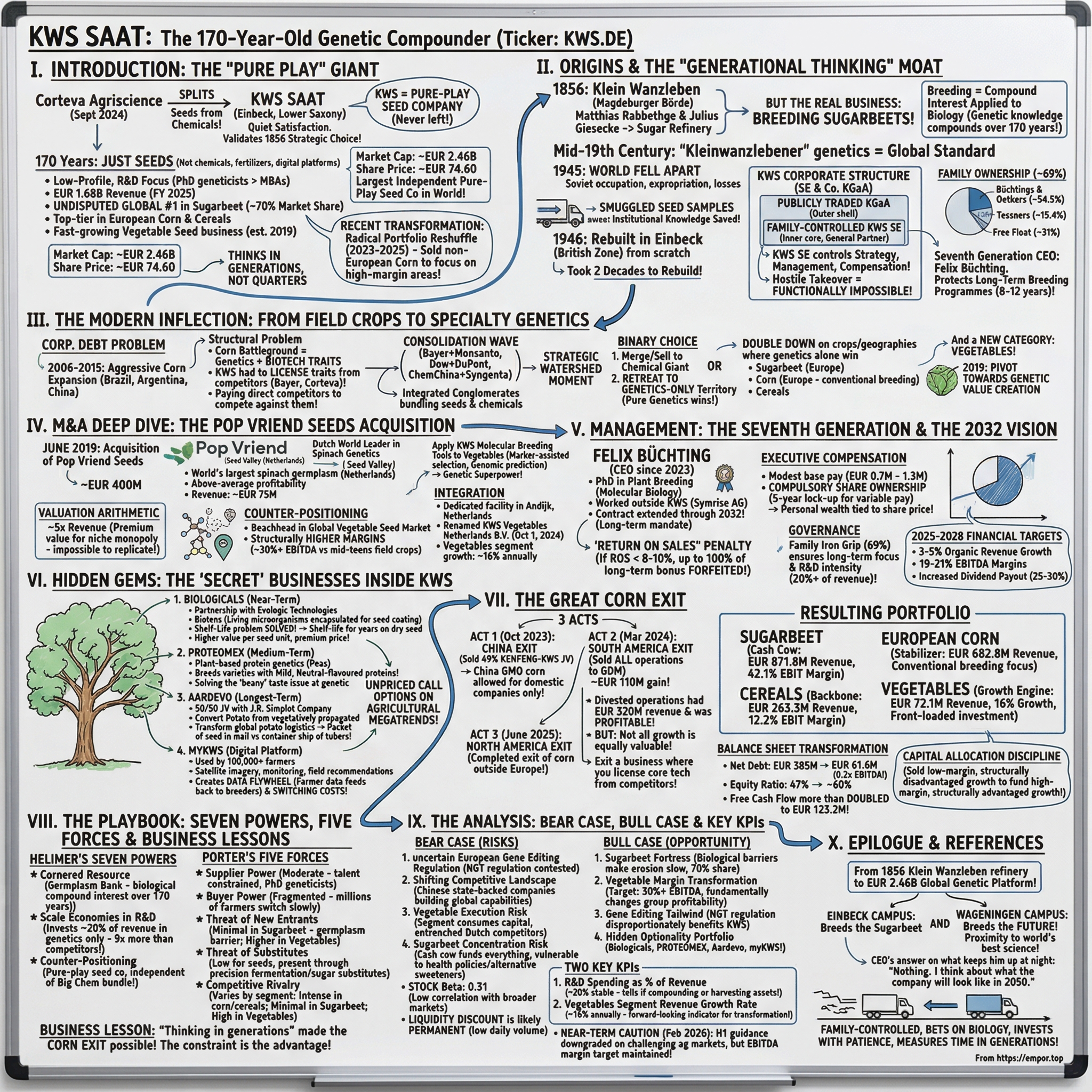

KWS SAAT: The 170-Year-Old Genetic Compounder

I. Introduction: The "Pure Play" Giant

In September 2024, the CEO of Corteva Agriscience — the seed-and-chemical giant spun out of the DowDuPont merger — stepped before investors and announced what many in the industry had long suspected was coming: the company would split itself in two, separating its seed business from its crop protection chemicals business. The market cheered. Analysts wrote notes about "unlocking shareholder value" and "strategic clarity." The stock moved.

Seven hundred kilometres to the east, in Einbeck, a quiet university town in Lower Saxony where half-timbered houses line medieval streets and the local beer has been brewed since 1378, the management of KWS SAAT SE & Co. KGaA permitted themselves a moment of quiet satisfaction.

They had been waiting for this moment — not anxiously, not urgently, but with the patient certainty of people who know that the rest of the industry will eventually arrive at the conclusion they reached a very long time ago.

They did not issue a press release. They did not post on LinkedIn. They did not schedule a CNBC appearance. That is not how KWS operates.

But Corteva's decision to separate seeds from chemicals was, in effect, a validation of a strategic choice that KWS had made not in 2024, not in 2019, but in 1856.

The world's largest agrochemical conglomerate had just announced that it was becoming what KWS already was: a pure-play seed company. The rest of the industry was finally arriving at the conclusion that KWS had never left.

For one hundred and seventy years, KWS has done exactly one thing: seeds. Just seeds. Not chemicals. Not fertilisers. Not digital farming platforms bolted onto herbicide subscriptions. Seeds. The genetic blueprints that determine whether a sugarbeet produces thirty tonnes of sugar per hectare or eighteen. Whether a spinach plant resists downy mildew in a California winter or succumbs to it. Whether a rye crop survives a late frost in northern Poland or dies in the field.

The purity of that focus is almost monastic. In an era when every agribusiness conglomerate diversifies into chemicals, digital platforms, and financial services, KWS does one thing and does it extraordinarily well.

The scale is easy to understate because the company is so deliberately low-profile. There is no KWS logo on a Formula One car. There is no KWS Super Bowl advertisement. The company's headquarters in Einbeck, Lower Saxony, looks more like a research campus than a corporate power centre — because it is one. Walk through the corridors and you will find more PhD plant geneticists than MBAs, more greenhouses than conference rooms, more soil samples than PowerPoint decks.

KWS generated EUR 1.68 billion in revenue in the fiscal year ending June 2025. It is the undisputed global number one in sugarbeet seed, commanding approximately 70 percent of the world market — a dominance so complete that if you have eaten sugar in Europe, you have almost certainly consumed sugar from a KWS variety. It is a top-tier player in European corn and cereals. And since a transformative acquisition in 2019, it is building a fast-growing vegetable seed business anchored by global leadership in spinach genetics.

Now for the numbers — and the numbers are where the story starts to get interesting.

The market capitalisation sits at approximately EUR 2.46 billion at a share price of roughly EUR 74.60. For context, that is roughly the size of a mid-tier American regional bank — a valuation that would be unremarkable in most sectors but is extraordinary in the global seed industry.

Only Corteva, Bayer's crop science division, and Syngenta command significantly larger seed operations. KWS is the largest independent pure-play seed company in the world — independent meaning it does not sell chemicals, and pure-play meaning it does nothing but seeds.

For all its scale and strategic importance, KWS remains remarkably under-followed by the international investment community. The company trades on Frankfurt's XETRA exchange as a member of the SDAX index, though "trades" is perhaps generous — average daily volume is roughly 23,000 shares, making this one of the most illiquid mid-cap stocks in Germany. The founding families — the Büchtings, the Oetkers, and the Tessners — control approximately 69 percent of the shares through a pooling agreement, leaving a free float of roughly 31 percent. The current CEO, Felix Büchting, is the seventh generation of the founding family. Seventh generation. In a country where most companies do not survive three generations, this is remarkable.

But the thesis that makes KWS worth studying is not its size or its history. It is its present strategic transformation — one of the most decisive portfolio reshuffles in recent European industrial history. Between 2023 and 2025, KWS executed one of the most decisive portfolio reshuffles in European industrial history: it sold its entire corn business in South America, China, and North America — hundreds of millions of euros in revenue, growing revenue, profitable revenue — to concentrate resources on sugarbeet dominance, European corn, and a new high-margin vegetable genetics platform. The company voluntarily shrunk itself to become stronger. Few public companies have the governance structure or the management courage to make that choice. The company simultaneously invested in biological seed treatments, plant-based protein genetics, and a hybrid potato joint venture that could transform global food logistics.

In a world of incremental corporate change, KWS executed a radical reshaping of its entire business portfolio — and did it with the quiet determination that characterises everything this company does.

This is the story of a company that thinks in generations, not quarters — and what happens when that long-term orientation collides with a global agricultural industry undergoing its most radical consolidation since the Green Revolution.

It is also a story about what "focus" really means — not as a consulting buzzword, but as a lived strategic discipline sustained across wars, occupations, and industry upheavals.

It is the story of a family that lost everything in 1945, rebuilt from seed samples smuggled across an occupation boundary, and quietly assembled one of the most defensible competitive positions in modern agriculture.

What follows is that story, told in full.

From the 1856 "Klein Wanzlebener" sugar factory to the high-tech greenhouses of the Dutch "Silicon Valley of Seeds," the arc of KWS traces the tension between patience and ambition, between heritage and reinvention. And it raises a question that goes beyond any single company: in an age of quarterly capitalism and activist investors, can generational thinking still create superior economic outcomes?

II. Origins and the "Generational Thinking" Moat

Every great business story has an origin myth. KWS's begins not in a garage or a dorm room but in the fertile black soil of central Germany.

The town of Klein Wanzleben sits on the fertile Magdeburger Börde plain east of the Harz Mountains — a region where deep loess soils, deposited by Ice Age winds, have sustained intensive agriculture for centuries. In 1856, Matthias Christian Rabbethge and Julius Giesecke established a sugar refinery there.

But from the beginning, the real business was not refining sugar. It was breeding sugarbeets.

The distinction matters enormously, and it is worth pausing to understand why, because the entire KWS story hinges on it. Most people in the food industry have never thought carefully about it. But once you see the distinction, you cannot unsee it.

A refinery processes whatever raw material arrives at its gate. The quality of a refinery's output is constrained by the quality of its input. A breeder does something fundamentally different. A breeder shapes the raw material itself — selecting parent plants with incrementally higher sugar content, crossing them, evaluating the offspring, discarding the failures, preserving the successes, and repeating the process across seasons and years and decades.

Think of it as compound interest applied to biology. The metaphor is not casual — it is precise. Every generation of breeding builds on the genetic selections of the generation before. Skip a generation, and you lose the compounding. Keep at it for 170 years, and the accumulated genetic knowledge becomes an asset that no competitor, no matter how well-funded, can replicate from scratch.

The compounding has been extraordinary.

In the mid-nineteenth century, sugarbeet varieties from Klein Wanzleben became the global standard. Farmers from France to Russia sought "Kleinwanzlebener" genetics because they consistently outperformed local varieties. The name became a brand before branding existed — synonymous with beet quality the way Champagne became synonymous with sparkling wine or the way "Meissen" became synonymous with porcelain.

Karl Büchting, a son-in-law who married into the Rabbethge family, commercialised the operation and gave his name to the dynasty that would control the company for seven generations. It is one of the great ironies of corporate history that the family that built the world's most valuable seed company was not the founding family — it was the family that married into it.

The Büchting family brought commercial discipline to what had been primarily a scientific endeavour. They built distribution networks across Europe, establishing testing stations in multiple climates, and creating the organisational infrastructure that allowed genetic improvements to reach farmers at scale.

Then came 1945, and the world fell apart.

What happened next is one of the most extraordinary survival stories in European industrial history — and it deserves to be told in detail, because it explains why KWS's culture is what it is today.

Klein Wanzleben lay in the Soviet occupation zone. The communist government expropriated everything — breeding stations, seed stocks, laboratories, land, nearly a century of carefully selected plant material. The loss was not merely financial. It was biological — and biological losses, unlike financial ones, cannot be recovered by raising capital or restructuring debt. Ninety years of accumulated genetic progress — the carefully selected breeding lines, the tested populations, the parent material from which future varieties would be developed — was in the hands of a regime that had no interest in private plant breeding and every intention of collectivising agriculture. In the chaos of the occupation's early weeks, key employees and family members managed to physically transport seed samples and critical breeding material westward in trucks before Soviet troops fully consolidated control. It was, in the most literal sense possible, a re-seeding of the business. The physical act of carrying seed samples across an occupation boundary in trucks was the founding moment of the modern KWS — the moment when institutional knowledge was saved from political destruction.

The successor company was established in 1946 in Einbeck, within the British occupation zone. The choice of Einbeck was not random — it was close enough to the original territory that the soil and climate conditions were similar, allowing the rescued breeding lines to be tested in familiar environments. They started from a single location with a fraction of their prior resources.

No laboratories. No established field trial network. No distribution infrastructure. Just seed samples, knowledge, and an extraordinary determination to rebuild. It is the kind of origin story that shapes a corporate culture for generations — and at KWS, it has.

Think about the alternative paths available to the Büchting family in 1946. They could have emigrated to the United States, where seed companies were well-capitalised and the agricultural research infrastructure was the world's best. They could have diversified into farming, food processing, or agricultural equipment — businesses that did not require rebuilding decades of genetic material from fragments. They could have sold what remained and walked away.

They chose none of those paths.

The decision to rebuild rather than emigrate or diversify was the first expression of what would become KWS's defining characteristic: the willingness to take the long view, absorb catastrophic losses, and rebuild patiently because the alternative — abandoning decades of genetic knowledge — was unthinkable.

There is an analogy here to the luxury goods industry, where houses like Hermès have survived wars, occupations, and economic upheavals by clinging to their craft knowledge. The raw materials can be replaced. The machinery can be rebuilt. What cannot be recreated from scratch is the accumulated expertise — the institutional knowledge of which crosses produce which results, which genetic combinations yield which traits. KWS's seed samples were the equivalent of Hermès's craftsmen: the irreplaceable human capital that carried the institutional knowledge forward.

The rebuild took two decades. By the 1960s, KWS had re-established itself as Europe's premier sugarbeet breeder. The company expanded into cereals in the decades that followed, achieving a technical breakthrough in hybrid rye that cemented its reputation in plant science and demonstrated that the molecular biology capabilities developed for sugarbeet could be applied across crop species — a principle that would guide KWS's strategy for the next six decades.

The corporate structure reflects this generational philosophy in every detail. In 2019, KWS converted to an SE & Co. KGaA — a Kommanditgesellschaft auf Aktien, the distinctly German legal form that is part stock corporation, part limited partnership. For non-German observers, the structure deserves a brief explanation because it is the legal architecture that makes KWS's entire strategy possible.

The publicly traded entity is the KGaA, where anyone can buy shares on XETRA. So far, so normal. But sitting inside that structure is KWS SE, a separate European stock corporation controlled by the founding families, which serves as the sole general partner. Think of it as a nesting doll: the outer shell (the KGaA) is publicly traded and accessible to all investors, but the inner core (KWS SE) is locked behind family control and holds all the real power. KWS SE has exclusive authority to appoint management, set compensation, and determine strategy. The supervisory board of the KGaA has curtailed powers — it cannot remove management or set pay. The practical effect is that a hostile takeover is functionally impossible. Period. Full stop. No exceptions. Even acquiring 100 percent of the free float — every single publicly traded share — gives an acquirer no control over management or strategy. The keys to the kingdom are locked inside the KWS SE structure, and the families hold those keys.

The ownership numbers tell the story of how the families have maintained control across generations.

The Büchting and Oetker families hold approximately 54.5 percent of voting rights through a formal pooling agreement first established in 1994 and renewed by subsequent generations. Marie Th. Schnell succeeded her father Arend Oetker on the supervisory board in 2016, ensuring continuity of the family partnership into a new generation — the kind of deliberate, planned succession that distinguishes families who take generational stewardship seriously from those who leave succession to chance. The Tessner family holds roughly 15.4 percent.

Together, the three families control approximately 69 percent — an iron grip that ensures strategic continuity across leadership transitions but also ensures that minority shareholders have no ability to influence governance, capital allocation, or management selection.

This is emphatically not a structure designed to maximise short-term shareholder value. And that is entirely the point. It is not designed to attract activist investors. It is not designed to facilitate leveraged buyouts. It is a structure designed to do one thing exceptionally well: protect management's ability to invest in breeding programmes that take eight to twelve years to produce commercial varieties — programmes that would be cancelled in the first budget review at a company facing quarterly earnings pressure from activist shareholders.

Consider that for a moment. The breeding programme that produces a blockbuster sugarbeet variety in 2036 must be funded today. A CEO who faces activist pressure in 2027 will cut that programme to protect next quarter's earnings. The KGaA structure exists precisely to prevent that outcome. The trade-off is real: the stock's illiquidity and governance discount are the price shareholders pay for a management team that can think in decades rather than quarters. Whether that trade-off is worth it depends entirely on whether you believe the long-term compounding of genetic assets creates more value than the short-term capital allocation optimisation that public market pressure enables.

The answer, if the last 170 years are any guide, is yes. But 170 years of history does not guarantee the next 170. And the next two decades of KWS's history — the vegetable pivot, the gene editing revolution, the rise of Chinese competitors — would put that belief to the test.

III. The Modern Inflection: From Field Crops to Specialty Genetics

Between 2006 and 2015, KWS pursued the strategy that most European seed companies pursued: aggressive international expansion into the world's largest and fastest-growing corn markets. It was the obvious play. It was the consensus play. And as is often the case with consensus plays in business, the obvious path turned out to be the most dangerous one.

The logic was straightforward — deceptively so, as it turned out. Corn is the world's most valuable seed crop by far — a market worth roughly EUR 15 billion annually, driven by feed demand for livestock, ethanol mandates, and population growth in emerging economies. Brazil, Argentina, and China together represented the most attractive growth opportunities on the planet.

KWS built and acquired corn operations across South America with the methodical thoroughness that characterises German industrial expansion. It picked up SEMILIA and DELTA, Brazilian seed companies, in 2012. It established a joint venture in China with Beidahuang Kenfeng Seed Co., entering the market through a local partner who understood the regulatory landscape. Revenue grew. The footprint expanded. International corn became a meaningful part of the portfolio.

But a structural problem lurked beneath the growth numbers, and it took nearly a decade to become undeniable. It was the kind of problem that does not show up in a single quarter's earnings — it reveals itself slowly, like a crack in a foundation that widens imperceptibly until the wall shifts. It was not a problem of execution — KWS's people in Brazil were good at their jobs.

KWS's corn germplasm was competitive. Its breeders were talented. Its field operations were efficient. The problem was structural — embedded in the very architecture of the global corn seed market. And structural problems, unlike operational problems, cannot be solved by working harder or executing better.

To understand the problem, you need to understand how the modern corn seed market actually works — because it operates on a fundamentally different model from sugarbeet or vegetables.

In corn — particularly in the Americas — the competitive battlefield was not genetics alone. It was genetics plus biotech traits: herbicide tolerance, insect resistance, stacked traits combining multiple modifications in a single hybrid. These transgenic traits were overwhelmingly owned by two companies: Monsanto (now Bayer) and DuPont Pioneer (now Corteva). Two companies. Two gatekeepers controlling the technology that every other seed company needed to compete. To compete in Brazilian or Argentine corn, KWS had to license these traits from its direct competitors, paying royalties on the very technology that differentiated its products. Every bag of KWS corn seed sold in Brazil contained licensed Bayer or Corteva technology, with a royalty payment flowing directly to the companies KWS was trying to outcompete.

Pause and let that sink in. KWS was paying its direct competitors for the right to compete against them.

The analogy would be Samsung paying Apple a licence fee for iOS on every Galaxy phone it sold. You can build a viable business on that model — Samsung did, after all — but you will never achieve the margins or strategic independence of a company that controls its own core technology.

Meanwhile — and this is the context that makes KWS's subsequent strategic decisions comprehensible — the global seed industry was undergoing the most dramatic wave of consolidation in its history. Bayer announced the acquisition of Monsanto for USD 63 billion. Dow and DuPont merged and subsequently spun off Corteva. ChemChina acquired Syngenta for USD 43 billion. BASF picked up seed and herbicide assets divested by Bayer as a regulatory concession. In the space of three years, the industry map was redrawn. The result was an industry dominated by three or four integrated chemistry-and-seeds conglomerates, each bundling herbicide-tolerant seed genetics with proprietary herbicides in a system designed to create farmer lock-in. Buy Bayer's corn seed and you need Bayer's herbicide. Buy Corteva's soybean seed and you need Corteva's crop protection programme.

The bundling model was extraordinarily profitable for the companies that controlled both halves of the equation — and existentially threatening for a pure-play seed company that controlled neither the chemistry nor the biotech traits.

This was the watershed moment. The moment when the strategic landscape shifted beneath KWS's feet. And the response would define the company's future for the next several decades.

This was the moment that defined KWS's future. The company faced a binary choice. Option one: merge with or sell to one of the chemical giants, as virtually every other independent seed company in the world was doing. Option two: retreat to the territory where genetics alone — without bundled chemistry or licensed biotech traits — could win.

KWS made the radical choice. The choice that no management consultant would have recommended. The choice that would have gotten a CEO fired at most publicly traded companies.

It chose option two. Instead of trying to compete in a market where its competitors controlled the complementary assets — a fight it could never win — KWS would double down on crops and geographies where pure genetics — the thing it was genuinely world-class at — was the primary source of competitive advantage. Sugarbeet in Europe, where KWS already held 70 percent market share. Corn in Europe, where GMO restrictions meant conventional breeding excellence was the differentiator rather than transgenic traits. Cereals, where hybrid rye and oilseed rape rewarded deep germplasm knowledge.

And then there was a category KWS had never seriously competed in before. A market that had been hiding in plain sight — overlooked by the Big Ag conglomerates because it was too fragmented, too varied, and too small for companies that measured success in billions of tonnes.

It was a market that offered structurally higher margins, less dependence on biotech traits, and a global growth rate nearly double that of field crops. It was also a market dominated by privately held Dutch and Japanese companies that had been breeding for decades and had no interest in selling.

But in 2019, an opportunity appeared. And KWS, with the patience of a 163-year-old company, was ready to seize it.

In June 2019, KWS announced the acquisition that signalled the new strategic direction: the purchase of Pop Vriend Seeds, the Dutch world leader in spinach seed genetics, for approximately EUR 400 million.

The announcement was met with a mixture of excitement and bewilderment by the analyst community. KWS — the sugarbeet company, the corn company, the company that operated in the world of field-scale commodity agriculture — was buying a spinach seed business? In the Netherlands? For EUR 400 million?

The deal represented roughly 20 percent of KWS's market capitalisation at the time — a bet large enough to reshape the company's identity. To put that in perspective, it would be equivalent to Apple spending roughly USD 700 billion on a single acquisition. The scale of the commitment, relative to the company's size, signalled that this was not a diversification experiment. It was a strategic pivot.

The era of chasing corn volume in Brazil was ending. The era of genetic value creation in vegetables was beginning.

It was, in the language of strategy, a classic case of counter-positioning — retreating from a battleground where the rules favoured the incumbents and advancing toward a battleground where KWS's unique capabilities gave it the advantage. The question was whether management had the courage to execute the retreat before the retreat was forced upon them.

IV. M&A Deep Dive: The Pop Vriend Seeds Acquisition

To understand why the EUR 400 million price tag was justified — and why it might actually have been a bargain — you need to understand what Pop Vriend Seeds was, where it was located, and why spinach genetics are more valuable than they sound.

Pop Vriend Seeds was founded in 1956 — exactly one hundred years after KWS — by a man named Pop Vriend near Wageningen in the Netherlands. If you know anything about plant science, the name Wageningen triggers immediate recognition. Wageningen University & Research is widely regarded as the world's leading institution in agricultural science. Within a fifty-kilometre radius of the campus sit Rijk Zwaan, Enza Zaden, Bejo Zaden, and East-West Seed — collectively, the densest cluster of vegetable seed breeding expertise on the planet. The Dutch call it "Seed Valley," and the label is not marketing hyperbole. It is a description of competitive reality.

Pop Vriend had spent six decades doing, in vegetables, what KWS itself had done in sugarbeet: building what amounted to a quiet monopoly in a specific crop's genetics through patient accumulation of knowledge, germplasm, and breeding expertise that no amount of money could shortcut.

The crown jewel was spinach. The company held the world's largest collection of spinach germplasm — the raw genetic diversity from which commercial varieties are bred. Its varieties dominated the global spinach seed market, from the baby-leaf spinach packed into plastic clamshells at American supermarkets to the bunched spinach sold at wet markets across Asia. The company also held strong positions in beans, carrots, and other vegetable crops, generating approximately EUR 75 million in annual revenue with what KWS described as "above-average profitability."

The valuation arithmetic is worth examining carefully, because it reveals how the economics of plant breeding differ from the economics of most industrial businesses.

The EUR 400 million price tag implied a valuation of roughly five times revenue — expensive by industrial standards, but logical when benchmarked against comparable vegetable seed transactions. Established vegetable seed companies with deep germplasm and dominant positions in specific crops routinely command premium valuations for a simple reason: their competitive advantages are almost impossible to replicate. Germplasm depth — the genetic diversity accumulated over decades of systematic collection and breeding — is the ultimate cornered resource. No amount of venture capital can manufacture forty years of backcross populations and disease resistance screening data. Paying a premium for a niche monopoly was, by this logic, cheaper than trying to build it from nothing.

A second way to look at the valuation helps illuminate why the premium was justified.

The EUR 400 million price tag also implied a valuation of roughly five times revenue — a multiple that made value investors wince and growth investors nod. The question investors asked at the time — and it was a fair question — was whether KWS was paying too much for a niche business far from its core competency in field crops.

The answer depends on understanding both what KWS was buying and what it planned to do with it.

And the answer begins with a distinction that is easy to miss if you do not spend time in the seed industry — but that is fundamental to the economics of vegetable breeding.

What KWS was buying was not just a spinach company. That is how the financial press reported it, but it fundamentally misunderstood the strategic logic.

KWS was buying a beachhead in the global vegetable seed market — a market estimated at EUR 6 to 8 billion annually, growing at 4 to 6 percent per year, and characterised by structurally higher margins than field crops. Established vegetable seed companies like Rijk Zwaan and Enza Zaden operate at EBITDA margins of 30 percent or higher.

Let that number register: 30-plus percent EBITDA margins. Compare that to the mid-teens margins of diversified field crop seed companies. The margin differential is not accidental — it reflects the value of genetic precision in vegetables, where a new variety that resists a specific pathogen or extends shelf life by two days can command a significant price premium from commercial growers.

What KWS was buying was, in the language of Hamilton Helmer, a cornered resource — a germplasm library that represented decades of irreplaceable biological capital. But what it planned to do with that resource was where the real strategic vision lay.

What KWS planned to do with Pop Vriend was apply the molecular breeding tools it had developed over decades of sugarbeet and corn breeding — marker-assisted selection, genomic prediction models, high-throughput phenotyping, doubled-haploid techniques — to vegetables. Think of marker-assisted selection as GPS for plant breeding: instead of crossing plants and waiting years to see how the offspring perform in the field, breeders can test seedlings for specific DNA markers linked to desirable traits and identify winners in weeks rather than seasons. Genomic prediction goes even further, using statistical models to predict a plant's performance based on its entire genome before it even flowers. These tools, developed at enormous expense for high-value crops like corn, were being applied to vegetables for the first time — essentially giving Pop Vriend a genetic superpower it could never have afforded to develop on its own.

The integration strategy was deliberate and respectful — a lesson learned from decades of watching agricultural M&A failures where acquiring companies imposed their culture on the target and destroyed the very expertise they had paid for.

KWS moved its vegetable headquarters to the Netherlands, building a state-of-the-art facility in Andijk with 6,600 square metres of greenhouse space, dedicated laboratories, and 25 R&D specialists. The facility, powered by 360 solar panels on its roof, was a permanent commitment — not a temporary project office. On October 1, 2024, Pop Vriend Seeds was officially renamed KWS Vegetables Netherlands B.V., completing the symbolic and operational integration.

The renaming was more than administrative housekeeping. It was a statement: Pop Vriend is not a subsidiary or a portfolio company. It is KWS. The vegetable business is not an experiment or a side project — it is the future of the company.

The early results suggest the integration is working.

Revenue from the vegetables segment reached EUR 72.1 million in FY2024/25, growing at approximately 16 percent annually — roughly triple the growth rate of the overall seed market. The segment reported a negative EBIT of EUR 45.8 million — a number that looks alarming in isolation.

But context changes everything. Vegetable seed breeding is, like pharmaceutical drug development, a front-loaded investment game. You spend years and tens of millions of euros developing varieties across multiple crop species. Then, when a successful variety enters the market, it generates high-margin revenue for a decade or more because the germplasm and regulatory approvals are proprietary. Management has targeted full commercialisation of all strategic vegetable crops by 2028 and a top-five global position in vegetable seeds by 2030. Those are ambitious targets, but the trajectory is encouraging.

Whether KWS overpaid for Pop Vriend will not be answerable for another five years. That is the nature of seed industry M&A — the payoff comes not in the first year or the fifth, but in the tenth and the twentieth, when the breeding programmes that were accelerated by the acquisition produce varieties that dominate their categories. But the integration logic — bringing industrial-scale molecular biology tools to a fragmented market dominated by companies that breed primarily through traditional phenotypic selection — is precisely the kind of cross-pollination (pun fully intended) that creates disproportionate value when executed well.

V. Management: The Seventh Generation and the 2032 Vision

In the world of family-controlled German Mittelstand companies, the transition from one generation to the next is the moment of maximum risk. History is littered with examples of family firms that thrived under the founder or second generation and then collapsed when the heirs proved unequal to the challenge. The question that hangs over every family business is whether the next generation earned their position or inherited it.

Felix Büchting was born in 1974, studied agrobiology at the University of Stuttgart-Hohenheim, and completed his PhD in plant breeding with a molecular biology focus at Oregon State University. He is not a financial engineer parachuted into the CEO office by a private equity sponsor. He is a scientist who grew up in a family where dinner table conversation revolved around heterosis effects in sugarbeet and the finer points of cytoplasmic male sterility.

In Büchting's case, the answer appears to be: earned. His path to the CEO office was anything but a coronation. After joining KWS in 2005 as a trainee in the corn segment in France — a deliberate choice to start at the operational periphery rather than at headquarters — he left the company entirely in 2010. For six years, he worked at Symrise AG, the German flavours and fragrances company, managing agricultural raw materials sourcing. The departure was, by most accounts, a decision to prove himself in a different industry and avoid the perception that his career was a function of his surname rather than his competence. It is the kind of decision that speaks volumes about character — and about the family culture that shaped him. The Büchtings, for all their control over KWS, have never treated the CEO office as a birthright. Each generation has had to earn it.

He returned to KWS in 2016 as Regional Director for Cereals — a role that put him in charge of a significant business unit without the protective halo of the CEO's office. He was appointed to the Executive Board in 2019, and became CEO — or, in KWS's formal terminology, Spokesperson of the Executive Board — in January 2023. His contract was extended through the end of 2032, giving him a nine-year runway to execute the strategic transformation. In an era when average CEO tenure in listed companies is four to six years, a nine-year mandate tells you everything about the time horizon on which KWS operates. It also tells you something about the board's confidence in Büchting's vision — extending a CEO's contract through 2032 is not a decision made lightly, even by a family-controlled board.

The modesty of the CEO compensation — by the standards of companies with comparable revenue — is itself a signal about the culture.

The executive team around Büchting consists of three other board members: CFO Jörn Andreas, Nicolas Wielandt, and Sebastian Talg. Total compensation for the four-member board ranges from EUR 775,000 for the CFO to EUR 1.28 million for Büchting.

For a company with EUR 1.68 billion in revenue, these numbers are modest — strikingly so by the standards of German DAX or MDAX companies with comparable scale. But the modesty of the base pay is deliberate, because the real incentive mechanism is not the pay cheque. It is the compulsory share ownership.

The real incentive mechanism is not the pay cheque — it is the compulsory share ownership, and it is unlike anything at most public companies.

KWS requires Executive Board members to use a substantial portion of their variable compensation to purchase KWS shares, which are then subject to a five-year lock-up. No selling. No hedging. No derivatives. No escape hatches. For the duration of their tenure and for five years after departure, management's personal wealth is mechanically tied to the share price. This is not the "skin in the game" of a CEO who buys a symbolic number of shares with personal funds for the annual report photograph. This is structural alignment embedded in the compensation architecture.

But the share lock-up is only half the story. The alignment deepens with a mechanism that has few parallels in European corporate governance — one that most investors miss on first reading of the remuneration report.

It is called the Return on Sales penalty. If the company's return on sales falls below 10 percent over a multi-year measurement period, the long-term bonus is reduced by 25 percent. Below 9 percent, the reduction increases to 50 percent. Below 8 percent, the entire long-term bonus is forfeited — 100 percent, gone. There is also a clawback provision allowing KWS SE to reclaim variable payments already disbursed if subsequent events reveal that the targets were not genuinely met.

Consider what this structure incentivises and what it prevents — because the design of an incentive system reveals more about a company's true priorities than any mission statement or strategic plan. Management cannot profit from short-term cost cutting that destroys long-term R&D capability, because the share lock-up forces them to hold through the consequences. Management cannot tolerate margin erosion, because the ROS penalty destroys their bonus. And management cannot manipulate short-term metrics, because the clawback hangs over any suspect performance. From FY2024/25 onward, ESG targets were formally integrated into both short-term and long-term incentives, approved at the AGM with 98 percent shareholder support — a level of consensus that reflects the alignment between family values and institutional investor expectations on sustainability.

The governance architecture surrounding this management team is the 69 percent family iron grip described earlier. And here, the tension between governance and performance comes into sharpest focus. The question for outside shareholders is whether the benefits of long-term strategic continuity outweigh the costs of governance exclusion. The historical record suggests they do — KWS has compounded revenue at mid-single-digit rates for decades while maintaining R&D intensity that would be politically impossible at a company facing activist pressure. That track record is the strongest argument for the governance structure — and against the governance discount that the market applies. But the governance discount is real, and the illiquidity that results from the concentrated ownership means the stock can trade at significant discounts to intrinsic value for extended periods without any mechanism for correction.

The strategic framework for the next phase was laid out at the November 2025 Capital Markets Day in Einbeck — an event that, characteristically for KWS, received almost no coverage in the international financial press despite containing more strategic content than most companies deliver in a decade of investor days.

The theme was "Lead. Build. Advance." Lead in established crops — sugarbeet, European corn, cereals. Build the vegetable and food ingredients businesses. Advance innovation through gene editing and hybridisation of new crop species. Financial targets for 2025 to 2028 included 3 to 5 percent organic revenue growth, 19 to 21 percent EBITDA margins, and an increased dividend payout ratio of 25 to 30 percent, up from the historical 20 to 25 percent. The payout increase is worth noting because it was not forced by activist pressure or shareholder revolt. It was a voluntary gesture of discipline from a management team that controls 69 percent of the votes and could easily have justified reinvesting every euro. When a family-controlled company voluntarily increases its dividend payout ratio, it is sending a signal about capital discipline that carries more weight than the same decision at a widely held company where activists are watching.

But the most intriguing parts of the KWS story are not in the segments that appear in the earnings report. They are in the businesses and technologies that analysts barely mention — the hidden options on the future that a company with a 170-year time horizon has the luxury of developing without quarterly scrutiny. They are in the businesses and technologies that barely register in analyst coverage.

VI. Hidden Gems: The "Secret" Businesses inside KWS

If the previous sections described what KWS is — the headline business of breeding and selling seeds — this section explores what KWS could become. And the optionality embedded in the company's R&D portfolio is, in many ways, more interesting than the current earnings.

Beneath the headline numbers — sugarbeet, corn, cereals, vegetables — KWS operates a portfolio of emerging businesses and technologies that could materially reshape the company's profile over the next decade. These are not moonshots run by a skunkworks team in a forgotten building. They are logical extensions of KWS's core capability in plant genetics, applied to adjacent problems that happen to sit at the intersection of massive global megatrends.

Start with biologicals, because it is the most commercially advanced and the one most likely to contribute meaningful revenue in the near term.

The biologicals programme represents a fundamental shift in how seeds are prepared for planting. Traditional seed treatment involves coating seeds with synthetic chemical compounds — fungicides, insecticides, nematicides — that protect the germinating seedling from soil-borne pathogens and pests. The chemicals work, but they face escalating regulatory pressure in Europe and growing resistance from consumers and retailers who associate chemical seed treatments with broader concerns about agrochemical impacts on biodiversity and water quality.

KWS looked at this problem and saw an opportunity. Instead of fighting the regulatory trend, why not ride it? Instead of defending chemical seed treatment, why not replace it with something better?

In partnership with Evologic Technologies, an Austrian biotech company spun out of the Vienna University of Technology, KWS developed Biotens — a technology that encapsulates beneficial microorganisms, living bacteria and fungi, in plant-based microbeads for seed coating. The microbeads protect the organisms during storage and transport, then release them into the soil when the seed germinates. The bacteria colonise the root zone, improve nutrient uptake, and enhance the plant's natural stress tolerance.

The technical challenge is worth appreciating in detail, because it represents the core moat of the programme — and because it illustrates a broader principle about where competitive advantages come from in agricultural biotechnology. Living microorganisms are fragile. They die when exposed to desiccation, heat, or UV light — conditions that are routine in seed storage and transport. A bag of treated seed might sit in a warehouse for months before planting. The bacteria on that seed must survive, dormant but viable, through those months and then activate upon contact with soil moisture. Biotens solved this shelf-life problem by creating a protective matrix that maintains microbial viability for years on a dry seed. This is where the moat lies. A competitor can isolate the same bacterial strains from any handful of soil — the microbes are not proprietary. But replicating the stabilisation technology — the formulation that keeps living organisms alive for years in a desiccated state — is a separate and formidable challenge.

The commercial implications are significant. When you can stabilise living organisms on a seed for years, you have solved the shelf-life problem that has plagued biologicals companies since the beginning of the industry.

KWS launched its first commercial Biotens product in 2022: a sugarbeet biostimulant containing six bacterial strains. The company holds exclusive licences for application to sugarbeet, rapeseed, rye, and potatoes. The margin impact is elegant in its simplicity.

Biologicals add value per seed unit without requiring additional land, manufacturing capacity, or distribution infrastructure. The incremental cost is the microbeads and the coating process. The incremental revenue is a premium price per bag of seed.

If biologicals represent KWS's near-term hidden business, PROTEOMEX represents the medium-term one — and it sits at the intersection of two of the largest consumer trends in the global food industry.

PROTEOMEX is KWS's plant-based protein genetics platform. KWS is the European market leader in pea seeds. Peas have become the preferred raw material for plant-based protein products — pea milk, pea protein isolates, plant-based meat analogues — because they are allergen-friendly, sustainably produced, and nutritionally dense. But pea protein has a problem that anyone who has tried a pea-based burger or milk can attest to: it tastes like peas. The characteristic "beany" flavour, caused by lipoxygenase enzyme activity during processing, is the single largest barrier to mainstream adoption. Anyone who has tasted a first-generation pea protein shake knows exactly what this means — and why it matters for a market projected to be worth tens of billions.

The typical approach in the food industry is to solve this problem through processing — adding flavours, masking agents, or using chemical treatments to neutralise the off-notes. KWS is taking the opposite approach — solving the problem at the genetic level rather than the processing level. This is a distinction that matters enormously, because genetic solutions are permanent while processing solutions are costly and imperfect.

PROTEOMEX breeds pea varieties with naturally milder, neutral-flavoured proteins — eliminating the beany taste before the pea is even harvested, rather than trying to process it out after the fact. At the November 2025 Capital Markets Day, KWS partnered with vly, a Berlin food-tech startup, to present the first pea-protein milk alternative made from PROTEOMEX varieties. The collaboration is more than a marketing exercise — it is a proof of concept for an entirely new value chain.

If the programme succeeds at commercial scale, KWS positions itself as the upstream genetic designer in the plant protein value chain — capturing value at the seed level from a consumer trend worth billions.

The longest-dated option in KWS's portfolio — and the one with the most dramatic potential impact — is Aardevo, a 50/50 joint venture with J.R. Simplot Company — the Idaho-based agricultural conglomerate that is one of the world's largest suppliers of frozen french fries, primarily to McDonald's. Aardevo's mission sounds deceptively simple, but its implications are potentially revolutionary: convert the potato from a vegetatively propagated crop to a true-seed hybrid crop. The implications, however, are revolutionary. To understand why this matters, you need to understand how potatoes are currently grown — because the current method is, from a logistics standpoint, almost comically inefficient.

Today, potatoes are grown by cutting seed tubers into pieces and planting them — a method that is expensive, bulky, and prone to disease transmission. A single hectare of potato production requires roughly two tonnes of seed tubers. Shipping those tubers across oceans is prohibitively expensive, which is why potato varieties are often region-specific.

Now imagine the alternative. A hybrid potato grown from botanical seed — tiny seeds that weigh almost nothing, ship in envelopes, and start disease-free — would transform global potato logistics. A farmer in sub-Saharan Africa could receive a packet of seed in the mail rather than waiting for a container ship full of tubers. The implications for food security in the developing world are immense. Aardevo is early-stage — the biology of converting a vegetatively propagated crop to a true seed crop is extraordinarily difficult. But KWS's 50 percent ownership represents an unpriced option on one of the most potentially transformative developments in global food security. If it works, it could be worth multiples of the entire current market capitalisation. If it does not, the write-off is manageable.

The final hidden business is the one that ties all the others together: the digital platform myKWS, used by more than 100,000 farmers across KWS's markets. It integrates satellite imagery, crop monitoring, variety selection tools, field-specific recommendations, weather data, and market analyses. The platform won both the iF Design Award and the Red Dot Design Award in 2020 — unusual recognition for an agricultural technology tool, and a signal that KWS invested meaningfully in user experience. But the real strategic value of myKWS is not the tool itself — it is the data flywheel it creates: farmer usage data — which varieties perform best in which soil types, at which planting densities, under which weather conditions — feeds back to KWS breeders, who use it to improve variety development. And it builds switching costs: a farmer with years of accumulated field-specific data on myKWS faces a real cost in moving to a competitor's system. The data is portable in theory but sticky in practice.

Step back and look at the full portfolio of hidden businesses.

Each of these — biologicals, PROTEOMEX, Aardevo, myKWS — represents a call option on an agricultural megatrend. Any one could become material at scale. Collectively, they represent a portfolio of bets that no other single seed company is positioned to make. And this is the crucial point: the optionality is not accidental. It is the direct product of 170 years of accumulated genetic capability, a fortress balance sheet, and a governance structure that allows management to invest without the pressure of quarterly earnings expectations. But the strategic transformation that freed up the capital and management bandwidth to pursue them required an act of corporate courage that most public companies would never attempt.

VII. The Great Corn Exit

The great corn exit unfolded in three acts across eighteen months — each one building on the logic of the last, each one stripping away another layer of the old KWS and revealing the new one underneath.

In October 2023, KWS announced the sale of its 49 percent stake in the KENFENG-KWS joint venture, along with its Chinese corn portfolio and licences, to its partner Beidahuang Kenfeng Seed Co. The price was in the "mid-double-digit million euro" range, generating a positive earnings impact of EUR 28.1 million. The catalyst was straightforward and external: China had revised its GMO corn regulations to permit development only by domestic companies, effectively locking out foreign participants. It was a geopolitical door closing — and KWS, characteristically, took it as a signal to exit rather than a problem to fight. When the rules of the game change to make your participation structurally impossible, the rational response is to take your chips off the table.

China was the appetizer. Five months later, the far more consequential announcement came — the main course. On March 25, 2024, KWS revealed it would sell its entire South American corn business — all subsidiaries in Brazil, Argentina, Uruguay, and Paraguay, plus licences for KWS breeding material — to GDM, an Argentinian plant genetics company. The deal closed on August 2, 2024, at a price in the "mid-three-digit million euros," generating approximately EUR 110 million in one-time gains.

The gain was meaningful, but the strategic significance dwarfed the financial one. KWS had just sold the business that most analysts considered its growth engine. It had done so willingly, at what appeared to be a fair price, and it had used the proceeds to strengthen its balance sheet for the next phase of growth. It was the corporate equivalent of burning the boats after landing on a new shore.

This was not a fire sale. This was not a distressed divestiture. This was not a company shedding unprofitable assets to survive.

This was the opposite. The divested operation had been generating roughly EUR 320 million in annual revenue — growing, profitable at mid-single-digit operating margins, and operating in some of the world's most attractive agricultural markets. Selling it required admitting something that few corporate managements are willing to say out loud: not all growth is equally valuable. Growth in a market where you licence core technology from your direct competitors, paying them royalties on the technology that differentiates your products, is structurally less attractive than growth in markets where you own the entire value chain. Every KWS corn seed sold in South America contained a Bayer or Corteva biotech trait, with a royalty payment flowing to the competitor's bottom line. The margins KWS earned after those royalties were structurally lower than what the integrated players earned on their own seed. And as trait technology evolved, KWS's dependence on its competitors' willingness to licence the latest innovations deepened.

The final act came in June 2025. The corn exit was completed, when KWS agreed to sell its shares in AgReliant Genetics and its rights to corn genetic material in North America, taking a write-down of EUR 20.7 million partially offset by approximately EUR 30 million in positive operating effects. With that final transaction, KWS exited corn in every market outside Europe.

With those three transactions complete, the resulting portfolio is dramatically different from the one that existed three years earlier. KWS had, in effect, performed open-heart surgery on itself — removing a major organ and rerouting the circulatory system to feed different parts of the body. The four segments now tell a coherent strategic story.

Sugarbeet is the cash cow — EUR 871.8 million in revenue in FY2024/25 with a 42.1 percent EBIT margin, a staggering number for a seed business that reflects the biologically complex nature of the crop and KWS's near-monopolistic market position. European corn is the stabiliser and the beneficiary of the GMO-restricted regulatory environment — EUR 682.8 million in revenue, with a slight EBIT loss due to transition costs from the global exits, but with a strong long-term thesis in a market where EU GMO restrictions favour conventional breeding excellence. Cereals is the European backbone — EUR 263.3 million in revenue at a 12.2 percent EBIT margin, cash-generative with minimal capital intensity. And vegetables is the growth engine — EUR 72.1 million in revenue growing at 16 percent annually, with deep investment losses that represent the front-loaded cost of building a franchise.

The beauty of this portfolio construction is that each segment serves a different strategic function. The cash cow funds the R&D. The stabiliser provides scale. The backbone delivers consistent returns. And the growth engine promises to transform the earnings profile over the next decade. It is a portfolio designed for the long term — which is exactly what you would expect from a company controlled by families who measure time in generations.

If the segment mix tells you what KWS is becoming, the balance sheet tells you how it is paying for the transformation. Net debt dropped from EUR 385 million to EUR 61.6 million — just 0.2 times EBITDA. Read that number again: 0.2 times EBITDA. In an era when most industrial companies carry leverage of 2 to 3 times EBITDA, KWS is essentially unlevered. The balance sheet transformation created dry powder for the selective vegetable M&A that management identified as a priority at the Capital Markets Day. The equity ratio rose from 47 percent to approximately 60 percent. Free cash flow from continuing operations more than doubled to EUR 123.2 million.

The balance sheet is now a strategic weapon. In an industry where numerous family-owned European vegetable breeders are approaching generational transitions — the founders are aging, the next generation may not want to run a seed company, and the capital needs of modern molecular breeding are escalating — KWS has the financial firepower to be the acquirer of choice. The fortress balance sheet at 0.2 times leverage gives KWS optionality that no debt-laden competitor possesses.

The capital allocation message is unambiguous, and it deserves to be stated plainly because it is so rare. KWS sold low-margin, structurally disadvantaged growth in corn to fund high-margin, structurally advantaged growth in vegetables and biologicals. It is the kind of capital allocation discipline that Warren Buffett preaches but that most corporate managements find psychologically impossible to practice — because it requires admitting that some of your existing businesses, despite growing, are not worth keeping. It is the textbook capital allocation decision that business school professors use as case studies and that corporate managers almost never actually make — because selling a growing business requires admitting that growth alone is not valuable, that the quality of the growth matters more than its quantity. The corn exit was only possible because KWS's governance structure shields management from the short-term earnings pressure that would make such a decision politically impossible at a widely held public company.

VIII. The Playbook: Seven Powers, Five Forces, and Business Lessons

Every company claims to have competitive advantages. Most are exaggerating. The value of Hamilton Helmer's Seven Powers framework is that it provides a rigorous test for distinguishing genuine moats from marketing rhetoric.

Helmer's framework illuminates why KWS's competitive position is more durable than its modest public profile suggests.

The primary power — and the one that matters most — is cornered resource, specifically the germplasm bank. KWS has systematically collected, catalogued, and bred from plant genetic material for 170 years. The sugarbeet germplasm library alone represents tens of thousands of accessions — individual genetic samples, each characterised for sugar content, disease resistance, yield, bolting tendency, and dozens of other traits — that have been crossed, tested, selected, and improved across more than a century and a half of breeding cycles. This is not the kind of resource that a well-funded competitor can replicate. It is not a factory that can be built, a patent that will expire, or a software platform that can be cloned. Germplasm is biological compound interest, and the 170-year head start is a moat that gets wider every year.

The second power is scale economies in R&D — and here the numbers tell a story that is hard to appreciate without context. KWS invested EUR 349 million in research and development in FY2024/25 — 20.8 percent of revenue.

Let that number sink in. Twenty percent of revenue, year after year, plowed back into R&D. This ratio exceeds the pharmaceutical industry average and is among the highest of any industrial company globally. It is roughly double what most seed competitors spend as a percentage of revenue. And here is the crucial distinction. Unlike Bayer or Corteva, which split their R&D budgets across seeds, herbicides, fungicides, insecticides, and digital tools, KWS concentrates 100 percent of its R&D investment on genetics. Every single euro goes toward improving the core product — the seed. Every euro goes toward improving the core product — the seed.

The arithmetic is brutal for competitors. The scale economy operates as a competitive treadmill. Run the numbers.

A smaller competitor spending 20 percent of a EUR 200 million revenue base invests EUR 40 million in R&D. KWS, spending 20 percent of EUR 1.68 billion, invests nearly nine times as much. But the gap does not just exist in a single year. It compounds, because breeding is cumulative — each generation of research builds on the last. The competitor must not only match KWS's current spending but also close the gap created by decades of prior investment. This is the self-reinforcing cycle Helmer describes: the leader invests more, develops better varieties, captures more market share, generates more revenue, and invests still more.

The third power is counter-positioning — and it is the power that the Big Ag consolidation wave inadvertently handed to KWS. By remaining a pure-play seed company that does not sell chemicals, KWS occupies a unique position in the competitive landscape. For farmers who want to avoid the "Big Chem" lock-in — the system where buying Bayer's seed requires buying Bayer's herbicide — KWS is the credible independent alternative. KWS seed works with any crop protection programme, from any supplier. This independence was validated — dramatically — when Corteva announced its separation in September 2024. The chemistry-seed bundle model is under pressure, and KWS, never having bundled, finds itself ahead of a trend that its larger competitors are only now scrambling to address.

Helmer's framework tells us where the moats are. Porter's Five Forces tells us what competitive pressures operate around those moats — because having a moat is one thing, and being able to defend it is another.

Supplier power is moderate — KWS's primary inputs are land, scientific talent, and laboratory equipment, none of which is monopolised. The real supply constraint is PhD-level plant geneticists, a talent pool where Big Pharma and Big Ag compete fiercely, but the Einbeck campus and the Wageningen ecosystem provide recruiting advantages. Buyer power is fragmented — KWS sells to millions of individual farmers through distributor networks, and no single customer represents a meaningful share of revenue. This is the structural beauty of the seed business: your customer base is as fragmented as the landscape itself. Farmers switch seed varieties slowly because they want to observe multi-year field performance before committing. Threat of new entrants is minimal in sugarbeet — the germplasm barrier is essentially insurmountable. In vegetables, the barriers are lower but still significant, requiring a decade to build commercial variety portfolios. Threat of substitutes is low in the traditional sense — and this is worth emphasising because it is so unusual. There is no substitute for seed — but present in a structural sense through alternative sweeteners that could reduce demand for beet sugar and through long-term shifts toward precision fermentation. Competitive rivalry varies dramatically by segment — and the variation is the key to understanding KWS's strategic positioning.

Rivalry is intense in corn and cereals, where Bayer, Corteva, Syngenta, Limagrain, and BASF all compete aggressively. In sugarbeet, rivalry is minimal — a natural consequence of KWS's 70 percent market share and the biological barriers that make it nearly impossible for new entrants to challenge the leader. In vegetables, rivalry is high among entrenched Dutch competitors — Rijk Zwaan, Enza Zaden, Bejo Zaden — that have deep germplasm, strong customer relationships, and 30-plus percent EBITDA margins.

KWS is the challenger in this market, not the incumbent. That is a humbling position for a 170-year-old company to occupy, but it is also an honest one — and honesty about competitive position is a prerequisite for building a viable strategy.

The deepest business lesson from KWS — and the one that transcends the seed industry and applies to any company in any sector — is what "thinking in generations" actually makes possible when it is genuine rather than rhetorical. The corn exit was only viable because the governance structure insulates management from the short-term backlash that would follow at a widely held company. A CEO who sells EUR 320 million in growing revenue at a normal public company faces analyst downgrades, activist campaigns, and board pressure. A CEO whose family controls 69 percent of the votes and whose governance structure makes hostile intervention impossible can make that decision and execute it over 18 months without distraction. The KGaA structure, the family control, the illiquidity — all of these features that public market investors typically view as negatives are precisely the features that enable the long-term capital allocation decisions that create the most value.

The structure is the strategy. The constraint is the advantage. And the illiquidity is the price of patience.

This insight — that governance structures determine the range of possible strategies, and that the "worst" governance features from a short-term shareholder perspective can be the "best" features from a long-term value creation perspective — is the central lesson of the KWS story.

IX. The Analysis: Bear Case, Bull Case, and Key KPIs

Any honest assessment must begin with the bears, because it is the bears who identify the risks that the bulls are tempted to overlook.

The bear case rests on four pillars, each of which deserves careful consideration.

First, European gene editing regulation remains uncertain. The EU provisionally approved the NGT regulation in December 2025, creating a framework where NGT-1 organisms — those with modifications that could have occurred naturally — would be exempt from GMO labelling, while NGT-2 organisms would face stricter requirements. Implementation is expected around 2028, but the regulation remains politically contested. Germany abstained. Austria and Hungary opposed it. KWS has invested heavily in molecular biology infrastructure that positions it to benefit from gene editing liberalisation — management estimates CRISPR tools could accelerate breeding by approximately 30 percent. If NGT regulation is delayed, diluted, or reversed, the return on that investment is diminished.

Second, the competitive landscape is shifting in ways that are difficult to forecast. Chinese state-backed seed companies are building global capabilities. Chinese firms have historically focused on domestic rice and wheat, but government-backed consolidation and technology programmes are expanding their reach into new geographies and crop species. Whether this competitive pressure extends into sugarbeet and specialty vegetables remains an open question, but the trajectory is clear.

Third — and this is the risk that is most directly within management's control — the vegetable segment carries execution risk. At negative EUR 45.8 million in EBIT, the vegetables business is consuming significant capital during a multi-year development programme. The entrenched competitors — Rijk Zwaan, Enza Zaden, Bejo Zaden — have decades of germplasm depth and the advantage of private ownership that insulates them from public scrutiny. If KWS's vegetable strategy underperforms expectations, the accumulated losses represent meaningful capital misallocation.

Fourth, and perhaps most fundamentally, sugarbeet concentration risk is real and material. The segment's 42 percent EBIT margin funds nearly everything — the vegetable expansion, the biologicals programme, the R&D intensity, the dividend. But this extraordinary profitability depends on continued European demand for beet sugar. Health policy initiatives targeting sugar consumption, the development of alternative sweeteners, or trade liberalisation favouring cheaper cane sugar from Brazil could all pressure the cash cow. A margin compression from 42 percent to 30 percent in sugarbeet would fundamentally alter the company's ability to fund its strategic ambitions.

A word on liquidity, because it shapes the practical reality of investing in KWS regardless of the fundamental thesis. The stock's beta of 0.31 signals genuinely low correlation with broader markets — tied to biology, weather, and food demand, not to interest rates or consumer sentiment. But average daily volume of roughly 23,000 shares means institutional investors face significant market impact building or exiting positions, and the structural illiquidity discount is likely permanent.

Now for the bull case — and it is equally compelling, which is what makes KWS such a fascinating company to analyse.

Start with the crown jewel. Sugarbeet is a biological fortress. The crop's biennial lifecycle — requiring two years to complete its reproductive cycle and a period of cold-induced vernalisation to trigger flowering — makes breeding programmes extraordinarily slow and expensive. KWS's 70 percent market share is not a position that erodes quickly, because no competitor can accelerate the biology. Recent innovations — CONVISO SMART, a non-GMO herbicide tolerance system, and CR+, a multi-disease resistance platform — demonstrate that KWS is actively strengthening its dominance rather than merely defending it.

The second pillar of the bull case is the vegetable margin transformation. If it succeeds — and the early evidence is encouraging — it would fundamentally change the earnings profile. Established vegetable seed companies operate at 30-plus percent EBITDA margins. If KWS's vegetable segment approaches those levels at scale — say EUR 200 to 300 million in revenue at 25 percent EBITDA margins — the incremental contribution would materially shift group profitability from the current 20.9 percent EBITDA margin toward levels that would justify a significant re-rating.

The third pillar is the gene editing tailwind. If EU NGT regulation is implemented as currently envisioned, it would disproportionately benefit KWS as Europe's most molecularly capable seed company — the one that concentrates 100 percent of R&D on genetics. The fortress balance sheet provides firepower for selective vegetable M&A during a period when numerous family-owned European vegetable breeders are approaching generational transitions. And the optionality portfolio — biologicals, PROTEOMEX, Aardevo, myKWS — represents a collection of unpriced call options on agricultural megatrends, each of which could become material at scale without requiring significant additional capital because the underlying capabilities already exist.

For investors or observers who want to track the KWS story going forward without drowning in the complexity of four business segments across dozens of countries, two KPIs stand above all others — the twin vital signs that will tell you whether the strategic transformation is succeeding or failing.

The first is R&D spending as a percentage of revenue — currently 20.8 percent and remarkably stable around 20 percent for years. Any sustained decline below this level would signal a strategic shift away from the pure genetics model, potentially in response to margin pressure or a change in management priorities. The R&D ratio is the vital sign that tells you whether KWS is compounding genetic assets or harvesting them.

The second is vegetables segment revenue growth rate — currently approximately 16 percent annually. If R&D intensity tells you whether KWS is investing in the future, vegetable revenue growth tells you whether those investments are paying off.

This metric determines whether the vegetable margin transformation thesis plays out. If growth accelerates beyond 20 percent, the segment reaches critical mass faster and the breakeven timeline shortens. If growth decelerates to single digits, the years of accumulated investment losses stretch further and the strategic logic of the Pop Vriend acquisition comes under question. The trajectory of vegetable revenue is the single most important forward-looking indicator for the company's earnings evolution.

A note of near-term caution is warranted, because the most recent results remind us that even the best-positioned companies operate in the real world of weather, commodity prices, and farmer economics.

In February 2026, the H1 FY2025/26 results introduced a note of near-term caution. Revenue guidance was downgraded from approximately 3 percent growth to "at previous year's level," citing challenging agricultural markets and an expected decline in global sugarbeet acreage.

The downgrade is a useful reminder of a truth that applies to every seed company: genetics set the ceiling, but weather and commodity prices set the floor. The EBITDA margin target of 19 to 21 percent was maintained — a signal that while the top line may be weather-dependent, the underlying margin structure remains intact. The episode served as a reminder that seed companies, however excellent their genetics, ultimately depend on farmers' planting decisions — decisions driven by commodity prices, weather expectations, and government support programmes that lie outside any breeder's control.

X. Epilogue and References

Every business story has a beginning. Not all of them have the kind of continuity that allows you to trace a direct line from the founding to the present. KWS does.

The founding documents from 1856 Klein Wanzleben speak of a sugar refinery with ambitions to improve the raw material. One hundred and seventy years later, the sugar refinery is long gone, but the raw material improvement business has become a EUR 2.46 billion market capitalisation platform that spans sugarbeet, corn, cereals, vegetables, biologicals, plant proteins, and digital farming.

The November 2025 Capital Markets Day in Einbeck — themed "Lead. Build. Advance." — laid out the map for the next seven years with a clarity and specificity that is unusual for a company of this size. The financial targets are clear: 3 to 5 percent organic revenue growth, 19 to 21 percent EBITDA margins, and a dividend payout ratio of 25 to 30 percent. The strategic ambition is broader: lead in established crops, build the vegetable and food ingredients businesses to scale, and advance innovation through gene editing and hybridisation of new crop species. Each pillar represents a different time horizon — leading is about defending what exists today, building is about scaling what was acquired yesterday, and advancing is about creating the capabilities for what will matter in 2040.

The Wageningen food valley ecosystem, where KWS built its vegetable headquarters, represents the physical manifestation of that forward bet — a permanent commitment to a geography and a talent pool that signals this is not a diversification experiment but a generational strategy. Within fifty kilometres of KWS Vegetables Netherlands sit the research institutions, the competitor companies, the talent pool, and the innovation infrastructure that will shape the future of plant genetics. It is the Silicon Valley of seeds — and like Silicon Valley, the clustering effect creates a talent density and knowledge spillover that no individual company can replicate in isolation. KWS located itself there deliberately — because in the seed business, proximity to the world's best science is not a convenience but a competitive necessity. The Einbeck campus breeds the sugarbeet. The Wageningen campus breeds the future.

Together, they represent the two poles of KWS's identity — the deep roots in German agricultural tradition and the forward-looking ambition to reshape global food genetics.

For those who want to go deeper, the primary sources tell the story better than any summary.

KWS SAAT's FY2024/25 annual report, published after the fiscal year ending June 30, 2025, contains the detailed segment-level financials and strategic commentary that underpin the portfolio transformation described above. The report documents the continuing operations at EUR 1.68 billion in revenue, with sugarbeet at EUR 871.8 million, corn at EUR 682.8 million, cereals at EUR 263.3 million, and vegetables at EUR 72.1 million. The KWS remuneration report, available through the company's investor relations site, provides full detail on the mandatory share purchase, five-year lock-up, and Return on Sales penalty mechanisms that shape management incentives.

The EU NGT regulation, provisionally approved in December 2025 with implementation expected circa 2028, represents the most significant regulatory development for European plant breeding in decades and deserves close monitoring by anyone following the sector. KWS's molecular biology infrastructure and pure-genetics business model position it among the primary beneficiaries if the regulation is fully implemented — a regulatory tailwind that could accelerate breeding timelines by approximately 30 percent, according to management estimates.

The interplay between regulatory change and competitive positioning is one of the most important dynamics to watch in the European seed industry over the coming years.

There is a story — possibly apocryphal, but too good not to share — that when Felix Büchting was asked at a conference what keeps him up at night, he replied: "Nothing. I think about what the company will look like in 2050."

Whether the story is true or not, it captures something essential about KWS. This is a company whose time horizon makes the anxiety of quarterly capitalism look absurd. KWS remains what it has been since the seed trucks rolled west from Klein Wanzleben in 1945: a family-controlled company that bets on biology, invests with patience, and measures its time horizon not in quarters or even years but in generations.

The sugarbeet varieties still grow in the fields of the Magdeburger Börde, not far from where Klein Wanzleben once stood. The seed samples that were carried west in trucks in 1945 have, through seventy years of continuous breeding, produced varieties that yield more sugar per hectare than the founders could have imagined.

Whether the market will eventually value that patience as a premium rather than a discount — and whether the seventh generation can execute the transformation that turns a sugarbeet seed company into a global genetic platform for food — is the question that will determine whether KWS's next 170 years are as remarkable as its first.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music