The Domestic Colossus: The Story of Lloyds Banking Group plc

I. Introduction & Episode Roadmap

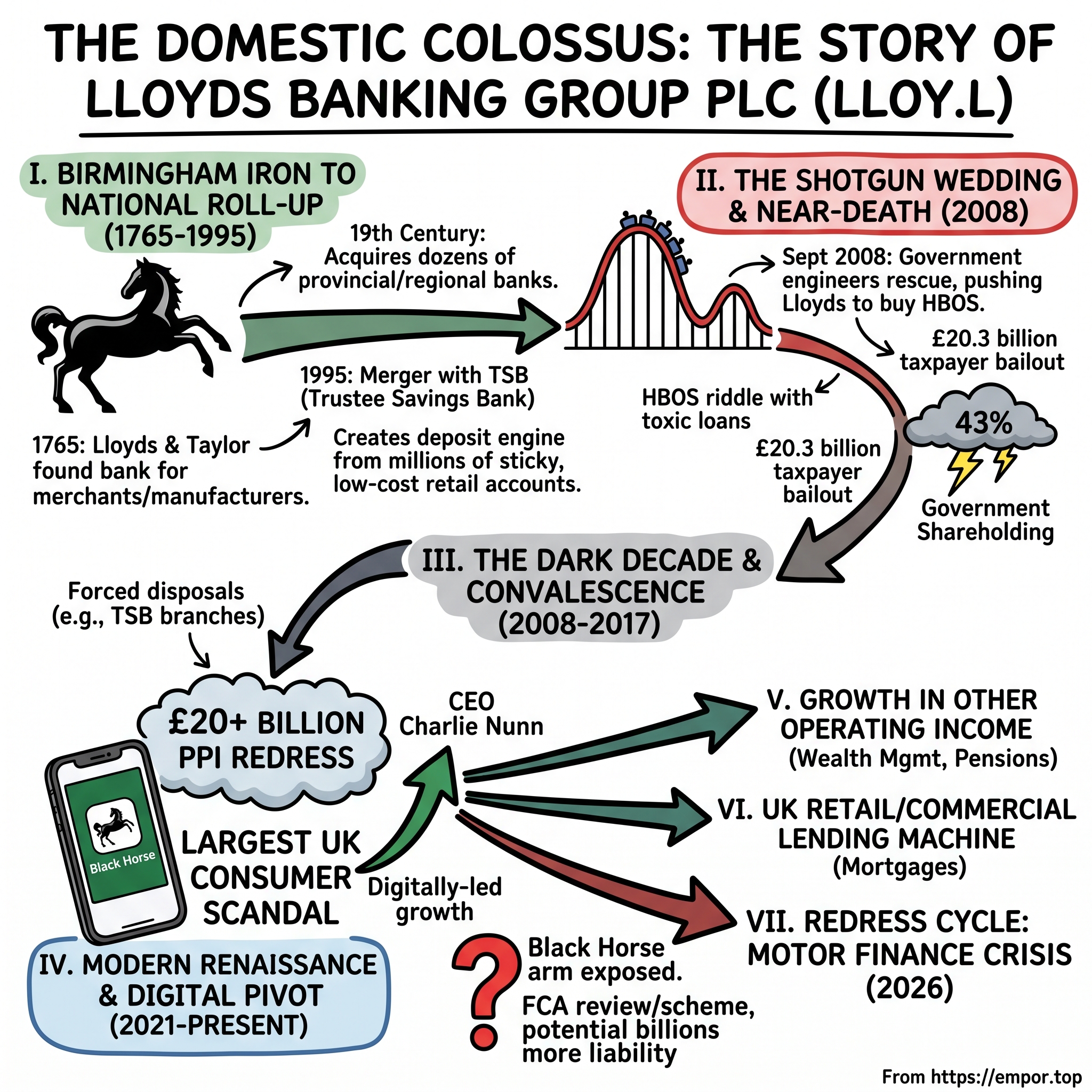

Picture a black horse. Not a real one, but the galloping silhouette that has hung over British high streets for more than a century — the emblem of a bank so woven into the fabric of the United Kingdom that roughly one in three Britons keeps money with it, borrows from it, or insures their life through it. Now ask a harder question. How does an institution that began in 1765 as a side business for a Birmingham iron merchant and a button maker end up controlling close to a fifth of every new mortgage pound lent in Britain, serving over 26 million customers, and running what is by active-user count the largest digital bank in the country?

That is the paradox at the heart of Lloyds Banking Group, and it is worth naming up front, because it defines everything. Lloyds is not Barclays, with its swashbuckling Wall Street trading floor. It is not HSBC, which earns most of its money in Hong Kong and books London almost as an afterthought. Lloyds is something rarer and, in its way, more revealing: an almost pure bet on a single economy. It has no meaningful global investment bank. It has virtually no operations outside the United Kingdom. Strip away the branding and Lloyds is a giant, leveraged, deposit-funded wager on whether British households can pay their mortgages and whether British companies can service their loans. If the UK economy sneezes, Lloyds catches a cold. If the UK housing market booms, Lloyds prints money.

This is a story with four acts, and each one teaches a different lesson about banking.

The first is the roll-up — a century and a half of patient provincial acquisition, in which a Quaker partnership swallowed dozens of small regional banks and eventually merged, in 1995, with the Trustee Savings Bank to build the deposit engine that still powers the group today.

The second is the near-death — the moment in September 2008 when the British government effectively marched Lloyds into a shotgun wedding with HBOS, a fast-growing mortgage lender that turned out to be riddled with toxic loans. That single decision converted the most conservative bank on the high street into a ward of the state, requiring a £20.3 billion taxpayer bailout and a 43% government shareholding.7

The third is the dark decade — the long convalescence under state ownership, the forced disposals, and the surreal spectacle of Lloyds paying out more than £20 billion to customers it had mis-sold payment protection insurance, the single largest consumer-redress event in British financial history.

And the fourth, the one we are living through as of mid-2026, is the modern renaissance — CEO Charlie Nunn's attempt to convert a chastened post-crisis utility into a digitally-led growth machine, cashing in on a decade-high interest-rate environment, even as a fresh regulatory storm blows in from an unexpected direction: motor finance, where Lloyds' Black Horse arm has become the single most exposed lender in a nationwide redress scheme that could ultimately rival PPI in scale.4

Three themes will recur. The first is the illusion of diversification — how a bank with three divisions and dozens of brands is, in economic substance, one enormous interest-rate and UK-credit trade. The second is the structural power of low-cost retail deposits — the quiet, boring current account that is the real crown jewel here. And the third is the inevitability of the redress cycle — the uncomfortable truth that UK consumer finance seems to manufacture a mass mis-selling scandal roughly once a generation, and that a bank this big will always be the largest target.

A word, too, on the posture of this telling. Lloyds is a formidable company with a genuinely dominant franchise, and it would be easy to write its recent history as a triumphant recovery narrative — the plucky survivor that paid back the taxpayer with interest and rebuilt itself into a digital champion. Much of that is true. But the job here is not to applaud; it is to weigh. A dominant deposit franchise and a strong capital return record sit alongside a concentrated one-country risk profile and an unresolved multi-billion-pound regulatory liability, and an honest account holds all of those in view at once. Where management says it will win, we will ask what evidence supports the claim and what could prove it wrong. With that established, let us begin where the black horse first appeared: in the smoke of the Industrial Revolution.

II. Birmingham Iron, Provincial Roll-Ups, and the TSB Merger (1765–1995)

In 1765, Birmingham was the loudest place in England. It was the forge of the Industrial Revolution — a town of hammers, furnaces, and workshops turning out buttons, buckles, guns, and the iron that fed the coming age of steam. Into this din stepped two men: Sampson Lloyd, an iron merchant from a Quaker family, and John Taylor, a manufacturer who had made a fortune in gilt buttons and enamelled snuff boxes. Together they opened a bank. It had no branches, no marble hall, no galloping horse — just a partnership and a ledger.

Here is the thing modern readers miss about eighteenth-century banking: it had almost nothing to do with what we now call retail customers. There were no current accounts for ordinary families, no debit cards, no mobile apps. A bank like Lloyd's existed to grease the machinery of trade. It discounted bills of exchange, extended credit to manufacturers, and helped the merchants of the Midlands finance the iron, coal, and steam power that were remaking the world. The bank was, in effect, embedded in a supply chain. Its fortunes rose and fell with the workshops of Birmingham. That DNA — a bank as the financial plumbing of the real economy rather than a casino of its own — would prove remarkably durable.

The nineteenth century turned Lloyds from a local partnership into a national institution, and it did so through a strategy that would look entirely familiar to any private-equity roll-up artist today. In 1865, the bank converted from a private Quaker partnership into a joint-stock company, giving it access to shareholder capital. And then it went shopping. Over the following decades Lloyds absorbed dozens of regional and family-owned banks scattered across the English countryside — the kind of small, undercapitalised local banks that were vulnerable to the periodic panics that swept Victorian finance. Each acquisition brought new deposits, new customers, and a new town on the map. By the early twentieth century, Lloyds had rolled itself up into one of the "Big Five" clearing banks that dominated British high-street finance, a position it has essentially never relinquished.

The pattern here is worth dwelling on, because it recurs throughout the whole Lloyds story. Growth by acquisition is the house style. When it works — buying solvent regional banks at sensible prices during a fragmented era — it compounds beautifully into scale and density. When it goes wrong, as it spectacularly would in 2008, it can nearly kill the institution. The same corporate instinct produced both outcomes.

There is a lovely piece of iconography buried in this history that tells you something about how banking brands are built. The galloping black horse that adorns every Lloyds branch and card is not a modern marketing invention; it is one of the oldest trade signs in British finance, inherited through acquisition from a London goldsmith-banker whose premises on Lombard Street had displayed it since the seventeenth century. When Lloyds absorbed that firm, it absorbed the symbol too, and it has ridden with the bank ever since. That is the roll-up strategy distilled into a logo: Lloyds did not so much invent its identity as accumulate it, buying up the heritage, deposits, and trust of institutions older and smaller than itself, and welding them into something national. Trust in banking is not manufactured overnight; it is compounded across generations, and a symbol that has meant "safe" for three centuries is worth more than any advertising budget.

For a period in the twentieth century, Lloyds did flirt with the wider world — it built an international arm with operations reaching into Latin America and beyond, chasing the growth that overseas lending seemed to promise. But those adventures ended badly, most painfully in the Latin American debt crises of the 1980s, which inflicted heavy losses and seared into the institution a lasting suspicion of foreign lending. Long before the post-2008 retreat made "pure-play UK bank" a virtue of necessity, Lloyds had already learned, the hard way, that its comparative advantage lay at home. The retrenchment of the 2010s was in that sense a return to type, not a departure from it.

The most consequential deal of the modern era, before the catastrophe, came in 1995, when Lloyds Bank merged with the Trustee Savings Bank to form Lloyds TSB. The deal was arranged as a takeover dressed as a merger, and it capped a period in which Lloyds, under chief executive Sir Brian Pitman, had reoriented the entire company around a single, almost heretical idea for its time: that the point of a bank was not to grow its balance sheet as large as possible, but to maximise the return it earned on shareholders' equity. Pitman was, in a sense, the first modern Lloyds executive, drilling into the organisation a discipline about capital and returns that would echo in every strategy document the group has published since. The TSB merger was the pure expression of that philosophy — not empire-building for its own sake, but the acquisition of the cheapest, stickiest funding base in the country to power a high-return domestic machine. To understand why this mattered, you have to understand what TSB was. The trustee savings banks had grown out of a nineteenth-century social movement to encourage thrift among the working class — humble institutions where labourers, servants, and clerks could safely deposit their modest savings. By the late twentieth century that heritage had produced something enormously valuable: a vast, granular base of small, loyal, ultra-sticky retail deposits, spread across millions of ordinary households who rarely moved their money.

For a bank, that is close to the ideal raw material. Deposits from millions of small savers are cheap — you pay little or no interest on them — and they are stable, because no single depositor's departure matters and inertia keeps most of them in place for years. Lloyds brought to the marriage its strength in middle-market commercial lending and corporate risk management. TSB brought the deposit engine. The combined Lloyds TSB became a money-printing machine on the high street, consistently posting some of the best cost-to-income ratios in the sector. It was, by the standards of the late 1990s and early 2000s, boringly, enviably profitable. That reputation for conservative, deposit-funded prudence is exactly what makes the next chapter so shocking — because it is the story of how the most cautious bank in Britain made the most reckless decision of them all.

III. The Shotgun Wedding: The HBOS Disaster of 2008

Every disaster needs a protagonist who believes he is the hero. In the story of 2008, that role belonged not to Lloyds but to its future victim: HBOS, the brash mortgage giant that spent the early 2000s making Lloyds look like a fusty relic.

HBOS was itself a product of merger. In 2001, Halifax — Britain's largest former building society, a mortgage-lending powerhouse that had demutualised and floated on the stock market — combined with the venerable Bank of Scotland to create HBOS. On paper it was a marriage of the biggest mortgage brand in the country with one of the oldest names in British banking. In practice it became something more dangerous: a growth machine with its foot flat on the accelerator. Where Lloyds funded its lending with sticky retail deposits, HBOS increasingly funded its explosive mortgage and commercial-property growth by borrowing in the wholesale money markets — that is, by relying on other banks and institutions to lend it short-term cash, which it then lent out long. It pushed hard into commercial real estate development and highly leveraged buyouts, exactly the kind of lending that looks brilliant in a boom and lethal in a bust. HBOS was, in the language of the day, the disruptor. It was taking share. And it was doing it on a funding model that assumed the wholesale markets would always be open.

The warnings had been there, and they had been ignored — which is what makes the HBOS story a genuine tragedy rather than mere bad luck. Inside the bank, a head of group regulatory risk named Paul Moore had raised alarms years earlier that the sales culture was running ahead of the risk controls, that the machine was growing faster than it could safely be managed. He was removed from his post. His warnings, aired publicly only after the collapse, became one of the defining "we told you so" moments of the crisis. The lesson is one every investor should internalise: in the late stages of a lending boom, the people warning that growth is unsafe are usually right and usually unpopular, and the market rewards the optimists right up until the moment it annihilates them.

Then, in September 2008, the wholesale markets slammed shut. The collapse of Lehman Brothers triggered a global seizure in funding: banks stopped trusting one another, and the short-term money that HBOS depended on to roll over its obligations simply vanished. A bank that had borrowed short to lend long, without a deep cushion of sticky deposits, was suddenly staring at operational insolvency — not in months, but in hours. HBOS shares went into freefall as depositors and counterparties bolted. It was, in the most literal sense, a bank running out of cash to open its doors.

What happened next is one of the most extraordinary episodes in British corporate history. Rather than let HBOS fail outright and detonate a panic across the entire banking system, the government of Prime Minister Gordon Brown engineered a rescue by pushing it into the arms of the one large British bank still seen as strong: Lloyds TSB. Competition law, which would normally have blocked a merger that handed one institution such a dominant share of UK mortgages and current accounts, was set aside in the name of financial stability. Lloyds' chairman Sir Victor Blank and chief executive Eric Daniels were persuaded that they were being offered the deal of a lifetime — the chance to acquire the nation's premier mortgage franchise at a crisis discount, creating an unassailable retail champion.

They were catastrophically wrong, and the reason is a masterclass in the dangers of deal-making under duress. The due diligence was rushed, conducted at speed in the middle of a market meltdown, with the government urging haste. Lloyds' management saw the Halifax brand and the mortgage book; what they underweighted was the rot inside HBOS's corporate and commercial-property loan portfolio and the sheer size of its wholesale funding hole. They believed they were buying a jewel at a discount. They were in fact buying a balance sheet whose true losses would, over the following years, obliterate Lloyds' own hard-won capital strength.

There is a governance detail here that active investors should never forget, because it is the kind of thing that repeats. The deal was so obviously advantageous to Lloyds' management's ambitions — and so clearly enabled by a government waving away the competition rules that would normally have blocked it — that the board's critical faculties appear to have been overwhelmed by the opportunity. The prize of becoming an unassailable national champion was dangled, the political pressure was intense, the timetable was compressed, and the ordinary discipline of "walk away if the numbers don't add up" evaporated. Lloyds' own shareholders were asked to approve the acquisition, and they did, in late 2008 — a reminder that even sophisticated institutional owners can be swept up in a narrative of once-in-a-lifetime opportunity. When a deal is framed as a patriotic rescue and a strategic coup at the same time, the hardest thing in the world is to say no.

Was it, in the cold verdict of M&A history, an overpay? Emphatically yes — not on the sticker price, which was modest, but on the hidden liabilities that came bolted to it. The comparison with peers is damning. Barclays, staring at the same crisis, refused the government's capital and instead raised money privately, avoiding both nationalisation and the worst of the toxic acquisitions; it even picked over the carcass of Lehman Brothers to buy clean US investment-banking assets cheaply. HSBC, funded by its vast Asian deposit base, rode out the storm without a UK bailout. Lloyds, the conservative one, the deposit-rich prudent one, made the single most value-destructive acquisition of the entire crisis — and in doing so converted itself from rescuer into casualty. The bill for that miscalculation would be paid not by Eric Daniels, but by British taxpayers, and it would come due within months.

IV. Under the State's Shadow: Nationalization and the £20 Billion PPI Nightmare (2008–2017)

By January 2009, the arithmetic was brutal and public. The combined weight of HBOS's souring loans was crushing the newly formed Lloyds Banking Group, and no amount of management optimism could paper over the hole. The bank that had been positioned as a pillar of strength needed rescuing itself. The government stepped in with capital, and step by step the state's ownership climbed until the taxpayer held roughly 43% of the enlarged group, having injected £20.3 billion to keep it standing.7 The most cautious bank on the high street was now, in effect, an arm of HM Treasury.

The rescue did not come in a single clean cheque, either, which is why the episode was so corrosive to confidence. It came in stages, as the true depth of the HBOS losses revealed itself quarter after grinding quarter — each new disclosure of impaired commercial-property loans and bad corporate credit forcing another injection, another dilution, another lurch downward in the share price. Lloyds initially agreed to enter a government insurance scheme designed to cap losses on its worst assets, then, as its position clarified, negotiated its way out of it through a colossal capital-raising, tapping existing shareholders for billions to stand on its own feet rather than sink deeper into state dependence. That decision — to raise private capital and claw back independence rather than accept a larger government safety net — was arguably the first genuinely shrewd move of the crisis era, and it set the template for the disciplined, capital-focused recovery that followed.

State ownership came with strings, and they were tight. Because the bailout counted as state aid under European Union competition rules, Brussels demanded a pound of flesh: Lloyds was forced to carve out a chunk of its own body and set it free to restore competition. A network of hundreds of branches was ordered to be hived off to restore competition on the high street. Lloyds' first attempt to offload them — a plan to sell the package to the Co-operative Bank — collapsed in some embarrassment when the buyer's own finances imploded, forcing Lloyds to instead float the branches on the stock market as a resurrected TSB in 2014, before that entity was swiftly swallowed by Spain's Banco Sabadell the following year. The government's rescue had, ironically, forced Lloyds to give back some of the very scale the HBOS deal was supposed to deliver — and the botched Co-op sale was an early sign that carving a living business out of a banking giant is far messier than a regulator's tidy diagram suggests. There is a lesson buried here for any acquirer that dreams of building an unassailable monopoly: get too dominant, and the regulator will simply amputate the excess.

Into this wreckage, in 2011, walked the man who would define Lloyds' recovery: António Horta-Osório, a Portuguese banker poached from Santander UK, where he had built a reputation as a relentless, detail-obsessed operator. His playbook was ruthless in its clarity. Simplify the bank. Kill complexity. Prune the sprawling international footprint that Lloyds had accumulated over the decades — exiting dozens of countries — and refocus every ounce of energy on the one thing Lloyds actually understood: UK retail and commercial banking. Cut costs relentlessly. Rebuild capital. This was the moment Lloyds consciously chose to become the pure-play domestic bank it remains today. The "no international investment bank, no overseas adventures" identity that we described at the outset is not an accident of history; it was a deliberate strategic retreat, chosen in the ashes of 2008 and executed with discipline over the following decade.

But even as Horta-Osório shrank and simplified, a second monster was rising from Lloyds' past — and this one had nothing to do with HBOS. It was payment protection insurance, or PPI. For years, British banks had aggressively sold PPI alongside loans, credit cards, and mortgages: a product supposedly designed to cover repayments if a borrower fell ill or lost their job, but frequently sold to people who could never claim on it, often without their informed consent, and at extraordinary margins. When regulators and the courts finally ruled that this constituted mass mis-selling, the industry faced a compensation bill of a scale no one had imagined. PPI became the largest consumer-finance scandal in British history, and Lloyds — the biggest retail bank, with the biggest back book of sold policies — was the biggest payer of all, ultimately setting aside more than £20 billion in redress and administration costs, well over half of the entire industry's liability.

Sit with that number for a moment, because it explains a great deal about the modern company's psychology. Twenty billion pounds is not a rounding error; it is a decade-long drain of cash that might otherwise have gone to rebuilding capital and paying shareholders. PPI, layered on top of the HBOS losses, is why Lloyds' recovery took as long as it did, and why its management became so allergic to risk and so obsessed with conservative provisioning. It is also, as we will see, the ghost that haunts every conversation about motor finance today: investors who lived through PPI learned never to trust a bank's "final" estimate of a redress bill.

The mechanics of how the state actually exited are themselves instructive, because they were the opposite of the panicked entry. Rather than dump its enormous shareholding on the market in one destabilising block, the government sold its Lloyds stake gradually over several years through a carefully managed trading plan — dribbling shares into the market day after day, in quantities small enough not to crater the price. It was patient, unglamorous financial engineering, and it worked. The share overhang that might have depressed Lloyds' valuation for years was instead worn down steadily until it disappeared.

The long night finally ended in May 2017. The government sold its last remaining shares, fully returning Lloyds to private ownership. In a rare happy footnote to a crisis rescue, the Treasury recouped its entire £20.3 billion — and, counting dividends and share sales, walked away with around £900 million more than it had put in, a modest but symbolically important profit for taxpayers.78 Lloyds emerged from state ownership stripped down, chastened, and clean: a streamlined, pure-play UK banking utility. The survival phase was over. The question now was whether a bank that had spent a decade in intensive care could learn to grow again — and that question would fall to a new captain.

V. The Pivot to Charlie Nunn: A Digital-First Strategy & Rebuilding OOI (2021–Present)

When Charlie Nunn took the helm in August 2021, he inherited a bank that had finished bleeding but had not yet learned how to run. His predecessor had stopped the patient dying; Nunn's job was to make it move. And Nunn's background hinted at how he intended to do it. He was not a career high-street banker in the mould of the men who ran Lloyds during the crisis. He had spent years as a partner at McKinsey, then risen at HSBC to run its global wealth and personal banking business — a role steeped in two ideas that would define his Lloyds strategy: digital distribution at scale, and the pursuit of fee income from managing customers' wealth rather than merely lending them money.

Before assessing the strategy, it is worth being clear-eyed about how Nunn is paid, because incentives reveal intent. In May 2026, shareholders approved a new directors' remuneration policy, and under it Nunn was granted a long-term incentive award of 6,685,044 ordinary shares, a package that in outperformance scenarios — where the share price climbs substantially — could push his total remuneration toward the high teens of millions of pounds.10 The structure is where it gets interesting. The bulk of those shares, 75%, cannot vest for three years and then must be held for a further two; the remaining quarter is locked up for four years.10 Vesting is tied to hard 2026–2028 performance conditions: return on tangible equity, the cost-to-income ratio, and sustainability targets. On paper, this is exactly the kind of long-dated, performance-gated pay design that governance advocates ask for — it forces the CEO to care about where the bank is in 2028, not just next quarter. A skeptic would note two things, however. First, share-price-linked upside in a bank is heavily a bet on the interest-rate cycle, which no CEO controls; a rising rate environment can make management look brilliant regardless of execution. Second, the very metrics being rewarded — RoTE and cost-to-income — are the ones management itself guides the market to, creating a closed loop worth watching.

On capital allocation, the record so far has been genuinely disciplined, and this is the strongest evidence in management's favour. For the 2025 financial year, Lloyds returned roughly £3.9 billion to shareholders, combining ordinary dividends — a final dividend of 2.43 pence per share — with a share buyback of up to £1.75 billion, all funded by strong underlying capital generation rather than by leveraging up the balance sheet.1 The bank ended 2025 with a common equity tier 1 capital ratio of 14.0%, comfortably above its own target, and signalled its intent to keep grinding that surplus back to owners as it converges toward a target ratio of around 13.0% by the end of 2026.1 Returning capital while holding a fortress balance sheet is precisely what a post-crisis bank should do, and Lloyds has done it consistently. The open question, which the motor finance section will confront directly, is whether that generosity is sustainable if a redress bill balloons.

The growth strategy itself carries a simple three-word banner: Grow, Focus, Change.

Grow is about rebuilding what the bank calls "other operating income" — the capital-light fee revenue that does not depend on the interest-rate cycle. The crown jewel of this effort is the push into mass-affluent wealth management: targeting the millions of UK customers who hold somewhere between roughly £50,000 and £250,000 in investable assets, who are wealthy enough to matter but not rich enough to be fought over by private banks. Lloyds has been consolidating and rebranding its wealth and investment operations under the Lloyds banner, with the aim of cross-selling investments, pensions, and retirement products to customers who already bank with it. The strategic logic is sound: Lloyds already owns the customer relationship and the transaction data; converting a current-account holder into a fee-paying investment client is far cheaper than acquiring one. The evidence that it is working, however, remains thin relative to the ambition — this is a business Lloyds is trying to build, not one it has already won, and it is competing against entrenched investment platforms and nimble fintechs for exactly the same wallets.

Focus is the less glamorous, more certain half of the plan: shrinking the physical estate. Lloyds has continued to close hundreds of branches as customer behaviour migrates to screens, ripping cost out of expensive high-street real estate. This is not a growth story; it is a margin story, and it is one of the more reliable levers management holds.

Change is the technology bet — pouring investment into digital platforms and, increasingly, generative AI, which management has framed as a driver of meaningful value in 2026 and beyond. The scale here is Lloyds' genuine structural advantage: the group counts tens of millions of active digital users and mobile-app customers, giving it a per-user technology efficiency that a small challenger bank simply cannot match. When you can spread a billion-pound annual technology budget across a customer base that large, each incremental digital feature costs a fraction per head of what it costs a rival with a tenth of the users. That, more than any wealth-management aspiration, is the durable edge.

It is worth pausing on the credibility of this whole transformation, because Nunn's strategy is not the first time a Lloyds chief executive has promised to modernise the bank and lift returns, and a neutral observer should grade management on delivery rather than PowerPoint. The honest scorecard, several years in, is mixed but leans positive. The concrete, controllable pieces — branch closures, cost discipline, capital returns — have been executed largely as promised, and the guidance discipline on capital generation and distributions has been good; management has broadly hit the return-of-capital targets it set. The softer, more ambitious pieces — the leap in fee income from wealth, the reinvention of Lloyds as a growth company rather than a spread lender — remain works in progress that the numbers do not yet vindicate. A fair verdict is that this is a management team that reliably delivers on the things it can control and talks a bigger game on the things it cannot yet prove. That is a meaningfully better profile than the overpromising of the pre-crisis era, but it is not the same as having earned the benefit of the doubt on the growth story. The wealth transformation is a hypothesis, and as of mid-2026 the market is right to treat it as one.

One vivid, over-covered sideshow deserves a brief mention precisely because it is so often oversold: Lloyds Living, the group's own build-to-rent and shared-ownership housing business, formerly branded Citra Living. The idea of a bank becoming a landlord captures headlines, and Lloyds has built partnerships with housebuilders and now manages several thousand homes. But set against a balance sheet of well over £450 billion in assets, a portfolio of a few thousand rental properties is a rounding error — strategically interesting as a hedge and a toehold in the housing ecosystem, financially immaterial today. It is a good example of the discipline this article demands: size the story to the money, and do not let a photogenic side project distract from where the profits actually come from. And where they come from is the machine we turn to next.

VI. Inside the Machine: Retail & Commercial Banking Economics

Strip away the brands, the app, the wealth ambitions and the landlord experiments, and Lloyds is really three businesses stacked on one enormous pool of cheap deposits. The first half of 2025 lays the proportions bare, and the numbers tell you exactly where the profit engine lives.11

The Retail division is the beating heart. In the six months to June 2025 it generated net income of roughly £5,279 million — close to 60% of the group total — and underlying profit of about £1,974 million, or around 55% of the group's underlying profit.11 This is the mortgage-and-current-account machine: home loans under the Halifax, Lloyds and Bank of Scotland brands, credit cards, personal loans, and the mass of everyday current accounts that fund the whole enterprise. Commercial Banking, serving UK small and mid-sized companies, contributed the next largest slice — net income of about £2,688 million, roughly 30% of the total, and underlying profit near £1,194 million, about a third of the group's profit.11 And Insurance, Pensions & Investments — the wealth generator, the business Nunn wants to grow — remained comparatively small, at net income of around £611 million and underlying profit of roughly £144 million, a single-digit share of the group.11

Read those proportions carefully and a truth jumps out that undercuts some of the corporate narrative: for all the talk of diversifying into capital-light fee income, Lloyds today is overwhelmingly a lender, and overwhelmingly a mortgage lender. The wealth business is a promise about the future, not a pillar of the present. That is not a criticism — it is simply the reality an investor must price.

Now, why is a bank funded by ordinary current accounts such a good business when interest rates are high? The answer is a concept called the net interest margin, and it is worth explaining slowly because it is the single most important number in the whole company. Imagine Lloyds holds hundreds of billions of pounds in current accounts on which it pays customers little or no interest — money that just sits there because people rarely move their main account. Now imagine the Bank of England raises its base rate to fight inflation. Lloyds can invest or lend that near-free money at the higher market rate, charging borrowers more for mortgages while still paying depositors almost nothing. The gap between what it earns on its assets and what it pays for its funding is the net interest margin, and in a high-rate world that gap widens into a gusher of profit. Bankers call the reluctance of deposit rates to rise in step with the base rate the "deposit beta" — the lower it is, the more the bank keeps for itself.

That structural hedge deserves its own moment, because it is one of the least understood but most important features of the modern Lloyds profit engine. Left to its own devices, a bank funded by no-interest current accounts would see its income swing violently with the base rate — feast when rates are high, famine the instant they fall. To smooth that ride, Lloyds invests a large slice of its deposit base into a laddered portfolio of fixed-rate assets, staggered so that only a fraction matures each year and gets reinvested at whatever the prevailing rate happens to be. The effect is to average out interest income over a multi-year horizon, like a homeowner who fixes portions of their savings at different times. In a rising-rate world the hedge is a slight drag, because older, lower-yielding tranches are still rolling off. But in a falling-rate world it becomes a powerful shock absorber: even as new rates drop, the bank keeps earning the higher yields locked in years earlier. This is the single biggest reason Lloyds' earnings will not fall off a cliff the moment the Bank of England cuts — and it is why management can talk about rising structural-hedge income even in a year when the base rate is expected to decline.

The recent figures show the whole mechanism in full flow. Lloyds' banking net interest margin reached 3.06% across 2025 and climbed further to 3.17% in the first quarter of 2026, up fourteen basis points year on year, helping drive a statutory pre-tax profit of £2.0 billion for that single quarter and net income of £4.8 billion, up 9%.12 On the back of it, management raised full-year 2026 net interest income guidance to above £14.9 billion, citing higher-for-longer rate expectations and rising income from the structural hedge.2 The upgrade is telling: it signals that management sees the income tailwind persisting even as consensus expects rates to ease, precisely because the hedge is now reinvesting maturing tranches at yields well above the depressed levels of the 2010s.

There is a second half to the profitability equation that the net interest margin alone can hide, and a careful investor keeps one eye on it at all times: credit quality. A bank can report a fat margin and a rising profit while, unseen, the loans on its book quietly deteriorate. The measure to watch is the impairment charge — the money Lloyds sets aside each quarter to cover loans it expects to go bad. Through 2025 and into 2026, those charges have stayed modest, reflecting a UK economy that, while sluggish, has not tipped into the kind of unemployment surge or house-price crash that turns mortgages sour. That benign credit environment is doing a lot of quiet work in the strong headline numbers. It is also, crucially, not something management controls — it is a gift of the macro cycle, and it is the first thing that would reverse in a downturn. When commentators call Lloyds a "housing-market proxy," this is the mechanism they mean: the group holds a mortgage book of several hundred billion pounds, and the value of that book — and the losses hidden within it — moves with the health of British households. In good times the impairment line flatters the results; in bad times it is where the pain arrives first and hardest.

But the very mechanism that makes Lloyds a money-printer in good times contains its own poison, and management knows it. It is called deposit migration. When savings rates across the market climb, customers eventually notice that their current account pays them nothing while a savings account pays several percent — and they start shifting their money. Every pound that moves from a zero-interest current account to a higher-yielding savings account raises Lloyds' cost of funding and squeezes that precious margin. So the net interest margin is not a permanent gift; it is a balance between customer inertia (which favours the bank) and customer greed (which does not). Watching whether that migration accelerates is one of the most important things an investor in Lloyds can do.

Which brings us to the arena where Lloyds' scale is most visible: the UK mortgage market, an oligopoly dominated by a handful of giants. Lloyds sits unambiguously at the top. In 2024 it wrote around £47 billion of gross mortgage lending, lifting its market share to 19.4% — comfortably the largest in the country.9 Behind it, the landscape shifted dramatically: Nationwide Building Society, having completed its £2.3 billion purchase of Virgin Money, vaulted into second place with roughly 17.3% share, overtaking NatWest, which slipped to around 11.2%.9 Santander UK remains a persistent price competitor, with Barclays and HSBC UK fighting over the more premium end. Together the big lenders control the clear majority of the market.

What is striking is how Lloyds wins. It does not, generally, win on price — in a market where borrowers compare two-year and five-year fixed rates to the last basis point, competing on rate alone is a race to the bottom that compresses everyone's margins. Lloyds wins on distribution and data: the Halifax brand in particular functions as the great gateway for first-time buyers, funnelling millions of new borrowers into the group, while decades of transaction history let Lloyds price risk with an information edge a challenger cannot replicate. Scale begets data, data begets better underwriting, better underwriting begets scale. It is a quietly powerful loop. But it is a loop built on one enormous, undiversified bet — that British borrowers keep paying — and in 2026 a very different kind of bill arrived for a corner of the lending book almost no one outside the industry had been watching.

VII. Overhangs & Redress: The Motor Finance Commission Crisis of 2026

For years, buying a car on finance in Britain worked in a way most customers never understood — and that ignorance was, quite literally, the business model. When you walked into a dealership and financed a car, the salesman arranging your loan was often not a neutral broker. Under an arrangement known as a discretionary commission arrangement, or DCA, the lender allowed the dealer to adjust the interest rate on your loan, and here was the catch: the higher the rate the dealer set, the bigger the commission the lender paid the dealer. In other words, the person helping you finance your car had a direct, undisclosed financial incentive to charge you more. Lloyds sat at the centre of this market through Black Horse, the UK's largest motor-finance lender. The Financial Conduct Authority banned discretionary commission arrangements in 2021, but by then millions of these loans had already been written.

Then, in January 2024, the regulator reopened the past. The FCA launched a formal review into historic discretionary commissions, examining agreements stretching back years, and the entire motor-finance industry suddenly faced a question with an unknowable answer: how much would it owe customers who had been overcharged without their knowledge? For two years the sector lived under a cloud of legal uncertainty. The uncertainty was amplified, not resolved, by the courts: a series of judgments worked their way up the legal system, at one point threatening to expand liability dramatically by suggesting that almost any undisclosed commission — not merely the discretionary kind — could be unlawful, a reading that would have blown the potential bill wide open across the whole of consumer lending. Higher courts eventually pulled some of that expansive interpretation back, narrowing the scope, but the episode showed exactly why bank investors treat redress liabilities as radioactive: the size of the bill depends not on a fixed set of facts but on evolving judicial and regulatory interpretation, and it can lurch by billions on a single ruling. The defining moment came on 30 March 2026, when the FCA drew a line under the debate and confirmed an industry-wide, mandatory consumer redress scheme.4

The scale the regulator set out was sobering. The scheme covers agreements taken out between 6 April 2007 and 1 November 2024 in which a commission or lender tie applied — approximately 12.1 million eligible agreements — with the FCA estimating total industry redress of around £7.5 billion and an average payout in the region of £830 per agreement.5 For the lender with the largest motor-finance book in the country, this was never going to be a small bill. And Lloyds' provisioning history tells the story of an estimate that kept climbing.

The credibility test is right here in the numbers. Lloyds started conservatively, with an early provision of a few hundred million pounds when the review first opened. As the FCA's thinking hardened through 2025, it added substantially more, and by the time the full-year 2025 results were published the total motor-finance provision had reached £1.95 billion — with the 2025 charge alone at £968 million, up from £899 million booked in 2024.1 That £1.95 billion is now the largest motor-finance provision of any lender in the United Kingdom, a direct reflection of Black Horse's market leadership.4 Following the FCA's final rules, Lloyds reviewed its position in the first quarter of 2026 and left the provision unchanged, taking only a minimal £11 million remediation charge and telling the market that £1.95 billion remained its best estimate.2

On the Q1 2026 earnings call, this was exactly where analysts pushed hardest, and their skepticism was not idle.3 Management's posture on the call was one of calm reassurance — the provision was adequate, the methodology conservative, the £11 million top-up trivial — but reassurance is precisely what a skeptical investor should interrogate rather than accept. The tell in these situations is not what management asserts but how much of the assertion rests on assumptions the company itself acknowledges are uncertain: the eventual complaint volumes, the proportion of eligible customers who actually come forward, the average redress per case, and the operational cost of processing millions of claims. Each of those is a variable, and each moved against the industry during PPI. The reason the number matters so much is a four-letter word that haunts every UK bank investor: PPI. That scandal began, in the industry's early estimates, as a manageable few-billion-pound problem and ballooned, over years of expanding claims and regulatory reinterpretation, into a bill north of £40 billion — of which Lloyds alone paid more than £20 billion. Investors who lived through that arc have learned a hard lesson: a bank's confident, "definitive" cap on a consumer-redress liability is an opening bid, not a final number. So when Lloyds' management insists that £1.95 billion is adequate, the market's memory supplies its own caveat. Bear-case analysts have floated total exposure scenarios materially above the provision, in some cases toward £3.5 billion or more, and the honest answer is that no one — not management, not the analysts, arguably not the FCA — yet knows where the final figure lands.

The redress timetable itself is worth laying out, because it maps directly onto the moments when Lloyds' costs and complaint volumes could jump. An industry-wide pause on handling motor-finance complaints was scheduled to lift at the end of May 2026, with the redress scheme opening first to more recent agreements — those from the period after April 2014 — over the summer, before extending at the end of August 2026 to the older tranche of claims dating back to 2007. A final deadline for complaints was set for the following year.56 The second tranche matters most, because older agreements are the hardest to document and the most likely to generate disputes, appeals, and administrative expense. An investor tracking Lloyds should watch that late-2026 window closely: a surge in complaint volumes or operational cost as the older claims open would be the earliest hard signal that the £1.95 billion estimate is under strain.

The situation is made more complicated still by the fact that the scheme itself is under legal siege. As of early July 2026, parts of the scheme have been suspended after the Upper Tribunal agreed to hold matters on terms while lenders and other parties challenge aspects of the FCA's approach — meaning the very timetable above is now uncertain, capable of slipping as the litigation plays out.4[^7] For an investor, this is the worst kind of overhang: large, quantified only as an estimate, and now wrapped in litigation whose outcome could push the total up or down. The single most important thing to watch in the coming quarters is whether Lloyds' complaint volumes and operational costs spike as older claims come into scope, and whether that £1.95 billion figure holds — or begins the same slow, grinding upward creep that defined PPI. This is the live regulatory wound in the Lloyds story, and it sits uncomfortably alongside an otherwise strengthening operating performance.

VIII. The Playbook: 5 Forces, 7 Powers, and Investing Lessons

Step back from the noise of provisions and margins, and ask the structural question an investor should always ask: what, exactly, protects this business from competition? Lloyds is a useful case study precisely because its moat is real but narrow — strong in a few dimensions, conspicuously absent in others. Two analytical frameworks help map it: Hamilton Helmer's 7 Powers and Michael Porter's Five Forces.

Start with Helmer's powers, and the strongest is scale economies. Lloyds spends on the order of a billion pounds a year on technology and digital development, and it amortises that fixed cost across a customer base of tens of millions of active digital users. The per-user economics are the whole game. A challenger bank with a fraction of the customers must either spend proportionally as much — crippling its cost structure — or accept an inferior product. This is a genuine, durable advantage, and it is the single best argument for Lloyds' long-term resilience. It is also the mechanism that lets Lloyds close branches and push customers to the app without losing them: the digital experience is good enough because Lloyds can afford to make it good.

The second power is switching costs, and here the verdict is more nuanced — moderate, but real. Britain has, unusually, made current-account switching almost frictionless through the Current Account Switch Service, which moves your direct debits and salary automatically within days. In theory this should have eroded bank stickiness to nothing. In practice, consumer inertia has proven astonishingly resilient: most people simply never switch their primary current account, year after year, and that inertia is the foundation of Lloyds' cheap-deposit advantage. The switching cost here is psychological rather than contractual, but it is no less economically valuable for that — it is the reason the net interest margin works.

The third power is brand. The Halifax and Lloyds names carry more than a century of high-street heritage and trust, and — crucially — they function as acquisition funnels, the default first port of call for a first-time buyer seeking a mortgage. Brand in banking is not glamour; it is the quiet assumption that this institution will still exist, and honour your deposit, in thirty years.

Now the honest part: what powers does Lloyds not have? It has no network effects — your Lloyds account becomes no more valuable because your neighbour also banks with Lloyds. And it has no counter-positioning; if anything, Lloyds is on the wrong side of that dynamic. The fintech challengers — 数字银行-style app-only banks such as Monzo and Starling — are the ones counter-positioning against Lloyds, offering a slicker experience unburdened by the cost of legacy branches and mainframe systems. Lloyds cannot fully replicate their model without cannibalising its own economics, which is the classic incumbent's dilemma. Its defence is scale and trust, not innovation.

Porter's Five Forces sharpen the same picture. Rivalry is high: the big mortgage lenders price-match one another relentlessly, which structurally caps how fat mortgage margins can get, especially at the low-margin two- and five-year fixed-rate end. The consolidation of Nationwide and Virgin Money into a stronger number-two lender has, if anything, intensified this — Lloyds now faces a scaled mutual competitor able to price aggressively without the same shareholder pressure for returns. The bargaining power of depositors is rising: in a high-yield world, savers are more mobile than they used to be, forcing Lloyds to pay up to retain deposits or watch them migrate — the deposit-beta problem in Porter's language. The threat of new entrants is real but contained: the app-only challengers have proven they can win customers, particularly the young, but they have found it far harder to win the primary banking relationship — the account where the salary lands and the direct debits sit — which is the only relationship that generates cheap, sticky deposits. Many a Monzo customer also keeps a Lloyds or Halifax account for the mortgage and the salary. And the threat of substitutes is low: for all the innovation in fintech and peer-to-peer lending, the mainstream retail bank remains the fundamental mechanism through which Britons buy homes and finance their lives. Nobody is about to replace the mortgage. The bargaining power of borrowers, meanwhile, is modest at the individual level but growing at the aggregate level, as price-comparison sites and mortgage brokers commoditise the shopping experience and push lenders toward transparent, competed-away pricing.

The lesson for investors is that Lloyds' moat is a deposit moat, not a technology or product moat. Its edge is the millions of people who will never move their current account, and the scale that inertia funds. That is a powerful thing to own — but it is also a passive, defensive advantage, vulnerable to a world in which switching finally becomes normal, or in which rates fall and the cheap-deposit magic fades. Which is precisely the tension at the centre of the bull and bear cases.

IX. The Bull vs. Bear Case & Active Investor Stress Test

Every investment in Lloyds is, at bottom, an argument between two views of the same facts. Let us give each its strongest form.

The bull case begins with the observation that, in a stable or elevated interest-rate environment, Lloyds is close to a cash-generating utility. The return on tangible equity reached around 17% in the first quarter of 2026, a level that signals genuine capital efficiency — the bank is wringing a high return out of every pound of equity it holds.2 For the full year 2025, statutory RoTE came in at 12.9%, or a stronger 14.8% once the motor-finance charge is stripped out, and management guided toward RoTE above 16% for 2026, on the way to higher still.1 The digital transformation gives the bull case a self-help engine independent of rates: as branches close and technology absorbs more of the workload, the cost-to-income ratio grinds down toward the sub-50% target, mechanically lifting profitability. And the capital story is the payoff — strong capital generation funds a steady drumbeat of dividends and buybacks, giving shareholders a yield that is among the more attractive in the sector. In short: a dominant, efficient, well-capitalised franchise returning cash hand over fist.

The bear case does not dispute the profits; it disputes their durability, and it has three sharp points.

The first is interest-rate vulnerability. The same net interest margin that gushes profit in a high-rate world compresses fast when the Bank of England cuts. Because Lloyds is so overwhelmingly a spread lender, a rapid series of rate cuts would erode net interest income more quickly than the wealth and fee businesses could possibly compensate. The structural hedge softens and delays this, but it does not eliminate it. Lloyds' earnings are, to a degree its diversified peers' are not, a leveraged play on the rate cycle — and cycles turn.

The second is the motor-finance black hole already described. If actual redress claims exceed the £1.95 billion provision — and the PPI precedent gives real weight to that fear — the first casualty would be the buyback. Capital that is currently being returned to shareholders would instead be diverted to fund redress, and the equity story would deflate. The provision is management's best estimate, but as of mid-2026 it is an estimate wrapped in active litigation, which is the definition of an unquantified tail risk.

The third, and most fundamental, is the UK-economy trap. Lloyds' great strength — its focused, pure-play domestic model — is also its defining vulnerability. It has essentially zero geographic diversification. A British recession, a spike in unemployment, stubborn inflation, or a genuine house-price collapse would flow almost immediately into rising credit-impairment charges, and there is no offsetting Asian or American business to cushion the blow. An activist or short-seller stress-testing Lloyds would frame it bluntly: this is not a diversified global bank; it is a single-country, single-cycle credit and rate bet wearing the costume of a diversified financial-services group. Every quarter of good numbers is also a quarter closer to the cycle that tests that thesis.

It is worth puncturing one piece of consensus mythology while we are here, because it colours how many investors think about Lloyds. The myth is that Lloyds is a "safe," "boring," "defensive" bank — a utility you can tuck away and forget. The reality is more subtle. Lloyds is operationally conservative and extremely well capitalised, which is genuinely defensive. But its earnings are not defensive at all; they are highly geared to two volatile external forces — the interest-rate cycle and the UK credit cycle — with almost nothing to offset a downturn in either. A truly defensive business has earnings that hold up when the environment sours; Lloyds has earnings that soar when rates are high and benign, and compress when they are not. The safety is in the balance sheet, not the income statement. Conflating the two — assuming that a fortress capital position implies stable profits — is one of the more common analytical errors made about this company.

An activist or governance-minded critic would push on a few additional pressure points. The portfolio, while focused, still carries the perennial question of whether the insurance, pensions and investments arm truly belongs inside a bank or would be worth more spun out — a "diworsification" challenge that periodically surfaces at every universal bank. There is the question of whether a bank generating this much surplus capital should be returning even more of it, faster, rather than holding buffers that arguably flatter management's optionality at shareholders' expense. And there is the ever-present accountability question that trails any bank with a redress history: whether the board's provisioning judgments are genuinely independent and conservative, or shaded by the institutional desire to protect the dividend and the buyback. None of these is a scandal; all of them are legitimate lines of inquiry that a serious owner would keep open rather than closed.

Weighing the two, the intellectually honest conclusion is that both are true simultaneously. Lloyds is a superbly efficient deposit franchise generating strong returns and disciplined capital distributions — and it is a concentrated, cyclical wager on one economy with an unresolved regulatory liability attached. The stock is neither obviously cheap for what it is nor obviously expensive; it is a machine whose value depends almost entirely on two things a shareholder cannot control: the path of UK interest rates and the final size of the motor-finance bill.

Which is why, for anyone tracking this company, the analysis collapses to a small number of variables worth monitoring above all others. First, the banking net interest margin — the single cleanest read on whether the profit engine is widening or compressing; a sustainable level above roughly 3.00% is the marker of health. Second, the cost-to-income ratio — the proof of whether the digital transformation is real, with the sub-50% target as the test. Third, return on tangible equity — the summary statistic that folds margin, costs, and credit into one number, with management's stated ambition above 16% for 2026 as the yardstick. Watch those three, alongside the trajectory of the motor-finance provision, and you will understand this business better than any headline.

X. Epilogue & Episode Wrap-Up

There is a strange symmetry to the Lloyds story. It began in 1765 as the financial arm of an iron trade, a bank embedded in the machinery of the Industrial Revolution — conservative, provincial, and tied utterly to the fortunes of the real economy around it. Two and a half centuries later, after a near-death experience, a decade as a ward of the state, the largest consumer-redress bill in British history, and a digital reinvention, it is still, in its deepest character, exactly that: a conservative, domestic institution whose fate rises and falls with the British economy. The technology has changed beyond recognition. The essential bet has not.

The narrative arc — from eighteenth-century iron financier, to post-crisis nationalised utility, to twenty-first-century digital colossus — is in many ways the story of modern British capitalism itself: the ambition, the overreach, the state rescue, the long convalescence, and the disciplined, unglamorous recovery. Lloyds is the economy's mirror, which is both the reason to own it and the reason to fear it.

If there is a lesson here for founders, operators, and investors alike, it is a double one, and the two halves sit in tension. The first is a warning: a merger made in panic, without the discipline of proper diligence, can poison a healthy enterprise for a decade — the HBOS deal took the most prudent bank in Britain and nearly destroyed it, and no amount of subsequent competence fully erased the cost. The second is more hopeful: a dominant, low-cost retail deposit franchise, protected by nothing more exotic than customer inertia and brand trust, is one of the most resilient moats in all of finance. It survived 2008. It survived PPI. It is being tested again by motor finance. Whether it keeps compounding from here depends less on management's ambition and more on two forces beyond any executive's control — the interest-rate cycle and the health of the nation whose economy Lloyds so faithfully reflects. For a bank that started in the forges of Birmingham, that is a fittingly elemental place to end.

References

-

2025 Results — News Release, Lloyds Banking Group, 2026-01-29 ↩↩↩↩↩

-

Q1 2026 Interim Management Statement Presentation, Lloyds Banking Group, 2026-04-29 ↩↩↩↩

-

Earnings call transcript: Lloyds Banking Group Q1 2026 — Investing.com, 2026-04-29 ↩

-

FCA confirms motor finance redress scheme — Financial Conduct Authority, 2026-03-30 ↩↩↩↩

-

PS26/3: Motor finance consumer redress scheme — Financial Conduct Authority, 2026-03-30 ↩↩

-

The return of Lloyds Banking Group to private ownership — National Audit Office, 2018 ↩↩↩

-

Lloyds bank: UK government sells off final shares, but did it make a profit? — Euronews, 2017-05-17 ↩

-

Lloyds and Nationwide seal top spots as largest resi and BTL lenders — Mortgage Finance Gazette, 2025-07-18 ↩↩

-

Lloyds Banking Group plc — Form 6-K (Director/PDMR Shareholding, LTIP awards), U.S. Securities and Exchange Commission, 2026-05 ↩↩

-

2025 Half-Year Results — News Release, Lloyds Banking Group, 2025-07-24 ↩↩↩↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube