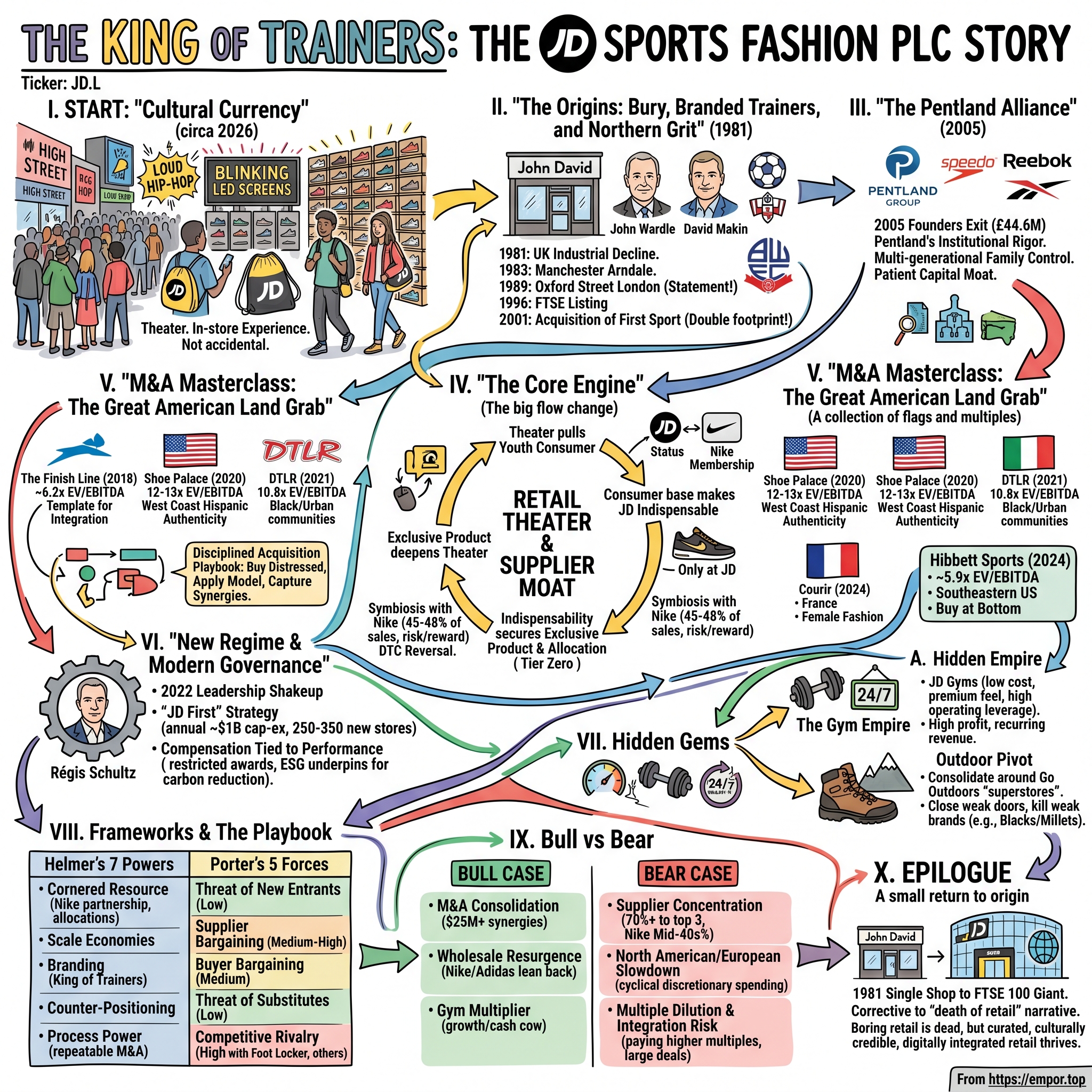

The King of Trainers: The JD Sports Fashion plc Story

I. The Sneaker as Cultural Currency

Walk down a high street in Manchester, Birmingham, or Brixton on a Saturday afternoon and you will hear a JD Sports store before you see it. Bass-heavy drill or hip-hop spills out onto the pavement. Inside, LED screens flash in black and yellow, walls of boxed trainers stand stacked like a sneaker armory, and teenagers move through the space less like shoppers and more like worshippers in a temple of footwear. They leave clutching the unmistakable yellow-and-black drawstring duffle bag — a bag that, once slung over a shoulder, becomes a walking advertisement carried for free across every bus stop, school gate, and council estate in Britain. This is not accidental. It is, in the truest sense of the word, theater.

For the better part of two decades, the conventional wisdom in retail held that the physical store was a dying species. The internet would hollow it out. Direct-to-consumer brands would cut out the middleman. Amazon would eat everything else. And for a stretch between roughly 2017 and 2022, the two most powerful athletic brands on the planet — Nike and Adidas — appeared to believe exactly that, pouring billions into selling directly to consumers and quietly starving their wholesale partners of product. The retailers were supposed to wither.

JD Sports did the opposite. It became more essential. By 2026, the company that started as a single shop in the unglamorous Greater Manchester town of Bury had grown into a FTSE 100 constituent operating more than 3,400 stores across roughly 30 countries, with revenue north of £10.5 billion.1 More remarkably, it had achieved something almost no other retailer on earth could claim: the world's most powerful brands needed JD more than JD needed any single one of them. When Nike's direct-to-consumer gamble cooled, it did not retreat to a generic department store. It deepened a "Connected Partnership" with JD, plugging its own membership program directly into JD's loyalty system.7

That is the puzzle this story tries to solve. How does a brick-and-mortar trainer shop build a moat so deep that two suppliers, each individually far larger than JD itself, find themselves structurally dependent on it? The answer is not one thing. It is a layered system: a cult-like in-store experience that no website can replicate, an allocation status with suppliers that no upstart can buy, roughly half of its product range available nowhere else, and — quietly underneath it all — a discipline around capital and acquisitions that would make a private equity partner nod in approval.

Here is the roadmap. We begin in Bury in 1981 with two unlikely founders. We trace the handover to the Pentland Group, the multi-generational family conglomerate that bought a controlling stake and then mostly got out of the way. We dissect the core engine — retail theater and the supplier moat. We walk through a masterclass in international M&A, from the great American land grab to the European female play. We meet Régis Schultz, the French executive now steering the ship. We uncover the hidden businesses — a 24/7 gym empire and an outdoor consolidation play — that almost nobody talks about. And we close with the frameworks, the bull and bear cases, and the one or two numbers that actually matter for anyone trying to understand where this company goes next.

Let's start where every good origin story starts: with two men who had no obvious business being in business together.

II. The Origins: Bury, Branded Trainers, and Northern Grit

The founding of JD Sports does not have a monsoon moment or a garage in California. It has something far more British: a town in Greater Manchester, a recession, and a partnership between a man twice the age of his collaborator. In 1981, the United Kingdom was deep in industrial decline. Unemployment was climbing toward three million. The North of England, in particular, was being hollowed out as factories closed. It was, on paper, an absurd time to open a retail shop.

John Wardle was not a natural retailer. By the time he co-founded the business at the age of 36, he had already lived several lives. He had been a Manchester fireman. He had worked as a civil servant. And, in the detail that says the most about him, he had been a footballer on the books at Bolton Wanderers before injury ended that dream. Retail was, in effect, his third career — a man searching for the thing that would finally stick. The "John" and the initials of the venture would eventually give the company half its name.

His partner could not have been more different. David Makin was eighteen years old. Where Wardle brought life experience and capital steadiness, Makin brought something rarer and more valuable: an almost preternatural instinct for what young people actually wanted to put on their feet. Together, "John" and "David" became JD. And the first and most important decision they made was a decision about what not to sell.

The default model for a sports shop in 1981 was the generalist sporting-goods store — a cluttered emporium of cricket bats, footballs, tennis rackets, shin pads, and the occasional rack of plimsolls. It was a business of breadth, of stocking a little of everything for the weekend amateur athlete. Makin's insight, and the hill he was willing to die on, was that this was precisely the wrong business to be in. The future was not in equipment for people who played sport. It was in footwear for people who wanted to look like they played sport. Youth culture was beginning to treat athletic trainers not as gym kit but as everyday street fashion — a uniform of identity, status, and belonging. Makin convinced Wardle to abandon the heavy, low-margin generic goods and concentrate exclusively on premium branded footwear.

That pivot — from performance to lifestyle, from breadth to curated depth — is the genetic code of everything JD Sports would later become. The first shop opened in Bury on July 19, 1981.1 It was small, but it had a point of view, and points of view scale. By 1983 they had pushed into the Manchester Arndale Centre, the regional shopping hub, planting the flag in a location with real footfall. Through the 1980s they built out a Northern English footprint, store by store, learning the grammar of youth retail: which brands sold, which colorways moved, how the energy of a shop floor could itself become a product.

The truly audacious move came in 1989, when JD opened on Oxford Street in London. For a Manchester regional chain, planting a store on the most famous shopping street in the country was a statement of ambition far beyond its size — a declaration that this was not going to remain a Northern curiosity. Regional dominance gave way to national presence, and in 1996 the company formalized its arrival by listing on the London Stock Exchange as "John David Sports plc."1 The two founders were now running a public company.

The next decade was about scale, and the defining move was the 2001 acquisition of First Sport, which roughly doubled JD's store footprint by adding more than 200 locations in a single stroke.1 It was an early demonstration of a muscle JD would later flex repeatedly on a global stage: the ability to absorb another retailer's estate and re-skin it in the JD image. But running a fast-growing public retailer is a different sport from founding one, and by the early 2000s the founders were ready to move on.

The exit came in 2005. Having already sold down over the years, Wardle and Makin sold their remaining holding — a roughly 45% stake — to the Pentland Group for approximately £44.6 million, ending the founder era.1 It is one of those numbers that looks almost quaint with hindsight, given what the company would become worth, but it reflected the JD of its moment: a strong regional player, not yet the global force. Makin, restless as ever, would go on to apply everything he had learned to build a direct competitor, Footasylum — a chain that, in one of retail's neater ironies, JD itself would later attempt to acquire and find itself entangled with regulators over.

The founders had built the engine. But it would take a different kind of owner — patient, capital-rich, and steeped in the global mechanics of sneaker distribution — to turn that engine into a juggernaut. That owner had a history with athletic footwear stranger and more lucrative than almost anyone else's on earth.

III. The Pentland Alliance and the Transition to Institutional Moats

To understand why the Pentland Group was the perfect owner for JD Sports, you have to go back to a transaction so improbable it sounds invented. In 1981 — the very same year Wardle and Makin opened in Bury — Pentland, the British family business controlled by the Rubin family, paid $77,500 for a 55% stake in a small, then-obscure American running-shoe company called Reebok.8 Over the following years, as Reebok rode the aerobics boom into a global phenomenon, that tiny stake became worth hundreds of millions of dollars. It remains one of the great venture-scale returns in the history of consumer products, and it was earned not by a Silicon Valley fund but by a family-owned British conglomerate.

The lesson Pentland took from the Reebok experience was profound and durable: footwear culture is a generational, global force, and the money is made by those who understand distribution, brand relationships, and the patience to ride a cultural wave for decades rather than quarters. This was not a family that needed to be taught what a trainer meant to a sixteen-year-old.

By the time it took control of JD Sports, Pentland was a sprawling private conglomerate. It owned, among others, the swimwear icon Speedo, the outdoor-gear brand Berghaus, the football-equipment maker Mitre, and the rugby specialist Canterbury.8 This was a house of brands run by people who lived and breathed the supply chain — who understood both sides of the table, manufacturing and retail, brand and store.

The 2005 takeover of the founders' stake therefore brought something more than capital. It brought institutional rigor and a global rolodex. Pentland's relationships and its understanding of how brands allocate product, manage inventory, and build cultural cachet plugged directly into JD's retail engine. Where the founders had instinct, Pentland added system. The combination — Northern retail intuition married to global conglomerate discipline — is the foundation on which the modern company was built.

The structural feature that matters most for any long-term investor, though, is control. As of early 2026, the Pentland Group held a 54.4% majority stake in JD Sports.1 That single fact reshapes how the entire company behaves. JD is a FTSE 100 company with the daily liquidity and scrutiny of a public listing, but it is governed, in effect, like a family business. A multi-generational family office holding the majority of the shares is not going to panic-sell on a weak quarter, demand a dividend the balance sheet cannot support, or force a short-term decision to hit a near-term earnings print.

This shield against short-term public-market pressure is itself a form of competitive advantage. It is what allows JD to do things that quarter-to-quarter-managed retailers struggle to do: buy distressed competitors at the bottom of their cycle, invest heavily in the in-store experience when the payback is years out, and absorb the messy, margin-dilutive early phase of integrating a newly acquired chain without flinching. Patient capital, in retail, is a moat unto itself — and JD has it in a way almost no listed competitor does.

For an investor, the practical implication is twofold. On one hand, the Pentland majority provides stability and a long-term orientation that aligns reasonably well with fundamental shareholders who think in years. On the other, minority holders should be clear-eyed that they are passengers: the controlling family's interests, not the marginal public shareholder's, set the strategic direction. With that ownership backdrop established, we can turn to the thing the company actually does — and the in-store machine that makes the whole edifice work.

IV. The Core Engine: Retail Theater and the Supplier Moat

Picture two stores selling the exact same Nike trainer. One is a quiet, well-lit aisle in a department store, the shoe sitting on a shelf under a polite little price card. The other is a JD store: the lights are dramatic, the music is loud enough to feel in your chest, the walls are a cliff-face of boxes in black and yellow, the staff are young and move with the energy of people who genuinely care which colorway just dropped, and a screen overhead is playing a hype reel for the latest release. Same shoe. Completely different product. Because in the second store, you are not buying a shoe. You are buying into a scene.

This is what JD insiders and the wider industry call "retail theater," and it is the first layer of the company's moat. The high-contrast aesthetic, the curated soundtrack drawn from grime, drill, and hip-hop, the deliberate sensory intensity — all of it is engineered to make the store a destination, a hangout, a place where the target youth demographic wants to be, not merely transact. A website cannot replicate the feeling of being there with your friends on a Saturday. A sprawling generic sports megastore, all fluorescent lights and forklift pallets, actively repels it. JD's stores are designed as community spaces, and that emotional pull is precisely the thing e-commerce cannot commoditize.

But theater alone does not explain the depth of the moat. The second and more powerful layer is the relationship with the suppliers — above all, Nike. JD is the global strategic retail partner of choice for both Nike and Adidas, and the dependence runs deep in both directions. Nike alone has accounted for somewhere in the range of 45 to 48% of JD's total sales.2 That is an enormous concentration, and we will return to it as a genuine risk in the bear case. But it also reflects a symbiosis that JD has worked relentlessly to make irreplaceable.

The clearest expression of that symbiosis came in 2022, when JD became the first European retailer to launch a "Connected Partnership" with Nike.7 In plain terms, the two companies wired their loyalty programs together: JD's own membership system, "JD Status," was linked directly with "Nike Membership." For the shopper, this means a single connected experience — access to exclusive Nike products, shared digital inventory visibility, and instant rewards delivered through the app. For the two companies, it means something more strategic. Nike gets a direct, data-rich line to the youth consumer at the physical point of culture; JD gets privileged access to the most coveted product and membership perks that no rival can match. Once a brand has integrated its loyalty infrastructure into a retailer's app, unwinding that relationship becomes genuinely painful. Integration is stickiness.

The third layer is the product itself. Roughly half of JD's inventory consists of so-called "Special Make-Ups," or SMUs — exclusive colorways, materials, and silhouettes negotiated directly with the brands and available only at JD.2 The marketing shorthand is "Only at JD," and it is the answer to retail's oldest vulnerability: if a customer can buy the identical product anywhere, they will buy it wherever is cheapest, and the retailer is reduced to a commodity price-taker. By ensuring that around half its range exists nowhere else, JD breaks that comparison entirely. You cannot price-shop a shoe that only one chain is allowed to sell.

Underneath the SMUs sits the allocation hierarchy — the invisible pecking order that determines which retailers receive the hot product and which are left with the leftovers. When a lifestyle silhouette catches fire — the Adidas Samba, the Gazelle, the Campus 00s during their recent cultural surge — the brands do not spread that scarce, high-demand inventory evenly. They send it to their top-tier partners first and in volume. JD's "Tier Zero" status means it receives deep allocations of exactly the products that drive sneaker culture, while lower-tier retailers are effectively starved.2 In a business where being out of the shoe everyone wants is fatal, guaranteed access to the hero product is a structural advantage that compounds: more hot product draws more customers, which justifies even deeper allocations.

All of this was thrown into sharp relief by what we might call the DTC reversal. From roughly 2017 to 2022, Nike and Adidas pursued aggressive direct-to-consumer strategies, betting that the future was selling straight to the consumer through their own apps and stores, and pulling back from wholesale partners. The logic was seductive — capture the full margin, own the customer data, control the brand presentation. But the strategy hit a wall. Selling directly is operationally expensive, it sacrifices the cultural reach and curation that great retailers provide, and when fashion cycles turned and inventory piled up, the brands discovered they needed strong wholesale partners both to capture youth culture and to clear product at scale. By the early 2020s, the brands were "leaning back" into premium wholesale — and the premium wholesale partner with the deepest cultural credibility and the best physical theater was JD.8

The takeaway for an investor is that JD's moat is not a single feature but a reinforcing system: theater pulls in the youth consumer, that consumer base makes JD indispensable to the brands, that indispensability secures the exclusive product and allocation, and the exclusive product deepens the theater. Each layer makes the others harder to attack. With the engine understood, the question becomes how JD turned this domestic system into a global one — and that story is largely a story of disciplined acquisition.

V. The Great American Land Grab: An M&A Masterclass

For all the talk of retail theater and brand relationships, the thing that genuinely separates JD Sports from its peers — and the thing fundamental investors should study most closely — is its conduct as a buyer of companies. Plenty of retailers grow by acquisition. Very few do it with discipline. JD's record reads less like a typical retail roll-up, which tends to overpay at the top of the cycle in a fit of empire-building, and more like a patient value investor's playbook: buy distressed assets at low multiples, apply a proven operating model, and capture the synergies. The United States — the largest athletic footwear market in the world, and a highly consolidated one — became the proving ground.

The first major move was The Finish Line in 2018. Finish Line was a large, struggling American chain, and JD acquired it for $13.50 per share in cash, an equity value of roughly $558 million and an enterprise value of about $588 million.39 What matters is not the headline figure but the multiple: JD paid around 6.2 times EV/EBITDA.3 To judge whether that was cheap or dear, you have to benchmark it against the comparable universe. Sporting-goods and athletic retailers at the time traded in a band of roughly 5.9 to 6.5 times — Foot Locker around 6.2 to 6.5 times, Dick's Sporting Goods around 6.0 to 6.5 times. JD paid squarely in the middle of the industry range for a company that was struggling, which means it paid a normal price for a turnaround it believed it could execute. It did not overpay.

The proof that it was a bargain came from an unlikely source: Finish Line's own shareholders, some of whom filed a class-action lawsuit alleging the price was unfairly low.9 Few things validate a buyer's discipline like the seller's shareholders complaining they were underpaid. What JD acquired was a footprint of more than 930 locations, including the Finish Line concessions operating inside Macy's department stores — instant, massive scale in a market it had barely touched. JD then did what it does: applied the retail theater model, converted underperforming Finish Line stores to the JD fascia, and drove operating margins up on an estate that had been languishing. It was the template for everything that followed.

If Finish Line was about footprint, the next two deals were about demographics — buying not just stores but specific cultural niches that JD's existing brand could not easily reach on its own. In 2020, JD acquired Shoe Palace for $681 million, at an estimated 12 to 13 times EV/EBITDA.4 That is, on its face, an expensive multiple — roughly double what JD paid for Finish Line. But the logic was strategic rather than purely financial. Shoe Palace gave JD immediate, credible access to the West Coast Hispanic consumer and a portfolio of prime real estate in California and Texas, two of the most important markets in the country. Some doors you cannot build your way into; you have to buy your way in, and you pay for authenticity.

The following year, 2021, brought DTLR, acquired for $495 million at 10.8 times EV/EBITDA.5 DTLR's strength was its deep positioning in Black and urban communities across the East Coast and Midwest — a different demographic and a different geography from Shoe Palace, completing a kind of cultural map of the American sneaker consumer. Together, the Shoe Palace and DTLR deals showed that JD understood something subtle: the U.S. is not one market but many overlapping cultural markets, and owning credibility in each requires owning the retailer that already has it. The premium multiples were the price of authenticity, and JD was willing to pay it where authenticity could not be manufactured.

Then the strategy crossed back over the Atlantic with a different goal entirely. In 2024, JD acquired the French chain Courir at an enterprise value of €520 million, roughly £453 million, structured as €325 million in cash plus €195 million in assumed debt.1 On around €65 to 70 million of EBITDA, that worked out to roughly 7.5 to 8.0 times EV/EBITDA, and about 10.3 times EV/EBIT. Now, that multiple was higher than JD's own depressed trading multiple at the time, which had fallen to around 4 to 5 times — a point the bears seize on, and rightly so. But it was still well below the active-lifestyle industry median of around 11.3 times, so in absolute terms JD was not overpaying for the sector. And the strategic rationale was unusually clean: Courir holds roughly a 16% market share in France and is positioned squarely at a female, fashion-conscious customer.1 JD's historical skew was young and male; Courir directly rebalanced that, adding a demographic JD had under-served. Complementary, not redundant — exactly the kind of fit that makes integration worthwhile.

The largest and most recent of the major deals was Hibbett Sports, also in 2024, at an enterprise value of about $1.1 billion, or $87.50 per share in cash.6 The multiple was roughly 5.9 times EV/EBITDA on a forward basis, or about 6.2 times trailing adjusted EBITDA.6 Here the discipline shows most clearly. Hibbett had historically traded in a band between roughly 7.1 and 9.8 times EBITDA; JD bought it near a deep cyclical low, paying a multiple at the bottom of its historical range. Hibbett's value was its enormous footprint in Southeastern U.S. community markets — smaller towns and suburban locations where it was often the destination for athletic footwear. In 2026, JD announced plans to prune roughly 175 underperforming Hibbett stores to optimize productivity, while converting key remaining locations into higher-margin JD storefronts.1 Buy at the bottom, cut the dead weight, re-skin the survivors in the more profitable fascia — the Finish Line template, run at a billion-dollar scale.

Step back and the pattern across all five deals is unmistakable. JD pays low multiples for footprint and turnaround (Finish Line, Hibbett), and is willing to pay up only for irreplaceable demographic access (Shoe Palace, DTLR, Courir). It buys at cyclical lows when it can. And it has a repeatable integration playbook — convert fascias, cut underperformers, capture supply-chain synergies — that turns acquired estates into JD machines. For investors, the M&A record is arguably the single best evidence that management allocates capital like owners rather than empire-builders. But a roll-up of this scale lives or dies on execution, and execution is a function of leadership. So who is running this machine now?

VI. The New Regime: Régis Schultz and Modern Governance

Every long-running company has a moment when it stops being defined by the people who built it and starts being defined by the institution it has become. For JD Sports, that moment crystallized in 2022. The company's long-serving executive leadership — the team that had driven the spectacular growth of the prior decade — departed amid a significant shakeup, and the board used the transition to pivot toward a more institutionalized model of corporate governance. The era of the dominant founder-operator personality gave way to the era of the professional global executive.

The man hired to lead that era was Régis Schultz, who became chief executive in September 2022.8 Schultz was, in many ways, a deliberate counterpoint to JD's scrappy Northern English origins. He was a French executive with a deeply international résumé: senior roles at Al-Futtaim, the Middle Eastern retail giant that operates everything from automotive to fashion across the Gulf, and earlier at Monoprix, the French grocery and lifestyle chain. This was not a man steeped in the culture of the Bury shop floor. He was a builder of large, complex, multi-geography retail operations — which is precisely what JD had become and precisely what it needed to manage going forward.

Schultz wasted little time setting the agenda. He launched the "JD First" strategy, a five-year growth plan with genuinely aggressive ambitions: deploying over $1 billion in annual capital and opening somewhere between 250 and 350 new stores per year globally.8 This was a declaration that JD intended to press its advantage at scale rather than consolidate and coast — to keep planting the black-and-yellow flag in new markets while the brand relationships and the M&A machine were running hot. For a company already past £10 billion in revenue, committing to that pace of organic store growth on top of acquisitions signals real conviction about the durability of the moat.

How Schultz is paid tells you a great deal about how the board wants him to behave, and it is worth dwelling on because executive incentives are where governance becomes concrete. His base salary was £1.1 million, which represented only around 44% of his total compensation — meaning the majority of his pay was variable and at risk.11 For the 2025 financial year, his total pay came in around £2.0 million, including a bonus of £824,000.11 Critically, that bonus was restricted to just 38% of the maximum possible, because the company missed its stretch target of £1 billion in profit before tax.11 That is the system working as designed: when management falls short of an ambitious goal, the variable pay is genuinely cut rather than quietly back-filled. Compensation that actually moves with performance is a healthier sign than a guaranteed package dressed up as incentive.

Schultz also has skin in the game in the most direct way. He holds roughly 5.43 million shares, and demonstrated his alignment by buying stock on the open market at around 90.06 pence in early 2025 — putting his own money in at a price the market was offering, not just receiving free grants.11 An executive buying shares with personal cash is one of the more credible signals available, because it cannot be faked by a remuneration committee.

The long-term structure is where the real alignment lives. The bulk of Schultz's long-term incentive — the Performance Share Plan, around 70% of the long-term award — is tied to demanding targets running through 2028.11 These include adjusted earnings per share in a target range of 12.9 to 15 pence, cumulative free cash flow of between £1.4 billion and £1.75 billion, and specific strategic milestones around U.S. integration and synergy capture, with Hibbett singled out. The remaining 30%, the Restricted Share Plan, vests over three years with an additional two-year holding period, which keeps the executive's wealth locked to the share price well beyond the vesting date and discourages short-term price manipulation.

There is also an ESG underpin that is worth flagging precisely because it has teeth: vested stock awards can be cut by up to 20% if the company fails to maintain specific environmental and carbon-reduction targets, including a CDP rating of 'B'.11 This is not the toothless ESG box-ticking common in many remuneration reports; a one-fifth haircut on vested equity is a material financial consequence, and it pulls climate performance into the same place as financial performance.

Finally, the governance backdrop. Schultz operates with the explicit backing of the majority owner, Pentland — a crucial source of stability that few public-company CEOs enjoy. That stability was tested and, arguably, reinforced in April 2026, when Chairman Andrew Higginson departed following tactical disagreements at board level.1 Boardroom departures can read as instability, but in this case the resolution cleared the way for a more unified focus on the global scaling agenda, with the controlling shareholder firmly behind the CEO. For investors, the governance picture is one of professionalized management, genuinely performance-linked pay, and a controlling owner providing top cover. The risk, as always with a controlled company, is that the interests being protected are ultimately the family's. With leadership and incentives mapped, we can turn to two parts of the business that rarely make the headlines but matter more than their size suggests.

VII. Hidden Gems: The Gym Empire and the Outdoor Pivot

Most investors who follow JD Sports think of it purely as a trainer retailer. They miss two businesses tucked inside the group that tell you something important about how management thinks — about operating leverage, about distressed real estate, and about the discipline to consolidate rather than sprawl. The first of these is a gym chain, and it has quietly become one of the most attractive units in the entire company.

JD Gyms is a low-cost, premium-feel, 24/7 fitness chain — the kind of place that charges a modest monthly membership but delivers an experience that feels more upmarket than the price suggests. In the 2025 financial year, its revenues grew 21% to £122 million, and adjusted profit surged 42% to £42.1 million.10 Pause on the relationship between those two numbers. Profit grew twice as fast as revenue, which is the signature of high operating leverage: once a gym has covered its fixed costs — the rent, the equipment, the core staffing — each incremental member's fee falls almost straight through to profit. A gym at 80% capacity is dramatically more profitable than the same gym at 50%, and as the estate matures, the economics improve mechanically.

The scale tells the rest of the story. JD Gyms reached 100 gyms in the UK with 572,000 members.10 The strategy is elegant and very much in the JD spirit: take distressed commercial real estate — the kind of large-format retail or leisure space that the post-pandemic property market left cheap and available — and convert it into high-end fitness floors under the JD brand. Cheap space in, premium memberships out, with the JD brand creating a lifestyle ecosystem that cross-promotes apparel and footwear to a captive, fitness-engaged audience. It is the retail-theater instinct applied to fitness: control the physical environment, make it a place people want to be, and let the brand do double duty. For a group whose core is exposed to fashion cycles and supplier concentration, a high-margin, recurring-revenue, locally-rooted cash generator is a genuinely valuable diversifier — and one the market arguably under-appreciates.

The second hidden story is the outdoor segment, and it is interesting for the opposite reason — it is a story of disciplined subtraction. JD inherited and assembled a complex portfolio of technical outdoor brands: Go Outdoors, Blacks, and Millets, names familiar to any British hiker or camper.1 The problem with running multiple legacy outdoor banners is that it dilutes everything — marketing spend is split, brand identity is muddied, and scale economies are lost across too many small fascias. Management recognized that owning three sub-scale outdoor brands was worse than owning one brand at real scale.

The pivot has been to consolidate aggressively around the larger, high-volume Go Outdoors "superstore" format, treating it as the single scaling vehicle for the entire outdoor segment. In the 2025 financial year, JD closed 24 standalone stores and converted 27 Blacks locations into Go Outdoors.1 The logic mirrors the Hibbett pruning playbook: rather than nurse a fragmented estate of underperforming banners, close the weak doors and channel volume into the format that works. It is unglamorous, margin-focused capital discipline — the same instinct that runs through the whole company.

What both of these segments reveal is a management team that thinks in terms of real estate, operating leverage, and concentration of resources, not just sneaker fashion. The gym business shows JD can build a high-margin recurring-revenue engine from cheap space; the outdoor pivot shows it has the discipline to kill its own weaker brands in service of scale. Both instincts — build leverage, concentrate force — are the same ones that show up in the acquisition record. Which brings us to the part of the story where we put the whole company under the analytical microscope.

VIII. Frameworks and the Playbook

Having walked through the history, the engine, the deals, and the leadership, it is worth slowing down to ask the structural question that matters most for a long-term investor: why is JD Sports defensible, in the rigorous sense that strategists mean? Two frameworks help — Hamilton Helmer's 7 Powers, which catalogs the specific sources of durable advantage, and Michael Porter's Five Forces, which maps the competitive pressures on an industry. Let's use both as lenses rather than checklists.

Start with Helmer. The most important power JD holds is what Helmer calls a Cornered Resource — exclusive access to a coveted asset on terms others cannot replicate. For JD, that resource is its "Global Strategic Partner" and "Connected Partnership" status with Nike and Adidas, and the Tier Zero allocations that come with it. This is the deepest part of the moat precisely because it cannot be bought. An upstart retailer with unlimited capital still cannot purchase the right to receive deep allocations of the hottest silhouettes or to integrate its loyalty program into Nike's membership system. Those relationships were earned over decades of being the most culturally credible physical home for the brands' products, and the brands have every incentive to keep the partner list short. A new entrant is structurally locked out of the very inventory that drives sneaker culture.

The second power is Scale Economies. Operating more than 3,400 stores globally gives JD purchasing power, freight and logistics cost advantages, and real leverage in rent negotiations that smaller chains simply cannot match. The company's "buy deep, not wide" philosophy — concentrating purchasing on hero products in massive volume rather than spreading thinly across a long tail — maximizes margins on the items that actually sell and amplifies the scale benefit. Size begets better terms begets better economics.

The third is Branding. "King of Trainers" is not merely a marketing slogan; it is an identity embedded in global youth culture, and specifically in the grime, hip-hop, and drill music scenes whose aesthetics and audiences overlap almost perfectly with JD's customer. The ubiquitous yellow-and-black duffle bag functions as a free, walking billboard carried across every city in Britain and increasingly beyond. Brand power lets JD command attention and loyalty in a way that pure price competition cannot dislodge.

The fourth is Counter-Positioning — historically, JD positioned itself against the traditional British discount sports retailers, the Sports Direct model of piling cheap rackets and discounted footballs high and selling them low. While that model competed on price and breadth, JD treated sneakers as premium fashion, investing in lighting, music, theater, and limited releases. A discounter cannot easily copy that without abandoning the cost structure that defines it — which is exactly what makes counter-positioning durable.

The fifth is Process Power — JD's repeatable, hard-to-imitate capability for identifying distressed regional multi-brand sneaker retailers (Finish Line, Hibbett, the European chains), acquiring them at attractive multiples, and integrating them into the global operating model while capturing supply-chain synergies. This is organizational know-how built up over many deals, and it is the engine behind the consolidation thesis.

Now flip to Porter's Five Forces, which describes the weather system the company operates in. The threat of new entrants is very low: because the brands are shrinking their partner lists rather than expanding them, the door to the premium tier is effectively closed to newcomers. The bargaining power of suppliers is medium-high — Nike and Adidas wield enormous brand power and supply a concentrated share of JD's product, which is a real source of pressure; but the loyalty integration and JD's role as the curator of physical "brand theater" make the relationship genuinely symbiotic, because the suppliers need JD's regional touchpoints as much as JD needs their product. The bargaining power of buyers is medium: consumers have little loyalty to a store if it doesn't have the product they want, but the roughly 50% "Only at JD" exclusive range and the loyalty status tie shoppers to the JD fascia in a way generic retailers cannot. The threat of substitutes is low — sneakers and athleisure have become permanent fixtures of global casual dress, and formal footwear poses little real threat to that secular shift. And competitive rivalry is high, with global players like Foot Locker — and its deepening relationships with the broader sporting-goods ecosystem, including Dick's Sporting Goods — competing hard for the same consumer and the same product allocations.

The synthesis of both frameworks points to the same conclusion: JD's advantages are real and layered, with the cornered-resource supplier relationship as the keystone, but the structure also concentrates risk in those same supplier relationships and exposes the company to intense rivalry and consumer cyclicality. That tension is exactly what the bull and bear cases are made of.

IX. Bull versus Bear

Every durable investment thesis is really an argument between two coherent stories, and JD Sports offers unusually clear versions of both. Let's lay them out honestly, because the same facts that power the bull case contain the seeds of the bear case.

The bull case rests on three pillars. The first is the M&A consolidation play. If JD successfully folds Hibbett and Courir into its operating machine — converting fascias, pruning the weak stores, capturing the synergies — it stands to realize meaningful annual cost savings, with management pointing to figures in the order of $25 million or more in immediate annual synergies from the integration work. Given JD's demonstrated track record on Finish Line, the base rate for execution here is encouraging rather than speculative. The second pillar is the wholesale resurgence — the structural reversal of the DTC era, with Nike and Adidas continuing to scale back direct ambitions and reinvest in premium physical retailers. As the indispensable premium wholesale partner, JD is a direct beneficiary of the brands rediscovering that they need great retailers. The third pillar is the gym multiplier: if JD can replicate its low-cost, high-margin fitness model internationally, it has a genuinely profitable, recurring-revenue cash-cow division growing alongside the core, providing both diversification and a higher-quality earnings stream than fashion retail alone.

The bear case is equally coherent and should not be dismissed. The first and most serious risk is supplier concentration. More than 70% of JD's product relies on just a handful of brands — Nike, Adidas, and New Balance chief among them — with Nike alone in the mid-40s as a percentage of sales.2 This is the flip side of the cornered-resource power: JD's fortunes are lashed to the design and brand health of suppliers it does not control. If Nike suffers a sustained product-design slump, a brand misstep, or a strategic shift, it hits JD's top line directly and immediately, and there is no quick way to diversify away from a relationship that is also the company's greatest asset. The keystone of the moat is also the keystone of the risk.

The second bear pillar is the North American and European macro slowdown. JD's customer is the discretionary spender, often young and price-sensitive, and athletic footwear is a discretionary purchase. Slowing consumer spending across the U.S. and Europe pressures near-term sales and squeezes margins precisely as JD is absorbing the costs of integrating large acquisitions. The company has bought heavily into the American market at the same time that American consumer confidence faces cyclical headwinds — a timing risk that is real even if the long-term thesis holds.

The third is multiple dilution and integration risk. JD has, in cases like Courir, acquired international assets at multiples around 7.5 to 8 times EBITDA while its own stock traded at a depressed 4 to 5 times. Buying assets at higher multiples than your own can depress overall group valuation metrics unless the synergies are realized quickly and the market re-rates the combined entity. If integration stumbles — if the synergies prove slower or smaller than promised — the company will have spent premium prices for businesses that drag rather than lift the group multiple. Roll-ups are unforgiving of execution slippage, and the larger the deals, the higher the stakes.

How do these net out against the competition? Against Foot Locker, JD's principal global rival, JD generally enjoys stronger brand-partner positioning and a more disciplined acquisition record, though both face the identical supplier-concentration exposure and the same cyclical consumer. Against Sports Direct and the discount end, JD competes on premium experience and exclusive product rather than price, a position that holds well in good times but can feel exposed when consumers trade down in a downturn. The honest assessment is that JD is among the best-positioned physical retailers in its category, with a genuine moat — but it is not immune to the cycle, and its greatest strength and greatest vulnerability are the same relationship.

Which leaves the practical question: if you can only watch a couple of numbers, what should they be? Three KPIs matter most for tracking this business going forward. The first is like-for-like (organic) sales growth, the cleanest read on whether the core retail engine is healthy independent of acquisitions and new-store openings — for a retailer, this is the vital sign. The second is gross margin, which captures the health of the SMU/exclusive-product strategy and the supplier relationship; margin erosion would be the earliest warning that the moat is leaking or that the brands are shifting terms. The third, for the medium term, is U.S. integration and synergy capture, specifically the realized cost savings and store-conversion productivity from Hibbett — the single biggest determinant of whether the great American land grab creates or destroys value. Watch those three, and you are watching the things that actually move this company.

X. Epilogue

There is a tidy symmetry to the JD Sports story. It began in 1981 with a single small shop in Bury, opened by a former fireman on his third career and an eighteen-year-old with an instinct for what teenagers wanted on their feet. Four and a half decades later, that storefront has become a global blueprint for how physical retail not only survives the internet age but thrives in it — a FTSE 100 company spanning thousands of stores and three continents, with the world's most powerful brands queuing to integrate their loyalty programs into its app.

The deeper lesson, the one worth carrying away, is a corrective to a decade of lazy conventional wisdom. Physical retail is not dead. Boring physical retail is dead. The generic, undifferentiated store with no relationship to the consumer and no leverage over its suppliers was always going to be commoditized and hollowed out by e-commerce. But a retailer that controls the relationship with the end consumer — through theater, through community, through cultural credibility — and integrates digitally with its suppliers, and maintains rigorous discipline in how it deploys capital and prices its acquisitions, can build a multi-billion-pound empire that the brands themselves cannot route around.

JD Sports earned its crown not by selling shoes, but by becoming the place where sneaker culture lives, the partner the brands cannot replace, and the buyer that consistently pays the right price. Whether it holds that crown depends, as it always has, on the next allocation, the next integration, and the next generation of teenagers walking out of those black-and-yellow doors with a duffle bag over one shoulder.

References

-

JD Sports Results and Reports Archive — JD Sports Fashion plc ↩↩↩↩

-

Acquisition of The Finish Line, Inc. — JD Sports Fashion plc News, 2018 ↩↩

-

Acquisition of Shoe Palace — JD Sports Fashion plc News, 2020 ↩

-

Acquisition of DTLR Villa — JD Sports Fashion plc News, 2021 ↩

-

JD Sports Completes Acquisition of Hibbett, Inc. — JD Sports Fashion plc News, 2024 ↩↩

-

JD Sports Launches Connected Partnership with Nike — JD Sports Fashion plc News, 2022 ↩↩

-

JD Sports Chief Régis Schultz Plots Global Sneaker Dominance — Financial Times ↩↩↩↩↩

-

Finish Line Merger Agreement with JD Sports — Form 8-K, SEC, 2018 ↩↩

-

JD Gyms records double-digit sales growth as it hits 100 gyms milestone — Retail Gazette ↩↩

-

JD Sports CEO Régis Schultz pay packets reveal retail targets — City A.M. ↩↩↩↩↩↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube