Rolls-Royce Holdings plc: The Turnaround of a British Crown Jewel

I. Introduction & Episode Roadmap

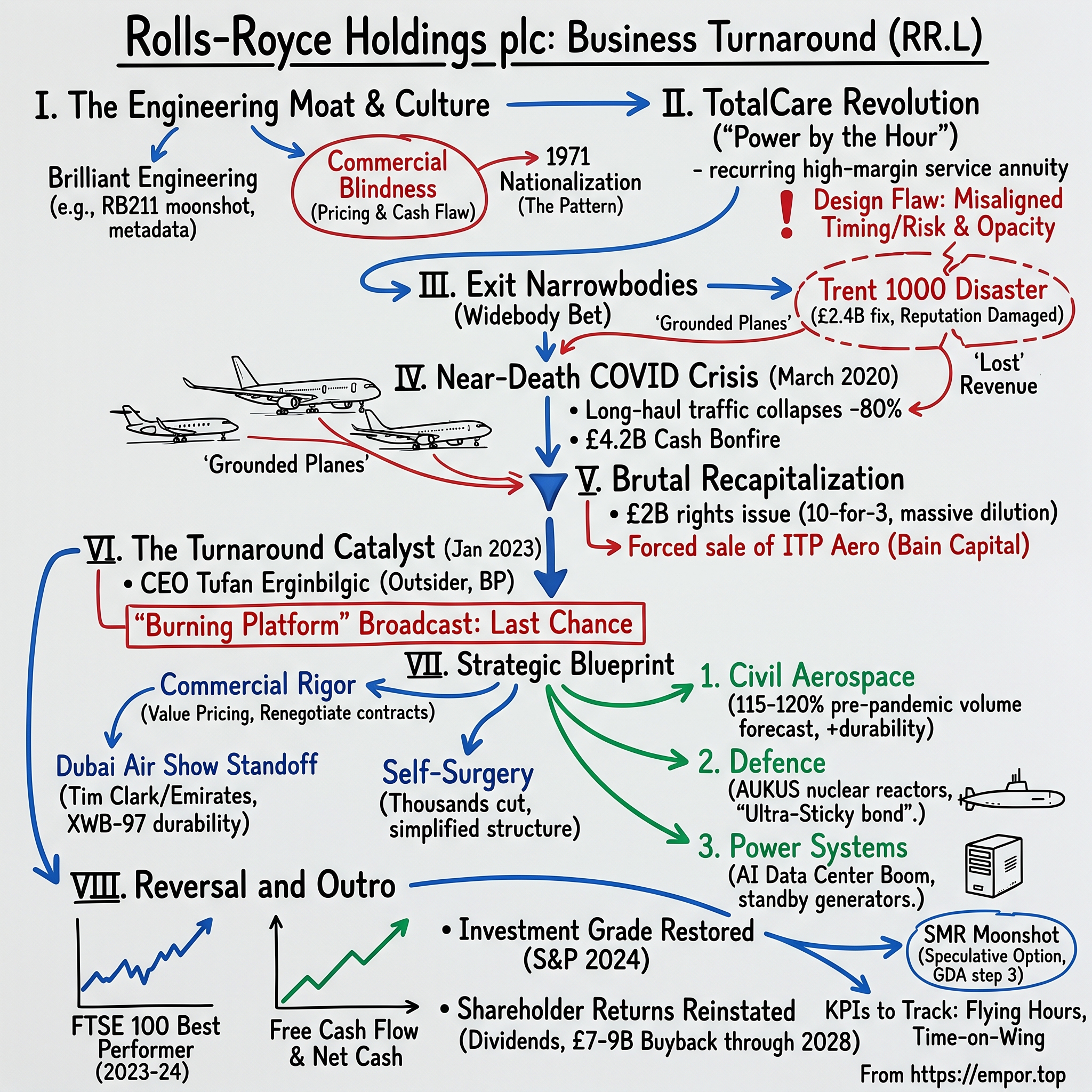

Picture a Tuesday morning in late January 2023. A newly installed chief executive, barely three weeks into the job, stands before an internal broadcast camera at Rolls-Royce and tells 42,000 engineers, machinists, and managers something no British corporate leader is supposed to say out loud about a national treasure: you are standing on a "burning platform." Their company, he said, had for years been "destroying value," delivering financial performance that was simply "unsustainable." This was not a struggling start-up. This was the maker of the engines under the wings of the world's most advanced widebody jets, the builder of the nuclear reactors that power Britain's submarines, an institution woven into the country's self-image since 1906. And its new boss was telling them, in effect, that the whole thing was on fire.45

That scene is the hinge of one of the most dramatic corporate reversals in modern industrial history. In 2020, Rolls-Royce burned through £4.2 billion of cash in a single year and came within touching distance of insolvency.13 By the 2025 financial year, reported in February 2026, it generated £3.3 billion of free cash flow, sat on £1.9 billion of net cash, and posted a group operating margin of 17.3%.1 Its shares were the single best performer on the FTSE 100 in both 2023 and 2024. A company that had been left for dead had become one of Europe's most talked-about industrial compounders.

To grasp how violent that reversal was in market terms: an investor who bought Rolls-Royce shares near the pandemic lows and held on saw one of the great multi-year re-ratings in modern European equities, as a stock left for dead compounded into a FTSE 100 leader. That is the kind of return that makes people believe in miracles — and precisely the kind of narrative a neutral analyst should interrogate hardest, because the line between a genuine structural transformation and a well-timed cyclical bounce is exactly where investors lose the most money by assuming the answer.

Here is the paradox at the heart of the story. Rolls-Royce has, for a century, been globally synonymous with uncompromising engineering. It solves thermodynamic and metallurgical problems that almost no one else on Earth can solve — designing a machine that spins at thousands of revolutions per minute, runs hotter than the melting point of the metal its blades are made from, and does so reliably for tens of thousands of hours at 40,000 feet. And yet, again and again, that same company was brought to its knees — not by a lack of technology, but by a structural blindness to cash, pricing, and the brutal arithmetic of long-cycle contracts. The engineering was never the problem. The commerce was. That single sentence is the thesis of this entire episode, and everything that follows is the evidence for it.

The pivot point is a man named Tufan Erginbilgic, a hard-nosed former BP downstream executive who arrived with no aviation background and no sentimental attachment to the Rolls-Royce mystique — which turned out to be exactly the point. His weapon was not a new engine. It was a spreadsheet and the willingness to walk away from bad deals.

To understand how he did it, and whether it lasts, we need to understand the three pillars the company actually stands on:

- Civil Aerospace — a genuine widebody engine duopoly, one of only two Western firms that can build a large jet engine, with an aftermarket moat measured in decades.

- Defence — sticky, national-security-critical work: fighter engines, and above all the nuclear propulsion plants for the Royal Navy's submarines, now supercharged by the AUKUS pact.

- Power Systems — the "silent engine" of the group, an industrial power business quietly riding the biggest energy story of the decade: the AI data-center build-out.

Over the next sections we will unpack how a firm this good at engineering could be this bad at capitalism for so long: the origin of the moat and the flaw baked into it, the fateful decision to abandon the narrowbody market, the Trent 1000 durability disaster, the near-death pandemic recapitalization, and finally the pricing-and-capital-allocation masterclass that followed. Throughout, we will keep an independent posture. Management says it has permanently re-rated the business. Our job is to ask what evidence supports that — and what could still break it.

II. The Engineering Heritage: Split of the Crown Jewels

The founding myth is almost too neat. In 1904, Charles Rolls — an aristocratic motoring enthusiast and one of the first Britons to own a car — was introduced over lunch in Manchester to Henry Royce, a self-taught engineer of obsessive perfectionism who had built a quiet, beautifully made motorcar because he found the ones he could buy shoddy. Rolls could sell; Royce could build. Their partnership was formalized in 1906, and the credo that emerged — "Take the best that exists and make it better" — would calcify, over a century, into both the company's greatest asset and its most expensive vice.

We will move quickly through the deep history, because the relevant lesson is cultural, not chronological. In the First World War, Royce turned his perfectionism to aero engines, and the Eagle powered the first non-stop transatlantic flight. In the Second, the Merlin engine — in the Spitfire and Hurricane, and later the American P-51 Mustang — became one of the defining pieces of hardware of the air war. By mid-century, Rolls-Royce was not merely a British company; it was a piece of British identity, the physical proof that a rain-soaked island could out-engineer anyone.

Then came 1971, and the lesson that still echoes through every page of this story. The company had bet its future on the RB211, a next-generation turbofan for the Lockheed L-1011 TriStar, an American widebody. To win the contract, Rolls-Royce had done two things that should sound eerily familiar by the end of this article: it priced the engine aggressively to secure the airframe slot, and it promised a technical leap it had not yet proven. The centerpiece of that leap was Hyfil, a revolutionary carbon-fiber composite fan blade — light, strong, and, on paper, a generation ahead of anyone else. It was exactly the kind of moonshot metallurgy at which Rolls-Royce believed itself unrivalled.

The blades shattered. Under bird-strike testing — the standard requirement that an engine survive a goose being fired into it at takeoff speed — the composite fan blades disintegrated, forcing an expensive, humiliating retreat to conventional titanium and blowing a hole in the weight and performance targets the whole contract was built on. Development costs ran wildly over the fixed price Rolls-Royce had agreed. In February 1971, the company that built the Merlin declared bankruptcy. Edward Heath's Conservative government — a free-market administration ideologically opposed to bailing out failing businesses — nationalised it within days, because the alternative, letting Britain's strategic aero-engine base and its defence supply chain collapse, was politically and militarily unthinkable. That single fact — that the British state would not, could not, let Rolls-Royce die — is a subsidy of confidence the company has drawn on ever since, and one worth remembering when we get to 2020. It is also the first appearance of the pattern that defines the company: brilliant engineering ambition, undone not by the engineering but by the commercial terms wrapped around it.

The nationalisation forced a divorce. In 1973 the luxury car division was hived off as Rolls-Royce Motors — the Spirit of Ecstasy, the Silver Shadow, the world that most people picture when they hear the name. That business would eventually be carved between BMW (which won the rights to the Rolls-Royce marque) and Volkswagen (which took Bentley and the Crewe factory). The aero-engine and industrial business — the actual subject of this story — remained in state hands until Margaret Thatcher's government privatised Rolls-Royce plc in 1987.

The car and aero businesses had never really been the same company in spirit, only in name. The cars were about craftsmanship and status; the engines were about pushing the outer edge of the physically possible. But they shared, and passed down, a single inheritance: the conviction that being the best was self-justifying, that a Rolls-Royce commanded respect and therefore did not need to grub around over price. In the luxury-car world, that instinct is a business model — scarcity and mystique are the product. In the aero-engine world, sold to hard-nosed airline procurement departments squeezing every cent out of their fleet costs, the same instinct was a slow leak.

What survived the split, then, was a culture. An engineering-first, problem-obsessed, quality-at-any-cost DNA that could design a jet engine to survive being fired at 40,000 feet for twenty-five years — and that was, in the same breath, almost totally indifferent to whether the contract underneath that engine actually made money. The prestige of the name may even have made things worse, breeding a complacency that a hungrier, less celebrated company could never have afforded. Rolls-Royce built the best. It just never learned, until very recently, to charge for it. That tension is the engine of everything that follows — and it found its purest expression in a billing model the company invented in the 1990s.

III. The Engine Flying Hour & TotalCare Revolution: Helmer's 7 Powers

Here is a genuinely brilliant idea, and a genuinely dangerous one, wearing the same suit.

For most of aviation history, an engine maker sold you an engine and then sold you spare parts when it broke — a transactional, unpredictable, faintly adversarial relationship. In the late 1990s, Rolls-Royce turned that model inside out with a program it branded TotalCare, built on a deceptively simple pricing concept: "Power by the Hour." The airline no longer bought maintenance piecemeal. Instead it paid Rolls-Royce a fixed dollar rate for every hour each engine spent flying — an "engine flying hour," or EFH. Rolls-Royce, in return, took on the entire burden of keeping that engine healthy: the overhauls, the shop visits, the spare parts, the durability risk, all of it, for the twenty-plus-year life of the aircraft.

To see why this created such a formidable competitive position, it helps to run it through Hamilton Helmer's "7 Powers" framework, which asks not "is this a good business?" but "what specifically prevents a competitor from taking the profit away?"

Switching costs are the primary power here, and they are enormous. When an airline chooses an engine for a specific airframe — say, the Trent XWB for the Airbus A350 — it is not making a purchase. It is entering a marriage. Every subsequent overhaul, every spare blade, every service technician, every data feed flows through Rolls-Royce's proprietary ecosystem for the entire operational life of that fleet, which can stretch a quarter-century. You cannot re-engine an A350 with a competitor's product; the engine and the airframe are certified as one. Once the choice is made, the airline is locked in, and Rolls-Royce holds a two-decade annuity. The analogy is the razor and the blade, except the razor lasts twenty-five years and the customer physically cannot buy anyone else's blades.

Scale economies are the powerful secondary force. Designing, certifying, and industrialising a modern high-bypass turbofan costs billions of dollars and takes the better part of a decade, with no revenue until the thing flies. That upfront wall is so high that only two Western companies can clear it for widebody engines: GE Aerospace and Rolls-Royce. (Pratt & Whitney sits largely on narrowbodies.) This is not a market where a well-funded start-up disrupts the incumbents. The barrier to entry is measured in decades and tens of billions.

So far, so wonderful — a locked-in customer, a two-player market, recurring high-margin service revenue. This is the moat that value investors dream about. And yet TotalCare, as originally structured, contained a design flaw that would nearly destroy the company twice.

The flaw was misaligned timing and misaligned risk. To build the installed base — to win the airframe slot in the first place — Rolls-Royce routinely sold the engine itself at a loss or on wafer-thin margins, betting on decades of service cash to make the economics work. That is a perfectly rational bet in a stable world. But it front-loaded all the cost and back-loaded all the profit, creating a yawning gap between when cash went out and when it came back. Worse, under a flat per-hour rate, Rolls-Royce absorbed every operational downside — if an engine turned out to be less durable than promised and needed more shop visits, that was Rolls-Royce's problem, not the airline's — while its upside on each contract was effectively capped at the agreed rate. The company had written itself an insurance policy against its own engineering mistakes, and priced the premiums as if it would never make any.

And then there was the accounting, which deserves a moment because it is where the model did its most quiet damage. Under the long-term service agreements, Rolls-Royce had to make assumptions today about events twenty years away — how many hours each fleet would fly, how much each overhaul would cost in 2035, how durable an engine would prove over a lifetime it had not yet lived. Those assumptions fed into "contract assets" and deferred balances on the balance sheet, and small changes in them could swing reported profit by hundreds of millions of pounds without a single pound of cash moving. Think of it as a builder booking the full profit on a twenty-five-year maintenance contract on day one, based on a guess about how often the roof will leak over the next quarter-century — and then discovering, a decade in, that the roof leaks far more than assumed.

The mismatch between engine deliveries, deferred service revenue, contract assets, and long-dated cash flows produced financial statements so labyrinthine that even sophisticated analysts struggled to say what the business actually earned in a given year. Reported profit and real cash generation could diverge for a decade at a stretch. For years this opacity flattered the story; it let the company book optimistic paper profits on contracts whose cash economics were, in truth, deeply uncertain. When Rolls-Royce eventually moved to cleaner accounting standards, the scale of the previously flattering assumptions became painfully visible. The moat was real. But the model built on top of it obscured exactly how much — or how little — that moat was being monetised, which is a dangerous thing for any management team, because you cannot fix a problem you cannot see on your own income statement. To understand how that latent risk became an actual catastrophe, we have to follow the company as it deliberately walked away from the safest cash flows in aviation.

IV. Exiting the Narrowbodies: The Widebody Bet and the Trent 1000 Crisis

In 2011, Rolls-Royce made a decision that looked, at the time, like disciplined focus, and looks now like betting the company on a single roll of the dice.

It sold its 32.5% stake in International Aero Engines (IAE) — the consortium behind the V2500 engine that powered thousands of Airbus A320-family narrowbody jets — to partner Pratt & Whitney for $1.5 billion, a deal announced in 2011 and completed in June 2012. Rolls-Royce retained a stream of payments tied to future V2500 flying hours for fifteen years, so it did not walk away empty-handed. But strategically, it had made a choice: it was getting out of the single-aisle business to concentrate its capital and engineering firepower on the large widebody market.10

The logic was seductive. Widebody engines are bigger, more complex, higher-value, and carry richer aftermarket economics. Long-haul international travel was booming. Why fight in the commoditised, price-competitive narrowbody scrum when you could own the premium end? Double down on the crown jewels.

Here is what that logic missed. The narrowbody market — the Airbus A320 and Boeing 737 families — is the workhorse of global aviation. It is enormous, high-volume, and, crucially, resilient. Domestic and short-haul flying recovers first after any shock and is far less exposed to the specific cocktail of risks that hammer long-haul: geopolitics, fuel-price spikes, visa regimes, and — as the world would shortly learn — pandemics. By exiting narrowbodies, Rolls-Royce turned itself into something rare and dangerous: a pure-play bet on international long-haul widebody traffic. Its competitors kept a foot in both camps. GE, Pratt & Whitney, and Safran continued to harvest the steady, high-volume cash flows of the single-aisle fleets. Rolls-Royce had sold its umbrella just before the storm.

Within the widebody world, the map settled into a clear pattern. GE Aerospace locked up the Boeing side — exclusive on the 777 and forthcoming 777X, and the dominant choice on the 787 Dreamliner. Rolls-Royce built its fortress on Airbus: exclusive on the A350 with the Trent XWB, and the sole engine on the re-engined A330neo with the Trent 7000. Two giants, each entrenched on its preferred airframer, meeting head-to-head only occasionally. A comfortable duopoly — provided your engines actually worked as advertised.

The exclusivity is worth dwelling on, because it is a genuine double-edged sword. Being the only engine option on the A350 means every single A350 ever built, and every one that will be built for decades, carries Rolls-Royce metal and feeds the Rolls-Royce aftermarket. There is no competitor splitting the fleet, no share to lose to a rival on that airframe. But it also means Rolls-Royce's civil fortunes are welded to the commercial success of specific Airbus programs and to the health of the long-haul routes those aircraft fly. If the A350 sells well and long-haul thrives, Rolls-Royce prints money. If either falters, there is no diversification to cushion the blow. Exclusivity concentrates the upside and the downside in equal measure — and Rolls-Royce had just concentrated its entire civil future into that single, cyclical basket.

Which brings us to the Trent 1000, the engine that shared the 787 Dreamliner with GE's GEnx, and the disaster that turned a manageable rivalry into a rout.

Beginning around 2016, operators of Trent 1000-powered 787s began reporting a cascade of durability problems: cracking and premature corrosion in turbine blades, compressor issues, blades wearing out far faster than designed. Because the affected components had to be inspected and replaced on aggressive schedules, aircraft piled up on the ground waiting for parts and shop slots. At the worst of it, dozens of 787s sat idle around the world. Airlines — All Nippon Airways, British Airways, LATAM and others — were furious, and they had every right to be: under the Power-by-the-Hour logic, a grounded plane flies no hours, so the durability failure hit Rolls-Royce twice, once in remediation cost and once in lost revenue. The direct fix-it bill alone climbed above £2.4 billion over several years.

The mechanism of the pain is worth making concrete, because it shows how the TotalCare model amplified an engineering problem into a financial one. Normally, a durability issue is the airline's headache — its plane, its downtime. But under Power by the Hour, Rolls-Royce had contractually promised to keep those engines flying and to bear the maintenance cost. So when the blades cracked early, Rolls-Royce had to design the fix, manufacture replacement parts at emergency pace, pay for the shop visits, and, in many cases, compensate airlines for aircraft it could not keep airborne. The company was, in effect, paying to repair its own mistake on hardware it had already sold, on a contract that gave it no ability to pass the cost on. Every crack was a direct hit to Rolls-Royce's cash, not the customer's.

The reputational damage cut deeper still. In the one widebody program where GE and Rolls-Royce competed head-to-head for the same airframe, Rolls-Royce's reliability stumble handed GE the argument. The GEnx captured the lion's share of new 787 orders, and Rolls-Royce's position on the Dreamliner withered. For a company whose entire moat rested on a promise — trust us with a twenty-five-year marriage because our engineering never fails — the Trent 1000 was a betrayal of the core brand asset. It is no coincidence that when Tim Clark of Emirates went looking for a stick to beat Rolls-Royce with years later, he reached for durability: the Trent 1000 had made "will it actually last?" the most powerful question any airline could ask. The crisis proved that the durability risk baked into TotalCare was not theoretical, and it left the company financially and reputationally weakened at the worst possible moment, walking straight into a black swan that would test whether it could survive at all.

V. The Near-Death Experience: COVID-19 and the Panic Recapitalization

In March 2020, the specific, concentrated risk that Rolls-Royce had spent a decade building into its business model detonated all at once.

COVID-19 did not merely slow aviation; it switched off the exact slice of aviation that Rolls-Royce depended on. Long-haul international travel — the widebody flying that generated engine flying hours — collapsed by more than 80% almost overnight. Borders slammed shut. A350s and 787s were flown to desert boneyards and parked. And because Rolls-Royce's civil revenue was, by design, tethered to EFH, its cash inflows did not decline. They evaporated.

This is the moment the elegant TotalCare model revealed its hidden fragility. The revenue was variable and had gone to zero. The costs were not. The vast fixed base of factories, engineering programs, and — still — the Trent 1000 remediation liabilities kept demanding cash regardless of whether a single engine turned in the sky. A business that had quietly transferred all the operational downside onto its own balance sheet now discovered what that meant when the downside arrived for every engine simultaneously.

The result was a cash bonfire. Rolls-Royce burned through £4.2 billion of free cash flow in 2020 — a figure that, for a company of its size, is not a bad year but an existential one.13 Management was staring at a genuine solvency question: could the maker of Britain's submarine reactors actually run out of money?

The rescue was brutal, and it was led by then-CEO Warren East, the former ARM Holdings boss who had been running Rolls-Royce since 2015. In October 2020, East executed one of the largest emergency recapitalizations in recent British corporate history: a package assembling roughly £5 billion of fresh liquidity, anchored by a deeply discounted £2 billion rights issue structured as a 10-for-3 offer — meaning existing shareholders had to stump up cash for ten new shares for every three they held, just to stand still. The share price fell to a seventeen-year low. On top of the equity came new bonds, a term loan, and access to UK Export Finance-backed guarantees.12 Existing holders who could not or would not follow their money were massively diluted. The company survived, but the equity base had been shattered.

Even that was not enough to satisfy the covenants and rebuild liquidity. To raise cash and reassure lenders, Rolls-Royce was forced to sell assets into the teeth of a depressed market — and the most painful of these was ITP Aero, its prized Spanish aero-engine components subsidiary, a genuinely strategic, growing business. In a deal completed in September 2022, ITP Aero went to a consortium led by Bain Capital for an enterprise value of roughly €1.8 billion.9

It is worth pausing on the price, because forced sales tell you something about who holds the leverage. On the numbers, ITP changed hands at an EV/EBITDA multiple in the low-to-mid teens — respectable in the abstract, but well shy of the 15-18x that high-quality aerospace suppliers commanded in healthier windows. This was a distressed seller in a distressed market parting with a strategic asset to protect the parent, and the buyer, a private-equity consortium led by Bain, knew it. Private equity's entire edge is patient capital and the ability to buy when public companies are forced to sell; ITP Aero was a textbook example. It plugged the balance sheet, but it permanently stripped out a fast-growing components business the company would have loved to keep — and handed the upside of any recovery to Bain rather than to Rolls-Royce shareholders.

There is a governance point buried here that a skeptical investor should notice. The company was diluting long-term shareholders through a deeply discounted rights issue and selling strategic assets cheap at the same time — the two most value-destructive things a business can do, both forced by the same liquidity crisis. That is not a criticism of Warren East, who was playing a bad hand as well as anyone could and whose recapitalization genuinely saved the company. It is a reminder of what the pre-2023 business model had built up: a balance sheet so fragile that a single demand shock left the board with no good options, only survivable ones. That is the real cost of the pandemic for Rolls-Royce: not just the £4.2 billion of cash it burned, but the crown jewel it had to sell to stop the bleeding, and the shareholder value it had to torch to raise equity at the bottom. The company that emerged in 2022 was solvent, diluted, smaller, and demoralised — a burning platform, as its next leader would put it, even if the fire was no longer visible from outside.

VI. The Turnaround Catalyst: Tufan Erginbilgic & BP's Downstream Playbook

When the Rolls-Royce board went looking for Warren East's successor, they did something the institution had rarely done. They hired an outsider with no aerospace pedigree at all.

Tufan Erginbilgic is a Turkish-born, chemical-engineering-trained executive who spent more than two decades at BP, rising to run its Downstream division — the refining, trading, and retail-fuels business — where he built a reputation for wringing hard cash returns out of complex, capital-heavy operations, reportedly doubling the division's earnings and sharply lifting returns during his tenure. That background matters. Downstream oil is a business where you do not control the price of your feedstock or, often, your product; you survive by relentless operational discipline, by pricing every marginal molecule correctly, and by an absolute focus on cash return on capital. Erginbilgic arrived at Rolls-Royce in January 2023 fluent in exactly the language the company had never learned to speak.

He did not ease in. Within weeks he delivered the "burning platform" broadcast that opened this story, telling staff the company's historical performance was "unsustainable," that it had been "destroying value" relative to peers, and — the line that stung most inside a proud engineering culture — that this was, in his words, "our last chance."4 To the British establishment, publicly savaging a national champion looked reckless, even disloyal. Commentators noted, however, that it was precisely the shock the organisation needed: a leader with no emotional investment in the mythology, willing to name the problem out loud.5 Complacency, in a firm that had twice been saved from its own hubris, was the enemy.

There is a deeper reason his outsider status mattered, and it goes to how engineering cultures fail. A lifer promoted from within Rolls-Royce would have carried the same unspoken assumptions that had accreted over a century: that winning the airframe slot was victory in itself, that the aftermarket would eventually justify any concession, that being the best engineers in the room was the same thing as running the best business. Those assumptions were not stupid; they were how the company had always understood itself. But they were exactly what needed to be challenged, and a person who shares a culture's assumptions is the last person who can see them, let alone break them. Erginbilgic could look at a beloved TotalCare contract and see, without sentiment, that it was a loss-making obligation dressed up as a strategic asset. His ignorance of the mythology was his most valuable qualification.

He brought a partner in the numbers. Helen McCabe, also an alumnus of BP, joined as chief financial officer, and the two aligned the top of the house around a single, unfamiliar idea: capital has a cost, and every contract, every program, and every product must earn a return above it. The message was not "sell more engines." It was "make more money." In a company where the highest status had always belonged to the engineers who solved the hardest physics, this was a quiet cultural revolution — a reassertion that the finance function's questions were not an obstacle to good engineering but a discipline that made it worth doing.

The playbook that followed had a name inside the company — "commercial rigor" — and a philosophy: value-based pricing over volume. For decades Rolls-Royce had chased market share, winning airframe slots at any price to build the installed base, trusting the aftermarket to bail out the economics later. Erginbilgic tore that up. If a deal did not clear the return hurdle, the company would walk away from it. It began refusing low-margin engine sales and, more aggressively, reopening and renegotiating the terms of existing long-term service agreements to claw back pricing that had been given away too cheaply.

The most public test of this resolve came from a very loud customer. At the 2023 Dubai Air Show, Sir Tim Clark, the formidable president of Emirates, launched a broadside at Rolls-Royce, publicly questioning the durability of the Trent XWB-97 — the higher-thrust engine variant for the Airbus A350-1000 — in the punishing heat and sand of the Gulf, and making clear Emirates would not order the aircraft unless Rolls-Royce improved the engine and its maintenance economics.6 For a company still nursing the Trent 1000 scars, a durability attack from one of aviation's most influential buyers was a direct threat.

Erginbilgic did not fold. He publicly defended Rolls-Royce's pricing, insisting the company would not sign business that failed to deliver an appropriate return, and framed the standoff as a matter of principle: premium engines command premium prices.7 This was the turnaround thesis made flesh — the willingness to alienate a marquee customer to protect margin, the exact opposite of the old share-at-any-cost instinct.

It is worth being precise about what the Emirates fight does and does not prove, because it is easy to romanticise. Standing firm on price is admirable discipline if the engine is genuinely worth the premium and the customer eventually pays it. It is a strategic blunder if the durability concern is real and unaddressed, and the customer simply buys someone else's aircraft — as Emirates has signalled it might, favouring Boeing's GE-powered 777X. The standoff is therefore not a clean win for management; it is an open wager. Rolls-Royce is betting that its XWB-97 durability upgrades will satisfy Emirates before the lost order becomes permanent, and that other A350 customers will accept the pricing precedent it is defending. As of mid-2026 that wager was still live and unresolved, which is exactly why a neutral observer should file it under "conviction being tested," not "vindication."

Underneath the headline fights ran a quieter, equally important program of self-surgery: thousands of non-manufacturing and middle-management roles eliminated, procurement centralised, duplicated engineering functions stripped out, and a simplification of a bloated organisational structure that had accumulated layer upon layer over decades. The point of the de-layering was not merely to cut cost; it was to change the metabolism of the company — faster decisions, clearer accountability, and a cost base lean enough to convert the moat's revenue into actual cash rather than into overhead. There is a risk in this too, and it is a real one for an engineering company: cut too deep into technical talent and institutional knowledge, and you can win this year's margin at the expense of the next decade's engine programs. So far the evidence suggests the cuts fell mainly on bureaucracy rather than on engineering capability, but it is a balance that bears watching. Whether all of this genuinely changed the economics, or merely flattered a cyclical recovery in flying hours, is the question the segment numbers can begin to answer.

VII. Segment-Level Deep-Dive: Civil, Defence, and the Power Systems Boom

Before diving into the three businesses, it is worth anchoring the whole story in one line of numbers, because it captures the transformation more starkly than any adjective. Group underlying operating profit went from £652 million in 2022 — a thin 5.1% margin — to £2,464 million in 2024 at a 13.8% margin, and then to roughly £3.46 billion in 2025 at a 17.3% margin.12 In three years, the profit pool more than quintupled and the margin more than tripled. The question every serious investor should ask is where that came from, and how durable it is. So let us open the hood on each segment.

1. Civil Aerospace (The Primary Value Driver)

This is the engine of the turnaround, in both senses. Civil Aerospace — the Trent widebody family plus a lucrative business-aviation franchise (the BR700 and newer Pearl engines for long-range private jets) — swung from a barely-there 2.5% operating margin in 2022 to 16.6% in 2024 and then 20.5% in 2025.1 An eight-fold expansion in margin over three years is not a rounding error; it is a different business.

How did they do it? Three levers, all pulling the same direction. First, volume recovery: large-engine flying hours climbed back toward and past pre-pandemic levels as long-haul travel healed, and the guidance for 2026 is for flying hours at 115-120% of 2019 levels — the annuity switched back on and then some.1 Second, price: the value-based pricing discipline and the renegotiation of TotalCare terms flowed straight through to the aftermarket, so each of those recovered flying hours now earns more than it used to. Third, and most elegantly, durability: the engineering programs to extend "time-on-wing" — how long an engine stays under a plane before it must come off for overhaul — directly lower Rolls-Royce's own maintenance liability under the Power-by-the-Hour model. A more durable engine means fewer shop visits, which means less cost that Rolls-Royce has to absorb, which means more of each flying-hour dollar drops to cash. The very risk that nearly sank the company in the Trent 1000 era, once inverted, became a margin tailwind.

There is a fourth, quieter contributor worth naming: business aviation. The BR700 and newer Pearl engines power ultra-long-range private jets — Gulfstreams and the like — a market that proved far more resilient through the pandemic than commercial widebodies, because the wealthy kept flying privately when everyone else was grounded. It is a smaller slice of Civil, but a high-margin, less-cyclical one that helped steady the segment while the big Trents were parked in the desert.

The honest caveat: a meaningful part of this is cyclical. Flying hours recovered because the world reopened, not solely because of management genius. A useful way to think about it is that the recovery in traffic filled the reservoir, but the pricing and durability changes widened the pipe through which each unit of traffic converts into cash — and only the second of those is structural. Separating the structural gains (pricing, durability, cost) from the cyclical ones (traffic) is the central analytical challenge in valuing Rolls-Royce today, and it is why the sustainability of that 20.5% margin — not its existence — is the real debate. The bulls point to the durability programs and the renegotiated contracts as evidence the pipe is genuinely wider; the bears note that we have not yet seen this cost structure tested through a real downturn in flying hours. Both are, for now, partly right.

2. Defence (The Ultra-Sticky Moat)

If Civil is the growth story, Defence is the ballast — and, arguably, the most defensible franchise in the entire group. Its margins barely moved through the chaos: 11.8% in 2022, 14.2% in 2024, 14.4% in 2025.12 That stability is the point. Defence does not fly on holiday, so it did not collapse in the pandemic; it is the diversification that kept the group breathing while Civil was dark.

The portfolio spans the EJ200 that powers the Eurofighter Typhoon, the lift system for the vertical-landing F-35B — the clever piece of engineering that lets a supersonic stealth fighter hover and land like a helicopter — and engines for military transport aircraft. But the true crown jewel, and one of the widest moats in global industry, is nuclear submarine propulsion. Rolls-Royce is the sole provider of the nuclear reactors that power the Royal Navy's submarine fleet: the Astute-class attack boats, the Dreadnought-class ballistic-missile submarines that carry Britain's continuous-at-sea nuclear deterrent, and now the multi-decade, tri-national AUKUS program to build a new submarine class with Australia and the United States.

Consider why this moat is essentially unassailable. There is no competitor — no other British entity has the capability, and no government would import so sensitive a technology. There is no substitute; a submarine reactor is not a product you can re-tender. The customer is a sovereign state that treats the capability as existential to national survival, which means the price is set by strategic necessity rather than by a competitive bidding war. And the contracts run for decades, often with cost-recovery structures and government backing that insulate Rolls-Royce from the cyclical shocks that batter the civil business. In Helmer's terms this is switching costs and scale economies fused with something even rarer — a national-security dependency that no procurement officer would ever dream of putting out to open tender. The AUKUS pact, in particular, extends the visibility of this backlog well into the second half of the century and pulls in the industrial weight of the United States and Australia. For a long-term investor, Defence is the part of Rolls-Royce that is closest to a bond with an engineering department attached: lower-growth than Civil, but with a durability of cash flow the civil business can only envy. The tradeoff is that it will never grow at hyperscale rates — which is precisely why the third segment has become so interesting.

3. Power Systems (The Data Center Secular Tailwind)

And then there is the business almost nobody was talking about three years ago, which has become the most exciting secular story in the group. Power Systems is built around MTU Friedrichshafen, the storied German maker of large high-speed diesel and gas engines and power-generation systems. Rolls-Royce first took a stake in the parent (then Tognum) and completed the story in 2014 by buying Daimler's remaining 50% for €2.43 billion — a full price at roughly 14x EBITDA, but one that secured a high-quality industrial platform outright.11 Its margins tell their own recovery tale: 8.4% in 2022, 13.1% in 2024, 17.4% in 2025.12

What lit the fire under Power Systems was, of all things, artificial intelligence. Here the technology is worth explaining plainly, because it is the crux of the story. A large AI data center is essentially a warehouse full of tens of thousands of power-hungry chips training and running models, and it cannot tolerate even a momentary loss of power — a few seconds of blackout can corrupt a training run that cost millions to compute and take the facility offline. Grid power, however reliable, is never guaranteed to that standard. So every serious data center backs itself up with banks of large standby generators — diesel or gas engines that spin up the instant grid power wavers — sized to carry the entire facility. MTU's high-power units are exactly the industrial-grade product the hyperscalers and colocation operators want, and they buy them in quantity, because the cost of a generator is trivial next to the cost of an outage.

The result is that a business which for decades tracked ordinary industrial GDP suddenly found itself bolted onto the single fastest capital-spending wave of the decade. As AI data-center construction exploded, so did orders for backup power, and MTU's order book and margins climbed with it. This has become a genuine second engine of high-margin cash flow and, just as importantly, it materially diversifies the group away from aviation cyclicality — Power Systems does not care whether long-haul travel is up or down. It is the closest thing Rolls-Royce has to a pure play on the AI infrastructure theme, hiding inside a century-old aero-engine company.

The skeptic's note: data-center backup demand is real and large, but it is also a capex cycle, and capex cycles turn. Power Systems' recent margins ride both operational improvement and an unusually hot end-market. It is a powerful tailwind — but a tailwind, not a law of nature. Which is precisely the right lens to bring to the group's most speculative bet of all.

VIII. SMRs & Clean-Tech: Speculative Optionality vs. Core Realities

Every turnaround eventually faces a temptation: to take the cash the core is finally throwing off and pour it into a moonshot. Rolls-Royce's moonshot is nuclear — and, so far, management has kept it on a notably short leash.

Small Modular Reactors (SMRs) are the headline. The idea is to build compact, factory-manufactured nuclear power stations — Rolls-Royce's design is rated at 470 megawatts of electrical output — that can be produced repeatably and dropped onto sites far faster and cheaper than the vast one-off mega-projects that have made conventional nuclear a byword for cost overruns. The strategic logic for Rolls-Royce is unusually credible, because the company has been building safe, compact nuclear reactors for submarines for over half a century. This is not a company wandering into an unfamiliar science; it is one of the few private entities on Earth with a live, multi-decade nuclear engineering pedigree.

The program has real momentum. The Rolls-Royce SMR design entered Step 3 — the final phase — of the UK's Generic Design Assessment (GDA), the Office for Nuclear Regulation's rigorous multi-year review of a reactor's safety and design, having progressed there in 2024 with the overall assessment expected to complete around 2026.15[^16][^17] And in 2025, Rolls-Royce SMR was selected as the preferred bidder in the UK government's competition to build the country's first fleet of small modular reactors — a genuine anchor customer and validation.15

But here is where the independent posture matters most. For all the excitement, SMRs today represent a minimal slice of revenue and, in cash terms, are a net investment drag — Rolls-Royce is spending on the program, not harvesting from it. Commercial power generation at scale is years away, contingent on regulatory sign-off, project financing, planning permission, and first-of-a-kind construction risk that the nuclear industry has a long, painful history of underestimating. Every major Western nuclear project of the past two decades has run late and over budget; "modular" and "factory-built" are the industry's answers to that curse, but they are promises, not yet proof. The correct way to size SMRs in a valuation today is as an option — potentially valuable, genuinely strategic, but speculative and unpriced — that must not be allowed to distract from the engine margins actually paying the bills. The moment SMR spending starts eating into group free-cash-flow discipline, or the moment management starts talking about it as a core earnings driver rather than a long-dated option, the thesis changes and the skeptic's antennae should rise. For now, the reassuring signal is that management itself frames SMRs modestly, and has structured the venture to draw heavily on UK government co-funding rather than on Rolls-Royce's own balance sheet.

The revealing counterpoint is what Erginbilgic did with the other futuristic projects. Under his "operational focus" doctrine, Rolls-Royce pulled back from or divested speculative electric and hybrid-aviation ventures — the zero-emissions flight demonstrators that had absorbed R&D capital and management attention with no near-term return. That decision tells you something important about the current regime's priorities: immediate cash returns over far-future novelty, discipline over dazzle. It is the clearest signal that the pricing revolution and the cost surgery are not tactics but a genuine change in what the company values — which is exactly the raw material for the broader lessons this story offers.

IX. Playbook: Key Strategic & Investing Lessons

Step back from the specifics, and Rolls-Royce delivers four lessons that travel well beyond aerospace.

Lesson 1: Engineering excellence is meaningless without commercial discipline. This is the thesis of the whole story. You can build the most thermodynamically efficient, most durable engine in the world, but if you price it on cost-plus habit rather than the value it delivers, and if you sign twenty-five-year service contracts with thin, non-inflation-protected margins, you are not running a business — you are quietly transferring your shareholders' wealth to your customers. For decades, Rolls-Royce's airline customers captured much of the value that Rolls-Royce's engineers created. The turnaround did not require a better engine. It required someone to charge properly for the engines they already had.

Lesson 2: "Power by the Hour" is a double-edged sword. Recurring, high-margin service revenue tied to usage is a beautiful thing in a stable macro environment — predictable, sticky, compounding. But a contract that hands you all the operational downside (durability misses, engine wear, a global travel ban) while capping your upside is not an annuity; it is a short volatility position wearing an annuity's clothes. It pays steadily right up until the tail event, and then it pays catastrophically the wrong way. The genius of the model and the flaw of the model were the same feature, viewed in different weather.

Lesson 3: Beware cyclical exclusivity. By selling its narrowbody position to focus on premium widebodies, Rolls-Royce converted itself into a leveraged bet on one of the most cyclical, shock-prone slices of the global economy — long-haul international travel. Focus felt like strength; it was concentration risk. What saved the company when that bet blew up was precisely the diversification the widebody strategy had de-emphasised: the steady cash of Defence and the industrial breadth of Power Systems. Concentration magnifies returns in the good years and can be fatal in the bad ones.

Lesson 4: A "burning platform" turnaround needs an agent willing to break the furniture. Legacy engineering champions rot from cultural complacency, not technical failure. Reversing that requires a leader psychologically free enough to insult a national institution to its face, to stare down a marquee customer in public, and to kill beloved pet projects. Erginbilgic's outsider status — no aerospace romance, no debts to the old guard — was not a gap in his résumé. It was the qualification. The lesson for investors watching other stagnant incumbents: the right change agent is often the one the existing culture would never have chosen.

There is a meta-lesson that ties the four together, and it is the most useful one for investors screening other companies. A great business can hide a broken one inside it for a remarkably long time, especially when a wide moat and a proud history mask weak commercial discipline. Rolls-Royce's moat was never in doubt; its returns on capital were dismal for years anyway. The mispricing opportunity — the reason the stock could rise so far so fast once the change came — existed precisely because the moat and the returns had been decoupled for so long that the market had stopped believing they would ever reconnect. When a genuinely advantaged business is being run without commercial rigor, the arrival of a manager who supplies the missing discipline can release enormous latent value very quickly, because the raw material was there all along. The trick, and the danger, is telling the difference in advance between a business that is under-earning its moat and one that simply has no moat and a good excuse.

Those lessons are the abstract. The concrete question for anyone weighing the stock today is whether the improvement is a new plateau or a cyclical peak — which is where the bull and bear cases collide.

X. The Investment-Story Spine: Bull vs. Bear & Activated Stress Test

Let us war-game this honestly, because a story this good invites confirmation bias, and the whole point of an independent platform is to resist it.

The bull case rests on the claim that Rolls-Royce has undergone a structural, not merely cyclical, re-rating. The evidence is not trivial. Group operating margin above 17%, £3.3 billion of free cash flow, and a swing from a diluted, near-insolvent balance sheet to £1.9 billion of net cash are hard facts, not projections.1 The balance-sheet repair matters for a reason that compounds: investment-grade credit ratings were restored across all three major agencies during 2024 — S&P returned the company to investment grade in March 2024 for the first time in years.14 A better rating lowers the interest rate the company pays on its debt, which frees up cash, which strengthens the balance sheet further, which supports the rating — a virtuous circle that is the exact inverse of the doom loop the company was trapped in during 2020, when a collapsing balance sheet threatened to raise its cost of capital just as it most needed cheap money. Regaining investment grade also reopened the door to shareholder returns. Dividends were reinstated at the 2024 results and lifted to 9.5 pence for 2025, alongside a completed £1 billion buyback and a new multi-year buyback program of £7-9 billion running through 2028.12 On top of that sit two genuine secular tailwinds — AI-driven data-center power demand lifting Power Systems, and an AUKUS-anchored defence backlog measured in decades — that are, crucially, independent of the civil-aviation cycle. If pricing discipline and durability gains prove permanent, the earnings base is real, and the company will have transformed from a leveraged bet on long-haul travel into a diversified industrial with three uncorrelated growth engines.

The bear case is not that the numbers are fake — it is that they may be near a peak. Widebody flying hours have recovered to above 2019 levels; by definition, that is a cyclical high, not a low, and a global recession would crater the very engine flying hours that drive Civil's cash. The supply chain remains fragile: shortages of parts and skilled labour have repeatedly delayed engine overhauls across the industry, which can cap the aftermarket volumes the bull case depends on. And the pricing strategy has a cost — the Emirates standoff is not resolved. At the June 2026 IATA meeting, Tim Clark reported "no progress," reaffirming that Emirates would not order the A350-1000 until the Trent XWB-97's durability in hot, dusty conditions was fixed, even as Rolls-Royce insisted its upgrade program would roughly double the engine's durability in such environments.8 Hold the line on price and you may protect margin at the cost of long-term share to GE Aerospace. Both cannot be maximised at once.

Run this through Porter's Five Forces and the picture sharpens. Barriers to entry are almost absolute — the two-player widebody structure and multi-decade certification cycle mean no new rival is coming. Rivalry is intense but rational: GE and Rolls-Royce compete fiercely for airframe slots but, once installed, both enjoy captured aftermarkets. Buyer power is the interesting force — individually, airlines are locked in by switching costs, but the very largest buyers, an Emirates or a major leasing company, retain real leverage at the point of engine selection, which is exactly the pressure Clark is applying. Supplier power has been an acute problem: a fragmented aerospace supply base has been a genuine constraint on output. Substitutes, in the classic sense, barely exist — until you remember that the ultimate substitute for a Rolls-Royce widebody engine is an airline choosing a GE-powered Boeing instead of an RR-powered Airbus.

Through Helmer's 7 Powers, the two dominant powers remain switching costs and scale economies, as laid out earlier. What is new — and this is the crux of the entire episode — is that a moat only produces returns if management is willing to charge for it. Rolls-Royce always had the powers. What it lacked, until 2023, was the pricing will to convert them into cash. That is less a new source of power than the belated exercise of an existing one, and it is inherently reversible: a future management could give the pricing back just as easily as this one took it.

On management credibility, the behavioural record is strong — the most persuasive part of the bull case, and worth scrutinising closely because credibility is the one asset a turnaround cannot fake for long. Erginbilgic and McCabe set mid-term 2027 targets at the November 2023 Capital Markets Day — £2.5-2.8 billion of operating profit, £2.8-3.1 billion of free cash flow, and a 16-18% return on capital — and then hit the profit target essentially two years early, delivering roughly £3.46 billion in 2025.31 Rather than declare victory, they raised the bar, upgrading the 2028 targets (previously framed around £3.6-3.9 billion of operating profit) to a materially higher £4.9-5.2 billion of operating profit and £5.0-5.3 billion of free cash flow at the 2025 results.1

What makes this more than a lucky streak is the consistency of the story across every touchpoint. The language of "commercial rigor," value-based pricing, and cash-return discipline that Erginbilgic used in the 2023 burning-platform broadcast is the same language running through the Capital Markets Day, the subsequent annual reports, and the earnings calls — a narrative that has not quietly shifted its goalposts or invented new metrics to flatter a miss. When management has had to explain the Emirates standoff or supply-chain constraints, it has generally done so in concrete terms rather than deflecting. A leadership team that sets specific numeric targets, beats them early, raises them, tells a consistent story across filings and calls, and simultaneously restores the dividend and returns capital has earned real analytical benefit of the doubt. Incentives reinforce it: the CEO's remuneration is heavily weighted toward long-dated equity, and disclosed shareholding requirements far exceed the usual norm, tying his personal outcome to the share price years out rather than to this year's bonus. The one caveat a skeptic would enter is that beating targets set at the bottom of a recovery is easier than sustaining performance at the top — credibility earned on the way up is tested, and only really proven, on the way down.

Where would an activist or skeptical short press? On four points. First, sustainability: prove that Civil's 20% margin survives the next downturn rather than being a reopening sugar-high. The margin has never been tested through a falling flying-hour environment under the new pricing regime, and a short would argue that the market is capitalising a peak-cycle number as if it were permanent. Second, the pricing-versus-volume tension: if walking away from deals like the A350-1000 quietly cedes the next generation of installed base to GE, today's fat margin is tomorrow's shrinking aftermarket, because in this business market share won today is the annuity harvested for the following twenty-five years. A short would frame Erginbilgic's discipline as mortgaging the long-term fleet for near-term optics. Third, capital allocation: a £7-9 billion buyback commitment is a strikingly bold promise for a company that was issuing deeply discounted equity to survive barely five years ago. Buying back stock at a re-rated, multi-year-high valuation, funded by peak-cycle cash flow, can destroy value as efficiently near a top as it creates value near a bottom — and it is the mirror image of the dilutive rights issue that so damaged shareholders in 2020. Fourth, the durability tail: the Trent 1000 and the XWB-97 questions are reminders that a single serious in-service failure can still, under the service-contract model, convert into a multi-hundred-million-pound cash liability with little warning.

None of these are red flags of mismanagement, and a fair-minded bear would concede that the track record cuts the other way. They are the legitimate stress tests that separate a durable compounder from a well-timed cyclical — and the honest answer today is that the evidence points toward genuine structural improvement, but not yet conclusively, because the one thing that would settle the debate, a full civil-aviation downturn met with the new cost structure and pricing discipline intact, has not yet happened.

Which points to the KPIs that actually matter — the three numbers a long-term owner should track above all others:

- Large Engine Flying Hours (fleet utilisation). This is the direct throttle on TotalCare aftermarket cash. When flying hours move, the cash engine moves with them.

- Civil Aerospace operating margin. The single cleanest test of whether the 20%-plus achieved in 2025 is a sustainable baseline or a cyclical peak. This is the number the entire bull-bear debate turns on.

- Average time-on-wing of the Trent XWB and Trent 1000. The unglamorous durability metric that quietly determines everything: longer time-on-wing means fewer shop visits, lower maintenance liability, and more cash retained per flying hour. It is where engineering excellence and cash generation finally meet on the same line of the model.

XI. Epilogue & Outro

Rolls-Royce is, in the end, a story about the gap between capability and capitalism — and about how long that gap can persist inside an institution too proud, and too protected, to close it.

For a century, this was a company that could do the hardest things in engineering and the easiest thing in business badly: charge for its work. It built the Merlin and went bankrupt on the RB211. It invented a brilliant service model and nearly died from its hidden flaw. It owned one of the widest moats in global industry and let its customers keep much of the value that moat created. The technology was never in doubt. The commercial nerve was.

The transformation of the last three years did not add a new source of power to the business. It did something rarer and, for investors, more instructive: it finally exercised the power that was there all along. That distinction is not academic. A company that invents a new moat is doing something extraordinary and unrepeatable; a company that finally charges properly for a moat it already owned is doing something that, in principle, any disciplined successor could sustain — or any complacent one could squander. Which of those two futures Rolls-Royce grows into will be decided not in a wind tunnel but in the pricing meetings, the capital-allocation debates, and the willingness of whoever succeeds Erginbilgic to keep saying no to a bad contract when the whole institutional culture, and a very loud customer, is pushing them to say yes. Erginbilgic's real innovation was not a machine but a stance — that a premium product must command a premium price, that capital has a cost, and that a national treasure is not exempt from the discipline of return on capital. Whether that stance survives the next downcycle, the next durability scare, or a future management with softer resolve is the open question the numbers cannot yet answer.

The ultimate takeaway is a warning as much as a triumph. Moats — switching costs, scale economies, the whole armoury of durable advantage — are only worth what management is willing to charge to defend them. Rolls-Royce always had the moat. It took an outsider with a refinery operator's instincts, and no reverence for the mythology, to price it correctly. The engineering made the company great. The pricing, at last, made it valuable.

References

-

Rolls-Royce Holdings plc 2025 Full Year Results — Rolls-Royce plc, 2026-02-26 ↩↩↩↩↩↩↩↩↩↩

-

Rolls-Royce Holdings plc 2024 Full Year Results — Rolls-Royce plc, 2025-02-27 ↩↩↩↩

-

Rolls-Royce Capital Markets Day 2023 — Rolls-Royce plc, 2023-11-28 ↩

-

Rolls-Royce boss says company is 'burning platform' — Financial Times, 2023-01-26 ↩↩

-

Tufan Erginbilgic's 'burning platform' speech was just what Rolls-Royce needed — Financial Times, 2023-02-23 ↩↩

-

Emirates and Rolls-Royce clash over Airbus A350 engines — Reuters, 2023-11-14 ↩

-

Rolls-Royce CEO defends engine pricing after Emirates spat — Bloomberg, 2023-11-16 ↩

-

Emirates upbeat on Boeing 777X, no progress in Airbus A350-1000 engine spat — Reuters, 2026-06-09 ↩

-

Rolls-Royce completes sale of ITP Aero to Bain Capital consortium — Rolls-Royce plc, 2022-09-15 ↩

-

Rolls-Royce completes sale of IAE stake to Pratt & Whitney — Rolls-Royce plc, 2012-06-29 ↩

-

Rolls-Royce to buy Daimler stake in engine joint venture for €2.43bn — Reuters, 2014-03-07 ↩

-

Rolls-Royce rights issue: all you need to know — interactive investor, 2020-10-01 ↩

-

Rolls-Royce projects free-cash outflows of about £2bn this year — The Irish Times, 2021-02-11 ↩↩

-

Rolls-Royce regains investment-grade rating amid CEO turnaround — Bloomberg, 2024-03-14 ↩

-

Rolls-Royce SMR moves to next stage of UK GDA — World Nuclear News, 2024-07-31 ↩↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube