Metsä Board: The Great Pivot from Paper to Premium Packaging

I. Introduction: The Luxury Box in Your Hand

Pick up the most expensive perfume on the counter at a Helsinki department store. Turn the box over. Run your fingers along the surface—crisp, bright white, impossibly smooth, with that satisfying structural rigidity that whispers "premium" before you even see the price tag. Now do the same thing with a pharmaceutical blister pack in Tokyo, a chocolate box in Zurich, or a cosmetics carton in New York. There is a reasonable chance that the material cradling those products began its life as a spruce tree in a Finnish forest, owned by a farmer who also grows potatoes and milks cows.

That farmer is one of roughly 90,000 forest owners who collectively control Metsäliitto Cooperative, the parent entity behind Metsä Group—and by extension, behind Metsä Board Oyj, one of the most quietly remarkable corporate transformations in European industrial history. Metsä Board does not make the perfume. It does not design the packaging. What it does is produce the fresh fibre paperboard—folding boxboard and white kraftliner—that forms the structural backbone of premium consumer packaging worldwide. It is the invisible partner behind some of the most recognizable brands on earth, and most consumers have never heard of it.

The thesis of this story is deceptively simple: how does a loss-making, debt-laden Finnish paper company called M-real—caught on the wrong side of the digital revolution, hemorrhaging cash, and staring down structural decline—reinvent itself as a high-margin, pure-play leader in sustainable packaging? The answer involves a cooperative ownership structure that functions like a competitive moat, a series of gut-wrenching mill closures and asset sales, a pair of massive capital bets on converting paper machines into board machines, and a philosophical commitment to thinking in decades rather than quarters. It is the story of a company that burned its own platform—deliberately, methodically—and built something entirely new on the ashes.

The journey from M-real to Metsä Board is not merely a case study in corporate restructuring. It is a case study in how industrial companies can navigate secular decline without succumbing to it, how cooperative ownership can be a strategic asset rather than a governance liability, and how sustainability can transition from a marketing slogan to an actual business model. Along the way, it raises uncomfortable questions about what happens when the transformation is complete and the next act has to begin—questions that the company confronts right now, in early 2026, as it navigates a brutal cyclical downturn with a new CEO and a new strategy.

To understand where Metsä Board stands today, we need to start with the forest—and the 90,000 people who own it.

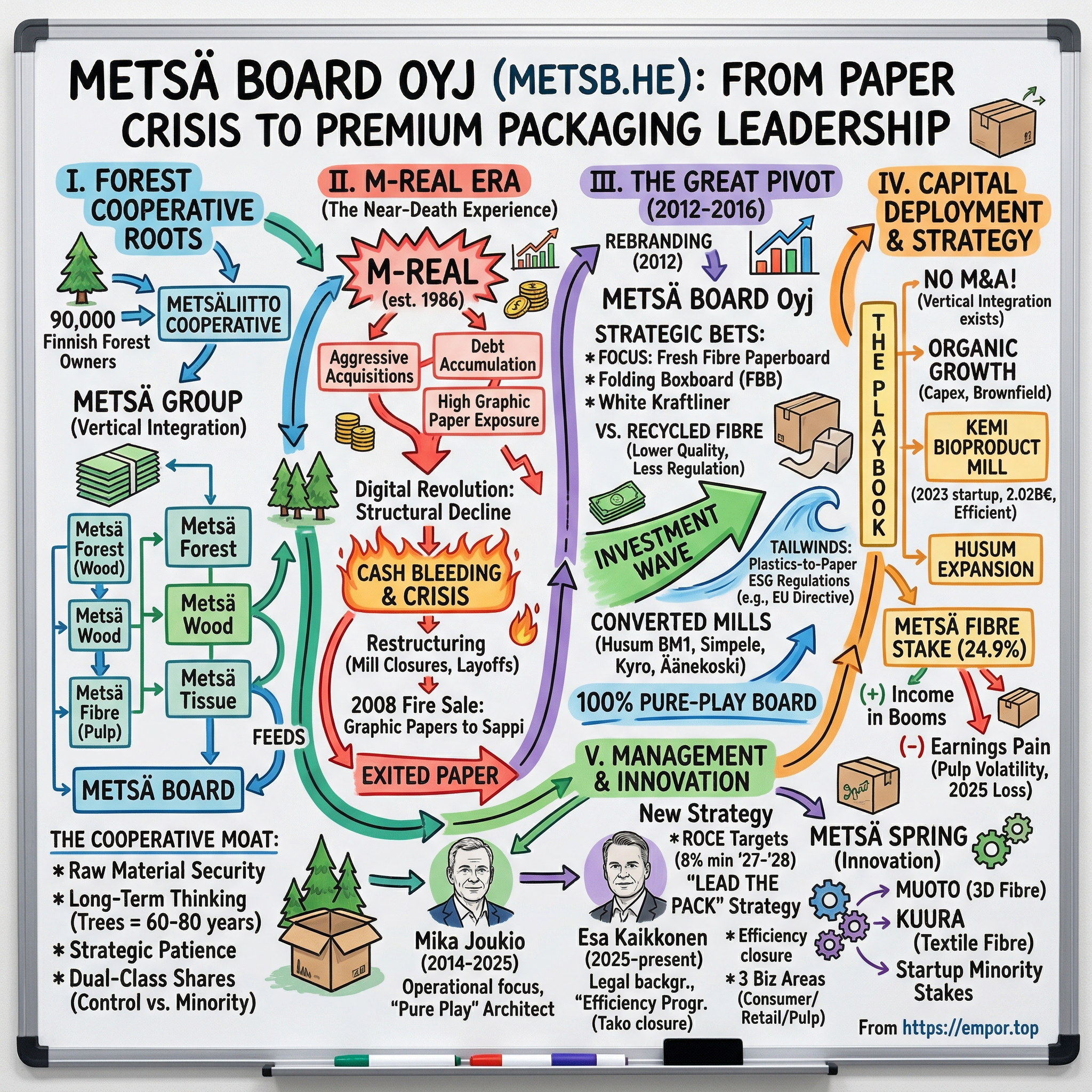

II. The Cooperative Moat: Metsä Group Origins

Picture a map of Finland. Nearly 75 percent of it is covered in forest—roughly 22 million hectares of birch, pine, and spruce stretching from the southern coast to the Arctic Circle. Now picture that forest divided into hundreds of thousands of privately owned parcels, many of them small family holdings passed down through generations. In most countries, this fragmented ownership structure would be a logistical nightmare for an industrial company trying to secure reliable wood supply. In Finland, it became the foundation of one of the world's most distinctive corporate structures.

Metsäliitto Cooperative was formally established in 1947, though its roots stretch back further into the tradition of Finnish forest-owner collaboration. The concept was straightforward: individual forest owners, each too small to negotiate effectively with large industrial buyers, would band together into a cooperative that could aggregate their timber supply, invest in processing capacity, and return the value to members. By 2026, the cooperative counts over 90,000 members—approximately one in three Finnish private forest owners—who collectively own roughly half of all private forests in Finland. That is an extraordinary concentration of a critical natural resource, held not by a corporation or a sovereign wealth fund, but by tens of thousands of individual families.

The cooperative sits atop a vertically integrated industrial empire called Metsä Group, which operates five distinct business areas arranged like a value chain. At the bottom is Metsä Forest, the wood procurement and forest services arm that manages the relationship with member-owners and handles timber harvesting. Above that sits Metsä Wood, producing engineered wood products. Then comes Metsä Fibre, one of Europe's largest producers of chemical pulp—the intermediate product that transforms raw wood into the cellulose fibres used in paperboard, tissue, and other products. Metsä Board converts that pulp into premium paperboard. And Metsä Tissue produces consumer tissue and cooking papers.

This vertical integration is the cooperative's "unfair advantage," and it operates on multiple levels. The most obvious is raw material security. When Metsä Board needs Northern Bleached Softwood Kraft pulp—the premium grade that gives fresh fibre paperboard its characteristic strength, brightness, and printability—it does not have to go to the open market and compete with Chinese tissue manufacturers or Brazilian packaging companies for supply. It sources from Metsä Fibre, in which it holds a 24.9 percent ownership stake. And Metsä Fibre, in turn, sources its wood from the cooperative's 90,000 forest owners. The wood literally flows from the forest floor to the finished packaging carton within a single corporate family.

But the deeper advantage is philosophical. A cooperative owned by forest farmers operates on a fundamentally different time horizon than a publicly traded corporation answerable to quarterly earnings expectations. Trees are not annual crops. A spruce planted in Finland today will not be harvested for 60 to 80 years. When your shareholders are literally growing assets that take a human lifetime to mature, "long-term thinking" is not a corporate buzzword—it is a structural requirement. This orientation shaped every major strategic decision Metsä Board made during its transformation, from the willingness to endure years of painful restructuring to the appetite for billion-euro capital investments with decade-long payback periods.

The cooperative structure also creates a distinctive governance dynamic. Metsäliitto holds approximately 42.5 percent of Metsä Board's total shares but controls roughly 62 percent of voting rights through a dual-class share structure in which A shares carry 20 votes each while B shares carry one vote. This means the cooperative exercises effective control over Metsä Board's strategic direction while minority shareholders—who trade the freely listed B shares on Nasdaq Helsinki—ride along. For minority investors, this arrangement offers stability and strategic continuity. It also means they have virtually no ability to force changes in direction, block related-party transactions, or push for short-term value extraction. Whether this is a feature or a bug depends entirely on whether you trust the cooperative's judgment—and on that score, the historical track record from 2012 onward has been remarkably strong.

Among Finland's "Big Three" forest industry companies, Metsä Group is the only one organized as a cooperative. Stora Enso and UPM-Kymmene are conventional listed corporations with dispersed institutional ownership. This distinction matters because it gave Metsä Board's management a degree of strategic freedom that its peers did not enjoy—freedom to make painful, value-destructive decisions in the short term (closing mills, writing off assets, exiting profitable-but-declining businesses) in service of a long-term vision. It is the corporate equivalent of a patient family office versus a hedge fund, and it proved decisive during the darkest years of the transformation.

The cooperative moat is real, but it is not impregnable. Wood supply from Finnish forests is ultimately finite, constrained by sustainable harvesting limits and increasingly by biodiversity regulations. The cooperative's members are aging—succession planning for small forest holdings is a growing concern. And the governance structure, while providing stability, can also produce inertia when speed is required. Still, for an investor trying to understand why Metsä Board succeeded where many European paper companies failed, the cooperative is the first and most important piece of the puzzle. It provided the raw material security, the strategic patience, and the governance stability that made everything else possible.

That patience would be tested to its absolute limit during the M-real era.

III. The M-real Era: The Near-Death Experience

The modern corporate entity that became Metsä Board was born in December 1986, when Metsäliitto's industrial arm merged with G.A. Serlachius—a company whose roots stretched back to 1868, when a groundwood mill was established in Mänttä, Finland. The merged entity, called Metsä-Serla, spent the 1990s doing what every ambitious European industrial company did during that decade: acquiring aggressively, expanding capacity, and building scale across multiple product categories. By 2001, when the company rebranded as M-real, it had assembled a sprawling portfolio of paper and board mills across Finland, Sweden, Germany, the UK, Hungary, and Switzerland. It was one of the largest paper producers in Europe.

It was also building a house of cards.

The acquisitions of the 1990s had been funded with debt, predicated on the assumption that European demand for graphic paper—the coated and uncoated papers used in magazines, catalogues, advertising inserts, and office printing—would continue growing or at least hold steady. That assumption was about to collide with reality. The rise of digital media, email, and eventually smartphones and tablets did not merely slow the growth of graphic paper demand. It put it into permanent structural decline. Between 2000 and 2015, European graphic paper demand fell by roughly 40 percent, and the decline accelerated with each passing year.

M-real was catastrophically exposed. It had invested billions in paper capacity that was becoming worthless. Its mills were running at declining utilization rates, its pricing power was evaporating, and its debt load—accumulated during the acquisition spree—was crushing. The company was bleeding cash, and the bleeding was getting worse, not better.

In October 2006, M-real launched what it euphemistically called an "extensive restructuring programme." The reality was far more brutal. The Sittingbourne mill in the UK was shuttered in January 2007. Paper machines at the Gohrsmühle mill in Germany followed a month later. Board plants in Hungary and Finland were sold off. Asset divestitures ultimately totaled approximately 700 million euros, exceeding the original 500-million-euro target—a sign of how desperate the situation had become.

The landmark transaction came on September 29, 2008—less than two weeks after Lehman Brothers collapsed—when M-real sold its entire Graphic Papers Business Area to South Africa's Sappi for an enterprise value of 750 million euros. The deal included the Kirkniemi and Kangas mills in Finland, the Stockstadt mill in Germany, and the Biberist mill in Switzerland, representing 1.9 million tonnes of total annual capacity. It was a fire sale conducted during a financial apocalypse, and it reduced M-real's net debt by roughly 630 million euros.

The Sappi transaction was the moment of truth. M-real had effectively sold the business it was built on—graphic paper—and committed itself to a future in paperboard. But that future was far from certain. The remaining board mills needed investment, the balance sheet was still stressed, and the organizational culture was traumatized by years of closures, layoffs, and strategic reversals. The company was alive, but barely.

What happened next was not a sudden breakthrough. It was a slow, deliberate, and occasionally painful process of rebuilding—one that would take the better part of a decade and require a new name, a new strategy, and ultimately a new identity. The decision to stop trying to fix the paper business and instead exit it entirely was, in retrospect, the single most important strategic choice in the company's history. Many European paper companies made the opposite choice—doubling down on cost reduction, capacity rationalization, and consolidation within the declining paper market. Most of those companies are still struggling today. M-real chose to leave.

The question was: leave for where?

IV. The Great Inflection (2012–2016): The Pivot to Board

In March 2012, the company formerly known as M-real did something that might seem trivial but was actually profound: it changed its name to Metsä Board Oyj. The rebranding was not mere cosmetics. It was a public declaration that the company's identity was no longer defined by paper. The word "Board" was now literally in the name—a signal to customers, employees, investors, and competitors that this was a different company with a different future.

The name change coincided with the final stages of a strategic pivot that had been building since the mid-2000s. Since 2005, the company had been systematically shifting its product mix from graphic paper toward fresh fibre paperboard—specifically, folding boxboard and white kraftliner. Folding boxboard, or FBB, is the material used to make the rigid cartons that hold cereal boxes, perfume packages, pharmaceutical products, and consumer electronics. White kraftliner is the premium-grade outer layer used on corrugated shipping boxes and shelf-ready retail packaging. Both products share a critical characteristic: they are made from fresh (virgin) wood fibre rather than recycled fibre, which gives them superior strength, brightness, printability, and food safety properties.

This distinction—fresh fibre versus recycled fibre—was central to Metsä Board's strategic bet. The conventional wisdom in the packaging industry during the 2000s was that recycled fibre was the future: cheaper to produce, environmentally virtuous, and "good enough" for most applications. Metsä Board took the opposite view. They argued that as brands became more sophisticated about packaging as a marketing tool, and as food safety regulations tightened, the premium characteristics of fresh fibre would command an increasing price premium. They also anticipated—years before it became an ESG buzzword—that the global push to replace single-use plastics with paper-based alternatives would create massive new demand for high-performance paperboard that recycled fibre simply could not satisfy.

The first major investment wave came in 2011 and 2012, when the company expanded folding boxboard capacity at its Simpele, Kyro, and Äänekoski mills in Finland, adding roughly 150,000 tonnes of annual production. But the truly transformative bet came in December 2014, when Metsä Board committed approximately 170 million euros to install a new, state-of-the-art folding boxboard machine—designated BM1—at the Husum mill in Sweden.

The Husum investment was an "all-in" moment. The mill, located on the coast of northern Sweden, had been a paper production site for decades. Converting it to produce folding boxboard required not just installing a new machine but fundamentally reconfiguring the entire mill's operations—pulp preparation, energy systems, water treatment, logistics. The new machine, an OptiConcept M board machine supplied by Finland's Valmet, started up in 2016 with an annual capacity of 600,000 tonnes, making it the largest and most modern folding boxboard machine in Europe.

Simultaneously, Metsä Board ceased all paper production. The last paper machines were shut down or sold, and by 2016 the company was a pure-play paperboard producer. The transformation that had begun with the Sappi sale in 2008 was complete. In the space of eight years, the company had gone from being one of Europe's largest paper producers to being a focused, premium-grade paperboard company with zero exposure to the declining graphic paper market.

The timing proved prescient. In the years following the Husum conversion, the European Union began rolling out increasingly aggressive regulations targeting single-use plastics. The EU Single-Use Plastics Directive, adopted in 2019, banned certain plastic products and set collection and recycling targets for others. Consumer brands—especially in luxury goods, cosmetics, food, and pharmaceuticals—began actively seeking paper-based packaging alternatives that could match the visual and structural quality of plastic without the environmental stigma. Metsä Board's fresh fibre folding boxboard was exactly what they needed: strong enough to protect products, bright enough to print beautifully, and made from a renewable, recyclable, biodegradable raw material sourced from sustainably managed Nordic forests.

The plastic-to-paper tailwind was real, and Metsä Board was one of the few companies positioned to capture it at scale. But capturing it required capital—vast amounts of capital—deployed with discipline over many years. The cooperative's patient ownership structure was about to prove its worth once again.

For investors watching the transformation unfold, the key insight was that Metsä Board had not merely survived the paper industry's decline—it had used the crisis as a catalyst to reposition itself in a structurally growing market with higher margins, stronger pricing power, and more defensible competitive advantages. The question was whether the capital deployed to get there would generate adequate returns.

V. Capital Deployment and the M&A Playbook

In an era when most industrial transformations are driven by mergers and acquisitions—buy the capability you lack, absorb a competitor, pay bankers a fee, and call it "strategic"—Metsä Board chose a different path. The company has been conspicuously absent from the M&A market, preferring instead to invest organically in its existing mill infrastructure through massive brownfield expansions and conversions. This is an unusual choice in the forest products industry, where consolidation has been the dominant strategic playbook for decades, and it reveals something important about how the company thinks about value creation.

The logic is rooted in the cooperative structure. When your parent company controls the wood supply and your sister company produces the pulp, you do not need to acquire competitors to secure raw materials or achieve vertical integration—you already have it. What you need is more efficient conversion capacity: larger, faster, more modern machines that can turn pulp into paperboard at lower cost per tonne. That is fundamentally a capital expenditure problem, not an M&A problem. And Metsä Board has pursued it with remarkable discipline.

The centerpiece of this approach is the Kemi bioproduct mill—though technically this was a Metsä Fibre investment, not a Metsä Board one, the distinction is somewhat academic given the integrated nature of the group. Announced in 2020 and started up on September 20, 2023, after approximately two and a half years of construction, the Kemi mill represented a 2.02 billion euro investment—the largest single capital project in Finnish forest industry history. The mill produces 1.5 million tonnes per year of softwood and hardwood pulp, generates 2 terawatt-hours of renewable electricity annually (roughly 2.5 percent of Finland's total electricity consumption), and uses zero fossil fuels in its operations.

For Metsä Board specifically, the Kemi investment had a direct benefit: the adjacent Metsä Board paperboard mill received upgraded infrastructure and logistics, and its white kraftliner capacity was expanded from 425,000 to 465,000 tonnes per year. A transferred unbleached pulp line added another 180,000 tonnes of capacity. A separate development programme at the Kemi board mill reduced water consumption by 40 percent and energy use by 5 percent per tonne of paperboard produced.

How does the Kemi investment benchmark against industry peers? UPM's Paso de los Toros pulp mill in Uruguay, which started up in the same year, cost approximately 3 billion euros for 2.1 million tonnes of capacity—roughly 1,430 euros per tonne. Kemi's 2.02 billion euros for 1.5 million tonnes works out to about 1,350 euros per tonne, a modest but meaningful advantage driven partly by the existing site infrastructure and partly by the energy self-sufficiency that eliminates ongoing fossil fuel costs. The comparison is imperfect—different geographies, wood species, and product mixes—but it suggests that Metsä Fibre achieved competitive capital efficiency despite building in one of Europe's highest-cost labor markets.

Back at Husum, the investment did not stop with BM1. Between 2021 and 2023, Metsä Board invested over 210 million euros to expand folding boxboard capacity by an additional 200,000 tonnes per year, bringing the mill's total FBB capacity to approximately 800,000 tonnes. The expansion started up in November 2023 and was formally inaugurated in 2024. And in a clever financial move, Metsä Board sold a 30 percent stake in the Husum pulp mill to Norra Skog, a Swedish forest-owner cooperative, securing additional wood supply from Swedish forests while sharing the capital burden of pulp production.

The organic investment strategy has clear advantages: it avoids the integration risks and cultural clashes that plague most industrial M&A, it allows precise control over technology and capacity specifications, and it generates assets that are purpose-built for the company's specific product mix. The consulting firm BCG highlighted this contrast in a 2018 study that characterized both Billerud (then BillerudKorsnäs) and Metsä Board as "Nordic Comeback Kids" but noted that Billerud chose M&A as its primary growth mechanism while Metsä Board chose organic investment. Both approaches worked, but they created very different risk profiles.

The 24.9 percent stake in Metsä Fibre deserves special attention as a piece of financial engineering. By holding a minority stake rather than full ownership, Metsä Board captures the economic benefit of pulp production—receiving a proportional share of Metsä Fibre's profits—without consolidating its full balance sheet. This is significant because pulp is among the most cyclical commodities in the world, with prices swinging violently based on supply-demand dynamics, Chinese inventory cycles, and capacity additions. Full ownership of a pulp company would inject enormous earnings volatility into Metsä Board's income statement. The minority stake provides a cushion of pulp-related income during boom years while limiting the damage during busts.

Or at least, that is how it is supposed to work. In 2025, the arrangement went spectacularly wrong. Collapsed market pulp prices turned Metsä Fibre from a profit contributor to a profit drag, and the negative share of result from the pulp business was a major contributor to Metsä Board's full-year operating loss. The 24.9 percent stake, designed as a strategic asset, became a source of significant earnings pain. In February 2026, the ownership structure shifted when Metsäliitto acquired a 5.1 percent stake in Metsä Fibre from Japanese trading house Itochu, raising the cooperative's direct holding to 55.2 percent while Itochu retained 19.9 percent. Whether this signals a future restructuring of the ownership remains to be seen.

The capital deployment story illustrates both the strength and the vulnerability of Metsä Board's model: disciplined, long-horizon investment in world-class assets, funded by a patient cooperative owner, but subject to the brutal cyclicality of commodity markets that no amount of strategic positioning can entirely eliminate.

VI. Current Management: The Steady Hands

On June 10, 2014, a quiet announcement from Helsinki changed the trajectory of Metsä Board. Mika Joukio, a career Metsä Group insider who had begun his working life 35 years earlier at the Tako board mill in Tampere, was appointed CEO. Joukio had risen through the ranks in the most literal sense possible—from mill operations through progressively senior leadership roles across the group's various businesses, most recently serving as CEO of Metsä Tissue. He was not a turnaround consultant parachuted in from outside. He was not a private equity operator. He was a papermaker who understood every stage of the production process from wood chip to finished carton, and he brought that operational intimacy to the top job.

Joukio's leadership style was the antithesis of the "empire building" that had characterized the M-real era. Where his predecessors had chased scale through acquisitions and geographic diversification, Joukio was relentlessly focused on operational excellence, product mix optimization, and return on capital. Under his watch, the company completed its exit from paper, commissioned the Husum BM1 machine, expanded FBB capacity at multiple mills, and navigated the company toward its identity as a pure-play premium paperboard producer. He was the architect of the "Pure Play" era—the executive who took the strategic direction set by the board and the cooperative and translated it into operational reality.

The management philosophy under Joukio reflected a broader shift in how industrial companies think about competitive advantage. Rather than pursuing volume growth for its own sake, the focus was on "lightweighting"—developing proprietary technologies that allow a folding boxboard carton to deliver the same structural performance with significantly less material. Metsä Board's engineers achieved weight reductions of up to 30 percent compared to conventional boards while maintaining identical strength and printability. This is not merely a cost optimization; it is a value proposition for brand owners who can ship more product per pallet, reduce their carbon footprint per package, and lower their material costs—all while maintaining the premium look and feel that luxury and pharmaceutical brands demand.

The compensation structure for senior management tells its own story about priorities. The Long-Term Incentive plans were anchored to Return on Capital Employed—a metric that forces management to think carefully about both the numerator (operating profit) and the denominator (the capital base). In a capital-intensive industry where the temptation to invest in ever-larger machines is constant, tying executive compensation to ROCE creates a natural discipline against empire building. The target was set at levels that required genuine operational improvement, not just revenue growth.

But the governance reality of Metsä Board creates a unique tension. The company is publicly listed on Nasdaq Helsinki, with minority shareholders trading the B shares. Yet Metsäliitto Cooperative controls approximately 62 percent of voting rights through its concentration of A shares (which carry 20 votes each versus one vote for B shares). The cooperative's economic ownership, including through subsidiaries, stands at about 51.8 percent of total shares. This means that Metsä Board's management serves two masters: the cooperative, which prioritizes long-term forest value and employment in Finnish communities, and public market investors, who care about returns, dividends, and share price appreciation. When those interests align—as they did during the growth phase of the transformation—the structure works beautifully. When they diverge, minority shareholders have limited recourse.

On April 7, 2025, that tension surfaced in a dramatic way. Mika Joukio stepped down as CEO "by agreement with the Board of Directors"—the kind of corporate language that usually signals something other than a fully voluntary departure. After 11 years at the helm, the architect of the Pure Play transformation was replaced by Esa Kaikkonen, another career Metsä Group insider with 27 years in the organization. Kaikkonen had served as CEO of Metsä Tissue from 2018 to 2025, as Executive Vice President of Metsä Wood from 2013 to 2018, and as Group General Counsel from 2003 to 2013. His legal background and his experience running Metsä Tissue—a consumer-facing business with its own brand and distribution challenges—brought a different skill set to the CEO role.

The timing of the CEO change was not coincidental. By early 2025, it had become clear that the cyclical downturn in paperboard markets was not a brief dip but a sustained contraction. Full-year 2025 results would ultimately reveal comparable operating losses of 80 million euros, a negative ROCE of 3.1 percent, and zero dividends—a stark reversal from the profitable years of 2017 through 2023. The Husum mill, the crown jewel of the transformation, was the single most significant contributor to the full-year loss, hammered by weak demand, US import tariffs, and collapsed pulp prices.

Kaikkonen moved quickly. In July 2025, he launched a 200-million-euro EBITDA improvement programme targeting completion by the end of 2028, eliminating 310 positions across the company. In January 2025, even before formally taking the CEO role, the board had announced the closure of the Tako board mill in Tampere—the very mill where Mika Joukio had started his career—affecting 208 jobs. The Kyro mill would undergo efficiency enhancements. The expected annual EBITDA improvement from these actions alone was approximately 30 million euros.

In March 2026, Kaikkonen unveiled a new strategy branded "Lead the Pack" with financial targets for 2026 through 2030. The company was reorganized into three business areas: Consumer Packaging (designated the growth engine), Retail Packaging (focused on profitability), and Market Pulp (oriented toward self-sufficiency). The new ROCE targets were set at a minimum of 8 percent for 2027 to 2028 and a minimum of 12 percent from 2029 onward—ambitious targets given the negative ROCE in 2025. Revenue in the Consumer Packaging segment was targeted to grow at a compound annual rate of over 4 percent from the 2025 baseline. The dividend policy was maintained at a minimum of 50 percent of annual net income over time, though with zero dividends paid for 2025, this was more aspiration than near-term commitment.

For minority shareholders, the management transition raises a fundamental question: was Joukio's departure a sign that the cooperative lost confidence in the Pure Play strategy, or was it simply a recognition that the next phase of the company's evolution requires different leadership skills? The "Lead the Pack" strategy suggests continuity rather than rupture—the core commitment to fresh fibre paperboard remains intact. But the emphasis on profitability improvement, cost reduction, and disciplined capital allocation signals a shift from the growth-oriented mindset of the Joukio era toward a more defensive posture appropriate to the current market environment.

VII. The Hidden Business: Metsä Spring and the Future of Fibre

Deep within the Metsä Group organization chart, tucked away from the quarterly earnings calls and mill capacity announcements, sits something unusual for a 150-year-old forest products company: a startup incubator. Metsä Spring is Metsä Group's innovation company, and its mandate is to develop entirely new product categories from wood fibre—products that do not yet exist at commercial scale and that could, if successful, create billion-euro revenue streams from a raw material that the cooperative already owns in abundance.

The most advanced of these ventures is Muoto, a 3D fibre packaging technology developed in partnership with Valmet. A demonstration plant at Äänekoski has been operational since May 2022, producing moulded fibre packages using a process that converts wet wood pulp directly into three-dimensional shapes without intermediate processing steps. The resulting products—food trays, fruit punnets, gift packaging—feature a three-layer structure that is renewable, recyclable, and biodegradable. Think of the plastic trays that hold strawberries or cherry tomatoes at the grocery store. Muoto's technology can produce fibre-based alternatives that perform comparably—protecting the product, withstanding moisture, and looking presentable on the shelf—without any fossil-based materials.

The opportunity here is genuinely enormous. The European market for plastic food trays and containers runs into the tens of billions of euros, and regulatory pressure to eliminate single-use plastics is intensifying with each legislative cycle. If Muoto can achieve cost parity with plastic trays while offering a sustainability advantage, the addressable market is massive. But the technology is still at demonstration scale, and the path from demo plant to commercial production involves significant technical and commercial risk. Metsä Spring has secured partnerships—including a notable collaboration with Fiskars for branded packaging—but the revenue contribution remains immaterial at the group level.

The second major venture is Kuura, a textile fibre made from softwood pulp. The project has been in development since 2014 and currently operates at demo and semi-industrial scale at Äänekoski. The value proposition is environmental: Kuura's greenhouse gas emissions are approximately one-quarter those of cotton and up to 80 percent lower than lyocell, a competing wood-based textile fibre. In 2024, Kuura received Canopy's "Green Shirt" rating—a recognition of responsible sourcing practices—and Metsä Group launched a pre-study for the first commercial Kuura mill, hiring Rami Karhu to lead the concept design.

The textile fibre market is vast—global demand for fibre exceeds 100 million tonnes annually, with cotton and polyester dominating. Wood-based alternatives like viscose, lyocell, and modal have carved out niche positions, but none has achieved true scale dominance. If Kuura can deliver superior environmental performance at competitive cost, it could capture a meaningful share of a market that dwarfs the paperboard industry. But this is a multi-decade bet requiring hundreds of millions in capital investment, and the technology has yet to prove itself at commercial scale.

Beyond Muoto and Kuura, Metsä Spring holds minority stakes in several other innovative ventures: Innomost (extracting valuable compounds from tree bark), Montinutra (nutritional supplements from forest biomass), Fiberwood (insulation materials from wood fibre), and Woodio (bathroom fixtures made from wood composite). Collectively, these ventures represent a portfolio of options on the future value of wood fibre—options that cost relatively little to maintain but could prove transformative if even one or two succeed at scale.

Turning to the core business, it is worth pausing to understand the distinction between Metsä Board's two primary product segments, which serve different end markets with different growth characteristics.

Folding boxboard, with approximately 1.3 million tonnes of annual capacity across the Husum, Simpele, Kyro, and Äänekoski mills, is the premium product. FBB is used for consumer packaging where visual appearance, print quality, and product protection are paramount—perfume boxes, pharmaceutical cartons, food packaging, and electronics boxes. The customer base includes some of the world's most demanding brand owners, and switching costs are meaningful because brands require consistent colour matching, surface quality, and structural performance across global production runs. If a luxury cosmetics brand has qualified Metsä Board's FBB for its packaging, switching to an alternative supplier requires extensive testing, qualification, and potential production disruption. This creates customer stickiness that partially insulates the business from commodity-style price competition.

White kraftliner, with approximately 700,000 tonnes of capacity at the Kemi and Husum mills, serves the corrugated packaging and shelf-ready retail packaging markets. This segment is more volume-oriented and more exposed to competitive pressure from recycled-fibre alternatives. The growth thesis here rests on e-commerce—as more goods are shipped directly to consumers, demand for high-quality corrugated packaging with premium-printed outer layers increases.

As of 2025, the Consumer Packaging segment (essentially folding boxboard) has been designated as the growth engine under the new "Lead the Pack" strategy, while the Retail Packaging segment (white kraftliner and related products) is focused on profitability improvement. This segmentation reflects a clear-eyed assessment that FBB offers higher margins, stronger competitive moats, and better long-term growth prospects than linerboard—but that linerboard remains an important cash flow contributor when managed for efficiency rather than growth.

The Tako mill closure in 2025 was a tangible expression of this prioritization. The mill, located in central Tampere, was one of Metsä Board's oldest production sites—the same facility where folding boxboard production had begun back in 1932. But its city-centre location limited expansion possibilities, its energy costs were high, and its small scale made it uncompetitive against the massive Husum machine. Closing it was operationally rational but emotionally difficult—a reminder that the transformation from M-real to Metsä Board did not end in 2016 but continues to demand hard choices.

VIII. The Playbook: Hamilton's 7 Powers and Porter's 5 Forces

To understand whether Metsä Board's strategic position is truly durable—or merely a well-executed repositioning that could be replicated by competitors—it is worth applying the analytical frameworks that sophisticated investors use to assess competitive moats.

Hamilton Helmer's "7 Powers" framework identifies seven distinct sources of persistent competitive advantage. Metsä Board can credibly claim at least three of them, with varying degrees of strength.

The first and most obvious is Cornered Resource. In Helmer's framework, a cornered resource is an input that a company has preferential access to and that competitors cannot readily replicate. For Metsä Board, the cornered resource is the Finnish and Swedish forest base, accessed through the Metsäliitto Cooperative's 90,000 member-owners. No competitor can replicate this arrangement. Stora Enso and UPM source wood from similar Nordic forests, but they do so as arms-length purchasers, not as the industrial arm of the forest owners themselves. This gives Metsä Board a structural advantage in raw material security and, potentially, in raw material cost—though the latter advantage is moderated by the cooperative's obligation to pay fair prices to its members.

The second power is Scale Economies. The Kemi bioproduct mill (Metsä Fibre) and the Husum BM1 folding boxboard machine are among the largest, most efficient single-site assets in the global forest products industry. The Husum FBB machine alone, with 600,000-plus tonnes of annual capacity, produces more folding boxboard than many competitors' entire mill portfolios. Scale confers advantages in unit cost (spreading fixed costs across more tonnes), energy efficiency (larger boilers and power plants operate at higher thermal efficiency), and logistics (concentrated production enables more efficient warehousing and shipping). These scale advantages compound over time as the fixed-cost base is amortized and operating experience accumulates.

The third is Process Power—proprietary know-how that delivers superior outcomes and that competitors cannot easily observe or replicate. Metsä Board's lightweighting technology is the clearest example. The ability to produce a folding boxboard carton that delivers equivalent structural performance with 30 percent less wood fibre is not simply a matter of running the machine faster or using a better recipe. It involves deep understanding of fibre morphology, multi-layer board construction, surface treatment chemistry, and the interaction between board properties and downstream converting and printing processes. This knowledge is embedded in the organization's engineering teams, process engineers, and application laboratories, and it cannot be acquired through a licensing deal or a hiring spree.

Two additional powers deserve mention as partial or emerging. Brand Power is nascent—Metsä Board is not a consumer brand, but in the B2B world of packaging materials, the company's reputation for consistency, sustainability credentials (CDP A List ratings, EcoVadis Platinum), and technical support creates a form of brand preference among specifiers and procurement professionals. And Switching Costs, while not absolute, are real for brand owners who have qualified Metsä Board's FBB for their packaging lines and would face significant time and cost to requalify an alternative supplier.

Porter's Five Forces framework offers a complementary lens.

The threat of substitutes is actually a tailwind for Metsä Board rather than a headwind—an unusual situation. The primary substitutes for paper-based packaging are plastic-based packaging and, to a lesser extent, aluminum. Regulatory pressure across Europe and increasingly in North America is systematically raising the cost and reducing the acceptability of plastic packaging, particularly single-use plastics in consumer-facing applications. Every plastic tray, blister pack, or clamshell that gets legislated out of existence is a potential conversion to paper-based alternatives. This is not a hypothetical—it is happening now, and it represents the most powerful structural growth driver in the paperboard industry. The EU's Packaging and Packaging Waste Regulation, expected to strengthen further in coming years, codifies this trajectory.

The bargaining power of buyers is the most significant competitive threat. Metsä Board's customers include some of the world's largest consumer goods companies, pharmaceutical manufacturers, and packaging converters. These buyers are large, sophisticated, and price-sensitive. They have multiple supplier options (Stora Enso, BillerudKorsnäs, Mayr-Melnhof, International Paper) and the ability to play suppliers against each other. However, this power is mitigated by two factors. First, for premium applications where colour consistency, surface quality, and food safety certification are critical, the switching costs discussed above create meaningful customer stickiness. A luxury brand cannot simply swap board suppliers mid-production run without risking inconsistency in its packaging appearance. Second, packaging material is typically a small fraction of the total product cost for high-end goods—the board in a perfume box represents a tiny percentage of the perfume's retail price—which reduces price sensitivity relative to quality and reliability concerns.

The bargaining power of suppliers is complicated by the cooperative structure. In one sense, Metsä Board's primary supplier—the cooperative's forest-owning members—has enormous power, since they collectively control the company's raw material base. But the cooperative structure aligns supplier and owner interests, transforming what would normally be an adversarial relationship into a collaborative one. For non-wood inputs (chemicals, energy, logistics), Metsä Board faces the same supplier dynamics as its peers, with no particular advantage or disadvantage.

The threat of new entrants is low. Building a world-scale folding boxboard machine requires capital investment measured in hundreds of millions of euros, deep technical expertise, years of commissioning and optimization, and established customer relationships. The barriers to entry are formidable. No significant new FBB capacity has been built in Europe by a new entrant in decades—all recent capacity additions have come from existing players expanding their mill portfolios.

Competitive rivalry within the industry is intense but structured. The European FBB market is dominated by a small number of large producers—Metsä Board, Stora Enso, and BillerudKorsnäs among them—who compete on product quality, technical service, sustainability credentials, and, inevitably, price. The market is cyclical, and during downturns (like 2025), overcapacity drives aggressive pricing behavior that compresses margins across the industry. During upswings, disciplined capacity management can support pricing power. The key competitive dynamic to watch is whether the current generation of large-scale capacity expansions (Metsä Board at Husum, Stora Enso at various sites) creates a period of structural oversupply that depresses returns below cost of capital—or whether demand growth from the plastic-to-paper transition absorbs the new capacity and supports healthy margins.

For investors tracking Metsä Board's ongoing performance, two key performance indicators stand above all others. The first is Comparable Return on Capital Employed—the metric that management has anchored its own incentive compensation to, and the single best measure of whether the company's enormous capital investments are generating adequate returns. The new targets (8 percent minimum by 2027-2028, 12 percent minimum from 2029) provide clear benchmarks against which to assess progress. The second is FBB delivery volumes, which serve as the most direct real-time indicator of market demand and competitive positioning. When FBB deliveries are growing and ROCE is climbing, the investment thesis is working. When both are declining—as they were in 2025, with FBB deliveries falling roughly 10 percent—the thesis is under stress.

IX. Conclusion: The Bear/Bull Case

Metsä Board is not a commodity company in any conventional sense, even though its products are made from wood and priced in euros per tonne. It is better understood as a "Sustainability-as-a-Service" partner for the Fortune 500—a company that provides the material foundation for brands seeking to replace plastic with paper, reduce their packaging carbon footprint, and meet increasingly stringent regulatory requirements, all while maintaining the premium visual and structural quality that their products demand.

The bull case rests on three pillars. First, the regulatory tide is running strongly in Metsä Board's favor. The EU's Packaging and Packaging Waste Regulation, single-use plastics directives, and food contact regulations are systematically expanding the addressable market for fresh fibre paperboard at the expense of plastic packaging. This is not a cyclical trend—it is a structural shift driven by legislation, consumer preferences, and brand owner commitments that would be politically and commercially difficult to reverse. Second, the capital investments of the past decade have created a manufacturing base that is genuinely world-class. The Husum BM1 machine, the expanded Kemi mill complex, and the ongoing modernization of the Finnish mill portfolio give Metsä Board some of the lowest unit costs and highest quality levels in the global FBB industry. Third, the cooperative ownership structure provides strategic patience and raw material security that publicly traded competitors cannot easily replicate. When the cycle turns—and commodity cycles always turn—Metsä Board's patient ownership base allows it to invest through the downturn rather than cutting capital expenditure to preserve short-term earnings.

The bull case also incorporates the optionality embedded in Metsä Spring. If Muoto achieves commercial scale in moulded fibre packaging, or if Kuura reaches viability as a textile fibre, either venture could add hundreds of millions in revenue from wood fibre that the cooperative already controls. These are free options with asymmetric upside, and they are not reflected in most conventional valuations of the company.

The bear case is equally compelling. The most immediate concern is cyclicality. Despite the premium positioning and sustainability narrative, Metsä Board's earnings remain profoundly cyclical—as the 2025 results demonstrated with brutal clarity. Comparable operating losses of 80 million euros, negative ROCE, zero dividends, and a CEO departure do not describe a company that has fully escaped the commodity trap. Pulp price volatility, transmitted through the 24.9 percent Metsä Fibre stake, can overwhelm the board business's operating performance in adverse market conditions. The company's new net debt to EBITDA ceiling of 2.5 times provides some balance sheet discipline, but it also limits financial flexibility during extended downturns.

Energy costs represent a structural risk that is particularly acute for Nordic producers. While the Kemi bioproduct mill's energy self-sufficiency mitigates this exposure for the Finnish operations, the Husum mill in Sweden remains exposed to Nordic electricity market volatility. The increasing electrification of industrial processes in the Nordics is driving structural increases in electricity demand that may keep prices elevated for years.

The competitive landscape is also evolving. Stora Enso, having completed its own painful restructuring under CEO Hans Sohlström, is investing aggressively in packaging materials and may emerge as a more formidable competitor. BillerudKorsnäs continues to invest in premium virgin fibre packaging. And outside the Nordic region, producers in Asia and South America are building modern FBB capacity with lower labor and energy costs. The assumption that Nordic producers will permanently command a price premium for their products rests on sustainability credentials and proximity to European customers—advantages that could erode if global competitors invest in equivalent certifications and logistics capabilities.

The governance risk for minority shareholders deserves frank acknowledgment. Metsäliitto's 62 percent voting control means that the cooperative's priorities will always take precedence over minority shareholder preferences. When those priorities align with value creation—as they did during the transformation years—this is a powerful advantage. But the cooperative also has obligations to its forest-owning members that may not always align with maximizing the Metsä Board share price. Wood pricing, employment decisions in rural Finnish communities, and capital allocation across the broader Metsä Group are all areas where the cooperative's interests could diverge from those of public market investors.

If Metsä Board were a consumer brand, you might call it the Hermès of industrial packaging—a company that has deliberately positioned itself at the premium end of its market, investing in quality, sustainability, and customer intimacy rather than competing on price. The analogy is imperfect, of course. Hermès does not face the cyclicality of commodity markets, and its customers do not have the option of switching to a recycled-fibre alternative when prices spike. But the strategic intent is similar: to occupy a position in the market where competitive advantages compound over time and where price is secondary to quality, reliability, and brand trust.

The transformation from M-real to Metsä Board is one of the most successful industrial pivots in recent European business history. Whether the next chapter—navigating the current downturn, delivering on the "Lead the Pack" strategy, and capitalizing on the plastic-to-paper transition—proves equally successful will determine whether Metsä Board is remembered as a once-in-a-generation transformation story or as a company that won the battle against paper decline only to face a new set of challenges it was not quite prepared for.

X. Outro

What began as a struggling Finnish paper company called M-real—drowning in debt, trapped in a declining industry, and forced to sell its core business to a South African competitor during the worst financial crisis in a generation—has emerged as Metsä Board, a focused, premium-positioned leader in fresh fibre paperboard with world-class manufacturing assets, a unique cooperative ownership structure, and a front-row seat to the most significant packaging materials transition in decades.

The story is not over. Under new CEO Esa Kaikkonen, the company faces the immediate challenge of restoring profitability from the 2025 trough, delivering on its ambitious ROCE targets, and making the right capital allocation decisions as the plastic-to-paper transition creates both opportunities and competitive pressures. The Metsä Spring ventures—Muoto and Kuura—represent intriguing but unproven bets on the future value of Nordic wood fibre. And the cooperative ownership structure, which proved to be a decisive advantage during the transformation years, will continue to shape the company's strategic choices in ways that public market investors must understand and accept.

Metsä Board trades on Nasdaq Helsinki under the ticker METSB. For anyone interested in the intersection of industrial transformation, sustainability, cooperative governance, and Nordic forestry—and for investors who think in decades rather than quarters—it is a story worth following closely.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube