LSEG: The $27 Billion Pivot from Exchange to Data Empire

I. Introduction & Episode Roadmap

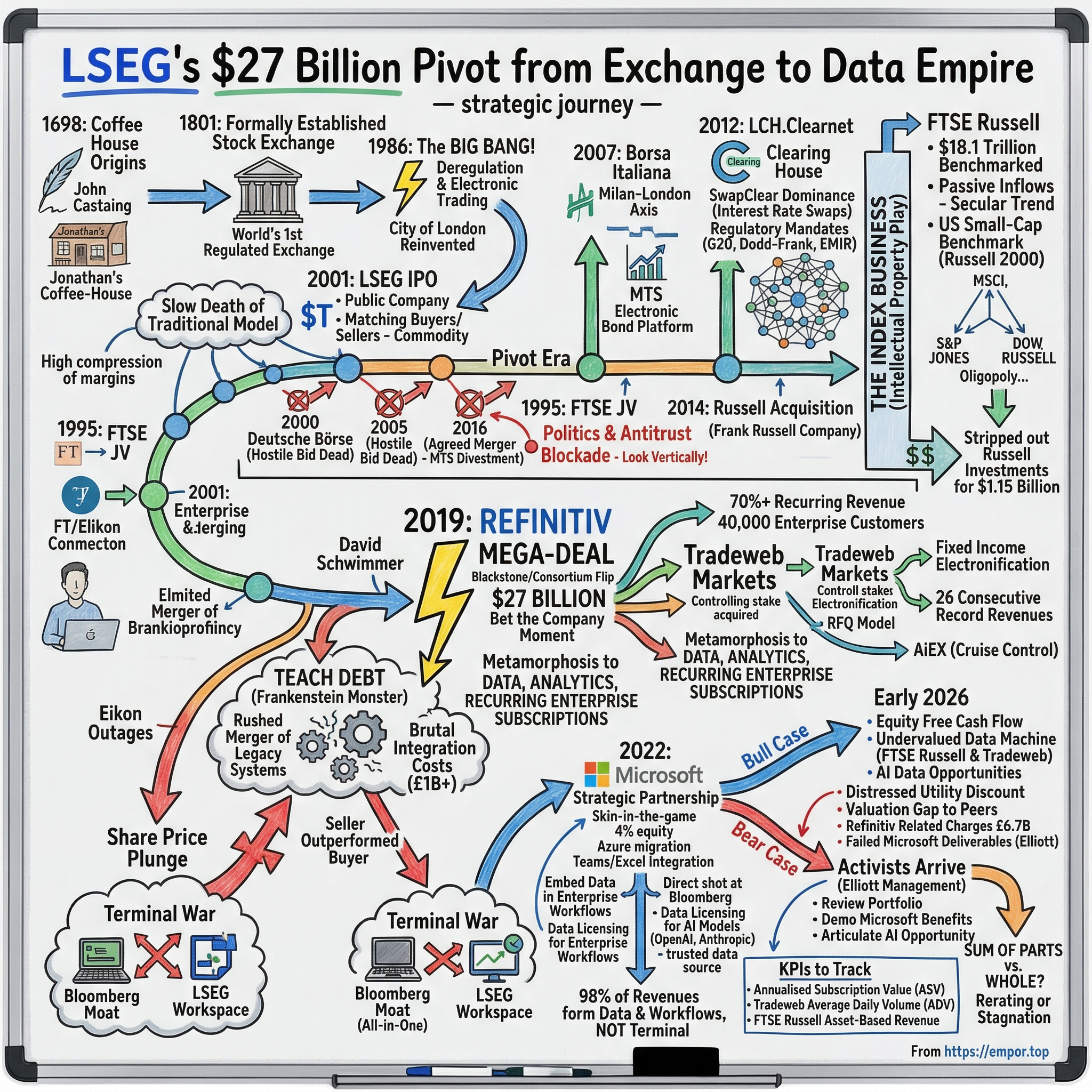

Picture the City of London in the summer of 2019. David Schwimmer, barely a year into his tenure as CEO of the London Stock Exchange Group, stands before a room of analysts and journalists to announce something that will fundamentally alter the identity of a 300-year-old British institution. He is about to tell them that LSEG will acquire Refinitiv, the former financial data arm of Thomson Reuters, for twenty-seven billion dollars. Not a bolt-on deal. Not a tuck-in acquisition. A full-blown corporate metamorphosis, the kind of bet that either defines a CEO's legacy in gold or buries it in rubble.

The number itself was staggering. Twenty-seven billion dollars made it the largest acquisition in London Stock Exchange history by an order of magnitude. But the strategic logic was what made seasoned observers do a double-take. LSEG was not buying another exchange, or another clearing house, or another index provider. It was buying a data company with 40,000 enterprise customers, hundreds of thousands of terminal users, and a technology stack that had been neglected for the better part of a decade.

Overnight, the London Stock Exchange Group would transform from a business where the majority of revenue came from facilitating financial transactions to one where more than seventy percent of revenue would come from data, analytics, and recurring enterprise subscriptions.

The backdrop to this move is the slow death of the traditional exchange model. For most of the twentieth century, stock exchanges were toll booths on capitalism. You wanted to buy shares in Shell or Barclays? You paid the exchange a fee. But deregulation, electronic trading, and relentless competition from dark pools and alternative venues had compressed those margins to near-nothing. The average cost of executing an equity trade had fallen by more than ninety percent over thirty years. Running a stock exchange was increasingly like running a utility: steady but low-growth, vulnerable to every regulatory whim and technological disruption.

LSEG's leadership saw this reality with brutal clarity. The future of financial market infrastructure was not in matching buyers and sellers. It was in owning the data that buyers and sellers need to make decisions, in building the indices that trillions of dollars passively track, in running the clearing houses where risk is netted and managed, and in embedding financial workflows so deeply into enterprise technology that switching becomes unthinkable.

The Refinitiv deal was the most dramatic expression of this thesis, but it was not the first. It was the culmination of a fifteen-year strategic pivot that began with the acquisition of Borsa Italiana in 2007, accelerated with the purchase of LCH and the creation of FTSE Russell, and reached its logical conclusion with the Refinitiv megadeal and the subsequent ten-year partnership with Microsoft.

This is the story of how a coffee-house-born exchange became a data empire. It is a story of visionary strategy and painful execution, of regulatory chess and activist pressure, of tech debt and AI ambition. It is the story of a company that understood the future before its peers, bet everything on that understanding, and is still, as of early 2026, fighting to prove the bet was worth it.

The major themes: the death of the traditional exchange model, the genius of index businesses, the agony of tech debt, and the Microsoft partnership that could change financial workflows forever.

Along the way, there are lessons about corporate reinvention that apply far beyond financial markets: how to manage transformational M&A, why the seller sometimes wins more than the buyer, and what happens when a three-century-old institution collides with Silicon Valley's pace of innovation.

II. The Coffee House Origins & Early History

In 1698, a man named John Castaing began posting a handwritten list at Jonathan's Coffee-House in Exchange Alley, a narrow lane in the heart of the City of London. The list was called "The Course of the Exchange and other things," and it tracked the prices of stocks, commodities, and foreign exchange rates. It was, in the most literal sense, the first financial data product in British history.

Traders who had been expelled from the Royal Exchange for being too rowdy gravitated to Jonathan's, where deals were struck over coffee and the line between gossip and market intelligence was nonexistent. Think of it as the Bloomberg Terminal of its day, except the terminal was a wooden table, the data feed was a man with a quill, and the subscription fee was a cup of coffee.

For the next century, this informal market grew in fits and starts. Brokers eventually outgrew the coffee house, moved to larger premises, and on March 3, 1801, formally established the Stock Exchange under a subscription basis. It became the world's first regulated stock exchange, a distinction that mattered enormously as London emerged as the financial capital of the British Empire.

For nearly two hundred years, the Exchange operated as a private members' club. Through two world wars, the rise and fall of the gold standard, and the dissolution of empire, the London Stock Exchange remained the beating heart of British capitalism. But that continuity masked a creeping irrelevance.

By the mid-1980s, the Exchange was an anachronism. Trading still happened on a physical floor, with "jobbers" making markets and "brokers" executing orders in a single-capacity system that had barely changed since the Victorian era. Jobbers were not allowed to deal directly with the public; brokers were not allowed to trade for their own account. Fixed commissions meant there was no price competition. Foreign firms were locked out. The City of London, once the undisputed centre of global finance, was losing ground to New York and Tokyo, where deregulation was already well underway.

Then came October 27, 1986: the Big Bang. In a single day of sweeping deregulation, Margaret Thatcher's government eliminated fixed commissions on securities trading, authorized dual-capacity dealing so that firms could both broker and deal, opened the Exchange to foreign ownership, and replaced floor-based open-outcry trading with electronic screens.

The impact was immediate and profound. Within months, American and European investment banks poured into London. Goldman Sachs, Morgan Stanley, Deutsche Bank, and UBS established massive trading operations. The old member firms, many of them family-run partnerships that had operated for generations, were swallowed whole. The physical trading floor emptied out; within a few years, it was a museum piece.

The Big Bang did not just modernize the London Stock Exchange. It reinvented the City of London as a global financial centre, positioned between the time zones of New York and Tokyo, offering a regulatory environment that was simultaneously rigorous enough to be trusted and flexible enough to attract international capital. London became the world's largest foreign exchange market, the dominant centre for international bond issuance, and the hub for European equities trading.

The cultural transformation was equally dramatic. Before the Big Bang, the City was a genteel world of pinstripe suits, long lunches, and old-school ties. After it, the City became a meritocratic, high-intensity trading floor culture driven by American-style compensation and global ambition. The Exchange's own identity was swept up in this transformation.

The Exchange itself became a public company in July 2001, listing on its own market after completing its demutualisation. It was a symbolically loaded moment: the institution that had enabled thousands of companies to go public was itself going public for the first time.

But the IPO also exposed an uncomfortable truth. As a public company, LSEG now had to answer to shareholders who cared about revenue growth, margins, and earnings per share. And the core business of matching equity buyers and sellers was becoming a commodity. Electronic trading platforms were proliferating. Chi-X, BATS, and Turquoise were siphoning volume away from the main exchange. Fees were falling.

The existential question facing LSEG's leadership was stark: if merely running an exchange is a race to the bottom, what business should we actually be in?

The answer would take fifteen years and tens of billions of dollars to fully articulate. But the seeds were already being planted. And the first lesson LSEG would learn on its path to reinvention was that the most obvious move, merging with another exchange, was also the most politically impossible one.

III. The Early M&A Era: Borsa Italiana & LCH

Before LSEG could reinvent itself, it first had to survive a decade of attempted takeovers and failed mergers that reads like a corporate soap opera. The early 2000s were the era of exchange consolidation fever, and every major European bourse was either hunting or being hunted.

The logic seemed irresistible: combine exchanges, eliminate duplicate technology, cross-list products, and create pan-European liquidity pools that could rival the NYSE and Nasdaq. In practice, it was a graveyard of nationalist egos, regulatory vetoes, and activist revolts.

The most persistent suitor was Deutsche Börse. The Frankfurt-based exchange operator, led by the ambitious Werner Seifert, made three separate attempts to merge with or acquire the London Stock Exchange over seventeen years.

The first came in May 2000, when the two announced a planned merger. It collapsed almost immediately. The ostensible reason was disagreement over price and governance, but the deeper issue was political. The idea of a German company absorbing the London Stock Exchange was, to put it gently, not popular in the City. The British press treated it as a sovereignty question.

Seifert, frustrated but undeterred, tried again in 2004-2005, launching a hostile bid. This time the deal was torpedoed not by London but by his own shareholders. Chris Hohn, the founder of The Children's Investment Fund, had built an eight percent stake in Deutsche Börse and led a ferocious revolt. Hohn argued that Seifert was overpaying and that the money would be better returned to shareholders. The revolt succeeded spectacularly: Seifert was forced out of his own company, one of the most dramatic shareholder uprisings in European corporate history.

The third and most serious attempt came in March 2016, when Deutsche Börse and LSEG announced an agreed "merger of equals." This time, both sides wanted it. The combined entity would have been Europe's largest exchange group. But the deal made it all the way to the European Commission's review before dying on the antitrust altar. The Commission concluded that combining the two companies would create a de facto monopoly in the clearing of fixed-income instruments, largely because of LSEG's MTS sovereign bond trading platform. The Commission demanded LSEG divest MTS. LSEG refused, and the deal was officially blocked on March 29, 2017.

Three attempts over seventeen years, all failures. The exchange consolidation dream in Europe was dead. The contrast with the United States, where NYSE and Euronext had merged, where NASDAQ had acquired OMX, where ICE had swallowed the New York Board of Trade and then NYSE itself, was stark. In America, exchange consolidation worked. In Europe, political and regulatory resistance made it virtually impossible.

These failed mergers taught LSEG's leadership a crucial lesson: nationalist politics and antitrust regulators would always block horizontal exchange consolidation in Europe. If LSEG wanted to grow, it would have to grow vertically, moving up the value chain into data, indices, and post-trade services rather than sideways into more exchanges. This insight, born of repeated failure, would prove to be the most strategically important conclusion in LSEG's modern history.

The first major step in this vertical direction was the acquisition of Borsa Italiana in 2007. LSEG paid 1.6 billion euros in an all-share deal for the Milan-based exchange, giving Borsa Italiana shareholders twenty-eight percent of the enlarged company.

The headline story was European expansion, the creation of a London-Milan axis that would dominate European equities and fixed-income trading. But the real strategic prize was tucked inside the deal: MTS, Borsa Italiana's electronic platform for trading European government bonds. MTS gave LSEG its first meaningful exposure to fixed-income markets and the recurring data revenues that came with them. The bond market, unlike equities, was still largely opaque and over-the-counter, which meant that owning a platform where government bonds were priced and traded was enormously valuable for generating reference data.

The irony, of course, is that MTS would later become the poison pill that killed the Deutsche Börse merger and that LSEG would ultimately be forced to sell Borsa Italiana entirely to get the Refinitiv deal done. But that lay years in the future.

The more consequential acquisition came in 2012, when LSEG moved to take majority control of LCH.Clearnet, the London-based clearing house. LSEG paid 813 million euros for a fifty-eight percent stake, a price that looked modest at the time and looks like highway robbery in retrospect.

To understand why, you need to understand what happened to clearing after the 2008 financial crisis. And to understand clearing, a simple analogy helps. Imagine two kids trading baseball cards. If Kid A gives Kid B a card and Kid B promises to pay tomorrow, there is counterparty risk: Kid B might not show up. A clearing house is like the teacher who stands in the middle, collecting the card from Kid A and the money from Kid B, guaranteeing that both sides get what they were promised. In financial markets, when the "cards" are billions of dollars in derivative contracts and the "kids" are global banks, that guarantee function becomes systemically critical.

Before the 2008 crisis, most over-the-counter derivatives, the swaps and options that Warren Buffett famously called "financial weapons of mass destruction," were traded bilaterally between banks with no central party guaranteeing the trades. When Lehman Brothers collapsed in September 2008, the cascading counterparty risk nearly brought down the entire financial system. Nobody knew who owed what to whom. The interconnected web of bilateral obligations became a death spiral.

The G20's response, hammered out at the Pittsburgh Summit in 2009, was to mandate that all standardized OTC derivatives be cleared through central counterparties. In the United States, this was implemented through the Dodd-Frank Act, with mandatory clearing taking effect from March 2013. In Europe, through the European Market Infrastructure Regulation, phased in from June 2016. These were not suggestions. They were legal requirements, and they created an enormous structural tailwind for any clearing house that was already positioned in the OTC derivatives space.

LCH's SwapClear service, which had been launched quietly in 1999, was perfectly positioned to catch this tailwind. By the time the mandates took effect, SwapClear was already clearing the overwhelming majority of vanilla interest rate swaps globally, handling twenty-eight currencies and tenors up to fifty-one years. The regulatory mandate did not create SwapClear's dominance; it cemented it into law.

Liquidity in clearing is self-reinforcing. The more participants clear through a single venue, the more efficient the netting of positions becomes, which reduces the capital each participant needs to post as margin, which attracts more participants. It is one of the purest network effects in financial services, comparable to the network effects of a social media platform, except that the "users" are the world's largest banks and the "content" is trillions of dollars in financial risk.

For LSEG, owning the majority of LCH meant owning one of the most structurally critical pieces of infrastructure in global finance: a business with massive barriers to entry, regulatory protection, and the kind of predictable, fee-based revenue that made exchange listing fees look quaint. SwapClear alone processes roughly ninety-five percent of all cleared vanilla interest rate swaps globally, across twenty-eight currencies and tenors stretching up to fifty-one years. That kind of market share, underpinned by regulatory mandate, is the closest thing to a government-granted monopoly that exists in private financial infrastructure.

The lesson from both the Borsa Italiana and LCH acquisitions was clear: the highest-value businesses in financial infrastructure are not the ones that match buyers and sellers, but the ones that sit at choke points where network effects and regulation create self-reinforcing dominance. LSEG was not done building its portfolio of hidden gems. The next acquisition would be even more elegant in its strategic logic.

IV. The Index Business: FTSE Meets Russell

If clearing was LSEG's infrastructure play, indices were its intellectual property play. And the story of how LSEG built one of the world's premier index businesses begins with a joint venture and a newspaper.

FTSE International was established in 1995 as a fifty-fifty partnership between the London Stock Exchange and the Financial Times, which was then owned by Pearson. The name itself, FTSE, was simply an acronym for Financial Times Stock Exchange, and its flagship product was the FTSE 100, the index of the hundred largest companies listed in London. The FTSE 100 had been calculated since January 1984 and had become as synonymous with British financial markets as the Dow Jones Industrial Average was with American ones. When BBC newsreaders said "the Footsie rose twenty points today," they were talking about FTSE's product.

But an index business is not just about brand recognition. It is about something far more powerful: the trillions of dollars that passively track indices.

Here is how the economics work. Every index fund, every ETF, every pension scheme that benchmarks its performance against the FTSE 100 or the FTSE All-World Index pays a licensing fee to the index provider. The fee is tiny as a percentage of assets, typically a few basis points, but when multiplied across trillions of dollars, the numbers become enormous.

And because switching from one benchmark index to another is extraordinarily disruptive for an asset manager, involving portfolio rebalancing, client communication, regulatory filings, and potential tax consequences, these fees are among the stickiest revenue streams in all of finance. An asset manager would sooner change their prime broker, their office lease, and their CEO than change their benchmark index. That is the power of the index business.

In December 2011, LSEG bought out Pearson's fifty percent stake for 450 million pounds, becoming the sole owner of FTSE International. But LSEG's ambitions for the index business were far larger than the UK market. The real prize was on the other side of the Atlantic.

In June 2014, LSEG announced the acquisition of the Frank Russell Company for 2.7 billion dollars, the largest deal in London Stock Exchange history at that time. Frank Russell was an American institution, founded in 1936 in Tacoma, Washington, by a man who started out selling mutual fund research to individual investors.

Over the decades, Russell had evolved into two distinct businesses under one roof. The first was an index business that maintained the Russell 1000, Russell 2000, and Russell 3000 indices, which together benchmarked trillions of dollars in US assets. The Russell 2000, in particular, had become the definitive benchmark for US small-cap stocks, the index that every small-cap fund manager's performance was measured against.

The second was an investment management business, Russell Investments, which ran multi-asset portfolios and consulting services for institutional clients.

LSEG wanted the indices. It decidedly did not want the asset management business, which was lower-margin, more competitive, and created potential conflicts of interest with the index licensing clients. If you are the company that decides which stocks go into the index, you probably should not also be the company running funds that trade those stocks.

So in a move that demonstrated increasingly sophisticated capital allocation, LSEG stripped out Russell Investments and sold it in October 2015 to a consortium led by TA Associates for 1.15 billion dollars. The net cost of acquiring the Russell index franchise was therefore roughly 1.55 billion dollars, a price that looks remarkably prescient given what the business has become.

The merger of FTSE and Russell created FTSE Russell, a global index powerhouse that combined the FTSE's strength in international and emerging market indices with Russell's dominance in US small and mid-cap benchmarking.

The numbers tell the story of why this matters. As of late 2025, approximately 18.1 trillion dollars is benchmarked to FTSE Russell indices globally. Of that, 11.8 trillion dollars is benchmarked specifically to the Russell US Indexes, with 2.7 trillion in pure passive index-tracking funds and 658 billion in ETFs.

To put the scale in perspective, the annual Russell Reconstitution, when companies are added to or removed from the Russell indices based on updated market capitalizations, triggers more than 200 billion dollars in trading volume in a single day. It is one of the largest scheduled liquidity events in global markets, and it happens because FTSE Russell decided to rebalance its index. That is market power. FTSE Russell was also moving to a semi-annual reconstitution schedule beginning in 2026, a change designed to improve index accuracy and generate additional reconstitution-related trading activity.

FTSE Russell generated 918 million pounds of revenue in 2024, growing at nearly eleven percent organically. In 2025, the division continued to grow at over seven percent on a constant currency basis, with asset-based revenues, the fees linked to the amount of money tracking the indices, surging more than eighteen percent as markets rose and inflows into passive products accelerated.

The competitive landscape in indices is a three-way oligopoly. MSCI dominates international and emerging market benchmarking, the standard that global institutional investors use when deciding how to allocate money across countries. S&P Dow Jones Indices, owned by S&P Global, dominates US large-cap benchmarking through the S&P 500, arguably the most famous index in the world.

FTSE Russell's unique position is its strength in US small and mid-cap indexing through the Russell 2000, its broad international coverage through the FTSE All-World and FTSE Developed series, and its growing presence in fixed-income and ESG indices. The switching costs in this business are so high that asset managers often describe changing their benchmark index as roughly as pleasant as changing their prime broker, which is to say, something they would rather avoid at almost any cost.

For LSEG, FTSE Russell represents a nearly ideal business: high margins, recurring revenue, massive switching costs, and secular growth driven by the unstoppable shift from active to passive investing. It is the hidden giant inside LSEG, often overshadowed by the drama of Refinitiv but arguably the most strategically valuable division in the entire company.

But in 2018, LSEG's new CEO would decide that even this was not enough. He would bet the company on something far bigger.

V. The Refinitiv Mega-Deal: The Bet the Company Moment

David Schwimmer does not look like the stereotype of a City of London CEO. A Yale-educated lawyer with a master's degree from Tufts' Fletcher School of Law and Diplomacy, he spent twenty years at Goldman Sachs in a career that took him from the Financial Institutions Group to the innermost circles of the firm's leadership.

He advised on landmark deals like the NYSE-Archipelago merger that transformed the New York Stock Exchange from a mutual into a publicly traded technology company. He served as chief of staff to Lloyd Blankfein when Blankfein was Goldman's president and COO, a role that gave him a front-row seat to how a global financial institution is run at the highest level. He ran Goldman's Russia and CIS investment banking operations during the volatile mid-2000s, and eventually led the firm's global market structure and metals and mining businesses.

He understood market infrastructure not as an abstraction but as something he had spent two decades advising, analyzing, and restructuring. When LSEG announced his appointment as CEO in April 2018, the message was unmistakable: this was a company preparing for a transformational deal, and it had hired a dealmaker to lead it.

Schwimmer joined on August 1, 2018. Barely a year later, in August 2019, he unveiled the Refinitiv acquisition.

To understand the Refinitiv deal, you first need to understand what Refinitiv was and how it ended up on the market. Thomson Reuters had spent decades building the Financial & Risk division, its terminal and data business that competed with Bloomberg. At its peak, the Eikon terminal was on hundreds of thousands of desktops across the global financial industry.

But by the mid-2010s, the division was struggling. Bloomberg was winning the terminal war through relentless product investment, its unmatched messaging network that functioned as a social network for finance, and an all-in-one platform that traders, portfolio managers, and analysts found indispensable. Thomson Reuters' technology platform, the product of decades of acquisitions that were never fully integrated, was creaking under the weight of its own complexity. Reuters had acquired Telerate, Bridge Information Systems, and a dozen smaller data vendors over the years, each with its own architecture, its own data formats, and its own technical debt. The result was a Frankenstein's monster of legacy systems held together with digital duct tape.

In January 2018, a consortium led by Blackstone, the private equity giant, along with the Canada Pension Plan Investment Board and Singapore's GIC, struck a deal to acquire fifty-five percent of Financial & Risk from Thomson Reuters at a valuation of twenty billion dollars. Thomson Reuters retained forty-five percent. The consortium funded the deal with roughly three billion dollars of equity and 14.5 billion dollars of debt. The business was rebranded as Refinitiv, and the deal closed on October 1, 2018.

Blackstone's playbook was straightforward: take a neglected division of a media conglomerate, strip out costs, improve margins, and either IPO or flip it to a strategic buyer. The "flip" came faster than anyone expected. Just ten months after Blackstone's deal closed, LSEG announced it would acquire all of Refinitiv in an all-share transaction valuing the business at twenty-seven billion dollars.

The arithmetic made critics howl. Blackstone had paid twenty billion dollars. LSEG was paying twenty-seven billion, a thirty-five percent premium for a business that had barely changed in the interim. Blackstone's consortium had put in roughly three billion dollars of equity. In barely a year, that equity had roughly tripled. It was one of the fastest and most profitable flips in private equity history, and LSEG's shareholders were the ones writing the check. At roughly thirteen to seventeen times EBITDA, depending on the adjustments, LSEG was paying a full price by any measure.

Schwimmer's defense was strategic, not financial. He argued that combining LSEG's exchange, clearing, and index businesses with Refinitiv's data, analytics, and distribution platform would create a financial market infrastructure company with unmatched breadth. More than seventy percent of the combined company's revenue would be recurring. The data business would give LSEG direct relationships with 40,000 enterprise customers. And critically, Refinitiv came with a majority stake in Tradeweb, the fast-growing electronic trading platform for fixed-income markets, which Schwimmer viewed as one of the most valuable assets in the deal.

The market initially cheered. LSEG shares rose on the announcement as investors bought into the vision of a data-driven future. But the path to closing was long and tortuous. The European Commission launched a lengthy Phase II investigation, probing the competitive implications of combining LSEG's exchange and clearing infrastructure with Refinitiv's data and trading platforms.

Ultimately, the Commission granted conditional approval in January 2021. The condition, however, was painful: LSEG had to divest Borsa Italiana, the Italian exchange it had acquired back in 2007. LSEG sold its entire ninety-nine percent stake in the Borsa Italiana Group, including MTS, to Euronext for 4.325 billion euros. The deal completed on April 29, 2021. The proceeds went straight to paying down acquisition debt. It was the price of admission for the Refinitiv transformation, and it meant that the European expansion LSEG had pursued for fourteen years was undone in a single regulatory stroke. For LSEG veterans who had worked on the Borsa Italiana integration, who had spent years building the London-Milan connection and the MTS bond trading franchise, it was a gut-wrenching sacrifice. But Schwimmer was clear-eyed: the Refinitiv prize was worth more than what was being given up. The future of LSEG was data, not Italian equities.

Then came the reckoning.

In March 2021, barely two months after the Refinitiv transaction closed on January 29, LSEG shares plunged thirteen percent in a single day. The trigger was a set of numbers that blindsided investors: LSEG disclosed that integrating Refinitiv would cost approximately one billion pounds, far more than the market had anticipated.

The technology challenges were staggering. Refinitiv's Eikon terminal was built on a technology stack that industry observers described as "decades of unintegrated acquisitions with distinct technical parameters." One detailed analysis called it "a rushed merger of two different product roadmaps, operating architectures, and technology stacks." Put simply, Refinitiv's technology was a Frankenstein's monster of legacy systems, and making it work as a unified, modern platform would require years of painstaking and expensive remediation.

CEO Schwimmer himself was forced to publicly address repeated Eikon outages, calling them "completely unacceptable" and blaming "a corrupted server issue with our authentication system." For traders who depend on their terminals the way surgeons depend on their instruments, these outages were more than embarrassing. They were existential threats to client retention.

The share price impact was brutal and sustained. LSEG stock had been a London market darling, delivering a stunning 1,980 percent total return from March 2009 to the pre-Refinitiv announcement in July 2019. After the acquisition closed, the story changed dramatically.

Over the four-plus years since completing the deal through early 2026, LSEG shares returned roughly twenty-two percent, less than half the FTSE 100's forty-two percent gain over the same period. Return on equity, which had been in the twelve to fifteen percent range before the acquisition, plummeted to roughly three and a half to four percent by 2024. Debt increased by 1.8 billion pounds even after the Borsa Italiana proceeds. Gross financing costs consumed twenty-six percent of operating profit by 2024, up from ten percent in 2020.

Through the end of 2024, LSEG had spent 1.3 billion pounds on Refinitiv integration costs alone, split roughly evenly between operating expenses and capital expenditure. When you add in 4 billion pounds of acquisition-related amortisation, 688 million pounds in impairments, and 728 million in net financing costs, the total adjusted-away Refinitiv-related charges from 2021 through 2024 reached a staggering 6.7 billion pounds. That is the real, all-in cost of transforming a three-hundred-year-old exchange into a data company.

Meanwhile, Thomson Reuters, freed from the struggling Financial & Risk division, surged one hundred eighty-three percent over the same period. The seller had outperformed the buyer by a factor of nearly six on a compound annual growth rate basis. It was a painful irony that LSEG's leadership could not ignore: the company that sold the asset was thriving, while the company that bought it was struggling under the weight of integration.

The bull case for the Refinitiv deal was never that it would be easy. It was that the long-term strategic positioning, owning the data layer of global financial markets alongside the index, clearing, and trading infrastructure, would ultimately justify the cost.

By 2025, there were signs of progress. Annualised subscription value growth was running at nearly six percent. Total group revenue hit nearly nine billion pounds, with adjusted EBITDA margins above fifty percent and equity free cash flow of 2.4 billion pounds. The integration spending was winding down, with 2025 costs of 133 million pounds, down sharply from 226 million the year before.

But the market remained skeptical, and with the shares down roughly thirty-six percent from their February 2025 highs, the burden of proof still rested squarely on Schwimmer and his team. Hidden within the Refinitiv deal, however, was an asset that would prove to be worth the price of admission on its own.

VI. Hidden Giants: Tradeweb & The Fixed Income Boom

Buried inside the Refinitiv deal was an asset that many analysts now consider the single most valuable thing LSEG acquired: a controlling stake in Tradeweb Markets, the electronic trading platform for fixed-income securities and derivatives.

Tradeweb's story begins in 1996, when a handful of Wall Street dealers, led by Goldman Sachs, created a platform for electronically trading US government bonds. The idea was simple but radical for the time. Government bonds, the most liquid securities in the world, were still traded primarily by phone.

A trader at a hedge fund who wanted to buy ten million dollars of ten-year Treasuries would call three or four dealers, ask for prices, compare them verbally, and execute by saying "done" into a phone handset. It worked, but it was slow, opaque, and riddled with informational asymmetry. The dealer knew exactly how many other dealers the client was calling and could shade prices accordingly. The client had no easy way to prove they got the best execution.

Tradeweb brought the request-for-quote, or RFQ, model to fixed income. Think of it like a reverse auction: a buy-side trader electronically sends a request to multiple dealers simultaneously, all of them see they are competing, and the trader sees competing prices on a screen and can execute in seconds. It sounds unremarkable today, but in the late 1990s, it was a genuine disruption.

The dealers initially resisted, because transparency reduces the spread they can capture on each trade. But the efficiency gains were too compelling, and one by one, the major fixed-income asset classes, government bonds, investment-grade credit, swaps, mortgage-backed securities, migrated to electronic execution. The shift was accelerated by the 2008 financial crisis, which created intense regulatory pressure for greater transparency and better execution documentation in bond markets. Regulators on both sides of the Atlantic wanted to see proof that institutional investors were getting best execution on their bond trades, and electronic platforms provided the audit trail that voice trading never could.

By the time of its IPO, Tradeweb had grown from a niche government bond platform into a multi-asset-class powerhouse handling treasuries, corporate bonds, derivatives, money market instruments, and even equities.

Tradeweb went public in April 2019 in a highly successful IPO, but Refinitiv retained majority ownership. When LSEG acquired Refinitiv, it inherited that controlling stake, which stood at approximately fifty-one percent as of late 2024. LSEG has repeatedly stated it has no plans to sell.

The growth trajectory is remarkable by any standard. Tradeweb reported its twenty-sixth consecutive year of record annual revenue in 2025, reaching 2.05 billion dollars, up nearly nineteen percent year-over-year. Net income surged sixty-two percent to 921 million dollars.

Average daily trading volume across all asset classes exceeded 2.6 trillion dollars, with January 2026 volumes hitting 3.1 trillion, driven by double-digit growth in rates, credit, and money markets. As of early 2026, Tradeweb's standalone market capitalisation was approximately 23.6 billion dollars, meaning LSEG's fifty-one percent stake was worth roughly twelve billion dollars, or nearly a quarter of LSEG's entire market cap in a single subsidiary.

The structural tailwind behind Tradeweb is the ongoing electronification of fixed-income trading, a shift that is best understood by comparison to what happened in equities decades ago. In stock markets, electronic trading reached near-total penetration by the early 2000s. Virtually no equities are traded by phone today. In fixed income, the shift is still in its middle innings at best. Voice trading still accounts for a significant share of corporate bond and derivatives execution, particularly for large or complex trades. Every percentage point of additional electronification in a market measured in hundreds of trillions of dollars of annual volume represents an enormous revenue opportunity for platforms like Tradeweb.

One of the most compelling innovations driving Tradeweb's growth is AiEX, its Automated Intelligent Execution protocol. AiEX allows institutional investors to set rules-based parameters for automated trading: if a request for quote comes back within certain spread and size thresholds, execute automatically without human intervention.

This is not algorithmic trading in the high-frequency sense, where computers race to shave microseconds off execution times. It is workflow automation for buy-side trading desks, freeing human traders to focus on complex, high-touch transactions while routine trades execute themselves. Think of it as cruise control for bond trading. AiEX adoption has been accelerating, particularly in European credit markets, where it contributed to a fifteen-plus percent increase in average daily volumes.

For LSEG, Tradeweb serves multiple strategic purposes beyond raw revenue growth. It is a high-growth engine driving the Capital Markets division to nearly eighteen percent organic growth. It generates the real-time pricing data that feeds into LSEG's data and analytics products, creating a virtuous cycle where more trading activity produces more data, which makes the data products more valuable, which attracts more customers.

And it provides a platform where LSEG can embed additional services, from pre-trade analytics to post-trade reporting and regulatory compliance, creating the kind of vertically integrated ecosystem that makes customer relationships sticky.

The competitive landscape in electronic fixed-income trading is increasingly crowded. MarketAxess, Tradeweb's most direct competitor in credit markets, has carved out a strong position in US investment-grade bonds through its proprietary Open Trading protocol. Bloomberg, ICE Bonds, and various dealer-to-dealer platforms compete across different asset classes and protocols. But Tradeweb's breadth across rates, credit, equities, and money markets, combined with its dominant position in US Treasuries and European government bonds, gives it a diversification advantage that no single competitor matches.

If the Refinitiv deal is ultimately judged a success, Tradeweb will be a major reason why. The crown jewel was hiding in the Frankenstein's monster all along. But even crown jewels need a modern setting, and the challenge of rebuilding Refinitiv's technology infrastructure would require a partner with capabilities far beyond LSEG's own.

VII. The Microsoft Partnership & Current Management

By 2022, LSEG's leadership had reached a sobering conclusion about the technology challenge they faced. Refinitiv's legacy infrastructure, the product of decades of acquisitions by Reuters and Thomson Reuters, could not simply be patched or upgraded. It needed to be rebuilt from the ground up on modern cloud architecture. And LSEG, for all its financial engineering prowess, was not a technology company. It needed a partner with world-class cloud infrastructure, deep enterprise relationships, and the engineering talent to execute a migration of extraordinary complexity. It needed Microsoft.

In December 2022, LSEG and Microsoft announced a ten-year strategic partnership that went far beyond a typical cloud migration deal. Microsoft would acquire an approximately four percent stake in LSEG, purchasing shares from the Blackstone and Thomson Reuters consortium. LSEG committed to spending a minimum of 2.8 billion dollars on Microsoft cloud products over the ten-year term. Scott Guthrie, Microsoft's Executive Vice President of Cloud and AI, would join the LSEG board as a non-executive director. This was not a vendor-client relationship. It was a strategic alliance with real skin in the game on both sides. Microsoft was not just selling cloud services; it was investing in the outcome. And LSEG was not just buying technology; it was buying a decade-long commitment from one of the world's most capable engineering organisations.

The vision was ambitious. LSEG's entire data platform and technology infrastructure would migrate to Microsoft Azure, replacing the patchwork of on-premise data centres and legacy systems that Refinitiv had accumulated over decades.

But the headline-grabbing piece was the plan to embed LSEG's financial data and analytics directly into Microsoft 365 and Teams. Imagine a portfolio manager who can pull real-time bond pricing data into an Excel spreadsheet that updates live, or a compliance officer who can run regulatory checks within Teams without leaving the application, or an investment banker who can query LSEG's vast historical databases using natural language through an AI assistant embedded in their daily workflow. The idea was to meet financial professionals where they already work, inside Microsoft's productivity suite, rather than forcing them onto a separate terminal.

This was a direct shot at Bloomberg. The Bloomberg Terminal's greatest strength has always been its all-in-one ecosystem: messaging, analytics, trading, news, all in a single proprietary platform with its distinctive black and orange interface. But that ecosystem also means Bloomberg users must live inside Bloomberg's world. LSEG's bet was that the next generation of financial professionals would prefer data integrated into the tools they already use, Microsoft tools that are already on every desk in every financial institution, over a monolithic terminal experience. If Bloomberg's model is the walled garden, LSEG's model is the open highway.

LSEG Workspace, the rebranded and rebuilt successor to the Eikon terminal, became the centrepiece of this strategy. Priced at approximately 22,000 dollars per user per year, competitive with Bloomberg's 24,000 to 27,000 dollar range, Workspace was designed as a cloud-native platform with seamless Microsoft integration and built-in compliance features. The theory was compelling. The execution has been harder.

As of early 2026, the Microsoft partnership had come under intense scrutiny. Elliott Management, the activist hedge fund that built a stake in LSEG in February 2026, argued publicly that the partnership "has failed to deliver so far and other companies are moving much faster." Disbursement of the 2.8 billion dollar commitment had been slow through 2024, raising questions about whether the technical complexity of migrating decades of legacy data onto Azure was proving more difficult than anticipated.

There were also broader competitive dynamics at play. Bloomberg, far from standing still, had been aggressively building its own AI capabilities. FactSet, S&P Capital IQ, and a host of specialized fintech competitors were all investing heavily in cloud-native platforms. The terminal market, where Bloomberg controlled roughly thirty-three percent and LSEG held roughly twenty percent, was not getting easier.

Yet there were signs that LSEG was pivoting its distribution strategy in a more promising direction. Rather than trying to win the terminal war through Workspace alone, LSEG began licensing its data for consumption through AI models and cloud platforms. During 2025, LSEG signed long-term data contracts worth approximately 1.9 billion pounds with major global institutions and expanded partnerships with OpenAI, Microsoft, Databricks, and Anthropic for distributing financial data through cloud and AI channels.

The insight was that as AI reshapes financial workflows, the value may not be in the terminal at all, but in being the trusted data source that feeds whatever interface financial professionals use, whether that is a terminal, a chatbot, or an AI agent. In 2025, eleven leading global banks also agreed to acquire a twenty percent stake in LSEG's Post Trade Solutions unit for 170 million pounds, valuing the unit at 850 million, a sign that LSEG's institutional clients wanted to co-invest in the infrastructure rather than merely subscribe to it.

Through all of this, David Schwimmer has remained at the helm, though not without controversy over his compensation. In April 2024, LSEG's board pushed through a major overhaul of executive remuneration. Schwimmer's base salary was raised from one million pounds to 1.375 million, and his maximum potential total compensation was increased to 13.2 million pounds.

The board justified the increase by benchmarking against US peers like CME Group, Nasdaq, Intercontinental Exchange, S&P Global, and MSCI, arguing that LSEG's CEO was dramatically underpaid relative to peers running comparable businesses. Schwimmer's stock ownership requirement was raised to six times his base salary, and eighty percent of his compensation was tied to long-term performance metrics including total shareholder return and earnings per share growth.

The shareholder vote passed, but with significant dissent. Nearly eleven percent of shareholders voted against, a notable rebellion by UK corporate governance standards where even single-digit opposition is considered a strong protest. The dissent reflected a broader frustration: Schwimmer was being paid like the CEO of a high-growth US data company, but LSEG's share price was performing like a struggling UK financial conglomerate.

His actual total compensation for 2024 came in at 7.9 million pounds, up forty-six percent from the prior year, with his annual bonus paid at seventy percent of the maximum. His entire economic incentive is now laser-focused on proving that the Refinitiv integration, the Microsoft partnership, and the AI pivot can permanently re-rate LSEG's valuation multiple.

In February 2026, the pressure ratcheted up further when Elliott Management emerged as an activist shareholder with roughly eighty billion dollars in assets under management. Elliott's demands were pointed: review the portfolio and consider asset sales, launch a five-billion-pound share buyback, demonstrate concrete benefits from the Microsoft partnership, and articulate clearly why AI is an opportunity rather than a threat to LSEG's business model.

LSEG responded with a three-billion-pound buyback program over twelve months, a fifteen percent dividend increase, and pointed to the 2.1 billion pounds in share repurchases already completed during 2025. But Elliott's presence signals that the window for patience is narrowing. The question now is whether the strategic framework that underpins LSEG's transformation is robust enough to justify the continued faith of its shareholders.

VIII. Playbook: Strategy & Framework Analysis

Strip away the history and the drama, and LSEG's strategic position can be analyzed through two powerful frameworks that illuminate both its strengths and its vulnerabilities.

Hamilton Helmer's 7 Powers

The most valuable powers in LSEG's arsenal are network economies, switching costs, and cornered resource.

Network economies are most visible in LCH's clearing business. In central clearing, every additional participant improves capital efficiency for all existing participants through multilateral netting. Here is how it works: if ten banks clear their interest rate swaps through LCH, the netting of offsetting positions reduces the margin each bank needs to post. When the eleventh bank joins, the netting improves for everyone, because there are more offsetting positions to cancel out.

This creates a flywheel that is nearly impossible for a new entrant to replicate. A competitor would need to convince a critical mass of banks to simultaneously move their clearing, a coordination problem so severe that it functions as an almost insurmountable barrier to entry. It is the same dynamic that makes it nearly impossible to launch a new social network: everyone is already on the existing one, and the value of being there increases with each additional participant. SwapClear's roughly ninety-five percent market share in vanilla interest rate swaps is a direct consequence of this dynamic.

Tradeweb benefits from a related but distinct form of network economies. In electronic trading, liquidity attracts liquidity. The more dealers provide prices on Tradeweb, the tighter the spreads for buy-side clients. The tighter the spreads, the more buy-side firms use the platform. The more buy-side flow, the more attractive it is for dealers to provide prices. This virtuous cycle has driven twenty-six consecutive years of record revenue and makes it increasingly difficult for competing platforms to break in.

Switching costs are the bedrock of the index and data businesses. For FTSE Russell, the cost of switching a benchmark index is not just financial. It involves portfolio rebalancing that can trigger taxable events, client communication and consent requirements, regulatory filings, updates to investment mandates and marketing materials, and operational changes to portfolio management systems. The effort and risk of switching are so disproportionate to the licensing fees that most asset managers simply never do it. This is why index businesses can sustain pricing power decade after decade while most commodity businesses see their margins compressed to nothing.

In the data and analytics business, switching costs manifest differently but are equally powerful. Enterprise data feeds are deeply embedded in clients' risk management systems, trading platforms, and regulatory reporting infrastructure. Replacing a data provider means months of parallel running, extensive testing, and the risk that downstream systems dependent on specific data formats and identifiers will break. LSEG's real-time pricing data, reference data, and end-of-day valuations are woven into the operational fabric of thousands of financial institutions. The proprietary identifiers themselves, the SEDOL security codes, the Reuters Instrument Codes, are hardcoded into systems that would need to be reprogrammed to accept alternatives.

Cornered resource is where LSEG's position is more nuanced. The "London Stock Exchange" brand itself carries three centuries of institutional authority, but brand alone is not a durable competitive advantage in financial infrastructure. The more valuable cornered resources are the proprietary datasets, the historical pricing databases going back decades, and the regulatory relationships that give LSEG's data a provenance and reliability that competitors struggle to replicate.

Where LSEG is weaker in the 7 Powers framework is in scale economies and counter-positioning. Scale economies exist, but they are less decisive than in pure technology businesses because regulatory fragmentation means that serving additional geographies requires incremental compliance costs. Counter-positioning, the power derived from a business model that incumbents cannot copy without damaging their existing business, does not apply to LSEG. It is itself the incumbent.

Porter's Five Forces

The threat of substitutes varies dramatically across LSEG's business lines and represents the most important force to monitor. In the terminal business, Bloomberg is the dominant substitute, with approximately thirty-three percent market share versus LSEG's roughly twenty percent. Bloomberg's all-in-one platform creates an ecosystem stickiness that LSEG has struggled to replicate. FactSet, S&P Capital IQ, and emerging AI-native platforms all represent substitutes of varying credibility. In clearing, substitutes are limited by regulation and network effects. In indices, MSCI is the primary alternative for international benchmarking, while S&P Dow Jones dominates US large-cap.

Bargaining power of buyers has historically been high, particularly for data products where large banks can negotiate volume discounts and threaten to build in-house alternatives. However, LSEG's strategy of embedding data into enterprise workflows through the Microsoft partnership is explicitly designed to reduce buyer power by increasing switching costs. If LSEG data is flowing through Microsoft Teams and Excel into compliance and risk systems, the data provider relationship becomes architecturally entrenched rather than contractually negotiable.

Bargaining power of suppliers is relatively low. LSEG's primary inputs are technology talent, data center capacity, and regulatory licenses, none of which are controlled by a small number of suppliers with pricing power.

Threat of new entrants is moderate and evolving. In clearing, the threat is near zero. In indices, the threat is low because of the enormous installed base of assets already benchmarked. In data and analytics, however, the threat from AI-native platforms and alternative data providers is the most important strategic question LSEG faces. If large language models can synthesize financial data from multiple sources and deliver insights without requiring a traditional terminal or data feed, the value of LSEG's distribution channels could erode even as the value of its underlying data increases. This is why LSEG's partnerships with OpenAI, Anthropic, and Databricks are so strategically important: they represent an attempt to position LSEG's data as the authoritative source feeding the AI models, rather than being disintermediated by them.

Rivalry among existing competitors is intense across every segment. S&P Global, MSCI, Bloomberg, ICE, CME Group, and Deutsche Börse are all well-capitalized, strategically ambitious competitors with overlapping business lines.

The competitive intensity is highest in data and analytics, where the combination of legacy terminal competition and emerging AI disruption creates genuine strategic uncertainty. Bloomberg, in particular, is a formidable rival because it is privately held, which means it can invest for the long term without quarterly earnings pressure, and because its Terminal's messaging network creates social switching costs that no amount of data quality can overcome. When a trader's entire professional network communicates through Bloomberg chat, switching terminals means switching social networks, a far harder decision than switching data providers.

The capital allocation narrative running through all of this is LSEG's deliberate, sometimes painful transition from cyclical, transaction-based revenue to predictable, recurring enterprise subscriptions. In 2015, before the Refinitiv deal, the majority of LSEG's revenue was transaction-based, rising and falling with market volatility and trading volumes. Today, roughly seventy percent of total group revenue is recurring, driven by data subscriptions, index licensing, and clearing fees with minimum guaranteed volumes.

This transformation has compressed returns in the short term, as the integration costs and tech debt remediation have consumed billions. But if the strategy works, LSEG will emerge as a business with Bloomberg-like revenue predictability, running on Microsoft-scale infrastructure, with the switching costs of a benchmark index provider. That is the prize Schwimmer is playing for.

IX. Bear vs. Bull Case

The debate over LSEG among institutional investors is unusually polarized. The bears and bulls are not just disagreeing about execution or timing. They are fundamentally disagreeing about what kind of company LSEG is.

The Bear Case: The Distressed Utility Discount

Bears argue that LSEG is a stitched-together conglomerate masquerading as a growth company. The case starts with valuation. LSEG trades at roughly eleven times enterprise value to EBITDA, a significant discount to peers. CME Group, the Chicago-based derivatives exchange, trades at roughly sixteen times. S&P Global, the data and ratings giant, trades at roughly eighteen times. MSCI, the index powerhouse, commands an even richer multiple.

If the market believed LSEG was truly a high-quality, recurring-revenue data business, it would trade at a premium. Instead, it trades at a discount, and bears argue the market is right. The valuation gap, they contend, reflects the reality that LSEG is not one business but several, bolted together through acquisitions, and that the whole is worth less than the sum of its parts because of the management complexity and integration drag.

The tech debt problem, they say, is not solved, merely stabilized. Eikon lost approximately 900 million pounds in revenue from market share erosion before being rebranded as Workspace. Bloomberg's moat, its all-in-one ecosystem, its messaging network that functions as a social network for finance, its relentless investment in product, is simply too wide to breach. LSEG is spending 2.8 billion dollars on a Microsoft partnership that, in Elliott Management's pointed words, "has failed to deliver so far." The terminal business is fighting a war it cannot win.

Bears also point to the financial burden of the Refinitiv acquisition. The 6.7 billion pounds in adjusted-away costs is not an abstraction. It represents real cash and real dilution. Return on equity has been crushed to levels one-third of pre-acquisition performance. The share price has underperformed the broader FTSE 100 since the acquisition closed. Thomson Reuters, which sold the business and walked away, has outperformed LSEG by a factor of nearly six on a compound annual growth rate basis. Sometimes, the bear case goes, the seller knows more than the buyer.

There is also a structural governance concern that bears highlight. LSEG is a London-listed company competing against US-listed peers, which means it faces UK shareholder activism norms, UK executive compensation constraints, and the UK regulatory environment.

American financial infrastructure companies can more easily attract top talent with higher pay, buy back shares more aggressively, and pursue acquisitions without the same level of political and regulatory scrutiny. LSEG may be permanently disadvantaged by its listing jurisdiction, the very market it operates. The irony is not lost on observers: the company that runs the London Stock Exchange may itself be undervalued partly because it is listed in London rather than New York.

The Bull Case: The Underappreciated Data Machine

Bulls argue that the market is pricing LSEG for the pain of integration while ignoring the strategic position the integration has created. The discount to peers, they say, is precisely the opportunity.

Start with FTSE Russell. This is a nearly one-billion-pound revenue business growing at double digits, with switching costs that make customer churn negligible, operating in a sector where passive investing is a multi-decade secular tailwind. Eighteen trillion dollars is benchmarked to FTSE Russell indices. As global wealth grows and passive penetration increases, especially in markets outside the United States where indexing is still relatively underpenetrated, this number can only go up. FTSE Russell alone, if separately valued at the multiples commanded by MSCI's index business, could be worth twenty to twenty-five billion dollars, roughly half of LSEG's entire enterprise value.

Then there is Tradeweb. LSEG owns fifty-one percent of a publicly traded company with a market cap of 23.6 billion dollars and a growth rate that any technology CEO would envy. Twenty-six consecutive years of record revenue. Average daily volumes of 2.6 trillion dollars. A leadership position in the electronification of fixed-income markets that is still in its middle innings. LSEG's Tradeweb stake alone is worth approximately twelve billion dollars.

LCH's clearing business benefits from regulatory mandates and network effects that are essentially permanent. No rational regulator is going to unwind the post-2008 central clearing requirements. And no rational market participant is going to voluntarily move their interest rate swap clearing away from a platform that clears the vast majority of the global market.

On the AI front, bulls see LSEG's data assets as enormously valuable in a world where AI models need authoritative, real-time financial data. The 1.9 billion pounds in long-term data contracts signed in 2025, the partnerships with OpenAI, Anthropic, and Databricks, are early evidence that LSEG's data is being consumed through new channels at premium prices.

If AI disintermediates the terminal, it does not disintermediate the data. The data is the foundation that AI builds on, and LSEG owns vast quantities of it with provenance and reliability that new entrants cannot easily replicate. This is the crucial insight: ninety-eight percent of LSEG's revenues come from data and workflows, not from the terminal itself. The terminal is merely one distribution channel.

The Microsoft partnership, while slow to deliver visible results, represents the kind of deep infrastructure rebuild that takes years before it inflects. When it does, Workspace-on-Azure will offer financial professionals something Bloomberg cannot: seamless integration with the productivity tools they already use, at a lower total cost of ownership, with AI capabilities built in from the ground up. The minimum spend commitment of 2.8 billion dollars means LSEG is fully invested in the build, and Microsoft's four percent equity stake and board seat mean the tech giant is equally committed.

Finally, there is the free cash flow story. With integration costs winding down and adjusted EBITDA margins above fifty percent, LSEG generated 2.4 billion pounds of equity free cash flow in 2025. The three-billion-pound buyback program, the fifteen percent dividend increase, and the accelerating share repurchase pace suggest management sees the shares as significantly undervalued. If recurring revenue continues to grow at mid-to-high single digits, margins expand as integration costs fade, and Tradeweb maintains its growth trajectory, the free cash flow generation over the next five years could be substantial enough to force a re-rating.

KPIs to Track

For investors following LSEG's ongoing evolution, three metrics matter above all others.

First, Annualised Subscription Value growth. ASV measures the run-rate value of LSEG's recurring data subscriptions and is the single best indicator of whether the core data business is driving organic growth or merely maintaining the status quo. ASV growth of 5.9 percent at December 2025 is respectable but needs to accelerate toward seven or eight percent to justify a premium multiple.

Second, Tradeweb Average Daily Volume. ADV is the best real-time proxy for the electronification trend and Tradeweb's competitive position. Sustained double-digit ADV growth signals that the structural shift from voice to electronic trading is accelerating and that Tradeweb is capturing share.

Third, FTSE Russell asset-based revenue growth. Because these revenues are directly linked to the assets benchmarked to FTSE Russell indices, they capture both market appreciation and net inflows into passive products. The underlying trend of passive investing adoption makes this a structural growth metric, though it is amplified or dampened by market movements.

These three numbers collectively tell the story of whether LSEG's data, trading, and index businesses are compounding in the way the bull case requires. If all three are accelerating simultaneously, the re-rating thesis becomes very difficult to argue against. If any one stalls, particularly ASV, it signals that the Refinitiv integration has not delivered the organic growth engine that justified the acquisition premium.

X. Epilogue & Takeaways

The London Stock Exchange Group's transformation over the past fifteen years is one of the most ambitious and consequential corporate metamorphoses in modern financial history. A three-hundred-year-old institution that began with handwritten price lists in a coffee house has deliberately reinvented itself as a global data and analytics powerhouse, spending tens of billions of dollars in the process and accepting years of depressed returns, shareholder frustration, and activist pressure as the cost of the journey.

The lessons for operators and investors are both specific and universal, and they speak to questions that every board room considering a transformational acquisition should wrestle with.

On integration, the Refinitiv deal illustrates the true cost of tech debt in M&A with painful clarity. When you acquire a business built on decades of unintegrated technology stacks, the sticker price is just the beginning. The real cost is the years of remediation work, the hundreds of millions in annual integration spending, the outages that embarrass your CEO into calling them "completely unacceptable," and the market share erosion that occurs while you are rebuilding the engine in flight. Every acquirer believes they can fix the technology faster than they actually can. LSEG is no exception, and the 6.7 billion pounds in adjusted-away costs stands as a monument to that universal hubris.

On strategy, LSEG's journey validates the thesis that in financial infrastructure, owning the data is always more profitable than facilitating the transaction. The exchange business, matching buyers and sellers, is increasingly a commodity. But the data that flows through the exchange, the indices that benchmark trillions of dollars, the clearing infrastructure that manages counterparty risk, the analytics that inform investment decisions, these are the high-margin, recurring-revenue businesses with genuine switching costs and network effects.

LSEG understood this earlier than most, even if the execution has been messier than the strategy. The company's evolution mirrors a pattern seen across financial infrastructure globally: exchanges that remained pure trading venues have stagnated, while those that pivoted to data, indices, and post-trade services, like Intercontinental Exchange with its acquisition of the NYSE and subsequent data push, have thrived.

The question is whether LSEG paid too high a price for its education.

On capital allocation, the FTSE Russell deal stands out as a masterclass in buy-strip-keep dealmaking. Buying Frank Russell for 2.7 billion, selling the investment management arm for 1.15 billion, and keeping the index business that now generates nearly a billion pounds in annual revenue with massive switching costs and secular growth tailwinds was elegant, decisive capital allocation. It was the kind of deal that looks obvious in hindsight but required real conviction at the time: LSEG paid a premium for an American company in a market segment it had no track record in, and the wisdom of the move only became clear as passive investing exploded over the following decade.

The Refinitiv deal, by contrast, remains a work in progress. The strategic logic was sound but the price was aggressive, the integration burden was underestimated, and the competitive environment has only intensified. Whether it ultimately proves to be brilliant or reckless will depend on execution over the next three to five years.

On the Microsoft partnership, the jury is firmly still out. The vision of embedding financial data into productivity workflows is compelling. The technical challenge of migrating decades of legacy infrastructure to the cloud while maintaining the reliability that financial institutions demand is enormous. Microsoft's board seat and equity stake provide alignment, but alignment is not execution. The partnership needs to produce tangible products that win market share before the 2.8 billion dollar commitment starts to look like an expensive bet on a thesis that never materialized.

As of March 2026, LSEG sits at a crossroads. The integration spending is winding down. The free cash flow is accelerating. Tradeweb is growing faster than ever. FTSE Russell continues to compound. But the stock is down thirty-six percent from its highs, Elliott Management is circling, and the market is demanding proof that the sum of the parts is worth more than the whole.

David Schwimmer has bet his career and LSEG's future on the conviction that a data empire built on three centuries of institutional trust can compete with both Bloomberg's terminal dominance and Silicon Valley's AI ambitions.

The next chapter of this three-hundred-year-old story may be the most consequential yet.

XI. Further Reading & References

-

LSEG 2025 Preliminary Results — Full-year earnings report and segment breakdown, published February 2026 by London Stock Exchange Group.

-

"Sink or Schwim: An LSEG Saga" — The Terminalist's deep analysis of the Refinitiv integration, tech debt challenges, and shareholder returns since the acquisition.

-

European Commission Decision on Deutsche Börse/LSEG Merger (2017) — The antitrust ruling that blocked the third attempted merger and shaped LSEG's subsequent strategic direction.

-

Tradeweb Markets Q4 and FY2025 Financial Results — Tradeweb's full-year earnings demonstrating the twenty-sixth consecutive year of record revenue.

-

"The Big Bang: How the City of London Was Transformed" by David Kynaston — The definitive account of the 1986 deregulation that reshaped London's financial markets.

-

LSEG and Microsoft Strategic Partnership Announcement (December 2022) — Original press release detailing the ten-year partnership, Azure migration, and four percent equity stake.

-

LSEG Annual Report 2024 — Comprehensive financial statements, segment reporting, and management discussion of Refinitiv integration progress.

-

Blackstone/Thomson Reuters Financial & Risk Transaction (2018) — Deal documentation and structure of the consortium acquisition that created Refinitiv.

-

"Trillions" by Robin Wigglesworth — Essential context for understanding the secular trend driving FTSE Russell's index business and the rise of passive investing.

-

Elliott Management's LSEG Investment Thesis (February 2026) — Media reports and analyst commentary on the activist's demands for portfolio review, share buybacks, and Microsoft partnership accountability.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube