National Grid plc: Electrifying the Monopolist

I. Episode Introduction & The Trillion-Dollar Grid Paradox

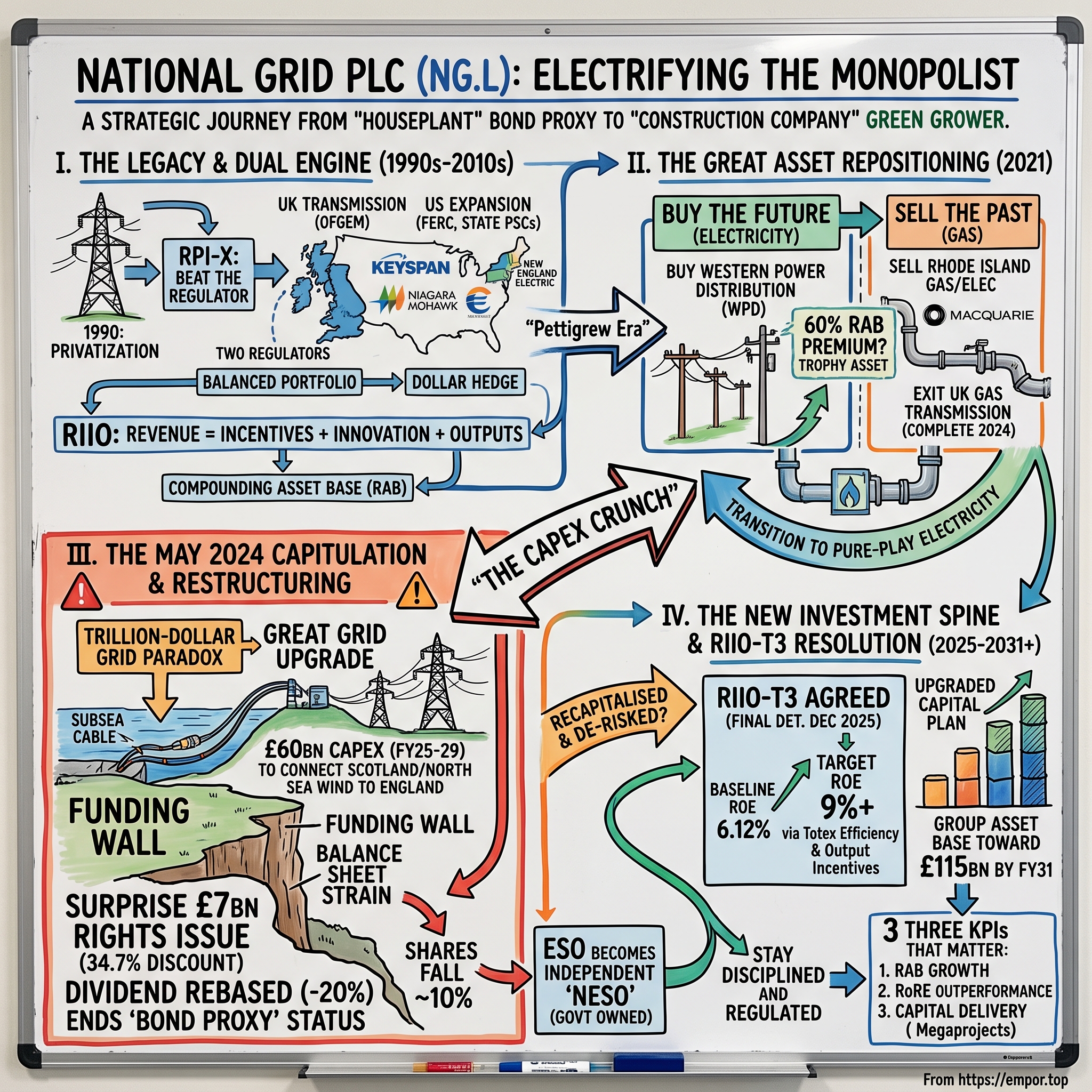

There is a particular kind of stock that pension funds and widows and orphans have loved for a century. It does not do anything exciting. It sends you a cheque. It sits in the portfolio like a well-behaved houseplant, absorbing inflation, throwing off a yield, asking nothing of you. For decades, National Grid plc — the company that owns the physical wires carrying electricity across England and Wales, and a sprawling utility empire across the American Northeast — was exactly that plant. Boring. Defensive. A "bond proxy" you bought and forgot.

Then, on the morning of May 23, 2024, the houseplant tried to eat the room.

National Grid's management, led by chief executive John Pettigrew, walked investors into a surprise that no one on the buy-side had priced in: a fully underwritten £7 billion rights issue — the largest cash call by a UK-listed company since the depths of the Global Financial Crisis — priced at 645 pence per new share, a 34.7% discount to the theoretical ex-rights price.12 In the same breath, the company "rebased" its dividend, resetting it roughly 20% lower to reflect the flood of new shares, and quietly ended a growth streak that income investors had treated as a law of nature.3 The shares fell about 10% on the day.[^4] For a company whose entire investment identity was reliability, the message landed like a betrayal.

Here is the paradox at the centre of this story. National Grid is not a speculative startup burning cash to chase a market. It is a regulated monopoly. It owns the tollbooth — the high-voltage transmission network that every kilowatt-hour in England and Wales must physically cross, and the poles-and-wires distribution systems that reach millions of homes in New York and New England. Its revenues are set by regulators, largely insulated from competition, and indexed to inflation. This is supposed to be the safest business model in capitalism. So how does the owner of the tollbooth end up in a capital crunch severe enough that it must go to its own shareholders, hat in hand, and dilute them by nearly a third?

The short answer is that National Grid decided — or was forced by the physics of decarbonisation — to stop being a cash cow and start being a construction company. Management committed to a capital investment program of around £60 billion over five years (FY2025 to FY2029), close to double the prior five-year pace, to rewire Britain and America for a net-zero grid.2 A regulated utility earns a return on the capital it sinks into the ground — its "Regulated Asset Base" — so in theory, spending more is the growth engine. But you cannot fund £60 billion of concrete, copper, and subsea cable on debt alone without blowing through the credit metrics that keep your borrowing cheap. Something had to give. In May 2024, it was the shareholders.

This is the story of how a 20th-century wires monopoly became a 21st-century growth-and-capex machine, and whether that transformation is a structural opportunity or an expensive gamble dressed in the language of the energy transition. To get there, we will trace:

- The origins of Britain's supergrid and the Thatcher-era privatization that created National Grid.

- The transatlantic "dual engine": how buying into New York and New England reshaped the company.

- The audacious 2021 portfolio swap — selling gas, buying Britain's largest distribution network at a record premium — and the question of whether management overpaid.

- The machinery of regulated returns: RPI-X, RIIO, and the RIIO-T3 battle that concluded only months before this writing.

- And the explicit "why win / why not" spine that any long-term owner of this stock must weigh.

Let's start where the wires do.

II. The Legacy of Privatization & Grid Origins

Picture Britain in the aftermath of the Second World War: a patchwork of municipal and private power stations, each an island, wired to its own town with no coherent way to share electricity across the country. If your local station tripped, your lights went out — never mind that a plant fifty miles away had spare capacity. The engineering answer to this fragmentation was radical for its time: build one giant national machine.

That machine was born under the Central Electricity Generating Board (CEGB), created in 1957, which took on the task of constructing a single, synchronised, high-voltage "supergrid" stitching the nation's power stations together. This was engineering as nation-building — the 275kV and later 400kV backbone that made it possible to run the whole country as one electrical system. For three decades, generation and transmission lived together inside a state monopoly. Electricity was a public service, planned centrally, priced politically.

Then came the revolution. In 1990, Margaret Thatcher's government privatized the electricity sector — one of the boldest and most consequential deregulations of the era. The insight driving it was that the industry was not one business but several, with very different economics. Generation — building and running power stations — could be made competitive; multiple firms could compete to sell electricity into a pool. Retail supply could eventually be opened to competition too. But the transmission grid — those high-voltage steel towers and the wires strung between them — was a textbook natural monopoly. It made no economic sense to build a second set of pylons alongside the first. So the grid was carved out and handed to a new entity to own and operate: National Grid. Generation was privatized and fragmented; the wires were privatized and kept whole.

That distinction — competitive where competition works, regulated where it doesn't — is the DNA of everything that follows. National Grid inherited the one asset in the system that no rival could ever replicate, and in exchange for that protected position, it accepted that a regulator, not the market, would set its prices. In 1995, National Grid was floated on the London Stock Exchange, beginning its life as a publicly traded company and eventually consolidating into National Grid plc.4

From RPI-X to RIIO: how a monopoly gets paid

Here is the concept that determines whether you make or lose money owning this stock, explained plainly. A regulated monopoly cannot simply charge what it likes; if it did, it would gouge captive customers. So the regulator — in Britain, Ofgem — sets the rules for how much revenue the company is allowed to collect. Get those rules right in your favour and you compound wealth for decades. Get them wrong and you own a very expensive, very safe way to lose to inflation.

The original framework was called RPI-X. The idea, imported from British Telecom's privatization, was elegant: let the company raise prices each year by the retail price index minus an efficiency factor "X." If inflation ran at 4% and X was set at 3%, prices could rise only 1%. The company was thereby forced to cut costs faster than inflation, and — in theory — passed the savings to consumers. RPI-X was brilliant at squeezing fat out of sleepy nationalised monopolies. But it had a fatal flaw for the modern era: it rewarded cutting, not building. A framework designed to make a company spend less is precisely the wrong tool when the national priority becomes spending vastly more to decarbonise.

So in 2013, Ofgem replaced it with RIIO — "Revenue = Incentives + Innovation + Outputs." The name is ungainly but the mechanism is the whole game. Under RIIO, the company is allowed to earn a specified rate of return on its Regulated Asset Base (RAB), also called Regulated Asset Value (RAV) — essentially the accumulated, inflation-adjusted value of all the infrastructure it has built and paid for. Spend capital wisely, and that asset base grows; the allowed return is applied to a bigger base; earnings compound. Crucially, RIIO bolted incentives onto this: hit reliability, customer-service, and environmental targets and you earn bonus returns (called Output Delivery Incentives); miss them and you're penalised. Beat the regulator's cost assumptions on total expenditure ("totex") and you keep a share of the savings.

The practical upshot is that a well-run network operator under RIIO can earn meaningfully more than the baseline "allowed" return by executing better than the regulator assumed. That outperformance margin — the gap between what you're allowed and what you actually deliver — is the closest thing a monopoly has to entrepreneurial upside. Hold that idea; it becomes the crux of the bull case, and the battleground of the RIIO-T3 fight, later in this story. For now, the takeaway is simpler: by the early 2010s, National Grid was a mature, cash-generative UK monopoly operating under a framework that finally rewarded investment. The question was where to grow. The answer, initially, lay 3,000 miles west.

III. The US Expansion & Transatlantic Dual Engine

By the late 1990s, National Grid's leadership faced a pleasant problem and an unpleasant one. The pleasant problem: the UK business threw off enormous cash. The unpleasant one: British regulators, having wrung efficiency out of the grid through RPI-X, kept tightening allowed returns. A monopoly that can't raise domestic prices and can't build much new needs somewhere else to put its capital to work. Management looked across the Atlantic and saw a fragmented, under-consolidated American utility landscape — and a chance to diversify its regulatory risk across two continents so that no single regulator held all the cards.

The buying spree came in three great waves. In 2000, National Grid planted its flag in America by acquiring New England Electric System together with Eastern Utilities Associates for roughly $3.2 billion, instantly making it a serious utility operator in Massachusetts and the surrounding states.5 In 2002, it pushed into upstate New York with the purchase of Niagara Mohawk for around $3 billion, a deal that gave it a dominant network position across a vast swath of New York State.5 And then, in 2007, came the blockbuster: the acquisition of KeySpan for about $7.3 billion in equity value (an enterprise value near $11.8 billion once debt was included), which handed National Grid the gas and electric distribution networks serving New York City, Long Island, and parts of New England.6 In seven years, National Grid had gone from a UK-only wires company to one of the largest utilities in the northeastern United States.

Two regulators, two very different games

To understand why this mattered strategically, you have to understand how differently the two sides of the Atlantic pay their monopolies — because National Grid was deliberately assembling a portfolio that balanced them.

In Britain, regulation is unified and national: one regulator, Ofgem, sets a multi-year framework covering the whole network with heavy emphasis on capital investment and performance incentives. It is high-stakes and formulaic, a single negotiation every five years that determines your fate.

In the United States, regulation is fragmented and layered, which is either a nightmare or a hedge depending on your temperament. At the federal level, the Federal Energy Regulatory Commission (FERC) oversees interstate transmission and has historically allowed relatively generous, stable returns on equity — often in the 10%-plus range — because it wants to encourage investment in the bulk power system. At the state level, bodies like the New York Public Service Commission and the Massachusetts Department of Public Utilities govern the local distribution networks through periodic "rate cases": grinding, quasi-legal negotiations over exactly how much a utility can charge households, how much storm-damage cost it can recover, and how fast it can raise bills. These proceedings are intensely political — no state regulator wants to be seen waving through a rate hike — but they are also frequent, granting the operator repeated bites at resetting its economics rather than one make-or-break decision per half-decade.

The economic logic of the dual engine

What National Grid built, whether by design or by opportunistic accretion, was a barbell. On one end sat the UK: high capital intensity, incentive-driven, feast-or-famine on the five-year regulatory cycle, but with real upside for operational outperformance. On the other sat the US: steadier, rate-base-driven, less spectacular but more diversified across states and regulators, and denominated in dollars — a natural currency hedge for a sterling-reporting company.

The independent read on this era is more mixed than the strategic tidiness suggests. The US expansion did genuinely diversify the business and gave National Grid a second, large rate base to grow. But American gas and electric distribution also came with the messier, more politically exposed parts of utility life: aging infrastructure, storm liability, gas-safety obligations, and rate cases that can turn hostile. And a heavy weighting toward gas distribution, in particular, would look increasingly awkward as the world's climate policy turned against the molecule. By the mid-2010s, a new chief executive would look at this sprawling, gas-heavy, two-continent portfolio and conclude that it needed to be radically reshaped. That reshaping — the boldest corporate chess match in the company's modern history — is where we turn next.

IV. The Great Asset Repositioning of 2021: Buying the Future

When John Pettigrew became chief executive in 2016, he was the ultimate insider — a man who had joined National Grid as a graduate engineer and spent his entire career inside its networks, rising through operations until he understood the physical grid better than almost anyone alive. That operational fluency shaped a conviction that would define his tenure: in a decarbonising world, the winning bet was electricity, and the losing bet was gas. Electricity was the vector through which wind, solar, and nuclear would reach homes and factories. Gas — the fossil molecule National Grid had spent billions acquiring in America and long transported across Britain — was, in his framing, a stranded future. So Pettigrew set out to sell the past and buy the future, and he did it through an interlocking sequence of transactions of remarkable scale and ambition.

The three-step pivot

Step one — buying Western Power Distribution. In March 2021, National Grid agreed to acquire Western Power Distribution (WPD), the UK's largest electricity distribution business, from the American utility PPL Corporation. The equity value was £7.8 billion, and the enterprise value — including debt — reached roughly £14.2 billion.67 WPD served millions of homes across the Midlands, the South West, and Wales, and it was widely regarded as the best-run distribution operator in Britain. In one stroke, National Grid vaulted from owning no UK electricity distribution to owning the largest such network in the country. It later rebranded the business National Grid Electricity Distribution.

Step two — selling Rhode Island. In the same breath, National Grid agreed to sell The Narragansett Electric Company, its Rhode Island electric and gas utility, to PPL for an equity value of $3.8 billion (about £2.7 billion).67 This was not a coincidence; it was a partial swap. National Grid was trading a smaller, gas-heavy American asset — sold at a rich US valuation — for a larger, pure-electricity British one, and using the proceeds to help fund the purchase. Structuring it as a two-way deal also made the strategic story cleaner to regulators: this was portfolio realignment, not empire-building.7

Step three — exiting UK gas transmission. The final and most symbolically important move was National Grid's retreat from the gas business it had operated for decades. It sold a 60% stake in its UK gas transmission network — rebranded National Gas — to a Macquarie-led consortium (Macquarie Asset Management and British Columbia Investment Management), a deal that completed in early 2023.[^9] It then exited the remaining position, selling the final 20% stake for £686 million in a deal completed in September 2024, formally ending National Grid's ownership of the pipes that carry Britain's gas.[^10] The pivot to pure-play electricity was, on paper, complete.

Did they overpay? The RAV premium question

Now the uncomfortable part, and the reason a neutral analyst cannot simply applaud the strategy. Regulated network assets have an anchor value — the Regulated Asset Value on which the regulator lets you earn a return. When one utility buys another, the price is usually quoted as a premium to RAV: pay a 20% premium and you've paid £1.20 for every £1.00 of regulated asset base. Historically, UK regulated utility deals had changed hands at premiums in the range of roughly 10% to 30% — the extra reflecting the value of expected outperformance and the scarcity of these assets.

National Grid paid for WPD at an implied premium to RAV in the region of 60% — roughly double the top of that historical band. Management's defence was that WPD was a generational, one-off asset: the crown jewel of UK distribution, the best-run network in the country, and a foundation on which to build a pure-play electricity champion positioned squarely in the path of the energy transition. There is genuine merit in that argument. WPD was not a fixer-upper; it was the trophy.

But price is what you pay, and the independent verdict has to weigh the timing. National Grid stretched its balance sheet to the limit to fund a premium acquisition in 2021 — precisely at the trough of the interest-rate cycle, just before global rates began their sharpest surge in a generation. A utility carries a great deal of debt by design, and the value of a rate-regulated business is acutely sensitive to the cost of that debt. By paying top dollar for WPD and financing it heavily, National Grid loaded up on leverage right before leverage got dramatically more expensive. Whether WPD was a masterstroke or an overpay depends heavily on how the next decade of returns and interest rates plays out — but the balance-sheet strain it created was not hypothetical. Within three years, it would help force the largest cash call the UK market had seen in fifteen years. That is the reckoning we turn to now.

V. The Capex Crunch & The May 2024 Capitulation

To grasp what happened in May 2024, you first have to grasp the physical problem National Grid had signed up to solve — because the money crunch was downstream of an engineering crunch.

The Great Grid Upgrade

Britain's plan to decarbonise electricity has a geography problem. The wind blows hardest, and the offshore wind farms are biggest, off the coasts of Scotland and in the North Sea — far from where the electricity is actually consumed, in the dense population centres of England. The grid Britain inherited was built for a 20th-century world where power stations sat near cities and coalfields. It was never designed to haul gigawatts of Scottish and North Sea wind power hundreds of miles south. Connecting the new green generation to demand therefore requires not a tune-up but a re-architecting of the network — the largest overhaul of Britain's grid since it was built.8

National Grid branded this effort the Great Grid Upgrade, and its centrepieces are engineering megaprojects of a scale the company has rarely attempted. Several are high-voltage direct current (HVDC) subsea "superhighways" — think of them as express electricity motorways laid along the seabed, able to move vast quantities of power efficiently over long distances with far lower losses than conventional lines. The Eastern Green Link projects (EGL1 and EGL2) are subsea cables running down the east coast to carry Scottish renewable power into England; Sea Link connects East Anglia and Kent; and the Norwich to Tilbury project reinforces the network across the east of England to absorb the coming wave of offshore wind.8 These are multi-billion-pound, multi-year builds involving specialised cable-laying vessels, high-voltage converter stations, and planning consents that can take years to secure.

The funding wall

To deliver this, National Grid unveiled a capital plan of around £60 billion over five years (FY2025–FY2029), close to double its previous five-year investment pace.2 For a regulated utility, spending is growth — but only if you can fund it without wrecking your credit rating. And here is the mechanical trap that sprung in 2024.

Rating agencies grade utilities partly on gearing — the ratio of debt to the value of the business — and on cash-flow-to-debt coverage. Investment-grade credit ratings are not a vanity metric for a company like this; they are the difference between borrowing cheaply and borrowing expensively across tens of billions of pounds of debt. A utility that leans too hard on new borrowing to fund its capex risks a downgrade, which raises its cost of debt, which erodes the very returns the capex was meant to generate. National Grid, already carrying the leverage from the WPD purchase, simply could not fund a £60 billion program on debt alone and keep its credit metrics intact. The equation didn't close. The missing piece had to come from equity.

The capitulation

On May 23, 2024, National Grid announced the fix. It launched a fully underwritten £7 billion rights issue, offering shareholders 7 new shares for every 24 they held, at 645 pence each — a 34.7% discount to the theoretical ex-rights price, engineered to be steep enough to be near-certain of full take-up.12 The raise was expected to net about £6.8 billion after roughly £165 million of costs, and management earmarked the proceeds explicitly to fund the higher-growth £60 billion investment phase.2 Alongside the raise, the company rebased its dividend, resetting the payout to reflect the enlarged share count rather than continuing to grow it off the old base.3 In practical terms, the total dividend was reset roughly 20% lower — and a multi-decade record of progressive dividend growth, the single feature that had defined National Grid as an income stock, was broken.

The market's reaction was not gentle. The shares dropped around 10% on the announcement, and income-focused investors — many of whom owned the stock precisely for its unbroken dividend history — felt blindsided.[^4] The rights issue was later confirmed to have been almost fully taken up, as the deep discount had all but guaranteed.9

The credibility question

This is where a neutral platform has to depart from the company's own framing. The strategic case for the raise is defensible: if the £60 billion program genuinely earns regulated returns on a compounding asset base, funding it with equity today can create value tomorrow, and a stretched balance sheet is a worse place to build from than a repaired one. On the substance, reasonable investors can support the decision.

On the process, management's credibility took a real hit. In the run-up to May 2024, guidance had leaned reassuring, and the scale and imminence of a dilutive equity raise were not telegraphed — investors were, in effect, presented with a fait accompli. For a management team that had built its reputation on predictability, springing the largest UK cash call since the financial crisis as a surprise was a self-inflicted wound to trust. The lesson for anyone underwriting this stock going forward is that the "steady, predictable" reputation and the actual behaviour of the management team diverged at the single most important capital-allocation moment of the decade. That divergence is a data point, and it should be weighed when management next says "trust us."

Cleaning up the org chart

One more move rounded out this period of restructuring. National Grid had long operated Britain's Electricity System Operator (ESO) — the control-room function that balances supply and demand across the grid in real time. Owning both the wires and the system operator created an inherent conflict of interest: the body deciding which projects the grid needs was owned by the company that profits from building them. To resolve this, the government agreed a £630 million deal to bring the ESO into public ownership, and in October 2024 it was relaunched as the independent, publicly owned National Energy System Operator (NESO).[^13] National Grid shed a business but also shed a conflict — and, not incidentally, received cash at a moment when cash was precious.

With the balance sheet recapitalised and the portfolio simplified, the natural question becomes: where does National Grid actually make its money now? To evaluate the £60 billion bet, you have to see the engine underneath it.

VI. Core Business Segment Breakdown & Profit Pools

Strip away the narrative and National Grid is, at heart, five distinct profit pools bolted onto one balance sheet. Understanding where the money comes from — and, just as importantly, where the asset value sits — is the difference between grasping the investment case and merely reciting the headlines. The figures that follow are drawn from the FY2025 (year ended 31 March 2025) reporting.[^14]

UK Electricity Transmission is the historic heart of the company — the high-voltage supergrid across England and Wales. In FY2025 it generated roughly £1,428 million of underlying operating profit on a regulated asset base of about £20,570 million, the single largest asset base in the group.[^14] Its economics are governed by Ofgem's RIIO transmission frameworks, and its earnings are driven above all by how much capital it can prudently deploy and how efficiently it executes — underlying transmission profit rose about 9% in the year, helped by higher totex allowances including "fast money" on accelerated strategic investment.[^14] Its notional peers are the Scottish transmission owners, SSE plc and Iberdrola's ScottishPower. This is the division most levered to the Great Grid Upgrade; it is where the £60 billion story lives or dies.

UK Electricity Distribution — the former WPD, now National Grid Electricity Distribution — contributed roughly £1,203 million of underlying operating profit on a regulated asset base near £12,235 million.[^14] Distribution is the lower-voltage network that actually reaches homes and businesses, and it runs under Ofgem's RIIO-ED2 framework. Its drivers are the volume of new connections (heat pumps, EV chargers, and housing all plug in here) and reliability incentives. Its peers are the other UK distribution network operators: UK Power Networks (owned by an ENGIE-led consortium), SSEN Distribution, SP Energy Networks, and Berkshire Hathaway's Northern Powergrid.

New York Regulated was, strikingly, the highest-earning division in FY2025, contributing around £1,450 million of underlying operating profit on an asset base of roughly £17,923 million.[^14] This is the sprawling gas and electric distribution empire assembled through Niagara Mohawk and KeySpan, governed by the New York Public Service Commission through multi-year rate filings. Its closest US peers are Consolidated Edison and Iberdrola's Avangrid.

New England Regulated added about £924 million of underlying operating profit on an asset base near £9,422 million, spanning gas and electric distribution and FERC-regulated transmission across Massachusetts and neighbouring states, overseen by the Massachusetts Department of Public Utilities.[^14] Eversource Energy and Unitil are the comparable regional players.

The single most important structural fact in that list is the balance. The core regulated utility profit splits almost exactly down the middle: roughly £2,631 million from the UK and £2,374 million from the US.[^14] National Grid is not a British utility with an American appendage, nor the reverse. It is a genuinely transatlantic business, and that dollar-sterling balance is both a diversification benefit and a source of currency translation noise in the reported numbers.

The hidden option: National Grid Ventures

The fifth pool is different in kind. National Grid Ventures (NGV) is the company's non-regulated, merchant arm, and it contributed around £380 million of operating profit in FY2025 — under 8% of the total, which is exactly the right way to size it.[^14] NGV owns the subsea interconnectors — cables like Viking Link (to Denmark), Nemo Link (to Belgium), and BritNed (to the Netherlands) — that physically wire Britain to continental Europe. The economics are cleverly counter-cyclical: when European power is cheaper than British power, the cables import it; when Britain is cheaper, they export. NGV effectively arbitrages the price gap between markets, which is why it is described as "merchant" rather than regulated — its returns rise and fall with volatility rather than a fixed formula. Regulatory caps limit the upside, and in FY2025 outperformance above the cap meant NGV returned around £89 million to UK consumers rather than keeping it.[^14] It is a small but genuinely differentiated asset — the one piece of the portfolio whose returns aren't set by a rate case.

So what does this segmentation tell an investor? Three things. First, the growth narrative is overwhelmingly a UK transmission story — that is where the incremental capital and asset-base growth is concentrated. Second, the current earnings ballast is remarkably balanced across the Atlantic, which cushions any single regulator's decision. Third, the "exciting" merchant business is deliberately tiny; anyone buying National Grid for interconnector optionality is buying an 8% tail on a 92% regulated body. The company is, and will remain, a regulated-returns machine — which makes the people negotiating with the regulators, and the regulators themselves, the decisive variables. To them we now turn.

VII. Current Management & Governance Stress Test

Every regulated utility is, in the end, a bet on two things: the quality of its operators and the disposition of its regulators. National Grid's operators have a strong hand; its recent conduct at the negotiating table with investors is where the scrutiny belongs.

The men in charge

John Pettigrew has run National Grid since 2016, and he is a lifer in the most literal sense — an engineer who came up through the networks and knows the physical grid intimately. That operational depth is his genuine strength; under his leadership, the UK grid has remained among the most reliable in the world, and US rate cases have been settled with a steadiness that eludes some American peers. His weakness, in the eyes of the market, is capital allocation — specifically the WPD premium and the surprise 2024 raise, both of which invited the charge that a brilliant operator was a less sure-footed dealmaker.

Andy Agg, chief financial officer since 2019, is the former group financial controller who has been the architect of the financial plumbing behind the pivot — the 2021 M&A sequence and the 2024 recapitalisation both bear his fingerprints. Together, Pettigrew and Agg represent institutional continuity: neither is an outsider brought in to shake the place up, which cuts both ways. Continuity means deep knowledge and no learning curve; it also means the same team that stretched the balance sheet is the team asking investors to trust the repair.

Skin in the game

On alignment, the numbers are genuinely strong and worth stating plainly. National Grid requires its CEO to hold shares worth 500% of base salary; Pettigrew's holding has run well above that threshold, reported in the region of 1,616% of salary — an enormous personal stake in the share price.10 Agg, required to hold 400% of salary, has held roughly 978%.10 In 2025, the company raised the maximum opportunity under its Long-Term Performance Plan (to 400% of salary for the CEO and 350% for the CFO), explicitly tying larger potential payouts to successful delivery of the multi-year capital program.10 The optimistic reading is that management's wealth is now bound tightly to executing the £60 billion plan well. The skeptical reading — the one an activist would press — is that raising incentive ceilings in the same window that management is asking shareholders to backstop a dilutive raise is exactly the kind of thing that deserves a hard look at the AGM.

The RIIO-T3 poker game — resolved

The single most consequential regulatory event of this cycle was the RIIO-T3 price control, which sets the rules for UK electricity transmission from April 2026 to March 2031 — the very framework governing the returns on the Great Grid Upgrade.

The process unfolded over 2025. On 1 July 2025, Ofgem published its Draft Determinations, proposing a baseline real (CPIH-linked) cost of equity in the region of 5.6%–5.7% — a figure the network companies immediately protested as too low to attract the capital the transition demands, against their own calls for something closer to 6.3%.[^16] National Grid spent the second half of 2025 arguing, publicly and in submissions, that the framework had to be both "investable and workable."

The Final Determination landed on 4 December 2025. Ofgem set a baseline real allowed cost of equity of about 5.70%, and — for National Grid Electricity Transmission specifically — a real allowed return on equity of 6.12% at 60% gearing, higher than the draft but still below the ~6.3% the company had sought.1112 Critically, National Grid accepted the determination rather than contesting it further, and used the moment to upgrade its plans: it now targets an overall return on equity above 9% across the T3 period (the gap above the ~6% baseline earned through totex efficiencies and output incentives), guides to at least £70 billion of group capital investment over five years, and expects group assets to swell to roughly £115 billion by FY2031.1213

That resolution matters for the story in two ways. First, it removed the single largest overhang — investors now know the regulatory rules of the game for the flagship division through 2031. Second, it validated, at least directionally, the logic of the 2024 raise: Ofgem confirmed a large, fundable investment pipeline, which is exactly what the equity was raised to build. But note the honest asymmetry: the 9%-plus return is a target, contingent on the company actually delivering the efficiencies and hitting the incentives, while the ~6% baseline is what the regulator guarantees. The difference between those two numbers is the entire equity case — and it must be earned, year after year, not assumed.

On the whole, then: operationally credible, financially bruised, regulatorily de-risked but not de-risked to zero. The management question going forward is narrow and answerable — will the next five years of delivery be as steady as the operating history or as jarring as the May 2024 surprise? To judge that, it helps to see who National Grid is racing against.

VIII. Industry Landscape & Competitor Benchmarking

Utility "competition" is a strange beast. National Grid does not compete for customers in the way a retailer or a bank does — no household in the West Midlands can choose a rival to WPD's wires. The competition is instead for capital, for regulatory goodwill, and for the operational reputation that earns you the benefit of the doubt in a rate case. Seen through that lens, the landscape sorts into clear camps.

The UK map

In transmission, Britain is carved into three fiefs. National Grid owns England and Wales — the largest and most valuable slice. The two Scottish transmission networks belong to SSE plc (through SSEN Transmission) and Iberdrola (through ScottishPower). All three operate under the same Ofgem RIIO framework, which makes them less rivals than comparators: Ofgem explicitly benchmarks them against one another, so a peer's efficiency becomes the yardstick against which your own allowances are set. Being the biggest and most scrutinised has a double edge — scale and visibility, but also nowhere to hide.

In distribution, National Grid Electricity Distribution is the largest UK network operator by customer numbers, serving on the order of eight million connections across the Midlands, South West, and Wales. Its peers each own a regional monopoly: UK Power Networks (ENGIE-led ownership) holds the dense, valuable London and South East territory; Northern Powergrid (Berkshire Hathaway) covers the North East and Yorkshire; SP Energy Networks (Iberdrola) and SSEN Distribution hold others. Density matters here — a network packed with customers per mile of wire, like UKPN's London footprint, is structurally more efficient than a rural one.

The US benchmark

In America, National Grid's regulated businesses are measured against high-quality Northeast peers. Consolidated Edison — the pure-play New York operator — tends to trade at a premium valuation precisely because of its clean, single-jurisdiction exposure; investors pay up for regulatory simplicity. Eversource Energy, National Grid's New England neighbour, offers a cautionary comparison: a well-regarded rate-base operator that nonetheless bruised itself badly on offshore-wind investments, a reminder that even sober utilities can stumble when they wander into merchant or development risk. The read-across for National Grid is pointed — its own value depends on staying disciplined and regulated, not on chasing developer-style returns.

7 Powers: where the moat actually is

Applying Hamilton Helmer's 7 Powers framework clarifies what is durable here and what is merely large.

The dominant power is Cornered Resource. National Grid's rights-of-way, easements, and the installed high-voltage lines themselves are effectively impossible to replicate. You cannot get planning consent to build a second national transmission grid alongside the first; the land, the permits, and the physics all forbid it. This is the deepest, most defensible moat a company can have — a legally and physically protected monopoly over an essential asset. It is why the business is safe. It is not, however, why the business grows; a moat protects returns, it doesn't generate them.

The secondary power is Scale Economies, but of an unusual sort. Deploying north of £10 billion a year in capital requires balance-sheet heft, deep capital-markets access, and institutional relationships that a smaller operator cannot match. Scale here is less about unit cost and more about the sheer capacity to absorb capital — an advantage that compounds precisely because the investment task is so enormous.

What National Grid conspicuously lacks are the demand-side powers — no network effects that grow with users, no brand pricing power, no switching costs in the consumer sense, because the customer has no choice to begin with. Its moat is supply-side and legal, not competitive. That distinction is the whole personality of the stock: enormously protected, structurally low-risk on the downside, but with an upside capped by a regulator rather than unlocked by a flywheel.

Porter's Five Forces: the regulator is everything

Porter's framework produces an almost comically lopsided picture. Rivalry is near zero by design — monopoly territories don't compete. Threat of new entrants is negligible for the same reason no one builds a parallel grid. Buyer power is diffuse — millions of captive households have no individual leverage.

The two forces that matter both point at the same place. Supplier power is extraordinary — but the "supplier" is the regulator. Ofgem and the US state commissions set the price, the allowed return, and the recoverable costs. National Grid's entire economic model is, in essence, the management of that single relationship. And the threat of substitutes is low-to-medium and long-dated: decentralised rooftop solar, home batteries, and local microgrids could, over decades, nibble at grid dependence — but ironically, connecting all that distributed generation back into a balanced system still runs through National Grid's backbone. The transition that threatens the edges of the grid deepens dependence on its core.

The strategic conclusion is unavoidable: for National Grid, the competitor that matters is not SSE or ConEd. It is the regulator across the table — which is why the RIIO-T3 outcome mattered more than any rival's move, and why the investment case ultimately rests on regulatory returns rather than market share. That case deserves to be stated explicitly, and stress-tested.

IX. Investment-Story Spine & Bull vs. Bear Case

Every long-term thesis on this stock reduces to a single wager: that National Grid can pour £70-billion-plus into the ground over five years, earn its regulated return plus a margin of outperformance on that growing base, and do it without a supply-chain blowup, a regulatory clawback, or a financing shock eating the returns. Here is the honest case on both sides.

The bull case — why it wins from here

One: the essential picks-and-shovels of net zero. Whatever wins the generation race — offshore wind, solar, new nuclear, or some mix — every electron must travel through National Grid's wires to reach demand. The company sells the one input the entire transition cannot route around. This is a genuine structural tailwind, not a marketing slogan: electrification of heat and transport plus renewable build-out both require more grid, and National Grid owns the grid.

Two: a repaired, de-risked balance sheet. The pain of the May 2024 raise bought something real. With roughly £6.8 billion of fresh equity absorbed, the balance sheet is materially stronger, and management has framed the £70 billion program as fundable through 2031 without a repeat cash call.212 If that holds, the worst of the dilution is behind, not ahead.

Three: compounding asset-base growth. This is the mathematical core. With group assets guided toward roughly £115 billion by FY2031, and regulated earnings calculated as a return on that base, the asset base itself becomes a compounding machine.12 A high-single-digit annual growth rate in the regulated asset base, earning a mid-single-digit-plus real return, mechanically produces years of earnings growth — the closest thing a utility offers to a predictable compounder.

The bear case — what could break it

One: capex execution and supply-chain risk. This is the most serious threat, and it is not theoretical. Building HVDC subsea cables and thousands of new pylons depends on globally scarce inputs — high-voltage transformers, converter stations, specialised cable-laying vessels — for which National Grid competes against every other grid operator on earth simultaneously trying to decarbonise. Planning consents can drag for years. And critically, regulators do not fully underwrite cost overruns; blow the budget on Eastern Green Link and shareholders, not consumers, may eat part of the difference. A £70 billion program executed 15% over budget is a very different investment than one delivered on plan.

Two: regulatory tightening. The RIIO-T3 Final Determination gave National Grid a workable framework, but the allowed cost of equity still came in below what the company sought, and the outperformance portion of returns — the gap between the ~6% baseline and the 9%-plus target — must be earned, not banked.1112 If Ofgem's incentive targets prove harder to beat than assumed, or if US state commissions squeeze allowed returns to keep consumer bills down in a cost-of-living-sensitive political climate, the realised return on £70 billion could disappoint even if the capital is deployed flawlessly.

Three: inflation and the cost of capital. A utility is a leveraged spread business — it earns a regulated return and funds itself with debt, and it profits on the gap. Regulated revenues are inflation-linked, which helps, but if interest rates stay higher for longer, the cost of servicing and refinancing an ever-larger debt stack can compress the equity return. The very rate environment that made the WPD deal look expensive is the same one that determines whether the £70 billion program clears its cost of capital.

The three KPIs that actually matter

An investor cannot track everything, so track these three:

First, Regulated Asset Base (RAB/RAV) growth. This is the engine. Watch whether the asset base is compounding toward the roughly £115 billion FY2031 guidance. If it grows on plan, earnings growth largely takes care of itself; if it stalls, the whole thesis stalls.

Second, Return on Regulatory Equity (RoRE) outperformance. This is the margin the company earns above the regulator's baseline through totex savings and output incentives — the difference between the ~6% allowed return and the 9%-plus target. It is the single best gauge of whether National Grid is a merely adequate operator or an outperforming one. Watch the gap, and watch whether it's widening or eroding.

Third, capital delivery. Track the percentage of planned annual capex actually deployed on time and on budget, especially on the flagship megaprojects. Delivery is the story now; a company that can't spend its plan efficiently cannot grow its asset base, and a company that overspends destroys the returns on what it builds.

The neutral verdict is that the bull and bear cases are not equally weighted across time. The structural demand for grid is about as certain as anything in investing. The uncertainty is entirely on execution and returns — can this specific management team deploy this specific mountain of capital at the assumed efficiency and cost? The moat guarantees the business survives. It guarantees nothing about the rate of return. That is the honest shape of the wager.

X. Epilogue & Episode Wrap-up

Step back from the detail and National Grid's last decade tells a story that generalises far beyond one British utility. It is the story of what happens when a mature, cash-returning "operating expense" business is forced by external change to become a "capital expenditure" business — when a company built to run assets efficiently must suddenly build assets at unprecedented scale. The two identities are almost opposites. One prizes cost discipline and steady payouts; the other demands enormous investment, balance-sheet risk, and deferred reward. National Grid tried to be both at once, and in May 2024 the contradiction snapped: the dividend record broke, the shares fell, and the market was reminded that even the safest monopoly must pay a price if it stretches too far, too fast, to buy the future.

The other lesson is about the seductive tidiness of strategic narratives. On paper, the 2021 pivot — sell gas, buy WPD, go pure-play electricity, ride the transition — was elegant. In practice, it was executed at a premium price and financed at the worst possible moment in the rate cycle, and the tidy story required an untidy £7 billion rescue to hold together. Strategy and timing are different disciplines, and National Grid was better at the first than the second.

So the closing question is the one we opened with. Is National Grid a defensive bond proxy — a dependable income stock for the cautious — or has it genuinely transformed into a structural green-growth compounder? The honest answer, as of mid-2026, is that it is trying to be the second while still being priced and owned partly as the first, and the reconciliation of those two identities will play out over the RIIO-T3 period through 2031. The regulatory rules are now set. The £70-billion-plus plan is defined. The balance sheet is repaired. What remains is delivery — the least glamorous and most decisive variable of all. For the long-term investor, the wires are the moat, but the execution is the return, and only one of those is guaranteed.

The source links below contain the deep-dive raw data behind this story.

References

-

7 for 24 fully underwritten £7bn Rights Issue — National Grid plc / Investegate, 2024-05-23 ↩↩

-

National Grid Full Financial Framework & Capital Plan Announcement — National Grid, 2024-05-23 ↩↩↩↩↩↩

-

National Grid launches £7 billion rights issue to fund green grid — Reuters, 2024-05-23 ↩↩

-

The British are Coming: UK's National Grid to Acquire KeySpan — Natural Gas Intelligence, 2006 ↩↩

-

National Grid's £7.8 Billion Acquisition of Western Power Distribution and $3.8 Billion Sale of The Narragansett Electric Company — Cravath, Swaine & Moore LLP, 2021 ↩↩↩

-

National Grid plc Form 6-K: WPD acquisition announcement — U.S. SEC / National Grid, 2021-03-18 ↩↩↩

-

Results of Rights Issue — National Grid plc / London Stock Exchange, 2024-06 ↩

-

National Grid Annual Report and Accounts 2024/25 — Directors' Remuneration Report — National Grid, 2025 ↩↩↩

-

RIIO-3 Final Determinations for the Electricity Transmission, Gas Distribution and Gas Transmission sectors — Ofgem, 2025-12-04 ↩↩

-

National Grid details Ofgem RIIO-T3 decision and 6.12% equity return — National Grid Form 6-K / StockTitan, 2025-12-04 ↩↩↩↩↩

-

Upgraded 5-year framework and RIIO-T3 acceptance — National Grid plc / Investegate, 2025-12-04 ↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube