change their behavior, learn a new app, or even know that the home had been "smartened." The intelligence was hidden, silent, and unobtrusive.

This seemingly trivial insight, that the best smart home device is one that nobody notices, turned out to be the key to mass adoption. It meant Shelly devices could be installed in rental apartments without modifying the landlord's property. They could be deployed in elderly relatives' homes without requiring technology training. They could be fitted by electricians during routine renovations without adding complexity. And they could be removed just as easily, a renter moving out could pull the relay, restore original wiring in minutes, and take the device to their next apartment.

And then came the decision that defined the brand forever. Shelly actively encouraged users to flash third-party firmware onto their devices. If you bought a Shelly 1 and wanted to replace the stock firmware with Tasmota or ESPHome, you could do so without voiding the warranty. This was the equivalent of a car manufacturer telling you to replace the engine management computer with your own software and still bring the car in for warranty service.

To appreciate how radical this was, consider the prevailing approach. Every other smart home manufacturer treated their firmware as proprietary and locked down. Tuya devices, if you flashed alternative firmware, voided the warranty and often bricked the device. Sonoff made it technically possible but actively discouraged it. Ring and Nest devices were completely locked ecosystems where user-modifiable firmware was architecturally impossible.

It was not altruistic. It was strategically brilliant. It was what Clayton Christensen called "asymmetric motivation": doing something your competitors are structurally unwilling to do. By embracing the open-source community, Shelly gained something no amount of marketing spend could buy: trust.

The Home Assistant community, a global network of hundreds of thousands of smart home enthusiasts who run their own home automation servers, adopted Shelly as the de facto standard for affordable, locally controlled hardware. YouTube reviewers, bloggers, forum moderators, and Reddit commentators became an unpaid global sales force, producing thousands of tutorials, reviews, and integration guides. Every YouTube video titled "Best Smart Home Relay — Why Shelly Wins" was, in effect, a free commercial produced by someone who genuinely believed in the product. No advertising agency can manufacture that kind of authenticity.

The economics of this community-driven growth model are worth pausing on. Traditional consumer electronics companies spend between fifteen and twenty-five percent of revenue on sales and marketing. Apple, with arguably the strongest brand in consumer technology, spends roughly seven percent. Shelly, by cultivating an organic community of evangelists, achieved its growth with marketing expenditure that is a fraction of what traditional competitors spend.

The community also served as a remarkably effective product feedback loop.

Shelly engineers actively monitored the Home Assistant forums, Reddit's smart home communities, and German-language DIY electronics boards. Feature requests that came from power users, things like improved MQTT implementation, better webhook support, or specific dimmer curve profiles, often appeared in firmware updates weeks later.

This tight feedback cycle between the developer community and the engineering team created a pace of iteration that larger, more bureaucratic competitors simply could not match. At Philips, a firmware change to the Hue bridge might take months to navigate through product management, QA, legal review, and staged rollout. At Sonoff, firmware updates were infrequent and often broke backward compatibility. At Shelly, a firmware update could go from community feature request to beta release in weeks, and from beta to stable release in a month.

The native Home Assistant integration, which allowed Shelly devices to be automatically discovered and controlled within the open-source platform, cemented the relationship. Home Assistant had grown from a hobby project by a Dutch developer named Paulus Schoutsen into the de facto standard for privacy-conscious, locally controlled smart homes. Its user base expanded from tens of thousands in 2017 to hundreds of thousands by 2020, and each new Home Assistant user was a potential Shelly customer. The integration created a flywheel: more Home Assistant users meant more Shelly customers, which meant more community content, which attracted more Home Assistant users.

The product line expanded rapidly through 2018, 2019, and 2020. The Shelly 2 offered dual-relay control for blinds and shutters. The Shelly Dimmer brought smart dimming to conventional lights. The Shelly Plug provided smart outlet functionality. Each product followed the same philosophy: small, affordable, open, and invisible once installed. A US office was established in Las Vegas in 2019. By 2020, the Shelly brand had achieved something marketing textbooks say is impossible for a low-budget company: genuine brand loyalty in a commoditized hardware market.

But there was a ceiling to the community-driven model.

The Home Assistant community, while passionate and growing, represented a niche: technically sophisticated users willing to run local servers and debug YAML configuration files. These were early adopters by definition, the kind of people who spent Saturday afternoons soldering headers onto circuit boards and debugging network configurations.

To grow beyond this niche, Shelly needed to reach two audiences that the community could not serve: mainstream consumers who wanted a simple app experience, and professional electricians who needed products they could install at scale with minimal configuration. That required a different kind of leadership.

III. The Professional Shift and the XETRA Upgrade

In November 2021, Shelly listed on the Frankfurt Stock Exchange's XETRA platform. The shares were admitted to the Prime Standard, the highest transparency segment of the Deutsche Börse, requiring quarterly reporting, IFRS accounting standards, and English-language disclosure. The initial listing price was fourteen euros and fifty cents per share.

The XETRA listing made Allterco the first Bulgarian company with shares directly admitted to a regulated foreign market. This was not just a capital markets maneuver. It was a statement of intent. The message was deliberate and coordinated: the company hired a German executive, listed on the German stock exchange, and established its European headquarters in Munich. If German institutional investors, the most important pool of capital for European mid-cap technology companies, were going to take Shelly seriously, the company needed to speak their language, literally and figuratively.

The Prime Standard admission also imposed discipline. Quarterly reporting, IFRS accounting standards, and English-language disclosure created the kind of transparency framework that institutional fund managers expect before committing capital. For a company transitioning from a small Bulgarian exchange where reporting standards were less rigorous, this was a meaningful governance upgrade.

The stock languished through much of 2022 and early 2023, trading in the mid-teens as the global semiconductor shortage disrupted supply chains and European technology sentiment soured. This was a frustrating period for early believers. The underlying business was performing well, but the market was not paying attention to a Bulgarian-listed company trading on a foreign exchange with minimal analyst coverage and almost no institutional ownership.

But from mid-2023 onward, as revenue growth accelerated and the professional strategy gained traction, the stock entered a sustained re-rating that would carry the share price from the mid-teens to nearly seventy euros at its peak. As of April 2026, those shares trade at roughly fifty-six euros, nearly a four-fold increase in just over four years. The fifty-two-week range stretches from roughly thirty-three euros to seventy-two euros, reflecting the kind of volatility that comes with a rapidly growing company and a thin free float.

The corporate evolution continued in parallel with the financial one. In June 2023, an Extraordinary General Meeting approved the name change from Allterco JSCo to Shelly Group Plc. In October 2023, another EGM approved the conversion to a Societas Europaea. The legal transformation was completed in December 2024.

The Societas Europaea legal form, used by companies like BASF, Porsche, and Airbus, signals commitment to pan-European governance standards and facilitates cross-border operations. It also positions the company more credibly for future inclusion in European equity indices beyond the SDAX. Shelly is not a Bulgarian company that happens to sell in Europe. It is a European company that happens to be headquartered in Bulgaria. The distinction matters for institutional investors who have country-specific allocation limits or who prefer companies domiciled under familiar European legal frameworks.

The capital allocation philosophy throughout this period stood in sharp contrast to the acquisition-driven strategies that have defined, and in many cases destroyed, value in the smart home industry.

Consider the wreckage that littered the landscape. Google acquired Nest for 3.2 billion dollars in 2014. The acquisition was supposed to give Google a beachhead in the connected home. Instead, Google spent years trying to integrate a product line that alienated its original user base, saw multiple founders and key executives depart, and failed to generate the kind of revenue growth that would justify a three-billion-dollar purchase price. The Nest thermostat, once the poster child of elegant smart home design, became a cautionary tale about what happens when a hardware company is absorbed by a software giant with fundamentally different priorities.

Samsung purchased SmartThings for two hundred million dollars in 2014 and struggled to maintain developer interest as the platform languished under layers of corporate bureaucracy. The product went through multiple architectural rewrites, each one alienating the existing developer community that had been the platform's primary asset.

Amazon took yet another approach, pouring billions into Alexa-powered devices sold at or below cost, essentially subsidizing hardware to harvest voice data and build an advertising and commerce pipeline. This strategy generated massive device distribution but questionable profitability, and the Alexa division reportedly went through significant layoffs in 2022 and 2023 as Amazon's leadership questioned whether the investment was generating adequate returns.

Shelly's M&A approach was the opposite: surgical, infrequent, and almost comically frugal. The first notable deal was the acquisition of a sixty-percent stake in GOAP d.o.o., a Slovenian IoT company that produced Qubino-branded smart home devices, for two million euros. The strategic logic was clear: Qubino specialized in Z-Wave protocol devices, giving Shelly access to a protocol ecosystem that complemented its Wi-Fi-first approach. The company was renamed Shelly Tech and integrated into the broader portfolio.

The second deal was even more striking. In July 2024, Shelly acquired the assets of LOQED B.V., a Dutch smart lock company undergoing insolvency proceedings, for one hundred and fifty thousand euros. For that sum, Shelly obtained technology, intellectual property, existing inventory, and the supplier network. The first batch of one thousand units sold out immediately. Four thousand additional units were pre-sold.

Paying one hundred and fifty thousand euros for a functioning smart lock product line with existing customer demand is the kind of deal that makes venture-capital-backed competitors weep. It exemplifies the disciplined, cash-conscious approach to capital allocation that the founders brought from their VAS-era roots.

The company also acquired an additional fifty-percent stake in Shelly Asia Ltd in 2024, consolidating ownership of its online sales and production oversight operations in the region where its manufacturing supply chain is centered.

The pattern across all these transactions reveals a management team that views M&A as a scalpel, not a sledgehammer. Each deal addressed a specific strategic need: Qubino for Z-Wave protocol access, LOQED for smart lock entry, Shelly Asia for supply chain control. None was large enough to create integration risk or distract management from the organic growth engine that remains the company's primary value creator.

There has also been an intriguing balance sheet movement that deserves closer attention. Approximately one hundred million euros was repositioned to the holding company level, described by management as preparatory for potential capital increases, acquisitions, or cash distributions. No specific targets have been disclosed, but the positioning suggests a war chest for a larger deal, likely in professional building automation or energy management. Given the company's disciplined track record of paying two million for Qubino and one hundred fifty thousand for LOQED, any significant deployment of a hundred-million-euro war chest would represent a substantial escalation in M&A ambition and would warrant close scrutiny.

The organic versus inorganic growth philosophy is worth highlighting. Unlike many technology companies that use acquisitions as a substitute for innovation, Shelly has overwhelmingly grown organically. The vast majority of its product line was developed internally. The acquisitions were capability additions filling specific protocol or product category gaps, not revenue purchases. This approach keeps integration risk low and preserves the lean operating culture that is one of the company's competitive advantages.

The SDAX inclusion, confirmed on April 10, 2026, represents the culmination of this institutional transformation. Index inclusion triggers automatic buying from passive funds, places Shelly on the radar of the broader German institutional community, and provides the liquidity foundation that larger investors require.

IV. Management: The Retail Meets Visionary Duo

By 2021, Shelly had a problem most startups would envy.

Demand was outpacing the company's ability to manage it. The product line had expanded from the original relay to include dual relays, dimmers, plugs, RGBW controllers, sensors, and the Pro line for commercial applications. Sales were growing explosively, particularly in the DACH region. But the company was still being run like a startup, with the founders handling everything from product development to investor relations.

Dimitar Dimitrov is the technical visionary of the partnership. He understood telecommunications infrastructure from the VAS era, saw the IoT opportunity before most of the market, and made the crucial decision to embrace openness as a competitive strategy. His engineering instincts, honed through years of building mobile billing systems and then consumer hardware, gave Shelly its technical DNA: small devices, open protocols, local-first architecture. Dimitrov is the kind of founder who monitors GitHub issues and reads user forum posts, maintaining a direct connection to the developer community that built Shelly's reputation.

Svetlin Todorov is the international strategist. He ran the US-based division, Global Teracomm, during the telecommunications years and provided the cross-border perspective that shaped Shelly's global expansion. While less publicly visible than Dimitrov, Todorov's influence on the company's international architecture, from the Singapore operations to the US market entry, has been substantial.

Together, the two founders own approximately two-thirds of the company, with Dimitrov holding roughly thirty-seven percent and Todorov holding roughly thirty percent. That level of insider ownership, sustained through an IPO and a decade of growth, sends an unmistakable signal about management's long-term commitment. Neither founder sold significant stock until June 2024, when Dimitrov sold roughly ten million euros worth and Todorov sold roughly six and a half million euros worth, both at thirty-three euros per share. These disposals, while significant in absolute terms, represented small fractions of their total holdings and were consistent with the portfolio diversification that long-tenured founder-owners typically undertake when their personal wealth becomes concentrated in a single asset.

But the founders recognized that the next phase required a different kind of leader.

Someone who understood European retail at scale. Someone who could build distribution networks, negotiate with major electronics retailers, professionalize the supply chain, and, critically, position Shelly as a credible brand for professional installers, not just hobbyists.

They found Wolfgang Kirsch. His background read like it had been designed in a laboratory specifically for this role. Born in 1963 in Cornberg, a small town in Hesse, Germany, Kirsch's career was defined by twenty-five years at MediaMarktSaturn, Europe's largest consumer electronics retailer. He joined in 1993 and rose to become Chief Operating Officer, responsible for operations across sixteen countries. At MediaMarktSaturn, Kirsch managed the digital transformation of a massive bricks-and-mortar retail operation, connecting online and offline channels, optimizing supply chains, and building operational infrastructure to compete against Amazon.

After leaving MediaMarktSaturn in 2018, Kirsch consulted for corporations and midsize companies on digital transformation, including work with McKinsey and private equity firms. In November 2021, he was appointed CEO of the newly founded Allterco Europe GmbH, based in Munich.

The timing was not coincidental. November 2021 was also the month of the XETRA listing. The dual listing and the Kirsch appointment were two halves of the same strategy: transforming Shelly from a community-driven Bulgarian startup into a pan-European technology company.

Kirsch's impact was immediate and measurable. The professional installer network grew by roughly five hundred percent, from about nine hundred installers to over five thousand three hundred. The mix of professional versus consumer customers shifted from eighty-twenty in favor of consumers to seventy-thirty, a significant rebalancing that carries important implications for average order values, customer lifetime value, and recurring revenue potential.

The distribution strategy under Kirsch also evolved. Shelly products became available through major European electronics retailers and electrical wholesalers, channels that the founders' startup-era direct sales approach had not penetrated. The company's presence at trade shows expanded from hobbyist-oriented events to professional electrician conferences and building technology expos. The brand identity shifted, subtly but deliberately, from "the smart relay that nerds love" to "the professional IoT platform that electricians trust."

Kirsch now serves as co-CEO alongside Dimitrov. Their contracts were extended in February 2025: Dimitrov through end-2030, Kirsch through end-2028. Kirsch has made personal share purchases, buying at twenty euros in August 2023, a signal of confidence when the stock was trading at roughly a third of its current price. His compensation includes share bonuses distributed over multiple years, aligning him with long-term shareholder interests.

The founder transition was managed with an elegance that many growth companies fail to achieve.

Dimitrov remained as co-CEO, focusing on product and technology. Todorov remained on the board, providing strategic oversight. The founders did not leave. They stepped sideways, ceding operational control to a professional manager while retaining the equity stakes and strategic influence that ensure long-term alignment.

A secondary but important minority shareholder is Impetus Capital, a Bulgarian equity investment firm that holds approximately twenty-nine percent. Impetus co-founder Nikolay Martinov took a stake in 2015, providing hardware funding during the critical pivot from VAS to IoT. Martinov now serves as an independent board member, providing corporate governance oversight and capital markets expertise.

The free float remains narrow, which the company has been systematically working to address. The June 2024 share placement of approximately five hundred thousand shares, representing about 2.7 percent of total share capital, was specifically designed to increase the free float toward the threshold required for SDAX index inclusion. BIT Capital, the fund run by Jan Beckers specializing in high-growth internet and technology companies, participated in the placement, providing a notable institutional endorsement. Index inclusion, which arrived in April 2026, triggers automatic buying from passive funds, improving liquidity and broadening the investor base.

The "Retail Meets Visionary" characterization of the co-CEO structure captures something essential about Shelly's current management approach. Dimitrov provides the product intuition and technical credibility that keeps the developer community loyal. Kirsch provides the operational infrastructure, distribution muscle, and institutional investor credibility that a billion-euro company requires. The two skill sets are genuinely complementary rather than overlapping, which is why the dual-CEO model has worked where so many others fail. The cultural challenge is maintaining "startup speed" in a publicly traded company with growing institutional obligations. So far, the pace of product development, multiple new product lines per year, firmware updates measured in weeks rather than months, suggests that the startup DNA has survived the corporate evolution.

V. The Hidden Businesses: Beyond the Relay

Walk into the basement of a modern European apartment building. Open the electrical distribution panel, the gray metal box that houses the circuit breakers.

There is an increasing chance that sitting alongside the traditional breakers, snapped onto the same DIN rails, are Shelly Pro devices: smart relays, energy meters, and increasingly, intelligent circuit breakers that combine protective functions with remote monitoring, control, and energy measurement.

This is the first hidden engine, and it represents the most strategically important shift in the company's history: from consumer gadgets to permanent building infrastructure.

The Shelly Pro line consists of DIN-rail mounted devices designed for professional installation. For non-technical readers, a DIN rail is an industry-standard metal rail used in commercial and industrial electrical panels worldwide. Shelly Pro devices snap onto these rails just like a standard circuit breaker. These are emphatically not consumer products. They are installed by licensed electricians in commercial buildings, hotels, office complexes, and multi-unit residential developments.

Once installed, they become part of the building's permanent electrical infrastructure. They do not get replaced because a homeowner decides to try a different brand. The switching costs are not just financial but regulatory: removing and replacing an electrical panel device requires a qualified electrician and, in many jurisdictions, a compliance inspection. A building with forty Shelly Pro units in its electrical panel is effectively locked into the ecosystem for the life of the building, which could be twenty or thirty years.

The Pro 3EM, a three-phase energy meter for solar systems and commercial power monitoring, has become a best-seller. At IFA 2025, Shelly unveiled what it described as the world's first smart Miniature Circuit Breakers in a compact one-module form factor. These are intelligent circuit breakers combining protection with remote monitoring and energy measurement. The initial range covers six to twenty-five amperes, with a full product range up to sixty-three amperes planned. The smart circuit breaker market is forecast to grow from roughly two and a half billion dollars in 2024 to five point eight billion dollars by 2033.

The second hidden engine is Shelly's move toward silicon independence.

In March 2023, the company announced a partnership with Espressif Systems to develop customized Shelly chips.

This is a co-design arrangement: Espressif designs and manufactures the silicon, but to Shelly's specifications. The customized chip doubles flash memory from four to eight megabytes and includes enhanced security features. Think of it like this: most smart home companies buy generic "off-the-rack" chips and build their products around the chip's limitations. Shelly is having the tailor make a bespoke suit, still using the same fabric supplier but cut to exact specifications.

The strategic significance is twofold.

First, supply chain security. During the global semiconductor shortage of 2021 and 2022, companies dependent on generic commodity chips faced months-long delays. By co-designing with a guaranteed supply commitment, Shelly insulates itself from the worst effects of future disruptions. Second, it positions the company as a platform. The Shelly X module enables third-party manufacturers to embed Shelly's smart functionality into their own products, creating a potential licensing revenue stream.

The product generations tell the evolution story clearly. Gen1 used generic ESP8266 chips, the same commodity microcontrollers used by dozens of competitors. Gen2 moved to the more powerful ESP32, offering more memory and processing headroom. Gen3, launched in 2023, represented the first major leap: a customized Espressif chip with doubled flash memory and Shelly's own real-time operating system, Shelly OS. This was no longer a commodity device running generic firmware. It was a proprietary platform.

Gen4, unveiled at CES 2025, took another step forward. Wi-Fi 6 provides faster, more reliable connectivity in dense wireless environments, the kind of apartment building where dozens of smart devices compete for bandwidth. The flash memory doubled again. And native multi-protocol support, Wi-Fi, Bluetooth, Zigbee, and Matter, all on a single chip, eliminated the need for protocol-specific bridges or hubs that plague competing ecosystems.

Shelly also introduced LoRa add-on capability for Gen3 and Gen4 devices, enabling long-range communication of up to five kilometers. LoRa stands for Long Range, a wireless protocol designed for IoT applications that need to cover large distances with minimal power consumption. Think agricultural sensors monitoring soil conditions across a vineyard, remote building monitoring for vacation properties, or campus-wide automation for university campuses or industrial parks. Standard Wi-Fi works brilliantly inside a house or office, but it struggles to reach a sensor in an outbuilding two hundred meters away. LoRa solves that problem with a fundamentally different radio approach that trades speed for range. By offering LoRa as an add-on rather than built-in, Shelly keeps the base product affordable while giving professional users the option to extend range far beyond what Wi-Fi can achieve.

Matter also deserves explanation in this context. For years, the smart home industry suffered from a compatibility nightmare. Devices built for one ecosystem often did not work with another. A Philips Hue bulb worked with Apple HomeKit but not natively with Google Home. A Ring doorbell worked with Alexa but not with HomeKit. Matter, developed jointly by Apple, Google, Amazon, Samsung, and others through the Connectivity Standards Alliance, is an open protocol designed to ensure interoperability across all major platforms.

Shelly's early embrace of Matter is strategically important because it turns what could have been a threat into a tailwind. If all smart home devices must speak the same language, the differentiator becomes hardware quality, price, local control capability, and developer ecosystem, precisely the areas where Shelly excels. Matter levels the playing field on basic interoperability but does nothing to diminish Shelly's advantages in openness, pricing, and community support.

The third hidden engine is the nascent cloud and software business.

While Shelly's competitive identity is built on local control and data privacy, the company also offers an optional cloud service. The Shelly Cloud app had 2.7 million users at end-2025, growing forty-six percent year-on-year. Premium app subscribers reached approximately thirty-eight thousand, growing sixty-one percent. SaaS revenue in the first nine months of 2025 was just over half a million euros, a negligible revenue contribution but a proof of concept for recurring revenue.

The real potential is in energy management as a service.

As European electricity prices remain elevated and solar adoption accelerates, households and businesses need tools to monitor consumption, optimize self-consumption of solar energy, and manage time-of-use tariffs. Shelly has launched a Solar Platform in beta for PV installations with Modbus inverter integration, and announced strategic partnerships with Zendure for balcony power plants and energy storage, and with EcoFlow for portable power solutions. The vision is not just "smart home" but "smart grid": using distributed Shelly devices to balance solar generation, EV charging, and heat pump operation across thousands of homes simultaneously.

The installed base of nearly thirty million devices, many with energy metering capabilities, creates a distribution channel for software-based energy management services. Consider the math: if Shelly converts even five percent of its 2.7 million cloud users into premium subscribers at ten euros per month, that would represent roughly sixteen million euros in annualized recurring software revenue at margins well above the hardware business. This is speculative, but the distribution, the installed base, and the data infrastructure are already in place.

The regional revenue breakdown illustrates the geographic expansion. In fiscal 2025, the DACH region generated sixty-two million euros, growing twenty-seven percent. The rest of Europe contributed seventy-four million euros, growing fifty-one percent. The rest of the world added thirteen million euros, growing fifty-four percent. Faster growth outside the German-speaking core suggests that newer markets are entering the steep part of the adoption curve.

The daily device activation rate, which grew forty-five percent year-on-year in fiscal 2025, is perhaps the most telling metric. It measures not just sales but actual deployment: someone unpacking a device, connecting it to Wi-Fi, and integrating it into their home or building. This is the heartbeat of the Shelly ecosystem.

VI. The Playbook: 7 Powers and Porter's 5 Forces

The most interesting strategic question about Shelly is not whether it can grow. It clearly can.

The question is whether it can defend that growth. Amazon could build an open, local-first smart home relay tomorrow. Google has the engineering talent to do it in a weekend hackathon. Apple has the brand trust to sell it at twice the price. Why have none of them done it?

The answer lies in Hamilton Helmer's concept of counter-positioning, perhaps the most elegant of his seven strategic powers. Counter-positioning exists when a challenger adopts a business model that an incumbent cannot replicate without damaging its existing business. It is not that the incumbent lacks the capability. It is that the incumbent lacks the motivation, because the new approach would cannibalize the very business model that generates its current profits.

Amazon's smart home strategy is built around Alexa, which feeds voice data collection, which feeds advertising and product recommendations. Offering a device that operates entirely locally, with no data flowing to Amazon's servers, would undermine the economic rationale for the entire Alexa ecosystem. Why would Amazon give away the one thing that justifies selling Echo devices at a loss?

Google faces the same structural constraint: its business model depends on data. Every Google Nest device is a node in a data collection network that feeds Google's advertising revenue engine. An open, local-first device that sends nothing to Google's servers would be an engineering curiosity with no business model attached.

Apple comes closest to Shelly's positioning, having made privacy a marketing pillar. But Apple's premium pricing strategy prevents it from competing in the ten-to-twenty-euro relay market where Shelly dominates. Apple's HomeKit ecosystem is designed to sell more iPhones and iPads, not to provide affordable building automation for European electricians.

This is Shelly's primary strategic power: it occupies a position that the dominant incumbents cannot attack without cannibalizing their own business models. As long as big-tech smart home strategy is built on data harvesting and ecosystem lock-in, Shelly's open, local-first approach remains structurally advantaged among the growing segment of consumers and professionals who value privacy and interoperability.

The second power is what Helmer calls a cornered resource. In Shelly's case, the resource is not a patent or a mine. It is a community. The Home Assistant developer community, the professional electrician network, and the YouTube ecosystem surrounding Shelly represent an asset that cannot be purchased or replicated. Once a professional installer has built their business around Shelly products, learned the APIs, configured dozens of customer installations, and developed a reputation as a Shelly specialist, the switching cost is not the price of hardware. It is the cost of retraining, recertifying, and rebuilding an entire professional practice.

The third power is switching costs, which compound at the professional level. A building with forty Shelly Pro units installed in its electrical panel is locked into the ecosystem for the life of the building. These are not consumer gadgets that get swapped out with the next trend. They are permanently wired into infrastructure that operates for twenty or thirty years.

The fourth power is process power: the operational discipline that comes from building a hardware company in a market, Bulgaria, that forces profitability from day one. The fifty-eight percent gross margin that Shelly achieves on physical hardware is remarkable. For comparison, Tuya, the Chinese IoT platform company, reports gross margins in the forty to forty-five percent range. Sonoff devices operate on thinner margins with higher volumes. Shelly's margin advantage reflects a combination of efficient manufacturing, premium pricing justified by quality and openness, and a direct-to-consumer distribution model that avoids the margin erosion of traditional retail channels.

The fifth power, less developed but emerging, is scale economies. As Shelly grows, it can spread R&D costs, particularly the investment in custom silicon and Shelly OS, across a larger device base. R&D investment exceeded four million euros in fiscal 2025, modest by technology industry standards but meaningful for a company of Shelly's size. The customized Espressif partnership gives Shelly supply chain advantages that smaller competitors cannot access.

Now apply Porter's Five Forces to test whether these strategic powers hold up under competitive pressure.

The threat of new entrants is moderate in the consumer segment but low in the professional segment. This asymmetry is crucial. Building a consumer Wi-Fi relay is not technically difficult, and Chinese manufacturers could flood the market. But building professional-grade DIN-rail devices that meet European electrical safety standards, integrate with KNX building automation protocols, and carry the certifications required for commercial installations is a substantially higher barrier.

The threat of substitutes centers on the Matter protocol. Matter, developed jointly by Apple, Google, Amazon, Samsung, and others, is an open protocol designed to ensure interoperability among smart home devices. If Matter achieves universal interoperability, does it commoditize the device layer? So far, the answer is no. Matter defines a communication protocol, not a product experience. Two Matter-compatible devices can interoperate but still differ enormously in build quality, local control capability, API depth, and community support. Shelly's bet is that Matter raises the floor for interoperability while leaving ample room for differentiation above the protocol layer. Matter is actually a tailwind: it validates Shelly's open approach and removes the "ecosystem lock-in" advantage that big-tech competitors previously enjoyed.

The supplier power dynamic deserves attention as a potential vulnerability. Shelly's co-development partnership with Espressif reduces dependency on spot-market chip procurement, but Espressif itself is a single point of failure. If Espressif were acquired, sanctioned, or disrupted, Shelly's chip supply would be at risk.

The bargaining power of buyers varies sharply by segment.

In the DIY consumer market, buyer power is high because switching costs are low and alternatives are plentiful. A consumer can easily swap a twelve-euro Shelly relay for a fifteen-euro Sonoff alternative. But in the professional installer market, buyer power diminishes significantly. An electrician who has standardized on Shelly Pro devices, who has configured their installation templates around Shelly's APIs, and whose customers expect Shelly's app experience, has limited incentive to switch to an unproven alternative, even if it is cheaper.

Competitive rivalry is intense but fragmented, and the dynamics differ sharply between Shelly's consumer and professional segments.

In the consumer space, Shelly competes with Sonoff, Tuya-based white-label products, TP-Link's Tapo line, Xiaomi's Aqara devices, and IKEA's DIRIGERA ecosystem. Sonoff is the closest direct competitor: similar product categories, similar price points, similar DIY following. But Sonoff's devices have historically been more cloud-dependent and less polished in their local API implementation. Tuya represents a different kind of threat: it is a platform enabling hundreds of white-label brands to produce smart home devices, creating a flood of cheap, interchangeable products that commoditize the low end. Shelly's response has been to compete on quality, documentation, and community trust rather than on price alone.

TP-Link entered the smart relay market in 2025 with Matter-enabled modules. While initial products are more consumer-focused and less feature-rich than Shelly's offering, a company with TP-Link's manufacturing scale and distribution reach could potentially compress Shelly's margins in the consumer segment.

In the professional space, the competition shifts dramatically. Established building automation systems like KNX, a wired protocol that has been the European standard for decades, Loxone, a premium Austrian system, and Control4, the American dealer-installed platform, all cost orders of magnitude more. A KNX installation requires dedicated bus wiring, specialized programming tools, and certified integrators, resulting in system costs that start at ten thousand euros for a basic home. Shelly Pro offers comparable DIN-rail functionality at a fraction of the cost using standard Wi-Fi instead of proprietary wiring.

Shelly sits in what might be called the "Golden Middle": professional-grade capability at consumer-grade pricing. It is small enough to care about the twelve-euro DIY sale but increasingly capable enough to win the twelve-thousand-euro commercial building project. That dual positioning is a strategic advantage that none of its direct competitors can match.

Shelly claims more than six percent market share in the European smart home IoT market and aims to grow at roughly three times the overall market growth rate, targeting forty-plus percent revenue growth against an industry expanding at ten to fifteen percent annually. If European or US tariff policies create headwinds for Chinese-manufactured competitors like Tuya and Sonoff, Shelly's European-branded positioning could become an additional advantage.

VII. Bear vs. Bull

The bear case begins with a simple, brutal word: commoditization.

It is the word that keeps every hardware CEO awake at night, and it describes a simple, brutal dynamic. The components inside a Shelly relay, a Wi-Fi microcontroller, a relay switch, a power supply, a PCB, are all commodity parts available from dozens of suppliers. The firmware, while well-designed, is not protected by patents that would prevent replication. If TP-Link, with its massive global distribution, decides to launch a full line of open-API, locally controlled relays at prices that undercut Shelly by thirty percent, the margin story changes.

Commoditization is not hypothetical. It is the default trajectory for consumer electronics. The history of the industry is littered with companies that enjoyed a temporary technological or brand advantage, only to see it eroded by cheaper, "good enough" alternatives manufactured at scale in China. The question for Shelly is whether its advantages, the community, the brand trust, the professional installer network, the custom silicon, constitute durable differentiation or merely a temporary head start.

The second bear concern is geographic concentration.

The DACH region generated roughly forty-one percent of fiscal 2025 revenue. While "Rest of Europe" and "Rest of World" are growing faster, a recession in Germany or a regulatory change affecting smart home device installations could materially impact the company's largest market.

The third concern is the thin free float.

With founders holding two-thirds of shares and Impetus Capital holding roughly twenty-nine percent, freely traded shares remain constrained. The June 2024 placement improved this modestly, and SDAX inclusion should attract passive fund buying, but liquidity risk persists. The share price nearly tripled from mid-2023 to April 2026, but this appreciation occurred with very limited trading activity, meaning sharp swings on relatively small volumes are possible.

There is also a bear risk around the US market. Shelly has established a presence in Boca Raton, Florida, and has been selling in the US for several years. But the American smart home market is structurally different from the European market. American homes use different electrical standards (120V versus 230V), different wiring conventions, and different switch form factors. The competitive landscape is dominated by Lutron, Leviton, and GE in the professional switch market, and by Amazon-ecosystem products in the consumer market. Building a credible US sales organization with distribution, customer support, and regulatory compliance for a market that operates under UL standards rather than CE marking requires significant investment and local expertise. Whether a Bulgarian-born company with a German co-CEO can scale effectively in the American market remains an open question.

A further concern worth noting is the Espressif dependency. The co-design partnership provides advantages but also creates a single point of failure. Espressif is a Shanghai-based company, and the geopolitical dynamics affecting Chinese semiconductor firms could potentially impact Shelly's chip supply. The customized nature of the co-developed silicon makes switching to an alternative chipmaker more difficult than it would be with generic components.

The bull case starts with what might be called the "KNX replacement" thesis. This is the argument that transforms Shelly from a "consumer gadget story" into a "European infrastructure play."

This is the argument that gets professional building automation investors excited, and it deserves careful unpacking. Professional home and building automation using the KNX wired protocol is an established market in Europe. A professional KNX installation for a typical home costs between ten and twenty thousand euros, requiring dedicated bus wiring, specialized programming tools, and certified system integrators. Shelly Pro offers comparable functionality, DIN-rail mounting, energy monitoring, scene control, scheduling, and increasingly KNX protocol support, at a fraction of the cost. A full Shelly Pro installation for a similar home might cost one to two thousand euros in hardware, with significantly lower installation labor because the devices use standard Wi-Fi rather than dedicated wiring.

This is a classic disruptive innovation pattern. The incumbent technology is excellent but expensive and complex. The disruptive technology is simpler and cheaper, initially targeting the low end where KNX is overkill, but steadily improving in capability until it becomes "good enough" for the mainstream professional market.

The KNX industry knows this. The nervous conversations at industry conferences, where established integrators wonder aloud whether Wi-Fi-based systems will erode their market, have been growing louder each year. Some KNX integrators have quietly begun adding Shelly Pro products to their offerings as a lower-cost option for clients who cannot justify the full KNX investment. The five thousand three hundred installers in Shelly's network are the leading edge of this disruption.

The second bull pillar is the electrification tailwind. This is perhaps the most powerful secular force working in Shelly's favor, and it deserves careful examination because it reframes Shelly from a "smart home gadget company" into a "European energy infrastructure play."

European regulations mandating energy efficiency monitoring, solar panel optimization, heat pump integration, and EV charging management are creating demand for exactly the kind of connected electrical infrastructure that Shelly provides. The European Union's Energy Performance of Buildings Directive is pushing member states to require energy monitoring and smart building capabilities in new construction and major renovations. The proliferation of rooftop solar installations across Germany, the Netherlands, and Southern Europe creates millions of households that need tools to optimize self-consumption.

As time-of-use electricity tariffs become more common across Europe, the ability to automatically shift energy consumption becomes not just a convenience but a meaningful financial optimization. Running the dishwasher when solar panels are generating, charging the EV battery when electricity is cheapest at night, pre-heating the home before peak rates kick in: these are optimizations that require exactly the kind of circuit-level monitoring and control that Shelly's Pro 3EM energy meter and smart circuit breakers provide.

If Shelly can position itself as the "Intel Inside" of the smart electrical panel, the device that sits behind every solar inverter, EV charger, and heat pump in Europe, the addressable market expands by an order of magnitude beyond consumer home automation. The smart circuit breakers unveiled at IFA 2025 are positioned squarely at this opportunity. The global smart circuit breaker market is forecast to grow from two and a half billion dollars in 2024 to five point eight billion by 2033, and Shelly is among the first to offer consumer-grade pricing for devices in this category.

The smart circuit breakers unveiled at IFA 2025 are positioned squarely at this opportunity: devices that sit in every electrical panel, monitoring and controlling energy flows at the circuit level. If Shelly can capture even a modest share of the multi-billion-dollar smart circuit breaker market, the addressable opportunity expands by an order of magnitude compared to the consumer relay business.

The financial trajectory supports the bull narrative. Revenue grew from 74.9 million euros in fiscal 2023 to 106.7 million in fiscal 2024 to 149.7 million in fiscal 2025. Adjusted EBIT reached 37.7 million euros in fiscal 2025, a twenty-five percent margin. The company guides for fiscal 2026 revenue between one hundred ninety-five and two hundred five million euros, with EBIT between forty-seven and fifty-two million. If achieved, that represents a near-tripling of revenue in three years while maintaining or expanding margins.

The balance sheet reflects the founders' conservative instincts. The equity ratio stands at seventy-eight percent. The company carries no meaningful debt. This is a company that grew up without venture capital, and that origin story is embedded in its financial DNA.

The valuation narrative deserves consideration. Shelly trades at roughly forty times trailing earnings. For a mature hardware company, this would be expensive. But the comparison to pure hardware companies is misleading. Shelly's fifty-eight percent gross margin profile is closer to software than traditional electronics. Tuya, the closest public comparable, trades at lower gross margins despite being a larger business. If investors begin to view Shelly less as a hardware vendor and more as a hardware-enabled software platform, a reframing that the SaaS revenue growth and energy management roadmap support, the valuation framework shifts.

The financial trajectory under the dual-CEO leadership supports the bull narrative. Revenue grew from 74.9 million euros in fiscal 2023 to 106.7 million in fiscal 2024 to 149.7 million in fiscal 2025. To put that growth rate in perspective: doubling revenue every two years, while maintaining twenty-five percent operating margins, is a combination that very few hardware companies in the world achieve at any scale. Adjusted EBIT reached 37.7 million euros in fiscal 2025, a twenty-five percent margin. The company guides for fiscal 2026 revenue between one hundred ninety-five and two hundred five million euros, with EBIT between forty-seven and fifty-two million. If achieved, this would represent a near-tripling of revenue in three years.

The balance sheet reflects the founders' conservative instincts. The equity ratio stands at seventy-eight percent. The company carries no meaningful debt. Free cash flow was 1.5 million euros in fiscal 2025, modest relative to profitability but reflecting the working capital requirements of a high-growth hardware business that must pre-fund inventory and component purchases. As growth moderates, free cash flow conversion should improve.

For investors tracking Shelly's ongoing performance, two KPIs matter above all. The first is the professional customer mix: the percentage of revenue from professional installers and commercial accounts versus DIY consumers. This ratio, which shifted from eighty-twenty to seventy-thirty under Kirsch's leadership, is the single best indicator of whether the company is successfully moving up the value chain from hobbyist hardware to building infrastructure.

The second KPI is the Shelly Cloud and premium app subscriber count, currently 2.7 million and approximately thirty-eight thousand respectively. These numbers are the leading indicators of whether the recurring software revenue model, still embryonic at roughly half a million euros, has a realistic path to becoming a meaningful revenue stream.

VIII. Epilogue: The Acquired Take

In December 2024, Shelly Group completed its transformation into a Societas Europaea.

The rebranding, from a Bulgarian joint-stock company called Allterco to a European Company called Shelly Group SE, was the final step in a corporate evolution that mirrors the product evolution: from local and specific to global and standardized, while retaining the core identity that made it special in the first place.

The 2026 product roadmap is the most ambitious in the company's history. It includes categories Shelly has not previously entered: smart locks in multiple configurations from premium to budget, leveraging the LOQED acquisition; a camera product line that extends the brand from electrical infrastructure into security; and the commercial launch of the smart circuit breakers that represent Shelly's most ambitious move into professional electrical infrastructure.

R&D investment exceeded four million euros in 2025 and is expected to increase as the company develops its customized silicon roadmap, expands firmware capabilities across the growing product line, and builds out the energy management software platform that could transform the business model from hardware-centric to a hybrid hardware-plus-recurring-software model.

The company operates from a footprint that spans the entire value chain: product development in Sofia and Solkan, Slovenia; manufacturing oversight in Shenzhen; European distribution from Munich and Poland; US operations from Boca Raton, Florida.

The installer network of five thousand three hundred professionals provides a capillary distribution system reaching commercial projects and residential renovations across Europe. It is this network, more than any single product, that gives Shelly a distribution advantage that new entrants cannot easily replicate.

The company's geographic footprint provides operational resilience that a single-headquarters company would lack. If tariffs or regulatory changes disrupt one corridor, the team has the relationships and expertise to adjust.

Shelly is proof of a thesis that the European technology ecosystem has long struggled to validate: that it is possible to build a world-class, high-growth, profitable hardware-enabled technology company outside of Silicon Valley and Shenzhen. The ingredients were specific to the company's origins: founders who understood telecommunications infrastructure, a home market that demanded profitability from day one, a product philosophy that prioritized openness over lock-in, and a community of users who became evangelists precisely because the company respected their intelligence and their data.

The lesson of the Shelly story is deceptively simple: in a world of proprietary software, openness is a feature. In an industry built on lock-in, the company that lets users leave is the one they choose to stay with. In a market dominated by trillion-dollar incumbents, the twelve-euro relay that works without the cloud turned out to be the most subversive product in consumer technology.

The smart home market is littered with companies that started with idealistic visions and ended up building walled gardens. Wink imposed a mandatory monthly subscription, alienating its entire user base. Insteon shut down its cloud servers without warning in 2022, bricking millions of devices. Revolv, acquired by Google, had its servers terminated in 2016, rendering every device useless.

Shelly's local-first architecture is, at its core, a bet that these kinds of betrayals destroy more value than they create.

It is a bet that a company respecting users' autonomy can build a more durable competitive position than one exploiting their dependency.

Twenty-nine million devices in one hundred and thirty countries suggest the bet is working. The daily device activation rate continues to accelerate. The professional installer network is expanding. The product line is broadening from consumer relays into professional circuit breakers, smart locks, cameras, and energy management systems. Each new product category extends the addressable market while leveraging the brand trust, distribution network, and community ecosystem that took a decade to build.

The SDAX inclusion, effective April 2026, is a milestone that symbolizes the extraordinary distance traveled. A Bulgarian company founded to sell SMS ringtones, listed on one of the world's least liquid stock exchanges, now sits alongside German industrial mid-caps in a benchmark index. The journey from the Bulgarian Stock Exchange to the Deutsche Börse's SDAX took less than five years. The journey from ringtones to smart circuit breakers took twenty.

The founders, now in their forties, still own two-thirds of the company. The professional management team, led by Kirsch, brings the operational discipline needed to scale. The product roadmap provides multiple vectors for growth. And the structural advantages, counter-positioning against big tech, community-driven adoption, and an expanding regulatory tailwind from energy efficiency mandates, remain firmly in place.

Whether Shelly becomes a multi-billion-euro acquisition target for a Schneider Electric or Siemens, or whether it builds an independent path as the de facto standard for European energy management, depends on what happens next. The argument for acquisition is compelling.

Schneider Electric, ABB, or Siemens could integrate Shelly's consumer and professional IoT platform into their existing building management portfolios, gaining instant access to twenty-nine million installed devices and a thriving developer community. The argument for independence is equally compelling.

Shelly's founders have shown no inclination to sell, and their two-thirds ownership stake gives them the voting power to block any unwanted approach.

The founders built a company that respects its users. The question is whether the market will reward that respect at scale.

IX. Key Resources

- Shelly Group Investor Relations: corporate.shelly.com

- Shelly Developer Wiki and API Documentation

- Home Assistant Community Forums: ground zero for Shelly's grassroots adoption

- Interviews with Wolfgang Kirsch on the MediaMarkt-to-IoT transition

- Shelly-Espressif chip partnership technical specifications

- IFA 2025 Smart MCB announcement and professional building automation roadmap

- The Matter Protocol Specification: Connectivity Standards Alliance

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube