Lenzing AG: The Fabric of the Future

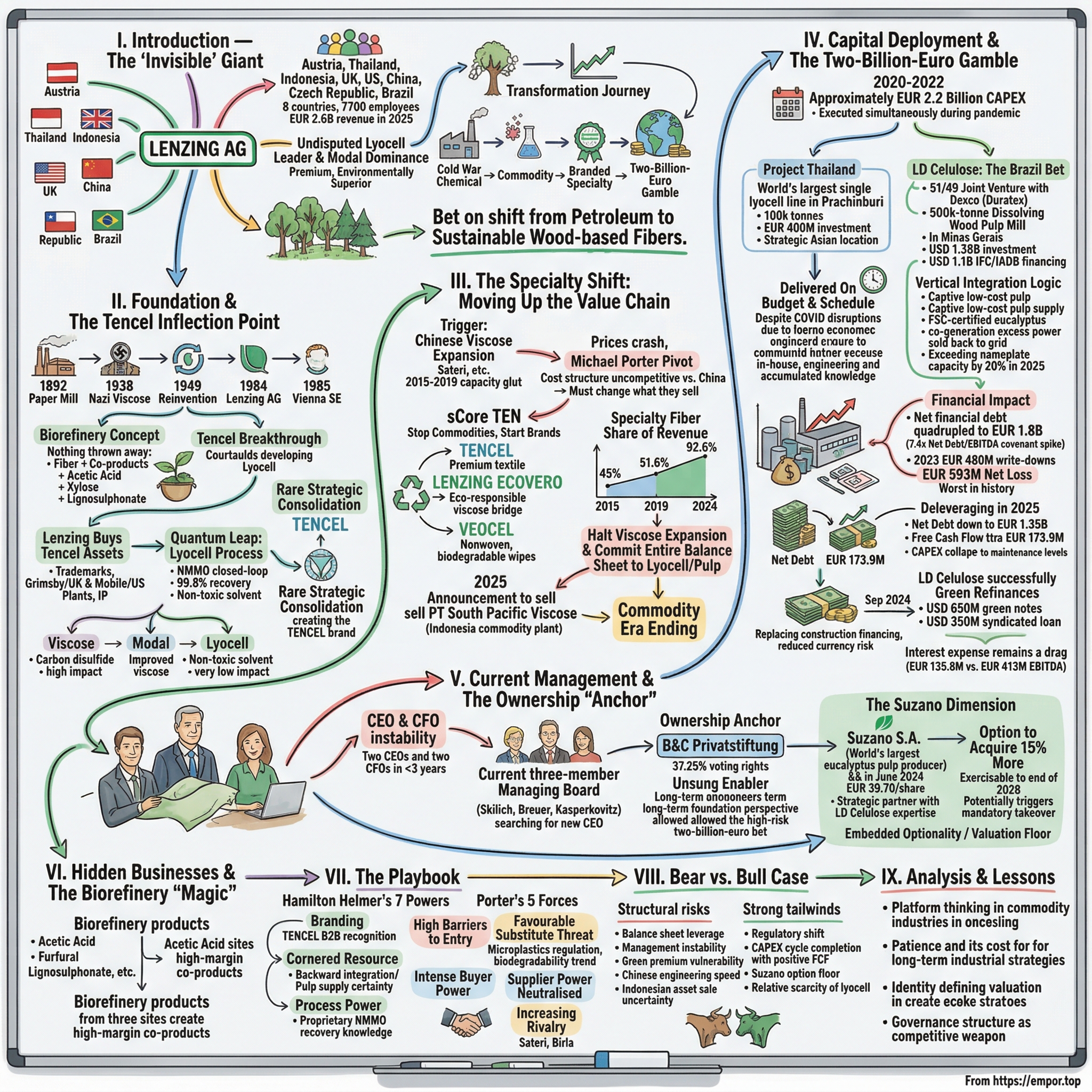

I. Introduction — The "Invisible" Giant (0:00 – 10:00)

Reach into your wardrobe right now. Pull out a shirt—something soft, something that drapes well. Check the label.

If it says "Lyocell," "Modal," or "TENCEL," you are holding a piece of Austrian industrial genius in your hands.

The fiber in that garment started its life as a beechwood or eucalyptus tree. It was dissolved in an organic solvent in a closed-loop process that recovers 99.8 percent of the chemicals used. It was spun into filaments finer than a human hair.

Then it was shipped to a mill in Bangladesh or Vietnam, woven into fabric, dyed, cut, and sewn into the shirt you are now holding. The entire journey—from Alpine forest to garment rack—is one of the most sophisticated industrial supply chains in the world.

And most consumers have no idea it exists.

Most people have never heard of the company that made that fiber. But the fashion industry has.

Every major global brand—from Zara to Lululemon, from H&M to Marks & Spencer—sources fiber from Lenzing AG. With roughly 380 textile brand partners, Lenzing has quietly built what amounts to an "Intel Inside" strategy for sustainable fashion.

The TENCEL hangtag—a small label sewn into a garment that identifies the fiber origin—is one of the very few B2B ingredient brands in textiles that consumers actually recognise and seek out.

When a shopper in a London department store sees that hangtag, a growing number of them associate it with softness, environmental responsibility, and quality. That consumer recognition—for a raw material that is invisible in the finished product—is extraordinarily rare and extraordinarily valuable.

Think about that for a moment. You do not know who manufactured the aluminium in your laptop. You do not know who refined the petroleum in the plastic of your water bottle. But an increasing number of consumers know who made the cellulose fiber in their shirt. That is branding at the molecular level.

Lenzing AG is headquartered in the small town of Lenzing, Upper Austria, population roughly five thousand, nestled between Alpine foothills and the southern shore of Lake Attersee. From this unlikely base—a town so small that the company's factory is the town—the company generated EUR 2.6 billion in revenue in 2025.

It operates production sites across eight countries—Austria, Thailand, Indonesia, the United Kingdom, the United States, China, the Czech Republic, and Brazil—and employs approximately 7,700 people.

It is the undisputed global leader in lyocell fiber and a dominant force in modal—together representing the premium, environmentally superior end of the man-made cellulosic fiber spectrum.

The story of Lenzing is a story about transformation. Not one transformation, but a series of them, each building on the last.

From wartime viscose factory to Cold War–era chemical conglomerate. From commodity fiber producer to branded specialty player. From European manufacturer to global platform. And now, from a company drowning in the debt of a two-billion-euro capital investment cycle to one emerging on the other side with the most vertically integrated, environmentally defensible fiber platform in the world.

The thesis is straightforward: Lenzing bet its entire balance sheet on the conviction that the world's textile industry would be forced—by regulation, consumer preference, and physical reality—to move away from synthetic fibers derived from petroleum and toward cellulosic fibers derived from sustainably managed forests.

That bet is now being tested. The plants are built. The debt is real. And the regulatory tailwinds that Lenzing has been waiting for are finally arriving.

The question is whether the company can survive long enough to collect the payoff—and whether the payoff justifies the price of admission.

II. Foundation & The Tencel Inflection Point (10:00 – 25:00)

The industrial site in Lenzing has roots stretching back to 1892, when Emil Hamburger built a paper mill exploiting local timber and Alpine water.

But the company as it exists today was born in darkness.

In 1938, following the Nazi annexation of Austria, Thuringische Zellwolle AG—a German synthetic fiber company—established Zellwolle Lenzing AG on the site. The establishment was partly achieved by expropriating the Bunzl family's existing paper mill assets. The new factory was designed to produce viscose staple fiber for the German war effort. Production began in September 1939, weeks after the invasion of Poland.

The wartime origins are not a footnote—they shaped the company's identity for decades.

After the war, the Bunzl family's assets were restituted in 1949, and the company embarked on a long process of reinvention. Through the 1950s and 1960s, Lenzing developed expertise in cellulose chemistry that went beyond basic viscose, including partnerships with Courtaulds of Britain and Hoechst of Germany.

The company was renamed Chemiefaser Lenzing AG and eventually Lenzing Aktiengesellschaft in 1984, shedding the last vestiges of its wartime identity. It listed on the Vienna Stock Exchange in 1985.

For a company born from forced industrialisation, the rebranding was not merely cosmetic. It represented a genuine philosophical shift—from a factory that existed to serve a state to a company that existed to innovate for markets. That distinction matters because it explains the R&D culture that would produce Lenzing's most important breakthroughs.

The first genuinely transformative insight came in the 1980s, when Lenzing's engineers began developing what they called the "biorefinery" concept.

The core idea was deceptively simple: a tree is not just cellulose. It is cellulose, hemicellulose, lignin, acetic acid, xylose, furfural, and dozens of other chemical compounds.

Traditional viscose production treated everything except the cellulose as waste. The biorefinery approach treated every component as a potential revenue stream. Nothing was thrown away.

The beechwood that entered the Lenzing factory emerged as fiber, yes—but also as food-grade acetic acid for pickling and preservatives, xylose for low-calorie sweeteners, magnesium lignosulphonate for construction and agriculture, furfural for industrial solvents, and sodium sulfate for detergents.

This zero-waste philosophy became the intellectual foundation for everything that followed.

It embedded sustainability not as a marketing exercise but as an economic imperative—every tonne of wood generated more revenue when every component was captured and sold. The biorefinery was not just good for the environment; it was good for margins.

This is worth pausing on, because it inverts the usual narrative around industrial sustainability. Most companies treat sustainability as a cost—something they do to satisfy regulators or burnish their reputation. Lenzing built a business model where sustainability was the source of margin expansion. The more completely you used the tree, the more money you made. Environmentalism was not the cost of doing business; it was the business.

Meanwhile, across the English Channel, a parallel story was unfolding that would eventually converge with Lenzing's trajectory.

Courtaulds Plc, the British fiber giant, had invested more than GBP 100 million developing a revolutionary new fiber technology. The breakthrough was dissolving cellulose in an organic solvent called NMMO—N-methylmorpholine N-oxide—rather than the toxic carbon disulfide used in viscose production.

The resulting fiber, which Courtaulds branded "Tencel," was produced through a process called lyocell.

The difference between lyocell and viscose is not incremental—it is categorical.

Viscose production generates hazardous carbon disulfide and hydrogen sulfide emissions. Lyocell production uses a non-toxic solvent that is recovered and recycled at rates exceeding 99 percent. The environmental gap is comparable to the difference between a coal plant and a solar farm: the same end product—electricity in one case, cellulose fiber in the other—produced through fundamentally different processes with fundamentally different environmental footprints.

But Courtaulds could not capitalise on its own invention. The company was a victim of the late-1990s conglomerate dismemberment trend. In 1998, Akzo Nobel acquired Courtaulds.

The fiber business was bundled into a division called Accordis, which was subsequently sold to CVC Capital Partners, a private equity firm. CVC attempted to acquire Lenzing in 2001 to consolidate the global lyocell market, but the EU Commission blocked the deal on antitrust grounds—the combination would have created too dominant a position.

The irony is exquisite. European regulators blocked CVC from buying Lenzing because the combination would be anti-competitive. Three years later, Lenzing bought the same assets from CVC anyway—and created the very same combination the regulators had feared. The difference, apparently, was who was doing the buying.

By 2004, CVC was looking for an exit. The Tencel business was underperforming under private equity ownership. And Lenzing was waiting.

On May 4, 2004, Lenzing completed the acquisition that would define its next two decades.

From CVC's holding company, Lenzing purchased the Tencel trademark, the Grimsby production plant in the United Kingdom, the Mobile, Alabama plant in the United States, approximately 80,000 tonnes per year of lyocell capacity, and all associated intellectual property. The price was never publicly disclosed—and multiple industry sources have suggested the valuation was extraordinarily low relative to the strategic value of what was acquired.

Lenzing's own lyocell capacity at the time was approximately 40,000 tonnes per year, produced at a plant in Heiligenkreuz, Austria, that had been operational since 1997. The Tencel acquisition tripled that capacity to roughly 120,000 tonnes overnight—and, critically, consolidated the global branded lyocell market under a single owner.

Before the deal, there were two competing lyocell brands: Courtaulds-era Tencel and Lenzing Lyocell. After the deal, there was one: TENCEL, by Lenzing.

The brand confusion ended. The marketing spend consolidated. And Lenzing gained a ten-year head start over any competitor who might try to develop lyocell capacity from scratch—because the technology, while not impossible to replicate, required decades of process optimisation to achieve the solvent recovery rates and fiber quality that made it commercially viable.

A brief technical aside is warranted here, because understanding the difference between the three main fiber types is essential to understanding Lenzing's competitive position.

Viscose—the oldest technology, dating to the late nineteenth century—dissolves wood pulp in carbon disulfide and caustic soda, creating a viscous solution that is extruded through spinnerets into an acid bath. The process works, but carbon disulfide is toxic, flammable, and produces hydrogen sulfide gas. Environmental compliance costs are high. Chinese producers accept those costs because their regulatory environment allows it. European and North American producers face mounting pressure to either eliminate the process or invest heavily in abatement.

Modal is an improved version of viscose—the same basic chemistry but with modified process parameters that produce a fiber with higher wet strength and softer hand feel. Lenzing's TENCEL Modal uses beechwood from sustainably managed Central European forests and a modified production process with lower environmental impact. It sits in the middle of the quality and sustainability spectrum—better than standard viscose, not as clean as lyocell.

Lyocell is the quantum leap.

The cellulose is dissolved in NMMO, a non-toxic organic solvent. The solution is extruded through spinnerets in a dry-jet wet-spinning process—fibers pass through an air gap and then into a coagulation bath. The NMMO is washed out, captured, purified through multiple stages of filtration and evaporation, and returned to the dissolution stage.

The recovery rate exceeds 99.8 percent—meaning less than 0.2 percent of the solvent is lost per cycle. No carbon disulfide. No hydrogen sulfide. Dramatically lower water consumption. And the resulting fiber is stronger, softer, and more versatile than viscose.

Why does the 99.8 percent matter so much?

Because NMMO is expensive. At industrial volumes—hundreds of thousands of tonnes of fiber per year—even a small drop in recovery translates into millions of euros in additional chemical costs and environmental waste.

Lenzing has been optimising this recovery process since the 1990s—more than thirty years of institutional knowledge in fluid dynamics, filtration chemistry, and evaporation engineering that cannot be purchased off the shelf or licensed from a technology provider. It must be learned, and the learning takes decades.

Consider the math. If a plant produces 100,000 tonnes of fiber per year and uses roughly 1.5 tonnes of NMMO per tonne of fiber, that is 150,000 tonnes of solvent cycling through the system annually. At 99.8 percent recovery, 300 tonnes are lost. At 99.0 percent—still impressive by any industrial standard—3,000 tonnes are lost. At current NMMO prices, the difference in annual chemical costs alone is measured in tens of millions of euros.

That is the moat. Not a patent. Not a trade secret locked in a vault. But thirty years of accumulated operational knowledge embedded in the institutional memory of engineers in a small Austrian town.

The Tencel acquisition gave Lenzing the brand, the technology, and the market position. But it would take another decade before the company fully committed to the specialty strategy that would define its modern identity.

That commitment required a crisis—and the crisis came from China.

It is worth noting how unusual the Tencel deal was in the broader sweep of corporate acquisitions. Most transformative acquisitions in industrial history—Standard Oil buying competitors, InBev acquiring Anheuser-Busch, Mittal acquiring Arcelor—involve one large company buying another large company. The Tencel deal was different. Lenzing did not buy a company. It bought a technology and a brand that had been orphaned by three consecutive owners (Courtaulds, Akzo Nobel, CVC) who never understood what they had.

The history of business is littered with technologies that failed not because the technology was wrong but because the owner was wrong. Xerox PARC invented the graphical user interface and the mouse but failed to commercialise them—Apple did. Kodak invented the digital camera but failed to capitalise on it—everyone else did. Courtaulds invented lyocell but failed to build it into a global brand—Lenzing did. The pattern is the same: the inventor creates the breakthrough, but the commercialiser captures the value.

III. The Specialty Shift: Moving Up the Value Chain (25:00 – 45:00)

Between 2015 and 2019, Chinese viscose producers expanded capacity at a pace that overwhelmed global demand.

Sateri, Tangshan Sanyou, Xinjiang Zhongtai, and a constellation of smaller state-linked manufacturers pushed total Chinese viscose staple fiber capacity from approximately four million tonnes to over 5.1 million tonnes in just four years. By the end of 2018, China's top six producers controlled more than 74 percent of the domestic market.

The price impact was devastating.

Viscose staple fiber prices fell roughly 15 percent below the 2009 cyclical low in nominal terms—approximately 30 percent in real terms by early 2020. For Lenzing, which at that point still derived a significant share of revenue from commodity viscose, the message was brutally clear.

The Chinese producers had structural cost advantages—lower labour costs, state-subsidised energy, less stringent environmental compliance—that made it impossible for a European manufacturer to compete on price alone.

This is the classic Michael Porter scenario: when your cost structure is structurally higher than your competitors' and you cannot lower it, you must change what you sell. Lenzing could not become China. It had to become something China could not replicate.

Lenzing's response was the strategy that management branded "sCore TEN"—a name combining "scoring" (performance), "core" (strengthening fundamentals), and "TEN" for TENCEL.

The essence was simpler than the acronym: stop selling commodities, start selling brands.

The brand architecture took shape rapidly.

TENCEL became the umbrella brand for premium textile fibers—both lyocell and modal varieties. The positioning was clear: if you want the most sustainable, highest-quality man-made cellulosic fiber available, with full traceability and environmental certification, you buy TENCEL.

LENZING ECOVERO, launched in 2017, targeted the eco-responsible viscose segment. It offered a more sustainable version of standard viscose with lower emissions and water usage, backed by EU Ecolabel certification. This was the bridge product—for brands that wanted to improve their sustainability profile but were not yet ready for the full premium of lyocell.

VEOCEL was positioned as the brand for nonwoven applications—biodegradable wipes, hygiene products, medical textiles, and other single-use applications where full biodegradability within thirty days, even in marine conditions, represented a genuine functional advantage over synthetic alternatives.

Three brands, three segments, one underlying technology platform. It was elegant—and it worked.

The de-commoditisation worked faster than anyone expected.

The share of specialty fibers in Lenzing's total fiber revenue climbed from roughly 45 percent in 2015 to 51.6 percent in 2019, hitting the initial target a year early.

By 2024, specialty fibers represented an extraordinary 92.6 percent of fiber revenue.

The commodity business had been almost entirely replaced by branded, premium-priced products. In less than a decade, Lenzing had transformed itself from a company where nearly half its revenue came from commodity fiber sold at Chinese-competitive prices to one where more than nine-tenths came from differentiated, branded products.

That number—92.6 percent—deserves emphasis. It means that out of every hundred euros of fiber revenue Lenzing earns, fewer than eight come from undifferentiated commodity product. The rest carries a brand, a sustainability certification, and a price premium. In an industry where most producers are price-takers selling into a commodity market, Lenzing has achieved a degree of pricing power that is unusual for any manufacturer, let alone one producing raw materials.

But brands alone were not enough. The truly bold strategic decision was the one that followed: Lenzing would halt expansion in standard viscose and bet the company's balance sheet on building massive new lyocell and dissolving wood pulp capacity.

The logic was that lyocell—with its closed-loop process, superior environmental profile, and growing consumer recognition—was the future of man-made cellulosic fiber. And the future required scale. Scale required capital.

And capital, deployed at this magnitude, required conviction that most public companies—answerable to quarterly-focused shareholders—would never have mustered.

In 2025, Lenzing took the specialty thesis to its logical conclusion. The company announced a strategic review of PT South Pacific Viscose, its 220,000-tonne-per-year commodity viscose plant in Purwakarta, Indonesia—effectively putting it up for sale.

An EUR 82.1 million non-cash impairment was booked on the Indonesian operations.

Simultaneously, Lenzing announced more than EUR 100 million in new investment at its Austrian sites through 2027, doubling down on premium fiber production.

The message was unambiguous: the commodity era at Lenzing is ending. The specialty era is all that remains.

But the cost of building that specialty platform nearly broke the company.

The Indonesia impairment is particularly revealing because it demonstrates the irreversibility of the specialty pivot. Once Lenzing committed to TENCEL and lyocell, the commodity viscose business became not just uncompetitive but actively harmful—diluting the brand story, consuming management attention, and depressing group margins. Keeping the Indonesian plant running made sense when viscose was the core business. It makes no sense when viscose is the business you are trying to exit.

This is a pattern familiar to anyone who has studied strategic transitions: the old business does not just become less important—it becomes antagonistic to the new strategy. IBM's mainframe business did not just shrink as cloud computing grew; it actively impeded IBM's ability to pivot to cloud because resources, attention, and organisational identity remained anchored in the legacy business. Lenzing is executing the same transition, and the Indonesia divestiture is the clearest signal that the transition is reaching its terminal stage.

The EUR 200-million-plus cost savings programme—designed by CFO Breuer before his formal appointment—was the operational complement to the strategic pivot. It targeted procurement efficiencies, energy optimisation, headcount rationalisation, and logistics consolidation across the global production network. By end of 2025, the full run-rate savings had been realised. This was not a one-time restructuring charge; it was a permanent reduction in the cost base that improves margins at every volume level.

IV. Capital Deployment & The Two-Billion-Euro Gamble (45:00 – 1:10:00)

Between 2020 and 2022, Lenzing spent approximately EUR 2.2 billion on capital expenditures—the most aggressive investment cycle in the company's history.

Two projects consumed the vast majority of that spending, and both were executed simultaneously, during a global pandemic, through the worst supply chain disruptions in modern industrial history.

That timing was not a choice. Both projects had been years in planning. Construction had begun or was about to begin when COVID-19 hit. To halt construction midway—with foundations poured, equipment ordered, and project financing drawn—would have been as costly as pushing through. So Lenzing pushed through.

Project Thailand

The first project was the construction of the world's largest single lyocell production line in Industrial Park 304, Prachinburi Province, approximately 150 kilometres northeast of Bangkok.

The plant was designed for 100,000 tonnes per year of TENCEL lyocell fiber capacity, with site infrastructure sized for several additional production lines in the future. This was not a modest capacity addition. One hundred thousand tonnes per year from a single line represented a step-change in lyocell production scale—roughly equivalent to the entire capacity Lenzing had acquired from CVC in 2004.

Total investment was approximately EUR 400 million.

Construction began in the second half of 2019, continued through COVID-19 lockdowns and global logistics chaos, and the plant was officially opened in 2022, with first commercial TENCEL shipments in early 2023.

The location was strategic: positioned in the heart of Asia's textile manufacturing region, close to the garment factories in Vietnam, Bangladesh, and Cambodia that consume the fiber. Previously, Asian customers received TENCEL fiber shipped from Austria or the UK—thousands of kilometres and weeks of ocean freight. Thailand put the production within trucking distance of the demand.

The Thai plant was a technical achievement—delivered on schedule and on budget during a pandemic, which is rare for a complex industrial project. It reached full capacity utilisation within its first year of operation.

To appreciate how unusual this is, consider the base rate. According to research by Bent Flyvbjerg at Oxford University, large industrial construction projects are delivered on time and on budget less than 10 percent of the time. Cost overruns of 50 percent or more are common. The Lenzing Thailand plant was delivered within budget and within months of the original timeline—during the most disruptive period for global construction in living memory.

Part of the explanation lies in Lenzing's approach to plant design. The company does not outsource its core process engineering. The lyocell production technology—the spinnerets, the NMMO recovery system, the air-gap spinning process—is designed and specified in-house by Lenzing's engineering teams in Austria. The construction itself is contracted out, but the intellectual core of the plant remains proprietary. This means Lenzing controls the variables that matter most for operational performance—the chemistry, the process parameters, and the equipment specifications.

The Thailand plant also incorporated lessons from decades of operating the Austrian, British, and American facilities. Each successive plant Lenzing builds benefits from the accumulated knowledge of every plant that came before. This is the manufacturing equivalent of compound interest—small improvements in process design, equipment layout, and operational procedures compound over decades into significant performance advantages.

LD Celulose: The Brazil Bet

The second project was far larger, far more complex, and far more consequential for the balance sheet.

LD Celulose was a 51/49 joint venture between Lenzing and Dexco (formerly Duratex), one of Brazil's largest forestry and wood products companies. The project involved building a 500,000-tonne-per-year dissolving wood pulp mill in the Triangulo Mineiro region of Minas Gerais state, surrounded by Dexco's eucalyptus forests.

Total investment was approximately USD 1.38 billion, financed through a USD 1.1 billion package from the International Finance Corporation and the Inter-American Development Bank.

The scale is worth visualising. A 500,000-tonne dissolving wood pulp mill is one of the largest single-site chemical processing facilities one can build. The eucalyptus logs enter at one end. At the other end emerge bales of dissolving wood pulp—snow-white sheets of nearly pure cellulose ready to be dissolved into fiber at Lenzing's production plants around the world.

In between sits a cathedral of chemical engineering: digesters the size of apartment buildings, recovery boilers that capture and burn black liquor to generate steam and electricity, bleaching sequences, and a 144-megawatt clean energy co-generation facility.

Understanding why Lenzing needed a pulp mill in Brazil requires understanding the vertical integration logic.

Dissolving wood pulp is the primary raw material for all of Lenzing's fiber production—lyocell, modal, and viscose alike. Without its own pulp supply, Lenzing was buying on the open market from producers like Sappi, Bracell, and Suzano, at prices that fluctuated with global commodity cycles.

Every spike in pulp prices compressed Lenzing's fiber margins. The cost of raw materials was the single largest variable in the company's profitability—and it was entirely outside management's control.

The Brazil mill was designed to solve that problem permanently.

Captive, low-cost dissolving wood pulp supply from FSC-certified eucalyptus plantations, with a co-generation facility that produces more electricity than the mill consumes. The surplus is sold back to the Brazilian public grid—turning an energy cost into a revenue stream.

Ground work began in 2020. The mill commenced operations in April 2022 and reached near-nominal capacity within the same year.

By 2025, the plant was exceeding its nameplate capacity by roughly 20 percent—producing approximately 600,000 tonnes per year from a mill designed for 500,000.

This kind of over-performance on a greenfield industrial facility is rare and speaks to the quality of the engineering work. It also speaks to the JV partner—Dexco's forestry operations feed the mill with a reliable, sustainably certified wood supply that keeps the digesters running at full throughput.

The pulp feeds Lenzing's own fiber plants globally, with surplus sold as merchant pulp.

The Financial Impact

The financial impact of building two world-scale plants simultaneously was severe.

Net financial debt quadrupled from EUR 410 million at the end of 2020 to EUR 1.8 billion at the end of 2022. The net debt to EBITDA ratio spiked to 7.4 times—a level that triggered covenant concerns and forced the company to raise EUR 392 million in a capital increase in 2023 to maintain compliance.

The equity ratio dropped from 45.8 percent to 37.8 percent.

To put this in perspective: 7.4 times leverage is the kind of ratio you see in highly leveraged buyouts, not in industrial companies listed on European stock exchanges. Lenzing had effectively LBO'd itself—except instead of buying another company, it had built two factories from scratch.

In 2023, Lenzing booked approximately EUR 480 million in non-cash write-downs on the Thailand and Brazil assets, reflecting the gap between construction cost and fair market value in a challenging macro environment.

The result was a net loss of EUR 593 million—the worst in the company's history.

The write-downs were painful for existing shareholders. But they also represented a financial reset—booking the investment losses upfront, strengthening the balance sheet on a go-forward basis, and positioning the company to generate returns on assets carried at lower book values.

By 2025, the deleveraging trajectory was clear.

Net debt declined to EUR 1.35 billion. Net debt to EBITDA improved to 3.3 times. Free cash flow turned decisively positive at EUR 173.9 million. Capital expenditure collapsed to EUR 141 million—maintenance levels.

The company shifted from building mode to harvesting mode.

In September 2024, LD Celulose refinanced its original project finance with USD 650 million in green notes and a USD 350 million syndicated term loan—replacing the construction financing with longer-term capital on more favourable terms.

The refinancing was a milestone: it signalled that credit markets viewed the Brazil operation as a stable, cash-generating asset rather than a risky construction project. When investment banks are willing to write green notes against your industrial facility, the market is telling you something about asset quality.

The "green" designation itself is significant. Green bonds carry specific requirements—the proceeds must fund projects with measurable environmental benefits, and the issuer must report on impact metrics. The fact that LD Celulose qualified reflects the facility's environmental profile: FSC-certified wood supply, self-generated clean energy, surplus electricity exported to the grid, and dissolving wood pulp that enables the production of biodegradable fibers replacing petroleum-based synthetics. The entire value chain, from eucalyptus plantation to fiber, has a measurable carbon footprint advantage over the polyester supply chain it competes against.

For Lenzing, the Brazil refinancing also reduced a key risk: currency mismatch. LD Celulose generates revenue in US dollars (dissolving wood pulp is globally traded in USD) but operates in Brazil with costs denominated in Brazilian reais. The original IFC/IADB financing was structured in USD, which provided a natural hedge. The new green notes and term loan maintain that USD denomination, preserving the hedge and avoiding the reais exposure that has bedevilled other foreign investors in Brazilian infrastructure.

Interest expense in 2025 was EUR 135.8 million—a massive drag on a company with EUR 413 million in EBITDA. Roughly one euro in three of operating profit goes to servicing debt. The company has not generated a net profit since 2021—four consecutive years of net losses.

Management's target is to reduce net debt to EBITDA below 2.5 times, but achieving that requires both continued debt reduction and EBITDA expansion.

The gamble has been placed. The cards have not yet been fully turned over.

V. Current Management & The Ownership "Anchor" (1:10:00 – 1:30:00)

If the capital investment cycle was Lenzing's greatest strategic gamble, the management turnover that accompanied it has been its greatest governance challenge.

The company has cycled through two CEOs and two CFOs in less than three years. For a company executing one of the most complex industrial transformations in European manufacturing, this level of leadership instability is deeply unusual—and concerning.

Stephan Sielaff joined Lenzing as CTO and COO in March 2020 and was elevated to CEO. His background was in chemicals and industrial efficiency—he held a Master of Engineering from the University of Dortmund, with stints at Unilever, Symrise, and Archroma, the Swiss specialty chemicals company where he served as COO from 2014 to 2020.

Sielaff's mandate was to execute the Thailand and Brazil projects while maintaining operational discipline. He departed by mutual agreement on August 31, 2024. The circumstances were never fully disclosed, but the timing—shortly after the record write-downs and capital raise—suggests a board that held its CEO accountable for the financial consequences of the investment cycle, even if the strategic logic remained sound.

Rohit Aggarwal, who had served as Chief Fiber Officer, was promoted to CEO on September 1, 2024. His tenure lasted less than five months.

He resigned for personal reasons effective January 31, 2026, though he will serve as an advisor through September 2026. An internal promotion to the top job followed by a resignation within five months is not the kind of leadership transition that inspires confidence—regardless of the stated reasons.

As of April 2026, Lenzing has no CEO.

The company is run by a three-member Managing Board: Christian Skilich as Chief Pulp Officer and CTO (mandate extended to May 2029); Mathias Breuer as CFO (from January 1, 2026, having previously designed the EUR 200-million cost reduction programme); and Georg Kasperkovitz as COO.

A six-member Executive Committee supplements the board with commercial leadership. The Supervisory Board is actively searching for a new CEO.

The CFO transition was equally consequential. Nico Reiner, who navigated the company through the covenant crisis and capital raise since January 2023, chose not to extend his mandate. His replacement, Breuer, brings an operational finance profile focused on cost reduction rather than capital markets—suggesting the board sees the current phase as one requiring execution discipline rather than financial engineering.

That assessment is probably correct. The era of raising capital and building plants is over. The era of running them efficiently, paying down debt, and extracting returns has begun. A CFO who designed a EUR 200-million cost reduction programme is arguably better suited to this phase than one who managed a capital raise.

The Foundation

The ownership structure above all of this is the most important feature of Lenzing's governance—and the primary reason the company was able to pursue its two-billion-euro capital programme.

B&C Privatstiftung—a foundation established in December 2000 by Bank Austria AG and Creditanstalt AG—controls 37.25 percent of Lenzing's voting rights.

As a Stiftung, B&C has no owners. It is governed by trustees legally bound to pursue the foundation's stated purpose: promoting Austrian entrepreneurship and safeguarding the long-term profitability and growth of its portfolio companies. B&C's philosophy is industrial continuity over short-term shareholder returns—keeping Lenzing's headquarters, production, and core R&D in Austria.

This governance structure is the unsung enabler of everything Lenzing has achieved.

Imagine pitching the following to a typical institutional investor in 2019: "We are going to spend EUR 2.2 billion building two factories simultaneously, during a pandemic, in Thailand and Brazil. Our leverage will spike above seven times EBITDA. We will need to raise emergency equity. We will book the largest loss in company history. But in five to seven years, we will have the most vertically integrated, environmentally certified fiber platform in the world."

No PE-backed, no activist-shadowed, no quarterly-earnings-obsessed company would have approved that pitch. B&C did—because foundations think in decades, not quarters.

The Suzano Dimension

In June 2024, a new shareholder entered the picture.

Suzano S.A.—the world's largest eucalyptus pulp producer, headquartered in São Paulo, Brazil—acquired 15 percent of Lenzing's voting rights from B&C at EUR 39.70 per share, approximately EUR 230 million. Suzano received two Supervisory Board seats.

More significantly, Suzano holds an option to acquire an additional 15 percent from B&C, exercisable from one year after closing through the end of 2028. If exercised, this purchase would trigger a mandatory takeover offer under Austrian law—because the combined B&C-Suzano syndicate would see Suzano's effective influence rise to a level requiring a public bid.

The combined B&C and Suzano syndicate holds 52.25 percent of voting rights, with B&C retaining sole control within the syndicate. Goldman Sachs Group holds approximately 9.87 percent of shares, with the remainder in free float.

The Suzano investment is the most strategically significant ownership change at Lenzing in a generation.

Suzano is not a financial investor. It is a strategic partner with deep knowledge of eucalyptus forestry and dissolving wood pulp production—precisely the expertise needed to optimise LD Celulose's performance.

The option for the additional 15 percent creates embedded optionality for shareholders: at the current share price of EUR 24.90, significantly below Suzano's EUR 39.70 entry price, the possibility of a premium takeover bid provides downside support that most small-cap industrial stocks lack.

Put differently: the world's largest pulp company paid EUR 39.70 per share less than two years ago. The stock today trades at EUR 24.90. Either Suzano dramatically overpaid—which is possible but unlikely for a company with deep expertise in the underlying industry—or the market is mispricing Lenzing.

Sustainability targets carry a 20 percent weighting in the long-term incentive programme. Lenzing claims to be the only regenerated cellulosic fiber producer with a scientifically confirmed net-zero target—a 90 percent reduction in absolute Scope 1, 2, and 3 emissions by 2050, validated by the Science Based Targets initiative.

VI. Hidden Businesses & The Biorefinery "Magic" (1:30:00 – 1:50:00)

Lenzing reports three segments—Division Fiber, Division Pulp, and Others—but the real business architecture is more nuanced, and some of the most interesting value creation happens where investors look least.

The Fiber Engine

The Fiber Division generated approximately EUR 1.9 billion in revenue in 2025, with total fiber sales volumes of roughly 904,000 tonnes.

Within this, textiles account for approximately 64 percent of fiber revenue and nonwovens for approximately 36 percent. The specialty fiber share has reached 92.6 percent—an extraordinary concentration in branded, premium-priced products.

The textiles business—primarily TENCEL lyocell and TENCEL modal—is the core engine.

TENCEL has achieved something rare in B2B industrial marketing: genuine consumer recognition. When a shopper sees the TENCEL hangtag, a growing percentage know what it means and are willing to pay a premium.

That consumer pull creates demand that flows backward through the supply chain—from brand to garment factory to fabric mill to fiber producer. It is the "Intel Inside" model applied to textiles.

The analogy to Intel is not casual. Intel spent decades and billions of dollars building a component brand that consumers demanded even though they never interacted with the component directly. Nobody opens their laptop to admire the processor. But "Intel Inside" influenced purchasing decisions because it signalled performance and reliability. TENCEL functions identically: nobody sees the fiber in their shirt, but the hangtag signals sustainability and quality.

The VEOCEL Opportunity

But the segment deserving more investor attention is nonwovens—the VEOCEL brand.

Nonwoven fibers are used in products most consumers use daily without thinking: facial wipes, baby wipes, feminine hygiene products, medical dressings, industrial cleaning cloths.

The vast majority of these products today are made from synthetic fibers—polyester and polypropylene—that do not biodegrade.

A synthetic wipe flushed down a toilet persists in the environment for centuries. It accumulates in sewage systems, creating the infamous "fatbergs" that plague urban water infrastructure. A cellulosic wipe made from VEOCEL fiber biodegrades fully within thirty days, even in marine conditions.

This biodegradability is not just a marketing claim—it is becoming a regulatory requirement.

The EU Single-Use Plastics Directive restricts synthetic fibers in single-use products. EU Regulation 2023/2055 restricts intentionally added microplastics. The forthcoming Ecodesign delegated acts for textiles, expected around 2027, will address microfiber shedding from polyester and nylon garments.

Each of these regulatory frameworks mechanically expands the addressable market for biodegradable cellulosic fibers. Twenty-three brand partners in Europe and North America were co-branding with VEOCEL by 2024.

The nonwovens market is particularly attractive because it is consumable rather than durable. A shirt lasts years. A wipe is used once and discarded. The repeat purchase cycle is days or weeks, not years. This creates higher-velocity demand and more predictable revenue streams.

The market size for nonwoven wipes alone exceeds USD 20 billion globally, and cellulosic fibers represent a small but rapidly growing share. If municipal wastewater authorities—who spend billions annually clearing fatbergs from sewers—succeed in pushing regulations that mandate biodegradable wipes, the shift from synthetic to cellulosic could accelerate dramatically. Several European municipalities are already moving in this direction.

For Lenzing, nonwovens also offer a pricing dynamic that differs from textiles. In textiles, Lenzing competes against the full spectrum of fibers—cotton, polyester, viscose. In nonwovens, the primary competition is synthetic polymers that face existential regulatory risk. The pricing power in a market where your competitors' products are being regulated out of existence is structurally superior to pricing power in a market where your competitors merely offer an inferior product.

The Biorefinery Value Stream

The biorefinery products represent a genuinely hidden value stream.

Lenzing operates biorefineries at three sites: Lenzing in Austria, Paskov in the Czech Republic, and LD Celulose in Brazil.

When wood is cooked to extract cellulose, the non-cellulose components are captured, purified, and sold as co-products.

The product list reads like a chemistry set: biobased acetic acid at food-grade quality. Furfural for refining lubricating oil. Magnesium lignosulphonate for construction and agriculture. Xylose for low-calorie sweeteners. Sodium sulfate for detergents. Soda ash for industrial use. All biocertified. The company claims 100 percent utilisation of wood constituents.

Specific biorefinery revenue is not separately disclosed.

But the economics are structurally attractive: high-margin, low-capital-intensity revenue with near-zero marginal cost. The chemicals are inherent in the wood and the recovery infrastructure is already built.

As pulp volumes scale—particularly from Brazil, where production now exceeds nameplate capacity by 20 percent—biorefinery revenues should scale proportionally.

The beauty of the biorefinery model is that it turns cost centres into profit centres. In a traditional pulp mill, the non-cellulose components of wood are waste that must be managed and disposed of. In Lenzing's biorefinery, those same components are revenue streams. The waste disposal cost becomes negative—the company gets paid to take it away.

The Pulp Division

The Pulp Division serves a dual purpose: captive supply to Lenzing's own fiber plants plus merchant market sales.

Dissolving wood pulp sales volumes rose 27 percent year-over-year in 2025 as LD Celulose hit its stride.

The merchant pulp sales provide a revenue buffer when fiber demand softens—Lenzing can sell more pulp externally rather than let the mill sit idle. This optionality—switching between captive use and merchant sales depending on market conditions—provides a degree of margin management flexibility that few competitors enjoy.

TreeToTextile

In February 2026, Lenzing took a controlling stake in TreeToTextile, a Swedish innovation company developing next-generation sustainable fiber technology.

The investment positions Lenzing at the frontier of cellulosic fiber innovation—exploring production methods that could further reduce energy consumption and chemical usage. It is a modest financial commitment with potentially significant strategic implications.

TreeToTextile is essentially Lenzing's hedge against its own technology becoming obsolete. If a better way to turn trees into textiles emerges, Lenzing wants to own it—not compete against it.

This approach mirrors what the smartest technology companies do with potentially disruptive innovations. Google did not wait for a competitor to build a better search engine—it acquired YouTube, Android, and DeepMind. Intel did not wait for ARM to disrupt x86—though arguably it moved too slowly. Lenzing, by taking a controlling stake in TreeToTextile, is ensuring that the next generation of cellulosic fiber technology, whatever form it takes, remains within its ecosystem.

The broader "Others" segment also includes Lenzing's engineering services division, which licenses process technology and provides technical consulting to third-party fiber producers. This may seem paradoxical—why help potential competitors?—but it reflects a pragmatic calculation: if the cellulosic fiber market is going to grow, it is better for Lenzing to earn licensing revenue from competitors using its technology than to have those competitors develop their own, potentially superior, alternatives. It is the same logic that led ARM to license its chip designs to everyone: if the market is going to exist regardless, better to be the platform it runs on.

VII. The Playbook: Hamilton's 7 Powers & Porter's 5 (1:50:00 – 2:10:00)

Hamilton Helmer's 7 Powers framework reveals three durable competitive advantages at Lenzing.

Power 1: Branding

The first is Branding. TENCEL is one of the very few B2B fiber brands with genuine consumer recognition.

The analogy to Intel Inside is apt—an ingredient brand that creates consumer pull in a market where the ingredient is invisible in the final product. No one sees the fiber in their shirt. But the TENCEL hangtag conveys softness, sustainability, and quality.

That brand equity took decades to build, cannot be replicated quickly, and creates a pricing premium that commodity producers cannot capture.

Sateri may be building lyocell capacity at pace, but building a consumer-facing ingredient brand is fundamentally different from building a factory. Factories can be built in two years. Brands take twenty.

Power 2: Cornered Resource

The second is a Cornered Resource: access to FSC and PEFC certified wood at scale, combined with the LD Celulose backward integration.

Lenzing's pulp supply chain—captive eucalyptus plantations in Brazil feeding a 500,000-plus-tonne dissolving wood pulp mill—provides cost certainty and sustainability certification that merchant-market buyers cannot match.

The wood is FSC-certified. The energy is self-generated. The surplus electricity is sold to the grid.

This supply chain cannot be replicated by writing a cheque. It requires forestry concessions, environmental permits, years of plantation development, and a billion-dollar facility. The time-to-capability gap is measured in decades.

Power 3: Process Power

The third power is Process Power: the proprietary lyocell solvent recovery system.

The 99.8 percent NMMO recovery rate is the result of more than thirty years of continuous process optimisation. This accumulated know-how is not documented in a patent that expires. It lives in the institutional knowledge of Lenzing's process engineers, in the specific configurations of equipment, and in operating procedures refined across millions of production hours.

A competitor building a new lyocell plant will start at a lower recovery rate and need years of operational learning to approach Lenzing's performance. Every percentage point of lower recovery translates directly into higher chemical costs and lower margins.

Process power is perhaps the most underappreciated competitive advantage in industrial markets because it is invisible. There is no patent to point to, no brand logo, no regulatory barrier. There is just the accumulated institutional knowledge of how to run a chemical process slightly better, year after year, decade after decade. It is difficult to measure, impossible to steal, and prohibitively expensive to replicate.

Porter's Five Forces

Porter's Five Forces paint a mixed but fundamentally favourable picture.

Barriers to Entry are high. A world-scale lyocell plant costs EUR 400 million or more. The dissolving wood pulp supply chain requires billion-dollar investments. Environmental certifications take years. Co-marketing relationships with 380 global fashion brands cannot be built overnight. New entrants face a multi-year, multi-billion-dollar programme before they can compete at scale.

Threat of Substitutes runs in Lenzing's favour. The primary substitute—polyester—does not biodegrade, sheds microplastics, and faces tightening EU regulation. Recycled polyester, while better than virgin, still sheds microplastics and does not biodegrade at end of life. Cotton competes on naturalness but requires enormous water and land—approximately 10,000 litres of water per kilogram, versus a fraction of that for lyocell. The structural trend favours cellulosics over synthetics.

Bargaining Power of Buyers is the primary competitive challenge. Lenzing's customers are global fashion brands with enormous purchasing power—Inditex, H&M, Lululemon—and multiple sourcing options. They can and do play fiber suppliers against each other on price. The TENCEL brand mitigates this—a brand with its own consumer following gives the supplier leverage—but Lenzing is still subject to buyer concentration dynamics.

Bargaining Power of Suppliers has been substantially neutralised by LD Celulose. Before the Brazil mill, Lenzing was exposed to volatile dissolving wood pulp prices. With captive supply, that exposure has been dramatically reduced. Lenzing has gone from being a price-taker in its most important raw material market to being largely self-sufficient.

Competitive Rivalry is intense and increasing.

Sateri opened a 100,000-tonne lyocell mill in Nantong, China in late 2023 and is targeting significant further expansion. Birla Cellulose, part of Aditya Birla Group's Grasim Industries, is the world's largest viscose producer and building its own lyocell capacity.

Chinese state-linked producers are scaling lyocell lines. The lyocell market is no longer Lenzing's monopoly.

But Lenzing retains advantages in brand recognition, environmental certification, process efficiency, and backward integration that no single competitor currently matches across all dimensions. Sateri has scale but lacks the brand. Birla has the brand ambition but lacks the process maturity. Chinese producers have cost advantages but lack the certifications Western brands increasingly require.

The competitive moat is not any single factor—it is the combination of all of them. This is what Helmer would call a "power bundle"—multiple reinforcing advantages that are individually formidable but collectively almost impossible to replicate.

Consider what a competitor would need to match Lenzing's position: EUR 400 million for a lyocell plant. USD 1.4 billion for a pulp mill. Two decades of process optimisation to achieve competitive solvent recovery. Ten years of brand building to create consumer recognition. Environmental certifications that take years to obtain. Co-marketing relationships with hundreds of global brands that take years to establish.

The total investment required—in capital, time, and organisational capability—exceeds USD 5 billion and two decades. No competitor is attempting all of this simultaneously. They are picking pieces: Sateri has the plant but not the brand. Birla has the ambition but not the backward integration. Chinese state producers have the scale but not the certifications.

This fragmented competitive landscape is Lenzing's greatest protection. As long as no single competitor assembles the full stack, the pricing premium holds.

VIII. Bear vs. Bull Case (2:10:00 – 2:25:00)

The Bear Case

The bear case starts with the balance sheet.

Net financial debt stands at EUR 1.35 billion against EUR 413 million in EBITDA—a leverage ratio of 3.3 times, well above the company's target of below 2.5 times.

Interest expense consumed EUR 135.8 million in 2025—nearly a third of EBITDA. Four consecutive years of net losses have eroded the equity base from EUR 2.1 billion to EUR 1.36 billion. The equity ratio at 29.6 percent provides limited cushion.

If a cyclical downturn in textile demand coincides with higher-for-longer interest rates, the combination of depressed EBITDA and elevated interest expense could force another capital raise. The dilution of 2023 is still fresh in shareholders' memories.

The management instability is concerning. Two CEOs in eighteen months, two CFOs in three years, and no current CEO.

A controlling shareholder that cannot retain a chief executive raises questions about board-management dynamics. Is the Supervisory Board micromanaging? Is the compensation uncompetitive? Are operational targets unrealistic? The market does not know, and that uncertainty itself carries a cost.

The competitive threat from Sateri is real. If Sateri's lyocell capacity reaches scale and its certifications satisfy global fashion brands, the TENCEL premium could narrow.

The "green premium" that consumers pay is vulnerable to economic downturns—when retailers face margin pressure, sustainability premiums are often the first to be squeezed. A recession that forces brands to prioritise cost over sustainability would hit Lenzing's pricing power directly. The 2008 financial crisis and the 2020 COVID shock both demonstrated that sustainability commitments are the first casualty of margin compression. Brands that proudly proclaimed their sustainable sourcing strategies in boom times quietly reverted to cheaper suppliers when revenues fell.

There is also the question of whether the lyocell technology advantage is as durable as the bull case assumes. While Lenzing has thirty years of process optimisation behind it, the basic chemistry of lyocell is well understood and published in academic literature. The NMMO solvent process is not protected by active patents—the original Courtaulds patents have long since expired. What remains is know-how, not intellectual property in the legal sense.

Chinese chemical engineering capabilities are formidable and improving rapidly. If a Chinese producer dedicates sufficient engineering talent and investment to optimising lyocell production—as Chinese companies have done in solar panels, batteries, and high-speed rail—the process power gap could narrow faster than the bull case assumes. The question is not whether Chinese producers can learn to make lyocell—they already can. The question is how quickly they can close the efficiency gap on solvent recovery.

Finally, the EUR 2.6 billion revenue figure flatters the underlying economics. A significant portion of that revenue comes from the Pulp Division selling merchant dissolving wood pulp at commodity prices. Strip out the merchant pulp sales and the effective fiber revenue—the high-margin, branded business that the bull case rests on—is smaller than the headline suggests.

The Indonesian situation adds uncertainty. PT South Pacific Viscose, the 220,000-tonne commodity viscose plant under strategic review, may prove difficult to sell in a market where Chinese producers dominate commodity viscose. If the sale fails, Lenzing is stuck operating a declining asset that drags on group margins and management attention.

The Bull Case

The bull case rests on three structural pillars.

First, the regulatory tailwind is arriving.

The EU Single-Use Plastics Directive, the microplastics restriction under REACH, and the forthcoming Ecodesign delegated acts are systematically disadvantaging synthetic fibers and mechanically expanding the market for biodegradable cellulosic alternatives.

Lenzing, with its EU Ecolabel certification, Digital Product Passport-ready fiber identification technology, and full suite of sustainability credentials, is arguably the most compliance-ready fiber producer in the world.

As regulation tightens, brands will need certified, traceable, biodegradable fiber. Lenzing is first in line. The EU is not doing this as a favour to Lenzing—but the effect is the same. Every regulation that restricts polyester expands the addressable market for lyocell.

Second, the capital expenditure cycle is over.

The plants are built. The EUR 2.2 billion in cumulative investment is done. Capex has collapsed to maintenance levels. Free cash flow is positive and growing.

Every euro of revenue that flows through the Thailand and Brazil assets does so at near-zero incremental capital cost. The operating leverage is enormous: as utilisation rises and pricing improves, margin expansion flows almost entirely to the bottom line and to debt reduction.

This is the classic post-capex-cycle inflection point. The pain of building is over. The reward of operating should follow—if the demand is there.

Third, the Suzano option creates a valuation floor.

Suzano paid EUR 39.70 per share for its initial 15 percent—the current share price of EUR 24.90 represents a 37 percent discount to what the world's largest pulp company paid less than two years ago.

If Suzano exercises its option for the additional 15 percent, it triggers a mandatory takeover offer.

The strategic logic of a Suzano-Lenzing combination—the world's largest pulp producer merging with the world's leading specialty fiber producer—is compelling. Suzano supplies the raw material. Lenzing converts it into the highest-value end product. The vertical integration synergies would be substantial.

This embedded optionality provides downside protection that most small-cap industrials lack.

There is a fourth element to the bull case that deserves mention: the sheer scarcity of what Lenzing offers.

The global textile market consumes approximately 113 million tonnes of fiber per year. Of that, polyester accounts for roughly 57 percent—about 64 million tonnes. Cotton accounts for roughly 24 percent. Man-made cellulosic fibers—viscose, modal, and lyocell combined—account for roughly 6 percent, or about 7 million tonnes.

Within that 7 million tonnes, lyocell represents a small fraction—probably less than one million tonnes globally. Lenzing's share of global lyocell production is dominant.

If the regulatory and consumer trends that favour cellulosic over synthetic fibers continue—and there is considerable evidence that they will—the bottleneck is not demand but supply. There is simply not enough lyocell production capacity in the world to absorb even a modest shift away from polyester. Every percentage point of the global fiber market that shifts from polyester to cellulosics represents roughly 640,000 tonnes of new demand.

Lenzing, with its world-scale plants already built and operating, is one of the very few producers positioned to capture that demand growth without requiring significant new capital investment. The plants are built. The capacity is available. The only question is whether the demand will come—and regulation is ensuring that it does.

IX. Analysis & Lessons (2:25:00 – 2:40:00)

The first lesson from Lenzing is about platform thinking in commodity industries.

The company took a fiber—a physical product competing in a global commodity market against lower-cost Chinese producers—and turned it into a platform by co-marketing with brands.

The TENCEL hangtag is not just a label; it is a distribution system for trust. When a brand attaches it to a garment, it borrows Lenzing's sustainability credibility. When a consumer sees it, they receive a quality signal the brand alone might not convey.

The fiber becomes a platform for reputation transfer—and that platform justifies a pricing premium the physical product alone never could.

The second lesson is about patience—and its cost.

Building a dissolving wood pulp mill in Brazil and a lyocell plant in Thailand simultaneously, during a pandemic, with payoff horizons measured in decades, is the kind of investment only a company with a patient controlling shareholder can execute.

B&C's foundation structure—no owners, no exit pressure—provided the governance backbone. Most listed companies would have been forced to halt or scale back when COVID struck, supply chains collapsed, or the equity ratio dipped below 30 percent. B&C held firm.

The cost of that patience was borne by minority shareholders—through dilution, write-downs, and four years without a net profit. Whether the eventual payoff justifies that cost remains the central question.

The third lesson concerns identity.

Is Lenzing a chemical company? A textile company? A sustainability IP shop? The answer is probably all three, which makes it difficult for the market to value.

Chemical multiples undervalue the brand premium. Textile multiples overweight consumer cyclicality. Sustainability multiples are speculative. Lenzing trades at roughly 7 times trailing EBITDA—a valuation reflecting the market's uncertainty about which category this company belongs to.

Companies that defy categorisation often trade at discounts until the market finds a framework. For Lenzing, that framework may not arrive until the balance sheet normalises and net profits return—at which point the valuation discount may close rapidly.

There is a fourth lesson, perhaps the most subtle: the relationship between governance structure and strategic ambition.

Lenzing's two-billion-euro bet was only possible because B&C is a foundation, not a fund. A pension fund would have demanded quarterly returns. A private equity owner would have demanded an exit timeline. An activist investor would have demanded a capital return programme. None of these governance structures would have tolerated four years of net losses, a capital raise, and a leverage ratio above seven times.

Only a foundation—with no owners, no exit pressure, and a mandate measured in perpetuity rather than fund cycles—could provide the governance stability needed for an investment with a twenty-year payoff horizon.

This is not an argument that foundation ownership is always superior. It has costs: slower decision-making, potential for complacency, limited external accountability. But for companies pursuing long-duration industrial strategies—where the payoff horizon exceeds the typical fund lifecycle—foundation ownership provides a structural advantage that no other governance model can match.

The Austrian Stiftung model, in this context, is not a corporate governance curiosity. It is a competitive weapon.

Key Performance Indicators

For investors tracking Lenzing's ongoing performance, two KPIs cut closest to the business trajectory.

EBITDA margin measures whether the specialty pivot is translating into profitability. The current 15.9 percent is improving but remains below what a branded, de-commoditised business model should eventually deliver.

If Thailand and Brazil are running at high utilisation, specialty fiber share is above 90 percent, and EBITDA margin is not expanding toward the high teens or low twenties, the specialty premium is not being captured. Watch this number quarterly.

Net debt to EBITDA measures the pace of deleveraging. The current 3.3 times is above the 2.5-times target. The trajectory of this ratio—driven by both EBITDA expansion and absolute debt reduction—determines how quickly Lenzing transitions from a company burdened by its investment history to one with the financial flexibility its competitive position warrants.

If EBITDA margin expands to 20 percent on EUR 2.6 billion in revenue—EUR 520 million in EBITDA—and debt declines to EUR 1.2 billion, the ratio drops to 2.3 times. That is the scenario where the investment thesis is validated.

Lenzing sits at a peculiar crossroads.

The assets are world-class. The competitive position is defensible. The regulatory environment is increasingly favourable. The balance sheet is stressed but healing. The management team is incomplete.

And the fundamental question—whether the world will pay a premium for fibers from forests rather than oil wells—is being answered, slowly and unevenly, in Lenzing's favour.

The company is, in many ways, a microcosm of the broader industrial transition that the twenty-first century demands. The old economy ran on petroleum, linear supply chains, and disposable products. The new economy runs on renewable feedstocks, closed-loop processes, and biodegradable materials. Lenzing has bet its entire existence on the proposition that this transition is real, irreversible, and accelerating.

If that proposition is correct—and the evidence from EU regulation, consumer surveys, brand sustainability commitments, and physical reality suggests it is—then Lenzing's current share price reflects the cost of building the platform, not the value of operating it. The cost is known and quantified: EUR 2.2 billion in capital expenditure, EUR 1.35 billion in net debt, four years of net losses. The value remains to be proven—but the assets are in place, the technology works, the brand is established, and the regulatory wind is at the company's back.

Whether the market recognises this before or after Suzano exercises its option may determine whether current shareholders participate in the upside or merely observe it from the sidelines. The clock on that option runs through the end of 2028—giving Suzano, and by extension the market, roughly two and a half years to decide whether the world's most integrated cellulosic fiber platform is worth more than what the equity market currently says it is.

X. Epilogue & References

- Lenzing AG Annual and Sustainability Reports (2020–2025), available at reports.lenzing.com

- Lenzing FY2025 results announcement, March 2026

- Tencel Group acquisition, May 4, 2004

- sCore TEN strategy documentation

- LD Celulose JV press releases (2020–2025); refinancing September 2024

- Thailand Prachinburi plant opening, 2022

- Suzano 15% stake acquisition, June 11, 2024 (closed August 30, 2024)

- B&C Privatstiftung mission statement and governance framework

- EU Single-Use Plastics Directive (SUPD)

- EU Regulation 2023/2055 on microplastics (REACH Annex XVII, Entry 78)

- Ecodesign for Sustainable Products Regulation (ESPR)

- Sielaff departure, August 2024; Aggarwal resignation, January 2026

- PT South Pacific Viscose strategic review and EUR 82.1M impairment, 2025

- TreeToTextile controlling stake, February 2026

- Courtaulds / Accordis / CVC Capital Partners historical documentation

- Lyocell process technology: Lenzing.com and ScienceDirect references

- EU Commission Decision blocking CVC/Lenzing merger, 2001 (Case COMP/M.2187)

- Global fiber market data: Textile Exchange Preferred Fiber and Materials Market Report 2025

- Bent Flyvbjerg, "Over Budget, Over Time, Over and Over Again" (Oxford University)

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube