J Sainsbury plc: The Battle for the British Basket

I. The £125 Million Goodbye

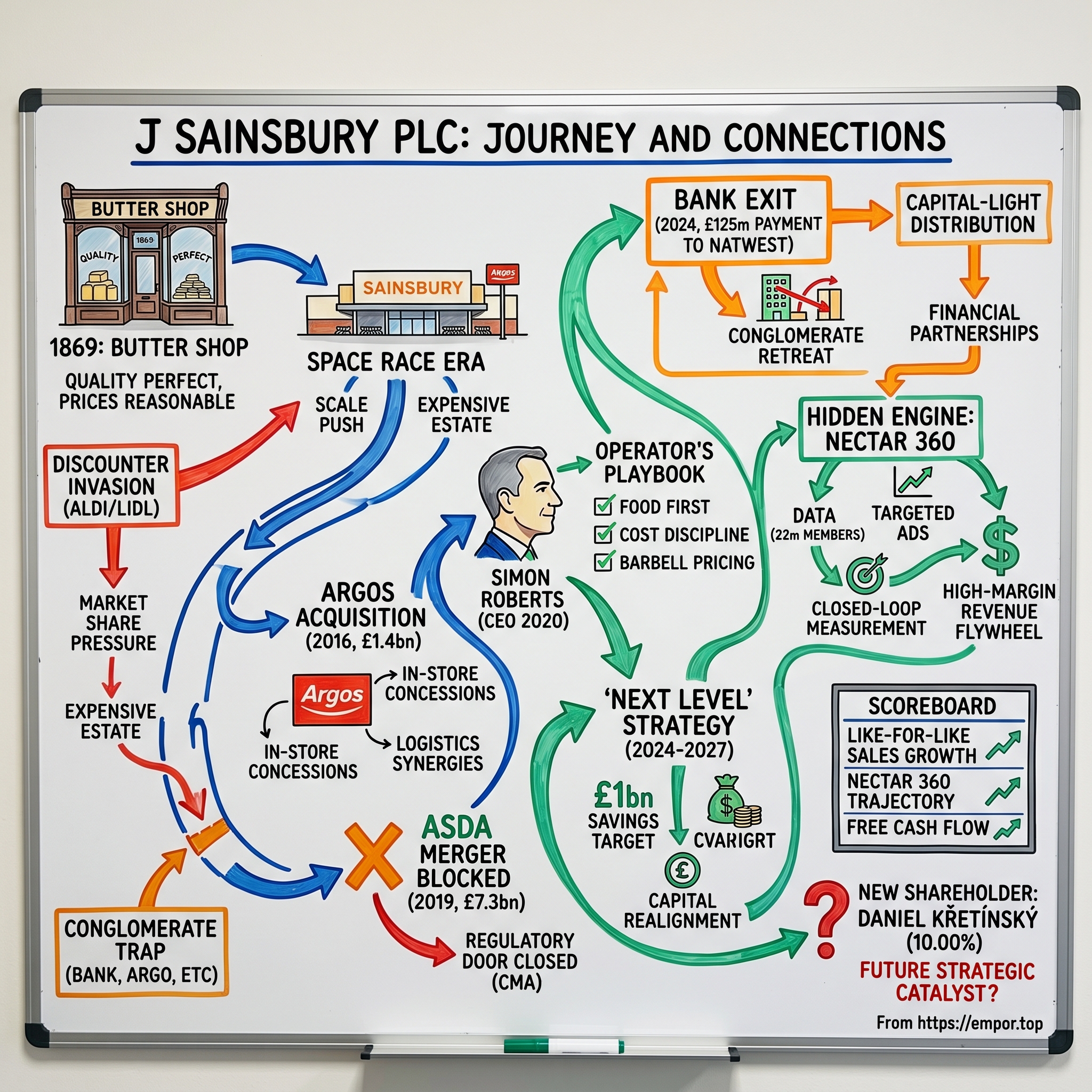

In June 2024, the management team at J Sainsbury plc gathered to sign off on a transaction that would make most first-year MBA students recoil. They were going to pay a competitor to take a business off their hands. Not sell it. Not spin it off. Pay for the privilege of being relieved of it.

The competitor was NatWest Group, one of Britain's "big four" high-street banks. The business being handed over was the beating heart of Sainsbury's Bank — roughly £2.5 billion in customer loans, credit cards, and retail deposits, built up patiently over more than a quarter of a century.3 And the cheque flowed in the direction you would least expect. Sainsbury's agreed to contribute around £125 million of capital to NatWest as part of the deal, effectively a transfer premium to make the whole thing go away cleanly and quickly.3

Pause on that for a moment. One of Britain's most recognizable companies — a 150-year-old retail institution that sells groceries to roughly a third of the country — looked at a banking division holding billions in assets and concluded that the smartest financial move available was to pay someone else to own it.

To an outsider, it reads like an admission of failure. To anyone who understands the brutal arithmetic of modern retail and the punishing capital rules that govern modern banking, it was something closer to a masterstroke. It was the cleanest possible expression of a strategy that had been building for years: ruthless focus, capital discipline, and the recognition that a supermarket is not, and should never have tried to be, a financial conglomerate.

This is the central tension of the Sainsbury's story. For most of the last two decades, the company chased scale, diversification, and the comforting idea that a great retailer should sell you everything — your weekly shop, your sofa, your car insurance, your holiday money, your mortgage. And one by one, each of those bets ran into a wall: German discounters who undercut them on price, a competition regulator who blocked their escape route, and a capital base that was being stretched across too many businesses earning too little.

The thesis of this episode is that Sainsbury's spent the last ten years performing one of the most disciplined acts of corporate triage in British retail history. They escaped the conglomerate trap. They survived an existential assault from the hard discounters. They abandoned the dream of growth-by-merger after a regulator slammed the door. And in the process, they discovered that their single most valuable hidden asset was not their bank, not their vast property estate, and not even the physical act of selling food. It was data — a high-margin advertising and loyalty machine sitting quietly inside a low-margin grocery business.

Here is the roadmap. We start in Victorian London, with a dairy shop on Drury Lane, and trace how the British grocery market evolved into the bare-knuckle brawl it is today. We then walk through the three defining strategic episodes of the modern era: the audacious £1.4 billion acquisition of Argos, the disastrous and ultimately doomed £7.3 billion merger attempt with Asda, and the clean break from banking. We meet Simon Roberts, the operator's operator now running the company, and dissect the "Next Level" playbook. We pull apart Nectar 360, the retail-media goldmine that may be the most important thing Sainsbury's owns. And finally we war-game the whole UK grocery sector through Hamilton Helmer's 7 Powers and Porter's 5 Forces, before closing on the curious arrival of a Czech billionaire on the share register.

Let's begin where every great retail story begins: with a shopkeeper who believed he could do it better.

II. A Victorian Butter Shop and the Space Race Hangover

The year is 1869. Drury Lane in London's Holborn is not the theatrical district romantics imagine — it is crowded, noisy, and frequently filthy, a warren of working-class tenements where food hygiene is more aspiration than reality. Into this opened a tiny shop run by a young couple, John James Sainsbury and his wife Mary Ann.1 They sold butter, milk, and eggs. And they sold them with an obsession that would define the company for the next century and a half: cleanliness, order, and a promise distilled into a single phrase — "Quality perfect, prices reasonable."

It sounds quaint. It was, in fact, radical. In an era when much of British food retail meant produce of dubious provenance sold from sawdust-strewn floors, the Sainsbury's proposition was that a shop could be spotless, the goods could be trustworthy, and the prices could still be fair. Mary Ann reportedly ran the shop floor while John James worked the supply side, and the partnership built something that spread store by store across London. The marble counters, the tiled walls, the white-aproned staff — Sainsbury's was selling reassurance as much as it was selling dairy.

We are not going to spend an hour in the nineteenth century, because the truth is that the company's distant past, romantic as it is, tells you relatively little about the investment case in 2026. What matters is the throughline: from the very beginning, Sainsbury's competed on quality and trust rather than rock-bottom price. That positioning — slightly upmarket, slightly more expensive, but reliably better — is the strategic DNA that explains both the company's resilience and its later vulnerability.

Fast-forward through the twentieth century at speed. The family-run counter shops gave way, after the Second World War, to American-style self-service supermarkets. The customer picked up a basket, walked the aisles, and paid at a till — a revolution in labour efficiency and store throughput. Sainsbury's rode that wave to become, for a long stretch of the post-war era, the dominant force in British grocery, the aspirational middle-class shop where you went for better food.

Then came the era that still casts its shadow over the company's balance sheet: the Space Race.

Through the 1990s and 2000s, the great British grocers — Sainsbury's, Tesco, and Asda chief among them — became convinced that the path to victory was physical. Bigger stores. More of them. Better locations. The logic was seductive and, for a while, correct: more selling space meant more sales, more sales meant more buying power, and more buying power meant lower costs and fatter margins. So they spent billions hoovering up land banks and erecting cavernous superstores and hypermarkets on the edges of British towns, ringed by acres of car parking. It was an arms race in concrete and steel, and the prize was square footage.

The problem with arms races is that they rarely end when you want them to. The grocers built and built, locking up enormous amounts of capital in high-cost property, on the assumption that British shoppers would keep filling ever-larger trolleys on a single weekly trip. And then two things happened that broke that assumption.

The first was the rise of online and convenience shopping, which fragmented the big weekly shop into smaller, more frequent baskets — top-up trips to local stores, deliveries to the door. Suddenly a 100,000-square-foot hypermarket on a ring road looked less like an asset and more like a liability: expensive to run, expensive to heat, and increasingly half-empty in the back corners where the homewares and electronics used to fly off the shelves.

The second was an invasion. And it came, improbably, in the form of bare-bones boxes flying German flags.

Aldi — split historically into the two sister companies Aldi Süd and Aldi Nord — and Lidl, owned by the privately held Lidl Stiftung & Co. KG, arrived in Britain with a model that was the precise opposite of the Space Race. They didn't build hypermarkets. They built small, cheap, ruthlessly efficient stores stocking a deliberately narrow range — perhaps 1,500 to 2,000 product lines against a big supermarket's 30,000-plus. The shelves were stacked with own-brand goods sold from the cardboard cases they shipped in. There was no theatre, no marble counters, no aspiration. There was just price — frequently 30 to 40% below the legacy supermarkets on comparable items.

For years, the British grocery establishment dismissed them. The discounters were for someone else, the thinking went — not for the aspirational Sainsbury's shopper who cared about quality. That complacency proved expensive. When the financial crisis hit and household budgets tightened, middle-class shoppers who had never imagined setting foot in an Aldi discovered that the milk was the same milk, the discount was real, and the social stigma had evaporated. The discounters stopped being a fringe and became a structural force, marching from a couple of percent of the market toward, eventually, a combined share rivalling the legacy players.

This is the trap that Sainsbury's found itself in by the mid-2010s. It was sitting on a vast, expensive estate built for a model of shopping that was fragmenting. Its core middle-class customers were defecting, basket by basket, to the discounters. And its entire historical positioning — quality, but at a premium — was precisely the positioning most exposed to a competitor screaming "same quality, far cheaper."

The Space Race hangover demanded a response. Sainsbury's needed a new playbook, and it needed one fast. The first big swing would be an attempt to grow into a business the discounters couldn't touch — a business they didn't even compete in. It would be the boldest acquisition in the company's history, and it would have nothing to do with food.

III. The Argos Gambit

By 2016, the mood inside Sainsbury's was one of strategic urgency bordering on anxiety. Online shopping was no longer a curiosity; it was a tidal force. And on the horizon loomed the most fearsome competitor in the history of retail — Amazon — which had spent years methodically dismantling the economics of selling anything that could be boxed and shipped. Books, electronics, toys, homewares: category after category was being hollowed out. For a grocer that earned a wafer-thin margin on food and had hoped to make up the difference selling higher-margin general merchandise, this was a clear and present danger.

The then-CEO, Mike Coupe, and his team reached a striking conclusion. If Amazon was going to eat non-food retail, Sainsbury's needed a non-food business with two things Amazon couldn't easily replicate: a trusted brand in general merchandise, and a physical network that could deliver to customers faster than a parcel from a distant warehouse. There was an obvious target. Argos.

For anyone outside Britain, Argos requires a brief explanation, because it is a genuinely peculiar institution. Argos was a catalogue retailer — for decades, you walked into a store, flipped through a thick laminated catalogue chained to a counter, scribbled the product code of the kettle or the trampoline or the games console you wanted onto a little paper slip with a tiny golf pencil, queued at a till, paid, and then waited for a staff member to retrieve your item from the warehouse behind the wall. No browsing aisles of stock. It was, in essence, an analogue version of e-commerce that had existed since the 1970s — order from a catalogue, collect or have delivered. And crucially, it had quietly built one of the most sophisticated same-day fulfilment networks in the country.

Argos sat inside a listed parent company called Home Retail Group, which also owned the home-improvement chain Homebase. And here the chess began. Before Sainsbury's could acquire what it actually wanted — Argos — it needed the structure to be clean. So the path was cleared: Home Retail Group sold Homebase to the Australian conglomerate Wesfarmers for around £340 million, removing the part of the business Sainsbury's had no interest in.2 With Homebase gone, Sainsbury's moved on the prize, launching a recommended offer for Home Retail Group valued at approximately £1.4 billion.2

Now, the Acquired question: did they overpay?

This is where the deal gets genuinely interesting, because on the numbers, Sainsbury's drove a hard bargain. Home Retail Group carried a substantial cash pile on its balance sheet — around £309 million. When you acquire a company, the cash it holds effectively reduces what you're really paying for the operating business, because that cash becomes yours. Netting it out, the effective enterprise value — the true economic price of the Argos business itself — came down to roughly £1.1 billion.

Against Argos's retail earnings, that implied an EV/EBITDA multiple of around 4.1 times. For the non-finance listener, EV/EBITDA is simply a way of asking: how many years of a business's core operating profit am I paying to own it? A multiple of four-ish is cheap — it says the market had largely given up on Argos as a structurally declining catalogue dinosaur. And the comparison to peers makes the point vividly. Sainsbury's own shares traded at around 5.1 times that same measure. Morrisons sat near 7 times. And the recovering market leader, Tesco, commanded around 9 times. Even recent deals in the sector, like Steinhoff's acquisition of the discount chain Poundland for around £610 million, had cleared at richer multiples. By those yardsticks, Sainsbury's was buying a real business with real cash flows at a distressed price.

But a cheap multiple only matters if you can actually do something with the asset. This is the part of the Argos story that elevates it from "bargain hunting" to "strategic masterclass." Sainsbury's didn't buy Argos to run it as it was. They bought it to fold it into their own real estate.

Recall the Space Race hangover — all those big stores with too much space and too few high-margin sales. Argos was the answer. Sainsbury's began closing down expensive, standalone Argos high-street shops, each with its own rent, its own rates, its own staff, and its own heating bill, and re-opening them as "digital concessions" inside existing Sainsbury's supermarkets. A corner of the grocery store, previously underperforming, became an Argos collection point. The customer ordered online or at a kiosk; the goods arrived via Argos's existing logistics network; and Sainsbury's paid almost no incremental rent because it already owned the building.

The financial logic was beautiful. Sainsbury's had targeted around £120 million in annual EBITDA synergies from the combination, and it hit that target ahead of schedule by ruthlessly executing this co-location strategy. Every standalone store closed and absorbed into a supermarket stripped out a rent bill while keeping the sales. Every previously dead square foot of grocery space started earning its keep. And the supermarket itself benefited — shoppers coming to collect an Argos order frequently picked up a few groceries on the way out.

There was a deeper strategic prize, too. Argos's fulfilment network gave Sainsbury's a genuine "hub-and-spoke" same-day delivery capability for general merchandise — the supermarkets as hubs, the vans and the network as spokes. In an age where Amazon's entire competitive weapon is speed and convenience, Sainsbury's had bought itself a credible same-day offer in toys, electronics, and homewares that an online-only player would struggle to match without building physical locations of its own.

So the verdict on the Argos gambit is overwhelmingly positive: a piece of capital allocation that maximized the yield of an underused asset base, built a logistics moat against Amazon, and did it at a price that, in hindsight, looks like a steal. It was Sainsbury's at its strategic best — patient, structural, and financially disciplined.

Which makes what came next all the more painful. Flush with the confidence of having pulled off the Argos integration, Sainsbury's reached for a far bigger prize. And this time, instead of buying a complementary business at a discount, it tried to swallow a direct rival. The regulator was waiting.

IV. The £7.3 Billion Merger That Never Was

In the spring of 2018, Mike Coupe was caught on camera in a moment that would haunt him. Waiting in a TV studio before an interview about the deal he was about to announce, and apparently believing his microphone was off, he quietly hummed the show tune "We're in the Money." The clip leaked. It became, for critics, the perfect symbol of executive hubris — a CEO crooning about a windfall before the public, the regulator, or arguably reality had weighed in.

The deal he was humming about was enormous. Sainsbury's proposed to merge with Asda, the British supermarket then owned by the American giant Walmart, in a transaction valued at around £7.3 billion.[^5] The strategic rationale was, on paper, irresistible. Sainsbury's had spent years watching Tesco tower over the market with the scale advantages that come from being number one. A combined Sainsbury's-Asda would leapfrog Tesco to become Britain's largest grocer, commanding north of 31% of the market.[^5] The promise was scale — the buying power to squeeze suppliers, the cost base to fund lower prices, and the heft to finally answer the discounters on their own terms.

Coupe and his team believed they had a winning structure. Walmart would take cash and a significant equity stake in the combined company, getting a graceful exit from a British market where Asda had been losing ground. The two chains, the argument went, were complementary — Asda strong in the north and among value shoppers, Sainsbury's strong in the south and the middle-class basket. Management projected that the combined buying power would let them cut prices on everyday items by around 10%, a benefit they insisted would flow straight to consumers. They even pledged £1 billion in what they described as "enforceable" price cuts to win over the authorities.[^5]

It was not enough. Not even close.

The deal landed on the desk of the Competition and Markets Authority, the UK's antitrust regulator, and the CMA did what good competition regulators do: it ignored the rhetoric and went straight to the local map. Because the genius and the curse of grocery competition is that it is intensely local. A shopper in a particular town doesn't care that the merged company will be efficient nationally; they care whether the merger means the only two big supermarkets within driving distance now belong to the same owner. And when the CMA modelled the country town by town, the picture was damning.

In April 2019, after an in-depth investigation, the CMA blocked the merger outright.[^5] Its reasoning was forensic. The regulator found that the tie-up would lead to a "substantial lessening of competition" in 537 local areas where Sainsbury's and Asda stores overlapped, at 127 fuel stations, and across the national market for online grocery delivery.[^5] In plain terms: in hundreds of communities, combining the two chains would hand the merged entity so much local dominance that it could quietly let prices drift up and service drift down, and shoppers would have nowhere better to go. Sainsbury's had offered to divest up to 150 stores to address the overlaps, but the CMA judged the remedy inadequate against the sheer breadth of the problem.[^5]

It was a humiliation. The CMA's decision didn't just reject the deal; it implicitly rejected the entire premise — the idea that scale-by-consolidation was a legitimate path forward for a top-tier British grocer. The door to growth-by-merger had not merely been closed; it had been bricked up.

The market's reaction was brutal. Sainsbury's shares slumped, falling around 5% on the worst of the news and touching their lowest level in roughly three decades — a wipeout that erased the optimism the deal had inspired. The strategic damage was worse than the share-price damage. Sainsbury's was now stranded. It had bet its forward strategy on getting bigger, and it had been told, definitively, that it could not. Walmart, for its part, simply moved on, eventually selling Asda to the billionaire Issa brothers — the entrepreneurs behind the EG Group petrol-station empire — in partnership with the private equity firm TDR Capital, in a heavily debt-financed buyout that would load Asda with leverage for years to come.

Here is where the story turns, and turns decisively. The Asda rejection, painful as it was, forced a reckoning that Sainsbury's might otherwise have avoided for years. If you cannot grow bigger, the only option is to grow better. If you cannot acquire your way to advantage, you have to operate your way there. The blocked merger killed the scale dream and, in killing it, cleared the ground for a completely different strategy — one built on focus, cost discipline, and squeezing more value out of the core grocery business rather than bolting on more businesses around it.

That pivot would soon have a name and a champion. But before the new strategy could fully take hold, Sainsbury's had to deal with the most awkward legacy of its old, sprawling, "sell-everything" ambitions. It had to figure out what to do about the bank.

V. The Bank Exit

There was an idea that captivated British supermarket executives for the better part of two decades, and it went something like this: we have millions of customers walking through our doors every week, we have their trust, and we have a brand they see more often than they see their actual bank. Why on earth would we let them buy their credit card, their loan, their car insurance, and their holiday money from anyone but us?

It was the one-stop-shop dream, applied to financial services. And so, in 1997, Sainsbury's Bank was born — one of the first of the supermarket banks, a venture that would over the years offer personal loans, credit cards, savings accounts, insurance, and travel money to the grocery faithful. Tesco did the same. For a while it felt visionary: capital-light distribution riding on top of a captive retail audience.

Then the world changed underneath it. The 2008 financial crisis triggered a global re-write of banking regulation, and the new rules were merciless about one thing in particular — capital. Regulators, having watched banks blow themselves up, now demanded that any institution holding loans and deposits set aside large buffers of capital against the risk of losses. The economics of banking were transformed. A loan book was no longer just a stream of interest income; it was a magnet for regulatory capital, money that had to sit on the balance sheet doing nothing but absorbing theoretical losses.

For a giant bank, that capital intensity is the cost of doing business, spread across a vast operation. For a sub-scale supermarket bank, it was poison. Sainsbury's Bank found itself caught in the worst possible middle ground. It was far too small to compete with the major high-street clearing banks, who enjoyed enormous economies of scale in technology, funding, and compliance. But it was far too large and complex to be run as a casual side-hustle. It was a real bank, with real regulatory obligations, locking up real capital — capital that could otherwise have been returned to Sainsbury's shareholders or, better still, poured into the price war where the company actually needed to fight.

This is the conglomerate trap in its purest form. A business that made strategic sense in one era had become, in another, a drain — quietly consuming capital and management attention while earning returns that didn't justify either. The discipline of good capital allocation says that when you find yourself in that position, sentiment is the enemy. It doesn't matter that you founded the thing, that it carries your name, that it once seemed like the future. What matters is whether owning it is the best use of the next pound of capital. For Sainsbury's Bank, by the 2020s, the answer was clearly no.

So under the new strategy — which we'll come to shortly — Sainsbury's resolved to do something clean and decisive: exit banking entirely. In June 2024, it struck the deal with NatWest, agreeing to transfer the bank's core portfolio of around £2.5 billion in customer loans, credit card balances, and retail deposits.3 And here we return to the puzzle we opened with — the £125 million flowing the "wrong" way.

Why would Sainsbury's pay to leave? The answer lies in the nature of what was being transferred. A banking portfolio is not like a shop you can simply lock up and sell. It comes wrapped in legacy liabilities, ongoing regulatory capital requirements, and operational complexity that a buyer has to absorb. Sainsbury's had two realistic alternatives to a clean transfer. It could wind the book down slowly over many years — a grinding, capital-consuming process of letting loans mature and deposits run off, all while keeping the regulatory machinery running. Or it could sell the assets at a steep discount to compensate a buyer for taking on the baggage.

Instead, Sainsbury's chose speed and finality. By contributing roughly £125 million of capital to NatWest as part of the transaction, it effectively paid to make the portfolio attractive enough to transfer cleanly and immediately, freeing itself from years of slow wind-down.3 Think of it as paying a premium for certainty — converting a long, messy, capital-trapping exit into a single clean break. For a management team obsessed with freeing up capital and simplifying the business, £125 million to be done with banking forever was a price worth paying.

The transaction moved through the formal machinery over the following year, gaining High Court approval in April 2025 and taking legal effect on May 1, 2025, when NatWest formally absorbed the portfolio.4 The mechanism — a court-sanctioned banking business transfer — is the standard legal route for moving large books of regulated banking assets between institutions, and its completion marked the effective end of Sainsbury's life as a deposit-taking bank.

But the bank's lending book was only one piece of the financial-services puzzle, and the exit was methodical. Sainsbury's sold its travel money operation to the foreign-exchange specialist Fexco, completing that piece in 2024.[^13] And it transferred its insurance business into a partnership model — moving the actual underwriting risk to specialists like Allianz and the LV brand, while keeping a relationship with customers as a distributor rather than a risk-bearer.

This last point is the strategic crux. Notice the transformation in the shape of the business. Before, Sainsbury's owned the financial products — it held the loans, took the deposits, bore the insurance risk, and consequently bore the capital cost. After, it became a partner: it lends its brand and its customer access to specialists who own the risk and the capital burden, and it collects a commission for the introduction. The economics flipped from capital-intensive ownership to capital-light distribution. Sainsbury's gets to keep offering its customers financial products — preserving the customer relationship — without tying up a single pound of regulatory capital against them.

That is the difference between a conglomerate and a focused retailer with smart partnerships. And it captures, in miniature, the entire philosophy of the era now dawning at the company — an era defined less by what Sainsbury's owns and more by what it has the discipline not to own. To understand how that philosophy took hold, we need to meet the man who has spent the last several years imposing it.

VI. The Operator: Simon Roberts and the New Guard

If Mike Coupe's defining image was humming a show tune about money before a merger that collapsed, Simon Roberts's defining image is almost the opposite: a CEO who is far happier standing in the chilled aisle at six in the morning, watching how the shelves get filled, than he is sketching grand acquisitions in a boardroom.

Roberts took the top job in June 2020 — a baptism by fire, given that he assumed command in the teeth of the COVID-19 pandemic, when supermarkets had become front-line essential infrastructure and grocery logistics were under unprecedented strain.1 He was not a parachuted-in financier or a celebrity hire. He was a career retail operator, and a deeply experienced one. Before Sainsbury's, he had run the health-and-beauty chain Boots, one of the most demanding operating jobs in British retail. He then joined Sainsbury's as Retail and Operations Director — the executive responsible for the actual stores, the supply chain, the daily grind of getting goods onto shelves and customers through tills.

This background matters enormously, because it explains the entire strategic posture of the company under his leadership. Roberts is, by temperament and training, an operator, not a dealmaker. His reputation is for disciplined, data-led, store-floor execution — the unglamorous, relentless work of taking cost out of a system and putting service back into it. After the Asda fiasco, Sainsbury's needed precisely that. It needed someone constitutionally allergic to distracting mega-M&A and constitutionally drawn to the hard, incremental gains of running a tighter ship.

His strategy bore the names to match. First came "Food First" — a deliberate, almost defiant reassertion that Sainsbury's core job was to sell groceries brilliantly, not to be a financial conglomerate or a property play. Food First was the antidote to a generation of diversification. And then, building on it, came the current three-year strategy unveiled in February 2024 and branded "Next Level Sainsbury's."5 The name signals confidence — the basics are fixed, now we climb.

What does Next Level actually demand? The targets Roberts set for the period running to March 2027 are bracingly specific. The headline is £1 billion in structural cost savings, to be wrung out of the business over the course of the plan.5 This is not vague aspiration; it is a hard operational programme. The savings come from automating supply chains, redesigning store operations, and — in moves that generated plenty of headlines — closing in-store cafés and hot-food counters like the patisserie and pizza counters that had become low-return distractions from the core job of selling groceries efficiently.8 In January 2025, the company announced a restructuring of its central operations and a management reorganization explicitly aimed at this efficiency drive.8

The crucial second half of the equation is what those savings are for. Roberts isn't cutting costs to flatter short-term margins; he's recycling them into two things. The first is price — specifically, funding the "Aldi Price Match" programme that keeps hundreds of everyday Sainsbury's products pegged to discounter prices, neutralizing the very weapon that hammered the legacy grocers for a decade. The second is quality at the top end — expanding the premium "Taste the Difference" own-label range, which lets Sainsbury's capture higher-margin trade-up spending from customers who want to treat themselves. It is a barbell: match the discounters at the bottom, out-class them at the top, and use cost savings to fund both.

Now, the part long-term investors always want to understand — how is the man at the top paid, and is he aligned with shareholders? The answer at Sainsbury's is reasonably reassuring. Roberts's base salary was set at £1.00 million for the financial year 2026, with a modest 3% increase to around £1.04 million slated for FY27 — restrained for a company of this size.[^3] His total realized pay, however, reached around £5.43 million in FY26, the vast majority of which came not from salary but from performance-related bonuses and Long-Term Incentive Plans.[^3] In other words, roughly four-fifths of his pay is at risk and tied to whether the company actually delivers.

The alignment goes deeper than annual bonuses. Roberts is bound by a shareholding requirement to hold shares worth 300% — three times — his base salary, a guideline he comfortably exceeds, holding roughly 0.11% of the entire company directly.[^3] That may sound like a small percentage, but against Sainsbury's market value it represents personal skin in the game running into the millions. And he is subject to a strict post-employment holding requirement, obliging him to retain shares for two years after he leaves — a structure specifically designed to stop a departing executive from juicing short-term numbers and cashing out. It forces him to care about where the company is two years after he's gone.

Roberts has not done it alone, and the supporting cast matters. The financial architect of the recent transformation is Bláthnaid Bergin, who became Chief Financial Officer, having been appointed to the role in 2023.1 Bergin has been central to the capital-realignment story — including the bank divestment that headlines this episode — and her own alignment is substantial: she holds in the region of 466,134 ordinary shares and was awarded over 710,000 performance-linked nil-cost options under the 2024 Long-Term Incentive Plan, tying a large slice of her future wealth to the plan's success.1

Overseeing the board through this entire turbulent passage — from the post-Asda wreckage to the bank exit — has been the chairman, Martin Scicluna, a seasoned governance hand who provided stability when the company badly needed it. In a sign that the transformation chapter is maturing into something more settled, Sainsbury's formally began searching for his successor in June 2026, preparing for an orderly handover ahead of the 2027 Annual General Meeting.[^12] Succession planning of this kind, done early and openly, is exactly what long-term investors like to see — it signals a board managing its own renewal rather than lurching from crisis to crisis.

So the leadership picture is one of focus, alignment, and discipline. But all that operational rigour would be merely defensive — a story of surviving the discounters and tidying up the balance sheet — were it not for one thing. Buried inside this low-margin grocery business is an engine that earns margins more typical of a software company. And it may be the single most important reason to pay attention to Sainsbury's at all.

VII. The Hidden Engine: Nectar 360 and the Retail Media Goldmine

Here is a number that should reframe how you think about the entire grocery industry. A typical supermarket earns an operating margin somewhere in the range of 2 to 4%. That means for every £100 of groceries that pass over the scanner, the company keeps perhaps two to four pounds of operating profit before interest and tax. It is one of the most brutal business models in the developed economy — enormous revenue, microscopic margins, and a constant knife-fight on price.

Now imagine that sitting inside that grim, low-margin grocery business is a second business — one that runs at margins so high they would look at home in a Silicon Valley software company. That business is called Nectar 360, and understanding it is the key to understanding why Sainsbury's might be more interesting than its grocery numbers suggest.

Let's start with what it is, because the name is unhelpful. Nectar began life decades ago as a coalition loyalty card — one of those points schemes shared across multiple retailers, where you collected points buying petrol or groceries and redeemed them for vouchers. For years it was a fairly pedestrian marketing programme. The turning point came in 2018, when Sainsbury's bought full control of the Nectar business, taking ownership of the loyalty scheme and, far more importantly, the river of data flowing through it.[^10]

To grasp why that data is so valuable, you have to understand what a loyalty card actually does. Every time a shopper scans their card or app at checkout, they hand the retailer a perfectly detailed record of who bought what, when, where, how often, and at what price. Multiply that across millions of customers and billions of transactions, and you have something extraordinary: a real-time, first-party map of British consumer behaviour. Not a survey. Not an estimate. The actual purchases of actual people. In an advertising world that has been thrown into chaos by privacy rules and the death of third-party cookies, first-party purchase data — data the company collects directly from its own customers, with their consent — has become one of the most precious commodities in marketing.

Under Roberts, Sainsbury's took that asset and built a genuine retail-media platform around it: Nectar 360. And the scale of the underlying data is the foundation of everything. Nectar 360 draws on the purchasing behaviour of over 22 million active members, tracking real-time transactional behaviour across both Sainsbury's and Argos — meaning it sees not just what you buy for dinner but what you buy for your home.[^10]

The flywheel that supercharged this began in 2023, when Sainsbury's launched "Nectar Prices."[^10] The mechanic is simple and, frankly, a little coercive in the way all great loyalty schemes are: to get the lowest advertised price on a huge range of products, you have to scan your Nectar card or app. No scan, no discount. This was a direct lift of the playbook Tesco had pioneered with "Clubcard Prices," and it worked exactly as intended. Faced with paying more for not scanning, shoppers scanned. The result was a roughly 35% year-on-year surge in digitally active Nectar users, which is to say a 35% surge in the richness and breadth of the first-party data Sainsbury's was collecting.[^10] Every shopper chasing a discount was, in effect, volunteering to be measured.

So now you have the data. How do you turn it into those software-like margins? You sell access to it — carefully, and to people desperate to buy it. Nectar 360 packages this purchasing data and sells advertising and insight services to over 900 global brands and media agencies.[^10] Think about who those advertisers are: the Procter & Gambles, the Unilevers, the Coca-Colas of the world — the consumer-goods giants whose products line the supermarket shelves. These companies spend billions trying to figure out whether their advertising actually causes anyone to buy anything. Nectar 360 can answer that question with a precision that traditional advertising can only dream of.

Here's the magic, and it's worth slowing down on because it's the whole point. A brand can buy a targeted ad — say, a discount on a particular cereal aimed specifically at households that buy a competitor's cereal — and place it on Sainsbury's digital app, or on one of the more than 2,500 in-store digital screens the company has deployed across its estate.[^14] And then Nectar 360 can do the thing that breaks open the value: it can match that ad exposure back to the checkout and tell the brand, with hard data, whether the people who saw the ad actually bought the product. This is the holy grail of advertising — "closed-loop" measurement, proof that the marketing pound translated into a sale. For decades, brands lived by the old lament that they knew half their advertising was wasted but didn't know which half. Nectar 360 sells them the answer.

This is why the margins are so different from groceries. Selling an advertising slot or a data-insight subscription carries almost no incremental cost — the data already exists, the screens are already installed, the app already runs. Nearly every additional pound of retail-media revenue drops toward the bottom line. It is, functionally, a high-margin software-and-advertising business wearing a supermarket's clothing.

The financial ambition reflects that. Sainsbury's has targeted delivering over £100 million in incremental profit from Nectar 360 by March 2027.[^10] To feel the weight of that number, remember the grocery margin math. To generate £100 million of profit selling food at, say, a 3% margin, you'd have to sell something on the order of £3 billion of additional groceries — an almost inconceivable volume increase in a saturated market. Nectar 360 can generate comparable profit by selling data and ads off a cost base that's already paid for. That is what operating leverage looks like, and it is why retail media has become the obsession of every major grocer on earth.

Nectar 360 is the crown jewel, but it isn't the only "hidden" business tucked inside the supermarket. Two others deserve a mention. The first is Tu Clothing, Sainsbury's own-brand fashion line, which is sold inside the supermarkets themselves. By riding on the enormous footfall of grocery shoppers and paying essentially zero standalone retail rent — the rails sit in space the company already occupies — Tu has quietly grown into one of the UK's largest clothing brands by volume. It is the Argos co-location logic applied to fashion: monetize space you already own with a higher-margin product.

The second is Smart Charge, Sainsbury's venture into ultra-rapid electric-vehicle charging. The strategic insight here is, once again, about real estate. Sainsbury's owns hundreds of prime sites with large car parks in exactly the locations where people want to charge their cars while they do something else — like a weekly shop. By installing high-margin rapid chargers on land it already controls, Sainsbury's turns parking spaces into a growing energy-retail business and gives customers another reason to choose its stores. It's early, but it's a textbook example of squeezing optionality out of a cornered asset.

All of which raises the question that should anchor any long-term analysis of this company. In a sector this brutal, what is it that actually protects Sainsbury's? Where are the moats — and where are the cracks? To answer that, we need to war-game the whole British grocery battlefield.

VIII. War Games: The Moats and the Battlefield

Strip away the branding and the marble-counter heritage, and the question every long-term investor must answer about Sainsbury's is coldly structural: in one of the most competitive industries on the planet, what stops the profits from being competed away? The best tools for this are Hamilton Helmer's 7 Powers — a framework for identifying genuine, durable competitive advantages — and Michael Porter's classic Five Forces. Let's run Sainsbury's through both, honestly, including where the moats are shallow.

Start with scale economies, the first of Helmer's powers — the advantage that comes from spreading fixed costs over greater volume. Here Sainsbury's verdict is moderate, not dominant. The uncomfortable truth is that in pure grocery, Tesco is the scale king, commanding roughly 28% of the UK market against Sainsbury's roughly 15.2% — a clear and durable number-two position, but a number-two position nonetheless.6 That gap matters: Tesco's greater volume gives it superior buying power with suppliers and more fixed costs to spread. Where Sainsbury's claws back an edge is in non-food. The Argos acquisition handed it general-merchandise scale economies — in sourcing, logistics, and fulfilment — that smaller rivals like Morrisons and the post-buyout, debt-laden Asda simply cannot match. So Sainsbury's scale power is real but uneven: a follower in food, a leader in the general-merchandise niche it carved out.

The strongest arrow in the quiver is the second power, the cornered resource — and for Sainsbury's, that resource is real estate. Britain is not America; it cannot simply bulldoze farmland and erect a hypermarket. The Town and Country Planning Act and the country's notoriously restrictive zoning regime make it extraordinarily difficult and slow to win permission for new large-format stores, especially in the dense urban and suburban catchments where the most valuable customers live. Sainsbury's existing network of prime, well-located stores is therefore something close to irreplaceable — a portfolio that could not be rebuilt from scratch at any reasonable cost, because the planning permissions to build it largely cannot be obtained anymore. This is a genuine, high-power moat, and it is precisely what makes the company's property estate so strategically valuable even after the Space Race left it overbuilt. The same land that was a liability when half-empty becomes a fortress when it's the only land you're allowed to trade from.

Third, switching costs — and here the assessment is moderate but rising. Classic theory says groceries have near-zero switching costs; a shopper can defect to the Tesco across the road tomorrow. But loyalty mechanics complicate that. The longer a customer uses Nectar Prices and accepts personalized app offers, the more the system learns their habits and feeds them tailored discounts on the exact products they buy. Walking away means abandoning an accumulated stream of personal savings and starting from scratch with a rival's algorithm. It's a soft lock-in — psychological and financial rather than contractual — but in a market where margins are decided at the margin, even a soft tether on millions of shoppers is worth a great deal.

Fourth, and most exciting, network effects — which in Sainsbury's case live almost entirely inside the retail-media engine we just dissected. Nectar 360 is a genuine two-sided marketplace, and it exhibits a real flywheel: more active loyalty members generate more transactional data; more data attracts more brand advertising spend; more advertising revenue funds better personalized discounts; better discounts attract and retain more members. Round and round it goes, each turn strengthening the next. This is the one place in the business where Sainsbury's has something resembling a tech-platform dynamic rather than a retail one. It's still early and the power is best described as low-to-moderate today, but it is the part of the moat most capable of deepening over time rather than merely holding.

Fifth, counter-positioning — the power that nearly killed the legacy grocers, now substantially neutralized. Counter-positioning is what happens when a new entrant adopts a business model that incumbents cannot copy without damaging their existing business. The discounters wielded it brilliantly: their low-SKU, bare-bones, own-label model was something Sainsbury's couldn't imitate without cannibalizing its own higher-margin range and confusing its quality positioning. For years this was a one-way assault. But Sainsbury's found an answer in "Aldi Price Match," surgically matching the discounters on hundreds of the highest-volume everyday items while leaving the rest of its proposition intact, and funding the price gap out of the £1 billion cost-savings programme. It didn't beat the discounters' model; it defused the specific weapon — taking the price reason to defect off the table for the items shoppers price-check most. The counter-positioning power that once threatened to be fatal has been eroded to something manageable.

Now flip to Porter, which looks not at a single company's advantages but at the structural attractiveness of the industry — and UK grocery is, by Porter's lens, a famously difficult place to earn returns.

Rivalry among existing competitors is extreme — arguably the defining feature of the sector. Tesco, Sainsbury's, Asda, Morrisons, and the two German discounters are locked in continuous, brutal price competition, with every player matching, undercutting, and advertising against the others week after week. This is the force that keeps grocery margins pinned to the floor and explains why operational excellence, not pricing power, is the name of the game.

The threat of new entrants is low, which is the industry's saving grace. Building a national grocery business from scratch would require constructing supply chains, distribution networks, and a store estate — and, as established above, acquiring the planning permissions to build that estate is close to impossible. The capital and time barriers are immense. The real "new entrants" of the last two decades weren't startups; they were the deep-pocketed German discounters who simply imported a proven model and out-spent everyone on patience.

The bargaining power of suppliers is low to moderate. Against the consumer-goods brands, the supermarkets hold the whip hand — control of shelf space is control of access to the customer, and a brand that loses its facings in Sainsbury's loses millions in sales. But the power is not absolute. Agricultural inflation and supply-chain shocks have, at times, handed fresh-food producers and farmers some leverage, particularly on staples where supply is genuinely constrained and consumers notice empty shelves.

The bargaining power of buyers is high. Shoppers face minimal switching costs, can compare prices instantly online, and have more grocery options within reach than ever — a structural reality that the soft loyalty lock-in only partly offsets. The customer, ultimately, holds enormous power, and that power is exactly why the rivalry stays so vicious.

The threat of substitutes is moderate and evolving. The traditional weekly shop now competes with rapid-delivery apps and meal-kit services like HelloFresh, which offer convenience the big shop can't, alongside food delivery and dining out. None of these has displaced the core grocery trip, but collectively they nibble at share of stomach and force the incumbents to invest in their own convenience and delivery propositions.

Put it all together and you get a clear-eyed picture. UK grocery is a structurally tough, low-margin, fiercely competitive industry where the dominant force is rivalry and the dominant defensive asset is irreplaceable real estate. Sainsbury's competitive position within it rests on three genuine pillars — its cornered property estate, its non-food scale through Argos, and the budding network effects of Nectar 360 — partly offset by its permanent number-two status in core grocery and the relentless power of price-sensitive buyers. It is not a fortress with a single deep moat; it is a well-defended position held together by several moderate ones and one potentially deepening platform.

That assessment sets up the practical questions any investor should carry forward — the lessons of the Sainsbury's transformation, and the few metrics that actually reveal whether the strategy is working.

IX. The Playbook

Step back from the blow-by-blow, and the Sainsbury's story of the last decade offers a handful of lessons clean enough to carry into the analysis of almost any large, mature company facing disruption.

The first is the scale illusion versus operational excellence. The blocked Asda merger is the cautionary tale at the heart of this story. Sainsbury's bet its forward strategy on the idea that bigger is automatically better — that consolidating to number one would solve its competitive problems. The CMA's rejection didn't just block a deal; it exposed the flaw in the logic. Scale pursued through defensive mega-mergers runs straight into antitrust walls, and even when it doesn't, it often destroys more value in integration risk and distraction than it creates. What actually rebuilt Sainsbury's was the opposite instinct: organic volume growth, capital efficiency, and obsessive operational improvement. The lesson for operators and investors alike is to be deeply skeptical of "transformational" M&A pitched as a substitute for getting better at the core business.

The second is retail media as a margin engine — and more broadly, the recognition that the most valuable asset inside a legacy company is often not on its balance sheet. For years, Sainsbury's thought of itself as a merchant: it bought goods, marked them up, and sold them. The Nectar 360 insight was that it was also, all along, a data network — sitting on a uniquely valuable record of consumer behaviour that could be monetized at software-like margins. The broader lesson is to look at mature, low-margin businesses and ask what proprietary data, attention, or distribution they control that could be turned into a high-margin second act. The grocery aisles fund the data machine; the data machine may ultimately drive the returns.

The third is the discipline of divestment — the willingness to pay to exit. The bank transaction is the textbook case. The instinct of most management teams, faced with a sub-scale division they built and named, is to defend it, to wait for it to turn around, to fall victim to the sunk-cost fallacy. Sainsbury's did the harder, smarter thing: it recognized that the bank was consuming capital it could deploy better elsewhere, and it paid a premium to be rid of it cleanly. Knowing what not to own — and being willing to spend money to achieve focus — is as much a part of great capital allocation as knowing what to buy.

The fourth is asset co-location — the Argos store-in-store model. The deepest lesson here is that enormous financial value can be unlocked without building anything new, simply by changing the product mix and use of real estate you already control. Sainsbury's didn't construct a new logistics empire to fight Amazon; it slotted Argos into the dead corners of stores it already operated and watched the synergies compound. Tu Clothing and Smart Charge are the same idea in different clothes. For any asset-heavy business, the question "what else could this space do?" can be worth more than any greenfield expansion.

These four lessons share a common spine: focus, capital discipline, and the creative monetization of assets you already own. Which leads naturally to the final question — given all this, what should an investor actually watch?

X. Epilogue: The Czech Billionaire and the Road to 2027

In the closing months of 2025 and into early 2026, a new name began climbing the Sainsbury's share register, and it was not one the City had expected. Daniel Křetínský — the Czech billionaire whose growing portfolio of European industrial, energy, and retail assets had earned him the nickname "the Czech Sphinx" for his inscrutable dealmaking — was building a position through his Vesa Equity investment vehicle. By early 2026, that stake had reached 10.00%, making Vesa the single largest shareholder in J Sainsbury plc.7

His ascent was all the more striking for whom he overtook. For nearly two decades, the largest strategic shareholder in Sainsbury's had been the Qatar Investment Authority — the sovereign wealth fund of Qatar, which had first built a position back in the late 2000s and at one point held close to 20% of the company, even mounting a takeover approach during the buyout boom years. By the time Křetínský arrived at the top of the register, the Qatari fund had scaled its long-held position back to 6.82%, ceding the top spot it had occupied for years.7

What does Křetínský's emergence mean? That is the open question hanging over the company. He has a track record of taking significant stakes in undervalued, asset-rich Western businesses — he is a major shareholder in the UK's Royal Mail parent and in various retail and energy names across Europe — and the obvious speculation is whether his interest presages a fuller takeover approach, a push for a breakup of Sainsbury's prized property estate, or simply a patient value investment in a company he believes the market has underrated. For long-term shareholders, his presence is a double-edged catalyst: it puts a sophisticated, deep-pocketed owner on the register who clearly sees value, but it also raises the prospect of strategic upheaval, leverage, or financial engineering that may or may not align with existing investors' interests. The arrival of a concentrated, activist-capable holder of this size is precisely the kind of ownership shift that warrants close attention.

Set against that backdrop, the operational story comes down to whether Simon Roberts can deliver the Next Level numbers. The targets for March 2027 are unambiguous: £1 billion in structural cost savings, and a goal of generating around £1.6 billion in retail free cash flow over the course of the plan — the genuine cash thrown off by the core retail business after the investment needed to keep it running.5 Hitting those numbers would validate the entire post-Asda strategy: that focus and operational excellence, not scale-by-merger, were the right path. Missing them would reopen every question about whether a number-two grocer can really out-execute its way to durable returns in so brutal an industry.

And the second open question is whether Nectar 360 can keep scaling toward — and beyond — that £100 million incremental profit target, growing into a standalone profit powerhouse rather than a useful sideline. If it can, the investment thesis shifts: Sainsbury's stops looking purely like a low-margin grocer and starts looking like a grocer with a high-margin data business attached, deserving of a different valuation lens entirely.

For investors trying to cut through all of this, the signal-to-noise ratio is best on a small number of metrics. The most important is like-for-like grocery sales growth versus the market — the cleanest read on whether Sainsbury's is actually winning or losing share against Tesco and the discounters, and the truest test of whether the Aldi Price Match and quality strategy is working. The second is the trajectory of Nectar 360 profit — the proof of whether the high-margin engine is genuinely scaling. And the third is retail free cash flow and the progress on the £1 billion cost programme — the evidence of whether the operational discipline is converting into the cash that ultimately funds dividends, buybacks, and reinvestment. Track those three, and you are tracking the heart of the story. Margin, market share, and the data machine: everything else is detail.

It is a long way from a butter-and-eggs counter on Drury Lane in 1869. The Victorian shop that sold quality and trust to a grubby London street survived the rise of the self-service supermarket, the concrete excess of the Space Race, the digital revolution, and the German discount invasion that humbled half its peers. It tried to become a conglomerate and a financial-services group, and it had the discipline to retreat from both. What emerged is leaner, sharper, and more focused than it has been in a generation — a 157-year-old retailer that finally understands its most valuable asset was never the bank or the buildings, but the relationship it has with the millions of British baskets it fills every single week, and the data that relationship throws off. Whether that is enough to thrive, rather than merely survive, in the most competitive grocery market on earth is the question the next three years will answer.

References

-

J Sainsbury plc Annual Report 2025 — J Sainsbury plc, 2025-06-05 ↩↩↩↩

-

Sainsbury's Acquires Home Retail Group (Argos) for £1.4bn — London Stock Exchange, 2016-04-01 ↩↩

-

Sainsbury's Agrees Sale of Core Banking Business to NatWest — Reuters, 2024-06-20 ↩↩↩↩

-

NatWest Acquisition of Sainsbury's Bank Portfolio Receives High Court Approval — Retail Banker International, 2025-04-15 ↩

-

Next Level Sainsbury's Strategy Launch Presentation — J Sainsbury plc, 2024-02-07 ↩↩↩

-

Kantar Worldpanel UK Grocery Market Share Data — Kantar, 2026-05-19 ↩

-

Czech Billionaire Daniel Kretinsky Becomes Largest Sainsbury's Shareholder — Financial Times, 2026-01-12 ↩↩

-

Sainsbury's Announces Restructuring of Central Operations and Management Reorganization — J Sainsbury plc, 2025-01-28 ↩↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube