Shell plc: The Arbitrage Sovereign & The Capital Discipline Pivot

I. Introduction & The Valuation Arbitrage

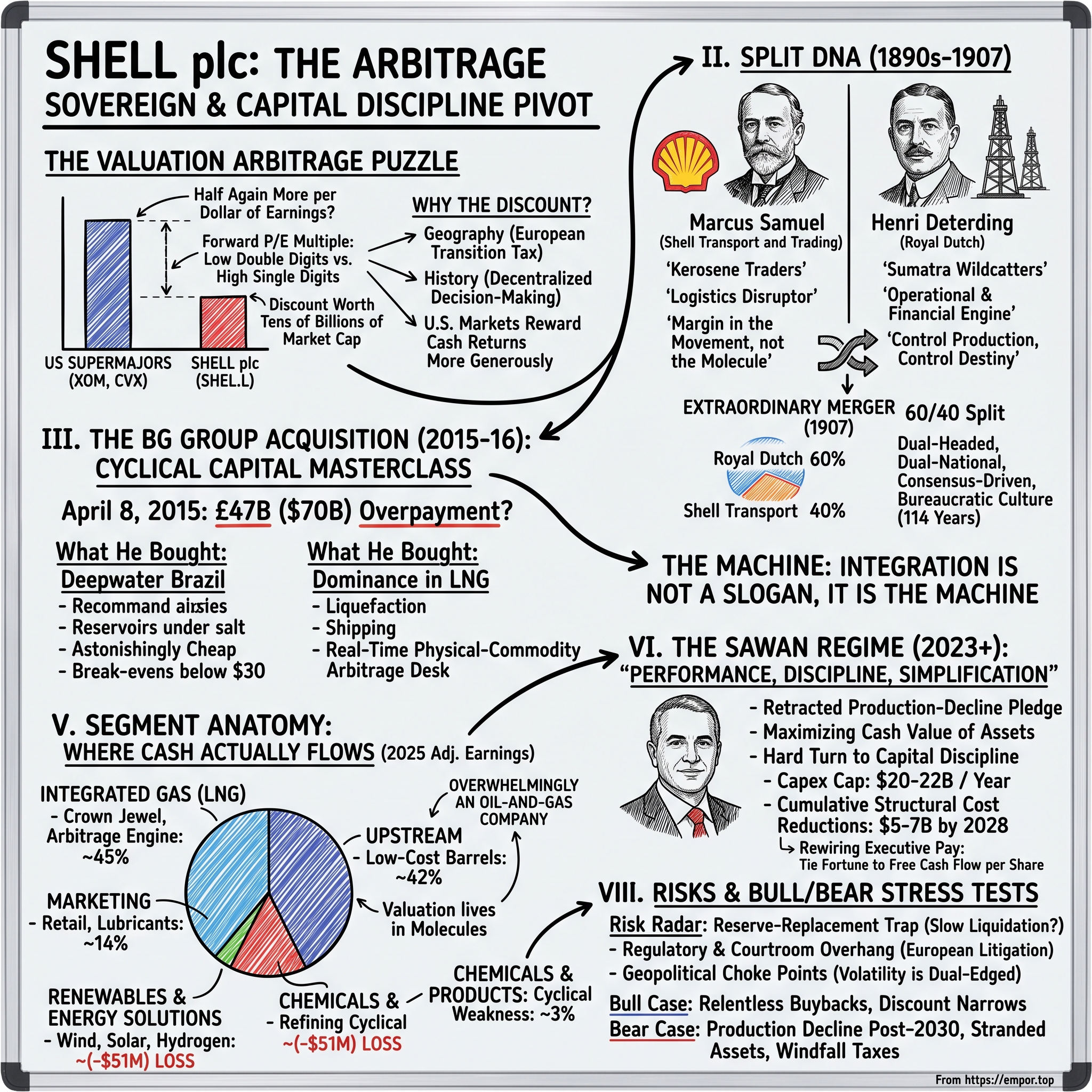

Picture two oil companies sitting side by side on a trading screen in the summer of 2026. Both pump crude from the deepest oceans on Earth. Both sell fuel at forecourts on five continents. Both throw off tens of billions of dollars in cash every year and hand most of it back to shareholders. One of them, though, is worth roughly half again as much per dollar of earnings as the other. The expensive one is headquartered in Texas. The cheaper one is headquartered a mile from the Thames, and its ticker — SHEL.L — is the tell.1

This is the puzzle that animates everything Shell's management does today. The world's largest and most sophisticated liquefied natural gas trading machine trades at a persistent discount to its American supermajor rivals. Where ExxonMobil and Chevron command forward price-to-earnings multiples in the low double digits, Shell has spent years stuck in the high single digits, its enterprise value a low multiple of the cash flow it generates. On a like-for-like basis, the gap has at times been worth tens of billions of dollars of market capitalization — a discount not because Shell produces less cash, but because of where it is listed, how it is regulated, and what investors fear its future holds.

Why does a barrel of Shell's earnings cost less than a barrel of Exxon's earnings? Part of the answer is geography. European supermajors carry a "transition tax" in their multiples: investors worry that European boards, European courts, and European politics will force them to spend shareholder cash chasing low-return green projects while their American peers drill unapologetically. Part of it is history — a century of consensus-driven, decentralized decision-making that made Shell brilliant at engineering and sluggish at capital allocation. And part of it is that the U.S. capital markets simply reward oil-and-gas cash returns more generously than London's do.

The company spent the first half of the 2020s trying to demolish every structural reason for that discount. It dropped the "Royal Dutch" from its name. It fled the Netherlands for the United Kingdom. It collapsed a baroque dual-class share structure — the A shares and B shares that had divided its equity since 1907 — into a single clean line of stock on the London Stock Exchange. It walked away from a Dutch climate ruling that had threatened to put a court in charge of its emissions strategy. And under a new chief executive, it staked its credibility on a single, unglamorous promise: to stop trying to please everyone and instead behave like the disciplined cash machine its low multiple implied it should be.

This is a story about that pivot — but also about whether it is real. Over the next sections we will trace Shell's split DNA back to a London seashell merchant and a Dutch jungle wildcatter; dissect the $70 billion BG Group acquisition that was ridiculed as an overpayment and turned out to be the most important capital-deployment decision of the modern supermajor era; walk through the climate-litigation shockwave and the corporate escape from The Hague; open the hood on the segments where the cash actually flows; and stress-test the "Performance, Discipline, and Simplification" strategy against the moats it claims and the risks that could break it. Throughout, the posture is neutral. Management says it can close the valuation gap. Our job is to ask what evidence supports that, and what would prove it wrong. It begins, as these things so often do, with two ambitious men who could not stand each other.

II. Split DNA: Kerosene Traders & Dutch Explorers (1890s–1907)

In the 1880s, a young Londoner named Marcus Samuel took over a curio business his father had built importing decorative seashells and lacquered boxes from the Far East to feed the Victorian mania for exotic knick-knacks. The shells gave the future company its name and, eventually, its scallop logo. But Samuel was not destined to sell trinkets. He was destined to move kerosene — and to do it in a way nobody had dared.[^2]

At the time, the global oil trade was effectively owned by John D. Rockefeller's Standard Oil, which shipped kerosene in tin cans packed into wooden crates, a system as expensive as it was clumsy. Samuel's insight was almost embarrassingly simple: what if you moved oil the way you moved water — in bulk, in the hull of a purpose-built ship? In 1892 his tanker the Murex became the first bulk oil tanker to pass through the Suez Canal, a feat that required convincing the canal's cautious authorities that a hold full of flammable liquid would not incinerate the most important waterway on Earth. It did not. The Suez route slashed the cost and time of shipping oil from the Caspian to Asian markets, and Samuel's Shell Transport and Trading Company was born as a logistics disruptor — a trader that won not by finding oil but by moving it more cleverly than anyone else. That instinct, that the margin lives in the movement and not just the molecule, is the oldest gene in Shell's body.

Six hundred miles away in The Hague, a very different company was forming around a very different man. Royal Dutch was in the messy, capital-devouring business of actually pulling oil out of the ground — in this case the malarial jungles of Sumatra in the Dutch East Indies. Its defining figure was Henri Deterding, a former bank clerk with a photographic memory for numbers and an almost frightening will to win. Deterding built Royal Dutch into a formidable operational and financial engine, and he understood something Samuel's traders did not fully grasp: in a fight against Standard Oil, whoever controlled production controlled destiny. Deterding and Rockefeller circled each other for years, the Dutchman determined never to be swallowed.

By the early 1900s both companies had reached the same uncomfortable conclusion. Alone, each was vulnerable — Shell had ships and markets but thin production; Royal Dutch had oil and discipline but less commercial reach. Together they might survive the Standard Oil juggernaut. So in 1907 they did something extraordinary: they merged their operations while keeping two separate parent companies alive, in a 60/40 split favoring the larger, cash-richer Dutch side. Royal Dutch of The Hague took 60 percent; Shell Transport of London took 40 percent. It was a merger of equals that was not quite equal, and it hard-wired two things into the company for the next 114 years. First, a dual-headed, dual-national, consensus-driven culture that made Shell deliberative, decentralized, and famously bureaucratic — a company where big decisions required Anglo-Dutch agreement and endless committee. Second, a permanent split-brain identity, half trader and half producer, that would eventually become the source of both its greatest competitive weapon and its deepest valuation curse. The 60/40 structure would not be fully unwound until 2022 — and when it finally was, it would be under duress. To understand why the unwinding felt so radical, though, you first have to understand the single deal that made Shell the company worth fighting over.

III. The BG Group Acquisition: A Masterclass in Cyclical Capital Deployment

By early 2015, the oil industry was staring into an abyss. Crude prices, which had sat comfortably above $100 a barrel for years, had collapsed by more than half in a matter of months as U.S. shale flooded the market and OPEC refused to blink. Across the sector the reflex was identical and universal: slash capital spending, cancel projects, hoard cash, and pray for the price to recover. It was a moment for defense. Everyone knew that.

Everyone except Ben van Beurden. On April 8, 2015, the Shell chief executive — a soft-spoken Dutch chemical engineer who had spent his career inside the company — announced that Shell would acquire BG Group, the exploration-and-production spinoff of the old British Gas, for roughly £47 billion, or about $70 billion, in cash and stock.[^3] The offer valued BG at a premium of roughly 50 percent over its undisturbed share price — a staggering markup to pay at the very bottom of a brutal cycle, when the accepted wisdom was that asset prices had further to fall.2

The market's verdict was swift and unkind. Shell's shares dropped sharply on the announcement as investors did the arithmetic and recoiled: Shell was taking on a mountain of debt and paying a fat premium to buy an oil company just as oil looked structurally broken. Analysts warned that the deal put Shell's dividend — the single most sacred number in the portfolios of a generation of British and Dutch pension funds — at risk. For a company whose entire investor base was built on the promise of an uninterrupted payout stretching back to the Second World War, that was close to heresy. Van Beurden spent the following year defending the logic to skeptical shareholders, and the transaction did not formally close until February 15, 2016, by which point oil had fallen even further and the criticism had grown louder.3

And then, slowly, the ridicule curdled into envy. Because van Beurden had not bought oil — he had bought two things the market did not know how to price at the bottom of a cycle.

The first was deepwater Brazil. BG owned some of the best acreage on the planet: stakes in the pre-salt fields off the Brazilian coast, including Lula and Libra, developed alongside the state-controlled producer Petrobras. These were geological freaks — vast reservoirs trapped beneath a thick layer of salt two kilometers under the seabed, expensive to reach but astonishingly cheap to produce once flowing, with break-evens that would eventually sit below $30 a barrel. In an industry where the scarcest asset is a barrel that makes money at low prices, Shell had just cornered a supply of them, and it had done so when nobody else had the nerve to bid.

The second thing van Beurden bought was dominance in liquefied natural gas. BG was a major LNG player, and folding it into Shell made the combined company the undisputed heavyweight of the global LNG trade — the business of super-cooling natural gas to minus 162 degrees Celsius until it shrinks to one six-hundredth of its volume and becomes a liquid you can load onto a ship and sail anywhere on Earth. Overnight, Shell controlled an unmatched portfolio of liquefaction plants, long-term supply contracts, a fleet of specialized carriers, and regasification terminals on the receiving end.

Here is the part that most observers missed in 2015, and it is the crux of the entire Shell investment case. Owning all the physical links in the LNG chain does not just let Shell sell gas — it lets Shell trade gas. When you control liquefaction on one side of the world, ships in the middle, and regasification terminals on the other, you can watch the price of gas in Asia and the price of gas in Europe drift apart, and then physically redirect a cargo already at sea toward whichever market is paying more that week. You are not merely a seller of molecules; you are running a real-time physical-commodity arbitrage desk on a planetary scale, capturing the spread between markets that a company with only a plant, or only a ship, or only a contract could never touch. Integration is not a slogan here. It is the machine. BG was the acquisition that fed the machine — and the integration was completed faster and delivered more synergies than management had promised, an early data point suggesting the "overpayment" was nothing of the sort. It also, unwittingly, loaded the company with the emissions and the exposure that would soon put it in front of a judge.

IV. The Dual Crisis: Climate Court & The Dual-Class Collapse (2021–2022)

On May 26, 2021, in a courtroom in The Hague, a Dutch district court did something no court had ever done to an oil company. Ruling in a case brought by the environmental group Milieudefensie — the Dutch arm of Friends of the Earth — the court ordered Royal Dutch Shell to cut its global, absolute carbon emissions by 45 percent by 2030 compared with 2019 levels. Crucially, the order covered not just Shell's own operations but its Scope 3 emissions — the carbon released when customers burn the fuel Shell sells them, which is the overwhelming majority of any oil company's footprint. A single national court had, in effect, appointed itself the arbiter of a multinational's global strategy.4

The ruling landed like a thunderclap, and it did not arrive alone. Later in 2021, the American activist investor Dan Loeb and his hedge fund Third Point disclosed a multibillion-dollar stake in Shell and began agitating publicly for something radical: break the company up. Loeb's argument was that Shell was trying to be two incompatible things at once — a cash-gushing legacy fossil-fuel producer beloved by yield investors, and an aspiring clean-energy champion beloved by nobody in particular — and that this strategic straddle was precisely why the stock traded at a discount. Split it, Loeb argued, and each piece would be worth more than the muddled whole.

Shell's board rejected the breakup. But it clearly agreed with the diagnosis underneath it: that the company's structure, its domicile, and its legal exposure had become an active drag on its value. And so, in the space of a few months, the board took the most consequential set of corporate-structure decisions in the company's history.

In November 2021 Shell announced it would move its tax residence and headquarters from The Hague to London, drop "Royal Dutch" from its name to become simply Shell plc, and — most importantly for investors — collapse its century-old dual-class structure into a single line of ordinary shares.5 The old A and B shares were relics of the 1907 merger: A shares carried Dutch tax heritage and were subject to a 15 percent Dutch dividend withholding tax that made buybacks clumsy and cross-border ownership a headache, while B shares routed dividends through a UK mechanism to avoid it. Unifying them into one share, domiciled in London, did something mundane-sounding but strategically enormous: it made large-scale share buybacks vastly simpler and more tax-efficient. A company that wants to shrink its share count aggressively needs a clean, single, buyback-friendly equity structure — and Shell had just built one. The Dutch government reacted with fury at losing one of its corporate crown jewels; Shell reacted by pointing at the withholding tax and the courtroom and heading for the exit.[^8]

Then the legal story turned. On November 12, 2024, the Hague Court of Appeal overturned the 2021 ruling. The appeals court did not exonerate Shell entirely — it affirmed that the company carries an "unwritten" duty of care to help mitigate dangerous climate change — but it held that a court cannot impose a specific numerical reduction target, such as 45 percent, on an individual company, because no such universal figure applies to every country and sector. Shell welcomed the decision publicly; Milieudefensie called it a setback but not a defeat.[^9]6

The fight, predictably, did not end there. Milieudefensie filed a cassation appeal to the Dutch Supreme Court in early 2025, and in April 2026 it launched an entirely new lawsuit against Shell — this time demanding not a percentage cut but an outright halt: no new oil and gas fields brought into production, and a mandated glide-path of emissions reductions between 2030 and 2050. Milieudefensie pointed to Shell's interest in some 700 undeveloped oil and gas fields as the target of its new claim.78 For investors, the lesson of the entire saga is not who won any single round. It is that European courts have become a permanent, unpredictable arena for fossil-fuel producers — an overhang that no appeals-court victory fully removes, and one more reason a Texas listing trades richer than a London one. Which raises the practical question the litigation always dances around: where does Shell's money actually come from?

V. Segment Anatomy: Where the Cash Actually Flows

Strip away the transition rhetoric, the courtroom drama, and the branding, and a company is just a machine for converting capital into cash across a handful of business lines. For Shell, the machine reported adjusted earnings of $18.5 billion for the full year 2025, on adjusted EBITDA of roughly $56 billion and cash flow from operations of about $43 billion.910 The interesting question is not the total. It is the mix — because the mix reveals what Shell truly is, as opposed to what it sometimes says it is.

Start with the crown jewel: Integrated Gas, the LNG business. It generated adjusted earnings of roughly $8.4 billion in 2025, comfortably the largest single contributor at around 45 percent of the group total.11 This is the segment that houses the liquefaction plants, the shipping, and above all the global trading desk — the arbitrage engine described earlier. It is high-margin, it is hard to replicate, and it is the closest thing an oil major has to a genuine proprietary edge. When Shell's management talks about being "more valuable," this is the segment they are pointing at.

Next comes Upstream — the classic exploration-and-production business of finding oil and gas and pumping it. It delivered roughly $7.7 billion, about 42 percent of earnings. This is the engine room: the low-cost deepwater barrels from Brazil and the Gulf of Mexico that BG helped secure, plus conventional oil and gas production around the world. It is cyclical, it rises and falls with the crude price, but at Shell's cost position it is a reliable cash generator. Together, Integrated Gas and Upstream produced close to 87 percent of Shell's earnings in 2025. That single figure is the most important fact in this entire section: whatever else Shell is, it is overwhelmingly an oil-and-gas company, and its value lives in molecules.

The remaining segments are supporting cast. Marketing — the retail forecourts, the premium Shell V-Power fuels, the lubricants business that is quietly one of the best in the world, and commercial road-transport fuels — contributed roughly $2.7 billion, about 14 percent.11 It is the stable-yield business: less exposed to commodity swings, high return on capital, the part of Shell that behaves almost like a consumer brand. Then Chemicals and Products — refining and petrochemicals — limped in at roughly $0.6 billion, around 3 percent, dragged down by a global glut of refining and petrochemical capacity that has crushed margins across the industry. This is the cyclical weak spot, and management has made clear it intends to shrink and high-grade it rather than defend it.

And then there is the segment that generates all the headlines and almost none of the money: Renewables and Energy Solutions — wind, solar, hydrogen, electric-vehicle charging, and carbon offsets. In 2025 it ran at a small net loss, roughly negative $51 million.11 After a corporate cost line of around negative $920 million for central overhead and financing, the segments reconcile to that $18.5 billion group total. The renewables number is the reality check that punctures the transition narrative from the outside. For all the strategic prominence the energy transition commands in Shell's presentations and its critics' lawsuits, the green portfolio was, in hard cash terms, a rounding error that lost money. That gap — between the strategic oxygen renewables consume and the cash they produce — is precisely the tension a new chief executive was hired to resolve. He resolved it by choosing a side.

VI. The Sawan Regime: "Performance, Discipline, Simplification"

When Wael Sawan took over as chief executive on January 1, 2023, the succession looked, on paper, like continuity. Sawan was a lifer — a Lebanese-Canadian engineer who had spent his entire career at Shell, most recently running the very Integrated Gas and Renewables businesses that sat at the heart of the transition debate. If anyone was going to keep faith with the green agenda, surely it was the man who had just been running it.

Instead, Sawan did something closer to a controlled demolition of the previous strategy. His predecessor's "Powering Progress" framework had committed Shell to shrinking its oil production by 1 to 2 percent a year through the decade — an explicit promise to liquidate the most profitable part of the business on principle. Sawan retracted it. Under his framing — reduced to three words that appear on nearly every slide, "Performance, Discipline, and Simplification" — the goal was no longer to manage decline gracefully but to maximize the cash value of the assets Shell actually owned, and to close the valuation gap with the Americans by behaving more like them.12

In practice that meant a hard turn toward capital discipline. Sawan capped cash capital spending at roughly $20–22 billion a year for the 2025–2028 period, down from the $22–25 billion range that had prevailed, signaling that Shell would spend less and return more.13 He set a target of $5–7 billion in cumulative structural cost reductions by the end of 2028 against a 2022 baseline — not one-off savings but permanent reductions in the company's running costs. And he took a scalpel to the green experiments that were losing money: Shell moved to sell its home-energy retail businesses in the UK and Germany, scaled back its carbon-offset ambitions, exited low-return offshore wind joint ventures, and narrowed its renewable-power focus to a handful of markets where it believed it could actually earn a return. The message to investors was unambiguous — Shell would no longer spend shareholder cash to buy applause from ESG rating agencies.

The capital-return machine that discipline was meant to feed had already been primed. In 2021 Shell had agreed to sell its entire Permian Basin shale position in Texas to ConocoPhillips for $9.5 billion in cash, earmarking $7 billion of the proceeds for additional shareholder distributions.14 That war chest, combined with the buyback-friendly single-share structure built during the London move, let Shell commit to returning 30–40 percent of its cash flow from operations to shareholders through the cycle, with buybacks as the preferred tool. Reducing the share count year after year is the mechanical heart of the entire thesis: even if total profits merely hold flat, fewer shares means higher earnings and cash flow per share — the yardstick Sawan has repeatedly said matters most.

The clearest tell of how seriously the board takes the American-comparison framing is how it decided to pay its chief executive. Sawan's own stake in Shell is modest — on the order of 0.013 percent of the company, worth perhaps $25–30 million, meaningful to him but a rounding error against the company's value.15 So the board proposed leverage instead of ownership. Ahead of the 2026 annual meeting, Shell moved to raise the maximum long-term share award for the chief executive from 600 percent to 900 percent of base salary, a change that could lift Sawan's maximum annual pay toward £19 million and was justified explicitly by the need to benchmark against U.S. rivals, whose bosses have historically out-earned their British peers by roughly three to one.1617 Reasonable people can disagree about whether that is bold alignment or simply importing American pay inflation into a London-listed company. What is not in dispute is the intent: to tie the chief executive's fortune to free cash flow per share and total shareholder return, and to make closing the Exxon-Chevron gap the thing he is personally paid to achieve. Whether he can deliver depends on whether the moats underneath the strategy are real.

VII. The Strategic Moat: 7 Powers & 5 Forces Analysis

Every oil major insists it has an edge. Most are lying, or at least exaggerating, because crude oil is the definitional commodity — a barrel from Shell is molecularly identical to a barrel from BP, and the price is set by global benchmarks no single producer controls. So the honest analytical question is narrow: after you strip away the parts of Shell that are pure commodity exposure, is there anything left that a competitor genuinely cannot copy? Run through Hamilton Helmer's 7 Powers framework, and two candidates survive scrutiny.

The first, and by far the most important, is a blend of scale economies and process power located in the LNG trading desk. A single liquefaction plant confers no special advantage — plenty of companies own one. A single cargo of LNG has no power; it is just gas on a boat. What Shell possesses is different in kind: the largest portfolio of LNG supply positions in the world — secured through decades of long-term contracts and joint ventures, including participation in the giant North Field expansions with the state-owned قطر للطاقة QatarEnergy — married to a proprietary global system of shipping, storage, and trading infrastructure. That combination lets Shell do something no smaller player can: continuously re-optimize where every molecule goes, diverting cargoes mid-voyage toward the highest-priced market and capturing arbitrage spreads between Asia, Europe, and the Americas. This is process power in the truest Helmer sense — an advantage embedded in an organization's accumulated systems, relationships, and know-how that a rival cannot buy off the shelf, because it took decades of physical scale to build the information network that makes the trading profitable. It is the one part of Shell that plausibly deserves a premium multiple, and it is also, not coincidentally, the part most opaque to outside investors, since Shell does not break out trading profits in detail.

The second surviving power is a cornered resource: the pre-salt Brazilian acreage acquired via BG, with break-evens below $30 a barrel. In an industry where the scarce commodity is not oil but cheap oil, owning a large position in some of the lowest-cost barrels on the planet is a durable structural advantage — one competitors cannot replicate because the acreage is finite and already spoken for.

Now flip to the demand side and run Porter's Five Forces. The threat of substitutes is the force that defines Shell's terminal value, and it cuts both ways. In the long run, electrification and cheap solar and wind genuinely threaten oil demand — that is not green propaganda, it is arithmetic, and it is the single biggest reason the whole sector trades cautiously. But in the medium run, natural gas and LNG are unusually well insulated, because gas is both a bridge fuel that displaces dirtier coal and a baseload and industrial fuel that intermittent renewables cannot yet replace when the wind drops and the sun sets. Shell's tilt toward gas over oil is, in effect, a bet on the length of that bridge. Rivalry among the supermajors — Exxon, Chevron, TotalEnergies, BP, Shell — is best understood as a consolidated oligopoly competing for a limited pool of world-class capital projects, but with pricing dictated by external commodity benchmarks rather than by the players themselves. And the bargaining power of buyers for LNG specifically is low precisely at the moments Shell cares about most: when supply tightens, nation-states and utility grids that need energy density right now become remarkably price-tolerant, which is exactly when the trading desk earns its keep. The moats, in short, are real but narrow — concentrated in gas and in Brazil, and vulnerable at the edges. Which is why the risks deserve as much airtime as the powers.

VIII. Risks, Stress Tests, and the Risk Radar

Here is the uncomfortable question a skeptical investor should ask about the entire "Performance, Discipline, and Simplification" story: is capital discipline a strategy, or is it a slow-motion liquidation dressed up as one?

That is Risk 1, the reserve-replacement trap, and it is the sharpest critique of Sawan's regime. An oil-and-gas company is a depleting asset by nature — every barrel pumped is a barrel gone, and reserves must be continuously replaced through exploration and development or the company quietly shrinks toward zero over a decade or two. By capping capital spending at $20–22 billion a year and simultaneously committing to return 30–40 percent of operating cash flow to shareholders, Shell is deliberately spending less on finding new barrels than it might. Management's answer is that discipline means drilling only the best barrels and that quality beats quantity. The bear's answer is that this is what a company says right before it liquidates itself to flatter near-term cash flow and please yield investors — sacrificing the production base of 2032 to fund the buyback of 2026. Both cannot be right, and the honest verdict is that we will not know for years. That uncertainty is itself a reason the market applies a discount.

Risk 2 is the regulatory and courtroom overhang, and it needs no elaboration beyond what the litigation saga already showed. The Dutch Supreme Court cassation appeal remains live, the April 2026 lawsuit demanding an end to new field development is only beginning its journey through the courts, and the broader European legal and political environment has demonstrated that it can and will attempt to constrain fossil-fuel operators in ways no U.S. court would contemplate. Even if Shell wins every case, the mere existence of the arena raises its cost of capital relative to Exxon and Chevron. Litigation risk here is not a tail event; it is a permanent feature of being a European oil major.

Risk 3 is geopolitical and physical: the plumbing of Shell's business runs through a handful of maritime choke points — the Strait of Hormuz, the Strait of Malacca, the Bab el-Mandeb — through which its LNG carriers and crude tankers must physically pass. A closure or conflict at any of these would, paradoxically, cut both ways for Shell: it would disrupt supply and endanger cargoes, but it would also blow open exactly the price spreads its trading desk is built to exploit. Volatility is not uniformly the enemy of an arbitrageur.

Pull these together into a bull-and-bear stress test. The bull case is mechanical and, on its own terms, coherent: Sawan keeps shrinking the share count by a meaningful clip every year through relentless buybacks, structural costs fall on schedule, the high-margin LNG portfolio ramps up as new projects come online, and as the market watches Shell behave indistinguishably from a U.S. major, the valuation discount to Chevron and Exxon narrows — delivering a re-rating that rewards patient shareholders on top of the cash returns. The bear case is that the discipline is really under-investment in disguise: production goes into decline after 2030, high-cost European and Asian refining assets become stranded liabilities, and a fresh adverse climate ruling or a European windfall tax imposes capital-destroying costs at the worst possible moment. The activist's version of the bear case is sharper still — that Shell's conglomerate complexity, its opaque trading profits, and its straddle between two continents' expectations mean it should still be broken up, and that management's incrementalism is leaving value on the table that a cleaner structure would unlock. The truth is that both cases hinge on the same three or four variables, which is what makes Shell such an interesting company to watch rather than to grade. What can be extracted with more confidence are the lessons the story teaches.

IX. Playbook: Key Business & Investing Lessons

The first lesson is the oldest cliché in finance, and Shell spent $70 billion proving it is a cliché because it is true: buy when there is blood in the streets. The BG Group acquisition was mocked because it violated the cyclical reflex — everyone else was cutting when Shell was buying, and paying a rich premium at the trough looked like recklessness. But paying a high premium for tier-one, structurally advantaged assets at the moment of maximum pessimism turned out to be one of the highest-returning capital-deployment decisions any supermajor made in the modern era. The counterintuitive truth is that the premium mattered far less than the timing and the asset quality; a fair price for great assets at the bottom beats a bargain price for mediocre assets at the top. The discipline this requires — deploying capital aggressively precisely when your instincts and your shareholders are screaming at you to hoard cash — is exactly why so few companies actually do it.

The second lesson is about identity: pragmatism beats dogma, in both directions. Shell's valuation suffered for years not because it was too green or too brown, but because it was ambiguously both — trying simultaneously to satisfy ESG rating agencies and traditional energy value investors, and in the attempt convincing neither. Strategic straddles feel prudent and read as hedging, but markets punish them with a complexity discount because investors cannot tell what they own. Sawan's contribution, whatever one thinks of its ethics or its long-run wisdom, was to pick a lane — cash-generative oil and gas, with renewables demoted to opportunistic — and execute it without apology. The lesson is not that his lane is the right one. It is that a clearly chosen and consistently executed strategy earns a higher multiple than an ambivalent one, because clarity is itself something the market pays for.

The third lesson is the one that generalizes far beyond energy: physical scale can unlock trading power. On its own, a commodity business is a miserable place to invest — no pricing power, no differentiation, margins set by the marginal producer. But a sufficiently large physical footprint changes the game, because it becomes the substrate for an information and logistics network that a smaller competitor cannot build. Shell's LNG trading desk is not profitable because Shell is clever; it is profitable because Shell is big enough that its plants, ships, and terminals generate a real-time picture of global gas flows that becomes a proprietary trading advantage. Scale, in other words, can convert a standard commodity into a high-barrier arbitrage platform — the difference between selling a product and running a market. It is the single most underappreciated source of durable advantage in heavy industry, and it is the reason the most interesting question about Shell is not what it drills but what it knows.

X. Epilogue & Critical KPIs to Watch

So where is Shell headed? Toward a single, measurable finish line that management has all but drawn on the floor: narrowing the valuation discount to ExxonMobil and Chevron. Everything the company has done since 2021 — dropping the Dutch name, fleeing to London, unifying the shares, retracting the production-decline pledge, capping capex, cutting costs, and rewiring executive pay around free cash flow per share — points at that one target. The strategy is internally coherent. Whether it works is an empirical question that the next several years will answer, and the answer will show up in a small number of numbers rather than in any press release.

For investors trying to separate the signal from the corporate narration, three metrics matter more than all the others.

The first is return on average capital employed, or ROACE — the blunt test of whether Shell earns a decent return on the money it deploys. Management has framed a through-the-cycle return above 10 percent as the bar of a company that allocates capital well. Watch whether Shell clears it consistently, not just in high-price years, because a discipline strategy that does not lift returns on capital is just cost-cutting with better slides.

The second is the delivery of the structural cost reductions — the $5–7 billion of permanent, cumulative cost savings targeted by the end of 2028 against the 2022 baseline. This is the cleanest test of management credibility available, because it is specific, time-bound, and hard to fudge. A company that hits an explicit multiyear cost target it set for itself has earned some benefit of the doubt on its other promises; one that quietly redefines the baseline or lets the number slip has told you something important about how much its guidance is worth.

The third, and the one Sawan himself has elevated above all others, is free cash flow per share growth — the compounding of cash generated per unit of ownership, which captures the whole thesis in a single figure because it rises both when the business generates more cash and when the share count shrinks. Management has pointed toward double-digit compound annual growth in this metric through 2030 as the prize. It is the right yardstick precisely because it is the hardest to game: you cannot manufacture durable growth in cash flow per share with accounting; you have to earn the cash and retire the shares. If that number compounds as promised, the valuation gap with the Americans will likely close on its own, and the sovereign of the LNG arbitrage will have made its case in the only language the market ultimately respects. If it stalls, all the simplification in the world will not have been enough.

References

-

Shell plc (SHEL.L) Stock and Financial Information — London Stock Exchange ↩

-

Royal Dutch Shell Goes All-In with $70 Billion Purchase of BG Group — Oil & Gas 360, 2015-04-08 ↩

-

Shell-BG merger is effective as of 15 February 2016 — Enerdata, 2016-02-15 ↩

-

Milieudefensie v Shell: Dutch appeals court overturns ruling that Shell must reduce its CO2 emissions by 45% — Mayer Brown, 2024-11 ↩

-

Shell Dropping 'Royal Dutch' from Name and Moving Corporate HQ to UK — Reuters, 2021-11-15 ↩

-

Milieudefensie Lodges Appeal to Supreme Court of the Netherlands — Milieudefensie, 2025-02-11 ↩

-

Milieudefensie launches new Climate Case against Shell: no new oil and gas fields — Milieudefensie, 2026-04-21 ↩

-

Shell Faces New Climate Lawsuit Over Oil & Gas Drilling, Emissions — ESG Today, 2026-04 ↩

-

Shell plc Fourth Quarter 2025 Results Presentation — Shell plc, 2026-02-05 ↩

-

Oil giant Shell posts weakest quarterly profit in nearly five years, keeps buybacks steady — CNBC, 2026-02-05 ↩

-

Shell Q4 results sees adjusted earnings drop to $3.3bn — Energy Voice, 2026-02-05 ↩↩↩

-

Wael Sawan's Pragmatic Shift at Shell Prioritizes High-Margin Oil and Gas — Financial Times, 2023-06-14 ↩

-

Shell plc Capital Markets Day 2023 — Strategic Presentations and Webcast — Shell plc, 2023-06-14 ↩

-

Shell signs agreement to sell Permian interest for $9.5 billion to ConocoPhillips — Shell plc, 2021-09-20 ↩

-

Shell plc — Form 6-K FY2026 (Remuneration) — U.S. Securities and Exchange Commission, 2026 ↩

-

Shell CEO Sawan set to earn £4.5m more a year — Sharecast, 2026 ↩

-

The U.S.-U.K. pay gap is real — just look at how much Exxon Mobil, Chevron, Shell, BP CEOs make — Fortune, 2024-04-12 ↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube