ORLEN: The Making of a Central European Energy Supermajor

I. Introduction — The "Exxon of the East" (0:00 – 0:08)

Somewhere between Berlin and Vilnius, spread across the flat expanse of the North European Plain, a company most Western investors have never heard of controls a staggering share of the energy infrastructure that keeps Central Europe running.

It refines crude oil in Poland, the Czech Republic, and Lithuania. It pumps natural gas from beneath the Norwegian Sea. It generates electricity for three million Polish households. It operates the region's largest network of fuel stations—more than 3,400 across seven countries. And it is building the Baltic Sea's newest offshore wind farm, a 1.2-gigawatt cathedral of steel and composite blades rising from the grey waters twenty-three kilometres off the Polish coast.

Its annual revenue reached PLN 267 billion in 2025. Its name is ORLEN. And its story is one of the most ambitious—and controversial—corporate transformations of the twenty-first century.

The transformation happened fast.

In 2017, ORLEN was a mid-sized Central European refiner—dependent on Russian crude, boxed in by larger competitors, and largely invisible to international capital markets. By the end of 2022, it had swallowed Poland's second-largest refinery, the national gas monopoly, and a major electricity utility. It had quintupled its workforce, tripled its asset base, and secured a twenty-year crude supply agreement with Saudi Aramco.

The company that emerged was no longer an oil company. It was something new—a state-backed, multi-utility energy conglomerate with upstream gas production in Norway, downstream retail in Germany, petrochemical capacity rivalling anything in Western Europe, and a green transition budget that dwarfs the GDP of several EU member states.

The thesis is straightforward but provocative: ORLEN is an experiment. It is the Polish state's answer to a question that every fossil-fuel-dependent nation must eventually confront—how do you take a legacy hydrocarbon business and reshape it into something that can survive 2050?

The experiment is expensive. Strategy 2035, announced in January 2025, envisions PLN 350 to 380 billion in cumulative capital expenditure over the next decade—roughly EUR 85 to 90 billion. Forty percent of that is earmarked for green and transition investments: offshore wind, small modular nuclear reactors, hydrogen infrastructure, energy storage.

The experiment is also political. The Polish State Treasury holds 49.9 percent of ORLEN's shares. Every change of government in Warsaw brings the potential for management turnover, strategy reversal, and capital allocation upheaval. The previous CEO was dismissed and is now facing criminal prosecution. The current CEO was selected from a pool of 260 candidates and is six months into a wholesale strategic review.

Whether ORLEN represents the blueprint for how a fossil fuel giant survives the energy transition—or a cautionary tale about political interference in corporate governance—depends on who you ask, and when.

One thing is beyond dispute: this is the largest company most global investors have never studied. In a world obsessed with the energy transition narratives of Shell, BP, TotalEnergies, and Equinor, the company quietly building Central Europe's largest offshore wind farm, pursuing small modular nuclear reactors, and operating a retail network larger than any single Western European major's in the region has received almost no attention from English-language analysts. That obscurity may itself be an opportunity—or a warning.

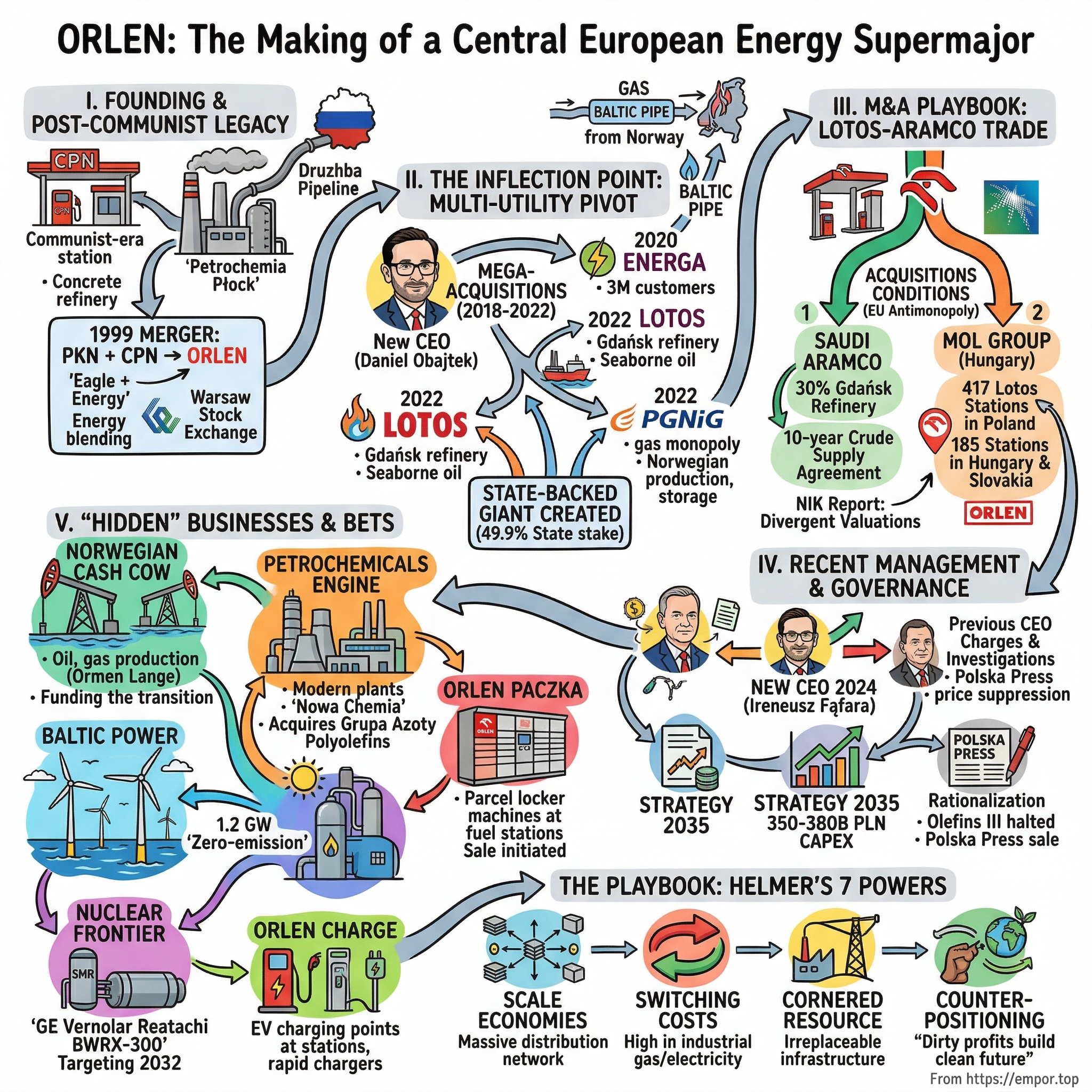

II. Founding & The Post-Communist "CPN" Legacy (0:08 – 0:20)

To understand ORLEN, you have to understand a petrol station.

Not a modern one with artisanal coffee and electric vehicle chargers, but a communist-era CPN station—Centrala Produktów Naftowych—the kind that dotted Polish highways in the 1980s. Concrete islands. Dirty pumps. A single attendant behind glass. No competition, because there was no private enterprise. CPN was the state petroleum distribution monopoly, and every litre of fuel sold in Poland flowed through its network.

At the other end of the supply chain sat Petrochemia Płock—a vast refining and petrochemical complex built in the 1960s on the banks of the Vistula River, roughly one hundred kilometres northwest of Warsaw. Płock sat at the terminus of the Druzhba—"Friendship"—pipeline, the Soviet-era crude oil artery that carried Russian oil westward through Belarus into Poland and onward to Germany. The refinery processed Russian Urals crude and little else. Its entire business model was predicated on cheap, reliable flows of Russian oil.

In 1998, the Polish government decided to merge these two entities. The logic was classic post-communist rationalisation: combine the upstream processing of Petrochemia Płock with the downstream distribution of CPN, creating a vertically integrated national oil company that could hold its own against regional competitors.

The merger closed on September 7, 1999, creating Polski Koncern Naftowy. The brand name "ORLEN" was added shortly after—chosen from over a thousand naming contest submissions, blending "orzeł" (eagle) and "energia" (energy). Within weeks, the company listed on the Warsaw Stock Exchange, selling a 30 percent stake to public investors, with shares also available in London.

It was one of the landmark post-communist privatisations in Central Europe. But it created a company with a fundamental vulnerability.

ORLEN was a price taker. It bought Russian crude at prices set by global markets, refined it into fuel, and sold that fuel through its domestic stations. When oil prices rose, margins compressed. When oil prices fell, margins expanded—but so did political pressure to pass savings to consumers rather than shareholders.

The company spent its first fifteen years locked in this cycle, buffeted by forces entirely beyond its control. It competed against MOL of Hungary—a faster, more aggressive company that had already diversified into upstream production and international refining. It competed against OMV of Austria, which had deep pockets and Western European institutional backing. And it competed against the fundamental reality of geography: Poland sits between Russia and Western Europe, dependent on both for supply and demand.

The one thing ORLEN had was scale. The Płock refinery, with a processing capacity of roughly 16 million tonnes per year, was among the largest in Central Europe. The CPN station network—roughly 1,800 locations at the time of the merger—was the densest in the region.

These physical assets could not be replicated quickly or cheaply. A refinery of Płock's scale takes a decade to permit and build. A national fuel station network takes decades to assemble, one site at a time—negotiating leases, obtaining environmental permits, building tanks, pouring concrete. They were, in Helmer's framework, a cornered resource—not because of any legal monopoly, but because the sheer capital cost of replicating them created a durable barrier to entry.

But scale in refining without upstream production is like owning a bakery without a wheat field. You are always one supply shock away from crisis.

The competitive dynamics of the 2000s and 2010s illustrated this vulnerability clearly. MOL of Hungary—run by the aggressive and strategically brilliant Zsolt Hernádi—had diversified into upstream production and international refining far earlier than ORLEN. MOL bought Croatia's INA, built a presence in Pakistan, and developed a trading operation that gave it crude sourcing flexibility ORLEN lacked.

OMV of Austria had the advantages of Western European capital markets—lower borrowing costs, deeper institutional investor relationships, and a more diversified shareholder base. Both competitors could absorb oil price shocks that left ORLEN scrambling.

ORLEN tried to respond. In 2006, it acquired a controlling stake in Mažeikių Nafta—Lithuania's sole refinery, now operating as ORLEN Lietuva. The deal gave ORLEN its first international refining asset and a foothold in the Baltic states. It also acquired refineries in the Czech Republic—Unipetrol, which operates the Litvínov and Kralupy refineries—creating a multi-country refining footprint.

But these acquisitions, while geographically diversifying, did not solve the fundamental problem: ORLEN remained a price taker on its most important input. Every barrel of crude was purchased at prices set by global markets, processed at margins dictated by the crack spread, and sold at prices influenced by political pressure.

The supply shock that ORLEN had been dreading for decades—the abrupt cutoff of Russian crude—would eventually arrive, in the most dramatic fashion imaginable, in February 2022.

The early vulnerability to supply disruption created the institutional obsession that defines ORLEN today: energy sovereignty. The phrase appears in every strategic document, every investor presentation, every CEO speech. It is not a slogan. It is the operating philosophy of a company that spent its formative years acutely aware that its most important input—Russian crude oil—could be weaponised at any moment.

That obsession would eventually drive the most aggressive corporate consolidation in Central European history.

III. The Inflection Point — The "Multi-Utility" Pivot (0:20 – 0:45)

The transformation began, as transformations often do, with a political appointment.

In February 2018, Poland's ruling Law and Justice party (PiS) installed Daniel Obajtek as CEO of ORLEN. Obajtek's background was unusual, to put it charitably. He had been the mayor of Pcim—a small town in the Carpathian foothills with a population of roughly ten thousand—and had subsequently run ARiMR, the Agency for Restructuring and Modernisation of Agriculture. He had no energy industry experience. No engineering credentials. No capital markets background.

What he had was political backing, enormous personal ambition, and a mandate from the PiS government to do something dramatic.

The dramatic thing he did was this: over the next four years, Obajtek executed three mega-acquisitions that transformed ORLEN from a regional refiner into a multi-utility energy conglomerate controlling every link in the energy value chain—from the wellhead to the wall socket.

The Energa Acquisition (2020)

The first move was Energa—one of Poland's "Big Four" electricity distribution companies, serving roughly three million customers across northern Poland with 1.3 gigawatts of installed generation capacity.

ORLEN announced a tender offer in December 2019 at PLN 7 per share, later raised to PLN 8.35, valuing the roughly 80 percent stake at approximately PLN 2.77 billion. The deal closed on April 30, 2020—delayed by two weeks because of the COVID-19 pandemic.

Was it a bailout or a brilliant vertical integration?

The answer depends on your priors. Energa was struggling. Its generation assets included aging coal and lignite plants facing mounting carbon costs under the EU Emissions Trading System. Its distribution grid required billions in investment. Its share price had cratered. Critics argued that ORLEN was being used as a state-directed vehicle to absorb a failing public utility—socialising Energa's losses across ORLEN's shareholder base.

The strategic bull case was different: an integrated energy company that controlled both fuel production and electricity generation could hedge across commodity cycles. When oil prices fell, electricity prices typically rose (because gas-fired generation set the marginal price in European power markets). Owning both businesses created a natural portfolio effect. And Energa's distribution grid—22 terawatt-hours of delivered electricity across northern Poland—was a physical asset that no competitor could replicate.

There is a useful analogy here. Think of Berkshire Hathaway's acquisition of BNSF Railway in 2009. Warren Buffett did not buy a railroad because he liked trains. He bought it because he believed the physical infrastructure—the rail network itself—was an irreplaceable asset that would generate returns for decades. Energa's electricity distribution grid is the same kind of asset. Wires and transformers are not exciting. They are not disruptable. And they are not replicable. That is precisely what makes them valuable.

Regardless of motive, the Energa deal established the template for what followed: state-directed consolidation of Poland's energy sector under a single corporate roof.

The "Merger of Three Kings"

The Energa acquisition was appetiser. The main course was the simultaneous absorption of Grupa Lotos and PGNiG—Poland's second-largest refiner and the national gas monopoly, respectively.

Lotos brought the Gdańsk refinery—a Baltic Sea–facing facility that complemented Płock's inland position and provided direct access to seaborne crude imports. Combined refining capacity rose to approximately 35 million tonnes per year—among the largest in Europe.

PGNiG brought something even more valuable: upstream gas production. Roughly one hundred licences on the Norwegian Continental Shelf, including a 14 percent stake in Ormen Lange—Norway's second-largest gas field, with a production life extending beyond 2045. PGNiG's Norwegian assets produced approximately 40.5 million barrels of oil equivalent in 2024, including 4.5 to 4.6 billion cubic metres of natural gas—an increase of 45 percent year-over-year. This gas now flows directly to Poland via the Baltic Pipe subsea pipeline, which entered service in late 2022, bypassing Russia entirely.

PGNiG also brought a vast domestic gas distribution network serving millions of industrial and residential customers, underground storage facilities that provide strategic reserves against supply disruptions, and—critically—long-term contracts with extremely high switching costs. An industrial customer connected to PGNiG's pipeline network cannot simply switch to a different gas supplier. The physical infrastructure creates lock-in that no amount of competitive pricing can overcome.

The share exchange ratios reflected the relative scale of the companies involved. For Lotos, shareholders received 1.075 ORLEN shares for each Lotos share held. For PGNiG, the ratio was 0.0925 ORLEN shares per PGNiG share, with fractional shares compensated in cash.

The Lotos merger closed on August 1, 2022. The PGNiG merger closed on November 2, 2022. ORLEN's share capital nearly doubled, from PLN 783 million to PLN 1.45 billion. The State Treasury's stake mechanically increased from 27.5 percent to approximately 49.9 percent—because the state had held significant positions in both Lotos and PGNiG, and those positions converted to ORLEN shares.

Why did the Polish state decide to create one "giga-company" instead of maintaining three competing energy players?

The logic was twofold.

First, scale. The energy transition requires capital expenditure measured in tens of billions of euros. No single Polish energy company had the balance sheet to fund offshore wind farms, nuclear reactors, hydrogen infrastructure, and petrochemical modernisation simultaneously. Consolidation created a single entity with PLN 153 billion in equity and PLN 46 billion in annual operating cash flow—a balance sheet capable of competing with Western European majors like TotalEnergies and Shell.

Second, sovereignty. Russia's invasion of Ukraine in February 2022—occurring precisely between the announcement and closing of the Lotos and PGNiG mergers—brutally validated the thesis that energy security required centralised control. When Russian gas flows to Europe collapsed, Poland's position was vastly stronger than Germany's or Austria's—because the Baltic Pipe was already under construction, PGNiG's Norwegian production was already flowing, and the Gdańsk refinery could receive seaborne crude from non-Russian sources.

The timing was either extraordinary foresight or extraordinary luck. Probably both.

The post-merger ORLEN was a fundamentally different company. Revenue jumped from PLN 111 billion in 2021 to PLN 373 billion in 2023—a more than threefold increase that reflected not organic growth but the absorption of two entire companies. The workforce expanded from roughly 20,000 to over 60,000. The asset base encompassed everything from offshore gas platforms in the North Sea to village petrol stations in rural Poland.

The complexity was staggering. Integrating three corporate cultures—the commercially aggressive refining culture of Płock, the engineering-driven gas culture of PGNiG, and the utility culture of Energa—into a single operating company was a management challenge of the first order. Different IT systems, different procurement processes, different labour agreements, different regulatory frameworks. The technical challenge of running a refinery has nothing in common with the technical challenge of operating an electricity distribution grid.

Whether ORLEN has actually captured the integration synergies that justified the mergers remains an open question. Management has claimed cumulative cost savings in the billions of złoty, but the opacity of the post-merger financial reporting makes independent verification difficult. The FY 2024 results—depressed by massive write-downs and one-off charges—suggest that the integration costs were larger, and the synergies slower to materialise, than the original projections implied.

IV. M&A Playbook — The Lotos-Aramco Trade (0:45 – 1:05)

Every merger of this scale comes with conditions. The European Commission's Directorate-General for Competition does not allow a dominant refiner to absorb its nearest competitor without extracting concessions. The conditions imposed on the ORLEN-Lotos merger created one of the most controversial transactions in recent Central European corporate history.

To secure EU antitrust approval, ORLEN was required to divest significant Lotos assets to third parties. The remedies were designed to preserve competition in the Polish fuel market and prevent ORLEN from achieving an unacceptable degree of market dominance.

Two buyers emerged.

Saudi Aramco acquired a 30 percent stake in Rafineria Gdańska—the Gdańsk refinery—plus full ownership of a logistics subsidiary. The fixed payment was approximately PLN 1.15 billion, with additional variable elements linked to future performance. Critically, Aramco committed to a ten-year crude oil supply agreement—guaranteeing ORLEN access to Saudi crude at market prices, diversifying supply away from Russian dependence.

MOL Group of Hungary acquired 417 Lotos fuel stations in Poland for approximately USD 610 million. In a reciprocal swap, ORLEN acquired 144 MOL stations in Hungary and 41 in Slovakia for EUR 229 million. The net effect was that ORLEN traded scale in its dominant home market for geographic diversification into two new countries.

The controversy centred on price.

Poland's Supreme Audit Office—the NIK—published a devastating report in February 2024 finding that ORLEN received approximately PLN 4.6 billion for all divested assets combined, but that the NIK's own valuation estimated fair value at approximately PLN 5 billion higher. The Gdańsk refinery stake alone was valued by auditors at roughly PLN 4.6 billion—yet sold to Aramco for PLN 1.15 billion.

The gap between the NIK's valuation and the transaction price is staggering. If the auditors are right, the Polish state—through ORLEN—effectively subsidised Saudi Aramco's entry into the Polish refining market to the tune of several billion złoty.

Management's defence, articulated under the Obajtek regime, was that the financial analysis misses the strategic dimension. The Aramco relationship, the argument goes, bought three things that cannot be valued on a discounted cash flow spreadsheet.

First, security of supply. A ten-year crude supply agreement with the world's largest oil producer, signed at the precise moment when Russia's weaponisation of energy supplies was reshaping European geopolitics. The value of knowing you will have crude oil when your competitors may not is, by definition, incalculable.

Second, a seat at the table. The relationship with Aramco opened doors to technology sharing, joint ventures in petrochemicals, and potential collaboration on downstream investments in the Middle East. ORLEN went from being an anonymous Central European refiner to a strategic partner of the world's most important oil company.

Third, regulatory clearance. Without the Aramco divestiture, the EU Commission would not have approved the Lotos merger. The alternative—no merger at all—would have left Poland with three sub-scale energy companies incapable of funding the energy transition independently. The "cost" of the Aramco deal, in this framing, was the price of admission to the multi-utility strategy.

Whether you find this argument compelling depends on how you value optionality versus tangible assets. Traditional financial analysis says ORLEN overpaid—or rather, undersold. Strategic analysis says the company traded a minority stake in a refinery for a twenty-year relationship with the Saudi kingdom. The truth is probably somewhere in between: the deal was necessary for the strategy to work, but the price could have been better.

The MOL station swap is easier to assess. ORLEN traded 417 stations in its home market—where it already had overwhelming dominance—for 185 stations in Hungary and Slovakia, where it had none. The financial terms were roughly market-rate. The strategic value was geographic diversification and a foothold in two new retail markets.

Combined, the total ORLEN retail network now exceeds 3,400 stations across Poland, Germany, the Czech Republic, Hungary, Slovakia, Lithuania, and Austria—the largest fuel station network in Central Europe. In Poland alone, ORLEN operates approximately 1,929 stations under the ORLEN brand, complemented by roughly 607 in Germany (under both the ORLEN and Star brands), 436 in the Czech Republic, and smaller networks across the remaining countries. The retail business also includes the Stop Cafe convenience store chain, which transforms fuel stations from pure-play fuel dispensers into convenience retail destinations—a model pioneered by Norwegian operator Circle K and now standard across European fuel retailing.

For investors, the Lotos-Aramco episode illustrates the central tension in evaluating ORLEN: the company consistently makes strategically logical decisions whose financial execution raises legitimate questions. The strategy is sound. The price is debatable. And the governance framework that produced these decisions has since been swept away by a change of government.

A useful comparison is the European Commission's treatment of other major energy mergers. When Shell merged with BG Group in 2016, the regulatory concessions were modest—asset sales in a few specific geographies. When Wintershall merged with DEA, the conditions were largely behavioural. The Lotos remedies were among the most aggressive in recent European energy history—reflecting the Commission's legitimate concern about concentration in the Polish fuel market, but also creating the conditions for the Aramco pricing controversy.

The question investors must ask is not whether the Aramco deal was good or bad in isolation. It is whether the entire multi-utility strategy—which required the Lotos merger, which required the Aramco divestiture—was worth the cumulative cost. The answer depends on whether ORLEN's integrated asset base generates enough incremental value over the next two decades to justify the price paid at each step along the way.

V. Current Management & Governance (1:05 – 1:20)

On February 1, 2024, the new Polish government—a coalition led by Prime Minister Donald Tusk—dismissed Daniel Obajtek as CEO of ORLEN.

The dismissal was not surprising. Tusk's coalition had campaigned partly on a promise to clean up state-owned enterprises that, in their view, had been captured by PiS for political purposes. ORLEN was Exhibit A.

What followed was a comprehensive accounting of the Obajtek era—and the picture that emerged was troubling.

Polish prosecutors opened at least a dozen investigative files. The allegations ranged from the prosaic to the extraordinary. There were contracts worth PLN 393,600 paid to a private detective agency without competitive tender. There were allegations of false testimony in court proceedings. There were claims that ORLEN had restricted distribution of a left-wing political magazine at its fuel stations.

More substantively, prosecutors investigated the pre-election fuel price suppression—a practice in which ORLEN allegedly absorbed fuel price increases before elections to benefit the ruling party, at an estimated cost to shareholders of PLN 5.7 billion. There were losses exceeding PLN 1.5 billion from a Swiss subsidiary's failed Venezuelan oil prepayments. And there was the Aramco asset pricing discussed above.

Perhaps the most unusual acquisition of the Obajtek era was Polska Press—Poland's largest regional media group, controlling dozens of newspapers and websites across the country. A state-owned energy company buying a media empire struck even sympathetic observers as overreach. Reporters Without Borders cited the acquisition as a factor in Poland's decline to 66th on the Press Freedom Index. Norway's sovereign wealth fund placed ORLEN on a governance watchlist.

Obajtek was elected to the European Parliament on the PiS ticket in June 2024. In October 2025, the European Parliament voted to lift his immunity, enabling Polish prosecutors to proceed. He denies all charges, calling them a political witch hunt.

The legal overhang matters for investors beyond the headline risk. If prosecutors ultimately secure convictions related to the Aramco pricing or the Olefins III cost overruns, the resulting judgments could potentially allow ORLEN to pursue claims against former executives—recovering some portion of the value destroyed. Conversely, a protracted legal process creates ongoing media noise that may depress the stock's re-rating potential even if the underlying business performs well. The legal proceedings are likely to last years, and their outcome is genuinely uncertain.

The New Guard

The search for Obajtek's replacement attracted 260 candidates. The selection committee chose Ireneusz Fąfara, whose appointment took effect on April 11, 2024.

Fąfara's profile is the inverse of his predecessor's. Born in 1960, he spent seven years running ORLEN Lietuva—the Lithuanian refining subsidiary—from 2010 to 2017, giving him deep operational knowledge of refining economics. He had previously served as CEO of Bank Gospodarstwa Krajowego, the Polish state development bank, and held a senior role at ZUS, the social insurance institution. He is a career technocrat—a banker who knows the energy business, not a politician who was given one.

His early moves signalled a clear break with the Obajtek era.

He halted the Olefins III petrochemical project in December 2024, after costs had ballooned from an original PLN 13.5 billion to an estimated PLN 80 billion or more—a sixfold overrun that management characterised as unsalvageable. The cancellation saved an estimated PLN 15 billion in remaining committed capital.

He initiated the divestiture of Polska Press—calling it a "bad and unnecessary investment" at a January 2025 press conference. He signed a term sheet in September 2025 for the potential sale of Orlen Paczka, the parcel locker business, to Poczta Polska—reflecting a "focus on core energy" philosophy.

And in January 2025, he unveiled Strategy 2035—ORLEN's ten-year roadmap, centred on PLN 350 to 380 billion in cumulative capital expenditure, with the explicit goal of transforming ORLEN from a fossil fuel company into a diversified energy platform.

The current management board includes Magdalena Bartos as CFO, Wiesław Prugar overseeing upstream, Ireneusz Sitarski running retail, and Robert Soszyński leading strategy and sustainable development. An August 2025 reshuffle replaced several board members—a reminder that governance stability at ORLEN remains aspirational rather than structural.

The Ownership Anchor

The State Treasury's 49.9 percent stake is both ORLEN's greatest asset and its greatest liability.

The asset: no activist investor can force a breakup, no hostile bidder can acquire the company, and no short-term pressure can derail a ten-year capital programme. The state provides patient capital in a way that no institutional investor can.

The liability: every election is a potential CEO change. Every government has its own industrial policy priorities. Every prime minister views ORLEN as an instrument of state power—because it is one. The company's dividend policy, capital allocation, and strategic direction are all subject to political influence that no Western European major faces.

International institutional investors apply a persistent governance discount—typically 20 to 30 percent versus Western European integrated majors on an EV/EBITDA basis. The gap is not a reflection of asset quality—it is a reflection of governance risk.

The Nationale-Nederlanden pension fund holds approximately 5.2 percent—the second-largest shareholder after the state. The remainder is in free float, held by a mix of Polish retail investors—for whom ORLEN is a dividend staple—and international institutional funds with varying degrees of comfort with Polish political risk.

The management compensation structure reflects the hybrid identity. Fąfara earned PLN 2 million in 2024 for roughly eight months of service. His deputy Witold Literacki earned PLN 2.5 million—the highest on the board. These figures are modest by Western European standards—the CEO of TotalEnergies earned roughly EUR 6 million—reflecting both the political optics of state ownership and the compensation constraints that come with public-sector governance norms.

Whether compensation levels are sufficient to attract and retain world-class management talent—particularly in competition with private-sector energy companies—is an ongoing concern. The CEO of Equinor earns roughly three times what Fąfara earns. If ORLEN wants to recruit internationally, it will need to offer internationally competitive packages. The state owner's willingness to approve such packages remains untested.

VI. "Hidden" Businesses & Segment Deep-Dive (1:20 – 1:40)

ORLEN's financial statements report five main segments: Refining, Petrochemicals, Energy, Retail, and Upstream. But the real story lies in the businesses that do not fit neatly into any single segment—the "hidden" operations that either generate disproportionate value or represent strategic bets on entirely new markets.

The Norwegian Cash Cow

The single most important asset ORLEN acquired through the PGNiG merger is not in Poland. It is beneath the Norwegian Sea.

ORLEN Upstream Norway holds roughly one hundred licences on the Norwegian Continental Shelf, with production from twenty active fields. The crown jewel is a 14 percent stake in Ormen Lange—Norway's second-largest gas field, located in deep water roughly 120 kilometres off the coast of Kristiansund. Ormen Lange's production life extends beyond 2045, making it one of the longest-duration producing assets in the North Sea.

In 2024, ORLEN's Norwegian operations produced approximately 40.5 million barrels of oil equivalent, including 4.5 to 4.6 billion cubic metres of natural gas—a 45 percent increase year-over-year. The company targets 6 billion cubic metres per year from Norway by 2030.

This gas now flows directly to Poland via the Baltic Pipe—a subsea pipeline that entered service in late 2022, running from the Norwegian North Sea through Denmark and across the Baltic seabed to Poland. The Baltic Pipe eliminated Poland's historical dependence on Russian gas imports. It is the physical infrastructure that makes "energy sovereignty" a reality rather than a slogan.

The Norwegian upstream is ORLEN's highest-margin business. It produces in one of the world's most stable regulatory environments, in hard currency (Norwegian kroner and US dollars), with production costs well below those of ORLEN's domestic Polish upstream.

Consider the margin profile. Norwegian gas is produced at relatively low unit costs—the fields are mature, the infrastructure is built, and the Norwegian fiscal regime, while taxing production heavily, provides investment allowances that keep effective costs manageable. The gas is sold at European hub prices, which since 2022 have been structurally elevated compared to the pre-invasion era. The spread between production cost and sale price—the operating margin on each cubic metre—is among the highest of any business within the ORLEN group.

The company targets 6 billion cubic metres per year from Norway by 2030 and 12 billion cubic metres in total gas production across all geographies. If achieved, the Norwegian upstream alone would generate sufficient cash flow to fund a significant portion of the annual renewable energy investment programme.

This is the fundamental alchemy of ORLEN's energy transition model: high-margin hydrocarbon production generating the cash flows that will be reinvested into offshore wind, nuclear, and hydrogen. The irony is not lost on anyone—the company's greenest future depends on the continued profitability of its dirtiest present. But the irony is also the strategy. Without Norwegian gas profits, there is no Baltic Power. Without refining margins, there are no SMRs. The "dirty" businesses are not obstacles to the transition. They are the funding mechanism.

The Petrochemicals Engine — and the Olefins III Debacle

ORLEN's petrochemical operations—based primarily at the Płock complex—produce olefins, polyolefins, PTA, phenol, acetone, glycols, and fertilisers. These are the building blocks of modern industrial chemistry: the plastics, the packaging materials, the synthetic fabrics, the agricultural inputs.

The strategic logic of petrochemicals is compelling. As the world transitions away from burning hydrocarbons for energy, the demand for hydrocarbons as chemical feedstock remains robust—perhaps even grows. People will stop putting oil in their cars. They will not stop using plastics, pharmaceuticals, or fertilisers. Moving from "burning oil" to "making things out of oil" is the refiner's escape route from the energy transition.

The Olefins III project was supposed to be the physical expression of this strategy—a new steam cracker at Płock with 740,000 tonnes per year of ethylene capacity and 340,000 tonnes of propylene, plus five downstream processing units. It was announced as Europe's largest petrochemical investment in twenty years.

The original budget was PLN 13.5 billion—roughly USD 3 billion.

What happened next is one of the more spectacular cost blowouts in European industrial history. Under the Obajtek management, costs escalated to an estimated six times the original budget—somewhere north of PLN 80 billion. The project was halted entirely by Fąfara's team in December 2024.

The cancellation write-downs contributed to ORLEN's depressed FY 2024 net income of PLN 1.5 billion—down from PLN 20.7 billion the prior year. To appreciate the scale of the collapse: ORLEN earned PLN 9.57 per share in FY 2025, a recovery from PLN 1.27 in the impairment-laden FY 2024, but the Olefins III write-down alone likely exceeded the entire project's original budget.

The Olefins III failure carries important lessons about the risks of megaproject execution in state-controlled enterprises. Cost escalation on this scale—six times the original budget—is not a miscalculation. It is a systemic failure of project governance. It suggests that procurement processes were inadequate, contractor oversight was insufficient, and the internal controls that private-sector companies use to contain cost overruns were either absent or ignored. Whether this failure was driven by political interference, management incompetence, or the inherent difficulty of building a world-scale steam cracker during a pandemic is debatable. What is not debatable is the result.

The cancellation freed an estimated PLN 15 billion in remaining committed capital, and allowed management to redirect petrochemical strategy toward a replacement initiative called "Nowa Chemia"—repurposing existing infrastructure beginning around 2030.

In a related move, ORLEN signed a preliminary agreement in March 2026 to acquire full control of Grupa Azoty Polyolefins—a polypropylene plant at Police, on the Baltic coast—for PLN 1.35 billion, expected to close in the third quarter of 2026. The acquisition represents a pragmatic alternative to the megaproject approach: buying existing, operating capacity rather than building from scratch.

Orlen Paczka — The Logistics Surprise

Perhaps the most unexpected business hidden inside ORLEN is Orlen Paczka—a parcel locker network that grew from roughly 1,800 machines at the end of 2022 to approximately 7,000 by late 2025.

The concept was deceptively clever: use ORLEN's 1,900-plus Polish fuel stations as physical beachheads for last-mile logistics. Every station already has electricity, lighting, security cameras, and regular foot traffic. Adding a parcel locker is a modest incremental investment that generates entirely new revenue.

Orlen Paczka became Poland's second most recognised parcel locker brand, with 11 percent market share and 75 percent brand recognition—though it remained a distant second to InPost, the dominant player with 57 percent market share.

In September 2025, under Fąfara's rationalisation programme, ORLEN signed a term sheet with Poczta Polska—the state postal service—for a potential full sale of the Orlen Paczka business. The signal was clear: an energy company should not be in the parcel delivery business, however clever the original thesis.

Baltic Power — Offshore Wind

If Orlen Paczka represents what ORLEN is shedding, Baltic Power represents what it is becoming.

Baltic Power is a 50/50 joint venture with Northland Power of Canada to build a 1.2-gigawatt offshore wind farm in the Baltic Sea, roughly 23 kilometres from the Polish coast. The project involves 76 Vestas V236-15.0 megawatt turbines—each standing over 260 metres tall, roughly the height of a sixty-five-storey building—mounted on 78 monopile foundations driven into the seabed.

Total investment is approximately EUR 4.73 billion, financed through a USD 5.2 billion project finance package assembled from 25 institutions, including the European Investment Bank and the European Bank for Reconstruction and Development.

Construction commenced in February 2025. By early 2026, all 78 monopiles and 76 transition pieces had been installed. More than 30 turbines were operational by August 2025. Full commissioning is expected in the second half of 2026.

When complete, Baltic Power will supply roughly 1.5 million households and reduce CO2 emissions by approximately 2.8 million tonnes per year.

To put 1.2 gigawatts in context: that is roughly equivalent to the output of a mid-sized coal-fired power station, but with zero fuel costs, zero emissions, and a design life of twenty-five to thirty years. The wind, unlike coal, does not need to be purchased or transported. Once the turbines are installed, the marginal cost of electricity generation approaches zero. The economics of offshore wind are fundamentally different from any generation technology ORLEN has operated before.

Baltic Power is the first of four offshore wind farms ORLEN plans in the Baltic Sea, targeting a combined capacity of approximately 5.5 gigawatts. The pipeline includes projects that will likely require partnerships with international developers—ORLEN does not yet have the internal capability to design and execute offshore wind construction without partners like Northland Power.

Strategy 2035 targets 12.8 gigawatts of total installed renewable capacity by 2035—including offshore wind, onshore wind, and solar—plus 1.4 gigawatts of energy storage. Additionally, the company plans to expand its gas-fired combined-cycle gas turbine capacity from 1.8 to 4.3 gigawatts, positioning gas as the "transition fuel" that provides baseload flexibility while renewables scale.

The Nuclear Frontier

The most ambitious—and most speculative—element of ORLEN's energy transition portfolio is nuclear.

ORLEN Synthos Green Energy (OSGE), a 50/50 joint venture with Synthos Green Energy, is pursuing the deployment of GE Vernova Hitachi Nuclear Energy BWRX-300 small modular reactors across Poland. The plan calls for 24 reactors, with the first unit at Włocławek targeted for 2032. Strategy 2035 targets 0.6 gigawatts of installed SMR capacity by 2035.

In February 2026, a Poland Generic Design Agreement was signed at the US Department of Energy in Washington DC—a preliminary regulatory milestone. OSGE has sought environmental permitting for six Polish locations.

The caveat is significant: no operating BWRX-300 reference plant exists anywhere in the world. ORLEN is betting on frontier technology that has never been commercially demonstrated at scale. The first-mover risk is real—but so is the first-mover advantage if the technology works.

To understand why Poland is so interested in nuclear, one must understand the baseline: Poland currently generates roughly 70 percent of its electricity from coal. That is not a typo. In 2026, one of the EU's largest economies remains overwhelmingly dependent on the dirtiest fossil fuel for its electricity supply. The EU Emissions Trading System makes every tonne of coal-fired carbon dioxide progressively more expensive. Poland's coal plants are simultaneously aging out of their design lives and becoming economically unviable.

The country needs baseload replacement capacity that is low-carbon, dispatchable (meaning it can generate electricity on demand, unlike wind or solar), and scalable. SMRs tick all three boxes—if they work, if they can be built on time, and if costs can be controlled. Those are three significant "ifs." But the alternative—continuing to burn coal at escalating carbon prices while building intermittent renewables that require expensive storage and grid reinforcement—may be even riskier.

ORLEN Charge — The EV Infrastructure Play

One final hidden business deserves mention: ORLEN Charge, the company's electric vehicle charging network.

ORLEN operates over 1,200 charging points across Poland, with modern hubs offering up to 400-kilowatt fast charging capability. The network is expanding rapidly into Germany—where ORLEN plans to add 160 new high-power charging points by end of 2026 through partnerships with regional operators—and into the Czech Republic and Lithuania.

The strategic logic mirrors the parcel locker thesis but with a critical difference: while Orlen Paczka is being sold off as non-core, ORLEN Charge is being doubled down on. The reason is obvious. A fuel station company must eventually become a charging station company. The customer who today fills up with diesel will tomorrow plug in an EV. If ORLEN does not own the charging infrastructure, it loses the customer—and the station becomes an empty forecourt.

Every fuel station is a potential charging hub. The real estate, the electricity connection, the customer foot traffic, the convenience retail—all transfer seamlessly to an EV charging model. ORLEN's 3,400-station network is not just a retail fuel asset. It is a pre-built EV charging platform waiting to be activated.

VII. The Playbook — Hamilton's 7 Powers & Porter's 5 Forces (1:40 – 1:55)

Hamilton Helmer's 7 Powers

Four of Helmer's seven powers are present at ORLEN, in varying degrees of durability.

Scale Economies. ORLEN's distribution network—3,400 stations across seven countries, pipelines connecting refineries to terminals, gas storage facilities, electricity distribution grids—creates per-unit cost advantages that no competitor can match in the Central European geography. The fixed costs of operating a pipeline from Płock to Warsaw are the same whether you push 100,000 barrels per day or 200,000. The more volume flows through the system, the lower the per-unit cost. This is classical scale economics, and ORLEN's post-merger asset base has pushed it to a level where no regional competitor comes close.

Switching Costs. In retail fuel, switching costs are negligible. A driver will buy petrol wherever the price is lowest or the station is most convenient. But in ORLEN's industrial gas and electricity businesses—the PGNiG and Energa legacies—switching costs are extraordinarily high.

An industrial customer consuming millions of cubic metres of natural gas per year under a multi-year supply contract cannot easily switch providers. The physical pipeline connection, the metering infrastructure, the billing system, the regulatory framework—all create friction. A factory connected to ORLEN's gas grid would need to build new physical infrastructure to receive gas from a competitor, assuming a competitor even has pipeline access to that location. In many cases, ORLEN is the only supplier with physical connectivity—not because of any legal monopoly, but because of the geography of installed infrastructure.

Cornered Resource. ORLEN's physical infrastructure—refineries, pipelines, terminals, storage facilities, distribution grids—constitutes a cornered resource in Helmer's framework. These are not assets that can be replicated by writing a cheque. Building a refinery takes a decade of permitting, environmental review, and construction. Laying a pipeline requires rights-of-way, regulatory approval, and years of excavation. Installing an electricity distribution grid serving three million customers requires decades of accumulated infrastructure.

The 14 percent stake in Ormen Lange is a particularly pure example. Norwegian Continental Shelf licences are allocated by the Norwegian government through competitive rounds that occur infrequently and are oversubscribed. New entrants cannot simply purchase production—they must win regulatory approval, demonstrate technical capability, and secure financing for deepwater operations. ORLEN inherited these licences through PGNiG, which had been building its Norwegian portfolio for decades. The time-to-capability gap is measured not in years but in generations.

Counter-Positioning. This is the most intellectually interesting power at work.

ORLEN is using the cash flows from its "dirty" oil refining and gas production to build the "clean" infrastructure—offshore wind, nuclear, EV charging—that will eventually make the refining business obsolete. The incumbents it competes against in the green space—pure-play renewable developers, European utilities—do not have access to the same cash generation. And the companies it competes against in the hydrocarbon space—other refiners—are not investing at the same rate in renewables.

ORLEN sits between two worlds, funding the future from the profits of the past. Counter-positioning works when incumbents in one market cannot rationally adopt the new strategy because it would cannibalise their existing business. For ORLEN, the opposite is true: it is rationally cannibalising its own refining business because the alternative—being a pure-play refiner in 2040—is economic suicide.

Porter's Five Forces

Barriers to Entry: Very high. The combined capital cost of replicating ORLEN's integrated asset base—refineries, pipelines, retail network, gas distribution, power generation, upstream production—exceeds EUR 50 billion. No new entrant could credibly assemble this portfolio in less than two decades. The barrier is not regulatory (though regulation helps); it is physical. These are atoms, not bits.

Threat of Substitutes: Mixed. For transportation fuel, the threat is existential—electric vehicles are the substitute, and their adoption curve is accelerating. For industrial gas and heat, the threat is lower—natural gas has no near-term substitute for many industrial processes. For petrochemicals, the threat is minimal—there is no substitute for ethylene as a feedstock for polyethylene. ORLEN's multi-utility structure hedges across these different substitution timelines.

Buyer Power: Moderate. In retail fuel, buyers have near-perfect price transparency and minimal switching costs. In industrial gas, buyer power is constrained by physical infrastructure and contract terms. In electricity distribution, prices are regulated—buyers have no power at all.

Supplier Power: Significantly reduced by vertical integration. Before the PGNiG merger, ORLEN was dependent on external gas suppliers—primarily Russia. Today, ORLEN produces its own gas in Norway and distributes it through its own pipeline. Before the Lotos merger, crude supply was concentrated. Today, the Aramco relationship plus seaborne access via the Gdańsk refinery provides diversification. Supplier power has been structurally neutralised by the multi-utility consolidation.

Competitive Rivalry: Intense in retail fuel (MOL, Shell, BP are all active in the region) but manageable in gas distribution (near-monopoly) and electricity distribution (regulated, territorial). The competitive landscape differs radically by segment—which is precisely why the multi-utility structure exists. ORLEN does not need to win every battle. It needs to win enough battles across enough segments to generate the aggregate cash flow that funds the transition.

VIII. Business & Strategy Lessons (1:55 – 2:10)

The "National Champion" Playbook

The most fundamental question ORLEN raises is whether a state-controlled entity can ever be as efficient as a private one.

The evidence is mixed. On one hand, the Obajtek era produced the strategic vision that created the multi-utility structure—a vision that no private-sector CEO, answerable to quarterly earnings, would likely have pursued. The three mergers were bold, strategically sound, and ultimately transformative. On the other hand, the same era produced the Olefins III cost blowout, the Polska Press acquisition, the questionable Aramco pricing, and the pre-election fuel price suppression.

State control enables long-duration strategic thinking. It also enables abuse of corporate resources for political purposes. The ORLEN experience suggests that these two outcomes are not alternatives—they are simultaneous. The same governance structure that allowed the multi-utility pivot also allowed the detective agency contracts and the media acquisition.

The lesson for investors is not that state ownership is inherently good or bad. It is that state ownership introduces a specific risk factor—political capture—that must be priced independently of the underlying business economics. The 20 to 30 percent EV/EBITDA discount that ORLEN trades at versus Western peers is the market's estimate of that political risk premium. Whether the discount is too large or too small depends entirely on one's assessment of Polish democratic institutions and the durability of the current governance reforms.

Vertical Integration as Survival

The second lesson is that "pure-play" refiners are a dying species. The companies that will survive the energy transition are those that own multiple links in the energy value chain—upstream production to hedge feedstock costs, downstream retail to capture consumer margins, electricity generation to participate in the power transition, and petrochemicals to preserve hydrocarbon demand beyond the transportation fuel era.

ORLEN understood this earlier and executed it more aggressively than any European peer except possibly TotalEnergies. The result is a company that generates cash from natural gas production in Norway, refining in Poland, fuel retail in Germany, electricity distribution in northern Poland, and—increasingly—offshore wind in the Baltic Sea. No single commodity price, no single technology disruption, and no single regulatory change can kill all of these businesses simultaneously.

The multi-utility structure is not elegant. It does not lend itself to a simple equity story. Analysts struggle to value it because the components span different industries with different multiples and different growth profiles. But it is resilient—and in a world where the energy transition creates existential risk for single-product companies, resilience may be the most valuable attribute a business can possess.

The "Regulated Monopoly" Paradox

The third lesson concerns the inherent tension between social responsibility and fiduciary duty.

ORLEN's state owner expects the company to keep pump prices low, maintain employment in refinery towns, fund national energy infrastructure, and deliver dividends to the Treasury. These objectives frequently conflict. Every złoty spent suppressing fuel prices before an election is a złoty not paid to shareholders or invested in wind farms. Every employee retained at an uneconomic facility is a drag on margins.

The progressive dividend policy—guaranteed annual increases of PLN 0.15 per share—is an attempt to formalise the balance. The FY 2024 dividend was PLN 6.00 per share, yielding roughly 4.7 percent at the current price. But the real test comes when Strategy 2035's capital expenditure ramps to PLN 48 billion in its peak spending year of 2027. If cash flows tighten, will the state accept lower dividends to fund wind farms? Or will it force ORLEN to borrow—adding leverage to a balance sheet that is currently conservatively geared at 0.55 times net debt to EBITDA?

The answer will reveal whether the Polish state views ORLEN as a public company with a strategic mandate or as a government department with a stock listing.

There is a historical parallel worth noting. France's EDF—Électricité de France—operated for decades as a state-controlled utility that was expected simultaneously to provide cheap electricity to French consumers, maintain employment in nuclear communities, fund massive capital programmes, and deliver returns to the state. The tension between these objectives eventually contributed to EDF accumulating more than EUR 60 billion in debt and being taken fully private by the French state in 2023.

ORLEN's management insists that its situation is different—that the multi-utility structure provides revenue diversification that EDF lacked, and that the state's commitment to maintaining a public listing imposes market discipline that EDF avoided. Whether this distinction proves meaningful or merely semantic will depend on how the capital allocation decisions of the next decade play out.

IX. Bear vs. Bull Case & Analysis (2:10 – 2:25)

The Bear Case

The bear case against ORLEN rests on three pillars.

Political risk. The State Treasury's 49.9 percent stake means that ORLEN's management, strategy, and capital allocation are all hostage to Polish electoral politics. The company has had two CEOs in less than three years—and the current CEO serves at the pleasure of a coalition government whose own stability is not guaranteed. Every governance reform implemented by Fąfara could be reversed by a future administration. The "state discount" in the valuation is not a market inefficiency to be arbitraged—it is a permanent structural feature of the investment.

Capital commitment. Strategy 2035 envisions PLN 350 to 380 billion in cumulative capex over a decade. Even for a company generating PLN 46 billion in annual operating cash flow, this is an enormous commitment. Peak spending of PLN 48 billion in 2027 will require significant external financing—either debt or equity—at a time when European interest rates may remain elevated. The Olefins III debacle demonstrates that ORLEN has a documented track record of cost overruns on large industrial projects. If offshore wind or nuclear costs escalate similarly, the financial consequences could be severe.

White elephant risk. The SMR nuclear programme is betting on technology that has never been commercially demonstrated. The EV charging network is competing against private-sector specialists with lower cost structures. The petrochemical replacement strategy—"Nowa Chemia"—is replacing one megaproject with another, albeit more modestly scoped. Each of these initiatives carries execution risk that compounds across the portfolio.

There is a deeper structural concern: is ORLEN attempting too many things simultaneously? The portfolio spans refining, petrochemicals, electricity generation, electricity distribution, gas production, gas distribution, offshore wind, nuclear, EV charging, and retail convenience—across seven countries. This is not diversification. It is "diworsification"—the risk that management attention is spread so thin across so many disparate businesses that none receives the focus required to achieve operational excellence.

The GE comparison is instructive. General Electric under Jack Welch and Jeff Immelt became a conglomerate that spanned jet engines, power turbines, healthcare equipment, media (NBC Universal), financial services (GE Capital), and consumer appliances. The theory was that diversification reduced cyclicality and that "GE management systems" could run anything. The reality was that complexity destroyed value, capital allocation became opaque, and the financial services tail eventually wagged the industrial dog. GE's subsequent breakup into three separate companies—GE Aerospace, GE Vernova, and GE HealthCare—was an explicit acknowledgment that the conglomerate model had failed.

ORLEN's defenders would argue the comparison is inapt: unlike GE, all of ORLEN's businesses are connected through the energy value chain. Gas production feeds power generation. Refining produces petrochemical feedstock. Retail stations serve as platforms for EV charging. The portfolio is a system, not a collection of unrelated businesses. But the GE counter-argument remains: even when businesses are theoretically connected, the management complexity of operating them all simultaneously under one roof may exceed the integration benefits.

The Bull Case

The bull case rests on equally compelling foundations.

Regional hegemony. ORLEN is the only company in Central Europe with the balance sheet, the infrastructure, and the political mandate to build the energy systems of the future. No competitor—not MOL, not OMV, not any domestic Polish company—can credibly build offshore wind farms, deploy SMR nuclear reactors, operate an EV charging network, and maintain refining capacity simultaneously. ORLEN's scale is not just a cost advantage. It is a prerequisite for participation in the energy transition at the required pace.

Balance sheet strength. Net debt to EBITDA of 0.55 times is extraordinarily conservative for an integrated energy company. ORLEN has more financial headroom than any comparable European player. Fitch rates the company BBB+ with a stable outlook. Free cash flow was PLN 16.5 billion in FY 2025. The company is not leveraged—it is under-leveraged. The capacity to invest is real.

Valuation arbitrage. ORLEN trades at 3.4 times trailing EBITDA versus 4.7 times for TotalEnergies and 5.2 times for Shell. If the governance reforms stick—if the Polska Press divestiture completes, if the Olefins III write-downs are absorbed, if the new management team demonstrates operational credibility—there is no fundamental reason for a 30 percent discount. Even a partial re-rating to 4.0 times would imply significant share price appreciation.

The regulatory tailwind is structural. The EU's climate legislation—the Fit for 55 package, the Carbon Border Adjustment Mechanism, the revised Emissions Trading System—systematically increases the cost of carbon-intensive activities and systematically favours companies investing in decarbonisation. ORLEN's Strategy 2035, with 40 percent of capex directed toward green and transition investments, positions the company on the right side of regulatory momentum. Companies that are not investing in the transition will face rising carbon costs with no offsetting revenue from renewables. ORLEN will face the same rising carbon costs—but will have 12.8 gigawatts of renewable capacity generating carbon-free revenue.

The Aramco relationship has strategic value. Whether the sale price was fair or not, the relationship exists. A ten-year crude supply agreement with the world's largest oil producer provides supply certainty that no comparable Central European company enjoys. As the global energy market fragments along geopolitical lines—with some crude flows sanctioned, others restricted, and others politically sensitive—guaranteed access to Saudi crude is genuinely valuable.

Key KPIs

For investors tracking ORLEN's ongoing performance, two metrics cut closest to the trajectory of the business.

EBITDA per barrel of oil equivalent processed measures the integrated margin across the entire value chain—from upstream gas production through refining to retail distribution. This metric captures whether the multi-utility structure is actually creating value through vertical integration, or whether the complexity is destroying margins. A rising EBITDA per barrel indicates that the integration synergies are real—that owning the gas field, the pipeline, the refinery, and the station simultaneously generates more value than owning each separately. A falling one suggests that the operational complexity is overwhelming the theoretical benefits of scale. In FY 2025, ORLEN generated PLN 39.6 billion in EBITDA on consolidated revenue of PLN 267 billion—an EBITDA margin of approximately 14.8 percent. Tracking how that margin evolves as the integration matures and the renewable assets begin generating revenue will tell investors more about the strategy's success than any individual project milestone.

Net debt to EBITDA measures the pace at which Strategy 2035's capital programme consumes the balance sheet. At 0.55 times today, the ratio provides enormous headroom. The critical question is where this ratio sits in 2027—the peak spending year. If it remains below 2.0 times, the capital programme is self-funding. If it breaches 2.5 times, the company may need to raise equity or cut dividends. This single ratio captures the tension between the scale of ORLEN's ambitions and the capacity of its balance sheet to fund them.

X. Conclusion — Final Reflections (2:25 – 2:35)

In Central Europe, energy is not a commodity. It is geography.

Poland sits on the North European Plain—flat, exposed, historically vulnerable to pressures from both east and west. For centuries, Poland's security depended on the willingness and ability of its neighbours to refrain from invasion. Energy security follows the same logic: for decades, Poland depended on the willingness of Russia to continue supplying crude oil and natural gas.

ORLEN exists because Poland decided it could no longer afford that dependence.

The multi-utility consolidation—Energa, Lotos, PGNiG—was not a typical corporate strategy exercise. It was an act of state-building, executed through the mechanism of a publicly listed company.

The result is an entity that controls the production, transportation, refining, distribution, and retail sale of energy across Central Europe—from the Norwegian Continental Shelf to the German Autobahn. It operates refineries in four countries. It distributes electricity to three million households. It produces gas from twenty fields in Norway's deepest waters. It runs filling stations in seven nations. And it is building wind turbines in the Baltic Sea, pursuing nuclear reactors in the Polish heartland, and rolling out electric vehicle chargers on the Autobahn.

There is no company in Europe—and perhaps no company in the world—with a comparable combination of geographic scope, vertical integration depth, and energy transition ambition relative to its size. TotalEnergies is larger. Shell is more globally diversified. Equinor has more upstream production. But none of them combines all of these elements across a single, coherent geography the way ORLEN does across Central Europe.

Whether this is the blueprint for how a fossil fuel giant survives 2050 or a cautionary tale about the limits of state-directed capitalism depends on execution. The strategy—scale through consolidation, fund the transition through hydrocarbon cash flows, build renewable capacity before the regulatory cliff arrives—is sound. The governance—a controlling state shareholder, management turnover with every election, documented instances of political capture—is not.

The Lotos and PGNiG mergers were strategically necessary. They created a company with the scale and diversification to survive the energy transition. The execution—the Aramco pricing, the Olefins III blowout, the media acquisition—was uneven at best. The new management team under Fąfara has moved quickly to rationalise the portfolio and restore investor credibility. Whether those reforms survive the next election cycle remains the central uncertainty.

ORLEN trades at a 30 percent discount to Western European majors—3.4 times trailing EBITDA versus 4.7 times for TotalEnergies and 5.2 times for Shell. The stock has roughly doubled from its fifty-two-week low of PLN 62.34 to approximately PLN 128.58 as of early April 2026, suggesting the market is beginning to price in the operational recovery and strategy reset.

That discount prices in the political risk, the governance uncertainty, and the execution challenges. It does not price in the Norwegian upstream assets producing 40 million barrels of oil equivalent per year, the Baltic Power wind farm approaching commissioning, the strongest balance sheet in the Central European energy sector at 0.55 times net debt to EBITDA, the progressive dividend yielding roughly 4.7 percent, or the strategic relationship with Saudi Aramco.

The current market capitalisation of approximately PLN 149 billion—roughly EUR 35 to 36 billion—places ORLEN in the same range as OMV but at a fraction of the multiple applied to TotalEnergies, despite operating an asset base that spans more segments and more geographies than the Austrian company.

Somewhere between those two valuations—the discount for what ORLEN is, and the premium for what it could become—lies the answer to the most interesting question in Central European energy: can a national champion also be a world-class company?

The answer, as with so much about ORLEN, depends on the next election—and the one after that. In the meantime, the turbines are turning in the Baltic, the gas is flowing from Norway, and the stations are still pumping fuel from Berlin to Vilnius. Because in Central Europe, energy is not just a commodity. It is geography, it is sovereignty, and it is the most consequential corporate experiment on the continent. The experiment continues.

References

- PKN ORLEN Annual Reports and Investor Presentations (2020–2025)

- ORLEN Strategy 2035 announcement, January 2025

- PKN ORLEN FY 2025 results, March 2026

- Merger of PKN ORLEN and Grupa Lotos, August 1, 2022

- Merger of PKN ORLEN and PGNiG, November 2, 2022

- Energa tender offer and acquisition, April 30, 2020

- NIK (Supreme Audit Office) Report on ORLEN-Lotos asset divestitures, February 2024

- Saudi Aramco-Rafineria Gdańska agreements, November 30, 2022

- MOL Group station swap agreements, 2022

- Baltic Power project updates, ORLEN corporate website (2025–2026)

- ORLEN Synthos Green Energy BWRX-300 announcements (2025–2026)

- Ireneusz Fąfara appointment announcement, April 11, 2024

- Daniel Obajtek immunity decision, European Parliament, October 7, 2025

- Fitch Ratings: PKN ORLEN BBB+ stable

- Baltic Pipe commissioning, Q4 2022

- Olefins III project halt announcement, December 2024

- Grupa Azoty Polyolefins preliminary acquisition agreement, March 2026

- Notes from Poland investigative reporting on ORLEN governance (2024–2025)

- Reporters Without Borders, Press Freedom Index (Polska Press coverage)

- EU Emissions Trading System, Fit for 55 package, Carbon Border Adjustment Mechanism documentation

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube