Kingfisher plc: Building the Omnichannel Giant of Home Improvement

I. Introduction & Episode Roadmap

Picture a builder on a half-finished extension somewhere in suburban Birmingham. It's a Tuesday morning, the plasterer is due at noon, and he has just discovered he is three boxes of screws and one cordless drill short of being able to start. In the old world, that meant downing tools, climbing into the van, fighting traffic to the nearest trade counter, and writing off ninety minutes of a paid working day. In 2026, he taps an app, and roughly twenty minutes later a courier pulls up to the kerb with exactly what he ordered. He never left the site.

That builder is the beating heart of a £12.9 billion retail empire that most people outside the United Kingdom and France have never knowingly thought about. The company is Kingfisher plc, and the apex predator of European home improvement hides behind a confusing thicket of brand names — B&Q, Screwfix, Castorama, Brico Dépôt, Koçtaş — none of which carry the parent's name. Its total sales reached £12,945 million for the year ended 31 January 2026.3

How did this happen? How did a sprawling, faintly ridiculous British retail conglomerate — one that at various points owned Woolworths, the electrical chain Comet, the pharmacy group Superdrug, and a record label — shed almost all of it and reinvent itself as the continent's titan of paint, plywood, and power tools? That is the first thread of our story.

The second thread is a single acquisition. In July 1999, Kingfisher quietly bought a mail-order screw catalogue from the Somerset town of Yeovil for £83.7 million.1 At the time it had roughly £28 million in annual turnover and sold fixings to tradesmen through a fat paper book.2 In the year just ended, that business — Screwfix — generated well over £2.7 billion in sales.3 It is, quite plausibly, one of the most value-accretive deals in the history of British retail, and almost nobody noticed it happen.

The third thread is a paradox that has tormented Kingfisher's boardroom for forty years. Home improvement is gloriously profitable when you get it right, because a £400 bag of cement-and-timber margin compounds across thousands of stores. But it is fiendishly hard to globalise. Bathroom fittings, plug sockets, plumbing standards, and the very cultural question of whether a homeowner picks up a drill themselves all differ wildly from one country to the next. Kingfisher learned this the expensive way — through a costly buyout in France and an outright capital cremation in China.

So here is the roadmap. We will trace the long arc from conglomerate to pure-play. We will linger on the Screwfix masterstroke. We will benchmark two very different uses of shareholder capital — the Castorama buyout and the China disaster — against each other. We will dissect the "One Kingfisher" centralisation crisis that nearly broke the company, and the "Powered by Kingfisher" decentralisation that rescued it. We will meet the management team, examine the hidden growth engines hiding inside an unglamorous DIY retailer, and finish by war-gaming the competitive moats and the bull and bear cases. Let's build.

II. Roots & Evolution: From Conglomerate to Pure-Play DIY

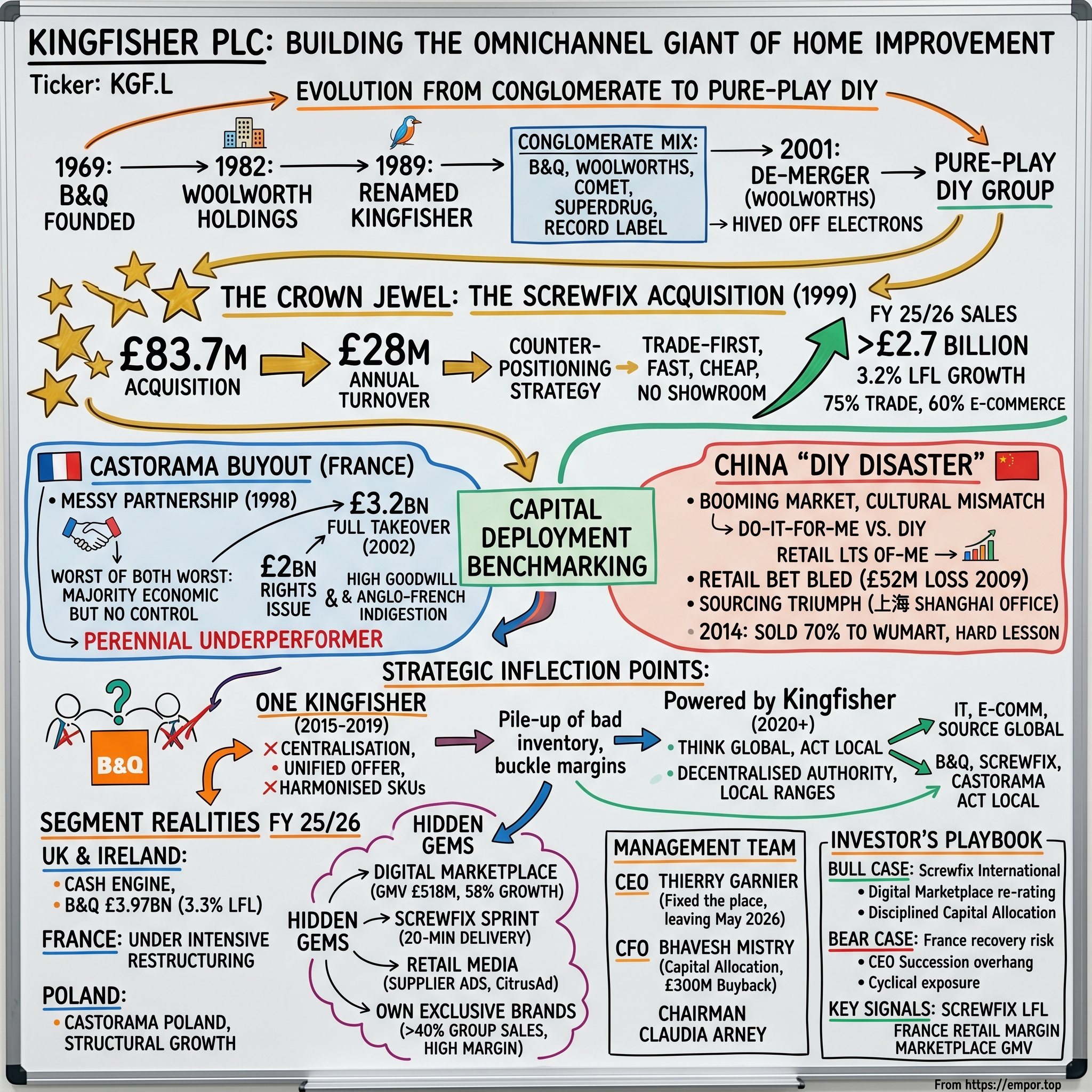

The origin of Kingfisher is, fittingly for a company that sells flat-pack furniture, a bit of a bolt-together job. The DIY brand at the centre of it all, B&Q, started in 1969 when two men — Richard Block and David Quayle — opened a discount home-and-garden warehouse in Southampton. They smashed their surnames together into "Block & Quayle," mercifully shortened to B&Q, and in doing so imported into Britain an idea then sweeping America: the big-box hardware shed where ordinary people, not just tradesmen, could buy the materials to improve their own homes.1

The corporate parent arrived by a far stranger route. In September 1982, a syndicate of institutional investors led by the merchant bank Charterhouse Japhet launched a £310 million takeover of the venerable but flagging British arm of F.W. Woolworth, using a specially created shell called Paternoster Stores. By November the bid had succeeded, and the entity was renamed Woolworth Holdings.1 B&Q came along inside that Woolworth empire. The parent would not adopt the name Kingfisher until 1989 — a deliberate rebrand to signal that this was no longer simply the company that ran Woolworths.

For most of the 1980s and 1990s, what we now call Kingfisher was a textbook British retail conglomerate, and a slightly bewildering one. Under its umbrella at various times sat Woolworths the variety store, Comet the electricals chain, Superdrug the health-and-beauty discounter, B&Q the DIY shed, and a clutch of smaller ventures. The logic of the day was diversification: spread across enough retail formats and the cycles would smooth each other out. The reality was that conglomerates of this kind tend to be valued by the market at a discount — investors struggle to price a grab-bag, and capital sloshes from the strong businesses to prop up the weak ones.

By the late 1990s, the board had absorbed a hard truth that was reshaping retail everywhere: focus beats breadth. The most profitable, most defensible, most cash-generative thing inside the portfolio was home improvement. A DIY shed has structural advantages a variety store can only dream of — large average basket sizes, project-driven repeat visits, limited fashion risk, and the wonderful fact that a kitchen, once sold, often drags flooring, lighting, and paint along with it. Comet's televisions, by contrast, were a margin-thin race to the bottom against the coming horror of online electronics retail.

So Kingfisher did something that, in hindsight, looks visionary: it dismantled itself on purpose. The crown moment came in 2001, when it demerged its general merchandise arm — the Woolworths and related businesses — into a separately listed company, freeing Kingfisher to become what its strategists called a pure-play home improvement group. The electricals business was hived off in the same restructuring wave. What remained was DIY, and DIY only.1

That clarity unlocked an ambition: Europe. Britain alone could not absorb Kingfisher's appetite, so the company planted flags across the Channel — building beachheads in France through Castorama and Brico Dépôt, in Poland, and across Iberia. The strategic bet was that the big-box model that worked in Southampton would translate to Lille, Warsaw, and Madrid.

It half worked. And the reasons it only half worked — the reasons the British playbook did not glide effortlessly across borders — would define the next two decades of triumphs and self-inflicted wounds. But before we get to the wounds, we have to tell the story of the one deal that justified everything: the screw catalogue from Yeovil.

III. The Crown Jewel: The Screwfix Acquisition of 1999

The best acquisitions rarely look like much at the time. In the summer of 1999, while the financial world was hyperventilating about dot-com valuations and pets.com, Kingfisher wrote a cheque for £83.7 million and bought a business that mailed thick paper catalogues of screws, drill bits, and plumbing fittings to tradesmen.1 Screwfix Direct had, at the point of sale, roughly £28 million of annual turnover and had only just launched its first website, in February of that year — five months before Kingfisher swallowed it.2 The price worked out to under three times revenue for a small mail-order operation. Nobody put it on the front page.

To understand why this turned out to be a generational home run, you have to understand what Screwfix actually was — and what it deliberately was not. A standard B&Q superstore is a cathedral of retail real estate: vast display floors, towering kitchen showrooms, a forest of signage, a sea of car-parking, and the costly choreography of visual merchandising designed to make a browsing family imagine a new conservatory. It is built for the discretionary weekend DIYer who wanders the aisles, and that experience costs an enormous amount per square foot to deliver.

Screwfix threw all of that in the skip. Its founding insight was that a professional tradesman does not want to browse. He knows precisely what he needs — a box of 4mm wood screws, a specific tap, a particular drill — and he wants it fast, cheap, and in stock. So Screwfix stripped the model to its skeleton: a hyper-dense, warehouse-style operation, a comprehensive printed catalogue with every product code laid out, and a digital-first inventory system that knew exactly what was on the shelf. No showroom theatre. No wasted square footage. Just a transaction machine optimised for speed and price.

This is what strategy nerds call counter-positioning, and it is one of the most powerful moats in business. Screwfix wasn't simply a cheaper version of a big-box DIY store — it was a structurally different animal whose unit economics the incumbents could not copy without cannibalising themselves. If a traditional DIY retailer tried to match Screwfix's bare-bones, high-density, trade-first format, it would have to gut the very showroom experience that justified its own store footprint and pricing. The incumbent is trapped by its own success. That is why counter-positioning is so lethal: the bigger and more committed the rival, the harder it is for them to respond.

Then came the genius second act: physical trade counters. In 2005, Screwfix opened its first bricks-and-mortar trade counter, marrying the catalogue's range with the immediacy of "click, drive ten minutes, collect."2 The tradesman could order online or by phone and pick up within minutes, or increasingly just walk in. Over the next two decades, the counter network spread across the United Kingdom like a fungus, eventually numbering in the high hundreds, each one a small, cheap, high-throughput box rather than an expensive superstore.

The compounding is the whole point of the story. Screwfix crossed £1 billion in sales around 2016. It surpassed £2 billion in the year to early 2021, at which point management began openly eyeing international expansion.[^5] In the year just ended, Screwfix delivered well over £2.7 billion of sales, with like-for-like growth of 3.2% in a soft market, and it now draws roughly three-quarters of its revenue from trade customers and around 60% from e-commerce.3 From £28 million to north of £2.7 billion is a near-hundredfold increase in turnover across the life of the ownership, all from a business bought for less than the cost of a single flagship superstore today.

The lesson for capital allocators is almost uncomfortable in its simplicity. The flashy, expensive, strategically "obvious" deals are not where the returns hide. The returns hid in an unglamorous catalogue business with a differentiated model and decades of runway, bought cheap and — crucially — given room to grow rather than being strangled inside a corporate straitjacket. Hold that last phrase in your mind, because Kingfisher was about to spend a fortune learning the opposite lesson on the other side of the English Channel.

IV. Capital Deployment Benchmarking: The Castorama Buyout & the China "DIY Disaster"

If Screwfix is the case study in capital well spent, the next two episodes are the control group — what happens when a great operator makes great-operator mistakes with the chequebook. They are worth studying precisely because they rhyme with the Screwfix success while inverting it.

Start in France. Through the late 1990s, Kingfisher had built a position in Castorama, France's leading big-box DIY chain. But the structure of the relationship was a mess. Kingfisher held a majority economic stake — around 55% — yet under the terms of a French partnership arrangement struck in 1998, it lacked the management and voting control that would normally accompany such ownership. It was the worst of both worlds: enough exposure to feel the pain, not enough authority to fix anything. The founding Dubois family and the partnership terms boxed Kingfisher into the back seat of a car it had paid to own.

The only exit was to buy the whole thing. In May 2002, Kingfisher moved to take full control of Castorama, and the price of escaping its own structuring mistake was eye-watering. To fund it, the company launched a £2 billion rights issue — at the time the largest in United Kingdom corporate history — tapping shareholders for fresh equity, with the proceeds going toward a buyout of the Castorama shares it did not already own that totalled roughly £3.2 billion.[^6] To prise control loose from minority holders who knew Kingfisher had no choice, it had to pay a hefty control premium on top of an already full price.

Was it worth it? The honest answer is that Kingfisher overpaid to correct an unforced error. Benchmarked against the disciplined French competitor Adeo — the privately held empire behind Leroy Merlin, widely regarded as the best operator in European home improvement — Kingfisher's French assets have spent the subsequent two decades as the perennial underperformer. The deal saddled the group with a mountain of goodwill, years of integration friction, and a structural case of Anglo-French cultural indigestion: a British head office trying to run a proud French retail institution, with predictable results. France remains, to this day, the part of the empire that analysts circle in red ink. We will return to its current margins later; for now, file Castorama as a deal where the strategic necessity was real but the price destroyed value.

Now sail east, to the more spectacular failure. In the 2000s, Kingfisher chased the irresistible logic of the era — a billion-plus Chinese consumers, a booming property market, surely a once-in-history opportunity for a DIY retailer — and built out B&Q China. The problem was a cultural mismatch so fundamental it should have been fatal on the whiteboard. The entire Western DIY model rests on the homeowner doing it yourself. But the Chinese housing market was built around 帮我做 — the "do-it-for-me" expectation. Apartments were typically sold as bare concrete shells, and the prevailing norm was to hire decorators and tradesmen to fit them out. The middle-class homeowner Kingfisher imagined wandering the aisles choosing paint swatches mostly did not exist; the work was outsourced. Selling self-service DIY into a do-it-for-me culture was like selling lawnmowers to people who live in apartments.

Here is the genuinely instructive twist. Kingfisher's engagement with China was not a total loss, because the company was doing two completely different things there. As a sourcing hub, China was a triumph — Kingfisher's purchasing offices, anchored in 上海 Shanghai, gave it enormous leverage over manufacturers and underpinned the private-label strategy that we will come to.[^13] Buying from China worked brilliantly. Selling to Chinese consumers was the black hole. Same country, opposite outcomes, and the contrast is the whole lesson: a sourcing relationship and a retail market are entirely different bets that happen to share a map.

The retail bet bled for years — B&Q China posted a loss of around £52 million in 2009 alone — and eventually management did the disciplined, unglamorous thing and cut it. In December 2014, Kingfisher sold a 70% controlling stake in its remaining 39 B&Q China stores to the Chinese supermarket group 物美 Wumart (Wumei) for £140 million, handing over operational control and booking the retreat as a hard lesson in the limits of transplanting a business model across a cultural chasm.[^7]

Two deals, two warnings. Castorama says: never sign a structure that separates your money from your control, because buying back control later is the most expensive purchase there is. China says: a market that looks identical on a spreadsheet — same product category, vastly larger population — can be a different planet once human behaviour enters the model. Both lessons would soon be tested at home, in the most ambitious and most damaging strategic experiment Kingfisher ever attempted on itself.

V. Strategic Inflection Points: "One Kingfisher" versus "Powered by Kingfisher"

By the mid-2010s, Kingfisher's leadership looked at its collection of national champions — B&Q in Britain, Castorama and Brico Dépôt in France, Castorama in Poland, plus the rest — and saw what looked like an obvious, almost embarrassing inefficiency. Each banner bought its own products, ran its own supply chain, designed its own ranges. Why should the group negotiate five times with five sets of suppliers for what was essentially the same drill? Why not pool that buying power, unify the ranges, and let the full weight of a multi-billion-pound European retailer land on every supplier negotiation?

Thus was born "One Kingfisher," the centralisation programme launched in 2015. The thesis was scale economics in its purest form: design a single, unified own-brand offer — branded GoodHome — and roll it out across every country, harmonising the product ranges so that a kitchen tap sold in Lille was the same kitchen tap sold in Lyon and Leeds. On a slide, it was beautiful. The projected synergies ran into the hundreds of millions. The logic was the same logic that makes Costco and Walmart terrifying: buy once, buy huge, win on cost.

And it nearly destroyed the company.

The flaw was the one Kingfisher should have learned in China and France: home improvement does not standardise. A French homeowner's plumbing connects to French standards; a British one to British standards. Electrical fittings, dimensions, fixings, finishes, the colours that sell in Warsaw versus the colours that sell in Manchester — the local variation that looks like trivial detail on a head-office spreadsheet is, on the shop floor, the entire business. When central buyers in a unified office pushed harmonised ranges into stores whose customers wanted something subtly but importantly different, the result was a slow-motion operational pile-up. Products that didn't fit local demand sat unsold. The things customers actually wanted went out of stock. Inventory ballooned in the wrong SKUs and had to be written down. Margins buckled. And country managers — the people closest to the customer — watched their local expertise be overruled from the centre and pushed back hard.

The numbers told the story of a self-inflicted wound: years of disappointing results, repeated stock availability problems, and write-downs that ate the very synergies the programme had promised. By the late 2010s, "One Kingfisher" had become a cautionary tale in retail circles about the danger of confusing scale with sameness. Scale is a weapon; sameness imposed on genuinely different customers is a liability dressed up as efficiency.

The rescue came with a change of leadership and a near-total reversal of philosophy. The new doctrine, articulated from 2020 onward, was "Powered by Kingfisher" — and the preposition matters. The brands would no longer be melted down into one; they would be powered by a shared platform while retaining their own identity, their own ranges, and their own authority to respond to local customers. B&Q would be B&Q. Screwfix would be Screwfix. Castorama, Brico Dépôt, each free to merchandise for the people actually walking through their doors.

Crucially, this was not a rejection of group scale — it was a sharpening of where scale legitimately helps and where it actively hurts. The group would centralise the things that are genuinely the same everywhere and invisible to the customer: IT infrastructure, e-commerce and the digital marketplace technology, data, and the sourcing of own-exclusive brands where a global supply chain genuinely lowers cost without dictating the local assortment. It would decentralise the things that must be local: range decisions, pricing, store experience, the customer relationship. The slogan for this is "think global, act local," but the substance is harder and more honest than the slogan — it is a continuous discipline about which decisions belong at the centre and which belong at the edge.

That rebalancing is the hinge on which the modern company turns, and the person who installed it deserves a proper introduction. Which brings us to the management team.

VI. Under the Hood: Current Management, Shareholding & Incentives

In September 2019, Kingfisher handed the keys to a Frenchman who had spent the bulk of his career not in DIY at all, but in groceries. Thierry Garnier arrived from the French retail giant Carrefour, where he had run the enormous and notoriously difficult Asian operations.6 On paper, hiring a supermarket executive to run a home improvement group sounds like a category error. In practice, it was inspired — because the problem Kingfisher had was not really about paint and plywood. It was about operating a sprawling multi-country retailer without strangling its local businesses, and that was precisely the puzzle Garnier had spent years untangling at Carrefour.

Garnier's defining act was the strategic U-turn we just described: dismantling the centralising apparatus of "One Kingfisher" and replacing it with the decentralised, platform-plus-autonomy model of "Powered by Kingfisher." He had near-perfect timing on one front and brutal timing on another. Months into his tenure, the COVID-19 pandemic locked Europe's population inside their homes — and a captive nation with disposable income suddenly wanted to repaint the spare room, build a deck, and finally fix the bathroom. Home improvement boomed, e-commerce penetration leapt, and Garnier rode the wave while using the windfall to accelerate the digital transformation that now defines the company. He then steered through the inevitable normalisation as the boom faded and consumers tightened, holding the strategy steady where a weaker CEO might have lurched.

Then, in May 2026, came the bombshell. Garnier announced he would step down as chief executive, having been recruited to lead one of Europe's largest grocery groups, the Dutch-Belgian giant Ahold Delhaize, where he was nominated to succeed the retiring Frans Muller as CEO in April 2027.[^8]5 Under the terms of his departure, Garnier is serving a twelve-month notice period, meaning that as of this writing in June 2026 he remains in active command of Kingfisher through the transition, with the board running a search for his successor.8 We will treat the succession as a live risk in the bear case; for now, note that the man leaving is the man who fixed the place, which sharpens the question of whether the fix outlives the fixer.

A word on how Kingfisher pays its leaders, because incentive design tells you what a board actually wants. Garnier's package was overwhelmingly tilted toward performance rather than guaranteed salary — the large majority of his total remuneration came in variable, performance-linked form, structured so that a relatively modest fixed salary sat beneath a stack of annual bonus and long-term share awards. He was bound by a demanding shareholding requirement obliging him to build and hold Kingfisher stock worth several multiples of his base salary, the mechanism by which boards try to force executives to feel share-price pain and gain the way owners do. His long-term incentive plan was wired to the metrics the company most wants to move: retail profit, earnings per share, the growth of the digital marketplace, and the recovery of the troubled French margins. In other words, the pay plan is a map of the strategy — fix France, grow the platform, compound the profit.

Alongside the CEO sits a relatively new chief financial officer. Bhavesh Mistry joined Kingfisher in January 2025, succeeding Bernard Bot, having previously served as CFO of the FTSE-listed property group British Land from 2021, with earlier senior finance roles at Tesco and other large consumer businesses.6 His mandate is the unglamorous but decisive work of a turnaround maturing into a cash machine: rigorous capital allocation, disciplined cost control, converting profit into free cash flow, and returning surplus capital to shareholders. On that last point, the company has been emphatic — it completed a £300 million share buyback programme and announced a fresh £300 million programme, alongside a maintained dividend, signalling a board that believes its own shares are worth more than the market is paying and that the business now throws off more cash than it needs to reinvest.4 The chairman through this period has been Claudia Arney, in the role since November 2018.6

Strategy and stewardship are in place. But the most interesting part of Kingfisher in 2026 is not the org chart — it is the cluster of high-growth, high-margin businesses germinating inside what looks, from the outside, like a sleepy chain of DIY sheds.

VII. The "Hidden Gems" & Segment-Level Realities

If you only read the headline, you would file Kingfisher as a mature, cyclical, low-growth bricks-and-mortar retailer — total sales up just 1.3% in the year to 31 January 2026, like-for-like up 1.4%, in a sluggish European consumer environment.4 That headline is true and almost completely misses the point. The interesting story is what is happening inside the mix.

Start with the geography. The United Kingdom and Ireland is the cash engine, and it is humming. B&Q grew total sales 3.9% to £3,971 million with like-for-like up 3.3%, while Screwfix kept compounding, and the combined UK and Ireland operation delivered retail profit of £575 million, up nearly 3%.34 This is the part of the empire that works, that gains market share, and that funds everything else. France is the perennial patient: both French banners, Castorama and Brico Dépôt, posted modestly negative like-for-like sales, and the segment remains under intensive operational restructuring to drag its weak margins back toward something respectable.4 Poland, run as its own profitable engine through Castorama Poland, held roughly flat in a soft local market but remains a structurally attractive growth story, with the group continuing to add medium-format and compact stores to extend its lead.

Now the gems — the four initiatives that explain why this is not merely a tired retailer.

The first and most exciting is the digital marketplace. In plain terms, Kingfisher has done to its websites what Amazon did to its own: opened them up to third-party sellers. Instead of only selling its own inventory, the company lets independent merchants list their products on B&Q's and its other sites, takes a commission on every sale, and never touches the stock. The reason this matters so much is the economics. Selling your own product means buying it, warehousing it, and bearing the risk it doesn't sell. Marketplace sales are almost pure margin — a software-like commission stream with near-zero inventory risk, the highest-quality revenue a retailer can earn. In the year just ended, marketplace gross merchandise value — the total value of goods sold across the platforms — leapt 58% to £518 million, with B&Q's marketplace alone reaching 3.7 million product listings and £445 million of that total.34 It is still small against £12.9 billion of group sales, but it is growing fast and flowing disproportionately to profit. This is the closest thing a DIY retailer has to a tech business hiding in its income statement.

The second gem is Screwfix Sprint — the twenty-minute delivery service from the opening of this story. Launched in 2021, Sprint dispatches tools and materials from local Screwfix outlets directly to a builder on a job site, often within twenty minutes, via the mobile app, covering a large majority of the UK population.[^11] Strategically, it is far more than a convenience feature. For a working tradesman, time is money in the most literal sense — every hour spent driving to a counter is an hour not billed. By collapsing that errand into a tap, Sprint embeds Screwfix into the daily workflow of the trade in a way that is genuinely hard to dislodge. It is a logistics moat built on the back of the densest trade-counter network in the country.

The third gem is retail media. This is the quietest and, per pound, possibly the most profitable. Kingfisher's websites and apps now attract enormous traffic — with e-commerce running at around 21% of group sales, that is a vast audience of people actively shopping for specific products.4 Partnering with the advertising technology firm CitrusAd, the company launched a media arm that lets suppliers pay to promote their products to that audience — sponsored listings, native ads, the same model that turned Amazon's advertising business into a profit juggernaut. The brilliance is that the audience already exists and the cost of serving an ad is trivial, so nearly every pound of advertising revenue drops through to profit. It monetises attention the company was generating for free.

The fourth gem is the oldest and the foundation beneath the others: own exclusive brands. Names like Erbauer, Magnusson, and Diall mean nothing to the casual shopper, and that is exactly the point — they are Kingfisher's own private labels, designed in-house and manufactured through its global sourcing network anchored in Asia. Together they account for well over 40% of group sales.4 Private label is a margin machine: by cutting out the branded manufacturer's markup and controlling the product from factory to shelf, Kingfisher captures meaningfully higher margins than it earns reselling a national brand, while building customer loyalty to products that can be bought nowhere else. This is where the China sourcing capability — the half of the China story that worked — pays off every single day.

So beneath the cyclical, low-growth surface sits a profitable trade-logistics network, a fast-growing marketplace, a near-pure-profit media stream, and a deep private-label franchise. The question for any investor is whether these moats are durable. Time to war-game them.

VIII. Strategic Frameworks: Porter's Five Forces & Hamilton's Seven Powers

Let's put Kingfisher on the analyst's bench and pull it apart with two classic frameworks — Hamilton Helmer's Seven Powers, which asks what durable advantages a business actually possesses, and Michael Porter's Five Forces, which asks how attractive its industry is to compete in.

Run the Seven Powers first. The most obvious is scale economies. Kingfisher's global purchasing apparatus — sourcing offices in hubs including 上海 Shanghai and across Asia — lets it commission own-exclusive-brand products in enormous volume, giving it price leverage over manufacturers that a regional rival simply cannot match.[^13] The crucial subtlety, learned the hard way through "One Kingfisher," is that this power is real only on the cost side of genuinely common products; the moment scale is used to dictate local assortment, it curdles from advantage into liability. Kingfisher now wields it correctly.

The sharpest power in the portfolio is counter-positioning, and it lives at Screwfix. As we dissected earlier, Screwfix's stripped-down, trade-first, high-density model cannot be copied by a traditional big-box DIY incumbent without that incumbent destroying its own showroom economics. This is the rare moat that gets stronger the more committed your competitor is to the old way, and it is the single most underappreciated asset in the group.

Then there is a network effect, modest but compounding, inside the digital marketplace. More third-party sellers listing more specialised stock makes the platform more useful to more contractors and DIYers, which attracts more buyers, which attracts more sellers — the classic flywheel that turned generic e-commerce sites into ecosystems. It is early and far from Amazon-scale, but the direction of travel is unmistakable, and unlike the others it improves with size at near-zero cost.

Finally, switching costs, concentrated in the trade. Once a builder runs his ordering through Screwfix's app, relies on Sprint to keep his job moving, holds a TradePoint trade account at B&Q, and runs a corporate credit line through the group, the friction of switching to a rival rises with every job. None of these is individually decisive, but woven together they form a sticky operational loop around the professional customer — the most valuable and most loyal customer a home-improvement retailer can have.

Now the Five Forces, which assess the industry itself. The threat of new entrants is extremely low: replicating a continent-spanning network of stores, depots, sourcing offices, and last-mile logistics requires capital and operational depth measured in billions and decades. The bargaining power of suppliers is low — Kingfisher's scale and private-label capability mean it can switch or in-source, leaving manufacturers as the weaker party at the table. The bargaining power of buyers is split, and this split is the whole game: the casual DIY shopper is fiercely price-sensitive and one browser tab away from comparing prices, giving them real power, whereas the professional tradesman prioritises speed, availability, and on-site delivery far above shaving a few pence — which is precisely why Kingfisher has tilted so hard toward the trade. Competitive rivalry, finally, is high and unrelenting: in the UK it battles Travis Perkins and the Wickes-style merchants; in France and Poland it faces the formidable Adeo/Leroy Merlin; and everywhere it must reckon with Amazon's gravitational pull on the discretionary DIY shopper.

Net it out and a clear picture emerges. The home-improvement industry is structurally attractive — high barriers, weak suppliers — but commoditised at the DIY end and ferociously competitive. Kingfisher's edge is not the DIY shopper at all; it is the trade franchise, where counter-positioning, switching costs, and logistics compound into something genuinely defensible. The strength of the moat scales directly with how professional the customer is.

IX. The Investor's Playbook & Bull vs. Bear Case

Stand back from the detail and the investment debate over Kingfisher resolves into a clean clash of two stories. Let's make the case for each, fairly.

The bull case rests on three pillars. First, Screwfix is not finished — having conquered Britain, it is exporting its counter-positioned model abroad, with France the obvious next frontier, and a successful international Screwfix would add a second compounding growth engine on top of the UK cash machine. Second, the digital transformation is demonstrably working and not yet reflected in how the market values the company: marketplace GMV growing 58% to £518 million is the kind of trajectory that, sustained, re-rates a "tired retailer" into something the market pays more for, and because that revenue is near-pure margin it flows straight to high-quality profit.34 Third, capital allocation is now a strength rather than a worry — a maintained dividend of 12.40 pence per share, back-to-back £300 million buyback programmes, and roughly £512 million of free cash flow in the year just ended say a board that is disciplined, confident, and willing to shrink the share count when the price is right.4 In the bull's telling, you are buying a misunderstood compounding platform priced like a melting ice cube.

The bear case is just as coherent. First, France refuses to heal: Castorama and Brico Dépôt remain a structural drag on group returns, the restructuring is years old and still unfinished, and every euro of underperformance there dilutes the excellent returns earned in Britain.4 A serious investor should treat French retail profit recovery as the single most important unproven assumption in the whole thesis. Second, the succession overhang is real — the CEO who architected the entire turnaround is leaving for Ahold Delhaize, and however orderly the twelve-month transition, retail history is littered with companies that lost the thread the moment the visionary walked out the door.[^8]8 Third, and most simply, this is a consumer-discretionary business chained to the European housing cycle: when interest rates bite, house moves stall, and consumers postpone the new kitchen, Kingfisher feels it directly and immediately, and no amount of marketplace cleverness fully insulates it from a cyclical downturn.

How do the two stories reconcile with the competitive analysis? They map onto the buyer-power split almost perfectly. The bull case is fundamentally a bet on the trade — Screwfix, Sprint, switching costs, the defensible end of the business. The bear case is fundamentally a worry about the DIY and cyclical end — France's discretionary shopper, the housing cycle, the price-comparing browser. The same company contains both, which is why reasonable analysts disagree.

If an investor is going to track Kingfisher with discipline, the noise must be stripped away to a tiny number of signals that actually reveal whether the thesis is intact. Three stand out. The first is Screwfix like-for-like sales growth, because it is the cleanest read on the health of the company's best and most defensible franchise; as long as Screwfix compounds, the core engine is intact. The second is France (Castorama and Brico Dépôt) retail profit margin, because it is the make-or-break variable in the bear case and the largest single swing factor in group returns — recovery validates the bulls, continued erosion validates the bears. The third is marketplace GMV growth, because it is the leading indicator of whether the high-margin digital transformation is real and durable or a one-off pandemic-era bump. Watch those three, and the rest is largely commentary. (As a fourth, softer dimension, watch the CEO succession itself — who is hired, and whether they reaffirm or revise "Powered by Kingfisher," is the qualitative tell on execution risk.)

X. Epilogue & Outro

Two lessons echo out of the Kingfisher story, and they are almost mirror images of each other.

The first is the Screwfix lesson, and it is a lesson about humility before unglamorous things. The single best decision in this company's modern history was not a bold continental land-grab or a transformational mega-merger. It was buying a small, dull, mail-order catalogue of screws for less than the cost of one superstore, recognising that its stripped-down model was structurally different rather than merely cheaper, and then — this is the part that is genuinely hard for a large corporation — leaving it alone to compound for a quarter of a century. Great acquisitions often look boring at the moment of purchase. The discipline is in seeing the runway and resisting the urge to "improve" the thing into the corporate average.

The second is the centralisation lesson, written in the red ink of "One Kingfisher" and the goodwill of Castorama and the abandoned shelves of B&Q China. Scale is a weapon, but it is a weapon with a specific use. Pointed at cost — at sourcing, at shared technology, at the things customers never see — it is devastatingly effective. Pointed at the customer-facing assortment, at local taste, at the thousand small differences between a kitchen in Lyon and a kitchen in Leeds, it backfires, because it confuses bigness with sameness and tries to standardise the one thing that must stay local. The art of running a multi-country retailer, the thing Garnier ultimately got right, is knowing exactly which decisions belong at the centre and which belong at the edge — and having the discipline to never, ever mix them up.

A British conglomerate that once sold sweets and televisions and pharmaceuticals and pop records taught itself, painfully and over forty years, to do one thing supremely well across an entire continent. Whether the next leader holds that line — keeping the trade engine roaring, healing France, and letting the hidden gems compound — is the open question that the builder on his half-finished extension, tapping his app for a twenty-minute delivery, neither knows nor needs to.

References

-

Full year results for the year ended 31 January 2026 — Kingfisher plc, 2026-03-24 ↩↩↩↩↩↩

-

Kingfisher: Strong FY25/26 Performance Driven by Strategic Progress — Insight DIY, 2026-03-24 ↩↩↩↩↩↩↩↩↩↩

-

Ahold Delhaize announces Thierry Garnier as nominee for Chief Executive Officer; Frans Muller to retire in 2027 — Ahold Delhaize, 2026-05-06 ↩

-

London Stock Exchange: Kingfisher plc (KGF) Overview — London Stock Exchange, 2026-06-18 ↩

-

Thierry Garnier to step down as Kingfisher CEO and join Ahold Delhaize — Retail Week, 2026-05-06 ↩↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube