Reckitt Benckiser Group plc: The Ultimate Margin Machine and the $18 Billion Hangover

I. Episode Roadmap & The $60 Million Panic

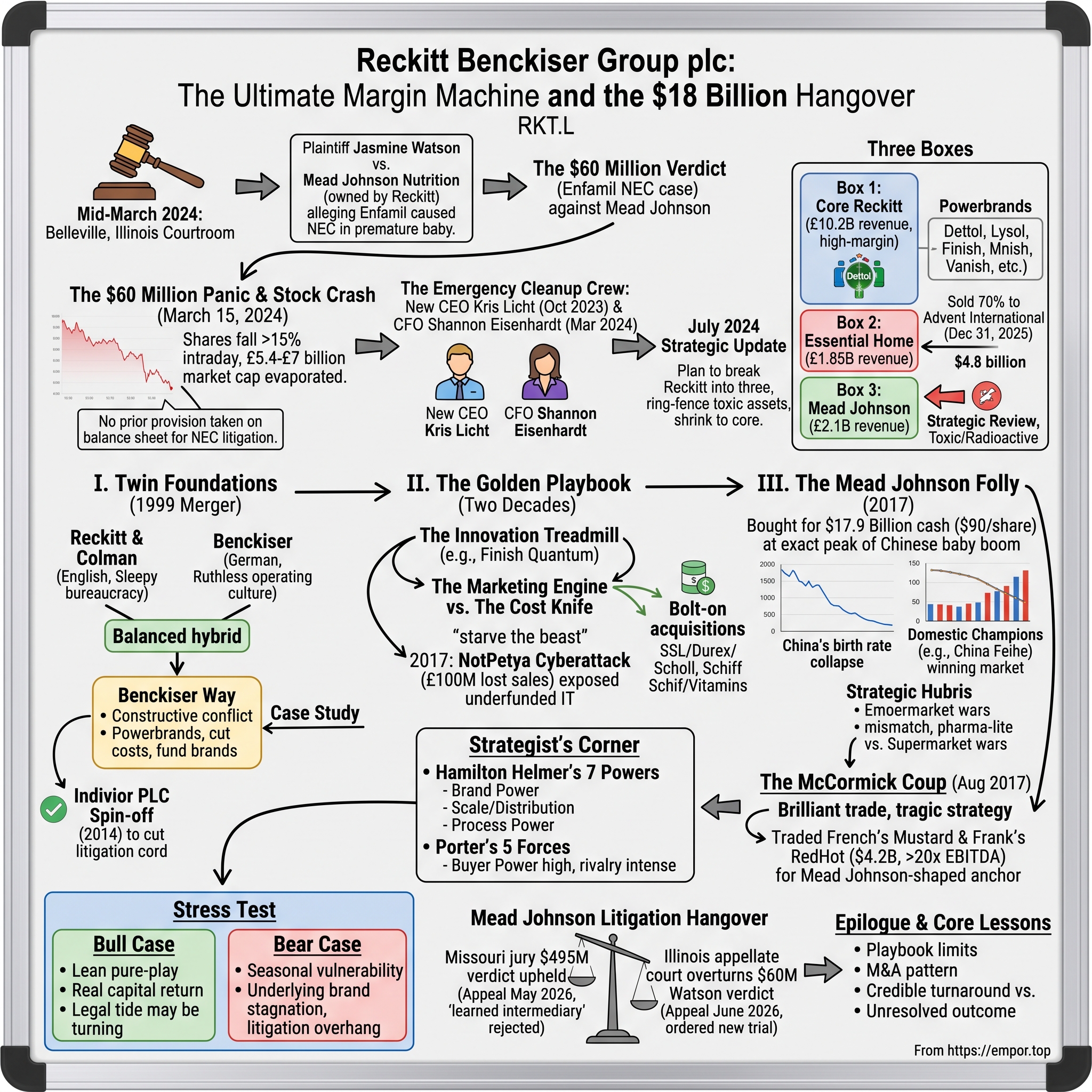

Picture a courtroom in Belleville, Illinois — St. Clair County, a working-class corner of the American Midwest about twenty minutes east of St. Louis. It is mid-March 2024. The jury has been deliberating over a question that, on its surface, sounds like a public-health debate and, on its balance sheet, turns out to be an existential threat to a FTSE 100 blue-chip headquartered four thousand miles away in Slough, England. The plaintiff, Jasmine Watson, alleged that a specialized bovine-milk-based formula — Enfamil, fed to her premature baby in a hospital neonatal unit — caused necrotizing enterocolitis, or NEC, a devastating intestinal disease that kills a meaningful share of the preterm infants it strikes. The defendant was Mead Johnson Nutrition, the maker of Enfamil. And Mead Johnson, since 2017, had been owned by Reckitt.

The jury returned its number on a Wednesday: $60 million against Mead Johnson.2 It was the first Enfamil NEC case in Illinois to reach a verdict, a test case in the truest sense — a single data point that the market would use to price hundreds of pending claims sitting behind it.

The reaction tells you everything about how markets work when a previously-ignored tail risk suddenly acquires a price. When London opened on Friday, March 15, 2024, shares of Reckitt Benckiser Group plc (RKT.L) went into free fall. The stock dropped more than 15% intraday and closed down roughly 14.6% — the worst single-session collapse in the company's history as an independent public company.1 Somewhere between £5.4 billion and £7 billion of market capitalization evaporated in a single six-hour trading window, dragging the shares to levels not seen in a decade.116

Here is what genuinely alarmed investors, and it is a detail worth dwelling on: Reckitt had taken no provision on its balance sheet for the NEC litigation.16 In accounting terms, management had judged that a future outflow was not "probable and reliably estimable." In market terms, that judgment now looked like a company that had been caught flat-footed by a liability it had inherited along with a business it arguably never understood. A $60 million verdict, by itself, is a rounding error for a group doing well over £14 billion in annual revenue. But multiply it across hundreds of plaintiffs, layer in punitive damages, and the math stops being a rounding error and starts being a question about whether the entire Mead Johnson acquisition was a generational mistake.

That Friday is our entry point, but it is not really our story. Our story is what the crisis forced. Within four months, CEO Kris Licht and his newly-installed CFO Shannon Eisenhardt stood in front of investors and announced the July 2024 Strategic Update — a plan to break Reckitt into three pieces, ring-fence the toxic assets, and shrink the company back down to the high-margin hygiene-and-health core that made it great in the first place.4 By the end of 2025, they had carved out the Essential Home business — Air Wick, Calgon, Cillit Bang, Woolite — selling a 70% stake to private-equity house Advent International at an enterprise value of up to $4.8 billion.5 Mead Johnson, meanwhile, sat in a corner of the portfolio labeled "under strategic review," radioactive and unsellable.

So this is a deconstruction story. It is the tale of consumer packaged goods' ultimate "margin machine" — a company that for two decades ran the most disciplined brand-compounding engine in Europe — and how that very discipline, applied to the wrong industry at the wrong moment, produced an $18 billion hangover. We will trace the arc: the ruthless German operating culture that built it, the bolt-on acquisitions that proved the model, the catastrophic 2017 lunge into infant formula at the exact peak of the Chinese baby boom, and the surgical dismantling now underway. Throughout, we will keep one question in front of us — not whether management says it can fix this, but what evidence says they can.

Let us start where the discipline came from. And that means starting with two very old companies, one English and sleepy, one German and merciless.

II. Twin Foundations & The Culture of Conflict (1999 Merger)

If you want to understand why Reckitt behaves the way it does, you have to understand that the name on the door is a bit of a historical accident. The DNA isn't really Reckitt's. It's Benckiser's.

Start with the English half. Isaac Reckitt leased a starch mill in Hull, on England's chilly North Sea coast, in 1840. Over the following century, the firm that bore his name folded in laundry blue, metal polish, and eventually merged in 1938 with Colman's — the Norwich mustard house founded in 1814, the one whose tagline joked that it made its fortune not from the mustard people ate but from the mustard they left on the side of the plate. By the late twentieth century, Reckitt & Colman was a perfectly respectable, perfectly unexciting FTSE constituent: a sprawling federation of hundreds of local household and food brands, many of them regional, few of them globally marketed, run by a courteous British bureaucracy that prized stability over ambition. It threw off cash. It did not threaten anyone.

Now the German half. Benckiser traces to 1823, when Johann A. Benckiser set up a chemicals business in Pforzheim, in Germany's southwest. For most of its life it was an industrial-chemicals concern. But in its modern incarnation — shepherded in the late twentieth century by the reclusive German billionaire family behind it and a young executive cadre obsessed with operational rigor — Benckiser reinvented itself as a specialist in consumer household chemicals: dishwasher products, fabric care, surface cleaners. What made Benckiser different was not its products but its temperament. It ran hot. It cut costs to the bone, innovated at a frantic pace, and demanded that every manager defend every line of spend. It was a company built like a sports team that fired the bottom of the roster every season.

In 1999, these two collided. The merger of Reckitt & Colman with Benckiser was billed, in the polite language of the era, as a "merger of equals." It was nothing of the sort. In practice, Benckiser's culture swallowed the combined group whole. The new entity took a hyphenated name — Reckitt Benckiser — but the operating philosophy, the personnel decisions, and above all the attitude came from Pforzheim, not Hull. The Englishmen ran the heritage; the Germans ran the company.

What emerged in the early 2000s was a corporate culture so distinctive it became a case study in business schools: the so-called "Reckitt Way." Its central, almost paradoxical, value was "constructive conflict." Where most large consumer-goods companies prized consensus and politeness, Reckitt institutionalized argument. Meetings were combative by design. Ideas were attacked on their merits, status be damned, and the expectation was that the best argument — not the most senior voice — won. Pay was brutally leveraged toward performance, with outsized bonuses for those who delivered and a fast exit for those who didn't. The company deliberately hired a multinational mix of ambitious managers and threw them into internal competition. It was not for everyone. It produced enormous turnover. It also produced, for a long stretch, the best margins in the industry.

The other pillar — the one that matters most for the investment story — was the Powerbrand concept. Reckitt looked at its inherited long tail of hundreds of small local brands and made a ruthless strategic choice: stop spreading capital and talent across a thousand mediocre products, and concentrate everything behind a short roster of global category leaders. Finish dishwasher tablets. Vanish stain removers. Dettol antiseptic. Air Wick, Harpic, Calgon, Lysol, Mortein, Nurofen. The logic was simple and powerful: a brand that is #1 or #2 in its category, marketed globally, can command premium pricing and fund its own innovation. A small local brand cannot. So Reckitt fed the winners and starved — or sold — everything else.

That choice is the foundation of everything that follows. It is why Reckitt, for two decades, generated gross margins north of 55% in categories that competitors treated as low-margin commodities. The question the rest of this story asks is whether a playbook this sharp could be aimed at the wrong target — and what happens when it is. To answer that, we need to see the playbook running at full speed.

III. The Golden Playbook & The Dark Side of Extreme Lean

Walk into a major supermarket and look at the dishwasher aisle. There is a cheap tablet, and there is Finish Quantum, sitting at a meaningful premium with a little red ball embedded in it that supposedly does something the cheap tablet cannot. That little red ball is the entire Reckitt strategy compressed into a single product.

The innovation treadmill

Reckitt's core trick was to take products that consumers regarded as undifferentiated chores — washing dishes, cleaning toilets, removing stains — and relentlessly re-engineer the format every few months. New chamber. New gel. New "Oxi Action" booster in Vanish. New "Power" claim. The famous internal cadence was roughly a six-month innovation cycle, and the point of it was less about chemistry than about leverage over retailers. Every time Reckitt launched a visibly new, better-marketed version, it forced grocers to clear shelf space for it and to keep paying for the branded premium rather than handing the slot to a private-label knockoff. Innovation, in other words, was a moat-maintenance tool. It justified gross margins in the mid-to-high fifties in categories where the underlying cost to manufacture was trivial.3

The analytical point worth stating plainly: this is real pricing power, but it is rented, not owned. It has to be re-earned every cycle with fresh marketing and fresh product news. The day Reckitt stops running on the treadmill, the premium starts eroding toward private label. We will see this tension surface again and again.

The marketing engine — and the cost knife

The other half of the model was financial. Reckitt ran one of the leanest fixed-cost structures in consumer goods, historically squeezing corporate and overhead costs down toward and below 15% of sales, while plowing roughly 12–13% of revenue back into advertising and brand-building. The philosophy: every pound not spent on bureaucracy is a pound that can buy brand equity, and brand equity is what lets you charge more than the store brand. It was a self-reinforcing flywheel — cut fat, fund brands, raise prices, expand margin, repeat.

But there is always a dark side to running a company this lean, and Reckitt's showed up in the form of chronically underfunded infrastructure. When you celebrate cost-cutting as a core value, the things that get cut first are the things that don't show up in next quarter's numbers: IT systems, supply-chain redundancy, spare manufacturing capacity. For years, this looked like brilliance. Then it looked like recklessness.

NotPetya: the bill for "starving the beast"

On June 27, 2017 — nine years to the day before this article is being written — a piece of malware called NotPetya, which had spread out of a compromised Ukrainian tax-software provider and is now widely understood to have been a state-grade cyberweapon, tore through corporate networks worldwide. Reckitt's severely under-invested IT estate was spectacularly exposed. The attack landed just days before the close of the second quarter, paralyzing factories and shipping systems across multiple markets. Production of Nurofen, Dettol, and Durex stalled; orders went unfilled and, critically, some of that revenue never came back.11 Reckitt told investors the episode knocked roughly two percentage points off second-quarter revenue growth and cost on the order of £100 million in lost sales, forcing a downward revision to full-year guidance.11 The supply chain had been cut so close to the bone that there was simply no buffer to absorb the shock.

The lesson — and management would eventually internalize it the hard way — is that "extreme lean" optimizes for visible margin while quietly accumulating invisible fragility. The same instinct that produced sector-leading profitability also produced a company that could be brought to its knees by a single attack. Keep that tension in mind; the current turnaround is, in large part, an admission that the beast had been starved too long.

The pivot to consumer health: bolt-ons that actually worked

While the household business minted cash, Reckitt was quietly executing a smarter, more durable strategy on the side — building a Consumer Health franchise through disciplined acquisitions that plugged directly into its existing distribution engine. Two deals defined this era.

In 2010, Reckitt acquired SSL International — owner of the Durex condom brand and Scholl footcare — for £2.5 billion, a rich multiple of roughly 17–18 times EBITDA.7 It looked expensive, but it bought two beautiful categories: intimate wellness and footcare, both high-margin, both emotionally resistant to private-label substitution. Nobody, it turns out, wants to buy the supermarket's own-brand condom. That defensiveness is exactly what Reckitt prized.

Then in 2012 came a genuine prizefight. Reckitt wanted Schiff Nutrition, a Salt Lake City vitamins-and-supplements maker behind MegaRed, Airborne, and Move Free. Germany's Bayer had already agreed to buy Schiff at $34 a share. Reckitt simply bulldozed in over the top with a superior cash offer — a roughly 24% premium to Bayer's price — and walked away with the company for about $1.4 billion, a steep ~16.5x EBITDA.8 It was aggressive, it was opportunistic, and it gave Reckitt an instant foothold in the lucrative US vitamins, minerals, and supplements market. Classic Benckiser: see the asset you want, pay up decisively, win.

The Indivior spin-off: cutting the litigation cord

There is one more pre-2017 move that reads, in hindsight, as deeply ironic. In 2014, Reckitt spun off its pharmaceutical arm as a separately-listed company, Indivior PLC. The crown jewel of that business was Suboxone, a sublingual film used to treat opioid addiction — a product facing both a looming generic cliff and a gathering storm of litigation over its marketing. By spinning it out, Reckitt insulated the clean consumer-goods parent from the legal and patent risk of a controversial pharmaceutical. Indivior would go on to settle a thicket of antitrust and federal claims for hundreds of millions of dollars in the years that followed.9

Sit with the irony. In 2014, Reckitt's management was sophisticated enough to recognize that a product with serious product-liability and litigation exposure did not belong inside a consumer-goods compounder, and surgically removed it. Three years later, the very same company would spend $18 billion to bolt on a different product — infant formula — carrying a litigation profile every bit as dangerous. Which brings us to the deal that defines the modern Reckitt story, and very nearly broke it.

IV. The Mead Johnson Folly & The McCormick Coup (2017)

In February 2017, Reckitt's then-CEO Rakesh Kapoor stood before investors and pitched the biggest acquisition in the company's history as a masterstroke of strategic logic. On February 10, 2017, Reckitt agreed to buy Mead Johnson Nutrition — the maker of Enfamil infant formula — for $90 per share in cash, a transaction valued at approximately $17.9 billion including net debt.6 Reckitt was, in one move, vaulting into the premium infant-nutrition market, a category management described as a natural extension of its consumer-health ambitions: trusted brands, premium pricing, defensive demand, and — the magic word — China.

Strategic hubris, in plain sight

Here is the problem that should have been visible from the start. Infant formula is not a fast-moving consumer good in any sense that Reckitt's playbook understood. It is, in the industry's own shorthand, a "pharma-lite" category — heavily regulated, scientifically sensitive, and sold through clinical, hospital-led channels where pediatricians and neonatal units are the gatekeepers. The Reckitt machine was tuned to win supermarket shelf wars with six-month product relaunches and aggressive advertising. None of that translates to a world where the buyer is a hospital procurement committee, the influencer is a doctor, and the regulatory framework treats your product as something close to a medical necessity for vulnerable infants. The cultural and operational mismatch was not a detail; it was the whole risk.

The benchmarking trap: overpaying for secular decline

Now, on the pure deal math, Reckitt's management had a defensible-looking argument, and it is worth understanding why, because it shows how dangerous comparable-based valuation can be. The infant-nutrition M&A comps of the prior decade were eye-watering: France's Danone had paid around 22x EBITDA for Numico in 2007, and Nestlé had paid roughly 20x EBITDA for Pfizer's infant-nutrition business in 2012. Against that backdrop, Reckitt's price — about 17.4x trailing EBITDA, or roughly 14x once you credited projected cost synergies — looked positively disciplined. By the logic of comps, Reckitt got a bargain.

The fatal flaw is that comps tell you what other people paid; they do not tell you what the asset is worth going forward. And Reckitt bought at the absolute cyclical peak. Two structural forces were about to converge against it. First, China's birth rate — the entire bull case for premium formula demand — was about to collapse, falling year after year as the long tail of the one-child policy and a generational shift in family economics took hold. Second, and just as damaging, a wave of fierce domestic Chinese champions was about to take the market. The standout was 中国飞鹤 China Feihe, which weaponized exactly the things foreign players were bad at: local-language marketing built around "fresher, more suitable for Chinese babies" messaging, deep distribution into lower-tier cities, and nationalist tailwinds after earlier foreign-brand safety scares faded from memory. Feihe and its domestic peers ate the premium foreign brands alive. The asset Reckitt bought began decaying almost from the moment the ink dried, and within a few years Reckitt was taking multi-billion-pound writedowns against the Mead Johnson goodwill.

The analytical takeaway: a "cheap" multiple on a peaking, structurally-challenged cash flow is not cheap. It is a value trap dressed in the clothing of discipline. Reckitt paid a disciplined-looking price for a business whose best days were behind it on the very day of purchase.

The McCormick coup: brilliant selling, tragic strategy

To help fund Mead Johnson and keep leverage from spiraling, Reckitt put its food division on the block — and here, briefly, the company showed how good it could be on the other side of a negotiating table. In July 2017, it agreed to sell French's Mustard and Frank's RedHot sauce to America's McCormick & Company for $4.2 billion, a deal that completed that August.10

Look at what McCormick paid: roughly seven times revenue and north of 20x EBITDA for a condiments business.10 By any standard, Reckitt extracted a spectacular price as a seller. On the trade alone, it was a coup.

But step back and the strategic picture is tragic. Reckitt sold a stable, beloved, high-moat, capital-light condiments business — the kind of brand that compounds quietly for a century, that nobody disrupts, that generates cash like a utility — in order to help pay for a volatile, capital-intensive, culturally alien infant-formula asset that started losing value immediately. It traded a French's-shaped jewel for a Mead Johnson-shaped anchor. The selling was masterful; what it funded was the worst capital-allocation decision in the company's history. That single swap — out of durable condiments, into decaying formula — is the cleanest illustration in this entire story of how a great operating company can still destroy enormous value through M&A.

The bill for all of this would not come due in full until that Illinois courtroom in 2024. But by then, the people in charge were no longer the people who had made the bet. Which brings us to the cleanup crew.

V. The Turnaround: Kris Licht, Shannon Eisenhardt, and Management Incentives

For a brief, deceptive moment, the Mead Johnson problem disappeared. Then a global pandemic arrived and made it disappear even harder — before bringing it roaring back.

The pandemic mirage

When COVID-19 swept the world in 2020, demand for Lysol and Dettol went vertical. Consumers disinfected everything; retailers couldn't keep surface sprays in stock; Reckitt's hygiene brands enjoyed the kind of demand spike that comes once a generation. Revenue surged, the share price recovered, and the structural rot inside the legacy portfolio — the decaying formula business, the underinvested supply chain, the debt taken on to buy Mead Johnson — was conveniently masked by a tidal wave of pandemic hygiene sales. It was, in retrospect, a sugar high. As hygiene demand normalized through 2022 and 2023, every underlying problem resurfaced, now compounded by the litigation that was building in American courtrooms. The pandemic didn't fix Reckitt; it just postponed the reckoning.

The new guard

Into this walked two operators with markedly different profiles than the founders of the mess.

Kris Licht became CEO in October 2023. Crucially, he was not an outsider parachuted in to point fingers — he was the architect of the very transformation he would now have to deliver. A former McKinsey partner and PepsiCo operator, Licht joined Reckitt in 2019 as Chief Transformation Officer, the executive specifically tasked with designing the company's "rejuvenation." That meant the unglamorous, expensive work the old Benckiser culture had always deferred: spending billions to rebuild the long-starved supply chain and IT backbone, the exact weaknesses NotPetya had exposed years earlier. By the time he took the top job, Licht already owned the strategy intellectually. The risk in that, which a skeptical investor should note, is that an insider who designed the plan is poorly positioned to admit the plan is wrong; the benefit is continuity and deep operational knowledge. Which dominates is something only the results will reveal.

Shannon Eisenhardt became CFO in March 2024 — arriving, by brutal timing, in the same month as the Watson verdict that wiped out billions in value. Her résumé is a consumer-goods finance pedigree: roughly two decades at Procter & Gamble, the gold standard of CPG financial discipline, followed by a senior CFO role at Nike running finance for its Consumer, Brand & Marketplace operations. She brought a P&G-trained obsession with disciplined capital allocation and a global retail playbook. The pairing is telling: a strategist-insider CEO and a financially-rigorous outsider CFO, installed precisely as the company's worst latent risk detonated.

Skin in the game — and how to read it

A turnaround is only as credible as management's incentive to see it through, so the structure of executive pay matters. According to Reckitt's directors' remuneration framework, Licht's package was built around a base salary of roughly £1.1 million, a target annual bonus of about 120% of base (with a maximum reaching multiples of salary and a third of any bonus deferred into shares for three years), and long-term incentive awards that vest over three years with a further mandatory two-year holding period after vesting.17 He was required to build and hold a substantial personal stake — on the order of 200,000 shares, worth roughly £9–10 million — and, importantly, to keep holding shares for two years after leaving the company.17 Eisenhardt's package centered on a base of around £760,000 with a multi-year requirement to accumulate roughly 100,000 shares.17

Why does this granular detail matter? Because the shape of the incentive is designed to defeat short-termism. A "hold for two years post-employment" clause means an executive cannot juice the share price, vest out, and walk away before the chickens come home — they are financially handcuffed to the durability of their decisions. For a company whose central sin was a value-destroying acquisition followed by years of under-investment to flatter near-term margins, an incentive structure that forces a long-term holding period is at least directionally the right answer. Whether it produces good decisions is, of course, a separate question from whether it discourages bad ones.

Realistic targets, fewer excuses

The most encouraging behavioral signal from the new team has been a tonal shift away from the old habit of blaming macro headwinds for misses. Licht and Eisenhardt launched a program they branded "Fuel for Growth," with an explicit, falsifiable target: drive fixed and corporate costs down from around 22% of revenue toward roughly 19% by 2027, and reinvest the savings directly into advertising behind a focused roster of core Powerbrands.3 This is, in a sense, the old Benckiser flywheel — cut fat, fund brands — rebuilt for a leaner, more transparent era, with public numbers investors can actually hold them to. Setting a specific, measurable cost target with a date attached is the opposite of vague reassurance, and it gives the market a yardstick. The next sections test whether the underlying business can carry the weight of those promises — starting with the radical restructuring that gave the plan its architecture.

VI. The Great Carve-Out & Sizing the Core Business

In July 2024 — four months after the share price cratered — Licht and Eisenhardt did something the old Reckitt would have found almost heretical. They announced they were going to make the company smaller.4

Three boxes

The July 2024 Strategic Update tore up Reckitt's tangled global-business-unit structure and re-sorted the entire portfolio into three clean, strategically distinct buckets.4 The logic was to separate the things worth keeping from the things worth selling and the things that simply had to be quarantined.

For the financial year 2025, the group reported total net revenue of around £14.2 billion.3 Mentally, split that into three.

The first and by far the largest box is Core Reckitt — roughly £10.2 billion of revenue, built around eleven Powerbrands spanning hygiene and consumer health: Dettol, Lysol, Finish, Vanish, Harpic, Durex, Mucinex, Nurofen, Gaviscon, Strepsils, Veet. This is the high-growth, high-margin engine — the part of the company management actually wants to be. In FY2025, Core Reckitt delivered like-for-like net revenue growth of about 5.2%, and its adjusted operating margin expanded to roughly 26.7%, up about 90 basis points year on year, powered especially by strong emerging-market demand.3 That is genuinely healthy. The whole strategic project is, in effect, an attempt to let the market value this business on its own merits.

The second box is Essential Home — roughly £1.85 billion of slower-growth, mature household brands like Air Wick, Calgon, Cillit Bang, and Woolite. Management's verdict on this box was unsentimental: it didn't fit the high-growth thesis, so it had to go. In July 2025 Reckitt agreed to sell a 70% controlling stake to private-equity firm Advent International, at an enterprise value of up to $4.8 billion (a figure that included up to roughly $1.3 billion of deferred and contingent consideration); the deal closed on December 31, 2025, with Reckitt retaining a 30% equity interest.5 We will come to what Reckitt did with the proceeds.

The third box is Mead Johnson — the infant-formula business, around £2.1 billion of revenue, sitting under "strategic review" and overhung by the NEC litigation.4 It is the box nobody can figure out how to empty. More on that in the stress test.

A note on what management isn't doing: it has not reproduced the kind of conglomerate structure that lets a CEO hide a weak division inside a strong group. By drawing these hard lines, Licht and Eisenhardt have made each piece's performance — and saleability — legible to outside investors. That transparency is itself a form of accountability.

The competitive field around the core

It is tempting to look at £10 billion of Powerbrands and conclude Reckitt is a giant. Within its niches, it is. But zoom out to the full battlefield and Reckitt is a mid-sized fish among whales, which shapes everything about its strategy.

Consider the neighborhood. Kenvue — the consumer-health business spun out of Johnson & Johnson, with brands like Tylenol, Listerine, Band-Aid, Aveeno, and Neutrogena and around $15 billion in revenue — was itself swallowed in a transformational deal: in November 2025, Kimberly-Clark agreed to acquire Kenvue at an enterprise value of approximately $48.7 billion, creating a roughly $32 billion-revenue health-and-wellness behemoth.12 Haleon plc, the consumer-health champion carved out of GSK (Sensodyne, Advil, Voltaren, Centrum), runs around £8 billion of revenue with formidable brand power. Above both loom the true titans: Procter & Gamble, north of $80 billion in revenue, dominating premium household cleaning (Tide, Cascade) and oral care (Crest, Oral-B); and Unilever, north of €50 billion, strong in home disinfection (Domestos) and personal care (Dove).

The strategic implication is sharp. Reckitt cannot win on sheer scale against P&G or a combined Kimberly-Clark-Kenvue. Its entire defensibility rests on being #1 or #2 in specific, narrow, defensible niches — being the disinfectant brand, the dishwasher-tablet brand, the chest-congestion brand — rather than the biggest player overall. Depth of category leadership, not breadth, is the moat. The consolidation happening around it (Kimberly-Clark/Kenvue being the headline) only raises the stakes: as competitors bulk up, Reckitt's bet that focus beats size becomes the central question of the investment case.

The hidden jewel: intimate wellness

One under-appreciated corner of Core Reckitt deserves a spotlight, because it is exactly the kind of asset the market tends to overlook inside a big portfolio. The Intimate Wellness category — Durex, K-Y, and a fast-growing feminine-hygiene brand called Intima — posted like-for-like growth of around 12.5% in FY2025, with Intima sales nearly doubling in China on rapid adoption.3 In absolute terms it is still a small slice of the Health portfolio. But its character is what makes it strategically valuable: high-margin, non-seasonal, emotionally resistant to private label, and structurally protected from the cold-and-flu volatility that whipsaws the rest of the self-care business. In a company whose biggest weaknesses are litigation overhang and seasonal earnings swings, a double-digit-growth, recession-resistant, intimate-care franchise is precisely the sort of quiet compounder that supports a premium valuation — if management keeps feeding it. To understand why categories like this matter so much, we need to put Reckitt's moat under a proper analytical microscope.

VII. The Strategist's Corner: Hamilton's 7 Powers & Porter's 5 Forces

Strip away the narrative drama and a single question determines whether Core Reckitt is a good business: how durable is its ability to charge more than the store brand for what is, chemically, often a near-identical product? Two frameworks help us interrogate that — Hamilton Helmer's 7 Powers and Porter's Five Forces — and the honest answer they produce is "strong, but conditional."

Hamilton Helmer's 7 Powers, applied

Brand Power — extremely high, but rented. This is Reckitt's marquee power. Brands like Dettol, Lysol, and Mucinex carry deep consumer trust built over decades, and that trust lets Reckitt charge a 20–40% premium over private label. When a parent reaches for a disinfectant to protect a sick child, "the trusted one" wins over "the cheap one" — that is brand power doing real economic work. But, as established with the innovation treadmill, this power is not a one-time moat you dig and forget. It must be continuously re-purchased with marketing spend and product news. The moment the advertising stops or the innovation stalls, the premium begins to bleed toward private label. Brand power here is a lease, not a freehold — which is exactly why the "Fuel for Growth" reinvestment math is so central to the thesis.

Scale / Distribution Advantage — strong. Reckitt's global footprint gives it something a challenger brand cannot easily replicate: guaranteed, dominant shelf positioning with the world's biggest retailers — Walmart, Target, the major European grocers, the Indian and Chinese trade. Being a "must-stock" supplier across thousands of stores worldwide is a genuine structural edge, and it is the thing a new entrant simply cannot buy at any reasonable price.

Process Power — niche but real. In pockets, Reckitt owns hard-to-copy know-how. The clearest example is Mucinex, whose proprietary bi-layer, sustained-release tablet technology — one layer dissolves fast, the other slow, releasing the active ingredient over twelve hours — has been genuinely difficult for generics to replicate. In a layperson's terms, it is the difference between a candy that dissolves instantly and one engineered to melt at a precise, controlled rate. That formulation complexity is a small but durable moat in specific OTC products, and it is the kind of advantage that doesn't require constant marketing to sustain.

What Reckitt notably lacks: network economies, switching costs of any depth (a consumer can swap dishwasher tablets next week with zero friction), and cornered resources. Its moat is brand plus distribution plus a sprinkle of process — formidable, but of the type that demands constant reinvestment to stay intact.

Porter's Five Forces

Bargaining power of buyers — high. The "buyers" here are not consumers but the giant retailers, and they squeeze relentlessly. Walmart and Amazon have every incentive to push Reckitt's margins down, promote private label, and demand trade spend. Reckitt's only real counter is the must-carry power of its top brands: a grocer that drops Dettol or Finish risks annoying shoppers, which gives Reckitt just enough leverage to defend pricing. It is a permanent, grinding tug-of-war.

Threat of new entrants — low to medium. Building a global brick-and-mortar consumer-goods business from scratch is brutally capital-intensive, which protects the incumbents. But the qualifier matters: digital-native, direct-to-consumer brands can now bypass the shelf entirely in specialized personal-care and wellness niches, reaching consumers through social media and subscription models. The barrier protects the old channel, not necessarily the category.

Threat of substitutes — medium. The substitute that haunts Reckitt is private label, and it is getting better. As retailers invest in high-quality own-brand products that perform nearly as well for meaningfully less money, Reckitt must continuously justify its premium through demonstrable efficacy and marketing. Every recession that trains consumers to "trade down" and discover that the store brand is fine is a structural threat to the premium.

Rivalry — intense. Reckitt, P&G, Unilever, Haleon, and the consolidating Kenvue/Kimberly-Clark are locked in permanent combat for the same shelf space and the same consumer attention. There is no comfortable equilibrium here, only a continuous arms race of innovation and advertising.

The three KPIs that actually matter

For a long-term investor trying to monitor whether the thesis is working, three numbers cut through the noise:

-

Like-for-like (LFL) net revenue growth for Core Reckitt. Management's credibility rests on consistently delivering in roughly the +4% to +6% range. This is the single best read on whether the Powerbrands are genuinely growing on volume and mix, not just price. FY2025's ~5.2% sat squarely in the zone; the early 2026 wobble (next section) shows how fragile it can be.3

-

Adjusted operating margin. The "Fuel for Growth" cost program lives or dies here. Group adjusted operating margin improved to about 24.9% in FY2025 from roughly 24.5% the prior year, with Core Reckitt's margin meaningfully higher.3 Watch whether margin keeps grinding up toward the 2027 ambition — that is the proof the cost discipline is real and being reinvested wisely rather than just cut.

-

Free cash flow conversion. The ability to turn operating profit into actual cash (management targets north of 90% conversion) is what funds the dividend, the deleveraging, and the buybacks. For a company carrying acquisition debt and a litigation tail, cash conversion is the oxygen supply.

Three numbers, one question each: is the top line growing on substance, is the cost machine delivering margin, and is it all turning into cash? Now let us pressure-test the whole edifice against the people who get paid to bet it falls apart.

VIII. Stress Test: The Activist Bull vs. Bear Case

Every compelling investment debate has a skeptic in the room asking the uncomfortable questions. Let us hand that skeptic the microphone first.

The activist / skeptic stress test

Why is Mead Johnson still here? The most pointed activist challenge is also the simplest. Management has been promising to "review strategic options" for the nutrition business for years, yet it remains stapled to the balance sheet. Until it is fully divested or demerged, the whole company trades at a conglomerate discount — investors refuse to pay a clean consumer-health multiple for a group that still has a litigation-soaked infant-formula problem buried inside it. The skeptic's framing is that every quarter Mead Johnson stays is a quarter management is failing to deliver the "simpler, purer Reckitt" it keeps promising.

The litigation overhang — and why it makes Mead Johnson nearly unsellable. Here is the crux. The NEC litigation is not one lawsuit; it is a mass tort with hundreds of active cases across federal multidistrict litigation and state courts. The numbers coming out of trials are not trivial. In a parallel case against rival Abbott, a Missouri jury's $495 million verdict (including $400 million in punitive damages) over Similac formula was upheld on appeal in May 2026 — and, critically, the appellate court rejected the "learned intermediary" defense, reasoning that preterm infant formula is food, not a prescription medical product.14 That ruling cuts directly against the defendants' core legal shield. The practical consequence for Reckitt is brutal: a business facing a multi-billion-pound, hard-to-quantify liability tail is effectively unsellable to a traditional strategic buyer, who would never assume that open-ended risk. The litigation doesn't just dent earnings; it freezes management's ability to execute the very divestiture investors are demanding.

The bull case

A lean, pure-play powerhouse. Strip out Essential Home (sold) and eventually Mead Johnson, and what remains is a focused, highly profitable, ~£10 billion consumer-health-and-hygiene pure-play with sector-leading margins and a genuine emerging-market growth engine. That is a fundamentally more valuable and more legible company than the sprawling conglomerate of 2017.

Real capital return. This is not just narrative; it shows up in cash going back to shareholders. The Advent transaction funded a planned return of approximately $2.2 billion to shareholders via a special dividend and associated share consolidation, alongside an ongoing buyback program.5 A management team that says it will simplify and then actually hands the proceeds back — rather than rolling them into the next empire-building acquisition — is demonstrating exactly the capital discipline that was missing in the Mead Johnson era. Behavior, not words.

The legal tide may be turning — partially. In June 2026, an Illinois appellate court overturned the original $60 million Watson verdict — the very verdict that triggered the 2024 crash — finding that the trial judge had wrongly rejected arguments under the learned intermediary doctrine (the principle that a manufacturer's duty to warn runs to the prescribing physician, not directly to the parent).13 The court ordered a new trial rather than dismissing the case outright, but the directional signal cheered bulls: appellate courts reinforcing the learned-intermediary shield would lower the ultimate liability ceiling across the entire docket.

But notice the tension the honest analyst must flag: the Illinois appellate court leaned toward the defense on learned intermediary, while the Missouri appellate court explicitly rejected it by classifying formula as food.1314 That is not a clean turning tide; it is a genuinely unsettled, jurisdiction-dependent legal landscape where the ultimate liability could land anywhere across a very wide range. Anyone who tells you the litigation is "basically resolved" in either direction is selling certainty that does not yet exist.

The bear case

Seasonal vulnerability is real and recurring. Reckitt's self-care earnings are hostage to the weather. The Q1 2026 trading update was the live demonstration: a mild winter with low cold-and-flu incidence (down roughly 10% versus the prior season) sent seasonal OTC revenue down about 11%, dragging Core Reckitt's like-for-like growth down to just 1.3% for the quarter — versus 3.1% excluding the seasonal effect.15 Management maintained full-year guidance and pointed to innovation launches and emerging-market strength to make up the gap, but the episode underscored how a single warm winter can stall the headline growth number that the whole equity story depends on.15 When your premium valuation rests on consistent +4–6% growth, double-digit swings in a major category from something as uncontrollable as flu season are a structural weakness.

Underlying brand stagnation. Strip out price increases and the picture in some mature categories is less rosy: volume growth runs flat, a signal that a chunk of recent "growth" has been inflation passed through rather than more units sold. Flat volumes in the face of high-quality private label and nimble digital challengers is the slow-motion risk to the entire brand-power thesis — it is what the erosion of "rented" pricing power looks like before it shows up in the headline numbers. The bull says innovation and marketing will defend the premium; the bear says the treadmill only ever runs to stand still, and one day the legs give out.

Where does that leave the war-game? Reckitt is a genuinely high-quality operating business wrapped around an unresolved legal time bomb and exposed to a category — formula — it should arguably never have entered. The bull and bear are not really arguing about the quality of the core; they agree it is good. They are arguing about whether management can detach the core from the wreckage before the wreckage drags the whole thing down to its value. That is the question the final reckoning turns on.

IX. Epilogue & Core Business Lessons

Step back from the courtroom drama, the writedowns, and the carve-outs, and Reckitt's story distills into a few hard lessons that apply far beyond one British consumer-goods company.

The power and the pitfalls of playbooks. Benckiser built one of the most formidable operating playbooks in consumer goods: extreme cost discipline, relentless innovation cadence, ruthless brand focus, leveraged pay-for-performance. In its home territory — hygiene, household care, OTC self-care — that playbook is a genuine competitive weapon, and it still is. But a playbook that brilliant breeds a dangerous confidence: the belief that excellence in execution translates to excellence in any market. It does not. Aimed at regulated pediatric nutrition — a clinical, hospital-led, scientifically sensitive category with entirely different rules — the same playbook was not just ineffective; it was actively misleading, because it gave management the false certainty to overpay for a structurally declining asset. The lesson is not "Reckitt is bad at operating." It is that operating excellence and strategic judgment are different muscles, and a company can be world-class at one while failing catastrophically at the other.

The M&A lesson. The contrast within Reckitt's own history could not be cleaner. The disciplined bolt-on deals — SSL's Durex and Scholl, Schiff's vitamins — worked precisely because they plugged into the existing distribution engine and leveraged the core competency. They scaled what Reckitt already did well. The transformational, debt-fueled lunge — Mead Johnson — destroyed enormous value because it introduced severe cultural, operational, and regulatory friction the organization was never equipped to handle, funded by the sale of one of its best durable assets. The pattern generalizes: bolt-ons that extend a proven engine tend to create value; transformational acquisitions that require an organization to become something it is not tend to destroy it. The bigger and bolder the deal, the more the burden of proof should rise — and the more skeptical investors should be of comps-based reassurance that "the multiple looks reasonable."

Final reflections. Whatever one concludes about the 2017 decision, the current management team has, so far, behaved like adults cleaning up after a party they did not throw. Under the intense pressure of a generational litigation crisis, Licht and Eisenhardt have executed a genuinely radical portfolio simplification — splitting the group into legible pieces, selling Essential Home at a respectable price, handing real cash back to shareholders, and setting public, falsifiable cost and growth targets rather than hiding behind macro excuses. That is the conduct of a credible turnaround, and it deserves to be acknowledged as such.

But credit for process is not the same as proof of outcome, and the honest verdict is that the two things that will actually determine Reckitt's fate remain unresolved. Can management contain — and ultimately detach — the Mead Johnson liability before the litigation, still unsettled across hostile and friendly jurisdictions alike, crystallizes into a multi-billion-pound number? And can it reignite genuine volume growth across the eleven core Powerbrands, proving that its brand power is a durable freehold and not just an expensively-rented lease on a treadmill that never stops? The margin machine still runs. Whether it can outrun its own $18 billion hangover is the question every share of RKT.L is, right now, an open bet on.

References

-

FTSE 100 giant Reckitt responds to share price plunge as Enfamil baby formula lawsuits mount — City A.M., 2024-03-15 ↩↩

-

Reckitt Benckiser (RKT) Falls After $60 Million Jury Verdict Over Formula — Bloomberg, 2024-03-15 ↩

-

Results for the year ended 31 December 2025 — Reckitt Benckiser Group plc, 2026-03-05 ↩↩↩↩↩↩↩

-

Reckitt Announces Major Strategic Update — Reckitt Benckiser Group plc, 2024-07-24 ↩↩↩↩

-

Advent to acquire majority stake in Reckitt's Essential Home portfolio — Advent International, 2025-07-18 ↩↩↩

-

Kirkland Represents Mead Johnson on Acquisition by Reckitt Benckiser for Approximately $17.9 Billion — Kirkland & Ellis LLP, 2017-02-10 ↩

-

Reckitt — corporate history of SSL International and Schiff Nutrition acquisitions ↩

-

Reckitt Benckiser bids $1.4bn for Schiff — NutraIngredients, 2012-11-22 ↩

-

Indivior Announces Agreement to Resolve Suboxone Antitrust Litigation — Indivior PLC ↩

-

McCormick Completes Acquisition of Reckitt Benckiser's Food Division — McCormick & Company, Inc., 2017-08-17 ↩↩

-

Reckitt Benckiser blames NotPetya outbreak for £100m revenue loss — Computing, 2017-07-06 ↩↩

-

Kimberly-Clark to Acquire Kenvue, Creating a $32 Billion Global Health and Wellness Leader — PR Newswire, 2025-11-03 ↩

-

Appeals court dumps $60M baby formula NEC verdict vs Mead Johnson — Madison-St. Clair Record / Legal Newsline, 2026-06 ↩↩

-

Court upholds $495 million verdict against Abbott Laboratories in case over preterm infant formula — Jefferson City News-Tribune, 2026-05-07 ↩↩

-

Q1 Results 2026 Trading Update — Reckitt Benckiser Group plc, 2026-04-22 ↩↩

-

Reckitt Shares Sink as Investors See More Trouble From Baby Formula Lawsuits — U.S. News / Reuters, 2024-03-15 ↩↩

-

Annual Report and Accounts 2025 — Directors' Remuneration Report, Reckitt Benckiser Group plc ↩↩↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube