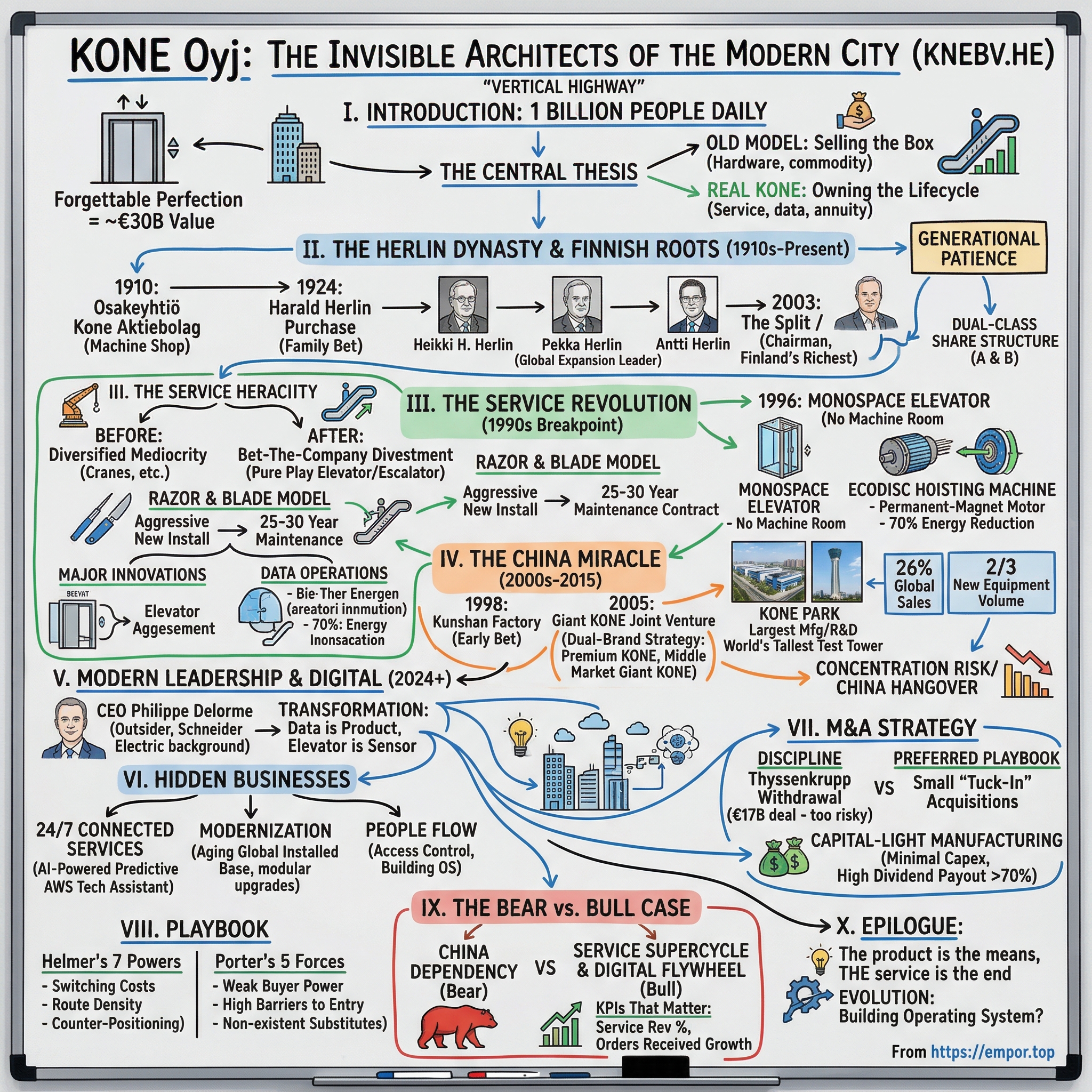

KONE Oyj: The Invisible Architects of the Modern City

I. Introduction: The Vertical Highway (0:00–0:05)

Picture this: you walk into a skyscraper in Shanghai, tap your phone against a turnstile, and an elevator whisks you to the forty-second floor without pressing a single button. The doors open silently, the ride was smooth, and you never once thought about the machine that moved you. That invisibility is the product. That forgettable perfection is worth roughly thirty billion euros.

KONE Oyj, the Finnish elevator and escalator giant, moves over one billion people every single day. Not per year. Per day. That number is so large it almost loses meaning, so consider it differently: KONE's installed base of elevators and escalators handles more daily passenger trips than the entire global airline industry. Every morning, in cities from Helsinki to Hong Kong, Mumbai to Manhattan, KONE's equipment serves as the unseen circulatory system that makes vertical life possible. Without it, modern cities simply do not function. A fifty-story office tower with broken elevators is not an office tower; it is a concrete monument to uselessness.

Most investors, when they hear "elevator company," think of heavy steel, greasy cables, and low-margin industrial hardware. They picture a business that competes on price to install a metal box in a shaft. That mental model is about thirty years out of date. The real KONE is a high-margin service and data business that happens to manufacture elevators as a customer acquisition tool. The company earns its keep not by selling the box, but by owning the lifecycle of every box it installs — maintaining it, monitoring it with sensors and AI, modernizing it when it ages, and eventually replacing it with the next generation. Each new elevator sold is not a transaction. It is the opening of a thirty-year annuity stream.

This is the central thesis of KONE: the transition from "selling the box" to "owning the lifecycle." It is a playbook that turns a commodity product into a proprietary service, a hardware sale into a software subscription, and a one-time customer into a captive one. The elevator industry's Big Four — Otis, Schindler, TK Elevator, and KONE — collectively control more than half the global market and earn pretax returns on capital north of twenty percent each. But KONE, arguably more than any of its peers, has mastered the art of making that transition look effortless. How a small Finnish machine shop pulled this off over the course of a century is a story worth telling.

II. The Herlin Dynasty and Finnish Roots (0:05–0:15)

In 1910, a company called Osakeyhtiö Kone Aktiebolag was registered as a subsidiary of Gottfr. Strömberg Oy, a Finnish electrical equipment maker. "Kone" means "machine" in Finnish, and the name was apt — this was a modest machine shop with about fifty employees, importing and assembling elevators under a license from the American firm Graham Brothers. Finland at the time was a Grand Duchy of the Russian Empire, sparsely populated, and not exactly the place you would bet on producing a future global industrial champion. But that smallness turned out to be the company's first strategic advantage. With a domestic market too tiny to sustain any real ambition, KONE was forced to look outward from the very beginning. Internationalization was not a growth strategy; it was a survival instinct.

The pivotal moment came in 1924, when a businessman named Harald Herlin purchased the company. This was not a corporate acquisition in the modern sense — it was a family bet, and it set the course for a century. Harald became chairman and ran the business until 1941, when his son Heikki H. Herlin took over, serving as president from 1932 onward. Heikki, in turn, passed the torch to his son Pekka Herlin in 1964. Pekka was the architect of KONE's first great expansion. Under his leadership from 1964 to 1986 as president, and then as chairman from 1987 until his death in 2003, KONE transformed from a Nordic industrial player into a genuinely international competitor. Pekka understood something that many family-controlled companies miss: the home market would never be enough, and the only way to survive was to build scale through aggressive international expansion and acquisition.

When Pekka died in 2003, the succession was not entirely smooth. It was discovered that he had rewritten his will in 1999, bequeathing the majority of his KONE holdings to his eldest son, Antti. A family dispute followed. The resolution was Solomonic: the company was effectively split in two. Antti retained the controlling stake in the original KONE elevator business, while his three siblings were given control of Cargotec, a heavy cargo machinery division. All four Herlin siblings became billionaires. But the split clarified KONE's identity. No longer a diversified conglomerate with interests in everything from cranes to cargo handling, KONE became a pure-play elevator and escalator company — a focus that would prove enormously valuable.

Antti Herlin, who had served as CEO since 1996 and deputy chairman before that, became chairman in 2003. Today, he remains Finland's richest person, with a net worth estimated by Forbes at roughly $4.7 billion. His ownership, structured through holding companies Holding Manutas and Security Trading, represents approximately 51% of KONE's shares and a commanding 62.7% of the voting rights. This is possible because of KONE's dual-class share structure: Class A shares carry significantly more votes than the publicly traded Class B shares. The structure is a fortress against short-termist activist investors, hostile takeovers, and the kind of quarterly panic that afflicts many publicly traded industrial companies.

What the Herlin dynasty provides is something money cannot easily buy: generational patience. When your controlling shareholder has a century-long family legacy in the business, you can make twenty-year bets. You can invest in China a decade before the returns materialize. You can walk away from an eighteen-billion-euro acquisition because the risk-reward is wrong. You can spend years building a digital services platform without the market punishing you for short-term margin compression. The Herlin family's stewardship is the invisible hand that shapes every major strategic decision at KONE, and it is arguably the company's single most underappreciated asset. Today, the next generation is already in position: Jussi Herlin serves as Vice Chair of the Board, and Anna Herlin sits as a Board member.

III. The Great Inflection Point: The Service Revolution (0:15–0:35)

By the late 1980s, KONE had a problem that many successful industrial companies eventually face: it had diversified itself into mediocrity. The company had expanded into cranes, wood-handling equipment, and various other machinery lines through the boom decades of the 1960s and 1970s. These businesses were fine individually, but together they created a conglomerate that was lagging behind focused competitors like Otis and Schindler in its core elevator business. Technology and production costs were slipping. The company was spread too thin.

The decision that changed everything happened between 1993 and 1995, when KONE divested every business except elevators and escalators. This was not a minor portfolio trim; it was a bet-the-company strategic reset. The logic was straightforward but required courage: elevators and escalators were the only businesses where KONE had a realistic path to global leadership, and the only ones with the right economic characteristics to justify the effort. Everything else was a distraction.

But the real insight was not just about what to sell. It was about what to build. Beginning in the 1980s and accelerating through the 1990s, KONE's leadership recognized a profound truth about the elevator business: manufacturing and installing elevators is a low-margin commodity activity, but maintaining them is a gold mine. Think about the economics. A new elevator installation is a competitive bid, often won on price, with margins that can be painfully thin. But once that elevator is installed in a fifty-story building, the building owner needs someone to maintain it — inspecting, lubricating, adjusting, replacing worn parts, responding to emergency calls, ensuring compliance with safety codes. That maintenance contract typically runs for the life of the equipment, which can easily be twenty-five to thirty years. And the original equipment manufacturer has a massive advantage in winning and retaining that contract, because they designed the system, they have the proprietary parts, they wrote the service manuals, and they trained the technicians.

This is the "razor and blade" model applied to vertical transportation. Price the razor (the new elevator installation) aggressively to capture the installed base, then earn the real money on the blades (decades of maintenance contracts). By 1997, KONE held maintenance and modernization contracts on more than 400,000 elevators worldwide. By the late 1990s, new equipment sales represented only 41% of the company's revenue. The majority of the business had shifted to service and maintenance — a recurring, high-margin, capital-light revenue stream with extraordinary customer retention.

The cultural shift required to execute this transition should not be underestimated. KONE had to transform its identity from "engineers who build" to "technicians who serve." This is harder than it sounds. Engineers take pride in designing and manufacturing complex machines. Service technicians take pride in keeping those machines running perfectly, day after day, in the field. These are different skill sets, different mindsets, and different career paths. KONE invested heavily in training, in field service infrastructure, and in building a culture that elevated the importance of the service technician to the same status as the design engineer.

The transition was turbocharged by a genuine technological breakthrough. In 1996, KONE introduced the MonoSpace elevator and the EcoDisc hoisting machine. This was, without exaggeration, revolutionary. Traditional elevators required a dedicated machine room — typically located at the top of the building — to house the heavy motors and gearboxes that moved the car. The machine room added significant construction cost, consumed valuable building space, and complicated architectural design. KONE's MonoSpace eliminated the machine room entirely. The EcoDisc used a compact permanent-magnet electric motor that was small enough to fit inside the elevator shaft itself. No machine room, no wasted floor space, lower installation costs, and dramatically better energy efficiency — the EcoDisc reduced energy consumption by as much as seventy percent compared to conventional geared motors.

The MonoSpace was hailed as the most important innovation in the elevator industry in decades, and it gave KONE a genuine technological edge over competitors. More importantly, it lowered the cost of new installations, making it easier to price aggressively and capture more of the installed base — which then fed the service revenue machine. This combination of strategic refocus, cultural transformation, and technological innovation is the foundation of KONE's current financial profile: return on invested capital consistently above twenty percent, operating margins approaching twelve percent, and a business model that generates enormous free cash flow with minimal capital expenditure requirements.

For investors, the key takeaway from this era is structural. The service revolution was not a one-time earnings boost; it permanently changed the economic engine of the business. Every elevator KONE installs today is an annuity that will generate service revenue for decades. The installed base is the moat.

IV. The China Miracle (2000s–2015) (0:35–0:55)

In the early 2000s, China was beginning the largest urbanization project in human history. Hundreds of millions of people were moving from rural villages to cities, and those cities needed buildings — apartment towers, office complexes, shopping malls, metro stations, hospitals, airports. Every one of those buildings needed elevators and escalators. The question for the global elevator industry was not whether China would be a big market, but how big, and who would be positioned to capture it.

KONE's answer was to go all-in. While competitors like Otis and Schindler were cautious, treating China as one market among many and hedging their bets with incremental investments, KONE made a disproportionate strategic commitment. The company established its first Chinese manufacturing facility in Kunshan, near Shanghai, in 1998. This was early — at a time when many Western industrial companies were still debating whether China's growth was sustainable or a bubble waiting to burst. KONE bet that it was sustainable, and they structured their entire Asian strategy around that conviction.

The critical move came in 2005 with the formation of the Giant KONE Elevator joint venture. This was not a typical joint venture where a Western company licenses its brand and technology to a local partner and collects royalties. KONE engineered a dual-brand strategy that was far more ambitious. The premium "KONE" brand served the top tier of the market — international developers, Class A office towers, luxury residential projects — while the "Giant KONE" brand targeted the massive middle market of standard residential and commercial construction. This dual-brand approach let KONE compete across the entire price spectrum without diluting its premium positioning. It was a strategic masterstroke. In a market where hundreds of millions of apartments were being built in a single decade, leaving the mid-market to local competitors would have been leaving enormous volume on the table.

The supply chain redesign required to serve China was equally impressive. Chinese construction operated at what became known as "China Speed" — project timelines that would be unimaginable in Europe or North America. A forty-story residential tower might go from groundbreaking to occupancy in eighteen months. Elevator manufacturers needed to match that pace or lose the contract. KONE invested in building its Kunshan Industrial Park into a manufacturing colossus. At roughly 240,000 square meters, the purpose-built KONE Park includes three elevator factories and an escalator factory. It became KONE's largest manufacturing unit in the world, as well as its largest overseas R&D center, featuring the world's tallest elevator test tower above ground. This was not just a factory — it was an integrated manufacturing and innovation campus designed to serve the Chinese market at Chinese speed.

By the 2010s, KONE had delivered more than 1.6 million units in China and maintained over 600,000 elevators in the country. China became KONE's single largest market globally, accounting for approximately 26% of global sales and, more importantly, representing roughly two-thirds of KONE's new equipment market volumes worldwide. The scale of this achievement is remarkable: a Finnish company with no natural geographic advantage in Asia had built a dominant position in the world's most competitive and fastest-growing elevator market.

In 2016, KONE completed the full acquisition of Giant KONE, bringing the entire Chinese operation under direct KONE ownership and control. This move gave KONE full operational integration, allowing it to push its digital services, maintenance platforms, and quality standards across the entire Giant KONE installed base. It also positioned the company for the next phase of the Chinese market: the transition from new installations (which were beginning to slow as the construction boom matured) to maintenance and modernization of the enormous installed base that had been built over the prior two decades.

The China bet paid off spectacularly. But it also created a concentration risk that shapes the investment debate around KONE to this day. When one country accounts for more than a quarter of your revenue and two-thirds of your new equipment volume, any structural slowdown in that country hits hard. The Chinese real estate crisis that began in 2021-2022, with major developers like Evergrande and Country Garden defaulting on their debts, sent tremors through the entire elevator industry. KONE's new equipment orders in China declined meaningfully, and the stock price reflected the anxiety. Whether this is a cyclical dip in a market that will recover, or a permanent structural shift in Chinese construction patterns, remains the single most important question for KONE investors. We will return to this in the bear and bull cases.

V. Modern Leadership: From Industrial to Digital (0:55–1:10)

On October 25, 2023, KONE made an announcement that surprised many industry watchers. Philippe Delorme, a French executive with over twenty-five years at Schneider Electric, would become President and CEO of KONE Corporation effective January 1, 2024. This was a departure from KONE's historical pattern. For decades, the company had been led by internal veterans and Herlin family members. Antti Herlin served as CEO from 1996 to 2006. His successor, Matti Alahuhta, was a Nokia veteran but spent over a decade at KONE before taking the top job. Henrik Ehrnrooth, who succeeded Alahuhta, was a KONE insider who had risen through the ranks. Delorme was different — an outsider, and a deliberate signal that KONE's next chapter would require a different kind of leadership.

Delorme's background at Schneider Electric was specifically relevant. As Executive Vice President of Europe Operations and a member of Schneider's Executive Committee from 2009 to 2023, he had led the transformation of a traditional electrical equipment company into a software-driven energy management and automation business. He understood how to layer digital services on top of industrial hardware, how to build recurring software revenue streams, and how to manage the cultural tension between hardware engineers and software product managers. These were exactly the skills KONE needed for its next strategic phase.

The mandate Delorme inherited was clear: accelerate KONE's transformation from an elevator manufacturer that offers digital services into a digital services company that manufactures elevators. The distinction might sound semantic, but it reflects a fundamental shift in how the company creates and captures value. In the old model, the elevator is the product and maintenance is the aftermarket. In the new model, the data and software platform is the product, and the elevator is the sensor network that generates the data.

Educated at Centrale Paris and holding an MBA from Sciences Po Paris, Delorme brought both engineering depth and business sophistication. His early moves at KONE focused on innovation and digital technologies as differentiators for growth, pushing the organization to think of itself as a technology company with industrial roots rather than an industrial company dabbling in technology.

But here is where the Herlin governance structure proves its worth. In many public companies, bringing in a transformative external CEO creates tension with the board, risk of strategic whiplash, and vulnerability to activist pressure if short-term results disappoint. At KONE, Antti Herlin remains the anchor as Chairman, with 62.7% of voting rights. The family's long-term orientation provides air cover for Delorme to make investments in digital infrastructure, AI capabilities, and software talent that might depress margins in the short term but build enormous value over a decade. The owner-operator mentality persists even with professional management at the helm.

The management incentive structure reinforces this alignment. KONE's executive compensation is tied to long-term value creation metrics rather than short-term earnings beats. The dual-class share structure — Class A shares carrying disproportionate votes relative to Class B shares traded on the Helsinki exchange — means that the family's interests and management's incentives are aligned on the same time horizon. This is not a company where the CEO needs to worry about a proxy fight if next quarter's margins dip by fifty basis points.

For investors evaluating KONE's leadership transition, the critical question is execution. The strategy is sound — every industrial company in the world is trying to add software and services revenue. But very few have the installed base, the data infrastructure, and the customer relationships to actually pull it off. KONE does, and it now has a CEO with the specific experience to make it happen.

VI. Hidden Businesses: The "Invisible" Growth Engines (1:10–1:25)

Walk into the maintenance control center of a major commercial building in London or Tokyo, and you might notice something unexpected: a real-time dashboard showing the status of every elevator in the building — door cycle counts, motor temperature, stopping accuracy, ride smoothness, number of starts per hour. This is KONE 24/7 Connected Services, and it represents something far more valuable than a fancy monitoring screen. It is the embryo of a high-growth, AI-powered services business embedded inside a century-old industrial company.

Here is how it works. KONE installs IoT sensors on elevators and escalators that continuously measure dozens of variables — door operations, motor temperature, vibration patterns, stopping accuracy, energy consumption, passenger traffic patterns. This data streams via wireless connection to KONE's cloud-based analytics platform, where AI algorithms analyze the information in real time. The system does not just detect faults; it predicts them before they happen. A subtle change in vibration frequency might indicate that a bearing will fail in three weeks. A gradual drift in stopping accuracy might signal that the brake pads need replacement. The system identifies these symptoms, diagnoses the likely cause, and dispatches a maintenance technician with the right parts and the right instructions before the equipment actually breaks down.

The results are striking. According to KONE, the platform has achieved 70% more fault detection and 40% fewer equipment issues compared to traditional scheduled maintenance. In 2025, KONE took this further by co-developing with Amazon Web Services a "Technician Assistant" — a generative AI tool that uses large language models to provide field technicians with instant answers based on the specific asset's maintenance history, IoT data, and relevant technical documentation. Imagine a technician standing in front of a malfunctioning elevator, asking their phone a question, and getting a diagnosis specific to that exact unit's history and sensor readings. That is what KONE is building.

The strategic significance of this platform extends beyond maintenance efficiency. Connected services create a data moat. Every day, KONE's connected equipment generates millions of data points about how elevators perform in different building types, different climates, different usage patterns. This data makes the AI models better, which makes the predictions more accurate, which makes the service more valuable, which gives KONE more reason to connect more equipment, which generates more data. It is a classic flywheel, and it creates a competitive advantage that deepens over time. A new entrant cannot simply build the same platform because they lack the training data from hundreds of thousands of connected units.

The second hidden growth engine is modernization. This is the business of upgrading or replacing aging elevator equipment in existing buildings. Think of it as the renovation market for vertical transportation. A building that was constructed in 1985 might have perfectly good structural bones, but its elevators are slow, energy-hungry, unreliable, and lack modern safety features. The building owner has two choices: tear everything out and install completely new equipment, or modernize — replacing key components like the drive system, controller, and doors while keeping the basic structure. Modernization is typically less expensive and less disruptive than full replacement, and KONE has become expert at offering modular upgrade packages that breathe new life into aging equipment.

This market is enormous and growing for a simple demographic reason: the massive wave of elevator installations that occurred globally between the 1960s and 1990s is now reaching the age where modernization becomes necessary. KONE estimates that millions of elevators worldwide are growing old and in need of upgrades. In China, the enormous installed base built during the construction boom of the 2000s and 2010s will begin entering the modernization cycle within the next decade. In Europe and North America, buildings from the postwar construction era are already deep in modernization territory. KONE's modernization services are brand-agnostic — they can modernize any elevator from any manufacturer — which dramatically expands their addressable market beyond their own installed base. And modernization margins are excellent, often higher than new installation margins, because the work is less competitive and more relationship-driven.

The third hidden engine is People Flow — KONE's venture into access control, building security, and "people flow" software. KONE Office Flow integrates elevator dispatch with building access control, allowing tenants to tap their smartphone or access card and be automatically routed to the correct elevator going to their floor. KONE Access integrates with turnstiles, building doors, and elevator systems to create a seamless, touchless movement experience throughout a building. These products transform KONE from an elevator company into a building operating system company. The addressable market expands from "buildings that need elevators" to "buildings that need to move people efficiently and securely." Each of these solutions deepens the customer relationship, increases switching costs, and generates recurring software revenue.

VII. M&A Strategy: The Discipline of Not Overpaying (1:25–1:40)

In February 2020, KONE and its partner CVC Capital Partners withdrew from discussions to acquire Thyssenkrupp's Elevator Technology business. The bid was reportedly worth approximately seventeen billion euros — one of the largest industrial deals of the decade if it had closed. The withdrawal surprised many observers who expected KONE to fight for a deal that would have made it the world's undisputed leader in elevators by a wide margin.

The backstory reveals a company with uncommon valuation discipline. Thyssenkrupp, the troubled German industrial conglomerate, was desperate to sell its elevator division — its most profitable asset — to raise cash for its struggling steel and other industrial operations. The elevator business was genuinely excellent, with a massive global installed base and strong service margins. KONE saw the strategic logic: acquiring Thyssenkrupp Elevator would have approximately doubled KONE's size and created overwhelming scale advantages in service route density.

But the risks were formidable. Antitrust regulators in Europe would almost certainly have required significant divestitures — potentially stripping away exactly the service routes and installed base that made the deal attractive in the first place. More critically, Thyssenkrupp's deteriorating financial condition created execution risk. Integrating a seventeen-billion-euro acquisition while the seller is in financial distress, during a period of antitrust uncertainty, with potential divestiture requirements, was a recipe for value destruction. KONE's management and the Herlin family made the disciplined call: the price was too high, the risks too uncertain, the integration too complex. They walked away. Advent International and Cinven ultimately acquired the business for approximately seventeen billion euros. It was the deal that got away, but KONE's restraint said everything about how the company approaches capital allocation.

KONE's preferred M&A playbook is the opposite of mega-mergers. The company executes a steady stream of small "tuck-in" acquisitions — buying local elevator service companies in target markets and immediately integrating them into KONE's global platform. The list is long and unglamorous: Fairway Elevator Company in Philadelphia, Advanced Elevator Technologies in Boston, Continental Services in Florida, Detroit Elevator Company in Michigan, Capitol Elevator in Sacramento. Across thirteen acquisitions in seven countries, the pattern is consistent. KONE identifies a local service shop with a solid installed base and good customer relationships but limited technology and scale. It acquires the company at a modest valuation — typically in the range of six to eight times EBITDA for service businesses of this type — and then plugs it into KONE's digital platform, supply chain, and training infrastructure. The result is usually a meaningful improvement in margins as the acquired company benefits from KONE's scale in parts procurement, its predictive maintenance technology, and its operational best practices.

This approach compounds over time. Each tuck-in acquisition adds to the installed base, which adds to the service revenue stream, which improves route density, which improves margins, which generates more free cash flow, which funds the next acquisition. It is a patient, unsexy, relentlessly effective capital deployment strategy. And it works precisely because KONE has the discipline to avoid the ego-driven mega-deal and focus on the boring but profitable work of buying local service portfolios one at a time.

The capital allocation discipline extends to shareholder returns. KONE runs what can only be described as a capital-light manufacturing model. The company requires minimal reinvestment in property and equipment relative to its revenue — capital expenditures have run at barely one to two percent of revenue in recent years. This means that the vast majority of operating cash flow — which hit 1.3 billion euros in 2025 — is available for dividends and opportunistic investments. KONE paid roughly 932 million euros in dividends in 2025, representing a payout ratio well above seventy percent. The company has historically supplemented regular dividends with special dividends when cash accumulates beyond what the business needs. In 2022, total dividends paid reached nearly 1.1 billion euros.

The combination of high returns on invested capital, minimal reinvestment requirements, and disciplined capital allocation creates a financial profile that is unusual for an industrial company. KONE generates cash like a software company but trades like a manufacturer. For long-term investors, the question is whether the market will eventually re-rate the stock to reflect the true quality of the underlying business model.

VIII. Playbook: Hamilton's 7 Powers and Porter's 5 Forces (1:40–2:00)

To understand why KONE's competitive position is so durable, it helps to run the business through the two most widely used frameworks for analyzing economic moats.

Switching Costs: The Heaviest Moat. Hamilton Helmer's 7 Powers framework identifies switching costs as one of the most powerful sources of competitive advantage. In KONE's case, switching costs are not just high — they are physically embedded in concrete and steel. Once an elevator is installed in a fifty-story building, it is not coming out. The mechanical system is integrated into the building's structure, the electrical systems are wired to proprietary controllers, the safety systems are calibrated to specific parameters, and the entire installation is certified by local regulators. Switching to a different manufacturer's equipment does not mean changing a vendor; it means ripping out a major building system, which can cost millions of dollars and take months while the building is partially inoperable. In practice, this almost never happens. The original equipment manufacturer retains the maintenance contract for the life of the equipment, which can be twenty-five to thirty years or longer. This is not a theoretical moat; it is a physical one.

Scale Economies and Route Density. The second major power is scale economies, expressed through what the industry calls "route density." A KONE service technician based in central London might maintain thirty elevators within a two-mile radius. Each additional elevator KONE wins in that same neighborhood makes the technician more productive — they spend less time traveling between jobs and more time actually servicing equipment. The fixed cost of the technician, the van, the tools, and the parts inventory gets spread across more units. This means that the market leader in any given city or neighborhood has a structural cost advantage over smaller competitors. It is the same dynamic that makes waste collection and pest control such attractive businesses: route density is a compounding advantage that is extremely difficult for smaller players to replicate.

Counter-Positioning. There is a subtler power at work here as well. KONE's shift from hardware to digital services represents a form of counter-positioning against traditional competitors and independent maintenance companies. The independent service shops that compete for maintenance contracts cannot afford to build an IoT platform, an AI analytics engine, and a global data infrastructure. They compete on price and personal relationships, but they cannot match the predictive maintenance capabilities that connected services provide. And KONE's own competitors — Otis and Schindler — are pursuing similar strategies, but KONE's early and aggressive investment in connected services has given it a meaningful data advantage.

Porter's Five Forces: An Oligopoly with Reinforcing Barriers. Porter's framework paints an equally favorable picture. The threat of new entrants is minimal. The elevator industry requires massive up-front investment in R&D, manufacturing, and — most critically — a global service network. Safety regulations vary by country and are extraordinarily demanding; getting certified to install and maintain elevators in dozens of jurisdictions takes years and millions of dollars. The combination of regulatory barriers, capital requirements, and the need for a local service presence in every major city makes it nearly impossible for a new competitor to enter the industry at scale. There has not been a meaningful new entrant in the global elevator market in decades.

The bargaining power of buyers is structurally weak. The customers — property developers, building owners, property managers — are highly fragmented. There are millions of building owners in the world, each making individual purchase decisions. They face four major elevator suppliers who dominate the market. This classic fragmented-buyer-vs-concentrated-seller dynamic gives the Big Four significant pricing power, particularly in the service and maintenance segments where switching costs make the buyer a captive customer.

Supplier power is moderate but manageable. Elevator components are largely commodity inputs — steel, electrical motors, cables, circuit boards — sourced from multiple suppliers. KONE's scale gives it strong bargaining leverage in procurement.

The threat of substitutes is essentially nonexistent. There is no alternative to elevators in multi-story buildings. Stairs are not a substitute for a forty-story office tower. And within the elevator category, the product is mature and standardized enough that differentiation occurs primarily through service quality and digital capabilities rather than fundamental product differences.

Competitive rivalry among the Big Four is intense but rational. This is a classic oligopoly where the major players compete vigorously for new installation contracts but maintain discipline on pricing in the vastly more profitable service segment. Price wars in service would be mutually destructive, and all four companies understand this. The industry structure naturally encourages rational competition — a characteristic that sustains high returns across the cycle.

IX. The Bear vs. Bull Case (2:00–2:15)

The Bear Case: The China Hangover. The most significant risk to KONE's investment case is concentrated in a single word: China. The country accounts for approximately 26% of KONE's revenue and roughly two-thirds of its new equipment volume. The Chinese real estate sector has experienced a severe structural downturn since 2021, with major developers defaulting, housing starts declining, and overall construction activity contracting. This is not a typical cyclical downturn. The demographic underpinnings of China's housing market have shifted: population growth has stalled, urbanization rates are approaching the levels of developed economies, and the era of building entire cities from scratch is likely over. If the Chinese new installation market settles permanently at a level significantly below its 2020 peak, KONE will have an oversized manufacturing and sales infrastructure in a market that no longer needs it. The Kunshan mega-factory, the dual-brand strategy, the thousands of technicians — all of these assets become liabilities in a structurally smaller market.

The second bear argument is valuation. KONE has historically traded at a premium to the broader industrials sector, reflecting its high returns on capital and recurring revenue mix. At recent prices around 57 euros per share, the stock trades at roughly 19 times trailing EBITDA and 30 times trailing earnings. If earnings growth stalls — because China drags down new equipment volumes and the service transition takes longer than expected — the premium multiple becomes harder to justify. The stock could re-rate downward even if the underlying business remains healthy.

There is also a competitive risk worth monitoring. Otis Worldwide, spun out of United Technologies in 2020, is a focused, publicly traded pure-play with its own digital transformation agenda. TK Elevator, under private equity ownership, is investing aggressively. And Chinese domestic manufacturers like SJEC and Canny are gaining share in the lower end of the market. If the Big Four's oligopoly loosens, margins could face pressure.

The Bull Case: The Service Supercycle. The bull case rests on a simple but powerful thesis: KONE is in the early innings of a multi-decade service and modernization supercycle that will more than offset any decline in Chinese new installations.

Start with the installed base. KONE maintains hundreds of thousands of elevators and escalators worldwide. That installed base is growing every year, even if new installation growth slows, because the stock of existing equipment accumulates faster than old equipment is decommissioned. Each unit in the installed base generates recurring service revenue. As more of that equipment gets connected to KONE 24/7, the revenue per unit increases because connected services command premium pricing. The math is straightforward: a growing installed base, multiplied by increasing revenue per unit, equals a powerful organic growth engine that requires minimal capital investment.

Next, consider modernization. The global installed base of elevators includes millions of units that were installed between 1960 and 2000. These units are entering the window where modernization becomes necessary — old enough to be inefficient and unreliable, but installed in buildings that remain structurally sound. KONE's modernization business is brand-agnostic, meaning it can modernize elevators originally installed by competitors. This dramatically expands the addressable market beyond KONE's own installed base.

The digital flywheel is perhaps the most underappreciated element of the bull case. Every connected elevator generates data that improves KONE's predictive models. Better predictions mean less downtime, which means happier customers, which means higher retention, which means more connected units, which means more data. This is a winner-takes-most dynamic that favors the company with the largest connected base. KONE's early investment in this area, combined with its recent integration of generative AI tools for technicians, positions it well to capture a disproportionate share of value as the industry digitizes.

Finally, the People Flow and building operating system opportunity represents optionality that is not reflected in the current stock price. If KONE successfully expands from elevator maintenance into building-wide access control, people flow optimization, and integrated building management, the addressable market expands dramatically. This is not guaranteed — it requires execution in software and systems integration that is different from KONE's traditional strengths. But the Delorme appointment signals that the company is serious about this transition.

The KPIs That Matter. For investors tracking KONE's ongoing performance, two metrics deserve close attention above all others:

First, service and maintenance revenue as a percentage of total revenue — and its growth rate. This metric captures the health of the recurring revenue engine and the progress of the installed-base monetization strategy. If service revenue is growing faster than new equipment revenue, the business is getting structurally better over time.

Second, orders received growth at comparable exchange rates. This is the leading indicator. Orders received today become revenue twelve to eighteen months from now. The comparable exchange rate adjustment strips out currency noise and reveals the underlying demand trajectory. KONE's 2025 orders grew 6.8% at comparable rates — a healthy signal despite China headwinds. Watching this metric quarter to quarter will tell you before anything else whether the business is accelerating or decelerating.

X. Epilogue and Final Reflections (2:15–2:25)

In 1910, a small Finnish machine shop with fifty employees began assembling elevators under license from an American manufacturer. Over the next century, four generations of the Herlin family transformed that shop into a global company that moves a billion people daily, generates over eleven billion euros in annual revenue, and earns returns on capital that most technology companies would envy. The journey from selling imported elevator kits to running an AI-powered predictive maintenance platform spanning sixty countries is one of the most remarkable — and least celebrated — business transformations in industrial history.

The lesson for founders and business builders is deceptively simple but fiendishly difficult to execute: turn a commodity product into a proprietary service. KONE did not win by building a better elevator. It won by building a better relationship with the building owner — a relationship that starts with the installation, deepens through decades of maintenance, and now extends into digital monitoring, access control, and building management. The product is the means; the service is the end. Every industrial company claims to be "moving to services." Very few have actually done it as thoroughly and profitably as KONE.

The future holds a genuinely fascinating strategic question: will KONE eventually become a "Building Operating System" company rather than an elevator company? The ingredients are in place — connected hardware, software platforms, access control integration, people flow analytics. If Delorme can execute the digital transformation that his Schneider Electric background prepared him for, KONE could evolve into something that looks more like a building technology platform than a traditional industrial manufacturer. The elevator becomes just one node in a network of building systems that KONE manages, monitors, and optimizes. The addressable market would grow by an order of magnitude.

Whether that vision materializes remains to be seen. What is clear today is that KONE has spent a century building the kind of competitive position — massive installed base, switching costs embedded in concrete, recurring revenue streams, family governance that thinks in generations — that compounds quietly and relentlessly. In a world obsessed with disruption and hypergrowth, KONE is a reminder that some of the best businesses are the ones you never think about. The elevator arrives. The doors open. You step inside and forget that anything remarkable just happened. That forgettable perfection, multiplied by a billion trips a day, is worth more than most people realize.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube