Marks and Spencer Group plc: The Ultimate Retailing Turnaround

I. Introduction & Episode Roadmap

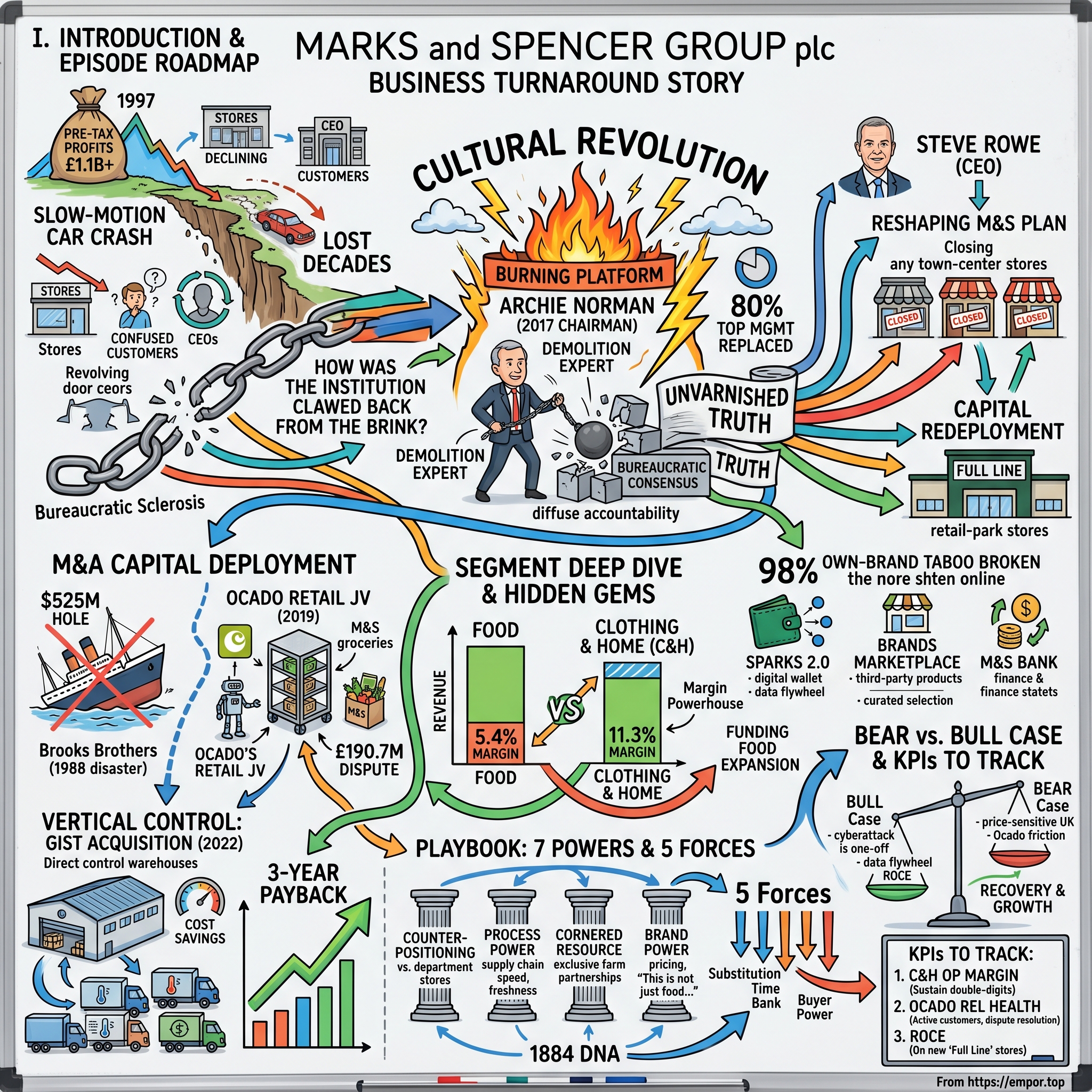

Picture the British high street in the spring of 1997. The Spice Girls are at number one, Tony Blair is about to sweep into Downing Street, and on Baker Street in London sits the corporate headquarters of the most admired retailer in the country. That year, Marks & Spencer did something no British retailer had ever done before: it posted pre-tax profits north of £1.1 billion.1 To put that in perspective, roughly one in three pieces of clothing sold in the United Kingdom carried the M&S label, and the company's underwear business alone clothed the nation so thoroughly that the cliché went, "everyone in Britain is wearing M&S knickers, whether they admit it or not." The stock was a blue-chip cornerstone of every pension fund. M&S wasn't just a retailer; it was a national institution, somewhere between a utility and a member of the royal family.

And then, almost immediately, it began to die.

What followed was one of the most painful, drawn-out corporate declines in modern business history — a slow-motion car crash spanning the better part of two decades. The food was still good. The underwear still sold. But the magic leaked away. The fashion turned frumpy. The stores grew drafty and tired. A parade of chief executives and would-be saviors cycled through the revolving doors of Baker Street, each promising a renaissance, each tinkering at the edges, each ultimately defeated by the same enemy: not a competitor, but the company's own culture. M&S had become a bureaucratic cathedral, an organization so convinced of its own genius that it had stopped listening to anyone — its customers least of all.

This is the story of how that institution clawed its way back from the brink. Because today, in 2026, Marks & Spencer is something almost nobody would have predicted a decade ago: one of the great turnaround stories in global retail. The company has reclaimed its place in the FTSE 100. Its food halls are arguably the best in Britain. Its clothing is, improbably, fashionable again. And it has reinvented itself from a creaky high-street department store into a digitally-led, vertically integrated premium grocer fused with a style-led fashion business.

How does that happen? How does a 140-year-old retailer — the very archetype of the dinosaur that disruption is supposed to kill — reinvent its entire operating model while keeping its soul intact?

That's the question we're chasing in this episode. And the answer, it turns out, has a handful of recurring threads. There's the brutal, almost surgical capital allocation of the current management team, set against a history of jaw-dropping value destruction. There's the "burning platform" — a deliberate act of cultural arson lit by a chairman who'd seen this movie before. There's the strange split-personality of the business model, where a quiet, ferociously profitable clothing arm secretly funds the expansion of a lower-margin, fast-growing food empire. And there's the ultimate stress test: a catastrophic cyberattack in 2025 that froze the company's digital nervous system for weeks, and the phoenix-like recovery that followed in 2026.

There's a useful way to frame what makes this story unusual. Most celebrated turnarounds in business history fall into one of two buckets. Either a company invents something genuinely new and rides it back to relevance — think of a tech firm catching a platform shift — or a financial engineer arrives, strips out costs, loads on debt, and squeezes out a return before moving on. M&S did neither. It didn't invent a new product category, and it wasn't financially engineered by a private-equity raider. What it did was rarer and, frankly, harder: it took a 140-year-old operating model that had rotted from the inside and rebuilt it organ by organ — culture, capital allocation, supply chain, real estate, technology — while the patient was awake and still serving customers. That's open-heart surgery without anesthetic, and it's why the case is so instructive.

We'll walk through all of it — the market-stall origins, the lost decades, the cultural revolution, the M&A masterclass (and the historical disasters that preceded it), the vertical integration chess moves, and the financial architecture that holds it all together. Let's start where every great institution starts: with a refugee and a penny.

II. Succession, Trust, & The Own-Brand DNA

In 1884, a young man named Michael Marks stepped off a boat and into the grey industrial sprawl of northern England. He was a Polish-Jewish refugee from the town of Słonim, in what was then the Russian Empire, fleeing the pogroms that were tearing through Eastern Europe. He spoke almost no English. He had no capital to speak of, no connections, and no obvious path forward. What he had was a pack of haberdashery goods and a willingness to walk.

He ended up in Leeds, working as a traveling peddler, then took a fixed pitch at the open-air Kirkgate Market.2 And here Marks made the decision that would, in a very real sense, still be shaping the company 140 years later. The problem he faced was simple but profound: with limited English, haggling over prices with customers was a nightmare. So he didn't. He took all the goods that cost a single penny, threw them together on one section of his stall, and hung up a sign that became retail legend: "Don't ask the price, it's a penny."

It's worth pausing on the genius hidden inside that bit of necessity. Marks had stumbled onto something that modern retailers spend fortunes trying to engineer: radical price transparency and trust. There was no negotiation, no anxiety, no sense that the clever customer got a better deal than the timid one. Everyone paid a penny. Everyone was treated the same. The "Penny Bazaar" was a hit, and as Marks expanded across the north of England, he needed a partner to handle the back-office side of a growing business. In 1894 he found one: Thomas Spencer, a cashier at the wholesale company that supplied him. Spencer put in £300 for a half share, and Marks & Spencer was born.2

Now, the early history matters less for its dates than for the DNA it encoded — two pillars that, remarkably, still hold up the entire edifice today.

The first pillar is own-brand execution. As the business grew through the early twentieth century, M&S made a radical bet: it would not be a middleman selling other people's products. It would design and specify its own goods, made to its own exacting standards by manufacturers who worked exclusively to its brief. In 1928, this philosophy got a name — St Michael, a brand under which virtually everything M&S sold would be marketed for the next seventy years.2 The St Michael label was a promise: if it carried that name, M&S stood behind it completely, because M&S had effectively made it. This was the opposite of the department-store model, where the retailer is essentially a landlord renting floor space to brands. M&S owned the whole chain of trust from factory to fitting room.

The second pillar was trust, expressed through two relationships the company treated as sacred. With customers, M&S pioneered a no-questions-asked refund policy at a time when "buyer beware" was the norm — you could bring something back, and they'd take it back, full stop. With suppliers, M&S did something even more unusual: it treated its manufacturers and its British farming families not as transactional vendors to be squeezed on every order, but as long-term partners. The company would work hand-in-glove with a textile mill or a vegetable grower for generations, sharing standards, sharing know-how, and — crucially — sharing the upside of getting it right.

There's one more piece of early DNA worth flagging, because it explains a strain of the company's character that runs straight through to the present. M&S was, from early on, paternalistic — toward its staff as much as its customers. Long before "stakeholder capitalism" became a conference buzzword, M&S was building staff canteens, providing pensions and welfare schemes, and treating its workforce as part of an extended family. Some of this was enlightened self-interest and some of it was genuine conviction, but the effect was the same: M&S accumulated a vast reservoir of institutional loyalty and public goodwill. That reservoir is a double-edged thing. It's the reason the British public roots for M&S the way it roots for few other companies — there is real affection there, the kind you can't buy with advertising. But it's also the reason the company found it so agonizing, decades later, to close stores and fire managers; the very loyalty that was an asset in good times became an anchor when hard choices arrived. Hold that tension in mind, because it explains why the cultural surgery of the 2010s had to be so deliberately brutal.

Why does any of this matter to an investor looking at the company in 2026? Because here's the thing that's easy to miss about the modern turnaround: the current management team did not invent a new M&S. They went back and excavated the original one. Every strategic pillar you'll hear about in this episode — the obsessive focus on own-brand quality, the language of "trusted value," the deep supplier partnerships that let the company offer premium products at non-premium prices, the mission to win back the mythical "Mrs M&S" who drifted away during the lost decades — all of it is a modernization of Michael Marks's 1884 playbook. The genius of the recovery wasn't reinvention. It was remembering.

But before the remembering came the forgetting. And to understand just how far M&S fell, we have to go back to that billion-pound peak — and watch it curdle.

III. The Bureaucratic Sclerosis & The Lost Decades

Success, it turns out, is a far more dangerous teacher than failure. Failure forces you to ask questions. Success convinces you that you already have all the answers.

By 1997, M&S had every answer. The company had been compounding goodwill for a century, and it had developed a corporate culture to match its station — confident, deliberate, inward-looking, and utterly convinced that the M&S way was simply the correct way. There's a famous detail from this era that captures it perfectly: for a long stretch, M&S didn't accept any credit cards except its own store card, on the theory that customers should adapt to M&S rather than the other way around. The company had become, in effect, a high-street utility. People shopped there the way they paid their water bill — out of habit, because that's just what one did.

The trouble with running a business like a utility is that utilities don't have to fight for customers. And right at the moment M&S was busy admiring its billion-pound trophy, the people who were about to take those customers were sharpening their knives.

On the fashion side, the threat came in the form of a revolution in how clothes get from a designer's sketch to a shopper's bag. A Spanish company called Inditex — the parent of Zara — had pioneered "fast fashion," a model built on a supply chain so responsive it could spot a trend on a Milan runway and have a version of it hanging in stores within weeks. From Japan came 株式会社ファーストリテイリング Fast Retailing Co., Ltd., the owner of ユニクロ Uniqlo, which attacked from a different angle — tech-driven basics, relentless on quality and price, a kind of "LifeWear" engineered in fabric labs. These competitors treated the supply chain as a weapon. M&S treated it as a committee process. While Zara turned its range over in a fortnight, M&S's lumbering buying cycle meant decisions made many months in advance — and by the time the clothes hit the shelves, they often looked exactly as dated as a year-old prediction tends to look. The word that attached itself to M&S clothing in this period was lethal: frumpy. Once you become the brand your customer's mother shops at, you have a very long way back.

On the food side, M&S found itself caught in a vise. It had pioneered premium ready meals and high-quality convenience food — genuinely innovative stuff. But it was neither the cheapest nor, increasingly, the most aspirational. Above it sat Waitrose, hoovering up the affluent middle-class grocery shopper with a full-range supermarket experience. Below and around it sat the "Big Four" — Tesco, Sainsbury's, Asda, and Morrisons — with the scale, the parking, the petrol stations, and the loyalty schemes to do the family's entire weekly shop. M&S Food, by contrast, was largely stuck in small high-street stores where you might grab a sandwich and a treat but could never do a proper trolley-load. It was a treat business in a world that was consolidating around convenience and scale.

It's worth understanding why the bureaucracy itself was so deadly, because "bad culture" is the kind of phrase that sounds like a soft excuse for hard failures. In M&S's case the culture was the hard failure. Consider how a clothing range actually got made. A buyer would have an idea; that idea would pass through layers of committee review, technical sign-off, merchandising negotiation, and senior approval — each layer adding caution, smoothing edges, and adding months. By the time a garment cleared the gauntlet and reached a store, the fashion moment that inspired it had often passed, and the design had been compromised by so many hands that it pleased no one in particular and everyone in general. This is the mechanism by which "frumpy" gets manufactured. It isn't that M&S employed bad designers; it's that the system was engineered to strip the conviction out of every decision. Compare that to Zara, whose entire organizational design existed to compress the distance between an idea and a shelf. M&S was, structurally, the slowest animal in a race that had just gotten much faster.

The same disease infected the company's relationship with reality. Because accountability was diffuse and bad news traveled slowly, senior leadership could persist in comfortable narratives long after the numbers stopped supporting them. Like-for-like sales — the crucial measure of whether existing stores are selling more or less than the year before — would soften, and the organization would reach for explanations: the weather, the economy, a tough comparison with last year. Anything but the product. A culture that cannot say "our clothes are not good enough" out loud cannot fix its clothes. That inability to speak plainly is precisely what the next chairman would identify as the thing he had to destroy first.

And underneath all of this sat the real, structural problem — the one that the parade of failed turnarounds never managed to fix. M&S's store estate was a relic. The company owned and leased an enormous portfolio of giant, multi-floor properties anchored in the dead center of Britain's town centers — buildings that had been prime real estate in 1955 and were drafty, expensive, hard-to-navigate liabilities by 2005. They had no parking. They sat in town centers that were themselves hollowing out as shoppers migrated to out-of-town retail parks and, increasingly, to their laptops. And M&S's online operation, when it finally built one, ran as a completely separate world, bolted on rather than woven in.

So why did turnaround after turnaround fail? Because each new leadership team treated the symptoms — a fashion refresh here, a marketing campaign there, a new logo, a celebrity model — while leaving the underlying disease untouched. Nobody wanted to grasp the genuinely painful nettles: shutting down the beloved-but-obsolete town-center cathedrals, demolishing the bureaucracy that produced the frumpy clothes in the first place, and rewiring the entire company around a digital-first future. Those moves required not a strategist but a demolition expert. In 2017, M&S finally hired one.

IV. The "Burning Platform" & Cultural Revolution

Archie Norman did not need the money, and he did not need the headache. By the time he agreed to become chairman of Marks & Spencer in 2017, he was already a living legend in British retail — the man who had walked into a near-bankrupt Asda in 1991 and walked out, eight years later, having transformed it into a powerhouse that he then sold to Walmart for £6.7 billion. He'd been a Member of Parliament. He'd chaired ITV. He had nothing left to prove. What he had, instead, was a particular and rare skill set: Norman was perhaps the only person alive who genuinely understood how to fix a sick retailer from the inside, and what he saw at M&S frightened him.3

His diagnosis became the defining metaphor of the entire turnaround. M&S, he declared, was a business standing on a "burning platform." The image is borrowed from the world of offshore oil rigs — the idea that a worker on a flaming platform faces a stark, terrifying choice: leap into the freezing, dangerous sea, or stay and burn. Doing nothing is not survival; doing nothing is death. Norman's point was brutal and deliberate. M&S did not have the luxury of incremental change, of another gentle fashion refresh. It was, he argued, a company that could quite plausibly cease to exist — and the only thing more dangerous than the fire was the comfortable belief that there wasn't one.

This is the part of the story that separates Norman from his predecessors, and it's worth dwelling on because it's the actual mechanism of the turnaround. The previous saviors had tried to fix M&S's products. Norman went after M&S's culture — specifically, the paralyzing bureaucracy that had calcified over decades of success. In his telling, M&S had become an organization that ran on "bureaucratic consensus": decisions were made by committee, accountability was diffuse, and the highest virtue was getting along rather than getting it right. Bad news traveled slowly, if at all, because no individual owned the outcome. Everyone could point at the process.

So Norman set out to, in his own phrase, "fracture the culture." He demanded what he called the "unvarnished truth" — an end to the polished presentations and managed messaging that had kept Baker Street comfortable while the business decayed. And he backed it up with a level of personnel change that was genuinely shocking for an institution as tradition-bound as M&S: over his early years, he and his CEO replaced something like 80% of the top management team. The message was unmistakable. The old guard, however loyal, however steeped in M&S lore, was part of the problem. The culture of consensus had to give way to a culture of individual accountability — where a named human being owned each decision and lived with the result.

Norman couldn't do this alone, and he didn't try. His partner in the early years was Steve Rowe, the chief executive — and Rowe's biography is its own kind of M&S poetry. Rowe was an M&S lifer in the most literal sense: his father had been a senior executive at the company, and Steve himself had started on the shop floor as a Saturday boy, working his way up through nearly every part of the business over more than three decades. If Norman was the outsider with the blowtorch, Rowe was the insider who knew exactly which walls were load-bearing. Together they launched the "Reshaping M&S" plan, and its centerpiece was the most painful decision the company had avoided for twenty years: closing the stores.

This was emotional surgery. Many of the town-center stores slated for closure had been community fixtures for generations — places where local people had bought their first work suit, their wedding outfit, their children's school uniforms. Shutting them down meant accepting that an entire chapter of M&S's identity was over. The plan ultimately targeted the closure of more than 100 of these legacy locations, a managed retreat from the dying high street designed to free up capital and energy for the future: bigger, better-located "Full Line" stores with parking, and a digital ecosystem that would finally be woven into the core of the business rather than bolted onto the side.

There's a subtlety here that investors should appreciate, because it's where Norman's experience really showed. Closing stores is not, by itself, a strategy — plenty of dying retailers close stores on the way to the grave, shrinking toward zero. The difference between a managed retreat and a death spiral is what you do with the capital and attention you free up. Norman and Rowe framed the closures not as cost-cutting but as redeployment: every drafty town-center cathedral that came down was meant to fund a better-located store, a sharper supply chain, or a digital capability. The discipline was in refusing to let the savings simply leak away into propping up a declining status quo. A retreat that funds an advance is strategy; a retreat that funds nothing is just slow liquidation. M&S, for the first time in a long time, was retreating with a purpose.

It also required an unusual tolerance for short-term pain, and this is a recurring feature of the whole turnaround worth naming early. Closing stores, writing down property, and severing legacy arrangements all hit the reported profit line in the year you do them, often hard. A management team focused on the next quarterly headline would flinch. Norman's entire philosophy was that you take the pain in concentrated doses, tell shareholders the unvarnished truth about why, and trust that a cleaner, more focused business compounds faster afterward. It's a deceptively simple idea that an astonishing number of companies cannot execute, because it requires leaders willing to look worse in the short run to be better in the long run.

It was the right surgery. But surgery alone doesn't make a patient thrive — and the bolder question hanging over Norman and Rowe was what M&S should buy, build, and bet on to actually grow again. That question would produce both the best and, in M&S's history, the very worst deals the company ever made.

V. M&A Capital Deployment: Masterclass vs. Historical Disasters

To appreciate just how disciplined M&S's modern dealmaking has become, you first have to understand how spectacularly bad the company used to be at it. And there's no better cautionary tale than the time M&S decided it wanted to be American.

In 1988, flush with confidence and cash, M&S looked across the Atlantic and bought Brooks Brothers — the venerable American clothier, outfitter of presidents, the very definition of East Coast preppy establishment — for roughly $750 million.4 On paper, the logic had a certain appeal: a premium, heritage clothing brand, a natural fit for a company that prided itself on quality and tradition. In practice, it was a disaster from almost the first day. M&S never figured out how to integrate the brand or grow it. The cultural distance between a British own-brand mass retailer and an American luxury tailoring house turned out to be a chasm. The numbers stagnated. And in 2001, after thirteen years of frustration, M&S threw in the towel and sold Brooks Brothers to Retail Brand Alliance for about $225 million.4

Do the arithmetic and it stings: a loss of roughly $525 million in nominal terms, before you even account for thirteen years of management attention squandered and capital tied up going nowhere. The Brooks Brothers episode became the textbook M&S example of value destruction through unfocused international expansion — buying a brand it didn't understand, in a market it couldn't crack, for a price it could never justify. Keep that $525 million hole in mind, because it's the benchmark against which the modern team's discipline should be measured.

Now fast-forward to 2019, and watch the same company make a very different kind of bet. M&S's food business had a glaring strategic gap: in a world rushing online, M&S had no scalable way to deliver groceries to people's homes. Building a national e-commerce grocery operation from scratch is one of the most capital-intensive, logistically brutal challenges in all of retail — it had taken others decades and billions. So instead of building, M&S bought its way in. In February 2019, it announced it would acquire a 50% stake in Ocado Retail, forming a joint venture with Ocado Group.5

The structure is worth understanding because it became the source of a long-running fight. M&S agreed to pay up to £750 million for its half of the business: an initial £562.5 million in cash up front, plus a deferred payment of £190.7 million that was contingent on Ocado Retail hitting certain performance targets down the road.5 In exchange, M&S replaced Waitrose — Ocado's previous grocery partner — as the source of the food flowing through Ocado's slick, automated warehouses and out to British doorsteps. Ocado, for its part, got a committed long-term partner and a guaranteed supply of premium products; M&S got an instant, world-class online grocery channel it could never have built natively, plus the chance to put its own-brand food in front of a young, affluent, digital-first customer base.

So — did M&S overpay? At the time, plenty of critics thought so. Paying a rich multiple for half of an online grocery business that was still burning cash struck many observers as an act of desperation, the move of a company so terrified of being left behind in e-commerce that it overpaid for a seat at the table. And then the timing got complicated in a way nobody anticipated. The COVID-19 pandemic sent online grocery demand through the roof in 2020 and 2021, briefly making the deal look like a stroke of genius — before the inevitable post-COVID hangover arrived, demand normalized, e-commerce valuations cratered across the board, and the picture muddied again.

That hangover lit the fuse on a genuinely bitter dispute, one that remains live as of 2026. When the time came to settle up on that £190.7 million deferred payment, M&S refused to pay it in full, arguing that Ocado Retail had simply missed the performance targets the payment was tied to.[^6] Ocado Group fired back that the targets should have been adjusted to account for the wild distortions of the pandemic — that it wasn't fair to hold the business to pre-COVID benchmarks after COVID had scrambled everything. The two partners — supposedly aligned in a 50/50 joint venture — found themselves locked in a financial and legal standoff over a nine-figure sum, a reminder that even the smartest deal structures can curdle when reality refuses to cooperate with the spreadsheet.[^6]

It's worth sitting with the deeper logic of why the Ocado structure was so much smarter than the Brooks Brothers approach, because the contrast is the whole lesson. With Brooks Brothers, M&S bought 100% of a business in a market it didn't understand and then had to operate it — taking on all the risk, all the capital, and all the management burden, while possessing none of the local knowledge required to succeed. With Ocado, M&S bought 50% of a business in a market it understood intimately — British groceries — and paired with a partner who supplied the one thing M&S genuinely lacked: world-class warehouse automation and last-mile delivery technology. The joint-venture structure split the risk and married complementary strengths. M&S brought the product, the brand, and the customer trust; Ocado brought the robots and the logistics software. Neither could have done it alone as well as they could together. That's the difference between a deal designed to acquire and a deal designed to combine — and it's why one ended in a fire sale and the other, for all its courtroom drama, created enormous strategic value.

There's also a quieter benefit that doesn't show up in the headline economics: optionality and learning. By sitting inside a pure-play online grocer, M&S got a front-row education in how digital food retail actually works — basket composition, delivery economics, customer-acquisition costs, the brutal mathematics of the last mile. That knowledge bleeds back into the rest of the business, informing everything from how M&S thinks about its own store-based online fulfillment to how it prices and ranges its products. You cannot buy that kind of operating insight on a consultant's slide; you can only get it by being in the room while the business runs.

But here's the strategic reality that the corporate friction obscures, and it's the part that matters most for the long-term investor: the joint venture itself is a structural masterpiece, friction and all. Ocado Retail's sales have been growing at strong double-digit rates — on the order of 13% to 17% year-over-year — giving M&S Food a scalable, high-growth online channel bolted onto its premium brand without M&S having to sink billions into building warehouses and robots itself. The lawyers can fight over £190.7 million for years. The strategic value of owning half of Britain's leading pure-play online grocer, stocked with your own products, dwarfs the dispute. M&S learned the Brooks Brothers lesson: this time, it bought capability it could actually use, in a market it actually understood.

And if Ocado gave M&S a digital front end for its food, the company's next deal would go after the other end of the chain entirely — the cold, unglamorous, mission-critical world of logistics.

VI. Vertical Control: The Gist Logistics Acquisition

Some of the most consequential decisions in retail happen in places no customer ever sees: refrigerated warehouses on the edge of motorways, fleets of temperature-controlled lorries running through the night, the invisible plumbing that gets a punnet of strawberries from a field to a shelf before it wilts. For decades, M&S had outsourced this plumbing for its food business to a specialist logistics company called Gist. And for decades, that arrangement quietly leaked money and control.

The problem with renting your most critical infrastructure is that you're forever at the mercy of the landlord's contract. M&S's legacy logistics arrangements had become expensive and, worse, structurally misaligned — M&S was paying premium rates on long-standing contracts while having limited ability to redesign the supply chain for the digital, convenience-led future it was racing toward. The cold chain is the beating heart of a premium fresh-food business; you cannot promise "fresh" while outsourcing the very thing that keeps food fresh. So in 2022, M&S did the logical thing: it stopped renting and bought the whole operation.6

In September 2022, M&S completed the acquisition of Gist for an initial £145 million in cash, with the total deal structure worth up to £255 million depending on future property-related proceeds.6 On its face, £145 million for a logistics company is the kind of transaction that barely makes the business pages. But dig into the multiple, and this deal becomes a small masterclass in disciplined capital allocation — arguably the purest expression of how the modern M&S thinks about money.

Here's the math, translated out of finance-speak. When you buy a business, one common way to gauge whether you paid a fair price is to compare the purchase price to the business's annual earnings, measured as EBITDA — essentially, the cash profit the operation throws off before accounting for interest, taxes, and the wear-and-tear of its assets. Gist was generating around £55 million in proforma EBITDA. So at an initial £145 million, M&S paid somewhere in the range of just 2.6 to 4.6 times EBITDA, depending on exactly how you account for the deal's moving parts.6

Why is that remarkable? Because logistics businesses simply don't sell that cheaply. The going rate for acquiring a logistics operation typically runs somewhere between 6 and 10 times EBITDA. M&S, in other words, acquired a critical, high-utility asset for roughly half — or less — of what the market would normally charge. How did it pull that off? Because M&S was Gist's anchor customer. The business was, in large part, already built around serving M&S; there was no bidding war for a logistics company whose biggest client could simply walk away. M&S held all the negotiating leverage, and it used it ruthlessly.

The payoff was equally striking. By bringing the operation in-house, M&S could rip up those legacy high-cost contracts and run the cold chain at its own true cost. The acquisition was projected to pay for itself in just three years — a three-year payback against the company's standard internal hurdle of five years for capital projects.6 In plain terms, M&S demanded that any big investment earn its money back within five years, and this one did it in three. That gap between the hurdle and the result is the whole philosophy in miniature: buy essential capability, buy it cheap because you have the leverage, and make sure it pays you back fast.

There's a second-order benefit to owning the logistics that's easy to overlook from the outside: data and control over the whole flow of goods. When you outsource your supply chain, you also outsource visibility into it — you see what your logistics provider chooses to show you. When you own it, you can see everything, in real time, and you can redesign the network around the way your business is actually changing. As M&S pivots toward more convenience formats, more online fulfillment, and more retail-park stores, owning Gist means it can re-route, re-time, and re-engineer the cold chain to match — rather than negotiating every change through a third party whose incentives don't align with yours. In a business where freshness is the product, controlling the pipes is controlling the product.

Set the two deals side by side and you can see the modern M&S mind at work. Ocado was about owning the digital front door to the customer. Gist was about owning the physical pipes behind the wall. Both were about converting things M&S used to rent — capability and control — into things M&S owns. And both were executed by a management team whose defining trait is an almost allergic reaction to overpaying. To understand where that discipline comes from, we need to meet the man now running the company.

VII. Current Management & The Ultimate Cybersecurity Test

Stuart Machin has a phrase he repeats so often that it has become something of a corporate mantra at M&S: he describes himself as "positively dissatisfied." It's a deliberately uncomfortable formulation. The "positive" half acknowledges that things are going well — that the turnaround is working, the profits are up, the strategy is landing. The "dissatisfied" half insists that none of that is good enough, that there is always slack to cut, a process to sharpen, a customer to win back. It is, in essence, the operational opposite of the complacency that nearly killed M&S in the first place. And it's the personality trait that, more than any other, defines the man who became sole chief executive in 2022.

Machin is a retailer's retailer. Before he ran all of M&S, he ran its food business as Managing Director, and before M&S he'd cut his teeth in the relentlessly competitive worlds of Australian and British grocery and discount retail. He is not a strategy consultant who learned retail from a deck; he is an operator who learned it from the shop floor and the supply chain. When he talks about being positively dissatisfied during record profit years, it isn't false modesty — it's the genuine instinct of someone who has watched too many retailers die of self-satisfaction.

What makes the current management team credible to investors, though, isn't just temperament — it's how their incentives are wired. And M&S's remuneration structure is worth understanding in detail, because it reveals what the board actually wants the executives to optimize for. Machin's base salary was set at £865,700 for the 2025/26 year, rising to £909,000 for 2026/27.7 But base salary is the least interesting part of the package. The real money sits in the Performance Share Plan, which can pay out up to 250% of salary — and crucially, it only pays out if the executives deliver on a specific trio of metrics: return on capital employed, adjusted earnings per share, and relative total shareholder return.7

Decode those three, because together they form a kind of anti-empire-building tripwire. Return on capital employed measures whether the money the company invests actually earns a good return — it's the metric that would have screamed "stop!" during the Brooks Brothers years. Adjusted earnings per share keeps the focus on real, growing profit per share rather than empty revenue growth. And relative total shareholder return measures M&S's stock performance against its peers, so management only wins big if shareholders beat the alternatives. Tie a CEO's pay to those three things and you get a CEO who allocates capital like Gist and Ocado — cheaply, with discipline, and with a horror of overpaying.

The alignment goes one level deeper still. M&S requires its CEO to personally hold shares worth 300% of base salary — three times his annual pay locked up in the company's stock, so that his own wealth rises and falls with shareholders'.7 Machin's personal stake runs to roughly 0.11% of the company, worth on the order of £11 million.7 That's real skin in the game: when M&S stumbles, Machin doesn't just earn a smaller bonus — he watches a meaningful chunk of his net worth evaporate alongside every other shareholder. Which brings us to the moment that tested whether all this fine talk about accountability and alignment was real, or just the kind of thing companies write in their annual reports.

Over the Easter weekend of 2025, M&S was hit by a cyberattack.

The attackers were associated with a notorious cybercrime collective known as Scattered Spider — a loose, sophisticated group known for socially engineering its way past corporate defenses and then detonating ransomware inside the victim's systems. They crippled M&S's digital nervous system. The consequences were immediate and severe: online fashion sales were frozen entirely for roughly seven weeks, and the click-and-collect service — the increasingly central feature that lets customers order online and pick up in store — was suspended for around four weeks.8 For a company that had spent the better part of a decade painstakingly weaving digital into the core of its business, watching that nervous system go dark was a nightmare scenario made real.

The financial damage was staggering. M&S faced a direct recovery and remediation bill of £131.3 million — the raw cost of rebuilding and securing its systems.[^10] On top of that sat an estimated £300 million in lost sales, the revenue that simply never happened while the website sat dark and the click-and-collect counters stood idle.[^10] All told, the attack drove a roughly 24% drop in adjusted pre-tax profit for the financial year, pulling it down to £671.4 million.[^10] After years of climbing the mountain, M&S had been knocked back down a quarter of the way in a matter of weeks by a group of anonymous criminals.

And here is where the culture Archie Norman set out to build in 2017 either meant something or it didn't. Faced with a profit collapse caused by an external attack — something no reasonable person would blame on the executives' day-to-day performance — Machin and his leadership team made a choice that tells you everything about how the modern M&S thinks about accountability. They voluntarily scrapped their own annual bonus schemes for the 2025/26 financial year.[^10] They didn't have to. The cyberattack wasn't their fault in any conventional sense. But the principle of "unvarnished truth" and alignment with shareholders meant that if the owners of the business were absorbing a brutal hit, the stewards of the business would absorb it too. It was a costly, unforced gesture — and exactly the kind of gesture that the M&S of 1997 would never, in a thousand years, have made.

It's worth being precise about what kind of test this really was, because it cuts to something fundamental about modern retail. M&S had spent a decade transforming itself from a chain of physical stores into a digitally-led ecosystem — an ecosystem in which the website, the app, the loyalty program, and click-and-collect were not add-ons but load-bearing walls. The cyberattack was, in a grim sense, the bill for that transformation. The more digital a business becomes, the more catastrophic a digital outage is. A purely physical retailer with no e-commerce would have shrugged off a hack of its website; M&S, having staked its future on integration, found that integration weaponized against it. This is the uncomfortable paradox sitting underneath every digital-first strategy in modern commerce: the same connectivity that creates efficiency and customer intimacy also creates a single, enormous attack surface. M&S's recovery is reassuring, but the episode is a permanent reminder that cyber risk is now a first-order operational risk for any company that has digitized its core — not an IT footnote, but a board-level concern on par with supply-chain disruption or a demand shock.

The response also revealed something about how M&S now communicates with its owners. Rather than minimize the breach or bury it in vague language, the company quantified the damage in detail — the recovery bill, the lost sales, the profit impact — and put numbers on the table that no PR department enjoys publishing. That willingness to disclose precisely how bad it was is itself a product of the "unvarnished truth" culture; an M&S of an earlier era would have been tempted to fog the whole thing. For investors, a management team that tells you the bad news in specifics is worth more than one that tells you good news in generalities, because it means the numbers you do get can be trusted.

The board, meanwhile, made its own move to steady the ship. Recognizing that ripping out a steadying hand in the middle of a crisis would be reckless, it extended Archie Norman's tenure as chairman for an additional three years — from September 2026 through 2029 — deliberately stretching past the standard corporate-governance guidelines on how long a chairman should serve, and securing full shareholder backing to do it.[^11] In an era when governance codes are treated as gospel, M&S essentially argued that stability during a genuine crisis mattered more than ticking the box on tenure limits — and persuaded its owners to agree. The platform had caught fire again, in a way nobody predicted. The difference was that this time, the people standing on it knew exactly what to do.

VIII. Segment Deep Dive & "Hidden" Gems

Strip away the drama — the cyberattack, the cultural revolution, the courtroom skirmishes — and a question remains that any serious investor has to answer: where does the money actually come from? And the answer reveals a business with a fascinating, almost paradoxical split personality, where the part that gets the headlines is not the part that makes the margins.

Start with the half everyone talks about: M&S Food. In the 2024/25 financial year, Food generated revenue of £9.03 billion, with an adjusted operating profit of £484.1 million — a margin of around 5.4%.9 Nine billion pounds is an enormous, high-volume, fast-growing engine. This is the business that fills the stores, drives the footfall, and powers all those "This is not just food" cravings. But look at that 5.4% margin. Grocery is a brutal, thin-margin grind — you move mountains of product to earn a modest slice on each item. Food is the scale engine, the volume machine, the reason millions of people walk through M&S doors every week. What it is not is the company's profit center.

Now look at the half that gets less attention: Clothing & Home. In that same 2024/25 year, C&H generated revenue of £4.20 billion — less than half of Food's top line. But it threw off £475.3 million in adjusted operating profit, almost exactly as much as the far larger Food business, at a margin of 11.3%.9 Read those two numbers together and the picture snaps into focus. Clothing & Home earns more than double the margin of Food on less than half the revenue. It is, in the truest sense, a quiet cash cow — a high-margin, own-brand fashion business whose profits quietly fund the expansion, the store rotations, and the supply-chain investments of the lower-margin Food empire.

This is the structural secret of M&S, and it's the opposite of how most people perceive the company. The popular image is of M&S as primarily a food business that also, somewhat embarrassingly, sells slightly dull clothing. The financial reality is that the "dull" clothing business is a margin powerhouse subsidizing the glamorous food expansion. Understanding that inversion is the single most important thing an investor can grasp about how M&S really works — and it's why sustaining that double-digit clothing margin matters so much to the whole machine.

This is also a good place to puncture a couple of myths that cling to M&S, because the consensus narrative and the financial reality diverge in instructive ways. Myth number one: "M&S is a food company now." As the segment numbers make plain, that's backwards on profitability — clothing earns more than double the margin of food. The food halls generate the footfall and the love, but the fashion floor generates the disproportionate profit. Myth number two: "The clothing turnaround is all about style." Style matters, and M&S has genuinely sharpened its ranges, but the 11.3% margin isn't primarily a fashion story — it's a supply-chain and own-brand story. Because M&S designs and sources its own clothing without paying brand royalties to third parties, it keeps margin that a multi-brand department store has to share. The "trendier clothes" you read about in the press are the visible tip; the invisible nine-tenths is a sourcing and full-price-sell-through machine that quietly defends those margins season after season. And myth number three, the most stubborn: "M&S is a tired old high-street name in terminal decline." That was true for the better part of two decades. The whole point of this episode is that the financials stopped agreeing with the cliché some years ago — and the gap between perception and performance is exactly the kind of thing long-term investors are paid to notice before everyone else does.

But beneath these two big segments sit several "hidden gems" — businesses and assets that don't get their own glossy spread in the annual report but that quietly compound the company's advantages. There are three worth knowing.

The first is Sparks — specifically, the relaunched Sparks 2.0, which went live in April 2026. The original Sparks was M&S's loyalty program, but the 2.0 version reinvented it as a digital-first wallet built around direct cash rewards rather than the arbitrary, hard-to-value points that clutter most loyalty schemes.[^13] The strategic prize here isn't the rewards themselves — it's the data. Sparks has over 18 million members, and the relaunch was an instant hit, racking up 5 million app logins on day one alone.[^13] Think about what that gives M&S: a direct, owned line of communication to 18 million customers, complete with a rich picture of what each one buys and wants. In an era where retailers pay Google and Meta enormous sums for "programmatic advertising" — essentially renting access to their own customers through someone else's platform — owning a proprietary marketing channel of this scale is a structural cost advantage and a data flywheel rolled into one. Every purchase teaches M&S something; every insight sharpens the next offer.

The second gem is the most quietly radical: the Brands marketplace. Remember the century-old DNA — the iron rule that M&S sells only its own products, the St Michael philosophy of total own-brand control? Online, M&S has carefully broken that taboo. Its website now hosts a curated selection of third-party brands — names like Clinique in beauty and Nobody's Child in fashion — turning the M&S platform into a digital marketplace.9 This is a genuinely clever move, because it threads a needle. M&S gets to widen its online range and earn high-margin marketplace economics (taking a cut of other brands' sales without holding all the inventory risk) while keeping its physical stores as a pure own-brand temple. The brand stays protected where it matters most, and gets monetized in a new way where it doesn't.

It's worth dwelling for a moment on why the marketplace move is more profound than it first appears, because it represents a genuine philosophical evolution rather than a mere range extension. For 140 years, the answer to "why should I trust this product?" at M&S was "because M&S made it." The own-brand model and the trust it generated were inseparable. By selling third-party brands online, M&S is making a subtler bet: that the trust it has built is now strong enough to extend to products it merely curates rather than manufactures. In effect, M&S is monetizing its reputation as a tastemaker — telling customers, "we didn't make this, but we vouch for it." That's a powerful and high-margin position if it works, because curation requires far less capital than manufacturing. But it carries a real risk worth naming: every third-party product M&S hosts is a small wager of its hard-won trust. Sell enough mediocre other-brand goods and the halo that took a century to build could dim. Management's discipline in keeping the marketplace tightly curated — and keeping the physical stores a pure own-brand sanctuary — is what keeps that risk contained. It's a tightrope, walked deliberately.

The third gem is M&S Bank, a long-standing financial-services joint venture operated with HSBC. It offers the kind of products — credit, insurance, payment services — that deepen a customer's relationship with M&S and quietly lock them in, all while generating profit without M&S having to carry the full regulatory and capital burden of running a bank itself. It's not a headline business, but it's a sticky, profitable thread in the broader web of customer loyalty. Together, these three gems point at something larger than their individual contributions — they're the connective tissue of a business that has rebuilt not just its stores and its supply chain, but the very sources of its competitive advantage. Which raises the analytical question at the heart of this episode: what, exactly, are those advantages, and how durable are they?

IX. Playbook: The 7 Powers & 5 Forces Analysis

Every great business, the investor Hamilton Helmer argues in his framework "7 Powers," is protected by some durable source of advantage that competitors can see plainly but still cannot copy. The interesting thing about M&S is that it can credibly claim not one of these powers but several — and they happen to map almost perfectly onto the original 1884 DNA. Let's wargame them.

Start with what Helmer calls Counter-Positioning, which is the subtlest and arguably the strongest. M&S operates as a roughly 98% own-brand retailer. Now, why can't a traditional department store — a Debenhams, a House of Fraser in its heyday — simply copy this? Because their entire business model is built on the opposite premise: they make their money by renting floor space and concessions to third-party brands and earning margin on those brands' goods. For such a retailer to pivot to 98% own-brand would mean blowing up its existing revenue model, alienating the brand partners it depends on, and building product-development and supplier capabilities it has never possessed. The incumbent can see exactly what M&S is doing and still cannot follow without committing commercial suicide. That's textbook counter-positioning: an advantage protected not by secrecy but by the rival's own business model holding it hostage.

Next, Process Power — an advantage embedded in the way a company does things, refined over years and impossible to buy off a shelf. This is where the Gist acquisition pays a second dividend. By owning its cold-chain logistics outright rather than renting it, M&S controls speed-to-shelf for fresh food in a way a competitor relying on third-party logistics providers structurally cannot. The freshness of an M&S strawberry isn't a marketing claim; it's a physical consequence of owning the pipes. Competitors can rent good logistics, but they cannot rent logistics built and optimized around their specific products and their specific stores over years of iteration.

Third, the Cornered Resource — exclusive access to something valuable that others simply cannot get. For M&S, that resource is its network of British farming and supplier families, many of them partners for generations. These aren't spot-market vendors selling to the highest bidder; they're deeply integrated, long-cultivated relationships that secure premium, exclusive agricultural supply lines. A discount grocer chasing the lowest price on the open market cannot replicate generational trust. You can't acquire a fifty-year relationship; you can only spend fifty years building one.

And fourth, the most visible power of all: Brand. The famous "This is not just food, this is M&S Food" campaign — with its slow-motion close-ups of molten chocolate puddings and its hypnotic voiceover — is more than memorable advertising. It is a pricing-power machine. It conditions customers to perceive M&S food as a premium experience worth paying a premium for, which in turn protects the company's margins against both inflation and the relentless price pressure of discount rivals. When a brand can make a customer feel that a sandwich is an indulgence rather than a commodity, that brand can charge more — and that pricing power flows straight to the bottom line.

A word of intellectual honesty about these powers, because the bull-case version can be told too smoothly. The most fragile of the four is probably the brand power, precisely because it's the most dependent on continued execution. Counter-positioning and the cornered farming resource are structural — they're protected by other companies' business models and by the simple impossibility of manufacturing decades of relationships overnight. But brand power is earned fresh every day at the point of sale. A few seasons of disappointing clothing, a food-quality scandal, a sustained period where the premium isn't visibly justified, and the "this is not just food" magic curdles back into "why am I paying more for this?" Brands are assets that depreciate the instant you stop investing in them. M&S learned this the hard way during the lost decades, when the brand carried the company on fumes long after the products stopped deserving it. The power is real, but it is a power that must be continually re-won, not a moat that stays full on its own.

Now flip to Michael Porter's classic Five Forces and you can see how M&S's strategy has deliberately reshaped the competitive battlefield. The most acute threat to a legacy retailer is the threat of substitution — the migration of shoppers away from physical stores and toward pure e-commerce — combined with the high bargaining power of buyers, who in a commoditized market can simply click to the cheapest option. M&S's "Reshaping for Growth" store-rotation strategy is, in effect, a direct answer to both forces. By retreating from hollowed-out town centers and redeploying into convenient, well-located "Full Line" retail parks — places with parking, with space for a full food and clothing range, with easy click-and-collect — M&S has positioned its physical estate as a complement to e-commerce rather than a victim of it. The store becomes a fulfillment hub and an experience that the laptop can't replicate, blunting the substitution threat and reducing customers' incentive to defect to a faceless online rival on price alone.

It's an impressive constellation of advantages. But no constellation is permanent, and the smart investor's job is to ask not just "what protects this business?" but "what could break it?" So let's close by putting the bull and the bear in the ring together.

X. Bear vs. Bull Case & KPIs to Track

Here, then, is the argument — the genuine, two-sided debate that any owner of this business should be able to hold in their head at once.

The bull case starts with the proposition that the 2025 cyberattack, for all its drama, was a one-off — a discrete, non-recurring blow rather than a structural wound. And the early evidence supports that read: in the second half of the 2025/26 financial year, profits had already rebounded by 4.1%, suggesting the underlying business absorbed the hit and kept moving.[^10] From there, the bull points to the compounding machines we've already met. The Sparks 2.0 data flywheel should sharpen M&S's ability to drive high-margin clothing sales to exactly the right customers at the right moment, lifting the most profitable part of the business. And the store-rotation strategy is delivering double-digit improvements in sales density — more revenue per square foot — as customers flock to the new retail-park locations. Put those together and you have a business whose three engines — premium food, high-margin fashion, and a digital loyalty layer — are all firing in the same direction, with a management team allergic to wasting a pound. The bull's M&S is a compounder that the market still partly mistakes for a tired old department store.

The bear case is not a caricature, and it deserves to be taken seriously. The first plank is the UK consumer, who remains stubbornly price-sensitive in an economy that has put household budgets under sustained strain. As long as money is tight, the German discounters — Aldi and Lidl — keep chipping away at grocery market share, offering "good enough" quality at prices M&S structurally cannot match. M&S's entire food proposition rests on persuading customers to pay more for better; in a deep enough cost-of-living squeeze, "better" loses to "cheaper," and the premium halo dims. The second plank is the Ocado relationship. That £190.7 million deferred-payment dispute is not just a number on a spreadsheet — it's a symptom of a partnership where the two sides' interests have visibly diverged.[^6] If the friction between M&S and Ocado Group turns genuinely toxic, it could disrupt the single most important runway M&S has for growing food sales online. A joint venture where the partners are suing each other is a fragile foundation for a strategic future.

Layer the two analytical frameworks back over this debate and the tension sharpens. The bull is essentially betting on the durability of Helmer's powers — that counter-positioning, process power, the cornered farming resource, and the brand will keep margins fat and rivals at bay. The bear is essentially betting that Porter's forces reassert themselves — that the bargaining power of a skint consumer and the substitution threat of the discounters and pure-play online grocers grind down even the best-defended incumbent. Both can be partly right; the question is the balance, and the balance is what the numbers will reveal over time.

So what should a long-term investor actually watch? Not the noise — not every monthly sales wobble or headline about the latest celebrity campaign. Three KPIs cut closest to the heart of the thesis, and they're the ones to track.

The first is the Clothing & Home operating margin. This is the engine room of the whole financial model — the high-margin cash cow that funds everything else. The single most important question for the business is whether M&S can sustain that double-digit margin, somewhere around 11%, year after year. If that margin holds or expands, the bull case has legs. If it erodes — if the clothing business has to discount its way to growth — the entire funding structure of the company comes under pressure.

The second is the health of the Ocado Retail relationship, measured both by active-customer growth in the joint venture and by the eventual resolution of that £190.7 million dispute. Active customers tell you whether the online food runway is actually lengthening; the legal resolution tells you whether the partnership is a durable asset or a slow-motion divorce. Watch both.

The third is the return on capital employed of the new "Full Line" retail-park rollouts. This is the metric that connects the strategy to the discipline. M&S is pouring capital into new stores; ROCE on those stores answers the only question that ultimately matters about that spending — is it earning a good return, or is it Brooks Brothers all over again? It's the same question the company's own incentive structure is built to force management to answer honestly.

Track those three — the clothing margin, the Ocado relationship, and the returns on new stores — and you'll know, long before the headlines do, whether the ultimate retailing turnaround is a finished triumph or merely a very good chapter in a story that, 140 years after a Polish refugee hung up a sign in a Leeds market, is still being written.

References

-

Marks and Spencer Group plc Stock Profile (MKS.L) — London Stock Exchange ↩

-

M&S Annual Reports & Financial Results — Marks and Spencer Group plc ↩

-

Reuters Marks and Spencer Group plc Stock Quote & Corporate Actions — Reuters ↩↩

-

Press Release: Marks and Spencer and Ocado Group Announce Creation of Joint Venture — Marks and Spencer Group plc, 2019-02-27 ↩↩

-

Press Release: Marks & Spencer Acquires Gist Limited to Deliver Food Supply Chain Benefits — Marks and Spencer Group plc, 2022-09-30 ↩↩↩↩

-

M&S Annual Report — Directors' Remuneration, Marks and Spencer Group plc ↩↩↩↩

-

M&S Profit Slumps After Scattered Spider Ransomware Attack — Cybernews, 2026-05-21 ↩

-

M&S Annual Reports & Financial Results — Marks and Spencer Group plc ↩↩↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube