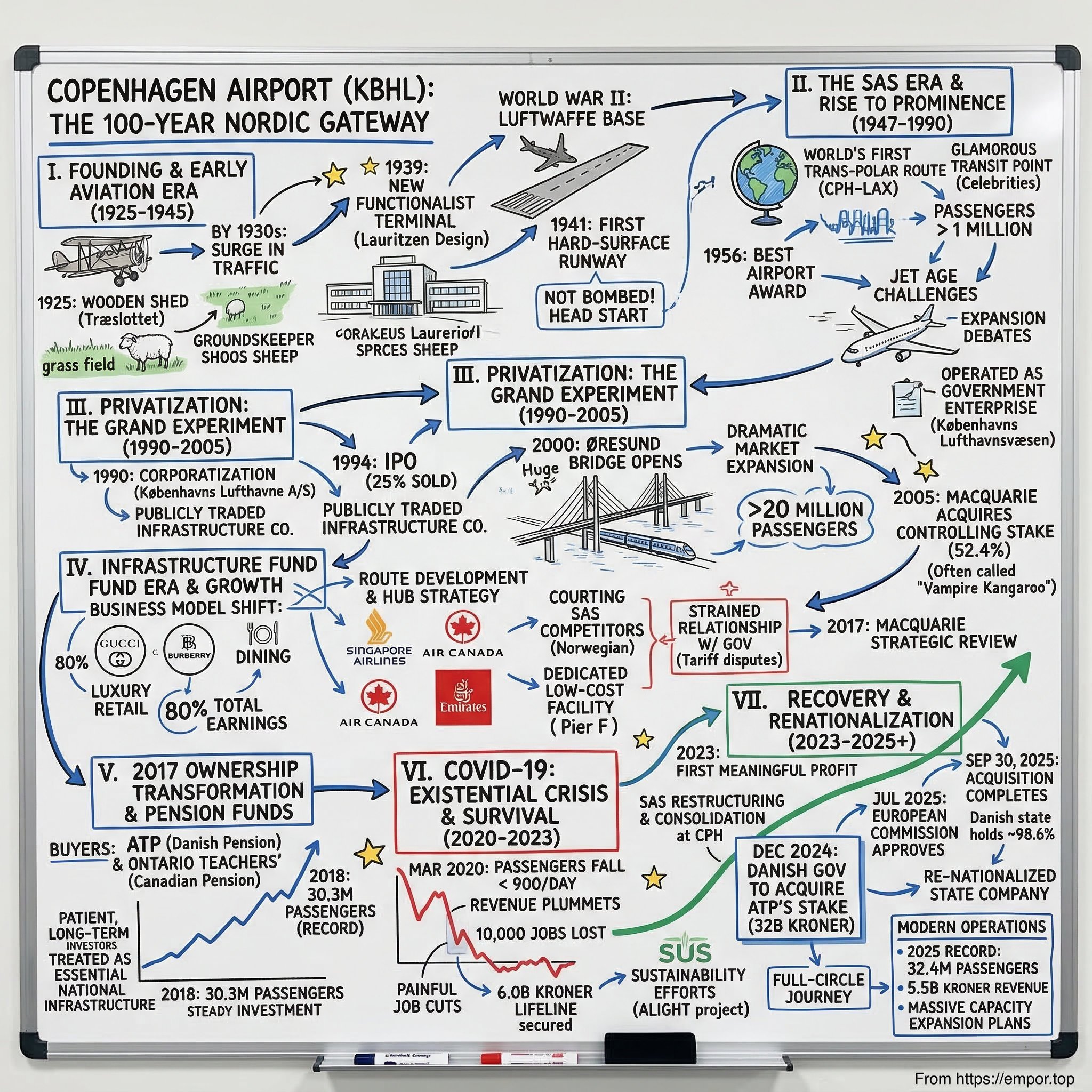

Copenhagen Airport: The 100-Year Nordic Gateway

I. Introduction and Episode Roadmap

Picture this: it is 1925, and on the windswept island of Amager, just south of Copenhagen's city center, a flock of sheep grazes lazily on a grass strip. Every so often, a groundskeeper shoos them aside so a biplane carrying a handful of passengers can rattle down the field and take off into the grey Danish sky. The terminal is a wooden shed so charming that locals call it "Træslottet" — The Wooden Castle. In its first full year of operation, the airport handles 5,082 passengers. Not per day. Not per hour. For the entire year.

Fast forward a century. In 2024, Copenhagen Airport processed 29.9 million passengers. In 2025, it shattered its all-time record with 32.4 million travelers passing through its terminals — more than six times Denmark's entire population. It is the largest airport in the Nordic countries, the primary gateway connecting Scandinavia to the world, and the hub for one of Europe's oldest airlines. And in September 2025, the Danish government completed a 32 billion kroner acquisition to bring it almost entirely back under state ownership, closing one of the most fascinating circles in modern infrastructure history.

The central question of this story is deceptively simple: how did a grass runway on a tiny Danish island become Northern Europe's most critical aviation hub — and why did the Danish government just spend roughly $4.5 billion to renationalize it after three decades of privatization?

Copenhagen Airport celebrated its 100th birthday on April 20, 2025, laying claim to one of the longest continuous operating histories of any commercial airport on Earth. But the centennial was not just a celebration. It was a moment of reckoning — a chance to evaluate the extraordinary experiment Denmark had conducted with this piece of critical national infrastructure. Over ten decades, Copenhagen Airport had been a government enterprise, a publicly traded company, an infrastructure fund plaything, a pension fund investment vehicle, and finally, once again, a state-owned asset. Each ownership chapter left its mark, for better and worse.

The themes running through this story are universal to anyone thinking about infrastructure investing: Can private capital actually improve public assets? What happens when financial engineering meets physical engineering? How does a small country maintain control of its most important gateway to the world? And perhaps most provocatively — was the privatization a success that the government simply decided to reverse, or was it a cautionary tale that took thirty years to fully play out?

To answer these questions, we need to go back to the beginning — to a time when aviation itself was an experiment, and Denmark bet that a grass field on Amager would become something extraordinary.

II. Founding and Early Aviation Era (1925–1945)

On April 20, 1925, Copenhagen Airport opened without fanfare. There was no ribbon-cutting ceremony, no political speeches, no champagne. Denmark was mired in economic difficulty — unemployment exceeded 20 percent, the krone was weakening, and the post-World War I optimism that had briefly lifted Scandinavian spirits had largely evaporated. Opening an airport felt almost frivolous. But the Danish government, operating through a newly created entity called Københavns Lufthavnsvæsen, understood something that many European governments did not yet grasp: commercial aviation was coming, and the countries that built infrastructure early would capture disproportionate advantage.

The facilities were almost comically modest by modern standards. The terminal was a wooden structure, attractive enough in its simplicity to earn the "Wooden Castle" nickname from locals. Beyond it stretched a grass runway, maintained by the airport's most reliable employees — a herd of sheep whose sole job was to keep the grass trimmed. Whenever an aircraft needed to depart or land, someone would herd the sheep to the edges of the field. The airport also featured a couple of hangars, a balloon mast from an earlier era of flight, and a hydroplane landing stage for seaplanes arriving from across the Øresund strait.

The primary airline tenant was Det Danske Luftfartselskab, or DDL — Danish Air Lines — which initially operated chartered aircraft before acquiring its first proper commercial airliner, a French-built Farman F.121 that could carry nine passengers. It was, by any measure, a tiny operation. But what Copenhagen lacked in scale, it made up for in geography. Situated at the crossroads of Scandinavia, the Baltic, and continental Europe, the airport sat at a natural nexus of Northern European air routes. This geographic logic — obvious in hindsight, visionary at the time — would prove to be the airport's most durable competitive advantage across the next century.

Growth came faster than almost anyone anticipated. By the early 1930s, takeoffs and landings had surged from a few hundred annually to nearly 6,000, and by 1939 the number had reached 50,000. Annual passengers climbed from 5,000 to 72,000 in just over a decade. The grass runway and wooden terminal were no longer adequate for an airport handling this volume, and in 1932, the first proper terminal building was constructed.

But it was the terminal that came next — completed in 1939 — that truly put Copenhagen Airport on the map. The Danish government commissioned one of the country's most celebrated architects, Vilhelm Lauritzen, to design a new terminal worthy of an international gateway. Lauritzen, who had introduced functionalism into Danish architecture after travels through Central Europe, produced something revolutionary. His terminal featured a radical innovation that seems obvious today but was genuinely novel at the time: a clear separation of airside and landside operations, with arriving and departing passengers flowing through distinct sections of the building. This basic organizational principle would become the template for virtually every major airport terminal built in the twentieth century.

The building itself was a masterpiece of functionalist design. The concourse roof was just twelve centimeters thick, yet its undulating concrete form gave it an almost ethereal lightness — one architectural critic wrote that it looked "as if it were a cloth about to blow away in the Amager wind." The restaurant featured a double-curved facade reflecting Cubist influences, and Lauritzen collaborated with the legendary furniture designer Finn Juhl on the terminal's lamps, signage, and furnishings. The materials were industrial and cost-conscious throughout, except for deliberate moments of luxury: Greenlandic marble at the entrances, Junkers beech parquet wall cladding, and a distinctive brass railing on the main staircase. It was simultaneously practical and beautiful — Danish design philosophy distilled into an airport.

Then came the war. When Nazi Germany occupied Denmark in April 1940, Copenhagen Airport was effectively commandeered for military use. Civil operations were suspended except for periodic flights to Sweden and to destinations within the Reich. The German Luftwaffe used the airport as a base, and during the occupation years, the military invested in upgrading the facilities. In the summer of 1941, the first hard-surface runway opened — 1,400 meters long and 65 meters wide — replacing the grass strips that had served since 1925.

Here is where Copenhagen Airport caught one of its greatest historical breaks. Despite serving as a Luftwaffe base throughout the war, the airport was never bombed. The RAF and Allied air forces, whether by strategic calculation or sheer luck, left Kastrup intact. When World War II ended in May 1945, Copenhagen possessed something almost no other European city could claim: a modern international airport with hard-surface runways, functional facilities, and no war damage whatsoever. While London, Berlin, Amsterdam, and Paris faced years of reconstruction, Copenhagen Airport was ready for business immediately. It was a head start that would prove invaluable in the aviation boom that was about to begin — and one that would set the stage for the most important airline partnership in the airport's history.

III. The SAS Era and Rise to Prominence (1947–1990)

On August 1, 1946, three national carriers — Denmark's DDL, Sweden's Svensk Interkontinental Lufttrafik, and Norway's Det Norske Luftfartselskap — formalized one of the most audacious airline partnerships in aviation history. Scandinavian Airlines System, better known as SAS, was born. The logic was elegant: no individual Scandinavian country had the population or traffic volume to sustain a competitive international airline, but combined, the three nations could field a carrier capable of competing with the likes of BOAC, Pan American, and Air France. It was, in essence, the European Union model applied to aviation decades before the EU existed.

For Copenhagen Airport, the founding of SAS was transformational. Copenhagen was designated as the airline's primary hub — a decision driven partly by geography (Copenhagen sat at the southern tip of Scandinavia, closest to continental Europe), partly by the airport's undamaged infrastructure, and partly by Denmark's strategic positioning between the Baltic and the North Sea. Traffic increased rapidly. The airport that had handled 72,000 passengers on the eve of World War II was suddenly processing hundreds of thousands annually, and the growth showed no signs of slowing.

But the moment that truly elevated Copenhagen Airport from regional facility to global destination came in November 1954, when SAS launched the world's first scheduled trans-polar route, flying from Copenhagen to Los Angeles with stops in Søndre Strømfjord, Greenland and Winnipeg, Canada. The polar route was a masterstroke of both aviation engineering and marketing. By flying over the top of the world instead of the conventional route across the Atlantic, SAS shaved hours off the journey between Scandinavia and the American West Coast. The flights used Douglas DC-6B aircraft, and the navigation challenges over the magnetic pole were formidable — SAS employed specialized polar navigators, led by the legendary Einar Sverre Pedersen, who guided aircraft through regions where conventional compass navigation was unreliable.

The polar route proved to be a publicity sensation. Hollywood stars and film producers, accustomed to grueling multi-stop journeys between Los Angeles and Europe, discovered that flying SAS via Copenhagen was faster and more comfortable than the alternatives. Copenhagen Airport became a glamorous transit point, and for several years in the mid-1950s, the terminal buzzed with celebrities heading to and from the film capitals of Europe. The tariff structure was particularly clever — SAS offered free transit connections to other European destinations via Copenhagen, meaning that American tourists could stop in Denmark and continue onward at no additional airfare. Copenhagen was not just a hub; it was a free stopover on the way to anywhere in Europe.

By 1956, the polar service had expanded to three flights per week, and in 1957, SAS launched an even more ambitious service — the first around-the-world route over the North Pole, flying Douglas DC-7Cs from Copenhagen to Tokyo via Anchorage. Copenhagen Airport was now, improbably, a waypoint on the route connecting America, Europe, and Asia. The airport's reputation soared. In 1956, Copenhagen Airport won the award for the world's best airport — a remarkable achievement for a facility that had been a grass field just three decades earlier. Passenger numbers surpassed one million, having doubled capacity in just four years.

The jet age brought new challenges and opportunities. When jet airliners arrived in the 1960s, their longer runway requirements sparked intense debate about airport expansion. Jets needed substantially more tarmac than the propeller aircraft they replaced, and plans were drawn up to extend the airport either into the existing communities around Kastrup or onto Saltholm, a small uninhabited island in the Øresund strait. Local residents organized protests, and the expansion stalled for years — an early example of the NIMBY dynamics that would bedevil airport development worldwide for decades to come.

Despite the expansion debates, passenger growth continued relentlessly. By 1972, annual passengers exceeded eight million. The airport had evolved from a curiosity into essential infrastructure — the kind of facility that Denmark's economy could not function without. The commercial ecosystem around the airport had grown dense and complex, with thousands of jobs tied directly and indirectly to its operations. SAS had matured into one of Europe's premier airlines, and Copenhagen's position as its primary hub created a self-reinforcing cycle: more routes attracted more passengers, which justified more routes, which attracted more airlines beyond SAS.

Throughout this entire era — from the founding of SAS in 1946 through the late 1980s — Copenhagen Airport operated as a government enterprise. Københavns Lufthavnsvæsen reported to the Danish government, and investment decisions, pricing, and operational strategy were all subject to political oversight. The model had served Denmark well during the postwar aviation boom, but by the late 1980s, a new economic orthodoxy was sweeping through Europe. Margaret Thatcher had privatized British Airways and was eyeing BAA, the company that operated Heathrow and Gatwick. Governments across Europe were questioning whether state-owned enterprises were the most efficient way to run commercial infrastructure. Denmark, though culturally more cautious about privatization than Britain, was not immune to these arguments — and Copenhagen Airport, profitable and well-run, was an obvious candidate for the experiment that was about to begin.

IV. Privatization: The Grand Experiment (1990–2005)

In 1990, the Danish government transformed Københavns Lufthavnsvæsen from a government enterprise into a limited company — Københavns Lufthavne A/S. It was a subtle but critical change. The airport was no longer simply a department of the Danish state; it was now a corporate entity with a board of directors, articles of incorporation, and the legal capacity to issue shares. The corporatization was the necessary precursor to what came next.

Four years later, in 1994, Denmark took the plunge. The government sold 25 percent of its stake in Copenhagen Airports, and the company was listed on the Copenhagen Stock Exchange. It was one of the earliest airport privatizations in the world — preceding even the BAA privatization by strategy if not by chronology — and it reflected a deliberate Danish approach. Rather than selling the entire airport in one fell swoop, the government chose a staged divestment that would allow it to maintain control while testing the private market's appetite for airport equity.

The appetite proved robust. In 1996, the government sold an additional 24 percent, and in 2000, a further 17 percent was divested. By the turn of the millennium, the Danish state's direct holding had been reduced to roughly 34 percent — still a blocking minority, but no longer a controlling position. The airport was now, in effect, a publicly traded infrastructure company, and the market was valuing it accordingly.

The privatization unleashed a wave of investment that the government-run airport had never undertaken. In the years immediately following the 1994 IPO, Copenhagen Airports invested massively in new infrastructure — terminal expansions, technology upgrades, retail facilities, and runway improvements. The logic was straightforward: as a publicly traded company, CPH needed to grow revenue and earnings to justify its stock price, and the most direct path to growth was investing in capacity and commercial amenities. This was precisely the argument that privatization advocates had made — that private capital would unlock investment that government budgets had constrained.

But the investment came at a cost. Debt increased substantially as CPH borrowed to fund its capital program. The company was leveraging its balance sheet in a way that would have been politically difficult under government ownership, and some critics argued that the airport was trading long-term stability for short-term growth. This tension — between the conservative, patient stewardship of government ownership and the aggressive, growth-oriented approach of private capital — would become the central drama of Copenhagen Airport's next three decades.

Then, on July 1, 2000, everything changed. The Øresund Bridge opened, connecting Denmark and Sweden by motorway and rail for the first time in history. The bridge — one of the most ambitious infrastructure projects in European history, spanning nearly eight kilometers of open water before diving into a four-kilometer tunnel — transformed Copenhagen Airport overnight. The airport, which had served Copenhagen's metropolitan area of roughly 1.3 million people, suddenly became the primary international airport for the entire Øresund Region — a cross-border metropolitan area encompassing approximately 4.2 million people across Denmark and southern Sweden.

The impact was immediate and dramatic. Swedish travelers from Malmö, Lund, Helsingborg, and other cities in Skåne province could now reach Copenhagen Airport by train in under 30 minutes. Malmö's own airport, never a major international hub, became increasingly irrelevant for long-haul travel. Copenhagen gained a massive catchment area without building a single new runway. It was the ultimate infrastructure network effect — one piece of transportation infrastructure (the bridge) dramatically amplifying the value of another (the airport). The bridge's design reflected this symbiosis: the tunnel section was specifically engineered to avoid interfering with Copenhagen Airport's flight paths, a constraint that added substantial cost and complexity to the bridge project but preserved the airport's operational integrity.

In 2006, for the first time in its history, Copenhagen Airport exceeded 20 million passengers, reaching 20.9 million — a milestone that would have seemed fantastical to the airport's founders eight decades earlier. The Øresund effect was real and measurable, and it fundamentally altered the competitive dynamics of Nordic aviation.

Against this backdrop of surging traffic and infrastructure-driven growth, a new kind of investor arrived. In 2005, Macquarie Infrastructure and Real Assets, the infrastructure arm of Australia's Macquarie Group, acquired a controlling stake of approximately 52.4 percent in Copenhagen Airports. Macquarie operated through a multi-tiered holding structure — its European Infrastructure Fund III invested through Kastrup Airports Parent ApS, which in turn controlled 57.7 percent of CPH shares. If this sounds complex, it was meant to be. Macquarie had pioneered the infrastructure fund model, treating airports, toll roads, and utilities as financial assets that could be optimized through leverage, fee extraction, and operational efficiency gains.

Macquarie was not universally beloved. The Australian financial press had coined the nickname "Vampire Kangaroo" for the firm's reputation of aggressively extracting management fees and performance fees from the assets it controlled. From Macquarie Airports alone, the parent company earned roughly 44 million Australian dollars in annual base fees and 255 million Australian dollars in performance fees over a six-and-a-half-year period. The infrastructure fund model generated extraordinary returns for Macquarie's investors, but critics argued that the fees came at the expense of long-term asset quality and that the aggressive use of leverage left infrastructure assets vulnerable to economic downturns.

Macquarie's entry into Copenhagen Airport marked the beginning of a new chapter — one defined by financial sophistication, operational optimization, and a fundamentally different relationship between the airport's owners and the Danish state. The question was whether the Vampire Kangaroo would drain the patient or cure it. As the next decade would reveal, the answer was more nuanced than either side initially expected.

V. The Infrastructure Fund Era and Growth Phase (2005–2017)

To understand what Macquarie did with Copenhagen Airport, you first need to understand how airport economics work. An airport like CPH generates revenue from two fundamentally different streams. The first is aeronautical revenue — the charges that airlines pay to use the airport's runways, taxiways, terminals, gates, and baggage systems. These charges are regulated under EU legislation, must be cost-based and uniform for all airlines, and are negotiated through a structured process. An airport cannot simply jack up aeronautical charges to boost profits; the regulatory framework constrains pricing and ensures that airlines are not held hostage by monopoly infrastructure.

The second revenue stream — non-aeronautical revenue — is where the real money is made. This includes everything that happens inside the terminal that is not directly related to moving aircraft: retail shops, restaurants, bars, duty-free outlets, car parking, hotel operations, real estate leasing, and advertising. Unlike aeronautical charges, non-aeronautical revenue is largely unregulated and limited only by the airport's ability to attract passengers and persuade them to open their wallets while waiting for flights.

Copenhagen Airport under Macquarie leaned heavily into the non-aeronautical opportunity. By the mid-2010s, the commercial side of the business accounted for 44 percent of all revenues but a staggering 80 percent of total earnings. The shopping and food outlets alone generated 48 percent of non-aeronautical revenue. This was not accidental. CPH pursued a deliberate differentiation strategy, attracting leading luxury and Scandinavian design brands — Royal Copenhagen porcelain, Georg Jensen silver, Mulberry, Gucci, Burberry — to create a retail environment that felt more like a high-end shopping district than an airport concourse. The strategy earned CPH consistently high rankings in the Skytrax World Airport Awards, and in 2017, the airport was named the best airport in Northern Europe.

The business model was clever but not without risk. An airport that derives 80 percent of its earnings from shopping and dining is, in effect, a mall with runways. When passengers are flowing through in record numbers and spending freely, the economics are spectacular. But the model contains an embedded vulnerability: if traffic drops sharply — because of a pandemic, say, or an economic crisis — the non-aeronautical revenue evaporates just as fast as the aeronautical revenue, but the fixed costs of maintaining an airport remain stubbornly high.

Macquarie also invested heavily in route development and hub strategy. The improvement of Terminal 3, used primarily by Star Alliance carriers, attracted prestigious long-haul operators. Singapore Airlines, Air Canada, and Thai Airways all established scheduled weekly services out of Copenhagen — routes that would have been unthinkable at a Nordic airport a generation earlier. The airport's growing reputation and modern facilities then attracted competitors to Star Alliance as well, creating a virtuous cycle where infrastructure investment drew airlines, airlines drew passengers, and passengers justified further investment.

The most significant new airline relationship was with Norwegian Air Shuttle, the Scandinavian low-cost carrier that was aggressively expanding its long-haul network in the 2010s. Norwegian was a direct competitor to SAS, and its presence at Copenhagen Airport represented a philosophical shift. Under government ownership, CPH had essentially been SAS's captive airport. Under private ownership, the airport was actively courting SAS's competitors — a strategy that boosted traffic volumes but created political tension. CPH also opened its doors to Gulf carriers like Qatar Airways and Emirates, as well as Air India, further diversifying its route network beyond the traditional European and North American markets.

To accommodate the growing low-cost segment, CPH opened a dedicated low-cost carrier facility — initially called CPH Go, later renamed Pier F — in October 2010. The separate facility allowed the airport to serve budget carriers with a lower-cost operational model while maintaining premium service levels in the main terminals. It was a practical solution to a challenge that many European airports struggled with: how to capture low-cost traffic without undermining the premium positioning that drove non-aeronautical revenue.

During its twelve years of ownership, Macquarie invested more than 10 billion Danish kroner in Copenhagen Airport. The investment delivered results: passenger numbers grew from roughly 19 million in 2005 to nearly 30 million by the time Macquarie began contemplating its exit. The airport won numerous industry awards for quality and efficiency. By most operational metrics, the Macquarie era was a success.

But the relationship between Macquarie and the Danish government grew increasingly strained. The government, which retained a significant minority stake and regulatory oversight, began pushing for lower aeronautical tariffs — essentially asking the airport to charge airlines less for using its facilities. For Macquarie, whose investment thesis depended on robust cash flows and returns to fund investors, lower tariffs meant lower returns. The tension was structural: the Danish government's interest as a regulator and minority shareholder (keeping costs low for airlines and passengers) conflicted directly with Macquarie's interest as a majority owner (maximizing cash flows and asset value). This is the fundamental challenge of privatized infrastructure, and Copenhagen Airport became a textbook case study.

By 2017, the relationship had reached a breaking point. On May 23, 2017, Macquarie announced that it would undertake a strategic review of its investment in Copenhagen Airports — Wall Street code for "we're looking to sell." Macquarie had more than doubled its initial investment, generating excellent returns for its fund investors. But the Danish government's pressure on tariffs, combined with the political environment that increasingly favored "long-term" infrastructure investors over financial funds, made it clear that Macquarie's tenure was drawing to a close.

The question was: who would buy one of Northern Europe's most important airports? The answer would come from an unlikely corner — the intersection of Danish and Canadian pension fund capital.

VI. The 2017 Ownership Transformation

When Macquarie put its Copenhagen Airport stake under strategic review, the Danish government was clear about what it wanted: long-term investors who would treat the airport as essential national infrastructure rather than a financial asset to be optimized and eventually flipped. The message was aimed squarely at the infrastructure fund community, which had developed a reputation for acquiring public assets, loading them with debt, extracting fees, and selling them on to the next fund in a daisy chain of ownership that prioritized returns over stewardship.

The buyers who emerged could not have been more different from Macquarie. ATP — Arbejdsmarkedets Tillægspension — is Denmark's largest pension fund, established by the Danish Parliament in 1964 as a supplement to the state pension. With over five million members (essentially every Danish worker), roughly 925 billion kroner in assets under management, and a mandate to provide secure retirement benefits for decades to come, ATP is the definition of a patient, long-term investor. It is, in a very real sense, Denmark investing in Denmark.

ATP's partner in the transaction was the Ontario Teachers' Pension Plan, the Canadian pension fund that manages retirement benefits for over 340,000 active and retired schoolteachers in Ontario. OTPP had been an investor in Copenhagen Airports since 2011 and was one of the first pension plans globally to invest in private infrastructure assets. Its investment philosophy centered on acquiring majority or co-controlling stakes in high-quality core infrastructure — assets providing vital services with stable, inflation-protected cash flows — and holding them for the long term.

Together, ATP and Ontario Teachers' acquired Macquarie's 57.7 percent stake in Copenhagen Airports for approximately 9.8 billion Danish kroner, roughly 1.3 billion euros. For ATP, it was the largest single investment in the fund's history. The scale of the commitment reflected ATP's conviction that Copenhagen Airport was not just a good investment but a strategically important piece of Danish infrastructure that belonged in Danish hands.

The transaction was more than a change of ownership. It represented a philosophical shift in how Copenhagen Airport would be governed. ATP's chief executive stated simply: "The airport in Copenhagen is key infrastructure in Denmark and we are proud to be one of its stewards going forward." The word "steward" was carefully chosen — it signaled a fundamentally different mindset from the financial engineering approach that had characterized the Macquarie years.

Ontario Teachers' was equally explicit about the transition. The fund noted that during its six years partnering with Macquarie, Copenhagen Airports had received numerous industry awards for quality and efficiency, and that it looked forward to "continuing and growing on this track record of success" in partnership with ATP. The emphasis on continuity was important: the pension funds were not acquiring the airport to revolutionize it but to protect and incrementally improve what was already one of Europe's best-run airports.

Under pension fund ownership, Copenhagen Airport continued to invest and grow. Over the fourteen years that Ontario Teachers' was involved in CPH, nearly 18 billion kroner was invested in modernizing and expanding the airport. The approach was different from Macquarie's — less aggressive, less leveraged, more focused on operational excellence than financial optimization — but the results were strong. Passenger numbers climbed to 30.3 million in 2018, a new all-time record, and the airport consistently ranked among Europe's best for punctuality, passenger satisfaction, and operational efficiency.

The pension fund ownership model appeared to offer the best of both worlds: the investment discipline and commercial focus of private ownership, combined with the long-term perspective and alignment with national interests that government ownership provided. If the story had ended here, Copenhagen Airport would have been a straightforward success story — a privatization that worked, followed by a transition to even better-aligned owners.

But then a virus arrived from Wuhan, and everything fell apart.

VII. COVID-19: Existential Crisis and Survival (2020–2023)

Before the pandemic, approximately 83,000 travelers passed through Copenhagen Airport every single day. It was a relentless, round-the-clock operation — planes landing and departing every few minutes, terminals humming with the organized chaos of modern air travel, shops and restaurants generating the non-aeronautical revenue that funded the airport's operations and investment.

Then, in March 2020, that number fell to less than 900.

The collapse was instantaneous and total. Denmark implemented some of the strictest travel restrictions in Europe, and international air travel — Copenhagen Airport's reason for existence — effectively ceased. In the first nine months of 2020, just 6.7 million passengers passed through the terminals, a decline of 71.3 percent from the same period in 2019 — representing 16.6 million fewer passengers. Revenue plummeted by 59.8 percent, falling from 3.3 billion kroner to 1.3 billion. The full-year 2020 total was 7.5 million passengers, with most of those concentrated in January and February before restrictions took hold.

The human cost was devastating. The Danish aviation industry lost an estimated 10,000 jobs, the majority at Copenhagen Airport and its surrounding ecosystem. SAS announced redundancies of up to 1,700 employees in Denmark alone. Norwegian Air, already financially fragile before the pandemic, made more than 600 Danish pilots and cabin crew redundant. Between them, SAS and Norwegian had accounted for 51 percent of traffic at Copenhagen Airport. When your two largest tenants are simultaneously laying off thousands of employees, the scale of the crisis is existential, not cyclical.

CPH's management responded with the grim efficiency that the situation demanded. In late August 2020, the airport cut more than 600 positions — a painful but necessary measure to reduce the burn rate. Capital expenditure was slashed. Every non-essential investment was deferred or cancelled. The focus narrowed to a single objective: survival.

In May 2020, CPH secured a critical lifeline. The company entered into a two-year facilities agreement totaling 6.0 billion kroner with a syndicate of banks — a combination of a 2.0 billion kroner term loan and a 4.0 billion kroner credit facility. CPH also negotiated waiver agreements with existing lenders, providing relief from certain loan covenants that the airport could no longer meet given the collapse in revenue. Without these financial arrangements, Copenhagen Airport would have faced potential covenant breaches and the cascading consequences that follow. The new facilities ensured that CPH could continue to meet its financial commitments and maintain the minimum investment necessary to keep the airport operational.

The summer of 2020 offered a brief, false dawn. Destinations increased from 18 in early June to approximately 100 by August, as European travel restrictions partially eased. But passenger numbers remained 80 to 85 percent below the previous summer's levels. The hoped-for recovery stalled as successive waves of infection prompted renewed restrictions, and 2021 proved almost as brutal as 2020. In the first half of 2021, just 1.4 million passengers used Copenhagen Airport — down 72.5 percent from the already catastrophic first half of 2020. March 2021 saw 106,000 passengers, the lowest monthly figure since the 1970s.

The pandemic also exposed a structural vulnerability that had been quietly developing for years. The shopping malls and food outlets that had been the crown jewel of CPH's business model were experiencing a steady decline in penetration even before COVID struck. The percentage of travelers who bought something from the airport's shops or restaurants had fallen from 65 percent in 2015 to 55 percent in 2019. The causes were familiar to anyone in retail: smartphone shopping, changing consumer habits, and the increasing time pressure of modern travel. COVID accelerated these trends dramatically, as passengers who did fly often rushed through terminals wearing masks, in no mood to browse luxury goods.

This was the fundamental fragility of the non-aeronautical revenue model. When non-aeronautical activities account for 44 percent of revenue but 80 percent of earnings, a sustained decline in retail penetration does not just trim margins — it threatens the entire financial architecture of the airport. The aeronautical side of the business, constrained by regulation and designed to recover costs rather than generate profits, cannot compensate for lost commercial revenue. Copenhagen Airport was, in many ways, a victim of its own success in commercializing its terminals.

But the crisis also catalyzed something unexpected. CPH and several major Danish companies partnered with the City of Copenhagen to launch facilities for sustainable aviation fuel production in the Greater Copenhagen area. A consortium led by CPH, in collaboration with 14 European partners and the Danish Technological Institute, won an EU tender to create the ALIGHT project — an ambitious initiative aimed at building the sustainable airport of the future, addressing everything from energy supply and passenger transport to sustainable heating and cooling. The airport had declared itself carbon-neutral for its own operations in 2019, and the pandemic, paradoxically, created both the urgency and the breathing room to accelerate the sustainability agenda.

The financial losses were staggering — CPH recorded a deficit of 600 million kroner in 2020 — but Copenhagen Airport survived. The pension fund owners, with their long time horizons and deep pockets, proved to be exactly the right kind of shareholders for a crisis of this magnitude. A more leveraged, return-focused owner might have been forced into asset sales or restructuring. ATP and Ontario Teachers' simply absorbed the losses and waited for recovery. It was a powerful, if expensive, validation of the long-term infrastructure investor model that the Danish government had championed in 2017.

The recovery, when it came, was faster than almost anyone dared hope — though it would take until 2025 for passenger numbers to fully surpass pre-pandemic levels. And by the time they did, the ownership structure of Copenhagen Airport had changed once again.

VIII. Recovery and Renationalization (2023–2025)

Copenhagen Airport reported a pre-tax profit of 398 million kroner for 2023 — the first meaningful profit since the pandemic — on passenger volumes of 26.8 million, a 21 percent increase from the previous year though still 12 percent below the 2019 peak of 30.3 million. The recovery was real but incomplete, and the airport was simultaneously navigating the fallout from SAS's Chapter 11 bankruptcy filing in July 2022.

The SAS restructuring was a pivotal event for Copenhagen Airport, though not in the way that many observers initially feared. SAS had filed for bankruptcy protection in the United States, weighed down by low-cost carrier competition, rising fuel costs, the closure of Russian airspace following the Ukraine invasion, and a devastating pilots' strike that had grounded 50 percent of flights. The restructuring eliminated over two billion dollars in debt, renegotiated leases on 59 aircraft (saving approximately 98 million dollars annually), and brought in new ownership led by Castlelake, Air France-KLM (with a 19.9 percent stake), Lind Invest, and — crucially — the Danish State, which took a 25.8 percent share.

The restructured SAS made two decisions that dramatically benefited Copenhagen. First, it consolidated from three roughly equal Scandinavian hubs down to Copenhagen as its clear primary hub. Second, it switched from the Star Alliance to SkyTeam, aligning with Air France-KLM and opening code-share opportunities across a different and complementary global network. For Copenhagen Airport, the combination was transformational: more SAS flights concentrated at CPH, plus new partnership routes through the SkyTeam alliance, plus new service from American Airlines eager to compete on transatlantic routes that the SAS-Air France-KLM partnership made more attractive.

In 2024, the recovery accelerated. Copenhagen Airport handled 29.9 million passengers — just shy of the 2018 record — with 175 destinations served across 342 routes. Revenue surged to 5.07 billion kroner, a 25 percent year-over-year increase, with aeronautical revenue jumping 40 percent as traffic volumes normalized and the new charges framework took effect. Transfer passengers reached 5.7 million, a 19 percent increase that reflected Copenhagen's strengthening position as a connecting hub. December 2024 was the best December in the airport's history.

It was against this backdrop of robust recovery that the Danish government made its most consequential decision regarding Copenhagen Airport since the original privatization three decades earlier. In December 2024, Finance Minister Nicolai Wammen announced a conditional agreement for the Danish state to acquire ATP's 59.4 percent stake in Københavns Lufthavne for 32 billion kroner — approximately 4.5 billion dollars. Combined with the state's existing stake of approximately 39.2 percent (accumulated through the original retained shares and subsequent acquisitions), the transaction would give the Danish government roughly 98 percent ownership of the airport.

The renationalization was the product of a political coalition that included the governing Social Democrats, the Socialist People's Party, and the Social Liberals. Notably, the Conservative Party declined to sign the final agreement, arguing that the state should not necessarily hold such a dominant majority share. The political debate was substantive: conservatives pointed out that the airport had performed well under private and pension fund ownership, while the coalition argued that critical national infrastructure of this importance required direct state control to ensure alignment between airport development and national economic interests.

Wammen framed the decision in terms of national sovereignty and strategic importance. "Copenhagen Airport is of enormous importance both to the people of Copenhagen and to all of Denmark," he stated, while pledging an "arm's length principle" that would keep the government out of day-to-day operations. The subtext was clear: Denmark had watched its most important transportation asset pass through three different ownership regimes in three decades, and the government had concluded that the only way to guarantee long-term alignment between airport strategy and national interests was to own the asset outright.

SAS welcomed the renationalization enthusiastically. President and CEO Anko van der Werff called it "a crucial step for Danish and Scandinavian connectivity," arguing that strengthening Copenhagen Airport as a global hub required close collaboration between all stakeholders. For SAS, which was now partially state-owned itself, having a state-owned hub airport created a natural alignment of interests that had been impossible under Macquarie or even the pension fund owners. The airline noted that its expansion plans from Copenhagen — positioning the airport as a premier global gateway to and from Scandinavia — required substantial coordinated investment from both SAS and CPH.

The European Commission approved the transaction on July 16, 2025, and the acquisition completed on September 30, 2025. The Danish state now holds approximately 98.6 percent of Copenhagen Airports A/S. The remaining shares are scattered among retail investors who held through the various ownership transitions.

But the political agreement contained a crucial caveat. The government does not intend to maintain near-complete ownership permanently. The agreement includes a provision requiring the state to gradually reduce its ownership stake to 50.1 percent through one or more future divestments, while retaining a majority position. In other words, Denmark plans to privatize the airport again — but this time, it will do so from a position of control, setting the terms and selecting investors rather than watching a financial cascade of ownership changes from the sidelines. The 50.1 percent threshold ensures that the government will never again face the situation it confronted in the Macquarie era, where a foreign infrastructure fund held effective control over Denmark's most important gateway.

The full-circle journey — from government enterprise to publicly traded company to infrastructure fund asset to pension fund holding to re-nationalized state company — took exactly thirty-five years. Whether it represents a triumph of pragmatic governance or an expensive admission that the privatization was a mistake depends on where you sit. What is undeniable is that Copenhagen Airport emerged from the cycle in better shape than it entered: more modern, more connected, more commercially sophisticated, and now on the cusp of its most ambitious expansion in decades.

In 2025, Copenhagen Airport set a new all-time passenger record of 32.4 million, generating revenue of 5.5 billion kroner and an operating profit of 1.84 billion kroner with a 49.6 percent EBITDA margin. The board proposed no dividend, signaling that the cash would be reinvested in the massive capacity expansion that the state-owned airport now has the freedom to pursue without the pressure of returning capital to financial investors. It was, perhaps, the most Danish outcome imaginable: a century of pragmatic experimentation, ending with the country quietly taking back control of its own front door.

IX. Modern Operations and Competitive Position

Stand in the departures hall of Copenhagen Airport today and the scale of the operation is quietly impressive. More than 160 destinations are served by 54 airlines, with 342 active routes spanning six continents. European routes account for 84 percent of total traffic, with the United Kingdom the most popular country destination at 2.8 million passengers annually, followed by Spain and Norway at 2.5 and 2.4 million respectively. The airport employs over 17,000 people, making it one of the largest single-site employers in Denmark.

What makes Copenhagen Airport's competitive position particularly interesting is not just its size but its efficiency trajectory. Despite handling a growing number of passengers — 32.4 million in 2025, up from 29.9 million the year before — the number of passenger flights taking off or landing has actually decreased by nine percent over the past five years. This seemingly paradoxical trend reflects a fundamental shift in the aviation industry: airlines are replacing older, smaller aircraft with newer, larger, and more fuel-efficient models. The average load factor — the percentage of seats sold on each flight — has also increased. More passengers, fewer flights, fuller planes. For an airport constrained by two runways and surrounded by urban development, this trend is enormously valuable: it allows CPH to grow passenger volumes without proportional growth in the runway operations that drive noise complaints and environmental impact.

The hub strategy has matured significantly. A growing number of passengers — 5.7 million in 2024, a 19 percent year-on-year increase — now use Copenhagen as a connecting point rather than a final destination. The majority of these transfer passengers fly in from secondary airports in Sweden, Norway, and Germany, connecting through CPH to 175 destinations worldwide. This connecting traffic is the hallmark of a true hub airport and represents a competitive moat that is extraordinarily difficult for rival airports to replicate. Once an airport achieves critical mass as a connecting hub, the network effects become self-reinforcing: more connecting routes make the airport more attractive for new route launches, which attract more connecting passengers, which justifies even more routes.

In the competitive landscape of Nordic aviation, Copenhagen's position is strong but not unassailable. Oslo Gardermoen, the second-largest Nordic airport at 26.4 million passengers, boasts the title of the world's most punctual large airport, with a 91.2 percent on-time departure rate that embarrasses most of its global peers. Stockholm Arlanda, at 22.7 million passengers, benefits from serving Sweden's largest economy but suffers from its 40-minute rail journey to the city center — nearly three times Copenhagen's 15-minute connection. Helsinki Vantaa, with 16.3 million passengers, has carved a distinctive niche as the gateway between Europe and Asia, leveraging Finnair's hub to offer the shortest flight times between many European and East Asian city pairs.

Copenhagen's competitive advantages are structural and difficult to replicate. Its proximity to the city center — 15 minutes by train, or roughly 8 kilometers — is among the closest of any major European airport. The Øresund Bridge catchment area, encompassing 4.2 million people across two countries, gives CPH a passenger base significantly larger than Copenhagen's metropolitan population alone. Its on-time performance ranks second among large European airports. And its cargo operation, at 345,000 tonnes annually, is the largest in the Nordics — a revenue stream that provides diversification from passenger-dependent income.

The sustainability program adds another dimension to CPH's competitive positioning. The airport has been carbon-neutral for its own operations since 2019 and has set targets to be entirely emission-free by 2030 for airport operations and ground transport, with a 2050 target for complete carbon neutrality across all scopes — including air traffic, on-airport companies, and surface access. These are ambitious targets, and the airport's participation in EU-funded sustainability initiatives like the ALIGHT project demonstrates genuine commitment rather than mere greenwashing. As European regulators increasingly incorporate environmental performance into airport licensing and expansion decisions, Copenhagen's sustainability leadership could become a meaningful competitive advantage.

For investors evaluating Copenhagen Airport's position and tracking its ongoing performance, two metrics matter above all others. The first is revenue per passenger — the total revenue generated divided by the number of passengers processed, which captures both aeronautical pricing power and commercial spending per traveler. This single number encapsulates the airport's ability to monetize its traffic, and trends in this metric reveal whether growth is coming from volume alone or from genuine value creation. The second is transfer passenger share — the percentage of total passengers who are connecting through CPH rather than originating or terminating. This metric measures the strength of Copenhagen's hub function and the depth of its competitive moat, since transfer passengers represent incremental revenue that competing airports cannot easily poach. Together, these two KPIs tell you whether Copenhagen Airport is growing profitably and whether its strategic position as a connecting hub is strengthening or eroding.

The Vilhelm Lauritzen terminal, the 1939 functionalist masterpiece that established Copenhagen Airport's architectural identity, still stands on the airport grounds. In 1999, in a remarkable feat of engineering, the entire 110-meter-long, 2,240-tonne structure was moved 3,800 meters across the runway and rotated 180 degrees in a single overnight operation while most air traffic over Copenhagen was suspended. The Danish government invested 100 million kroner in its preservation, and the building — now a national heritage site — is used for receiving heads of state and special occasions. Its design principles continue to inform CPH's expansion plans, including the upcoming Terminal 3 expansion scheduled for 2028.

There is something fitting about that preserved terminal. Copenhagen Airport has always been, at its core, a Danish institution — practical, well-designed, efficient, and quietly excellent. It has survived world wars, ownership experiments, financial crises, and a pandemic. It has been a government department, a stock market darling, an infrastructure fund asset, and a pension fund portfolio holding. Now, a century after a flock of sheep kept its grass runway trimmed, it belongs to Denmark again. The next chapter — how the state manages the airport it spent 32 billion kroner to reclaim, and whether a partial re-privatization can capture the benefits of private capital without the drawbacks — will determine whether Copenhagen Airport's second century matches the extraordinary trajectory of its first.

X. Bull Case, Bear Case, and Strategic Assessment

The Bull Case

Copenhagen Airport's competitive position rests on structural advantages that are nearly impossible for competitors to replicate. Analyzed through Michael Porter's Five Forces framework, the picture is compelling. The threat of new entrants is essentially zero — nobody is building a new airport to compete with CPH in the Copenhagen metropolitan area, and the Øresund Bridge catchment area creates a natural monopoly spanning two countries. Supplier power (airlines) is moderate but manageable; while individual carriers can threaten to reduce service, the airport's diverse base of 54 airlines means no single carrier holds outsized leverage, and SAS's post-restructuring consolidation at CPH actually strengthens the relationship. Buyer power (passengers) is limited because travelers generally choose airlines and destinations, not airports — Copenhagen is simply where you fly from if you live in the Øresund Region. The threat of substitutes is real but manageable: high-speed rail competes on short-haul European routes, but no rail connection can replace CPH for intercontinental travel. And competitive rivalry among Nordic airports, while genuine, is constrained by geography — a passenger in Malmö is not going to drive five hours to Stockholm Arlanda when CPH is 25 minutes away by train.

Through the lens of Hamilton Helmer's 7 Powers framework, Copenhagen Airport's most powerful moat is arguably network economics — the self-reinforcing dynamic where more routes attract more passengers, which attract more airlines, which launch more routes. A hub airport with critical mass of connecting traffic becomes exponentially more valuable with each additional route, and competing airports face a cold-start problem in trying to replicate that network. CPH also benefits from counter-positioning relative to its Nordic competitors: by investing early in low-cost carrier accommodation, luxury retail, and sustainability infrastructure, it made strategic choices that established airports like Stockholm Arlanda and Oslo Gardermoen chose not to match, at least not at the same scale or pace. And the geographic advantage — proximity to city center, the Øresund bridge — constitutes a form of cornered resource that no amount of investment by competitors can neutralize.

The 2025 record of 32.4 million passengers, combined with 5.5 billion kroner in revenue and a nearly 50 percent EBITDA margin, demonstrates that the business is operating at a high level. The SAS restructuring and consolidation at CPH, the Air France-KLM partnership, and the growing transfer passenger volumes all point to a strengthening hub function. State ownership, while introducing political risk, also eliminates the short-term financial pressures that private owners imposed and allows for the kind of long-term capacity investment that airport infrastructure requires. The planned Terminal 3 expansion, scheduled for 2028, would add significant capacity and modernize the passenger experience.

The Bear Case

The most immediate risk is political. State ownership means political oversight, and political priorities do not always align with commercial optimization. The Danish government has pledged an "arm's length principle," but maintaining that separation under pressure — when constituents complain about noise, when politicians demand lower charges for favored airlines, or when environmental groups oppose expansion — requires institutional discipline that few governments sustain indefinitely. The history of state-owned enterprises globally suggests that operational efficiency tends to erode over time under government control, particularly when the urgent commercial pressures of private ownership are absent.

The non-aeronautical revenue model, while recovering from the pandemic, faces structural headwinds. The pre-COVID decline in retail penetration — from 65 percent to 55 percent between 2015 and 2019 — reflected global consumer trends that the pandemic accelerated rather than caused. E-commerce, duty-free price transparency, and changing travel demographics (younger travelers spend less in airport shops) all suggest that the 80-percent-of-earnings contribution from commercial activities may be difficult to maintain. If commercial revenue per passenger continues to decline, the airport will need to grow aeronautical charges to compensate — creating tension with airlines and regulators.

Competitive threats, while contained, are not negligible. Helsinki Vantaa's position as the Asia gateway could erode Copenhagen's connecting traffic if Asian airlines consolidate their European hub operations. Oslo's expansion plans and consistently superior punctuality performance create a credible alternative for Norwegian travelers who currently connect through CPH. And the planned re-privatization — reducing state ownership to 50.1 percent — introduces execution risk: the government must find buyers who share its long-term vision, at a price that represents fair value for taxpayers, in a market that may or may not be receptive when the time comes.

The board's decision to pay no dividend in 2025 despite record revenue signals that substantial capital expenditure lies ahead. Infrastructure investment creates long-term value but compresses near-term returns. The Terminal 3 expansion and sustainability initiatives will require billions of kroner over the coming decade, and the airport's ability to fund these investments while maintaining financial flexibility will be tested.

The SAS dependency, while reduced from historical levels, remains significant. SAS's post-restructuring financial position is improved but not yet proven over a full economic cycle. If the airline were to experience renewed financial difficulty, the impact on Copenhagen Airport's traffic and revenue would be substantial, even with the diversified carrier base.

Myth vs. Reality

There is a prevailing narrative that Copenhagen Airport's privatization was a failure that the renationalization corrected. The reality is more nuanced. The privatization unlocked billions of kroner in investment that modernized the airport and drove passenger growth from under 20 million to over 30 million annually. The Macquarie era, for all its financial engineering, produced an objectively better airport than the government enterprise that preceded it. The renationalization was less a repudiation of privatization than a recognition that infrastructure of this strategic importance requires an ownership structure aligned with national interests over decades, not fund cycles. Whether the state can deliver the operational discipline and investment commitment that private capital provided remains the open question — and the answer will determine whether Copenhagen Airport's remarkable century of growth extends into its second hundred years.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube