The Redemption of NatWest: From the World's Most Toxic Bank to Full Privatisation

I. Introduction & Episode Roadmap

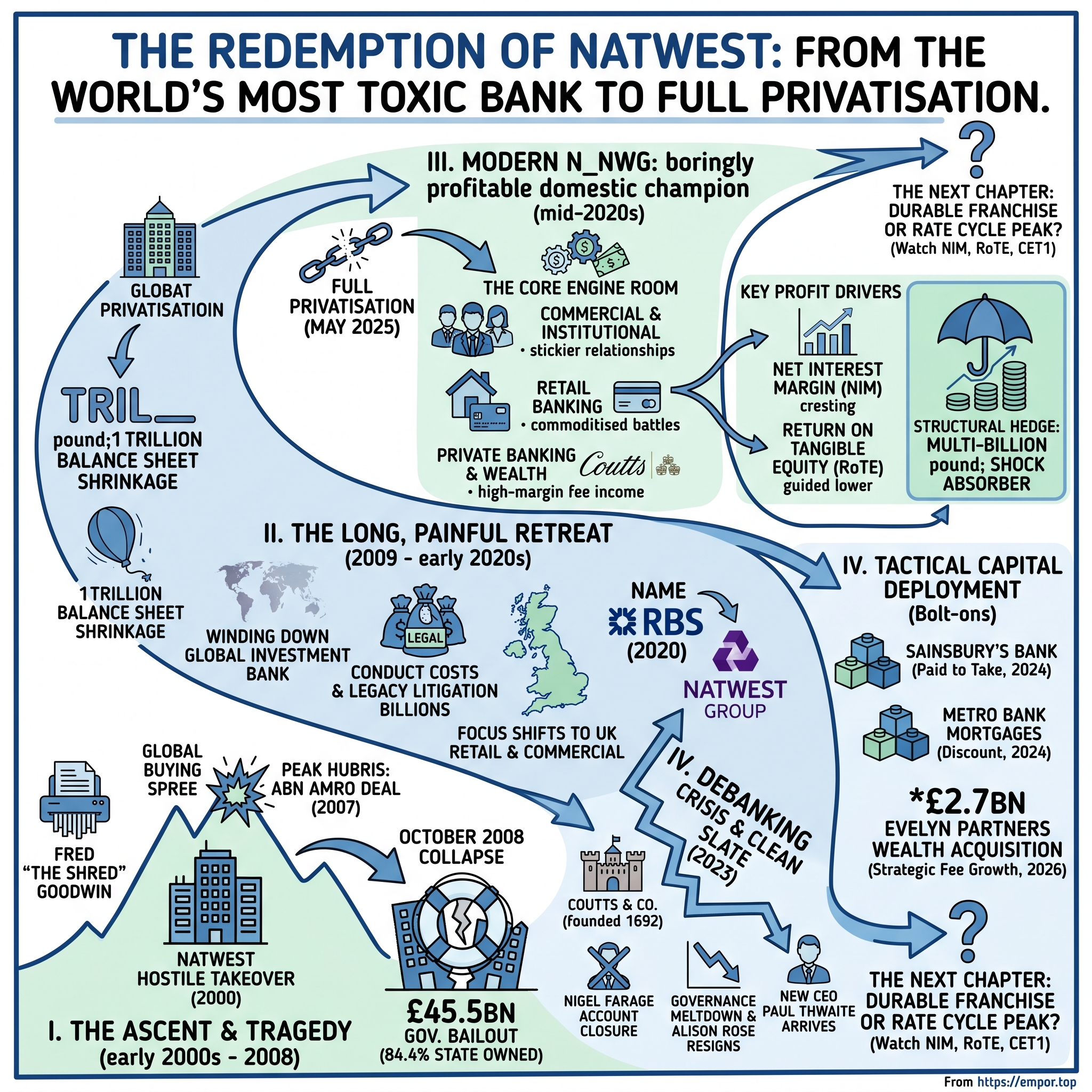

Start with the number that broke a nation's confidence: £45.5 billion. That was the size of the rescue package the UK government injected into the Royal Bank of Scotland between 2008 and 2009, ultimately handing the state an 84.4% ownership stake in what had briefly been the biggest bank on Earth.23 In the tabloid shorthand of the era, RBS became "the world's most toxic bank" — a byword for reckless expansion, banker excess, and the socialisation of private losses. When the group unveiled a 2008 operating loss of £40.7 billion, it was the largest annual loss in British corporate history.3

Now hold that image against the company that exists today. Rebranded as NatWest Group plc and trading on the London Stock Exchange under the ticker NWG.L,5 the bank reported 2025 total income of £16.6 billion, up 13.2% on the year, and net attributable profit of £5.5 billion.1 It delivered a return on tangible equity of 19.2% — a figure that would be the envy of almost any large bank in Europe — and raised its total dividend by 51% to 32.5 pence per share while launching another buyback.1 The toxic bank had become a cash machine.

How did that happen? The transformation is almost hard to believe in its scale. The bank shrank its balance sheet by roughly a trillion pounds, wound down a global investment bank that had spanned continents, retreated to the British Isles, changed its own name to escape its reputation, survived a "debanking" scandal in 2023 that cost it its chief executive, and re-emerged as the UK's leading commercial lender and a growing force in private wealth. And in 2026, freed of state ownership, it is deploying capital again — this time in careful domestic bolt-ons rather than continent-spanning conquests.

We will tell this story in three acts. The first is the tragedy: the ascent and collapse of RBS under Fred Goodwin, the man they called "Fred the Shred." The second is the long convalescence: the decade of shrinking, de-risking, and rebranding under a succession of restructuring CEOs. The third is the modern chapter: a domestically focused, capital-returning compounder run by a low-profile insider, Paul Thwaite, and a new chairman, Rick Haythornthwaite, and the question every investor now has to answer — is this a durable franchise, or a well-managed bank enjoying the tailwind of a favourable interest rate cycle that has already peaked?

To answer that, we have to go back to Edinburgh, to a mid-sized Scottish clearing bank with delusions — or perhaps visions — of grandeur.

II. The Tragedy of "Fred the Shred": The Ascent and Epic Collapse of RBS

Picture the boardroom of the Royal Bank of Scotland in Edinburgh at the turn of the millennium. For nearly three hundred years, RBS had been a respectable but unremarkable institution — a clearing bank at the northern edge of Britain's financial system, dwarfed by the London giants. Then a chartered accountant named Frederick Anderson Goodwin arrived, and everything changed.

Goodwin was not a banker by training. He was an accountant from Paisley who had earned a fearsome reputation cleaning up the collapse of the Bank of Credit and Commerce International, one of the largest banking fraud liquidations in history. He carried into RBS an accountant's obsession with cost and an operator's ruthlessness. The nickname that followed him — "Fred the Shred" — was earned honestly, for his willingness to strip out costs and jobs with a speed that awed rivals and terrified subordinates.3 Colleagues described a leader who ran meetings like interrogations and whose attention to detail extended to the colour of the carpets in new branches and, famously, to complaints about the pattern on the biscuits served in the executive dining room.

The takeover that made a legend

Goodwin's defining moment came in 2000. RBS launched an audacious £21 billion hostile bid for National Westminster Bank — NatWest — a London institution roughly three times its size.3 It was the largest takeover in British banking history to that point, and it pitted the Scottish upstart against the Bank of Scotland in a bruising contest for control. RBS won. What followed cemented the myth: Goodwin's team integrated NatWest with a speed and thoroughness that the market had never seen, eliminating thousands of jobs, ripping out duplicate systems, and extracting "synergies" that flowed straight to the bottom line.

Here is the crucial lesson, and it is a lesson about human psychology as much as finance: the NatWest integration worked too well. A single spectacular success taught RBS's leadership that it could digest anything. Goodwin was knighted in 2004 for services to banking.3 The bank had become, in its own mind, an integration machine — and a machine that believes it cannot fail is a machine that will keep feeding itself larger and larger meals until it chokes.

The global buying spree

Through the mid-2000s, RBS expanded on every front. It pushed into American retail banking through its Citizens franchise, built out a global investment bank, and chased scale wherever it could find it — all while running on the thin capital cushions that regulators of the era permitted and markets rewarded. Capital, in the pre-crisis worldview, was expensive and lazy; the smart bank held as little of it as possible and leveraged the rest. RBS was very smart, by that definition. It was also, it turned out, one hard shock away from insolvency.

The fatal deal: ABN AMRO

The final act of hubris arrived in 2007. RBS assembled a consortium with Belgium's Fortis and Spain's Banco Santander to launch a €71 billion (roughly £55 billion) takeover of the Dutch banking giant ABN AMRO — outbidding Barclays in a battle that dominated European finance for months.3 It remains the largest bank acquisition in history. RBS took the most complex, capital-hungry pieces: the global wholesale banking operations and the Asian businesses.

Two things made this catastrophic rather than merely aggressive. First, RBS bought at the absolute peak of the credit cycle, in the summer of 2007, just as the first cracks in the American subprime market were appearing. Second — and this is the detail that later inquiries seized upon — the due diligence was cursory. An official review would conclude the deal proceeded on the basis of "inadequate due diligence," essentially two lever-arch files and a CD.3 RBS was paying tens of billions for assets it had barely inspected, funding the purchase largely with borrowed short-term money, at the very moment global funding markets were about to freeze solid.

October 2008: the collapse

They froze. Within a year of completing the ABN AMRO deal, wholesale funding evaporated, the assets RBS had bought sight-unseen turned toxic, and the bank that had just been the largest in the world discovered it could not fund itself past the end of the week. Picture the reality behind the headline: a bank whose balance sheet had swollen to around £2 trillion — larger than the entire annual output of the British economy — was days, by some accounts hours, from being unable to let ordinary customers withdraw cash from their accounts. When a bank that big fails, it does not fail quietly; it takes the payments system, the mortgages, the salaries, and the pensions of a nation with it. That is why there was never really a choice about whether to rescue it.

In October 2008, the British government stepped in with what became a £45.5 billion rescue, eventually taking that 84.4% stake.23 Goodwin departed after nine years as chief executive, and in 2012 he was stripped of his knighthood — a public ritual of humiliation almost without precedent in modern Britain.3 Subsequent official reviews were withering, concluding that the ABN AMRO acquisition had gone ahead on the basis of "inadequate due diligence" and that the bank had operated with a capital cushion so thin it could absorb almost no shock at all.3 The story of RBS is not, in the end, a story about clever men making one unlucky bet. It is a story about a culture that had convinced itself risk was something that happened to other, less capable banks.

The analytical takeaway for an investor is not simply "banks can fail." It is more specific and more useful: RBS's collapse was the predictable end-state of a business model that treated capital as waste, integration skill as a licence to acquire without limit, and a rising market as proof of managerial genius. Every strength that built RBS — cost discipline, acquisitive confidence, thin capital efficiency — became, under stress, the mechanism of its destruction. The bank that emerged on the other side would be built on the opposite instincts. But first, someone had to clean up the wreckage of the largest balance sheet in the world.

III. The Long, Painful Retreat: Shrinking a Trillion-Sized Balance Sheet

If Fred Goodwin's era was about addition, the decade that followed was about subtraction — and subtraction, it turns out, is far harder and less glamorous than acquisition. There are no triumphant press conferences for a bank that successfully makes itself smaller.

The trillion-pound diet

The man handed the wreckage was Stephen Hester, a polished, property-savvy executive plucked from British Land to replace Goodwin.3 His mandate was unlike any normal banking job: he was not there to grow the bank but to dismantle most of it without detonating the financial system in the process. Hester created what was effectively an internal "bad bank" — a vast workout division tasked with winding down the assets that had made RBS the biggest and most dangerous bank on the planet.

The numbers are almost incomprehensible. Over Hester's tenure, RBS reduced its assets by hundreds of billions of pounds — a figure that, across the full multi-year retreat, approached a trillion pounds of balance sheet shrinkage. Complex derivatives books were unwound trade by trade. International subsidiaries were sold. Whole business lines that had taken years to build were closed in months. It was, in effect, the largest deliberate corporate demolition in British history, and it had to be done delicately, because a fire sale would have destroyed value and rattled markets. The government's Asset Protection Scheme insured the worst of the toxic assets, buying time for the orderly wind-down.

The strategic point here is subtle but important. A bank is not a factory you can simply shut down; it is a web of obligations, counterparties, and long-dated contracts. Unwinding one worth a trillion pounds without triggering a second crisis was a genuine feat of financial engineering — one that generated no headlines precisely because it succeeded. Alongside the wind-down ran the government's Asset Protection Scheme, a state insurance wrapper that ring-fenced the most poisonous assets and gave the market confidence that RBS could not implode a second time.3 It was, in effect, the government renting out its own balance sheet to buy the bank time to heal.

The conduct-cost decade

Restructuring the balance sheet, however, turned out to be only half the penance. The other half was paying for the sins of the boom years. Across the 2010s, RBS bled billions in conduct and litigation costs — settlements for the mis-selling of payment protection insurance to retail customers, penalties tied to the manipulation of benchmark interest rates, a bruising and reputationally toxic controversy over the treatment of struggling small-business borrowers, and, largest of all, a multi-billion-dollar settlement with United States authorities over the mortgage-backed securities it had sold in the run-up to the crisis. Year after year, just as the underlying bank began to look healthier, another provision would land and swallow the profits. For most of the decade after the bailout, RBS did not pay its shareholders — including the taxpayer — a single dividend. The drought did not end until the late 2010s, once the worst of the legacy litigation was finally behind it. For an investor, this is the under-told half of the recovery: the operational turnaround was necessary but not sufficient; the bank could not truly begin again until it had finished paying for its past.

McEwan and the pivot home

If Hester stabilised the patient, it was Ross McEwan, a plain-spoken New Zealander who took over in 2013, who decided what the recovered bank should be. His answer was radical in its modesty: stop trying to be a global investment bank at all. Under McEwan, RBS completed its retreat from international wholesale banking and refocused almost entirely on the British Isles — retail banking, commercial and SME lending, and private wealth. The global empire was gone; what remained was a bank that did ordinary things for ordinary British households and businesses. That decision — to trade the glamour of global finance for the reliability of domestic banking — is the single most important strategic pivot in the modern company's history, and everything profitable about NatWest today flows from it.

Shedding the name itself

By 2020, the bank faced a subtler problem: it had cleaned up its business but not its reputation. The name "Royal Bank of Scotland" had become politically radioactive — synonymous, in the public mind, with the 2008 crash and bankers' bonuses. So in July 2020, under CEO Alison Rose, the group did something audacious: it renamed the entire holding company after one of its subsidiaries, becoming NatWest Group plc. The logic was that the NatWest brand accounted for the large majority of the group's customers and carried none of the toxic associations of the RBS name.3 It was a corporate identity transplant on a grand scale — an admission that a name can be a liability worth billions.

The taxpayer's ledger

And what of the £45.5 billion? Here the story resists the tidy redemption arc. When the government sold its final shares in May 2025, the Treasury confirmed the uncomfortable arithmetic: across seventeen years of share sales, dividends, and fees, the state had recovered around £35 billion of its £45.5 billion outlay, leaving taxpayers roughly £10.5 billion out of pocket.2 The government's exit had been executed patiently — through directed buybacks in which NatWest itself repurchased large blocks of state stock, and through open-market trading plans that sold shares gradually to avoid crashing the price. It was orderly and professional. But it was still a loss.

The awkward decade of the state as shareholder

It is easy to underrate how much the presence of the government on the share register shaped the bank for seventeen years. A bank majority-owned by the state is a strange animal. Every decision about executive pay became a front-page political controversy; bonus rounds triggered parliamentary rows; and management operated under the permanent, competing pressures of maximising taxpayer value while also being expected to lend generously to British households and businesses through thick and thin. The overhang was financial as well as political: the market always knew the state was an eventual seller of billions of pounds of stock, and that certainty of future supply sat on the share price like a stone. Institutional investors, particularly overseas ones, were wary of owning a bank whose largest shareholder was a government that could be lobbied, that capped pay, and that might dump stock at any time. Understanding this overhang is essential to understanding why full privatisation is treated as a genuine catalyst rather than a symbolic footnote: it removes a discount that had nothing to do with the quality of the underlying business.

The honest framing is this: the £10.5 billion was not a return on an investment — it was the price of a fire extinguisher. The government never bought RBS to make money; it bought stability, and stability is expensive. Whether £10.5 billion over seventeen years was a good price for averting the collapse of Britain's payments system is a question of counterfactuals no one can settle. What is not in dispute is that, by mid-2025, the state was gone, and NatWest was, for the first time since the crisis, a fully private company answerable only to its shareholders. Which made the timing of its next crisis — a self-inflicted one — all the more excruciating.

IV. The Debanking Crisis & The Clean Slate

Coutts & Co. is not an ordinary bank. Founded in 1692, it is the bank of the British Establishment — historically the bankers to the Royal Family, and to this day a byword for discreet, exclusive private banking. To hold a Coutts account is to signal that one has, quite literally, arrived. Which is precisely why the events of 2023 were so damaging: the scandal did not erupt in some obscure trading desk, but at the most prestigious address in the entire NatWest empire.

The account closure

In June 2023, Coutts moved to close the accounts of Nigel Farage, the polarising politician and Brexit campaigner. The bank's initial line was purely commercial — that Farage no longer met the wealth threshold expected of a Coutts client.[^8] But Farage, suspecting otherwise, filed a subject access request, forcing the bank to hand over its internal file on him. What that file revealed turned a routine account closure into a national firestorm.

The governance meltdown

The internal document showed that a Coutts committee had weighed Farage's political and social views — deeming them at odds with the bank's "values" — as part of the decision to exit the relationship.[^8] Suddenly the story was no longer about one man's bank balance. It was about whether a bank could, and should, close a customer's account because it disapproved of his opinions. "Debanking" entered the national vocabulary. The political class, across the spectrum, recoiled at the idea of financial institutions acting as arbiters of acceptable belief.

Then came the fatal error. Alison Rose, NatWest's chief executive, had dined with a senior BBC journalist and, in the course of that conversation, discussed Farage's relationship with Coutts — leaving the impression that the closure was purely commercial. The BBC ran the story; it was inaccurate; and Rose, it emerged, had been the source. She had discussed a client's confidential banking affairs with the press. For a bank whose entire private-wealth proposition rests on discretion, there is scarcely a more damaging thing a CEO could do.[^8]

The fall of Alison Rose

The unravelling was swift and brutal. Initially, the NatWest board backed Rose. But within hours, under intense pressure from Downing Street — the government was, remember, still a major shareholder — that support collapsed. On 25 July 2023, Rose resigned, acknowledging a "serious error of judgement."[^8] The financial consequences followed: a subsequent remuneration review saw her forfeit unvested share awards and bonus entitlements worth approximately £7.6 million.[^9] Peter Flavel, the chief executive of Coutts itself, departed shortly after. An independent review by the law firm Travers Smith later examined the account-closure process and its governance failures.[^8]

For investors, the episode was a live-fire test of governance, and the read is genuinely two-sided. On one hand, the board's willingness to remove a celebrated CEO and claw back her pay demonstrated that accountability had teeth. On the other, the entire fiasco — a confidentiality breach at the top of the house, a committee weighing a customer's politics, an initial board misjudgement — revealed cultural and governance weaknesses at exactly the moment the bank was trying to convince the world it had grown up. Redemption narratives are fragile; this one nearly cracked.

The arrival of Paul Thwaite

Into this wreckage stepped a man almost nobody outside the bank had heard of. Paul Thwaite had spent decades inside the organisation, most recently running its Commercial & Institutional division — the unglamorous engine room, not the executive suite. He was appointed interim CEO in the crisis and confirmed as permanent chief executive in February 2024.1 Thwaite's style is the deliberate antithesis of Fred Goodwin's: low-profile, execution-focused, allergic to grand strategic pronouncements. Where Goodwin sought to conquer, Thwaite talks about "consistency" and "delivery." Whether that is genuine temperament or careful positioning, the market has, so far, rewarded the quiet competence.

There is a deeper symbolism in the choice. For the first time in a generation, NatWest reached past the charismatic, externally celebrated executive and promoted the operator who actually understood how the money was made. Thwaite had spent his career in the commercial-banking trenches, arranging financing for British companies, not giving speeches at Davos. His elevation was, in a sense, the institutional embodiment of the whole post-crisis thesis: that boring, deep operational knowledge beats visionary ambition in a business whose primary job is not to lose money. The market's task now is to watch whether that operator's discipline survives contact with the temptations of a fully private, capital-rich bank — because the last time RBS had this much confidence and this much surplus, it went shopping in Amsterdam.

The politics of debanking

The Coutts affair also left a mark far beyond NatWest's own boardroom. It crystallised a genuine public-policy anxiety — that banks, having become quasi-public utilities on which no modern citizen can opt out of relying, might use that gatekeeping power to police opinion. The government of the day ordered a review of "debanking" rules, and regulators moved to tighten the requirements around how and why banks may close customer accounts and how much notice they must give. For NatWest, the episode is a permanent reminder that its wealth and private-banking ambitions carry a specific, recurring hazard: the same exclusivity that makes Coutts valuable also makes every account decision a potential political landmine. A franchise built on serving the powerful and the controversial is, by definition, a franchise perpetually one leaked memo away from a headline.

Testing management credibility

The right way to judge new management is not by its words but by its incentives and its behaviour over time. On incentives, the structure is demanding: Thwaite is required to build and hold a shareholding worth 500% of his base salary of roughly £1.15 million, and a large share of his variable pay comes through a Restricted Share Plan tied to strict capital and risk conditions rather than short-term profit targets.[^9] The design pushes toward long-term, risk-aware value creation — precisely the opposite of the thin-capital, growth-at-any-cost incentives that destroyed RBS.

Alongside him, Rick Haythornthwaite took the chairmanship in April 2024, tasked with stabilising the governance function that the Coutts affair had exposed. A seasoned chairman from outside banking, he has signalled board-level alignment through personal share purchases — the kind of "skin in the game" gesture that institutional investors watch closely, even if it does not, by itself, prove anything about strategy.

The credibility question, though, cannot be settled by pay structures and share purchases. It is settled by results. And to judge those, we need to look under the hood at how NatWest actually makes its money.

V. The Engine Room: Core UK Retail & SME Banking

Strip away the three-hundred-year history and the crisis drama, and NatWest today is a fairly simple machine — but a simple machine with an unusually powerful flywheel. To understand the flywheel, you have to understand the boring physics of a deposit franchise, because that is where nearly all the value is created.

Three businesses, one balance sheet

The £16.6 billion of income the group generated in 2025 comes from three main sources.1

The first and largest is Commercial & Institutional banking — the division Thwaite himself used to run, and the genuine profit engine. NatWest is the UK's largest business bank, serving on the order of one in five small and medium-sized enterprises in the country, with roughly a fifth of the SME and corporate banking market.[^12] This is high-margin, relationship-driven business: a mid-sized company does not just borrow from its bank, it runs its payroll, its treasury, its foreign exchange, and its payments through it. Those relationships are sticky and they throw off fees as well as interest.

The second is Retail Banking — the current accounts, credit cards, and mortgages of more than sixteen million personal customers.[^12] NatWest holds around an eighth of the vast UK residential mortgage market, a book north of £230 billion.[^12] Mortgages are low-risk (British homeowners rarely default, and loan-to-value ratios are conservative), but they are also fiercely commoditised, which means the retail book is a battleground of price competition with Lloyds, Barclays, and the building societies.

The third is Private Banking & Wealth, anchored by Coutts and now dramatically enlarged — a business we will come to shortly, because it is where the bank is placing its biggest strategic bet.

It is worth dwelling on why the commercial franchise, not the household one, is the crown jewel — because it inverts the intuition of most retail investors, who think of NatWest as "a high-street bank." A relationship with a growing British manufacturer or a regional property developer is worth many multiples of a personal current account. The company borrows on overdrafts and term loans, hedges its currency exposure, manages its cash across dozens of accounts, runs its supplier payments, and often banks its senior executives personally too. Each of those products carries a fee or a spread, and — crucially — the whole bundle is enormously painful to move. Being the bank to one in five of Britain's small and medium-sized businesses is not just a market-share statistic; it is a position at the centre of the country's economic plumbing, one that competitors cannot easily dislodge and that generates fee income alongside interest income. This is why the division Thwaite ran on his way up is the one the whole investment case ultimately rests on.

The physics of a sticky deposit base

Here is the mechanism that makes a British high-street bank so lucrative, explained plainly. Millions of customers keep money in current accounts that pay little or no interest. They do so out of inertia — switching banks is a hassle, direct debits and salary payments are wired in, and most people simply never move. That inertia is worth an enormous amount, because it hands the bank a colossal pool of funding that costs almost nothing. NatWest sits on hundreds of billions of pounds of such deposits.[^12]

Now, what does the bank do with money it can borrow for free? In a rising interest rate world, the answer is: earn a spread on it. But there is a problem. If rates can go up, they can also come down, and a bank that simply lends short-term against free deposits sees its income swing violently with the Bank of England's decisions. The solution — and the single most important financial concept in this entire story — is the structural hedge.

The multi-billion-pound structural hedge

Think of the structural hedge as a device for smoothing out the ride. The bank takes those sticky, non-interest-bearing deposits and, instead of leaving the income to bounce around with overnight rates, it invests them in a rolling ladder of fixed-rate instruments — typically swaps and gilts spread across five to ten years of maturities. Each month, a slice matures and is reinvested at whatever rates prevail; each month, the average yield of the whole portfolio drifts toward current market rates, but slowly. The effect is to convert a volatile income stream into a predictable, slowly-evolving one.

The scale is enormous. By the end of 2025 the hedge notional stood at around £198 billion, yielding roughly 2.4% and generating in the region of £4 billion of highly predictable income.[^12] And crucially, that yield is rising. Many of the older hedges were locked in during the pandemic era at rock-bottom rates of a fraction of a percent. As those low-yielding slices mature, they are being reinvested at today's far higher market rates. This is the "reinvestment tailwind," and it is the closest thing in banking to a mechanical, almost-guaranteed income increase.

Management has put concrete numbers on it. On the back of this reinvestment dynamic, NatWest guided that structural hedge income would increase by around £1.5 billion in 2026 versus 2025, and by a further £1 billion in 2027.1 Read that carefully: it is an incremental income stream the bank has already, in effect, locked in — a defensive wall against the Bank of England cutting rates. Even if the central bank slashes rates through 2026, the maturing pandemic-era hedges reinvesting at higher rates will keep pushing hedge income up.

Here is where an independent investor should insert a note of discipline, though. The structural hedge is a genuinely powerful shock absorber, but it is not free money and it is not permanent. Its tailwind depends on the gap between the old low-yielding hedges and current rates. If market rates fall far enough, fast enough, the reinvestment yield stops being higher than the maturing yield, and the tailwind flattens or reverses. The hedge also assumes the deposits stay put; if customers, finally roused from inertia by higher savings rates elsewhere, pull their money, the hedge notional shrinks. The mechanism is real, and it is currently a tailwind. It is not a law of nature.

That tension — a powerful, cash-generative core franchise versus the cyclical, rate-dependent nature of its earnings — is the central investment question. And it is precisely why management is now spending money to buy something the deposit machine cannot provide: capital-light, fee-based growth.

VI. Tactical Capital Deployment: The Art of the Bolt-On

Here is the poetic justice of the NatWest story. The bank that destroyed itself with the largest, most reckless acquisition in banking history is now — under Thwaite — practising the exact opposite discipline: small, cheap, domestic, low-risk bolt-ons, several of which the counterparties practically paid NatWest to take. If ABN AMRO was a cautionary tale about M&A hubris, the deals of 2024 through 2026 are a masterclass in its inversion.

Deal one: the bank someone paid NatWest to take

In June 2024, the supermarket group Sainsbury's decided it wanted out of banking altogether. Rather than run an auction and pocket a premium, Sainsbury's structured a deal that reads almost backwards: Sainsbury's paid NatWest to take over its retail banking book. NatWest acquired roughly £2.5 billion of unsecured personal loans and credit card balances, along with around £2.6 billion of customer savings, and about a million customer accounts — and Sainsbury's contributed approximately £125 million of cash to NatWest as part of the transfer.[^5]

Why would a seller pay the buyer? Because for a non-bank like Sainsbury's, running a regulated lending operation had become more trouble than it was worth — capital-hungry, compliance-heavy, and non-core. Exiting cleanly was worth paying for. For NatWest, the economics were close to ideal: it gained a million pre-vetted, already-profitable retail customers and a cash cushion to fund the integration. This is what disciplined capital deployment looks like — buying customers and deposits at a negative price because you are the natural, low-cost home for assets someone else can no longer efficiently hold.

Deal two: patience rewarded at Metro Bank

The Metro Bank story is even more instructive, because it lets us watch NatWest's discipline improve in real time. Back in 2021, NatWest bought a roughly £3.0 billion Metro Bank mortgage portfolio for about £3.13 billion — a small premium, struck at the peak of the ultra-low-rate mortgage boom, when everyone wanted mortgage assets.

Fast forward to September 2024. Metro Bank, under acute pressure to shore up its balance sheet in a higher-rate world, needed to sell. NatWest, holding the stronger hand, acquired a £2.4 billion portfolio of prime residential mortgages for about £2.3 billion in cash — buying high-quality assets at a discount to their face value.[^6] The contrast between the two deals is the whole point: the same buyer, the same type of asset, but a premium in the frothy market and a discount in the distressed one. That is counter-cyclical capital allocation — the discipline RBS conspicuously lacked when it bought ABN AMRO at the very top.

Deal three: the £2.7 billion bet on wealth

The bolt-ons above were tactical. The Evelyn Partners deal is strategic — and by some distance the largest acquisition NatWest has made since the 2008 bailout.

In February 2026, NatWest agreed to acquire Evelyn Partners, one of the UK's largest wealth managers, from the private equity firms Permira and Warburg Pincus, at an enterprise value of £2.7 billion.[^7] The deal completed on 30 June 2026.4 Evelyn brought roughly £69 billion of assets under management and administration; combined with NatWest's existing wealth operations (about £59 billion), the enlarged business commands around £127 billion of client assets, instantly creating one of the UK's leading private banking and wealth platforms.4

On price, the deal looks disciplined rather than desperate. Market commentary pegged it at roughly 15 times EBITDA before synergies and under 10 times after accounting for around £100 million of targeted annual run-rate cost synergies (against roughly £150 million of costs to achieve them).4[^7] For context, when Royal Bank of Canada bought Brewin Dolphin it paid in the mid-teens on an earnings multiple, and abrdn's purchase of Interactive Investor was struck considerably higher; against those benchmarks, NatWest does not appear to have overpaid — a meaningful signal from a company whose most famous act was overpaying.

Why wealth, and why now

The mechanics of handing money back

Sitting underneath all three deals is a capital-allocation philosophy that deserves its own moment, because it is the day-to-day expression of everything the bank learned from 2008. NatWest generates capital faster than it can profitably lend it out, and the disciplined response to that happy problem is to return the surplus rather than to chase growth for its own sake. The most striking illustration came during the government's exit itself: NatWest repeatedly bought back large blocks of its own shares directly from the Treasury in "directed" buybacks, using its surplus capital to simultaneously shrink the state's stake and reduce its own share count. It was a rare arrangement in which returning capital to the largest shareholder and accelerating the bank's own privatisation were the same transaction. Layer on top the ongoing open-market buybacks and a dividend the bank aims to set at around half of earnings, and the picture is of an institution whose primary use of cash is now giving it back — the polar opposite of the acquisition-hungry RBS that hoarded capital to fund the next conquest.1 The activist's caution applies here too: a bank that returns capital aggressively while guiding its safety buffer downward is making an implicit bet that credit losses stay benign. That bet is fine until a recession tests it.

The strategic logic ties directly back to the structural-hedge discussion. Traditional banking income is capital-intensive and cyclical — it rises and falls with interest rates and requires the bank to hold expensive regulatory capital against every loan. Wealth management income is the opposite: it is a recurring fee, charged as a percentage of client assets, that consumes very little capital. By bolting Evelyn onto Coutts, NatWest is deliberately shifting its earnings mix toward capital-light, fee-based revenue — building, in effect, a second income stream that does not depend on the direction of interest rates. Management estimated the deal would lift group fee income by around 20% before revenue synergies, at a CET1 capital cost of roughly 130 basis points.4

The independent caveat is equally clear. Wealth management is a people business, and the assets can walk out the door. The value of Evelyn sits substantially in its client relationships and its advisers, both of which can leave if the integration mishandles culture, technology, or compensation. NatWest is paying £2.7 billion for something that has legs. Integration execution — not the purchase price — will determine whether this becomes the growth engine management promises or an expensive lesson in the limits of buying loyalty. On the completion call, Thwaite framed the deal as accretive to growth and returns in year one and "an important step" in the strategy;4 whether the client assets and advisers stay to make that arithmetic real is the thing to watch.

Having assembled the pieces — a fortress deposit base, a structural hedge, a dominant SME franchise, and a newly enlarged wealth arm — the question becomes whether these amount to a durable competitive advantage, or merely a well-run bank in a good year. Time to war-game it.

VII. Strategic Frameworks: Porter's Five Forces & Hamilton Helmer's 7 Powers

Banking is a deceptively hard industry to build a moat in. The product — money — is perfectly fungible. Anyone can offer a loan or a savings account. And yet the UK banking market has been remarkably stable for decades, dominated by the same handful of names. To understand why, and to test how much of NatWest's advantage is real versus rhetorical, it helps to run the business through two classic frameworks.

Porter's Five Forces

Threat of new entrants: low to moderate. The regulatory barrier is the moat that never sleeps. To take deposits and lend at scale in the UK, a firm needs authorisation from the PRA and FCA and must hold billions in regulatory capital against its assets. This is enormously expensive and slow. Digital challengers like Monzo and Revolut have shown they can win the transaction layer — the app, the card, the everyday spending — and have captured millions of customers. But converting app users into a full-service bank that originates mortgages and lends to mid-sized companies is a different and far harder game, and the incumbents' scale in lending remains largely intact. The threat is real at the edges and modest at the core. The deeper strategic point is that the challengers have, so far, mostly won the parts of banking that are fun and cheap to run — the slick app, the instant notifications, the fee-free spending abroad — while the incumbents retain the parts that are boring, capital-intensive, and profitable: the mortgage book, the SME lending relationship, the vast pool of sticky deposits. A neobank can acquire a customer's attention with a beautiful interface, but to hold their salary, lend them a house, and finance their employer, it must build exactly the same expensive, regulated, capital-heavy machinery the incumbents already own. Some challengers are now attempting precisely that climb into full-service banking, and if they succeed at scale it would be the most serious long-term threat to NatWest's economics. But it is a slow, costly climb, and the incumbents are not standing still — NatWest spends heavily on its own digital platforms specifically to blunt the experience advantage that first drew customers to the challengers.

Bargaining power of buyers: high. This is the force that squeezes NatWest hardest. In mortgages and savings, the product is commoditised and the customer is increasingly empowered. The Current Account Switch Service has made moving banks a seven-day, low-friction process, and comparison sites make rate-shopping trivial. A depositor chasing yield can move with a few taps. This is precisely why the "sticky deposit" advantage, powerful as it is, rests on inertia that regulators are actively trying to erode — the FCA's Consumer Duty regime, with its emphasis on "fair value" in savings pricing, is a direct regulatory push to wake customers up and narrow exactly the deposit spread NatWest earns.[^10]

Competitive rivalry: intense. The UK is a consolidated oligopoly — Lloyds, NatWest, Barclays, and HSBC, plus Nationwide and Santander — and in a mature, low-growth market, oligopolists compete on price. Mortgage pricing wars are a recurring feature, and they compress margins for everyone. Rivalry is the permanent headwind against which NatWest's structural-hedge tailwind blows.

The other two forces — supplier power (the "suppliers" being depositors and wholesale funders) and threat of substitutes (fintech payment rails, private credit) — are present but secondary. The verdict from Porter is a market that protects incumbents from new competition while forcing them into brutal competition with each other.

Hamilton Helmer's 7 Powers

Of Helmer's seven sources of durable advantage, three genuinely apply to NatWest, and it is worth being precise about how strong each really is.

Scale economies: strong, and probably the real moat. NatWest's several-hundred-billion-pound deposit base gives it a structurally low cost of funding, and its size lets it spread the enormous fixed costs of technology, cybersecurity, and regulatory compliance across a vast customer base. A mid-sized bank pays nearly the same fixed compliance and IT bill on a fraction of the revenue. This cost advantage compounds and is very hard for a smaller rival to overcome — it is the most defensible thing about the franchise.

Branding: strong, but narrow. The Coutts name carries three centuries of exclusivity and cannot be replicated at any price — you cannot buy a 1692 founding date. That is a genuine, durable brand power. But note its scope: it applies to the high-net-worth wealth niche, not to the mass-market NatWest brand, where "brand" mostly means familiarity, not pricing power. The 2023 debanking scandal was, in part, a reminder that even a 300-year-old brand can be damaged by a single week of governance failure.

Switching costs: moderate to strong, depending on the customer. For a retail current-account holder, switching costs are low and falling — the whole point of the Switch Service. But for a mid-sized company that runs its payroll, treasury, foreign exchange, and multiple credit lines through NatWest, unwinding that web is genuinely painful and risky. This is why the Commercial & Institutional franchise is stickier and more profitable than the retail book, and why it, not mortgages, is the true engine.

The honest synthesis: NatWest's durable advantages are real but specific. Its scale-driven funding and cost advantage is formidable. Its commercial-banking switching costs are meaningful. Its Coutts brand is unique. But large parts of its business — mortgages, savings — enjoy little defensible advantage at all and compete on price. This is not a wide-moat monopoly; it is a low-cost incumbent in a protected oligopoly, with a couple of genuinely defensible niches. That distinction matters enormously for how much of the current profitability an investor should expect to persist.

VIII. Playbook: Business & Investing Lessons

Every great business story leaves behind a set of transferable lessons, and NatWest's arc — from the largest bank on Earth to insolvency to steady profitability — is unusually rich in them. Four stand out.

Lesson one: the peril of M&A hubris. The ABN AMRO deal has earned its place in business-school syllabuses as the definitive case study in acquisition disaster. The failure was not simply that RBS bought a bank; it was that it bought a huge, complex, capital-intensive business it had barely examined, at the peak of the cycle, funded with borrowed short-term money it could not roll over when markets froze. The lesson is not "don't acquire" — NatWest itself acquires happily today. It is that the price you pay, the diligence you do, the point in the cycle at which you buy, and the way you fund it matter more than the strategic logic of the deal. A brilliant strategic rationale executed at the wrong price and the wrong time is how empires die.

Lesson two: a sticky deposit franchise is a bank's crown jewel. The single most valuable asset NatWest owns does not appear as an asset on its balance sheet at all — it is the inertia of millions of customers who leave money in accounts paying almost nothing. In a rising-rate world, that free funding is a licence to earn a spread. The corollary, which investors must never forget, is that this advantage is behavioural, not contractual: it lasts exactly as long as customers stay asleep.

Lesson three: the structural hedge as a shock absorber. Managed well, a multi-billion-pound hedge lets a bank smooth its earnings, delay the pain of rate cuts, and turn a volatile income stream into a predictable one. It is one of the most under-appreciated tools in banking — invisible to most customers and even many investors, yet responsible for billions in reliable income. Its limitation, as we have said, is that it smooths the ride but does not change the destination: over a full cycle, hedge income still tracks the general level of rates.

Lesson four: the migration from lending to fees. The deepest strategic idea in the modern NatWest is the deliberate shift from capital-intensive, cyclical lending toward capital-light, recurring fee income — the logic behind the Evelyn Partners deal. Lending ties up expensive regulatory capital and rises and falls with the economy. Wealth-management fees consume little capital and compound with markets. For a bank trying to de-risk and de-cyclicalise its earnings, moving toward fees is the most efficient path — provided it can hold on to the assets and advisers it pays for. That "provided" is doing a great deal of work, and it is exactly where bulls and bears part company.

A fifth lesson, about culture and complacency. The most uncomfortable takeaway from the whole seventeen-year arc is that the same institution produced both the reckless empire-builder of 2007 and the disciplined operator of 2025 — the culture did not change because bankers became wiser, but because a near-death experience and a decade of state supervision forced it to. That raises the question no redemption story likes to ask: does the discipline survive once the disciplinarian leaves? The government is gone, the balance sheet is strong, the profits are flowing, and the bank is once again acquisitive. Those are precisely the conditions under which the last catastrophe incubated. Nothing about the current strategy resembles the ABN AMRO folly — the deals are small, cheap, and domestic — but the enduring lesson of RBS is that overconfidence arrives quietly, dressed as success, and that the moment a management team stops believing a crisis could happen to them is the moment the clock starts again. The most valuable thing an investor can track in NatWest is not a financial ratio at all; it is whether the institution keeps behaving like a bank that remembers.

IX. Bull vs. Bear: The Multibillion-Pound Question

So we arrive at the reckoning. Is NatWest a redeemed compounder that global institutions should own now that the state overhang is gone — or a well-run bank enjoying the last of a rate cycle that has already turned? Let us make the case both ways, but first, let us be disciplined about what to actually watch.

The three KPIs that matter most

Forget the dozens of metrics in the annual report. For NatWest, three numbers tell the story, and an investor tracking these over time will understand the business better than one drowning in detail.

Net interest margin (NIM). This is the spread between what the bank earns on assets and pays on funding — the core of a lender's profitability. NIM was 2.34% in 2025, up 21 basis points on the year, driven largely by the deposit and hedge dynamics we have described.1 On the FY2025 earnings call, management leaned heavily on the hedge reinvestment story to reassure analysts worried about the coming rate-cutting cycle — a framing worth testing against actual margin outcomes in the quarters ahead.6 The direction of NIM is the single cleanest read on whether the rate environment is helping or hurting.

Return on tangible equity (RoTE). This measures how much profit the bank squeezes from each pound of shareholder capital — the ultimate test of whether management is creating value. NatWest posted a striking 19.2% in 2025 and guided to greater than 17% for 2026.1 Note what that guidance implies: management itself expects returns to ease from the 2025 peak — an admission, in the numbers, that some of the current profitability is cyclical.

CET1 capital ratio. This is the bank's core capital buffer, the cushion that both satisfies regulators and funds shareholder returns. It stood at 14.0% at the end of 2025, and management is guiding it down toward roughly 13.0%.1 A bank deliberately running its capital ratio lower is signalling confidence — it means surplus capital being handed back to shareholders through dividends and buybacks rather than hoarded. It is also, an activist would note, less margin for error if credit losses spike.

The risk radar

NIM compression. The most immediate risk. If the Bank of England cuts rates faster than NatWest can reduce what it pays depositors, the spread narrows. The structural hedge softens this blow but does not eliminate it. The 2026 RoTE guidance below the 2025 level is management quietly acknowledging the pressure.

UK SME credit exposure. As the country's largest business lender, NatWest is uniquely geared to the health of the British economy. Here the mechanism matters: banking profits are extraordinarily sensitive to credit losses because of leverage. A bank earns a spread of a couple of percent on its assets but holds only a thin sliver of equity against them, so a seemingly modest rise in loan defaults — from benign levels to merely normal recessionary ones — can wipe out a large chunk of a year's profit through impairment charges. Small and medium-sized businesses are the first to feel a downturn, the first to miss payments when demand softens or input costs spike, and NatWest has more exposure to them than any peer. In good times this concentration is a margin advantage; in a recession it is the fault line along which the earnings crack first. The bank's greatest strength and its most concentrated macro risk are the same book of loans.

Operational and cyber resilience. A modern bank is, functionally, a technology company that happens to hold a licence to take deposits, and the entire deposit franchise rests on customers trusting that their money and their data are safe and always accessible. UK banks, NatWest included, have suffered high-profile IT outages that locked customers out of their accounts, and the threat surface only grows as services move fully digital and cyber-attackers grow more sophisticated. A serious data breach or a prolonged systems failure would strike at the one asset the whole model depends on — trust — and regulators now treat operational resilience with the same seriousness as capital adequacy. It is an unglamorous risk that rarely shows up in a valuation model until the day it suddenly dominates the headlines.

Wealth integration execution. As discussed, merging Evelyn Partners into Coutts is a cultural and operational challenge. Adviser departures or client outflows would quietly erode the very asset base the £2.7 billion was meant to buy.

Myth versus reality

Two consensus narratives about NatWest deserve a fact-check. The first myth is that privatisation itself transformed the business. It did not; the operational turnaround was largely complete years before the state sold its last share. What privatisation changed was the ownership structure and the perception, not the earnings power. Conflating the two risks crediting a share sale for profits that were earned by the deposit franchise and the rate cycle. The second myth, popular among skeptics, is that NatWest is "just a play on interest rates" — a bond fund with branches. That is too harsh. The commercial-banking switching costs, the SME market position, and the emerging fee-based wealth business are real, structural sources of value that do not simply evaporate when rates fall. The truthful synthesis sits between the two stories: a genuine franchise with durable niches, wrapped inside an earnings stream that is undeniably rate-sensitive and currently cresting.

The bull case

The bulls make three arguments. First, the removal of the state overhang is a genuine catalyst: for seventeen years, government ownership meant political interference in pay, a persistent supply of stock hanging over the market, and a discount that deterred some global institutions. That overhang is now gone.2 Second, the capital-return machine is formidable — a 14% CET1 ratio being managed down toward 13% means years of surplus capital flowing to shareholders through a rising dividend (targeting a 50% payout of earnings) and consistent buybacks.1 Third, the wealth pivot, if executed, structurally raises the quality of earnings by adding capital-light, rate-insensitive fee income.

The bear case

It is instructive to place NatWest against its closest mirror, Lloyds Banking Group. Both are domestically focused UK banks that emerged from the crisis under state ownership; both live and die by the British consumer and the British interest rate. The comparison sharpens the bull point: NatWest's larger tilt toward commercial and institutional banking gives it a business mix that is arguably higher-margin and stickier than a pure mortgage-and-cards retail bank, and its wealth ambitions now push it further from the commoditised core. But the comparison also sharpens the bear point: two near-identical banks competing for the same British deposits and the same British mortgages is the very definition of the oligopoly rivalry that grinds margins down. Neither can grow much without taking share from the other, and the weapon for taking share is price.

The bears counter with a single, unifying observation: we are at or past the peak of the interest rate cycle, and NatWest's spectacular 2025 numbers are, in large part, a gift of that cycle. Net interest margins have likely peaked; a sustained decline in rates will erode them regardless of the hedge. Layered on top is relentless mortgage-price competition from Lloyds, Barclays, and Nationwide, which caps organic growth and grinds down lending margins in the commoditised heart of the retail book. In this reading, the 19.2% RoTE is not a new normal but a high-water mark, and the honest question is not how high profitability can go but how gracefully it declines.

The activist's stress test

A skeptical long/short investor would push on a few things beyond the cyclical debate. On governance: the 2023 Coutts affair exposed a control-and-culture weakness at the top of the house, and while accountability was ultimately delivered, the episode is a reminder that reputational risk in a wealth franchise is real and recurring. On capital allocation: buying a wealth manager from private equity — sellers who are, by definition, sophisticated about exiting at the right price — invites the question of who got the better end of the £2.7 billion, and the answer will only be known once integration plays out. And on the earnings mix: a bull would call the structural hedge a "quality" earnings stream; a bear would call it a bet on the shape of the yield curve dressed up as an operating business. Both are partly right.

The synthesis is not a verdict but a framing. NatWest is unambiguously a better, safer, more profitable institution than the one that collapsed in 2008 — that transformation is real and hard-won. Whether today's profitability is a durable feature of a well-run oligopolist or a cyclical peak flattered by rates is the question that will define the next several years, and the three KPIs above are how a patient investor will know which story is winning.

X. Epilogue

Return, one last time, to that unremarkable morning in May 2025 — the trading plan, the block of shares, the spreadsheet quietly updating. It is worth sitting with how strange it is that the end of Britain's most traumatic corporate saga arrived without drama. But perhaps that is the entire point. The Royal Bank of Scotland made headlines by being the biggest and the boldest, and it nearly took the British financial system down with it. NatWest Group earned its redemption by becoming the opposite: smaller, duller, domestic, disciplined. The absence of drama was the achievement.

The arc is complete and worth stating plainly. A three-hundred-year-old Scottish clearing bank reached, under one man's hubris, to become the largest bank in the world, and shattered. It spent a decade shrinking a trillion pounds of balance sheet, retreating from the globe, and even shedding its own name. It stumbled, badly, in a self-inflicted governance crisis that cost it a chief executive. And it emerged, under quieter leadership, as a highly profitable, fully private, capital-returning bank focused on the boring, lucrative mechanics of British deposits, small-business lending, and private wealth.

The lesson NatWest offers is almost anti-heroic, and all the more valuable for it: in banking, simple and local, executed with discipline, beats global and complex almost every time. The empire that tried to conquer the world nearly destroyed itself; the bank that retreated to its own islands prospered.

For the long-term investor, the story does not end with the redemption — it merely resets the question. The genuinely hard analytical work begins now, in the ordinary years, when there is no crisis to focus the mind and no state supervisor to enforce restraint. The three numbers to watch are unglamorous and telling: the net interest margin, which reveals whether the rate cycle is friend or foe; the return on tangible equity, which management itself expects to ease from its 2025 peak and which will show whether the franchise can hold its quality as the tailwind fades; and the capital ratio, which will reveal, quarter by quarter, whether a cash-rich bank keeps its discipline or rediscovers its ambition. Everything essential about NatWest's next chapter is encoded in the interplay of those three figures and in one unquantifiable thing behind them — whether an institution that once forgot the meaning of risk has truly learned to remember it.

Whether that hard-won prosperity endures as the rate cycle turns is now the only question that matters — and it is one the market, at last free of the state's long shadow, will answer on its own.

References

-

NatWest Group plc Annual Results 2025 — Investegate / NatWest Group, 2026-02-13 ↩↩↩↩↩↩↩↩↩↩

-

Government sells final NatWest shares and confirms a £10.5bn loss to taxpayers — ITV News, 2025-05-30 ↩↩↩↩

-

NatWest: Key dates in the bank's history from rescue to privatisation — Bracknell News (PA), 2025-05-30 ↩↩↩↩↩↩↩↩↩↩↩↩↩

-

NatWest Group announces the completion of the acquisition of Evelyn Partners — NatWest Group, 2026-06-30 ↩↩↩↩↩

-

London Stock Exchange Company Page: NatWest Group plc (NWG) — LSE ↩

-

NatWest Group plc FY 2025 Earnings Call Webcast & Materials — Seeking Alpha, 2026-02-13 ↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube