PUMA SE: Speed, Style, and the Shadow of Herzogenaurach

I. Introduction: The Cat That Crossed the River

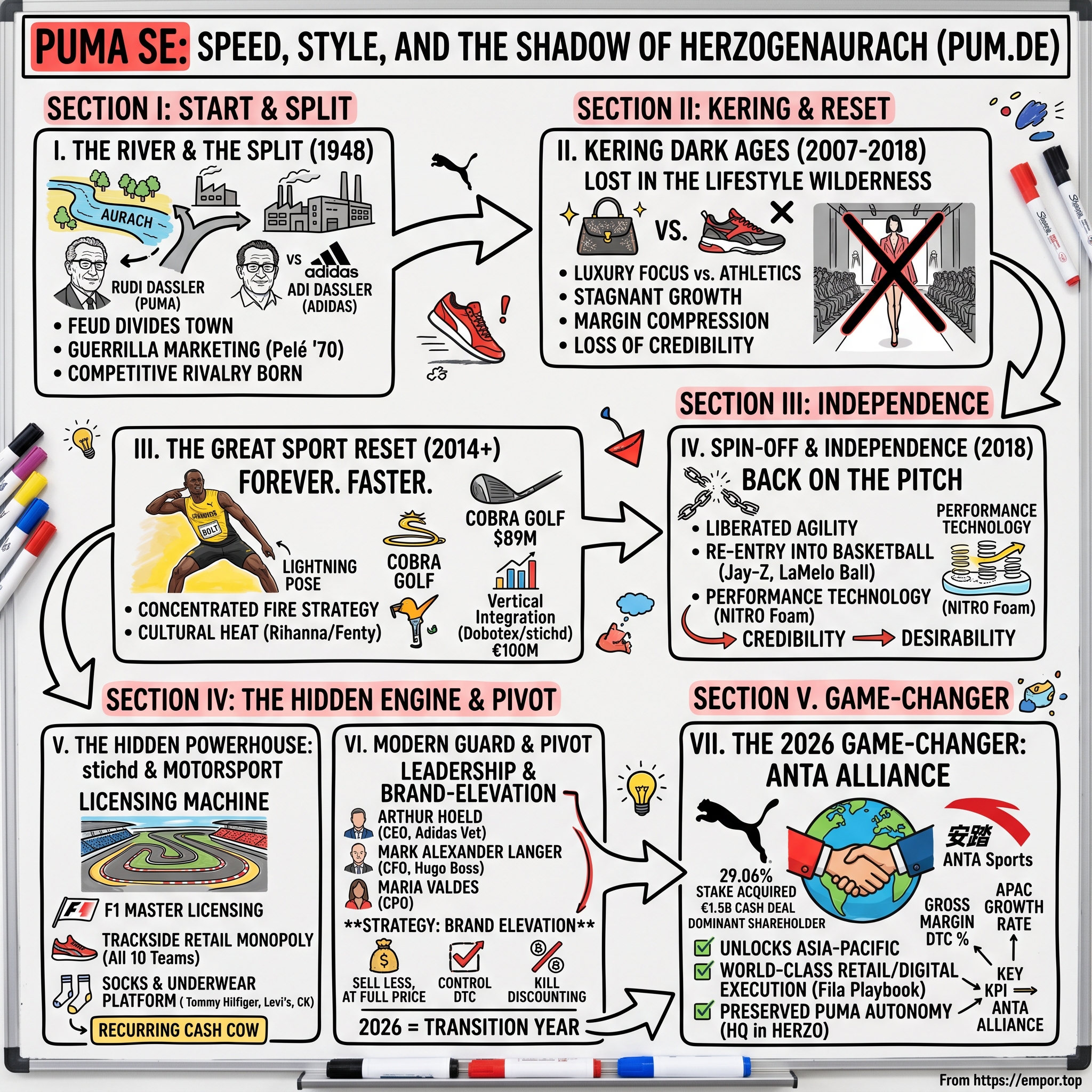

There is a small river in Bavaria called the Aurach. It is barely wide enough to deserve the name — in places you could throw a stone across it — and it winds, unremarkably, through a Franconian town of around 24,000 people called Herzogenaurach. For most of human history nothing of global consequence happened there. And then, almost eighty years ago, two brothers had a falling out so bitter that it permanently split a town, seeded two of the largest sportswear companies on Earth, and turned a sleepy farming community into the single most concentrated cluster of athletic-footwear talent, espionage, and ego anywhere in the world.

One of those companies is Adidas. The other is the subject of today's story: PUMA SE, which trades in Frankfurt under the ticker PUM.DE on Deutsche Börse's XETRA platform.1 By 2024 PUMA had grown into a roughly €8.8 billion-revenue global sportswear house, with a leaping-cat logo that ranks among the most recognized marks in existence — stamped on the boots of footballers, the suits of Formula 1 drivers, and the sneakers of teenagers from São Paulo to Shanghai.2

And yet, for a company of that scale and that brand recognition, PUMA has spent most of its modern life fighting a war on multiple fronts at once. It has fought to escape the gravitational pull of its larger sibling across the river. It endured a decade as the neglected, misunderstood stepchild inside a French luxury empire that wanted it to behave like a fashion house rather than an athletics company. It then engineered an escape, re-listed itself as an independent and transparent public company, and rebuilt its credibility on the pitch and the track. The leaping cat learned to run again.

The story we are telling has a dramatic, fresh twist — one that was still unfolding as of mid-2026. In the space of roughly a year, PUMA absorbed three seismic shocks at once. The first was a sweeping leadership overhaul that put a 25-year Adidas veteran in the CEO chair. The second was a hard strategic reset away from cheap, discounted volume toward what management calls "brand elevation." And the third — the most consequential of all — was the arrival of a new anchor shareholder from China: 安踏体育 ANTA Sports, which in January 2026 agreed to buy a 29.06% stake in PUMA from the Pinault family's Groupe Artémis for €1.5 billion in cash.3

That single transaction reframes everything. It hands PUMA a strategic partner with arguably the best retail and digital execution playbook in the global sporting-goods industry — and it does so in precisely the region where PUMA has always been weakest.

Across this episode we are going to chase four themes. First, how geographic determinism — a single river, a single town — created and still fuels a multi-billion-dollar corporate rivalry. Second, the financial beauty of "invisible" businesses: the unglamorous, high-velocity world of socks, underwear, and motorsport fanwear that quietly generates some of PUMA's most reliable cash. Third, a genuine capital-allocation masterclass in buying assets at the bottom of the market for almost nothing and turning them into profitable franchises. And fourth, the permanent, unresolvable tension at the heart of this entire industry — the war between athletic high performance and cultural lifestyle desirability, a tension PUMA has spent its whole life trying to straddle.

It helps to frame the playing field first, because the sporting-goods industry is one of the strangest in all of consumer business. It looks, from the outside, like a fashion business — fast-moving trends, seasonal drops, celebrity faces. But its economic engine is closer to a technology business fused with a sports-marketing operation. Brands spend hundreds of millions of dollars a year securing the feet and torsos of the world's best athletes, then spend hundreds of millions more on the research that lets those athletes run faster and jump higher, and then — only then — do they monetize the resulting credibility by selling lifestyle product to ordinary people who will never run a sub-ten-second hundred meters but want to feel a little of that magic. The brand that wins is the one that can sustain that whole loop — pay for the credibility, fund the technology, and convert both into desirability at the cash register — across decades. Nike has been the undisputed champion of that loop for forty years. Adidas has been the eternal number two. And PUMA, for most of its modern life, has been fighting to hold a clear and profitable number three against a swarm of challengers nipping at its heels.

What makes PUMA worth a deep dive, rather than a footnote in the Nike-Adidas duopoly story, is that its path to that number-three position has been anything but linear, and the strategic choices it has been forced to make — precisely because it lacks the resources of the two giants — are unusually instructive. A company that cannot out-spend its rivals must out-think them. That constraint is the mother of everything interesting about PUMA: the bargain-basement acquisitions, the hidden licensing engines, the willingness to bet on culture before the competition did, and now the decision to hand a chunk of its equity to the one outside partner that can give it something money alone could not buy. To see how those choices were forged, you have to start at the river.

II. The Split: A Town Divided by a River

Picture Herzogenaurach in the years after the Second World War. It is a town of cobbled streets and timber-framed houses, and its economy increasingly revolves around one thing: shoes. Specifically, the shoes coming out of a company called Gebrüder Dassler Schuhfabrik — the Dassler Brothers Shoe Factory — founded in the 1920s by two siblings with complementary gifts. Adolf, universally known as "Adi," was the craftsman, the obsessive tinkerer who cared about the shoe itself, the stitching, the spikes, the fit. Rudolf, known as "Rudi," was the salesman, the gregarious dealmaker who could move product.

For a while the partnership worked spectacularly. Dassler spikes were on the feet of Jesse Owens at the 1936 Berlin Olympics — an extraordinary early proof that the right shoe on the right athlete could become a marketing weapon. But the brothers' relationship curdled. The exact origin of the feud is the stuff of local legend — a mix of wartime tension, a misunderstood remark during an air raid, accusations of disloyalty, and the simple fact that two strong-willed men with opposite temperaments could not share one company. Whatever the true trigger, by 1948 the partnership was beyond repair.

So they split. Adi took the craftsman's half and founded what he called Adidas, a contraction of his own name. Rudi took the sales half, set up shop on the other side of the River Aurach, and founded a company he initially called Ruda before quickly rebranding it with a punchier, more athletic name: PUMA. The town divided with them. Workers, suppliers, even families chose sides. For decades, Herzogenaurach was known as "the town of bent necks," because locals would reflexively glance down at a stranger's shoes to see which brother's brand they wore before deciding whether to talk to them.

The division was total and, to outsiders, almost absurd in its completeness. The two firms reportedly drank at different pubs, the town had two football clubs, and intermarriage between an Adidas family and a PUMA family carried the faint scandal of crossing enemy lines. The brothers themselves never reconciled; they are buried at opposite ends of the same Herzogenaurach cemetery, as far apart in death as the layout would allow. It would be tempting to dismiss all of this as colorful folklore — except that the rivalry it created became one of the great competitive engines in business history. The two companies pushed each other relentlessly. They competed for every Olympic federation, every World Cup squad, every superstar athlete, and in doing so they more or less invented the modern practice of athlete endorsement, the practice of paying for credibility that now defines the entire industry. The most famous early skirmish came at the 1970 World Cup, when both companies fought over the most marketable footballer on Earth, Pelé. The story — part legend, part fact — is that the two sides reached a quiet truce not to bid against each other for him, only for PUMA to break ranks and pay Pelé to lace up his boots on camera moments before kickoff, ensuring the world's cameras caught the leaping cat. It was guerrilla marketing decades before the term existed, and it captured the PUMA temperament: scrappier, cheekier, and more willing to break the rules than its larger sibling.

Now, why does an eighty-year-old family quarrel matter to an investor evaluating PUMA in 2026? Because the consequences are structural, not sentimental. Both giants are still headquartered in the same small town, separated by that same little river. This produces a genuinely unique localized ecosystem — a dense, shared pool of footwear engineers, designers, pattern-makers, and supply-chain specialists who circulate between the two campuses across their entire careers. Talent poaching is not an occasional event; it is the ambient condition. The rivalry is not a marketing narrative cooked up for press releases — it is woven into the recruiting market, the local culture, and the competitive psychology of both firms.

There is a second dimension to the geography that matters even more for an investor than the folklore: the talent ecosystem. Because both companies sit in the same town, drawing from the same regional universities and the same generations of footwear engineers, the labor market in Herzogenaurach is effectively a single shared pool with two employers. A designer who learns her craft at Adidas may spend the back half of her career at PUMA, and vice versa. Suppliers, logistics specialists, and pattern-makers circulate constantly. This produces a strange and powerful effect: the two companies are simultaneously fierce rivals and a joint training academy for the entire global industry's talent. It also means the rivalry is personal in a way that transcends quarterly results. People who work at PUMA often grew up watching Adidas win, or had a parent who worked across the river, or were passed over for a job there. The competitive fire is not manufactured by the marketing department; it is ambient in the air of the town.

The most poetic possible illustration of all this arrived on July 1, 2025, when PUMA's new chief executive officer formally took the helm. His name is Arthur Hoeld, and he is a legendary Adidas veteran — a man who had spent roughly a quarter-century inside the three-stripes machine, including a senior role driving its global sales and commercial strategy, before stepping across to lead the cat.[^4] To run PUMA, he physically crossed the River Aurach. A senior leader leaving one bank of the river to command the company on the other is the corporate equivalent of a defection, and it tells you everything about how alive this rivalry remains. It also tells you something shrewd about PUMA's supervisory board: when you want to beat the company across the river, there is real value in hiring someone who spent twenty-five years learning exactly how it thinks, where its blind spots are, and which of its customers and accounts are vulnerable. The river is narrow. The gulf it represents is not — and PUMA just recruited a guide who knows the far bank intimately.

That town, and that rivalry, are the permanent backdrop. But PUMA's most painful modern chapter did not unfold in Herzogenaurach at all. It unfolded in Paris.

III. The Kering Dark Ages: Lost in the Lifestyle Wilderness

To understand why the Kering years stung so badly, you have to understand what PUMA was before them. Through the 1990s, the company had nearly died — bloated, unfocused, and bleeding money, a once-great name reduced to a discount-bin afterthought. Its rescue was one of the great turnaround stories of European business, engineered by a young executive named Jochen Zeitz, who became one of the youngest CEOs of a public German company when he took the top job in 1993 at just thirty. Zeitz did something genuinely original: rather than try to out-Nike Nike on pure performance, he repositioned PUMA at the intersection of sport and fashion — "sport-lifestyle" as a deliberate category — courting designers, doing collaborations, and turning the leaping cat into a streetwear and style object years before that fusion became industry gospel. By the mid-2000s, PUMA was one of the hottest, most profitable, and most admired brands in the sector. It was precisely because Zeitz had made PUMA so desirable that it caught the eye of a luxury buyer in the first place. The tragedy of what followed is that the buyer fell in love with the fashion veneer and never understood the athletic substance underneath it.

In 2007, a French luxury titan came shopping. The buyer was PPR — Pinault-Printemps-Redoute, the conglomerate later renamed Kering — controlled by the billionaire François-Henri Pinault, scion of one of France's great fortunes and the man who would go on to turn Gucci, Saint Laurent, and Bottega Veneta into a luxury powerhouse. PPR's thesis was bold and, on paper, fashionable: build a pioneering "Sport & Lifestyle" division, with PUMA as its anchor, that would sit alongside the group's hard-luxury houses and capture the booming intersection of athletics and style. The intellectual error embedded in that thesis was subtle but fatal — it assumed that PUMA's appeal was fundamentally a fashion phenomenon that could be managed with fashion-industry tools, when in fact PUMA's appeal rested on a foundation of athletic credibility that fashion alone could not sustain.

The price was serious money. PPR first acquired a 27.1% controlling stake in 2007 for roughly €5.3 billion, then launched a tender offer that pushed its holding above 60%.4 In one stroke, the leaping cat — a German athletics brand born from a shoemaker's feud — became a possession of the Parisian luxury establishment. The logic was that the same merchandising magic that made a Gucci handbag desirable could be sprinkled onto a sneaker.

It did not work. And the way it did not work is the instructive part. Kering, by instinct and DNA, treated PUMA like a fashion house. The center of gravity shifted toward high-fashion runway collaborations, lifestyle footwear, and fashion-forward apparel — the glamorous, image-driven end of the catalogue. Meanwhile, the parts of PUMA that made it a credible athletics company — research and development, high-performance running, the unglamorous grind of team sports and football boots — were systematically starved of capital and attention. In a business where credibility is earned on the pitch and the track and only then monetized in the mall, this was precisely backward.

The financial consequences showed up exactly where you'd expect. Top-line growth stagnated. Operating margins, which had been healthy when PPR bought in, compressed badly as the brand drifted and discounting crept in. But the deeper damage was to something that doesn't appear cleanly on an income statement: athletic credibility. PUMA found itself stranded in the worst possible position in all of consumer goods — the dreaded middle. It was not premium enough to command luxury-grade pricing power and margins the way an actual fashion house could. And it was no longer high-performance enough to go toe-to-toe with Nike or Adidas where games are won and athletes are signed. It was a sport brand that had forgotten how to be a sport brand, owned by people who didn't really want it to be one.

There is a deeper structural reason the mismatch was so corrosive, and it's worth dwelling on because it explains the entire shape of the later turnaround. A luxury house and a performance-sports company run on opposite clocks. Luxury rewards scarcity, heritage, and the deliberate restriction of supply — a Hermès handbag is more desirable precisely because you cannot easily get one. Performance sport rewards ubiquity and relevance — you win by being on the most feet, the most pitches, the most magazine covers, and by relentlessly out-innovating on technology that is, by its nature, quickly copied and commoditized. Apply luxury patience to a sport brand and you under-invest in the fast, expensive innovation cycle that keeps you credible. Apply sport-style volume to a luxury brand and you destroy the scarcity that justifies the price. Kering, staffed and led by people whose instincts were honed on the luxury clock, simply could not bring itself to spend on the unglamorous, fast-depreciating machinery of athletic R&D and grassroots team-sport sponsorship. So that machinery rusted.

This is the part of the story long-term investors should sit with, because it is a clean case study in how a good asset can be quietly degraded by a strategically mismatched owner. There was nothing wrong with PUMA's brand equity or its heritage. What was wrong was the operating model imposed on it — a luxury-first mindset, layered with conglomerate overhead, applied to a business whose entire moat depends on performance authenticity. The lesson generalizes: when evaluating any subsidiary inside a conglomerate, the question isn't just "is the brand good?" It's "does the parent understand what actually drives this business, and is it willing to fund that, even when it's unglamorous?" For PUMA inside Kering for the better part of a decade, the answer was no. Keep that question in your back pocket, because in 2026 PUMA acquired a new dominant shareholder, and the single most important thing to assess about that shareholder is whether it understands what actually drives this business. The contrast between Kering and ANTA on that exact dimension is the throughline of the entire investment case.

The turnaround, when it came, started not in the boardroom in Paris but on a running track — with the fastest man who has ever lived.

IV. The Great Sport Reset and the High-Yield M&A Bargains

If you want to pinpoint the moment PUMA remembered what it was, look at Usain Bolt with his arms spread wide in the "lightning bolt" pose, draped in PUMA from head to toe. Bolt was PUMA's defining athlete through the late 2000s and 2010s — a sprinter so dominant that he turned the 100 meters into a global event and made his sponsor's logo synonymous with raw, joyful speed. He was the human embodiment of the brand's rallying cry, the now-iconic tagline that would anchor the entire reset: "Forever. Faster."

That campaign was more than advertising. It was a strategic declaration of identity. "Forever. Faster." said, in three words, that PUMA was going to compete on athletic speed and agility — both literally, in the products and the athletes, and figuratively, in how fast the company moved through product cycles versus its lumbering rivals. After years of fashion drift, PUMA was planting a flag back on the performance side of the line.

The Bolt relationship is worth understanding as a piece of strategy, not just a sponsorship line item. For a brand that could not out-spend Nike and Adidas across every sport, the smarter play was concentration: rather than scatter a limited marketing budget thinly across dozens of athletes, anchor it on one transcendent, globally beloved figure whose dominance was so total that he became a walking billboard at every Olympics and World Championships for the better part of a decade. Bolt didn't just win; he won with charisma and joy, mugging for the cameras in his lightning-bolt pose with the leaping cat on his chest, generating billions of impressions of earned media that PUMA could never have afforded to buy outright. It was the Pelé playbook from 1970 updated for the broadcast age — find the single most magnetic athlete on the planet and make him synonymous with your logo. That is how a number-three brand competes: not by matching the giants dollar for dollar, but by concentrating fire on the highest-leverage targets.

But here is the genuinely clever bit, and it's where PUMA's strategy gets more sophisticated than a simple "back to sports" story. The company didn't abandon lifestyle and culture. It learned to do it correctly. The pivotal proof point came in 2014 with the signing of Rihanna, who became creative director of the Fenty PUMA line. The distinction that mattered was this: Rihanna wasn't a celebrity renting her face to a logo. She co-created a genuine product ecosystem — the Creeper sneaker became a sell-out cultural phenomenon. The insight was that lifestyle, done as authentic co-creation rather than as a cheap licensing veneer, could serve performance credibility instead of diluting it. Cultural heat and athletic authenticity didn't have to be enemies; if you cast the talent right and let them build, they could compound.

While the brand was getting its swagger back, something quieter and arguably more important for shareholders was happening on the balance sheet. PUMA was executing a series of disciplined, bottom-of-the-market acquisitions that built profitable auxiliary businesses for almost no money and almost no downside. Two deals define the playbook.

The first was Cobra Golf. In 2010, PUMA acquired the golf-equipment brand outright from Acushnet, the golf division of Fortune Brands.5 PUMA did not officially disclose the purchase price, but the figure widely reported in the trade and financial press was roughly $89 million — a striking number when you look at the history. Acushnet had paid an estimated $712 million to acquire Cobra back in 1996. So PUMA was stepping in to buy the brand for a small fraction of what it had cost a prior owner, after years of value destruction had done the heavy lifting on the price. Buying a recognizable brand at a fraction of revenue and a near-trivial multiple of cash earnings, after someone else has eaten the impairment, is about as close to a free option as M&A offers.

The strategic genius wasn't just the price — it was the contrast with the rival across the river. Adidas had spent big to build out TaylorMade in golf, and it eventually found itself stuck: the golf business became a drag, and Adidas offloaded TaylorMade to private-equity firm KPS in 2017 for a reported $425 million, a sale that capped years of struggle to make the category work at the price it had paid. PUMA, by contrast, had bought in so cheaply that it could afford to be patient and creative. It built Cobra PUMA Golf, and rather than chasing the traditional country-club golfer, it deliberately aimed at a younger, more lifestyle-oriented demographic through charismatic players like Rickie Fowler and, later, the analytics-obsessed bomber Bryson DeChambeau. The category never had to be a home run, because the entry cost was so low that it almost couldn't be a loss. That is what disciplined, counter-cyclical capital allocation looks like.

The deeper lesson of Cobra is a principle every disciplined capital allocator eventually learns: in M&A, the price you pay at entry determines the bulk of your return, far more than the operational brilliance you bring afterward. Adidas's TaylorMade experience and PUMA's Cobra experience were not really a contest of operators — they were a contest of entry prices. One side bought near the top and spent years trying to operate its way out of an overpayment; the other side bought near the bottom and was free to experiment, because even a mediocre outcome would be acceptable against an $89 million cost basis. When you buy an asset for roughly one times its cash earnings, you have purchased an enormous margin of safety. PUMA used that safety to do something creative — repositioning a stodgy equipment brand toward a younger, style-conscious golfer at the exact moment golf was trying to shed its country-club stuffiness — but the creativity was a bonus on top of a structurally great deal, not a rescue of a bad one.

The second deal was even more important to the long-term cash machine, even though it generated zero headlines. Between 2009 and 2012, PUMA acquired Dobotex, its primary licensee for socks and bodywear, in a phased transaction — first a majority 50.1% stake in 2009, then the remaining 49.9% in 2012 — for a total estimated investment in the order of €100 million. To understand why this mattered, you have to understand what a licensee is: it's the company that pays you a royalty to make and sell your branded socks and underwear, and pockets the difference. By buying its own licensee, PUMA stopped paying away the margin and instead captured the entire economics — wholesale and retail — of a category defined by high turnover and steady, repeat demand. Socks and underwear aren't glamorous, but people buy them constantly and rarely on deep discount. That business would grow into PUMA's most dependable recurring cash generator, and in 2019 it was rebranded under a name that will recur throughout the rest of this story: stichd.

What ties the Cobra and Dobotex deals together is a coherent philosophy that contrasts sharply with the empire-building instincts of larger rivals. PUMA, constrained by a smaller balance sheet and a tighter budget, learned to do M&A the way a value investor does it: buy cheap, buy assets with durable demand characteristics, integrate them quietly, and let the economics compound rather than chasing splashy, transformational deals that look good in a press release and bad on the return-on-invested-capital line three years later. Vertical integration into your own licensee, in particular, is one of the most reliable value-creating moves in consumer goods — you are buying a margin stream you were already generating but giving away, at a price set by a seller who doesn't fully appreciate what it's worth inside your house. It rarely makes headlines. It almost always makes money.

The reset had given PUMA back its identity and its cash engines. What it still didn't have was its freedom.

V. The Spin-Off and Independence: Back on the Pitch

By 2018, the experiment was over. After more than a decade, Kering quietly admitted that the luxury-meets-sport synergy thesis had not paid off, and that PUMA was a poor fit inside a company whose future was hard luxury — Gucci and Saint Laurent, not football boots and running spikes. Rather than sell PUMA outright to a single buyer, Kering chose an elegant exit: it distributed roughly 70% of PUMA's shares directly to its own shareholders, spinning the cat back out into the market as an independent, separately listed public company.6 (The Pinault family's holding company, Groupe Artémis, retained a meaningful anchor stake — a detail that will matter enormously in 2026.)

For PUMA, this was liberation. Overnight it became a transparent, agile, independently governed business again, no longer carrying conglomerate overhead or answering to a luxury-first parent that fundamentally misunderstood it. And freed from those constraints, PUMA started moving with exactly the velocity its tagline promised.

The clearest expression of the independent playbook was PUMA's dramatic re-entry into basketball in 2018 — a category it had essentially abandoned for decades. Basketball is the beating heart of American sneaker culture and the single most important battleground for the North American market, the one region where every global sportswear brand must eventually win. PUMA's move was characteristically bold: it brought in Jay-Z as creative director of its basketball division, instantly signaling cultural seriousness rather than a tentative toe in the water. It then signed generation-defining talent — most notably LaMelo Ball, a charismatic, social-media-native guard who became the face of PUMA Hoops and got his own signature shoe, and on the women's side, WNBA superstar Breanna Stewart. This was the Rihanna lesson applied to sport: pick culturally magnetic figures and build genuine product and storytelling around them, rather than simply buying logo placement.

There's a subtle financial logic to the basketball bet that's worth making explicit. North America is the market where PUMA has historically been weakest among the three big Western regions, and basketball is the single most efficient cultural lever for moving the needle there, because basketball footwear and the sneaker culture around it drive an outsized share of American youth brand preference. A relatively contained roster of the right signature athletes — a LaMelo Ball with his own shoe line and a massive social following — can generate brand heat far out of proportion to its cost, in a way that broad, undifferentiated advertising cannot. It is, once again, the concentrated-fire strategy of a challenger brand: find the highest-leverage cultural entry point and pour resources into it rather than spreading thin.

The other front was pure performance technology, and here PUMA had to answer a hard question: how do you reclaim credibility in elite running, the most technically demanding and prestige-laden category in the sport? The answer was foam. PUMA developed a proprietary cushioning technology it branded Nitro. For the non-engineer, here's the simple version: modern performance running shoes live or die on the foam in the midsole, the layer between your foot and the ground. Think of it like the suspension in a car — get it right and the ride feels effortless and responsive; get it wrong and every bump in the road jolts straight through to the driver. The holy grail is a midsole material that is simultaneously lightweight, springy (returning energy to the runner with each stride rather than absorbing it like a dead sponge), and durable enough to keep that springiness over hundreds of miles. The "nitro" in Nitro refers to the use of nitrogen gas injected into the foam to create that lightweight, energy-returning structure. It was PUMA's entry into an arms race that had been reset a few years earlier when Nike's plated, super-foam racing shoes rewrote what was physically possible in a marathon. Every serious brand suddenly needed its own answer, and a brand without a credible foam story was effectively conceding the most prestigious category in the sport.

Nitro mattered because elite running is where technical authenticity is manufactured. Win there — get your foam onto the feet of serious athletes running serious times — and the credibility cascades downhill into every casual jogger's purchase and every lifestyle shoe you sell at the mall. Lose there, and you slowly become a fashion brand that happens to make sneakers, which is exactly the fate PUMA had narrowly escaped under Kering. Reclaiming a defensible position in performance running was therefore not a vanity project; it was a defense of the entire brand's right to call itself an athletics company. The post-spin-off PUMA understood that its long-term pricing power depended on being genuinely good at sport, not merely looking the part.

For investors, the independence era is the hinge of the whole story. A spun-off company with no controlling strategic parent has nowhere to hide — its numbers are its own, its decisions are its own, and its successes and failures land directly on its own income statement. PUMA used that freedom to rebuild credibility across the two categories that matter most for long-term brand health: the cultural engine of basketball and the technical engine of elite running. But while those flashy, headline-grabbing categories were doing the work of brand-building, the company's most reliable profits were increasingly coming from a business almost no consumer has ever heard of.

VI. The Hidden Powerhouse: stichd, Formula 1, and the Licensing Machine

Let's start with the shape of the business, because the headline numbers reveal where the brand momentum lives — and where the quiet cash hides. In fiscal 2024, PUMA's sales broke down across three product divisions. Footwear was the giant and the brand-momentum generator at €4,733.6 million, or 53.7% of total sales — more than half the company, and the category where credibility is won. Apparel came next at €2,813.9 million, or 31.9%. And accessories, the smallest and least glamorous slice, contributed €1,269.7 million, or 14.4% of sales.7 That accessories line is easy to skip past. Don't — it is the quiet home of the hidden powerhouse.

There was also a structural shift worth flagging in the channel mix. Direct-to-consumer sales — PUMA's own stores and e-commerce, where it sells straight to the shopper rather than through a wholesale middleman — climbed to 27.5% of total sales, around €2,425.4 million in 2024.8 Why care? Because selling direct means PUMA captures the full retail margin instead of sharing it with a distributor, and it owns the customer relationship and the data. The steady migration toward DTC is one of the most important structural improvements in the entire model, and it directly enables the "brand elevation" strategy we'll come to shortly — you can't control how your brand is priced and presented if a wholesaler is doing it for you.

It's worth being precise about why the DTC mix is such a powerful lever, because it sits at the heart of both the bull case and the strategy. A wholesale sale is a sale of a product; a direct sale is a sale of a product plus control. When a third-party retailer buys PUMA product, that retailer decides where it sits on the shelf, what it's priced at, when it gets marked down, and what sits next to it. The brand surrenders the last and most important mile of the customer experience. Worse, when that retailer over-orders and needs to clear inventory, it discounts — and nothing erodes a premium positioning faster than a consumer learning to wait for the inevitable markdown. Direct channels flip all of that. PUMA sets the price, controls the presentation, sees exactly what's selling in real time (priceless data for inventory planning), and captures the retailer's margin for itself. The trade-off is that DTC requires capital and operational skill — stores cost money, e-commerce demands logistics and technology — which is precisely where a partner with world-class retail and digital execution would be enormously valuable. File that thought; it returns when ANTA arrives.

Now, stichd. Operating almost entirely behind the scenes, stichd is a cash-flowing engine built on two very different pillars, and together they make it one of the most interesting hidden assets in European consumer goods.

The first pillar is fashion essentials — the Dobotex inheritance, grown up. stichd designs, manufactures, and distributes socks, underwear, and swimwear. And here's the twist that makes it special: it doesn't only do this for PUMA. It runs the essentials business for a roster of major competitor brands too, including Tommy Hilfiger, Levi's, and Calvin Klein.9 Think about what that means. stichd has turned the unglamorous mechanics of essentials — design, sourcing, manufacturing, distribution — into a service it sells to rival fashion houses. It is, in effect, a specialist platform that happens to be owned by PUMA. Essentials are the definition of recurring, low-drama demand: high turnover, modest fashion risk, repeat purchase. It is exactly the kind of boring, dependable, high-velocity business that funds the expensive, risky glamour elsewhere in the group.

The second pillar is where it gets genuinely remarkable: motorsport fanwear. PUMA has long been dominant in racing — more on the depth of that dominance shortly — and stichd leveraged that position to win something extraordinary. In 2023, stichd became the Official Licensing Partner and Exclusive Trackside Retailer for Formula 1.[^11] PUMA and Formula 1 also entered a broader official partnership the same year.10 To grasp why this is a small monopoly, you have to picture a Grand Prix weekend. Tens of thousands of fans pour into a circuit. They want merchandise — team caps, driver shirts, jackets. And stichd controls the retail footprint that sells it to them. It operates up to 65 mobile stores across more than 20 races globally, and crucially, it sells merchandise for all ten teams on the grid — Ferrari, Mercedes-AMG, Red Bull, Aston Martin, and the rest. It is not betting on one team winning; it is the house, taking a cut of every fan's loyalty regardless of who's on the podium.

This is a beautiful business for reasons that go beyond the margins. Formula 1's global popularity has surged, supercharged by streaming-era storytelling that turned drivers into mainstream celebrities and pulled in a younger, broader, more global, and more female audience than the sport ever had before. stichd sits directly downstream of that boom, with an exclusive, contracted position at the physical point of sale. It is a cornered resource: you cannot replicate the exclusive trackside rights or the master licensing relationships by simply spending money, because the rights are already spoken for.

Consider the elegance of the "house" position one more time, because it is genuinely unusual. Most sponsorship money in sport is a bet — you back a team or an athlete and hope they win, because winners sell merchandise and losers don't. stichd's trackside retail position is structurally different: it sells the gear of every team to every fan, so it doesn't care who wins the championship. Whether the title goes to Ferrari's tifosi or to a resurgent Mercedes or to Red Bull, the fans still stream past stichd's stores and buy their tribe's colors. The business is hedged against the one variable — competitive results — that makes most sports merchandise so volatile. Layer on top of that the fact that this is a licensing-and-retail operation rather than a capital-intensive manufacturing bet, and you have something close to an annuity tied to the secular growth of one of the world's fastest-growing sports properties. For a company whose core footwear business is intensely cyclical and trend-dependent, owning a slice of that annuity is exactly the kind of ballast a thoughtful investor prizes.

There's also a strategic feedback loop between stichd's two pillars and PUMA's broader brand that is easy to miss. PUMA's deep, decades-long presence in motorsport — outfitting drivers and teams with footwear and apparel — is what earned it the credibility and relationships to win the F1 retail mandate in the first place. The fanwear monopoly, in turn, keeps the PUMA name woven through the entire spectacle of Formula 1 in front of a fast-growing global audience. Performance credibility begets commercial opportunity, which reinforces brand visibility, which supports performance credibility. It is the same virtuous loop that the whole company runs on, just expressed in a single, beautifully defensible niche.

So the picture that emerges is of a company with two distinct engines. There's the loud, expensive, brand-building engine — football, basketball, elite running — that generates cultural heat and footwear momentum but is intensely competitive and capital-hungry. And there's the quiet, high-margin, recurring-revenue engine — stichd's essentials platform and its Formula 1 retail monopoly — that throws off dependable cash with relatively little drama. A healthy PUMA needs both. The question that has dominated the last year is whether new leadership can make the loud engine as profitable as the quiet one.

VII. The Modern Guard: The Leadership Reset and the Brand-Elevation Pivot

The executive suite PUMA carries into the second half of the 2020s is, by design, almost a clean slate. To understand the company today, you have to look not at the leaders who built the turnaround but at the leaders running it now — and the speed of the turnover at the top is itself one of the central facts about this company.

At the center is Arthur Hoeld, who became chief executive officer on July 1, 2025, succeeding Arne Freundt.11 We've already met him as the man who crossed the river, and his pedigree is the whole point. Roughly 25 years inside Adidas — including running global sales — gave Hoeld an intimate, almost forensic understanding of how the rival across the Aurach actually wins and where it is vulnerable. PUMA's supervisory board did not hire him for caretaker stability; his mandate is commercial revitalization, restoring brand desirability, and instilling what the company repeatedly calls a "brand-first" mindset. He is a brand-and-commercial operator brought in to make the loud engine fire on all cylinders.[^14]

Alongside him on the finance side is Mark Alexander Langer, who joined as chief financial officer on May 1, 2026. Langer arrived with deep corporate discipline forged at Hugo Boss, the German fashion house where he served as CEO — exactly the profile you want when the job is to clean up the balance sheet, tighten the cash conversion cycle, and get a grip on inventory. Inventory management is not a footnote in apparel; carrying the wrong stock forces discounting, and discounting is precisely what the new strategy is trying to kill. There is a deeper reason a fashion-trained CFO matters here. The single most dangerous number on an apparel company's balance sheet is the inventory line, because unsold stock is a clock ticking toward a markdown — and a brand that habitually ends each season drowning in excess product has no choice but to discount, which trains its customers to never pay full price, which collapses the very premium positioning the rest of the company is trying to build. Someone who has run a fashion house has lived that doom loop intimately and knows the operational discipline required to escape it: tighter buys, faster replenishment, a willingness to leave some sales on the table rather than over-produce. Pairing a brand-first CEO with a disciplined, fashion-trained CFO is a deliberate balance: one foot on the accelerator of desirability, one hand on the brake of cost and inventory control.

The third pillar is Maria Valdes as Chief Product Officer — the creative force responsible for product innovation, marketing, and the cultural collaborations that determine whether PUMA's products are objects of desire or objects of clearance-rack indifference. In a business where the product is the brand statement, the CPO role is not support; it is front-line strategy.12

Now, the governance, because for long-term investors the incentive architecture is the tell. PUMA has built a compensation system explicitly designed to make executives behave like owners rather than hired hands. There are strict Share Ownership Guidelines: the CEO is mandated to hold PUMA shares equivalent to 100% of his gross annual base salary, and ordinary management board members must hold 50%. That forces personal skin in the game — a leader whose own net worth rises and falls with the share price thinks differently from one drawing a salary regardless of outcomes.

The variable pay is heavily weighted toward measurable performance. Short-term incentives are tied strictly to EBIT (a clean read on operating profitability) and relative sales growth (how PUMA grows versus its peer set, not just in absolute terms — which prevents management from taking credit for a rising tide). Long-term incentives are structured around a four-year virtual performance share plan tied to relative Total Shareholder Return and to core ESG sustainability targets, knitting environmental and social goals into the payout math rather than treating them as a side report. Total annual remuneration for the CEO is capped — at €20,000,000 — and the whole structure is backstopped by robust clawback provisions that let the company recover pay if results turn out to have been misstated or misearned. Caps plus clawbacks plus mandatory ownership is about as shareholder-aligned as European executive pay gets.

All of this machinery exists to serve one strategic idea: brand elevation. For years, like much of the industry, PUMA leaned on volume — push product into wholesale channels, accept heavy discounting to clear it, and chase revenue at the expense of margin and brand prestige. The new strategy deliberately reverses that. It means selling less but selling it at full price, controlling distribution, walking away from the discount-driven volume that erodes the brand's premium perception, and steering the business toward full-price sell-through. The explicit ambition is to cement PUMA as a premium, genuinely top-three global sports brand rather than a perennial value-oriented third option. It is, in a sense, a deliberate choice of quality of revenue over quantity of revenue — and it is exactly the kind of strategy that depresses the top line in the short run before (the bet goes) expanding margins and brand equity in the long run. Indeed, the company has framed its recent results as a reset, designating 2026 as a transition year on the road to that elevated position.13

For investors, brand elevation is the most important — and the most uncomfortable — strategic choice on the table, because it requires deliberately accepting pain. A volume-led company that suddenly refuses to discount and pulls back from low-quality wholesale distribution will, almost by definition, watch its reported revenue stall or even shrink for a period. The headline numbers will look worse before they look better. The entire bet rests on a belief that the quality of those reduced sales — higher full-price sell-through, fatter gross margins, a restored premium perception that eventually pulls demand back up — more than compensates for the lost volume over a multi-year horizon. This is a genuinely hard strategy to execute and an even harder one for public-market investors to stomach, because it asks them to look through a deliberately ugly transition. It also demands a patient shareholder base that won't panic at a soft revenue print and demand a return to the discounting drug. Which raises the obvious question: who is going to provide that patience and that capital through the lean years? As of early 2026, PUMA found an answer — in China.

VIII. The 2026 Game-Changer: The ANTA Sports Alliance

On January 27, 2026, the news broke that reframed PUMA's entire future. 安踏体育 ANTA Sports, the Chinese athletic-apparel titan, had signed an agreement to acquire a 29.06% stake in PUMA SE from Groupe Artémis — the Pinault family vehicle that had held its anchor position ever since the Kering spin-off.14 The price was €1.5 billion in cash, struck at €35 per share, valuing the overall transaction at roughly $1.8 billion, and ANTA confirmed it would fund the purchase entirely from its own internal cash resources.15 On completion, ANTA becomes PUMA's single largest and dominant anchor shareholder, displacing the Pinaults after nearly two decades of French ownership lineage.

The deal had to clear the usual gauntlet of antitrust and regulatory approvals across multiple jurisdictions, with the parties guiding toward a close by the end of 2026. As of this writing in June 2026, those clearances were progressing — notably, the Competition Commission of India granted its approval in June 2026 — and the transaction was moving steadily toward completion rather than facing any existential regulatory threat.16 ANTA was explicit that, at least initially, it did not intend to launch a full takeover bid for PUMA; the stated aim is a strategic anchor position and a review of avenues for future collaboration.

Why is this such a strategic masterstroke, and not merely a change of nameplate on the shareholder register? Three reasons.

First, the ANTA playbook is, frankly, the best in the business at exactly the thing PUMA needs. 安踏集团 ANTA Group has a near-flawless track record of acquiring international sports brands and scaling their retail and digital execution inside China and across Asia. It took Fila's China business and turned it into a juggernaut, transforming a sleepy license into one of the most profitable sportswear operations in the country. And through the Amer Sports vehicle it helped engineer the global rise of Arc'teryx, the premium outdoor brand, into a genuine status label. ANTA doesn't just buy brands; it knows how to operate foreign brands in Chinese retail, a skill that has humbled many Western companies who tried to do it alone.

The Fila turnaround deserves a moment, because it is the single best evidence for the ANTA thesis. When ANTA took control of Fila's China rights, the brand was a struggling also-ran with little relevance in the market. ANTA repositioned it as a premium, fashion-forward sportswear label, rebuilt its retail network around directly-operated stores that gave the company control over presentation and pricing, modernized its digital and e-commerce presence, and grew it into a multi-billion-renminbi business that became, for a stretch, the profit engine of the entire group. Notice what that turnaround actually was: a premiumization strategy executed through controlled, direct retail and sophisticated digital execution. That is, almost line for line, the playbook PUMA's own management is now trying to run with its brand-elevation and DTC push — except ANTA has already proven it can execute that exact playbook at scale, in the precise market where PUMA is weakest. This is the polar opposite of the Kering relationship. Where the French luxury parent fundamentally misunderstood the athletics business, ANTA understands the premiumization-through-controlled-retail business so intimately that it has become the global benchmark for it. The contrast in shareholder competence could hardly be sharper.

There is a second-layer point worth flagging on ANTA's discipline as an acquirer. The Amer Sports deal in particular showed that ANTA could buy a sprawling Western portfolio, focus relentlessly on the crown jewel (Arc'teryx), scale it primarily through the Chinese consumer's appetite for premium technical product, and ultimately crystallize enormous value — including by taking Amer public again at a far higher valuation. ANTA has, in other words, demonstrated not just operating skill but capital-markets sophistication and a willingness to be patient. Those are exactly the traits PUMA needs in an anchor shareholder shepherding it through a multi-year, deliberately painful brand-elevation transition.

Second — and this is the heart of the logic — Asia-Pacific is precisely where PUMA is weakest, which means it is where the upside is largest. In 2024, PUMA's Asia-Pacific sales were €1,805.5 million, roughly half the size of each of its two big regions: EMEA at €3,475.7 million and the Americas at €3,536.0 million.17 Read that as a glass half-full and the implication is enormous: the world's most important long-term growth market for sportswear is also PUMA's least-developed region, and the company is about to gain an anchor shareholder whose core competence is unlocking exactly that market. ANTA brings unparalleled supply-chain depth, digital commerce infrastructure, and physical retail reach across Greater China and the broader region — capabilities that would take PUMA a decade and a fortune to build alone, if it could build them at all.

Third — and crucially for those worried about a German icon being absorbed — the structure preserves PUMA's autonomy. While ANTA secures board representation commensurate with its large minority stake, PUMA retains its independent corporate governance, its registered SE (Societas Europaea) structure under European law, and its Herzogenaurach headquarters. This is an alliance, not an absorption. PUMA keeps its identity, its European legal home, and its leaping cat on the right bank of the Aurach, while gaining a powerful patron with the keys to the East.

It would be naive, however, to present this purely as a fairy tale, and a clear-eyed investor should weigh the genuine risks embedded in the structure. A near-30% holder is not a passive investor; it is a dominant force in the boardroom with the practical ability to shape strategy, and there is an inherent question of whether ANTA's interests as a Chinese sportswear group will always align perfectly with those of PUMA's minority shareholders — for instance, around sourcing, around which markets get prioritized, or around any eventual move to acquire more. There is also the delicate matter of two proud sportswear cultures, one German and rooted in eight decades of Herzogenaurach heritage, the other Chinese and accustomed to its own way of operating, learning to collaborate without the friction that has derailed many cross-border partnerships. And there is a geopolitical overlay that simply did not exist for the Kering deal: a Chinese strategic owner of a flagship German brand sits in the middle of an increasingly tense trade and technology relationship between China and the West, which could complicate everything from supply-chain decisions to consumer perception in certain markets. None of these risks negates the strategic logic, but honest analysis names them.

For long-term investors, the ANTA alliance nonetheless changes the risk-reward profile in a fundamental way. It pairs a patient, strategically motivated, deeply capable anchor shareholder with the brand-elevation turnaround, and it directly attacks PUMA's single biggest structural weakness — its underweight position in Asia — with a partner that has done this exact thing before. The strategic fit is about as clean as these things come. With the partnership in hand, the right way to evaluate PUMA from here is through the lens of competitive strategy.

IX. Playbook: The 7 Powers and the Five Forces

Let's war-game PUMA properly, using two complementary frameworks — Hamilton Helmer's 7 Powers, which asks what durable advantages a company actually holds, and Porter's Five Forces, which asks how attractive the industry it competes in really is.

Start with the Powers. The cleanest one PUMA holds is a Cornered Resource: stichd's exclusive trackside retail rights for Formula 1 and its master licensing partnerships with premium third-party brands like Tommy Hilfiger and Calvin Klein. A cornered resource is an asset you have preferential access to that rivals cannot simply buy their way into — and exclusive, contracted F1 retail rights are exactly that. No competitor can set up the official merchandise stand at a Grand Prix, because the rights are already PUMA's. It's narrow, but within its domain it is close to absolute.

The second power is Branding. This is the obvious one, and it is real: the leaping cat carries roughly eight decades of heritage, validated across generations by football icons like Pelé and Maradona, by the fastest sprinter in history, and modernized for the streaming age by cultural figures from Rihanna to LaMelo Ball. Branding power means a customer will pay more, or choose you over an objectively similar product, because of what the logo signifies. The honest caveat — and it's the whole point of the brand-elevation strategy — is that branding power erodes when you discount heavily and over-distribute. PUMA's branding power is genuine but has been partially squandered through years of volume-chasing, which is precisely why management is now trying to rebuild it.

The third is a localized form of Scale Economies. PUMA isn't the biggest sportswear company in the world — Nike and Adidas dwarf it overall. But in specific specialty niches it enjoys dominant scale, and motorsport is the standout. PUMA manufactures the fireproof racing suits and shoes for the vast majority of the Formula 1 grid. That is a category with real technical barriers (these are life-safety products subject to strict certification), and being the entrenched supplier to most of the grid gives PUMA a cost-and-credibility advantage that a new entrant simply cannot match at low volume. Dominate a small, defensible category and you own its economics.

The fourth is Counter-Positioning, which PUMA expresses through its leaner, faster operating model. The "Forever. Faster." philosophy isn't only marketing; it reflects a genuine attempt to run shorter product-development cycles and a more agile supply chain than the lumbering giants. PUMA was also, historically, early to embrace the sport-lifestyle intersection — leaning into fashion collaborations decades before it became industry orthodoxy. The caveat here is that counter-positioning is only a durable power if incumbents can't copy you without damaging their existing business, and agility is, frankly, copyable. So treat this as a real-but-contestable advantage rather than an unbreachable moat.

It's just as important to be honest about the powers PUMA lacks, because the gaps define the competitive risk. PUMA has essentially no network economies — a pair of PUMA trainers is not more valuable to you because your friends own them, the way a social network or a marketplace compounds with scale. It has little in the way of switching costs — a consumer who bought PUMA last year faces zero friction in buying Nike this year, because there's no lock-in, no ecosystem, no subscription tethering them. And it does not possess process power, the kind of hard-to-replicate operational excellence that lets a Toyota or a TSMC produce at a quality or cost rivals simply can't match; sportswear manufacturing is largely outsourced to the same contract factories everyone uses. So of Helmer's seven powers, PUMA holds parts of four and lacks three entirely. That is a respectable but not dominant moat profile — it explains why PUMA is a durable number three rather than a runaway leader, and why its competitive position requires constant, active defense rather than passive coasting.

Set against the competitive set, the picture sharpens further. Nike's powers are deeper across the board — vastly greater scale economies, a stronger brand, and arguably the beginnings of network and ecosystem effects through its apps and membership. Adidas shares PUMA's Herzogenaurach DNA but operates at roughly four to five times the revenue, giving it scale advantages PUMA cannot match. Meanwhile the specialist insurgents — On Running and Hoka — are running a focused counter-positioning play of their own against the giants, building intense brand and product credibility in premium running specifically, the very category where technical authenticity is most valuable and most defensible. PUMA's strategic challenge is that it is being attacked from both ends of the spectrum simultaneously: out-scaled by the giants above and out-focused by the specialists below. Its defense rests on the powers it genuinely holds — the F1 cornered resource, the motorsport scale niche, and a brand it is now spending heavily to re-elevate — plus the new strategic capability that ANTA brings in Asia.

Now flip to Porter's Five Forces — the industry weather PUMA has to operate in, and it is, candidly, harsh.

Competitive rivalry is extremely high — the defining feature of this industry. PUMA is sandwiched between two giants with vastly greater scale (Nike and Adidas) and simultaneously attacked by hyper-focused performance insurgents. On Running, the Swiss maker of the cloud-soled running shoe, and Hoka, the maximalist-cushioning brand, have both stormed the premium running market; Lululemon dominates premium athleisure. PUMA is fighting a two-front war: outgunned on scale from above, out-focused on premium niches from the side.

The bargaining power of buyers is moderate. Traditional wholesale distributors — the big retail chains that resell PUMA's products — hold real leverage, because they control shelf space and can play brands off against each other. But that power is steadily diminishing as PUMA shifts toward direct-to-consumer, now better than a quarter of sales. Every point of DTC growth is a point of leverage clawed back from the middleman.

The bargaining power of suppliers is low — a genuine structural advantage. PUMA outsources its manufacturing across a diversified base in Vietnam, China, Cambodia, and elsewhere. Because no single factory or country is irreplaceable, individual suppliers have little pricing leverage. The flip side, which belongs on any second-layer diligence checklist, is that this same outsourced footprint concentrates supply-chain, labor, tariff, and geopolitical risk in Asia — a risk that cuts in interesting directions now that PUMA's anchor shareholder is Chinese.

The threat of new entrants is moderate-to-low, and the asymmetry here is important. It is genuinely easy to launch a lifestyle sneaker brand — a clever designer with a contract manufacturer can do it. It is genuinely hard to build what PUMA has: global athletic distribution, real performance R&D like Nitro foam, certified motorsport manufacturing, and the multi-hundred-million endorsement networks that performance credibility requires. The lifestyle door is wide open; the performance-sports door is barricaded.

The threat of substitutes is high. A consumer has effectively endless alternatives at every price point — other sneakers, casual footwear, boots, even the choice to simply buy less. There is nothing forcing a customer to buy PUMA specifically, which loops directly back to why branding power and product desirability are existential rather than nice-to-have.

The composite picture: PUMA operates in a brutally competitive, substitute-rich industry where its scale-disadvantage versus the giants is real, but where it holds a handful of genuine, defensible powers — a cornered F1 resource, a localized motorsport scale moat, and real (if partially eroded) brand equity. The investment debate is fundamentally about whether management can widen those moats faster than the industry's harsh forces grind them down.

X. Myth vs. Reality, the KPIs, and the Bull-Bear Case

Before the verdict, it's worth puncturing a couple of consensus narratives, because the easy story about PUMA is usually slightly wrong.

The first myth: "PUMA is just the poor man's Adidas, a perennial also-ran." The reality is more interesting. PUMA is less a smaller Adidas than a different kind of company — one whose profit base leans unusually hard on hidden, high-margin, recurring engines (stichd's essentials platform and its Formula 1 retail monopoly) that have no real equivalent at its larger rivals. The second myth: "The ANTA deal means a Chinese takeover of a German icon." The reality, at least as structured, is a large minority stake with board representation but preserved European governance, SE legal structure, and Herzogenaurach headquarters — an alliance built to unlock Asia, not an absorption. Reading either myth literally leads you to misjudge the business.

A third myth worth puncturing: "Brand elevation is just corporate spin for 'we're shrinking.'" There's a sliver of truth that makes this one dangerous — the strategy genuinely does involve walking away from revenue in the near term, and a cynic could read soft sales as failure dressed up in strategy-deck language. But the test of whether elevation is real or merely a euphemism is not the revenue line at all; it's the margin line and the quality of distribution. If PUMA is genuinely selling more of its product at full price through channels it controls, gross margin expands and the brand's pricing power strengthens even as volume dips — that's elevation working. If revenue falls and margins stay flat or compress, then the cynic is right and it's just shrinkage. The strategy is falsifiable, and the data will tell the story. That's why the metrics you track matter so much.

One second-layer note belongs here, because it's material and easy to overlook. PUMA's manufacturing is concentrated in Asian contract factories, which keeps supplier power low but concentrates labor, human-rights, environmental, and tariff exposure — and the company's long-term incentive plan explicitly ties executive pay to ESG sustainability targets, signaling that these are board-level concerns, not afterthoughts. The arrival of a Chinese anchor shareholder cuts in two directions on this front: it deepens PUMA's relationship with Asian supply chains and demand, but it also entangles a German brand in the geopolitics of Western-Chinese trade tension, a risk with no clean precedent in PUMA's history. It is the kind of qualitative, hard-to-quantify exposure that doesn't show up in a valuation multiple but can move the business in a bad year.

So what should a long-term investor actually track? Amid all the noise, three KPIs matter most for monitoring whether this turnaround is working. First, gross margin — because the entire brand-elevation thesis lives or dies here. If management is genuinely selling more at full price and walking away from discounted volume, gross margin should expand; if it's not, the strategy is failing regardless of what the press releases say. Second, the Asia-Pacific growth rate — the single cleanest scoreboard for whether the ANTA partnership is delivering on its core promise of unlocking the East. Third, the DTC mix as a percentage of sales — the structural lever behind both pricing control and margin, and a direct read on whether PUMA is reclaiming power from the wholesale channel. Watch those three, and you'll know more about PUMA's trajectory than any quarter's headline revenue figure can tell you.

Now, the cases.

The bull case rests on three legs. First, the ANTA alliance successfully unlocks the massive, high-margin Chinese and Asia-Pacific market, turning PUMA's weakest region into its growth engine and re-rating the whole company. Second, the brand-elevation pivot under Arthur Hoeld works as designed — discounting falls, full-price sell-through rises, and gross margins climb back toward historical highs, proving PUMA can be a genuine premium top-three brand rather than a value option. Third, stichd keeps riding the global Formula 1 boom and the steady essentials business, acting as a stable, high-margin cash cow that funds the brand investment through the transition. Stack those together and you have an agile, independent, premium brand with a powerful Asian patron and a hidden cash engine — a genuinely attractive combination.

The bear case is equally coherent, and honest analysis requires taking it seriously. First, execution friction from relentless leadership churn: PUMA has cycled from Bjørn Gulden to Arne Freundt to Arthur Hoeld in well under three years, and every CEO transition resets strategy, unsettles the organization, and costs momentum. Stability is itself a competitive asset, and PUMA has lacked it. Second, the squeezed middle: if On Running and Hoka continue to capture the premium running consumer while Nike and Adidas defend the mass market, PUMA risks being stranded exactly where Kering once left it — not premium enough, not big enough — and the brand-elevation push could simply shrink the top line without delivering the premium repositioning. Third, the macro: full-price strategies are brutally exposed to weak consumer spending, and sluggish demand in Europe and North America could starve the elevation strategy of the very full-price demand it depends on, forcing PUMA right back into the discounting it's trying to escape.

The throughline of PUMA's whole modern history is a series of escapes. It escaped, partially, from the shadow of its sibling across the river — though that rivalry still defines its culture and just supplied its CEO. It escaped the lifestyle wilderness of the Kering years, where a luxury parent nearly hollowed out its athletic soul. It escaped into independence, rebuilt its credibility on the pitch, the court, and the track, and quietly assembled a hidden cash machine in socks and Formula 1 merchandise that almost no consumer ever notices. And now, with the brand-elevation reset under a defector from across the Aurach and a €1.5 billion anchor investment from the most capable brand-scaler in Asia, PUMA has positioned itself for what may be its most consequential race yet — the one that determines whether the leaping cat, eighty years after two brothers stopped speaking, can finally run on its own terms.

References

-

PUMA SE (PUM.DE) Stock Quote & Financial Summary — Reuters Markets ↩

-

PUMA SE Company Overview & Financial Tracking — Financial Times Companies ↩

-

ANTA Sports to Acquire 29.06% Stake in PUMA SE — World Footwear, 2026-01-28 ↩

-

Kering: A Timeline Behind the Building of a Luxury Goods Group — The Fashion Law ↩

-

PUMA Acquires Equipment Brand Cobra Golf — PUMA Newsroom, 2010 ↩

-

Puma Parent Company Kering Announces Plan To Sell 70% Of Its Stake — Yahoo Finance / Reuters, 2018 ↩

-

PUMA accelerates growth throughout 2024 and initiates program to increase profitability — PUMA Newsroom, 2025-01-22 ↩

-

stichd Official Homepage & Brand Portfolio — stichd Corporate ↩

-

PUMA and Formula 1 Enter Official Partnership — Business Wire, 2023-05-04 ↩

-

PUMA CEO Arne Freundt Steps Down, Succeeded by Adidas Veteran Arthur Hoeld — Retail Dive, 2025-05-14 ↩

-

Q4 & FY 2025 — PUMA completes reset in 2025; 2026 designated as transition year ↩

-

ANTA Sports Products Limited — Acquisition of 29.06% Stake in PUMA SE, Investor Relations Announcement ↩

-

Puma shares surge after Anta Sports buys stake for $1.8 billion amid turnaround efforts — CNBC, 2026-01-27 ↩

-

Firms steer Anta's EUR1.5bn acquisition of 29% stake in Puma — Law.asia ↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube