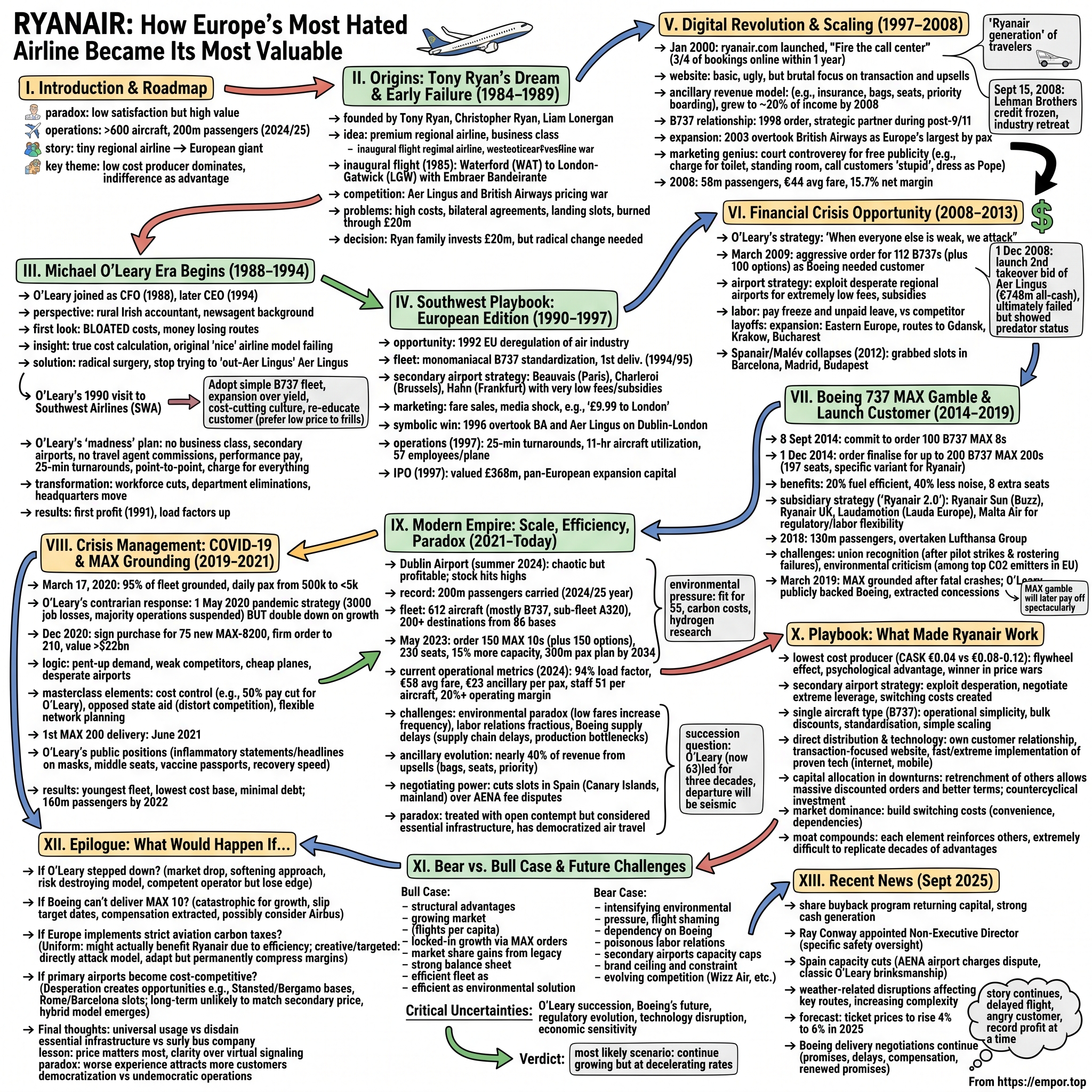

Ryanair: How Europe's Most Hated Airline Became Its Most Valuable

I. Introduction & Episode Roadmap

Picture this paradox: The airline that consistently ranks dead last in customer satisfaction surveys, whose CEO once suggested charging passengers to use the toilet, whose brand is synonymous with hidden fees and cramped seats—this same airline is worth more than Lufthansa, Air France-KLM, and IAG combined. Welcome to the Ryanair story. Today, Ryanair operates more than 600 aircraft, making it Europe's largest airline both in terms of fleet size and passengers carried. The Dublin-based carrier has carried its 200 millionth passenger in the 2024/25 year, a new record for both the airline and for European airline history. With a market capitalization of EUR30.29B as of August 2025, the ultra-low-cost carrier that everyone loves to hate has become aviation's most unlikely success story.

How did a tiny Irish regional airline, hemorrhaging money and teetering on bankruptcy, transform into a pan-European aviation colossus? How did a company that openly treats its customers with disdain build one of the world's most valuable airline franchises? And perhaps most importantly: what can we learn from the Michael O'Leary playbook that turned controversy into cash flow?

This is the story of regulatory arbitrage at scale, of turning Southwest's playbook into a European weapon, and of building a business so structurally advantaged that even universal customer hatred couldn't stop its ascent. It's about recognizing that in commodity businesses, the lowest cost producer doesn't just win—they dominate. And sometimes, being hated is just fine if you're also indispensable.

We'll trace Ryanair's journey from Tony Ryan's failed luxury experiment through O'Leary's radical transformation, examine how they turned every crisis into opportunity, and understand why their Boeing partnership became perhaps the most important vendor relationship in aviation history. Along the way, we'll see how a tax accountant from Mullingar became Europe's most notorious CEO, and how his willingness to say the unsayable became Ryanair's greatest marketing asset.

Buckle up—unlike on an actual Ryanair flight, this journey promises to be both comfortable and enlightening.

II. Origins: Tony Ryan's Dream & Early Failure (1984–1989)

The rain was hammering against the windows of Tony Ryan's office in Shannon when he first sketched out his vision for a new Irish airline. It was early 1984, and Ryan, already wealthy from founding Guinness Peat Aviation—the world's largest aircraft leasing company—saw an opportunity in the skies above Ireland. The government-owned Aer Lingus had a monopoly on Irish routes, charging eye-watering fares that made air travel a luxury for the wealthy. A round-trip ticket from Dublin to London cost more than most Irish workers earned in a month.

The story of Ryanair begins in the middle of 1984. The company was founded by three Irish businessmen – Tony Ryan (the founder of Irish aircraft leasing company Guinness Peat Aviation), Christopher Ryan, and Liam Lonergan, the owner of Irish travel firm Club Air. Tony Ryan's two sons also took leading roles in the startup, with Cathal Ryan bringing his flying experience as a pilot while Declan Ryan offered financial expertise gained while working as an accountant.

What Tony Ryan envisioned wasn't the no-frills carrier we know today. Far from it. His Ryanair would be a premium regional airline, offering business class service, frequent flyer programs, and all the amenities travelers expected from a proper airline. The Ryan family had made their fortune leasing aircraft to the world's major carriers—they understood the business from the inside out. Or so they thought.

The inaugural flight took off on July 8, 1985. Registered as EI-BPI, the plane carried just 15 passengers and was dedicated to the airline's only route, flying between Waterford (WAT), a regional airport in the south-east of Ireland, and London-Gatwick Airport (LGW). The aircraft was a Brazilian-made Embraer Bandeirante turboprop—about as far from a Boeing 737 as you could get while still calling yourself an airline.

Ryanair's first flights were offered at a return fare of just £99 ($126), which was less than half that being charged by Aer Lingus and British Airways. The incumbents didn't take this lying down. Predictably, the competitors soon began to drop their own fares in response to Ryanair's arrival, in what became one of Europe's first airline pricing wars.

The early numbers seemed promising. Ryanair flew around 82,000 passengers in its first year of operations on its single route. Emboldened by this initial success, the Ryans began expanding rapidly. They added larger aircraft—Hawker Siddeley HS748 turboprops with 46 seats, then BAC 1-11 jets. They launched new routes: Dublin to London, Cork to London, services to Brussels and Amsterdam. They introduced business class cabins, complimentary meals, even a frequent flyer program.

But here's where the story takes a dark turn. The European aviation market of the 1980s was nothing like today's deregulated free-for-all. Each route required bilateral agreements between governments. Landing slots at major airports were controlled by incumbent carriers. And those incumbents—Aer Lingus and British Airways—had deep pockets and government backing. They could afford to lose money on routes just to drive Ryanair out of business.

By 1989, Ryanair was carrying nearly 600,000 passengers annually, but it was hemorrhaging cash at an alarming rate. The company had burned through £20 million—a staggering sum for a small Irish airline. Tony Ryan faced a choice: pump more money into his failing airline or walk away.

In a decision that would prove pivotal, the Ryan family invested £20 million more into the airline. But money alone wouldn't save Ryanair. What they needed was someone who could completely reimagine what an airline could be. Someone willing to break every rule in the industry playbook.

Enter Michael O'Leary—though not as CEO, not yet. In 1988, Michael O'Leary joined the company as chief financial officer. A Trinity College Dublin graduate who'd worked at KPMG and run a newsagent business, O'Leary was originally hired as Tony Ryan's personal financial advisor. His first look at Ryanair's books must have been sobering. The airline was losing money on virtually every route. Its cost base was bloated. It was trying to be all things to all people and succeeding at none of them.

The luxury experiment had failed spectacularly. Ryanair had learned a painful lesson: you can't out-Aer Lingus Aer Lingus. If the company was going to survive, it needed a completely different approach. The stage was set for one of the most dramatic transformations in business history.

III. The Michael O'Leary Era Begins: From Tax Accountant to CEO (1988–1994)

Michael O'Leary's first day examining Ryanair's books in 1988 must have felt like performing an autopsy on a still-breathing patient. The company was technically alive but dying by a thousand cuts—expensive aircraft leases, bloated overhead, routes that lost money every single day. As Tony Ryan's financial advisor, O'Leary had one job: figure out if this airline could be saved or if it was time to pull the plug.

O'Leary wasn't supposed to be an airline executive. Born in Mullingar, County Westmeath, he'd studied business at Trinity College Dublin, worked briefly at KPMG, then tried his hand at running newsagent shops. He was, by his own admission, "a rural Irish accountant" with no aviation experience whatsoever. But Tony Ryan saw something in him—perhaps the willingness to ask uncomfortable questions that others wouldn't dare voice.

The first thing O'Leary did was strip away the polite veneer that typically surrounds airline finances. He calculated the true cost per passenger, per route, per minute of flight time. The numbers were catastrophic. The Dublin-London route, supposedly Ryanair's crown jewel, was losing money despite high load factors. Why? Because Ryanair was trying to compete on service with carriers that had structural advantages—better slots at Heathrow, corporate contracts, government support.

Due to decreasing profits, the company restructured in 1990, copying the low-fares model of Southwest Airlines, after O'Leary visited the company. But before that transformative trip to Dallas, O'Leary had to convince the Ryan family that radical surgery was needed. No more business class. No more free meals. No more trying to be a "nice" airline.

The resistance was fierce. Tony Ryan had built his reputation on understanding what airlines wanted—premium service, reliability, comfort. His sons, particularly Cathal who was a pilot, believed in the romance of aviation. O'Leary was proposing to turn Ryanair into the aviation equivalent of a city bus—basic transportation, nothing more.

The turning point came during a board meeting in late 1990. Ryanair had just posted another massive loss. The Ryan family faced a stark choice: inject more capital or shut down. O'Leary made his pitch: Give him six months to visit Southwest Airlines, study their model, and implement a similar approach in Europe. If it didn't work, they could liquidate with dignity rather than bleeding out slowly.

The Dallas pilgrimage that followed has become the stuff of business legend. O'Leary spent days at Southwest's headquarters, shadowing Herb Kelleher, studying their ten-minute turnarounds, understanding how they'd made money for nineteen consecutive years in the cutthroat U.S. market. In a 1994 lecture, O'Leary described the strategy as adopting a simple all Boeing 737 fleet, pursuing expansion over yield, creating a culture of cost-cutting, and "re-educating" the customer to prefer lower prices to "frills".

But here's what most people miss about O'Leary's Southwest education: he didn't just copy their operational model. He absorbed something deeper—the understanding that in commodity businesses, culture beats strategy. Southwest succeeded not just because of quick turnarounds but because every employee, from pilots to gate agents, understood that their enemy wasn't other airlines but the automobile. Their competition was the car, and they had to be not just cheaper but faster door-to-door than driving.

O'Leary returned to Dublin with a 10-point plan that would have seemed like madness to any traditional airline executive:

- Sell all aircraft except the Boeing 737s

- Eliminate business class entirely

- Stop serving free meals and drinks

- Move from primary to secondary airports

- Eliminate travel agent commissions

- Introduce performance-based pay for all staff

- Reduce turnaround times to 25 minutes

- Eliminate hub-and-spoke in favor of point-to-point

- Charge for everything beyond the seat itself

- Make the airline the most hated—and most profitable—in Europe

The transformation was brutal. Half the workforce was let go. Entire departments were eliminated. Routes that couldn't generate immediate profit were abandoned. The frequent flyer program was scrapped. Even the company headquarters was moved from Dublin's expensive city center to a prefab building at Dublin Airport.

In 1994, Michael O'Leary took the role of chief executive officer. By then, the transformation was already showing results. The airline that had lost £20 million by 1990 posted its first profit in 1991. Load factors increased. Costs per passenger plummeted.

But O'Leary wasn't satisfied with mere profitability. He wanted domination. And for that, he needed two things: capital to buy aircraft and a regulatory change that would open up European skies. The first would come from an IPO. The second was already in motion in Brussels, where bureaucrats were preparing to detonate the cozy world of European aviation.

The tax accountant from Mullingar was about to become the most feared man in European aviation. His weapon wouldn't be superior service or customer satisfaction. It would be something far more powerful: the relentless, ruthless pursuit of the lowest possible costs.

IV. The Southwest Airlines Playbook: European Edition (1990–1997)

"We're not trying to be Southwest Airlines," O'Leary told reporters in 1992. "We're trying to be better than Southwest Airlines." It was typical O'Leary bravado, but hidden within the bluster was a truth: Ryanair wasn't just copying Southwest's model—they were weaponizing it for European conditions.

The Southwest playbook was deceptively simple. Use one aircraft type to minimize training and maintenance costs. Focus on point-to-point flights rather than hub-and-spoke networks. Turn planes around in 25 minutes or less. Eliminate unnecessary frills. Keep planes in the air as many hours as possible. But implementing this in Europe required navigating a completely different landscape—one with multiple currencies, languages, and until recently, highly protected national airlines.

In 1992, the European Union's deregulation of the air industry in Europe gave carriers from one EU country the right to operate scheduled services between other EU states and represented a major opportunity for Ryanair. This was the moment O'Leary had been waiting for. While established carriers like Lufthansa and Air France scrambled to understand what deregulation meant, Ryanair was ready to pounce.

The first major decision was fleet standardization. The airline took delivery of its first Boeing 737 in the financial year 1994 to 1995. This wasn't just an operational choice—it was a philosophical statement. While competitors operated mixed fleets of Airbus and Boeing aircraft, Ryanair would become monomaniacally focused on a single type. Every pilot could fly every plane. Every mechanic knew every system. Parts inventory was simplified. Training costs plummeted.

But the real genius was in the secondary airport strategy. Where Southwest used alternative airports like Love Field in Dallas, Ryanair took this concept to an extreme that would have made even Herb Kelleher blush. Instead of flying to Paris, they flew to Beauvais—60 miles away. Instead of Brussels, they chose Charleroi. Instead of Frankfurt, they picked Hahn—a former U.S. military base 75 miles from the city.

These airports were desperate for traffic. Ryanair negotiated deals that would have been unthinkable at major hubs: multi-year agreements with guaranteed low fees, marketing support payments, even subsidies for new routes. Some airports literally paid Ryanair to fly there. It was regulatory arbitrage at its finest—using the desperation of regional airports to build an insurmountable cost advantage.

The customer re-education campaign was equally radical. O'Leary understood that European travelers, accustomed to flag carriers and regulated pricing, needed to be shocked into a new mindset. So he launched fare sales that grabbed headlines: £9.99 to London. £19.99 to Paris. Sometimes just £0.01, with taxes and fees extra. The media called it a publicity stunt. O'Leary called it marketing genius—every newspaper article about Ryanair's "crazy" prices was free advertising.

By 1996, it took over British Airways and Aer Lingus on the prized London-Dublin service. This was more than a commercial victory—it was a symbolic triumph. The route where Ryanair had started, where it had once tried to compete on service and failed miserably, was now theirs through sheer price discipline.

The operational metrics by 1997 were staggering: - Average turnaround time: 25 minutes (industry average: 60 minutes) - Aircraft utilization: 11 hours per day (industry average: 7 hours) - Employees per aircraft: 57 (industry average: 140) - Break-even load factor: 53% (industry average: 77%)

In 1997, Ryanair went public, using the funds raised to expand into a pan-European carrier. The IPO valued the company at £368 million—not bad for an airline that had been technically bankrupt just seven years earlier. But more importantly, it gave Ryanair the war chest it needed for massive expansion.

The investment thesis was simple: Europe had 370 million people versus America's 270 million, yet Americans took four times as many flights per capita. Deregulation would unleash massive latent demand for air travel. And when that demand materialized, the airline with the lowest costs would capture the lion's share.

By the end of 1997, Ryanair was carrying 4.3 million passengers annually. They had 18 routes. They were profitable. But they were still a minnow in the European aviation ocean. O'Leary's ambition was to become a shark. And the next phase of growth would require embracing a new tool that traditional airlines viewed with suspicion: the internet.

The Southwest playbook had been successfully transplanted to European soil. But O'Leary was about to add innovations that even Southwest hadn't imagined. The age of digital disruption was beginning, and Ryanair would ride it harder than anyone anticipated.

V. Digital Revolution & Scaling the Model (1997–2008)

The moment Michael O'Leary saw a passenger book a flight online for the first time, he reportedly turned to his IT director and said, "This changes everything. Fire the call center." It was January 2000, and while other airlines tentatively experimented with websites as digital brochures, O'Leary saw something different: the ultimate disintermediation tool.

In 2000, Ryanair launched its website, initially considering online booking a small component but it grew to handle three-quarters of bookings within a year. This wasn't just a channel shift—it was a complete reimagining of the airline-customer relationship. No travel agents taking commissions. No call center agents needing salaries. Just customers, credit cards, and a direct connection.

The website was deliberately basic—almost insultingly so. No fancy graphics. No smooth user experience. Just a brutal focus on one thing: converting browsers into buyers. O'Leary famously refused requests to improve the site's design, saying, "The website is perfect. It's ugly, but it works. Like our planes."

But here's what the aesthetics obscured: Ryanair.com became one of the most sophisticated e-commerce operations in Europe. They pioneered dynamic pricing algorithms that changed fares multiple times per day based on demand. They tested everything—button colors, words, placement—with the ruthlessness of a Silicon Valley startup. They turned the booking process into a gauntlet of upsells: insurance, car rentals, hotels, priority boarding, seat selection.

The ancillary revenue model emerged from this digital foundation. O'Leary described it in a 2001 interview, saying "The other airlines are asking how they can put up fares. We are asking how we could get rid of them". This wasn't hyperbole. By 2008, Ryanair was generating over €488 million from ancillary revenues—nearly 20% of total income.

The Boeing relationship deepened dramatically during this period. In 1998, Ryanair placed a US$2 billion order for 45 new Boeing 737-800 series aircraft. But this was more than a purchase order—it was a strategic partnership. Ryanair became Boeing's most reliable customer during the post-9/11 downturn, placing orders when others canceled. In return, Boeing gave Ryanair prices that competitors could only dream of.

The expansion across Europe was methodical and ruthless. Ryanair would identify a route dominated by a high-cost incumbent, enter with prices 70% lower, and watch as demand exploded. They didn't steal passengers from competitors as much as create entirely new markets. The plasterer from Poland could now afford to work in London. The pensioner from Manchester could buy a second home in Spain.

By 2003, Ryanair had overtaken British Airways to become Europe's largest airline by passenger numbers. But O'Leary's marketing genius truly shone in how he handled this success. Instead of corporate PR speak about "customer focus" and "service excellence," he deliberately courted controversy:

- Suggested charging for toilet use (never implemented, massive free publicity)

- Proposed "standing room" sections on planes (impossible regulatory-wise, headlines worldwide)

- Publicly called customers "stupid" for not printing boarding passes (outrage equals awareness)

- Dressed as the Pope to launch new routes to Rome (Catholic groups protested, bookings soared)

Every outrageous statement generated millions in free advertising. Media outlets couldn't resist covering O'Leary's latest provocation. And while journalists and consumer advocates expressed horror, customers kept booking flights. They might hate Ryanair, but they loved the prices.

The operational statistics by 2008 were extraordinary: - 58 million passengers carried - 163 routes across 26 countries - Fleet of 163 Boeing 737-800s - 32 bases across Europe - Average fare: €44 - Net margin: 15.7% (highest among major airlines globally)

But the most remarkable achievement was cultural. Ryanair had fundamentally changed how Europeans thought about air travel. It was no longer a luxury product but a commodity—like bus travel, only faster. Weekend trips to random European cities became normal. "Ryanair generation" entered the lexicon, describing young Europeans who thought nothing of flying to Barcelona for a weekend because it cost less than a tank of gas.

Then came September 15, 2008. Lehman Brothers collapsed. Credit markets froze. Passenger numbers plummeted industry-wide. Most airlines retrenched, canceled aircraft orders, and prayed for survival.

O'Leary saw opportunity. "This is our moment," he told the board. "When everyone else is weak, we attack."

The financial crisis wouldn't be Ryanair's doom. It would be their launching pad to total European domination.

VI. The Financial Crisis Opportunity (2008–2013)

"Never waste a good crisis." O'Leary didn't coin the phrase, but between 2008 and 2013, he turned it into an art form. While competitors slashed routes and parked aircraft in the Arizona desert, Ryanair went on one of the most aggressive expansion sprees in aviation history.

The numbers from late 2008 were sobering across the industry. Passenger traffic fell off a cliff. Business travel—the profit center for legacy carriers—evaporated overnight. Airlines like Alitalia needed government bailouts. Others, like Sterling Airlines and SkyEurope, simply vanished. The conventional wisdom was clear: hunker down, preserve cash, wait for recovery.

O'Leary's response? Order more planes. Lots more planes.

In March 2009, with aviation in freefall, Ryanair announced an order for 112 Boeing 737-800s with options for 100 more. The aviation press was stunned. But O'Leary understood something his competitors missed: Boeing was desperate. With carriers canceling orders worldwide, Boeing needed Ryanair more than Ryanair needed Boeing. The pricing Ryanair extracted remains confidential, but industry analysts estimated discounts of 50% or more from list prices.

The airport strategy during the crisis was equally brilliant. Regional airports across Europe faced catastrophe as airlines pulled out. Many had borrowed heavily to build new terminals during the boom years. Now they faced bankruptcy. Ryanair's negotiating team would arrive at these desperate airports with a simple proposition: "We'll save you, but here are our terms."

The deals struck during this period were extraordinary: - Guaranteed fees of less than €2 per passenger (major airports charged €20+) - Marketing support payments worth millions annually - Free office space and check-in facilities - Some airports literally paid Ryanair per passenger carried

Take Frankfurt-Hahn, a former U.S. military base that Ryanair had made into its German hub. During the crisis, the airport's owners were so desperate to keep Ryanair that they agreed to terms that would have seemed fantasy in normal times. Similar deals were struck in Spain, Italy, and Eastern Europe.

But the masterstroke was Ryanair's approach to labor during the crisis. While other airlines faced strikes over pay cuts and layoffs, O'Leary made his staff an offer: accept a pay freeze and unpaid leave, or watch as competitors' employees lose their jobs entirely. He pointed to the graveyard of failed airlines. The message was clear: you might not like working for Ryanair, but at least you have a job.

The expansion into Eastern Europe accelerated dramatically. These markets, previously dominated by loss-making national carriers, were virgin territory for the Ryanair model. Routes from London to Gdansk, Dublin to Krakow, Brussels to Bucharest—all launched during the supposed catastrophe of 2009-2010. The Polish plasterer market that Ryanair had identified years earlier exploded as Eastern Europeans sought work in Western Europe during the recession.

By 2011, while competitors were still recovering, Ryanair's statistics were staggering: - 75.8 million passengers (up from 58 million in 2008) - 1,500+ daily flights - 51 bases across Europe - Load factor: 83% - €2.8 billion in cash reserves

The crisis had also accelerated industry consolidation, and O'Leary was ready to feast on the carcasses. When Spanair collapsed in 2012, Ryanair immediately grabbed their slots at Barcelona and Madrid. When Malév Hungarian Airlines failed, Ryanair moved into Budapest within weeks. Each competitor's death made Ryanair stronger.

In October 2008, Ryanair withdrew operations from a base in Europe for the first time when it closed its base in Valencia, Spain, but this was tactical retreat, not weakness. Ryanair estimated the closure cost 750 jobs, but it demonstrated O'Leary's discipline—even during expansion, unprofitable bases would be ruthlessly eliminated.

The company also used the crisis to reset customer expectations even lower. Checked baggage fees increased. Credit card charges were introduced. Even printing a boarding pass at the airport now cost €40. When consumer groups howled, O'Leary's response was typical: "If you're stupid enough not to print your boarding pass, you deserve to pay €40."

The crisis years also saw Ryanair's most audacious takeover attempts. On 1 December 2008, Ryanair launched a second takeover bid of Aer Lingus, offering an all-cash offer of €748 million. The offer was a 28% premium on the value of Aer Lingus stock, during the preceding 30 days. Ryanair said, "Aer Lingus, as a small, stand-alone, regional airline, has been marginalised and bypassed, as most other EU flag carriers consolidate." The two airlines would operate separately. Ryanair stated it would double the Aer Lingus short-haul fleet from 33 to 66 and create 1,000 new jobs.

Though the Aer Lingus takeover ultimately failed due to competition concerns, it demonstrated Ryanair's transformation from upstart to predator. The company that had nearly died in 1990 was now trying to buy its former tormentor.

By 2013, as Europe emerged from recession, Ryanair stood triumphant. They had used the crisis to lock in a decade of advantaged growth through cheap aircraft and sweetheart airport deals. Competitors were weakened, some fatally. The stage was set for the next phase: becoming not just Europe's largest airline, but building a fleet advantage that would be impossible to replicate.

Enter the Boeing 737 MAX—Ryanair's biggest gamble yet.

VII. The Boeing 737 MAX Gamble & Launch Customer Status (2014–2019)

The Boeing executives in Seattle couldn't hide their relief when Michael O'Leary walked into the room in September 2014. The 737 MAX program was in trouble—not technically, but commercially. Airlines were hesitant about another new variant. Airbus's A320neo was winning orders. Boeing needed a statement customer, someone whose endorsement would validate the MAX program. They needed Ryanair.

On 8 September 2014, Ryanair committed to ordering 100 new Boeing 737 MAX 8s (plus options for an additional 100) for delivery in 2019. But O'Leary wasn't interested in the standard MAX 8. He wanted something special—something that would give Ryanair another structural advantage over competitors.

On 1 December 2014, the airline finalised its order for up to 200 Boeing 737 MAX 200s, a version of the 737 MAX 8 for low-cost airlines. The MAX 200 was essentially a custom variant designed for Ryanair—with 197 seats versus the standard 189. Eight extra seats might not sound revolutionary, but in Ryanair's high-volume model, it meant 4% more revenue per flight with essentially the same costs.

O'Leary christened it the "Gamechanger" aircraft, and for once, his hyperbole was justified. The MAX 200 promised: - 20% better fuel efficiency than the 737-800 - 40% lower noise footprint - Extra revenue from eight additional seats - Range to reach new markets like Turkey and Morocco

Boeing gave Ryanair extraordinary pricing—rumored to be under $40 million per aircraft for an airplane with a list price over $100 million. In return, Ryanair became the launch customer, the validator, the proof that the MAX program would succeed.

During this period, Ryanair also began building what O'Leary called "Ryanair 2.0"—a collection of subsidiaries designed to navigate the increasingly complex European regulatory environment. In 2019, the transition began from the airline Ryanair and its subsidiaries into separate sister airlines under the holding company.

The subsidiary strategy was clever: - Ryanair Sun (later Buzz) in Poland—targeting the Eastern European market with local labor contracts - Ryanair UK—a Brexit hedge, ensuring continued access to UK domestic routes - Laudamotion (later Lauda Europe) in Austria—acquiring Niki Lauda's failed airline for a foothold in the German-speaking market - Malta Air—leveraging Malta's favorable tax regime and EU membership

Each subsidiary operated under local labor laws, avoiding the pan-European union negotiations that plagued competitors. It was regulatory arbitrage refined to an art form.

The expansion continued at breakneck pace. By 2018, Ryanair was carrying 130 million passengers annually. They had overtaken Lufthansa Group to become Europe's largest airline by passengers carried. The network sprawled across 37 countries with 86 bases.

But success bred new challenges. Labor relations, always tense under O'Leary's leadership, reached a breaking point. In 2017, a rostering failure led to the cancellation of thousands of flights. Pilots, sensing weakness, organized strikes across Europe. For the first time, O'Leary was forced to recognize unions—a capitulation he had resisted for decades.

The environmental criticism also intensified. In 2018, Ryanair became the first airline and the only non-coal-power plant to be among the 10 companies with the highest amount of CO2 emissions in the EU. That year, Ryanair had an emission equivalent of 9.9 megatonnes of CO2. The paradox was stark: Ryanair's low fares had democratized air travel, but that democratization came with an environmental cost that was becoming impossible to ignore.

Then, in March 2019, disaster struck—though not for Ryanair directly. The Boeing 737 MAX was grounded worldwide after two fatal crashes. Every MAX aircraft was parked. Deliveries stopped. The airplane Ryanair had bet its future on was now toxic.

Lesser airlines might have panicked. O'Leary saw opportunity. While Boeing's stock price crashed and orders were canceled worldwide, O'Leary publicly backed Boeing: "This is still the best aircraft in the world. The problems will be fixed. And when they are, we'll be ready."

Behind the scenes, Ryanair's negotiating team went to work. Boeing was desperate to keep Ryanair as a customer. The terms extracted during this period remain confidential, but aviation analysts believe Ryanair received compensation worth hundreds of millions for the delivery delays, plus additional pricing concessions on future orders.

By late 2019, just as the MAX situation was stabilizing, a new crisis emerged. Reports from China spoke of a mysterious respiratory illness. Within months, it would bring global aviation to a complete halt. But once again, O'Leary would find a way to turn catastrophe into competitive advantage.

The MAX gamble would eventually pay off spectacularly. But first, Ryanair would have to survive the greatest crisis in aviation history.

VIII. Crisis Management: COVID-19 & The MAX Grounding (2019–2021)

March 17, 2020. Dublin Airport, usually bustling with Ryanair's signature yellow and blue, stood eerily silent. Of the 450 aircraft in Ryanair's fleet, 95% were grounded. Daily passenger numbers had fallen from 500,000 to fewer than 5,000. For the first time in three decades, Michael O'Leary faced a crisis that money and aggression couldn't solve.

The double punch of the MAX grounding and COVID-19 should have been fatal. Competitors with stronger balance sheets and government backing were collapsing. Norwegian Air needed state rescue. Flybe disappeared entirely. Virgin Atlantic begged for bailouts. The conventional playbook said: preserve cash, defer all capital expenditures, pray for government support.

O'Leary's response was characteristically contrarian. On May 1, 2020, Ryanair announced its pandemic strategy: The loss of 3000 jobs, announced on 1 May 2020, which affected mainly pilots and cabin crew. This came as the airline announced it would suspend the majority of its operations until June 2020. But while others were canceling aircraft orders, O'Leary was on the phone with Boeing.

In December 2020, Ryanair signed a purchase agreement with Boeing for 75 new MAX-8200 aircraft, increasing its firm order from 135 to 210, with a total value of over $22bn. The aviation world was stunned. In the depths of the worst crisis in industry history, Ryanair was doubling down on growth.

The logic was vintage O'Leary: "Every crisis ends. When this one does, there will be massive pent-up demand for travel. Half our competitors will be dead or crippled. Aircraft will be cheap. Airports will be desperate. This is our moment to grab market share that will last a generation."

In July 2020, Ryanair's CEO announced that the company had made a net loss of €185 million in the period April–June 2020. In comparison, in the same period of 2019, the firm made a net profit of €243 million. For any other airline, this would have been catastrophic. But Ryanair had something others didn't: €3.5 billion in cash reserves built up over decades of profitable operations.

The pandemic operations were a masterclass in crisis management:

Cost Control: Within weeks, Ryanair had negotiated salary cuts across the board—O'Leary himself took a 50% pay cut. Fixed costs were slashed by 85%. Every unnecessary expense was eliminated.

Government Relations: Unlike competitors who begged for bailouts, Ryanair actively campaigned against state aid, arguing it would distort competition. O'Leary knew that when government money dried up, subsidized competitors would struggle while Ryanair's lean model would thrive.

Network Planning: Instead of maintaining skeleton services everywhere, Ryanair concentrated on routes where travel was essential or restrictions were minimal. Domestic UK routes, essential worker corridors to Eastern Europe, repatriation flights—anywhere there was demand, Ryanair was ready.

The Boeing Relationship: Ryanair took delivery of its first MAX 200 in June 2021. The timing was perfect. While other airlines were still parking aircraft, Ryanair was taking delivery of the most fuel-efficient narrowbody in the world at prices that would never be repeated.

The most controversial aspect of Ryanair's pandemic response was O'Leary's public positions. While other airline CEOs spoke carefully about safety and gradual recovery, O'Leary was on every media outlet declaring: - Mask mandates were "nonsense" (while still enforcing them) - Middle seat blocking was "idiotic" (which research later supported) - Vaccine passports were essential (ahead of government policy) - Recovery would be "dramatic and rapid" (which proved correct)

Each inflammatory statement generated headlines, keeping Ryanair in public consciousness while competitors disappeared from view. When booking websites reopened, Ryanair was top-of-mind.

The environmental criticism during COVID took an unexpected turn. With flights grounded, emissions plummeted. But O'Leary used this to make a counterintuitive argument: "We're replacing old, inefficient aircraft with MAX 200s that burn 20% less fuel. We're not the problem—we're the solution. The problem is legacy carriers flying half-empty old jets."

By early 2021, while competitors were still bleeding cash, Ryanair was positioned for what O'Leary called "the mother of all recoveries." They had: - The youngest fleet in Europe (average age 6.5 years) - The lowest cost base (further reduced during COVID) - Minimal debt (€1.5 billion versus Lufthansa's €9 billion) - Locked-in growth via MAX deliveries - Competitors weakened or eliminated

The recovery, when it came, exceeded even O'Leary's optimistic projections. Ryanair carried 72 million passengers in 2021 and a record-breaking 160 million in 2022. The pent-up demand for travel was tsunami-like. And Ryanair, with its expanded fleet and weakened competitors, captured a disproportionate share.

The pandemic that should have killed Ryanair had instead strengthened its dominance. The MAX that should have been a liability became a competitive advantage. Once again, O'Leary had turned crisis into opportunity. But the biggest moves were yet to come.

IX. The Modern Empire: Scale, Efficiency & Environmental Paradox (2021–Today)

The scene at Dublin Airport in summer 2024 was chaos—but profitable chaos. Serpentine queues, frustrated passengers, overwhelmed staff. Yet Ryanair's stock price hit all-time highs. The contradiction captured everything about the modern Ryanair: universally disliked, undeniably essential, and impossibly profitable.

Ryanair welcomed its 200 millionth passenger for 2024/25, a new record both for the airline and for European airline history. 200 million passengers in a single calendar year is a new record both for Ryanair and for European aviation, with only a handful of other airlines worldwide able to match the feat.

The scale achieved is staggering. Ryanair's fleet currently consists of 612 aircraft, all of which are from the Boeing 737 family apart from a sub-fleet of 26 Airbus A320-200s operated exclusively by Lauda Europe. The operation spans 200+ destinations across 37 countries from 86 bases. On any given day, Ryanair operates over 3,000 flights—more than most airlines manage in a week.

In May 2023, Ryanair announced the order of 150 MAX 10s and an option to purchase a further 150. This wasn't just fleet expansion—it was a statement of intent. The MAX 10, with 230 seats versus the MAX 200's 197, would give Ryanair another 15% capacity per flight. By 2034, Ryanair plans to carry 300 million passengers annually—more than the entire U.S. domestic market today.

But growth has brought new challenges. The environmental paradox has become impossible to ignore. Ryanair's argument—that new, efficient aircraft carrying full loads are better than old jets flying half-empty—contains truth but sidesteps the larger issue: Ryanair's low fares have dramatically increased flying frequency. The pensioner who flies to Spain monthly, the student visiting home every few weeks—behaviors that didn't exist before Ryanair made them affordable.

Labor relations remain fractious. Despite recognizing unions, Ryanair continues to face strikes and disputes. The summer 2024 chaos was partly due to staff shortages—even Ryanair's aggressive recruitment couldn't keep pace with demand. The contradiction persists: employees hate working for Ryanair but need the jobs; Ryanair needs employees but refuses to pay premium wages.

The relationship with Boeing has evolved into mutual dependence. The airline was recently forced to scale back its ambitions for the year to 206 million passengers as a result of ongoing supply chain delays and production bottlenecks at the Boeing 737 final assembly line. "We are working with Boeing to accelerate deliveries. Although Boeing 737 production is recovering from the Boeing strike at the end of 2024, we do not expect sufficient units to arrive by the summer of 2025," O'Leary said. "We are confident of receiving the remaining 29 aircraft on our order by March 2026".

The ancillary revenue model has evolved into sophisticated science. Today's Ryanair passenger faces a gauntlet of upsells: - Seat selection: €4-30 - Priority boarding: €6-20 - Cabin bags: €6-25 - Checked bags: €20-40 - Insurance, car hire, hotels, transfers

Nearly 40% of Ryanair's revenue now comes from these extras. The advertised €9.99 fare is essentially a loss leader to get customers into the conversion funnel.

Recent strategic moves reveal O'Leary's continued willingness to play hardball. The announcement of cutting one million seats to Spain this winter—10% in the Canary Islands, 41% in mainland regions—over airport fee disputes shows Ryanair's negotiating power. When airports don't meet their terms, Ryanair simply leaves, knowing the economic impact will force capitulation.

The technology infrastructure has become surprisingly sophisticated. Dynamic pricing algorithms adjust fares in real-time. The mobile app, despite its basic appearance, handles millions of transactions daily. The operation control center in Dublin manages the entire network with remarkable efficiency—when weather disrupts competitors for days, Ryanair typically recovers within hours.

Current Operational Metrics (2024): - Load factor: 94% - Average fare: €58 - Ancillary revenue per passenger: €23 - Staff per aircraft: 51 - Operating margin: 20%+

The sustainability challenge looms largest. European governments are increasingly serious about aviation emissions. France has banned short flights where trains are available. The Netherlands wants to shrink Schiphol. Carbon taxes are coming. O'Leary's response remains defiant: "We're the solution, not the problem. Ban business class before you touch Ryanair."

Yet privately, Ryanair is hedging. They're investing in sustainable aviation fuel research. They're funding carbon offset programs. They're even exploring hydrogen aircraft for the 2030s. The company that built its fortune on cheap fossil fuel-powered flight knows the game is changing.

The succession question also lurks. O'Leary, now 63, has led Ryanair for three decades. His eventual departure will be seismic. The culture, the aggression, the controversy—they're inseparable from O'Leary himself. Can Ryanair maintain its edge without its infamous leader?

For now, the empire continues expanding. Every week brings new route announcements, new base openings, new battles with airports and regulators. The paradox deepens: the worse the customer experience, the more customers Ryanair attracts. The more they're hated, the more they're needed.

Ryanair has achieved something remarkable: they've made themselves infrastructure. Like water or electricity, people might complain about the service, but they can't imagine life without it. In democratizing air travel, they've fundamentally changed how Europeans live, work, and play.

X. Playbook: What Made Ryanair Work

After four decades and 200 million passengers, Ryanair's success might seem obvious in hindsight. But the playbook that built Europe's most valuable airline contains lessons that extend far beyond aviation. Here's how they did it—and why it's nearly impossible to replicate.

The Power of Being the Lowest Cost Producer

In commodity businesses, the lowest cost producer doesn't just win—they set the rules. Ryanair's cost per available seat kilometer (CASK) is roughly €0.04, compared to €0.08-0.12 for legacy carriers. This isn't a small advantage; it's a different game entirely.

The cost advantage compounds. Lower costs mean lower prices. Lower prices stimulate demand. Higher demand enables bulk purchasing. Bulk purchasing reduces unit costs. The flywheel accelerates until competitors can't even see Ryanair's taillights.

But here's what most miss: the cost advantage isn't just operational. It's psychological. When you know you're the lowest cost producer, you can make decisions others can't. You can start price wars knowing you'll win. You can walk away from negotiations knowing airports need you more. You can weather any crisis knowing you'll outlast competitors.

Secondary Airport Strategy and Negotiating Leverage

The genius wasn't just using secondary airports—it was turning their desperation into Ryanair's moat. Frankfurt-Hahn, Charleroi, Bergamo—these airports had massive infrastructure and no traffic. Ryanair became their lifeline, and negotiated accordingly.

The deals structured during expansion created switching costs for both sides. Airports invested in Ryanair-specific facilities. Local businesses built around Ryanair traffic. Regional governments became dependent on Ryanair-driven tourism. Breaking these relationships would hurt the airports more than Ryanair.

This created unprecedented negotiating leverage. When Barcelona raised fees, Ryanair moved flights to Girona. When Dublin got expensive, they emphasized Cork. The threat of leaving became Ryanair's nuclear option—one they regularly demonstrated they'd use.

Single Aircraft Type and Operational Simplicity

The all-Boeing 737 fleet seems obvious now, but it was radical when implemented. Every other airline operated mixed fleets for "flexibility." Ryanair chose constraint as strategy.

Single type meant: - Any pilot could fly any plane - Any engineer could fix any aircraft - Parts inventory was minimized - Training was standardized - Bulk purchasing maximized discounts - Operational complexity minimized

But the deeper insight was that simplicity scales while complexity compounds. As Ryanair grew from 10 to 600 aircraft, the single-type advantage multiplied. Competitors adding their 50th aircraft type faced geometric complexity increases. Ryanair adding their 500th 737 faced none.

Direct Distribution and Technology Adoption

Cutting out travel agents wasn't just about saving commission—it was about owning the customer relationship entirely. Every search, booking, and interaction generated data. Every customer touchpoint became an upsell opportunity.

The website's deliberate ugliness was strategic. Pretty websites make browsing pleasant. Ugly websites drive transactions. Ryanair wanted buyers, not browsers. The €2 billion in ancillary revenue validates the approach.

Technology adoption followed a pattern: be late to invest but extreme in implementation. Ryanair wasn't first to online booking, but when they adopted it, they went all-in faster than anyone. They weren't first to mobile, but their app now handles 50% of bookings. They wait for technology to be proven, then implement it more aggressively than anyone.

Using Controversy as Free Marketing

O'Leary understood something profound: in commodity businesses, awareness beats affection. Every outrageous statement—charging for toilets, standing seats, "stupid" customers—generated millions in free media coverage.

The controversy served multiple purposes: - Free advertising worth hundreds of millions annually - Positioned Ryanair as the anti-establishment option - Set expectations so low that reality seemed acceptable - Made O'Leary a celebrity CEO, personifying the brand - Distracted from serious issues while media focused on stunts

Traditional airlines spent fortunes on brand advertising trying to convince people they were slightly better than competitors. Ryanair spent nothing while dominating mental availability through controversy.

Capital Allocation During Downturns

The pattern repeated in every crisis: 1. Competitors retrench, cancel orders, seek bailouts 2. Ryanair negotiates massive aircraft orders at distressed prices 3. Airports and suppliers, desperate for business, accept Ryanair's terms 4. Ryanair emerges from crisis with lower costs and more capacity 5. Weakened competitors cede market share permanently

This countercyclical investment required two things: capital and conviction. The capital came from years of profitable operations. The conviction came from understanding that aviation always recovers because human desire to travel is fundamental.

Building Switching Costs Through Market Dominance

Once Ryanair dominates a route, it's nearly impossible to dislodge. They can offer 10 daily frequencies where competitors might manage two. Business travelers who claim to hate Ryanair end up flying them for convenience. The network effects compound.

The switching costs are subtle but powerful: - Customers know the Ryanair booking process - Airports have built infrastructure around Ryanair operations - Secondary cities depend on Ryanair for connectivity - Hotels and tourism businesses rely on Ryanair passengers - Even competitors plan around Ryanair's schedule

The Moat Compounds

Each element reinforces the others. Low costs enable low prices which drive volume which increases negotiating power which reduces costs further. The secondary airport strategy reduces costs while building switching costs. The controversy drives awareness which fills planes which justifies more aircraft orders which reduces unit costs.

After 40 years, the moat hasn't narrowed—it's widened. Competitors can copy tactics but can't replicate decades of compounding advantages. They can't recreate the airport relationships, the Boeing pricing, the brand awareness, or the cost structure.

The playbook worked because it was internally consistent, ruthlessly executed, and improved through repetition. Most importantly, it was built on a fundamental insight: in commodity markets, the lowest cost producer with the greatest scale wins. Everything else is commentary.

XI. Bear vs. Bull Case & Future Challenges

The investment community remains sharply divided on Ryanair. Bulls see an unstoppable force with decades of growth ahead. Bears see mounting risks that could finally clip Ryanair's wings. Both sides have compelling arguments.

The Bull Case: Structural Advantages in a Growing Market

The optimists point to mathematics. Europe has 450 million people but only 2.5 flights per capita annually, versus 8.0 in the United States. As Eastern European wealth grows and travel normalizes post-pandemic, the addressable market could double. Ryanair, with its unassailable cost position, will capture the lion's share.

The Boeing relationship represents a fortress. With 210 MAX 200s on order and options for 150 MAX 10s, Ryanair has locked in growth at prices competitors can't match. Boeing, desperate to maintain Ryanair as an anchor customer, will continue offering preferential terms. The aircraft advantage—more seats, better fuel efficiency—translates directly to margin expansion.

During the next 12 months, Ryanair's latest forecasts show the carrier will pass this new record and will carry an estimated 206 million passengers. The path to 300 million passengers by 2034 seems not just plausible but conservative.

Market share gains appear inevitable. Lufthansa, Air France, and IAG face structural disadvantages—hub complexity, legacy costs, union constraints—that can't be solved. Every crisis weakens them further while Ryanair emerges stronger. The pandemic proved this dynamic definitively.

The balance sheet provides enormous flexibility. With €4 billion in cash and minimal debt, Ryanair can weather any crisis while maintaining growth investments. They could survive two years with zero revenue—no competitor can make that claim.

Environmental regulations might actually help Ryanair. Their young, efficient fleet produces fewer emissions per passenger than any legacy carrier. Carbon taxes would hurt competitors more, widening Ryanair's cost advantage. The MAX 10, with 230 seats and superior fuel efficiency, could make Ryanair the "greenest" major airline by passenger-mile metrics.

The Bear Case: Accumulating Risks and Structural Headwinds

Skeptics see storm clouds gathering. Environmental pressure is intensifying beyond what carbon efficiency can address. France's short-flight ban could spread. Flight shaming is real among younger consumers. The regulatory environment that enabled Ryanair's growth could reverse sharply.

Boeing dependency has become a critical vulnerability. The MAX disasters, production delays, and quality issues reveal dangerous concentration risk. If Boeing stumbles again—and their track record suggests they might—Ryanair has no alternative. Airbus won't offer similar terms, and switching would destroy the single-type advantage.

Labor relations remain poisonous. The recognition of unions was a strategic defeat O'Leary never truly accepted. As labor markets tighten and workers gain bargaining power, Ryanair's cost advantage could erode. The summer 2024 chaos showed that even Ryanair can't operate without sufficient staff.

Secondary airports are reaching capacity. Many of Ryanair's key bases—Stansted, Bergamo, Charleroi—have limited expansion potential. Moving to primary airports would destroy the cost advantage. Geographic expansion is constrained by aircraft range and regulatory barriers.

The brand ceiling is real. Ryanair can't meaningfully raise prices without losing share to competitors. Business travelers, despite frequency advantages, still avoid Ryanair when possible. The brand perception limits pricing power permanently.

Competition is evolving. Wizz Air, with newer aircraft and lower labor costs, is attacking from below. EasyJet has strengthened its position at primary airports. New entrants with clean balance sheets and modern fleets keep emerging. The competitive moat might be narrower than it appears.

Critical Uncertainties

Several factors could tip the balance either way:

O'Leary Succession: His departure would be seismic. The culture, negotiating style, and controversy machine are inseparable from O'Leary himself. No obvious successor exists. The transition could either liberate Ryanair from his constraints or destroy what makes it unique.

Boeing's Future: If the MAX 10 certification delays extend beyond 2027, Ryanair's growth plans collapse. If Boeing's quality issues worsen, the reputational damage could be severe. The relationship that built Ryanair could destroy it.

Regulatory Evolution: A coordinated European carbon tax, mandatory sustainable fuel requirements, or slot restrictions at secondary airports could fundamentally alter Ryanair's economics. The regulatory arbitrage that enabled growth could evaporate.

Technology Disruption: High-speed rail expansion, particularly in Spain and France, directly threatens short-haul routes. Hyperloop, electric aircraft, or other innovations could obsolesce Ryanair's fleet. The company that disrupted European aviation could itself be disrupted.

Economic Sensitivity: Despite O'Leary's claims, Ryanair isn't recession-proof. A severe European downturn would hit discretionary travel hard. The operating leverage that amplifies profits in good times would savage margins in bad times.

The Verdict

The bull case rests on proven execution and structural advantages. The bear case depends on external factors outside Ryanair's control. History suggests betting against O'Leary is expensive, but trees don't grow to the sky.

The most likely scenario: Ryanair continues growing but at decelerating rates. The easy gains—replacing high-cost incumbents, opening new markets—are largely captured. Future growth requires harder battles against strengthened competitors and skeptical regulators.

The stock market's valuation implies confidence in continued dominance. But empires, even those built on the lowest costs and highest volumes, eventually face limits. Whether Ryanair has reached those limits or has another decade of conquest ahead remains the €30 billion question.

XII. Epilogue: What Would Happen If...

If O'Leary Stepped Down Tomorrow?

The market reaction would be swift and brutal—likely a 20% immediate drop. But the deeper question is whether Ryanair's culture would survive. O'Leary isn't just the CEO; he's the embodiment of Ryanair's ruthless efficiency and calculated controversy.

His successor would face an impossible choice: maintain the aggression and be compared unfavorably to O'Leary, or soften the approach and risk destroying what makes Ryanair work. The most likely outcome: a competent operator who maintains the business model but loses the negotiating edge and publicity genius that O'Leary brings.

The airline would probably become more "normal"—better labor relations, less controversy, gradual brand improvement. But normal airlines don't generate 20% operating margins. Within five years, Ryanair would likely resemble a larger, more efficient easyJet—successful but no longer exceptional.

If Boeing Can't Deliver the MAX 10 on Schedule?

This scenario is increasingly probable. Boeing's track record suggests the MAX 10 won't achieve certification before 2028, possibly later. For Ryanair, this would be catastrophic for growth plans but manageable operationally.

The immediate impact: growth targets would be pushed back 2-3 years. The 300 million passenger goal would slip to 2037. Competitors would gain breathing room. But Ryanair would extract massive compensation from Boeing—probably enough to fund share buybacks that would support the stock price.

Longer-term, Ryanair might be forced to consider Airbus. This would be O'Leary's nightmare—losing the single-type advantage, paying higher prices, admitting strategic error. But if Boeing continues stumbling, even Ryanair's loyalty has limits.

If Europe Implements Strict Aviation Carbon Taxes?

This is not if but when. The European Commission's "Fit for 55" package includes aviation in emissions trading schemes. By 2030, carbon costs could add €20-30 per ticket. The question is how it's implemented.

If applied uniformly, Ryanair might actually benefit. Their newer, fuller aircraft produce fewer emissions per passenger than competitors. A €25 carbon tax would hurt Lufthansa's half-empty long-haul flights more than Ryanair's packed short-hauls. O'Leary would complain publicly while privately celebrating competitive advantage.

But if governments get creative—taxing frequency rather than emissions, subsidizing rail alternatives, banning flights under 500km—Ryanair's model would be directly attacked. The company would adapt—they always do—but margins would compress permanently.

If Primary Airports Become Cost-Competitive?

The pandemic showed this is possible. Heathrow, Schiphol, and Frankfurt all offered unprecedented deals to attract traffic. If desperation makes primary airports affordable, Ryanair's secondary airport advantage evaporates.

But this seems unlikely to persist. Primary airports have structural costs—debt service, complex operations, legacy contracts—that prevent matching secondary airport pricing long-term. Once traffic recovers, they'll raise prices again.

More likely: a hybrid model emerges. Ryanair maintains secondary airport bases but opportunistically uses primary airport slots during off-peak times. They're already doing this in Rome and Barcelona. The pure secondary airport model might evolve, but the cost discipline would remain.

Final Thoughts: The Ryanair Paradox

Ryanair has achieved something unique in modern business: universal usage despite universal disdain. They've made themselves essential infrastructure while maintaining the service levels of a particularly surly bus company. They've democratized air travel while being decidedly undemocratic in their operations.

The lesson isn't that customer service doesn't matter—it's that in commodity businesses, price matters more. Ryanair proved that if you're cheap enough, reliable enough, and ubiquitous enough, quality becomes optional. This is either deeply cynical or refreshingly honest, depending on your perspective.

O'Leary once said, "We're not entering the restaurant business because I don't want to poison my customers." It was a joke, but it revealed a truth: Ryanair knows exactly what it is and isn't. They're not trying to be loved. They're not pretending to care. They're just trying to move humans from A to B as cheaply as physically possible.

In an age of corporate virtue signaling and brand purpose statements, Ryanair's clarity is almost refreshing. They have one purpose: low-cost air travel. Everything else—comfort, service, reputation—is negotiable.

Whether this model survives generational change, environmental pressure, and technological disruption remains uncertain. But for 40 years, betting against Ryanair has been a losing proposition. They've turned crises into opportunities, controversies into free marketing, and customer hatred into €30 billion of market value.

The ultimate irony: Ryanair, the airline that treats its customers with open contempt, has done more to democratize European travel than any government program or social initiative. Millions of Europeans have seen the continent because Ryanair made it affordable. Families separated by borders reunite regularly because Ryanair made it possible.

They might be the worst airline in Europe by every service metric. But they're also, undeniably, the most important. And in business, sometimes that's all that matters.

XIII. Recent News

September 2025 brings typical Ryanair headlines—expansion and conflict in equal measure. The company continues executing its massive share buyback program, returning capital to shareholders while the stock trades near all-time highs. This capital return, funded by extraordinary cash generation, reinforces management's confidence in the business model despite external pressures.

Board composition is evolving with the addition of Captain Ray Conway as Non-Executive Director, bringing specific oversight of air safety—a critical role given the MAX history and ongoing Boeing challenges. The appointment signals institutional maturity, even as O'Leary's operational grip remains absolute.

The Spain capacity cuts dominate current headlines. Ryanair's decision to reduce winter capacity by one million seats—10% in the Canary Islands, 41% in mainland regions—over AENA airport charges disputes is classic O'Leary brinksmanship. The Spanish government protests, tourism businesses panic, but Ryanair holds firm. History suggests Spain will capitulate; Ryanair's traffic is too important to lose.

Weather-related disruptions affecting key routes highlight operational challenges even Ryanair can't control. Climate change makes European weather increasingly unpredictable, adding cost and complexity to the ultra-efficient model. The company that masters everything struggles with atmospheric rivers and sudden storms.

Looking ahead, Ryanair has said it expects ticket prices to rise by 4% to 6% during 2025, with only a partial recovery from the 8% decline last year. This modest pricing power reflects both recovering demand and competitive dynamics—Ryanair can raise prices slightly but remains constrained by its low-cost positioning.

The Boeing delivery negotiations continue their familiar dance. Promises, delays, compensation, renewed promises. The MAX 10 certification timeline slips rightward while Ryanair extracts concessions. It's a dysfunctional relationship that somehow benefits both parties—Boeing keeps its largest customer, Ryanair gets unprecedented pricing.

As we observe Ryanair in late 2025, we see a company at the height of its powers yet facing accumulating challenges. The model that conquered Europe must now navigate environmental pressures, technological change, and eventually, management transition. Whether Ryanair's second act matches its first remains aviation's most compelling question.

The story continues, one delayed flight, one angry customer, one record profit at a time.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube