RELX: The Information Alchemy — From Print to AI Powerhouse

I. Introduction — The Most Successful Company You've Never Heard Of (0:00 – 0:10)

Open a bank account in the United States, and an invisible system instantly checks whether you are who you claim to be. Apply for car insurance, and a database silently retrieves every claim ever filed against your vehicle identification number. A doctor in Singapore looks up the latest treatment protocol for a rare lymphoma, and the clinical decision tool she uses draws from a corpus of thirty million peer-reviewed research papers. A first-year associate at a London law firm types a natural-language question into a search bar and receives a synthesised answer drawn from two hundred years of case law, ranked by relevance and predicted judicial outcome.

In each of these moments, the same company is at work. Its name is RELX.

Most investors—even sophisticated ones—have only a vague awareness of RELX. It is not a household name. It does not make consumer products. It does not advertise on television. Its CEO has given perhaps a dozen interviews in sixteen years. And yet, by almost any measure of sustained corporate performance, RELX is one of the most successful companies in Europe.

The numbers tell the story with unusual clarity. Revenue reached GBP 9.59 billion in 2025. Adjusted operating margins stood at 34.8 percent—higher than most software companies. Free cash flow conversion ran at 99 percent, meaning virtually every pound of reported profit turned into actual cash. The company has delivered more than three decades of consistent revenue growth, raised its dividend every year for over two decades, and returned GBP 1.5 billion to shareholders through buybacks in 2025 alone—with GBP 2.25 billion planned for 2026.

The enterprise value sits at roughly GBP 63 billion. Return on invested capital has consistently exceeded 15 percent—a level that indicates a business generating far more value than the capital it consumes.

How did a company that started life printing newspapers on Victorian-era presses become a data analytics powerhouse that some analysts now compare to Verisk, MSCI, and even the enterprise software giants? The answer is a thirty-year story of ruthless portfolio transformation—shedding every business that touched physical paper and replacing it with digital platforms that sit at the nexus of the world's most critical decisions: who to insure, who to hire, who to prosecute, what to prescribe, and what to publish.

The transformation was not glamorous. It involved selling off beloved magazine brands, enduring a decade of criticism from the academic community, and making a single USD 4.1 billion acquisition in 2008 that, at the time, was called reckless overpayment—and in hindsight turned out to be one of the most important deals in European corporate history.

This is the story of how a boring company became a brilliant one—and why, even after a sharp share price drawdown in early 2026 (falling from a fifty-two-week high of 4,183 pence to roughly 2,465 pence), the underlying business machine continues to accelerate.

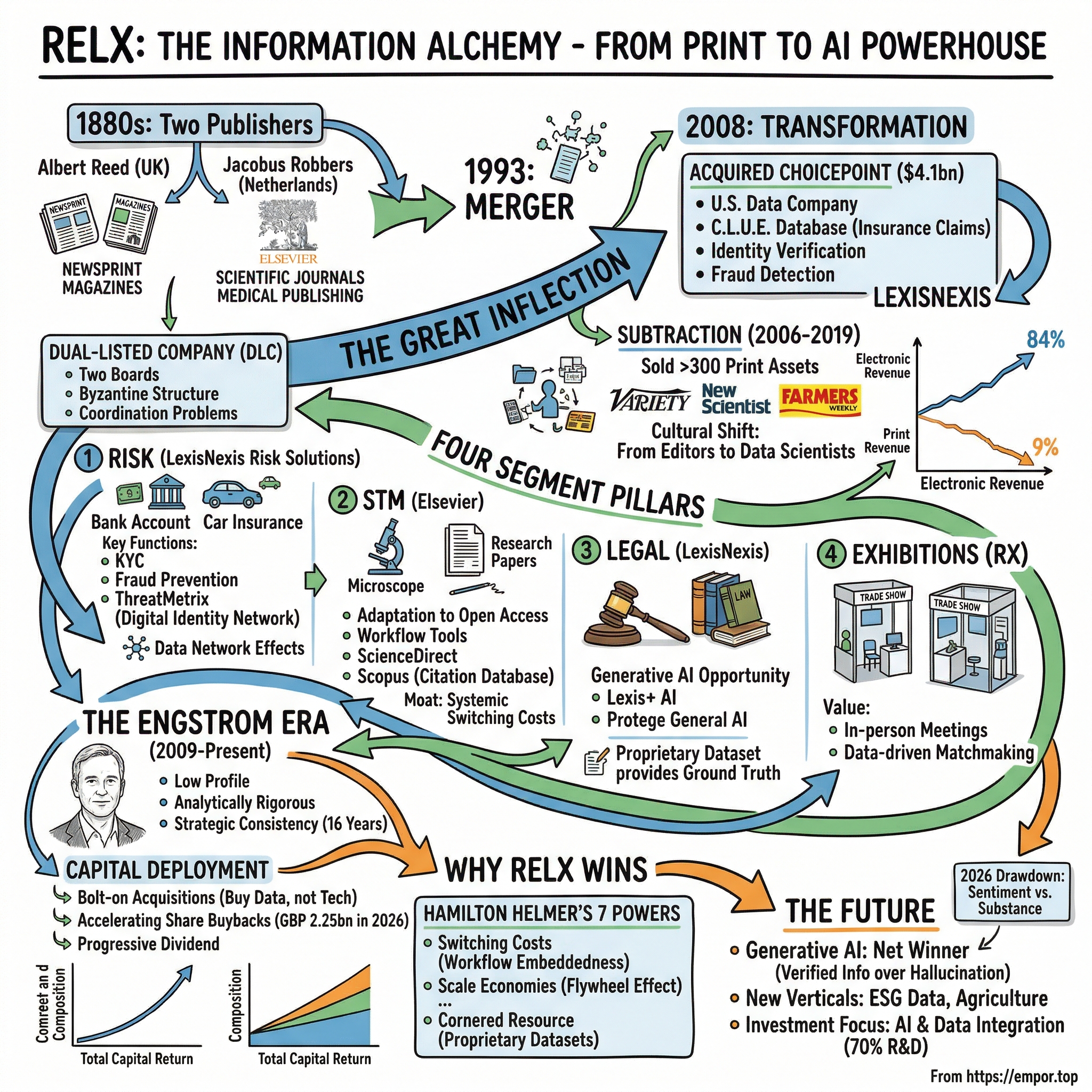

II. The Origins — A Tale of Two Publishers (0:10 – 0:25)

In 1894, in the industrial heartland of Victorian England, Albert Edwin Reed founded a newsprint manufacturing business. Reed's company grew methodically—first into paper production, then into magazine and book publishing—eventually becoming Reed International, one of Britain's largest publishing conglomerates. By the mid-twentieth century, Reed International owned trade magazines, consumer publications, and a vast paper-manufacturing operation. It was the kind of sprawling, diversified British industrial group that made sense in an era when "conglomerate" was not yet a dirty word.

Fourteen years earlier, in 1880, a Dutchman named Jacobus George Robbers had founded a publishing house in the Netherlands. He named it Elsevier—an homage to the historic Elzevir printing family, which had published Erasmus's works in the late sixteenth century. Robbers began with literary classics and the Winkler Prins encyclopedia. Over the following century, Elsevier pivoted decisively toward scientific and medical publishing, building what would become the world's largest portfolio of peer-reviewed academic journals.

By the early 1990s, both companies faced the same existential question: scale. The publishing industry was consolidating globally, and neither Reed International nor Elsevier had the heft to compete against emerging American media conglomerates. The solution was a merger—but not an ordinary one.

On January 1, 1993, Reed International and Elsevier combined their operations into a dual-listed company structure. Both parent entities—Reed International plc in London and Elsevier NV in Amsterdam—continued to exist as separately listed companies, each holding equalised economic interests in jointly owned operating businesses. The structure was Byzantine. Dual-listed companies are notoriously difficult to govern: two boards, two sets of shareholders, two regulatory regimes, and an endless stream of coordination problems.

Most dual-listed structures end in tears. BHP Billiton eventually unified. Unilever eventually unified. Shell eventually unified. The problem is fundamental: two sets of shareholders with potentially divergent interests, two boards that must agree on every strategic decision, and the constant overhead of maintaining parallel governance structures across different legal jurisdictions.

Reed Elsevier, against the odds, survived its dual-listed period for more than two decades before finally simplifying into a single entity in 2015 and rebranding as RELX—a name derived, with somewhat awkward creativity, from the first letters of its four divisions: Risk, Elsevier, and LexisNexis. Management described the naming process as "sort of playing Scrabble" with the division names. The result was a brand that nobody could pronounce correctly but that signalled a clean break from the publishing past.

The unification mattered for more than symbolic reasons. A single corporate structure meant simpler governance, more efficient capital allocation, and the ability to execute share buybacks without navigating the complexities of dual-listed share registries. It also made RELX easier for institutional investors to own—no more confusion about whether to buy the London-listed or Amsterdam-listed shares.

But in the 1990s and early 2000s, the merged company was still fundamentally a publisher. It owned trade magazines, academic journals, legal reference books, and business directories. Revenue came from subscriptions, advertising, and the physical sale of printed material. The business model was centuries old: acquire content, print it, distribute it, charge for access.

The internet threatened to destroy that model entirely.

The existential question arrived in the mid-1990s, when the World Wide Web began to make information freely accessible. If scientific papers could be shared online for free, why would a university pay Elsevier thousands of dollars for a journal subscription? If legal cases could be searched on government websites, why would a law firm pay for LexisNexis? If trade show information could be found on industry blogs, why would anyone attend a Reed Exhibitions event?

The company's response to this threat—slow at first, then accelerating through the 2000s—would define everything that followed. The critical insight, articulated most clearly by Erik Engstrom after he became CEO in 2009, was deceptively simple: RELX was not in the business of paper. It was not even in the business of content. It was in the business of information—and information, when structured, analysed, and embedded into customer workflows, becomes exponentially more valuable than the raw content from which it is derived.

A law firm does not want a book of cases. It wants to know which cases are relevant to the argument it is making, ranked by persuasiveness, with predicted judicial outcomes. A doctor does not want a journal article. She wants a clinical decision pathway that integrates the latest evidence with the patient's specific condition. An insurance underwriter does not want a database of claims. He wants a risk score—a single number that predicts the probability of a future loss.

The transition from "content provider" to "decision tool provider" is the central arc of the RELX story.

There is a useful analogy here. Think of Google Maps. The raw data—street addresses, coordinates, road networks—is essentially the same information that was always available in printed maps and atlases. But Google Maps is not a map. It is a real-time navigation and decision tool that tells you where to go, how long it will take, which route avoids traffic, and where to find the nearest petrol station. The value is not in the data itself. It is in the structuring, analysis, and contextualisation of the data into actionable intelligence.

RELX made the same conceptual leap—across legal research, scientific discovery, insurance underwriting, and identity verification simultaneously. And it began in earnest with a crisis.

III. The Great Inflection — The 2008 Transformation (0:25 – 0:55)

In the autumn of 2008, as Lehman Brothers collapsed and global credit markets froze, Reed Elsevier completed the acquisition that would reshape its identity for the next two decades.

The target was ChoicePoint Inc.—a US-based data company headquartered in Alpharetta, Georgia, that most people had never heard of. ChoicePoint's business was unglamorous but essential: it collected, structured, and sold data used by insurance companies to underwrite risk. Its flagship product was the C.L.U.E. database—Comprehensive Loss Underwriting Exchange—a proprietary repository of every auto and property insurance claim filed in the United States.

When you apply for car insurance in America and the insurer instantly knows about the fender-bender you had three years ago in a different state, that is ChoicePoint's data at work. When an employer runs a background check before hiring you, ChoicePoint was often the engine behind the screen. The company also provided identity verification, fraud detection, and drug testing administration services.

Reed Elsevier paid USD 4.1 billion in cash—comprising roughly USD 3.5 billion in equity value and USD 600 million in assumed net debt. At the time, the price represented approximately 15 times EBITDA. Critics were savage. The deal closed on September 19, 2008—five days after Lehman filed for bankruptcy. The financial press called it reckless. Analysts questioned whether a European publisher had any business buying an American data company at a premium multiple during a financial crisis.

The first-year post-tax return on the acquisition was 6 percent—respectable but hardly transformational. But the real value was not in the first-year returns. It was in what ChoicePoint became once integrated into the LexisNexis infrastructure.

ChoicePoint's datasets—insurance claims, criminal records, employment histories, property records—were combined with LexisNexis's existing legal and public records databases to create something genuinely new: a comprehensive risk analytics platform that could verify identity, predict fraud, assess insurance risk, and support regulatory compliance—all from a single integrated data ecosystem.

The acquisition moved RELX from "providing information" to "predicting risk." That distinction—between looking backward at what happened and looking forward at what might happen—is the difference between a publishing company and a technology company. And it is worth tens of billions of pounds in enterprise value.

To appreciate why this shift matters so much, consider how the insurance industry operated before ChoicePoint. An underwriter pricing a homeowner's policy would rely on the applicant's self-reported claims history, a credit score, and perhaps a phone call to the applicant's prior insurer. The process was slow, manual, and dependent on the honesty of the applicant. ChoicePoint's C.L.U.E. database replaced this entire process with a single electronic query that returned a comprehensive claims history—verified against insurer records, not self-reported—in seconds.

The productivity gain was enormous. What once took hours of phone calls and paperwork now took milliseconds. And the accuracy was dramatically higher, because insurers were no longer relying on applicants to truthfully disclose prior claims. The database knew. It was like replacing a hand-drawn map with GPS—the same destination, but a fundamentally different level of precision, speed, and reliability.

The implications for RELX's business model were equally transformative. A print publisher sells content once. A data analytics platform sells decisions continuously. Every time an insurer underwrites a policy, RELX collects a transaction fee. Every time a bank verifies an identity, RELX collects a transaction fee. The revenue model shifted from one-time content sales to recurring, usage-based revenue—a shift that mirrors the software industry's transition from perpetual licences to SaaS subscriptions. The result was predictable, recurring revenue with operating leverage that improved with every additional transaction.

But the ChoicePoint deal was only half of the 2008 transformation. The other half was subtraction.

Between 2006 and 2019, RELX executed approximately 65 separate asset disposals, selling roughly 300 print and advertising-dependent publications. Trade magazines that had been the company's bread and butter for decades—titles covering restaurants, hotels, broadcasting, and multichannel media—were sold or, in some cases, simply shuttered when no buyer could be found.

Variety, the legendary Hollywood trade publication, was sold to Penske Media in 2012. New Scientist went in 2017. Farmers Weekly, one of Britain's oldest agricultural titles, was sold to the Mark Allen Group in December 2019. Each sale was modest individually. Collectively, they represented a fundamental remaking of the company's identity.

The numbers tell the story. In 2006, print-derived revenue represented roughly 51 percent of RELX's total. By 2019, it had fallen to 9 percent. Today, approximately 84 percent of revenue is electronic and digital.

The cultural transformation was equally dramatic. In the old Reed Elsevier, the most powerful people in the organisation were editors—journalists and subject-matter experts who curated content and decided what to publish. In the new RELX, the most powerful people are data scientists and product managers who build algorithms, design workflow tools, and optimise user engagement metrics.

The transition from "editor-in-chief dominance" to "data scientist dominance" was not smooth. Legacy employees who had spent careers in print journalism found themselves reporting to technologists who had never written an article. But the direction was clear, and the CEO who drove it—Erik Engstrom, appointed in late 2009—was unapologetic about the transformation.

The 2008 crisis, in hindsight, was the best thing that ever happened to RELX. It forced decisions that might otherwise have been deferred for years. It created the conditions for the ChoicePoint acquisition—which might not have been possible at a reasonable price in a healthier market. And it established the strategic template that would guide the company for the next fifteen years: buy data, sell decisions.

The cultural dimension of this transformation deserves emphasis, because it is where most corporate pivots fail. Changing a company's product portfolio is relatively straightforward—you sell divisions and buy new ones. Changing a company's culture is exponentially harder.

In the old Reed Elsevier, career progression was editorial. You started as a junior editor, rose to managing editor, became editor-in-chief, and eventually ran a publishing division. The skills that mattered were editorial judgment, industry expertise, and relationship management with authors and advertisers. Success was measured in pages published, awards won, and advertising pages sold.

In the new RELX, career progression is technical. You start as a data analyst, learn to build predictive models, become a product manager overseeing a data platform, and eventually run a technology-driven business unit. The skills that matter are statistical modelling, software engineering, user experience design, and algorithmic optimisation. Success is measured in subscription revenue, customer retention rates, and the accuracy of predictive outputs.

The shift required not just new hires but new leadership at every level. Editorial veterans who had built their careers around content curation found themselves reporting to technologists whose understanding of the publishing industry was minimal but whose understanding of data architecture was deep. Some adapted. Many left. The transition was painful—but it was also the necessary precondition for everything that followed.

IV. Segment Deep Dive — The Four Pillars (0:55 – 1:25)

Risk — The Crown Jewel

If you were to strip RELX down to a single business and value it independently, the Risk segment—formally LexisNexis Risk Solutions—would likely command the largest share of the enterprise value.

Risk generated GBP 3.49 billion in revenue in 2025, growing at 8 percent on an underlying basis, with adjusted operating profit of GBP 1.31 billion—a margin of approximately 37 percent. It is the largest segment by revenue and by profit.

What does LexisNexis Risk Solutions actually do? The simplest way to understand it is this: it is the invisible verification layer behind most of the important financial decisions made in the United States and increasingly in the United Kingdom and beyond.

When you open a bank account, the bank needs to verify that you are who you claim to be—and that you are not on a sanctions list, a fraud watchlist, or a money-laundering risk database. That is KYC—Know Your Customer—and RELX's tools perform millions of these checks daily. When you apply for a mortgage, the lender checks your identity, your property history, and your insurance claims record. When an insurer prices your auto policy, it queries the C.L.U.E. database to see every claim associated with you and your vehicle. When an e-commerce platform processes your online purchase, RELX's ThreatMetrix system evaluates whether the transaction is legitimate or fraudulent—in real time, within milliseconds.

Think about what happens when an insurer joins the C.L.U.E. network. The insurer contributes its claims data—every fender-bender, every house fire, every liability claim. That data immediately improves the risk models used by every other insurer in the network. The new insurer benefits from access to a dataset far larger than anything it could build alone. The existing insurers benefit from the addition of the new insurer's data to the shared pool.

This is the definition of a data network effect—and it is extraordinarily difficult for competitors to replicate, because the dataset itself is the product. A startup entering the insurance analytics market cannot offer a comparable database because it has no historical claims data. It cannot acquire historical claims data because insurers will not share it with an unproven platform. And it cannot prove itself without the data. The chicken-and-egg problem is insurmountable.

The same dynamic applies in fraud detection. When a bank processes an online transaction through ThreatMetrix, the system compares the transaction's digital fingerprint—device type, IP address, behavioural patterns, location data—against a global database of billions of previous transactions. If the fingerprint matches a pattern associated with known fraud, the transaction is flagged. The more transactions the system processes, the more fraud patterns it learns, and the more accurate it becomes.

This is why the Risk segment has grown consistently at 7 to 10 percent per year for over a decade: the product literally gets better with every customer, every transaction, and every fraud attempt. It is a flywheel that accelerates as it scales.

The ThreatMetrix acquisition in 2018 was the second critical bet in the Risk segment's evolution. RELX paid approximately GBP 580 million—roughly USD 817 million—for a company that had built the world's largest digital identity network. ThreatMetrix processes billions of online transactions annually, building a probabilistic identity graph that can distinguish a legitimate customer from a fraudster based on device fingerprints, behavioural biometrics, and network analysis. The Emailage acquisition in 2020, at roughly USD 480 million, added email-based fraud scoring to the same platform.

Combined, these acquisitions gave RELX a position in digital identity verification that is nearly impossible to dislodge. The switching costs are enormous—a bank that has integrated RELX's fraud detection into its transaction processing infrastructure cannot simply rip it out and replace it with a competitor's product without months of integration work, regulatory re-approval, and operational risk.

The growth trajectory of the Risk segment tells the story. Revenue grew from roughly GBP 2 billion in 2018 to GBP 3.49 billion in 2025—a near-doubling in seven years, driven by the expansion of fraud detection, financial crime compliance, and identity verification services. The segment now accounts for more than a third of RELX's total revenue and an even larger share of its profit growth. When analysts call Risk the "crown jewel," they are not exaggerating. It is the engine that drives the entire company's growth rate.

STM — The Elsevier Engine

The Scientific, Technical & Medical segment—essentially Elsevier—generated GBP 2.71 billion in revenue in 2025, growing at 5 percent, with an adjusted operating margin of approximately 38 percent.

These margins have made Elsevier a target of sustained criticism from the academic community. The business model, at its core, involves receiving research papers for free from scientists (who are typically funded by taxpayers), coordinating peer review for free (reviewers are unpaid volunteers), and then selling access to the published papers back to the universities that employed the scientists—at prices that have risen faster than inflation for decades.

The "Cost of Knowledge" boycott, initiated in January 2012 by Cambridge mathematician Timothy Gowers, attracted over 20,000 signatories pledging not to publish in, review for, or serve on editorial boards of Elsevier journals. The University of California system cancelled its Elsevier subscriptions entirely in 2019. MIT followed in 2020. German universities entered a prolonged standoff that lasted years.

The "Elsevier is dying" narrative became conventional wisdom.

The narrative was wrong.

What actually happened was more nuanced. Elsevier adapted—not gracefully, and not without friction, but effectively. The company embraced Open Access publishing, where authors (or their funders) pay article processing charges to make papers freely available. By 2024, Elsevier was publishing over 120,000 Open Access articles annually, with the Open Access share exceeding 30 percent of new articles in many regions. Transformative agreements—institutional deals that bundle subscription access with Open Access publishing rights—were signed with over 2,000 institutions globally.

More importantly, Elsevier evolved beyond journals. The real growth engine in STM is no longer the journal subscription. It is the suite of workflow and analytics tools built on top of the content: ScienceDirect for research access, Scopus for citation analysis and research benchmarking, SciVal for institutional research performance assessment, ClinicalKey for clinical decision support, and Embase for biomedical literature search.

A university that cancels its Elsevier journal subscriptions can find alternative access to individual papers through interlibrary loan or preprint servers. But a university that disconnects from Scopus loses the ability to benchmark its research output against peer institutions—a capability that drives funding allocation, tenure decisions, and strategic planning. The switching cost on the analytics layer is far higher than on the content layer. That is the moat Elsevier has been quietly building for a decade.

There is a deeper point here about the nature of academic publishing that the "Elsevier is evil" narrative misses. The value of a scientific journal is not in the individual papers. It is in the curation—the peer-review process that validates which papers meet the quality threshold for publication—and in the citation network that connects papers to each other, creating a structured map of human scientific knowledge.

Scopus, Elsevier's citation database, contains the citation relationships between over 90 million documents. That network is not just a reference tool. It is the infrastructure on which university research offices, national funding bodies, and global ranking systems (like QS and Times Higher Education) depend to evaluate research quality. When a government decides how to allocate research funding across universities, it typically uses bibliometric data derived from Scopus or its competitors. The switching cost is not just institutional—it is systemic.

Legal — LexisNexis

The Legal segment generated GBP 1.81 billion in revenue in 2025, growing at 9 percent, with adjusted operating profit of GBP 415 million—a margin of roughly 23 percent and the fastest profit growth of any segment at 12 percent.

LexisNexis Legal has been in a decades-long battle with Thomson Reuters' Westlaw for dominance in legal research. For most of that period, Westlaw held the edge—particularly in the United States, where its editorial enhancements (headnotes, key numbers) were considered superior. LexisNexis competed on breadth—more documents, more jurisdictions—but Westlaw competed on quality.

Generative AI has scrambled that dynamic entirely—and may have given LexisNexis its best opportunity in decades to close the gap with Westlaw.

The reason is structural. In the pre-AI era, the value of a legal research platform lay in editorial curation—the headnotes, key numbers, and topical classifications that helped lawyers navigate millions of documents. Westlaw invested more in these editorial enhancements and was generally considered the higher-quality product. But in the AI era, the value lies in the underlying data itself—the raw corpus of case law, statutes, regulations, and secondary sources that large language models use to generate answers. Both LexisNexis and Westlaw have comprehensive corpora. The playing field, for the first time in decades, is more level.

In 2023 and 2024, LexisNexis launched Lexis+ AI—a conversational legal research tool that allows lawyers to ask natural-language questions and receive synthesised, citation-backed answers drawn from the full LexisNexis corpus. Instead of manually constructing Boolean search queries—a skill that took law students years to master—a lawyer can now type a question in plain English and receive a structured analysis with embedded citations that link directly to the underlying source documents.

The productivity implications are profound. A task that previously required a first-year associate four hours of research can now be completed in minutes. The value proposition shifts from "access to documents" to "time savings"—and time, for law firms billing at hundreds of dollars per hour, is the most valuable commodity of all.

By mid-2024, the product had rolled out across the US, UK, Australia, France, and Canada.

In August 2025, LexisNexis went further with Protege General AI—an agentic AI platform offering advanced reasoning and deep research capabilities. The platform lets users choose between multiple underlying AI models, including Anthropic's Claude and OpenAI's GPT, and can perform multi-step legal research tasks autonomously.

The significance of these products extends beyond revenue contribution. They represent a strategic bet that the value of legal research will shift from "access to documents" to "synthesised legal intelligence"—and that the company with the deepest proprietary dataset will produce the most accurate AI-generated answers.

To understand why data quality matters so much in legal AI, consider the consequences of getting it wrong. When a New York attorney used ChatGPT to draft a legal brief in 2023, the AI fabricated multiple case citations—cases that did not exist, with made-up docket numbers and fictional judicial opinions. The attorney was sanctioned by the court. The incident became a cautionary tale that spread through the legal profession like wildfire.

RELX's legal corpus, spanning centuries of case law across dozens of jurisdictions, is precisely the kind of "ground truth" data that large language models need to produce reliable outputs. When Lexis+ AI generates a legal research summary, every citation can be verified against the actual case in the LexisNexis database. The AI does not hallucinate because it is not generating from general knowledge—it is retrieving from a verified proprietary corpus.

A competitor could build a comparable AI interface. It could not replicate the underlying data. Thomson Reuters' Westlaw is the only platform with a comparably comprehensive legal dataset, which is why the legal AI race is essentially a two-horse contest. Everyone else is competing for third place in a market where third place may not be viable.

Exhibitions — RX

The Exhibitions segment—branded as RX—is the outlier in the portfolio. It generated GBP 1.19 billion in revenue in 2025, with 8 percent underlying growth and an adjusted operating margin of roughly 35 percent.

RX operates 286 face-to-face events across 25 countries—trade shows like MIPIM in real estate, World Travel Market in tourism, and dozens of industry-specific exhibitions in sectors ranging from electronics to jewellery.

COVID-19 nearly killed this business. Revenue collapsed to near zero in 2020 and 2021. The recovery has been stronger than most analysts expected, driven in part by the paradox that the more business moves online, the more valuable in-person meetings become. In a world where every interaction can be digital, the scarcity of face-to-face connection creates its own premium.

There is also a data angle. Every exhibition generates vast amounts of attendee data—who visited which booth, which sessions they attended, what products they showed interest in. This data, properly structured, becomes a lead generation tool for exhibitors. RX is increasingly positioning itself not as a trade show operator but as a data-driven matchmaking platform that happens to use physical events as its primary interface.

The strategic rationale for keeping Exhibitions—despite its obvious vulnerability to pandemics and its lack of digital purity—is twofold. First, the margins are excellent: 35 percent adjusted operating margins on a capital-light business model. RX does not own the exhibition venues. It does not build the booths. It organises the events, sells the space, and collects the data. Second, exhibitions generate recurring revenue—most major trade shows operate annually, and exhibitors book year after year because the leads they generate justify the cost.

Whether this rationale is sufficient to justify the strategic distraction of maintaining a physical events business inside a digital analytics company is a legitimate question. But the financial contribution—GBP 410 million in operating profit—buys a lot of forgiveness for strategic impurity.

Across all four segments, one pattern is consistent: the transition from selling content to selling workflow tools. In Risk, the product is not a database—it is an automated decision engine embedded in the customer's transaction processing. In STM, the product is not a journal—it is a research analytics platform embedded in the university's strategic planning process. In Legal, the product is not a case law library—it is an AI-powered research assistant embedded in the lawyer's daily workflow. In Exhibitions, the product is evolving from a trade show booth to a data-driven matchmaking platform embedded in the exhibitor's lead generation process.

The common thread is embeddedness. The deeper the product sits inside the customer's workflow, the more indispensable it becomes, the higher the switching cost, and the more predictable the revenue stream. This is the strategic architecture that Engstrom has built over sixteen years—and it explains why RELX's adjusted operating margin has expanded from the mid-twenties to nearly 35 percent over his tenure. Workflow tools command higher prices, generate better retention, and cost less to deliver at scale than raw content.

V. Current Management — The Engstrom Era (1:25 – 1:45)

Erik Engstrom is perhaps the least famous CEO of any major European company. He has run RELX since November 2009—sixteen years and counting—and in that time has given a handful of interviews, made no public pronouncements about politics or social issues, and maintained a profile so low that many investors who own RELX shares could not identify him in a photograph.

This is deliberate.

Engstrom, born in 1963, is Swedish. He holds a bachelor's degree from the Stockholm School of Economics, a master's from the Royal Institute of Technology in Stockholm, and an MBA from Harvard Business School, which he attended as a Fulbright Scholar. He started his career at McKinsey & Company, then moved into publishing as President and CEO of Bantam Doubleday Dell in North America, followed by a stint as President and COO of Random House Inc. In 2001, he joined General Atlantic Partners, the private equity firm, before being recruited to run Elsevier in 2004.

Five years later, he was elevated to CEO of the entire RELX group. The appointment was not flashy. There was no press tour, no transformation manifesto, no "100-day plan" leaked to the Financial Times. Engstrom simply began executing: selling print assets, acquiring data companies, investing in technology platforms, and methodically shifting the company's identity from publisher to analytics provider.

His management style has been described internally as "McKinsey meets private equity"—analytically rigorous, operationally focused, and relentlessly oriented toward capital efficiency. There are no vanity projects at RELX. There are no empire-building acquisitions. There are no corporate rebranding exercises, no expensive sponsorship deals, no flashy headquarters relocations.

There is a clear strategic framework—migrate from content to analytics, invest in organic growth, supplement with bolt-on acquisitions, return excess capital to shareholders—and the discipline to execute it year after year without deviation. The consistency is almost eerie. Read RELX's annual report from 2012, then read the one from 2025: the strategic language is virtually identical. The execution has simply compounded.

This consistency matters because corporate transformations usually fail precisely where RELX has succeeded: at sustaining focus over long periods. Most CEOs arrive with a transformation agenda, execute for three to five years, and then depart—leaving their successor to either continue the programme (unlikely) or start a new one (common). Engstrom has had sixteen years to execute a single, coherent strategy. The compounding effect of that consistency—in customer relationships, in technology investment, in data accumulation, in cultural alignment—is almost impossible to replicate in a company that changes direction every time it changes leadership.

The incentive structure reinforces this discipline. RELX's long-term incentive plans are tied to total shareholder return relative to peer groups measured in sterling, euros, and US dollars—a multi-currency approach that reflects the company's global investor base. The remaining components are linked to underlying business performance metrics including earnings per share growth and return on invested capital. Total compensation for Engstrom was approximately GBP 13.5 million in 2024—modest by the standards of companies generating comparable free cash flow, though reports indicated that RELX planned to increase his pay to align more closely with FTSE 100 peer CEO levels.

Nick Luff, the CFO since 2014, is a complementary figure. An Oxford mathematics graduate who qualified as a chartered accountant at KPMG, Luff built his career at P&O and then Centrica, where he served as Group Finance Director. At RELX, he has overseen a capital allocation programme that has become something of a masterclass in the European corporate landscape.

The pattern is consistent: generate approximately GBP 3.3 billion in adjusted cash flow (2025), allocate roughly 50 percent to dividends (GBP 67.5 pence per share, growing at approximately 7 percent per annum), deploy GBP 100 to 400 million annually on bolt-on acquisitions, and return the remainder through share buybacks (GBP 1.5 billion in 2025, GBP 2.25 billion planned for 2026). Net debt has remained stable at approximately 2.0 times EBITDA—high enough to provide tax-efficient leverage, low enough to maintain investment-grade ratings and financial flexibility.

The institutional shareholder base—dominated by BlackRock, Vanguard, and the large global asset managers—provides stability without interference. There is no activist agitating for a breakup. There is no family shareholder demanding special treatment. The company is managed with the discipline of a private equity portfolio company, but with the long-term horizon of a public compounder.

The result is a company that does not generate headlines but does generate returns. Under Engstrom's tenure, RELX's share price has compounded at rates that place it among the best-performing European equities of the past decade—delivering roughly 76 percent total return over ten years even after the significant 2026 drawdown.

One detail about Engstrom's background deserves particular attention: his stint at General Atlantic, the private equity firm, from 2001 to 2004. Private equity teaches a specific set of disciplines—ruthless focus on cash generation, intolerance for underperforming divisions, and an obsessive focus on return on invested capital rather than top-line revenue growth. These habits are visible in every aspect of RELX's current management approach: the relentless disposal of sub-scale businesses, the refusal to make dilutive acquisitions, and the systematic use of excess cash flow for buybacks rather than empire-building.

Paul Walker has served as Chairman since 2021, overseeing a board of ten members that includes four women and meets the standards of the UK Corporate Governance Code. Andy Halford joined as a non-executive director in April 2025. The board's composition reflects the company's global profile—but the strategic direction continues to flow from Engstrom's office with a consistency that borders on monotony.

In an industry where CEO tenure averages roughly five years, Engstrom's sixteen-year tenure is remarkable. It has provided the strategic continuity that made the transformation from publisher to analytics company possible—a transformation that requires patience, discipline, and the willingness to absorb short-term criticism in pursuit of long-term compounding.

VI. M&A and Capital Deployment (1:45 – 2:10)

RELX's acquisition strategy is the inverse of what most large European companies do. Where others pursue transformational mega-deals—often at premium multiples, often destroying value—RELX executes dozens of small, targeted bolt-on acquisitions that add specific datasets or capabilities to existing platforms.

The numbers are instructive. Annual acquisition spending has ranged from GBP 64 million (2021) to GBP 390 million (2022), averaging roughly GBP 150 to 250 million per year. The ChoicePoint deal in 2008 was the last acquisition exceeding USD 1 billion. Every deal since has been sub-billion—focused on buying data, not brands.

The ThreatMetrix acquisition in 2018 exemplified the approach. At GBP 580 million, it was large by RELX standards but small relative to the company's enterprise value. ThreatMetrix's digital identity network—processing billions of online transactions to distinguish legitimate users from fraudsters—slotted directly into LexisNexis Risk Solutions' existing fraud prevention platform. The data was immediately combinable with RELX's existing datasets, creating a unified identity verification system that neither company could have built alone.

Emailage, acquired in 2020 for roughly USD 480 million, followed the same pattern: a targeted dataset (email-based fraud risk scoring) integrated into an existing platform (LexisNexis Risk Solutions) to enhance an established product suite (identity verification and fraud prevention).

Cirium, the aviation data analytics business, illustrates a different facet of the strategy. Rebranded from FlightGlobal, Cirium provides flight tracking, fleet valuations, and airline operational analytics. It sits somewhat apart from RELX's core verticals—it is neither legal, nor scientific, nor insurance—but it shares the same underlying business model: proprietary data, structured and analysed, delivered through workflow tools, sold on subscription.

The discipline extends to what RELX does not buy. The company has consistently avoided acquisitions in adjacent "hot" sectors—no forays into media, no bets on social data, no expensive acquisitions of AI startups at hundred-times-revenue multiples. The strategy is to buy data and build technology on top of it, not to buy technology and hope data follows.

This restraint is worth dwelling on, because it distinguishes RELX from virtually every other large company claiming to be "technology-driven." The corporate landscape of the past decade is littered with companies that overpaid for technology acquisitions: AT&T's disastrous acquisition of Time Warner, IBM's overpayment for Red Hat, and countless examples of traditional companies paying venture-capital multiples for startups whose technology became commoditised within years.

RELX's approach is the opposite: buy the data, which is irreplaceable, and build the technology in-house, which is replicable but not the scarce asset. The technology layer on top of the data—the user interface, the AI models, the workflow integration—can always be improved incrementally. The data underneath cannot be recreated. By concentrating its M&A spending on data assets rather than technology companies, RELX has avoided the valuation traps that have destroyed shareholder value at so many European conglomerates attempting "digital transformation."

The capital allocation framework treats buybacks not as a residual afterthought but as a core return mechanism. The trajectory has been striking: minimal buybacks in 2021, GBP 550 million in 2022, GBP 850 million in 2023, GBP 1 billion in 2024, GBP 1.5 billion in 2025, and GBP 2.25 billion planned for 2026. At the accelerating pace, RELX is retiring a meaningful percentage of its share count annually—compounding earnings per share growth on top of organic revenue growth.

The progressive dividend—increased every year for over two decades, growing at roughly 7 percent per annum—provides income investors with a reliable and growing stream. The payout ratio hovers around 50 percent of adjusted earnings, leaving ample room for continued growth.

The total capital return equation is simple but powerful: in a company generating GBP 3.3 billion in annual cash flow, with GBP 150 to 250 million consumed by bolt-on acquisitions and roughly GBP 1.2 billion paid in dividends, the remaining GBP 1.5 to 2.0 billion flows into buybacks. This is a company that has solved the capital allocation problem—and solved it in a way that compounds shareholder value across multiple dimensions simultaneously.

Net debt has remained anchored at approximately 2.0 times EBITDA—GBP 7.2 billion at the end of 2025 against GBP 3.85 billion in EBITDA. This leverage level is deliberate: high enough to provide tax-efficient returns (interest expense is deductible), low enough to maintain the investment-grade credit ratings that institutional investors require. The stability of this ratio over time—despite billions in buybacks and acquisitions—demonstrates the underlying cash generation engine. RELX is not borrowing to fund buybacks. It is generating so much free cash flow that it can simultaneously pay dividends, buy companies, repurchase shares, and maintain leverage at a constant level.

The contrast with the broader European corporate landscape is instructive. Most large European companies either hoard cash on their balance sheets (destroying returns through negative real yields) or pursue aggressive M&A that consumes free cash flow and dilutes earnings. RELX does neither. It maintains financial discipline while maximising total returns to shareholders. The approach is not innovative—it is simply rare.

VII. The Playbook — Why RELX Wins (2:10 – 2:35)

Hamilton Helmer's 7 Powers

Three of Helmer's seven competitive powers are present at RELX in formidable strength.

Switching Costs. This is the dominant power.

Consider a mid-sized American law firm with fifty attorneys. Every lawyer's research workflow is built around LexisNexis: search protocols, saved queries, citation formats, document organisation, brief-drafting templates. The firm's knowledge management system is integrated with the LexisNexis API. Its billing system tracks LexisNexis usage for client pass-through charges. Its training programme for new associates is built around LexisNexis methodology.

Switching to Westlaw—or any alternative—would require retraining every lawyer, rebuilding every integration, reformatting every template, and enduring months of productivity loss while attorneys learn a new interface. The direct cost of the software licence is a fraction of the total cost of switching. The real switching cost is measured in thousands of billable hours lost—which, at rates of several hundred dollars per hour, dwarfs the subscription fee.

The same dynamic applies in every RELX segment. A hospital using ClinicalKey for clinical decision support cannot switch to Wolters Kluwer's UpToDate without retraining every physician and nurse. An insurer using the C.L.U.E. database for claims history cannot switch to a competitor without rebuilding its underwriting models. The deeper the product embeds into the customer's workflow, the higher the switching cost—and RELX has spent fifteen years deliberately embedding its products deeper and deeper.

Scale Economies. RELX's data assets exhibit powerful scale economies on both the supply side and the demand side.

On the supply side, the cost of maintaining a database of one billion risk profiles is only marginally higher than maintaining a database of 500 million. But the predictive accuracy of the algorithms trained on the larger dataset is substantially better. This means RELX can invest more in data acquisition and algorithm development than any smaller competitor—and the investment pays for itself through higher accuracy, which attracts more customers, which generates more data, which improves accuracy further. It is the classic flywheel.

On the demand side, each new customer in the Risk segment brings data that improves the product for every other customer. When a new bank joins the LexisNexis fraud detection network, its transaction data enriches the fraud models used by every other bank in the network. This is a demand-side scale economy—also known as a network effect—and it is the most defensible competitive advantage in data-driven businesses.

Cornered Resource. RELX's proprietary datasets constitute a cornered resource that no competitor can replicate through effort alone.

The C.L.U.E. database contains every insurance claim filed in the United States going back decades. Scopus contains the citation relationships between over 90 million documents spanning more than a century of scientific literature. The LexisNexis legal corpus covers case law from dozens of jurisdictions dating to the eighteenth century. The ThreatMetrix digital identity network has built probabilistic identity graphs from billions of online transactions.

These datasets cannot be scraped from the internet. They cannot be purchased from a data broker. They cannot be assembled by a well-funded startup in a few years. They are the product of decades of systematic data collection, curation, and structuring—and the institutional relationships required to maintain them (with insurers, courts, publishers, and government agencies) take years to establish.

A generative AI company—even one backed by billions in venture capital—can build a better user interface, a faster search algorithm, or a more conversational chatbot. What it cannot do is create the underlying data. And without the data, the AI produces hallucinations instead of reliable answers. In legal and medical applications, where accuracy is not a nice-to-have but a professional liability issue, the quality of the underlying data is everything.

Porter's Five Forces

Barriers to Entry: Extremely high. The capital cost of replicating RELX's datasets is not measured in dollars—it is measured in decades.

Consider what a hypothetical competitor would need to do to replicate just the Risk segment's position. It would need to convince thousands of US insurance carriers to share their claims data—a process that took ChoicePoint and its predecessors decades to accomplish. It would need to build relationships with state motor vehicle departments, criminal court systems, and property records offices across all fifty American states. It would need to process billions of online transactions to build a digital identity network comparable to ThreatMetrix. And it would need to do all of this while competing against an incumbent whose existing dataset makes its predictions more accurate with every passing day.

No amount of venture capital can compress decades of data accumulation into a two-year sprint. The barrier is not financial. It is temporal. Time is the moat.

Supplier Power: This is the one area of genuine vulnerability. In STM publishing, RELX's "suppliers" are researchers—and they are increasingly assertive. The Open Access movement, institutional boycotts, and government mandates requiring publicly funded research to be freely available all represent supplier power being exercised against Elsevier's traditional business model. RELX has mitigated this through transformative agreements and by shifting value from content access to analytics tools, but the tension is ongoing and structural.

Buyer Power: Moderate and segment-dependent. In legal research, law firms have limited alternatives (LexisNexis or Westlaw, with few credible third options). In insurance analytics, the C.L.U.E. database is effectively a monopoly resource. In STM, large university systems have occasionally exercised buyer power through subscription cancellations—but the cancellations have typically ended in renegotiated deals rather than permanent departures.

Threat of Substitutes: The most significant threat comes from generative AI. If a large language model can produce reliable legal research or clinical decision support without accessing RELX's proprietary databases, the value proposition erodes. RELX's counter-strategy—embedding its own AI capabilities on top of its proprietary data—is designed to ensure that the AI revolution enhances rather than displaces its products. So far, the strategy appears to be working: the Legal segment's 12 percent profit growth in 2025 suggests that AI is expanding the market rather than cannibalising it.

Competitive Rivalry: Intense but stable. Thomson Reuters—with a market capitalisation exceeding USD 80 billion—competes directly in legal through its Westlaw platform. Wolters Kluwer, the Dutch-listed information services company, competes in both legal compliance and clinical decision support (its UpToDate product rivals ClinicalKey). Verisk Analytics, focused on the US insurance market, competes in risk and insurance analytics. Springer Nature, privately held, competes in scientific publishing.

But no single competitor spans all four of RELX's segments. Thomson Reuters does not do scientific publishing. Wolters Kluwer does not do insurance analytics. Verisk does not do legal research. The breadth of the portfolio—spanning risk, science, law, and exhibitions—is itself a competitive advantage, because it allows RELX to invest in shared technology infrastructure (AI models, cloud platforms, data processing systems) that benefits all four segments simultaneously.

The competitive moat is not any single advantage—it is the reinforcing combination of proprietary data, workflow integration, scale economies, and switching costs across four distinct professional verticals. A competitor would need to match RELX on all four dimensions to compete effectively, and no competitor has attempted to do so.

VIII. The Future — Generative AI & The "Hidden" Growth (2:35 – 2:50)

There is a persistent fear in the investment community that generative AI will destroy information services companies by making their content freely available through AI-generated summaries. The fear is understandable. If ChatGPT can summarise a legal case or a medical study, why pay for LexisNexis or ClinicalKey?

The answer is accuracy—and liability.

A lawyer who relies on a general-purpose AI chatbot for case research and cites a hallucinated case in a court filing faces professional sanctions—as multiple real-world incidents have demonstrated since 2023. The most notorious case involved a New York attorney who submitted a ChatGPT-generated brief containing fabricated case citations in a federal court proceeding; the resulting sanctions and public humiliation sent shockwaves through the legal profession. A doctor who follows an AI-generated treatment recommendation that contradicts the peer-reviewed evidence faces malpractice liability. An insurance underwriter who uses an unvalidated risk score faces regulatory scrutiny from state insurance commissioners who require transparent, auditable methodologies.

In these high-stakes professional contexts, the value proposition is not "access to information." It is "verified, citation-backed, professionally reliable information." And producing that requires proprietary data that has been curated, structured, and validated over decades—precisely the assets RELX owns.

RELX allocated 70 percent of its R&D budget to AI and data integration in 2024. The investment has produced a wave of AI-enabled products across every segment: Lexis+ AI and Protege General AI in legal, ScopusAI and ScienceDirect AI in STM, Ask ICIS in energy and chemicals data, Nexis+ AI in business intelligence, and AI Assist through the Brightmine HR platform.

The strategic bet is that RELX is a "net winner" from generative AI—that AI will expand the market for its products rather than substitute for them. If the bet is correct, the AI revolution will increase the value of RELX's proprietary datasets (because they become the "ground truth" that AI models need to produce reliable outputs) and increase the willingness of customers to pay for AI-enabled analytics tools (because the tools save more time and produce better outcomes than manual research).

Beyond AI, RELX is expanding into adjacent data markets that leverage its existing capabilities in new verticals.

ESG data and carbon tracking represent emerging opportunities where structured, verified data is increasingly required by regulators. As European and American regulators mandate climate-related financial disclosures—through frameworks like the EU's Corporate Sustainability Reporting Directive and the SEC's climate disclosure rules—companies need reliable ESG data the same way they need reliable financial data. RELX's expertise in structuring unstructured information and delivering it through workflow tools positions it to become a significant provider of corporate sustainability analytics.

Agricultural data represents an even more intriguing frontier. By combining satellite imagery with weather data, soil chemistry databases, and historical crop yield records, RELX can build predictive models that estimate the probability of crop failure for specific fields in specific growing seasons. The application for crop insurance is obvious: instead of pricing policies based on broad regional averages, insurers can price them based on field-level risk assessments. The precision improves underwriting accuracy, reduces losses, and creates value for both the insurer and the farmer. This is the ChoicePoint thesis applied to agriculture—taking a manual, imprecise underwriting process and replacing it with automated, data-driven risk prediction.

The ICIS business, which provides pricing and market intelligence for the energy and chemicals sectors, and the Cirium aviation analytics platform represent additional "hidden" growth vectors that most analysts group under broader segment reporting but which individually represent substantial businesses with defensible competitive positions.

The bear case on these initiatives is execution risk: RELX has historically excelled at incremental improvement and bolt-on acquisition rather than greenfield innovation. Building entirely new data products in unfamiliar verticals—agriculture, ESG, carbon tracking—carries higher risk than acquiring established datasets in core markets. The company has no meaningful track record in agricultural insurance or ESG analytics, and it will be competing against specialised entrants who may move faster in these nascent markets.

There is also the question of AI cannibalisation. RELX's current thesis is that generative AI expands its addressable market by making its products more valuable. But there is an alternative scenario in which AI commoditises the analytics layer—the search, the synthesis, the recommendation—while the underlying data remains the only differentiator. In that scenario, RELX's margins would compress even as its data assets retained their strategic value. The company would still be essential, but it would be essential at lower margins. This scenario is speculative but not implausible, and it is the primary concern driving the 2026 share price decline.

The regulatory overhang on STM publishing remains material. Government mandates requiring Open Access to publicly funded research—including policies enacted in the US, EU, and China—could compress margins on the traditional subscription business over the medium term. RELX's response has been to shift value from content access to analytics tools, but the transition is incomplete and the regulatory pressure is ongoing.

On data privacy, LexisNexis Risk Solutions has faced scrutiny for providing personal data to US immigration authorities. Between 2005 and 2024, the Department of Homeland Security awarded RELX subsidiaries over USD 172 million in contracts through the Accurint platform. A lawsuit brought by immigrant rights organisations in 2022 was dropped in May 2024—potentially settled, though terms were not disclosed. LexisNexis reportedly stipulated contractually that it not be named in ICE press releases or marketing materials.

The reputational and regulatory risks associated with government surveillance contracts remain a consideration for ESG-conscious investors—and the tension between RELX's data analytics capabilities and individual privacy rights is likely to intensify as both the data and the AI tools become more powerful.

The 2026 share price drawdown—from 4,183 pence to approximately 2,465 pence, a decline of roughly 41 percent—deserves comment. The decline appears to reflect broader market concerns about AI disruption in information services, rather than any deterioration in RELX's underlying business performance. FY 2025 results showed accelerating revenue growth, expanding margins, and record free cash flow—the antithesis of a business being disrupted.

The compression of valuation multiples tells a striking story of sentiment versus substance. Trailing P/E fell from roughly 35 times at the peak to approximately 20 times at the trough. The forward P/E compressed to roughly 16 times—a level RELX has not traded at in over a decade. For a company growing earnings at high single digits with near-perfect cash conversion, the valuation reflects either a rational repricing of existential AI disruption risk or a market overreaction to a narrative that does not match the fundamentals. The disconnect between RELX's FY 2025 operating results—which were the strongest in the company's history by virtually every metric—and its share price performance in early 2026 is one of the more puzzling divergences in the European equity market. Time will tell which signal is correct.

IX. Conclusion — Final Reflections (2:50 – 3:00)

RELX is what happens when you apply software-as-a-service economics to a century of proprietary data.

The business model is deceptively simple: collect information that professionals need to make critical decisions, structure it into searchable and analysable formats, embed it into workflow tools that become indispensable to daily operations, and charge subscription fees that grow steadily year after year. The result is a company with 84 percent digital revenue, 35 percent operating margins, 99 percent free cash flow conversion, and a track record of consistent compounding that spans decades.

The quiet ones, it turns out, often build the biggest moats.

RELX does not hold press conferences to announce its quarterly results. Its CEO does not appear on CNBC. Its products are invisible to consumers. But behind every bank account opening, every insurance quote, every clinical decision, every legal brief, and every scientific citation, RELX's infrastructure hums along—processing, analysing, predicting.

For investors tracking RELX's ongoing performance, two KPIs cut closest to the trajectory of the business.

Underlying revenue growth measures whether RELX's products are becoming more valuable to customers. The metric strips out currency effects and acquisitions to reveal pure organic demand—the truest measure of whether the company's analytics tools are gaining traction or losing relevance. In 2025, underlying growth ranged from 5 percent in STM to 9 percent in Legal, with Risk at 8 percent and Exhibitions at 8 percent. The Legal segment's acceleration to 9 percent—from historically lower single-digit growth—is particularly significant because it suggests that AI-enabled products are expanding the addressable market rather than merely substituting for existing research tools.

If underlying growth across all segments remains consistently in the mid-to-high single digits, it indicates that customers are both renewing existing subscriptions and purchasing additional analytics capabilities on top of their base contracts. The compounding thesis holds as long as this pattern persists. If underlying growth decelerates toward low single digits—particularly in Risk or Legal—it would signal market saturation or competitive displacement, and the premium valuation multiple would come under pressure.

Adjusted free cash flow conversion measures whether reported profits are translating into actual cash. At 99 percent in 2025, RELX converts virtually every pound of operating profit into cash available for dividends, acquisitions, and buybacks. This metric is particularly important because it validates the quality of earnings—high conversion means the company is not papering over weak cash generation with accounting adjustments. Any sustained decline below 90 percent would warrant investigation.

The question RELX poses for investors is whether a company this consistent, this disciplined, and this deeply embedded in professional workflows can sustain its compounding trajectory in an era of AI disruption. The early evidence—accelerating growth in the Legal segment, expanding AI product suites across all divisions, and rising capital returns—suggests the answer is yes. But the evidence is still early, and the disruption is still unfolding.

What is not in dispute is the strategic position RELX has built over thirty years: proprietary data that cannot be replicated, workflow integration that creates prohibitive switching costs, and a management team that has demonstrated—through sixteen years of consistent execution—that boring, done brilliantly, can be one of the most powerful strategies in business.

Is RELX the most important technology company in Europe that is not ASML? The comparison is instructive. Both companies occupy dominant positions in industries that are invisible to consumers but essential to the functioning of modern economies. Both generate extraordinary margins from products that are embedded so deeply into customer workflows that switching is practically unthinkable. Both have compounded shareholder returns for decades through a combination of organic growth, disciplined capital allocation, and strategic clarity.

The difference is that ASML makes a physical product—lithography machines—whose dominance is visible and quantifiable. RELX's dominance is invisible. Its products are embedded in the infrastructure of decisions: the algorithms behind the insurance quote, the citations underlying the legal brief, the clinical pathway guiding the treatment decision. The invisibility is, paradoxically, the strength. What cannot be seen cannot easily be disrupted. And what cannot be disrupted compounds quietly, year after year, decade after decade.

The final irony of the RELX story is that the company's greatest competitive advantage may be its own boringness. In a market obsessed with narratives—AI hype, meme stocks, disruptive startups—the companies that generate the least excitement often generate the most sustainable returns. RELX does not have a charismatic founder. It does not have a consumer-facing product. It does not have a Twitter following. What it has is a century of proprietary data, a management team that has executed the same strategy without deviation for sixteen years, and a business model that converts information into cash with the efficiency and reliability of a Swiss watch.

The quiet companies build the biggest moats. RELX built one of the biggest in Europe—and most people still have not noticed. That may be the most bullish signal of all: in a market obsessed with narratives, the company with the least compelling story and the most compelling fundamentals often offers the most durable returns.

X. References

- RELX Annual Reports (2008, 2015, 2020-2025)

- RELX FY 2025 Results Announcement, February 2026

- ChoicePoint Inc. Acquisition Announcement, February 21, 2008

- ThreatMetrix Acquisition Announcement, 2018

- "The Cost of Knowledge" Boycott, initiated January 21, 2012 by Timothy Gowers

- University of California-Elsevier Subscription Cancellation (2019) and Transformative Agreement (2021)

- RELX Rebranding to RELX Group, effective July 1, 2015

- Lexis+ AI Launch and International Rollout (2023-2024)

- Protege General AI Launch, August 2025

- Erik Engstrom appointment as CEO, November 2009

- Nick Luff appointment as CFO, 2014

- RELX Capital Allocation and Share Buyback Programmes (2021-2026)

- Fitch/Moody's Credit Assessments of RELX

- DHS Contracts with LexisNexis Risk Solutions, as reported by investigative journalism outlets (2005-2024)

- EU Open Access Mandates and Plan S Documentation

- LSE Listing Prospectus, Reed Elsevier Dual-Listed Structure (1993)

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube