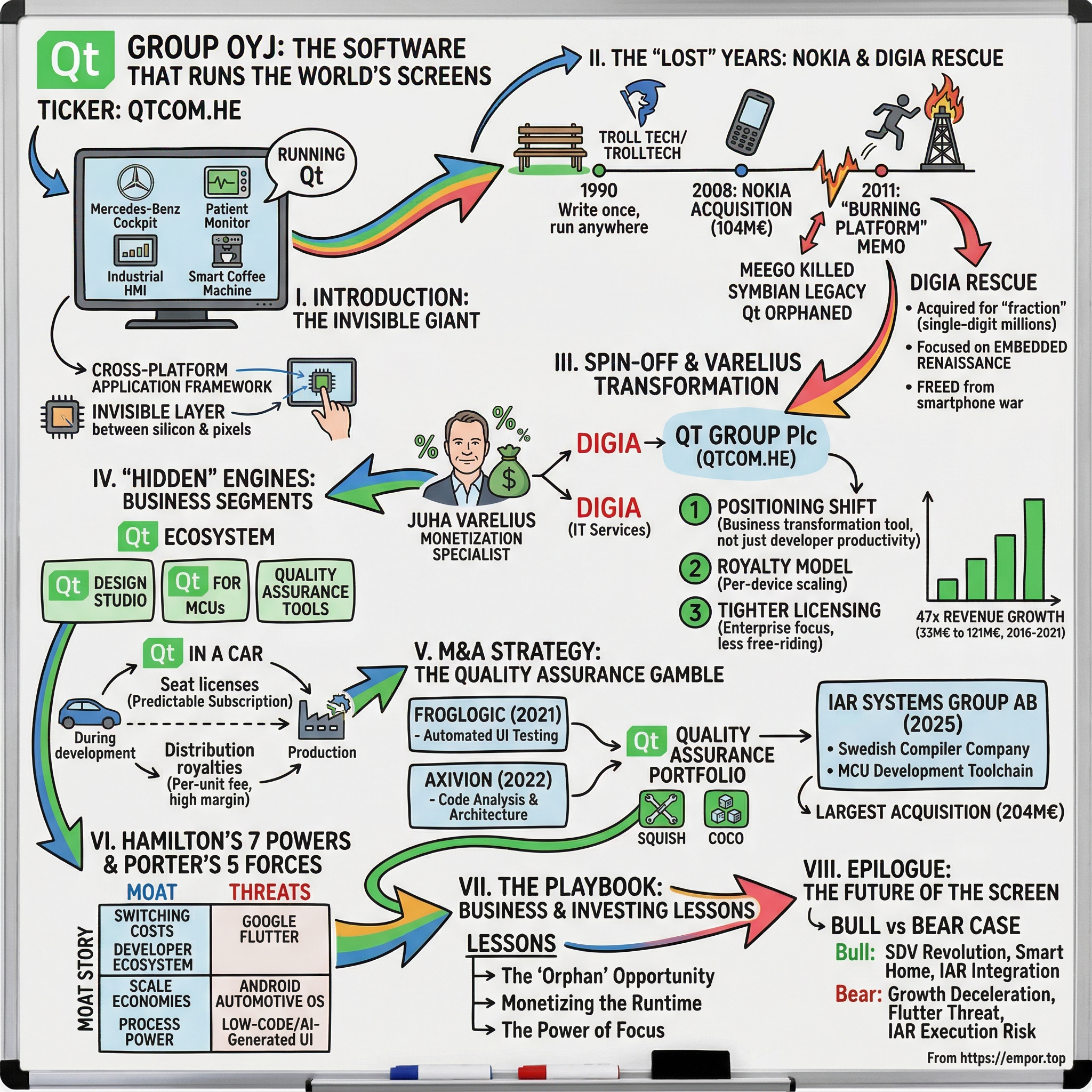

Qt Group: The Software That Runs the World's Screens

I. Introduction: The Invisible Giant

Right now, somewhere in Stuttgart, a Mercedes-Benz engineer is swiping through a prototype digital cockpit running sixty frames per second on a twelve-inch OLED display. In a hospital in Boston, a nurse is tapping through a patient-monitoring interface that must never freeze, never crash, never show a loading spinner when a life is on the line. In a factory in Shenzhen, an operator is adjusting parameters on an industrial HMI panel bolted to the side of a robotic welding arm. And in a kitchen in Seoul, someone is selecting the brew strength on the touchscreen of a smart coffee machine.

Every single one of those screens is running Qt.

Pronounced "cute"—yes, really—Qt is one of the most consequential pieces of software infrastructure that almost nobody outside the developer world has heard of. It is a cross-platform application framework, originally built in C++, that allows engineers to write a graphical user interface once and deploy it across dozens of operating systems and hardware targets. Think of it as the invisible layer between the silicon chip and the pixels you touch. The company behind it, Qt Group Oyj, trades on the NASDAQ Helsinki under the ticker QTCOM.HE, and its story is one of the most improbable survival narratives in European technology.

Here is the thesis: Qt began as a Norwegian dream of "write once, run anywhere" in the early 1990s, got swept up in Nokia's doomed smartphone ambitions, was left for dead after the most infamous internal memo in mobile history, and then was rescued for pennies on the dollar by a small Finnish IT services firm that saw what almost nobody else did—that while the smartphone war was lost, the rest of the physical world was just beginning to need beautiful, reliable, high-performance user interfaces. From that insight, Qt Group transformed itself from an orphaned developer tool into a toll booth on the Internet of Things and the Software-Defined Vehicle. At its peak in late 2021, the company commanded a market capitalization north of two billion euros, a roughly forty-seven-fold gain from its 2016 spin-off price. The stock has since corrected sharply—trading around four hundred seventy million euros in market cap as of early April 2026—but the underlying strategic position, and the questions it raises about embedded software monetization, remain as relevant as ever.

This is the story of how a "boring" C++ framework survived the death of Nokia, bet everything on the embedded renaissance, and built one of the most elegant business models in enterprise software: a per-device royalty that scales with the customer's success, not just their headcount. It is also a story about what happens when that growth narrative hits a wall, and whether the moat is as deep as the bulls believe.

Let us start at the moment everything almost ended.

II. The "Lost" Years: Nokia and the Digia Rescue

To understand why Qt's near-death experience matters, you need to rewind to a park bench in Trondheim, Norway, in 1990. Two computer science students at the Norwegian Institute of Technology—Haavard Nord and Eirik Chambe-Eng—were working on a database application for ultrasound images. The application needed to run on Unix, Windows, and classic Mac OS, and every existing toolkit for building graphical interfaces was either platform-specific, poorly designed, or both. So they decided to build their own. Haavard liked the way the letter "Q" looked in his Emacs typeface, and the "t" was a nod to "Xt," the X Window toolkit. Qt was born.

They incorporated as Quasar Technologies on March 4, 1994, later renamed Troll Tech, then Trolltech. The first public release of Qt hit the internet on May 20, 1995. What made it special was architectural: Qt abstracted away the operating system, allowing a developer to write one codebase in C++ and have it compile natively on Linux, Windows, macOS, and eventually dozens of embedded platforms. It was not a virtual machine like Java. It compiled to native machine code, which meant performance was essentially identical to hand-written platform-specific code. For developers building anything more complex than a simple form—think real-time data visualization, 3D rendering, or embedded device interfaces—this was transformative.

Trolltech grew steadily through the late 1990s and 2000s, building a loyal open-source community and a commercial licensing business. The company went public on the Oslo Stock Exchange in July 2006. And then Nokia came calling.

In January 2008, Nokia made a public voluntary tender offer for Trolltech at approximately one hundred four million euros—roughly one hundred fifty million dollars at the time. The rationale was straightforward and, in hindsight, tragically misguided. Nokia was the world's largest phone manufacturer and wanted Qt to become the unifying software layer across its two operating systems: Symbian, the aging but still dominant smartphone platform, and MeeGo, an ambitious new Linux-based mobile OS being co-developed with Intel. The idea was that developers would write Qt applications once and they would run beautifully on both. By June 2008, the acquisition was complete. Trolltech was renamed Qt Software, then Qt Development Frameworks. The Norwegian dream was now a cog in Finland's most important company.

For about two and a half years, this looked like it might work. Qt was being deeply integrated into Nokia's development stack. Developers were building applications. The MeeGo project was generating genuine excitement. And then, on February 8, 2011, everything detonated.

Stephen Elop, a Canadian executive who had joined Nokia as CEO from Microsoft just five months earlier, sent an internal memo to all Nokia employees that was immediately leaked to Engadget. It became known as the "Burning Platform" memo, and it is one of the most consequential documents in the history of the mobile industry. Elop wrote about a man standing on a burning oil platform in the North Sea, faced with the choice of certain death by fire or a potentially fatal leap into freezing water. The "platform" metaphor was deliberate—Nokia's software platforms, Symbian and MeeGo, were the burning ones. "We too, are standing on a 'burning platform,'" Elop wrote. "And we must decide how we are going to change our behavior."

Three days later, on February 11, Nokia announced a "strategic partnership" with Microsoft, adopting Windows Phone as its primary smartphone operating system. Symbian was relegated to legacy status. MeeGo was effectively killed. And Qt—the entire reason Nokia had spent one hundred fifty million dollars acquiring Trolltech—was suddenly an orphan. The framework that was supposed to be the foundation of Nokia's mobile future had no mobile future.

What followed was one of the most brutal value destructions in European tech history. During Elop's tenure from 2010 to 2014, Nokia's smartphone market share collapsed from thirty-three percent to three percent, the stock cratered, and the company accumulated approximately four point nine billion euros in cumulative losses before selling its handset division to Microsoft in 2014. But buried inside that catastrophe was a quiet transaction that would prove to be one of the great bargain acquisitions in software history.

In March 2011, almost immediately after the Burning Platform announcement, Nokia sold the commercial licensing business of Qt to Digia, a modest Finnish IT services company based in Helsinki. Then, in August 2012, Digia signed an agreement to acquire the entire remaining Qt business—the development framework, the open-source project, the R&D operation, and approximately one hundred twenty-five employees, most of them in Oslo and Berlin. The exact price was never publicly disclosed by either party, but contemporary reporting from TechCrunch and Engadget described it as a "fraction" of the one hundred fifty million Nokia had originally paid. Press accounts and industry estimates placed it in the single-digit millions of euros. Digia's own financial filings characterized the deal as having a "slightly positive" revenue impact and being "earnings neutral" for 2012.

Think about that for a moment. A cross-platform software framework used by tens of thousands of developers worldwide, with deep penetration into automotive, medical, and industrial markets, was essentially picked up for the price of a nice apartment in downtown Helsinki. Nokia was so desperate to shed non-core assets and so focused on the Windows Phone transition that Qt was treated as surplus inventory.

But Digia saw something that Nokia, in its smartphone tunnel vision, had missed entirely. The smartphone war was indeed lost—iOS and Android had won, and Qt would never be a meaningful mobile development platform. But the rest of the world—cars, medical devices, industrial machines, home appliances, wearable devices, point-of-sale terminals—was just beginning its transition to rich, touch-enabled graphical interfaces. These were embedded systems, and they had very specific requirements: real-time performance, deterministic behavior, small memory footprints, and the ability to run on a bewildering variety of hardware and operating systems. Qt was almost uniquely suited for this market. The "orphan" was not dying. It was being freed.

This is the pattern that sophisticated technology investors watch for obsessively: a genuinely valuable asset trapped inside a failing or distracted parent company, sold at distressed prices because the market cannot see past the parent's problems. Digia did not just buy a software framework. It bought a toll booth at the entrance to the embedded computing revolution, and it paid almost nothing for it.

III. The Spin-off and The Varelius Transformation

By September 2014, Digia had reorganized its Qt operations into a wholly owned subsidiary called The Qt Company, giving the business its own identity and management focus for the first time since the Nokia years. But the real inflection point came in 2016.

In August 2015, Digia's board began exploring a full demerger—separating the fast-growing Qt business from Digia's lower-margin domestic IT services operation. The logic was compelling. Digia's consulting business was a perfectly decent Nordic IT services company, but it had nothing in common with a global cross-platform software framework business. The two units had different growth profiles, different margin structures, different customer bases, and different capital allocation needs. Bundling them together meant that investors who wanted exposure to Qt's embedded software growth were also buying a portfolio of Finnish IT consulting contracts, and vice versa.

On May 1, 2016, the demerger was registered in the Finnish trade register. Qt Group Plc began trading on the NASDAQ Helsinki under the ticker QTCOM. And the man appointed to lead it was Juha Varelius, who had been Digia's CEO since 2008 and had effectively overseen the Qt business since the Nokia acquisition in 2012.

Varelius is a fascinating figure—and understanding him is essential to understanding what Qt Group became. He holds a Master of Science in Economics and an MBA, with a career background that included managerial roles at Yahoo and Sonera, the Finnish telecom company, before joining Digia. He is not a programmer. He is not an open-source evangelist. He is not a product visionary in the mold of a Steve Jobs or even a Linus Torvalds. What Varelius is, unmistakably, is a monetization specialist—a leader with an almost clinical focus on extracting commercial value from a technology asset that had historically been undermonetized.

The Qt community had long operated with a dual-licensing ethos: an open-source version (LGPL/GPL) for the community, and a commercial license for companies that wanted proprietary features, support, and the ability to ship closed-source products. Under Nokia, and even in the early Digia years, the commercial side was treated somewhat gingerly—there was always a tension between nurturing the open-source ecosystem and pushing harder on enterprise sales. Varelius resolved that tension decisively in favor of revenue.

His strategic shift can be summarized in three moves that transformed Qt from a developer tool into a business platform.

First, he reframed Qt's positioning. Under the old model, Qt was sold as a developer productivity tool—you bought it because it saved your engineers time. Under Varelius, Qt was repositioned as a "business transformation tool" for companies digitizing their physical products. The pitch was no longer "save your developers six months of porting work." The pitch was "we are the software layer that enables your company to ship software-defined products." This reframing justified much higher price points and moved the sales conversation from the engineering budget to the C-suite.

Second, he invested heavily in the distribution licensing model—the per-device royalty. This was the crucial insight. Selling developer seats was a fine business, but it scaled linearly with the customer's engineering headcount. The royalty model scaled with the customer's product shipments. If a car manufacturer designed its digital cockpit on Qt and then shipped two million vehicles, Qt collected a fee on every single unit. The royalty was typically a tiny fraction of the vehicle's bill of materials—perhaps a few dollars on a forty-thousand-dollar car—which made it almost invisible to procurement teams but enormously valuable in aggregate to Qt Group.

Third, he tightened the licensing terms. In 2020, Qt Group made changes to its open-source licensing that effectively required more commercial users to purchase paid licenses. The LTS (Long Term Support) releases, which enterprise customers depended on for stability, were restricted to commercial licensees. This was controversial in the open-source community—there were heated debates on forums and developer blogs—but it was commercially effective. It closed the "free-riding" gap where large companies were using Qt in commercial products under the open-source license without paying for a commercial agreement.

Varelius's shareholding tells its own story about alignment. He directly owns approximately one point six percent of Qt Group, a stake valued at around ten million euros at current prices—and worth considerably more at the 2021 peak. His compensation structure is heavily weighted toward long-term revenue growth and EBIT margin targets, which means he earns the most when Qt grows its topline while maintaining profitability. This is precisely the incentive structure that "compounder" investors look for: a CEO whose personal wealth is tied to the same metrics that drive long-term shareholder value.

The results of the Varelius transformation were extraordinary. From thirty-three million euros in revenue in 2016, Qt Group grew to one hundred twenty-one million in 2021—a compound annual growth rate of roughly thirty percent over five years. EBITA margins expanded from breakeven to the mid-twenties. The stock price, which opened at around three euros and seventy-six cents on the first day of trading in May 2016, reached approximately one hundred eighty euros by October 2021. Investors who bought at the spin-off and held to the peak earned roughly forty-seven times their money. It was one of the great Nordic small-cap stories of the decade.

The cultural shift was real, too. Qt Group under Varelius moved from a company that felt like an open-source project with a business attached to one that felt like an enterprise software company with an open-source project attached. Not everyone liked it—some long-time community members felt alienated by the tighter licensing and the harder commercial push—but from a business perspective, it worked. The question investors face now is whether the growth engine that powered that transformation has stalled, or merely paused.

IV. The "Hidden" Engines: Business Segments

To understand Qt Group's economics, imagine a simplified software stack inside a modern car. At the bottom is the hardware—processors, memory, displays. Above that sits an operating system, often a real-time Linux variant or an automotive-grade RTOS. Above the OS sits the application framework—this is where Qt lives—providing the tools to render graphics, handle touch input, manage animations, and connect the interface to the vehicle's underlying systems. And at the top sits the actual user interface: the maps, the media player, the climate controls, the instrument cluster.

Qt occupies that critical middle layer. It is not the hardware, not the operating system, and not the end-user application. It is the plumbing that connects all three. And its business model extracts value from two distinct points in the customer's workflow.

The first revenue stream is development licenses, often called "seat" licenses. These are per-developer subscriptions that give engineers access to the commercial Qt framework, the Qt Creator IDE, documentation, support, and the right to build proprietary applications. Pricing varies by tier and customer size, from roughly five hundred dollars per year for qualifying small businesses to enterprise-negotiated rates that can run into the tens of thousands per seat for large organizations. This is a classic enterprise software model—predictable, subscription-based, and correlated with the size of the customer's development team.

But the development license is not what makes Qt Group's business model special. The second revenue stream—distribution licenses, or royalties—is the hidden engine.

Here is how it works. When a company builds a desktop or mobile software application using Qt, they generally do not owe a per-unit royalty when they distribute that application to end users. But when a company builds a physical device—a car, a medical device, an industrial controller, a consumer appliance—that ships with Qt-based software embedded in it, they must purchase a distribution license for each device model, and in many cases pay a per-unit fee for every device shipped. The distinction is important: applications are royalty-free, but devices are not.

This creates a business dynamic that is almost uniquely attractive in enterprise software. Qt gets "designed in" to a product during the development phase, which might take two to four years for something like an automotive platform. Once the product launches, every unit that rolls off the assembly line generates revenue for Qt Group. The royalty per unit is deliberately kept small relative to the overall bill of materials—typically a few dollars on a device that might cost hundreds or thousands of dollars—so it does not trigger aggressive pushback from procurement. But when multiplied across millions of units, the numbers become substantial. And critically, the marginal cost to Qt of serving those additional units is essentially zero. The software is already written. The support infrastructure is already in place. Each incremental royalty dollar falls almost entirely to the bottom line.

This is why Qt Group's EBITA margins reached thirty-four percent in 2024. It is not because they are charging exorbitant prices for developer tools. It is because an increasing share of their revenue comes from high-margin, volume-driven royalty streams that scale with their customers' production volumes.

Beyond the core framework, Qt has been expanding its product surface in three notable directions.

The first is Qt for MCUs—microcontroller units. Traditional Qt requires a relatively powerful processor and a meaningful amount of RAM, which limits it to devices with significant computing budgets. Qt for MCUs uses a lightweight rendering engine called Qt Quick Ultralite that can run on bare-metal microcontrollers with as little as a few hundred kilobytes of RAM. This opens up an entirely new tier of devices: thermostats, washing machines, coffee machines, e-bike displays, small industrial panels—the sort of everyday objects that are increasingly getting touchscreens but cannot justify the cost of a full-blown application processor. Qt for MCUs 3.0, targeting full compliance with the EU's Cyber Resilience Act, is expected in mid-2026. The TAM expansion here is enormous: the microcontroller market ships billions of units annually, and the fraction of those that need graphical interfaces is growing rapidly.

The second expansion is Qt Design Studio, a visual design tool that attempts to bridge the gap between UI designers (who typically work in tools like Figma or Adobe XD) and the engineers who implement those designs in code. The idea is to allow designers to create pixel-perfect mockups that can be directly exported as working QML code—Qt's declarative UI language—eliminating the tedious back-and-forth translation process that plagues most product development teams. This is a competitive space, but Qt's advantage is that Design Studio produces output that is native to the Qt framework, not a separate artifact that needs to be reimplemented.

The third expansion is into quality assurance, which became a major strategic priority through two acquisitions—but those deserve their own section.

For investors tracking Qt's ongoing performance, two KPIs matter above all others. The first is the mix shift between development license revenue and distribution license revenue. As distribution royalties grow as a percentage of total revenue, margins should structurally expand and revenue should become more recurring and volume-driven. The second is net revenue retention or expansion within existing enterprise accounts—what Qt calls ARPA, average revenue per account. If Qt is successfully cross-selling new products (QA tools, MCU licenses, Design Studio) into its existing base of over twelve hundred enterprise customers, ARPA should trend upward consistently, indicating deepening customer relationships rather than just new logo acquisition.

V. M&A Strategy: The Quality Assurance Gamble

In the spring of 2021, Qt Group made a move that surprised many observers. The company announced the acquisition of Froglogic GmbH, a German developer of automated GUI testing tools, for thirty million euros—twenty-four million in cash and six million in newly issued Qt Group shares. Froglogic's flagship product, Squish, was the leading tool for automating the testing of graphical user interfaces, with particular strength in Qt-based applications but also supporting a wide range of other frameworks including Java, .NET, and web technologies.

Froglogic had generated revenue of six point five million euros in 2020 with EBIT of two point seven million—a healthy forty-two percent margin that reflected the asset-light nature of developer tooling businesses. At thirty million euros, Qt was paying roughly four point six times revenue and eleven times EBIT. By enterprise software standards, these were reasonable multiples for a profitable, growing, niche-dominant tool—not a bargain, but not an overpay either.

The strategic logic went deeper than the numbers. Qt was making a calculated bet that its customers did not just want to build user interfaces—they wanted to manage the entire lifecycle of those interfaces, from design through development through testing through deployment. If Qt could own the testing step as well as the development step, it could increase its share of each customer's software budget without needing to win new accounts. And because Squish was already the market leader for testing Qt-based UIs, the cross-selling opportunity was immediate: every existing Qt commercial licensee was a potential Squish customer.

Sixteen months later, in August 2022, Qt doubled down with a second acquisition: Axivion GmbH, another German company, this one focused on static code analysis and software architecture tools. The enterprise value was thirty-two million euros—twenty-four million in cash and eight million in shares—with an additional earn-out of up to twelve million euros contingent on Axivion's product revenue growth through 2024. Axivion had generated five million euros in revenue and one point five million in EBIT in 2021. The base-price multiple was roughly six point four times revenue, somewhat richer than Froglogic, reflecting the strategic premium Qt was willing to pay to fill another gap in its toolchain.

Axivion's products detect what the company calls "software erosion"—the gradual degradation of code quality and architectural integrity that occurs as large codebases evolve over time. Its tools perform static analysis, identify code clones (duplicated code segments), check compliance with safety standards like MISRA and CERT, and visualize dependencies within complex software architectures. For Qt's automotive and medical device customers, who must comply with stringent functional safety standards (ISO 26262 for automotive, IEC 62304 for medical), these capabilities were not nice-to-haves. They were increasingly required by regulators and auditors.

Together, Froglogic and Axivion gave Qt a quality assurance portfolio that it branded as "Qt Quality Assurance"—comprising Squish for automated UI testing, Coco for code coverage analysis, Test Center for test management, and the Axivion Suite for static analysis and architecture verification. The combined offering allowed Qt to tell a compelling story to enterprise customers: you can design your UI in Qt Design Studio, build it with Qt Creator and the Qt framework, test it with Squish and Coco, analyze its code quality with Axivion, and deploy it with Qt's distribution tools. The entire software development lifecycle, managed within a single vendor ecosystem.

This "workflow land grab" strategy is not unique to Qt—it is the same playbook that Atlassian ran with Jira-to-Confluence-to-Bitbucket, or that Synopsys and Cadence run in EDA. The logic is always the same: once you own one critical step in a customer's workflow, each adjacent step you capture increases switching costs and average revenue per account. The risk, of course, is "diworsification"—acquiring tangential businesses that distract management and dilute the company's focus. But both Froglogic and Axivion were tightly complementary to Qt's core. They served the same customers, addressed the same workflows, and could be sold by the same enterprise sales team. By the standards of small-cap software M&A, these were disciplined, bolt-on acquisitions rather than transformative gambles.

The biggest and most consequential acquisition came in 2025, when Qt Group announced in July that it would acquire IAR Systems Group AB, a Swedish company publicly traded on the Stockholm exchange, for approximately two hundred four million euros in an all-cash deal. IAR makes commercial C and C++ compilers and debuggers for microcontrollers—the exact hardware targets that Qt for MCUs was designed to run on. The strategic complementarity was obvious: IAR provided the compilation and debugging layer, Qt provided the UI framework layer, and together they could offer MCU developers an integrated toolchain from code editing to graphical interface deployment.

The IAR deal was completed in October 2025 with over ninety-four percent shareholder acceptance. At roughly two hundred four million euros, it was by far the largest acquisition in Qt Group's history—larger than the Froglogic and Axivion deals combined by a factor of three. It also came with execution risk: IAR was in the process of transitioning from perpetual licenses to a subscription model, a shift that Qt had experience managing but that typically creates short-term revenue headwinds as customers shift from large upfront payments to smaller recurring ones. Qt's 2026 guidance explicitly flagged that EBITA margins would be compressed to "at least fifteen percent" in part due to IAR integration costs, down from twenty-four percent in 2025.

The IAR acquisition represents Qt Group's most ambitious bet yet: that it can become the dominant end-to-end development platform for the microcontroller ecosystem, owning everything from the compiler to the graphical interface. If it works, the addressable market expands dramatically—MCU shipments number in the tens of billions annually. If it stumbles, the company will have spent its largest-ever capital outlay on a business in mid-transition, at a time when its own core growth rate has already decelerated.

VI. Hamilton's 7 Powers and Porter's 5 Forces

Every interesting business has a moat story. Qt Group's moat story is unusually clear in some dimensions and genuinely debatable in others. Let us examine it through both strategic frameworks.

Switching Costs: The Primary Power

This is Qt's strongest competitive advantage, and it is worth dwelling on why. When an automotive OEM decides to build its next-generation digital cockpit on Qt, that decision initiates a multi-year development program. Engineers learn the Qt framework. Design teams learn Qt Design Studio and QML. Testing teams build automation suites in Squish. Custom components and libraries are written against the Qt APIs. The entire software architecture is structured around Qt's rendering pipeline, event system, and platform abstraction layer.

Now imagine, three years into that program and six months before production launch, someone suggests switching to a different framework. Every line of QML code would need to be rewritten. Every custom widget would need to be reimplemented. Every test suite would need to be rebuilt. Every engineer would need to be retrained. The switching cost is not theoretical—it is measured in hundreds of millions of dollars of engineering time and, critically, in schedule delay. In automotive, where a six-month delay can mean missing a model year and losing a billion dollars in revenue, that schedule risk is what makes switching truly prohibitive.

This dynamic is even stronger in safety-critical domains like medical devices and aerospace, where the software must be certified against regulatory standards. Switching frameworks means re-certifying the entire software stack—a process that can take years and cost tens of millions of dollars. No rational procurement executive would force a framework change mid-program to save a few dollars per unit on Qt royalties.

Cornered Resource: The Developer Ecosystem

Qt has been around for over thirty years. There is a massive global ecosystem of C++ developers who have "Qt" as a primary skill on their resume. University courses teach Qt. Books and tutorials are written about it. Hiring managers at automotive Tier 1 suppliers specifically recruit for Qt experience. This creates a self-reinforcing cycle: companies choose Qt because they can find developers who know it, and developers learn Qt because companies use it.

This is not an impregnable moat—developers can learn new frameworks—but it creates meaningful friction. A company that switches away from Qt does not just need to retrain its existing team; it needs to hire new people with different skills in a tight labor market. The "cornered resource" here is not a patent or a license; it is the installed base of human capital.

Scale Economies: Spreading R&D Across Thousands of Customers

Supporting a cross-platform framework is extraordinarily expensive. Qt must work correctly on dozens of operating systems, hundreds of hardware platforms, and thousands of device configurations. Each new OS version, chip architecture, or display technology requires testing and potential adaptation. The R&D cost of maintaining this compatibility matrix is high, but it is spread across more than twelve hundred enterprise customers and hundreds of thousands of open-source users. No individual customer could afford to maintain this breadth of platform support independently, which is what makes using Qt economically rational even at premium price points.

Process Power and Counter-Positioning

Qt's thirty-plus years of cross-platform expertise represent accumulated process knowledge that would be extremely difficult for a new entrant to replicate. The subtle bugs, the platform-specific workarounds, the performance optimizations across different GPU architectures—this institutional knowledge is embedded in millions of lines of code and thousands of person-years of engineering experience. A startup attempting to build a competing cross-platform embedded UI framework would face a decade or more of catch-up.

Qt also benefits from a form of counter-positioning relative to Big Tech. Google could build a competing embedded UI framework (and has, with Flutter), but Google's incentive is to drive adoption of its own platforms (Android, Chrome OS, Fuchsia), not to provide a truly platform-neutral abstraction layer. Qt's independence—its willingness to support QNX, VxWorks, INTEGRITY, bare-metal RTOS, and every other embedded OS alongside Linux and Android—is a feature that platform-aligned competitors cannot credibly match.

Now let us turn to the competitive threats, where the picture becomes more nuanced.

Threat of Substitutes: The Flutter and Android Question

The most significant competitive threat Qt faces is Google Flutter, an open-source UI framework that has been gaining traction in automotive infotainment. Toyota, BMW, and Sony have announced Flutter adoption for various in-vehicle applications. Flutter offers rapid cross-platform development with an appealing hot-reload development experience and a growing developer community. For pure infotainment applications—media playback, navigation, app stores—where safety certification is not required, Flutter is a credible alternative.

However, Flutter's weakness is precisely where Qt's strength is greatest: safety-critical embedded systems. Flutter runs on the Dart virtual machine, which introduces non-deterministic garbage collection pauses—unacceptable for instrument clusters that must update at a guaranteed frame rate, or medical devices that must respond within strict timing constraints. Qt's C++ foundation provides deterministic performance and direct hardware access, which is why it dominates in instrument clusters, heads-up displays, ADAS interfaces, and medical device UIs where regulatory certification is required.

Android Automotive OS represents a different kind of competitive pressure. Major OEMs including Volvo, GM, and Renault have adopted AAOS for their infotainment systems, effectively ceding that software layer to Google. But here Qt plays a subtle game: Qt can run on top of Android as a UI layer, so AAOS adoption does not necessarily exclude Qt. Many vehicles use AAOS for the infotainment screen and Qt for the instrument cluster and other safety-critical displays. The relationship is more complementary than purely competitive.

HTML5 and web-based approaches are a persistent low-end threat. For simple interfaces—think a thermostat with a basic menu or a washing machine with cycle selection—a web-based UI running on a lightweight browser engine may be "good enough" at lower cost. This matters more at the low end of the device spectrum, which is exactly where Qt for MCUs is trying to compete.

Bargaining Power of Buyers

Qt's largest customers—Volkswagen, General Motors, Mercedes-Benz, Hyundai—are among the most powerful procurement organizations in the world. In theory, they should be able to squeeze Qt on pricing. In practice, the royalty model mitigates this. A few dollars per vehicle is a rounding error on a forty-thousand-dollar car, and attempting to negotiate that royalty down by fifty percent would save the OEM perhaps a dollar or two per unit—not worth the engineering risk of alienating a critical software supplier or, worse, triggering a framework switch.

That said, Qt's 2025 results revealed that large customers were exercising leverage in a different way: by shortening contract terms from three-year agreements to one-year agreements, and by deferring large multi-million-euro deals. This is the kind of buyer power that manifests not as price pressure but as timing pressure, and it contributed materially to Qt's growth slowdown from sixteen percent in 2024 to three and a half percent in 2025.

Threat of New Entrants

The barrier to entry in cross-platform embedded UI frameworks is high but not insurmountable. Slint, a Rust-based embedded UI toolkit, has emerged as a credible new entrant targeting the MCU and small-device market with a modern language and a clean API. LVGL, an open-source C-based graphics library, is widely used in cost-sensitive embedded applications. Crank Storyboard and others compete in specific niches. None of these currently match Qt's breadth, maturity, or enterprise support infrastructure, but they represent a long-tail of competition that prevents Qt from being truly monopolistic.

Industry Rivalry

The embedded UI framework market is relatively consolidated at the high end, with Qt as the clear leader for complex, safety-critical applications. But the broader market for "things that put pixels on screens" is intensely competitive, ranging from Big Tech platforms (Android, Apple) at the top to open-source libraries at the bottom. Qt's strategic position is strongest in the middle ground: devices that are too complex for a simple open-source library but too specialized for a generic mobile OS.

VII. The Playbook: Business and Investing Lessons

Lesson One: The "Orphan" Opportunity

Qt's journey from Nokia castoff to independent public company is a textbook case of what value investors call the "orphan opportunity"—a high-quality asset hidden inside a distressed or distracted parent, available at a fraction of its intrinsic value because the market is focused on the parent's problems rather than the subsidiary's potential.

When Digia acquired Qt from Nokia in 2012 for what appears to have been single-digit millions of euros, the investment community was not paying attention. Nokia was a slow-motion train wreck, shedding assets and employees as its smartphone business collapsed. Qt was a niche developer tool with an uncertain future. Nobody outside a small circle of Finnish investors and embedded systems engineers understood what Digia had bought.

The lesson is not just "buy distressed assets cheap"—it is that the best orphan opportunities arise when the parent's failure narrative is so overwhelming that the market cannot see the subsidiary's independent value proposition. Nokia's failure was in smartphones. Qt's opportunity was in everything except smartphones. The market's inability to separate those two narratives created the pricing anomaly that made the entire subsequent value creation possible.

Lesson Two: Monetizing the Runtime

Selling developer tools is a good business. Getting a royalty on every unit your customer ships is a great business. The distinction between Qt's seat-based license and its distribution royalty is the distinction between linear scaling and exponential scaling. A seat license grows with the customer's engineering team. A distribution royalty grows with the customer's production volume. In a world where the number of connected devices is expanding by billions per year—from cars to appliances to medical devices to industrial equipment—the distribution royalty model positions Qt to capture value from the entire embedded computing megatrend without needing to proportionally scale its own headcount or infrastructure.

The analog in other industries is instructive. ARM Holdings does not manufacture chips; it licenses chip designs and collects a royalty on every chip shipped by its licensees. Qualcomm collects patent royalties on every smartphone sold, regardless of whose modem is inside. Dolby collects a fee on every device that supports Dolby audio or video formats. Qt's distribution model is the same basic architecture: become an essential but low-cost ingredient in a high-volume product, and collect a small toll on every unit. The magic is in the multiplier effect: small per-unit fees multiplied by millions of units produce large revenue streams with near-zero marginal cost.

Lesson Three: The Power of Focus

After the Nokia debacle, Qt could have tried to compete in mobile development against iOS and Android. Some inside the company probably wanted to. Instead, under Varelius's leadership, Qt abandoned the mobile battlefield entirely and focused all its energy on the embedded and desktop markets where it had structural advantages: performance, cross-platform breadth, real-time capabilities, and deep hardware integration.

This is the "blue ocean" move that business strategists talk about but companies rarely execute cleanly. The mobile market was a red ocean—dominated by two platform giants with virtually unlimited resources. The embedded market was a blue ocean—fragmented, underserved, and growing rapidly as the physical world became digitized. By accepting the loss of mobile and focusing on embedded, Qt avoided a war it could not win and dominated a market its competitors were ignoring.

The Bull Case

The optimistic thesis for Qt Group rests on three pillars. First, the Software-Defined Vehicle revolution is still in its early innings. The average car today has multiple screens and is trending toward more—instrument clusters, central infotainment displays, rear-seat entertainment, heads-up displays, mirror replacements. Each screen is a potential Qt deployment. And as vehicles become software-defined platforms with over-the-air updates, the software layer becomes more valuable over the vehicle's lifetime, not less.

Second, the Smart Home and Smart Appliance market is enormous and barely penetrated. Today's dishwasher has physical buttons; tomorrow's will have a touchscreen. Today's HVAC system has a basic thermostat; tomorrow's will have a full graphical interface with scheduling, energy monitoring, and remote control. Qt for MCUs positions the company to capture this transition at the low end of the cost curve.

Third, the IAR acquisition gives Qt a potential stranglehold on the MCU development toolchain—from compiler to UI framework—in the fastest-growing segment of the embedded market. If the integration succeeds and the subscription transition proceeds smoothly, Qt could emerge with a significantly larger addressable market and a more deeply embedded position in the MCU ecosystem.

The bull case for Qt's stock specifically is bolstered by valuation: at roughly four hundred seventy million euros in market cap, the stock trades at less than a quarter of its 2021 peak, despite the business being significantly larger and more diversified. If growth re-accelerates—which management's 2026 guidance of "at least ten percent" at comparable currencies suggests is possible—the current valuation could prove to be a significant entry point.

The Bear Case

The pessimistic thesis has teeth as well. The most immediate concern is growth deceleration. Qt's revenue growth slowed from fifty-two percent in 2021 to sixteen percent in 2022 and 2024, and then to just three and a half percent in 2025. Management attributed the slowdown to macroeconomic uncertainty causing customers to defer large deals and shorten contract terms, but the question investors must ask is whether this is cyclical (temporary) or structural (permanent). If customers are finding that they need less Qt—because cheaper alternatives are good enough for their use cases, or because they are insourcing UI development—then the growth engine may not restart even when the macro environment improves.

The Flutter threat, while manageable today, is worth monitoring carefully. Google has deep resources and a strong developer community. If Flutter matures enough to handle safety-critical applications—perhaps through compilation to native code rather than running on the Dart VM—it could erode Qt's competitive moat in automotive and medical, the two highest-value verticals. This is not imminent, but it is not impossible over a five-to-ten-year horizon.

The IAR acquisition introduces meaningful execution risk. At two hundred four million euros, it is a bet-the-company scale deal for a firm with a market cap of under five hundred million. IAR is in the middle of a business model transition from perpetual to subscription licensing, which historically compresses revenue and margins before eventually expanding them. If the integration is bumpy—cultural clashes, customer attrition, technology integration delays—it could weigh on Qt's financials for several years.

There is also the "low-code" and "AI-generated UI" wildcard. If large language models become capable of generating high-quality embedded user interfaces from natural language descriptions, the value of a hand-crafted UI framework could diminish over time. This is speculative, but it is the kind of paradigm shift that could disrupt Qt's core value proposition in ways that are difficult to predict.

Finally, concentration risk deserves attention. Qt Group does not disclose individual customer revenue breakdowns, but the automotive industry is clearly the largest vertical. A prolonged downturn in global auto production—whether from trade disruptions, economic recession, or the transition complications between ICE and EV platforms—would directly impact Qt's distribution royalty revenue. The 2025 slowdown may have been partly attributable to exactly this kind of industry-level softness.

A brief note on financial health: Qt Group's balance sheet absorbed a significant expansion with the IAR acquisition, and the company's 2026 margin guidance reflects integration costs. Investors should monitor the pace of IAR's subscription transition and the combined company's free cash flow generation closely. There are no disclosed going-concern risks or auditor flags, but the step-up in financial leverage and operational complexity from the IAR deal is material.

VIII. Epilogue: The Future of the Screen

In February 2026, Qt Group published its full-year 2025 results. The headline numbers told a mixed story: net sales of two hundred sixteen million euros, up just three and a half percent year-over-year in reported terms, or six and a half percent at comparable exchange rates. EBIT was forty-two and a half million euros, representing a margin of nearly twenty percent—solid, but down from the thirty-four percent EBITA margin achieved in 2024, reflecting investment in the IAR integration and a revenue base that did not grow as fast as the cost structure. The fourth quarter, however, offered a glimmer of optimism: revenues of seventy-seven million euros, up nearly thirteen percent, with EBIT margins above thirty-one percent. The company's guidance for 2026 calls for at least ten percent revenue growth at comparable currencies and an EBITA margin of at least fifteen percent, with the margin compression reflecting IAR integration costs.

The stock market has rendered its verdict on the growth slowdown: at around twenty euros per share, Qt Group trades at roughly eleven percent of its October 2021 all-time high of approximately one hundred eighty euros. The decline reflects the multiple contraction that inevitably follows when a high-growth software company's growth rate decelerates by eighty percent (from fifty-two percent to three and a half percent in four years). Whether the current price represents a value trap or a generational buying opportunity depends entirely on whether growth re-accelerates—and the IAR acquisition, for all its risks, is management's clearest bet that it will.

What has not changed through all the stock price volatility is Qt's structural position in the embedded computing ecosystem. The world is not getting fewer screens. Cars are not going back to analog dials. Medical devices are not reverting to seven-segment LED displays. Factory equipment is not returning to physical toggle switches. The secular trend toward rich graphical interfaces on physical devices is decades-long and, if anything, accelerating as display costs decline and consumer expectations for "smartphone-like" experiences extend to every product category.

Qt is the C++ tax on the physical world. As long as things have screens and those screens need to be reliable, responsive, and deployed across multiple hardware platforms, Qt occupies a privileged position in the value chain. It is the toll booth between the silicon and the pixel, collecting a small fee on every device that passes through. The fee is small enough that most customers never seriously consider eliminating it, but large enough in aggregate to build a profitable, high-margin software business.

The question is not whether Qt's technology matters—it clearly does. The question is whether Juha Varelius and his team can navigate the IAR integration, reignite growth in the core business, and defend the competitive moat against Flutter, AAOS, and whatever AI-powered development tools emerge in the next decade. The next twelve to eighteen months—as the IAR subscription transition unfolds and the macroeconomic environment evolves—will be telling.

For investors watching from the sidelines, two numbers will tell the story going forward. First, the distribution-to-development revenue mix: a rising share of distribution (royalty) revenue signals that Qt is being designed into more devices, which is the leading indicator of long-term value creation. Second, ARPA (average revenue per account) across the enterprise customer base: rising ARPA means the QA tools, MCU offerings, and IAR products are successfully cross-selling into existing relationships, which is the mechanism by which Qt's bolt-on acquisitions either justify their price tags or do not.

Thirty-two years after two Norwegian students started building a toolkit on a park bench in Trondheim, the software they created touches more human lives than almost any other piece of code that does not have a consumer brand. It runs the screens in operating rooms, in cockpits at thirty thousand feet, in cars on every continent, and increasingly in the everyday appliances that populate kitchens and living rooms. It survived Nokia's collapse, thrived under Finnish reinvention, and now faces its next test: proving that the growth story still has chapters left to write.

IX. Top 5 Recommended Links for Further Research

-

Qt Group Investor Relations (qt.io/investors) — The Capital Markets Day presentations are essential reading for understanding the royalty model mechanics and management's long-term targets. The 2025 Financial Statements Bulletin published in February 2026 provides the most current financial picture.

-

Stephen Elop's "Burning Platform" Memo — The full text, originally leaked to Engadget on February 8, 2011, remains one of the most instructive documents in tech strategy. Understanding what happened at Nokia is essential context for appreciating the improbability of Qt's survival and the significance of the Digia acquisition.

-

Juha Varelius Interviews in Kauppalehti — Finland's leading business newspaper has conducted several in-depth interviews with Varelius over the years, particularly around the 2016 spin-off and the licensing model changes. These provide insight into his "efficiency-first" management philosophy and long-term strategic vision. Available in Finnish with translation.

-

Qt for Automotive Technical Whitepapers (qt.io) — These documents explain the Tier 1 supplier relationships, the safety certification pathway (ISO 26262), and how Qt integrates with automotive-grade operating systems like QNX, INTEGRITY, and Automotive Grade Linux. Essential for understanding why switching costs are so high in the automotive vertical.

-

IAR Systems Acquisition Documentation — The offer document and Qt Group's strategic rationale presentation from July 2025 detail the MCU development toolchain thesis and the expected synergies. This is the deal that will define Qt Group's next chapter, and the primary documents are worth reading carefully for anyone evaluating the company's forward trajectory.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube