Rightmove: The Unstoppable Toll Bridge of British Real Estate

I. Introduction: The Infinite Margin Machine

In the pantheon of tech gatekeepers, certain names command immediate recognition. Google owns search. Apple owns the app store. Amazon owns the buy button. But tucked away in a business park in Milton Keynes, a city most Londoners would struggle to find on a map, sits a company of roughly 900 people that owns something arguably more visceral, more emotionally charged, more deeply embedded in the British psyche than any of those: the very concept of moving house.

Rightmove is, by almost any measure, the most quietly dominant internet business in Britain. Over eighty percent of all consumer time spent on UK property portals flows through its servers. When a couple in Bristol starts idly browsing flats on a Sunday evening, when a family in Manchester agonizes over catchment areas, when a first-time buyer in London refreshes the same search at 11pm for the fourteenth consecutive night, they are almost certainly doing it on Rightmove. The platform attracts more than 125 million visits every month. The nation collectively spent over sixteen billion minutes browsing properties on it in 2024 alone. To put that in perspective, that is the equivalent of every adult in the United Kingdom spending roughly five hours per year staring at houses they will probably never buy.

But here is the number that makes fund managers sit up and pay attention.

Rightmove operates at approximately seventy percent operating margins. Not gross margins. Operating margins. That figure places it in rarefied air, not just within the FTSE 100 but across global technology.

For context, Meta operates at around thirty-five percent. Alphabet at roughly twenty-seven percent. Even Visa, often held up as the platonic ideal of a toll-bridge business, hovers around sixty-five percent. Rightmove beats them all.

And it does this with no inventory, no warehouses, no delivery fleet, no manufacturing, and essentially zero cost of goods sold. The company's gross margin is functionally one hundred percent. Every pound of revenue that comes in is essentially pure margin before you start paying salaries and server costs. The entire cost base is essentially people and technology. There are no raw materials, no supply chain disruptions, no freight costs, no currency hedging on imported components. When revenue grows, almost all of that growth drops straight to the bottom line.

The story of how this happened, how a defensive consortium project launched by four rival estate agency chains in the year 2000 became a multi-billion pound digital toll bridge that even Rupert Murdoch's News Corp could not manage to buy, is one of the most instructive case studies in network effects, pricing power, and strategic discipline that the UK stock market has ever produced.

It is a story about an industry that tried to control the internet and ended up being controlled by it.

About a business model so elegantly simple that its founders may not have fully understood what they were building.

And about a company that people love to use, love to browse, love to spend their Sunday evenings on, but that the people who actually pay for it, the estate agents, increasingly love to hate.

This is the story of Rightmove.

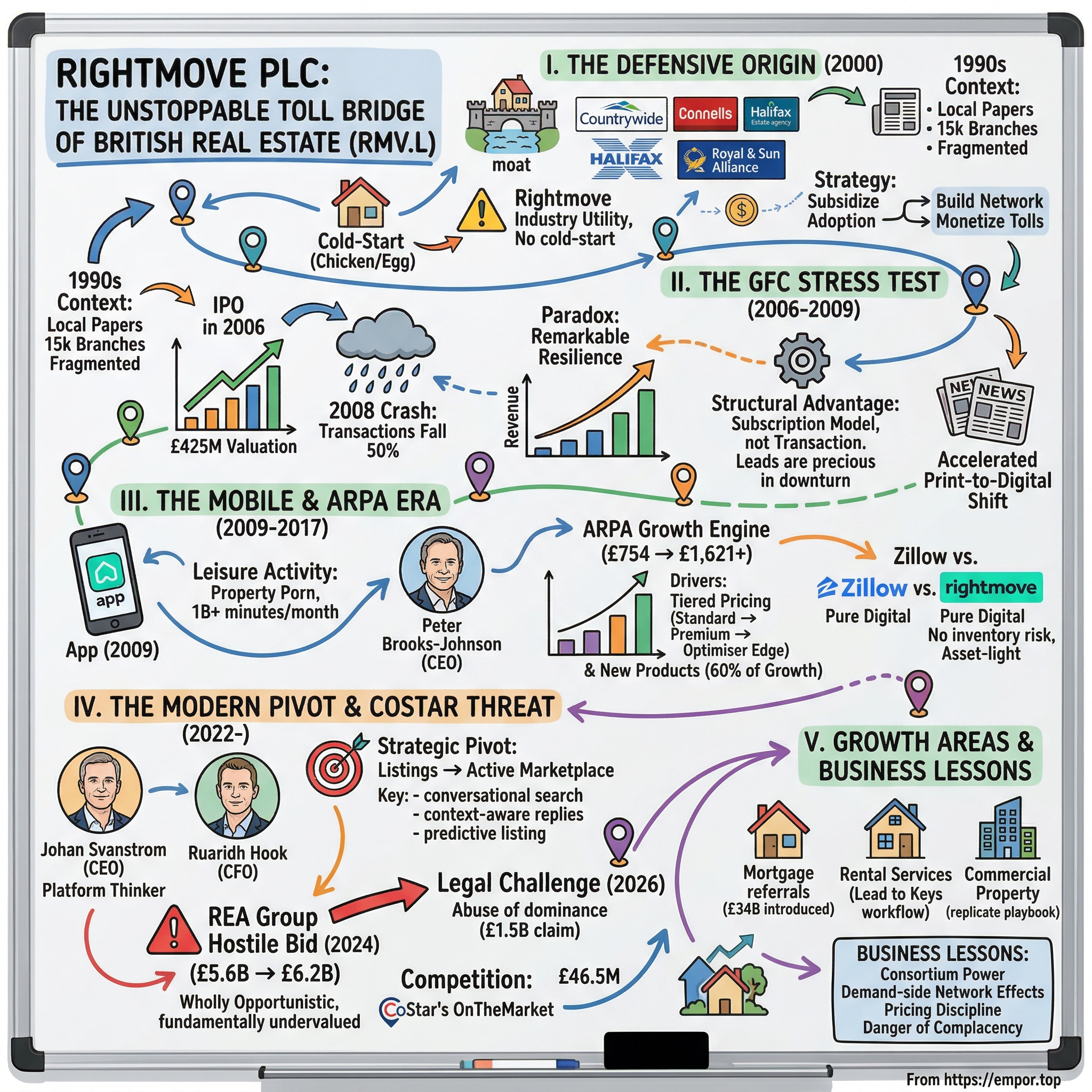

II. The Origin Story: A Defensive Moat

Picture the British property industry in the late 1990s.

Estate agents, those beloved and universally trusted pillars of the community, operated in a world built on local newspapers. The classified ads section of the Evening Standard, the back pages of the local press in every town from Aberdeen to Exeter, these were the lifeblood of the trade. An agent's ability to sell houses depended on their ability to buy column inches. It was a simple, analog, geographically fragmented business.

The industry was also deeply fragmented. Roughly 15,000 estate agency branches operated across England, Scotland, and Wales, most of them independent operations with a single office, a single shopfront window displaying property cards, and a Rolodex of local contacts built over years of community presence. The large corporate groups, Countrywide, Connells, Halifax's network, controlled perhaps twenty to twenty-five percent of the market between them. The rest was a patchwork of local fiefdoms, each competing primarily within a five-mile radius.

The economics were straightforward. An agent's core value proposition was access to buyers. Sellers chose agents based on who could bring the most serious prospects through their front door. And the primary channel for reaching those buyers was the classified advertising section of the local newspaper. The cost of those ads, which could run to hundreds of pounds per week for a busy office, was one of the largest line items on an agent's profit and loss statement. But there was no alternative. Television advertising was too expensive and too broad. Leafleting was too local. The newspaper classified was the sweet spot: geographically targeted, regularly read, and deeply embedded in the house-hunting ritual.

And then, with the gentle inevitability of a tide coming in, the internet arrived.

The large corporate estate agency groups saw the threat immediately.

If property listings moved online, if buyers started searching on websites instead of flipping through newsprint, then the power would shift. Whoever controlled the digital listing platform would inherit the role that newspapers had played for decades, the role of gatekeeper between sellers and buyers. And whoever controlled that gatekeeper role would have pricing power over every estate agent in the country.

The question was not whether it would happen, but who would control the digital equivalent of those classified pages. Would it be a Silicon Valley startup? A media company? A newspaper group trying to protect its turf? Or could the estate agents themselves build the platform and keep control?

The answer came in May 2000, when four of the UK's largest corporate estate agency groups, Countrywide plc, Connells Limited, Halifax (then part of the HBOS banking group), and Royal & Sun Alliance, jointly incorporated a new company called Rightmove. The logic was simple and, in hindsight, brilliant.

Each of these four groups controlled hundreds of estate agency branches across Britain. Countrywide alone operated over a thousand offices under brands like Bairstow Eves, Bridgfords, and Mann. Connells ran several hundred more. Halifax's estate agency arm was tied to its enormous mortgage lending operation, meaning it had a direct financial interest in making the home-buying process more efficient. Royal & Sun Alliance, an insurer, had a different angle entirely: its involvement in property transactions through buildings and contents insurance gave it a stake in any platform that accelerated the buying cycle.

Between them, these four shareholders held an enormous share of the nation's property listings. By pooling their inventory into a single online platform, they could create something that no lone startup could match: immediate critical mass.

The timing was both fortunate and deliberate. The dot-com bubble was inflating toward its peak, and venture capital was pouring into online classified businesses across every sector. In the US, Craigslist was eating into newspaper revenues. In the UK, companies like Fish4 (backed by newspaper groups) and Propertyfinder were already attempting to move property listings online. But none of them had solved the chicken-and-egg problem that plagues every marketplace: you need listings to attract buyers, and you need buyers to attract listings. Rightmove, by launching with the listings of four major corporate groups already in place, skipped the cold-start problem entirely.

The website launched in July 2000, and within months, the network effect began to take hold. Because the four founding shareholders contributed such a large proportion of the UK's property listings, Rightmove instantly became the most comprehensive place for buyers to search. And because buyers were there, other estate agents, independents who had no ownership stake in the venture, had little choice but to list their properties on it too. To not be on Rightmove was to be invisible to the majority of serious house-hunters. By 2004, just four years after launch, six thousand estate agency offices had signed up, representing half of all agents in the country. Monthly page views exceeded one hundred million.

There was a masterstroke in the founding structure that deserves attention. The founding shareholders did not just build Rightmove as a technology investment. They built it as a utility for the industry. The initial years were free for agents to list. Charging was only introduced in 2002, by which point Rightmove had become so integral to the property search process that agents could not afford to leave. It was the classic playbook of platform businesses: subsidize adoption, build the network, then monetize. Rightmove was doing this years before venture-capital-backed Silicon Valley startups made it fashionable.

The three founding directors, Ed Williams as Managing Director, Nick McKittrick handling technology and operations, and Miles Shipside on the commercial side, operated with a lean team. Shipside later described watching the company grow "from a three-man band to more than 500 employees." But the real asset was never the team or the technology. It was the network. By the mid-2000s, Rightmove had achieved something that is vanishingly rare in marketplace businesses: genuine demand-side lock-in on both sides of the platform simultaneously. Buyers went to Rightmove because agents listed there. Agents listed on Rightmove because buyers searched there. And crucially, unlike many two-sided marketplaces, neither side had a viable alternative.

There is an important structural detail about the early years that shaped everything that followed. Rightmove was not initially set up as a profit-maximizing entity. The founding shareholders viewed it as infrastructure, a shared utility that would benefit the industry by modernizing the listing process. The early management team operated with remarkable frugality. The company ran on a skeleton staff, with technology outsourced where possible and the focus relentlessly on two things: getting more agents to list and getting more buyers to search.

This utility mindset had a crucial consequence. It meant that Rightmove prioritized coverage over revenue in its formative years. The company was willing to offer free or heavily subsidized listings to win over skeptical agents, knowing that once the network reached critical mass, the power dynamic would shift irreversibly. It was a strategy borrowed, consciously or not, from the playbook of natural monopolies. Build the railroad. Get everyone using it. Then set the tolls.

The deep irony, the one that would play out over the next two decades, was baked into this founding DNA. Rightmove was created by estate agents, for estate agents, to protect the industry from outside disruption. And yet the platform they built would become the single largest cost most agents face, the most contentious relationship in their business, and the subject of a billion-pound legal claim alleging that Rightmove had abused the very dominance its founding agents helped create.

The agents built their own toll bridge. They just did not realize they would be the ones paying the toll.

But before the resentment came the validation. And the validation came in the most dramatic form possible: a global financial crisis.

III. Inflection Point 1: The IPO and the GFC Stress Test

On March 15, 2006, Rightmove floated on the London Stock Exchange at 335 pence per share, at the top end of a price range that had already been revised upward during the roadshow due to overwhelming institutional demand.

The company was valued at approximately 425 million pounds. Shares jumped roughly twenty percent on the first day of trading, with the price briefly touching 397 pence and valuing the business at close to half a billion pounds.

The founding shareholders retained significant stakes: Countrywide held around twenty-two percent, Connells and Halifax each held roughly twenty-two percent, and Royal & Sun Alliance held just under five percent. The IPO was not a full exit for any of them. It was a partial monetization that also gave Rightmove an independent currency, its own shares, and the public scrutiny that comes with a listing. For the founders, the implicit bet was that public market discipline would force Rightmove to innovate and grow faster than it would as a private joint venture.

The market, at that point, looked at Rightmove and saw a housing play. The UK property market was booming. Prices were rising. Transactions were plentiful. Estate agents were flush.

If you were bullish on UK housing, Rightmove was a leveraged way to play the theme. Analysts modeled it as a cyclical business, one that would rise and fall with the property market. Their earnings estimates were tied to transaction volumes and house prices. The price-to-earnings multiple reflected this perceived cyclicality.

The consensus was wrong. And the proof would arrive two years later with devastating clarity.

When the global financial crisis hit in 2008, the UK housing market did not merely slow down. It collapsed.

Property transactions fell by roughly fifty percent from their peak. Estate agents went out of business in droves. High streets that had boasted three or four competing agencies found themselves with one or none. For-sale boards gathered dust on streets where nothing was moving. Mortgage approvals, the lifeblood of the housing market, fell to levels not seen since records began.

This was the kind of environment that should have annihilated Rightmove. Its customers were going bust, its addressable market was shrinking, and the broader economy was in freefall.

Instead, something remarkable happened.

Rightmove's revenue grew from 56.7 million pounds in 2007 to 74 million pounds in 2008. Even in 2009, the worst year for UK property transactions in a generation, revenue only dipped to around 64 to 69 million pounds depending on the measure, and underlying operating profit actually increased slightly to 41.9 million pounds. Profit after tax hit a record 30 million pounds. Earnings per share grew twenty-eight percent.

In the middle of a housing catastrophe, Rightmove was setting profit records. Think about what that means. Transaction volumes had halved. Thousands of estate agency branches had closed permanently. House prices in some regions had fallen thirty percent. Mortgage lending had seized up almost entirely. And Rightmove was reporting its best-ever profitability.

The contrast with other property-adjacent businesses was stark. Countrywide, one of Rightmove's founding shareholders, saw its profits collapse. Foxtons, the flashy London-centric agency, would eventually go through a near-death experience. Mortgage brokers vanished. Surveyors saw their workloads crater. Every business that was tied to transaction volume suffered. But Rightmove, because it charged for presence rather than performance, was largely insulated from the volume collapse.

The reason was structural, and it taught the market a lesson it has never forgotten.

Rightmove is a subscription business, not a transaction business. It does not charge per sale. It does not take a commission when a house changes hands. It charges a monthly fee, per branch, for the right to list properties. And in a down market, when transactions are scarce and leads are precious, the few inquiries that do come through are more valuable than ever. An estate agent in 2009, sitting in an office with no buyers walking through the door, was not going to cancel the one platform that still generated leads. Canceling Rightmove in a downturn would be like a fisherman throwing away their net because the sea was rough. The remaining leads were a lifeline, and agents clung to them.

The 2008 crisis also accelerated a structural shift that had been building for years.

As agents cut costs, the first thing to go was newspaper advertising, the expensive, untrackable, geographically limited classified ads that had been the industry standard for generations. A full-page ad in a regional newspaper might cost several hundred pounds and reach perhaps fifty thousand readers, with no way to measure how many of those readers actually looked at the property section, let alone clicked through to make an inquiry. Rightmove's spending, by contrast, was measurable, nationwide, and by comparison, relatively affordable. Every inquiry could be tracked. Every view could be counted. Every lead could be attributed.

By April 2009, Rightmove's revenues had begun rising again even as traditional property advertising continued to decline. The crisis did not just test the business model; it actively strengthened Rightmove's competitive position by accelerating the migration from print to digital. What might have taken a decade of gradual shift was compressed into two years of forced adaptation. Newspapers that had relied on property classifieds for a significant share of their advertising revenue saw that income evaporate, and it never came back.

There is a deeper lesson here about asset-light business models that is worth dwelling on.

Across the Atlantic, the American property portal Zillow would eventually pursue a very different strategy. Zillow launched iBuying, a program where it actually purchased houses, renovated them, and resold them. The idea was to capture a share of the transaction value, not just the advertising spend. On paper, it looked transformative. Instead of collecting a few hundred dollars in advertising fees per listing, Zillow would capture the entire spread between purchase price and sale price, potentially thousands of dollars per transaction.

It was a catastrophic failure. Zillow's algorithms mispriced homes in a rapidly shifting market. The company ended up holding billions of dollars of real estate inventory that it could not sell at the prices it had paid. It lost hundreds of millions of dollars and eventually shut down the iBuying division entirely, laying off roughly a quarter of its workforce in the process.

Rightmove never entertained anything remotely similar. It has never owned a single property, never taken transaction risk, never employed a surveyor or a conveyancer. It is a pure digital platform, a classified advertising business dressed up in modern technology. And that purity, that disciplined refusal to chase adjacent revenue streams that carry real-world risk, is the foundation of its extraordinary margins.

The Zillow comparison is instructive for another reason. It illustrates the fundamental tension in property portal businesses between margin and ambition. The highest margins accrue to companies that do the least, that simply connect buyers and sellers without getting involved in the messy, capital-intensive, risk-laden reality of actual property transactions. The moment you step beyond the screen, beyond the listing, beyond the lead, you enter a world of physical assets, legal complexity, and financial risk that can destroy margins overnight. Rightmove has, so far, resisted that temptation.

The stock market gradually repriced Rightmove from a cyclical housing play to a quality compounder.

The share price, which had fallen roughly seventy-five percent from its 2007 peak to its 2009 trough, began a relentless march upward that would eventually take the company into the FTSE 100 and push its market capitalization above five billion pounds. The re-rating was one of the most dramatic in FTSE history. Investors who bought at the 2009 lows and held for a decade saw returns exceeding two thousand percent, making Rightmove one of the best-performing stocks of the post-crisis era.

The crisis had served as the ultimate stress test, and Rightmove had passed with a performance that most subscription software businesses would envy. It had demonstrated three things that the market would never forget. First, that the subscription model was genuinely counter-cyclical in terms of profitability, even if not entirely immune to revenue pressure. Second, that structural shifts like the migration from print to digital accelerated in downturns, permanently strengthening Rightmove's competitive position. And third, that a business with negligible variable costs, no inventory, and no physical infrastructure could sustain extraordinary margins even when its customers were going bankrupt.

The lesson was clear: in a market where leads are everything, the company that controls the flow of leads controls the industry. And Rightmove controlled roughly eighty percent of that flow. The question now was how to monetize it.

IV. Inflection Point 2: The Mobile Pivot and the Brooks-Johnson Era

In August 2009, with the financial crisis still reverberating through the economy, Rightmove launched its iPhone app.

It was early. Earlier than most UK companies, earlier than most media businesses, and earlier than almost any property company in the world. The timing was inspired. Over forty thousand users were already accessing Rightmove via their iPhones, accounting for ninety-five percent of the platform's mobile traffic. The app was an immediate hit, winning Revolution Magazine's award for best use of mobile and earning a spot in Apple's own television advertising campaign for the iPhone. By July 2011, it had been downloaded a million times. The iPad app followed in May 2010, racking up over one hundred thousand downloads in the Christmas period alone.

What happened next was less a technological shift and more a cultural one.

Property browsing on Rightmove became a leisure activity, a national pastime, something people did in bed at night with no intention of actually moving. The addictive quality of the app, the infinite scroll of property photos, the fantasy of a farmhouse in the Cotswolds or a Georgian townhouse in Bath, turned Rightmove from a utility into entertainment. The British even coined a word for it: "property porn." And Rightmove was the undisputed purveyor.

The phenomenon was remarkably sticky. Unlike social media apps that compete with each other for attention, or streaming services that battle over content libraries, Rightmove was competing primarily with itself. There was no comparable experience on another platform. Zoopla had similar listings but a less intuitive interface and fewer users. OnTheMarket would not launch until 2015. The result was that Rightmove occupied a unique niche in British digital life: it was simultaneously a practical tool for people actively moving and a fantasy escape for people who were not. The British have long been obsessed with property, but Rightmove gave that obsession a digital outlet available twenty-four hours a day. By 2018, consumers were spending over one billion minutes per month on the platform. By 2024, seventy-three percent of all time on Rightmove was via mobile devices.

This mobile-first transformation coincided with, and was partly driven by, the tenure of Peter Brooks-Johnson.

Brooks-Johnson joined Rightmove in 2006, the year of the IPO. He rose through the ranks with quiet determination, running the Agency business from 2008, becoming Managing Director of the operating subsidiary in 2011, COO in 2013, and finally CEO in 2017. His sixteen-year career at Rightmove spanned its transformation from a desktop website into a mobile-first lifestyle platform.

Under his leadership, the company introduced tiered pricing packages, initially structured as standard, enhanced, and premium tiers, that gave agents increasingly sophisticated tools for reaching buyers. Think of it as an airline model: economy gets you listed, business class gets you featured, and first class, eventually branded as "Optimiser Edge," gives you maximum exposure, priority placement in search results, featured property banners, and enhanced data analytics showing exactly how many views and inquiries each listing generates.

This tiered structure was the engine behind one of the most important metrics in the Rightmove story: ARPA, or Average Revenue Per Advertiser.

ARPA is the single number that tells you more about Rightmove's business trajectory than any other.

It represents the average monthly fee that each estate agency office pays to Rightmove. In 2015, ARPA stood at 754 pounds per month. By 2018, it had crossed the one thousand pound mark. By 2022, it reached 1,314 pounds. By 2025, it hit 1,621 pounds. That is a compound annual growth rate of roughly eight percent, achieved year after year, through booms and busts, through pandemics and political crises, with metronomic consistency.

To put 1,621 pounds per month in perspective, consider what an estate agent earns from a typical sale. The average UK house price is roughly 290,000 pounds. The typical agent commission is one to one-and-a-half percent, yielding perhaps 3,500 pounds per transaction. A reasonably busy office might complete eight to twelve sales per month. Against that backdrop, 1,621 pounds is a meaningful but manageable cost, roughly equivalent to one half of one completed sale per month. As long as Rightmove generates at least one serious buyer inquiry per month that would not have come through any other channel, the subscription pays for itself.

The industry analyst Anthony Codling has identified 2,500 pounds per month per branch as the eventual target, suggesting that Rightmove still has significant pricing runway ahead. That would represent a fifty-four percent increase from current levels. If achieved over six to seven years at the historical pace of eight percent annual growth, it implies that the ARPA story has at least another half-decade to run before reaching any natural ceiling.

The beauty of the ARPA model is that approximately sixty percent of the growth comes from agents voluntarily upgrading their packages or purchasing additional products, not from contractual price increases on renewal.

This is a critical distinction. When a business grows revenue primarily through price hikes on a captive customer base, it builds resentment. When growth comes from customers choosing to buy more because the additional products deliver measurable value, the dynamic is healthier. Rightmove has managed to do both, which partly explains both the extraordinary revenue growth and the growing agent frustration.

The analogy to cable television is apt. Cable companies raised prices every year, and customers hated them for it but paid because they had no alternative. Eventually, streaming arrived and the dam broke. Agents fear that CoStar's OnTheMarket could be their Netflix moment, a credible enough alternative to finally give them negotiating power. Whether that fear is justified remains the central competitive question facing Rightmove today.

On the M&A front, Rightmove under Brooks-Johnson was disciplined to the point of being parsimonious. The company's approach to acquisitions has been the antithesis of the Silicon Valley "grow at all costs" mentality. In 2019, Rightmove acquired Van Mildert, a tenant referencing and rent guarantee insurance business, for an initial sixteen million pounds with up to four million in deferred consideration. In early 2024, it bought HomeViews, a platform of verified resident reviews focused on the Build to Rent sector, for just eight million pounds. The Holiday Lettings business, acquired in 2007, was sold to TripAdvisor in 2010 for roughly twenty-one million pounds, delivering a seven-fold return on the original investment. These are not transformative deals. They are small, targeted tuck-ins designed to strengthen specific capabilities without diluting the core business or distracting management.

The verdict on this approach is straightforward: Rightmove does not buy growth because it does not need to. The combination of an expanding customer base, rising ARPA, and operating leverage on a fixed cost base delivers organic revenue growth in the high single digits year after year. Why take on integration risk and pay acquisition premiums when you can achieve the same result by releasing a new product tier?

There is a counterargument worth considering. Rightmove's reluctance to pursue international expansion, at a time when its model was proven and its balance sheet was pristine, may represent one of the largest opportunity costs in UK tech history. REA Group in Australia, Scout24 in Germany, and Hemnet in Sweden all built dominant property portals in their respective markets. Rightmove could have pursued any of these markets or built from scratch in others. Instead, it remained resolutely focused on the UK. The bulls call this discipline. The bears call it a lack of imagination. The truth is probably that Rightmove's management understood that their competitive advantage, the deeply embedded consumer habit of searching on Rightmove, was non-transferable to other geographies. Starting from scratch in a new country would mean competing against local incumbents with their own network effects, and Rightmove had no particular advantage in that fight.

Brooks-Johnson stepped down in March 2023 after sixteen years, leaving behind a company that had grown revenue from roughly 243 million pounds in 2017 to 364 million pounds in 2023, at margins that most software companies can only dream of.

His legacy is difficult to overstate. Under his leadership, Rightmove became one of the highest-quality businesses in British public markets: a company with no debt, minimal capital expenditure requirements, and a free cash flow conversion rate that approached ninety percent. He transformed it from a desktop website into a mobile-first lifestyle platform. He introduced the tiered pricing architecture that enabled ARPA to double over his tenure. And he did it all with a team of under a thousand people, operating from offices in Milton Keynes that most FTSE 100 executives would consider unpretentious.

He later became CEO of AutoScout24, Europe's largest online car marketplace, an interesting parallel that underscores how the skills required to run a dominant classified marketplace are highly transferable across categories. The playbook, build the largest inventory, attract the most buyers, then gradually monetize through tiered packages and value-added services, works whether you are selling houses or cars.

But the company he left behind was facing new questions. The ARPA growth engine, while still running, was generating increasing friction with customers. The competitive landscape was shifting with CoStar's entry. And the broader technology environment, with AI rapidly reshaping how consumers interact with information, demanded a different type of leadership. Was the era of quiet, steady extraction coming to an end? Could Rightmove evolve from a listings board into something more ambitious?

His successor would bring a very different playbook.

V. Modern Era: The Svanstrom Pivot and the AI Frontier

When Rightmove announced in October 2022 that it had hired Johan Svanstrom as its next CEO, the property industry was puzzled.

Svanstrom was not a property person. He was a travel person.

Born in Sweden in 1971 and educated at the Stockholm School of Economics, he had spent eight years at Expedia Group, rising to become the Global President of Hotels.com and the Expedia Affiliate Network, where he oversaw revenues exceeding three billion dollars and managed teams across four continents. His career at Expedia gave him something that no UK property executive could offer: deep experience in transforming a listings platform into an active marketplace. At Hotels.com, he had overseen the shift from simply displaying hotel rooms to actively facilitating bookings, managing reviews, personalizing recommendations, and using data to optimize the entire customer journey.

Before Expedia, he had led the Digital Innovations Group at McDonald's, run telecommunications startups, and served as a partner at EQT, the Swedish private equity firm, investing in growth-stage technology companies. It was an unusual CV for a UK property portal CEO, but then, the board was not looking for a property person. They were looking for a platform person.

The appointment puzzled industry insiders but made immediate sense if you understood where Rightmove needed to go. Under the previous leadership, Rightmove had been a listings platform, a digital classified board. It was extraordinarily profitable, but it was fundamentally passive: agents posted listings, buyers searched them, and Rightmove collected the subscription fee. Svanstrom's background at Expedia pointed toward a different model, one where the platform actively facilitates the transaction, matches supply with demand, and captures value at multiple points along the customer journey. In travel industry terms, the shift from "listings" to "marketplace." Hotels.com did not just show you a list of hotels. It helped you book, pay, review, and return. Rightmove, by contrast, essentially dropped you off at the estate agent's doorstep and walked away.

Svanstrom joined as CEO designate on February 20, 2023, and officially took the top job on March 6.

His compensation package reflected the board's expectations: total annual pay of approximately 1.59 million pounds, with over sixty percent tied to bonuses and equity. Notably, the performance shares granted to him, some 183,759 in total, do not vest until March 2030, and their value depends on share price and dividend growth targets being met. This is long-term alignment in a very concrete form. At current prices of around 433 pence, those shares are worth significantly less than they would have been at the 780 pence that REA offered. Svanstrom has a direct financial interest in proving the board's rejection was the right call.

The shift in key performance indicators under his leadership has been telling: where previous management focused primarily on leads generated and ARPA growth, Svanstrom has introduced broader "Strategic Growth Outcomes" as KPIs, signaling a move away from pure extraction toward platform expansion.

The cultural shift under Svanstrom has been palpable. Where Brooks-Johnson ran a tight ship focused on incremental monetization, Svanstrom talks about "velocity of innovation" and "platform thinking." He has reorganized the technology team, brought in product leaders from outside the property industry, and pushed for faster release cycles. The company that once shipped a handful of product updates per year now operates closer to a continuous deployment model. For a FTSE 100 company headquartered in Milton Keynes, this represents a genuine transformation in working culture.

But before Svanstrom could fully implement his vision, he had to navigate the most dramatic corporate event in Rightmove's history: a hostile takeover approach from the other side of the world.

In September 2024, REA Group, Australia's dominant property portal and a company majority-owned by Rupert Murdoch's News Corp, made an unsolicited bid for Rightmove.

The logic from REA's perspective was compelling. REA dominates the Australian property portal market in much the same way that Rightmove dominates the UK. It understands exactly how valuable these businesses are because it operates one. The UK housing market is roughly three times the size of Australia's. Acquiring Rightmove would create a global property portal colossus, combining the two most dominant English-language property platforms in the world under one roof. The potential for shared technology investment, data analytics, and best-practice transfer between the two platforms was obvious.

The question was never whether Rightmove was worth buying. It was whether the price was right.

The first approach, on September 10, 2024, valued Rightmove at approximately 5.6 billion pounds, or 705 pence per share, representing a twenty-seven percent premium to the undisturbed share price. The structure blended cash (305 pence per share) with new REA shares. Rightmove's board rejected it unanimously, calling the bid "wholly opportunistic" and stating that it "fundamentally undervalued" the company.

A second, improved bid was rejected days later.

A third, valuing Rightmove at approximately 6.1 billion pounds, was dismissed as "unattractive."

REA made a fourth and final approach on September 27, offering 346 pence in cash plus REA shares and a six-pence dividend, implying a total value of 780 pence per share and a valuation of approximately 6.2 billion pounds. On September 30, the board rejected this too, and Rightmove refused to grant REA access to due diligence materials, stating that its public disclosures were sufficient for any bidder to form a view.

REA walked away. Under UK Takeover Panel rules, they were barred from returning for six months.

The rejection was not without controversy.

Some shareholders felt the board was being stubborn, that a forty-plus percent premium to the pre-approach price was generous by any historical standard. Activist investors pointed out that Rightmove's share price had been under pressure, and that the bird in hand was worth taking.

But the board's calculus was clear: Rightmove's seventy percent margins, its monopolistic market position, and its long runway for ARPA and product growth meant that the intrinsic value of the business was substantially higher than anything REA had offered. In the board's view, selling at 780 pence would mean handing over decades of compounding value to a buyer who understood, precisely because they ran the Australian equivalent, just how valuable this asset was.

The fact that REA wanted it so badly was, paradoxically, the best argument for not selling. If REA, the operator of the closest global analogue to Rightmove, believed the company was worth at least 6.2 billion pounds, then the true long-term value was almost certainly higher. REA was not overpaying out of sentiment. It was making a calculated bet that the UK property portal market would continue to grow, and that the dominant player in that market was worth a substantial premium.

The six-month standstill period expired in March 2025. As of early 2026, REA has not returned with a new bid. The share price, which briefly spiked above 700 pence during the bidding war, has since fallen sharply, trading at approximately 433 pence as of April 2026. That decline, driven partly by the legal claim and partly by broader market concerns about UK consumer-facing businesses, puts the current market capitalization at roughly 3.5 billion pounds, well below REA's lowest rejected offer. The market is, in effect, offering Rightmove at a cheaper price than what the board unanimously rejected just eighteen months ago.

With the takeover drama behind him, Svanstrom has accelerated the technology transformation. In September 2024, alongside the REA defense, Rightmove also brought on a new CFO. Ruaridh Hook, who joined from Kantar, the WPP-owned data analytics business, took over finance responsibilities in September 2024. His background in data-driven businesses aligns with the company's pivot toward AI and analytics.

In 2025, Rightmove signed a multi-year partnership with Google Cloud, gaining access to the Vertex AI platform, Gemini large language models, and advanced data infrastructure.

This is not a cosmetic AI add-on of the kind that dozens of FTSE companies have announced in recent years. The company has thirty-one live AI initiatives across the business, each targeting a specific operational or consumer-facing improvement. One of the most significant is a conversational property search feature that allows users to describe what they want in natural language rather than filling in filter boxes. Another uses AI to help estate agents respond to buyer inquiries faster by generating context-aware, automatically drafted replies. The ambition, though it remains early, is to use Rightmove's proprietary dataset, decades of listing data, pricing history, and demand signals, to predict when a homeowner is likely to list their property before they even contact an agent. If Rightmove can crack that, it would represent the holy grail of property data: the ability to identify sellers before they self-identify.

The investment in AI has had a measurable impact on margins. Operating margins dipped from around seventy percent to sixty-seven percent in the 2025 financial year, as Rightmove increased its technology and product headcount. The company added dozens of engineers and data scientists, expanding its technology team in a way that would have been unthinkable under the previous management's cost-discipline ethos.

Whether this investment pays off in the form of sustainable new revenue streams or merely adds cost without proportionate return will be one of the key questions for investors over the next three to five years. The parallel with Expedia is instructive. Hotels.com, under Svanstrom's leadership, evolved from a simple booking engine into a data-driven platform that used customer behavior signals to personalize search results, optimize pricing, and predict demand patterns. If he can replicate even a fraction of that transformation at Rightmove, the company's competitive moat deepens significantly. If he cannot, Rightmove risks becoming a well-funded science experiment with compressed margins and no clear payoff.

Svanstrom is betting that the era of Rightmove as a "quiet utility" is over, and that the future belongs to an "aggressive tech" phase where the platform does far more than display listings.

VI. Hidden Businesses: The Strategic Growth Areas

For most of its history, Rightmove has been a one-trick pony, and a spectacular one at that.

The core Agency business, charging estate agents a monthly subscription to list residential properties for sale and for rent, generated the vast majority of revenue. In the 2025 financial year, total group revenue reached 425.1 million pounds, growing nine percent year on year.

But underneath this headline number, three smaller businesses are growing at rates that, if sustained, could meaningfully change the shape of the company over the next decade.

Rightmove labels these its "Strategic Growth Areas," and collectively they generated 29.1 million pounds in 2025, up twenty-five percent from the prior year.

That is still only about seven percent of total revenue, up from five percent in 2023, but the growth trajectory is striking. The company has guided for twenty to thirty percent growth from these areas in 2026. If that guidance is met, these businesses will cross the forty-million-pound mark and begin to represent a meaningful diversification of the revenue base.

The first, and perhaps the most strategically significant, is Mortgage and Financial Services.

This segment generated 6.8 million pounds in 2025, up forty-six percent year on year. It is small in absolute terms but enormous in what it represents strategically. The core product is a "Mortgage in Principle" integration that connects home-movers searching for properties on Rightmove directly with mortgage lenders. In 2025, Rightmove introduced thirty-four billion pounds of potential lending to its mortgage partners. The logic is elegant: Rightmove already captures the moment of highest intent in the home-buying journey, the point when someone is actively searching for a property. By connecting that moment to the financing decision, Rightmove inserts itself into a much larger value chain. A typical estate agent subscription generates roughly 1,600 pounds per month. A mortgage origination, by contrast, generates thousands of pounds in fees and commissions. Rightmove does not originate mortgages itself, but by becoming the matchmaker between borrowers and lenders, it captures a referral fee without taking on credit risk. This is the move from "finding a house" to "funding the house," and it represents a significant expansion of the addressable market.

The second growth area is Rental Services, built around a product called "Lead to Keys."

This generated 7.1 million pounds in 2025, up thirty-five percent. Lead to Keys is an end-to-end digital workflow tool for lettings agents, handling everything from the initial tenant inquiry through referencing, contract generation, and move-in.

Think of it as Shopify for lettings: instead of building their own systems for tenant screening, contract management, and move-in coordination, agents plug into Rightmove's platform and get a complete digital infrastructure out of the box. The product also includes ancillary sales of utilities, broadband, and insurance packages to tenants, which grew seventeen percent in the period. These ancillary revenues are particularly interesting because they represent a completely different revenue stream: instead of charging agents, Rightmove is capturing a referral fee from utility companies and insurers for connecting them with tenants at the moment of maximum intent, when they are setting up a new home. This is the most interesting strategic shift in Rightmove's recent history because it transforms the company from an advertising platform into something closer to a SaaS operating system for lettings agents. Instead of just charging agents to be visible, Rightmove is now charging them for the tools they use to run their day-to-day business. The switching costs here are materially different from a listings subscription. If an agent's entire lettings workflow runs on Rightmove's rails, leaving the platform means not just losing visibility but ripping out operational infrastructure.

The third growth area is Commercial Property.

This generated 15.3 million pounds in 2025, growing thirteen percent. Rightmove has quietly been replicating its residential playbook in the office, retail, and industrial property space, building out a new Property Details Page with substantially more data fields and integrating commercial listings into its Rightmove Plus analytics platform. Over seven hundred new partners have been added across all three growth areas since 2023. The commercial segment is smaller and slower-growing than the other two, but it represents a meaningful extension of the platform's reach into a sector where online penetration is still lower than in residential, suggesting a longer runway for digital adoption.

There is a fourth dimension to the growth story that sits outside the formal "Strategic Growth Areas" but deserves mention: Rightmove's data products. The company has been building out Rightmove Plus, an analytics platform for agents that provides local market intelligence, competitor benchmarking, and demand signals. While this is not yet broken out as a separate revenue line, it represents another layer of value that increases switching costs and supports ARPA growth. An agent who relies on Rightmove not just for listings but for their daily market intelligence briefing is even more deeply embedded in the ecosystem.

Taken together, these three businesses tell a story about where Rightmove is heading. The company that once simply displayed listings is evolving into an integrated platform that touches multiple points in the property transaction lifecycle. The Google Cloud partnership, with its access to AI models capable of analyzing Rightmove's vast proprietary dataset, underpins all three growth areas. If Rightmove can use AI to identify which renters are likely to become buyers, which buyers need mortgage referrals, and which commercial tenants are about to outgrow their space, it creates a data flywheel where each insight feeds the others. This is, at least, the vision. Whether it materializes will depend on execution over the next several years.

For investors watching the capital allocation, the shift is notable.

Rightmove has historically returned almost all of its free cash flow to shareholders through dividends and buybacks. In the 2025 financial year, free cash flow was 237.8 million pounds, and the company announced a ninety-million-pound share buyback program. Rightmove has no bank debt. Its balance sheet is effectively a large cash pile that grows by several million pounds every month. This pristine financial position gives management enormous flexibility: they could invest aggressively in growth, return capital to shareholders, or pursue acquisitions, all without touching a debt market.

The dividend has been a consistent feature. The company has maintained a progressive dividend policy, growing the payout year after year since its IPO. For income-oriented investors, Rightmove has been a reliable compounder of total returns through a combination of capital appreciation, buybacks, and dividends.

But the margin compression to sixty-seven percent in 2025, driven by increased investment in technology and people, signals that management is willing to sacrifice some near-term profitability to build these new revenue streams. This is a strategic bet. The question is whether this is the beginning of a virtuous investment cycle, where today's spending on AI and data infrastructure generates tomorrow's revenue streams, or the first crack in the margin story that has defined Rightmove for two decades.

VII. The Playbook: 7 Powers and Porter's 5 Forces

To understand why Rightmove has maintained its position for over twenty-five years, despite repeated attempts to dislodge it, it helps to examine the business through the twin lenses of Hamilton Helmer's 7 Powers framework and Michael Porter's Five Forces.

Start with network effects, the most powerful of Helmer's seven powers.

Rightmove operates a textbook two-sided marketplace. Approximately 19,000 estate agency offices list properties on the platform. Over 125 million visits per month come from property seekers. Each additional agent listing makes the platform more useful for buyers, and each additional buyer makes the platform more essential for agents.

But Rightmove's network effect is even stronger than this suggests, because it operates in a market with an unusual characteristic: the "product" (a house for sale) is typically listed in only one place, unlike, say, an airline ticket or a hotel room, which appears on multiple booking platforms. When an agent lists a property on Rightmove, that listing is the primary way most buyers will discover it. This gives Rightmove a near-monopolistic position as the "front page" of UK property.

Consider the contrast with travel. A hotel room at the Marriott in London appears on Booking.com, Expedia, Hotels.com, the Marriott website, and half a dozen aggregators. A house for sale on Acacia Avenue in Surbiton appears on whichever portals the listing agent subscribes to, and for the vast majority of agents, Rightmove is the non-negotiable first choice. This means that multi-homing, the ability to list on multiple platforms simultaneously, is theoretically possible but practically limited by cost and effort. The result is that Rightmove's network effect has a winner-take-most quality that is closer to a social network than to a traditional marketplace.

The second power is switching costs.

For an estate agent, canceling Rightmove is not merely inconvenient. It is potentially existential. An agent who leaves Rightmove loses access to over eighty percent of the consumer time spent on property portals. Their listings effectively become invisible to the majority of active buyers. In a market where generating buyer leads is the core function of an estate agency, losing access to the dominant source of leads is tantamount to closing the office. This is why, during the 2008 crisis, agents cut newspaper spending, cut staff, and cut office leases before they cut Rightmove. The subscription is the last expense to go because it is the one that most directly drives revenue.

The third power is what Helmer calls "cornered resource."

In Rightmove's case, it is data. After twenty-five years of operation, Rightmove possesses the most comprehensive dataset on UK property transactions, pricing, demand patterns, and buyer behavior ever assembled. No competitor, no government agency, and no private data provider has anything comparable.

The monthly Rightmove House Price Index, published since 2002, is one of the most widely cited property market indicators in the UK. It is referenced by the Bank of England, by mortgage lenders setting rates, by institutional investors making allocation decisions, and by millions of homeowners checking what their house might be worth. This index is not just a data product. It is a brand-building exercise that reinforces Rightmove's position as the authoritative voice on UK property.

The real-time demand signals are equally valuable: which properties are being viewed, how long they stay on the market, what price reductions trigger renewed interest, which postcodes are seeing sudden spikes in search activity. These signals are immensely valuable both for agents and for the mortgage, insurance, and moving services that orbit the property transaction. And they are signals that only the market leader has in sufficient volume to be statistically meaningful.

Now apply Porter's Five Forces.

The bargaining power of customers (estate agents) is superficially high: agents are organized, vocal, and deeply unhappy about annual price increases. The recent 1.5-billion-pound legal claim filed at the Competition Appeal Tribunal in April 2026, alleging that Rightmove abused a dominant position through excessive pricing, is the most dramatic expression of this frustration. Over 250 estate agencies have expressed support for the claim, brought by Jeremy Newman, a former member of the Competition and Markets Authority, and funded by litigation funder Innsworth Capital. Rightmove has called the claim "without merit" and vowed to defend it vigorously. But despite the noise, the actual bargaining power of agents is effectively neutralized by the lack of alternatives. Agents complain, but they pay, because the cost of not paying is higher than the cost of the subscription.

The threat of new entrants is the force that has been tested most directly, and the results are instructive.

In 2013, a group of leading estate agents, including Knight Frank, Savills, and Strutt & Parker, formed Agents' Mutual and launched OnTheMarket as an agent-backed challenger to the Rightmove-Zoopla duopoly. Their key weapon was the "one other portal" rule: agents who joined OnTheMarket could only list on one other portal besides it. The intended effect was to force agents to choose between Rightmove and Zoopla, breaking the duopoly. The actual effect was that most agents chose Rightmove and dropped Zoopla. OnTheMarket never achieved critical mass. The "one other portal" rule was challenged in court, upheld by both the Competition Appeal Tribunal and the Court of Appeal, but ultimately proved insufficient to shift buyer behavior. OnTheMarket floated on AIM in 2018, raising thirty million pounds, but never came close to threatening Rightmove's dominance. In December 2023, it was acquired by CoStar Group, the American commercial property data giant, for just ninety-nine million pounds, a fraction of the value its founders had hoped for. The irony was bitter: the agents' own rebellion primarily damaged Zoopla, the number two player, while leaving Rightmove's position as number one largely untouched.

CoStar's acquisition of OnTheMarket represents the most credible competitive threat Rightmove has faced.

CoStar is a thirty-billion-dollar company with deep pockets and a stated intention to invest "hundreds of millions of pounds" into the UK residential market over multiple years. Andrew Florance, CoStar's founder and CEO, has built his career on the conviction that information asymmetry in property markets is a solvable problem. He did it in US commercial real estate. He is now attempting it in UK residential. In its first year of ownership, CoStar poured 46.5 million pounds into OnTheMarket's sales and marketing, driving website visits up fifty-five percent, page views up one hundred and ten percent, and property listings up forty-seven percent. These are impressive numbers off a low base, and OnTheMarket claimed to overtake Zoopla in traffic in September 2024, though Zoopla disputed the claim. But overtaking the number two is a different proposition from threatening the number one. Rightmove's 125-million-plus monthly visits dwarf OnTheMarket's roughly seventeen million. The gulf in consumer engagement, measured in time spent on the platform, is even wider. CoStar's investment is meaningful, but the history of property portals suggests that the network effects protecting the market leader are extraordinarily durable. The last decade has demonstrated that you can spend tens of millions marketing an alternative portal, but you cannot easily replicate twenty-five years of consumer habit formation.

The remaining Porter forces, the bargaining power of suppliers and the threat of substitutes, are relatively benign.

Rightmove's "suppliers" are primarily technology infrastructure (servers, cloud services) and labor, neither of which presents unusual cost or supply risks. The Google Cloud partnership actually converts a key supplier relationship into a strategic asset, giving Rightmove access to cutting-edge AI tools at preferential terms in exchange for being a showcase customer.

The threat of substitutes, meaning entirely different ways of buying and selling property that bypass portals altogether, remains theoretical. Social media platforms like Instagram and TikTok have seen some agents experiment with direct-to-buyer marketing, and companies like Purplebricks and Yopa attempted to disrupt the traditional agency model with fixed-fee online alternatives. But these models have largely struggled. Purplebricks' share price collapsed from over 500 pence to under 10 pence before the company was acquired by Strike in 2023 for just one pound. The lesson was harsh but clear: the British public is willing to browse houses on their phones, but when it comes to the most expensive transaction of their lives, they still want a local agent who knows the streets, the schools, and the neighbors. And that agent still needs Rightmove.

Blockchain-based property transactions and direct-to-seller platforms are occasionally discussed in proptech circles but have made no material impact on the traditional model. The UK's property transaction system, with its reliance on solicitors, surveyors, mortgage lenders, and chains of interdependent buyers and sellers, is one of the most complex in the world. Disrupting the portal is comparatively simple next to disrupting the process itself.

VIII. Business Lessons: What Rightmove Teaches

Before turning to the investment case, it is worth stepping back from the financial data and distilling the broader business lessons that Rightmove's twenty-six-year journey offers. These are lessons that apply far beyond the property industry.

The first lesson is about the power of consortium-led platform creation. Most successful internet platforms were built by startups that fought their way to critical mass through venture capital and aggressive growth. Rightmove took a different path: it was built by the incumbents themselves, who pooled their inventory to create a shared utility. This approach solved the cold-start problem instantly but created a long-term governance challenge. The founding shareholders eventually sold their stakes, and the platform they created became an independent entity that set its own prices. The lesson for any industry contemplating a shared digital platform is this: be careful what you build, because you may end up being its most important customer rather than its owner.

The second lesson is about the enduring value of demand-side network effects in marketplace businesses. Rightmove's network effect is not just strong. It is self-reinforcing in a way that makes the platform progressively harder to displace over time. Every year that passes, more data accumulates, more consumer habits are formed, and the cost of replicating the platform's position increases. OnTheMarket's failure and Zoopla's decline are not evidence that competition is impossible. They are evidence that competition against a deeply entrenched two-sided marketplace requires a level of investment and patience that very few companies can sustain.

The third lesson is about pricing discipline in monopoly-like positions. Rightmove has raised ARPA at roughly eight percent annually for over a decade, a rate that is fast enough to compound impressively but slow enough to avoid triggering a full-scale industry revolt, at least until the 2026 legal claim. This careful calibration of pricing power, extracting value without killing the goose, is harder than it looks.

Many companies with dominant market positions overreach and create the conditions for their own disruption. Rightmove's genius has been to keep the subscription price at a level that is painful enough to generate complaints but not painful enough to justify the risk of canceling. The test of whether they have got this balance right is playing out right now, in courtrooms and in the market.

There is a fourth lesson, less discussed but equally important: the danger of high-margin complacency. When a company earns seventy pence of profit from every pound of revenue, the gravitational pull toward maintenance mode is enormous. Why innovate when the existing business generates such extraordinary returns? Why invest in new products when the cash flow from the old ones is so reliable? This complacency is what creates the opening for aggressive, well-funded disruptors. CoStar's entry into the UK market is a direct consequence of Rightmove's margins being so visibly attractive. Those margins are simultaneously Rightmove's greatest strength and its most prominent target.

And finally, there is a lesson about managing the relationship with customers who are also, in a sense, captives. Estate agents know they need Rightmove. Rightmove knows they know. This dynamic, where the customer relationship is rooted in dependency rather than delight, creates a fragility that may not be visible in the financial statements but is real nonetheless. The 2026 legal claim is the most dramatic expression of this tension, but it manifests in smaller ways every day: in angry agent forums, in the willingness of agents to trial competitors, and in the quiet resentment that builds when a supplier raises prices on a customer who cannot walk away.

IX. Bear vs. Bull and the Conclusion

Every investment thesis, no matter how compelling the business quality, must wrestle with the question of what could go wrong and what could go right beyond current expectations.

The bear case for Rightmove centers on three risks.

The first and most immediate is the 1.5-billion-pound legal claim. Filed at the Competition Appeal Tribunal in April 2026, the claim alleges that Rightmove's pricing constitutes an abuse of dominant position. The claimants point to Rightmove's eighty-percent-plus share of consumer time on property portals, its seventy percent operating margins, the highest in the FTSE 100, and the fact that annual fee increases have outpaced estate agents' commission earnings for three consecutive years. They argue these margins reflect "pricing made possible by market dominance rather than competition on the merits." The claim is fully funded by a litigation funder, which means it will be pursued aggressively regardless of the claimants' own financial resources. Rightmove's shares fell nearly nine percent on the day the claim was announced, wiping approximately 300 million pounds off the market capitalization. Even if the claim is ultimately unsuccessful, the legal process could take years, create negative headlines, and potentially embolden regulators to scrutinize Rightmove's pricing practices more closely. If successful, the financial and structural consequences could be material.

The second bear case risk is competitive.

CoStar Group has proven in other markets, notably the US, that it is willing to sustain years of losses to build scale in online property portals. Its US residential portal, Homes.com, has been backed by hundreds of millions of dollars of investment. If CoStar applies even a fraction of that firepower to the UK market through OnTheMarket, it could gradually erode Rightmove's pricing power, even if it never achieves parity in market share. The mechanism is straightforward: if agents have a credible alternative, they gain bargaining power, and Rightmove's ability to push through annual ARPA increases diminishes.

The third bear risk is the margin question.

The decline from roughly seventy percent to sixty-seven percent operating margin in 2025, driven by investment in technology and AI, breaks a multi-year trend of margin stability. If the Strategic Growth Areas fail to deliver proportionate revenue returns, Rightmove could find itself in the uncomfortable position of having compressed margins without gaining new sources of growth. The shift from a "quiet utility" to an "aggressive tech" phase carries execution risk, particularly for a company that has historically competed on distribution and pricing power rather than product innovation.

The bull case is equally compelling, and arguably more structural.

The most powerful version of the bull case is not that Rightmove continues doing what it has always done, but that it evolves into something larger. Today, Rightmove captures roughly 1,600 pounds per month per estate agency office. The total cost of a property transaction in the UK, including agent fees, legal fees, surveys, mortgage arrangement fees, and moving costs, typically exceeds ten thousand pounds. If Rightmove can expand its role from "finding a house" to facilitating the mortgage, the legal process, the survey, and the utilities switch, it captures a share of a vastly larger addressable market. The Mortgage in Principle integration is the most tangible step in this direction, and its forty-six percent growth rate in 2025 suggests meaningful traction. The Lead to Keys rental workflow product points in the same direction for the lettings market.

There is also a straightforward math case for continued growth.

ARPA at 1,621 pounds per month is still well below the 2,500-pound target that industry analysts have identified as achievable. If Rightmove can grow ARPA at seven to eight percent annually, broadly in line with the historical trend, and maintain its customer base of roughly 19,000 offices, the core business alone compounds at an attractive rate before any contribution from the Strategic Growth Areas.

For investors tracking Rightmove's ongoing performance, two metrics matter above all others.

The first is ARPA, the average revenue per advertiser per month. This single number captures both pricing power and product adoption, and its trajectory over time is the clearest signal of whether Rightmove is successfully expanding its share of each customer's wallet. When ARPA is growing at eight percent or more, it tells you that agents are either upgrading their packages, buying additional products, or accepting price increases without canceling. All three are signs of a healthy franchise. When ARPA growth decelerates, it tells you that agents are pushing back, downgrading, or finding alternatives. Watch this number every quarter. It is the canary in the coal mine.

The second is the share of consumer time spent on property portals, as measured by ComScore. This metric captures the demand-side network effect. As long as Rightmove maintains over seventy-five to eighty percent of consumer time, agents cannot afford to leave, and the pricing power that underpins ARPA growth remains intact. If that share begins to erode meaningfully, whether to CoStar-backed OnTheMarket or a new entrant, the entire investment thesis requires reassessment. The two metrics are deeply linked: consumer time share is the moat, and ARPA is the toll collected by the moat's owner.

On the ownership front, the failed REA Group takeover in 2024 was revealing.

REA's willingness to bid up to 6.2 billion pounds, and the Rightmove board's willingness to reject even that amount, speaks to a fundamental disagreement about long-term value. REA, which operates an analogous business in Australia, understood exactly what Rightmove was worth because it ran the playbook itself. The board's rejection was a bet that the standalone value exceeds what any acquirer would rationally pay, a bold claim that will be tested by the company's performance over the coming years.

Rightmove occupies a category of business that is extraordinarily rare.

It is a company with genuine monopoly economics, near-zero marginal costs, massive recurring revenue, and a product that its end-users genuinely love. Over sixteen billion minutes of consumer engagement per year is not the result of a captive audience with no other choice. It reflects a product that people actively enjoy using, even when they have no intention of moving. That combination of monopoly economics on the supply side and genuine consumer affinity on the demand side is what makes Rightmove so difficult to dislodge and so valuable to own.

The risk is that the very qualities that make Rightmove a great business, its dominance, its margins, its pricing power, have begun to generate the antibodies that could weaken it.

Legal challenges. Regulatory scrutiny. Agent resentment. Well-funded competition. Whether these forces prove to be headwinds that slow the machine or existential threats that break it will depend on execution by a management team that is, for the first time in the company's history, led by someone from outside the property industry.

Johan Svanstrom's bet, that the skills required to build a global travel marketplace transfer directly to property, is the central strategic question for the next chapter of the Rightmove story. He is asking Rightmove to be something it has never been: innovative. Not just incrementally better at what it already does, but fundamentally different in what it offers. For a company that has prospered precisely because it did not need to innovate, that is a radical proposition.

What is clear is that the toll bridge built by four estate agency chains in a Milton Keynes office park twenty-six years ago has proven to be one of the most durable competitive advantages in European technology.

The agents who built it to protect themselves from the internet ended up building the internet's most effective weapon against them.

That tension, between the platform's origins as an industry utility and its evolution into an industry toll collector, will define Rightmove's future as surely as it has defined its past.

The next chapter will be written by a Swedish travel executive in a Milton Keynes office park, armed with Google's AI and the most valuable property dataset in Britain, fighting off an Australian billionaire's portal, an American data giant's checkbook, and a billion-pound legal claim from the very agents who made the platform what it is.

If that is not the most British business story of the twenty-first century, it is hard to imagine what would be.

X. Epilogue and References

Key Resources for Further Research:

- Rightmove plc Annual Reports and Investor Presentations (plc.rightmove.co.uk)

- Rightmove Corporate History Timeline (plc.rightmove.co.uk/our-history)

- REA Group Takeover Defense Documents, September-October 2024

- Competition Appeal Tribunal Filing, Jeremy Newman v. Rightmove plc, April 2026

- CoStar Group Investor Day Presentations on UK Strategy, 2024-2025

- Cayucos Capital: "One of the Best Businesses Ever Conceived" (Substack analysis)

- Google Cloud Partnership Announcement, 2025

- OnTheMarket / Agents' Mutual: Competition Appeal Tribunal Ruling on "One Other Portal" Rule, July 2017

- Rightmove Monthly House Price Index Archive (rightmove.co.uk)

- Scott+Scott UK LLP: GBP 1.5 Billion Collective Proceedings Claim Filing Documents

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube