Sanofi: The Blockbuster Transition

I. Introduction: The €100 Billion Identity Crisis

On the morning of October 27, 2023, traders in Paris watched something that almost never happens to a €100 billion pharmaceutical company: it broke. In a single session, shares of Sanofi, France's largest drugmaker and one of the crown jewels of the CAC 40, collapsed roughly 19% intraday, closing down about 15.5% and wiping out on the order of €20 billion in market value—the worst day in the stock's modern history.12

What made the crash so unsettling was that nothing had actually broken. There was no failed Phase III trial, no product recall, no accounting scandal, no earnings miss of any consequence. What detonated the stock was a sentence. On the Q3 2023 call, CEO Paul Hudson quietly abandoned the company's long-promised target of a 32% operating margin for 2025 and announced instead that Sanofi would pour that money into research and development to "fully realize" its pipeline.3 To a French investor base that had spent years being told this company was finally learning cost discipline, it sounded like a bait-and-switch. The market's verdict was brutal and immediate.

That single trading session is the perfect entry point into Sanofi, because it captures the company's oldest tension in one afternoon. On one side sits the scientist's argument: pharma is a business where the only thing that ultimately matters is discovering medicines, and discovering medicines means spending, patiently, on research whose payoff is years away and impossible to schedule. On the other side sits the investor's argument: capital is not free, promises are a form of currency, and a management team that abandons a number it repeated for years has told you something about how much its future numbers are worth. Both arguments are correct. The art of running a drug company—the art Sanofi has struggled with for its entire modern existence—is holding both in your hands at once. On October 27, 2023, Hudson dropped one of them.

Fast-forward to the middle of 2026 and the picture has been reshuffled entirely. Hudson is gone—his mandate not renewed by the board in February 2026, his exit sweetened by a multi-million-euro package.4 In his place stands Belén Garijo, a Spanish physician-turned-executive and one of the most respected operators in European pharma, who took the reins at the close of the annual meeting on April 29, 2026.5 And the company has just completed the most dramatic act of corporate surgery in its history: it carved out Opella, its consumer-health arm and the maker of France's beloved Doliprane, selling control to an American private-equity firm at a €16 billion valuation.6

Here is the paradox that makes Sanofi such a fascinating study. This is a company that was not born in a laboratory. It was conceived inside a state-owned oil company as a diversification play, grew up through hostile takeovers and government-brokered mega-mergers into a sprawling French "national champion," and then—almost by accident of a 2007 partnership with a scrappy New York biotech—found itself sitting on one of the best-selling drugs in the history of medicine. Today more than a third of its revenue flows from a single molecule, Dupixent. The strategic question that hangs over everything Garijo now touches is deceptively simple: can a company defined by one spectacular asset build a future that does not depend on it?

To make sense of the company that trades today, it helps to hold two frames at once. The first is corporate: Sanofi in 2026 is essentially two businesses stapled together—a biopharma engine dominated by immunology and anchored by Dupixent, and a vaccines franchise built around infant protection—with the consumer-health division now spun out and the diabetes and cardiovascular heritage deliberately run down. The second frame is temperamental: this is a company perpetually caught between the scientist's patience and the investor's impatience, between the ambition to lead the world in immunology and the obligation to serve as a French national champion. Nearly every event in its history is a negotiation between those poles.

This is the story of how it got here—from oil diversification to corporate warfare, from the Genzyme masterstroke to the Regeneron golden ticket, through the October 2023 R&D "bloodbath" and the politically explosive Opella sale, to the leadership reset under Belén Garijo and the bull-and-bear case for Sanofi's next chapter. It is, at bottom, a story about the difference between owning a great asset and running a great business, and about whether Sanofi can finally make the two coincide.

II. The Strange Genesis: Oil, Hostile Mergers, and the Rollup Machine

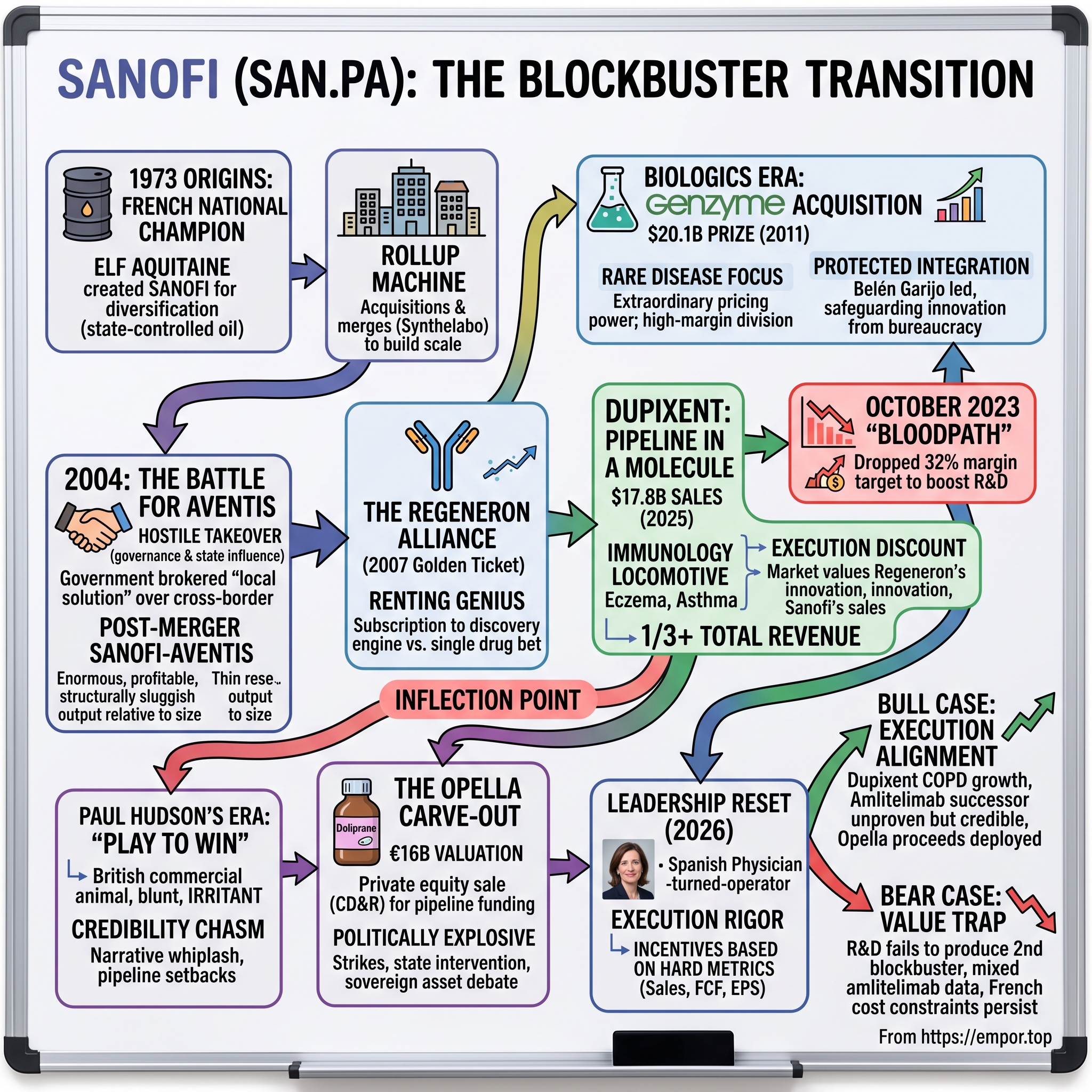

Most great drug companies trace their origins to a chemist and a bench. Sanofi traces its origins to a barrel of oil. In 1973, the French state-controlled oil group Elf Aquitaine created a subsidiary to diversify beyond hydrocarbons, and that subsidiary—cobbled together from pharma, cosmetics, and health assets—was named Sanofi.7 This was industrial policy dressed up as corporate strategy. France in the 1970s wanted a domestic healthcare champion, a company that could keep the nation self-sufficient in medicine the way Elf kept it supplied with fuel. From day one, then, Sanofi carried a political gene: it existed partly to serve French national interest, and that gene would shape—and constrain—its behavior for the next half-century.

There is something almost quaintly French about the setup. In the American model, a biotech is founded by a scientist with an idea and a garage; in the French model of the 1970s, a pharmaceutical company is created, top-down, by an oil conglomerate acting on the wishes of the state, as an instrument of national self-sufficiency. Sanofi did not begin with a molecule it was desperate to bring to patients. It began with a mandate. That distinction matters, because a company assembled to serve a strategic purpose tends to grow by acquisition rather than by discovery—and Sanofi did exactly that, accumulating brands, businesses, and eventually whole competitors rather than betting the house on its own laboratories. The rollup instinct was baked in at birth.

For its first two decades Sanofi behaved less like a research house than like a rollup machine, bolting on brands and businesses across pharmaceuticals, beauty, and even, at various points, ventures far from medicine. The defining move of its coming-of-age arrived in 1999, when Sanofi merged with Synthélabo—a pharmaceutical company controlled by cosmetics giant L'Oréal—to create Sanofi-Synthélabo, a mid-sized but nimble player with real drugs, real cash flow, and, crucially, two of the products that would define its next decade: the anti-clotting agent Plavix and the sleep drug Ambien. It was a marriage of two French houses, and it set the stage for something far larger. What Sanofi-Synthélabo lacked was scale. In an industry consolidating into a handful of global titans, a mid-cap French player looked like prey. It decided to become a predator instead.

The Battle for Aventis

Across the Rhine and along the Seine, a parallel consolidation had produced a giant. Germany's Hoechst and France's Rhône-Poulenc had merged their pharma operations to create Aventis, a sprawling Franco-German behemoth with a vast research footprint, a heavy chemical heritage, and the high-cost, heavily unionized culture that came with both. Aventis was bigger than Sanofi-Synthélabo. That did not stop the smaller company from trying to swallow it.

In January 2004 Sanofi-Synthélabo launched an unsolicited, hostile exchange offer for Aventis—initially valued at roughly €47.8 billion—in one of the largest and most theatrical takeover battles Europe had ever seen.8 Aventis fought back exactly as a cornered incumbent does: it dismissed the bid as inadequate, reached for poison-pill defenses, and courted a white knight in the form of Swiss giant Novartis. A cross-border deal with Novartis would have been the commercially logical outcome.

It never happened, and the reason is the most French thing in this entire story. The government of Jacques Chirac wanted what it openly called a "local solution." A Swiss takeover of Aventis—a company with deep French roots—was politically intolerable in Paris, where pharmaceutical sovereignty was treated as a matter of national security. So the state leaned on the scales. Paris pressured Aventis to reject the Swiss suitor and pushed Sanofi-Synthélabo to raise its bid, effectively engineering the outcome.8 The message to Novartis was unmistakable: this asset is not for sale to you at any price. In April 2004 the hostility dissolved into a friendly agreed deal worth roughly €54.5 billion, and Sanofi-Aventis was born—instantly one of the largest pharmaceutical companies on earth.8

Read that sequence carefully, because it is the single most important precedent in the company's history. A smaller French firm swallowed a larger one not purely on the merits, but because the state decided a foreign owner was unacceptable and used its influence to make sure a domestic solution prevailed. Every investor who has ever tried to model Sanofi's freedom of action runs into this wall: the company operates inside a country that regards it as a strategic national asset, and that country has demonstrated, in the most consequential deal of Sanofi's life, that it will intervene. The 2004 battle was not an aberration. It was the template.

The state had delivered its champion. But the victory came with a bill that would be paid in slow motion for the next two decades. Sanofi-Aventis inherited overlapping research sites scattered across multiple countries, a bloated and politically protected European cost base, thousands of employees whose positions were shielded by some of the world's most stringent labor protections, and a bureaucratic culture in which capital moved cautiously and cost-cutting collided with the law at every turn. Integration of two companies this size is hard everywhere; in France, where any large restructuring triggers formal consultation, negotiation, and often strikes, it is a multi-year siege. The company that emerged was enormous, profitable, and structurally sluggish—a national champion in the fullest sense, with all the strategic baggage the title implies. Its research output, for all the money flowing through it, was thin relative to its size. To become a modern innovator, Sanofi would eventually have to learn to buy science it could not invent, and—harder still—to protect that science from the bureaucratic machine that had bought it.

III. The Rare Disease Pivot: Genzyme and the Re-entry of Belén Garijo

By 2010 the champion had a demographic problem, and it was ugly. Sanofi-Aventis's profits leaned heavily on aging small-molecule blockbusters—above all Plavix, the anti-clotting drug that was one of the best-selling medicines in the world, and Lantus, its long-acting insulin franchise. Both faced looming patent expiry, the pharmaceutical equivalent of a cliff edge: the day generics arrive, revenue that took decades to build can evaporate in quarters. This is the recurring nightmare of the pharmaceutical business model, and it is worth dwelling on, because it explains almost every strategic decision Sanofi has made since. A drug patent is a temporary monopoly. During the patent's life, a successful medicine can earn margins that would make a software company blush. The moment it expires, generic manufacturers—who bore none of the research cost—flood in at a fraction of the price, and 80–90% of the revenue can vanish within a year or two. Every large pharma company is therefore permanently running up a down escalator, forced to discover new drugs fast enough to replace the ones about to fall off the cliff. In 2010, Sanofi was staring down two of the biggest cliffs in its history at once, and its own labs were not producing enough to fill the hole.

The answer was biology. Where a small-molecule pill can be copied atom-for-atom by any competent chemist, a biologic—a complex protein grown in living cells—is fiendishly hard to reverse-engineer, which gives it far more durable pricing power even after patents lapse. And no company embodied the promise of high-value biologics better than Genzyme, the Boston-based pioneer of rare-disease medicine.

A Wounded Target

Here is the detail that made the deal possible, and that most retellings omit: Sanofi did not pounce on Genzyme at the height of its powers. It pounced on a company in crisis. In 2009, a viral contamination—Vesivirus 2117—was discovered in a bioreactor at Genzyme's flagship Allston Landing manufacturing plant in Boston, forcing a temporary shutdown that crippled production of its most important drugs, Cerezyme and Fabrazyme, and triggered rationing for patients who depended on them.20 The manufacturing crisis deepened when regulators later found foreign particles—bits of steel, rubber, and fiber—in several Genzyme products, and the company ultimately signed a consent decree.20 The stock cratered, and a wounded Genzyme became exactly the kind of target activist investor Carl Icahn hunts. Icahn built a stake and waged a proxy fight, winning board seats in an agreement reached in 2010 and turning up the pressure on management to sell.21 By the time Sanofi came calling, Genzyme's board was cornered on multiple fronts.

That context reframes the acquisition. It was not simply a visionary bet on rare-disease biology; it was an opportunistic strike on a great franchise made temporarily cheap by operational failure. Genzyme resisted Sanofi's initial approaches as too low, which is why the final structure included a contingent value right—a form of "we'll pay you more if the assets perform" that bridged the gap between what Genzyme thought it was worth and what Sanofi would pay for a company still fixing its factories.

The $20.1 Billion Prize

In February 2011, after that drawn-out pursuit, Sanofi-Aventis agreed to acquire Genzyme for $74.00 a share in cash—approximately $20.1 billion—plus the contingent value right tied to milestones for Genzyme's multiple-sclerosis drug and to production recovery for its flagship enzyme therapies.9 The prize was Genzyme's portfolio of enzyme-replacement therapies for ultra-rare inherited disorders—drugs like Cerezyme for Gaucher disease and Fabrazyme for Fabry disease. For the handful of patients who need these medicines, there is often no alternative on earth; the "switching cost," to borrow Hamilton Helmer's language, is life itself. A patient stabilized on an enzyme-replacement therapy does not shop around, and no insurer refuses to cover a treatment for a fatal inherited disease with no substitute. That translates into extraordinary pricing power and revenue that is almost recession- and generic-proof—the closest thing pharma has to an annuity. The deal established what became Sanofi's high-margin Specialty Care division and, more broadly, announced that the company intended to buy its way into the biologics era.

But the deal's real significance for this story is not financial. It is the moment it introduced a particular executive to the top of Sanofi's culture. Genzyme was a fragile thing: an innovative, patient-obsessed, entrepreneurial American biotech now owned by exactly the kind of slow-moving European bureaucracy most likely to crush it. The job of integrating Genzyme without killing what made it valuable fell in large part to Belén Garijo, then a senior Sanofi executive who led the integration effort.5

Garijo's approach—protect Genzyme's operational autonomy while plugging it into Sanofi's global scale—is now cited as a case study in how not to destroy an acquired culture. The instinct of a large bureaucracy absorbing a smaller, faster company is to "harmonize" it: impose the parent's systems, processes, reporting lines, and pace, and in doing so strangle the very qualities that made the target worth buying. Garijo resisted that instinct. She ring-fenced what worked at Genzyme and connected it to Sanofi's scale where scale genuinely helped—manufacturing recovery, global commercial reach, regulatory muscle—without smothering its scientific and commercial autonomy. It worked, and it cemented her reputation inside the company as someone who could make the machine bend without breaking the thing it had swallowed.

Fifteen years later, when the board went looking for a CEO who understood both Sanofi's DNA and the discipline it lacked, that reputation would matter enormously—it is the thread that connects Section III to Section VII of this story, and it is why her eventual appointment felt less like a gamble than a homecoming. In 2011, in a smaller act of housekeeping, the company also dropped the hyphenated "Sanofi-Aventis" and rebranded simply as Sanofi—a cosmetic change that nonetheless signaled the ambition to stop being a collection of mergers and start being a single company. The bigger transformation, though, had already begun a few years earlier, in an unglamorous partnership with a New York biotech that almost nobody in Paris had heard of—a deal that would eventually dwarf even Genzyme in its importance.

IV. The Golden Ticket: The Regeneron Alliance and the Dupixent Miracle

In November 2007, while the financial world was busy inventing the crisis that would nearly end it, Sanofi-Aventis signed a deal that would quietly become the most valuable decision in its modern history—and it barely made headlines. The counterparty was Regeneron, a New York biotech founded by a physician, Leonard Schleifer, and led scientifically by the brilliant George Yancopoulos, with a proprietary antibody-discovery platform and a market capitalization a fraction of Sanofi's. Under the alliance, Sanofi took a large equity stake in Regeneron—raising its holding to roughly 19% by buying newly issued shares—and agreed to fund antibody-discovery research, initially at around $100 million a year and later rising above $160 million, in exchange for the right to co-develop and share profits on the antibodies that emerged.10

The genius of what Sanofi bought was not a drug; it was a machine for making drugs. Regeneron's platform, marketed under the name VelociSuite and including a technology called VelocImmune, is essentially an industrialized method for generating fully human antibodies quickly and reliably. Think of it as the difference between a single artisan hand-carving one chair and a factory that can produce a new, custom-designed chair on demand. Most biotech partnerships are a bet on one molecule. Sanofi's bet on Regeneron was a bet on a process—a subscription to a discovery engine that could keep producing candidates year after year. When you are a company whose own labs have disappointed relative to their size, renting the best discovery engine in the business is a rational, even inspired, move.

The economic architecture is worth understanding because it explains both the fortune Sanofi made and the discount Wall Street later slapped on it. Sanofi funded the lion's share of clinical development up front; profits on jointly developed drugs were split roughly evenly in the US and on a sliding scale abroad, with Sanofi's share of ex-US profit ranging higher; and—crucially—Sanofi books 100% of global product sales on its own income statement, then shares the profit with Regeneron.10 This accounting quirk matters more than it sounds. It means Sanofi's revenue line looks enormous, but a large slice of the underlying economics belongs to a partner who does not appear in that headline number. It is a structure that flatters the top line and complicates the bottom—and, as later sections show, it seeds a permanent question in investors' minds about how much of Sanofi's biggest success actually accrues to Sanofi.

A Pipeline in a Molecule

Out of that platform came dupilumab, sold as Dupixent. To understand why it matters, you need one idea about the immune system. A large family of allergic and inflammatory diseases—eczema, asthma, nasal polyps, and more—are driven by the same underlying "type 2" inflammatory pathway, orchestrated by two signaling molecules called IL-4 and IL-13. Dupixent blocks the shared receptor those two molecules use. Turn off that one switch, and you can calm a startling range of seemingly unrelated diseases at once. That is why the drug is often described as a "pipeline in a molecule": a single antibody that keeps unlocking new indications.

And unlock them it did. Dupixent launched first in atopic dermatitis—moderate-to-severe eczema, a miserable, itch-dominated disease with few good options—then marched through asthma, chronic rhinosinusitis with nasal polyps, eosinophilic esophagitis, prurigo nodularis, and, in the pivotal expansion, chronic obstructive pulmonary disease (COPD), a vast market it entered in 2024–2025. The COPD approval deserves emphasis because of the sheer size of the opportunity: COPD is one of the leading causes of death worldwide, afflicting hundreds of millions of people, and until Dupixent no biologic had cracked it. Sanofi and Regeneron had spent years and a fortune trying to prove that the same type-2 inflammation switch mattered in a subset of COPD patients, and when the data came through, it opened a market larger than all of Dupixent's previous indications combined. Each new indication, remember, added a new population of patients without the cost and risk of inventing a new drug—the economic definition of a pipeline in a molecule.

The financial result is one of the great commercial ramps in pharmaceutical history. In full-year 2025 Dupixent generated $17.8 billion in global net sales, up 26% year over year—growth of that magnitude on a base that large is almost unheard of for a drug nearly a decade past launch.11 By 2025 Dupixent alone represented more than a third of Sanofi's total revenue and was, by a wide margin, its single largest source of profit and cash. In Helmer's 7 Powers framework the drug rests on a cornered resource—co-ownership of a best-in-class immunology antibody with patent protection—reinforced by the scale economies of high-volume biologic manufacturing and Sanofi's global commercial sales force.

Yet the very structure that produced the miracle also produced a curse—a strategic asymmetry that has shadowed Sanofi's valuation for a decade. Because Regeneron is widely seen as the scientific brain and Sanofi as the commercial muscle, the market has tended to award the innovation credit—and the premium multiple that comes with being viewed as an inventor rather than a distributor—to Regeneron, while treating Sanofi as the sales organization that happens to book the revenue. This is more than a matter of perception. A pure-play US biotech with a hit drug and a productive platform trades at a rich multiple because investors are paying for its future discoveries; a sprawling European conglomerate that shares the economics of its biggest drug and cannot fully control its own narrative trades at a discount because investors are paying mainly for the drugs it already has.

The relationship has not always been harmonious, either. The two partners have at times been openly at odds, including litigation over commercial transparency in the collaboration—a reminder that a 50/50 profit split between a scrappy inventor and a giant marketer contains permanent, structural friction over who is doing the real work and who is capturing the value.12 The upshot is what analysts call Sanofi's "execution discount": a genuinely great asset, owned in part, run by a company the market has never been sure it fully trusts to convert scientific promise into shareholder return. Closing that trust gap—proving that Sanofi could be seen as an innovator and an operator rather than merely a distributor—became the central obsession of the man Sanofi hired in 2019 to shake the place awake.

V. The Paul Hudson "Play to Win" Era & The October 2023 Bloodbath

When Paul Hudson arrived as CEO in September 2019, he was, by the standards of French corporate life, an alien. He was British, blunt, and a pure commercial animal—he had run Novartis Pharmaceuticals from 2016, sat on that company's executive committee, and before that spent years at AstraZeneca with postings across the US, Japan, and Europe.22 He was not a scientist by training and not a product of the French establishment, and that was precisely the point. The board hired him to be an irritant: to break the polite, consensus-driven, cost-tolerant culture that the national-champion history had baked in, and to drag a sprawling conglomerate toward the focus that modern pharma demands. In December 2019, months after arriving, he unveiled the strategy that would define his tenure: "Play to Win," built on four stated priorities—focus the portfolio, lead with science, accelerate efficiency, and reinvent how the company works.22 To organize the effort, he restructured Sanofi into three global business units—Specialty Care, Vaccines, and General Medicines—and cordoned off Consumer Healthcare as a standalone unit, a structural choice that, in hindsight, was the first quiet step toward the Opella carve-out.22

The Triage

Hudson's central bet was focus. Sanofi, he argued, had spread itself across too many therapeutic areas, funding mediocre programs out of sentiment and habit rather than scientific conviction. So he made a decision that would have been unthinkable a decade earlier: he pulled Sanofi out of R&D in diabetes and cardiovascular disease—the company's historical heartland, the very franchises that Plavix and Lantus had built—to concentrate firepower on immunology and vaccines, where Dupixent had shown what winning looked like. To appreciate how radical this was, imagine a company walking away from research in the exact fields that made it famous, in a country where those franchises employed thousands. It was a genuine act of strategic courage, killing the past to fund the future—and the early results were encouraging enough that, for a couple of years, Hudson looked like the disruptor the board had ordered.

The problem was never the strategy. It was the sequencing, and the promise.

For years Hudson had also been selling investors on operational discipline, anchored by a concrete, memorable number: a 32% business operating margin by 2025. That target was the handshake, the thing that told a skeptical market this leopard had changed its spots. Then, on the Q3 2023 earnings call on October 27, he let go of it.3 Sanofi would instead accelerate R&D spending to push its pipeline, targeting cost savings to be redeployed into innovation, and it floated the eventual separation of its consumer-health unit.3 The margin promise was gone, replaced by a bet on a pipeline that would not pay off for years.

Narrative Whiplash

What happened next is a case study in how not to reset expectations. The market did not object to investing in R&D in principle—every serious pharma investor knows the industry runs on research. It objected to being told one story for years and handed a different one without warning, without a bridge, and without a compelling set of near-term catalysts to justify the pivot. Note the irony buried in the name: the October 2023 announcement was itself branded as entering the "next chapter of Play to Win," the very same strategy Hudson had launched in 2019.3 The label stayed the same while the promise underneath it changed completely. That is the kind of continuity-in-name, reversal-in-substance move that erodes trust faster than an outright admission of failure.

On the call, analysts pressed hard on exactly this point, and the tenor of management's answers shifted the narrative from "disciplined execution" to "long-term innovation splurge"—a language change that, absent concrete milestones, read to the market as narrative-shifting rather than confidence-inspiring. The abruptness registered as a credibility failure. As the stock cratered—about €20 billion of value gone in a day—the message analysts took away was that management's guidance could not be relied upon.12 Hudson had spent his tenure trying to close the execution discount that dogged Sanofi's valuation; in an afternoon, he widened it into a chasm. This is the heart of the management-credibility case against the Hudson era, and it is an analytical fact, not a matter of opinion: a team that sets a hard, memorable, multi-year target and then abandons it without a graceful bridge has taught the market to discount its next set of promises.

Worse, the pipeline did not rush to his rescue. The years that followed brought a run of high-profile disappointments that made the "spend now, win later" thesis harder to defend. The breast-cancer drug amcenestrant was discontinued after failing to deliver. And in late 2025, the multiple-sclerosis asset tolebrutinib—one of the pipeline's most-watched bets—received a Complete Response Letter from the FDA for its lead indication, a regulatory rejection announced just before the holidays on December 24, 2025.13 Each setback left the company leaning ever more heavily on the one franchise that never let it down, and deepened the discount its multiple carried against US peers. By early 2026 the board had seen enough of the gap between the promise and the proof. But the reckoning came only after the loudest, most politically charged episode of the entire Hudson era: the sale of a French national treasure.

VI. The Great Consumer Carve-Out: Opella and the CD&R Deal

To understand why selling a fever-reducer nearly became a matter of state, you have to understand what Doliprane means in France. It is the country's leading brand of paracetamol—the pill in nearly every French medicine cabinet, the thing a parent reaches for at 3 a.m., manufactured on French soil for generations. It is, in the most literal sense, a household name. And in 2024 Sanofi decided to sell control of the company that makes it.

The Rationale and the Mechanics

The logic flowed directly from Hudson's pure-play ambition. If Sanofi was going to be a focused biopharma company betting everything on immunology and vaccines, then its steady, unglamorous consumer-health division—maker of Doliprane, the allergy brand Allegra, and the laxative Dulcolax—was a distraction, however cash-generative. Better to spin it out, crystallize its value, and redeploy the proceeds into the high-risk, high-reward drug pipeline. Sanofi had already rebranded the unit as Opella in preparation.

In October 2024 Sanofi agreed to sell a controlling stake to the American private-equity firm Clayton, Dubilier & Rice, and the transaction closed on April 30, 2025. CD&R acquired a 50.0% controlling interest based on an enterprise value of €16 billion; Sanofi received total net cash proceeds of around €10 billion and retained a 48.2% equity-method stake in the business, keeping meaningful exposure to a high-cash-flow asset while handing over the steering wheel.614

On capital-allocation grounds, this was, by the standards of the consumer-health carve-out wave, a strong outcome. The mid-2020s saw big pharma collectively decide that slow-growing consumer-health units did not belong inside high-multiple drug companies, and the industry produced a natural experiment in how to exit them. Set Sanofi against the peer set: GSK spun Haleon—the maker of Sensodyne and Advil—off to public markets, and Johnson & Johnson did the same with Kenvue, the home of Tylenol and Band-Aid. Both chose the IPO/spin route, which crystallizes value but subjects it to the mercy of daily market pricing and often a disappointing initial reception. Sanofi took the other road: a private sale to a financial buyer, extracting a full valuation—reported at a multiple in the mid-teens on the unit's EBITDA—in cash and up front, while keeping a large minority stake for future upside.614

There is genuine skill in that structure. Selling control to private equity at a high multiple, banking €10 billion of certain cash today, and retaining 48.2% of the equity means Sanofi monetized the asset at a premium while preserving exposure to the operational improvements CD&R will presumably drive. But—and this is the part management cannot yet claim victory on—extracting a premium price is only half of good capital allocation. The other half is what you do with the money. The €10 billion is now earmarked for pipeline investment and bolt-on acquisitions, precisely the high-risk deployment that the reliable, boring Opella cash flows used to fund internally. Whether that redeployment earns a better risk-adjusted return than the steady stream it replaced is the open question, and it will not be answerable for years. Trading certainty for optionality is a defensible bet; it is not a free one.

When Capital Allocation Meets the Republic

The financial elegance of the deal collided head-on with French political reality, and the collision was violent. Selling a "sovereign" health asset—the maker of the nation's paracetamol—to a US buyout shop triggered exactly the reaction the national-champion heritage should have predicted. The choice of buyer made it worse: private equity, in the French popular imagination, is shorthand for financiers who load a company with debt, strip its costs, and flip it, and the idea of that model being applied to the factory that makes the country's fever medicine was politically radioactive. Opella workers went on strike; unions warned of offshoring and job losses; and politicians across the spectrum, from the left to members of the governing establishment, publicly attacked the sale, invoking security of supply and the memory of the pandemic-era shortages that had taught France the danger of depending on foreign-made medicines. The government made clear it expected guarantees before it would tolerate the transaction. For a brief, remarkable moment, the sale of a stake in an over-the-counter drug business became a genuine matter of state.

The resolution was as revealing as the uproar. The French state's investment bank, Bpifrance, took a 1.8% stake in Opella and joined the board—a small equity position but a large symbolic one.6 Its presence came bundled with binding commitments on preserving French jobs, maintaining domestic manufacturing sites, and safeguarding the security of supply for key medicines. It was the 2004 Aventis playbook in miniature: the state cannot always stop a deal, but it can extract a sovereignty tax as the price of its blessing. For investors, the episode is a permanent reminder that Sanofi's capital-allocation freedom is bounded by a stakeholder that does not appear on any share register but never entirely leaves the room. The same board that navigated that political minefield was, at that very moment, preparing to remove the CEO who had set it in motion.

VII. The Leadership Reset: Belén Garijo and Execution Rigor

The end, when it came, was procedural rather than dramatic. There was no public boardroom rupture, no leaked resignation letter. In February 2026 Sanofi's board of directors simply decided not to renew Paul Hudson's mandate as a director, and with it his tenure as CEO.4 After a career spent trying to convince the market that Sanofi could execute, Hudson had been undone by the perception that it—and he—could not. His exit terms were disclosed with unusual precision: a gross termination benefit of €5,207,750, plus a nine-month non-compete indemnity of €3,124,650 paid in installments, alongside pro-rated bonus and conditional performance shares.4 It was a soft landing for a hard fall.

The Return of the Integrator

Into the vacuum stepped Belén Garijo, and the choice was loaded with history. Garijo is a physician by training—Spanish, she began her career in clinical medicine, working in hematology, before moving into the pharmaceutical industry, and she never entirely shed the clinician's habit of asking whether the data actually support the claim.5 She had spent roughly fifteen years inside Sanofi, rising to run pharmaceutical operations for Europe and Canada and sitting on the executive committee, but the role that made her name was the one described in Section III: leading the Genzyme integration.5 She then left for Germany's Merck KGaA—the centuries-old Darmstadt family-controlled group, not to be confused with the American Merck—where she ran the healthcare business before ascending, in 2021, to CEO and chair of the executive board of the entire company. There she became one of the most prominent women running a major global corporation and built a reputation as a disciplined, numbers-driven operator with a famously low tolerance for vague science and vaguer excuses.

That last point is the crux of why the board wanted her. The knock on the Hudson era was not a shortage of ambition; it was a surplus of it, untethered from delivery. Garijo's entire professional brand is the opposite—rigor, prioritization, and a willingness to kill programs that cannot clear a high bar of probability. Where Hudson was hired to inject urgency into a sleepy company, Garijo was hired to inject discipline into a company that had, in the market's eyes, confused spending with strategy.

She took over as Sanofi's CEO at the close of the annual general meeting on April 29, 2026, after shareholders approved her appointment with strong support; the veteran executive Olivier Charmeil had bridged the gap as interim CEO during the transition.5 The symbolism was hard to miss: the board reached past the disruptor-outsider model that had produced the credibility crisis and back to a proven insider-operator who had already demonstrated she could impose order on a Sanofi acquisition without smothering it.

Incentives as Strategy

The clearest signal of the new regime is not in Garijo's biography but in her pay structure. Her variable compensation was designed around hard, quantitative, near-term financial targets—with substantial weightings on sales growth, free cash flow, and business earnings per share—rather than on the softer, longer-horizon "innovation" milestones that had characterized the prior era.4 Compensation design is strategy made legible: it tells you what the board actually wants. This one points squarely at cash generation, delivery against guidance, and disciplined pipeline triage—an explicit repudiation of the "visionary storytelling" that had detonated the stock in 2023.

The bet is coherent. But it is only a bet, and an independent observer should be candid about the ways it could fail even with the right person in charge. Compensation aligned to near-term cash and EPS is a powerful corrective to visionary drift, but it carries its own risk: a management team paid on short-horizon metrics can be tempted to under-invest in the long-cycle research that pharma ultimately lives on—the exact opposite error from Hudson's, but an error nonetheless. The industry is littered with companies that pleased the market for a few years by cutting R&D and then discovered, too late, that they had eaten their own future. The task facing Garijo is not simply to spend less than Hudson; it is to spend better—to fund the handful of programs most likely to produce the next franchise while starving the rest, and to do so without hollowing out the pipeline that must eventually replace Dupixent.

There is also the unglamorous structural reality she cannot wish away. Garijo's Genzyme-era credibility is real, and her Merck track record suggests she means what the incentive plan says. But she inherits a company still bound by French labor law, still sharing the economics of its crown jewel with a partner in New York, and still carrying a domestic cost base that no amount of executive resolve can quickly reshape. The most disciplined operator in the world cannot unilaterally close a French factory or renegotiate a decades-old alliance on favorable terms. The proof of the new era, as always, will be in the portfolio she now inherits—and in whether the market, burned once, is willing to believe the guidance a second time.

VIII. The Portfolio Today: Segment Dynamics & Competitive Landscape

Strip away the corporate drama and Sanofi in mid-2026 is really two businesses under one roof: a biopharma engine dominated by immunology, and a vaccines franchise that has quietly become one of the most interesting in the industry. Both are locked in specific, named fights.

Biopharma: Life After the Locomotive

The immunology business is Dupixent, and everyone at Sanofi knows the danger in that sentence. The drug's core patents begin to erode in the early 2030s, which means the entire company is, in effect, running a countdown clock. The strategic response is a pair of pipeline assets designed to catch the falling knife.

The first is amlitelimab, an antibody with a different mechanism from Dupixent: it targets OX40-ligand, aiming to dampen the initiating phase of the overactive immune response rather than the downstream signaling. In its Phase III COAST program in atopic dermatitis, results have been genuinely mixed rather than uniformly triumphant—COAST 1 met its primary and key secondary endpoints, and the SHORE study succeeded, but COAST 2 delivered a more equivocal readout, with the full data set presented at the 2026 American Academy of Dermatology meeting.1516 The tantalizing feature is a potential every-12-weeks dosing schedule, far less frequent than incumbents—a real convenience edge if the efficacy holds up. Whether amlitelimab can absorb even a fraction of the eventual Dupixent cliff is the single most important scientific question facing the company, and the honest answer today is that the evidence is promising but not yet decisive.

The second pillar is the BTK inhibitor rilzabrutinib, branded Wayrilz, which in August 2025 became the first BTK inhibitor approved in the US for immune thrombocytopenia (ITP), a bleeding disorder—a genuine first-in-class win.17 It has since been pursued in additional immune-mediated conditions, including warm autoimmune hemolytic anemia, for which it holds special regulatory designations.17 And tolebrutinib, left for dead in the US after its December 2025 CRL, secured a positive CHMP opinion in Europe in April 2026 and subsequent EU approval, keeping a narrower multiple-sclerosis launch alive on one side of the Atlantic even as it stalled on the other.13 The pattern across the pipeline is the same: real assets, real approvals, but a persistent gap between the ambition and the clean, blockbuster-scale wins the R&D splurge was supposed to buy.

Standing across the battlefield is AbbVie, and the comparison is instructive. AbbVie faced its own single-asset nightmare when Humira—for years the best-selling drug in the world—hit its patent cliff, and the company navigated it by building two successors, Skyrizi and Rinvoq, into a combined multi-billion-dollar immunology juggernaut before the old franchise fell. AbbVie is, in effect, the case study of the very problem Sanofi now faces: how a one-drug immunology giant survives the death of its blockbuster. That AbbVie pulled it off is the bull-case precedent; that it took years of flawless execution and two genuinely differentiated new drugs is the bear-case warning. Alongside AbbVie sit Pfizer, Novartis, and Eli Lilly, none of them slow and none of them poor. Sanofi did not invent the insight that type-2 and immune-mediated inflammation is a lucrative battleground, and it does not have the field to itself.

Myth versus reality. The consensus narrative treats Sanofi as "the Dupixent company plus some other stuff." The reality is more nuanced in both directions. On one hand, the dependency is real and arguably understated—strip out Dupixent's growth and the rest of the portfolio has looked pedestrian, which is exactly why the market assigns a discount. On the other hand, the reflexive assumption that Sanofi has "nothing behind Dupixent" is not quite fair: Wayrilz is a genuine first-in-class approval, Beyfortus is a bona fide vaccines blockbuster, and amlitelimab is a credible—if unproven—successor asset. The honest read is that Sanofi has candidates for a second act, but has not yet proven one. That gap between candidate and proof is the entire investment debate.

Vaccines: Winning the Right RSV War

The more quietly impressive story is in vaccines, and specifically Beyfortus (nirsevimab), a monoclonal antibody that protects infants against respiratory syncytial virus (RSV), co-commercialized with AstraZeneca. RSV is the leading cause of infant hospitalization; a single-shot passive antibody given to babies has proven both clinically valuable and commercially powerful, and Beyfortus scaled rapidly, generating around $1.8 billion in sales in 2024 with continued strong growth into 2025.18 Ahead of the 2025–26 season, Sanofi and AstraZeneca tripled production and began shipping early to lock in supply.18

They did so because a direct rival arrived. In June 2025 the FDA approved Merck's clesrovimab, branded Enflonsia, a second long-acting infant RSV antibody priced at $556 per dose—the first true head-to-head competitor to Beyfortus.19 The infant RSV market has just become a two-horse race, and Beyfortus's share is now something to watch each season rather than assume.

There is a neat strategic irony here that repays a moment's attention, because it illustrates how the type of product can matter more than the disease it targets. RSV threatens two very different populations: infants and the elderly. The pharma industry attacked both. For the elderly, GSK and Pfizer developed conventional active vaccines—Arexvy and Abrysvo—that train the patient's own immune system to fight the virus. For infants, whose immune systems are too immature to vaccinate effectively, Sanofi and AstraZeneca took the other approach: a monoclonal antibody that provides ready-made, passive protection in a single shot, essentially handing the baby the antibodies rather than teaching it to make them.

The market outcomes of those two bets have diverged sharply. The adult RSV vaccine market cooled hard in 2025–26 as US immunization advisory guidance turned more restrictive, narrowing the eligible population and sending Arexvy and Abrysvo sales lower. The infant antibody market, by contrast, has been buoyed by broad recommendations to protect essentially all newborns entering their first RSV season, giving Beyfortus a large, recurring, seasonal population. In hindsight, Sanofi backed the more durable side of the RSV opportunity—less because it out-forecast its rivals on the science than because passive infant immunization landed in a more favorable policy environment. That is a genuine, if partly fortunate, strategic win, and a reminder that in vaccines the recommending bodies—the CDC's advisory committee in the US and its equivalents abroad—are as important to the economics as the clinical data. The threat now is simply that Merck has arrived to split the prize.

IX. Playbook: Business & Investing Lessons

Step back from the individual battles and Sanofi's history offers a set of transferable lessons—some flattering, some cautionary—about how big pharma actually creates and destroys value.

Lesson 1: The Asymmetric Alliance. Sanofi's most valuable asset came not from its own labs but from renting genius. The Regeneron partnership—and to a lesser extent the AstraZeneca RSV collaboration—shows how a company with global commercial scale can partner with cutting-edge science and share in an outcome it could never have invented. But the lesson carries a warning printed in the fine print: when you are the muscle and someone else is the brain, the market gives the brain the credit. The "execution discount" is the tax you pay for a strategy built on other people's innovation, and it does not go away just because the revenue is real.

Lesson 2: The Conglomerate Cleansing Pain. The Opella carve-out illustrates how genuinely hard it is to convert a steady, boring, cash-generative unit into fuel for high-risk research. The financial case for focus is easy to write on a slide and brutal to execute in the real world, because the steady business you are shedding is exactly the one that funds you through the dry years—and because, when the asset is culturally or nationally beloved, the transition detonates political resistance that no spreadsheet anticipated.

Lesson 3: The Blockbuster Illusion. A single world-class product is a blessing that behaves like a drug in its own right—euphoric, then dependency-forming. Dupixent's cash flow gave Sanofi the luxury of avoiding hard choices, masked operational inefficiency, and let successive management teams defer the cost discipline the business needed. Concentration that looks like strength on the way up becomes single-point-of-failure risk on the way down. The healthiest thing that can happen to a one-drug company is to be forced, early, to build the second act.

Lesson 4: National Champion Constraints. From the 2004 Aventis intervention to Bpifrance's 2025 Opella stake, Sanofi's entire history is a lesson in operating a global capital-allocation playbook inside the gravitational field of a sovereign state. The French government is a permanent, unlisted stakeholder whose priorities—jobs, domestic manufacturing, supply security—do not always align with return on invested capital. For any investor in a "national champion," the political constraint is not noise around the model; it is part of the model. It caps how aggressively costs can be cut, shapes which deals are possible, and occasionally overrides the commercially optimal outcome entirely. The counterintuitive lesson is that this is not purely a cost. State backing has, at moments, been a source of protection and stability; the same government that blocks restructuring is the one that helped create the company and shielded it from a foreign takeover. Investors must price both sides of that relationship.

Lesson 5: Incentives Reveal Strategy. A recurring theme in this story is that you learn more about what a management team will actually do from its compensation structure than from its slide decks. Hudson's era was rich in vision and, ultimately, poor in the delivery the market wanted; the redesign of executive pay around near-term sales, cash flow, and EPS is a more credible signal of the new direction than any strategy presentation, precisely because it binds management to outcomes it cannot spin. When assessing any leadership transition, read the pay plan before the press release.

X. Analysis: Bull vs. Bear Case & Risk Radar

The Competitive Structure

Run Sanofi through Porter's five forces and the picture is a business with real moats and real exposure. The bargaining power of buyers is high and rising: US pharmacy-benefit managers and European state health systems are relentless on price, and a drug earning a third of your revenue is a fat target for negotiation. The threat of substitutes is structural—every blockbuster eventually meets biosimilar and generic competition, and Dupixent's early-2030s cliff is the substitute risk made concrete. Rivalry is intense and well-funded, nowhere more than the immunology marketing war against AbbVie's Skyrizi and Rinvoq. Against these pressures, Sanofi's defenses are the classic pharma moats: patent protection, the switching costs of irreplaceable rare-disease therapies, and the scale economies of global biologic manufacturing and distribution.

In Helmer's 7 Powers terms, the durable powers are the cornered resource of Dupixent and the rare-disease franchise, and scale economies in manufacturing and commercial reach. But it is worth being precise about a limitation of pharma's moats that many investors gloss over: a cornered resource protected by a patent is a moat with an expiry date printed on it. Unlike a network effect that compounds with every new user, or a brand that can strengthen for a century, a drug patent is a wasting asset by legal design—society grants the monopoly precisely so that it will one day end. This is why the pipeline question at Sanofi is existential rather than incremental. The company's most powerful advantages are, by their nature, temporary, and the entire enterprise is a race to manufacture new temporary advantages faster than the old ones dissolve. What Sanofi conspicuously lacks is a network effect or a broad consumer branding power that could outlast any single molecule—the Opella sale, ironically, handed the one genuinely durable, patent-independent consumer brand it owned to someone else.

The Bull Case

The optimistic story is a story about execution finally matching assets. In it, Garijo transplants Merck-style discipline and cost rigor into Sanofi, narrowing the execution discount that has dogged the stock for years and re-establishing the guidance credibility the 2023 reversal destroyed. Dupixent's COPD expansion drives the franchise toward and past €25 billion in annual sales, extending the runway well into the next decade and buying time for the successors to mature. Amlitelimab launches cleanly and proves it can inherit a meaningful chunk of the eczema and broader type-2 franchise—helped by its potential quarterly dosing convenience—defusing the patent cliff before it arrives. Wayrilz and the vaccines franchise add genuine, non-Dupixent growth. And the roughly €10 billion of Opella proceeds get deployed into accretive, mid-stage bolt-on acquisitions that seed the next generation of assets rather than being frittered on overpriced auctions. Do all of that, and today's "cheap French pharma"—perennially valued below its US peers despite owning one of the industry's best drugs—re-rates meaningfully as the market finally credits Sanofi as an operator, not just a distributor.

The Bear Case

The pessimistic story is the value trap—the most dangerous category of stock precisely because it looks like a bargain. In it, the pipeline keeps disappointing—more tolebrutinib-style rejections, more amcenestrant-style discontinuations—and the R&D spending that blew up the margin target in 2023 never produces a genuine second blockbuster. Amlitelimab's mixed COAST data turns out to foreshadow a good-but-not-great drug rather than a true Dupixent heir, capturing a slice of the market but nowhere near enough to offset the coming cliff. French labor and political constraints prevent the kind of cost surgery that would lift margins toward US-peer levels, so even flawless commercial execution cannot close the profitability gap. Beyfortus cedes share to Enflonsia season by season. And Sanofi remains structurally cheap—optically inexpensive, perpetually discounted, a company whose greatest asset is owned in part, whose profitability is capped by geography, and whose management keeps promising a re-rating that never quite arrives. In this version, the discount is not an opportunity; it is the market correctly pricing a business with a great present and an uncertain future.

The tension between these two cases is the whole investment question, and it can be stated crisply. Why Sanofi wins from here: a proven cash engine with years of runway left, a credible operator installed to close the credibility gap, a re-rating available simply by hitting the numbers, and €10 billion of firepower to buy the future. Why the case breaks: the entire thesis leans on a wasting asset and an unproven successor, inside a cost structure that cannot be optimized and a partnership that shares the spoils. Both are true today. The next three years of pipeline data and margin delivery will decide which one the market chooses to believe.

The Activist Stress Test

A skeptical long/short investor would press on several pressure points. Portfolio complexity: even post-Opella, is Sanofi focused enough, or does the retained 48.2% equity-method stake in a consumer business it no longer controls just add reporting noise and a lever for financial engineering rather than a clean outcome? An activist would argue for a clear plan to monetize the residual stake over time rather than let it sit as a strategic orphan on the balance sheet. Governance and disclosure: the pattern of setting a hard margin target and then abandoning it mid-cycle is exactly the kind of guidance whiplash activists seize on—can this board be trusted to hold the new management to the new EPS and cash-flow targets, or will those quietly slip too when the pipeline demands more cash? The credibility of the entire re-rating case hinges on the answer, and the burden of proof sits with management, not the skeptic.

Capital allocation is the richest vein. After years of promising discipline, the prior regime embarked on an unbudgeted R&D surge; the €10 billion of Opella proceeds is now the live test of whether this company can deploy a war chest without value destruction. Bolt-on M&A in biopharma is notoriously easy to do badly—paying up for late-stage assets at auction, or buying revenue rather than science—and an activist would demand strict return hurdles and transparency on every deal. And then the perennial French question, which no activist can fully resolve: how much of the "national champion" cost base could be optimized in a jurisdiction that permitted it, and how much shareholder value is permanently trapped by the fact that this one does not? The uncomfortable answer is that a meaningful chunk of the peer-discount is structural rather than fixable, which is precisely why the bull case leans so heavily on growth closing the gap rather than cost-cutting doing it.

The Risk Radar

Three risks dominate everything else. First, the Dupixent patent cliff of the early 2030s—the single-point-of-failure risk that gives every other question its urgency. Second, French regulatory and political deadlock—the structural inability to downsize and optimize a protected domestic cost base, which caps the margin story regardless of who is CEO. Third, the Beyfortus competitive threat from Merck's Enflonsia—a live, near-term contest whose seasonal share data will reveal whether Sanofi's best vaccine can hold its lead.

A fourth risk sits underneath all three and deserves flagging even though it is not unique to Sanofi: drug-pricing policy, above all in the United States. The US is where pharmaceutical profits are actually made—American prices subsidize the rest of the world—and it is precisely there that political pressure to cut those prices is most intense, from pharmacy-benefit-manager negotiating power to government-led price-setting mechanisms that can, over time, reach exactly the kind of high-revenue biologics Sanofi depends on. A drug earning well over $15 billion a year is not merely a commercial triumph; it is a large, visible target for any policy designed to lower national drug spending. For a company this concentrated in one blockbuster, an adverse shift in US reimbursement or pricing rules would strike directly at the cash flow that funds everything else. It is the kind of macro-regulatory risk that does not show up in a clinical readout but can quietly reset the value of the entire franchise.

The KPIs That Actually Matter

For an investor tracking this company, the noise is enormous and the signal is narrow. Three metrics carry most of the story. First, Dupixent quarterly sales growth and COPD launch velocity—the health of the engine, and the pace at which the runway extends; decelerating growth here would be the earliest warning that the cliff is arriving on schedule and the successors are not ready. Second, Beyfortus market share versus Enflonsia each RSV season—the clearest, cleanest read on whether Sanofi can defend a lead against a determined, well-resourced rival in a genuinely competitive market. Third, Amlitelimab's Phase III progression and regulatory timelines—the single best proxy for whether the post-Dupixent future is real or wishful; every readout, label, and submission date moves the odds on the entire long-term thesis. Watch those three, and layer in the core operating-margin trajectory under Garijo as the scorecard on whether the new discipline is more than a slogan. If the margin line starts climbing while the pipeline delivers, the value-trap fear dissolves; if margins stay stuck and the pipeline stumbles, the discount will have been right all along. Everything else—the political dramas, the personnel changes, the quarterly headlines—is texture around those four numbers.

XI. Epilogue & Outro

Sanofi has shed its skin more times than almost any company its size. It began as an oil company's diversification, became a chemical-and-pharma rollup, then a government-brokered national champion, then a rare-disease specialist, and now a self-styled pure-play biopharma leader betting its future on immunology and vaccines. Each transformation was real, and each left a residue—the political gene from its state origins, the cost base from its merger heritage, the dependency from its blockbuster.

Under Belén Garijo the strategic destination is, for once, not in dispute. The company knows what it wants to be: a focused, disciplined, cash-generative innovator that has learned to run a great business and not merely own a great asset. The map is drawn. The only question left—the same question that detonated the stock in 2023 and cost a CEO his job in 2026—is whether this company, with all its history pulling against it, can finally execute the plan it has so clearly written down.

References

-

Sanofi shares plunge after 2025 target dropped — MarketScreener/Reuters, 2023-10-27 ↩↩

-

Sanofi loses $21 billion in market value after dropping 2025 profit target — CNBC, 2023-10-27 ↩↩

-

Press Release: Sanofi Enters Next Chapter of Play to Win Strategy — Sanofi, 2023-10-27 ↩↩↩↩

-

Sanofi details Paul Hudson exit package and Belén Garijo CEO pay (Form 6-K) — StockTitan/Sanofi, 2026 ↩↩↩↩

-

Press Release: Annual General Meeting of April 29, 2026 — Belén Garijo appointed as Director and Chief Executive Officer of Sanofi — Sanofi, 2026-04-29 ↩↩↩↩↩

-

Press Release: Sanofi and CD&R close Opella transaction, create global consumer healthcare leader — Sanofi, 2025-04-30 ↩↩↩↩

-

Sanofi launches hostile bid for Aventis / battle for Aventis 2004 — NBC News, 2004 ↩↩↩

-

Sanofi-aventis to Acquire Genzyme for $74.00 in Cash Per Share Plus Contingent Value Right — PR Newswire, 2011-02-16 ↩

-

Sanofi-aventis and Regeneron Strategic Antibody Collaboration (Form 6-K) — Sanofi-aventis via SEC EDGAR, 2007-11-29 ↩↩

-

Regeneron Reports Fourth Quarter and Full Year 2025 Financial and Operating Results — Regeneron Pharmaceuticals, 2026 ↩

-

Regeneron tangles with Sanofi over commercial transparency in long-running Dupixent collaboration — Fierce Pharma ↩

-

Press Release: Sanofi provides update on tolebrutinib regulatory submission in non-relapsing secondary progressive multiple sclerosis — Sanofi, 2025-12-24 ↩↩

-

Sanofi nets €10B from Opella stake sale, eyes more 'bolt-on' deals — Fierce Pharma, 2025 ↩↩

-

Press Release: Sanofi's amlitelimab met all primary and key secondary endpoints in the COAST 1 phase 3 study — Sanofi, 2025-09-04 ↩

-

Press Release: AAD — new results from Sanofi's amlitelimab phase 3 studies in atopic dermatitis — Sanofi, 2026-03-28 ↩

-

Sanofi's Wayrilz approved in US as first BTK inhibitor for immune thrombocytopenia — Sanofi US, 2025-08-29 ↩↩

-

Feeling RSV heat from Merck, Sanofi lays out early supply plans for Beyfortus — Fierce Pharma, 2025 ↩↩

-

Merck scores FDA nod for Enflonsia, setting up RSV market battle vs. Sanofi and AstraZeneca's Beyfortus — Fierce Pharma, 2025-06 ↩

-

Virus stalls Genzyme plant (Allston Landing Vesivirus contamination) — Nature Biotechnology, 2009-08 ↩↩

-

Genzyme and Carl Icahn Reach Agreement — Fierce Healthcare, 2010 ↩

-

Sanofi CEO unveils new strategy to drive innovation and growth (Play to Win) — Sanofi via GlobeNewswire, 2019-12-09 ↩↩↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube