Nagarro: Engineering the Fluidic Enterprise

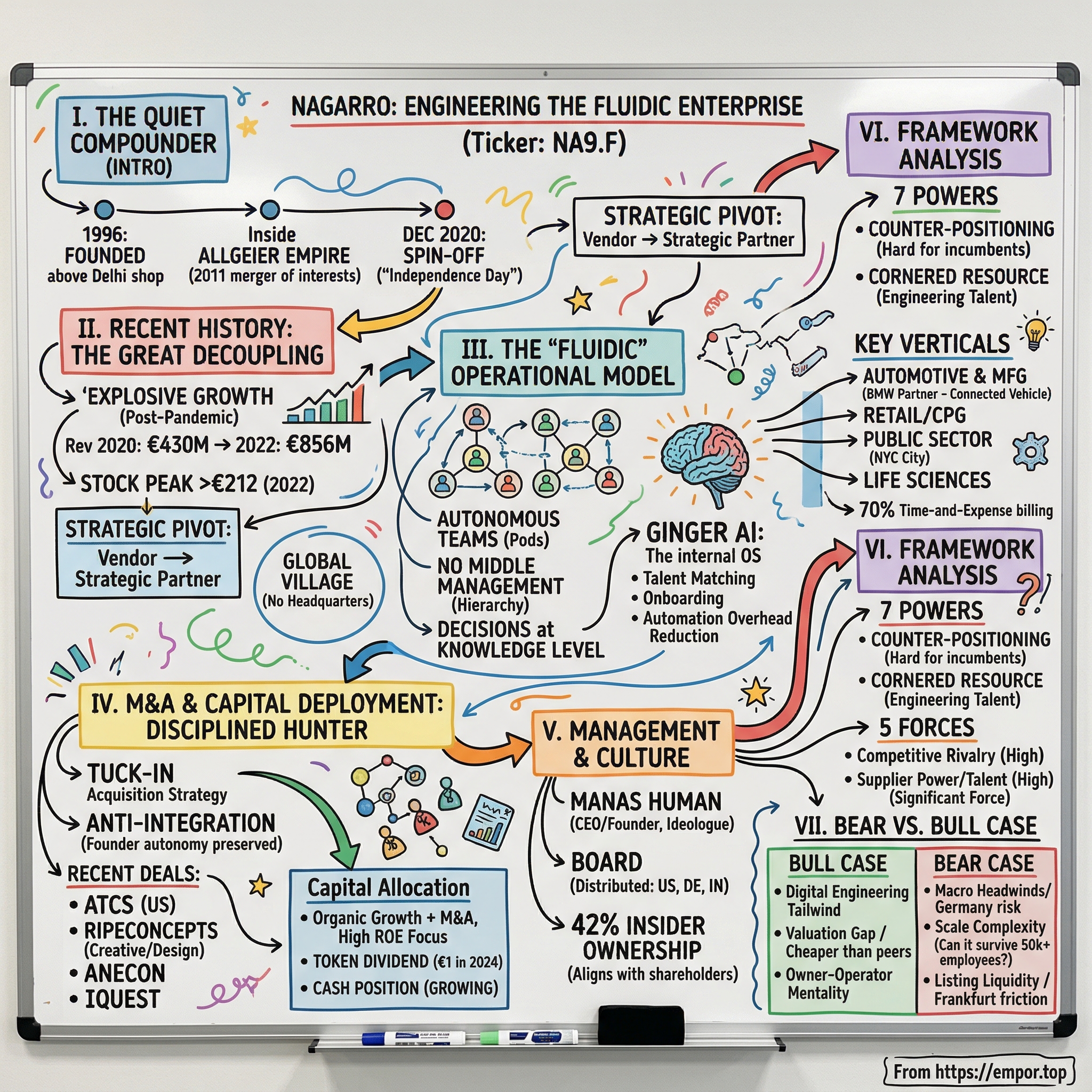

I. Introduction: The "Quiet" Compounder

In an era when every tech company races to slap "AI" onto its investor deck, there exists a category of business that rarely makes the front page of TechCrunch but quietly powers the digital transformation of the world's largest enterprises. These are the companies that build the plumbing — the integration layers, the real-time data pipelines, the custom software that makes a BMW reward you for driving electric, or that calculates optimal flight paths for over thirty thousand flights every single day. The companies that turn a CEO's PowerPoint vision into production-grade code.

Nagarro SE is one of those companies. And yet, to dismiss it as "just another IT services firm" would be like calling LVMH "just another handbag maker." There is something architecturally different about Nagarro — something that goes beyond what it sells and into how it is built.

Here are the numbers that set the stage: nearly eighteen thousand employees, spread across thirty-nine countries, serving clients like BMW, Lufthansa, Siemens, GE, and the City of New York. Revenue approaching one billion euros. A listing on the Frankfurt Stock Exchange under the ticker NA9.F that did not arrive through a traditional IPO roadshow, but through a surgical spin-off from its former parent, Allgeier SE, in December 2020. And a management team that collectively owns roughly forty-two percent of the company — the kind of skin-in-the-game ratio that would make a private equity partner nod approvingly.

But the real thesis here is not about revenue or headcount. It is about organizational design as competitive advantage. Nagarro has built something it calls the "Fluidic Enterprise" — a management philosophy that systematically eliminates the hierarchy, the headquarters mentality, and the bureaucratic drag that slows down the Accentures and TCSes of the world. Whether this model can scale from eighteen thousand people to fifty thousand — and whether it represents a durable structural advantage or a fragile experiment — is the central question of this story.

The arc runs from a 1996 founding above a shop in Delhi, through a decade inside the Allgeier empire, to a post-spin-off independence that unleashed a period of explosive growth, and now into a moment of maturation where the company must prove its model works not just in boom times but in the grinding macro environment of 2025 and 2026. Along the way, there are acquisitions made at bargain-basement multiples, an AI platform called Ginger that functions as the company's hidden operating system, a CEO who legally changed his last name to "Human," and a long-term ambition to reach ten billion dollars in revenue within a decade.

This is the story of Nagarro.

II. Recent History: The Great Decoupling

To understand why Nagarro exists as a public company today, you have to go back to a deal struck in the summer of 2011. Allgeier Holding AG, a mid-sized German IT conglomerate based in Munich, signed an agreement to acquire all shares in Nagarro Inc. But this was not a typical acquisition where the buyer writes a check and the founders cash out. In a twist that revealed something about the entrepreneurial DNA of the Nagarro team, the major Nagarro shareholders simultaneously acquired a stake in Allgeier itself. It was less a sale and more a merger of interests — Allgeier got access to over a thousand highly qualified engineers in India to address the chronic IT talent shortage in German-speaking markets, and Nagarro got a European distribution channel and balance sheet backing for international expansion.

For nearly a decade, the arrangement worked. Nagarro grew rapidly inside Allgeier, expanding from roughly eight hundred and forty employees and twenty-two million dollars in revenue in 2010 to over eight thousand employees and four hundred million euros in revenue by 2019. But as Nagarro grew, an increasingly obvious tension emerged. Allgeier was a portfolio of German-focused IT businesses — staffing, consulting, SAP services. Nagarro was a global digital engineering company competing against the likes of EPAM and Globant. The two businesses had different growth profiles, different investor bases, and increasingly different strategic needs. Nagarro was pulling away from the pack, and its valuation was being suppressed by the conglomerate structure.

The solution was a spin-off, executed on December 16, 2020. The mechanics were clean: every Allgeier shareholder received one Nagarro share for every one Allgeier share they held. Allgeier retained zero ownership in Nagarro post-separation — a full one hundred percent transfer. The operating businesses of Nagarro, along with iQuest (a Romanian software development firm) and Objectiva (a US and China operation), were bundled under a new holding company, Nagarro SE, incorporated as a European company based in Munich. A bank consortium committed a two hundred million euro credit facility to ensure the newly independent entity had financial firepower from day one.

Inside Nagarro, they called it "Independence Day." And the timing could not have been more consequential.

The spin-off landed in the middle of the post-pandemic digital acceleration — that extraordinary period from late 2020 through 2022 when every enterprise on the planet suddenly needed to digitize everything, yesterday. Companies that had been slowly modernizing their tech stacks hit the panic button. Cloud migrations that had been planned for 2025 got pulled forward to 2021. Digital customer experience projects jumped from "nice to have" to "existential." For companies like Nagarro, this was the equivalent of being a general contractor in a housing boom.

The numbers tell the story. Revenue went from four hundred and thirty million euros in 2020 to five hundred and forty-six million in 2021, then leapt to eight hundred and fifty-six million in 2022 — a fifty-seven percent year-over-year surge that is almost unheard of for a company of that size in professional services. The stock followed: from roughly sixty-nine euros at the time of listing to a peak above two hundred and twelve euros by early 2022, tripling in barely a year.

But the acceleration was not just about riding a macro wave. Nagarro used the moment to execute a strategic pivot that matters more than any single quarterly result. Before the spin-off, many clients viewed Nagarro as a "vendor" — a firm you called when you needed extra engineering hands on a project. After independence, with its own stock ticker, its own investor relations, and its own brand identity, Nagarro repositioned itself as a "strategic partner." The distinction is not semantic. A vendor gets a purchase order for a six-month project. A strategic partner gets a multi-year engagement to co-own a digital transformation roadmap. The average deal size grew, the client relationships deepened, and the revenue mix shifted toward longer-duration, higher-margin work.

Central to this transformation was what Nagarro calls the "Global Village" concept. Unlike the traditional IT services model where a company has a clear headquarters — Accenture in Dublin, TCS in Mumbai, Infosys in Bangalore — Nagarro deliberately avoids the headquarters trap. There is no single office where the CEO sits and all decisions flow from. The management board is distributed across the United States, Germany, and India. Global Business Units, the primary internal organizing structure, are led by people who can sit anywhere in the world, and those units are reorganized frequently to adapt to shifting market conditions. The result is an organization that can mobilize a cross-continental team for a client engagement in days rather than weeks — without routing decisions through three layers of regional management and a committee in some central headquarters.

This matters for investors because it directly affects two things that drive long-term value in professional services: talent utilization and client responsiveness. The companies that win in this industry are the ones that can get the right engineer in front of the right problem fastest, with the least organizational friction. Nagarro's global village model is engineered to do exactly that.

III. The Playbook: The "Fluidic" Organizational Model

Picture a typical large IT services company. There is a CEO at the top, then a layer of regional presidents, then country managers, then practice leads, then delivery managers, then team leads, then the actual engineers who write the code. Every decision navigates this hierarchy like a pinball bouncing through bumpers — slowly, unpredictably, losing energy at every level. When a client in Chicago needs a machine learning specialist who happens to be in Romania, the request travels up the Chicago org chart, across to the European org chart, down to the Romanian office, and back. By the time the specialist is allocated, the client's competitor has already shipped.

Nagarro looked at this and decided to throw it away.

The "Fluidic Enterprise" is not a marketing tagline — it is the core organizational operating system of the company, and arguably the single most important thing to understand about Nagarro's competitive positioning. The model is built on five principles: responsiveness, efficiency, trust, creativity, and sustainability. But the practical reality is simpler than the framework suggests. Nagarro operates as a network, not a hierarchy. Small, autonomous teams — sometimes called pods — form around client engagements and dissolve when the work is done. There is no permanent middle management layer owning a geography or a practice. Decisions are made where the knowledge is, not where the title is. An engineer in Bangalore with deep expertise in a client's tech stack has more authority over a technical decision than a vice president in Munich who has never touched the codebase.

Think of it as the difference between an army and a special forces unit. An army moves slowly because it needs chains of command to coordinate thousands of soldiers. A special forces team is small, elite, autonomous, and trusted to make decisions in the field. Nagarro is trying to build an entire organization of special forces teams — eighteen thousand people who operate with the speed and autonomy of a startup but the global reach of an enterprise.

The skeptical reader will immediately ask: how does this actually work in practice? Coordination problems do not disappear just because you declare your company "fluidic." The answer lies in a piece of technology that might be Nagarro's most underappreciated asset: an internal AI platform called Ginger.

Ginger AI is not a product that Nagarro sells to clients. It is the invisible operating system that makes the fluidic model possible. At its core, Ginger is an agentic AI system that serves as the primary interface between Nagarro's employees and the organization itself. When a project needs a specific skill set, Ginger's algorithms match available talent to the requirement, factoring in skills, availability, time zone, client history, and dozens of other variables. When a support ticket comes in, natural language processing routes it to the right department without human triage. When a new employee joins, Ginger generates a personalized onboarding flow tailored to their role, location, and the specific engagement they are joining.

To use a simple analogy: if Nagarro is a city, Ginger is the traffic management system. Without it, the "fluidic" model would devolve into chaos — eighteen thousand people running in different directions. With it, the organization self-organizes at a speed that traditional hierarchies simply cannot match. And because Ginger continuously learns from every interaction, every project allocation, every employee feedback loop, the system gets better the larger Nagarro gets. It is a rare example of an internal tool that creates genuine increasing returns to scale in a business — professional services — that is notorious for decreasing returns as companies grow.

This is separate from Genome AI, which is Nagarro's client-facing AI platform. Ginger is the inward-facing engine; Genome is the outward-facing one. The distinction matters because Ginger is not a profit center — it is a cost structure advantage. By automating the coordination overhead that typically requires hundreds of middle managers at a company of this size, Nagarro can run leaner than peers. The result is visible in the company's overhead ratios, which sit meaningfully below industry averages for firms of similar scale.

Now, let us look at where this model meets the market. Nagarro serves sixteen-plus industries, but a few verticals tell the strategic story.

In Automotive and Manufacturing, Nagarro has built one of its deepest moats. The partnership with BMW is the flagship example: Nagarro co-created the BMW Points and eDrive Zones system, which rewards customers with monetary incentives for driving in electric mode. This is not a simple app — it integrates with real-time vehicle telemetry, mobility service platforms, and accounting systems. Once Nagarro is embedded this deeply in a client's digital infrastructure, the switching costs are enormous. You do not rip out the team that built your connected vehicle platform and hand it to a competitor mid-program.

Retail and Consumer Packaged Goods represents the high-growth digital-first segment. These are companies racing to build direct-to-consumer channels, personalization engines, and supply chain visibility tools. The work tends to be greener-field and faster-moving than automotive, with shorter project cycles but higher volume.

The expanding footprint in Public Sector and Life Sciences represents Nagarro's horizontal growth strategy. The City of New York engagement is a notable proof point — government work is notoriously hard to win but extremely sticky once secured. Life sciences, with its regulatory complexity and data sensitivity, creates natural barriers to entry that favor established players with domain expertise.

In 2024, the automotive and industrial vertical remained the most dynamic growth area, while banking and financial services saw a slight decline of about one percent, and the horizontal tech vertical dipped nearly five percent. The revenue mix tells you something important: roughly seventy percent of Nagarro's work is billed on a time-and-expense basis, with thirteen percent on fixed price and sixteen percent on periodic services. This is a business that gets paid for engineering hours, which means utilization rates and billing rates are the two most important operational levers management can pull.

IV. M&A and Capital Deployment: The Disciplined Hunter

There is a species of corporate acquirer that views M&A as a transformational event — the kind of deal that gets announced with a press conference, a new logo, and a PowerPoint deck titled "Creating a Global Leader." These deals often destroy value. The integration is brutal, the cultures clash, the talent walks, and the acquiring company spends three years digesting what it bought instead of serving clients.

Nagarro does not play this game. Their M&A strategy is best described as "tuck-in" — small, targeted acquisitions that add a specific capability, a geographic foothold, or a client relationship, at a price that makes the math work even if everything goes wrong.

Consider the acquisition of ATCS in late 2021. ATCS was a US-headquartered IT solutions company with operations in India — exactly the kind of firm that plugs directly into Nagarro's delivery model. The purchase price was described as a "medium two-digit million USD" amount, plus a performance-based earn-out running through 2024. For a company generating meaningful revenue with an established US client base, that price tag — likely somewhere in the twenty to fifty million dollar range — represents roughly one to one-and-a-half times revenue. Compare that to the multiples paid in the broader IT services M&A market, where acquirers routinely pay three to five times revenue for similar assets. When EPAM or Globant buy a company, they are paying growth multiples on the assumption that they can accelerate the target's revenue. Nagarro buys at value multiples and then does the same acceleration — generating far higher returns on invested capital.

The RipeConcepts acquisition in 2022 followed a similar playbook. Based in Salt Lake City with over six hundred and fifty employees in the Philippines, RipeConcepts brought creative and design capabilities — a complement to Nagarro's engineering-heavy DNA. At roughly ten million euros in annual revenue, this was a modest deal by any measure, but it filled a strategic gap. As digital transformation matures, clients increasingly demand not just functional software but beautifully designed user experiences. RipeConcepts gave Nagarro that capability without paying a Silicon Valley premium.

The pattern repeats across the acquisition history: Anecon in Austria for test automation expertise, iQuest in Romania for Central European delivery capacity, Farabi Technology in Dubai for Middle East access, Conduct AS in Norway for Nordic consulting presence. Each deal is small enough that integration risk is minimal, targeted enough that the strategic rationale is clear, and priced cheaply enough that the return hurdle is low.

But perhaps the most distinctive element of Nagarro's M&A approach is what they do after closing. Most acquirers immediately begin "integrating" — which in practice means imposing the buyer's processes, systems, and culture on the acquired team. Nagarro takes what might be called an "anti-integration" philosophy. Acquired founders are encouraged to keep their entrepreneurial identity. Their teams are plugged into the Nagarro global sales engine and delivery network, but the day-to-day culture and operating rhythm of the acquired business is largely preserved. This matters enormously in professional services, where the primary asset walks out the door every evening. If you buy a company and immediately tell its best engineers that everything they knew about how to work is now wrong, those engineers update their LinkedIn profiles that weekend.

The capital allocation philosophy that underpins these deals reveals management's priorities. Nagarro prefers organic growth supplemented by high-return-on-equity acquisitions. There is no massive dividend program — the company proposed its first-ever dividend for fiscal year 2024 at just one euro per share, a token gesture that signals confidence without depleting the war chest. The cash position grew from one hundred and ten million euros at the end of 2023 to nearly one hundred and ninety-three million by the end of 2024, providing ample firepower for continued tuck-in deals.

The implicit message to shareholders is clear: we are going to reinvest most of our cash flow into growth, either organically or through disciplined acquisitions, because we believe the return on that reinvestment exceeds what you would earn in a dividend. In a business growing at mid-to-high single digits with adjusted EBITDA margins above fifteen percent, that logic holds — but only as long as management maintains its acquisition discipline. The moment Nagarro starts paying three-to-four times revenue for a "transformational" deal, the entire capital allocation thesis breaks.

V. Management: The Non-Founders Who Act Like Founders

In October 2022, Nagarro's CEO did something that no Fortune 500 executive has ever done. He legally changed his last name. Manas Fuloria became Manas Human — a deliberate, public act intended to, in his words, push religious and national identities into the background and embody the borderless, humanistic philosophy he had been preaching for years. Whether you find this inspiring or eccentric, it tells you something essential about the person running this company: this is not a caretaker CEO managing quarterly earnings. This is a founder-ideologue who views the organization as a manifestation of a worldview.

Manas Human was born in 1972, holds a PhD from IIT Delhi and a Master's from Stanford University in Technology and Operations Management. He co-founded Nagarro in 1996 in that modest office above a shop in Delhi, alongside Vikram Sehgal, Vikas Sehgal, Manmohan Gupta, and Priya Jadhav. From the beginning, Human was the organizational architect — the one obsessed not just with what Nagarro built for clients but with how Nagarro itself was built.

The management board today consists of three members: Manas Human as CEO with the title "Custodian of Entrepreneurship," Vikram Sehgal as co-founder and "Custodian of Operational Excellence," and Annette Mainka as "Custodian of Regulatory Compliance." The titles themselves — custodians rather than chiefs — reflect the anti-hierarchical ethos. All three were confirmed for another three-year term, and their base compensation is remarkably modest by public company CEO standards: Human earned four hundred and eighty-two thousand euros in 2024, Sehgal earned four hundred and ninety-one thousand, and Mainka earned four hundred and eighty thousand. For the CEO of a company approaching one billion euros in revenue, that base pay is a fraction of what peers at EPAM or Globant take home.

But the real compensation story is in the equity. And this is where Nagarro looks less like a German public company and more like a private equity portfolio company. Management collectively owns approximately forty-two percent of Nagarro's outstanding shares. The largest single holder is Carl Georg Durschmidt and his family at roughly twenty-one point six percent — Durschmidt was the CEO of Allgeier and retained his stake through the spin-off. Vikram Sehgal and his family hold about six point two percent through a combination of direct holdings and StarView Capital LLC. Manas Human holds approximately five point six percent directly and indirectly. Additional stakes are held by other founding-era executives.

This level of insider ownership creates an alignment between management and shareholders that is vanishingly rare in European public markets. When forty-two percent of the company is owned by the people running it, the incentives for empire building, excessive compensation, or reckless M&A are naturally constrained. Every euro of value destroyed comes directly out of management's pockets.

The Long-Term Incentive plans reinforce this culture. They are tied to EBITDA and organic growth targets that are, by management's own admission, aggressive. This is not the kind of LTI plan where executives hit their targets by showing up — the hurdles are designed to ensure that payouts only occur when the company delivers genuine outperformance. The structure mirrors what you would see at a private equity firm rather than a typical German DAX-adjacent company, and it goes a long way toward explaining why Nagarro's management behaves with an owner-operator mentality rather than a professional-manager mentality.

The geographic distribution of leadership deserves its own mention. The management board operates across the US, Germany, and India. The supervisory board, chaired by Christian Bacherl, includes members like Dr. Shalini Sarin and Jack Clemons, with proposed new additions including Martin Enderle and Hans-Paul Burkner — names that signal an intent to strengthen governance as the company matures. This distributed leadership is not just a symbolic nod to the global village concept; it is a practical necessity. When your clients, your engineers, and your growth markets span thirty-nine countries, having a leadership team clustered in a single city creates blind spots and bottlenecks.

The question investors must ask is whether this founder-led, mission-driven culture can persist as Nagarro scales. History is filled with companies that thrived under a visionary founder and then lost their edge when that founder stepped back or the organization grew past the point where personal relationships could hold it together. The fluidic model and the Ginger AI platform are, in part, Nagarro's answer to this challenge — an attempt to encode the founder's organizational vision into technology and systems that can operate independent of any single personality. Whether that encoding is complete and robust enough to survive the inevitable generational transition remains to be seen.

VI. Framework Analysis: 7 Powers and 5 Forces

To stress-test Nagarro's competitive position, it helps to apply two rigorous frameworks: Hamilton Helmer's 7 Powers, which asks where a company's durable advantages come from, and Michael Porter's 5 Forces, which maps the structural attractiveness of the industry itself.

Starting with Helmer's 7 Powers, the most compelling case for Nagarro lies in counter-positioning. The fluidic enterprise model — the flat structure, the autonomous pods, the absence of a headquarters mentality — is not something that the Big Four consulting firms or the Indian IT giants can easily replicate. Accenture, Deloitte, TCS, and Infosys are built on deeply entrenched hierarchies. Their organizational charts are their operating systems. To adopt Nagarro's model, they would need to dismantle their existing management layers, eliminate the regional fiefdoms that their senior partners have spent careers building, and fundamentally restructure how talent is allocated and decisions are made. This is not a technology gap that can be closed by buying a software tool. It is an organizational architecture gap that requires tearing down and rebuilding the house while everyone is still living in it. The incumbents know the fluidic model exists. They can study it, admire it, even reference it in their own strategy documents. But adopting it would be so painful and disruptive to their current operations that rational management teams will never attempt it. That is the definition of counter-positioning.

The second relevant power is what Helmer calls a cornered resource. In IT services, the critical resource is engineering talent — specifically, high-end engineers who can do complex digital transformation work, not commodity coders who bang out basic web forms. Nagarro has built a distinctive brand in the engineering talent market, particularly in India and Central Europe (Romania, Austria, Germany). The company's culture — the fluidic model, the distributed leadership, the emphasis on autonomy — is specifically designed to attract the kind of senior engineer who chafes under the bureaucracy of a TCS or Infosys. These engineers do not just want a paycheck; they want to work on interesting problems with autonomy and without being treated as interchangeable resources. Nagarro's ability to attract and retain this tier of talent — and to deploy it globally through the Ginger platform — is a cornered resource that competitors cannot simply buy their way into.

Switching costs represent the third power. Once Nagarro has built a client's core ERP system, connected vehicle platform, or AI engine, the client is not just buying services — they are embedded in Nagarro's engineering approach, tooling, and institutional knowledge. The BMW engagement illustrates this perfectly: Nagarro is so deeply integrated into BMW's digital vehicle ecosystem that switching providers would require not just finding replacement engineers but rebuilding years of accumulated domain knowledge and system-specific expertise. In professional services, the longer the engagement, the higher the switching costs — and Nagarro's shift from project-based "vendor" work to long-term "strategic partner" engagements is deliberately designed to maximize this dynamic.

Turning to Porter's 5 Forces, the picture reveals both structural advantages and genuine competitive pressures.

The threat of new entrants is low. Building an IT services firm with eighteen thousand high-caliber engineers across thirty-nine countries requires years of hiring, training, cultural development, and client relationship building. You cannot replicate this overnight with capital alone. The barrier is not financial — it is organizational and human. A well-funded startup could hire a hundred excellent engineers in Bangalore tomorrow, but it would take a decade to build the global delivery infrastructure, the client trust, and the institutional knowledge that Nagarro has accumulated.

Supplier power — in this case, the bargaining power of talent — is the most significant force acting on Nagarro's business. Software engineers are not commodities. The best ones are fiercely competed for, and in a market where FAANG companies, fintech unicorns, and well-funded startups all fish from the same talent pool, retention is an existential challenge. Nagarro's answer is cultural rather than purely monetary. They win the war for talent through the fluidic model's promise of autonomy, interesting work, and global exposure — not just through higher salaries, which they often cannot match against Big Tech compensation packages. The risk is that this cultural advantage erodes if the company grows too large or too bureaucratic, which is precisely why the organizational model is the single most important thing to protect.

Buyer power is moderate and increasing. Large enterprises are sophisticated purchasers of IT services and will aggressively benchmark providers against each other. The countervailing force is the switching costs discussed above — once engaged, clients tend to stay, but winning new clients requires competitive pricing and demonstrated capability.

The threat of substitutes has evolved dramatically with the rise of generative AI. Low-code platforms, AI coding assistants, and automated testing tools all have the potential to reduce the volume of human engineering hours required for certain types of work. This is a double-edged sword for Nagarro: on one hand, it threatens the time-and-expense billing model that generates seventy percent of revenue. On the other hand, it creates massive new demand for companies that can help enterprises actually implement, customize, and manage AI systems — which is exactly what Nagarro does. The net effect likely favors Nagarro in the medium term, but the business model will need to evolve from selling hours to selling outcomes as AI handles an increasing share of routine coding work.

Competitive rivalry is intense. Nagarro operates in a fragmented market with global players (Accenture, TCS, Infosys, Wipro), mid-tier peers (EPAM, Globant, Endava, Thoughtworks), and thousands of regional boutiques. Differentiation is difficult to sustain because services are inherently people-dependent and hard to patent. Nagarro's moat, such as it is, comes from the organizational model and the deep client relationships it enables — not from any proprietary technology or exclusive market position.

For investors tracking this business, the two KPIs that matter most are organic revenue growth rate in constant currency, which reveals whether Nagarro is winning in the market independent of acquisitions and currency fluctuations, and adjusted EBITDA margin, which shows whether the fluidic model's efficiency advantages are translating into actual profitability. These two numbers, taken together, tell you whether Nagarro is growing while maintaining the operational discipline that justifies its reinvestment-heavy capital allocation.

VII. The Bear vs. Bull Case

The bear case against Nagarro starts with a single word: macro. Germany's industrial core — automotive, manufacturing, chemicals — represents the beating heart of Nagarro's European business. Central Europe accounts for nearly twenty-nine percent of revenue, and much of that is tied to German enterprises. If Germany's manufacturing sector enters a prolonged downturn — and the signs in 2025 and 2026 have not been encouraging, with energy costs, EV transition pains, and Chinese competition all weighing on the Mittelstand — Nagarro will feel it. The company's 2025 guidance of one billion twenty million to one billion eighty million euros already hints at this pressure; management indicated they expect to come in near the lower end due to global macroeconomic challenges. First-half 2025 revenue grew just three point four percent year-over-year, and the adjusted EBITDA margin dipped to twelve point one percent in the second quarter, down from fourteen point five percent in the same period of 2024.

The second bear argument is what you might call the complexity tax. The fluidic model is elegant when it works, but can it survive fifty thousand employees? There is a reason most large organizations adopt hierarchy — it is a proven solution to the coordination problem at scale. As Nagarro grows, the risk is that the fluidic model becomes increasingly difficult to maintain, that informal networks of trust fray, that the Ginger AI platform hits limitations, and that the company quietly starts adding the middle management layers it has spent years avoiding. If that happens, Nagarro loses its primary differentiator and becomes just another mid-tier IT services company trading at a premium multiple.

Third, there is the liquidity and listing venue issue. Nagarro trades on the Frankfurt Stock Exchange with average daily volume of roughly fifty thousand shares and a current market capitalization of approximately five hundred and eighty-five million euros. This is tiny by institutional investor standards. Many US funds cannot own a position in a stock this small, and the Frankfurt listing means American investors face additional friction in buying shares. The result is a structurally thin shareholder base that amplifies volatility and may suppress valuation multiples relative to US-listed peers. The stock has fallen from a peak of over two hundred and twelve euros to roughly forty-five euros — a decline of nearly eighty percent that reflects not just macro headwinds but also the illiquidity discount that Frankfurt-listed mid-caps endure.

The AI substitution risk also deserves attention in the bear case. If generative AI coding tools dramatically reduce the demand for human engineering hours over the next five to seven years, Nagarro's core billing model — seventy percent time-and-expense — could face structural compression. The company would need to transition to outcome-based pricing or productize its offerings, which is a fundamentally different business model requiring different capabilities.

Now, the bull case.

The digital engineering tailwind is not a cyclical phenomenon — it is a multi-decade secular trend. Every industry on earth is in some stage of digitizing its operations, products, and customer interactions. The installed base of legacy systems that need to be modernized is enormous, and AI is accelerating the demand rather than replacing it. Companies need more engineering help to implement AI, not less. Nagarro's position as a high-end digital engineering partner — not a commodity outsourcer but a firm that can handle complex, mission-critical transformation work — puts it squarely in the path of this spending.

The valuation gap is the most obvious opportunity. Nagarro trades at roughly one times enterprise value to revenue. EPAM, which grew at a similar rate and has similar margins, trades at nearly two times. Globant sits around one point three times. Endava is at two point one times. Even accounting for the Frankfurt listing discount and the smaller market cap, Nagarro is meaningfully cheaper than its peer group on virtually every metric. On an EV/EBITDA basis, Nagarro trades at approximately nine times versus sixteen times for EPAM and eleven times for Globant. If Nagarro were listed on the NYSE or NASDAQ, with the liquidity and analyst coverage that comes with a US listing, a re-rating toward peer multiples would represent fifty to one hundred percent upside without any improvement in underlying business performance. There has been no indication that management is considering a US listing, but the optionality exists.

The ownership structure is itself a bull case. Forty-two percent insider ownership means management is eating its own cooking. The modest base salaries, the aggressive LTI hurdles, and the founder-led culture all suggest a management team that is optimizing for long-term value creation rather than short-term optics. CEO Manas Human has publicly stated an ambition to reach ten billion dollars in revenue within ten years — by roughly 2033. That is a tenfold increase from current levels, which is wildly ambitious. But even achieving a fraction of that growth, compounded with the current valuation discount, creates a compelling return profile.

The tuck-in M&A strategy provides a margin of safety on the capital allocation front. When you buy at one to one-and-a-half times revenue while peers pay three to five times, your hurdle rate for creating value is dramatically lower. Even if some acquisitions underperform, the blended return on invested capital remains attractive because the entry prices are so modest.

Finally, Nagarro's cash generation trajectory strengthens the setup. The cash position nearly doubled from one hundred and ten million euros to one hundred and ninety-three million euros in a single year. As the company crosses one billion euros in revenue and maintains margins in the fourteen-to-fifteen percent range, free cash flow generation should accelerate, providing both a cushion against macro headwinds and dry powder for opportunistic acquisitions.

The tension between the bear and bull cases ultimately comes down to a single bet: can the fluidic model scale? If it can — if Nagarro can grow to thirty thousand, then fifty thousand employees while maintaining its organizational agility, talent density, and client intimacy — then the current valuation is a gift. If the model buckles under its own weight, or if macro headwinds in Germany and the broader European economy persist, then the stock may remain in purgatory for longer than investors expect.

VIII. Conclusion and Playbook Lessons

The Nagarro story offers a lesson that extends well beyond IT services. The most durable competitive advantages often come not from what a company sells, but from how it is organized to sell it. Products can be copied. Technology can be replicated. But organizational architecture — the deep, structural way a company makes decisions, allocates talent, and coordinates across geographies — is extraordinarily difficult to imitate, precisely because it requires an incumbent to destroy what already works before building something new.

Nagarro's fluidic enterprise model is a bet that decentralization, trust, and AI-enabled coordination can outperform the traditional hierarchy at scale. It is a bet that the best engineers in the world want to work in a system that treats them as autonomous professionals rather than billable resources. And it is a bet that clients will increasingly value speed, agility, and depth of expertise over the brand reassurance that comes from hiring Accenture or Deloitte.

Whether Nagarro becomes the "LVMH of Engineering Services" — a platform that curates excellence across dozens of specialized practices — or whether it remains a well-run mid-tier player in a brutally competitive industry depends on the answers to questions that have not yet been resolved. Can the model survive the transition from founder-led to institution-led? Can it navigate the AI-driven transformation of its own industry? Can it close the valuation gap with US-listed peers, or will the Frankfurt listing remain a structural handicap?

What is clear is that Nagarro has built something genuinely different. In an industry defined by sameness — where one IT services firm's pitch deck is often indistinguishable from the next — the fluidic model stands out as a real architectural innovation. The financial results since the 2020 spin-off have been strong, the ownership structure aligns management with shareholders, and the acquisition discipline has been exemplary. The company approaches one billion euros in revenue with a clear strategic identity and a management team that thinks in decades, not quarters.

The final playbook lesson is perhaps the simplest: the best businesses are not just selling a product or a service. They are selling a new way of working. And when that new way of working is embedded so deeply in the organization's DNA that competitors cannot copy it without first destroying themselves, you have something that might just be a power.

IX. Top 10 Reference Links for Further Research

- Nagarro's "Fluidic Enterprise" framework — The foundational document explaining the organizational model, available on Nagarro's corporate website.

- 2020 Spin-off documentation — The original prospectus and Allgeier AGM materials from December 2020, detailing the mechanics of separation.

- Manas Human's keynote addresses — Public talks and interviews where the CEO articulates the philosophy behind fluidic organization and borderless talent deployment.

- Annual Report 2024 — The most recent full-year filing with segment-level revenue breakdowns, geographic data, and management commentary on strategic direction.

- Peer valuation comparison: Nagarro vs. EPAM vs. Globant vs. Endava — Financial data platforms tracking enterprise value multiples, margin profiles, and growth rates across the digital engineering peer group.

- Ginger AI platform announcements — Press releases and product documentation describing the internal AI system that powers talent allocation and organizational coordination.

- Global delivery model and hiring strategy — Investor presentation materials detailing the thirty-nine-country footprint and how engineering talent is sourced, developed, and deployed.

- Frankfurt Stock Exchange data (NA9.F) — Historical price data, trading volume, and ownership disclosures filed with the exchange.

- BMW digital transformation partnership — Published case studies covering the BMW Points, eDrive Zones, and connected vehicle platform work.

- M&A transaction history — A ledger of all acquisitions since the 2011 Allgeier combination, including ATCS, iQuest, Objectiva, RipeConcepts, Anecon, and recent tuck-ins, with available pricing and strategic rationale.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube