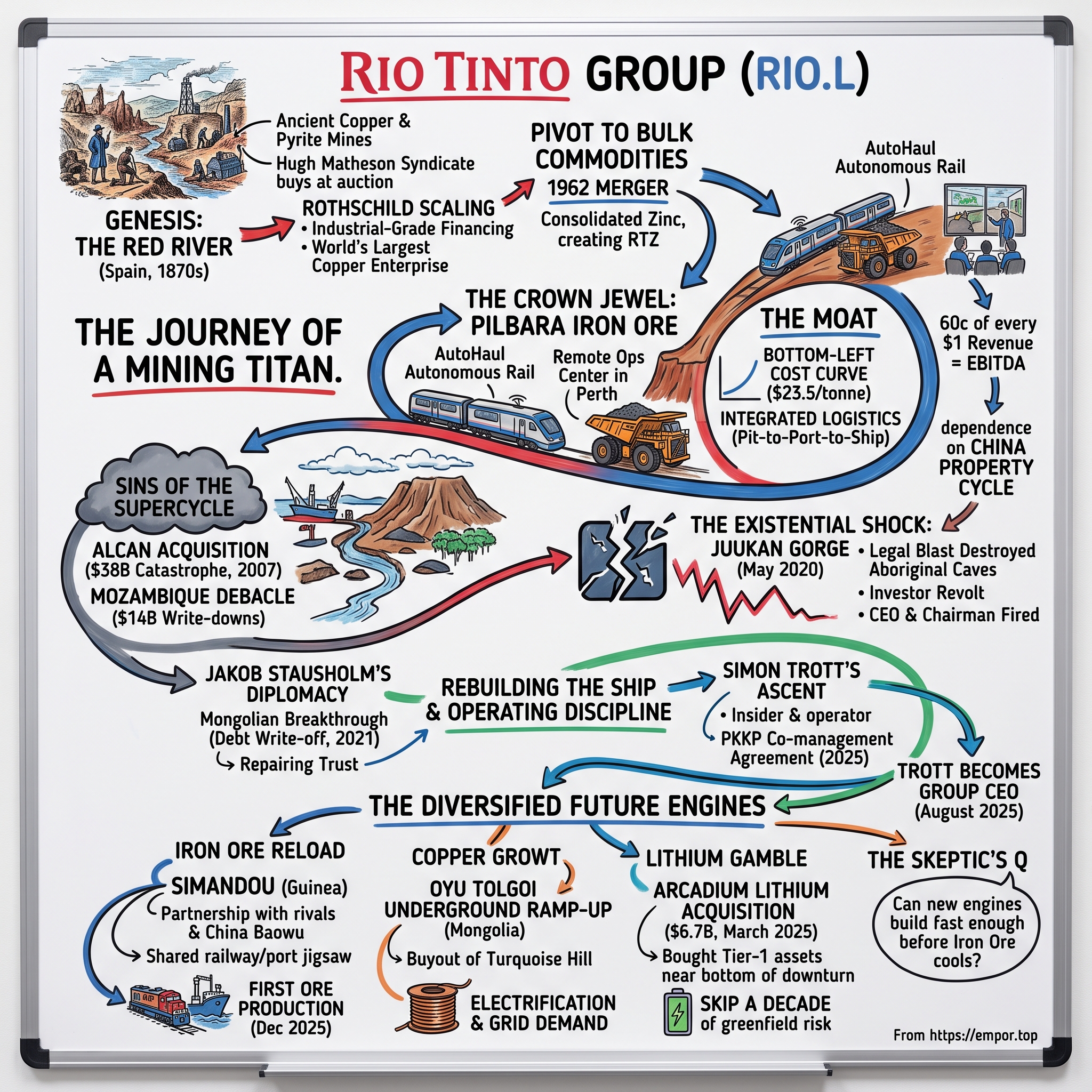

Rio Tinto Group: The Titan of the Cost Curve

I. Introduction & Episode Roadmap

Picture a driverless train nearly two and a half kilometres long, hauling 28,000 tonnes of iron ore across the red emptiness of the Western Australian outback. No driver sits in the cab. There is no cab worth speaking of. The train threads 1,700 kilometres of company-owned track, loads itself under automated chutes, and empties itself at a port on the Indian Ocean, all coordinated from an operations centre in Perth 1,500 kilometres away. This is the physical heartbeat of Rio Tinto Group, and it explains, better than any slide deck, how a company can extract one of the most abundant rocks on Earth and still print money in almost any market.

Rio Tinto (RIO.L on the London Stock Exchange, dual-listed with an Australian arm) is the world's second-largest diversified miner, behind only BHP. In 2025 it generated $57.6 billion of consolidated sales revenue and $25.4 billion of underlying EBITDA, the latter up 9% on the prior year.1 Those are the numbers of an industrial supertanker. But the number that tells the real story is a margin: in its iron ore division, Rio Tinto routinely converts more than 60 cents of every revenue dollar into EBITDA. In a commodity business, where the product is undifferentiated and the buyer cares only about price and grade, that should be impossible. Understanding why it is not impossible is the whole point of this story.

The cost-curve moat

Most businesses build moats out of brands, patents, or software lock-in. Rio Tinto's moat is dug out of the ground. Its core Pilbara iron ore system sits at the absolute bottom-left of the industry cost curve, producing at roughly US$23.5 per wet metric tonne in 2025 while the ore itself sold into a market that ranged from the $80s to well above $100 per tonne.1 When you are the lowest-cost producer of a commodity the world cannot do without, the high-cost producers set the price, and you pocket the difference as economic rent. That is the engine. Everything else in this story is either feeding that engine, spending its cash, or trying to reduce the company's terrifying dependence on it.

Themes and inflection points

Four threads run through the modern Rio Tinto story, and each is a lesson in its own right.

The first is an existential lesson in social licence. In May 2020, Rio Tinto legally blew up two 46,000-year-old Aboriginal rock shelters at Juukan Gorge to access a modest amount of higher-grade ore. The blast was legal. It was also a corporate catastrophe that cost the CEO, two senior executives, and eventually the chairman their jobs, and it rewired how the entire industry thinks about the ground beneath its mines.

The second is a study in M&A at the extremes: the disastrous $38 billion top-of-cycle acquisition of aluminium producer Alcan in 2007, set against the recent $6.7 billion all-cash purchase of Arcadium Lithium in March 2025, executed near the bottom of a brutal lithium downturn.5 Same company, opposite instincts, twenty years apart.

The third is the unlocking of megaprojects that had been frozen for decades: first ore from Simandou in Guinea in December 2025, and the ramp-up of the underground copper mine at Oyu Tolgoi in Mongolia.

The fourth is people. Rio Tinto passed the baton in August 2025 from Jakob Stausholm, the Danish outsider brought in to stabilise a company in crisis, to Simon Trott, the 25-year Pilbara insider who ran the iron ore machine.6 The choice of successor tells you what the board thinks the next decade is about: operating discipline, not diplomacy.

Let's start where the company started, on a poisoned river in southern Spain.

II. Older History: The Genesis of the "Red River"

The Río Tinto is one of the strangest rivers on Earth. It runs deep red and acidic through the hills of Andalusia, its waters so laden with dissolved metals that almost nothing lives in them. Scientists now study it as an earthbound analogue for Mars. For thousands of years, though, it meant something simpler to the people of Huelva: copper, silver, and pyrite, mined here since the Bronze Age and worked by the Phoenicians, the Romans, and the Moors before the seams were left to the Spanish crown.

By the 1870s the Spanish state's mines were tired, indebted, and badly run. In 1873, a syndicate of British and European investors led by the Scottish banker Hugh Matheson bought them at auction and, on 29 March 1873, registered a new vehicle to run them: The Rio Tinto Company.2 The winning bid was roughly £3.7 million, an enormous sum for the era, and it bought not a working business so much as a bet that modern capital and engineering could resurrect an ancient asset. That bet is, in essence, the same bet Rio Tinto makes today at Simandou.

The Rothschild scaling

The company that Matheson founded quickly outgrew Matheson's own resources. Scaling the Huelva operation, opening vast open-pit workings, building railways down to the coast, and shipping ore and pyrite across Europe, required industrial-grade financing. By the end of the 1880s, control had passed toward the House of Rothschild, whose capital turned Rio Tinto into the largest copper enterprise on the planet. Around the turn of the century, the Spanish mines were producing on the order of a tenth of the world's copper.2 For a stretch in the late nineteenth century, if you touched copper wire anywhere in the industrialising world, there was a fair chance the metal had come out of that red Andalusian valley.

Lessons in long-cycle capital

What matters for our story is not the copper itself but the corporate DNA that Huelva encoded. Three habits were formed here that still define Rio Tinto: enormous upfront spending on infrastructure long before the cash comes back; ownership of very long-life assets measured in decades rather than years; and constant, grinding negotiation with sovereign governments over who owns what lies beneath the soil. A miner is always, in the end, a guest on someone else's land. Rio Tinto learned that in Spain the hard way, through strikes, a notorious 1888 massacre of protesting workers and townspeople, and eventually a slow retreat, selling down its Spanish holdings by the mid-twentieth century.

The pivot to bulk commodities

The modern company was born not in Spain but in a 1962 merger. The Rio Tinto Company combined with the Australian miner Consolidated Zinc to create Rio Tinto-Zinc (RTZ), with an Australian operating arm, Conzinc Riotinto of Australia.2 That deal shifted the centre of gravity from European copper toward the vast, under-explored mineral basins of Western Australia. Within a few years the company would stumble into the Pilbara, the iron ore province that would come to define it. The red river of Spain gave way to the red dirt of Australia, and a copper company slowly became an iron ore company. That is where the real money was, and still is.

III. The Crown Jewel: Pilbara and the Iron Ore Money Printer

To understand Rio Tinto, you have to understand that it is, financially, an iron ore company wearing a diversified-miner costume. In 2025 the Iron Ore division generated $15.2 billion of underlying EBITDA, close to 60% of the entire group's total, even after an 11% decline driven by softer prices.1 Strip away iron ore and you have a solid mid-tier miner. Keep it, and you have one of the great cash machines in global industry. Every other ambition in this story, copper, lithium, decarbonisation, is funded, directly or indirectly, by Pilbara dirt.

What the Pilbara actually is

The Pilbara is not a mine. It is an integrated logistics empire the size of a small country. Rio Tinto runs 17 iron ore mines there, feeding four port terminals on the coast at Dampier and Cape Lambert, connected by roughly 1,900 kilometres of privately owned, heavy-haul railway.8 The genius is not any single element but the fact that Rio Tinto owns the whole chain, pit to port to ship. It does not rent the railway, negotiate with a port authority, or share the network with rivals on someone else's terms. It controls the entire flow of rock from the ground to the deck of a Chinese-bound bulk carrier.

The cornered resource

The first of Hamilton Helmer's "7 Powers" that Rio Tinto enjoys here is a cornered resource: privileged access to some of the world's highest-grade, lowest-impurity hematite. Grade matters enormously in iron ore. Higher iron content and lower contaminants mean a steel mill gets more metal and less waste from every tonne, which is why premium ore commands a premium price. Rio Tinto did not invent this ore; it simply secured tenure over an unusually good piece of the planet, decades ago, and has held it since. You cannot replicate a Pilbara. There is only one, and most of the best of it is already spoken for.

Process power: the robots in the desert

The second power is process power, and here Rio Tinto genuinely pioneered. It built AutoHaul, the world's first fully autonomous, long-distance heavy-haul rail network, trains that drive themselves across the outback with no one aboard. Its haul trucks, the four-storey giants that move ore inside the pits, increasingly drive themselves too, and its drills are automated and remotely supervised. Think of it as a single, semi-robotic factory that happens to be spread across an area larger than many European nations. The payoff is not just lower labour cost; it is consistency. Machines do not get tired at 3 a.m., do not vary their braking, and can be optimised centrally. In a business where a few cents per tonne compound across hundreds of millions of tonnes, that consistency is worth billions.

Scale economies and the cost curve

The third power is scale. Running the Pilbara at roughly US$23.5 per wet metric tonne in 2025, against ore that sold for multiples of that, is the payoff for a century of accumulated infrastructure and a decade of automation.1 This is the "bottom-left of the cost curve" position that management talks about constantly, and for once the rhetoric matches the reality. Imagine every iron ore producer in the world lined up from cheapest to most expensive. Global demand draws a line across that curve, and the price is set by the last, most expensive tonne needed to meet it. Rio Tinto sits at the far cheap end. When prices fall, the expensive producers at the right of the curve bleed and eventually shut, tightening supply, while Rio Tinto keeps earning. When prices rise, Rio Tinto's margin explodes. Heads it wins comfortably; tails it wins anyway.

The concentration risk nobody at Rio can hedge away

Now the uncomfortable part, the part an independent analyst has to say plainly. This same crown jewel is the company's single greatest vulnerability. Nearly 60% of group EBITDA depends on one product, sold overwhelmingly into one country, for one purpose: iron ore, to China, to make steel, largely for construction. Rio Tinto's fortunes are chained to the Chinese property and infrastructure cycle in a way management cannot fully diversify away in the near term. When Beijing builds, Rio Tinto prints. When Chinese steel demand structurally softens, as many believe it now is, the money printer slows, and no amount of automation in the Pilbara can offset a demand shock originating 6,000 kilometres away. That single dependency is why the rest of this story, copper, lithium, Simandou, exists at all. The company is racing to build a second engine before the first one loses altitude.

But before we get to the rebuild, we have to visit the wreckage, because Rio Tinto's recent history is also a cautionary tale about what happens when a cash machine convinces its owners they are geniuses.

IV. Sins of the Supercycle: The Tom Albanese and M&A Overpayment Era

By 2007, the commodity world had lost its mind, and Rio Tinto lost it along with everyone else. China's growth had ignited a "supercycle" in which metal prices seemed to have no ceiling. Boards that had spent the 1990s starved of returns were suddenly flush and fearful of being left behind. Into this euphoria stepped Tom Albanese, a geologist by training who became Rio Tinto's chief executive in May 2007. His first major act would define, and eventually end, his tenure.

The Alcan catastrophe

In 2007, Rio Tinto agreed to buy the Canadian aluminium giant Alcan for roughly $38 billion in an all-cash deal, one of the largest acquisitions in mining history. Two motives drove it, and neither aged well. The first was supercycle conviction: a belief that aluminium demand would compound indefinitely. The second was defensive. Rio Tinto was itself a takeover target; BHP was circling with a hostile approach, and swallowing Alcan made Rio Tinto larger, more indebted, and harder to digest, a classic "poison pill by acquisition." Management paid a full price at the top of the market partly to avoid being bought at the top of the market.

Then the timing revealed itself. The 2008 Global Financial Crisis hit within a year. Aluminium is brutally cyclical and brutally energy-intensive, essentially, you are selling congealed electricity, so it gets punished twice in a downturn: prices collapse while smelting input costs stay stubbornly high. Rio Tinto had bought a highly cyclical, capital-hungry business with borrowed money at the exact peak. The debt taken on to fund Alcan nearly sank the company; Rio Tinto was forced into an emergency rights issue and a controversial, later-abandoned tie-up with a Chinese state investor to shore up its balance sheet.

The Mozambique debacle

If Alcan was hubris, Riversdale was carelessness. In 2011, Rio Tinto paid about $3.7 billion for Riversdale Mining to secure coking coal deposits in Mozambique's Zambezi valley.3 The thesis rested on being able to move coal cheaply down the Zambezi River by barge. That assumption turned out to be, quite literally, unfloatable: the government never approved large-scale barging, and the alternative, hauling coal overland or building new rail and port infrastructure, blew up the economics entirely. The value evaporated almost as fast as it had been paid.

The $14 billion reckoning

The bill came due in January 2013. Rio Tinto announced write-downs of roughly $14 billion, the bulk against Alcan's aluminium assets and a chunk against the Mozambique coal misadventure, and Tom Albanese abruptly departed as chief executive.3 It was one of the largest value-destruction events in the sector's modern history, and its consequences outlived Albanese by a decade. The scar tissue produced a culture of extreme capital-allocation conservatism: for years afterward, Rio Tinto returned cash to shareholders and shied away from big deals, terrified of repeating 2007. That caution was rational, even admirable. But as we will see, it also meant the company arguably under-invested in growth for a decade, and it makes the recent Arcadium gamble all the more striking as a break from a hard-learned reflex.

For all the money lost in Canada and Mozambique, though, the deepest wound Rio Tinto inflicted on itself in this era did not show up as a write-down. It showed up as a hole in the ground where 46,000 years of human history used to be.

V. The Existential ESG Shock: Juukan Gorge

On 24 May 2020, in the middle of a global pandemic that had pushed everything else off the front pages, Rio Tinto detonated explosives at Juukan Gorge in the Pilbara. The blast, part of an expansion of the Brockman 4 mine, destroyed two rock shelters that archaeologists had shown were continuously occupied by humans for around 46,000 years, one of the most significant Aboriginal heritage sites on the Australian continent, containing artefacts including a 4,000-year-old plaited-hair belt genetically linked to the living Traditional Owners. The blast unlocked access to a relatively modest quantity of higher-grade ore. In exchange, Rio Tinto destroyed something irreplaceable and detonated its own reputation.

Legal, and indefensible

The most damning fact is that the blast was legal. Rio Tinto had obtained approval years earlier under Western Australia's antiquated 1972 Aboriginal Heritage Act, legislation that gave companies consent to disturb sites and gave Traditional Owners almost no power to withdraw it, even after new evidence of the site's staggering significance emerged. Internally, Rio Tinto had known for years how important the shelters were and had even considered options to avoid them. It proceeded anyway. This is the crux of the lesson: the company mistook legal permission for social licence, and discovered they are not the same thing. A permit protects you from regulators. It does not protect you from the moral judgment of your shareholders, your host communities, and the public.

The investor revolt

What turned a scandal into a governance earthquake was the reaction of Rio Tinto's own owners. When the board's first response was to dock the executives responsible a few million dollars in bonuses, Australia's powerful superannuation funds, long-term institutional shareholders managing the retirement savings of millions of Australians, refused to accept it. This was not activism from the fringe; it was the core shareholder base declaring that a slap on the wrist was unacceptable. They demanded structural accountability, and they had the votes to force it.

The exodus

The dominoes fell over the following months. Chief executive Jean-Sébastien Jacques, iron ore head Chris Salisbury, and corporate relations head Simone Niven all left. Then, in March 2021, chairman Simon Thompson announced he would not seek re-election, accepting ultimate accountability for a failure of governance that happened on his watch.[^4] A legally-sanctioned mining blast had cost a $100-billion company its chief executive and its chairman. In the history of corporate ESG, few events have so cleanly demonstrated that these risks are financial, not merely reputational.

Social licence as a hard economic asset

Here is the analytical takeaway, and it reframes the entire Pilbara moat we admired two sections ago. Rio Tinto's lowest-cost ore is only valuable if Rio Tinto is allowed to mine it. The company's mining leases sit on land whose Traditional Owners hold heritage rights and, increasingly, real negotiating power. If those relationships break down, the cheapest reserves on the planet become stranded rock. Juukan Gorge converted "social licence to operate" from a soft phrase in a sustainability report into a hard input on the cost curve, as real as diesel or rail capacity. Repairing that licence, at genuine cost to mine planning and flexibility, became the central task of the next management team. The company that broke the ground now had to prove it could be trusted to keep operating on it.

VI. Rebuilding the Ship: Jakob Stausholm's Diplomacy & Simon Trott's Ascent

When Rio Tinto needed a new chief executive in the wreckage of Juukan Gorge, it made a revealing choice. It did not promote a hard-charging mining operator. It elevated its chief financial officer, Jakob Stausholm, a Danish executive who had spent much of his career outside mining, at Shell and at the shipping and logistics group Maersk, before joining Rio Tinto in 2018. Stausholm was, in effect, hired as a repairman for trust: measured, unflashy, and untainted by the old iron ore culture. His mandate was not to find the next great orebody. It was to make Rio Tinto a company that governments and communities were willing to do business with again.

The Mongolian breakthrough

His first big test was Mongolia. Rio Tinto's Oyu Tolgoi copper project had been mired for years in a bitter dispute with the Mongolian government over costs, financing, and how much the state was effectively on the hook for. The standoff was blocking the development of a world-class underground copper mine. In December 2021, Stausholm cut the knot: Rio Tinto agreed to write off roughly $2.4 billion of debt that the Mongolian state owed in respect of the project, clearing the path to build the underground mine.4 Read narrowly, Rio Tinto "lost" $2.4 billion. Read correctly, it spent $2.4 billion of goodwill to unlock one of the most important copper deposits of the coming decades. It was the anti-Juukan: giving up value in the short term to preserve a relationship and a licence to operate. This is the Stausholm playbook in miniature.

The repairman in Perth

While Stausholm worked the capitals of the world, someone had to repair the crown jewel itself. In 2021, Rio Tinto appointed Simon Trott as chief executive of iron ore. Trott was the ultimate insider, a Western Australian who had spent more than two decades at Rio Tinto across commodities and geographies, and his brief in the Pilbara was threefold: stabilise operations after years of cost inflation and underperformance, and, above all, rebuild relations on the ground with the Traditional Owners whose trust the company had shattered.

The PKKP co-management agreement

The clearest evidence that something had genuinely changed came in May 2025, when Trott signed a co-management agreement with the Puutu Kunti Kurrama and Pinikura (PKKP) Aboriginal Corporation, the Traditional Owners of the land that included Juukan Gorge.[^6] The agreement embedded Indigenous participation directly into mine-life planning, giving Traditional Owners real influence, including effective vetoes, over how and where Rio Tinto operates on their country. An independent observer should note both sides of this. It is a meaningful structural change and a plausible new template for reducing heritage risk across the industry. It is also, unavoidably, a constraint: it trades some operational flexibility and speed for durability of licence. Management is betting that durability is worth more than flexibility. Given what the alternative cost, that is a defensible bet, but it is a bet, and it will show up in the pace and cost of future mine development.

The transition and the strategy

By 2025, with the reputation stabilised, Rio Tinto's board decided the era of diplomacy could give way to an era of operating discipline. In August 2025, Stausholm stepped down and Trott became group chief executive.6 The symbolism is hard to miss: the outsider hired to heal the company handed the reins to the consummate insider hired to run it. Trott moved quickly to simplify, reorganising Rio Tinto around three core segments, Iron Ore, Copper, and Aluminium & Lithium, collapsing a more complicated structure into three clear engines of value.

On capital allocation, the post-Albanese discipline still holds, at least on paper. Rio Tinto reaffirmed its commitment to returning 40–60% of underlying earnings as dividends through the cycle, and declared total ordinary dividends of 402 US cents per share for 2025, some $6.5 billion, at the top of that payout range for a full decade running.1 Capital expenditure, however, has climbed sharply as the growth projects ramp, reaching $12.3 billion in 2025, above the roughly $10 billion "steady-state" the company has historically guided toward.1 Executive incentives are tied to return on capital employed and to emissions-reduction targets, an explicit attempt to make sure the growth spending is disciplined and that another Juukan-style failure carries personal cost. The skeptic's question, which we will return to, is whether a company simultaneously promising capital discipline and spending record sums on Simandou, Oyu Tolgoi, and lithium can truly do both. The answer depends on the growth engines actually working. So let's look at them.

VII. The Copper & Lithium Growth Engine: Oyu Tolgoi & the Arcadium Lithium Gamble

If iron ore is Rio Tinto's present, copper is its most credible bet on the future, and in 2025 that bet started to pay. Copper underlying EBITDA surged 114% to $7.4 billion, driven by a 12% rise in copper sales volumes and a 9% increase in the LME copper price, with a meaningful assist from higher gold volumes and prices out of Mongolia.1 The logic behind the copper push is one of the most consensus trades in global resources: electrification, grids, data centres, electric vehicles, and renewables all consume enormous quantities of copper, and the world is not discovering enough new large deposits to keep pace. If you believe in decarbonisation, you almost have to believe in copper demand.

Oyu Tolgoi: the underground giant

The centrepiece of that copper story is Оюу Толгой Oyu Tolgoi in the Mongolian Gobi Desert, one of the largest known copper-gold deposits on the planet. The open pit has operated for years, but the real prize is deep underground, where the highest-grade ore sits, and 2025 marked its ramp-up toward commercial high-grade production. Getting here required removing not just political friction (the debt write-off) but also shareholder friction. In December 2022, Rio Tinto paid roughly $3.3 billion to buy out the minority holders of Turquoise Hill Resources, the Toronto-listed vehicle through which it had historically held the asset.7 That deal gave Rio Tinto a clean, direct 66% interest in Oyu Tolgoi, with the Mongolian state holding the other 34%, and it eliminated years of awkward, value-leaking tension with minority investors. Simplicity, again, as a strategy. Combined with the long-established Kennecott mine in Utah and its stake in Escondida in Chile, the world's largest copper mine, Oyu Tolgoi anchors Rio Tinto's ambition to grow copper into a genuine second pillar.

The Arcadium gamble

Then there is lithium, and here Rio Tinto did something that would have been unthinkable in the risk-averse decade after Alcan. On 6 March 2025, it completed the all-cash acquisition of Arcadium Lithium for $6.7 billion, paying $5.85 per share.5 What makes this fascinating is not the size, it is the timing and the price.

Rio Tinto paid roughly a 90% premium over Arcadium's undisturbed share price. On its face, a 90% premium screams "overpayment", the very sin that destroyed value in 2007. But look at the context. Arcadium's stock had been crushed because lithium prices had collapsed, down more than 80% from their manic 2022 peak, as a wave of new supply overwhelmed a temporary lull in EV demand growth. Rio Tinto was paying a huge premium over a deeply depressed price, which is a very different thing from paying a huge premium over a euphoric one. Arcadium itself was the product of the 2023 merger of Allkem and Livent, a combination once valued at around $10.6 billion; Rio Tinto acquired the merged entity for a fraction of that. In cost-curve terms, it bought Tier-1 producing lithium assets, brine operations in Argentina at Salar del Hombre Muerto and Olaroz, plus hard-rock and processing assets across Australia and Canada, at well below what it would cost to build them new.

Buying time instead of building it

The deepest rationale is about time, not just price. Building a lithium business from scratch, "greenfield", means a decade of exploration, permitting, community negotiation, and construction, with no revenue and constant risk of being blocked. Rio Tinto knew this pain intimately: its own greenfield Jadar lithium project in Serbia had been frozen by fierce environmental protests and a government revocation of its permits, a stark reminder that social licence can kill a project before the first shovel. Arcadium let Rio Tinto skip that decade, acquiring operating mines, real cash flow, and, crucially, deep chemical-processing expertise, turning raw lithium into the battery-grade chemicals customers actually buy, which is the genuinely hard part of the business.

Here is where an independent voice has to stay honest. The counter-cyclical logic is genuinely smart, and it is exactly the "buy at the trough" discipline the outline rightly praises. But it is not yet vindicated. If lithium prices stay depressed for years, and there is real risk they will, given how much new supply exists, then $6.7 billion of cash is tied up in assets earning thin margins, and the deal looks dilutive and early. Rio Tinto is not betting that lithium is cheap today; it is betting that in the 2030s, EV and grid-storage demand will overwhelm supply and its low-cost brine assets will earn high returns. That thesis is plausible. It is also unproven, and the market will not settle the argument for several years. What is beyond dispute is that Rio Tinto has decisively chosen to reload on growth, a company that spent a decade apologising for one acquisition is now making very large ones again.

Nowhere is that renewed appetite for scale more visible than in a West African jungle that has haunted the mining industry for thirty years.

VIII. Simandou: Bringing the "World's Largest Megaproject" to Life

For a generation, Simandou was mining's greatest tease. Buried under the forested mountains of southeastern Guinea lies the world's largest untapped deposit of high-grade iron ore, more than two billion tonnes of it, at grades that make even the Pilbara look ordinary. And for three decades it sat there, untouched, because the ore was the easy part. Getting it out required a railway across an entire country to a coast that had no port, through a nation with a history of coups, contested mining licences, and one of the most notorious corruption sagas in the industry's memory. Simandou was less a mining project than a geopolitical Rubik's cube.

The Pilbara of West Africa

The prize justified the pain. Simandou's ore runs at roughly 65–66% iron with very low impurities, and that specific quality is what makes it, in management's framing, "strategic to the core" of the energy transition. Ordinary iron ore goes into a blast furnace with coking coal, a process that is one of the largest single sources of industrial carbon emissions on the planet. Ultra-high-grade ore like Simandou's can instead feed Direct Reduced Iron (DRI) and Electric Arc Furnace (EAF) steelmaking, routes that can slash steel's carbon footprint dramatically, by up to around 70% in some pathways, especially if powered by clean electricity and, eventually, green hydrogen. In a world where steelmakers face mounting pressure to decarbonise, premium low-impurity ore should command a "green steel" premium. That is the bull thesis, and it is genuinely differentiated. The independent caveat: DRI/EAF adoption at scale is still early and expensive, so the size and durability of that premium is a forecast, not yet a fact.

The infrastructure jigsaw

The masterstroke of the modern Simandou deal was that Rio Tinto refused to build it alone. Rather than shoulder a colossal, single-country infrastructure bill by itself, an approach that would have concentrated all the political and financial risk on Rio Tinto's balance sheet, it assembled a consortium. Through its SimFer joint venture, Rio Tinto partnered with the Guinean government, with the rival Winning Consortium Simandou (which holds the northern blocks 1 and 2), and, critically, with China's state-owned steel behemoth 中国宝武钢铁集团 China Baowu Steel Group. Together they built the shared spine the project always needed: a trans-Guinean heavy-haul railway of more than 600 kilometres and a new deep-water port at Morebaya on the Atlantic coast.[^8] Bringing Baowu, Rio Tinto's own customer, into the ownership of the infrastructure was the key that turned the lock. It aligned the largest steelmaker on Earth with the success of the mine and split a bill too big for any single player to want to carry.

First ore

After thirty years of false starts, Simandou delivered first ore production and initial rail shipments in December 2025, with the inaugural cargo leaving Guinea before year-end.1 The system is now beginning a roughly 30-month ramp-up toward the joint venture's full capacity of around 60 million tonnes per year. Of an estimated $11.6 billion total development cost for the mine and infrastructure, Rio Tinto's share of the capital for its blocks 3 and 4 was about $6.2 billion. That is real money, and the ramp will not be smooth, first production is a milestone, not a finish line, and West African megaprojects rarely hit their timelines cleanly. But Simandou fundamentally changes Rio Tinto's iron ore story. For the first time in the company's history, it has a genuine, world-class alternative source of premium ore outside the Pilbara, and a partial hedge against its terrifying single-basin concentration. Whether Guinea's politics let it run smoothly is the open question we will stress-test shortly.

IX. Playbook: Business & Investing Lessons

Step back from the individual dramas and four durable lessons emerge, the kind that outlive any single commodity cycle.

Lesson 1: Social licence is an economic asset, not a slogan

The single most expensive thing Rio Tinto ever destroyed was not Alcan's value or Mozambique's coal. It was trust. Juukan Gorge proved that a permit is not permission, and that poor community relations translate directly into stranded reserves, executive turnover, and a lasting discount on the stock. Trott's co-management framework with the PKKP is the operational answer: build the community's veto into the plan from the start, accept the constraint, and buy durability. For any resource company, the lesson generalises: the licence to operate is a balance-sheet asset that does not appear on the balance sheet, and it is far cheaper to maintain than to rebuild.

Lesson 2: Master counter-cyclical M&A, and know which cycle you're in

The Alcan and Arcadium deals are the same company's opposite instincts, and the contrast is the whole lesson. Alcan was bought big, at the euphoric top, with borrowed money, partly for defensive reasons, and it nearly broke the company. Arcadium was bought at a fraction of the size, at a depressed trough, with cash, for strategic reasons. The discipline is not "never do M&A"; it is "buy assets when the crowd is selling them, not when the crowd is bidding them up." The catch, and an honest playbook must include it, is that troughs are only obvious in hindsight. Arcadium will only prove to be a masterstroke if lithium eventually recovers. Counter-cyclical buying is a superior strategy and a real risk at the same time.

Lesson 3: Share the infrastructure burden with your customer

Simandou stayed frozen for thirty years partly because everyone assumed one owner had to build everything. Rio Tinto unlocked it by bringing rivals and its own biggest customer, Baowu, into the ownership of the shared railway and port. The principle is powerful and underused: when a project's infrastructure is too big and too risky for one balance sheet, turn your customers and even your competitors into co-investors, so their capital and their self-interest align with yours. It converts a standalone bet into a shared one.

Lesson 4: Defend the bottom-left of the cost curve above all else

Every other advantage in mining is fragile except one: being the lowest-cost producer. Brands don't matter in commodities. Patents barely exist. But cost position is close to permanent, because it is built from geology and decades of sunk infrastructure that rivals cannot quickly replicate. This is Porter's cost-leadership taken to its logical extreme. When prices crash, the high-cost producers cut and close; the low-cost producer endures and emerges with more market share. Everything Rio Tinto does, the automation, the scale, the Simandou grade, ultimately serves this one imperative: stay at the bottom-left, and you survive every winter.

X. Analysis: Risk Radar, Bull vs. Bear Case, and KPIs

Now for the part where we play both the bull and the short-seller, because a company this cyclical and this concentrated deserves a genuine stress test rather than a cheer.

The skeptical investor's opening question

Start with the activist's blunt challenge. Roughly 60% of Rio Tinto's profit still comes from one commodity sold to one country. If iron ore fell to, say, $60 a tonne on a structural decline in Chinese construction, the group's earnings, and with them the dividend that income investors prize, would compress meaningfully. Rio Tinto's low cost means it would stay profitable, but "profitable" and "able to sustain a 60% payout plus record growth capex" are different things. So the fair question is: is Rio Tinto building its copper and lithium second engine fast enough to matter before the iron ore engine cools? The honest answer in mid-2026 is "getting closer, but not there yet." Copper EBITDA more than doubled in 2025, but iron ore is still the overwhelming majority of profit. The diversification is real and accelerating; it is not yet decisive.

The current risk radar

Three risks are material and worth naming precisely. The first is Chinese property stagnation, the direct demand mechanism for iron ore; a multi-year structural decline in Chinese housing starts would hit Rio Tinto's core cash flow with little offset. The second is resource nationalism and geopolitics, most acutely at Simandou, where Guinea's history of political instability and military-led government means the smooth ramp-up, and the tariffs charged for using that shared railway, sit at the mercy of decisions in Conakry. A government that renegotiates rail tariffs or export terms can quietly transfer a large slice of Simandou's economics from Rio Tinto to the state. The third is decarbonisation capital intensity: cleaning up Rio Tinto's aluminium smelters and operations toward net zero is enormously capital-hungry. The company is partly cushioned by its low-carbon Canadian hydro-powered smelters, a genuine asset in a carbon-constrained world, but the transition still competes for capital with growth projects and dividends.

The bull case

The bull case is a clean compounding story. Simandou ramps successfully and its ultra-high-grade ore earns a widening green-steel premium as DRI/EAF steelmaking scales. Oyu Tolgoi reaches peak high-grade underground production, and copper becomes a true second pillar just as electrification demand tightens the global copper market. Arcadium's lithium assets, bought at the trough, throw off high returns as EV and storage demand recovers later this decade. In this world, Rio Tinto transforms from a China-and-iron-ore proxy into a diversified supplier of the metals the energy transition cannot do without, while defending the lowest-cost position in bulk iron ore. Through Helmer's lens, it stacks cornered resource, process power, and scale economies across not one commodity but three.

The bear case

The bear case is equally coherent, which is exactly why this is interesting. China's property market enters a genuine multi-decade contraction, and iron ore demand never recovers to prior highs; the Pilbara stays profitable but the eye-watering margins fade. Guinea's government, seeing Simandou finally producing, renegotiates rail tariffs and export terms, capturing much of the upside the green premium was supposed to deliver. Lithium prices stay depressed through the decade, leaving the $6.7 billion Arcadium outlay looking early and dilutive. And the record capex required to build all this collides with the promise of capital discipline, forcing an uncomfortable choice between the growth pipeline and the dividend. In this world, Rio Tinto spends the decade running hard just to stand still.

Competitive frame

Against its peers, Rio Tinto sits in a specific spot. Versus BHP, the larger diversified rival, it is more concentrated in iron ore and has moved harder and earlier into lithium; BHP notably walked away from big lithium M&A and doubled down on copper and potash. Versus Brazil's Vale, Rio Tinto's Pilbara has historically offered more reliable, lower-cost supply, though Simandou now pits Rio Tinto's own new Guinean ore against Vale's high-grade Brazilian material for the premium, low-carbon steel market. Versus Fortescue, a pure-play Pilbara iron ore producer, Rio Tinto has vastly more diversification and a lower cost base. Porter's five forces are, on balance, favourable for the incumbents: the barriers to entry in bulk iron ore are close to insurmountable (you cannot build a new Pilbara), buyer power is concentrated but so is supply, and substitution risk, scrap-based steel recycling, is real but long-dated. The rivalry that matters is not for today's tonnes; it is for tomorrow's green-steel premium, and Simandou is Rio Tinto's entry ticket.

The three KPIs that matter most

An investor tracking this company through the cycle should watch three numbers above all others. First, Pilbara FOB unit cash cost, the single clearest gauge of whether the cost-curve moat is intact; management targets keeping it below roughly $24 a tonne, and any sustained drift upward would signal erosion of the core advantage.1 Second, copper-equivalent volume growth, the truest measure of whether the second engine is actually being built, and whether the dependence on iron ore is genuinely shrinking. Third, the combination of free cash flow and net debt to EBITDA, which together determine whether Rio Tinto can fund its growth pipeline and sustain its 40–60% dividend without stretching the balance sheet; net debt already climbed to $14.4 billion in 2025 as capex rose, so this is the dial where discipline and ambition visibly collide.1 Watch those three, and you will know how this story is actually unfolding long before the headlines do.

XI. Outro & Epilogue

The arc of Rio Tinto is, in the end, a 150-year meditation on scale and its discontents. It began on a poisoned red river in Andalusia with a bet that capital and engineering could resurrect an ancient asset, and it arrives, a century and a half later, at a jungle railway in Guinea and a brine pond in Argentina, making very much the same bet. Along the way it became one of the great cash machines in industrial history, and repeatedly proved that a company generating that much cash is perfectly capable of setting fire to it, at the top of the market in Canada, in the barge lanes of the Zambezi, and, most painfully, in a 46,000-year-old gorge that no write-down could ever restore.

What has changed is the company's relationship with the ground it stands on. The old Rio Tinto treated the land as an input and the community as an obstacle. The Juukan Gorge disaster forced a reckoning that produced, under Stausholm's diplomacy and now Trott's operating hand, a company that has learned, at brutal cost, that its cheapest reserves are worthless without permission to mine them, and that its next great orebody is only unlocked when it turns governments and even competitors into partners. Whether that lesson holds under the pressure of the next downturn, when the temptation to cut corners for a few dollars a tonne returns, is the test that lies ahead.

The insider now runs the show, the balance sheet is carrying more debt and more ambition than it has in years, and the whole edifice still rests, for now, on the price of one red rock shipped to one country. Rio Tinto's survival for 150 years is proof that it knows how to manage scale and geographic risk better than almost anyone. The next decade will reveal whether it has finally learned to manage itself.

References

-

Rio Tinto 2025 Full Year Results (Form 6-K) — Rio Tinto / SEC, 2026-02-18 ↩↩↩↩↩↩↩↩↩↩

-

Tom Albanese steps down as Rio Tinto CEO after $14bn Alcan and Mozambique write-downs — Financial Times, 2013-01-17 ↩↩

-

Rio Tinto to write off $2.4B Mongolian debt to restart Oyu Tolgoi expansion — Mining.com, 2021-12-14 ↩

-

Rio Tinto Completes Acquisition of Arcadium Lithium — Business Wire, 2025-03-06 ↩↩

-

Rio Tinto appoints Simon Trott as Chief Executive — Rio Tinto, 2025-07-15 ↩↩

-

Rio Tinto to pay $3.3 billion for full Turquoise Hill ownership — Mining.com, 2022-09-05 ↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube