NEXT plc: The Retail Operating System

I. Introduction & The Retail Paradox

Picture the British high street somewhere around 2020. The lights are going out, one famous fascia at a time. Debenhams, a department store that traded for 240 years, slides into liquidation and shutters all of its shops. Arcadia — the empire that owned Topshop, Topman, Dorothy Perkins, Burton, and Miss Selfridge, the very engine of British mall fashion — collapses into administration, and its crown-jewel brands are sold off as disembodied logos to online players who have no idea what to do with the physical stores. Amazon is eating retail margins for breakfast. ASOS and boohoo are convincing a generation that they never need to set foot in a shop again. The obituary for the legacy British clothing retailer has effectively been pre-written.

And in the middle of that carnage sits a company that began life in 1864 as a stuffy, ready-to-wear suit tailor in Leeds. By every law of retail Darwinism, this company should have been roadkill. Instead, it did something almost nobody saw coming. It became the toll road. As its competitors burned down, NEXT plc quietly walked over to the smoldering wreckage, picked up the best brands for pennies, and then offered to run the back-end plumbing of the very rivals it hadn't bought. By 2026, brands like Reiss, FatFace, Gap UK, and Victoria's Secret UK were no longer NEXT's enemies. They were NEXT's customers.

This is the paradox at the heart of one of the most quietly extraordinary corporate stories in Europe. NEXT did not win the internet age by being the flashiest e-commerce brand. It won by recognizing that the boring, expensive, capital-intensive infrastructure it had built decades earlier — warehouses, delivery fleets, and a consumer credit book — was not a legacy cost to be apologized for. It was a platform. And platforms, as every great technology investor knows, are where the real money lives.

The thesis we want to put on the table is deliberately provocative. NEXT plc is no longer best understood as a vertical clothing retailer that happens to have a website. It is closer to a Platform-as-a-Service and consumer-finance conglomerate that happens to wear the costume of a department store. There is a fashion business inside NEXT, and a very good one. But wrapped around it are three other businesses — a third-party marketplace, a retail-as-a-service operation, and a £1.28 billion consumer credit lender — that behave far more like software and financial-services companies than like a shop.1

How profitable is this machine? Entering 2026, group pre-tax profits cleared the £1.15 billion mark, an extraordinary figure for a UK-focused retailer in a decade of austerity, Brexit friction, and cost-of-living squeezes.1 To understand how a Victorian tailor got here, we need to follow four threads through this episode: the logistics DNA that was accidentally laid down by a 1980s catalog; the seamless transition from that catalog to the web; the capital-allocation genius of a CEO who took the top job at 33; and the launch of the high-margin engine that NEXT calls Total Platform.

Let's start where all the infrastructure was born — not on a screen, but in a hardback book full of fabric swatches.

II. Strategic Origins: Sowing the Seeds of Logistics

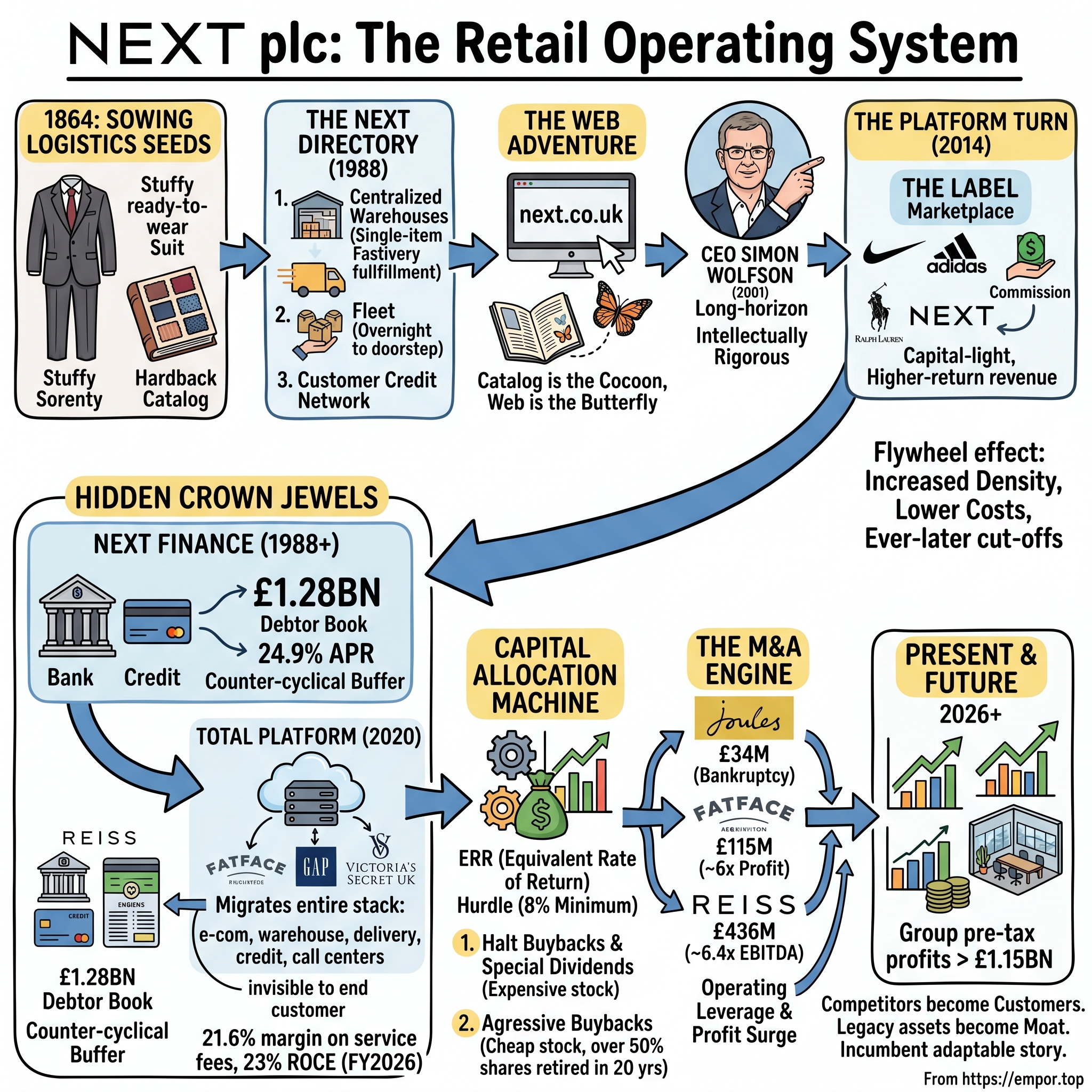

Every great platform company has an origin story that looks, in hindsight, like destiny but at the time looked like a normal commercial decision. For NEXT, that story does not begin with code. It begins with a suit.

In 1864, Joseph Hepworth founded a ready-to-wear tailoring business in Leeds, in the industrial heart of Victorian England.4 Hepworth & Son was, for over a century, exactly what it sounds like: a maker and seller of men's suits, a vertically respectable but deeply unglamorous brick-and-mortar operation. It manufactured cloth, it ran shops, it dressed working men in serviceable wool. For more than a hundred years, nothing about the company suggested it would one day be described as the cloud computing of fashion. It was slow, it was regional, and it was about as far from disruptive as a business could be.4

The first plot twist arrived in 1982. The Hepworth board, looking to modernize a tired chain, brought in a retail visionary named George Davies and handed him a mandate to invent something new.[^11] Davies did not just rebrand the shops. He invented a concept. The idea was to stop selling individual garments off racks like commodities and start selling coordinated outfits — a curated, color-matched, head-to-toe look that an aspirational middle-class customer could buy as a complete package. He called the new chain NEXT, and the in-store experience was built around what became known as the "Next Look."[^11] It was lifestyle retailing before that phrase existed, and it landed at exactly the right cultural moment. The 1980s British consumer wanted to look put-together and modern, and NEXT sold exactly that, pre-assembled.

The chain expanded rapidly, but the move that truly mattered — the one that would echo decades later — came in 1988. That year, NEXT launched the NEXT Directory.[^11] On the surface it was a mail-order catalog, which in 1980s Britain was a deeply downmarket proposition associated with cheap, slow, agent-based credit catalogs that respectable shoppers looked down on. Davies did something radical: he refused to make it downmarket. The NEXT Directory was a gorgeous, heavy, hardback coffee-table book, printed on premium paper, with actual fabric swatches stitched in so customers could feel the cloth before ordering.[^11] It treated mail order as a luxury experience rather than a discount one.

Here is the part that matters for everything that comes after. To deliver on the promise of that beautiful book — to let a customer flip through it at home, pick an outfit, and receive it quickly — NEXT had to build physical infrastructure that no normal shop chain needed. Three pillars, specifically.

First, a centralized warehouse network capable of high-frequency fulfillment — not just bulk-shipping pallets to stores, but picking, packing, and dispatching single items to individual homes. Second, a domestic delivery system geared toward fast, often overnight, doorstep logistics — a discipline almost no clothing retailer of the era possessed. And third, a customer credit network, because the Directory let people buy now and pay over time, which meant NEXT had to underwrite, extend, and collect consumer credit at scale.[^13]

Sit with that for a moment. In 1988, in order to sell sweaters out of a hardback catalog, NEXT was forced to become a logistics company, a parcel-delivery company, and a consumer lender — all at once, and all under one roof. None of this looked strategic at the time. It was simply the cost of making the Directory work. But it laid down a physical and operational blueprint — warehouses built for single-item home fulfillment, an overnight delivery muscle, and an in-house credit book — that was almost perfectly shaped for an invention that did not yet exist. When the internet arrived, NEXT would not have to build any of this. It already had it. The catalog was the cocoon; the web was the butterfly. And the person who would understand that better than anyone was about to take the corner office.

III. The Simon Wolfson Transformation & The Digital Masterclass

In 2001, NEXT did something that boards almost never do. It handed the keys to the entire company to a 33-year-old.

Simon Wolfson became chief executive of NEXT at an age when most managers are still fighting for a regional directorship, making him the youngest CEO in the FTSE 100 at the time.2 The cynical reading was obvious and unavoidable: his father, David Wolfson, had been a chairman of the company, and the surname carried weight. Nepotism whispers followed him into the job. But anyone expecting a coasting heir got the opposite. Wolfson turned out to be one of the most intellectually rigorous, numerate, and temperamentally disciplined operators British business has produced in a generation — a man the Financial Times would later dub "the retailer's retailer."2

Wolfson's defining trait is that he thinks like an owner who intends to be around for decades, even though he is not a founder. That long-horizon, skin-in-the-game mentality is not just a personality quirk; it is structurally reinforced. As of the mid-2020s, Wolfson directly held roughly 0.87% to 1.0% of NEXT — on the order of 828,162 shares — a stake worth somewhere between £110 million and £145 million depending on the share price.1[^6] His personal fortune is, in other words, not a diversified portfolio with a bit of NEXT in it. It is NEXT. When he weighs a buyback or an acquisition, he is quite literally moving his own net worth around.

That alignment got formalized further in a 2026 remuneration shake-up designed explicitly to keep him at the helm during the platform's scaling phase.[^6] The structure is worth understanding because it tells you what the board wants him focused on. His base salary was set at a relatively modest £1.0 million, but the long-term incentive plan maximum was raised to 400% of salary — and crucially, those payouts were tied to relative Total Shareholder Return and Earnings Per Share growth hurdles measured over a rolling three-year period.[^6] In plain terms: he gets paid for compounding the share price faster than peers and for genuinely growing per-share earnings, and he gets nothing for mediocre, index-hugging performance. It is an incentive scheme that punishes empire-building and rewards exactly the kind of disciplined capital return that has come to define his tenure.

But the real masterstroke of Wolfson's early years was not financial engineering. It was a single, almost obvious-in-hindsight insight about the internet. In the late 1990s and early 2000s, the conventional wisdom among legacy retailers was that "e-commerce" was a strange new species — a separate, experimental silo to be staffed by a small skunkworks team, kept at arm's length from the real business, and treated with suspicion. Many retailers spun up clumsy standalone websites that had nothing to do with their stores or their warehouses.

Wolfson saw it completely differently. He looked at next.co.uk and recognized that it was not a new business at all. It was simply the NEXT Directory rendered on a screen.[^13] The customer behavior was identical — browse from home, select, order for home delivery, pay on credit. And here was the magic: because NEXT had spent over a decade building the warehouses, the overnight delivery network, and the consumer credit book to serve the catalog, it already owned every piece of infrastructure the web demanded. There was nothing to build. NEXT could migrate millions of catalog customers onto the website with almost no friction, because the back-end — the part that actually costs hundreds of millions and takes years to perfect — was already humming.[^13]

This is why NEXT's digital transition was so smooth that it almost looked boring. While competitors were spending fortunes and years trying to bolt logistics onto a website, NEXT was simply pointing its existing logistics machine at a new front door. The infrastructure laid down to deliver a hardback catalog in 1988 turned out to be the perfect substrate for e-commerce in 2008.

The payoff arrived in 2012, and it was symbolic as much as financial. That year, NEXT overtook Marks & Spencer as the UK's most profitable clothing retailer.[^13] To appreciate what that meant, you have to understand that M&S was not just a competitor; it was the establishment, the grand institution of British clothing, the benchmark against which every other retailer measured itself. For the upstart from Leeds to surpass it on profitability was a genuine changing of the guard — a moment when the market quietly realized that NEXT's unglamorous, infrastructure-first model was simply better business than the high-prestige incumbent's.[^13] Having mastered selling its own clothes online, Wolfson then asked a question that would crack open an entirely new category of profit: why should NEXT only ever sell NEXT?

IV. The First Inflection Point: The LABEL Marketplace

There is a piece of folk wisdom that every retail executive absorbs early in their career, almost as gospel: retail is zero-sum. If a customer walks into your space and spends £60 on a Nike shirt, that is £60 they did not spend on one of your own shirts. The third-party brand is a competitor for the customer's wallet. You let them in at your peril. For decades, this logic kept retailers vertically jealous — protective of their floor space, hostile to rivals, determined to capture the entire margin on every garment a customer bought.

Around 2014, Wolfson decided this was a false choice, and the decision reshaped the company.[^13]

The reasoning went like this. A customer does not actually want to buy only NEXT-branded clothes. A customer wants to dress themselves and their family, and that means Nike trainers, Adidas tracksuits, Ralph Lauren polos, and a hundred other labels alongside NEXT's own ranges. If NEXT refused to stock those brands, the customer simply went elsewhere to buy them — and quite possibly did the rest of their shopping there too. By trying to capture 100% of a smaller basket, NEXT was losing the chance to capture a slice of a much bigger one. So NEXT launched The LABEL: a section of next.co.uk that invited third-party apparel and sportswear brands onto its storefront, turning the site from a single-brand shop into a curated multi-brand destination.[^13]

This was a profound business-model pivot disguised as a merchandising tweak. With The LABEL, NEXT stopped being purely a vertical retailer — a company that designs, sources, and sells its own goods and earns the full product margin while carrying the full inventory risk — and became, in part, a marketplace aggregator. On third-party sales, NEXT did not have to design the product, did not have to gamble on buying the inventory, and in many arrangements did not even have to own the stock. It curated, hosted, and fulfilled, and it took a commission. That is a fundamentally different and more attractive economic profile: capital-light, higher-return revenue that does not require betting the balance sheet on next season's color palette.[^13]

But the genuinely clever part — the part that reveals Wolfson's systems thinking — is the flywheel that The LABEL set spinning through NEXT's logistics network. Adding desirable third-party brands pulled more shoppers to next.co.uk. More shoppers meant more orders flowing through the same warehouses and the same delivery routes. And here is the crucial mechanic: in parcel logistics, density is everything. The more parcels a courier delivers per street, per van, per route, the lower the cost of delivering each individual parcel. So as marketplace traffic increased order density, NEXT's per-unit shipping and returns costs fell.[^12]

Falling per-unit costs then funded a competitive weapon that customers could feel directly: ever-later order cut-off times for next-day delivery. When your logistics network is dense and cheap enough, you can promise a customer that an order placed late at night will still arrive the next day — a promise that delights shoppers, pulls in still more orders, and tightens the loop further. The LABEL did not just add revenue; it made the entire logistics machine denser, cheaper, and faster, which made NEXT a better place to shop, which brought in more brands and more customers. Each turn of the wheel reinforced the next.

The LABEL proved that NEXT's infrastructure could profitably carry other people's brands on the front-end. That raised an even more radical question, and answering it would create the most valuable engine in the entire company. If NEXT could host a rival's products on its website, why couldn't it host a rival's entire business?

V. The Hidden Crown Jewels: Fintech & The Total Platform

To understand the two hidden engines inside NEXT, you have to stop thinking of it as a retailer for a few minutes and start thinking of it as, alternately, a bank and a cloud-services provider. Both descriptions are more accurate than they sound.

Start with the bank. Buried inside NEXT's results is a division, NEXT Finance, that most casual observers of the company never think about — and it is one of the most profitable parts of the entire group. Remember that consumer credit network NEXT built in 1988 to let catalog shoppers buy now and pay later? It never went away. It evolved into a modern revolving-credit operation, offering customers products branded as nextpay and pay in 3 — essentially a store credit account and an installment plan baked directly into the checkout.1

The scale here is genuinely striking. This division operates an active customer debtor book of around £1.28 billion — that is the total balance of credit NEXT has extended to its shoppers and is waiting to be repaid.1 On that book, NEXT charges interest at a standard variable APR around 24.9%, which is typical for store-card credit but enormously lucrative when applied to more than a billion pounds of balances.1 The result is that NEXT Finance generates high-margin interest income, routinely running a net margin above 10% and contributing over £100 million in segment profit.1

Why does this matter so much beyond the raw profit? Because it is counter-cyclical relative to the fashion business in a useful way. When fashion sales soften in a downturn, the credit book keeps generating interest income from existing balances, providing a buffer of high-margin earnings that smooths the inherent lumpiness of clothing retail. Of course, this cuts both ways — and we'll return to the risk that a genuinely severe recession poses to repayment rates on that book — but in ordinary cycles, the finance arm acts as a stabilizer that pure-play fashion retailers simply do not have. NEXT, in effect, quietly runs a small consumer bank attached to its shop.1

Now the cloud-services provider — and this is the crown jewel. In 2020, Wolfson asked the question that The LABEL had teed up. NEXT was already hosting rival brands' products on its website. Why stop there? Why not run a rival brand's entire back-end?[^12]

The answer was Total Platform, and it is best understood by analogy to cloud computing. Before Amazon Web Services, every company that wanted a website had to buy its own servers, build its own data centers, and hire its own infrastructure engineers — enormous fixed costs that had nothing to do with their actual product. AWS came along and said: don't do any of that. Rent our infrastructure, pay as you go, and focus on your actual business. Total Platform is the AWS of mid-market fashion retail. Under it, a partner brand migrates its entire operational stack onto NEXT's systems: the e-commerce website, the warehousing, the picking and packing, the shipping, the returns processing, the customer call centers, and even the consumer credit facilities.[^12]

The beauty of it is that the experience is invisible to the end customer. When a shopper visits the Reiss website or the FatFace website, they see a Reiss or FatFace storefront, with that brand's photography, tone, and identity intact. They have no idea that behind the curtain, every box is being packed, shipped, and returned by NEXT's automated mega-hubs — facilities like the state-of-the-art Elmsall 3 warehouse — and that the credit at checkout may be running on NEXT's rails.[^12] The brand keeps its soul; NEXT runs its body. Partners that have moved onto the platform include Reiss, FatFace, Gap UK, and Victoria's Secret UK, among others.[^12]

The economics of this segment are what make it the crown jewel. In the FY2026 results, Total Platform segment profits rose 17% to £90 million, up from £77 million the prior year.1 But the profit figure undersells the quality of the business. The margin on NEXT's service fees reached 21.6%, and — the number that should make any investor sit up — the segment delivered a Return on Capital Employed of roughly 23%.1 ROCE measures how much operating profit a business squeezes out of every pound of capital tied up in it, and 23% is a software-like return, not a retail-like one. NEXT is monetizing infrastructure it largely already owns, layering high-margin service fees on top of warehouses and systems whose fixed costs are already covered by its own retail volumes. Each incremental partner pours revenue through a machine that is mostly already paid for.[^12]

There is a wonderfully telling human footnote to the Total Platform story. In 2024, NEXT appointed a new Chief Financial Officer: Jonathan Blanchard.3 Blanchard had previously been CFO and COO of Reiss Group, where he personally orchestrated Reiss's migration onto NEXT's Total Platform.3 In other words, he had been a customer of the platform, executing the operational handover from the client's side, and clearly doing it superbly. Wolfson was so impressed by the quality of that execution that he hired the client's finance chief to run NEXT's own global financial operations. There is no better endorsement of a product than buying it and then poaching the person who implemented it on the other side of the table.

Having built engines that throw off this much high-quality cash, NEXT faced the question that ultimately separates great companies from merely good ones: what do you do with all the money? This is where Wolfson's most distinctive genius comes into view.

VI. Capital Allocation & The M&A Machine

Here is a question that sounds simple and bankrupts companies that get it wrong: when should a company buy back its own shares?

The default corporate answer is depressingly bad. Most CEOs buy back stock when they happen to have spare cash sloshing around — which is usually at the top of the economic cycle, when business is booming, the share price is high, and the buyback destroys value because they are paying a premium for their own equity. They then stop buying back, or can't afford to, precisely when the price is low and a buyback would create the most value. It is a near-perfect mechanism for buying high and not buying low, dressed up as shareholder friendliness.

Wolfson replaced this whole sloppy instinct with a single piece of mathematics, and it is the closest thing NEXT has to a secret formula. He governs buybacks using a metric he calls the Equivalent Rate of Return, or ERR. The concept is elegant: treat buying back your own shares as if it were any other investment, and demand a minimum rate of return on it. The ERR is calculated as the company's anticipated group pre-tax profits divided by its current market capitalization — essentially the earnings yield the company would "earn" by retiring its own stock at the prevailing price.1

NEXT sets a strict minimum ERR hurdle of 8%.1 The mechanism that follows is what makes it disciplined rather than decorative. If the share price climbs so high that the ERR drops below 8% — meaning buybacks would no longer clear the return hurdle — NEXT does not shrug and buy anyway because it has the cash. It stops. It halts the buyback and pivots to returning the surplus cash to shareholders through special dividends or so-called B-Share schemes instead.1 The 8% hurdle acts as a governor on the engine: it lets NEXT buy back aggressively when its own shares are cheap relative to earnings, and it forcibly redirects cash to other forms of return when the shares are expensive. The company treats its own stock with exactly the same cold-eyed scrutiny a good investor would apply to any external holding.

The cumulative effect of running this discipline for two decades is staggering. Over roughly twenty years, NEXT has retired more than half of its total shares outstanding.[^13] Think about what that means mechanically: even if total group profits had merely held flat, halving the share count would have doubled earnings per share, because the same profit is now divided among half as many shares. Layered on top of genuine profit growth, this share-count reduction has supercharged the per-share compounding that ultimately drives the stock — and it is precisely the behavior that Wolfson's own EPS-linked incentive plan rewards.[^6][^13]

The same value-investor temperament that governs the buybacks governs NEXT's M&A — and this is where Total Platform transforms from a profit segment into a strategic weapon. Most retail acquisitions destroy value because the acquirer overpays for a trendy brand and then struggles to integrate it. NEXT inverted the playbook. It hunts for established, often distressed or undervalued, British heritage brands; buys them cheaply; strips out their bloated legacy IT systems and warehousing overhead; migrates them onto Total Platform; and unlocks instant operating leverage. The platform de-risks the deal because NEXT knows, with near-certainty, that it can run the acquired brand's operations more cheaply and effectively than the brand could itself. Three deals show the pattern in action.

Take Reiss, the upmarket British fashion label, which NEXT acquired in stages. The decisive move came in September 2023, when NEXT bought out the private-equity firm Warburg Pincus's remaining stake, in a deal that valued Reiss's equity at £376 million and implied an enterprise value of roughly £436 million.[^8] Against Reiss's EBITDA of about £68.8 million, that worked out to an EV/EBITDA multiple of just 6.3 to 6.5 times.[^8] To put that in context, premium global apparel peers were routinely trading at 12 to 15 times EBITDA — so NEXT bought a premium, fast-growing brand for roughly half the going rate for its category. And the post-acquisition outcome validated the thesis spectacularly: once migrated onto Total Platform, Reiss's sales jumped by over 40% and profits surged by around 50% within a year, as the platform's logistics and digital muscle were applied to a brand that had been operating with far less efficient infrastructure.[^8][^12]

Then there is FatFace, the casual lifestyle brand, which NEXT acquired in October 2023 — taking 97% of the company for £115.2 million.[^3][^7] FatFace at the time was posting around £282 million in sales and £19.5 million in pre-tax profits, which means NEXT paid under 0.5 times sales and less than 6 times pre-tax profit for a stable, genuinely profitable business that was already plugged into NEXT's LABEL ecosystem.[^7] Those are the kinds of multiples value investors dream about — buying real earnings at a fraction of the revenue, with a clear operational path to making them grow.

And the most audacious deal of all: Joules, the British country-lifestyle brand famous for its wellington boots and floral prints. Joules collapsed into administration in late 2022, and in December of that year NEXT bought it out of bankruptcy for just £34 million, plus a further £7 million for its head office.[^9] This was a brand that had been generating well over £200 million in annual revenue, acquired for what amounts to pennies on the pound because it was distressed and the legacy operation was broken.[^9] Within about ten months, NEXT had migrated Joules onto Total Platform, stabilized its chaotic operations, and returned it to profitability — turning a bankrupt brand into a functioning, contributing asset by doing nothing more exotic than swapping out its plumbing.[^9]

It is worth contrasting this discipline with how rivals played the same game. ASOS bought the Topshop and Topman brand IP out of the Arcadia collapse, but it took on heavy, ultimately toxic debt to do so — and crucially, it bought only the intellectual property, the logos and designs, without the physical infrastructure to do anything differentiated with them. Frasers Group, the Mike Ashley empire, built a sprawling collection of distressed brands and retail stakes but never unified them onto a single, efficient underlying technology and logistics stack, leaving it a fragmented portfolio rather than an integrated machine. NEXT's edge was never just buying cheap. It was buying cheap into a pre-built platform that could immediately make the acquired business better. The brand provides the desirability; the platform provides the economics.

This combination — disciplined returns, disciplined acquisitions, all riding on owned infrastructure — is not just good management. It adds up to a genuine, durable competitive moat. To see exactly how durable, it helps to run NEXT through the two frameworks investors use to stress-test a moat.

VII. Competitive Framework Analysis: Hamilton's 7 Powers & Porter's 5 Forces

Strategy frameworks can be sterile when applied mechanically, but NEXT is one of those rare companies where the textbook powers genuinely light up — because its moat was built brick by brick over forty years rather than asserted in a pitch deck. Run it first through Hamilton Helmer's 7 Powers, the modern investor's standard toolkit for identifying durable competitive advantage.

The most obvious power is Scale Economies, expressed through logistics supremacy. NEXT owns its automated warehouses, like Elmsall 3, and runs direct-to-door courier networks rather than fully outsourcing to third parties.[^12] Because volume is spread across NEXT's own ranges, The LABEL's third-party brands, and every Total Platform partner, the cost of fulfilling each individual parcel is driven down to a level rivals cannot match. The visible proof for customers is the order cut-off time: NEXT can offer an 11 PM or even midnight cut-off for next-day delivery, a logistical feat that even Amazon struggles to match specifically in fashion, where the return rates and item handling are far messier than in general merchandise.[^12] The denser the network gets, the cheaper each parcel becomes, and the harder it is for anyone sub-scale to compete.

The second power, and arguably the stickiest, is Switching Costs, expressed as platform lock-in. When a brand like Reiss, FatFace, or Gap UK migrates its inventory, customer data, e-commerce backend, and consumer-credit structure onto Total Platform, it does not just sign a contract — it surgically wires its entire operational nervous system into NEXT's systems. Migrating off would mean rebuilding warehousing, re-platforming the website, re-establishing payment and credit infrastructure, and re-hiring operational staff, all while keeping the lights on for daily trading. The disruption would be catastrophic and the risk enormous. Once a partner is on the platform, they are, for all practical purposes, on it for good. That is why the segment's revenue is so much more predictable than ordinary fashion sales.

Third is Network Effects, running through The LABEL marketplace. As described earlier, this is a classic two-sided dynamic: more third-party brands attract more high-intent shoppers, and more high-intent shoppers make selling on next.co.uk increasingly mandatory for any fashion brand that wants meaningful UK online exposure.[^13] The marketplace becomes a place brands cannot afford to be absent from, which deepens the assortment, which pulls in still more shoppers.

Fourth, there is a Cornered Resource, and unusually it is not a patent or a mine but a person and a method: Wolfson himself and the disciplined capital-allocation framework, the ERR hurdle, that he built and embodies.2 A rival cannot simply copy the 8% hurdle rate from a slide; the value lies in the institutional willingness to actually obey it through cycles, to halt buybacks when others would plow ahead, and to walk away from glamorous deals. That temperament has compounded value for two decades and is genuinely difficult to replicate. (It is also, as the bear case will note, a concentration risk.)

Fifth, and perhaps most subtle, is Counter-Positioning. Total Platform works precisely because NEXT's natural competitors cannot easily copy it without undermining themselves. A legacy department store could in theory offer to run rivals' operations, but department stores are pathologically paranoid about sharing customer data with brands they compete against. Meanwhile, a traditional third-party logistics firm — a pure 3PL — can move boxes, but it has no consumer-facing storefront, no marketplace traffic, and no billion-pound consumer credit book to bundle in. NEXT sits in a unique position: a retailer that is willing to enable other retailers, backed by infrastructure no pure logistics player possesses. Incumbents who tried to respond would have to cannibalize their own positioning to do so.

Now run NEXT through Porter's Five Forces, which examines the structural attractiveness of the industry NEXT occupies. The threat of new entrants is very low: the capital expenditure and accumulated logistics expertise required to replicate automated warehouses and a national next-day distribution network represent an astronomical barrier — you cannot venture-fund your way to Elmsall 3 overnight. The bargaining power of buyers (consumers) is low to moderate: with nextpay credit balances tying customers in, and the convenience of returning items from hundreds of brands to any of NEXT's 450-plus physical stores, loyalty is structural rather than merely emotional.[^12] The bargaining power of suppliers, meaning the third-party brands on the marketplace, is low, because NEXT controls one of the premier direct-to-consumer digital gateways in the UK, and brands must accept its commission terms to reach those customers.

The two forces where NEXT faces real pressure are the more interesting ones. The threat of substitutes is moderate: global fast-fashion platforms and multi-brand online players offer consumers alternative ways to spend, and that competitive gravity never fully disappears. And competitive rivalry has historically been high — UK fashion retail is a brutal, low-margin knife fight. But here is NEXT's masterstroke, the thing that ties this entire episode together: it has substantially neutralized rivalry by converting its fiercest competitors — Reiss, FatFace, Gap UK — into high-margin platform clients.[^12] You cannot be at war with a company that runs your warehouses. NEXT did not win the rivalry by killing its rivals. It won by absorbing them into its economics. The competition didn't end. It got monetized. With the moat mapped, the fair question is what could still go wrong — and how NEXT stacks up against the giants playing a global version of this game.

VIII. Bull vs. Bear Case & Global Peer Benchmarking

To judge where NEXT can go from here, it helps to place it beside the global titans of apparel, because they reveal how unusual NEXT's chosen path actually is.

Consider first the Japanese giant, 株式会社ファーストリテイリング Fast Retailing — the parent of ユニクロ Uniqlo. Fast Retailing is a colossus, and its model is the near-opposite of NEXT's. It dominates through ferocious vertical integration: it designs, manufactures, and sells its own basic, high-quality apparel — the perfect white T-shirt, the down jacket that compresses into a pouch — through a hyper-efficient, tightly controlled supply chain. Its genius is in its own product. NEXT's genius, by contrast, is in other people's products and in the infrastructure that moves them. Where Uniqlo captures margin by perfecting and owning its garments, NEXT increasingly captures margin by aggregating and fulfilling the creativity of hundreds of brands. Both are excellent businesses; they are simply playing different games. One is the master craftsman; the other is the master platform.

Then there is the ultra-fast threat from 希音 Shein, the Chinese-founded fast-fashion juggernaut that has rewired the bottom of the market. Shein uses a real-time, AI-driven supply chain to test thousands of designs in tiny batches, scale up whatever sells, and ship astonishingly cheap clothing directly to consumers worldwide. On price and on speed-of-trend, Shein is close to unbeatable. So NEXT does not try to beat it there. Instead it positions itself further up the value chain — premium mid-market, better quality, more curated — and leans on the one set of advantages Shein structurally cannot replicate from a distant supply chain: immediate next-day delivery, instant physical returns to 450-plus local stores, and integrated consumer credit.[^12] Shein wins on the price tag; NEXT wins on the experience, the convenience, and the local moat. They are competing for partially different customers and partially different needs.

So what is the bull case for NEXT from here? It rests on Total Platform breaking out of Britain. If NEXT can scale the platform internationally — becoming the default cloud-and-logistics operating system for mid-market retail across Europe and North America — then the highest-margin, highest-ROCE part of the business becomes the growth engine for the whole group.[^12] In that scenario, the blended corporate margin, currently running somewhere around 18%, could expand toward and beyond 25% as the capital-light platform fees grow faster than the capital-heavy retail base. Layer on NEXT Finance scaling into something resembling a genuine independent digital bank, and you have a company whose profit mix shifts decisively away from selling clothes and toward selling infrastructure and financial services — a re-rating story, not just an earnings story.

The bear case is equally clear-eyed, and it has two prongs. The first is key-person risk, and it is real precisely because of how good Wolfson is. The capital-allocation discipline, the ERR governor, the willingness to buy out of administration and migrate rather than overpay for hype — these are, as the 7 Powers analysis flagged, a cornered resource embodied in one person. That is wonderful while he is in the chair and dangerous the day he leaves. Genius is hard to institutionalize. If Wolfson departed and a successor began buying back stock at the top of the cycle to please the market, or chasing trendy acquisitions at 14 times EBITDA, the very engine of NEXT's outperformance could quietly stall, and it might take years for the market to notice the discipline had gone.

The second prong is macroeconomic and credit risk, and it points straight at that £1.28 billion debtor book.1 The consumer credit arm is a high-margin blessing in normal times, but it is also a leveraged bet on the financial health of the British consumer. In a deep, structural UK downturn — the kind that combines falling discretionary spending with rising unemployment — NEXT would face a double hit: weaker clothing sales and deteriorating repayment rates on its credit book, with bad-debt provisions eating into the very profits that normally act as a counter-cyclical buffer. The buffer becomes a liability at exactly the wrong moment. The two halves of the business that usually offset each other could, in a severe enough recession, decline together.

For investors trying to keep this company honest over time, the noise should be filtered down to a very small number of signals. The first and most important KPI is Total Platform segment profit and its margin/ROCE trajectory — because that single line item is the entire re-rating thesis; if it keeps compounding at high-teens growth with ~20%-plus margins, the platform story is intact, and if it stalls, the bull case is in trouble. The second is NEXT Finance's debtor book quality — not just the size of the book but the bad-debt and impairment trends within it, which are the early-warning system for consumer stress. And the third, quieter signal is simply the ERR discipline itself: watching whether management continues to obey its own buyback hurdle through cycles, which is the truest test of whether the Wolfson playbook survives. Track those three and you understand most of what matters about NEXT. Those KPIs are also a neat distillation of the broader lessons this story teaches.

IX. Playbook & Core Lessons

Step back from the specifics, and NEXT's transformation hands operators and investors a compact set of durable lessons — the kind that travel well beyond fashion retail.

The first is sweat your fixed assets. The entire NEXT story turns on a single reframe that happened inside Wolfson's head. The legacy catalog infrastructure — the warehouses, the delivery fleet, the consumer credit book — could have been viewed the way most incumbents view their old physical estate: as a heavy, depreciating cost to be defended or wound down. Instead, NEXT recognized that this same infrastructure was a scalable, tech-enabled platform that could be rented out to other brands at extraordinary returns. The asset did not change. The perception of the asset changed, and that reperception created billions in value. The lesson for any incumbent staring at expensive legacy infrastructure is to ask whether the thing they think is a cost is actually a platform in disguise.

The second is value over glamour in M&A. NEXT never won a high-multiple bidding war for a hot, trending brand, and that abstinence is a feature, not a timidity. The discipline was to buy solid, often unloved heritage brands at low multiples — Reiss at roughly 6.4 times EBITDA, FatFace at under 6 times pre-tax profit, Joules straight out of administration — and then let operational synergy from the platform expand their margins.[^7][^8][^9] The returns came not from buying brilliantly-timed momentum but from the spread between a cheap purchase price and a pre-built engine that could make the acquired business measurably better. In M&A, the price you pay is the one variable entirely within your control, and NEXT treats it as sacred.

The third is math-driven shareholder returns. The 8% ERR hurdle is the philosophical heart of the company's capital discipline. Build a strict, transparent, mathematical formula for returning capital, and then — the hard part — actually stick to it through the emotional swings of the cycle. Never buy back stock merely to offset dilution or to ride momentum or to signal confidence. Treat every pound spent on your own shares with the same cold scrutiny you would apply to buying any other company's stock. The formula removes the ego and the cycle-timing errors that wreck most buyback programs.1

The fourth is the most elegant, and it is what makes the whole acquisition machine work: decentralize the creative, centralize the plumbing. When NEXT buys a brand, it deliberately lets that brand keep its creative independence — its own headquarters, its own design talent, its own distinct identity and customer voice. Reiss still feels like Reiss; Joules still feels like Joules. What the brands are required to surrender is only the invisible, non-differentiating "plumbing": the IT, the warehousing, the shipping, the returns, and the credit processing — the parts of a business where scale creates pure efficiency and where individuality creates pure waste.[^12] This is the precise opposite of the typical conglomerate mistake of crushing acquired brands into a bland centralized mold and destroying the very magic that made them worth buying. NEXT centralizes exactly the things that benefit from scale and decentralizes exactly the things that benefit from autonomy. Get that line right, and you can buy brand after brand without diluting any of them.

Put those four lessons together and you have the architecture of the entire company — which is the right place to land this story.

X. Outro

NEXT plc's journey is, in the end, the ultimate story of corporate adaptability — the rare case of a brick-and-mortar incumbent that did not merely survive the digital disruption but used its own legacy physical assets to build a moat that pure-play e-commerce companies, for all their capital and engineering talent, simply cannot replicate. The warehouses and delivery routes and credit systems that a beautiful 1988 catalog forced into existence turned out to be the perfect foundation for a 21st-century platform. NEXT did not fight the future from behind its legacy; it stood on top of it.

Entering 2026, the company sits at what looks like the peak of its financial powers, with group pre-tax profits clearing £1.15 billion and a profit mix tilting ever further toward high-margin platform fees and finance income.1 The Victorian suit tailor from Leeds has done something almost no incumbent in any industry manages. It turned its competitors into its customers, and its old infrastructure into its new growth engine. Whether the discipline that built all this can outlast the singular figure who embodied it is the question that will define the next chapter.

References

-

NXT.L Stock Analysis & Financials — London Stock Exchange ↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩

-

Lord Wolfson profile: The retailer's retailer — Financial Times, 2024-03-21 ↩↩↩

-

Next CFO Jonathan Blanchard appointment — NEXT plc Corporate Governance, 2024-01-18 ↩↩

-

Corporate Profile of J Hepworth & Son — Funding Universe, 2005-12-31 ↩↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube