Ocado Group: The Operating System for Global Grocery?

I. Introduction & Episode Roadmap

Picture three young men in the late 1990s, sitting on a fixed-income trading desk at Goldman Sachs in London, moving bonds around for institutional clients. They are good at it. They are paid extraordinarily well for it. And then they walk away from all of it to go sell groceries.

Not just sell groceries — to build, from absolutely nothing, a fully vertically integrated online supermarket in a country where, at the time, almost nobody bought their weekly shop over the internet. No stores. No brand. No supply chain. Just a thesis that the future of grocery would be picked not by a person pushing a trolley down an aisle, but by machines in a giant warehouse. That thesis would, over the next twenty-six years, make Ocado one of the most extraordinary and most polarizing stories in the history of the London Stock Exchange.

Here is the paradox that makes Ocado so endlessly debatable. Depending on which afternoon you ask, and which analyst you ask, Ocado is one of three completely different companies. It is a low-margin British grocery delivery business that has spent most of its life losing money. It is a genuinely world-class deep-tech robotics pioneer whose engineering rivals anything coming out of Silicon Valley or Boston. And it is one of the great battleground stocks of the modern era — a name that has minted fortunes for traders on the way up and incinerated them on the way down, in roughly equal measure.

The numbers tell the rollercoaster better than words can. Ocado floated in 2010 at 180 pence a share, into the teeth of a City establishment that thought the whole idea was a money-burning hobby for ex-bankers who should have known better. A decade later, in the strange, accelerated world of the COVID pandemic, the stock touched nearly £29. At that peak, the market briefly valued this perennially loss-making company at more than £20 billion — larger, for a giddy moment, than Tesco and Sainsbury's, the two giants of British grocery, combined. And then, just as violently, it fell back to earth, shedding roughly 90% of its value and dropping back below 200 pence, almost exactly where it had started its public life more than a decade earlier.

So which is the real Ocado? That is the question this episode tries to answer. And the deeper question underneath it is a thesis about the future of retail itself. Ocado's bet is that grocery — the most logistically brutal corner of all of retail, with its razor-thin margins, its perishable goods, its frozen and chilled and ambient temperature zones, its enormous range of products — will ultimately be won by whoever has the best automation. Ocado believes it has built that automation: a hyper-engineered "robot hive" that it now wants to license to every major grocer on earth as the operating system for online grocery. The bears believe something almost opposite — that the centralized, capital-devouring mega-warehouse is a beautiful machine built for the wrong economic era, a relic of zero-interest-rate thinking now colliding with a world of 5% rates and cautious customers.

Over the next several hours, we are going to trace the whole arc. The improbable founding and the brutal early years tethered to Waitrose. The audacious pivot from selling groceries to selling software and robots. The Kroger deal that re-rated the company into the stratosphere, and the pandemic that took it even higher. The acquisition spree, the great robotics-valuation bubble and its bursting, and the multi-year patent war with a Norwegian rival. The painful hangover of warehouse closures and partner pullbacks. The compensation battles around founder-CEO Tim Steiner, who is still, twenty-six years on, the man at the helm. The hidden businesses that almost nobody talks about — robotics for pharma and apparel, a bet on self-driving cars, micro-warehouses for one-hour delivery. And finally, the full bull-and-bear war-game, the frameworks, and the handful of numbers that actually matter if you want to follow this story from here.

Let's go back to the beginning, to the year 2000, and to three bond traders who decided they were going to deliver your bananas.

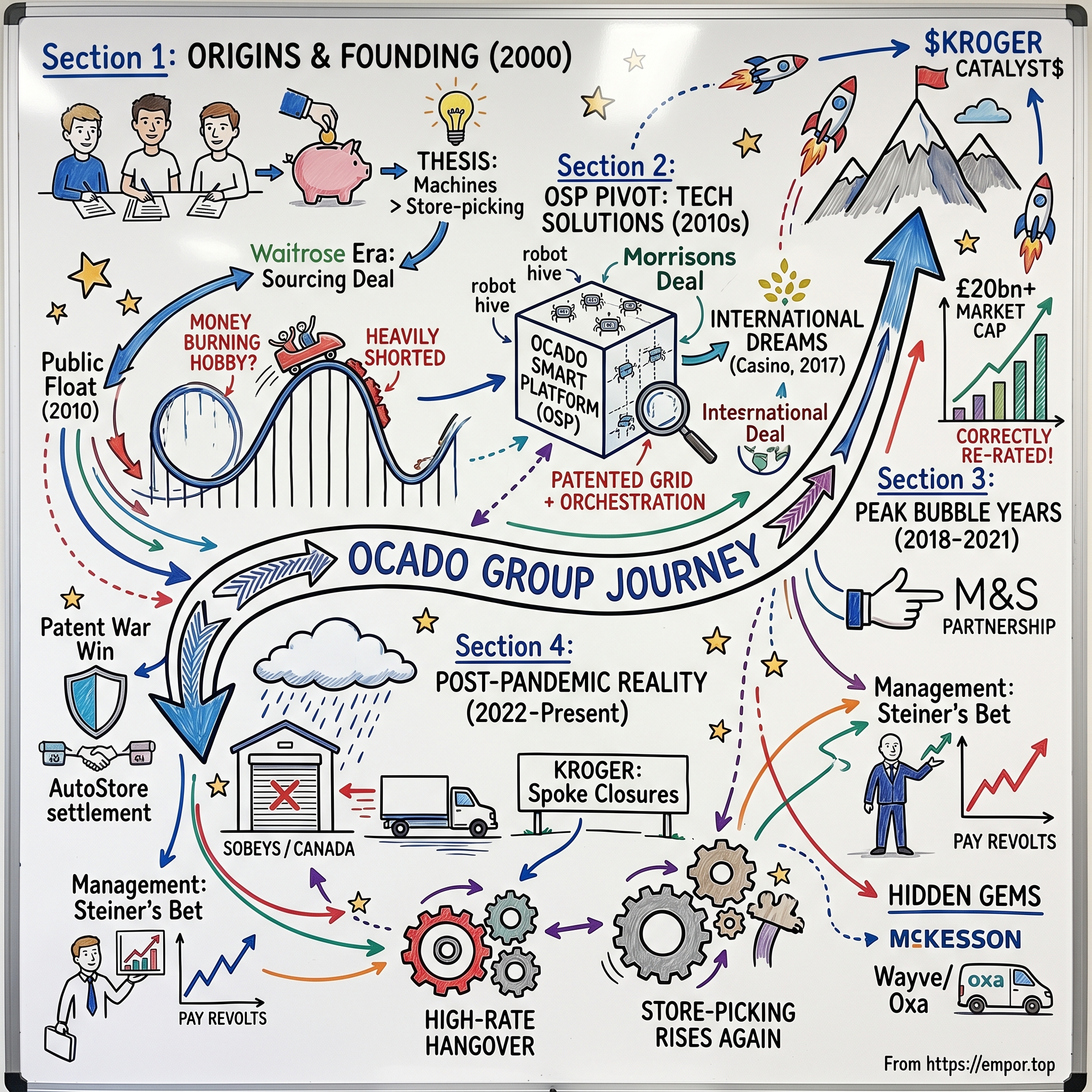

II. The Origins and the Waitrose Era (2000–2010)

The founding story has the texture of a dare. In April 2000, at the very crest of the first dot-com boom, Tim Steiner, Jason Gissing, and Jonathan Faiman — all alumni of Goldman Sachs, all in their early thirties — left the security of investment banking to start an online grocer.[^1] The timing looks insane in hindsight: within twelve months the dot-com bubble would burst spectacularly, and the graveyard of e-commerce was about to fill up with cautionary tales, most famously the American online grocer Webvan, which raised and then vaporized vast sums of capital trying to do more or less what Ocado proposed to do.

But the founders had an insight that separated them from the doomed crowd, and it is worth dwelling on because it became the company's entire genetic code. They believed that online grocery could never be made profitable through "store-picking." Store-picking is exactly what it sounds like: when you order online, an employee — or today, a gig worker — walks into a normal supermarket, pushes a cart up and down the aisles, and picks your items off the same shelves a regular shopper uses. It is cheap to start because you use stores you already have. But it is operationally miserable. The picker competes for space with actual customers, the store was never designed for it, items are constantly out of stock, and the labor cost per order is stubbornly high. The economics, the founders concluded, simply do not close.

The alternative was radical and terrifyingly capital-intensive: build a purpose-built warehouse — what the industry calls a Customer Fulfillment Centre, or CFC — designed from the ground up to do nothing but assemble online grocery orders efficiently. Centralize the inventory, optimize every motion, and let scale and engineering do what cramped store aisles never could. The problem, of course, is that you have to build the thing. And then you have to build the delivery fleet, the routing software to send those vans on efficient loops, the warehouse management systems, the website — essentially the entire stack, from the customer's screen to the bag on their doorstep. Established grocers, who were politely approached, mostly scoffed. Why pour hundreds of millions into a speculative warehouse when you already have stores on every high street?

That scoffing forced the defining decision of Ocado's early life: if no one would build the technology for them, they would build it themselves. This is the seed of everything that came later — the idea that Ocado was, even when it looked like a delivery company, secretly a technology company that happened to deliver groceries.

What it could not build itself was a brand and a grocery supply chain, and that is where Waitrose came in. Waitrose, the upscale, employee-owned British grocer beloved of the middle classes, struck a sourcing agreement that became Ocado's lifeline. The arrangement was elegant in its division of labor: Waitrose supplied the products and the trusted premium brand that reassured customers their salmon and their wine would be good; Ocado supplied the warehouse, the technology, the logistics, and the vans on the road. For a young company with no name recognition, borrowing Waitrose's halo was the difference between a credible proposition and a curiosity. The first deliveries went out in 2002, and through the 2000s Ocado slowly, expensively built a real and loyal customer base, particularly in and around London.

But "slowly and expensively" is the operative phrase. Ocado lost money year after year. Building warehouses and writing software from scratch consumes cash the way a furnace consumes coal, and the company's path to profit was always somewhere out on the horizon, never quite underfoot. Which set the stage for the second defining drama of the early era: the 2010 initial public offering.

The float, in July 2010, was one of the most contentious London had seen in years. The City's skeptics were vocal and they were many. Online-only grocery, they argued, was a structurally unprofitable hobby; the company had never made money; the valuation was a fantasy. Demand was soft enough that the IPO priced at 180 pence, below the original indicated range, and the shares promptly sagged in early trading.[^1] The stock became, almost immediately, one of the most heavily shorted names on the exchange — a magnet for hedge funds betting that the whole edifice would eventually collapse under its own cash burn.

Tim Steiner, for his part, was defiant. Where the shorts saw a doomed delivery business, he saw something else entirely taking shape inside the warehouses — and the deeper the company dug into the brutal margin math of physical grocery, the more convinced he became that the only escape was to climb up the stack, away from the misery of retail margins and toward the high ground of technology. Those early operational scars, the years of grinding to make the unit economics work, were precisely what convinced Steiner that Ocado's real prize was not selling groceries at all. It was selling the machine that sold the groceries. That conviction would, over the following decade, completely transform what kind of company Ocado was — and what the market was willing to pay for it.

III. The Smart Platform Pivot: Moving Up the Stack (2011–2017)

To understand the pivot that made Ocado famous, you have to first stand inside one of its early warehouses and notice what was wrong. By the early 2010s, the company had built large fulfillment centres that used the best available automation of the day — conveyor belts snaking for miles, cranes, the kind of equipment you would find in any advanced distribution facility. And it worked, more or less. But the engineers kept running into the same wall: this technology was built for a different problem.

Conventional warehouse automation was designed to move pallets and boxes of relatively uniform, non-perishable goods. Grocery is the opposite of that. A single customer order might contain a hundred different items spanning frozen peas, a chilled yogurt, a bunch of bananas that bruise if you look at them wrong, a heavy bag of flour, and a fragile carton of eggs — all of which must be picked quickly, kept at the right temperature, and assembled into bags in the right sequence so the eggs don't end up under the flour. Conveyor-and-crane systems were too slow and, crucially, too space-inefficient for this. They left vast aisles of dead air. In a business where every square metre of refrigerated warehouse is expensive and every minute of picking time eats into a wafer-thin margin, that inefficiency was fatal.

So Ocado's engineers did the audacious thing again: they reinvented the warehouse from physics first principles. The result was the Ocado Smart Platform, or OSP — and at its physical heart is a piece of engineering best described, in plain terms, as a giant three-dimensional grid, like an enormous aluminum chessboard built upward into a cube. Beneath the top surface of the grid sit the storage bins, stacked in columns dozens deep. And scurrying across the top surface, on rails, are hundreds of robots — each roughly the size of a washing machine — that zip around at speeds approaching nine miles an hour, passing within centimetres of one another without colliding.

It helps to have an analogy. Think of the grid as the world's most densely packed, fully automated game of Tetris, played in three dimensions and at high speed. When an order comes in, the nearest bots converge on the columns holding the needed items, reach down, and pluck out the bins. If the item you want is in a bin buried four deep, the bots will cooperatively dig — lifting the bins above it out of the way, much like you'd unstack cups to reach the one at the bottom — and hand off the right bin to a picking station where the items are assembled into your order. There are no aisles. There is almost no wasted space. The density is staggering.

The part that is genuinely hard to believe is the choreography. Hundreds of independent robots, moving at speed, inches apart, on a shared grid, must never collide and must constantly re-route around one another and around bots that pause to dig. Ocado had to build, essentially, an air-traffic-control system for robots — orchestration software running on custom, ultra-low-latency radio links, making thousands of decisions per second to keep the swarm flowing. This is the part competitors found hardest to copy, and it is the part that turned a warehouse into intellectual property.

And here is where the business model pivot becomes inseparable from the technology. Once you have built something this good — a full-stack operating system for online grocery, hardware and software together — why would you keep it locked inside your own modest British grocery business? The far bigger prize is to sell it to grocers all over the world. This was the great reframing: Ocado would stop telling the market "we deliver groceries" and start telling it "we sell the operating system and the robots that power online grocery for the planet's leading retailers." Instead of low-margin retail sales, the dream was high-margin, recurring licensing and fee income — the economics of a software platform rather than a supermarket.

The market needed proof this was real, and Ocado began to supply it. A landmark domestic deal came when rival UK grocer Morrisons agreed to use Ocado's technology and capacity, a striking endorsement because it meant a direct competitor was willing to run its online operation on Ocado's rails. Then came the breakthrough that mattered most for the new narrative: the first major international licensing deal, signed with France's Groupe Casino in 2017.1 An overseas grocer, choosing Ocado's platform to build its own automated warehouses — that was the data point the bulls had been waiting for. Slowly, the way the City talked about Ocado began to change. The word "grocer" started giving way to the word "technology." The re-rating had begun. But it would take a partner on the other side of the Atlantic, and the largest supermarket operator in the United States, to truly light the fuse.

IV. The Kroger Catalyst and the Peak Bubble Years (2018–2021)

On the morning of May 17, 2018, the Ocado share price did something that, for a perennially loss-making British delivery company, was almost surreal: it exploded upward, jumping by roughly half in a single session.[^3] The catalyst was a partnership announcement that, for the bulls, validated everything Steiner had been promising for nearly two decades. Kroger — the largest dedicated supermarket operator in the United States, a company with thousands of stores and revenue counted in the hundreds of billions of dollars — had chosen Ocado.

The deal was, by any measure, enormous. Kroger signed an exclusive partnership for online grocery in the US and committed to building a fleet of automated Customer Fulfillment Centres across America — initially with plans for up to twenty of them.[^3] Critically, Kroger also took an equity stake in Ocado of around 5%, putting hard money on the table and binding the two companies together.[^3] For a company that the City shorts had spent years dismissing, this was the ultimate vindication: the biggest grocer in the world's biggest consumer market had looked at every automation option available and concluded that Ocado's was the one worth betting on, exclusively.

The market's response was not just to raise its estimate of Ocado's future grocery sales. It was to completely re-classify the company. Overnight, Ocado stopped trading like a supermarket — valued on sales and slim margins — and started trading like a high-growth Silicon Valley software platform, valued on the dream of dozens of international partners each paying recurring, high-margin fees for decades. The whole point of a platform is operating leverage: you spend the money to build the technology once, and every additional customer who plugs in adds revenue at very high incremental margin. If you believed Ocado was at the start of a global land-grab to become the default operating system for online grocery, almost any valuation could be justified. And in 2018 and 2019, a lot of people chose to believe.

The next master-stroke was a piece of financial engineering that solved Ocado's oldest problem — how to fund all this without endlessly bleeding cash. In 2019, Ocado struck a joint venture with Marks & Spencer, the storied British retailer. M&S paid £750 million to acquire 50% of Ocado's UK retail business.2 Read that as what it was: Ocado took its lower-margin, capital-hungry domestic grocery operation, sold half of it for three-quarters of a billion pounds, and redeployed that cash into the high-capex global rollout of its platform. It was textbook capital reallocation — pull money out of the mature, margin-thin part of the business and pour it into the part the market was valuing at a premium.

The deal had a poignant casualty. The long Waitrose sourcing relationship — the lifeline that had made Ocado viable in its infancy — came to an end, and in September 2020 M&S products replaced Waitrose on the Ocado website, the culmination of the new joint venture.2 An entire chapter of Ocado's identity, the premium-grocer partnership that had defined its first two decades, closed in a single switchover.

And then came the event no model had forecast: the pandemic. When COVID-19 swept across the world in 2020 and lockdowns shut people in their homes, online grocery went from a convenience to a necessity overnight. Years of projected e-commerce adoption compressed into a matter of months. Demand for home delivery overwhelmed every grocer's capacity, and suddenly the value of a system that could fulfill online orders at massive scale and density looked not speculative but essential. Grocers around the world, watching their store-based operations buckle, rushed to sign automation deals. For Ocado, it was rocket fuel poured onto an already-burning narrative.

The stock went vertical. By early 2021, Ocado shares reached toward £29, and the company's market value briefly crossed £20 billion — the valuation that, as we noted, exceeded Tesco and Sainsbury's combined. Tim Steiner, the defiant founder the shorts had mocked, was now feted as a visionary technologist, a British answer to the platform titans of Silicon Valley. It was the absolute apex of the Ocado story. Flush with a soaring share price and a war chest, the company now did what richly valued companies at the top of a cycle tend to do: it went shopping.

V. M&A, Capital Deployment, and the "Robotics Bubble"

There is a particular kind of decision a company makes only at the top of a bubble, when its own stock is a magic currency and capital feels free. Late in 2020, with its valuation near the stratosphere, Ocado went on an acquisition spree aimed at one strategic gap. For all the brilliance of its grid and its swarm of bots, there was one thing Ocado's robots still could not do well: pick up an individual, arbitrary item — a single can, a single apple, a soft bag of bread — with a robotic arm, the way a human hand can. That last step, "piece-picking," remained stubbornly manual. So Ocado set out to buy its way to the front of the robotic-manipulation field.

It moved on three targets. The largest was Kindred Systems, a maker of AI-powered piece-picking robots, acquired for around $262 million.[^5] Alongside it, Ocado bought Haddington Dynamics, a specialist in advanced, low-cost robotic arms, for roughly $25 million, and later Myrmex, a developer of automated frame-loading and materials-handling robotics, for something in the region of $11 million in 2022.[^5] Taken together, these deals were meant to give Ocado ownership of the entire robotic motion problem — not just moving bins around a grid, but reaching in and grasping the individual products inside them.

Now, the natural question for any investor looking at a bubble-era shopping spree is: did they wildly overpay? And here the story takes an interesting turn, because the honest answer is that, relative to the insanity around them, Ocado was actually fairly disciplined. To see why, you have to look at what robotics assets were fetching in 2021, at the height of the mania. Fetch Robotics, an autonomous-warehouse-robot maker, was acquired by Zebra Technologies for $305 million on something like $10 million of revenue — a multiple of roughly thirty times sales.[^6] Berkshire Grey, another warehouse-robotics company, went public via a SPAC at a valuation that implied something like seventy-seven times its revenue.[^6] Against that backdrop of thirty- and seventy-times-revenue lunacy, Ocado's purchase of Kindred — at a price that worked out to roughly seven-and-a-half times the company's forward revenue — looks almost conservative. In a market that had lost its mind, Ocado was, relatively speaking, one of the more sober buyers in the room.

But the truest measure of just how insane that moment was, and how far the air would eventually come out of the balloon, is a single later transaction. In June 2023, Ocado bought a warehouse-robotics company called 6 River Systems from Shopify for $12.7 million.3 Here is the punchline: Shopify had paid $450 million for that very same company back in 2019.3 Ocado acquired it for a 97% discount to what the previous owner had paid — less than one times its revenue. Let that sink in. A robotics business that was worth nearly half a billion dollars at the peak changed hands, four years later, for roughly the price of a few suburban houses. No statistic captures the rise and collapse of robotics valuations more vividly. The bubble that had carried Ocado's own stock to £29 was the same bubble that had priced 6 River Systems at $450 million; when it burst, it took both numbers down together. The 6 River deal was Ocado, on the other side of the cycle, calmly buying distressed assets from the wreckage — a very different posture from the triumphant buyer of 2020.

While the valuation drama played out, a different and more consequential battle was being fought in courtrooms across several continents. Ocado's most fundamental asset is its intellectual property — the patented design of its cube-storage grid and the orchestration software that makes the swarm work. And a Norwegian company, AutoStore, claimed that Ocado had infringed its patents on cube-storage robotics. Ocado counter-claimed. What followed was a sprawling, multi-year, multi-jurisdiction patent war — exactly the kind of existential legal fight that can either validate a company's IP or gut it.

It ended, in July 2023, decisively in Ocado's favor. Under the settlement, AutoStore agreed to pay Ocado £200 million in cash, and all litigation between the two was dropped.[^8] For investors, the cash mattered, but the signal mattered more. A bruising legal contest had effectively confirmed that Ocado's core technology was genuinely differentiated and defensible — a "cornered resource," in the language of strategy, protected not just by engineering complexity but by patents that had been stress-tested in the most adversarial setting imaginable and held up. That defensibility is one of the strongest pillars of the entire bull case, and we will return to it. But for all the vindication in the courtroom, the macroeconomic ground beneath Ocado's business model was beginning to shift in ways no patent could protect against.

VI. The Post-Pandemic Hangover: Warehouse Closures and the Pivot to "Asset-Light" (2022–2026)

Every thesis that thrives in one economic regime gets tested by the next, and Ocado's whole model was, whether anyone admitted it or not, a creature of the era of free money. The mega-CFC strategy — spend $100 million or more building an enormous automated warehouse, on the promise of fee income flowing for decades — makes beautiful sense when interest rates are near zero, construction is cheap, and online demand only goes up. Starting in 2022, every one of those assumptions reversed at once, and the reversal was brutal.

Inflation drove up the cost of the steel and the construction that go into a giant warehouse just as central banks, fighting that same inflation, raised interest rates from near zero to north of 5%. For a model built on enormous upfront capital, higher rates are poison: they make the future fee income worth far less in today's money and make every borrowed dollar of construction cost far more expensive to service. At the same time, the pandemic tailwind didn't just fade — it partially reversed, as customers, freed from lockdowns, happily returned to shopping in physical stores. The grand economic case for the $100 million mega-warehouse, so compelling in 2020, became genuinely hard to make.

The consequences showed up first, and most painfully, in the behavior of Ocado's partners. Start with Canada. Empire Company Limited, the parent of grocer Sobeys, had been one of Ocado's marquee international wins. But as the economics soured, Empire pulled back hard. It paused indefinitely its planned fourth CFC, in Vancouver, and then in January 2026 moved to close its Calgary online-grocery hub outright.[^9] The financial admission that followed was the more damning signal: in June 2026, Empire reported a roughly $750 million write-down on its e-commerce assets — an enormous accounting acknowledgment that the value it had once ascribed to its Ocado-powered online business simply was not going to materialize.[^9] For investors reading the tea leaves, a write-down of that scale by a major partner is a flashing warning light about the real-world returns on these warehouses, and the kind of impairment that auditors and credit analysts scrutinize closely.

Then came the blow that struck at the very heart of the story: Kroger. The exclusive US partnership that had re-rated Ocado in 2018 carried an exclusivity arrangement that expired at the end of 2025, and as it lapsed, Kroger's posture changed dramatically. In January and February of 2026, Kroger closed operational facilities tied to the Ocado network — shutting "spoke" distribution sites and pulling back its automated footprint, with closures reported across Maryland, Wisconsin, and Florida, and a Nashville spoke facility shut as the e-commerce network was restructured.45 Kroger also walked away from plans for a major new CFC in North Carolina. Most tellingly of all, Kroger pivoted toward exactly the model Ocado had spent its entire existence arguing against: low-capex, store-based picking, in partnership with gig-economy players like Instacart and DoorDash. The largest grocer in America, having tried the centralized mega-warehouse approach, was now hedging hard toward the asset-light alternative.

This is the strategic gut-punch of the whole post-pandemic chapter, and it deserves to be stated plainly: Ocado's foundational thesis — that store-picking could never work and that centralized automation was the only path — was being undercut not by a startup, but by its own flagship customer choosing store-picking. The cheap, capital-free flexibility of letting a gig worker pick from existing shelves turned out to be exactly what cash-conscious grocers wanted in a high-rate world, even at the cost of worse unit economics per order. Ocado's beautiful machine was, in many boardrooms, losing to a person with a shopping cart and a smartphone app.

To its credit, Ocado adapted rather than dug in. The company that had once preached the gospel of the mega-warehouse and nothing else began, out of necessity, to embrace flexibility. It started offering smaller robotic grids, software to make existing stores' picking more efficient (in-store fulfillment, or ISF), and automated micro-fulfillment centres that could be slotted into existing buildings at a fraction of the cost of a full CFC. The pitch evolved from "build this enormous bespoke warehouse" to "let us automate your operation at whatever scale and capital intensity you can stomach." It was a humbling but probably necessary retreat from ideological purity toward meeting customers where they actually were. And presiding over this entire wrenching transition — from peak to trough, from triumphalism to restructuring — was the same man who had started the whole thing in 2000, and whose pay packet had by now become a story in its own right.

VII. Current Management: Tim Steiner's Empire, Incentives, and Revolts

Twenty-six years is a very long time to run anything. Most founders are gone — pushed out, bought out, or burned out — long before their company reaches that age. Tim Steiner is the great exception. Of the three Goldman bond traders who started Ocado in 2000, he is the last one still in the building, still in the chief executive's chair, still the singular human embodiment of the company's strategy and its stubbornness. To understand Ocado in 2026, you have to understand that it remains, in a very real sense, Tim Steiner's company — his bet, his conviction, his refusal to concede that the model is wrong.

That longevity cuts both ways. On one hand, there is a deep alignment between the man and the mission; nobody believes in the OSP thesis more completely than the person who has spent a quarter-century building it. On the other hand, a founder this entrenched, this identified with a single strategy, can struggle to pivot when the evidence turns against him — and shareholders have increasingly worried about exactly that. Nowhere has that tension boiled over more visibly than over the question of how much Tim Steiner gets paid.

Steiner has, for years, been one of the most highly paid and most fiercely criticized chief executives in Britain, and the fights over his compensation have become an almost ritual feature of Ocado's annual meetings. The original flashpoint was something called the Value Creation Plan, or VCP — a performance scheme designed in the boom years that could pay out extraordinary sums if Ocado's share price hit very ambitious targets. It drove major shareholder revolts in 2019 and again in 2022, as investors balked at the sheer scale of the potential awards. In the end, the VCP was effectively scrapped, undone by its own design: the "unprecedented share price volatility" of the post-pandemic crash made its targets — which required the stock price to roughly triple — so unreachable that the scheme lost its point as an incentive. A plan built to reward a soaring share price became meaningless when the share price collapsed.

So the board went back to the drawing board, and in April 2024 it brought forward a new remuneration plan — and promptly walked into another revolt. Nearly 20% of shareholders voted against the pay package, a strikingly large rebellion by the standards of UK corporate governance, where boards generally engineer comfortable majorities.6[^13] The plan was approved, but the size of the dissent was a clear shot across the bow. What had investors so agitated? The new scheme dangled a potential bonus for Steiner of up to £14.8 million — equivalent to a staggering 1,800% of his base salary — but only if the share price climbed all the way back to £29.69 by 2027.6[^13] In other words, the headline number was enormous, but it was contingent on the stock essentially returning to its pandemic peak, a recovery of more than tenfold from where it languished.

The friction was sharpened by the immediate context. While the company was reporting heavy pre-tax losses and the shares were trading around 200 pence — a small fraction of that £29.69 target — Steiner's actual realized total pay for the 2024 financial year rose to about £2.6 million, up from roughly £1.9 million the year before.6[^13] To many retail and institutional investors, the optics were hard to swallow: rising cash pay for the CEO, against a backdrop of mounting losses and a battered share price. Defenders countered that the truly large numbers were purely hypothetical, payable only if Steiner delivered a spectacular recovery that would enrich every shareholder along the way. But the controversy spoke to a deeper unease about whether the incentives were calibrated to reward genuine value creation or simply to backfill the wealth that the crash had wiped out.

There is, however, one fact that complicates any simple "greedy CEO" narrative, and it deserves real weight: Tim Steiner's own money is overwhelmingly tied up in the very stock he is trying to revive. His direct shareholding has been reported in the range of roughly 16.5 to 19.8 million shares, and his total direct and indirect interests amount to something on the order of 27.7 million shares — in the neighborhood of 4.4% of the entire company.7 That is an enormous personal stake, worth a fortune at the peak and a small fraction of that today. Whatever one thinks of the bonus scheme, Steiner did not cash out at £29 and walk away; the overwhelming majority of his net worth rose and fell with the same share price that ordinary shareholders have ridden down. His incentives, for better or worse, are genuinely bound to an eventual recovery — he wins big only if the long-suffering shareholders win first. That alignment is the strongest rebuttal to the pay critics, and it is worth holding in mind as we turn to the parts of Ocado that the pay headlines completely obscure: the businesses growing quietly outside of grocery.

VIII. Hidden Gems and Future Horizons

Here is something that rarely makes the front page of the Ocado story, drowned out as it is by share-price drama and pay revolts: some of the most interesting things the company is doing have nothing to do with groceries at all. Tucked inside the financials and the strategy decks are a handful of bets that, if even one of them lands, could meaningfully reshape what Ocado becomes. They are the optionality in the story — the lottery tickets the market mostly ignores while it argues about warehouse closures.

Start with the one that is already real and already growing: Ocado Intelligent Automation, or OIA. The logic is almost embarrassingly obvious once you hear it. Ocado has spent two decades and enormous sums building the world's best robotic grids, its ultra-lightweight "600 series" bots, and robotic picking arms (branded OCADEX). All of that technology was built to move groceries — but groceries are just one category of stuff that needs to be stored densely and picked quickly. So OIA takes the very same robotics and sells it into completely different industries: apparel, general merchandise, electronics, and, most promisingly, pharmaceuticals and healthcare. Same hardware, same orchestration genius, entirely new and enormous markets that have nothing to do with the cutthroat economics of supermarkets.

And it is working. OIA generated roughly £80 million of high-margin revenue across 2024 and 2025, and — crucially — it landed a landmark contract with McKesson Canada, a major healthcare and pharmaceutical distributor, in 2024.[^15] That McKesson deal matters out of all proportion to its size, because it is proof that Ocado's technology can win in a demanding, highly regulated, non-grocery vertical. If grocers in a high-rate world are skittish about $100 million warehouses, the entire universe of warehousing, logistics, and healthcare distribution is a vastly larger market — and one where Ocado's automation faces less of the perishable-goods misery that makes grocery so hard. OIA is the clearest evidence that the "deep-tech robotics company" framing of Ocado is not just a story for grocery investors; it is a business with its own legs, sitting inside the Technology Solutions segment and growing faster than almost anything else in the group.

The second bet is further out and far more speculative: Wayve. Ocado has invested in the British autonomous-driving startup Wayve, with its total commitment reaching roughly £41.7 million as of Wayve's $1.05 billion Series C funding round, led by SoftBank, in May 2024.[^16] What makes Wayve interesting — and a natural fit for Ocado — is its technical approach. Rather than relying on the expensive, pre-built high-definition maps that most self-driving companies depend on, Wayve pursues a "camera-first, mapless" approach: an AI that learns to drive the way a human does, from what it sees, rather than from a meticulously pre-mapped world. The strategic prize for Ocado is the last mile. If Wayve's technology matures, Ocado could one day offer its global OSP partners not just an automated warehouse but an automated delivery van — a fully autonomous, plug-and-play system that takes a grocery order from the robotic grid all the way to a customer's door without a human driver. The single largest variable cost in grocery delivery is the person behind the wheel; removing them would transform the economics. It is a long shot, but the upside is the kind that doesn't show up in any current valuation.

Related to that is Ocado's partnership with and stake in Oxa, the autonomous-vehicle software company formerly known as Oxbotica, which rebranded in 2023.[^17] Where Wayve aims at public-road delivery, Oxa's relevance to Ocado is more immediate and more contained: autonomous operation in controlled environments. That means autonomous yard management — self-driving trailer trucks and delivery vans maneuvering around the depots and warehouse yards Ocado already controls — and indoor autonomous mobile robots that move goods around inside facilities. Controlled environments are far easier to automate safely than chaotic public streets, which makes Oxa's applications a nearer-term efficiency play that compounds the automation Ocado already sells.

Finally, there is Ocado Zoom, the company's foray into quick commerce. Zoom uses micro-fulfillment centres — small automated warehouses tucked into urban areas — to enable rapid, roughly one-hour grocery delivery. It is, in a sense, Ocado answering the rise of ultra-fast delivery and, more importantly, doing so with far lower capital intensity than a full CFC. Zoom is part of the same broader strategic shift we saw in the asset-light pivot: smaller, cheaper, more flexible deployments that meet customers and partners where the economics actually work today. Taken together, OIA, Wayve, Oxa, and Zoom represent a portfolio of futures — some near, some far — that the market, fixated on the troubles in core grocery, has largely declined to pay for. Whether any of them deserves a price is a question best answered by stepping back and war-gaming the whole business through a strategic lens.

IX. Playbook: Powers, Forces, and Strategic Lessons

So let's put Ocado on the strategy table and dissect it properly, using the two frameworks that serious investors reach for: Hamilton Helmer's 7 Powers, which asks what durable advantages a business actually has, and Michael Porter's Five Forces, which asks how attractive the underlying industry is. The two together explain why Ocado can be simultaneously a genuinely advantaged company and a deeply troubled investment.

Begin with the Powers, because Ocado has some real ones. The strongest is switching costs, and they are about as extreme as switching costs get. When a global retailer adopts OSP, it does not simply install some software. It integrates Ocado's platform into its enterprise systems, its e-commerce storefront, and its physical operations, and then it spends $100 million or more building a bespoke robotic warehouse around Ocado's grid. Having done all that, the cost, disruption, and sheer risk of ripping it out to switch to a rival like AutoStore or Symbotic are close to prohibitive. This is genuine lock-in — the kind that makes existing partner revenue sticky and durable. The painful corollary, as Kroger demonstrated, is that switching costs only bind partners who actually build the warehouses in the first place; they do nothing to stop a partner from simply declining to build the next one.

The second clear power is a cornered resource: the patented cube-storage design and the robotic-orchestration software. This is not a soft claim. It was tested in the most adversarial way possible in the AutoStore litigation and emerged validated, with a £200 million settlement flowing to Ocado. Intellectual property that has survived a multi-jurisdiction patent war is about as proven as a cornered resource can be, and it is the foundation of Ocado's claim to be more than a commodity warehouse builder.

Ocado also has scale economies, though their power is more moderate. The enormous cost of developing the software is essentially fixed — write it once — so each additional international partner that plugs in should, in theory, drop a higher share of its fees straight to the bottom line. That is the operating-leverage dream that justified the platform valuation. The catch is that the hardware and deployment side remains stubbornly capital-intensive, so the pure software-style scale economics are diluted by the very physical heaviness of the model.

The fourth power, counter-positioning, is the one that has visibly eroded, and its erosion is central to the bear case. For years, Ocado's automated CFCs counter-positioned beautifully against legacy grocers, whose physical real estate and store-picking were structurally inferior for online fulfillment — and crucially, those incumbents couldn't easily copy Ocado without cannibalizing their own model. But counter-positioning requires that the incumbent be unwilling or unable to respond. The rise of cheap, hybrid store-picking software from the likes of Instacart handed grocers a third option that needs almost no upfront capital, and that bypassed Ocado's advantage entirely. The very power that once made Ocado special has been routed around.

Now flip to Porter's Five Forces and the picture darkens, because the industry Ocado competes in is structurally tough. The threat of substitutes is very high, and it is the dominant force in the whole analysis: gig-economy store-picking via Instacart and DoorDash requires essentially zero upfront capital from a grocer, which makes it a devastating substitute for Ocado's capital-heavy model precisely when capital is expensive. The bargaining power of buyers is also high — the buyers are giant grocery conglomerates like Kroger and Sobeys, sophisticated counterparties who can, and demonstrably did, pause or cancel rollouts the moment capital constraints bit. And competitive rivalry is intense: Ocado faces Symbotic, the automation company backed by Walmart — the one retailer larger and more formidable than Kroger — alongside AutoStore, Dematic, and others, all chasing the same automation budgets.

The strategic lesson that emerges is subtle and important. Ocado genuinely possesses durable, hard-won powers — the switching costs and the cornered resource are real and rare. But it deploys those powers inside an industry whose forces are punishing, and against a substitute that wins precisely on the dimension — capital intensity — where Ocado is weakest. A company can have a real moat around a castle that sits in a difficult kingdom. That tension is exactly why thoughtful investors can look at the same facts and reach opposite conclusions, which is precisely the debate we turn to now.

X. Analysis: Bear vs. Bull Case

Let's war-game both sides honestly, because Ocado is the rare stock where the bear case and the bull case are each genuinely coherent, and where reasonable, informed people land on opposite sides.

The bear case starts from the macro and works inward. The centralized mega-warehouse model, the bears argue, is simply too capital-intensive to make sense in a world of 5%-plus interest rates; the math that worked at zero rates does not work now, and may not work again for years. On top of that structural problem sits the visible reality of partner churn — the Kroger pullback and the Sobeys closures are not abstractions, they are operating facilities going dark, and because so much of Ocado's recurring revenue is linked to the volume flowing through live sites, every closed warehouse directly erodes the fee stream that the entire platform valuation rests on. Worst of all, the bears point to the cash burn: Ocado continues to spend heavily on research and development — on the order of hundreds of millions of pounds a year — which means the company keeps consuming capital, periodically diluting shareholders or taking on debt to fund a profitability that always seems to sit just over the next ridge. In this telling, Ocado is an engineering marvel that is also a value trap: brilliant technology attached to economics that may never close, in an industry actively routing around its strengths.

The bull case does not deny the troubles; it reframes them as the darkest hour before a dawn. The bulls argue that the closures were largely a Western, high-rate-shock phenomenon, and that the real test of OSP is whether it works at scale in dense, urban markets where land is scarce and delivery distances are short — which is to say, Asia. The crucial proof points are arriving now: a major CFC in Busan with South Korea's 롯데쇼핑 주식회사 Lotte Shopping Co., Ltd., expected to come online in early 2026,8 and sites in the Tokyo area with Japan's イオン株式会社 AEON Co., Ltd. Dense Asian cities are, in theory, the ideal habitat for Ocado's model: when real estate is extraordinarily expensive and customers are packed tightly together, the density of the grid and the efficiency of centralized fulfillment should shine in a way they never quite could in suburban America. If those hubs go live and prove highly profitable, the bulls argue, the entire "the model doesn't work" narrative collapses, because it will turn out the model just needed the right geography.

The bulls' second pillar is OIA — the non-grocery robotics business we examined earlier — which they see as proof that Ocado's technology has a vast addressable market beyond the supermarket, in warehousing, general merchandise, and especially pharma, where the McKesson Canada win is the template. And their third and most concrete pillar is financial: Ocado has targeted becoming cash-flow positive in the second half of 2026. That single milestone, if achieved, would change the story fundamentally — it would mean the company no longer depends on public markets to fund its existence, removing the dilution and going-concern anxieties that have haunted the bear case and giving Ocado the breathing room to let its long-term bets mature on its own balance sheet.

Which brings us to the discipline of focus. With a story this sprawling, it is easy to drown in metrics, so it is worth zeroing in on the few numbers that actually tell you whether the thesis is working — the dials a long-term investor should keep an eye on. The first and most important is free cash flow: is the company actually on track to hit cash-flow breakeven in H2 2026, and does it stay there? Everything in the bear case ultimately reduces to cash burn, and everything in the bull case ultimately reduces to ending it; this is the number that adjudicates between them. The second is the health and growth of live, fee-generating capacity — not announced deals or signed letters of intent, which the boom years proved can evaporate, but actual operational modules running and the order volume flowing through them, since that is what converts the platform promise into recurring revenue. And the third, the optionality dial, is Technology Solutions and OIA revenue, the cleanest read on whether the high-margin, capital-light, non-grocery future is genuinely arriving or merely being promised. Watch those three, and you will understand the Ocado story as it unfolds far better than any single quarter's headline loss can tell you.

XI. Epilogue & Outro

Step back from the noise — the £29 peak, the 90% crash, the pay revolts, the courtroom battles, the warehouses going dark — and a single, almost poignant shape emerges from the Ocado story. This is, at its core, the tale of an engineering masterpiece that got caught in the crosshairs of a macroeconomic cycle it could not control.

There is no serious argument that Ocado's technology is not extraordinary. The grid, the swarm of bots choreographed inches apart at nine miles an hour, the orchestration software that survived the most adversarial patent challenge a rival could mount — these are genuine triumphs of engineering, the product of a quarter-century of obsessive iteration. Three bond traders who had never run a warehouse in their lives ended up building, from a blank sheet of paper, what are arguably the most advanced grocery-fulfillment robots on the planet. That part of the story is not in dispute.

What is in dispute is whether brilliance of engineering is enough. Ocado's tragedy, if that is the right word, is one of timing and of capital. A model that demanded enormous upfront investment was born to thrive in an era of free money and accelerating online adoption, and it briefly did thrive, spectacularly. Then the era ended — rates rose, construction costs soared, customers drifted back to stores, and the cheap, capital-light substitute its founders had always disdained turned out to be exactly what a nervous industry wanted. The machine was magnificent; the environment turned hostile.

And so the story comes back, as it must, to Tim Steiner — the last founder standing, twenty-six years in, his personal fortune still lashed to the same mast as the shareholders who have ridden the stock down from the heavens. The remaining question is the one that will define his legacy and their returns alike: will the Asian mega-hubs prove the model works where density rewards it, will the hidden robotics business unlock a market beyond grocery, and will the company finally stop burning cash and stand on its own — vindicating a high-stakes technology gamble two and a half decades in the making? Or will Ocado remain a beautiful machine built for an economic era that has passed? By 2027, when Steiner's improbable £29.69 share-price target either expires worthless or comes astonishingly back into view, the long-suffering shareholders of Ocado Group will have their answer.

References

-

Kroger Closes Three Ocado Spoke Facilities in Strategic Review — Supermarket News, 2026-01-15 ↩

-

Kroger shuts Nashville spoke facility as e-commerce network shifts — Grocery Dive, 2026-02-18 ↩

-

Shareholders rebel over CEO Tim Steiner's £15m pay package — Reuters, 2024-04-29 ↩↩↩

-

Director/PDMR Shareholding Disclosure: Tim Steiner — London Stock Exchange RNS, 2026-06-12 ↩

-

Lotte Shopping outlines 'Value Enhancement' and Busan CFC project — Lotte Shopping Investor Relations, 2025-10-18 ↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube