Scanfil: The Silent Engine of the Northern European Industrial Renaissance

I. The Hook: The Most Important Company You've Never Heard Of

Pull up a map of Finland. Scroll north from Helsinki, past Tampere, past the lake country, into the flat farmlands of Ostrobothnia. You will find a town called Sievi. Population: roughly four thousand. There is a church, a school, a handful of shops, and a factory complex that generates over eight hundred million euros in annual revenue. That factory belongs to Scanfil Oyj, and if you have never heard of it, that is exactly how they like it.

Scanfil is what industry insiders call an EMS company—Electronic Manufacturing Services. Think of it as the invisible layer between the brands you recognize and the physical products they sell. When a European hospital installs a new diagnostic imaging machine, there is a reasonable chance Scanfil built it. When an EV charging station appears in a parking garage in Stockholm or Hamburg, Scanfil may have assembled the power electronics inside. When a building management system regulates climate in a new office tower, the control modules may have traveled through Scanfil's production lines in Estonia or Poland before arriving at the job site.

The lazy comparison is "the Foxconn of the North," but that misses something important. Foxconn built its empire on staggering volume—millions of identical smartphones rolling off identical lines. Scanfil occupies the opposite end of the spectrum: low volume, high mix, extreme complexity. Their sweet spot is the product that requires fifteen different printed circuit board variants, custom sheet metal enclosures, full system integration, and regulatory certification for medical or energy applications. It is the kind of manufacturing that cannot be easily automated away or offshored to the lowest-cost bidder, because the cost of failure—a misassembled defibrillator, a faulty grid inverter—is catastrophic.

From a tiny sheet-metal shop founded in 1976 to a billion-euro-revenue trajectory in 2026, Scanfil's story touches on nearly every major theme in European industrial history over the past half-century: the rise and fall of Nokia, the reshoring of manufacturing from Asia, the green energy transition, and the quiet power of family-controlled companies that think in decades rather than quarters. What follows is the story of how a company from a town most Finns have never visited became an indispensable backbone of European industry—and why it may be one of the most interesting "hidden" winners of the energy transition and the Western world's geopolitical pivot away from Chinese manufacturing dependence.

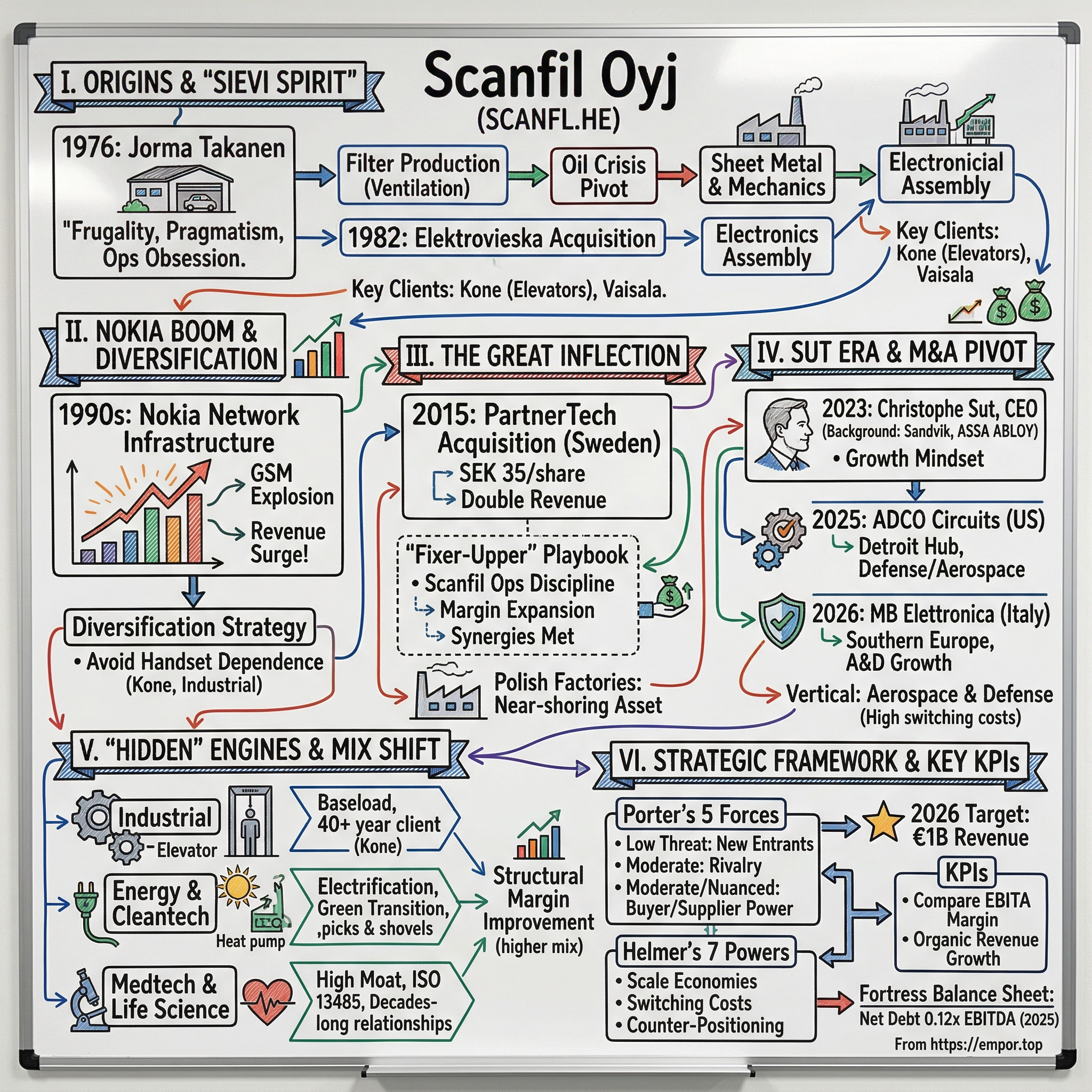

II. Origins and the Takanen DNA

Jorma Takanen was the kind of man Finland produces in small batches but never forgets. Born into a family of thirteen children in Sievi, his father a small-scale farmer who had fought in Finland's wars, Jorma grew up in the sort of Nordic austerity that either breaks people or forges them into something unusually resilient. He was gifted in mathematics—the quiet, obsessive kind of gift that manifests not as academic showmanship but as an instinct for efficiency, for squeezing the maximum output from the minimum input. He worked his way through Tampere Technical College, earning a degree in chemical engineering while simultaneously holding down a job and raising four children. By the time he founded Scanfil on June 4, 1976, he had already mastered the art of doing more with less.

The original business had nothing to do with electronics. Jorma noticed that the ventilation and vehicle filters sold in Finland were almost entirely expensive imports. His insight was simple: manufacture them locally, undercut the imports on price, and deliver faster. He started operations in his older brother's garage in Sievi. It was about as unglamorous as entrepreneurship gets—a man in a garage in a small Finnish town, cutting and shaping filter materials, selling to local businesses.

Then the world intervened. The oil crisis of the early 1980s hammered Finland's economy. Heating was regulated, car usage dropped, and demand for filters collapsed. Many entrepreneurs would have folded. Jorma pivoted. He had the equipment for cutting and shaping metal; he simply redirected it toward sheet metal processing and precision mechanics. This pivot—from filters to metal fabrication—was the foundational move that would eventually lead to everything Scanfil became. It was also the first expression of what might be called the "Sievi Spirit": a combination of extreme frugality, operational obsession, and pragmatic willingness to abandon a failing plan without sentimentality.

The second foundational move came in 1982, when Jorma acquired Elektrovieska Oy, a struggling electronics manufacturer. This was not a sophisticated private equity play. It was a local entrepreneur buying a distressed local business because he saw an opportunity to combine mechanical manufacturing with electronics assembly. But the acquisition brought two things that would prove transformative: it pulled Scanfil into the world of electronic manufacturing, and it delivered relationships with Kone, the elevator giant, and Nokia, which at the time was a sprawling Finnish conglomerate still years away from its mobile phone dominance. Scanfil initially supplied components for Nokia's MikroMikko computers—a product line that most people outside Finland have completely forgotten.

Through the rest of the 1980s, Jorma continued acquiring: Dinsi, a refrigerator equipment maker, and Elacon, an electronics engineering firm. Each acquisition followed the same pattern—buy a struggling operation, apply Sievi-level operational discipline, integrate the capabilities, and use the expanded offering to win new customers. It was a playbook that would prove remarkably durable over the next four decades.

Then came Nokia. By the early 1990s, Scanfil was manufacturing NMT base-station cabinets for Nokia's network infrastructure division. When GSM technology arrived and mobile telephony exploded across Europe, Nokia's orders, in the company's own words, "practically exploded." Scanfil rode the Nokia wave through the 1990s, expanding capacity, adding facilities, and growing at a pace that would have been unimaginable a decade earlier. Nokia became the dominant customer—a relationship that was simultaneously exhilarating and dangerous.

Scanfil's management understood the danger clearly. The company's own historical accounts acknowledge the internal debate about whether Nokia dependence was "a threat or an opportunity." The answer, as it turned out, was both. But unlike many Finnish suppliers who became entirely dependent on Nokia's handset business and were devastated when it collapsed in the late 2000s, Scanfil had two critical advantages. First, their Nokia work was concentrated in network infrastructure rather than handsets—a business that survived Nokia's smartphone implosion and was eventually sold to Nokia Networks. Second, Jorma's instinct for diversification—the same instinct that had pivoted the company from filters to metal to electronics—ensured that Scanfil never stopped cultivating non-Nokia customers. Kone, Vaisala, and a growing roster of industrial clients kept the revenue base from becoming fatally concentrated.

By the time Nokia's decline was undeniable, Scanfil was already a diversified contract manufacturer with capabilities spanning sheet metal, electronics assembly, and full system integration. The Nokia chapter had taught the company a lesson it would never forget: growth through a single customer is a sugar high, not a strategy. That lesson would inform every major decision that followed.

III. The Great Inflection: The PartnerTech Acquisition

In the spring of 2015, Scanfil's management team was staring at a fork in the road. The company had survived Nokia's decline, diversified its customer base, and established itself as a respected Nordic EMS player. But "respected Nordic EMS player" is not the same thing as "globally competitive." Revenue was approximately three hundred and twenty million euros. The company had strong margins and loyal customers, but it was essentially a regional operator with factories concentrated in Finland and the immediate Nordic neighborhood. To reach the next level—to compete for the large, multi-year contracts that global industrial companies award to their manufacturing partners—Scanfil needed scale, geographic reach, and a broader capability set. Fast.

On May 25, 2015, Scanfil announced a recommended cash offer to acquire PartnerTech AB, a Swedish EMS company listed on the Stockholm Stock Exchange. The offer was SEK 35 per share, and the total purchase price for 98.6 percent of the shares came to approximately forty-seven million euros, financed by a loan from Nordea Bank.

To understand why this deal was transformative, you need to understand what PartnerTech was—and what it was not. On paper, PartnerTech looked impressive: factories in Sweden, the United States, China, Poland, and the United Kingdom. A broad customer base spanning industrial, medical, and defense applications. Revenue that would roughly double Scanfil's top line overnight. But PartnerTech was struggling. Its margins were thin, its operations were inefficient, and its geographic sprawl had created complexity without commensurate returns. The company was, in EMS industry parlance, a "fixer-upper."

This is where the acquisition becomes genuinely impressive from a capital allocation perspective. In the EMS industry, companies typically trade at somewhere between 0.3 and 0.5 times enterprise value to sales. PartnerTech, because of its operational problems, was available at the low end of that range—or arguably below it. Scanfil was not buying a trophy asset at a premium. It was buying a distressed operation at a discount and betting that it could apply the Sievi Playbook—the same operational discipline that Jorma Takanen had been practicing since 1976—to fix it.

The bet paid off spectacularly. Scanfil consolidated PartnerTech from July 1, 2015, allocated roughly eleven million euros of the purchase price to long-term customer relationships, recognized seven million euros as goodwill, and set a synergy target of five million euros annually by 2017. Within twenty-four months, Scanfil had stripped out the inefficiency, rationalized the factory footprint, and integrated PartnerTech's operations into its own systems. Revenue roughly doubled. Margins expanded. The synergy targets were met on schedule.

What made it work was not financial engineering. There were no complex earn-outs, no creative accounting, no leveraged recapitalization. It was operational. Scanfil sent its people into PartnerTech's factories and applied the same principles that had governed Sievi since the 1970s: standardize processes, eliminate waste, invest in the workforce, and obsess over customer satisfaction. The PartnerTech integration remains one of the most accretive acquisitions in the history of European contract manufacturing—not because of the price paid, but because of what was done after the deal closed.

The strategic implications were equally significant. Overnight, Scanfil went from a Nordic company with a handful of factories to a genuinely international operator with production capabilities in Sweden, Poland, the United States, and China. The Polish factories, in particular, proved to be a massive asset. Poland offered lower labor costs than Scandinavia, strong engineering talent, improving infrastructure, and EU membership—a combination that made it an ideal near-shoring destination for European customers looking to move production out of Asia without sacrificing quality. The U.S. factory in Buford, Georgia, near Atlanta, gave Scanfil a foothold in the world's largest economy.

For investors, the PartnerTech deal was a proof of concept. It demonstrated that Scanfil's operational model was not just a local Finnish phenomenon but a genuinely portable capability that could be applied across geographies and cultures. It also established a template—"Buy and Fix"—that would define the company's M&A strategy going forward. The question after PartnerTech was not whether Scanfil could do acquisitions well; it was how many more they could find.

IV. Management: The Christophe Sut Era

For roughly fifteen years, from approximately 2008 to 2023, Scanfil was led by Petteri Jokitalo—a capable, steady-handed CEO who oversaw the PartnerTech integration and guided the company from a small Finnish operator to a mid-sized European EMS player. Jokitalo was a builder, not a showman. Under his watch, revenue grew from the low hundreds of millions to over nine hundred million euros at peak. Margins improved. The customer base diversified. It was a quietly excellent tenure.

But by 2023, Scanfil's board—chaired by Harri Takanen, Jorma's son and the family's representative—recognized that the next phase of the company's evolution required a different kind of leader. The PartnerTech playbook had worked. The question was how to scale it further, how to push Scanfil toward the billion-euro revenue mark, and how to position the company for the massive structural tailwinds building in European manufacturing: the energy transition, defense spending growth, and the geopolitical imperative to reshore supply chains from Asia.

On February 11, 2023, Scanfil announced that Christophe Sut would succeed Jokitalo as CEO. Sut joined the company on August 14, 2023, and formally assumed the role on September 1. His appointment signaled a clear strategic shift.

Sut is a French-Swedish dual citizen with a background that reads like a curriculum vitae designed by a management consulting algorithm for "ideal industrial CEO." He holds a master's degree in marketing and sales and a bachelor's in languages and mathematics. His career includes stints at ASSA ABLOY, the world's largest lock manufacturer, where he worked in business development across Sweden and France, and at Niscayah Group, a security services company. But the headline on his resume is Sandvik, the Swedish industrial giant. At Sandvik, Sut served as President of Manufacturing Solutions from 2021 to 2023 and as Executive Vice President of Global Solutions from 2016 to 2021. Sandvik is one of Europe's most admired industrial companies—a business that has mastered the art of high-margin, technology-driven manufacturing at global scale. Sut learned that playbook from the inside.

What Sut brought to Scanfil was not just operational competence—Scanfil already had plenty of that. He brought a growth-oriented strategic mindset and, crucially, the credibility and network to execute larger, more complex acquisitions. Within his first two years as CEO, Sut completed two transformational deals that fundamentally changed Scanfil's scale and strategic positioning.

The first was ADCO Circuits, a Michigan-based electronics manufacturer near Detroit. Scanfil acquired an eighty percent stake, completing the deal on December 10, 2025. ADCO was small—trailing twelve-month revenue of roughly thirty-five million dollars—but it was highly profitable, with an EBIT margin of over eleven percent, and it had something Scanfil badly wanted: significant exposure to the Aerospace and Defense sector, which accounted for thirty-seven percent of ADCO's revenue. The enterprise value was approximately twenty-five million dollars, making it a modest financial commitment with outsized strategic value. It also deepened Scanfil's U.S. footprint beyond the Atlanta factory, placing the company in the Detroit industrial corridor.

The second deal was larger and bolder. On January 22, 2026, Scanfil completed the acquisition of MB Elettronica, an Italian EMS company headquartered in Cortona, Tuscany. MB Elettronica brought roughly five hundred employees, four factories in Italy, and preliminary 2025 revenue of approximately one hundred and twenty million euros—growing at over twenty percent annually. The enterprise value was up to one hundred and twenty-three million euros, including a performance-based earn-out of up to thirty-two million euros tied to 2026 and 2027 results. Like ADCO, MB Elettronica had heavy Aerospace and Defense exposure—roughly forty percent of revenue.

These two acquisitions were not random. They reflected a deliberate strategic pivot under Sut's leadership. By adding Aerospace and Defense as a significant customer vertical—a sector characterized by long contract durations, high switching costs, and growing government budgets across Europe and North America—Sut was diversifying Scanfil's revenue mix while simultaneously pushing into segments with structural growth tailwinds. The acquisitions also expanded Scanfil's geographic footprint into Southern Europe (Italy) and deeper into the United States, creating a manufacturing network that now spans roughly sixteen factories across Europe, North America, and Asia.

The financial impact was immediate. Scanfil's 2026 revenue guidance of nine hundred and forty million to one billion sixty million euros represented a step change from the roughly eight hundred million earned in 2025. Comparable EBITA guidance of sixty-four to seventy-eight million euros implied continued margin expansion. For the first time, the billion-euro revenue milestone was within reach.

Behind Sut stands the Takanen family. Jussi Capital Oy, the family holding company founded in 2008, remains the anchor shareholder. Harri Takanen chairs the board. His brother Jarkko, another significant shareholder, chairs the Shareholders' Nomination Board as of September 2025. Between them, the Takanen family controls what is widely understood to be the single largest ownership block in the company—historically estimated at over thirty percent combined, though exact current figures are held in Finnish filings. This family ownership structure provides what institutional investors sometimes call a "long-termism shield." Sut can make five-year bets—like the MB Elettronica acquisition with its multi-year earn-out—without worrying about activist shareholders demanding immediate returns. It is a governance structure that rewards patience, and patience is precisely what operational transformation in manufacturing requires.

The management incentive structure reinforces this alignment. Sut and his executive team are tied to Total Shareholder Return and EBIT margin targets, ensuring that growth does not come at the expense of profitability. It is a simple, clean incentive structure that avoids the perverse incentives sometimes created by revenue-only or earnings-per-share targets.

V. The "Hidden" Engines: Segments and High Growth

Walk into one of Scanfil's factories—say, the facility in Pärnu, Estonia, or the one in Myslowice, Poland—and the first thing that strikes you is the diversity of what is being built. On one production line, technicians in cleanroom suits are assembling complex diagnostic equipment destined for a European hospital. On another, workers are integrating power electronics for EV charging stations. Down the hall, automated pick-and-place machines are populating circuit boards for building climate control systems. It looks less like a single factory and more like three or four different businesses sharing a roof.

That impression is not far from the truth. Scanfil reports its revenue across three customer segments—Industrial, Energy and Cleantech, and Medtech and Life Science—and the dynamics of each are strikingly different.

Industrial is the largest segment and the historical core of the business. In 2024, it generated approximately three hundred and sixty-eight million euros in revenue. This segment includes automation system modules, frequency converters, elevator control systems, and a wide range of industrial electronics. Kone, the Finnish elevator giant, has been a customer since the Elektrovieska acquisition in 1982—a relationship spanning more than four decades. Industrial is a stable, moderate-growth segment. It does not generate headlines, but it generates consistent cash flow and provides the baseload of factory utilization that allows Scanfil to absorb fixed costs efficiently.

Energy and Cleantech is the segment that gets growth investors excited. At roughly two hundred and sixty-six million euros in 2024 revenue, it is the second-largest segment, and it sits squarely in the path of Europe's most powerful structural trend: the electrification and decarbonization of the economy. Scanfil manufactures components and systems for EV charging infrastructure, heat pumps, reverse vending machines, air and water purification systems, and energy management equipment. Think of it as a "picks and shovels" play on the green transition. Scanfil does not own any of the brands—it does not sell EV chargers or heat pumps under its own name—but it builds the physical hardware that those brands depend on. When a European government announces a new subsidy for heat pump installations or a mandate for EV charging infrastructure in commercial buildings, the demand flows through to Scanfil's order books, often with a lag of six to twelve months.

The 2024 revenue decline in this segment—down seventeen percent year-over-year—reflected a broader European destocking cycle rather than any structural problem. Customers who had over-ordered during the pandemic supply chain panic were working through excess inventory. The underlying demand drivers—regulatory mandates, carbon reduction targets, building electrification requirements—remain intact and are accelerating.

Medtech and Life Science is the smallest segment at roughly one hundred and forty-six million euros in 2024 revenue, but it is arguably the most strategically valuable. This segment manufactures complex diagnostic equipment, medical analyzers, meteorological instruments, and life science devices. Vaisala, the Finnish maker of environmental and industrial measurement systems, is a long-standing customer. What makes Medtech special is the nature of the competitive moat. Manufacturing medical devices requires ISO 13485 certification—a rigorous quality management standard that takes years to achieve and maintain. Once a device manufacturer has validated Scanfil as its production partner and obtained regulatory approval for the finished product, switching to a different manufacturer is extraordinarily expensive and time-consuming. The customer would need to re-validate the entire manufacturing process, re-certify with regulatory bodies, and risk production disruption during the transition. For a medical device company shipping products to hospitals, that risk is simply unacceptable. The result is customer relationships that last decades, not years, and pricing power that exceeds what a contract manufacturer would normally enjoy.

Scanfil does not publicly disclose segment-level margins, but the logical inference—supported by EMS industry benchmarks—is that Medtech commands the highest margins, followed by Industrial, with Energy and Cleantech somewhat lower due to the more competitive and price-sensitive nature of the cleantech equipment market. The critical dynamic to understand is the "mix shift" that has been quietly reshaping Scanfil's profitability profile over the past decade. As Medtech and Industrial have grown as a proportion of total revenue, and as lower-margin Communication and Consumer Applications segments have shrunk (these segments were previously reported separately but have been consolidated or phased down in current reporting), the overall margin of the business has structurally improved. Adjusted operating margin reached 6.8 percent in 2024, and comparable EBITA margin hit 7.1 percent in 2025—both strong by EMS industry standards, where five to six percent is considered respectable.

This mix shift is not accidental. It is the result of deliberate customer selection and strategic investment in capabilities—particularly in certifications, cleanroom manufacturing, and system integration—that enable Scanfil to serve higher-value, higher-margin applications. Sut's acquisitions of ADCO Circuits and MB Elettronica, both with significant Aerospace and Defense exposure, represent the latest chapter of this story: adding yet another high-barrier, high-switching-cost customer vertical to the portfolio.

VI. The Strategic Framework: Competitive Moats and Industry Dynamics

To understand why Scanfil has been able to sustain margins above its peer group for over a decade, it helps to apply two of the frameworks most beloved by fundamental investors: Hamilton Helmer's 7 Powers and Michael Porter's 5 Forces.

Start with scale economies. Scanfil is the largest contract manufacturer in the Nordic region, roughly double the revenue of the number-two player, Kitron of Norway. This scale advantage is not about building more widgets per hour—Scanfil's model is low volume, high mix, which means traditional manufacturing scale economies (longer production runs, lower unit costs) are less relevant. Instead, Scanfil's scale advantage manifests in procurement leverage. When you are buying electronic components, connectors, sheet metal, and passive parts at the volume Scanfil does across sixteen factories, you get pricing from suppliers that smaller competitors like Note AB of Sweden or Hanza simply cannot match. You also get priority allocation during supply shortages—a factor that proved enormously valuable during the 2021-2022 semiconductor crisis, when the ability to secure components separated the winners from the losers in the EMS industry.

The second power is switching costs, and this is arguably Scanfil's most durable competitive advantage. In traditional contract manufacturing, switching costs are moderate—if one factory can build your product as well as another, you move for a better price. But Scanfil has systematically positioned itself not as a vendor but as a "solution partner" that embeds deeply in the customer's product development process. Scanfil engineers work alongside customer R&D teams during the design phase, contributing manufacturing expertise that influences component selection, assembly sequence, and testability. By the time a product reaches volume production, Scanfil's manufacturing process is not just building the customer's design—it is intertwined with it. The tooling, the test fixtures, the quality control protocols, and increasingly the regulatory certifications are all specific to the Scanfil-customer partnership. Walking away means re-engineering significant portions of the manufacturing process.

In Medtech, this dynamic approaches what Helmer would call a "Cornered Resource"—not because Scanfil owns a scarce physical input, but because the regulatory certification (ISO 13485, and often customer-specific validation protocols) creates a barrier so high that switching becomes practically impossible for the duration of a product's lifecycle, which in medical devices can span ten to fifteen years.

Now apply Porter's lens. The threat of new entrants into Scanfil's core markets is extremely low. Building a competitive EMS operation requires massive capital investment in factory infrastructure, automated assembly lines, testing equipment, and cleanroom facilities. It requires years of effort to obtain the relevant certifications—ISO 13485 for medical devices, aerospace quality standards for defense work, and the various environmental and safety certifications demanded by European industrial customers. It requires a track record of reliability that can only be built over decades. A startup cannot credibly bid on a contract to manufacture diagnostic imaging equipment for a major medical OEM. The barriers are not just financial; they are temporal. Time is the moat.

Supplier bargaining power is moderate. Scanfil depends on electronic component distributors and raw material suppliers, and during periods of shortage—as the 2021-2022 chip crisis demonstrated—suppliers hold significant power. However, Scanfil's scale provides partial insulation, and the company has invested in supply chain management capabilities that allow it to secure allocation more reliably than smaller competitors.

Buyer bargaining power is the most nuanced force. Scanfil's customers are typically large industrial companies with significant purchasing leverage. In theory, they could pressure Scanfil on pricing. In practice, the switching costs described above, combined with Scanfil's positioning as a value-added partner rather than a commodity supplier, create meaningful pricing stability. The critical insight is that for most of Scanfil's customers, manufacturing cost is not the primary concern—reliability, quality, speed to market, and regulatory compliance are. A medical device company will not switch manufacturers to save three percent on unit cost if the switch introduces even a small risk of production disruption or regulatory delay.

The competitive threat from substitutes is low in Scanfil's core segments. The main "substitute" for outsourced manufacturing is in-house production, and the long-term trend has been decisively in the opposite direction. As products become more complex and manufacturing investment requirements grow, OEMs increasingly prefer to outsource to specialists like Scanfil rather than maintain their own production capabilities. This structural outsourcing trend is one of the industry's most reliable growth drivers.

Rivalry among existing competitors is moderate and primarily regional. In the Nordic and Northern European theater, Scanfil competes with Kitron (Norway, approximately five hundred million euros in revenue), Note AB (Sweden, roughly three hundred million), GPV Group (Denmark, approximately five hundred million), Hanza (Sweden, roughly three hundred million), and Inission (Sweden, approximately two hundred million). None of these competitors match Scanfil's combined scale and geographic breadth. Globally, the EMS giants—Jabil at twenty-nine billion dollars in revenue, Flex at twenty-six billion, Sanmina at seven billion—operate at an entirely different scale but focus primarily on higher-volume segments (consumer electronics, automotive, telecommunications) where Scanfil does not compete directly. The competitive dynamic is less "war" and more "coexistence in adjacent niches."

What emerges from both frameworks is a picture of a business with quietly formidable competitive positioning. Scanfil does not have a flashy moat—no patents, no network effects, no viral consumer brand. Its moat is built from the accumulation of unglamorous advantages: operational excellence honed over decades, regulatory certifications that take years to obtain, customer relationships forged through co-development, and scale that provides procurement leverage without the bureaucratic sclerosis that afflicts the global giants. It is the kind of moat that does not photograph well but compounds relentlessly.

VII. The Playbook: Lessons in Operational Excellence and Capital Deployment

There is a persistent myth in technology investing that hardware manufacturing is a "bad" business—low margins, high capital intensity, commodity competition. The argument goes that the real value accrues to the intellectual property owner, the brand, the software layer, while the manufacturer is condemned to compete on cost in a race to the bottom. Foxconn's thin margins on iPhone assembly are often cited as the canonical example.

Scanfil's track record challenges this narrative. The company has demonstrated that contract manufacturing can be a genuinely attractive business if you choose your customers wisely, invest in capabilities that create switching costs, and maintain the operational discipline to convert revenue into returns on invested capital that rival or exceed many asset-light business models.

Consider the capital efficiency numbers. Scanfil's Return on Invested Capital has ranged from roughly ten percent to nearly fourteen percent over recent years, hitting 13.9 percent in 2023. For context, ROIC in the low teens is considered excellent for any manufacturing business. The global EMS giants—Jabil, Sanmina, Flex—operate at significantly higher absolute revenues but often generate comparable or lower ROIC, weighed down by the capital demands of their higher-volume, lower-margin segments. Scanfil consistently punches above its weight in capital efficiency because its high-mix, low-volume model requires less investment in dedicated production lines and specialized tooling. Each factory can serve multiple customers across multiple product categories, maximizing asset utilization.

The "Buy and Fix" acquisition model is another dimension of capital deployment that deserves scrutiny. Starting with PartnerTech in 2015 and continuing through ADCO Circuits and MB Elettronica in 2025-2026, Scanfil has demonstrated a repeatable playbook: identify operationally underperforming EMS companies with attractive customer bases and geographic positions, acquire them at valuations that reflect their current distress rather than their potential, and apply the Sievi operational template to unlock margin improvement. The PartnerTech deal was acquired at approximately forty-seven million euros for a business that contributed roughly three hundred million euros in additional revenue—a fraction of sales. ADCO Circuits was purchased at an enterprise value of roughly twenty-five million dollars for a thirty-five-million-dollar revenue business with eleven-percent-plus margins, implying the target was already well-run and Scanfil was paying a fair price for quality rather than buying distress. MB Elettronica, at up to one hundred and twenty-three million euros for a business doing one hundred and twenty million in revenue and growing at over twenty percent, was the most expensive acquisition relative to revenue—but the earn-out structure meant Scanfil was paying the premium only if performance materialized.

This disciplined, template-driven approach to M&A is worth contrasting with the acquisition strategies of many industrial conglomerates, which often overpay for "strategic" assets and then struggle with integration. Scanfil's advantage is that it is buying businesses that do essentially the same thing it does—contract electronics manufacturing—in different geographies. The integration playbook is therefore directly applicable. There is no need to learn a new industry or manage a fundamentally different business model. It is the same game, played on new fields.

The near-shoring tailwind deserves special attention because it represents a structural shift that could benefit Scanfil for years or even decades. The COVID-19 pandemic exposed the fragility of global supply chains concentrated in Asia. The subsequent geopolitical tensions between Western nations and China—trade restrictions, tariff threats, technology export controls—accelerated a trend that was already building: European and American companies actively seeking to move manufacturing closer to home. "Friend-shoring," "near-shoring," "reshoring"—the terminology varies, but the direction is clear.

Scanfil is positioned almost perfectly for this trend. Its factory network spans Finland, Sweden, Estonia, Poland, Germany, Italy, and the United States—all countries that qualify as "friendly" manufacturing destinations for Western companies. The Polish and Estonian factories offer cost structures that are competitive with (though not as cheap as) Chinese production, while providing the advantages of EU membership, geographic proximity to major European customers, shorter supply chains, and avoidance of geopolitical risk. The Italian factories acquired through MB Elettronica add Southern European coverage. The U.S. factories serve American customers who increasingly face regulatory or political pressure to source domestically.

Every major customer conversation today, according to EMS industry commentary, includes a discussion about supply chain resilience and geographic diversification. When a European medical device company or energy technology firm decides to move production out of China, Scanfil's network of European factories makes it one of the most obvious candidates to receive that volume. This is not theoretical future demand—it is happening now, and it is contributing to the order book growth that underpins Scanfil's 2026 revenue guidance.

VIII. Analysis: The Bear Case Versus the Bull Case

No investment thesis is complete without honest scrutiny of both sides, and Scanfil—despite its impressive track record—faces genuine risks that deserve clear-eyed assessment.

The Bear Case

The most obvious risk is cyclicality. Scanfil's customers are industrial companies, and industrial spending is inherently cyclical. When the European economy slows—as it did in 2024, when Scanfil's revenue declined nearly fourteen percent—order volumes drop, factory utilization falls, and margins compress. The 2024 revenue decline, from nine hundred and two million euros to seven hundred and eighty million, was not caused by competitive losses or operational failures; it was a broad-based destocking cycle affecting the entire EMS industry. But it demonstrated that Scanfil is not immune to macroeconomic gravity. A deep European recession could produce a more severe and prolonged downturn.

Labor cost inflation in Eastern Europe presents a medium-term structural risk. Poland and Estonia—where Scanfil operates factories specifically because of their cost advantages—have experienced rapid wage growth as their economies have developed and tightened labor markets have bid up skilled manufacturing wages. If this trend continues, the cost arbitrage between Eastern European and Western European manufacturing narrows, potentially undermining the value proposition of Scanfil's lower-cost factories. This is not an immediate threat—the cost gap remains significant—but it is a trend worth monitoring over a five-to-ten-year horizon.

Integration risk from the recent acquisitions cannot be dismissed. The PartnerTech integration was a clear success, but MB Elettronica is a larger, more complex deal involving four Italian factories and five hundred employees, with significant cultural differences from Scanfil's Nordic core. The Aerospace and Defense sector—which both ADCO and MB Elettronica serve heavily—has its own regulatory requirements, customer dynamics, and competitive landscape that Scanfil is still learning. The earn-out structure on MB Elettronica mitigates financial risk, but operational integration is never guaranteed.

Finally, there is what might be called "key person" concentration. Christophe Sut has been CEO for less than three years but has already reshaped the company's strategic direction through major acquisitions and a push into new verticals. If Sut were to depart—for personal reasons, a competitor's offer, or disagreement with the board—the company would face a disruptive leadership transition at a critical moment. The Takanen family's board presence provides continuity, but the family members are owners and governance figures, not operating executives. The operational momentum depends significantly on the current management team.

The Bull Case

The bull case rests on what might be called the "Triple Tailwind"—three structural trends, each individually powerful and collectively potentially transformative.

The first tailwind is the energy transition. Europe's commitment to decarbonization—expressed through the European Green Deal, Fit for 55 targets, building electrification mandates, and EV infrastructure requirements—creates sustained, regulatory-driven demand for the products Scanfil manufactures. Heat pumps, EV chargers, smart grid components, energy management systems—all require the kind of complex electronic and electromechanical assemblies that Scanfil specializes in. This is not speculative demand dependent on consumer trends; it is mandate-driven demand backed by government policy and subsidies. The 2024 destocking cycle was a temporary pause, not a reversal of the underlying trend.

The second tailwind is Medtech growth. Global healthcare spending continues to grow, driven by aging populations, expanding access in developing markets, and the increasing technological sophistication of diagnostic and therapeutic devices. Scanfil's medical device manufacturing capabilities—backed by ISO 13485 certification and decades of customer relationships—position it to capture a growing share of the outsourced medical device manufacturing market. The switching costs in this segment are so high that existing customer relationships are essentially annuities.

The third tailwind is friend-shoring and the geopolitical de-risking away from Asian manufacturing. As discussed previously, this trend is actively driving manufacturing volume toward Scanfil's European and American factory network. Every new tariff threat, every new trade restriction, every new corporate risk assessment that flags China dependency strengthens Scanfil's competitive position. The addition of Aerospace and Defense customers through the ADCO and MB Elettronica acquisitions adds another dimension: defense spending in both Europe and North America is increasing, and defense supply chains are subject to the most stringent domestic manufacturing requirements.

The valuation debate is essentially a question of categorization. If Scanfil is viewed as a "boring" cyclical manufacturer, it deserves a modest multiple. If it is viewed as a "high-growth" enabler of the energy transition and defense spending boom, with structural tailwinds and durable competitive advantages, it deserves a premium. The market, as of early 2026, appears to be debating this question in real time. With a market capitalization of roughly seven hundred and eighty million euros, the company trades at a valuation that reflects appreciation for its quality but does not fully discount the potential for sustained above-market growth.

The balance sheet provides an additional margin of safety. Net debt to EBITDA of 0.12x at the end of 2025 is essentially unleveraged—giving Scanfil significant dry powder for additional acquisitions while maintaining the financial conservatism that the Takanen family has always prioritized. The equity ratio of nearly fifty-four percent reflects a fortress balance sheet by manufacturing standards.

The KPIs That Matter

For investors tracking Scanfil's ongoing performance, two metrics stand out as the most important leading indicators. The first is comparable EBITA margin—the company's preferred profitability measure, which strips out acquisition-related amortization and one-time items. This metric captures the mix-shift story: as higher-margin Medtech and Defense revenue grows as a proportion of total sales, comparable EBITA margin should trend upward over time. Any sustained compression would signal either competitive pressure or a deterioration in customer mix. The second is organic revenue growth, separated from acquisition-driven growth. Scanfil's story depends on the claim that its end markets are structurally growing and that its customer relationships are deepening. Organic growth confirms this narrative; persistent organic decline would undermine it regardless of how many acquisitions the company completes.

IX. Conclusion and Final Reflections

Sievi, Finland, is not a place that features in the imagination of global investors. There are no gleaming tech campuses, no celebrity founders, no viral product launches. There is a factory complex in a small town, run by the descendants of a farmer's son who started cutting filters in his brother's garage fifty years ago. And yet, from this improbable origin, Scanfil has built something genuinely remarkable: a billion-euro-revenue manufacturing platform that serves as the hidden backbone of Europe's industrial modernization.

The story of Scanfil is, in many ways, the story of Finland itself—a small country that compensates for its lack of natural advantages with extreme operational discipline, pragmatic decision-making, and a long-term orientation that borders on the geological. Jorma Takanen's founding principles—frugality, customer obsession, the willingness to pivot when circumstances demand it—have proven more durable than any technology or market trend. They survived the oil crisis. They survived the Nokia boom and bust. They survived the pandemic supply chain crisis. And they are now fueling a company that stands to benefit from some of the most powerful structural trends in the global economy.

The transition from the Takanen founder era to the Sut growth era is still in its early innings. The ADCO and MB Elettronica acquisitions have reshaped the company, but they have not yet been fully integrated or proven out. The billion-euro revenue milestone remains a target rather than an achievement. The Aerospace and Defense vertical is new territory with its own challenges and learning curves.

But the template is established. The operational playbook works. The competitive position is strong and getting stronger. The balance sheet is clean. The family ownership provides strategic patience. And the structural tailwinds—energy transition, Medtech growth, friend-shoring—are not cyclical phenomena that will reverse with the next recession; they are generational shifts that will play out over decades.

Scanfil is a reminder that the most durable businesses are often the ones that stay quiet, focus on the unglamorous reality of making physical things work, and compound relentlessly in the background while the rest of the market chases the next headline. In a world increasingly obsessed with software, artificial intelligence, and digital disruption, there is something deeply compelling about a company that bets everything on being the best at the hard, physical, certified, regulated, painstaking work of manufacturing. It is not glamorous. It is not viral. But it is essential—and increasingly, it is scarce.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube