The Sage Group: The Geordie Giant's Great SaaS Pivot

I. Introduction: The "Hardest Trick in Software"

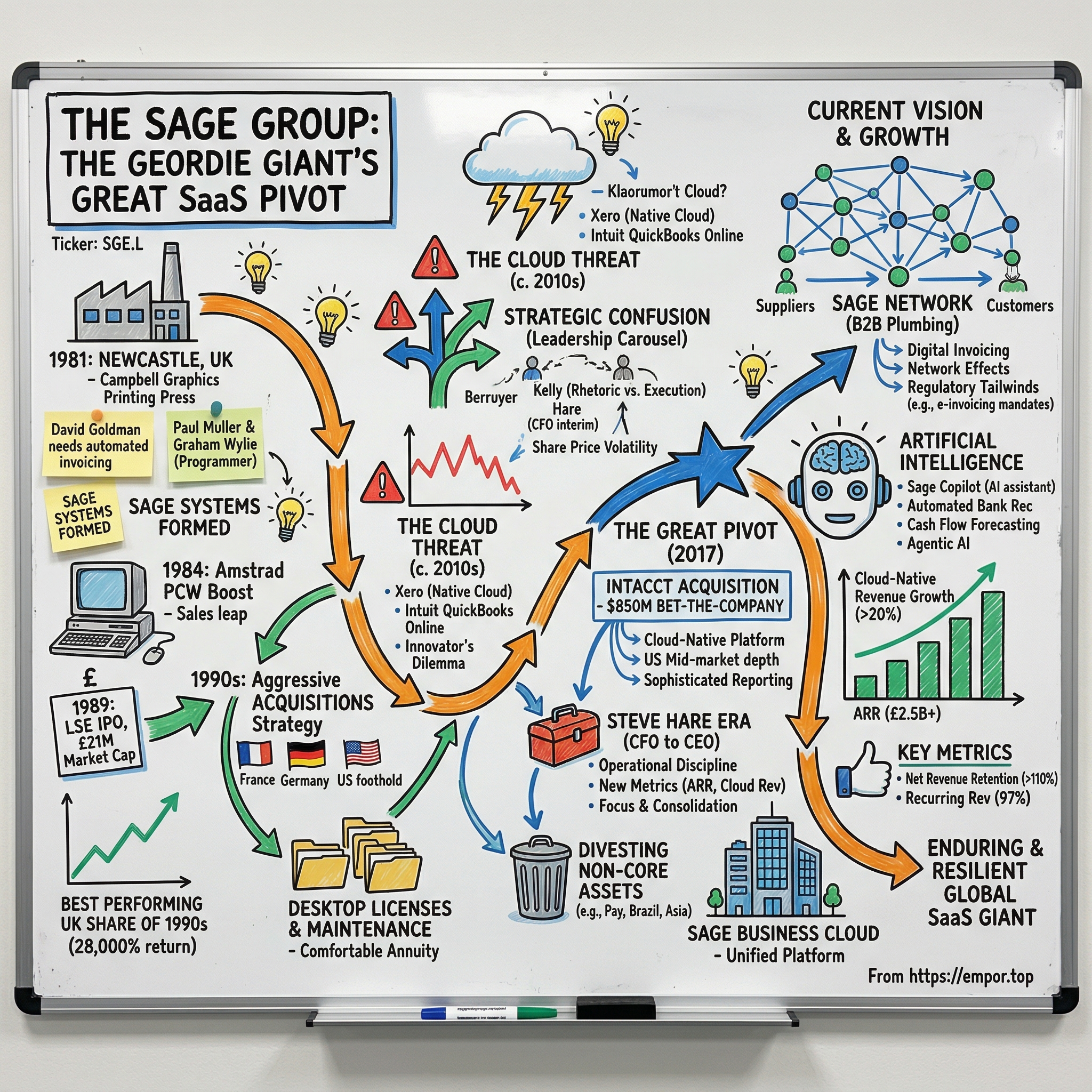

There is a parlour trick in enterprise software that almost nobody pulls off. You take a company built on desktop licenses, maintenance contracts, and the comfortable annuity of customers who are too embedded to leave, and you rebuild it — in flight, while the engine is running — into a cloud-native, subscription-first business. Microsoft did it with Office 365. Adobe did it with Creative Cloud. But for every one of those celebrated transformations, a dozen incumbents failed, slowly bleeding market share until they became footnotes in someone else's acquisition press release.

The Sage Group, headquartered not in Silicon Valley or even London but in the decidedly unglamorous city of Newcastle upon Tyne in northeast England, has quietly pulled off one of the most underappreciated versions of this trick in the history of enterprise software. Founded in 1981 as a side project to automate invoicing for a printing press, Sage grew into the backbone of the global small and medium enterprise economy. By the mid-2020s, it processed the payroll for an estimated quarter or more of the UK's private-sector workforce. Its software touched over six million businesses across twenty-three countries. Its annual recurring revenue crossed two and a half billion pounds. And yet, ask a technology investor in San Francisco about Sage, and you would likely get a blank stare.

That anonymity, paradoxically, is part of the story. Sage is not a company that inspires conference keynote worship or frothy venture capital narratives. It makes accounting software, payroll systems, and tax compliance tools — the plumbing of capitalism, not the chandelier. But plumbing, as any homeowner knows, is where the real money is. It is essential, deeply embedded, and extraordinarily painful to rip out and replace.

The central question of this story is whether Sage has truly completed the hardest trick, or whether the magic is still mid-performance.

The company went from a fragmented "house of brands" running dozens of legacy desktop products to a business that now generates ninety-seven percent recurring revenue, with cloud penetration north of ninety percent. It did so by making one enormous bet, an eight-hundred-and-fifty-million-dollar acquisition of a San Jose company called Intacct, and by installing a former CFO named Steve Hare who brought the operational discipline of a cost accountant to a transformation that had previously been managed with the strategic coherence of a yard sale.

The share price tells one version of the story: at roughly 818 pence, Sage trades near its fifty-two-week low, down more than forty percent from the highs it touched in 2025. The market appears skeptical. But the operational metrics tell another version entirely: ARR growing at eleven percent, cloud-native revenue growing at twenty-two percent, operating margins expanding, free cash flow exceeding five hundred million pounds, and a renewal rate by value above one hundred percent, meaning customers are, on average, spending more with Sage each year, not less.

From Newcastle beginnings to the Intacct gamble to the modern vision of a "Sage Network" powered by artificial intelligence, this is the story of the Geordie Giant's great SaaS pivot.

II. Origins: The 1981 Printing Press and the Desktop Boom

In the early 1980s, Newcastle upon Tyne was not a city anyone associated with the future of technology. The shipyards that had once defined the northeast were in terminal decline. Coal mining was contracting. Margaret Thatcher's government was reshaping the British economy in ways that hit the industrial north disproportionately hard. Against this backdrop, a middle-aged accountant-turned-printing-executive named David Goldman had an idea that seemed, at the time, almost absurdly modest.

Goldman had spent two decades running Campbell Graphics, a printing company in Newcastle, eventually rising to managing director. By 1981, with microcomputers becoming affordable enough for small businesses to contemplate, he began wondering whether the estimating, job costing, and invoicing work that consumed so much of his printing business could be automated. He was not a programmer. He was a practical businessman who understood numbers and hated inefficiency.

The northeast of England in the early 1980s was a region in deep economic distress. The shipyards along the Tyne and Wear, which had once built vessels for the Royal Navy and merchant fleets around the world, were in their death throes. Coal mining, the other great employer of the northeast working class, was contracting rapidly under a government that viewed the industry as an expensive anachronism. Unemployment in parts of Newcastle and Sunderland exceeded twenty percent. Against this bleak backdrop, the microcomputer revolution arrived like a small, improbable lifeline — not for the masses, but for the handful of entrepreneurs who could see what the technology made possible.

Goldman was one of those entrepreneurs. He reached out to Paul Muller, a visiting American lecturer at Newcastle University, and together they connected with Graham Wylie, an undergraduate who had just completed a degree in computer science and statistics.

Wylie was the technical talent. He had taken a summer job with a local accountancy firm, funded by a government small-business grant, and written record-keeping software that became the embryonic code behind what would eventually be Sage.

The three men formed Sage Systems on April 27, 1981, operating from what can charitably be described as modest premises. There was no venture capital, no incubator, no Silicon Valley ecosystem to nurture them. This was Newcastle in 1981, a city still reeling from industrial decline. The startup ecosystem consisted of a printing press, a university lecturer, and a student with a knack for programming.

Their first product was an accounting application designed to run on the Intertec SuperBrain, a clunky machine that used the CP/M operating system, the predecessor to DOS that most people have mercifully forgotten.

For the first three years, Sage was a tiny operation selling a niche product to a niche market. What transformed it was a machine that arrived in 1984: the Amstrad PCW, Alan Sugar's mass-market word processor and computer. The Amstrad was the first device that made computer ownership feasible for ordinary British small businesses. Goldman, with the instincts of a salesman who had spent years in the printing trade, immediately recognized the opportunity. He pushed Sage to repackage its accounting software for the Amstrad platform, and the results were staggering. Monthly sales leapt from roughly thirty copies to over three hundred within a year. By early 1986, driven by Goldman's expanding reseller network, they were moving six thousand copies a month.

What Goldman understood, and what gave Sage its foundational competitive advantage, was that accounting is local. Tax laws are local. Payroll regulations are local. The VAT rules that governed a Newcastle newsagent were different from the tax codes confronting a small business in Dallas or Düsseldorf. While American software companies built products for the US market and assumed the world would follow, Goldman built software that spoke the specific language of British tax compliance. Every budget announcement from the Chancellor of the Exchequer meant an update to Sage's software, and every update reinforced the dependency. If you were a British small business owner in the late 1980s, Sage was not just your accounting software — it was your translator for the byzantine world of PAYE, National Insurance, and VAT returns.

Sage floated on the London Stock Exchange on December 13, 1989, with a market capitalization of twenty-one million pounds. The company employed fifty people, generated nine million pounds in annual turnover, and posted two million in profit.

The IPO was not a blockbuster event by the standards of the era. London's financial establishment, fixated on the Big Bang deregulation of the City and the booming property market, paid little attention to a regional software company from the northeast. The City's analysts, most of whom had never visited Newcastle and had only a vague sense that it was somewhere north of Watford, could be forgiven for missing the significance of a small accounting software vendor listing at a twenty-one-million-pound valuation.

That indifference proved to be a gift. Without the pressure of inflated expectations, Sage could focus on what it did best: selling accounting software to small businesses and compounding returns for patient shareholders.

The decade that followed was extraordinary. Sage became the best-performing UK share of the 1990s, delivering a return of roughly twenty-eight thousand percent over ten years. That figure bears repeating: twenty-eight thousand percent. An investor who bought a thousand pounds of Sage shares at the IPO and held for a decade would have been sitting on a quarter of a million pounds by the turn of the millennium. The company entered the FTSE 100 in 1999, a remarkable achievement for a firm that had started life in a printing works less than two decades earlier.

Goldman retired as chief executive in 1994 and as chairman in 1997. He died in October 1999 after a long illness, leaving behind endowments to Newcastle University, Sunderland University, and, in a fitting tribute, the Sage Gateshead concert hall, the iconic Norman Foster-designed venue that sits on the banks of the Tyne. Graham Wylie, who had overseen software development as head of the UK business, departed in 2003 and was later knighted for his philanthropic work. The two founders had built something remarkable from almost nothing — a globally relevant software company born in one of the most economically disadvantaged regions of western Europe.

But before Goldman stepped back, he set in motion the strategic playbook that would define Sage for the next two decades: aggressive acquisition of local accounting software vendors around the world. If accounting is local, the reasoning went, then global dominance required buying the local champion in every market. It was a logical strategy, and it worked brilliantly — right up until it did not.

III. The Roll-Up Era and the Seeds of Stagnation

Paul Walker, who succeeded Goldman as chief executive in 1994, inherited a company with a proven formula and a mandate to scale it. Over the next sixteen years — one of the longest tenures of any FTSE 100 CEO — Walker transformed Sage from a UK accounting software vendor into a global conglomerate through a relentless campaign of mergers and acquisitions.

The deal sheet reads like a geography lesson. In 1992, Sage acquired Ciel to enter France. The same year brought Telemagic for CRM capabilities. These were small, bolt-on deals — the kind of acquisitions that barely merited a mention in the financial press. But they established a pattern that would accelerate dramatically over the following decade.

In 1998, Walker made his first truly transformative move: the two-hundred-and-sixty-three-million-dollar acquisition of State of the Art, the maker of MAS 90 and MAS 200, which gave Sage a serious foothold in the US mid-market. This was a different kind of deal. State of the Art served tens of thousands of American businesses with manufacturing, distribution, and accounting software. Its products were deeply embedded in the operations of small and mid-sized companies across the United States. For Sage, which had built its empire on British VAT compliance and PAYE regulations, this was a leap into a foreign market with fundamentally different accounting standards, tax rules, and competitive dynamics.

A year later, Sage scooped up Peachtree Software from ADP for one hundred and forty-five million dollars — literally weeks before Peachtree's planned IPO — giving it an entry-level US small business product with a million users. Peachtree was the American equivalent of Sage 50: the default accounting software for small businesses that could not afford — or did not need — a full ERP system. Together, State of the Art and Peachtree gave Sage coverage of both the entry-level and mid-market segments of the American small business economy.

In 2000, the four-hundred-and-forty-five-million-dollar purchase of Best Software added HR, payroll, and analytics capabilities. This was Walker's largest deal to date, and it marked Sage's expansion beyond pure accounting into the broader domain of business management software. The Best Software acquisition was particularly significant because it brought Abra, one of the leading HR and payroll platforms for mid-sized US businesses, into the Sage fold. Payroll, even more than general accounting, is a business function where accuracy is non-negotiable and switching costs are extreme. Getting payroll wrong means employees do not get paid correctly, tax withholdings are miscalculated, and regulatory fines follow. No finance director changes payroll providers willingly. Timberline Software followed in 2003, bringing construction and real estate accounting — a niche vertical with high switching costs and strong recurring revenue. ACCPAC arrived in 2004 from Computer Associates, adding mid-market accounting depth. Adonix, acquired in 2005, extended the French mid-market presence with an ERP solution that served manufacturing and distribution companies.

By the mid-2000s, Sage had entered the FTSE 100, operated in over twenty countries, and served millions of customers. Walker had executed the roll-up strategy with machine-like efficiency, and the financial results were impressive on the surface. But beneath those numbers, a problem was compounding.

Each acquired company retained its own brand, its own codebase, its own development team, and its own customer base. Peachtree was still Peachtree. MAS 90 was still MAS 90. ACCPAC was still ACCPAC. The products did not share a common database schema, a common user interface, or even a common programming language. Some were written in C++, others in Visual Basic, others in proprietary development frameworks that their original creators had long since abandoned.

The result was a "house of brands" that confused customers, frustrated partners, and created an enormous burden of technical debt. At its peak, Sage operated something in the range of twenty-five to thirty distinct product lines across nine countries, each with its own development roadmap, its own support infrastructure, and its own cultural identity.

A Sage salesperson in North America might need to understand the differences between half a dozen overlapping products to recommend the right one for a prospect, assuming they could figure out the differences at all. Partners who implemented Sage products had to maintain expertise across multiple platforms, each with its own certification programme, its own support procedures, and its own quirks.

Sage eventually attempted to impose order through a numerical rebranding — Peachtree became Sage 50, MAS 90 became Sage 100, ACCPAC became Sage 300 — but these were cosmetic changes. Underneath, each product remained a distinct application with its own architecture, its own database schema, and its own update cycle. The rebranding actually made things worse in some ways, because it created the illusion of a unified product portfolio where none existed. A customer who assumed that Sage 50 and Sage 100 were different tiers of the same product — a reasonable assumption given the naming — would discover that they were completely different applications with no upgrade path between them.

This mattered because, while Sage was assembling its portfolio of desktop products through acquisitions, the technology world was shifting beneath its feet.

The browser was becoming the platform. Salesforce, founded in 1999 by Marc Benioff, had proved that enterprise software could live in the cloud and be delivered as a service rather than a product. Amazon Web Services, launched in 2006, was making it possible for any startup with a credit card to provision enterprise-grade server infrastructure in minutes. Google had demonstrated with Gmail and Google Docs that browser-based applications could rival desktop software in speed, reliability, and user experience. The entire architecture of business computing was being rethought.

And a young company in New Zealand called Xero was about to demonstrate that accounting software could be reborn for the internet age.

When Walker departed in December 2010 after sixteen years, he left behind a company generating strong cash flows from a loyal but aging customer base — and a product portfolio that was architecturally incapable of competing in the cloud era. Revenue had grown from under one hundred million pounds to over one and a half billion. The company sat in the FTSE 100. By any conventional financial measure, Walker's tenure had been a success.

But the strategic picture was far less flattering. Sage had dozens of products serving overlapping markets with incompatible technology stacks. It had no cloud-native platform. It had no unified data architecture. And it had cultivated an organisational culture that valued acquisition-driven growth over organic innovation — a culture that would prove extremely difficult to change. The seeds of stagnation had been planted alongside every acquisition.

IV. The Cloud Threat and the Leadership Carousel

The years between 2010 and 2017 were, to put it diplomatically, a period of strategic confusion at Sage. Three different chief executives attempted to navigate the cloud transition, each with a different vision and none with sufficient time or organisational alignment to execute it.

Guy Berruyer, who had run Sage's mainland European and Asian operations, took over from Walker in October 2010. He was a competent operator who made modest improvements to the business but showed little urgency about the existential threat gathering on the horizon. While Berruyer managed Sage's portfolio, Xero — founded in 2006 by Rod Drury in Wellington, New Zealand — was building something fundamentally different: an accounting platform designed from the ground up for the cloud, with a modern user interface, real-time collaboration, an open API ecosystem, and the kind of design sensibility that made accountants actually enjoy using the software. That last point mattered more than technologists appreciated. Accountants are the channel through which small business accounting software is adopted. Win the accountant, win the client.

Simultaneously, Intuit was pouring resources into rebuilding QuickBooks as a cloud-native platform. QuickBooks Online would eventually accumulate over six and a half million subscribers globally, dwarfing Sage's installed base in the critical US market. Intuit's total revenue reached nearly nineteen billion dollars in fiscal 2025, and its market capitalization ballooned to nearly a hundred billion dollars. This was a company that had started in roughly the same place as Sage, selling desktop accounting software to small businesses, but had executed the cloud transition earlier, faster, and more decisively.

While these competitors were building for the future, Sage was milking the present.

The company's legacy desktop products, particularly Sage 50, the direct descendant of Goldman's original Amstrad-era software, still generated substantial recurring revenue from maintenance contracts. Every year, millions of customers paid Sage for software updates that were primarily driven by tax law changes. It was a beautiful business model: the government effectively mandated your product's relevance by changing the tax code annually. Every spring budget from the Chancellor of the Exchequer, every change to National Insurance thresholds or VAT rates, meant that businesses needed an updated version of Sage to remain compliant. And Sage charged them for the privilege.

But it was also a trap. The maintenance revenue was so predictable, so profitable, and so easy that it created an institutional resistance to cannibalizing it with a cloud offering that would initially be less profitable and more expensive to build. This is the classic innovator's dilemma, described by Clayton Christensen: the rational short-term decision is to keep milking the existing business, but the rational long-term decision is to cannibalize it before someone else does. Sage chose the short-term option for too long.

Berruyer retired in late 2014 and was succeeded by Stephen Kelly, Sage's first externally appointed chief executive. Kelly came from the UK government's Cabinet Office, where he had served as chief operating officer, and he arrived with a mandate to be the transformation CEO. His rhetoric was bold: Sage would become a cloud company, a platform company, a company fit for the twenty-first century. He spoke with infectious enthusiasm about "Sage Business Cloud," about artificial intelligence, about building a digital network that would connect millions of businesses.

The problem was execution. Kelly's tenure was marked by inconsistent operational performance, an inability to gain traction against Intuit in the US, and a steady loss of ground to Xero in Sage's home market. The gap between Kelly's ambitious rhetoric and the company's actual progress became a source of frustration for investors, employees, and partners alike. Strategy presentations grew more elaborate while the underlying metrics barely moved.

The share price, which had initially rallied on the promise of transformation, drifted back to July 2016 levels by mid-2018. Board members who had bet on Kelly's ability to accelerate the cloud transition began to question whether the company needed a different kind of leader — one who could deliver operational results rather than inspirational keynotes.

In April 2018, Sage issued a profit warning that cut full-year guidance and cited "inconsistent operational execution" — the corporate euphemism for a strategy that was not working. By August 31, 2018, Kelly was gone. The board announced he was "stepping down," but the abruptness of the departure and the immediate appointment of CFO Steve Hare as interim chief executive left little doubt about the involuntary nature of the transition.

Yet Kelly did leave one legacy that would prove transformational: the acquisition of Intacct. Whatever else went wrong during his tenure, that single deal changed the trajectory of the company. It is one of the great ironies of the Sage story that the CEO who failed at execution presided over the single most important strategic decision the company ever made. Sometimes the right call matters more than the right operator, even if you need a different operator to make the call pay off.

V. The Great Pivot: The Intacct Acquisition and the Rebirth

On July 25, 2017, Sage announced the largest acquisition in its history: the purchase of Intacct Corporation, a San Jose-based cloud accounting platform, for eight hundred and fifty million dollars. It was a bet-the-company moment, and at the time, plenty of observers thought Sage was overpaying.

To understand why the deal mattered, you need to understand what Intacct was. Founded in 1999 by Odysseas Tsatalos and David Chandler Thomas, Intacct was one of the first true cloud-native accounting applications ever built. Not "cloud-washed" — a desktop product with a browser bolted on — but genuinely multi-tenant, designed from its first line of code to run in a shared cloud infrastructure. By 2017, Intacct had eleven thousand customers, eighty-eight million dollars in annual revenue, and a reputation for exceptional depth in dimensional reporting, multi-entity consolidation, and revenue recognition for services businesses. It was particularly beloved by nonprofits, SaaS companies, and professional services firms — exactly the kind of sophisticated, mid-market customers that Sage needed but could not reach with its aging desktop products.

The critics who called the deal overpriced had a point, at least on the surface. Eight hundred and fifty million dollars for eighty-eight million in revenue implied roughly ten times revenue — a premium valuation for a company that was not yet profitable. For a company that had historically bought profitable, cash-generating businesses at modest multiples, this was a dramatic departure.

But context matters. The prior year, Oracle had acquired NetSuite for nine point three billion dollars, also at roughly ten to eleven times revenue. NetSuite was a broader operational ERP suite — financials, CRM, inventory, manufacturing, ecommerce — while Intacct was more narrowly focused on financial management. But Intacct's narrower focus came with deeper functionality in its core domain, and its multi-tenant architecture was arguably more modern than NetSuite's.

There was also the question of what Sage would have had to spend to build a comparable product from scratch. The history of enterprise software is littered with incumbents who tried to build cloud platforms internally and failed — not because they lacked engineering talent, but because their organisational culture, development processes, and legacy code made it almost impossible to build something genuinely new. Buying Intacct was not just buying a product; it was buying a team, a culture, and a competitive position that would have taken Sage a decade to build organically — time it simply did not have.

More importantly, the Intacct acquisition gave Sage something it desperately needed and could not build internally: a genuine cloud-native platform.

Every prior attempt to "cloudify" existing products, adding online backup, browser access layers, or connectivity features to desktop applications, had produced awkward hybrids that satisfied neither traditional users nor cloud-native expectations. Think of it like taking a horse-drawn carriage and bolting an engine onto it: technically it moves under its own power, but nobody would confuse it with a car. Intacct was a car. It was designed from its first line of code to live in the cloud, with automatic updates, shared infrastructure, and the kind of modern architecture that desktop-era software simply cannot replicate through incremental upgrades.

Intacct came with a development team that knew how to build cloud software, a customer base that expected cloud software, and a competitive position in the US mid-market that Sage had been unable to establish through its legacy products.

Sage financed the deal through cash on hand, existing credit facilities, and a new three-hundred-and-ninety-million-dollar term loan. Forty-three million dollars of the transaction involved converting Intacct employee shares into Sage shares, ensuring continuity of the technical team. In hindsight, the purchase price looks like a bargain. By fiscal year 2025, Sage Intacct was generating over four hundred and sixty million pounds in revenue and growing at more than twenty percent annually. Its US annualised recurring revenue was approaching half a billion pounds. International expansion, initially slow, had accelerated to over fifty percent growth outside the United States.

Alongside the Intacct acquisition, Sage embarked on a broader strategic consolidation under the banner of "Sage Business Cloud." The idea was to retire the confusing numerical product hierarchy — Sage 50, Sage 100, Sage 200, Sage 300, Sage X3 — and present customers with a unified cloud platform. This was easier said than done. The legacy products still generated enormous revenue and could not simply be switched off. But the directional intent was clear: Sage would become a cloud company, and Intacct would be its flagship.

The cleanup also involved selling off non-core assets at a pace that would have made a private equity firm proud. In 2017, the US payments business went to GTCR for two hundred and sixty million dollars. In 2019, Sage Pay — the UK and Ireland payments operation — was sold to Elavon for two hundred and thirty-two million pounds. The Brazilian business was divested to local management. The Polish subsidiary went to Mid Europa Partners for sixty-six million pounds. The Swiss business was sold for thirty-nine million. The Asia and Australia operations were sold to The Access Group for ninety-five million pounds. Product lines like ACT! and SalesLogix, once central to the portfolio, had already been offloaded years earlier.

Each disposal sharpened the company's focus and freed capital for reinvestment in cloud products and shareholder returns. The cumulative proceeds from these divestitures exceeded one billion pounds — capital that was recycled into product development, acquisitions, and buybacks.

The message to the market was unmistakable: the house of brands was being demolished, and a focused cloud company was being built in its place.

The Sage that emerged from this pruning bore little resemblance to the sprawling conglomerate of the Walker era. Where Walker had sought to be everywhere, doing everything, Hare's Sage aimed to be focused, disciplined, and ruthlessly prioritized. The product portfolio that had once numbered in the dozens was being consolidated into a handful of strategic platforms. The geographic footprint that had spanned two dozen countries was being concentrated on the markets where Sage had genuine competitive advantages: the United Kingdom, North America, France, Germany, Iberia, and South Africa.

The retained markets were not chosen arbitrarily. Each one either had a large installed base of Sage customers with high switching costs, a regulatory environment that favored Sage's compliance expertise, or a growing mid-market that Intacct could address. The divested markets were either too small to justify the management attention, too competitive to defend profitably, or too distant from the core product roadmap to benefit from shared development.

VI. Current Management: The Era of Steve Hare

On the last day of August 2018, Steve Hare inherited a company in the middle of a messy transformation. The previous CEO had been ousted. The share price was languishing. The cloud transition was behind schedule. And the organisation was demoralised by years of strategic whiplash. What Sage needed was not another visionary — it had heard enough visions. What it needed was an operator.

Hare's background made him almost comically well-suited for the job. He studied economics and accountancy at the University of Liverpool, trained as an auditor at Ernst and Young, and spent over a decade at General Electric — the company that, whatever its later troubles, was the gold standard of operational management in the 1990s. He went on to become CFO of Marconi, then CFO of the industrial conglomerate Invensys, before spending four years as a partner at the private equity firm Apax Partners, where he learned to think about businesses through the lens of value creation and capital allocation.

He joined Sage as CFO in 2014 under Kelly's leadership, was appointed interim CEO when Kelly departed, and was confirmed as permanent chief executive on November 2, 2018. The market's initial reaction was muted — appointing the CFO as CEO is often seen as a caretaker move. But Hare turned out to be anything but a caretaker.

His first strategic act was deceptively simple but profoundly consequential: he changed the metrics by which Sage measured itself.

Under previous leadership, the company had tracked license sales, total revenue, and other traditional software metrics that rewarded one-time transactions. Hare shifted the focus to annualized recurring revenue, subscription penetration, and cloud revenue growth. This was not just a reporting change. It was a signal to the entire organization about what mattered. When the CEO's bonus is tied to ARR growth and cloud penetration rather than license bookings, behavior changes fast. Salespeople stop pushing perpetual licenses and start pushing subscriptions. Product managers stop designing for one-time purchases and start designing for retention. The entire organizational immune system reorients around a different definition of success.

The operational discipline was immediate and sustained. Margins, which had been compressed during the cloud transition, began expanding. From roughly twenty percent underlying operating margin when Hare took over, Sage reached nearly twenty-four percent by fiscal year 2025. This was achieved not through dramatic cost-cutting but through the natural operating leverage of a subscription business: as customers migrated from low-margin perpetual licenses to higher-margin subscriptions, and as legacy products were retired, the cost structure improved.

Hare also proved to be an aggressive allocator of capital. Under his leadership, Sage has repurchased shares at a pace that has reduced the outstanding share count by roughly ten percent — from over a billion shares in 2019 to approximately nine hundred and seventy-eight million by fiscal 2025. In fiscal 2025 alone, the company spent six hundred and five million pounds on buybacks. A further three-hundred-million-pound programme was announced alongside the full-year results in November 2025. Combined with a progressive dividend that has grown at more than five percent annually, total shareholder returns have been substantial.

Hare's compensation reflects the alignment with shareholders that one would expect from a former private equity partner. His fiscal 2024 total remuneration was approximately four point six million pounds, comprising a base salary of nine hundred and twenty-five thousand pounds, an annual bonus of eight hundred and eighty-five thousand, and long-term incentive plan vesting of two point seven million. The long-term incentive vesting — the largest component — was tied to total shareholder return performance relative to the FTSE 100, where Sage delivered a hundred and fifteen percent return compared to forty-five percent for the index over the relevant measurement period. He holds shares worth approximately five point six million pounds directly, meaningful relative to his base salary.

One telling data point: in 2020, during the depths of the pandemic, Glassdoor named Hare the number one CEO in the UK. For a company that had been through the demoralising churn of three chief executives in four years, the stability and clarity that Hare brought should not be underestimated. Sage's employee engagement scores improved markedly under his leadership. Turnover in critical engineering roles declined. The company's ability to recruit cloud-native talent — historically a challenge for a Newcastle-based firm competing against London and Silicon Valley — improved as the cloud transformation gained credibility.

The cultural transformation was perhaps as important as the strategic one.

Under Walker, Sage had been a sales-driven organisation where the ability to close deals and integrate acquisitions was the most valued competency. The heroes of the Walker era were the dealmakers and the regional managers who hit their revenue targets. Under Hare, the heroes became the engineers and product managers who shipped cloud features and improved customer satisfaction scores.

This shift from a sales-driven to an engineering-led organisation is one of the hardest cultural changes a company can make, because it requires changing not just the org chart but the entire value system. Who gets promoted? Who gets the biggest bonus? Whose opinion carries weight in a product meeting? Under Hare, the answers to these questions changed, and the change was reflected in everything from hiring patterns to meeting agendas. This shift was not immediate or painless — it required changes in incentive structures, reporting lines, and the unwritten rules that govern how large organisations actually work — but by 2025, the cultural change was widely acknowledged both inside and outside the company.

His management philosophy can be summarised as "accountant-first." Sage's products are ultimately sold to and through accountants — the bookkeepers, CPAs, and chartered accountants who serve as the trusted advisors to small and medium businesses. If the accountant recommends Sage, the business adopts Sage. If the accountant migrates to Xero, the client follows. Every product decision, every interface design, every partnership is evaluated through the lens of whether it makes the accountant's life easier. It is not a glamorous strategy, but it is a deeply practical one that reflects Hare's understanding of where the real competitive battle is fought.

VII. The Hidden Business: Sage Network and AI

To understand why Sage is more interesting than its reputation suggests, you need to look at what is happening inside the business, beneath the top-line numbers that institutional investors track.

Start with Sage Intacct, which has become the company's growth engine. In fiscal year 2025, Intacct revenue reached four hundred and sixty-one million pounds, up twenty-three percent from the prior year. It now represents over forty-five percent of Sage's US revenue, up from roughly a third just three years earlier. The international expansion of Intacct, initially slow as the product was adapted for non-US accounting standards and regulatory requirements, has accelerated dramatically — annualised recurring revenue outside the United States crossed sixty million pounds and was growing at more than fifty percent.

What makes Intacct's growth particularly impressive is the market it serves. The US mid-market for financial management software — companies too large for QuickBooks, too small for SAP, and too sophisticated for basic cloud accounting — is one of the most attractive segments in enterprise software. These businesses have complex needs: multi-entity consolidation, dimensional reporting across projects and departments, sophisticated revenue recognition, and real-time financial visibility. The primary competitors are Oracle NetSuite and, increasingly, Workday. Intacct's advantage is depth of financial functionality. Where NetSuite offers breadth across the entire operational ERP spectrum — inventory, manufacturing, CRM, ecommerce — Intacct goes deeper on the financial management core. For a hundred-person professional services firm or a mid-sized nonprofit, that depth is exactly what matters.

Meanwhile, the legacy Sage products, Sage 50, Sage 200, Sage X3, continue to generate enormous cash flow. These are not dying businesses in the traditional sense. They serve millions of customers who are deeply embedded, and the migration to cloud-connected and eventually cloud-native versions is happening gradually rather than through forced obsolescence.

The dynamic is similar to what Microsoft experienced with Office. The desktop version did not disappear overnight when Office 365 launched. Instead, customers migrated over the course of years, often driven by specific triggers: a hardware upgrade, a new employee who expected cloud tools, or a regulatory change that required real-time collaboration. Sage is managing the same kind of gradual migration, and the key metric to watch is whether the cloud-native revenue growth rate exceeds the legacy attrition rate. So far, it does, comfortably.

The combination of Intacct's growth and the legacy portfolio's cash generation creates the classic "growth funded by cash cows" dynamic that makes business transitions sustainable.

But the most strategically ambitious initiative at Sage is neither a product nor a platform — it is a network. The Sage Network, which has been developed and expanded since roughly 2022, is a digital business-to-business network that connects small and medium businesses with their customers, suppliers, banks, and tax authorities through digitised invoicing and compliance workflows.

Here is why this matters. Think about what happens when a small business sends an invoice to a customer today. The seller generates the invoice in their accounting system, emails it as a PDF, and the buyer's accounts payable team manually enters the details into their own system. This double-entry of the same information across two separate systems is one of the great inefficiencies of modern commerce. Now imagine that both the buyer and the seller use Sage. The invoice data flows directly from one system to the other without manual re-entry. Errors drop. Processing time is cut in half. Cash flow visibility improves because both parties see the same data in real time.

This is the vision behind the Sage Network: to position Sage as the digital plumbing through which business-to-business transactions flow. The timing is fortuitous. Governments around the world are mandating electronic invoicing — France began requiring it, the European Union is expanding B2B e-invoicing regulations, and similar mandates are proliferating globally. Sage, sitting on a customer base of over six million businesses, is building compliance infrastructure that could become as essential and as sticky as the accounting software itself.

The network model also creates genuine network effects — one of the most powerful competitive advantages in business. Each additional business that joins the Sage Network makes the network more valuable for every existing participant. This is a fundamentally different dynamic from standalone software, where each customer's value is independent.

Consider the analogy to what happened in payments. Visa and Mastercard became enormously valuable not because their technology was superior — the basic concept of card payments is straightforward — but because they built networks that connected millions of merchants with billions of cardholders. Once the network reached critical mass, the cost of not being on the network exceeded the cost of joining it. If Sage can create a similar dynamic for business-to-business invoicing, it would transform the company from a software vendor into a network operator — a fundamentally more valuable and more defensible business model.

That is a big "if," and it is important to be honest about how early the Sage Network is in its development. Building B2B networks is notoriously difficult because both sides of the transaction need to be on the platform for the value to materialise. But the regulatory tailwinds — mandatory e-invoicing in France, expanding mandates across the European Union, Making Tax Digital in the United Kingdom — provide a forcing function that purely market-driven network effects lack. When the government mandates digital invoicing, the question is not whether businesses will join a digital network but which one.

On the artificial intelligence front, Sage launched Copilot in February 2024, an AI-powered assistant embedded across its product suite. By early 2025, over forty thousand customers had access across five markets. The features target the specific pain points that small business owners and accountants face daily: natural language queries for financial data, automated bank reconciliation, cash flow forecasting, variance analysis with real-time alerts, and proactive suggestions for improving working capital.

The AI strategy is pragmatic rather than revolutionary. Sage is not trying to build a general-purpose AI platform or compete with the large language model providers. Instead, it is applying AI to the specific, narrow, high-value tasks that its customers perform repeatedly.

Bank reconciliation, the tedious process of matching bank transactions to accounting entries, is a perfect example. A typical small business might have hundreds of bank transactions per month that need to be matched to invoices, receipts, and journal entries. Traditionally, a bookkeeper does this manually, line by line, often spending hours each week on what is essentially a pattern-matching exercise. AI can do this in seconds, with accuracy rates that improve over time as the system learns the business's specific patterns. For a small business owner who dreads month-end, this is not an abstract technology benefit. It is hours of their life returned to them.

Tax compliance, with its endless rules and edge cases, is another natural application.

In November 2025, Sage launched AI Developer Solutions, enabling partners and independent software vendors to build AI extensions on the Sage platform using Amazon Bedrock. In February 2026, it introduced agentic AI capabilities — autonomous agents that can execute multi-step financial workflows without human intervention. The roadmap points toward a future where the accountant's role shifts from data entry and compliance processing to advisory and strategic guidance, with Sage's AI handling the mechanical work.

For investors, the AI story is less about near-term revenue impact and more about competitive positioning and customer retention. If Sage can embed AI deeply enough into the accountant's daily workflow, the switching costs — already high — become even more formidable. The accountant who has trained Sage Copilot on their specific clients, workflows, and preferences has an additional reason never to leave.

VIII. The Playbook: Competitive Analysis and Strategic Position

To assess where Sage stands competitively, it helps to think through two analytical frameworks: Hamilton Helmer's Seven Powers and Michael Porter's Five Forces.

Sage's primary power, in Helmer's framework, is switching costs. This is not unique to Sage — all enterprise software benefits from switching costs to some degree — but in accounting and payroll software, the costs are unusually high. Consider what happens when a mid-sized business decides to migrate from Sage to a competitor. First, every historical transaction — every invoice, every journal entry, every payroll record going back years — must be migrated to the new system with perfect accuracy. Any error risks corrupting the financial records that the business relies on for tax compliance, audit, and management reporting. Second, every employee who touches the financial system must be retrained. For a company with a dedicated finance team, this means weeks of disrupted productivity during the most critical function in the business. Third, the migration itself creates audit risk. When a company changes its accounting system mid-year, auditors scrutinise the transition with particular intensity, looking for data integrity issues that could affect the reliability of financial statements.

The result is that once a company's historical ledger is embedded in Sage, the rational cost-benefit analysis almost always favours staying. The competitor's product would have to be dramatically better — not marginally, not somewhat, but dramatically — to justify the risk and expense of migration. This dynamic is particularly powerful in the mid-market, where companies are large enough to have complex financial data but too small to have dedicated IT teams that can manage a smooth transition.

The second notable power is what might be called a network effect, though it operates through an unusual mechanism: accountants. In the UK, Sage has an estimated forty percent market share in SME accounting software. This means that the majority of bookkeepers and accountants in Britain know how to use Sage products. They have been trained on Sage. Their workflows are designed around Sage. Their staff are hired partly based on Sage proficiency. This creates a self-reinforcing cycle: because most accountants know Sage, most small businesses use Sage, which means most new accountants learn Sage. Breaking this cycle would require a competitor to simultaneously win over both the accountant community and the small business community — a chicken-and-egg problem that has proven remarkably difficult to solve.

Xero has made meaningful inroads in the UK, particularly among younger accountants and tech-forward practices, but even after nearly two decades of effort, Sage's installed base remains substantially larger. According to recent UK market surveys, Sage maintains roughly forty percent market share in SME accounting software, with Xero at approximately twenty-five to thirty percent and QuickBooks trailing behind. The accountant moat is real, and it is deep.

One way to understand the power of this moat is to imagine what it would cost a competitor to replicate it from scratch. You would need to train hundreds of thousands of accountants on your software, build certification programs, create a partner ecosystem of bookkeeping firms, and establish your product as the default recommendation in accounting practices across the country. Xero has been working on this for nearly two decades and has not yet overtaken Sage in the UK. That is the definition of a durable competitive advantage.

From a Porter's Five Forces perspective, the competitive dynamics differ significantly across Sage's market segments. In the micro and small business segment — sole traders and companies with fewer than ten employees — the threat of new entrants is high. The barriers to building basic cloud invoicing and bookkeeping software are relatively low, and the market has attracted dozens of competitors. Xero and QuickBooks Online dominate this space globally, and Sage's legacy brand is sometimes perceived as old-fashioned by younger business owners.

But in the mid-market segment, where Sage Intacct competes, the picture is very different. Building financial management software that can handle multi-entity consolidation, sophisticated dimensional reporting, complex revenue recognition, and real-time financial intelligence across hundreds or thousands of transactions per day is genuinely difficult. The barrier to entry is not just technical — it is the accumulation of domain expertise across industries, accounting standards, and regulatory requirements that takes years to build. Oracle NetSuite, with the backing of one of the largest technology companies in the world, is the primary competitor. Microsoft Dynamics 365 competes at the edges. SAP Business ByDesign serves the upper mid-market. But for a pure-play cloud-native financial management platform focused on the core of the mid-market, the competitive field is surprisingly narrow.

Supplier power is minimal — Sage builds its own software and uses commodity cloud infrastructure from hyperscalers like AWS and Microsoft Azure, who compete aggressively on price. The primary supply constraint is engineering talent, particularly cloud-native developers and AI specialists, but this is an industry-wide challenge rather than a Sage-specific vulnerability.

Buyer power is moderate for new customers who can evaluate competitors but low for existing customers locked in by switching costs. The interesting dynamic here is the role of accountants as intermediaries. An accountancy practice that serves five hundred small business clients has significant collective buying power — if it decides to standardise on Xero, five hundred businesses migrate. This intermediary power is one of the reasons Sage invests so heavily in its accountant channel and partnership programmes.

The threat of substitutes is primarily the threat that businesses continue using spreadsheets rather than dedicated accounting software, a dynamic that actually works in Sage's favour as regulatory complexity increases and manual compliance becomes increasingly untenable. A more sophisticated substitute threat comes from banks and fintech platforms that embed basic bookkeeping and invoicing functionality into their own products. If a business's bank can automatically categorise transactions, generate VAT returns, and produce basic financial reports, the need for standalone accounting software diminishes. This is a longer-term threat, but one that Sage is addressing through partnerships — the Barclays collaboration announced in March 2026 is explicitly designed to position Sage as the accounting layer that sits behind the banking relationship rather than competing with it.

On capital deployment, Sage's approach under Hare has been a disciplined blend of organic investment and shareholder returns. Research and development spending has risen from roughly nine percent of revenue in 2016 to over fifteen percent in fiscal year 2025 — a meaningful increase that reflects the investment required to build cloud-native products and AI capabilities. At the same time, the company has returned capital aggressively through buybacks, reducing the share count by approximately ten percent over five years, and through a progressive dividend that has compounded at more than five percent annually. The balance sheet carries net debt of roughly one point two billion pounds, or about one point seven times EBITDA — conservative by software industry standards and well within the investment-grade range evidenced by its BBB-plus credit rating from Standard and Poor's.

IX. The Bear vs. Bull Case

The bull case for Sage rests on a simple proposition: the hard part is over. The company has successfully navigated the cloud transition that destroyed or diminished so many legacy software companies. Ninety-seven percent of revenue is now recurring. Eighty-three percent comes from subscriptions. Cloud penetration exceeds ninety percent. Sage Intacct is growing at more than twenty percent annually and has established itself as a credible alternative to NetSuite in the US mid-market. The legacy business, far from collapsing, continues to generate substantial cash flow that funds growth investment and shareholder returns.

The financial profile that emerges from these metrics is compelling. Revenue growth has accelerated to roughly ten percent organic, margins are expanding, and free cash flow conversion exceeds a hundred percent of net income. The business combines the growth characteristics of a cloud software company with the cash generation and predictability of a mature enterprise. The ARR base of two point five billion pounds provides extraordinary visibility into future revenue — more than ninety-seven percent of next year's revenue is essentially pre-sold before the fiscal year begins.

The addressable market is enormous and growing. The global market for SME business management software is measured in the tens of billions, and regulatory trends, mandatory digital tax filing, electronic invoicing mandates, increasing compliance complexity, are structural tailwinds that drive adoption of exactly the kind of software Sage sells.

The company operates in what might be the most recession-resilient segment of enterprise software. Consider the hierarchy of business expenses during a downturn: marketing budgets get cut first, then travel, then new hires, then capital expenditures. The finance function is the last to be touched, because it is legally required. A business can survive without a CRM system. It cannot survive without payroll software or tax compliance. This makes Sage's revenue base unusually defensive, a characteristic that is not always reflected in its valuation during risk-off market environments.

The institutional shareholder base reflects this quality perception. BlackRock holds approximately ten percent of the company, the largest single position. Vanguard, Capital Group, and Norges Bank Investment Management all hold meaningful stakes. The company carries an investment-grade credit rating of BBB-plus from Standard and Poor's, and its net debt of roughly 1.2 billion pounds, at about 1.7 times EBITDA, is conservative by software industry standards.

The Sage Network adds an additional layer of optionality. If Sage succeeds in building a digital network that facilitates business-to-business transactions across its customer base, the competitive moat deepens considerably and new revenue streams — transaction fees, data analytics, financial services — become possible. This is not priced into current expectations and represents genuine upside optionality.

The bear case, however, is not trivial. The first concern is innovation velocity. Sage is a forty-five-year-old company headquartered in northeast England, competing against Silicon Valley-backed companies with deep engineering talent pools and cultures of rapid iteration. Xero, despite being smaller, has consistently been perceived as more innovative and more beloved by its users. Intuit, with its massive scale and data advantages, can outspend Sage on product development by a wide margin. The question is whether Sage can sustain the product innovation required to win new customers, or whether its growth is primarily driven by price increases and cross-selling to an existing base that is shrinking through natural attrition.

The second concern is brand perception. In the UK, "Sage" is still associated by many business owners with the desktop software they used in the 1990s. Younger entrepreneurs are more likely to choose Xero or QuickBooks Online, and once a business is established on a competitor's platform, the switching costs that protect Sage's incumbency work against it. The accountant moat is powerful but not permanent — a generational shift in accountant preferences could erode it over a decade.

The third concern is the valuation question. Sage currently trades at roughly four to five times enterprise value to revenue. Pure-play cloud software companies like Workday trade at seven to eight times, and Intuit commands roughly ten times. This discount reflects the market's view that Sage is still a hybrid business, part cloud growth, part legacy maintenance.

There is a structural challenge here that goes beyond Sage's specific circumstances. European technology companies have historically traded at a discount to their American counterparts, even when the underlying business metrics are comparable. The reasons are debated: smaller domestic markets, less liquid capital markets, lower analyst coverage, cultural biases among global technology investors who default to US-listed companies. Sage suffers from all of these factors, and breaking out of the "European discount" may require not just continued execution but a fundamental shift in how global investors perceive UK-listed software companies.

If the cloud-native portion of revenue, currently growing at more than twenty percent, continues to increase as a share of the total, the blended multiple should naturally re-rate higher. But if growth decelerates or the legacy base erodes faster than expected, the discount could persist or widen.

For investors tracking this story, two key performance indicators matter above all others. First, Sage Intacct ARR growth — this is the engine that drives Sage's relevance in the mid-market and its claim to a cloud-native growth multiple. If Intacct growth remains above twenty percent, the transformation narrative holds. If it decelerates materially, the bear case strengthens. Second, net revenue retention rate across the cloud portfolio — this measures whether existing customers are spending more with Sage over time (through upselling, cross-selling, and price increases) or less (through downgrades and churn). A net retention rate above a hundred and ten percent, which is consistent with what Sage has delivered, indicates a healthy, expanding relationship with the customer base. A declining rate would signal trouble.

The current share price of approximately 817.6 pence, which has pulled back significantly from its fifty-two-week high, reflects some combination of broader technology sector de-rating and investor caution about macroeconomic impacts on SMB spending. At this price, the market capitalisation sits at approximately seven and a half billion pounds, implying a price-to-earnings ratio of roughly twenty-two times and an enterprise value to EBITDA multiple of approximately thirteen to fourteen times.

These multiples are not demanding by software industry standards. They sit well below the valuations commanded by pure-play cloud companies like Workday or ServiceNow, reflecting the market's view that Sage remains a hybrid business — part cloud growth story, part legacy maintenance operation. If the cloud-native portion of revenue continues to grow at twenty-plus percent and becomes the dominant contributor to total revenue, there is a plausible argument for multiple expansion. If the transition stalls, the current valuation may prove generous.

Whether that pullback represents opportunity or prescience depends entirely on whether the operational momentum continues. The free cash flow yield, at roughly six to seven percent, provides a margin of safety that pure growth stocks do not offer. For investors who believe in the transformation thesis, Sage offers an unusual combination: the growth profile of a cloud software company with the cash generation and valuation discipline of a mature enterprise.

X. Epilogue: The AI Future

In early 2026, Sage finds itself in a position that would have seemed almost unimaginable a decade earlier. The company that was once synonymous with dusty desktop software — the beige-box Sage 50 that sat in every British accountant's office — has become a cloud-first, AI-enabled platform generating two and a half billion pounds in largely recurring revenue. The Sage Network is live and expanding. Sage Copilot is in the hands of tens of thousands of customers. Agentic AI capabilities are being deployed across the product suite. A strategic partnership with Barclays, announced in March 2026, is integrating banking and accounting services for UK small businesses through embedded finance.

The latest quarterly results, for the three months ending December 2025, confirmed the trajectory: total revenue up ten percent organically, cloud-native revenue up twenty-four percent, subscription penetration at eighty-four percent, and full-year guidance for fiscal 2026 reaffirmed at nine percent or better organic growth with continued margin expansion. A new CFO, Jacqui Cartin, who joined from KPMG via Sage's finance team, took over from Jonathan Howell at the start of January 2026, ensuring continuity of the financial discipline that has characterised the Hare era.

The acquisitions have continued, though at a more targeted pace: Fyle, an AI-powered expense management platform, in July 2025; Criterion, a human capital management provider, in October 2025; and Akaolife in January 2026. Each acquisition reinforces the strategy of building a comprehensive platform for mid-market business management, layering additional functionality onto the Intacct core.

The deeper question, the one that this entire story has been building toward, is whether Sage represents a rare European technology success story or merely a competent manager of a declining installed base. The evidence increasingly supports the former interpretation. The cloud transition is not just underway — it is substantially complete. The growth engine is firing. The competitive position in the mid-market is strengthening. The AI investment is pragmatic and well-targeted. And the regulatory environment, with its expanding mandates for digital tax compliance and electronic invoicing, is a tailwind that shows no sign of reversing.

David Goldman, the Newcastle accountant who started automating invoices for a printing press in 1981, probably did not envision a multi-billion-pound global technology company.

But the instinct that drove him, that accountants needed software that understood the specific, local, granular complexity of their work, turns out to be as relevant in the age of artificial intelligence as it was in the age of the Amstrad.

There is something deeply satisfying about Sage's story, even for those with no financial interest in the company. It is a reminder that great businesses are not always built by visionaries with world-changing ambitions. Sometimes they are built by practical people solving practical problems — a printer who wanted to know where his money was going, a programmer who could write good code, and a succession of managers who understood that the most valuable software is not the most glamorous but the most essential.

The plumbing of capitalism does not change as fast as the chandelier. But the companies that control it tend to endure.

And in a world that is only becoming more complex, more regulated, more digital, more interconnected, the need for reliable, intelligent, deeply integrated financial software is not going away. Every new tax regulation, every e-invoicing mandate, every compliance requirement adds another layer of complexity that makes dedicated accounting software more necessary, not less. The spreadsheet era is ending, not because spreadsheets have gotten worse, but because the regulatory and operational demands on small business finance have gotten too complex for manual tools to handle safely.

Whether Sage is the company that meets that need for the next forty-five years is an open question. But the fact that it is still here, still relevant, and still growing after forty-five years of relentless technological change is itself a remarkable achievement, one that David Goldman, the practical Geordie businessman, would probably have appreciated more than anyone.

Appendix: Suggested Reading and Resources

- Sage Group plc Annual Report FY2025 (sage.com/investors)

- Sage Group plc Q1 FY2026 Trading Update (January 2026)

- TechCrunch: "Sage Group buys Intacct for $850M" (July 25, 2017)

- Diginomica: Analysis of Sage's Cloud Transformation under Steve Hare

- Hamilton Helmer, 7 Powers: The Foundations of Business Strategy

- Clayton Christensen, The Innovator's Dilemma

- Sage Copilot Product Documentation (sage.com/sage-copilot)

- Sage Network and E-Invoicing Mandates (sage.com/sage-network)

- Barclays-Sage Strategic Partnership Announcement (March 2026)

- Gartner and IDC research on accounting and ERP software markets

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube